Shareholder Rights Common Stock Offering

Investor Presentation

Northwest Bancorporation, Inc.

2

Legal Disclaimer

In the course of our presentation, we may discuss matters that are deemed to be forward-

looking statements, which are intended to be covered by the safe harbor for “forward-looking

statements” provided by the Private Securities Litigation Reform Act of 1995 (the “Reform

Act”)(1). Forward-looking statements, including those relating to our position and strategy

following completion of the transaction discussed herein, involve substantial risks and

uncertainties, many of which are difficult to predict and are generally beyond our control and

actual results may differ from management’s view. Additional information about risks of the

company achieving results suggested by any forward-looking statements may be found in

Company’s registration statement on Form S-3 under the heading “Risk Factors” as well as the

Company’s 10-K and other SEC filings incorporated by reference therein under the headings

“Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of

Operations.” Unless legally required, the Company disclaims any obligation to update any

forward-looking statements, whether as a result of new information, future events or otherwise.

looking statements, which are intended to be covered by the safe harbor for “forward-looking

statements” provided by the Private Securities Litigation Reform Act of 1995 (the “Reform

Act”)(1). Forward-looking statements, including those relating to our position and strategy

following completion of the transaction discussed herein, involve substantial risks and

uncertainties, many of which are difficult to predict and are generally beyond our control and

actual results may differ from management’s view. Additional information about risks of the

company achieving results suggested by any forward-looking statements may be found in

Company’s registration statement on Form S-3 under the heading “Risk Factors” as well as the

Company’s 10-K and other SEC filings incorporated by reference therein under the headings

“Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of

Operations.” Unless legally required, the Company disclaims any obligation to update any

forward-looking statements, whether as a result of new information, future events or otherwise.

(1) The Reform Act defines the term "forward-looking statements" to include: statements of management plans and objectives, statements regarding the future economic performance, and

projections of revenues and other financial data, among others. The Reform Act precludes liability for oral or written forward-looking statements if the statement is identified as such and

accompanied by "meaningful cautionary statements identifying important factors that could cause actual results to differ materially from those made in the forward-looking statements."

projections of revenues and other financial data, among others. The Reform Act precludes liability for oral or written forward-looking statements if the statement is identified as such and

accompanied by "meaningful cautionary statements identifying important factors that could cause actual results to differ materially from those made in the forward-looking statements."

3

Offering Summary

Issuer: Northwest Bancorporation, Inc.

Ticker: (OTCBB: NBCT)

Closing Stock Price (5/25/2010): $6.00

Tangible Book Value Per Share: $9.83

Type of Security: Common Stock

Offering Type: Non-Transferable Shareholder Rights

Transaction Size: $4,000,000

Upsize Option: 20% (up to $4,800,000)

Offer Price Per Share: $4.00

Shares Issued in Offering(1): 1,000,000

Pre-Offering Shares Outstanding(2): 2,385,693

Use of Proceeds: Improve capital position at the Bank and general

corporate purposes

corporate purposes

Expected Closing: July 1, 2010

(1) Shares issued based on a $4.0 million offering before the potential upsize option

(2) Shares outstanding as of 5/3/2010 per the Company S-3

4

Offering Rationale

Further strengthen balance sheet

• Increase tangible common equity and enhance capital ratios

• Proactive approach to uncertain economic and regulatory environment

Better positions the Company to take advantage of

opportunities resulting from market dislocation

opportunities resulting from market dislocation

• Favorable competitive landscape (big and small competitors struggling)

• Grow core deposits and attract new customers

• Attract and retain talented personnel

Shareholder rights offering is the least dilutive option for

shareholders to raise capital

shareholders to raise capital

• Current shareholders have the opportunity to purchase newly issued shares direct from the

Company without any fees

5

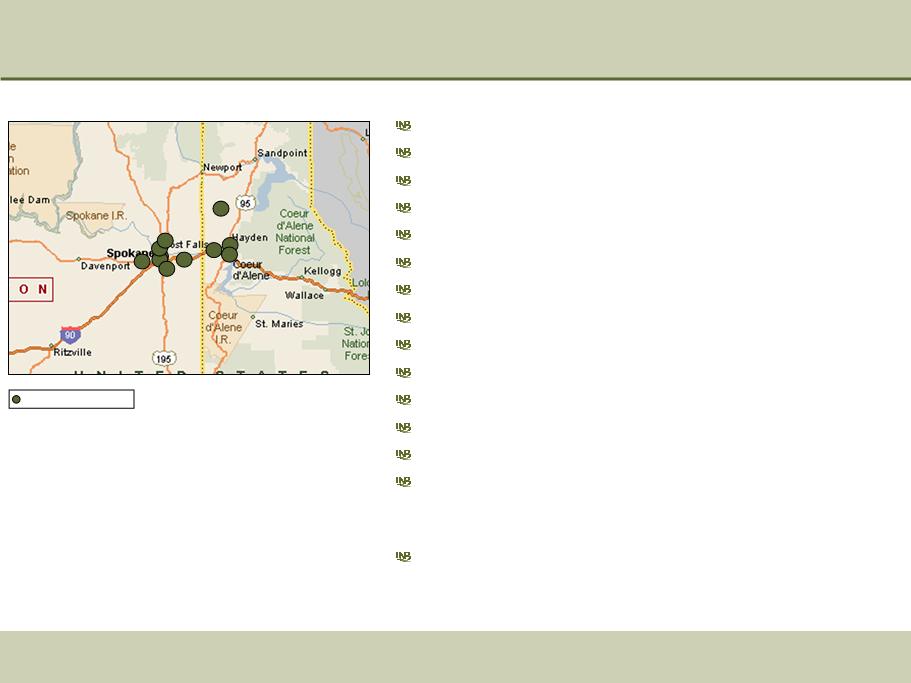

Company Profile

Company Name: Northwest Bancorporation, Inc.

Bank Name: Inland Northwest Bank

Year Established: 1989

Headquarters: Spokane, WA

Branch Network: 11 Branches (7 in WA and 4 in ID)

Assets: $398.2 million

Gross Loans: $315.4 million

Deposits: $343.3 million

Common Equity: $23.6 million

Net Income (Q1 2010): $586 thousand

Net Interest Margin (Q1 2010): 4.04%

Loan / Deposit Ratio: 91.9%

Regional Focus: Eastern Washington and Northern Idaho

Customer Focus: Small to medium-sized businesses

headquartered in our markets as well

as the owners and employees of these

businesses

Insider Ownership: 21.70%

NBCT branch location

Source: Financial data from Company 10-Q, as of 3/31/2010.

Ownership data from Internal Company Reports, as of 5/3/2010

Ownership data from Internal Company Reports, as of 5/3/2010

6

Investment Highlights

Returned to profitability in 1st Quarter 2010

Experienced and disciplined management team

Attractive and growing core deposit base

Growing net interest margin, operating revenue and core earnings

Largely avoided the major credit quality problems that have

plagued peers in the region

Competitor dislocation in our market area

Attractive valuation

7

1st Quarter Update

Earnings

Margin

Core Deposits

Credit Quality

Capital

• Profit of $586 thousand during Q1 2010

• Core earnings of $1.7 million during Q1 2010

• Operating revenue of $4.6 million during Q1 2010

• Net interest margin expanded to 4.04% during Q1 2010 compared to 3.40% for Q1 2009

• Core deposits increased by 10.08%, or $16.6 million compared to 12/31/2009

• Core deposits increased by 20.77%, or $31.2 million compared to 3/31/2009

• Non-accrual loans of $9.0 million, compared to $11.7 million at 12/31/2009

• Loan loss reserve of $7.2 million, compared to $7.1 million at 12/31/2009

Update on the financial results for the Company for the fiscal quarter ended 3/31/2010

• Risk based capital ratio increased to 12.57%

Source: Company 10-Q, as of 3/31/2010

Note: Core earnings excludes taxes, provision expense, expenses related to OREO and depreciation expense

Note: Operating revenue includes net interest income and non-interest income

Note: Core deposits exclude all CDs

8

Executive Management Team and Ownership

Executive Management Team and Current Insider Ownership

Source: Internal Company Reports, as of 5/3/2010

Name

Title

Age

Years With

Company

Ownership

%

Randall L. Fewel

Chief Executive Officer

61

16

2.05%

Holly A. Poquette, CPA

Chief Financial Officer

39

13

0.35%

Douglas J. Beaudoin

Manager of Mortgage Department

58

12

0.23%

Mark V. Dresback

Commercial Team Leader

50

9

0.22%

Elizabeth A. Herndon

Chief Retail Banking Officer

55

15

0.26%

Ronald G. Jacobson

Commercial Team Leader

54

9

0.38%

Scott W. Southwick

Chief Credit Officer

59

3

0.33%

All Executive Management and Directors as a Group (18 Persons)

21.70%

9

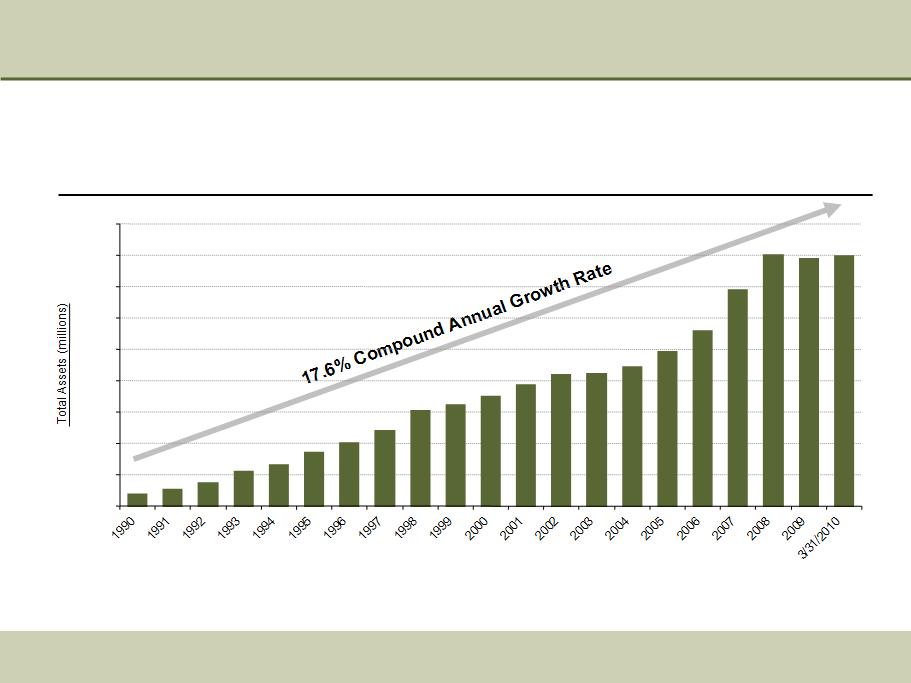

Conservative and Steady Growth

Total Assets (From 1990-Present)

Source: SNL Financial and Internal Company Reports

$17.6

$25.6

$36.5

$54.7

$65.6

$84.5

$99.5

$220.5

$245.5

$278.9

$343.7

$400.2

$398.2

$393.7

$151.9

$120.4

$161.2

$209.1

$192.9

$173.7

$210.5

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

10

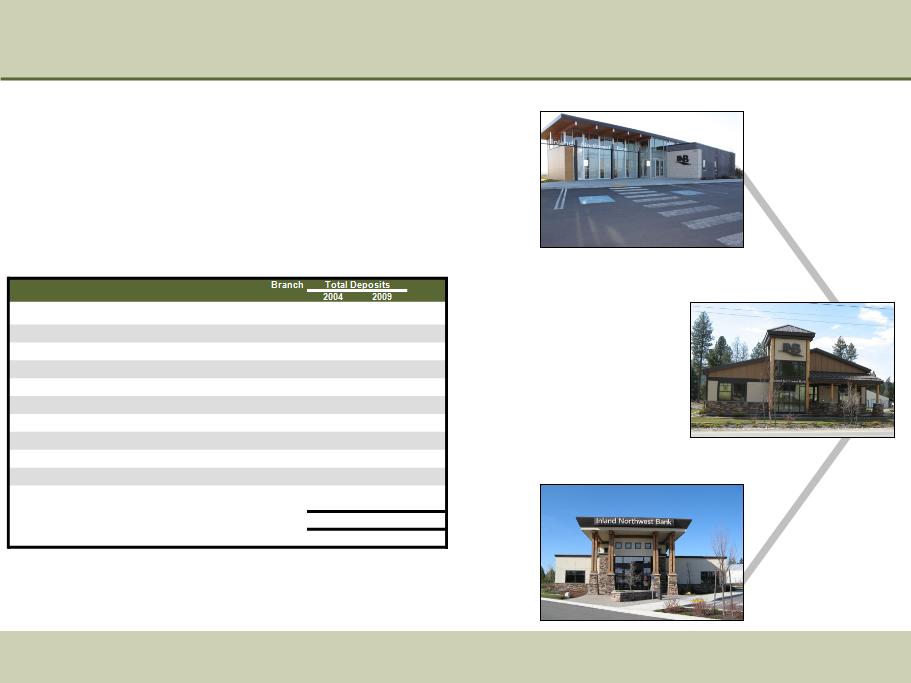

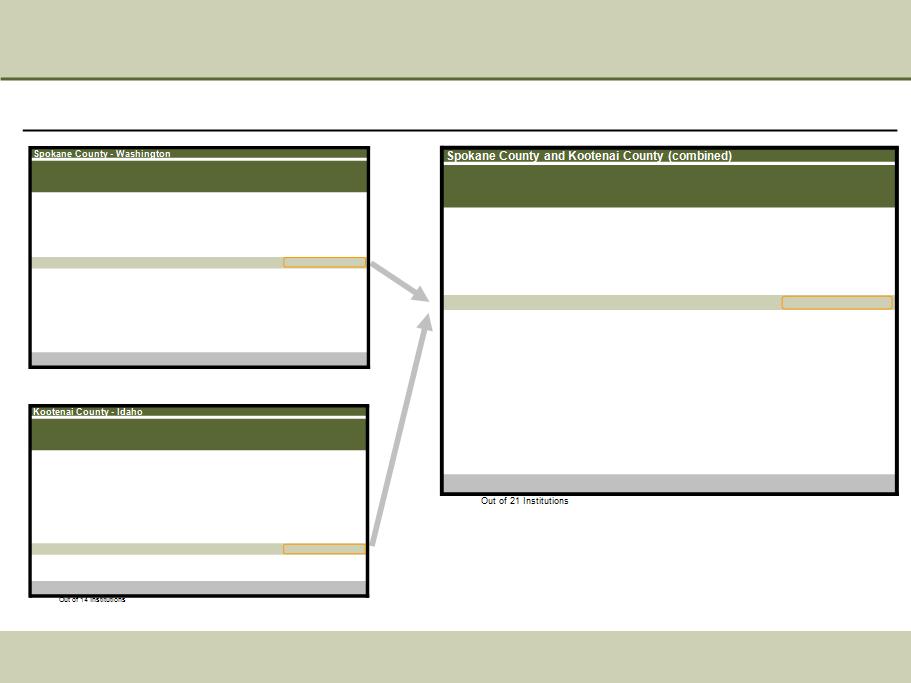

Attractive Branch Network

Regional concentration in Eastern Washington and Northern Idaho

• 11 branches across Spokane County and Kootenai County

• High quality full-service banking facilities

• 2 new branch locations opened since 2007 and 4 branch relocations since 2006

Source: SNL Financial and Internal Company Reports.

Deposit data as of 6/30 for the respective year

Deposit data as of 6/30 for the respective year

Branch Locations

Spirit Lake, ID

Airway Heights, WA

Coeur d’Alene (Hayden), ID

Address

City

County, State

Opened

CAGR

421 W Riverside Ave

Spokane

Spokane, WA

1989

$77,123

$133,519

11.6%

1021 E Hawthorne Rd

Spokane

Spokane, WA

1995

$15,324

$29,510

14.0%

1729 E Seltice Way

Post Falls

Kootenai, ID

1995

$4,884

$12,155

20.0%

15015 E Sprague Ave

Spokane Valley

Spokane, WA

1992

$17,454

$26,438

8.7%

11917 W Sunset Hwy

Airway Heights

Spokane, WA

1993

$11,385

$17,359

8.8%

518 W Francis Ave

Spokane

Spokane, WA

1996

$8,429

$23,483

22.7%

2905 E 57th Ave

Spokane

Spokane, WA

1997

$17,336

$32,875

13.7%

955 Ironwood Dr

Coeur d'Alene

Kootenai, ID

1998

$12,395

$23,273

13.4%

2110 N Ruby St

Spokane

Spokane, WA

1994

$15,738

$19,776

4.7%

30 W Prairie Ave

Coeur d'Alene

Kootenai, ID

2007

NA

$6,972

50.5%

31845 N 5th Ave

Spirit Lake

Kootenai, ID

2007

NA

$5,690

17.2%

Total Deposits

$180,068

$331,050

13.0%

Average Deposits

$20,008

$30,095

11

Established Market Share Position

Deposit Market Share

Source: Deposit market share data provided by SNL Financial, as of 6/30/2009.

Rank

Institution (State)

Number of

Branches

Deposits

in Market

Deposit

Growth

(1-Year)

Market

Share %

1

Sterling Financial Corp. (WA)

8

1,969,138

$

+12.8%

26.97%

2

W.T.B. Financial Corp. (WA)

16

1,746,867

$

+7.5%

23.93%

3

Bank of America Corp. (NC)

12

729,590

$

+17.7%

9.99%

4

JPMorgan Chase & Co. (NY)

13

578,672

$

-22.9%

7.93%

5

U.S. Bancorp (MN)

16

537,325

$

+2.3%

7.36%

6

Banner Corp. (WA)

16

440,592

$

-3.7%

6.04%

7

Wells Fargo & Co. (CA)

8

406,969

$

+19.0%

5.57%

8

Northwest Bancorporation, Inc. (WA)

7

282,960

$

+15.5%

3.88%

9

AmericanWest Bancorp. (WA)

7

175,843

$

-60.6%

2.41%

10

Riverbank Holding Co. (WA)

3

128,647

$

+17.0%

1.76%

11

Fairfield Financial Holdings (WA)

6

106,272

$

+5.8%

1.46%

12

State Bancorp Northwest (WA)

2

80,911

$

+7.6%

1.11%

13

Community Financial Group Inc (WA)

3

38,606

$

+22.4%

0.53%

14

Intermountain Community Bancorp (ID)

2

35,223

$

+13.7%

0.48%

15

Whitman Bancorporation Inc. (WA)

3

30,369

$

+21.5%

0.42%

16

Glacier Bancorp Inc. (MT)

1

9,579

$

+201.2%

0.13%

17

Dickinson Financial Corp. II (MO)

1

2,693

$

-15.8%

0.04%

Total For Institutions In Market

124

$ 7,300,256

+2.3%

Out of 17 Institutions

Rank

Institution (State)

Number of

Branches

Deposits

in Market

Deposit

Growth

(1-Year)

Market

Share %

1

Wells Fargo & Co. (CA)

8

325,244

$

+1.8%

19.74%

2

Glacier Bancorp Inc. (MT)

5

227,327

$

-3.7%

13.79%

3

Bank of America Corp. (NC)

5

206,031

$

+15.8%

12.50%

4

U.S. Bancorp (MN)

5

182,072

$

+18.3%

11.05%

5

W.T.B. Financial Corp. (WA)

4

156,560

$

-8.4%

9.50%

6

Idaho Independent Bank (ID)

2

129,539

$

-11.0%

7.86%

7

Intermountain Community Bancorp (ID)

4

104,727

$

+13.5%

6.36%

8

Coeur d'Alene Bancorp (ID)

3

76,729

$

-10.0%

4.66%

9

Sterling Financial Corp. (WA)

3

63,406

$

-6.4%

3.85%

10

JPMorgan Chase & Co. (NY)

2

56,225

$

-25.6%

3.41%

11

Northwest Bancorporation, Inc. (WA)

4

48,090

$

+3.9%

2.92%

12

AmericanWest Bancorp. (WA)

2

39,508

$

+61.2%

2.40%

13

Community 1st Bank (ID)

1

26,023

$

+86.9%

1.58%

14

Idaho Trust Bancorp (ID)

1

6,451

$

+98.1%

0.39%

Total For Institutions In Market

49

$ 1,647,932

+2.2%

Rank

Institution (State)

Number of

Branches

Deposits

in Market

Deposit

Growth

(1-Year)

Market

Share %

1

Sterling Financial Corp. (WA)

11

2,032,544

$

+12.1%

22.71%

2

W.T.B. Financial Corp. (WA)

20

1,903,427

$

+6.0%

21.27%

3

Bank of America Corp. (NC)

17

935,621

$

+17.3%

10.46%

4

Wells Fargo & Co. (CA)

16

732,213

$

+10.7%

8.18%

5

U.S. Bancorp (MN)

21

719,397

$

+5.9%

8.04%

6

JPMorgan Chase & Co. (NY)

15

634,897

$

-23.1%

7.10%

7

Banner Corp. (WA)

16

440,592

$

-3.7%

4.92%

8

Northwest Bancorporation, Inc. (WA)

11

331,050

$

+13.7%

3.70%

9

Glacier Bancorp Inc. (MT)

6

236,906

$

-0.9%

2.65%

10

AmericanWest Bancorp. (WA)

9

215,351

$

-54.2%

2.41%

11

Intermountain Community Bancorp (ID)

6

139,950

$

+13.6%

1.56%

12

Idaho Independent Bank (ID)

2

129,539

$

-11.0%

1.45%

13

Riverbank Holding Co. (WA)

3

128,647

$

+17.0%

1.44%

14

Fairfield Financial Holdings (WA)

6

106,272

$

+5.8%

1.19%

15

State Bancorp Northwest (WA)

2

80,911

$

+7.6%

0.90%

16

Coeur d'Alene Bancorp (ID)

3

76,729

$

-10.0%

0.86%

17

Community Financial Group Inc (WA)

3

38,606

$

+22.4%

0.43%

18

Whitman Bancorporation Inc. (WA)

3

30,369

$

+21.5%

0.34%

19

Community 1st Bank (ID)

1

26,023

$

+86.9%

0.29%

20

Idaho Trust Bancorp (ID)

1

6,451

$

+98.1%

0.07%

21

Dickinson Financial Corp. II (MO)

1

2,693

$

-15.8%

0.03%

Total For Institutions In Market

173

$ 8,948,188

+2.3%

12

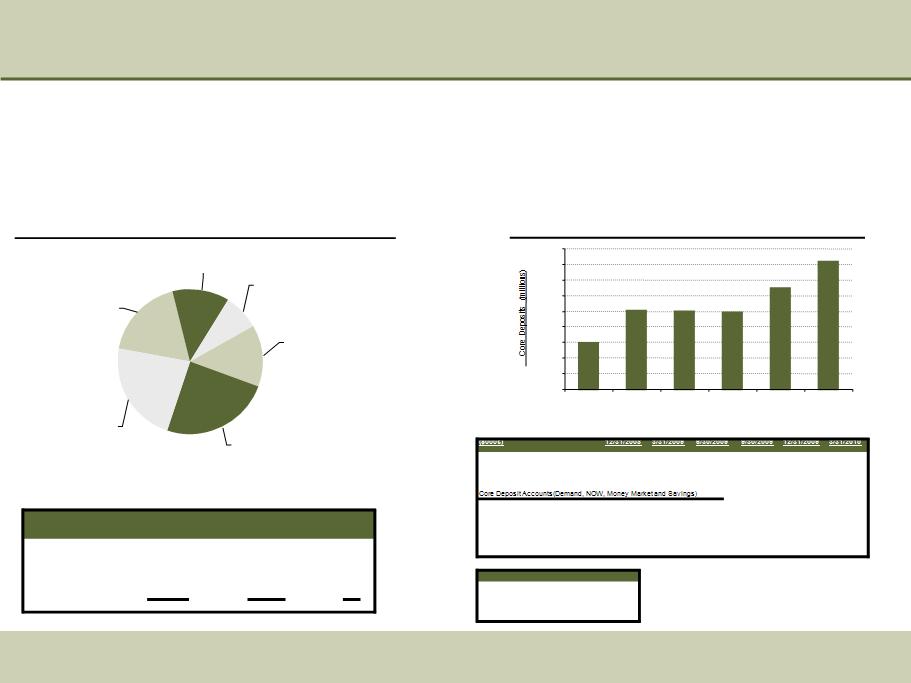

Deposit Composition

Core Deposits

Attractive and Growing Deposit Base

Source: Company 10-Q and Internal Company Reports, as of 3/31/2010

Note: Core deposits exclude all CDs

• Non-interest bearing deposits represent 18.4% of total deposit balances

• Core deposits increased $16.6 million, or 10.08% since 12/31/2009

• Non-core deposits decreased $11.0 million, or 6.38% since 12/31/2009

• Significant new account growth during 1st quarter 2010 with 656 net new core accounts, or a 4.45% increase in core accounts since 12/31/2009 (19.0%

annualized growth)

annualized growth)

Deposit Detail By Category

Money Market Accounts

8.1%

Savings Accounts

13.5%

CDs Under $100,000

24.3%

CDs $100,000 and Over

22.9%

Non-Interest Bearing

Demand

18.4%

NOW Accounts

12.8%

Balance

($000s)

% of

Total Bal.

# of

Accounts

% of Total

Accts.

Avg.

Cost

Non-Interest Bearing Demand

63,276

$

18.4%

8,783

44.1%

0.00%

NOW Accounts

43,826

12.8%

1,837

9.2%

1.28%

Money Market Accounts

27,735

8.1%

693

3.5%

1.03%

Savings Accounts

46,448

13.5%

4,105

20.6%

1.19%

CDs Under $100,000

83,552

24.3%

4,066

20.4%

2.96%

CDs $100,000 and Over

78,506

22.9%

442

2.2%

2.93%

Total Deposits

343,343

$

19,926

1.84%

$129.5

$150.1

$149.6

$149.2

$164.7

$181.3

$100

$110

$120

$130

$140

$150

$160

$170

$180

$190

12/31/2008

3/31/2009

6/30/2009

9/30/2009

12/31/2009

3/31/2010

Balances

Total Deposits

316,055

$

331,435

$

330,069

$

326,062

$

337,777

$

343,343

$

Core Deposits

129,466

$

150,107

$

149,623

$

149,193

$

164,683

$

181,285

$

Total Number of Accounts

14,029

14,333

14,431

14,546

14,749

15,405

Net New Accounts During Period

33

191

108

115

112

656

Core Deposit Trends

% of Total

41.0%

45.3%

45.3%

45.8%

48.8%

52.8%

% Growth From Prior Quarter-End

-5.08%

15.94%

-0.32%

-0.29%

10.38%

10.08%

2010 Q1

Cost of Core Deposits

0.76%

Cost of Interest Bearing Deposits

2.24%

Cost of Total Deposits

1.84%

Cost of Funds

1.97%

13

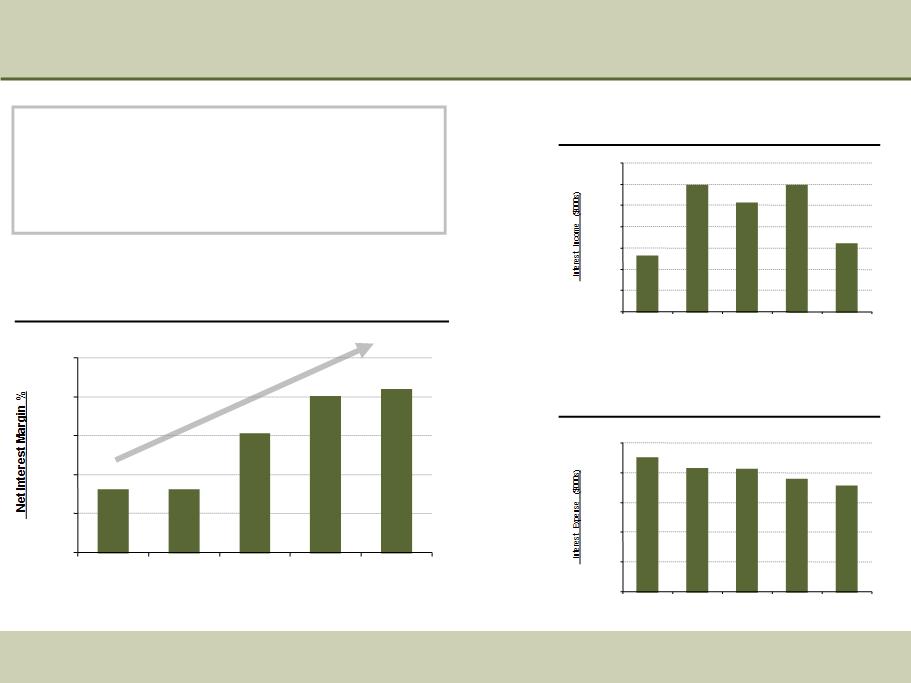

Net Interest Margin

• The Company’s net interest margin has expanded 64 basis

points since 1st quarter 2009

points since 1st quarter 2009

• Margin expansion is largely attributed to decreasing interest

expense and stable interest income

expense and stable interest income

• Interest expense of $1.8 million compared to $2.2 million in

Q1 2009, a decrease of $476 thousand or 21.3%

Q1 2009, a decrease of $476 thousand or 21.3%

Net Interest Margin

Interest Expense

Interest Income

Source: Company 10-Q, as of 3/31/2010

+ 64 basis

points

points

3.40%

3.40%

3.76%

4.00%

4.04%

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

$5,379

$5,545

$5,505

$5,545

$5,408

$5,250

$5,300

$5,350

$5,400

$5,450

$5,500

$5,550

$5,600

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

$2,236

$2,068

$2,043

$1,879

$1,760

$-

$500

$1,000

$1,500

$2,000

$2,500

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

14

Earnings Power

Operating Revenue

Core Earnings

Source: Company 10-Q and Internal Company Reports, as of 3/31/2010

Note: Core earnings excludes taxes, provision expense, expenses related to OREO and depreciation expense

Note: Pre-tax pre-provision income excludes income tax expense and provision expense

Note: Operating revenue includes net interest income and non-interest income

Returned to Profitability During 1st Quarter 2010

Results from 1st Quarter 2010

• Net interest income of $3.6 million

• Net income of $586 thousand (before preferred dividends)

• Net income for common shareholders of $417 thousand

• Operating revenue of $4.6 million

• Pre-tax pre-provision income of $1.3 million

• Core earnings of $1.7 million

Income Statement

$4,589

$4,341

$3,968

$4,226

$4,396

$3,750

$4,000

$4,250

$4,500

$4,750

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

$1,703

$965

$964

$1,307

$1,618

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

($000s)

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

Interest Income

5,379

$

5,545

$

5,505

$

5,545

$

5,408

$

Interest Expense

2,236

2,068

2,043

1,879

1,760

Net Interest Income

3,143

3,477

3,462

3,666

3,648

Provision Expense

1,180

1,800

2,400

1,967

500

Non-Interest Income

825

864

764

730

941

Non-Interest Expense

3,228

3,891

3,163

3,627

3,241

Income Tax Expense

(184)

(504)

(706)

346

262

Net Income

(256)

(846)

(631)

(1,544)

586

Preferred Dividends

87

171

173

165

169

Net Income For Common

(343)

$

(1,017)

$

(804)

$

(1,708)

$

417

$

Non-GAAP Measurements

Operating Revenue

3,968

$

4,341

$

4,226

$

4,396

$

4,589

$

Pre-Tax Pre-Provision Income

740

$

450

$

1,063

$

769

$

1,348

$

Core Earnings

964

$

965

$

1,307

$

1,618

$

1,703

$

15

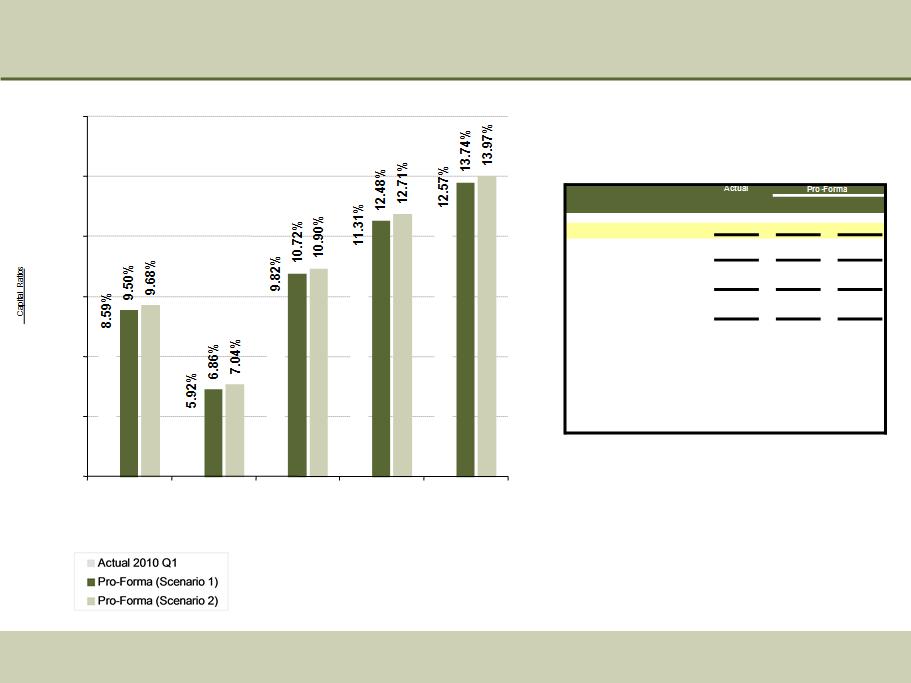

Capital Ratio Snapshot

Capital Snapshot

Northwest Bancorporation, Inc.

Source: Regulatory data from FR-Y9

Note: Pro-forma scenarios with gross offerings of $4.0 million and $4.8

million (respectively) and risk weighting of 0.0% on new capital

million (respectively) and risk weighting of 0.0% on new capital

Tangible Common

Equity Ratio

Equity Ratio

Leverage

Ratio

Ratio

Tier-1

Ratio

Ratio

Risk Based

Capital Ratio

Capital Ratio

Total Equity

Ratio

Ratio

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

($000s)

Scen. 1

Scen. 2

Common Equity (Actual)

23,587

$

23,587

$

23,587

$

Additional Capital From Offering

-

4,000

4,800

Common Equity

23,587

27,587

28,387

TARP Preferred Equity

10,618

10,618

10,618

Total Equity

34,205

38,205

39,005

Trust Preferred Securities

5,000

5,000

5,000

Total Tier-1 Capital

38,871

42,871

43,671

LLR Includable in Tier-2

4,333

4,333

4,333

Total Tier-2 Capital

4,333

4,333

4,333

Total Risk Based Capital

43,204

$

47,204

$

48,004

$

Capital Ratios

Total Equity Ratio

8.59%

9.50%

9.68%

Tangible Common Equity Ratio

5.92%

6.86%

7.04%

Leverage Ratio

9.82%

10.72%

10.90%

Tier-1 Ratio

11.31%

12.48%

12.71%

Risk Based Capital Ratio

12.57%

13.74%

13.97%

2010 Q1

16

Diversified Loan Portfolio

Loan Composition

Loan Detail By Category

Total Commercial Real Estate of 47.1%

Source: Company data from 10-Q and Internal Company Reports, as of 3/31/2010

* Gross loans excluding loans held for sale

Balance

($000s)

% of

Gross Loans

Owner-Occupied CRE

83,381

$

26.4%

Non Owner-Occupied CRE

65,132

20.7%

Commercial Real Estate

148,513

47.1%

1-4 Family and Multi-Family

49,534

15.7%

Commercial Construction

17,668

5.6%

Commercial Non-Real Estate

54,486

17.3%

Land and Land Development

35,091

11.1%

Consumer

10,091

3.2%

Gross Loans*

315,383

Less: Net Deferred Loan Fees

603

Gross Loans*, Net of Deferred Fees

314,780

Plus: Loans Held For Sale

1,466

Less: Loan Loss Reserve

7,175

Net Loans

309,071

$

Yield on Loans

6.37%

Yield on Earning Assets

5.99%

Gross Loans*

339,752

$

338,360

$

337,163

$

324,983

$

321,811

$

315,383

$

Loan / Deposit Ratio

107.5%

102.1%

102.1%

99.7%

95.3%

91.9%

Consumer

3.2%

Non Owner-Occupied

CRE

20.7%

1-4 Family and Multi-

Family

15.7%

Commercial Construction

5.6%

Commercial Non-Real

Estate

17.3%

Land and Land

Development

11.1%

Owner-Occupied CRE

26.4%

17

Credit Quality Snapshot

Non-Accrual Loan Composition (3/31/2010)

Credit Quality Statistics

Non-Accrual Loan Trends

Source: Company data from 10-Q and Internal Company Reports

Note: Non-performing assets excludes restructured loans

Note: Texas ratio = (non-performing assets + loans 90 days or greater past

due) / (tangible equity + loan loss reserve)

due) / (tangible equity + loan loss reserve)

$14.0

$11.0

$13.6

$11.7

$9.0

2.87%

3.63%

4.13%

4.10%

3.23%

$-

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

3/31/2009

6/30/2009

9/30/2009

12/31/2009

3/31/2010

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

Non-Accrual Loans

NAL / Loans

Consumer

0.6%

Commercial Non-

Real Estate

4.8%

Commercial Real

Estate

38.8%

1-4 Family

4.0%

Construction &

Development

51.8%

($000s)

3/31/2009

6/30/2009

9/30/2009

12/31/2009

3/31/2010

Beginning Reserve Balance

4,737

$

5,453

$

4,425

$

6,334

$

7,082

$

Plus: Loan Loss Provisions

1,180

1,800

2,400

2,047

500

Less: Net Charge-offs

464

2,843

496

1,199

407

Ending Reserve Balance

5,453

4,425

6,334

7,082

7,175

Credit Quality

Loans 30-89 Days Past Due

10,467

7,695

9,997

4,528

8,583

Loans 90+ Days Past Due

-

-

-

-

-

Non-Accrual Loans (NALs)

13,956

11,014

13,555

11,676

9,045

Other Real Estate Owned

2,635

4,134

3,880

3,672

3,401

Non-Performing Assets (NPAs)

16,591

15,148

17,435

15,348

12,446

Portion of NALs from Participation Loans

6,386

4,331

6,786

6,526

4,057

% of Total Non-Accrual Loans

45.8%

39.3%

50.1%

55.9%

44.9%

Credit Ratios

Reserves / Loans

1.60%

1.30%

1.93%

2.20%

2.28%

Reserves / NALs

39.1%

40.2%

46.7%

60.7%

79.3%

Reserves / NPAs

32.9%

29.2%

36.3%

46.1%

57.6%

NALs / Loans

4.10%

3.23%

4.13%

3.63%

2.87%

NPAs / Assets

4.16%

3.80%

4.43%

3.90%

3.13%

Net Charge-Offs / Avg. Loans

0.54%

3.34%

0.59%

1.47%

0.51%

Texas Ratio

39.0%

37.4%

41.5%

37.5%

30.1%

Non-Accrual Balances By Loan Type

Construction & Development

9,502

$

9,631

$

9,077

$

7,957

$

4,687

$

1-4 Family

195

202

511

190

360

Commercial Real Estate

2,222

428

3,310

3,191

3,507

Consumer

43

80

-

16

56

Commercial Non-Real Estate

1,993

896

658

434

436

18

Appendix

19

Historical Key Financials

Source: Company data from 10-Q and 10-K filings

Note: Operating revenue includes net interest income and non-interest income

Note: Pre-tax pre-provision income excludes income tax expense and provision expense

2005

2006

2007

2008

2009

3/31/2010

Balance Sheet ($000s)

Cash and Equivalents

10,570

$

12,369

$

12,271

$

11,414

$

18,119

$

21,522

$

Investment Securities

36,935

35,955

37,206

27,339

26,069

36,131

Net Loans

186,465

216,693

276,452

335,207

317,198

309,071

Loan Loss Reserve

2,252

2,586

2,711

4,737

7,082

7,175

Total Assets

245,465

278,947

343,716

400,231

393,702

398,238

Deposits

192,043

210,567

272,540

316,055

337,777

343,343

Borrowings

30,324

41,574

41,000

54,701

19,222

18,063

Tangible Common Equity

21,686

24,521

27,346

26,919

23,214

23,587

Total Equity

21,686

24,521

27,346

26,919

33,806

34,205

Income Statement ($000s)

Interest Income

13,687

$

17,884

$

21,768

$

23,124

$

21,974

$

5,408

$

Interest Expense

4,347

6,640

9,282

10,250

8,226

1,760

Net Interest Income

9,340

11,244

12,485

12,874

13,748

3,648

Loan Loss Provisions

324

360

420

3,955

7,347

500

Non-Interest Income

2,196

2,207

2,167

2,473

3,183

941

Non-Interest Expense

8,031

8,961

10,398

11,942

13,909

3,241

Net Income

2,160

2,780

2,638

(275)

(3,277)

586

Net Income Available to Common

2,160

2,780

2,638

(275)

(3,872)

417

Operating Revenue

11,536

13,451

14,652

15,347

16,931

4,589

Pre-Tax Pre-Provision

3,505

4,490

4,254

3,405

3,022

1,348

20

Historical Key Ratios

Source: Company data from 10-Q and 10-K filings

Note: Non-performing assets excludes restructured loans

Note: Texas ratio = (non-performing assets + loans 90 days or greater past

due) / (tangible equity + loan loss reserve)

due) / (tangible equity + loan loss reserve)

2005

2006

2007

2008

2009

3/31/2010

Performance Ratios

Net Interest Margin

4.39%

4.57%

4.35%

3.71%

3.67%

4.04%

Yield on Interest Earning Assets

6.39%

7.26%

7.58%

6.66%

5.87%

5.99%

Cost of Funds

2.04%

2.77%

3.31%

3.00%

2.28%

1.97%

Efficiency Ratio

69.6%

66.6%

71.0%

77.9%

82.2%

70.6%

Non-Interest Income / Avg. Assets

0.93%

0.83%

0.70%

0.66%

0.80%

0.95%

Non-Interest Expense / Avg. Assets

3.42%

3.39%

3.36%

3.21%

3.49%

3.27%

Return on Avg. Assets

0.92%

1.05%

0.85%

-0.07%

-0.97%

0.42%

Return on Avg. Equity

10.31%

11.94%

10.24%

-0.98%

-11.42%

4.91%

Loans / Deposits

98.3%

103.6%

102.0%

107.6%

95.3%

91.9%

Capitalization

Tang. Common Equity / Tang. Assets

8.83%

8.79%

7.96%

6.73%

5.90%

5.92%

Leverage Ratio

10.97%

10.82%

9.46%

8.03%

9.76%

9.82%

Tier 1 Ratio

13.48%

12.76%

10.95%

8.77%

10.94%

11.31%

Total Capital Ratio

14.70%

13.95%

11.96%

10.03%

12.20%

12.57%

Credit Quality

Non-Performing Assets / Assets

0.17%

0.11%

0.16%

4.70%

3.90%

3.13%

Non-Accrual Loans / Loans

0.21%

0.15%

0.20%

4.71%

3.63%

2.87%

Net Charge-Offs / Avg. Loans

0.03%

0.00%

0.09%

0.61%

1.49%

0.51%

Reserves / Loans

1.19%

1.19%

0.97%

1.39%

2.20%

2.28%

Reserves / Non-Performing Assets

533.6%

808.1%

490.2%

25.2%

46.1%

57.6%

Reserves / Non-Accrual Loans

556.0%

808.1%

495.6%

29.6%

60.7%

79.3%

Texas Ratio

1.8%

1.2%

1.8%

62.8%

37.5%

30.1%