UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________________________________

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

Commission file number 000-50368

________________________________________________________________

(Exact name of registrant as specified in its charter)

________________________________________________________________

| | |

| Delaware | | 26-1631624 |

| (State of Incorporation) | | (I.R.S. Employer Identification No.) |

145 Hunter Drive, Wilmington, OH 45177

(Address of principal executive offices)

937-382-5591

(Registrant’s telephone number, including area code)

________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, Par Value $.01 per share

Preferred Stock Purchase Rights

(Title of class)

Name of each exchange on which registered: NASDAQ Stock Market LLC

Securities registered pursuant to Section 12(g) of the Act: None

________________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | |

Large accelerated filer o | | Accelerated filer x |

Non-accelerated filer o (Do not check if a smaller reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, as of the last business day of the registrant’s most recently completed second fiscal quarter: $221,491,700. As of March 8, 2011, 63,652,228 shares of the registrant’s common stock, par value $0.01, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Stockholders scheduled to be held May 10, 2011 are incorporated by reference into Part III.

FORWARD LOOKING STATEMENTS

Statements contained in this annual report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in Item 7, that are not historical facts are considered forward-looking statements (as that term is defined in the Private Securities Litigation Reform Act of 1995). Words such as “projects,” “believes,” “anticipates,” “will,” “estimates,” “plans,” “expects,” “intends” and similar words and expressions are intended to identify forward-looking statements. These forward-looking statements are based on expectations, estimates and projections as of the date of this filing, and involve risks and uncertainties that are inherently difficult to predict. Actual results may differ materially from those expressed in the forward-looking statements for any number of reasons, including those described in “Risk Factors” starting on page 9 and “Outlook” starting on page 22.

Filings with the Securities and Exchange Commission

The Securities and Exchange Commission maintains an Internet site that contains reports, proxy and information statements and other information regarding Air Transport Services Group, Inc. at www.sec.gov. Additionally, our filings with the Securities and Exchange Commission, including annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports, are available free of charge from our website at www.atsginc.com as soon as reasonably practicable after filing with the SEC.

AIR TRANSPORT SERVICES GROUP, INC. AND SUBSIDIARIES

2010 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

| | | |

| | | | |

| | | | Page |

| PART I |

| Item 1. | | | |

| Item 1A. | | | |

| Item 1B. | | | |

| Item 2. | | | |

| Item 3. | | | |

| Item 4. | | | |

| | | |

| PART II |

| Item 5. | | | |

| Item 6. | | | |

| Item 7. | | | |

| Item 7A. | | | |

| Item 8. | | | |

| Item 9. | | | |

| Item 9A. | | | |

| Item 9B. | | | |

| | | |

| PART III |

| Item 10. | | | |

| Item 11. | | | |

| Item 12. | | | |

| Item 13. | | | |

| Item 14. | | | |

| | | |

| PART IV |

| Item 15. | | | |

| |

PART I

ITEM 1. BUSINESS

General Business Development

Air Transport Services Group, Inc. (“ATSG”), provides aircraft for lease, airline operations, aircraft maintenance and other related services primarily to the shipping and transportation industries. Through several subsidiaries, the Company offers a wide range of capabilities serving delivery companies, freight forwarders, airlines and government customers. ATSG wholly owns three independent airlines, ABX Air, Inc. (“ABX”), Capital Cargo International Airlines, Inc. (“CCIA”), and Air Transport International, LLC (“ATI”), each of which is certificated by the U.S. Department of Transportation. These airlines primarily transport cargo within the United States and include operations in Europe, Asia, the Middle East and throughout the Americas. ATSG includes an aircraft leasing subsidiary, Cargo Aircraft Management, Inc. (“CAM”), which leases its fleet of Boeing 767, 757, 727 and McDonnell Douglas DC-8 aircraft to ATSG’s airlines and to external customers.

ABX is based in Wilmington, Ohio and operates a fleet of Boeing 767 cargo aircraft. Between 1980 and August 2003, ABX was an affiliate of Airborne, Inc. (“Airborne”), a publicly traded, integrated delivery service provider. On August 15, 2003, ABX was separated from Airborne, and became an independent publicly traded company, in conjunction with the acquisition of Airborne by an indirect wholly-owned subsidiary of DHL Worldwide Express, B.V. ("DHL"). ATI, based in Little Rock, Arkansas, began operations in 1979 and was an affiliate of BAX Global, Inc. (“BAX/Schenker”) prior to 2006. ATI operates McDonnell Douglas DC-8 and Boeing 767 aircraft and provides airlift to BAX/Schenker, the U.S. Military and various other customers. CCIA obtained its airline operating certificate in 1996 and currently operates Boeing 727 and 757 aircraft, primarily providing air freight transportation for BAX/Schenker and DHL.

ATSG is incorporated in Delaware and its headquarters is in Wilmington, Ohio. ATSG’s common shares are publicly traded on the NASDAQ Stock Market under the symbol ATSG. ATSG was formed on December 31, 2007 from the reorganization of ABX for the purpose of creating a holding company structure. On December 31, 2007, ATSG completed the acquisition of CAM, ATI and CCIA which were together owned by a group of private investors. ATSG acquired all of the outstanding stock, stock options and warrants of these companies for a combination of cash, shares of ATSG and debt repayment. The overall transaction value was approximately $340 million, which ATSG partially financed through a $270 million unsubordinated term loan.

ATSG’s other subsidiaries are summarized below. (When the context requires, we may use the terms “Company” and “ATSG” in this report to refer to the business of ATSG and its subsidiaries on a consolidated basis.)

Airborne Maintenance and Engineering Services, Inc. (“AMES”), an aircraft maintenance and repair organization;

AMES Material Services, Inc. ("AMS"), which markets and sells aircraft parts;

ABX Cargo Services, Inc. ("ACS"), which operates mail sorting centers for the U.S Postal Service ("USPS");

LGSTX Services, Inc (“LGSTX”) which provides contract maintenance, ground support equipment rentals and fuel management for airlines.

We believe that offering a range of complementary solutions to shippers, freight forwarders and other airlines provides a competitive advantage for growth and diversification. Customers who lease our aircraft typically need related services, such as scheduled aircraft maintenance, line maintenance and crew training which our subsidiaries can provide. In 2010, we formed Airborne Global Solutions, Inc. ("AGS") to assist our subsidiaries in effectuating their sales and marketing plans. Through AGS, we can better leverage our customer relationships on additional business opportunities and market our aviation knowledge and the broad capabilities of our subsidiaries. AGS works with our customers in identifying their business and operational requirements and then works with our subsidiaries in forming a bundled solution of aircraft leases and related services to meet customer needs. AGS assists in marketing the capabilities of our three airlines to provide scalable airlift to a wide range of international locations.

The Company has a concentrated base of leading customers who have diverse lines of international cargo traffic. The three largest customers, DHL, BAX/Schenker and the U.S. Military, totaled 79% of the Company's consolidated revenues in 2010. Information about the Company's revenues and accounts receivable with these customers is presented

in Note B to the accompanying consolidated financial statements.

Background

The Company, through ABX, has had long term contracts with DHL since August 16, 2003. Beginning in August 2003, ABX operated primarily under two commercial agreements with DHL; an aircraft, crew, maintenance and insurance agreement (“DHL ACMI agreement”) and a hub services agreement (“Hub Services agreement”) both of which had become effective in conjunction with DHL's acquisition of Airborne. Under these agreements, ABX and DHL generally operated under a cost-plus pricing structure. ABX provided staff to conduct package sorting, as well as airport, facilities and equipment maintenance services for DHL under the Hub Services agreement. In 2008, DHL began to restructure its U.S. operations due to continued losses. Pursuant to its restructuring plans, DHL discontinued intra-U.S. domestic pickup and delivery services and now provides only international services to and from the U.S. In the third quarter of 2009, ABX ceased all remaining sort operations for DHL and the Hub Services agreement expired. Additionally, in the third quarter of 2009, DHL assumed management of aircraft fueling services for its U.S. network previously provided by ABX. The hub services operations and the aircraft fueling operations have been reported as discontinued operations since that time.

ABX continued to provide airlift for DHL’s international delivery services in the U.S. through ABX’s Boeing 767 aircraft under the DHL ACMI agreement until March 2010. At that point, the Company and DHL terminated the DHL ACMI agreement and executed new follow-on agreements effective March 31, 2010. Under the new agreements, DHL committed to lease13 Boeing 767 freighter aircraft from CAM and ABX was separately contracted to operate those aircraft for DHL under a five year crew, maintenance and insurance agreement ("CMI agreement"). As of December 31, 2010, DHL was leasing 11 of the 13 aircraft from CAM, all of which ABX operates for DHL under the CMI agreement. Two additional Boeing 767 aircraft are scheduled for lease to DHL before the end of the second quarter of 2011.

Description of Business

The Company has two reportable segments, "CAM" and “ACMI Services." Due to the similarities among the Company's airline operations, including the CMI agreement with DHL, the airline operations were aggregated into a single reportable segment, ACMI Services, in 2010. The Company’s other business operations, including aircraft maintenance and modification services, aircraft part sales, equipment leasing and maintenance, mail handling for the USPS and specialized services for aircraft fuel management, do not constitute reportable segments due to their size. Financial information about our segments and geographical revenues is presented in Note P to the accompanying consolidated financial statements.

CAM

CAM’s fleet consists of Boeing 767, Boeing 757, Boeing 727 and McDonnell Douglas DC-8 aircraft. CAM leases aircraft to ATSG airlines and to external customers, usually under multi-year contracts with a schedule of fixed monthly payments. Under a typical lease arrangement, the customer maintains the aircraft in serviceable condition at its own cost. At the end of the lease term, the customer typically is required to return the aircraft in approximately the same maintenance condition, as measured by airframe and engine time until the next scheduled maintenance event, as existed at the inception of the lease. CAM examines the credit worthiness of potential customers, their short and long-term growth prospects, their financial condition and backing, the experience of their management, and the impact of governmental regulation when determining the lease rate that is offered to the customer. In addition, CAM monitors the customer’s business and financial status throughout the term of the lease.

Through CAM, we plan to expand the Company's combined fleet of aircraft. Information about the Company's commitments for aircraft expenditures is included in Note I to the accompanying consolidated financial statements.

ACMI Services

Through its three airline subsidiaries, the Company provides airline operations to DHL, BAX/Schenker, other airlines, freight forwarders and the U.S. Military. A typical operating agreement requires the ATSG airline to supply, at a specific rate per block hour and/or per month, the aircraft, crew, maintenance and insurance for specified cargo operations, while the customer is responsible for substantially all other aircraft operating expenses, including fuel,

landing fees, parking fees and ground and cargo handling expenses. Charter agreements, including U.S. Military agreements, usually require the airline to provide full service, including fuel and other operating expenses, in addition to aircraft, crew, maintenance and insurance for a fixed, all-inclusive price.

In March 2010, the Company and DHL terminated the DHL ACMI agreement and executed new follow-on agreements. Through the new agreements, effective March 31, 2010, ABX operates aircraft that DHL either leased from CAM or owns itself. The new CMI agreement with DHL has an initial term of five years.

CCIA and ATI each have contracts to provide airlift to BAX/Schenker under ACMI agreements. BAX/Schneker provides freight transportation and supply chain management services, specializing in the heavy freight market for business-to-business shipping. The BAX/Schenker central hub is located in Toledo, Ohio. CCIA and ATI have the exclusive right to supply all main deck freighter airlift in BAX/Schenker's U.S. domestic network through December 31, 2011.

ATI provides airlift to the Air Mobility Command ("AMC"), which is organized under the U.S. Military. ATI contracts its unique fleet of McDonnell Douglas DC-8 combi aircraft to the AMC. The combi aircraft are capable of carrying passengers and cargo containers on the main flight deck. AMC awards flights to U.S. certificated airlines through annual contracts. For the government fiscal year 2011, AMC awarded ATI three international routes for combi aircraft. These routes are for destinations that are not within the areas of the Middle East conflicts. Additionally, ATI often operates temporary "expansion" routes for the AMC using its McDonnell Douglas DC-8 combi and freighter aircraft.

The Company has limited exposure to fluctuations in the price of aviation fuel under our contracts with DHL, BAX/Schenker and the U.S. Military. ATI procures the aircraft fuel for BAX/Schenker's U.S. domestic network and is reimbursed by BAX/Schenker for the price paid for fuel used. The charter agreements with the U.S. Military are based on a preset pegged fuel price and include a subsequent true-up to the actual fuel prices within two cents per gallon. DHL, like most of our ACMI customers, procures the aircraft fuel and fueling services necessary for their flights.

U.S. Postal Service

Since September 2004, the Company has provided mail sorting services under contracts with the USPS. Our subsidiary, ACS, manages USPS mail sort centers in Indianapolis, Indiana, Dallas, Texas and Memphis, Tennessee. Under each of these three contracts, ACS is compensated at a firm price for fixed costs and an additional amount based on the volume of mail handled at each sort center. Each contract was renewed in 2010 and has a two-year term, with expiration dates in either September or October 2012.

Cargo and Transportation Services

The Company provides brokerage services for airlift by arranging charters for customers using third party airlines as well as ATSG owned airlines.

Aircraft Maintenance and Modification Services

The Company provides aircraft maintenance and modification services to other airlines through its ABX and AMES subsidiaries. In May 2009, much of the aircraft maintenance, component repair and engineering business operations of ABX were transferred to a newly formed ATSG subsidiary, AMES. Organizing the aircraft maintenance and engineering capabilities separately from ABX was intended to facilitate a cost structure and marketing organization which can better compete in the aircraft maintenance industry.

ABX and AMES have technical expertise related to aircraft modifications as a result of ABX’s long history in aviation. They own many Supplemental Type Certificates (“STCs”). An STC is granted by the FAA and represents an ownership right, similar to an intellectual property right, which authorizes the alteration of an airframe, engine or component. ABX provides digital aircraft manuals for customers in conjunction with the modification of aircraft from passenger to cargo configuration.

AMES operates a Federal Aviation Administration (“FAA”) certificated 145 repair station, in Wilmington, Ohio, including hangars, a component shop and engineering capabilities. AMES is AS9100 quality certified for the aerospace industry. AMES markets its capabilities by identifying aviation-related maintenance and modification opportunities

and matching them to its capabilities. AMES’s marketable capabilities include the installation of avionics systems and flat panel displays for Boeing 757 and Boeing 767 cockpits. The flat panel display modernizes aircraft avionics equipment and reduces maintenance costs by combining multiple display units into a single instrumentation panel. AMES has the capabilities to perform line maintenance and heavy maintenance on DC-9, Boeing 767, 757, 737 and 727 aircraft. AMES has the capabilities to refurbish airframe components, including approximately 60% of the components for Boeing 767 aircraft.

Aircraft Parts Sales and Brokerage

AMS, which holds a certificate relating to free trade zone rights, is an Aviation Suppliers Association 100 Certified reseller and broker of aircraft parts. AMS carries an inventory of DC-8, DC-9 and Boeing 767 spare parts and also maintains inventory on consignment from original equipment manufacturers, resellers, lessors and other airlines. AMS customers include the commercial air cargo industry, passenger airlines, aircraft manufacturers and contract maintenance companies serving the commercial aviation industry, as well as other resellers.

Equipment and Facility Maintenance

LGSTX, formerly named ABX Equipment and Facility Services, Inc., provides contract services for aviation support and facility services throughout the U.S. LGSTX has a large inventory of ground support equipment, such as power units, airstarts, deicers and pushback vehicles that it rents to airports, airlines or other customers. LGSTX is also licensed to resell aircraft fuel. LGSTX arranges fueling services for customers and can provide fuel for aircraft charter customers.

Flight Crew Training

ABX and CCIA are FAA-certificated to offer flight crew training to customers and rent usage of their flight simulators for outside training programs. The Company has five flight simulators in operation, including one Boeing 767, one DC-8, one Boeing 727 and two DC-9 flight simulators. The Company’s Boeing 767, its Boeing 727 and one of its DC-9 flight simulators are level C certified. The level C flight simulators allow the Company to qualify flight crewmembers under FAA requirements without performing check flights in an aircraft. The DC-8 and the other DC-9 flight simulators are level B certified, which allows the Company to qualify flight crewmembers by performing a minimum number of flights in an aircraft.

Airline Operations

Flight Operations and Control

Airline flight operations, including aircraft dispatching, flight tracking and crew scheduling, are planned and controlled by personnel within each airline. All Company airline operations are conducted pursuant to authority granted to them by the FAA. ABX staffs aircraft dispatching and flight tracking 24 hours per day, 7 days per week from Wilmington, Ohio. CCIA flight operations, including flight tracking and crew scheduling, are controlled by on-duty personnel from CCIA’s operations center in Orlando, Florida, and the same functions for ATI are controlled from ATI’s operations center in Little Rock, Arkansas.

Maintenance

Our airlines’ operations are regulated by the FAA for aircraft safety and maintenance. Each airline performs routine inspections and airframe maintenance, including Airworthiness Directive and Service Bulletin compliance on all of their aircraft. The airlines’ maintenance and engineering personnel coordinate routine and non-routine maintenance requirements. Each airline’s maintenance program includes tracking the maintenance status of each aircraft, consulting with manufacturers and suppliers about procedures to correct irregularities and training maintenance personnel on the requirements of its FAA-approved maintenance program. The airlines contract with maintenance repair organizations (“MROs”), including AMES, to perform heavy airframe maintenance on airframes and engines. Each airline owns a supply of spare aircraft engines, auxiliary power units, aircraft parts and consumable items. The number of spare items maintained is based on the fleet size, engine type operated, and the reliability history of the item types.

Insurance

Our airline subsidiaries are required by the Department of Transportation (“DOT”) to carry liability insurance on each of their aircraft. Their aircraft leases, loan agreements and ACMI agreements also require them to carry such insurance. The Company currently maintains public liability and property damage insurance, and our airline subsidiaries currently maintain aircraft hull and liability insurance and war risk insurance for their respective aircraft fleets in amounts consistent with industry standards. CAM’s customers are also required to maintain similar insurance levels.

Employees

As of December 31, 2010, ATSG and its subsidiaries had approximately 2,065 employees, including 1,790 full-time employees and 275 part-time employees. ATSG employs approximately 600 flight crewmembers, 910 aircraft maintenance technicians and flight support personnel, 315 warehousing, sorting and logistics personnel, 65 employees for airport maintenance and logistics, 25 employees for sales and marketing and 150 employees for administrative functions. On December 31, 2009, the Company had approximately 2,020 employees.

Labor Agreements

The Company’s flight crewmembers are unionized employees. The table below summarizes the representation of the Company’s flight crewmembers at December 31, 2010.

| | | | | | | |

| Airline | | Labor Agreement Unit | | Contract Amendable Date | | Approximate Number of Employees Represented |

| ABX | | International Brotherhood of Teamsters | | 12/31/2014 | | 12.4 | % |

| ATI | | Airline Pilots Association | | 5/1/2004 | | 10.1 | % |

| CCIA | | Airline Pilots Association | | 7/31/2013 | | 6.4 | % |

Under the Railway Labor Act (“RLA”), as amended, the crewmember labor agreements do not expire, so the existing contract remains in effect throughout any negotiation process. If required, mediation under the RLA is conducted by the National Mediation Board, which has the sole discretion as to how long mediation can last and when it will end. In addition to direct negotiations and mediation, the RLA includes a provision for potential arbitration of unresolved issues and a 30-day “cooling-off” period before either party can resort to self-help, including, but not limited to, work stoppage.

Training

The flight crewmembers are required to be licensed in accordance with Federal Aviation Regulation (“FAR”), with specific ratings for the aircraft type to be flown, and to be medically certified as physically fit to fly aircraft. Licenses and medical certifications are subject to recurrent requirements as set forth in the FARs to include recurrent training and minimum amounts of recent flying experience.

The FAA mandates initial and recurrent training for most flight, maintenance and engineering personnel. Mechanics and quality control inspectors must also be licensed and qualified to perform maintenance on the Company operated and maintained aircraft. Our airline subsidiaries pay for all of the recurrent training required for their flight crewmembers and provide training for their ground service and maintenance personnel. Their training programs have received all required FAA approvals.

Industry

The primary competitive factors in the air cargo industry are price, fuel efficiency, geographic coverage, flight frequency, aircraft reliability and capacity. Our airline subsidiaries compete for domestic cargo volume principally with other cargo airlines and passenger airlines which have substantial belly cargo capacity. Other cargo airlines include Amerijet International, Inc., Astar USA, Inc. (“Astar”), Atlas Air Worldwide Holdings, Inc., National Airlines, Evergreen International, Inc., and World Airways, Inc. The industry is capital intensive and highly competitive.

Cargo volumes are highly dependent on the economic conditions and the level of commercial activity. Generally,

time-critical delivery needs, such as just-in-time inventory management, increase the demand for air cargo delivery, while higher costs of jet fuel generally reduces the demand for air delivery services. When jet fuel prices increase, shippers will consider using ground transportation if the delivery time allows. Historically, the cargo industry has experienced higher volumes during the fourth calendar quarter of each year due to increased shipments during the holiday season.

The scheduled delivery industry is dominated by integrated door-to-door carriers including DHL, the USPS, FedEx Corporation, BAX/Schenker and United Parcel Service, Inc. Although the volume of our business is impacted by competition among these integrated carriers, we do not usually compete directly with them.

Competition for aircraft leasing is generally effected by aircraft type, aircraft availability and lease rates. We target our leases to cargo airlines and delivery companies seeking medium widebody airlift.

The aircraft maintenance industry is labor intensive and typically competes based on cost, capabilities and reputation for quality. U.S. airlines may contract for aircraft maintenance with MROs in other countries or geographies with a lower labor wage base, making the industry highly cost competitive.

Intellectual Property

The Company owns a small number of U.S. patents that have nominal commercial value. The Company also owns many STCs issued by the FAA. The Company uses these STCs mainly in support of its own fleets; however, AMES has marketed certain STCs to other airlines.

Information Systems

The Company has invested significant management and financial resources in the development of information systems to facilitate cargo, flight and maintenance operations. The Company utilizes its systems to maintain records about the maintenance status and history of each major aircraft component, as required by FAA regulations. Using its systems, the Company tracks and controls inventories and costs associated with each maintenance task, including the personnel performing those tasks. In addition, the Company’s flight operations systems coordinate flight schedules and crew schedules. It has developed and procured systems to track crewmember flight and duty time, and crewmember training status.

Regulation

Our subsidiaries’ airline operations are generally regulated by the DOT, the FAA and the TSA. Those operations must comply with numerous security and environmental laws, ordinances and regulations. In addition, they must also comply with various other federal, state, local and foreign laws and regulations.

Environment

Under current federal, state and local environmental laws, ordinances and regulations, a current or previous owner or operator of real property may be liable for the costs of removal or clean-up of hazardous or toxic substances on, under, or in such property. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. In addition, the presence of contamination from hazardous or toxic substances, or the failure to properly clean up such contaminated property, may adversely affect the ability of the owner of the property to use such property as collateral for a loan or to sell such property. Environmental laws also may impose restrictions on the manner in which a property may be used or transferred or in which businesses may be operated and may impose remediation or compliance costs. Under its expired air park sublease with DHL, ABX and DHL are required to defend, indemnify and hold each other harmless from and against certain environmental claims associated with the Air Park in Wilmington, Ohio.

Our subsidiaries’ aircraft currently meet all known requirements for engine emission levels. However, under the Clean Air Act, individual states or the U.S. Environmental Protection Agency may adopt regulations requiring reduction in emissions for one or more localities based on the measured air quality at such localities. Such regulations may seek to limit or restrict emissions by restricting the use of emission-producing ground service equipment or aircraft auxiliary power units.

In addition, the European Commission has approved the extension of the European Union Emissions Trading

Scheme ("ETS") for greenhouse gas emissions to the airline industry. Under this decision, all Company airline subsidiary flights to and from any airport in any member state of the European Union will be covered by the ETS requirements beginning in 2012, and each year we will be required to submit emission allowances in an amount equal to the carbon dioxide emissions from such flights.

The federal government generally regulates aircraft engine noise at its source. However, local airport operators may, under certain circumstances, regulate airport operations based on aircraft noise considerations. The Airport Noise and Capacity Act of 1990 provides that, in the case of Stage 3 aircraft (all of our operating aircraft satisfy Stage 3 noise compliance requirements), an airport operator must obtain the carriers’ consent to or the government’s approval of the rule prior to its adoption. We believe the operation of our airline subsidiaries’ aircraft either complies with or is exempt from compliance with currently applicable local airport rules. However, some airport authorities have adopted local noise regulations, and, to the extent more stringent aircraft operating regulations are adopted on a widespread basis, our airline subsidiaries may be required to spend substantial funds, make schedule changes or take other actions to comply with such local rules.

The U.S. government, working through the International Civil Aviation Organization, has in the past adopted more stringent aircraft engine emissions regulations with regard to newly certificated engines and aircraft noise regulations applicable to newly certificated aircraft. Although these rules will not apply to any of our airline subsidiaries’ existing aircraft, additional rules could be adopted in the future that would either apply these more stringent noise and emissions standards to aircraft already in operation or require that some portion of the fleet be converted over time to comply with these new standards.

Department of Transportation

The DOT maintains authority over certain aspects of domestic air transportation, such as requiring a minimum level of insurance and the requirement that a person be “fit” to hold a certificate to engage in air transportation. In addition, the DOT continues to regulate many aspects of international aviation, including the award of international routes. The DOT has separately issued to ABX, CCIA and ATI Domestic All-Cargo Air Service Certificates for air cargo transportation between all points within the U.S., the District of Columbia, Puerto Rico, and the U.S. Virgin Islands. Additionally, the DOT has issued ABX, CCIA and ATI Certificates of Public Convenience and Necessity authorizing each of them to engage in scheduled foreign air transportation of cargo and mail between the U.S. and over 88 foreign countries. By maintaining these certificates, the Company, through its airline subsidiaries, can conduct all-cargo charter operations worldwide. Prior to issuing such certificates, and periodically thereafter, the DOT examines a company’s managerial competence, financial resources and plans, compliance, disposition and citizenship in order to determine whether the carrier is fit, willing and able to engage in the transportation services it has proposed to undertake.

The DOT has the authority to impose civil penalties, or to modify, suspend or revoke our certificates for cause, including failure to comply with federal law or DOT regulations. A corporation holding either of such certificates must qualify as a U.S. citizen, which requires that (1) it be organized under the laws of the U.S. or a state, territory or possession thereof, (2) that its president and at least two-thirds of its Board of Directors and other managing officers be U.S. citizens, (3) that less than 25% of its voting interest be owned or controlled by non-U.S. citizens, and (4) that it not otherwise be subject to foreign control. Neither type of certificate confers proprietary rights on the holder, and the DOT may impose conditions or restrictions on such certificates. We believe we possess all necessary DOT-issued certificates and authorities to conduct our current operations and continue to qualify as a U.S. citizen.

Federal Aviation Administration

The FAA regulates aircraft safety and flight operations generally, including equipment, ground facilities, maintenance, flight dispatch, training, communications, the carriage of hazardous materials and other matters affecting air safety. The FAA issues operating certificates and operations specifications to carriers that possess the technical competence to conduct air carrier operations. In addition, the FAA issues certificates of airworthiness to each aircraft that meets the requirements for aircraft design and maintenance. ABX, CCIA and ATI believe they hold all airworthiness and other FAA certificates and authorities required for the conduct of their business and the operation of their aircraft, although the FAA has the power to suspend, modify or revoke such certificates for cause, or to impose civil penalties for any failure to comply with federal law and FAA regulations.

The FAA has the authority to issue airworthiness directives and other mandatory orders relating to, among other

things, the inspection and maintenance of aircraft and the replacement of aircraft structures, components and parts, based on the age of the aircraft and other factors. For example, the FAA has required ABX to perform inspections of its Boeing 767 aircraft to determine if certain of the aircraft structures and components meet all aircraft certification requirements. If the FAA were to determine that the aircraft structures or components are not adequate, it could order operators to take certain actions, including but not limited to, grounding aircraft, reducing cargo loads, strengthening any structure or component shown to be inadequate, or making other modifications to the aircraft. New mandatory directives could also be issued requiring the Company’s airline subsidiaries to inspect and replace aircraft components based on their age or condition. As a routine matter, the FAA issues airworthiness directives applicable to the aircraft operated by our airline subsidiaries, and our airlines comply, sometimes at considerable cost, as part of their aircraft maintenance program. In addition to the FAA practice of issuing airworthiness directives as conditions warrant, the FAA has adopted new policies to address issues involving older, but still economically viable aircraft, on a more systematic basis. New FAA regulations mandate that aircraft manufacturers establish limits on aircraft flight cycles before which widespread fatigue damage might occur. Once these limits are established, carriers must then incorporate them into their maintenance programs over time. Once the limits are reached, airlines will be unable to continue to operate the aircraft without the FAA first granting an extension of time to the operator. As the manufacturers have not yet set the new limits, the Company cannot yet estimate the impact of the new rule on any of its airline subsidiaries.

The FAA has amended its policy regarding the proper application of airport rates and charges imposed on airlines. The amended policy provides greater flexibility to airport operators to impose charges that would allow for the imposition of “congestion fees” rather than uniform airport fees. If airports in the U.S. seek to use the flexibility offered by this new policy, it could have an impact on the cost of conducting our flight operations.

The FAA requires each of the airline subsidiaries to implement a drug and alcohol testing program with respect to all employees that engage in safety sensitive functions. Each of the airlines comply with these regulations.

Transportation Security Administration

The Transportation Security Administration (“TSA”), an administration within the Department of Homeland Security, is responsible for the screening of passengers, baggage and cargo and the security of aircraft and airports. Our airline subsidiaries comply with all applicable aircraft and cargo security requirements. The TSA has adopted cargo security-related rules that have imposed additional burdens on our airlines and our customers. Among other things, the TSA requires each airline to perform criminal history background checks on all employees. In addition, we may be required to reimburse the TSA for the cost of security services it may provide to the Company’s airline subsidiaries in the future.

Other Regulations

Various regulatory authorities have jurisdiction over significant aspects of our business, and it is possible that new laws or regulations or changes in existing laws or regulations or the interpretations thereof could have a material adverse effect on our operations. In addition to the above, other laws and regulations to which we are subject, and the agencies responsible for compliance with such laws and regulations, include the following:

| |

| • | The labor relations of our airline subsidiaries are generally regulated under the Railway Labor Act, which vests in the National Mediation Board certain regulatory powers with respect to disputes between airlines and labor unions arising under collective bargaining agreements; |

| |

| • | The Federal Communications Commission regulates our airline subsidiaries’ use of radio facilities pursuant to the Federal Communications Act of 1934, as amended; |

| |

| • | U.S. Customs and Border Protection inspects cargo imported from our subsidiaries’ international operations; |

| |

| • | Our airlines must comply with U.S. Citizenship and Immigration Services regulations regarding the citizenship of our employees; |

| |

| • | The Company and its subsidiaries must comply with wage, work conditions and other regulations of the Department of Labor regarding our employees. |

Security and Safety

Security

The Company’s subsidiaries have instituted various security procedures to comply with FAA and TSA regulations and comply with the directives outlined in the federal Domestic Security Integration Program. The airline subsidiaries’ customers are required to inform them in writing of the nature and composition of any freight which is classified as “Dangerous Goods” by the DOT. In addition, the Company and its subsidiaries conduct background checks on our respective employees, restrict access to aircraft, inspect aircraft for suspicious persons or cargo, and inspect all dangerous goods. Notwithstanding these procedures, our airline subsidiaries could unknowingly transport contraband or undeclared hazardous materials for customers, which could result in fines and penalties and possible damage to the aircraft.

Safety and Inspections

Management is committed to the safe operation of its aircraft. In compliance with FAA regulations, our subsidiaries’ aircraft are subject to various levels of scheduled maintenance or “checks” and periodically go through phased overhauls. In addition, a comprehensive internal review and evaluation program is in place and active. Our subsidiaries’ aircraft maintenance efforts are monitored closely by the FAA. They also conduct extensive safety checks on a regular basis.

ITEM 1A. RISK FACTORS

The risks described below could adversely affect our financial condition or results of operations. The risks below are not the only risks that the Company faces. Additional risks that are currently unknown to us or that we currently consider immaterial or unlikely could also adversely affect the Company.

The economic conditions in the U.S. and throughout the globe may negatively impact the demand for the Company’s aircraft and services.

Air cargo transportation volumes are strongly correlated to general economic conditions, including the price of aviation fuel. An economic downturn could reduce the demand for delivery services offered by DHL, BAX/Schenker and other delivery businesses, in particular expedited services shipped via aircraft. Accordingly, an economic downturn could reduce the demand for airlift and cargo aircraft leases. During an economic slowdown, customers generally prefer to use ground-based delivery services instead of more expensive air delivery services. If the price of aviation fuel rises significantly, the demand for cargo aircraft and air delivery services may decline further.

Our cost of providing airline services could be more than the contractual revenues generated.

The airlines each develop business plans for ACMI, charter and other operating contracts by projecting operating costs, crew productivity and maintenance expenses. Projections contain key assumptions, including flight hours, aircraft reliability, crewmember productivity and crewmember compensation and benefits. We may overestimate revenues, the level of crewmember productivity, and/or underestimate the actual costs of providing services when preparing for new business opportunities. If actual costs are higher than projected or aircraft reliability is less than expected, future operating results may be negatively impacted.

The Company’s three airlines rely on crews that are unionized. The respective collective bargaining agreements for ABX and CCIA were recently renegotiated and the collective bargaining agreement for ATI is scheduled for a ratification vote in mid-March 2011. If collective bargaining agreements increase our costs and we cannot recover the increases in costs, we may decide to terminate customer contracts or curtail planned growth. If disagreements arise, airline operations could be interrupted and business could be adversely affected until agreements are reached with the crewmembers.

Our airline operating agreements include on-time reliability requirements which can impact the Company's operating results and financial condition.

The airline operating agreements with DHL and BAX/Schenker contain monetary penalties if aircraft reliability falls below certain monthly thresholds. An airline could be found in default of an agreement if it does not maintain minimum thresholds over an extended period of time. The airline operating agreements also contain monthly incentive payments for reaching specific on-time reliability thresholds. As a result, our operating revenues can vary from period

to period depending on the achievement of those monthly incentives.

If ABX fails to maintain aircraft reliability above a minimum threshold in DHL's U.S. domestic network for two consecutive calendar months or three months in a rolling twelve month period, ABX would be in default of the CMI agreement with DHL. In that event, DHL may elect to terminate the CMI agreement, unless ABX maintains the minimum reliability threshold during a sixty-day cure period. If DHL terminates the CMI agreement due to an ABX event of default, ABX would be subject to a monetary penalty payable to DHL. The penalty at March 31, 2011 would be $15 million and will reduce to $10 million on March 31, 2012, and will remain at that amount through the initial term of the CMI agreement.

Under provisions of the CMI and lease agreements with DHL, DHL can terminate the CMI or lease agreements subject to early termination provisions.

DHL may terminate the CMI agreement for convenience at any time during the initial five-year term (other than the first twelve-months thereof) on the date that it ceases operating or causing to be operated the aircraft on air routes for which the origin and destination are within the United States, subject to providing six months notice and paying to ABX a termination fee. This termination fee will start at $70 million on March 31, 2011and amortize to zero during the remaining four year initial term of the CMI agreement. DHL may terminate one or more of the aircraft leases for convenience at any time after the first 24 months of the respective terms thereof, upon providing six months notice and paying to CAM a lump sum amount equal to six months rent. DHL may also terminate one or more aircraft leases at any time after the first 54 months of the term of the CMI agreement, in the event that DHL desires to transfer operational control of such aircraft, but is restricted from doing so by the terms of the collective bargaining agreement between ABX and its pilots' union providing that members of the pilots' union have the right to follow the aircraft to another operator, subject to providing six months notice and paying to CAM a lump sum amount equal to two months rent.

BAX/Schenker may reduce airlift requirements or contract for airlift with other providers.

CCIA and ATI have the exclusive right to supply all main deck freighter airlift in BAX/Schenker's U.S. domestic network. However, BAX/Schenker can remove an ATI or CCIA aircraft from service at the time an aircraft or engine on that aircraft requires a heavy maintenance event. ATI and CCIA's exclusive rights to supply airlift to BAX/Schenker is scheduled to expire on December 31, 2011, and BAX/Schenker has the right to terminate the exclusivity period before that date by paying a termination charge that declines ratably to zero through December 31, 2011.

AMC may not renew our contracts or may reduce the number of routes that we operate.

Our contracts with the AMC (an organization within the U.S. Military) are typically for one year and are not required to be renewed. The AMC may terminate the contracts for convenience or for an event of default, such as reliability. The number and frequency of AMC routes is sensitive to changes in military priorities and U.S. defense budgets.

Our business could be negatively impacted by adverse audit findings by the U.S. government.

Our U.S. Military contracts are subject to audit by government agencies, including with respect to performance, costs, internal controls and compliance with applicable laws and regulations. If an audit uncovers improprieties, we may be subject to civil or criminal penalties, including termination of such contracts, forfeiture of profits, fines and suspension from doing business with the U.S. Military.

Proposed rules from the Department of Transportation, the U.S. Federal Aviation Administration and the Transportation Security Administration would increase the Company's costs of operations and could reduce customers' utilization of airfreight.

In September 2010, the FAA proposed new rules for Flightcrew Member Duty and Rest Requirements (FMDRR). If implemented, the new rules would require a pilot to have nine hours for the opportunity to rest before reporting to flight duty and place other restrictions on the number of duty hours in particular time periods. If enacted, these rules could have a significant impact on ATSG airlines' costs of operation. The airlines would attempt to pass such additional costs onto their customers in the form of price increases. Customers, as a result, may seek to reduce their utilization of aircraft in favor of less expensive transportation alternatives. The ATSG airlines are each studying the proposed rules and evaluating the effect that the rules could have on their flight resources and costs.

The Company continues to make significant investments in additional aircraft which may impact the Company’s operating results and financial condition.

We plan to make capital investments to modify additional Boeing 767 standard freighter aircraft for service through 2011. We are also considering the development of a Boeing 757 combi variant. The actual demand for the Boeing 767 and 757 may be less than we anticipate. The actual lease rates for new modified aircraft may be less than we projected, or new leases may start later than we expect. Further, other airlines and lessors may be in a position to provide aircraft to the market before our aircraft are available for service.

The Company's future operating results and financial condition will depend in part on our subsidiaries’ ability to successfully deploy these aircraft in operations that provide a positive return on investment. Our success will depend, in part, on their ability to obtain and operate additional cargo volumes with customers other than DHL and BAX/Schenker, including international markets. Deploying aircraft in international markets can pose additional risks, regulatory requirements and costs.

The concentration of aircraft types and engines in the Company's airlines could adversely affect our operating and financial results.

The combined aircraft fleet is concentrated in four aircraft types. If any of theses aircraft types encounter technical difficulties that resulted in significant FAA Airworthiness Directives or grounding, our ability to lease the aircraft would be adversely impacted, as would our airlines' operations. The market growth in demand for the Boeing 767 and 757 aircraft types and configurations may be less than we anticipate. Customers may develop preferences for the Airbus A300-600 and A330 aircraft which provide capabilities similar to the Boeing 767 aircraft.

We rely on third parties to modify aircraft and provide aircraft and engine maintenance. If service providers do not deliver the level of service expected by our business, future operating results may be negatively impacted.

We rely on certain third party service providers that have expertise or resources that we do not have. An unexpected termination or delay involving such service providers could have a material adverse effect on our operations and financial results. We must effectively manage such third parties to meet aircraft modification schedules and maintenance events. A delay in an aircraft modification could adversely impact our revenues and our ability to place the aircraft in the market.

The Company could violate debt covenants.

The Company’s Credit Agreement and aircraft loans contain covenants, including, among other things, limitations on certain additional indebtedness, guarantees of indebtedness and the level of annual capital expenditures. The Credit Agreement and aircraft loans cross default. The Credit Agreement and loans stipulate events of default, including unspecified events that may have material adverse effects on the Company. If an event of default occurs, the Company’s cost of borrowings could increase, and the contractual repayment of debt may accelerate. Additionally, the Company’s ability to modify and deploy aircraft could be limited as a result.

Our access to liquidity could be less than we need for our expected growth plans and our cost of debt could increase.

The Company's existing Credit Agreement expires in December 2012. At that time, a balloon payment of $139.1 million is due to the consortium of banks that finance the Company's term loan, plus any draws on the revolving credit facility that may be outstanding on December 31, 2012. We are exploring alternatives which may secure longer term debt financing before the balloon payment is due. Alternatives which we may consider include amending and extending the current Credit Agreement beyond 2012, terminating and replacing the current Credit Agreement with a new bank facility as well as other alternatives. A new, follow-on credit agreement, assuming one can be obtained before 2012, may contain more restrictive covenants, dividend limitations, tighter restrictions on capital spending and higher costs of interest than the existing Credit Agreement. As of December 31, 2010, the Company had $3.6 million of capitalized loan origination costs and $4.6 million of unrealized losses from the hedging of interest payments that could adversely impact future operating results if the Credit Agreement is terminated early.

The ability to use net operating loss carryforwards to offset future taxable income for U.S. federal income tax purposes may be further limited.

Limitations imposed on the ability to use net operating losses (“NOLs”) to offset future taxable income could cause U.S. federal income taxes to be paid earlier than otherwise would be paid if such limitations were not in effect and

could cause such NOLs to expire unused, in each case reducing or eliminating the benefit of such NOLs. Similar rules and limitations may apply for state income tax purposes.

Significant ownership changes could limit our ability to use NOLs to offset future taxable income. In general, under Section 382 of the Internal Revenue Code of 1986, as amended (the “Code”), a corporation that undergoes an “ownership change” is subject to limitations on its ability to utilize its pre-change NOLs to offset future taxable income. In general, an ownership change occurs if the aggregate stock ownership of significant stockholders increases by more than 50 percentage points over such stockholders’ lowest percentage ownership during the testing period (generally three years).

We may need to reduce the carrying value of the Company’s assets.

The Company owns a significant amount of aircraft, aircraft parts and related equipment. Additionally, the balance sheet reflects assets for income tax carryforwards and other deferred tax assets. The removal of aircraft from service or continual losses from aircraft operations could require the Company to evaluate the recoverability of the carrying value of those aircraft, related parts and equipment in accordance with Financial Accounting Standards Board Accounting Standards Codification (“FASB ASC”) Topic 360-10, Property, Plant, and Equipment, and result in an impairment charge.

We have recorded significant amounts of goodwill and intangibles related to acquisitions. If we are unable to achieve the projected levels of operating results and these assets are impaired, it may be necessary to record a non-cash charge to earnings.

If the Company incurs operating losses or our estimates of expected future earnings indicate a decline, it may be necessary to reassess the need for a valuation allowance for some or all of the Company’s net deferred tax assets.

Penalties, fines and sanctions levied by governmental agencies or the costs of complying with government regulations could negatively affect our results of operations.

The operations of the Company’s subsidiaries are subject to complex aviation, transportation, security, environmental, labor, employment and other laws and regulations. These laws and regulations generally require our subsidiaries to maintain and comply with a wide variety of certificates, permits, licenses and other approvals. Their inability to maintain required certificates, permits or licenses, or to comply with applicable laws, ordinances or regulations could result in substantial fines or, in the case of DOT and FAA requirements, possible suspension or revocation of their authority to conduct operations.

The costs of maintaining the aircraft in compliance with government regulations could negatively affect our results of operations.

All aircraft in the Company’s airline subsidiaries’ in-service fleets were manufactured prior to 1990. Manufacturer Service Bulletins and the FAA Airworthiness Directives issued under its “Aging Aircraft” program cause operators of such aged aircraft to be subject to extensive aircraft examinations and require such aircraft to undergo structural inspections and modifications to address problems of corrosion and structural fatigue at specified times. The FAA may issue Airworthiness Directives that could require significant inspections and major modifications to such aircraft. The FAA may issue Airworthiness Directives that could limit the usability of certain aircraft types. The FAA is currently considering the issuance of an airworthiness directive that may require the replacement of the aft pressure bulkhead on Boeing 767-200 aircraft based on a certain number of landing cycles. If such an Airworthiness Directive is issued, all of the Boeing 767s within the Company will be affected over approximately a seven year period. The cost of compliance is estimated to be $1.0 million per aircraft.

In addition, new FAA regulations require that aircraft manufacturers must establish limits on an aircraft flight cycle as described in Item 1, under Federal Aviation Administration Regulation of this report. These regulations may increase our maintenance costs and eventually limit the use of our aircraft.

Failure to maintain the operating certificates and authorities of ABX, ATI and CCIA would adversely affect our business.

The airline subsidiaries have the necessary authority to conduct flight operations pursuant to the economic authority issued by the DOT and the safety based authority issued by the FAA. The continued effectiveness of such authority is subject to their compliance with applicable statutes and DOT, FAA and TSA rules and regulations, including any new rules and regulations that may be adopted in the future. The loss of such authority by an airline subsidiary could cause

a default of covenants within the Credit Agreement and would materially and adversely affect its airline operations, effectively eliminating the airline's ability to operate air services.

The Company may be affected by global climate change or by legal, regulatory or market responses to such potential climate change.

The Company is subject to the regulations of the U.S. Environmental Protection Agency and state and local governments regarding air quality and other matters. In part, because of the highly industrialized nature of many of the locations at which the Company operates, there can be no assurance that we have discovered all environmental contamination for which the Company may be responsible.

Concern over climate change, including the impact of global warming, has led to significant federal, state and international legislative and regulatory efforts to limit greenhouse gas emissions. The European Commission has mandated the extension of the European Union Emissions Trading Scheme ("ETS") for greenhouse gas emissions to the airline industry. Under this decision, all Company airline subsidiary flights to and from any airport in any member state of the European Union will be covered by the ETS requirements beginning in 2012, and each year we will be required to submit emission allowances in an amount equal to the carbon dioxide emissions from such flights. The U.S. Congress has considered the regulation of greenhouse gas emissions. Also, the U.S. Environmental Protection Agency could regulate greenhouse gas emissions, especially aircraft engine emissions. The cost to comply with potential new laws and regulations could be substantial for the Company. These costs could include an increase in the cost of the fuel and capital costs associated with updating aircraft. Until the timing, scope and extent of any future regulation becomes known, we cannot predict its effect on the Company’s cost structure or operating results.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

The Company leases portions of the air park in Wilmington, Ohio under a lease agreement with a regional port authority, the term of which expires in May of 2019. The lease includes corporate offices, 210,000 square feet of maintenance hangars and a 100,000 square foot component repair shop at the air park. ABX also has the non-exclusive right to use the airport, which includes one active runway, taxi ways and ramp space. .

As of December 31, 2010, the Company and its subsidiaries owned 54 aircraft, leased six aircraft under capital leases and four aircraft under operating leases, for a total of 64 aircraft in service condition. All of the aircraft were previously owned and operated. Once acquired, the aircraft were modified for cargo operations, except for one Boeing 767 aircraft that remains in passenger configuration. These aircraft are generally described as having medium to medium wide-body cargo capabilities. The cargo aircraft carry gross payloads ranging from approximately 48,000 to 119,500 pounds. These aircraft are well suited for intra-continental flights and medium range inter-continental flights. Because an airline's flight operations can be hindered by inclement weather, sophisticated landing systems and other equipment are utilized to minimize the effect that weather may have on flight operations. For example, ABX’s Boeing 767-200 aircraft are operated for Category III landings. This allows their crews to land under weather conditions with runway visibility of only 600 feet at airports with Category III Instrument Landing Systems.

The table below shows the combined in-service fleet of aircraft.

| | | | | | | | | | | |

| | | Number of Aircraft as of December 31, 2010 | | | | | |

| Aircraft Type | | Total | | Owned | Capital lease | Operating lease | Year of Manufacture | | Gross Payload (Lbs.) | | Still Air Range (Nautical Miles) |

| | | | | | | | | | | | |

| 767-200 SF (1) | | 32 | | 30 | - | 2 | 1982 - 1987 | | 67,000 - 91,000 | | 1,800 - 4,400 |

| 767-200 ER (3) | | 1 | | 1 | - | - | 1985 | | | | 5,000 |

| 767-300 SF (1) | | 1 | | - | - | 1 | 1989 | | 119,500 | | 1,800 - 4,400 |

| DC-8-F (1) | | 11 | | 11 | - | - | 1967 - 1969 | | 96,000 - 108,800 | | 1,800 - 4,400 |

| DC-8-CF (2) | | 4 | | 4 | - | - | 1968 - 1970 | | 80,000 - 85,000 | | 1,800 - 4,400 |

| 727-200 SF (1) | | 13 | | 6 | 6 | 1 | 1973 - 1981 | | 52,300 - 61,000 | | 1,200 - 2,100 |

| 757-200 SF (1) | | 2 | | 2 | - | - | 1984 - 1986 | | 48,000 - 68,000 | | 2,700 - 4,000 |

| Total in-service | | 64 | | 54 | 6 | 4 | | | | | |

In addition, as of December 31, 2010, CAM had two Boeing 767-200 aircraft and one Boeing 767-300 aircraft, not reflected in the table above, that were undergoing modification to a standard freighter configuration. CAM also had four Boeing 767-200 aircraft and two Boeing 767-300, not reflected in the table above, that were scheduled to undergo modification to standard freighter configuration. At December 31, 2010, the Company had three spare airframes that had been removed from service. The engines and rotables from these aircraft are being used to support other aircraft in the combined fleet. Provisions of the Company’s credit agreement require that the aircraft are maintained in airworthy condition. Exceptions to the requirement are made on a case-by-case basis with the consent of the lead agent to the credit facility. Such exceptions were granted by the lead agent for the spare airframes and the aircraft undergoing modification.

As of December 31, 2010, ABX operated 24 Boeing 767-200 aircraft and one Boeing 767-300 aircraft (11 of the 767-200 aircraft were leased by CAM to DHL and operated by ABX); ATI operated three Boeing 767-200 aircraft, 11 DC-8 freighter aircraft and four DC-8 combi aircraft; and CCIA operated 13 Boeing 727 aircraft and two Boeing 757 aircraft. CAM's Boeing 767 passenger aircraft is scheduled to begin an Atlantic operation in April 2011. In addition to these aircraft, CAM leased five Boeing 767-200 aircraft to other airlines.

We believe that our existing facilities, aircraft fleet and planned aircraft investments as described in Note I to the accompanying financial statements, are appropriate for our current operations and growth plans. We may make additional investments in aircraft and facilities if we identify favorable opportunities in the markets that we serve.

____________________

| |

| (1) | These aircraft are configured for standard cargo containers, including large standard main deck cargo doors. |

| |

| (2) | These aircraft are configured as “combi” aircraft capable of carrying passenger and cargo containers on the main flight deck. |

| |

| (3) | Passenger configured aircraft. |

ITEM 3. LEGAL PROCEEDINGS

Department of Transportation (“DOT”) Continuing Fitness Review

ABX filed a notice of substantial change with the DOT arising from its separation from Airborne, Inc., in August of 2003. The filing was initially made in mid-July of 2003 and thereafter updated in April of 2005, September of 2007, December of 2007 and March of 2010, with respect to subsequent events relevant to the DOT's analysis, including the reorganization of ABX under a holding company structure and the acquisition of Cargo Holdings International, Inc.

The DOT was required to determine whether ABX continues to be a U.S. citizen and is fit, willing and able to engage in air transportation of cargo. On January 24, 2011, the DOT issued an order dismissing its notice, dated August 6, 2003, requesting public comments on the procedures to be employed in reviewing the impact of the proposed substantial changes in ownership and operations on the citizenship of ABX. On March 4, 2011, the DOT notified ABX that, based on its review of the previously filed and updated information, it appears that ABX continues to be a U.S citizen and remains fit to conduct air transportation operations as a U.S. certificated air carrier.

Civil Action Alleging Violations of Immigration Laws

On December 31, 2008, a former ABX employee filed a complaint against ABX, a total of four current and former executives and managers of ABX, Garcia Labor Company of Ohio, and three former executives of the Garcia Labor companies, in the U.S. District Court for the Southern District of Ohio. The case was filed as a putative class action against the defendants, and asserts violations of the Racketeer Influenced and Corrupt Practices Act (RICO). The complaint, which was later amended to include a second former employee plaintiff, seeks damages in an unspecified amount and alleges that the defendants engaged in a scheme to hire illegal immigrant workers to depress the wages paid to hourly wage employees during the period from December 1999 to January 2005. On March 18, 2010, the Court issued a decision in response to a motion filed by ABX and the other ABX defendants, dismissing three of the five claims constituting the basis of Plaintiffs' complaint. Most recently, the Court issued a decision on October 7, 2010, permitting the plaintiffs’ to amend their complaint for the purpose of reinstating one of their dismissed claims. On October 26, 2010, ABX and the other ABX defendants filed an answer denying the allegations contained in plaintiffs’ second amended complaint.

The complaint is similar to a prior complaint filed by another former employee in April 2007. The prior complaint was subsequently dismissed without prejudice at the plaintiff’s request on November 3, 2008.

FAA Enforcement Actions

The Company’s airline operations are subject to complex aviation and transportation laws and regulations that are continually enforced by the DOT and FAA. The Company’s airlines receive letters of investigation (“LOIs”) from the FAA from time to time in the ordinary course of business. The LOIs generally provide that some action of the airline may have been contrary to the FAA’s regulations. The airlines respond to the LOIs and if the response is not satisfactory to the FAA, it can seek to impose a civil penalty for the alleged violations. Airlines are entitled to a hearing before an Administrative Law Judge or a Federal District Court Judge, depending on the amount of the penalty being sought, before any penalty order is deemed final.

The FAA issued LOIs to CCIA arising from a focused inspection of that airline’s operations during the fourth quarter of 2009 which could result in the FAA seeking monetary penalties against CCIA. ABX received an LOI from the FAA alleging that ABX failed to comply with an FAA Airworthiness Directive involving its Boeing 767 aircraft and proposing a monetary settlement. The Company believes it has adequately reserved for those monetary penalties being proposed by the FAA, although it’s possible that the FAA may propose additional penalties exceeding the amounts currently reserved.

Environmental Matters

The Ohio Environmental Protection Agency (“OEPA”) was contemplating a proceeding against DHL, in its former capacity as the owner of Wilmington Air Park (“ILN"), and ABX, in its former capacity as the permit holder for the stormwater treatment system at ILN, arising from the unauthorized discharge of stormwater from ILN on or about May 7, 2008, and seeking a monetary penalty in the amount of $210,000. DHL, which had agreed to indemnify ABX for claims arising from this matter under the terms of the Mutual Termination Agreement and Release, dated March 29, 2010, among DPWN Holdings (USA), Inc., DHL Network Operations (USA), Inc., DHL Express (USA), Inc., Air Transport Services Group, Inc. and ABX Air, Inc., subsequently held discussions with the OEPA regarding this matter. Thereafter, on January 5, 2011, the OEPA issued the Director's Final Findings and Orders pursuant to which DHL Express (USA), Inc. agreed to pay $80,000 to the OEPA in full settlement of the contemplated proceeding and related matters against DHL and ABX.

Other

In addition to the foregoing matters, we are also currently a party to legal proceedings in various federal and state jurisdictions arising out of the operation of our business. The amount of alleged liability, if any, from these proceedings cannot be determined with certainty; however, we believe that our ultimate liability, if any, arising from the pending legal proceedings, as well as from asserted legal claims and known potential legal claims which are probable of assertion, taking into account established accruals for estimated liabilities, should not be material to our financial condition or results of operations.

ITEM 4. RESERVED

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Common Stock

Our common stock is publicly traded on the NASDAQ Global Select Market under the symbol ATSG. Prior to May 21, 2008, our symbol on the NASDAQ Global Select Market was ABXA. The following table shows the range of high and low prices per share of our common stock for the periods.

| | | | | | | |

| 2010 Quarter Ended: | Low | | High |

| December 31, 2010 | $ | 5.99 | | | $ | 8.10 | |

| September 30, 2010 | $ | 4.48 | | | $ | 6.50 | |

| June 30, 2010 | $ | 3.52 | | | $ | 6.03 | |

| March 31, 2010 | $ | 1.78 | | | $ | 3.49 | |

| | | | |

| 2009 Quarter Ended: | Low | | High |

| December 31, 2009 | $ | 2.11 | | | $ | 3.50 | |

| September 30, 2009 | $ | 2.13 | | | $ | 4.06 | |

| June 30, 2009 | $ | 0.44 | | | $ | 2.49 | |

| March 31, 2009 | $ | 0.17 | | | $ | 0.84 | |

On March 8, 2011, there were 1,800 stockholders of record of the Company’s common stock. The closing price of the Company’s common stock was $8.25 on March 8, 2011.

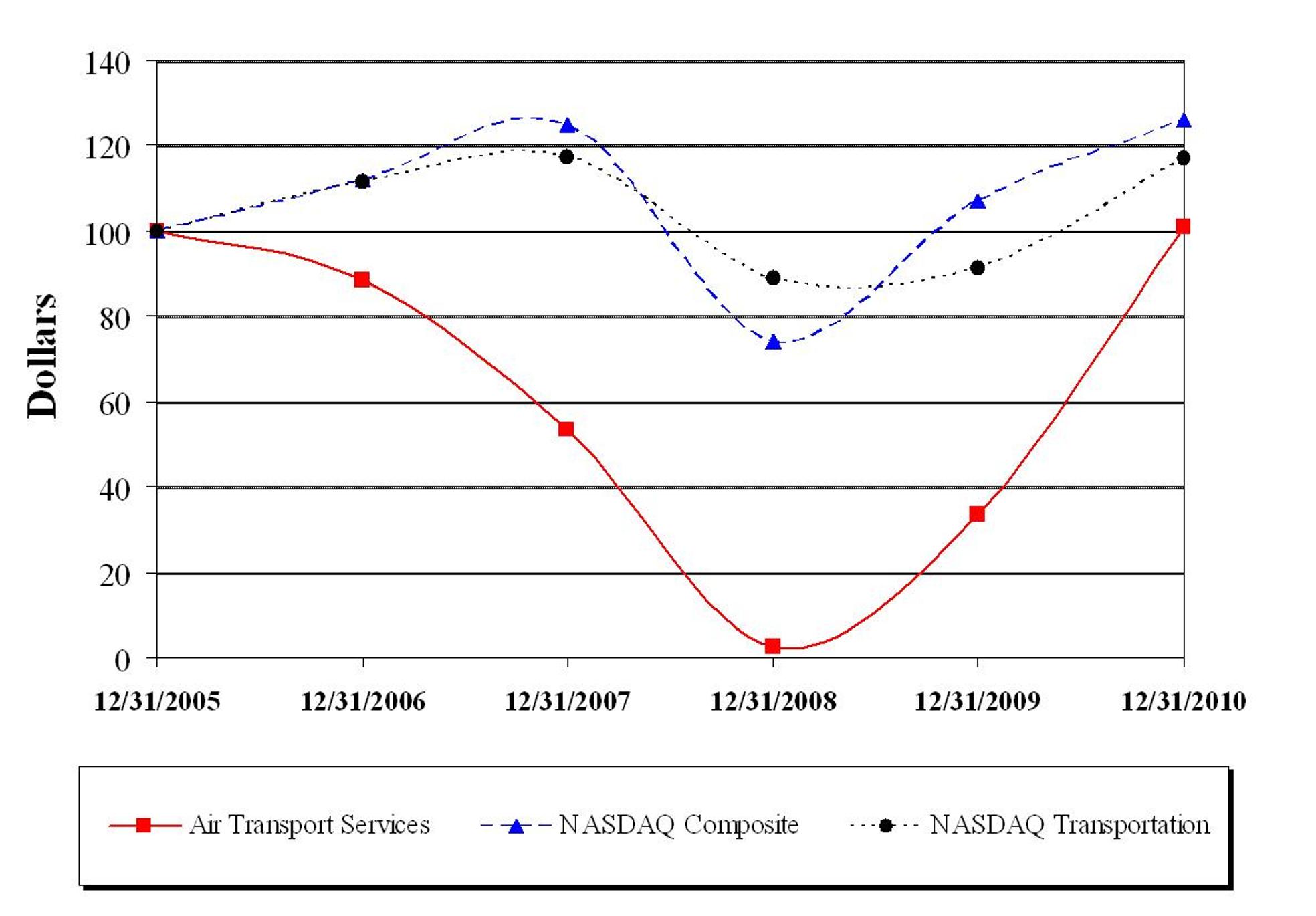

Performance Graph

The graph below compares the cumulative total stockholder return on a $100 investment in the Company’s common stock with the cumulative total return of a $100 investment in the NASDAQ Global Select Market and the cumulative total return of a $100 investment in the NASDAQ Transportation Index for the period beginning on December 31, 2005 and ending on December 31, 2010.

| | | | | | | | | | | | | | | | | |

| | 12/31/2005 | | 12/31/2006 | | 12/31/2007 | | 12/31/2008 | | 12/31/2009 | | 12/31/2010 |

| Air Transport Services Group, Inc. | 100.00 | | | 88.28 | | | 53.25 | | | 2.29 | | | 33.63 | | | 100.64 | |

| NASDAQ Composite Index | 100.00 | | | 111.74 | | | 124.67 | | | 73.77 | | | 107.12 | | | 125.93 | |

| NASDAQ Transportation Index | 100.00 | | | 111.57 | | | 117.39 | | | 88.90 | | | 91.15 | | | 117.01 | |

Dividends

The Company is restricted from paying dividends on its common stock in excess of $50.0 million during any calendar year under the provisions of its credit agreement. Under the provisions of its promissory note due to DHL, the Company is required to prepay the DHL note $0.20 for each dollar of dividend distributed to the stockholders of ATSG. The same prepayment stipulation applies to stock repurchases. No cash dividends have been paid or declared.

Securities authorized for issuance under equity compensation plans

For the response to this Item, see Item 12.

ITEM 6. SELECTED CONSOLIDATED FINANCIAL DATA

The following selected consolidated financial data should be read in conjunction with the consolidated financial statements and the notes thereto and the information contained in Item 7 of Part II, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The selected consolidated financial data and the consolidated operations data below are derived from the Company’s audited consolidated financial statements. | | | | | | | | | | | | | | | | | | | |

| As of and for the Years Ended December 31 |

| | 2010 | | 2009 | | 2008 | | 2007 | | 2006 |

| | (In thousands, except per share data) |

| OPERATING RESULTS (1): | | | | | | | | | |

| Continuing revenues | $ | 667,382 | | | $ | 823,483 | | | $ | 941,686 | | | $ | 573,256 | | | $ | 548,576 | |

| Operating expenses | 585,706 | | | 751,693 | | | 963,638 | | | 538,025 | | | 514,014 | |

| Net interest expense | 18,359 | | | 26,432 | | | 34,667 | | | 9,510 | | | 6,772 | |

| Earnings (loss) from continuing operations before income taxes (3) | 63,317 | | | 45,358 | | | (56,619 | ) | | 25,721 | | | 27,790 | |

| Income tax benefit (expense) (2) | (23,413 | ) | | (17,156 | ) | | (6,229 | ) | | (10,898 | ) | | 57,096 | |

| Earnings (loss) from continuing operations | 39,904 | | | 28,202 | | | (62,848 | ) | | 14,823 | | | 84,886 | |

| Discontinued earnings, net of tax (4) | (70 | ) | | 6,247 | | | 6,858 | | | 4,764 | | | 5,168 | |

| Net earnings (loss) | $ | 39,834 | | | $ | 34,449 | | | $ | (55,990 | ) | | $ | 19,587 | | | $ | 90,054 | |

| EARNINGS (LOSS) PER SHARE FROM CONTINUING OPERATIONS (1): | | | | | | | | | |

| Basic | $ | 0.64 | | | $ | 0.45 | | | $ | (1.01 | ) | | $ | 0.26 | | | $ | 1.46 | |

| Diluted | $ | 0.62 | | | $ | 0.44 | | | $ | (1.01 | ) | | $ | 0.25 | | | $ | 1.45 | |

| WEIGHTED AVERAGE SHARES (1): | | | | | | | | | |

| Basic | 62,807 | | | 62,674 | | | 62,484 | | | 58,296 | | | 58,270 | |

| Diluted | 64,009 | | | 63,279 | | | 62,484 | | | 58,649 | | | 58,403 | |

SELECTED CONSOLIDATED | | | | | | | | | |

| FINANCIAL DATA (1): | | | | | | | | | |

| Cash and cash equivalents | $ | 46,543 | | | $ | 83,229 | | | $ | 116,114 | | | $ | 59,271 | | | $ | 63,219 | |

| Deferred income tax asset (2) | 12,879 | | | 31,597 | | | 74,979 | | | 35,056 | | | 101,715 | |