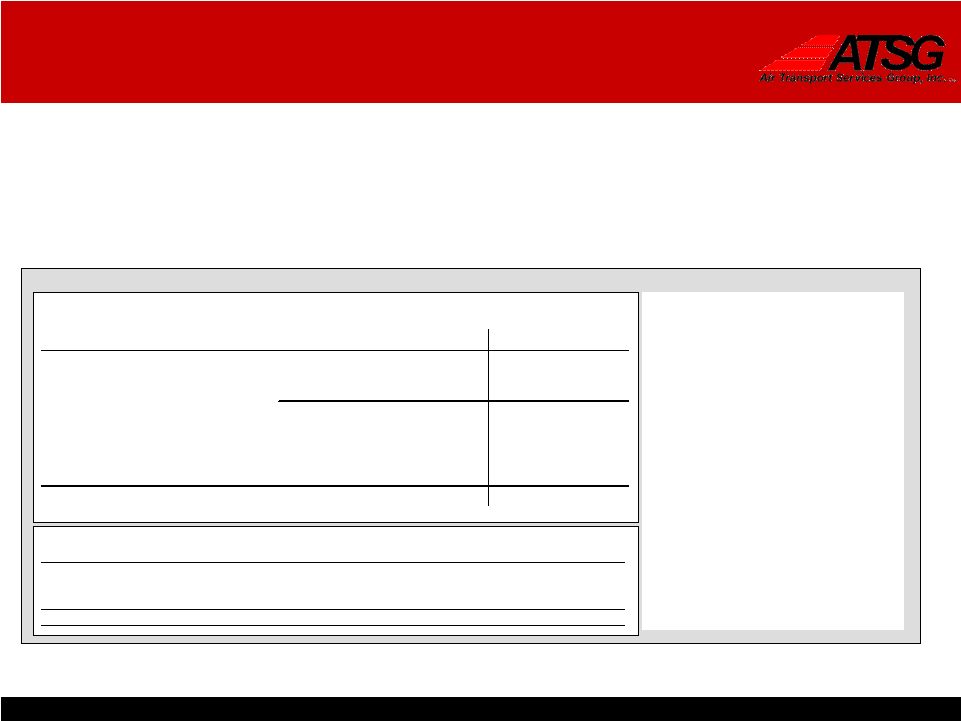

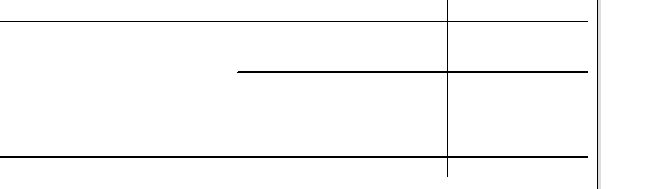

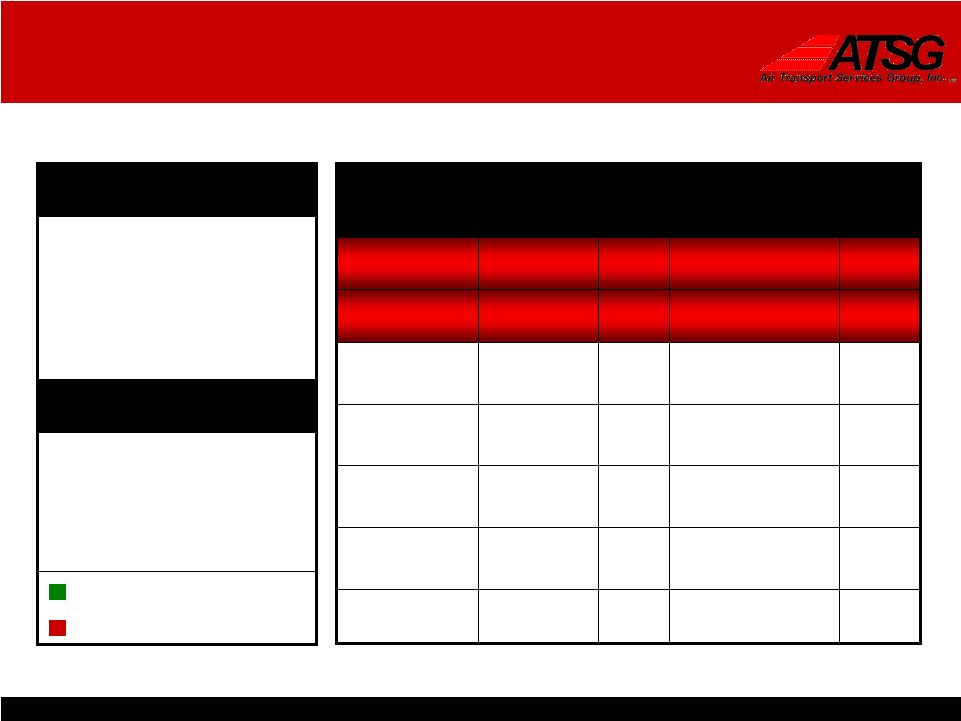

17 Balance Sheet Trend June 30, Dec. 31, June 30, Dec. 31 2010 2009 2009 2008 ASSETS CURRENT ASSETS: Cash and cash equivalents 63,660 83,229 112,064 116,114 Marketable securities - available-for-sale - - - 26 Accounts receivable, net of allowances 35,684 87,708 77,329 87,857 Inventory 5,740 5,226 7,611 11,259 Prepaid supplies and other 8,845 7,093 8,122 11,151 Deferred income taxes 31,597 31,597 20,171 20,172 Aircraft and engines held for sale - 30,634 32,901 2,353 TOTAL CURRENT ASSETS 145,526 245,487 258,198 248,932 Property and equipment, net 650,408 636,089 627,768 671,552 Other assets 29,948 21,307 23,265 25,281 Deferred income taxes - - 14,973 54,807 Intangibles 9,686 10,113 10,557 11,000 Goodwill 89,777 89,777 89,777 89,777 TOTAL ASSETS $925,345 $1,002,773 $1,024,538 $1,101,349 LIABILITIES AND STOCKHOLDERS' EQUITY CURRENT LIABILITIES: Accounts payable 31,912 38,174 30,625 36,618 Accrued salaries, wages and benefits 24,956 44,077 40,259 63,500 Accrued severance and retention 7,171 18,959 45,301 67,846 Accrued expenses 15,146 16,429 15,161 13,772 Current portion of debt obligations 36,788 51,737 62,774 61,858 Unearned revenue 16,775 15,340 9,232 14,813 TOTAL CURRENT LIABILITIES 132,748 184,716 203,352 258,407 Long-term obligations 287,269 325,690 380,225 450,628 Post-retirement liabilities 102,765 152,297 269,886 294,881 Other liabilities 59,311 44,044 17,163 17,041 Deferred income taxes 66,988 50,044 - - STOCKHOLDERS' EQUITY: Preferred stock, 20,000,000 shares authorized, including 75,000 Series A Junior Participating Preferred Stock - - - - Common stock, par value $0.01 per share; 638 634 635 632 Additional paid-in capital 503,441 502,822 490,349 460,155 Accumulated deficit (194,248) (211,085) (226,330) (245,534) Accumulated other comprehensive loss (33,567) (46,389) (110,742) (134,861) TOTAL STOCKHOLDERS' EQUITY 276,264 245,982 153,912 80,392 TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY $925,345 $1,002,773 $1,024,538 $1,101,349 |