Table of Contents

As filed with the Securities and Exchange Commission on January 13, 2011

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Capital Auto Receivables LLC

(Depositor)

(Exact name of Registrant as Specified in its Charter)

| Delaware | 6189 | 38-3082892 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

Capital Auto Receivables LLC Corporation Trust Center 1209 Orange Street Wilmington, Delaware 19801 (313-656-5500) | Ryan C. Farris, Vice President Capital Auto Receivables LLC 200 Renaissance Center Detroit, Michigan 48265 (313-656-5500) | |

(Address, including zip code, and telephone number, including area code, of principal executive offices of Registrant) | (Name, address, including zip code, and telephone number, including area code, of agent for service) |

With A Copy To:

Kenneth P. Morrison, P.C. Janette A. McMahan Kirkland & Ellis LLP 300 North LaSalle Street Chicago, Illinois 60654 (312-862-2000) | Richard V. Kent, Esq. General Counsel Capital Auto Receivables LLC 200 Renaissance Center Detroit, Michigan 48265 (313-656-5500) | Elizabeth A. Raymond Mayer Brown LLP 71 South Wacker Drive Chicago, Illinois 60606 (312-782-0600) |

Approximate Date of Commencement of Proposed Sale to the Public: from time to time after the effective date of this Registration Statement as determined in light of market conditions.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box. ¨

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend reinvestment plans, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ¨

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Unit(1) | Proposed Maximum Aggregate Offering Price(1) | Amount Of Registration Fee(2) | ||||

Asset Backed Securities | $0(2) | 100% | $0 | $0 | ||||

| (1) | Estimated solely for the purpose of calculating the registration fee. |

| (2) | The Registrant previously filed a Registration Statement on Form S-3 (Registration No. 333-147112) (as amended, the “Prior Registration Statement”) with the Securities and Exchange Commission, which became effective on January 18, 2008. Pursuant to the Prior Registration Statement, there are $18,052,591,000 of unsold amount of Asset Backed Securities thereunder as of the date of this Registration Statement (the “Unsold Securities”). A filing fee of $554,214.54 was paid in connection with the Unsold Securities. Pursuant to Rule 415(a)(6) of the Securities and Exchange Commission’s Rules and Regulations under the Securities Act of 1933, as amended, the Unsold Securities under the Prior Registration Statement are included in this Registration Statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus supplement and the accompanying prospectus is not complete and may be changed. We may not sell the securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus supplement and the accompanying prospectus are not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated , 20

Prospectus Supplement to Prospectus dated , 20 .

CAPITAL AUTO RECEIVABLES ASSET TRUST 20 -

Issuing Entity

$ Asset Backed Notes, Class A

$ Asset Backed Notes, Class B

$ Asset Backed Notes, Class C

CAPITAL AUTO RECEIVABLES LLC

Depositor

ALLY FINANCIAL INC.

Sponsor and Servicer

You should carefully consider the risk factors beginning on page S-9 in this prospectus supplement and page 2 in the prospectus.

The notes represent obligations of the issuing entity only. The notes do not represent obligations of or interests in, and are not guaranteed by, Ally Auto Assets LLC, Ally Bank, Ally Financial Inc. or any of their affiliates. Neither the notes nor the receivables are insured or guaranteed by any governmental entity.

This prospectus supplement may be used to offer and sell the notes only if accompanied by the prospectus. | [Class A-1 Notes] | Class A-2 Notes] | Class A-3 Notes | Class A-4 Notes | Class B Notes | Class C Notes | ||||||||||||||||||

| [A-2a Notes] | [A-2b Notes] | [A-4a Notes] | [A-3b Notes] | [A-4a Notes] | [A-4b Notes] | |||||||||||||||||||

| Principal Balance Interest Rate | [ ]% | [ ]% | [One- Month LIBOR plus ]% | [ ]% | [One- Month LIBOR plus ]% | [ ]% | [One- Month LIBOR plus ]% | [ ]% | [ ]% | |||||||||||||||

| Initial Distribution Date | ||||||||||||||||||||||||

| Final Scheduled Distribution Date | ||||||||||||||||||||||||

| Distribution Frequency | [Monthly] | [Monthly] | [Monthly] | [Monthly] | [Monthly] | [Monthly] | [Monthly] | [Monthly] | [Monthly] | |||||||||||||||

| Price to Public | ||||||||||||||||||||||||

| Underwriting Discount | ||||||||||||||||||||||||

| Proceeds to Depositor | ||||||||||||||||||||||||

The interest rate for each class of notes will be a fixed rate[, a floating rate or a combination of a fixed rate and floating rate if that class has both a fixed rate tranche and a floating rate tranche.

The aggregate principal amount of the notes being offered under this prospectus supplement is $ . | ||||||||||||||||||||||||

Credit Enhancement and Liquidity

| • | Reserve account, with an initial deposit of $ . |

| • | Overcollateralization in the initial amount of $ . |

| • | Class D Asset Backed Notes, with a principal balance of $ . The Class D Notes are not being offered under this prospectus supplement and will instead be sold in a private placement or retained by the depositor initially. |

| • | The Class D Notes are subordinated to the Class A Notes, the Class B Notes and the Class C Notes. |

| • | The Class C Notes are subordinated to the Class A Notes and the Class B Notes. |

| • | The Class B Notes are subordinated to the Class A Notes. |

| • | If the issuing entity issues floating rate notes, the issuing entity will enter into an interest rate swap with respect to each class or tranche of floating rate notes, with [ ] as the swap counterparty. |

| • | [Revolving Period. The issuing entity will not pay principal during the revolving period, which is scheduled to terminate on , . However, if the revolving period terminates early as a result of an early amortization event, principal payments may commence prior to that date.] |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus supplement or the prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

[Underwriters]

The date of this prospectus supplement is , 20

Table of Contents

IMPORTANT NOTICE ABOUT INFORMATION PRESENTED IN THIS

PROSPECTUS SUPPLEMENT AND THE ACCOMPANYING PROSPECTUS

We provide information to you about the notes in two separate documents:

| • | the prospectus, which provides general information and terms of the notes, some of which may not apply to a particular series of notes, including your series, and |

| • | this prospectus supplement, which provides information regarding the pool of receivables held by the issuing entity and specifies the terms of your series of notes. |

You should rely only on the information provided in the accompanying prospectus, this prospectus supplement, and any pricing supplement hereto, including the information incorporated by reference in the accompanying prospectus and this prospectus supplement. We have not authorized anyone to provide you with other or different information. We are not offering the notes in any state where the offer is not permitted.

You can find definitions of the capitalized terms used in this prospectus supplement in the “Glossary of Terms to Prospectus Supplement,” which appears at the end of this prospectus supplement and in the “Glossary of Terms to Prospectus,” which appears at the end of the accompanying prospectus.

The term “Ally Financial,” when used in connection with Ally Financial’s capacity as acquirer of the receivables, seller of the receivables to the depositor or servicer of the receivables, includes any successors or assigns of Ally Financial in such capacity permitted pursuant to the transaction documents.

i

Table of Contents

Prospectus Supplement

ii

Table of Contents

| S-56 | ||||

| S-56 | ||||

| S-58 | ||||

| S-58 | ||||

| S-59 | ||||

| A-1 | ||||

Prospectus | ||||

| 2 | ||||

| 6 | ||||

| 7 | ||||

| 7 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 14 | ||||

| 16 | ||||

| 16 | ||||

| 16 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 23 | ||||

| 24 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 27 | ||||

| 29 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 32 | ||||

| 32 | ||||

Changes to Servicer; Servicer Indemnification and Proceedings | 33 | |||

| 33 | ||||

| 34 | ||||

| 34 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 37 | ||||

iii

Table of Contents

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 39 | ||||

| 39 | ||||

Effects of Bankruptcy on Payments on the Notes and Certificates | 40 | |||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 44 | ||||

| 44 | ||||

| 45 | ||||

| 45 | ||||

| 46 | ||||

| 46 | ||||

| 46 | ||||

| 47 | ||||

| 47 | ||||

| 47 | ||||

| 49 |

iv

Table of Contents

This summary highlights selected information from this document and does not contain all of the information that you need to consider in making your investment decision. To understand the material terms of this offering of the offered notes, carefully read this entire document and the accompanying prospectus.

THE PARTIES

Sponsor

Ally Financial Inc., formerly known as GMAC Inc., or“Ally Financial.”

Issuing Entity

Capital Auto Receivables Asset Trust 20 - will be the issuing entity of the notes and the certificates. In this prospectus supplement and in the accompanying prospectus, we also refer to the issuing entity as the“trust.”

Depositor

Capital Auto Receivables LLC will be the depositor to the issuing entity.

Servicers

Ally Financial will be the servicer and Ally Servicing LLC, formerly known as Semperian LLC, will be the sub-servicer providing collection and administrative servicing for Ally Financial.

Indenture Trustee

[ ]

Owner Trustee

[ ]

THE NOTES

The issuing entity will offer the classes of notes listed on the cover page of this prospectus supplement. The notes will be available for purchase in denominations of $1,000 and integral multiples thereof, and will be available in book-entry form only. We sometimes refer to these notes as the“offered notes.”

The final scheduled distribution dates of the offered notes are listed on the cover page of this prospectus supplement.

The issuing entity will also issue [Class A-1 Notes with an initial principal balance of $ and] Class D Notes with an initial principal balance of $ . [The Class A-1 Notes will have a final scheduled distribution date of , 20 .] The Class D Notes will have a final scheduled distribution date of , 20 . [The Class A-1 Notes and] [t]he Class D Notes are not being offered under this prospectus supplement [and will be] [sold in one or more private placements] [or] [and] [initially retained by the depositor]. [If the Class D Notes are initially retained by the depositor, the depositor will retain the right to sell all or a portion of those retained notes at any time.]

Interest Payments

| • | The interest rate for each class of notes will be a fixed rate[, a floating rate or the combination of a fixed rate and a floating rate if that class has both a fixed rate tranche and a floating rate tranche]. [For example, the Class A-3 Notes may be divided into fixed and floating rate tranches, in which case the Class A-3a Notes will be the fixed rate notes and the Class A-3b Notes will be the floating rate notes.] We refer in this prospectus supplement to notes that bear interest at a [floating rate as“floating rate notes,”and to notes that bear interest at a] fixed rate as“fixed rate notes.” |

| • | [For each class or tranche of floating rate notes, if any, the issuing entity will enter into a corresponding interest rate swap.] |

| • | Interest will accrue on the notes from and including the closing date. |

S-1

Table of Contents

| • | The issuing entity will pay interest on the notes on the fifteenth day of each calendar month, or if that day is not a business day, the next business day, beginning on , 20 . We refer to these dates as“distribution dates.” |

| • | The issuing entity will pay interest on the [fixed rate] notes, other than the Class A-1 Notes, on each distribution date based on a 360-day year consisting of twelve 30-day months. The issuing entity will pay interest on the Class A-1 Notes on each distribution date based on the actual days elapsed during the period for which interest is payable and a 360-day year. |

| • | [The issuing entity will pay interest on the floating rate notes on each distribution date based on the actual days elapsed during the period for which interest is payable and a 360-day year.] |

| • | Interest payments on all classes of the Class A Notes will have the same priority. |

| • | The payment of interest on the Class B Notes is subordinated to the payment of interest on, and in limited circumstances payments of principal of, the Class A Notes, the payment of interest on the Class C Notes is subordinated to the payment of interest on, and in limited circumstances payments of principal of, the Class A Notes and the Class B Notes, and the payment of interest on the Class D Notes is subordinated to the payment of interest on, and in limited circumstances payments of principal of, the Class A Notes, the Class B Notes and the Class C Notes, in each case to the extent described in“Priority of Distributions[—Amortization Period] [— General].”In general, no interest will be paid on the Class B Notes on any distribution date until all interest due and payable on the Class A Notes has been paid in full, no interest will be paid on the Class C Notes on any distribution date until all interest due and payable on the Class A Notes and the Class B Notes has been paid in full, and no interest will be paid on the Class D Notes on any distribution date until all interest |

due and payable on the Class A Notes, the Class B Notes and the Class C Notes has been paid in full. |

Principal Payments

| • | [The issuing entity will not pay principal on the notes on any distribution date related to the revolving period.] |

| • | The issuing entity will pay principal on the notes monthly on each distribution date [related to the amortization period]. |

| • | The issuing entity will make principal payments on the notes based on the amount of collections and defaults on the receivables during the prior month. |

| • | On each distribution date [related to the amortization period], except as described below under“Priority of Distributions—Acceleration,”the amounts available to make principal payments on the notes will be applied as follows: |

| (1) | to the Class A-1 Notes, until the Class A-1 Notes are paid in full, |

| (2) | to the Class A-2 Notes, until the Class A-2 Notes are paid in full, |

| (3) | to the Class A-3 Notes, until the Class A-3 Notes are paid in full, |

| (4) | to the Class A-4 Notes, until the Class A-4 Notes are paid in full, |

| (5) | to the Class B Notes, until the Class B Notes are paid in full, |

| (6) | to the Class C Notes, until the Class C Notes are paid in full, and |

| (7) | to the Class D Notes, until the Class D Notes are paid in full. |

| • | The failure of the issuing entity to pay any class of notes in full on or before its final scheduled distribution date will constitute an event of default. |

S-2

Table of Contents

THE CERTIFICATES

On the closing date, the issuing entity will issue certificates. The certificates will be retained by the depositor and are not being offered under this prospectus supplement. The depositor will retain the right to sell all or a portion of the certificates at any time.

THE RECEIVABLES

Property of the Issuing Entity

The primary assets of the issuing entity will be a pool of fixed rate retail motor vehicle instalment sales contracts and direct purchase money loans used to finance the purchase of new and used cars and light trucks. We refer to the persons who financed their purchases with these contracts and loans as“obligors.”A portion of the contracts and loans sold to the issuing entity on the closing date [or during the revolving period] were [or will be] acquired or originated by Ally Financial or its subsidiaries under special incentive rate financing programs, and we refer to those contracts and loans as“subvented receivables.”We refer to the remaining contracts and loans that are not subvented receivables and are sold to the issuing entity on the closing date [or during the revolving period] as“non-subvented receivables.”We use the term“receivables”to mean both subvented receivables and non-subvented receivables. Further, when we use the term“remaining payments”on receivables as of a specific date, we mean all scheduled payments that have not been received prior to that specified date.

The receivables in the issuing entity will be sold on the closing date [and on each distribution date during the revolving period] by Ally Financial to the depositor, and then by the depositor to the issuing entity. The issuing entity will grant a security interest in the receivables and the other property of the issuing entity to the indenture trustee on behalf of the noteholders. Ally Financial or the depositor may be required to repurchase receivables from the issuing entity in specified circumstances, as detailed in the accompanying prospectus under“The Servicer—Servicing Procedures.”

The issuing entity’s property will, subject to other specific exceptions described in the prospectus, also include:

| • | the remaining payments on the receivables as of a cutoff date of , 20 and monies received with respect to those remaining payments; we refer to that date as the“[initial] cutoff date,” |

| • | [the remaining payments on the additional receivables as of the first calendar day of each month in which a pool of additional receivables is purchased and monies received with respect to those remaining payments; we refer to each of those dates as a“subsequent cutoff date,” and we refer to the cutoff date related to a particular receivable as the“applicable cutoff date” for that receivable,] |

| • | amounts held on deposit in trust accounts maintained for the issuing entity, |

| • | security interests in the vehicles financed by the receivables, |

| • | any recourse Ally Financial has against the dealers from which it purchased the receivables, |

| • | any proceeds from claims on insurance policies covering the financed vehicles, |

| • | the interest rate swaps and contingent assignment, if any, described below, |

| • | specified rights of the depositor under its purchase agreement with Ally Financial, and |

| • | all rights of the issuing entity under the related transfer agreement with the depositor. |

Receivables Principal Balance

The initial aggregate discounted principal balance of the subvented receivables to be sold to the issuing entity on the closing date, which is

S-3

Table of Contents

the present value of all remaining payments as of the [initial] cutoff date, discounted for each receivable, at the greater of % per annum and the actual annual percentage rate of the receivable, is $ . The initial aggregate discounted principal balance of the non-subvented receivables to be sold to the issuing entity on the closing date, which is the present value of all remaining payments as of the [initial] cutoff date, discounted for each receivable, at the greater of % per annum and the actual annual percentage rate of the receivable, is $ . The combined initial aggregate discounted principal balance of all the receivables, as calculated for each type of receivable as set forth above, as of the [initial] cutoff date is $ . We refer to this initial balance as the“initial aggregate receivables principal balance.”We refer to the aggregate principal balance of all receivables, as calculated for each type of receivable as of any given time, as the“aggregate receivables principal balance.”

As of the [initial] cutoff date, the % discount rate was applied to a receivables balance of $ , which is approximately % of the aggregate amount financed of all receivables of the issuing entity.

Overcollateralization

The initial aggregate receivables principal balance will exceed the aggregate principal balance of the notes on the closing date by approximately % of the initial aggregate receivables principal balance. [The application of funds as described in the [ninth] priority of distributions is designed to increase over time the amount of overcollateralization as of any distribution date to a target amount, which we refer to as the] [We use the term] [“overcollateralization target amount”] [to mean %] [The overcollateralization target amount will be %] of the initial aggregate receivables principal balance.

[Depositor Repurchase Option

The depositor has a one-time option to purchase receivables in an amount no greater than [ ]% of the initial aggregate receivables principal balance.]

[THE REVOLVING PERIOD

The issuing entity will not make payments of principal on the notes on distribution dates related to the revolving period.

The“revolving period” consists of the monthly periods from through , and the related distribution dates. We refer to the monthly periods and the related distribution dates following the revolving period as the“amortization period.”

If an early amortization event occurs, the revolving period will terminate early, and the amortization period will begin. See“The Transfer and Servicing Agreements—The Revolving Period” in this prospectus supplement.

On each distribution date related to the revolving period, amounts otherwise available to make principal payments on the notes will be applied to purchase additional receivables from the depositor for the purposes of maintaining the initial aggregate receivables principal balance and achieving the overcollateralization target amount. See“The Receivables Pool—Criteria Applicable to the Selection of Additional Receivables During the Revolving Period” in this prospectus supplement.

The amount of additional receivables and percentage of asset pool will be determined by the amount of cash available from payments and prepayments on existing assets. There are no stated limits on the amount of additional receivables allowed to be purchased during the revolving period in terms of either dollars or percentage of the initial asset pool. See“The Transfer and Servicing Agreements—The Revolving Period” in this prospectus supplement.

To the extent that amounts allocated for the purchase of additional receivables are not so used on any distribution date related to the revolving period, they will be deposited into the accumulation account and applied on subsequent

S-4

Table of Contents

distribution dates related to the revolving period to purchase additional receivables from the depositor.]

PRIORITY OF DISTRIBUTIONS

[Revolving Period

During the revolving period, the issuing entity will distribute available funds in the following order of priority:

| • | basic servicing fee payments to the servicer, |

| • | [if the issuing entity issues floating rate notes, the net amount payable, if any, to the swap counterparty, other than any swap termination amounts,] |

| • | interest on the Class A Notes [and any [senior] swap termination amounts on interest rate swaps related to the Class A Notes, pro rata,] |

| • | interest on the Class B Notes, |

| • | interest on the Class C Notes, |

| • | interest on the Class D Notes, |

| • | reinvestments in additional receivables and deposits into the accumulation account, as applicable, in the amount by which the aggregate principal balance of the notes exceeds the aggregate receivables principal balance, |

| • | [any subordinate swap termination payments on any interest rate swap related to the Class A Notes,] |

| • | [any costs of the indenture trustee incurred associated with a resignation of the servicer and the appointment of a successor servicer, to the indenture trustee,] |

| • | deposits into the reserve account, until the amount in the reserve account equals the specified reserve account balance, |

| • | reinvestments in additional receivables and deposits into the accumulation account, as applicable, in the amount by which the |

aggregate principal balance of the notes exceeds the aggregate receivables principal balance, as increased above, plus the amounts deposited in the accumulation account above, minus the overcollateralization target amount, |

| • | additional servicing fee payments to the servicer, and |

| • | any remaining amounts, to the certificateholders.] |

[Amortization Period] [General]

During the amortization period, [T]he issuing entity will distribute available funds in the following order of priority:

| • | basic servicing fee payments to the servicer, |

| • | if the issuing entity issues floating rate notes, the net amount payable, if any, to the swap counterparty, other than any swap termination amounts, |

| • | interest on the Class A Notes and any [senior] swap termination amounts on interest rate swaps related to the Class A Notes, if any, pro rata, |

| • | principal on the notes in an amount equal to the excess, if any, of the aggregate principal balance of the Class A Notes over the aggregate receivables principal balance, |

| • | interest on the Class B Notes, |

| • | principal on the notes in an amount equal to the excess, if any, of the aggregate principal balance of the Class A Notes and the Class B Notes—reduced by the amount of principal allocated to the notes above—over the aggregate receivables principal balance, |

| • | interest on the Class C Notes, |

| • | principal on the notes in an amount equal to the excess, if any, of the aggregate principal balance of the Class A Notes, the Class B Notes and the Class C Notes—reduced by the amounts of principal allocated to the notes above—over the aggregate receivables principal balance, |

S-5

Table of Contents

| • | interest on the Class D Notes, |

| • | principal on the notes in an amount equal to the excess, if any, of the aggregate principal balance of the notes—reduced by the amounts of principal allocated to the notes above—over the aggregate receivables principal balance, |

| • | deposits into the reserve account, until the amount in the reserve account equals the specified reserve account balance, |

| • | principal on the notes in an amount equal to the lesser of (a) the aggregate principal balance of the notes—reduced by the amounts of principal allocated to the notes above, and (b) the excess of the aggregate principal balance of the notes—reduced by the amounts of principal allocated to the notes above—over an amount equal to the aggregate receivables principal balance minus the overcollateralization target amount, |

| • | [any costs of the indenture trustee incurred associated with a resignation of the servicer and the appointment of a successor servicer, to the indenture trustee,] |

| • | [any subordinate swap termination payments on any interest rate swaps related to the Class A Notes,] |

| • | [additional servicing fee payments to the servicer,] and |

| • | any remaining amounts, to the certificateholders. |

Acceleration

If an event of default occurs and the notes are accelerated, until the time when all events of default have been cured or waived as provided in the indenture, the issuing entity will pay interest and principal first on the Class A Notes. Interest will be paid pro rata among the classes of Class A Notes, and principal will be paid

sequentially by class starting with the Class A-1 Notes. No interest or principal will be payable on the Class B Notes until all principal of and interest on the Class A Notes have been paid in full, no interest or principal will be payable on the Class C Notes until all principal of and interest on the Class A Notes and the Class B Notes have been paid in full, and no interest or principal will be payable on the Class D Notes until all principal of and interest on the Class A Notes, the Class B Notes and the Class C Notes have been paid in full.

RESERVE ACCOUNT

On the closing date, the depositor will deposit $ in cash or eligible investments into the reserve account. Collections on the receivables, to the extent available for this purpose, will be added to the reserve account on each distribution date, until the amount in the reserve account equals the specified reserve account balance. See“The Transfer and Servicing Agreements—Reserve Account”in this prospectus supplement for additional information.

To the extent that funds from principal and interest collections on the receivables are not sufficient to pay the basic servicing fee and to pay the amounts that are prior to the deposits into the reserve account as described under“Priority of Distributions”above, the amount previously deposited in the reserve account provides an additional source of funds for those payments.

[INTEREST RATE SWAPS

For each tranche of floating rate notes, if any, the issuing entity will enter into an interest rate swap with [ ] as the“swap counterparty”with respect to each class or tranche of floating rate notes.

Under each interest rate swap, on the business day prior to each distribution date, the issuing entity will be obligated to pay the swap counterparty an amount based on the notional amount of the related class or tranche of notes and a fixed interest rate and the swap counterparty will be obligated to pay the issuing

S-6

Table of Contents

entity an amount based on the notional amount of the related class or tranche of notes and a floating interest rate of [One]-Month LIBOR plus an applicable spread, if any. For each swap, the notional amount will equal the outstanding principal balance of the related class or tranche of notes. See“The Transfer and Servicing Agreements—Interest Rate Swaps”in this prospectus supplement for additional information.]

SERVICING FEES

The issuing entity will pay monthly to the servicer (a) a basic servicing fee equal to 1.00% per annum as compensation for servicing the receivables, (b) [an additional servicing fee up to 1% per annum, as described in the prospectus, that will be subordinated to all payments on the notes, and (c)] a supplemental servicing fee equal to any late fees, prepayment charges and other administrative fees and expenses collected during the month and investment earnings on the trust accounts.

REDEMPTION OF THE NOTES

When the aggregate receivables principal balance declines to % or less of the initial aggregate receivables principal balance, the servicer may purchase all of the remaining receivables. If the servicer purchases the receivables, the outstanding notes will be redeemed at a price equal to their remaining principal balance, plus accrued and unpaid interest thereon.

TAX STATUS

Kirkland & Ellis LLP, special tax counsel, has delivered its opinion that:

| • | the offered notes will be characterized as indebtedness for federal income tax purposes, and |

| • | the issuing entity will not be taxable as an association or publicly traded partnership taxable as a corporation. |

Each noteholder, by accepting an offered note, will agree to treat the offered notes as indebtedness for federal, state and local income and franchise tax purposes.

ERISA CONSIDERATIONS

Subject to the restrictions and considerations discussed under“ERISA Considerations”in this prospectus supplement and in the prospectus, the offered notes may be purchased by or for the account of (a) an “employee benefit plan” as defined in Section 3(3) of the Employee Retirement Income Security Act of 1974, as amended(“ERISA”), that is subject to the provisions of Title I of ERISA, (b) a “plan” as subject to Section 4975 of the Internal Revenue Code of 1986, as amended or (c) any entity whose underlying assets include “plan assets” by reason of an employee benefit plan’s or a plan’s investment in the entity. We suggest that any of the foregoing types of entities consult with counsel before purchasing the offered notes. See“ERISA Considerations”in this prospectus supplement and the prospectus for additional information.

[MONEY MARKET INVESTMENTS

The Class A-1 Notes will be “eligible securities” for purchase by money market funds under Rule 2a-7 under the Investment Company Act of 1940, as amended. Rule 2a-7 includes additional criteria for investments by money market funds. In May 2010, Rule 2a-7 was amended to include additional requirements relating to portfolio maturity, liquidity and risk diversification. If you are a money market fund contemplating a purchase of Class A-1 Notes, you should consult your counsel before making a purchase.]

RATINGS

We expect that the offered notes will receive credit ratings from at least two nationally recognized rating agencies hired by us.

The rating agencies have discretion to monitor and adjust the ratings on the offered notes. The offered notes may receive an unsolicited rating that is different from or lower than the ratings

S-7

Table of Contents

provided by the rating agencies hired to rate the offered notes. As of the date of this prospectus supplement, we are not aware of any unsolicited ratings on the offered notes. A rating, change in rating or a withdrawal of a rating by one rating agency may not correspond to a rating, change in rating or withdrawal of a rating from any other rating agency. See“The Ratings for the Securities Are Limited in Scope, May Be Unsolicited, May Not Continue to Be Issued and Do Not Consider the Suitability of the Securities for You” in the prospectus for more information.

RISK FACTORS

Before making an investment decision, you should consider carefully the factors that are set forth in“Risk Factors”beginning on page S-8 of this prospectus supplement and page 2 of the prospectus.

S-8

Table of Contents

In addition to the risk factors beginning on page 2 of the prospectus, you should consider the following risk factors in deciding whether to purchase the offered notes.

| Financial Market Disruptions and a Lack of Liquidity in the Secondary Market Could Adversely Affect the Market Value of Your Notes and/or Limit Your Ability to Resell Your Notes | The securities will not be listed on any securities exchange. Therefore, in order to sell your securities, you will need to find a willing buyer. The underwriters may assist in the resale of securities, but they are not required to do so. Additionally, recent and continuing events in the global financial markets, including the failure, acquisition or government seizure of several major financial institutions, the establishment of government bailout programs for financial institutions, problems related to subprime mortgages and other financial assets, the de-valuation of various assets in secondary markets, the forced sale of asset-backed and other securities as a result of the de-leveraging of structured investment vehicles, hedge funds, financial institutions and other entities, and the lowering of ratings on certain asset-backed securities, have caused a significant reduction in liquidity in the secondary market for asset-backed securities. This period of illiquidity may continue, and even worsen, and may adversely affect both the market value of your notes and your ability to sell the notes. As a result, you may be unable to obtain the price that you wish to receive for your notes or you may suffer a loss on your investment. Illiquidity can have a severely adverse effect on the prices of securities that are especially sensitive to prepayment, credit or interest rate risk, such as the notes. | |

| Recent Economic Developments May Adversely Affect the Performance and Market Value of Your Notes | The United States is experiencing a period of economic weakness that may adversely affect the performance and market value of your notes. This period has been accompanied by rising unemployment, decreases in home values, increased mortgage and consumer loan delinquencies and defaults and a lack of availability of consumer credit, which may lead to increased default rates on the receivables. If the economic downturn worsens or continues for a prolonged period of time, delinquencies and losses with respect to motor vehicle receivables could continue to increase, which could result in losses on your notes. In addition, this period has been accompanied by decreased consumer demand for motor vehicles and an increase in the inventory of used motor vehicles, which may depress the price at which repossessed motor vehicles may be sold or delay the timing of those sales. If the default rate on the receivables increases and the price at which the related vehicles may be sold declines, you may experience losses with respect to your notes. | |

S-9

Table of Contents

| The Sponsor, the Servicer and their Affiliates Must Comply with Governmental Laws and Regulations that are Subject to Change and Involve Significant Costs | Ally Financial and their affiliates are governed by numerous foreign, federal and state laws and the supervision and examination of various regulatory agencies. In July 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”), which is likely to adversely affect the financial services industry. The financial services industry will undergo increased regulation, such as additional disclosure and other obligations, restrictions on pricing and enforcement proceedings. The Dodd-Frank Act also creates a Consumer Financial Protection Bureau with rulemaking and enforcement authority over consumer finance businesses.

Compliance with applicable law and regulations may be costly because new processes, forms, controls and additional infrastructure may be required to comply with new requirements. Laws in the financial services industry are designed primarily for the protection of consumers. Any failure to comply with these laws and regulations could result in significant statutory civil and criminal penalties, monetary damages, attorneys’ fees and costs, possible revocation of licenses and damage to reputation, brand and valued customer relationships. Many provisions of the Dodd- Frank Act are required to be implemented through rulemaking by the applicable federal regulatory agencies. Therefore, the full impact of the Dodd-Frank Act on the financial markets and its participants and on the asset backed securities market in particular will not be known for some time. No assurance can be given that the Dodd-Frank Act and its implementing regulations, or the imposition of additional regulations including the orderly liquidation authority of the Dodd-Frank Act, will not have a significant adverse impact on the issuing entity, the depositor, the sponsor, or the servicer, including on the servicing of the receivables, or the price that a subsequent purchaser would be willing to pay for your notes. |

S-10

Table of Contents

| [New Car Incentive Purchase Programs and other Market Factors May Reduce the Value of the Vehicles that Secure the Receivables] | [The pricing of used cars is affected by the supply and demand for those cars, which, in turn, is affected by consumer demand and tastes, economic factors (including the price of gasoline and closure of dealerships), the introduction and pricing of new car models and other factors. Decisions by a manufacturer with respect to new vehicle production and brands, pricing and incentives may affect used car prices, particularly those for the same or similar models. An increase in the supply or a decrease in the demand for used cars may negatively impact the resale value of the vehicles securing the receivables. Decreases in the value of those vehicles may, in turn, reduce the incentive of obligors to make payments on the receivables and decrease the proceeds realized by the issuing entity from vehicle repossessions, which could result in losses on your notes.] | |

| The Class A Notes are Subject to Risk Because Payments on the Class A Notes are Subordinated to Servicing Fees and Other Payments | The Class A Notes are subject to risk because payments of principal and interest on the Class A Notes are subordinated, as described below, to servicing fees and other payments.

Principal and interest payments on the Class A Notes on each distribution date will be subordinated to the basic servicing fee due to the servicer and all payments owing to the swap counterparty in relation to the interest rate swaps, other than termination payments. Senior swap termination payments, if any, owing to the swap counterparty on the interest rate swaps related to the Class A Notes will be paid ratably with interest on the Class A Notes in proportion to their respective amounts.

This subordination could result in reduced or delayed payments of principal and interest on the Class A Notes. | |

| Class B Notes are Subject to Greater Risk Because the Class B Notes are Subordinated to the Class A Notes | The Class B Notes bear greater risks than the Class A Notes because payments of interest and principal on the Class B Notes are subordinated, to the extent described below, to payments of interest and principal on the Class A Notes.

Interest payments on the Class B Notes on each distribution date will be subordinated to servicing fees due to the servicer, payments to the swap counterparty, interest payments on the Class A Notes, and principal payments to the Class A Notes to the extent the aggregate principal balance of the Class A Notes as of the preceding distribution date exceeds the aggregate receivables principal balance as of the close of business on the last day of the immediately preceding monthly period. In addition, on each distribution date after an event of default occurs and the notes are accelerated, until the time when all events of default have been cured or waived as provided in the indenture, no interest will be paid on the Class B Notes until all principal of and interest on the Class A Notes have been paid in full. | |

S-11

Table of Contents

Principal payments on the Class B Notes will be subordinated in priority to the Class A Notes. No principal will be paid on the Class B notes until all principal of the Class A Notes has been paid in full. See“The Transfer and Servicing Agreements—Distributions” in this prospectus supplement.

This subordination could result in reduced or delayed payments of principal and interest on the Class B Notes. | ||

| Class C Notes are Subject to Greater Risk Because the Class C Notes are Subordinated in Priority to the Class A Notes and the Class B Notes | The Class C notes bear greater risks than the Class A Notes and the Class B Notes because payments of interest and principal on the Class C Notes are subordinated, to the extent described below, to payments of interest and principal on the Class A Notes and Class B Notes.

Interest payments on the Class C Notes on each distribution date will be subordinated to servicing fees due to the servicer, payments to the swap counterparty, interest payments on the Class A Notes and the Class B Notes, and principal payments to the Class A Notes and the Class B Notes to the extent the aggregate principal balance of the Class A Notes and the Class B Notes as of the preceding distribution date exceeds the aggregate receivables principal balance as of the close of business on the last day of the immediately preceding monthly period. In addition, on each distribution date after an event of default occurs and the notes are accelerated, until the time when all events of default have been cured or waived as provided in the indenture, no interest will be paid on the Class C Notes until all principal of and interest on the Class A Notes and the Class B Notes have been paid in full.

Principal payments on the Class C Notes will be subordinated in priority to the Class A Notes and the Class B Notes. No principal will be paid on the Class C Notes until all principal of the Class A Notes and the Class B Notes has been paid in full. See“The Transfer and Servicing Agreements—Distributions” in this prospectus supplement.

This subordination could result in reduced or delayed payments of principal of and interest on the Class C Notes. | |

S-12

Table of Contents

| [Availability of Additional Receivables During the Revolving Period Could Shorten the Average Life of the Notes] | [During the revolving period, the issuing entity will not make payments of principal on the notes. Instead, the issuing entity will purchase additional receivables from the depositor. The purchase of additional receivables will lengthen the average life of the notes compared to a transaction without a revolving period. However, an unexpectedly high rate of collections on the receivables during the revolving period, a significant decline in the number of receivables available for purchase or the inability of the depositor to acquire new receivables could affect the amount of additional receivables that the issuing entity is able to purchase. If the issuing entity is unable to reinvest the available reinvestment funds by the end of the revolving period, then the average life of the notes will shorten.

Amounts allocable to principal payments on the notes that are not used to purchase additional receivables during the revolving period will be deposited into the accumulation account. Among other early amortization events, it will be an early amortization event if the amount in the accumulation account on any distribution date during the revolving period exceeds [1.00]% of the initial aggregate receivables principal balance. See“The Transfer of Servicing Agreements—The Revolving Period” in this prospectus supplement. If that happens, the revolving period will terminate and the amortization period will commence, shortening the average life of the notes.

A variety of unpredictable economic, social and other factors may influence the availability of additional receivables. You will bear all reinvestment risk resulting from a longer or shorter than anticipated average life of the notes.] | |

| [Failure by the Swap Counterparty to Make Payments to the Issuing Entity and the Seniority of Payments Owed to the Swap Counterparty Could Reduce or Delay Payments on the Notes] | [As described further in the“The Transfer and Servicing Agreements—Interest Rate Swaps” in this prospectus supplement, if the issuing entity issues floating rate notes, the issuing entity will enter into a related interest rate swap because the receivables owned by the issuing entity bear interest at a fixed rate while the floating rate notes will bear interest at a floating rate based on [One]-Month LIBOR plus an applicable spread, if any.

If the floating rate payable by the swap counterparty is substantially greater than the fixed rate payable by the issuing entity, the issuing entity will be more dependent on receiving payments from the swap counterparty in order to make payments on the notes. In addition, the obligations of the swap counterparty under the interest rate swap are unsecured. If the swap counterparty fails to pay the net amount due, you may experience delays or reductions in the interest and principal payments on your notes. | |

S-13

Table of Contents

If the floating rate payable by the swap counterparty is less than the fixed rate payable by the issuing entity, the issuing entity will be obligated to make payments to the swap counterparty. The swap counterparty will have a claim on the assets of the issuing entity for the net amount due, if any, to the swap counterparty under the interest rate swap. Except in the case of termination payments, as discussed below, amounts owing to the swap counterparty will be senior to payments on the notes and the certificates. These payments to the swap counterparty could cause a shortage of funds available on any distribution date, in which case you may experience delays or reductions in interest and principal payments on your notes.

In addition, if the interest rate swap terminates as a result of a default by or circumstances with respect to the issuing entity, a termination payment may be due to the swap counterparty. The payment to the swap counterparty would be made by the issuing entity out of funds that would otherwise be available to make payments on the notes and would be paid from available funds[, and senior swap termination payments on the interest rate swap would be equal in priority to payments of interest on the Class A Notes and senior to all other payments on the notes]. The amount of the termination payment will be based on the market value of the interest rate swap at the time of termination. The termination payment could be substantial if market interest rates and other conditions have changed materially since the issuance of the notes and certificates. In that event, you may experience delays or reductions in interest and principal payments on your notes.

The issuing entity will make payments to the swap counterparty out of, and will include receipts from the swap counterparty in, its generally available funds—not solely from funds that are dedicated to the floating rate notes. Therefore, the impact would be to reduce the amounts available for distribution to holders of all securities, not just holders of floating rate notes.] |

S-14

Table of Contents

| Holders of the Class B Notes and the Class C Notes May Suffer Losses Because They Have Limited Control Over Actions of the Issuing Entity and Conflicts Between Classes of Notes May Occur | The most senior outstanding class of notes will be the “controlling class” under the indenture. Thus, while any Class A Notes are outstanding, that will be the controlling class. Thereafter, as long as any Class B Notes are outstanding, that will be the controlling class. Only thereafter will the Class C Notes be the controlling class.

The rights of the controlling class will include the following:

• following an event of default, to direct the indenture trustee to exercise one or more of the remedies specified in the indenture relating to the property of the issuing entity, including a sale of the receivables;

• following a servicer default, to waive the servicer default or to terminate the servicer;

• to remove the indenture trustee and appoint a successor; and

• to consent to specified types of amendments to the indenture and the transfer and servicing agreements.

In exercising any rights or remedies under the indenture, the controlling class may act solely in its own interests. Therefore, holders of Class B Notes or Class C Notes that are subordinated to the controlling class will not be able to participate in the determination of any proposed actions that are within the purview of the controlling class, and the controlling class could take actions that would adversely affect the Class B Notes or the Class C Notes.

Furthermore, the issuing entity’s failure to make a timely payment of interest will constitute an event of default under the indenture only if the failure relates to the controlling class. |

S-15

Table of Contents

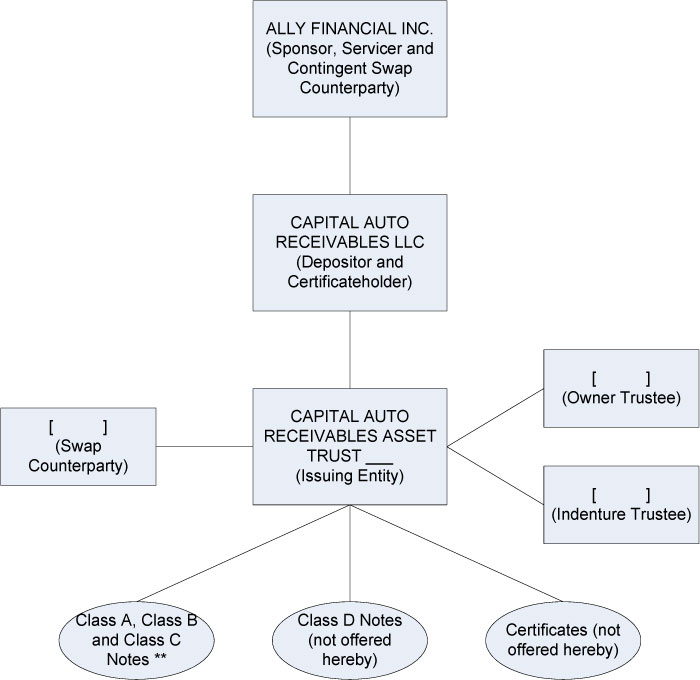

SUMMARY OF TRANSACTION PARTIES*

| * | This chart provides only a simplified overview of the relationships among the key parties to the transaction. Refer to this prospectus supplement and the prospectus for a further description. |

| ** | See“Summary—Priority of Distributions” for a description of the relative priorities of each class. |

S-16

Table of Contents

AFFILIATIONS AND RELATIONSHIPS AMONG TRANSACTION PARTIES

The owner trustee is not an affiliate of any of the depositor, the sponsor, the servicer, the issuing entity or the indenture trustee. However, the owner trustee and one or more of its affiliates may, from time to time, engage in arm’s-length transactions with the depositor, the sponsor, the servicer, the indenture trustee or affiliates of any of them, that are distinct from its role as owner trustee, including transactions both related and unrelated to the securitization of retail motor vehicle instalment sale contracts. The owner trustee and its affiliates, during the past two years, have not engaged in any transactions that are material to this transaction with any of the depositor, the sponsor, the servicer, the issuing entity or the indenture trustee that are outside of the ordinary course of business or that are other than at arm’s length. [Add description of specific transactions if material to investors in the notes.]

The indenture trustee is not an affiliate of any of the depositor, the sponsor, the servicer, the issuing entity or the owner trustee. However, the indenture trustee and one or more of its affiliates may, from time to time, engage in arm’s-length transactions with the depositor, the sponsor, the servicer, the owner trustee or affiliates of any of them, that are distinct from its role as indenture trustee, including transactions both related and unrelated to the securitization of retail vehicle instalment sale contracts. The indenture trustee and its affiliates, during the past two years, have not engaged in any transactions that are material to this transaction with any of the depositor, the sponsor, the servicer, the issuing entity or the owner trustee that are outside of the ordinary course of business or that are other than at arm’s length. [Add description of specific transactions if material to investors in the notes.]

[In addition, [ ] will be the swap counterparty. [ ] and [ ], an underwriter for the offered notes, are affiliates and have engaged in transactions with each other involving securitizations.]

The sponsor, the servicer and the depositor are affiliates and also engage in transactions with each other involving securitizations, including public offerings and private placements of asset-backed securities as well as commercial paper conduit financing, of retail vehicle instalment sale contracts, including those described in this prospectus supplement and others. [Add description of specific transactions involving the securitized assets or the securitization if material to investors in the notes.] Specifically, the depositor and Ally Financial have entered into an intercompany advance agreement through which the depositor may borrow funds from Ally Financial to fund its general operating expenses and, for some securitization transactions in which the depositor acts as the depositor, to pay for a portion of the receivables, the reserve account initial deposit and transaction expenses. Under the intercompany advance agreement, the loans bear a market rate of interest and have documented repayment terms.

On the closing date, the issuing entity is issuing certificates, not offered hereby. The depositor will initially retain the certificates, which represents the principal equity in the issuing entity. Therefore, the issuing entity is a direct subsidiary of the depositor and an indirect subsidiary of the sponsor. The depositor retains the right to sell all or a portion of the certificates at any time. Following any such sale to an unaffiliated third party, the issuing entity may cease to be an affiliate of either the sponsor or the depositor. The issuing entity has not engaged, and will not engage, in any material transactions with the sponsor or the depositor that are outside of the ordinary course of business or that are other than at arm’s length. [Add disclosure if the issuing entity engages in any transactions with the sponsor or depositor other than those described in the prospectus.]

S-17

Table of Contents

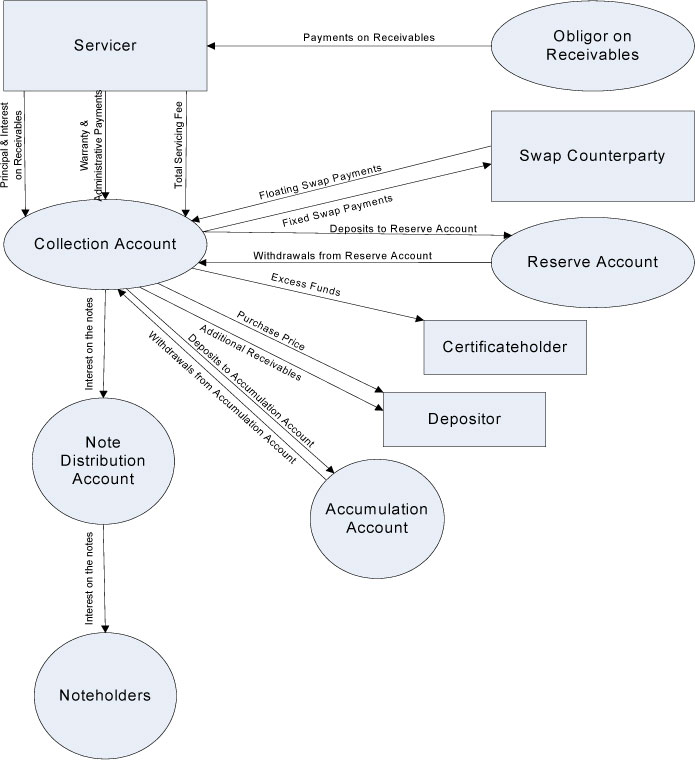

[SUMMARY OF MONTHLY DEPOSITS TO AND WITHDRAWALS

FROM ACCOUNTS DURING THE REVOLVING PERIOD]*

| * | This chart provides only a simplified overview of the monthly flow of funds during the revolving period. Refer to this prospectus supplement and the prospectus for a further description. |

S-18

Table of Contents

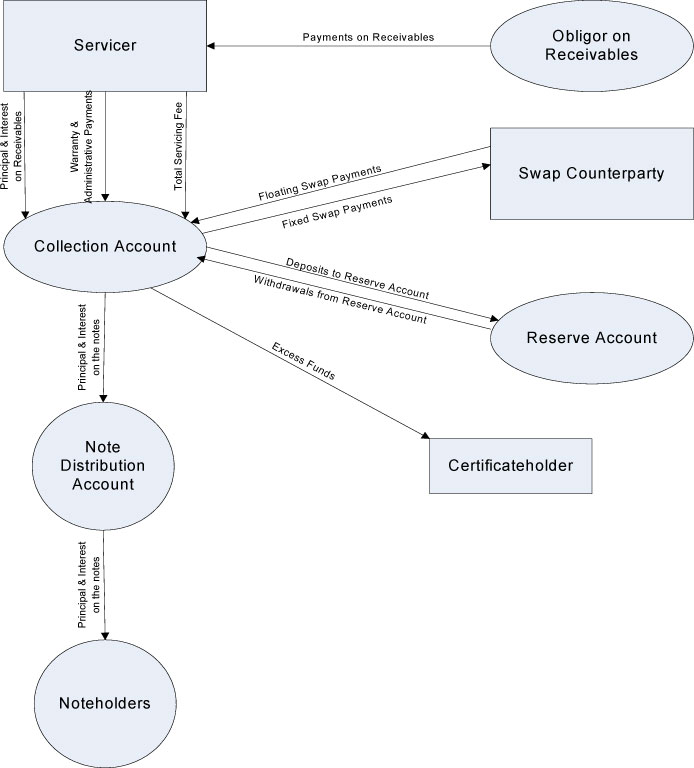

SUMMARY OF MONTHLY DEPOSITS TO AND WITHDRAWALS

FROM ACCOUNTS [DURING THE AMORTIZATION PERIOD]*

| * | This chart provides only a simplified overview of the monthly flow of funds [during the amortization period]. Refer to this prospectus supplement and the prospectus for a further description. |

S-19

Table of Contents

The issuing entity, Capital Auto Receivables Asset Trust—is a statutory trust formed under the laws of the State of Delaware with a fiscal year end of December 31. The trust will be established and operated pursuant to a trust agreement dated on or before the anticipated closing date of , 20 , which is the date the trust will initially issue the notes and certificates.

The trust will engage in only the following activities:

| • | acquire, hold and manage the receivables and other assets of the trust, |

| • | issue securities, |

| • | [enter into and make payments under the interest rate swaps related to the floating rate notes,] |

| • | make payments on the securities, and |

| • | take any action necessary to fulfill the role of the trust in connection with the notes and the certificates. |

The trust’s principal offices are in [ ], Delaware, in care of [ ], as owner trustee at the address listed in“The Owner Trustee”below.

The following table illustrates the capitalization of the trust as of , 20 , the [initial] cutoff date, as if the issuance of the notes and the certificates had taken place on that date:

[Class A-1 Asset Backed Notes] | $ | |||

Class A-2[a Notes | $ | |||

Class A-2b] Notes | $ | |||

Class A-3[a Notes | $ | |||

Class A-3b] Notes | $ | |||

Class A-4 Asset Backed Notes | $ | |||

Class B Asset Backed Notes | $ | |||

Class C Asset Backed Notes | $ | |||

Class D Asset Backed Notes | $ | |||

Asset Backed Certificates | $ | �� | ||

Total | $ | |||

The amount shown for the certificates is the initial level of overcollateralization. The holders of the certificates will be entitled to receive amounts representing the remaining overcollateralization after repayment of amounts owing on the notes. None of the [Class A-1 Notes, the] Class D Notes or the certificates are being offered by this prospectus supplement or the accompanying prospectus. The [Class A-1 Notes and the Class D Notes] will be sold in one or more private placements on the closing date or may be retained initially by the depositor. [The Class D Notes will be retained initially by the depositor and a][A]ll of the certificates will be retained initially by the depositor. The depositor will retain the right to sell all or a portion of [the Class D Notes and] the certificates at any time.

S-20

Table of Contents

[ ] is the owner trustee under the trust agreement. [ ] is a [ ]and an affiliate of [ ]. Its principal offices are located at [ ].

[ ] has acted as owner trustee on numerous asset-backed securities transactions, including acting as owner trustee on various auto loan and auto lease securitization transactions. While the structure of the transactions referred to in the preceding sentence may differ among these transactions, [ ], is experienced in administering transactions of this kind. [Add information with respect to the owner trustee.]

Ally Financial is the sponsor of the transaction set forth in this prospectus supplement and in the accompanying prospectus.

As of December 31, 2010, Ally Financial has originated over 65 securitizations of retail vehicle instalment sale contracts, through a combination of registered offerings and privately placed transactions. In those securitizations, Ally Financial has issued securities with an aggregate initial principal balance of approximately $120 billion. During a period from 2000 to 2004, Ally Financial’s securitizations in registered offerings consisted entirely of subvented receivables, while before and after that period, Ally Financial’s securitizations in registered offerings have consisted of a mixture of subvented and nonsubvented receivables. For lease assets, Ally Financial has effected over 15 securitizations, through a combination of registered offerings and privately placed transactions. The aggregate initial principal balance of securities issued in lease securitization is over $20 billion. In addition to retail automobile instalment sale contracts and leases, Ally Financial also originates and securitizes the receivables arising from loans to dealers for the financing of dealer inventory. To date, it has originated over 15 dealer floorplan securitizations, in both public and private placement transactions. In the dealer floorplan securitizations, Ally Financial has issued securities with an aggregate initial principal balance of over $50 billion. To date, none of the prior securitizations organized by Ally Financial have defaulted. In 2008 and early 2009, three of Ally Financial’s privately-placed auto lease securitizations experienced early amortization trigger events as a result of residual value losses. Additionally, two of Ally Financial’s dealer floorplan securitizations experienced early amortization triggering events in 2009.

For further details with respect to Ally Financial’s prior retail vehicle instalment sale contract securitizations over the prior five years, see“Appendix A—Static Pool Data”in this prospectus supplement.

Criteria Applicable to the Selection of [Initial] Receivables

The [initial] pool of receivables to be sold to the trust was selected from Ally Financial’s portfolio based on several criteria, including that each receivable:

| • | is secured by a new or used car or light truck, |

| • | is a Simple Interest Receivable, |

| • | was originated in the United States, |

| • | provides for level monthly payments that may vary from one another by no more than $5, |

| • | will amortize the Amount Financed over its original term to maturity, |

S-21

Table of Contents

| • | was originated or acquired by Ally Financial or its subsidiaries in the ordinary course of business, |

| • | has a first payment due date on or after , 20 , |

| • | was originated on or after , 20 , |

| • | has an original term of [ ] to [ ] months, |

| • | has a remaining term of not less than [ ] months, |

| • | as of the [initial] cutoff date, was not considered past due; that is, the payments due on that receivable in excess of $25 have been received within 30 days of the payment date, and |

| • | has an APR of not greater than [ ]%. |

The receivables in the [initial] pool of receivables on the closing date will be the same receivables that comprised the pool of receivables on the [initial] cutoff date.

The initial pool of receivables was selected from Ally Financial’s portfolio of receivables that meet the criteria described above and other administrative criteria utilized by Ally Financial from time to time. We believe that no selection procedures adverse to the noteholders were utilized in selecting the receivable in this [initial] pool of receivables.

[Additional receivables sold to the trust during the revolving period must meet substantially similar criteria. See“Criteria Applicable to Selection of Additional Receivables During the Revolving Period” below. However, these criteria will not ensure that each subsequent pool of additional receivables will share the exact characteristics as the initial pool of receivables. As a result, the composition of the aggregate pool of receivables will change as additional receivables are purchased by the issuing entity on each distribution date during the revolving period.]

The following tables describe the [initial] pool of receivables as of the [initial] cutoff date.

Each of the percentages and averages in the tables is computed on the basis of the amount financed of each receivable as of the [initial] cutoff date. The “Weighted Average Annual Percentage Rate of all Receivables in Pool” and “Weighted Average Annual Percentage Rate of Non-Subvented Receivables in Pool” in the following table are based on weighting by amount financed and remaining term of each receivable, each as of the [initial] cutoff date. The “Weighted Average Original Maturity” in the following table is based on weighting by original undiscounted principal balance of each receivable as of its date of origination. “Loan-to-Value Ratio” with respect to a receivable means the amount financed divided by the estimated vehicle value, multiplied by 100. The estimated vehicle value for a new vehicle is the dealer invoice cost of the vehicle. The estimated vehicle value for a used vehicle is the value received by Ally Financial from the dealer, independently validated by Ally Financial, based on a market guide, such as the Blackbook, indicating the value of the vehicle and the source from which that value was determined. “Weighted Average Loan-to-Value Ratio” is based on a weighting by original undiscounted principal balance of each receivable as of its date of origination. A FICO score is a measurement designed by Fair, Isaac & Company and calculated by the major credit bureaus using collected information to assess credit risk. “Weighted Average FICO Score” is based on a weighting by original undiscounted principal balance of each receivable as of the [initial] cutoff date [and excludes receivables with respect to which the obligor is a business account and receivables for which no FICO Score is available. Of the FICO Scores excluded from the Weighted Average FICO Score, , or %, are business accounts and the remaining , or %, are accounts for which FICO Scores are unavailable. In the table “Distribution of the [Initial] Receivables Pool by FICO Score,” those excluded accounts make up the “Business Accounts and Unavailable” category].

S-22

Table of Contents

Composition of the [Initial] Receivables Pool—(Total: New and Used)

S-23

Table of Contents

Composition of the [Initial] Receivables Pool—(Used)

Aggregate Amount Financed | $ | |||

Number of Contracts in Pool | ||||

Average Amount Financed | $ | |||

Weighted Average FICO Score | ||||

Weighted Average Loan-to-Value Ratio | ||||

Weighted Average Annual Percentage Rate of all Receivables in Pool | % | |||

Weighted Average Annual Percentage of Non-Subvented Receivables in Pool | % | |||

Discount Rate Applied to Receivables in Pool with Annual Percentage Rates at or below % | % | |||

Weighted Average Original Maturity | months | |||

Weighted Average Remaining Maturity (Range) | months ([ ] to [ ] months) | |||

Percentage of Contracts with Original Terms of less than or equal to 60 Months | % | |||

Percentage of Contracts with Original Terms of greater than 60 Months | % | |||

Percentage of Subvented Receivables in Pool | % | |||

Percentage of Non-Subvented Receivables in Pool | % |

S-24

Table of Contents

Distribution of the Initial Receivables Pool by Annual Percentage Rate—Aggregate

Annual Percentage Rate Range | Number of Contracts | Aggregate Amount Financed | Percentage of Aggregate Amount Financed | |||||||||

0.00% to 1.00% | $ | % | ||||||||||

1.01% to 2.00% | $ | % | ||||||||||

2.01% to 3.00% | $ | % | ||||||||||

3.01% to 4.00% | $ | % | ||||||||||

4.01% to 5.00% | $ | % | ||||||||||

5.01% to 6.00% | $ | % | ||||||||||

6.01% to 7.00% | $ | % | ||||||||||

7.01% to 8.00% | $ | % | ||||||||||

8.01% to 9.00% | $ | % | ||||||||||

9.01% to 10.00% | $ | % | ||||||||||

10.01% to 11.00% | $ | % | ||||||||||

11.01% to 12.00% | $ | % | ||||||||||

12.01% to 13.00% | $ | % | ||||||||||

13.01% to 14.00% | $ | % | ||||||||||

14.01% to 15.00% | $ | % | ||||||||||

15.01% to 16.00% | $ | % | ||||||||||

16.01% to 17.00% | $ | % | ||||||||||

17.01% to 18.00% | $ | % | ||||||||||

18.01% to 19.00% | $ | % | ||||||||||

19.01% to 20.00% | $ | % | ||||||||||

Total | $ | % | ||||||||||

Distribution of the Initial Receivables Pool by State

The [initial] pool of receivables includes receivables originated in all 50 states and the District of Columbia. The following table sets forth the percentage of the Aggregate Amount Financed in the states with the largest concentration of receivables. No other state accounts for more than % of the Aggregate Amount Financed. The following breakdown by state is based on the billing addresses of the obligors on the receivables:

State | Percentage of Aggregate Amount Financed | |||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

[Note: In accordance with Item 1111(b)(14), economic or other factors specific to any state or region in which obligors in respect of 10% or more of the pool of assets are located will be described to the extent that they may materially impact pool cash flows. This determination will be made based on the specific geographic distributions with respect to, and economic and other circumstances existing at the time of formation of, each pool.]

S-25

Table of Contents

Distribution of the [Initial] Receivables Pool by Loan-to-Value Ratio

Loan-to-Value Ratio | Number of Contracts | Average Amount Financed | Average Estimated Vehicle Value | Percentage of Contracts | ||||||||||||

Less than XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

XX to XX | $ | $ | % | |||||||||||||

Greater than XX | $ | $ | % | |||||||||||||

Total | % | |||||||||||||||

Distribution of the [Initial] Receivables Pool by FICO Score

FICO Band | Number of Contracts | Aggregate Amount Financed | Percentage of Aggregate Amount Financed | |||||||||

Business Accounts and Unavailable | $ | % | ||||||||||

Less than XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

XX to XX | $ | % | ||||||||||

Total | 100.00 | % | ||||||||||

Distribution of the Receivables Pool by Vehicle Make

Percentage of Aggregate | ||||

| Amount | ||||

Vehicle Make | Financed | |||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

S-26

Table of Contents

No other vehicle make accounts for more than [ ]% of the Aggregate Amount Financed.

Distribution of the Receivables Pool by Vehicle Model

| Percentage of Aggregate | ||||

Amount | ||||

Vehicle Model | Financed | |||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

| % | ||||

No other vehicle model accounts for more than [ ]% of the Aggregate Amount Financed.

[Criteria Applicable to the Selection of Additional Receivables During the Revolving Period

The additional receivables sold to the issuing entity during the revolving period will be selected from Ally Financial’s portfolio based on several criteria. These criteria include the requirements that each additional receivable:

| • | is secured by a new or used car or light truck, |

| • | is a Simple Interest Receivable, |

| • | was originated in the United States, |

| • | provides for level monthly payments which may vary from one another by no more than $5, |

| • | will amortize the Amount Financed over its original term to maturity, |

| • | was or will be originated or acquired by Ally Financial or its subsidiaries in the ordinary course of business, |

| • | has an original term of [ ] to [ ] months, provided that following the addition of all additional receivables on each subsequent cutoff date, the sum of the Amount Financed of all receivables ever sold to the issuing entity with an original term in excess of [ ] months may not exceed [ ]% of the Aggregate Amount Financed of all receivables ever sold to the issuing entity, |

S-27

Table of Contents

| • | as of its subsequent cutoff date, the additional receivable will not be considered past due; that is, the payments due on that additional receivable in excess of $25 will have been received within 30 days of the payment date, |

| • | has a remaining term as of its subsequent cutoff date of not less than [ ] months, |

| • | following the addition of all additional receivables on each subsequent cutoff date, the sum of the Amount Financed of all receivables ever sold to the issuing entity secured by used vehicles may not exceed [ ]% of the Aggregate Amount Financed of all receivables ever sold to the issuing entity, and |

| • | has a final maturity date no later than , 20 . |

The additional receivables will be selected at from Ally Financial’s portfolio of receivables that meet the criteria described above and other administrative criteria utilized by Ally Financial from time to time. We believe that no selection procedures adverse to the noteholders will be utilized in selecting the additional receivables.]

Delinquencies, Repossessions, Bankruptcies and Net Losses

For Ally Financial’s entire U.S. consumer automotive portfolio of new and used retail car and light truck receivables, including receivables sold by Ally Financial that it continues to service, the table on the following page shows Ally Financial’s experience for both new and used retail car and light truck receivables on a combined basis for:

| • | delinquencies, |

| • | repossessions, |

| • | bankruptcies, and |

| • | net losses. |

Fluctuations in delinquencies, repossessions, bankruptcies and net losses generally follow trends in the overall economic environment and may be affected by such factors as:

| • | competition for obligors, |

| • | the supply and demand for both new and used cars and light trucks, |

| • | consumer debt burden per household, and |

| • | personal bankruptcies. |

[Narrative disclosure of quarterly data to be added as appropriate]

There can be no assurance that the delinquency, repossession, bankruptcy and net loss experience on the receivables will be comparable to that set forth below or that the factors or beliefs described above will remain applicable.

S-28