Capital Auto Receivables LLC

200 Renaissance Center

Detroit, Michigan 48265

December 23, 2015

VIA EDGAR

Securities and Exchange Commission

450 Fifth Street, N.W.

Washington, D.C. 20549

| Attention: | Michelle Stasny |

| M. Hughes Bates |

| Re: | Capital Auto Receivables LLC |

| Registration Statement on Form SF-3 |

| Filed November 17, 2015 |

| File No. 333-208079 |

Dear Ladies and Gentlemen:

This letter is provided on behalf of Capital Auto Receivables LLC (the “Company”) in response to your letter dated December 15, 2015 (the “Letter”) relating to comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) in connection with the above-referenced submission. For your reference, we have listed your questions and our corresponding answers.

General

| 1. | Please confirm that the depositor or any issuing entity previously established, directly or indirectly, by the depositor or any affiliate of the depositor have been current with Exchange Act reporting during the last twelve months with respect to asset-backed securities involving the same asset class. Refer to General Instruction I.A.2. of Form SF-3. |

Response: The depositor and all affiliates of the depositor have been current and timely with Exchange Act reporting during the last twelve months with respect to asset-backed securities involving the same asset class. The CIK number for Ally Auto Assets LLC, the only affiliate of the depositor that has offered a class of asset-backed securities involving the same asset class as this offering, is 0001477336.

The CIK numbers for affiliated issuing entities that have issued asset-backed securities involving the same asset class as this offering and have been required to make Exchange Act reports during the last twelve months are set forth onExhibit A.

| 2. | Please confirm that all revisions made throughout the prospectus in response to the comments below will be applied to the applicable transaction documents, as necessary. |

Securities and Exchange Commission

December 23, 2015

Page 2

Response: We confirm that we have made revisions in response to the comments below both throughout the prospectus and in the applicable transaction documents, as necessary.

| 3. | Please confirm that delinquent assets will not constitute 20% or more of the asset pool on the date of any issuance of notes under this form of prospectus. Refer to General Instruction I.B.1(e) of Form SF-3. |

Response: We confirm that delinquent assets will not constitute 20% or more of the asset pool on the date of any issuance of notes under this form of prospectus.

Forward-Looking Statements

| 4. | Please delete your disclosure regarding forward-looking statements as the provisions do not apply to initial public offerings. |

Response: We believe it is appropriate to include some disclosure with respect to the forward-looking statements provided in the prospectus, including under “Summary—Ratings,” “Weighted Average Life of the Offered Notes” and in static pool disclosure provided in Appendix A and Appendix B. In order to be consistent with other ABS issuers, we have shortened and revised this section on page i.

Summary

Repurchases and Purchases of Receivables, page 8

| 5. | We note your disclosure that “[i]f the delinquency trigger is met … and a majority of the noteholders vote to direct a review of delinquent receivables” the asset representations reviewer will conduct a review. Please revise to clarify that the voting requirement to initiate a review is “at least a majority of the noteholders by aggregate principal balance of the notes who have voted choose to approve initiating the asset representations review and at least 5% of the noteholders by aggregate principal balance of notes outstanding cast a vote.” |

Response: We have revised our disclosure to clarify the voting requirements for the asset representations review in the “Summary” section on page 8 and in the “The Receivables Pool—Asset Representations Review” section on page 44.

Acquisition and Underwriting

Acquisition and Underwriting, page 27

| 6. | We note your bracketed disclosure on page 28 that “[a] portion of the lower FICO non- prime applications are manually decisioned [sic] by a dedicated underwriting team. In addition, these accounts require more restrictive underwriting criteria and more comprehensive document verification.” Please revise to clarify the following: 1) what |

Securities and Exchange Commission

December 23, 2015

Page 3

| constitutes a “lower FICO non-prime application,” 2) how is it decided which of these lower FICO non-prime applications are manually reviewed, 3) what are the more restrictive underwriting criteria for such applications, and 4) what constitutes more comprehensive document verification. |

Response: We consider several factors including FICO scores in making our underwriting decisions. For competitive reasons, we do not disclose the exact FICO score cutoff that constitutes the lower FICO score for non-prime applications but we generally consider it to be in the low 600s or lower. All applications are first evaluated through an automated process as described on page 28 of the prospectus. The algorithm will automatically approve or decline some applications based on different combinations of credit factors. As described in the prospectus, those applications which are not automatically approved or declined will be manually reviewed. This process applies to all our applications but a significant portion of the lower FICO score applications are more likely to be manually reviewed than applications with higher FICO scores. We have added examples of some of the more restrictive underwriting criteria and applicant verification procedures that may be required on page 28 of the prospectus.

Underwriting Exceptions, page 28

| 7. | We note your disclosure that approved applicants that do not comply with all the credit guidelines typically have strong compensating factors that indicate a high ability of the applicant to repay the receivable. Please revise to describe these compensating factors. |

Response: We have described some of these compensating factors on page 29 of the prospectus.

The Receivables Pool

Depositor Review of the [Initial] Receivables Pool, page 40

| 8. | We note your statement that a third party assisted in the review of the assets. Please confirm that, if you or an underwriter obtain a due diligence report from a third-party provider, you or the underwriter, as applicable, will furnish a Form ABS-15G with the Commission at least five business days before the first sale in the offering making publicly available the findings and conclusions of any third-party due diligence report you or the underwriter have obtained. See Section II.H.1 of the Nationally Recognized Statistical Rating Organizations Adopting Release (Release No. 34-72936) (Aug. 27, 2014). |

Response: We confirm that if we or an underwriter obtain a due diligence report from a third-party provider, we will, or we will require the underwriter to, as applicable, furnish a Form ABS-15G with the Commission at least five business days before the first sale in the offering making publicly available the findings and conclusions of any third-party due diligence report we or any underwriter have obtained.

Securities and Exchange Commission

December 23, 2015

Page 4

Exceptions to Underwriting Guidelines, page 42

| 9. | We note that the table explaining the nature of the exceptions categorizes exceptions only as either “credit characteristic exceeding guideline” or “collateral characteristic exceeding guideline.” With respect to “credit characteristic exceeding guideline” category, please breakdown further to more specifically describe each particular credit characteristic exception and the number of contracts and the percentage of aggregate amount financed for each such exception. Item 1111(a)(8) of Regulation AB requires, in part, disclosure about how such assets deviate from the disclosed underwriting criteria. |

Response: We believe we have complied with the requirements of Item 1111(a)(8) and have categorized the exceptions appropriately. We define a “credit characteristic” as an underwriting criterion primarily related to the creditworthiness of the obligor and provide examples of what we consider a “credit characteristic,” such as the obligor’s payment-to-income ratio or debt-to-income ratio. For our CARAT deals since 2013, the credit characteristic exceptions have historically ranged from 1 to 3% of the receivables pool, with an average of 2%. We believe that any additional breakdown is not material to investors and not required. We believe the examples that we have given for these exceptions adequately describe how such assets deviate from the underwriting criteria and comply with the rule.

| 10. | Please revise, to the extent applicable, to include information about the compensating factors that were used to make the determination to include such receivables, including data on the amount of assets in the pool, or sample, that are represented as meeting each such factor and the amount of the assets that do not meet those factors. Refer to Item 1111(a)(8) of Regulation AB. |

Response: We have described some of these compensating factors on page 42 of the prospectus. In each transaction, we will also provide disclosure regarding the receivables with only one underwriting exception and the number of receivables with one or more “layered” underwriting exceptions.

Asset Representations Review

Voting, page 45

| 11. | We note your statement that “[w]ithin [90] days of publication that the delinquency trigger has been met or exceeded in the monthly statement to securityholders on Form 10-D, the noteholders may determine whether a review of 60 day or more delinquent receivables should be initiated by the asset representations reviewer.” Later, you state that “noteholders will be allowed to vote for at least [150] days after the Form 10-D including disclosure that the trigger has been met or exceeded is filed.” Please revise to clarify whether the reference to 90 days relates to the number of days that noteholders have to initiate a vote or whether it relates to the number of days that noteholders have to complete the vote to direct a review by the asset representations reviewer. |

Securities and Exchange Commission

December 23, 2015

Page 5

Response: We have revised the language to clarify that the [90] day timeframe relates to initiating a vote as to whether a review should be performed, and the [150] day timeframe includes both the decision whether to request a vote and the voting window for all voters once 5% or more of the noteholders have demanded such a vote. Each time period is measured from the filing of the initial Form 10-D disclosing that a trigger has been met or exceeded.

Dispute Resolution, page 47

| 12. | We note that each notice from a noteholder “must be made in accordance with the requirements in the transaction documents.” Please revise to describe the requirements of the notice as set forth in the transaction documents. |

Response: We have revised the disclosure to reflect all requirements of the documents on page 47 of the prospectus. These requirements are necessary to evaluate whether a receivable is subject to repurchase and to properly respond within the required period. See page 45.

| 13. | We note in the Form of the Asset Representations Review Agreement that the Form 10-D summary will not include receivable-level information and will only include aggregated data for distribution to investors. In light of the notice requirements as set forth in the Form of Trust Sale and Servicing Agreement, specifically that the repurchase request must identify each receivable that is the subject of the request, the specific representation or warranty breached, the loss that occurred as a result of the breach, and the material and adverse effect of the breach on noteholders as whole, please clarify what information noteholders will be provided in order to make a sufficient notice. |

Response: We have revised the disclosure to state that a noteholder may request the detailed report of the asset representation reviewer’s findings from the sponsor. See page 46.

| 14. | We note your disclosure that, “[i]n the event that the asset representations reviewer determines that the representations and warranties related to a receivable have not failed, any repurchase request related to that receivable will be deemed to be resolved.” This limitation on the availability of dispute resolution appears inconsistent with the shelf eligibility requirement. Refer to General Instruction I.B.1(c) of Form SF-3 and Section V.B.3(a)(3) of the Asset-Backed Securities Disclosure and Registration Adopting Release (Release No. 33-9638) (“while we believed that our asset review shelf requirement would help investors evaluate whether a repurchase request should be made, we structured the dispute resolution provision so that investors could utilize the dispute resolution provision for any repurchase request, regardless of whether investors direct a review of the assets. We believe that organizing the dispute resolution requirement as a separate subsection in the shelf eligibility requirements will help to clarify the scope of the dispute resolution provision.”). Please revise accordingly. Please also revise Section 2.05 in the Form of Trust Sale and Servicing Agreement. |

Response: As we discussed with the Staff of the Commission in connection with the Ally Auto Assets LLC SF-3 Registration Statement, we do not believe that this statement is

Securities and Exchange Commission

December 23, 2015

Page 6

inconsistent with the rule or the instructions. We also note that this language has been included in the disclosure of several effective shelves filed by other issuers, including Ally Auto Assets LLC.

Whether an investor voted affirmatively, negatively or abstained in the vote to cause a review will not affect whether that investor can use the dispute resolution proceeding. An investor will also be entitled to refer a dispute related to any receivables that the asset representations reviewer did not review to a dispute resolution proceeding as well as any receivable that the asset representations reviewer reviewed and found to have failed a test.

We supplementally confirm that any investor will be entitled to refer a dispute related to any receivable to a dispute resolution proceeding.

| 15. | We note that, in the case of binding arbitration, the burden of proof for alleged breaches of the representations or warranties will shift from a preponderance of the evidence to clear and convincing evidence of a breach if at least [12] months of payments have been received with respect to the related receivable. The imposition of a higher evidentiary standard by the sponsor in such instance appears to discourage investors from pursuing arbitration. Please tell us why it is appropriate for the sponsor, and not the arbitration panel, to determine the evidentiary standard. |

Response: We have removed this language from page 48 of the “The Receivables Pool—Dispute Resolution” section.

| 16. | We note that “statistical sampling” will not be permitted for purposes of determining additional receivables that may be subject to a repurchase request. This language appears to constrain noteholders who are required, in making a repurchase request, to identify each receivable that is the subject of the request and the specific representation or warranty breached. Please remove or explain why such a provision would be appropriate to constrain noteholders in this way. |

Response: We have revised this language to permit statistical sampling as long as a breach is proved for any asset identified through such methods. See page 47. The language of the rule clearly presents the dispute resolution option as an asset-level remedy and, therefore, pool-level, generalized allegations based on statistical sampling are inappropriate.

| 17. | We note your disclosure that “the proceedings of the mediation or binding arbitration, including the occurrence of such proceedings, …will be kept strictly confidential by each of the parties to the dispute.” Please confirm to us that any restrictions will not infringe |

Securities and Exchange Commission

December 23, 2015

Page 7

| on the rights of noteholders to use the investor communication provision as required by General Instruction I.B.1(d) of Form SF-3. Please also revise in light of your statement that the sponsor and depositor will provide notice of the commencement of any arbitration on the Form 10-D in order to give other noteholders the right to participate in the arbitration proceeding. |

Response: We have revised the disclosure on page 48 to clarify that the confidentiality requirements are subject to exceptions to comply with the investor communications and the reports to securityholders requirements.

Credit Risk Retention

[Retained Eligible Horizontal Interest, page 79

| 18. | We note on page 80 that, in calculating the fair value, you have assumed that receivables prepay at a constant rate. In Section III.B.1.b. of the Credit Risk Retention Adopting Release (Release No. 34-73407) (Oct. 22, 2014), the agencies stated that we expect the key inputs and assumptions would not assume straight lines. Please tell us why you believe an assumption of a constant prepayment rate is appropriate. |

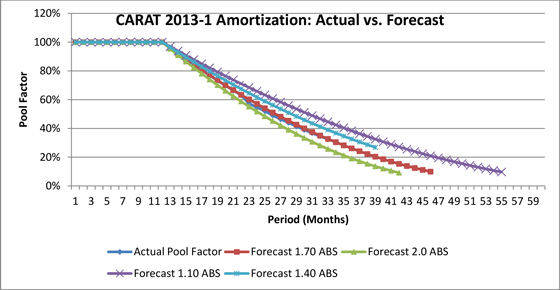

Response: As we noted in our response letter to the Commission dated September 24, 2015, with respect to the Ally Auto Assets LLC SF-3 Registration Statement, the prepayment model described in our disclosure measures prepayments as a percentage of the initial pool balance for each month. As a result, the rate of prepayments increases over time and results in a curve instead of a constant rate. The attachedExhibit B shows the actual pool balance amortization for one of our CARAT securitization transactions versus some of the prepayment rates presented in the prospectus supplement for that transaction. We will adjust the projection based on the nature of the collateral for each transaction as well as our historical experience with prepayments of other similar receivables.

The Indenture Trustee, page 110

| 19. | We note your discussion that the indenture trustee will be under no obligation to exercise any of the rights or powers under the indenture if it reasonably believes it will not be adequately indemnified. Please tell us why such contractual provisions would not undermine the indenture trustee’s duties in connection with actions required by the shelf eligibility criteria relating to dispute resolution and the asset representations review. |

Response: We have added language to clarify that the indenture trustee is required to comply with the asset representations review provisions on page 110 of the prospectus. We note that the indenture trustee does not have any responsibility in connection with investor communications, as these requests are directed through the servicer. Additionally, the indenture trustee has no defined responsibilities related to the dispute resolution procedures, with the exception of the responsibility to forward a repurchase request upon receipt.

Securities and Exchange Commission

December 23, 2015

Page 8

Exhibits

Form of Pooling and Servicing Agreement, page 21

| 20. | We note your statement that “the Seller shall review any Receivables with respect to which the Asset Representations Reviewer has determined that a breach of a representation or warranty set forth in Section 4.01 has occurred.” Please revise to make clear that the asset representations reviewer is not responsible for determining whether noncompliance with the representations or warranties constitutes a breach of a contractual provision. Please also revise Section 2.04(b) of the Form of Trust Sale and Servicing Agreement. |

Response: We have revised the Form of Pooling and Servicing Agreement to clarify that the asset representations reviewer is responsible for reporting the findings of its procedures pursuant to the Asset Representations Review Agreement and that it is the Seller who is responsible for determining whether noncompliance with the representations or warranties constitutes a breach of a contractual provision. See Section 5.08(b) of the Form of Pooling and Servicing Agreement. We have also revised Section 2.04(b) of the Form of Trust Sale and Servicing Agreement correspondingly.

Securities and Exchange Commission

December 23, 2015

Page 9

We hope that the foregoing has been responsive to the Staff’s comments. If you have any questions related to this letter, please contact my counsel, Janette McMahan of Kirkland & Ellis LLP, at (212) 446-4754.

| Sincerely, |

| /s/ Ryan C. Farris |

| Ryan C. Farris |

| President, Capital Auto Receivables LLC |

| cc: | Richard V. Kent, Capital Auto Receivables LLC |

| Janette McMahan, Kirkland & Ellis LLP |

EXHIBIT A

Name | CIK | |

| Ally Auto Receivables Trust 2010-5 | 0001507149 | |

| Ally Auto Receivables Trust 2011-1 | 0001511861 | |

| Ally Auto Receivables Trust 2011-2 | 0001518904 | |

| Ally Auto Receivables Trust 2011-3 | 0001522559 | |

| Ally Auto Receivables Trust 2011-4 | 0001529359 | |

| Ally Auto Receivables Trust 2011-5 | 0001534318 | |

| Ally Auto Receivables Trust 2012-1 | 0001538940 | |

| Ally Auto Receivables Trust 2012-2 | 0001543687 | |

| Ally Auto Receivables Trust 2012-3 | 0001550460 | |

| Ally Auto Receivables Trust 2012-4 | 0001555611 | |

| Ally Auto Receivables Trust 2012-5 | 0001560194 | |

| Ally Auto Receivables Trust 2013-1 | 0001573229 | |

| Ally Auto Receivables Trust 2013-2 | 0001589680 | |

| Ally Auto Receivables Trust 2014-1 | 0001610148 | |

| Ally Auto Receivables Trust 2014-2 | 0001619406 | |

| Ally Auto Receivables Trust 2014-3 | 0001627213 | |

| Ally Auto Receivables Trust 2015-1 | 0001647353 | |

| Ally Auto Receivables Trust 2015-2 | 0001652201 | |

| Capital Auto Receivables Asset Trust 2013-1 | 0001566328 | |

| Capital Auto Receivables Asset Trust 2013-2 | 0001579445 | |

| Capital Auto Receivables Asset Trust 2013-3 | 0001583965 | |

| Capital Auto Receivables Asset Trust 2013-4 | 0001592264 | |

| Capital Auto Receivables Asset Trust 2014-1 | 0001597032 | |

| Capital Auto Receivables Asset Trust 2014-2 | 0001605435 | |

EXHIBIT A

Name | CIK | |

| Capital Auto Receivables Asset Trust 2014-3 | 0001617626 | |

| Capital Auto Receivables Asset Trust 2015-1 | 0001630924 | |

| Capital Auto Receivables Asset Trust 2015-2 | 0001641832 | |

| Capital Auto Receivables Asset Trust 2015-3 | 0001649616 | |

| Capital Auto Receivables Asset Trust 2015-4 | 0001654785 | |

EXHIBIT B