1 1 Annual Meeting of Shareholders May 11, 2010 Exhibit 99.1 |

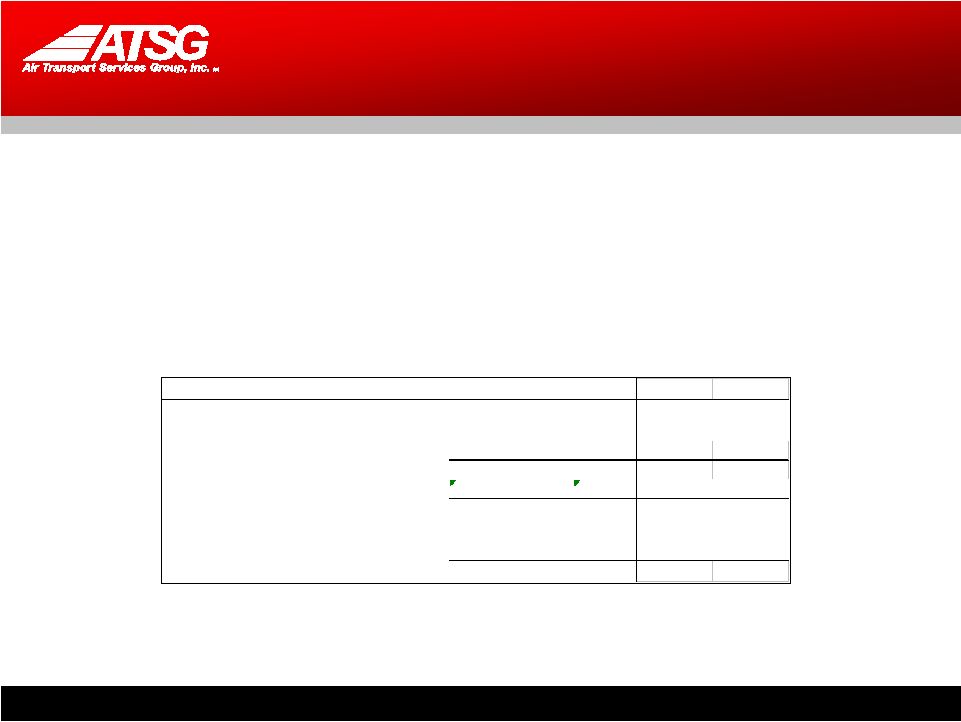

2 2 Safe Harbor Except for historical information contained herein, the matters discussed in this presentation contain forward-looking statements that involve risks and uncertainties. There are a number of important factors that could cause Air Transport Services Group's ("ATSG's") actual results to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, changes in market demand for our assets and services, the timely completion of 767 freighter modifications as anticipated under ABX Air’s new operating agreement with DHL, ABX Air’s ability to maintain on-time service and control costs under its new operating agreement with DHL, and other factors that are contained from time to time in ATSG's filings with the U.S. Securities and Exchange Commission, including its Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. Readers should carefully review this presentation and should not place undue reliance on ATSG's forward-looking statements. These forward-looking statements were based on information, plans and estimates as of the date of this release. ATSG undertakes no obligation to update any forward-looking statements to reflect changes in underlying assumptions or factors, new information, future events or other changes. ATSG, Inc. Non-GAAP Reconciliation Earnings from Continuing Operations Before Interest, Taxes, Depreciation, and Amortization (Adjusted EBITDA) (Unaudited) EBITDA and Adjusted EBITDA are non-GAAP financial measures and should not be considered alternatives to net income (loss) or any other performance measure derived in accordance with GAAP. EBITDA is defined as income (loss) from operations plus net interest expense, provision for income taxes, depreciation and amortization. The Company’s management uses these adjusted financial measures in conjunction with GAAP finance measures to monitor and evaluate its performance, including as a measure of liquidity. EBITDA and Adjusted EBITDA should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP, or as alternative measures of liquidity. 2007 2008 2009 1Q2009 1Q2010 25,721 (56,619) 45,358 13,193 10,784 Impairment of goodwill & intangibles 0 91,241 0 0 0 25,721 34,622 45,358 13,193 10,784 Interest Income (4,557) (2,335) (449) -178 -73 Interest Expense 14,067 37,002 26,881 7,646 5,189 Depreciation and amortization 51,635 93,752 83,964 21,473 20,800 86,866 163,041 155,754 42,134 36,700 GAAP Pre-tax Earnings (Loss) Reconciliation Statement ($ in 000s) Adjusted EBITDA from Cont. Oper. from Continuing Operations Adjusted Pre-Tax Earnings from Continuing Operations |

3 3 2009 in Review 2009 Financial Results & Balance Sheet Improvement 2010 Focus Goals DHL Agreements 767 Conversion Program Marketing Strategy Wrap-up & Your Questions Agenda Joe Hete President & Chief Executive Officer Quint Turner Chief Financial Officer Joe Hete President & Chief Executive Officer Rich Corrado Chief Commercial Officer Joe Hete President & Chief Executive Officer |

4 4 2009 Goals and Achievements Achievements Note balance reduced, capital leases transferred to DHL Superior service quality maintained 767 mod program on track; 4 completed by year-end 2009 Framework established with DHL to lease 13 767s, CAM leases 3 others Long-term debt reduced $135M, post- retirement obligations down $145M AMES established in May 2009 ABX Air pilots approve new CBA, reduced overhead costs by $21M Goals Restructure DHL promissory note and capital leases Continue to support DHL transition Reconfigure non-standard B767PC fleet to serve broad customer base Seek long-term commitments for B767 fleet Further strengthen balance sheet Leverage maintenance capability Align cost structure |

5 5 Financial Results & Balance Sheet Improvement Quint Turner, CFO |

6 6 2009 Financial Performance Annual Results $ in millions Non-DHL DHL ACMI DHL S&R Agreement Revenues from Continuing Operations $451.4 2008 $941.7 $823.5 $29.1 $29.1 2009 $419.3 $282.8 $121.4 $121.4 $461.2 Pre-tax Earnings From Continuing Operations 2008 $45.4 2009 $34.6* * Excluding goodwill and intangible impairment charges -$56.6 |

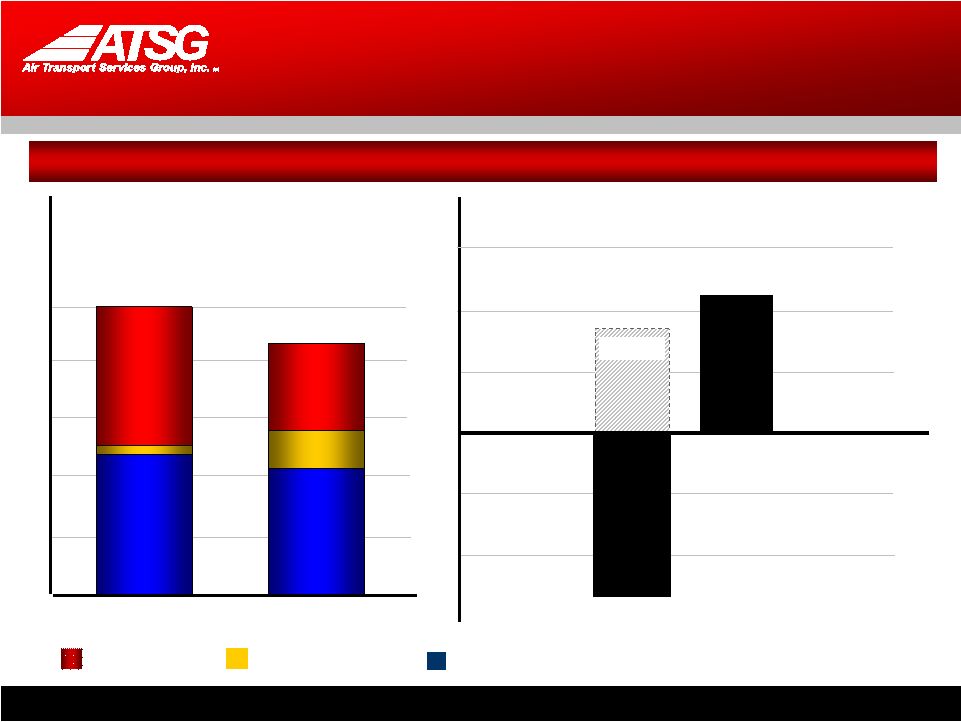

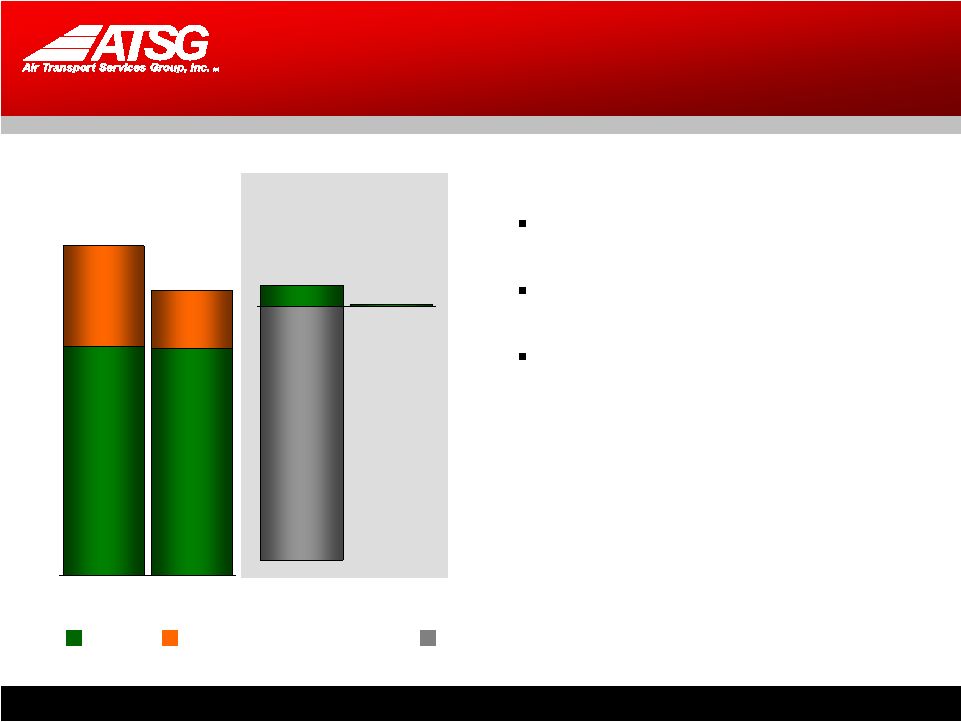

7 7 2009 Results – DHL Segment * * From continuing operations 2008 2009 2008 2009 Revenues Pre-tax Earnings Block hours down 78% as DHL converted U.S. to international- only service in January 2009 Severance & retention includes gains on pilot S&R, vacation reimbursement. Excludes discontinued operations (Hub Services and fuel) $282.8 $451.4 $121.4 $29.1 $404.2 $480.5 $11.2 $13.6 $16.7 $27.9 $14.4 $0.8 ACMI S&R $ in millions |

8 8 2009 Results – ACMI Services * * Earnings include intangible charges totaling $91.2 million pre-tax for goodwill, customer intangibles 2008 2009 Revenues Pre-tax Earnings 11% increase in block hours reflect additional 767s in service Fuel costs down 42%, lowering reimbursement revenues ABX Air ACMI losses, including transatlantic scheduled service $289.5 $292.8 $75.2 $128.2 $0.5 $7.1 $364.7 $421.0 2008 2009 Fuel & other Reimbursable ACMI Impairment charges -$84.1 -$91.2 $ in millions |

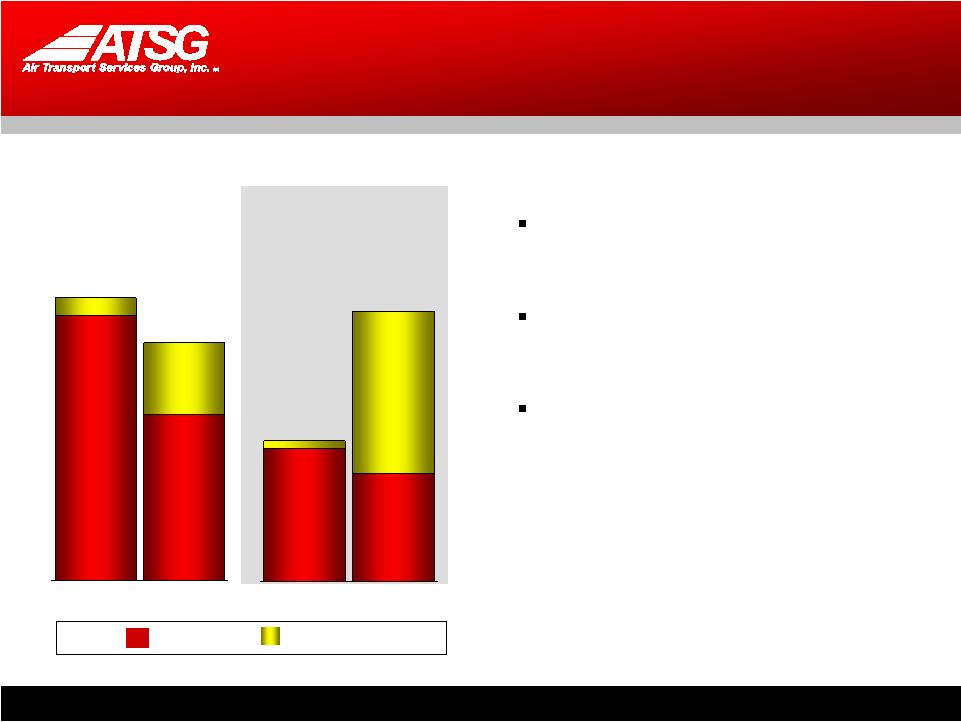

9 9 2009 Results – CAM 2008 2009 2008 2009 Revenues Pre-tax Earnings Eight 767 aircraft added during 2009 767 conversion program on track with seven of 14 now completed or in mod Amerijet leases in March first of two 767s including certification, pilot training, maintenance, etc. $47.5 $60.7 $18.1 $22.8 $ in millions |

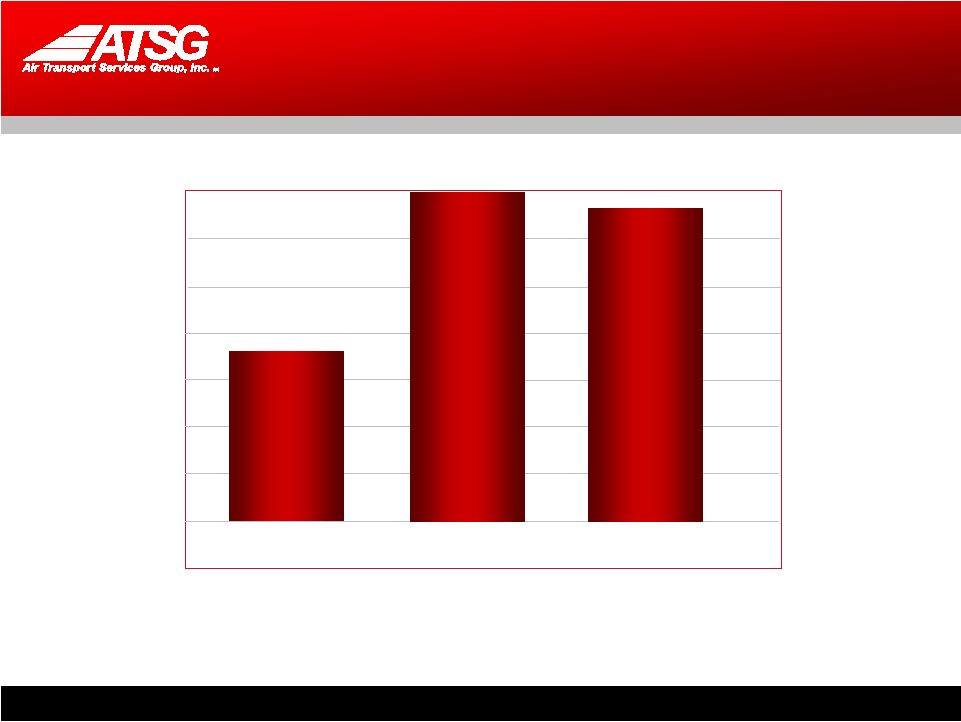

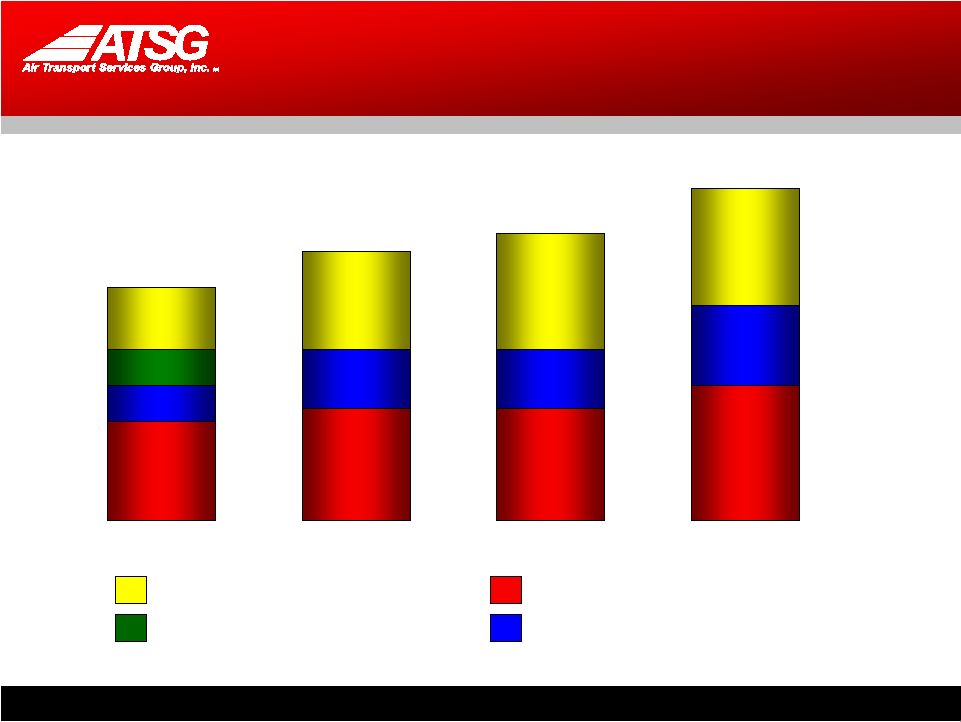

10 10 Adjusted EBITDA from Continuing Operations * 2007 $86.9 $94.5 M *Adjusted EBITDA from Continuing Operations is a non-GAAP financial measure and should not be considered as an alternative to net income (loss) or any other performance measure derived in accordance with GAAP. 2008 amounts exclude impairment charges totaling $91.2 million related to goodwill and customer intangibles. Please refer to Slide 2 for a statement showing a reconciliation of Adjusted EBITDA from Continuing Operations to GAAP Net Income." $163.0 2008 2009 $155.8 $ in millions |

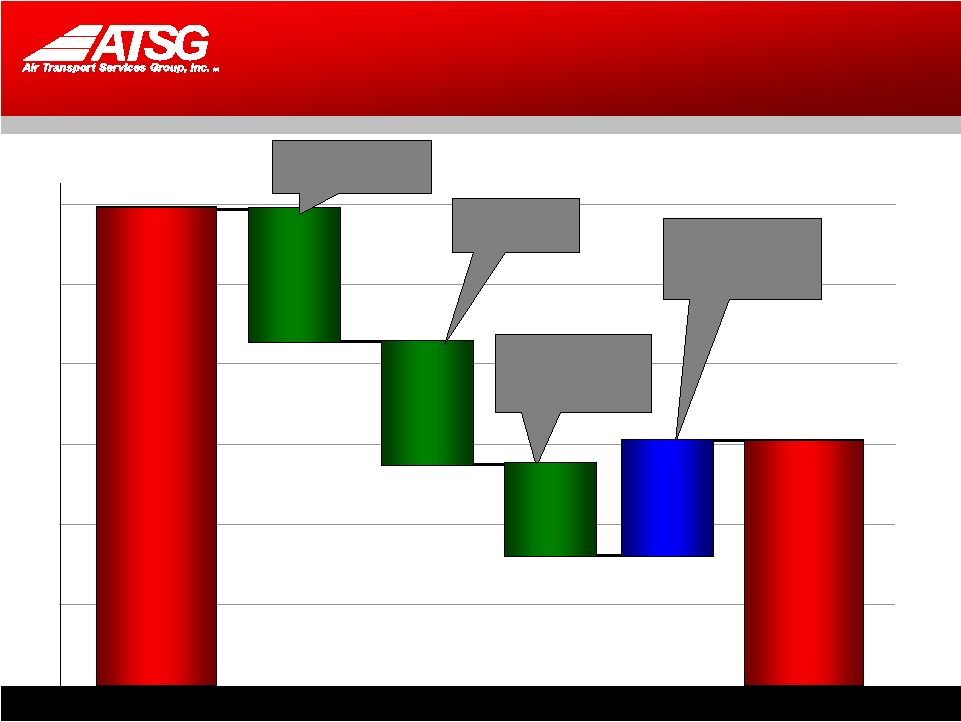

11 11 Total Debt declines $135 Million Transfer of Transfer of Aircraft Capital Aircraft Capital Leases to DHL Leases to DHL $46.3 $43.1 Principal Principal payments payments $377.4 $512.5 $45.7 DHL Promissory DHL Promissory Note Note Extinguishment Extinguishment $ in millions YE 2008 YE 2009 |

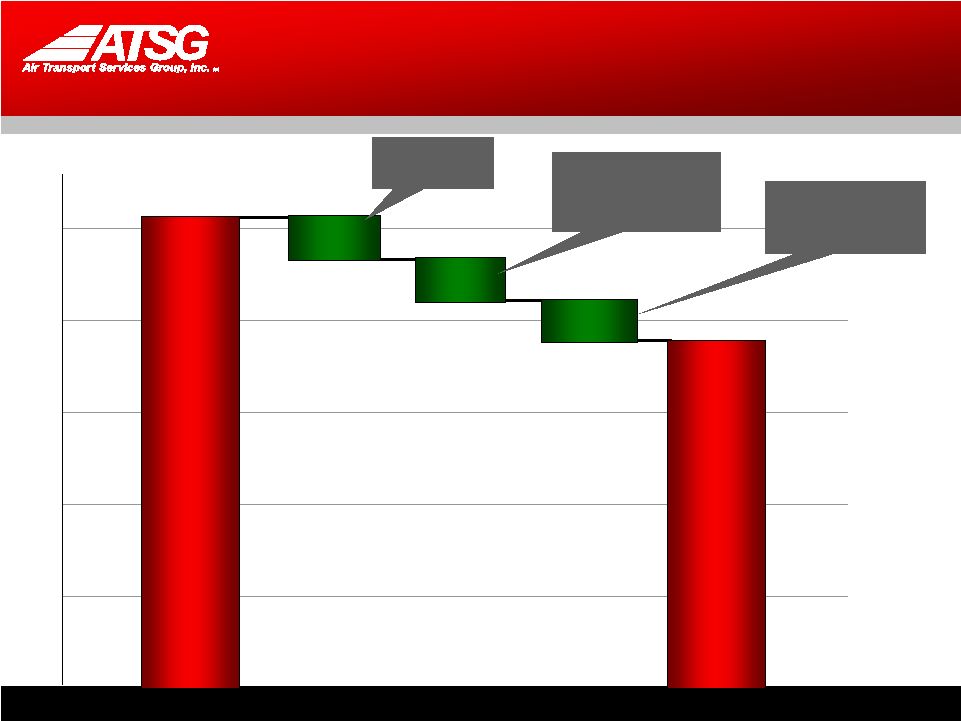

12 12 Post-retirement obligations decline $145 million $152.7 $297.3 Actuarial Actuarial costs & costs & adjustments adjustments $83.2 $75.8 $71.7 Employer Employer contributions contributions Workforce Workforce contraction contraction & plan freeze & plan freeze $57.3 $ in millions YE 2008 YE 2009 Gains on Gains on assets assets |

13 13 First Quarter 2010 Results Revenues Earnings DHL $ 48,487 DHL $ 8,283 ACMI Services 98,226 ACMI Services (900) CAM 17,802 CAM 6,539 Other 17,453 Other (1,336) Eliminations (21,024) Interest (1,802) Total- Cont. Oper. $ 160,944 Pretax Earnings–Cont. Oper. $ 10,784 Income Taxes (4,034) Net Earnings-Cont. Oper. $6,750 Net Earnings-Discont. Oper. 405 Net Earnings $7,155 $ in thousands |

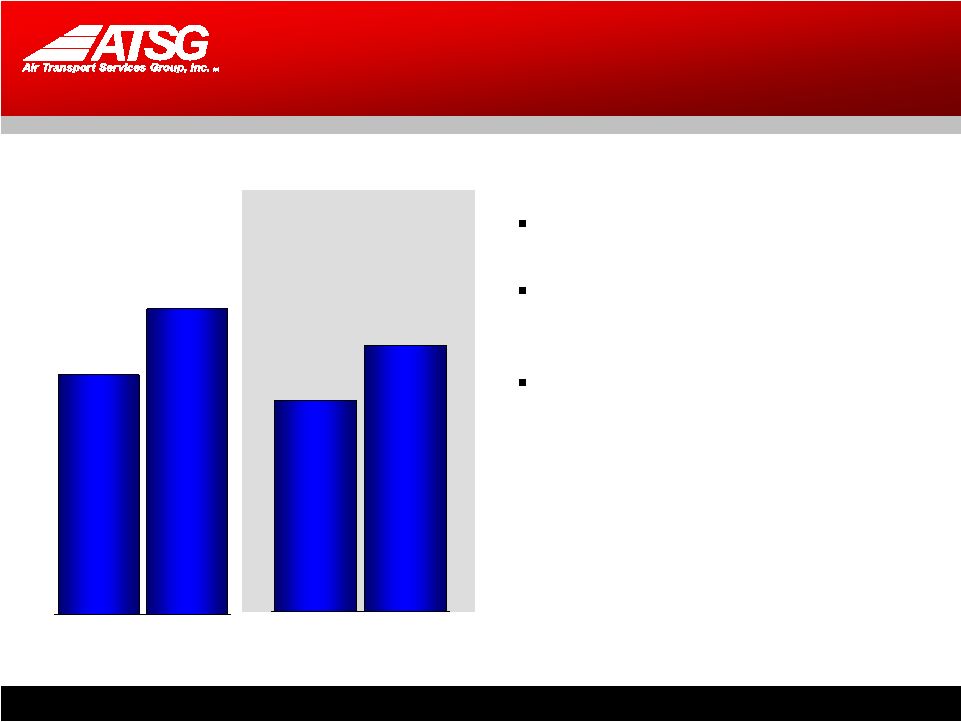

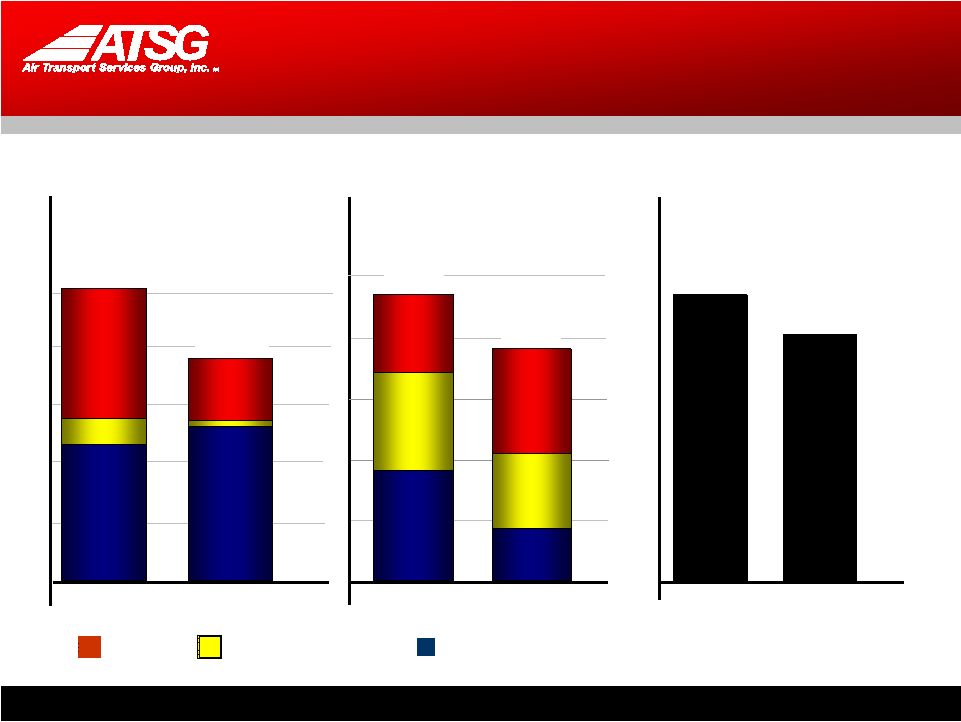

14 14 First Quarter 2010 vs. 2009 $ in millions Revenues from Continuing Operations 2009 2010 Non-DHL & Intercompany DHL ACMI Pre-tax Earnings from Continuing Operations $211.8 $160.9 $94.3 $19.2 $112.4 $44.5 2009 2010 $13.2 $10.8 $3.6 $5.1 $2.5 $4.8 $4.5 $3.5 Severance & Retention $98.2 $4.0 42.1 36.3 EBITDA from Continuing Operations 2009 2010 $42.1 $36.7 |

15 15 2010 Focus |

16 16 Plotting A Course For Growth 2010 Goals Execute and deliver results against new DHL Agreements Continue 767 conversions, deploy all freighters under long-term agreements Further strengthen balance sheet Leverage complementary service offerings in global marketing strategy Capture cost and workforce flexibility advantages from ABX CBA, AMES platform Strategically invest for growth and further diversification |

17 17 DHL Agreements |

18 18 New A+CMI Agreements with DHL New “A+CMI” Agreement Terms DHL leasing thirteen 767 aircraft from CAM under seven-year terms, unlocking market value of assets ABX to operate aircraft for DHL under separate five-year CMI agreement, with two-year extension right to DHL Economics based upon pre-defined fee, scalable for number of aircraft operated by ABX, with performance incentive bonuses CMI agreement subject to break-up fee should DHL elect to prematurely terminate Under the CMI, ABX contracts with AMES for airframe heavy maintenance, reimbursable by DHL under lease agreements The remaining $31M in the DHL Note will amortize over five-year term of the CMI with no cash requirement from ATSG; interest expense continues to be reimbursed Other Issues Resolved DHL agreed to pay ABX $31M to settle DC-9 and Boeing 767 aircraft put values DHL agreed to remit $11.2M in May to settle the reimbursement of accrued vacation paid to employees adversely impacted by DHL’s restructuring |

19 19 767 Conversion Program |

20 20 Deploying Our 767SFs 11-14 11-18 April 2011 Jan. 2012 DHL-CAM Leased SFs Other Customers-CAM Leased SFs 11-14 11 Jan. 2011 4 Pace of 767 modifications could be affected by possible assignment of modification slots to DHL. 7 11 April 2010 DHL- Interim Leased SFs ACMI Services – ACMI/Charter SFs 13 13 4 5-8 5-8 5-12 26 30 32 36 |

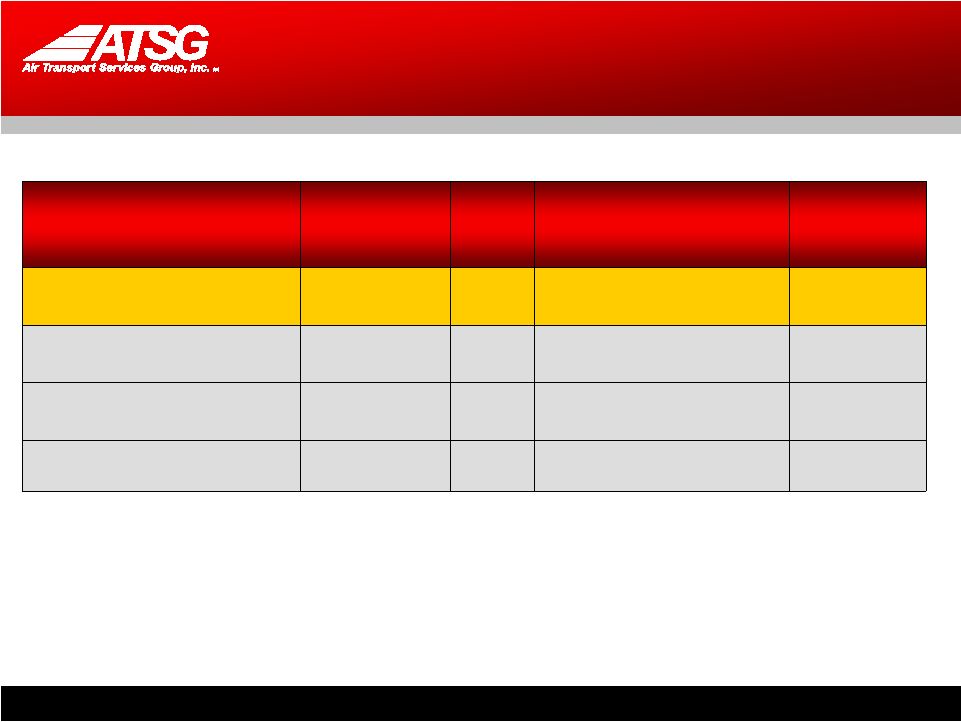

21 21 767 Advantages vs. Aging Fleets Aircraft Fuel (gal./ block hr) Crew Payload (lbs.)/ Capacity (cu.ft.) Range (NM) 767-200SF 1,380 2 100,000 / 11,138 2,800 A300-B4 1,900 3 99,200 / 11,445 1,680 DC-8 63 1,760 3 96,800 / 10,060 2,150 DC-8 73 1,600 3 111,800 / 10,060 2,470 |

22 22 Marketing Strategy Rich Corrado, Chief Commercial Officer |

23 23 Emerging Go-to-Market Strategy Drive higher return on capital by optimally positioning opportunities and bundling additional services CAM a neutral, non-airline, lead sales organization that can drive a bundled marketing strategy Develop packaged programs cross- selling entities Amerijet International program symbolizes this approach Market Approach Market Opportunities 767 ideal replacement for less efficient aircraft A300-B4 (47) DC-10-10 (59) DC-8 (55) Growth markets Domestic China-9.3% Intra-Asia-7.5% Europe-Asia-5.9% Europe-Africa-5.7% Source: ACMG, Boeing |

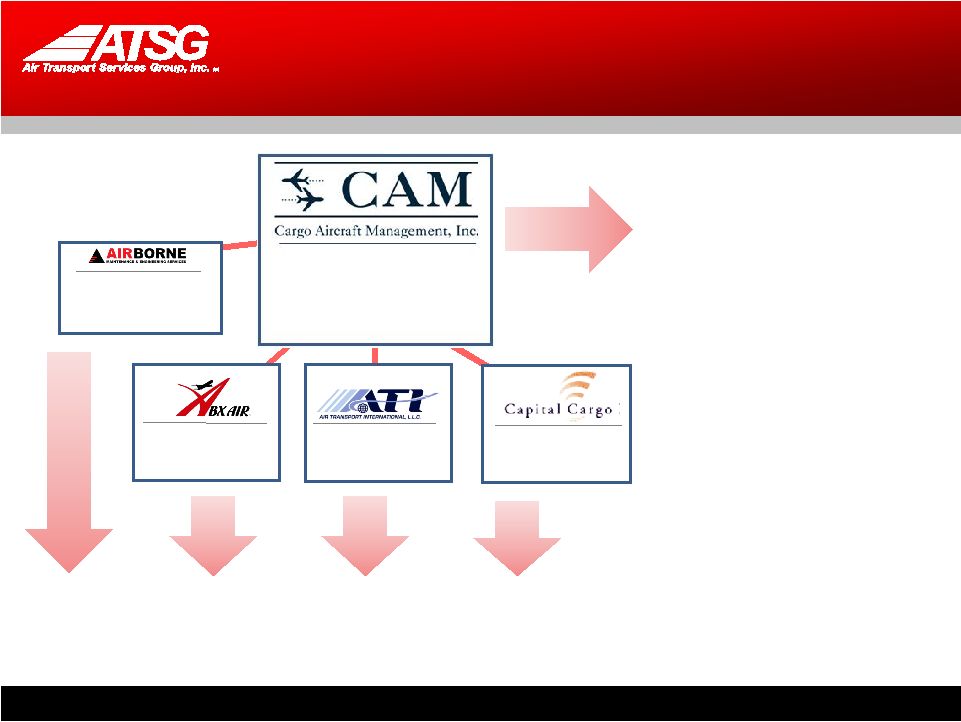

24 24 ATSG Portfolio Marketing Individual companies continue to market and sell their own services CAM will bundle and sell the services of the individual companies into short- and long-term solutions for new and existing customers • ACMI / Wet Leasing • Cargo Handling • Charter Services • ACMI / Wet Leasing • Combi-freighters • Charter Services • ACMI / Wet Leasing • Charter Services • Aviation Solutions • Bundled Programs • Aircraft Leasing • Conversion Services • Heavy Maintenance • Line Maintenance • Component Overhaul & Sales • Engineering Services |

25 25 Flexible Global Solutions Market Differentiation • 767-200 with GE CF6-80A engines • Low fuel cost • Low maintenance cost • Flexible configuration • Power By Hour engine services The Global Leader of Medium Wide Body Operating and Leasing Solutions Efficient Medium Wide-Body Aircraft • ACMI/wet leasing • CMI • Dry leasing • AMC charter • Full service charter • Flight operations • Heavy maintenance • Line maintenance • Maintenance programs • Engineering • Technical support • Manual services • Parts, components sales & service • Aircraft conversion services • Global aircraft deployment • Logistics support • DHL • TNT • UPS • Qantas • Amerijet • Air Mobility Command • CargoJet Bundled Maintenance Solutions Program Management Diverse Customer Experience |

26 26 Wrap-up and Your Questions Joe Hete, President & CEO |

27 27 2010 Achievements to Date Completed new fixed-price, multi-year agreements for aircraft leasing and CMI services with DHL Continued to reduce debt and strengthen balance sheet Leased 767F to Amerijet, illustrating ATSG’s complementary solutions opportunity Restructured and expanded TNT relationship into lower-risk ACMI for two aircraft Took delivery of three more 767Fs from mod Completed restructuring of ABX Air Placed deposits for three 767-300s |

28 28 Value Proposition Strong cash returns from modified freighters 767 leases lock in long-term cash flow ACMI/CMI flexibility provides lease migration path 10 modified 767 freighters to be deployed through 2011 Long-term agreements with well-established customers Lease/CMI provides entry point for expanded opportunities Integrated, value-added services Solid balance sheet and liquidity, growth capital capacity Well positioned for continued growth in global air cargo demand The Global Leader of Medium Wide-Body Operating & Leasing Solutions |

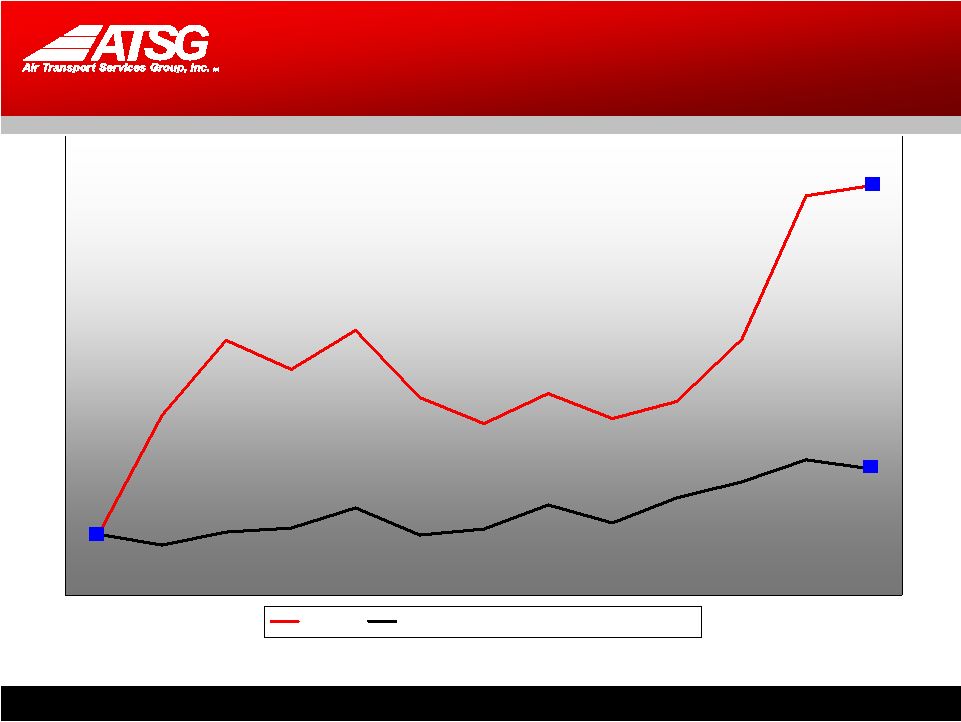

29 29 Investors Recognize ATSG Progress ATSG NASDAQ Transportation (IXTR) May 11, 2009 May 10, 2010 $0.77 $5.36 2155 1789 Values at close |

30 30 Shareholder Questions |