UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934 |

Commission file number 0-23881

COWLITZ BANCORPORATION

(Exact name of registrant as specified in its charter)

| | |

| Washington | | 91-1529841 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

927 Commerce Ave., Longview, Washington 98632

(Address of principal executive offices) (Zip Code)

(360) 423-9800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, No par value

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| | | | | | |

| ¨ Large accelerated filer | | ¨ Accelerated filer | | ¨ Non-accelerated filer | | x Smaller reporting company |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

¨ Yes x No

The aggregate market value of Registrant’s Common Stock held by non-affiliates of the Registrant on June 30, 2007, was $67,574,010.

Common Stock, no par value, outstanding as of February 29, 2008: 5,054,507

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement for the 2008 annual meeting of shareholders are incorporated by reference in Part III hereof.

TABLE OF CONTENTS

Note: This document has not been reviewed, or confirmed for accuracy or relevancy by the Federal Deposit Insurance Corporation.

Forward-Looking Statements

This discussion and information in this document, particularly in Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operation” and the accompanying financial statements, contain certain forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements, which are based on certain assumptions and describe future plans, strategies and expectations of the Company, are all statements other than statements of historical fact and are generally identifiable by words such as "expect", "believe", "intend", "anticipate", "estimate" or similar expressions. Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those stated. Examples of such risks and uncertainties that could have a material adverse affect on the operations and future prospects of the Company, and could render actual results different from those expressed in the forward-looking statement, include, without limitation: the factors described in Item 1A of this report, changes in general economic conditions, competition for financial services in the market area of the Company, the level of demand for loans, quality of the loan and investment portfolio, deposit flows, legislative and regulatory initiatives, and monetary and fiscal policies of the U.S. Government affecting interest rates. The reader is advised that this list of risks is not exhaustive and should not be construed as any prediction by the Company as to which risks would cause actual results to differ materially from those indicated by the forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements. In this Annual Report on Form 10-K we make forward-looking statements about the adequacy of our allowance for credit losses, the necessity of provisions for loan losses, the expected positive impact of our system conversion and our belief regarding the economic prospects of our market area and the related impact on loan growth and the quality of our loan portfolio.

PART I

Introduction

Cowlitz Bancorporation (the “Company”) was organized in 1991 under Washington law to become the holding company for Cowlitz Bank (the “Bank”), a Washington state chartered bank that commenced operations in 1978. The principal executive offices of the Company are located in Longview, Washington. The Bank operates four branches in Cowlitz County in southwest Washington. Outside of Cowlitz County, the Bank does business under the name Bay Bank with branches in Bellevue, Seattle, and Vancouver, Washington, and Portland, Oregon and a limited service branch in a retirement center in Wilsonville, Oregon. The Bank also provides mortgage banking services through its Bay Mortgage division with offices in Longview and Vancouver, Washington.

The Company offers or makes available a broad range of financial services to its customers, primarily small and medium-sized businesses, professionals, and retail customers. The Company’s goals are to offer exceptional customer service and to invest in the markets it serves through its business practices and community service. The Bank's commercial and personal banking services include commercial and real estate lending, consumer lending, international banking services, internet banking, mortgage banking and trust services. The Company’s customers have access to the Bank’s products and services through a variety of convenient channels such as 24 hour—7 days a week automated phone and internet access and ATMs, as well as through branch locations. Beginning in the first quarter of 2008, the Bank began offering its business customers remote deposit capture. This service allows customers to make deposits electronically without leaving their office.

On October 31, 2005, the Company acquired all of the outstanding shares of common stock of AEA Bancshares, Inc. (AEA), the parent company of Asia-Europe-Americas Bank, in an acquisition accounted for as a purchase. The acquisition is consistent with the Company’s business banking expansion strategy in King County, Washington. The former Asia-Europe-Americas Bank office in Seattle operates as a Bay Bank branch. Also based in the Seattle office, in the second quarter of 2006 the Company established its international banking department.

Prior to 2004, the Company also operated Bay Mortgage and Bay Escrow offices in Bellevue and Seattle, Washington. As part of a strategy to consolidate resources into commercial banking and reduce reliance on mortgage lending activities, those offices were closed during the fourth quarter of 2003 and first quarter of 2004.

For the year 2007, the Company recorded net income of $86,000 or $0.02 per diluted share. At December 31, 2007, the Company had total assets of $514.2 million, total liabilities of $458.7 million, and total shareholders’ equity of $55.5 million. Book value per share was $10.99 at year-end 2007. At December 31, 2007, net loans were $391.5 million, approximately 76% of total assets, and total deposits were $441.2 million.

Products and Services

The Company offers a broad portfolio of products and services tailored to meet the financial needs of individuals and small business customers in its market areas. The Company believes this portfolio is generally competitive with the products and services of its competitors, including community banks, major regional and national banks, thrifts and credit unions.

Deposit Products. The Company offers non-interest-bearing and interest-bearing checking accounts, savings accounts, money market accounts, individual retirement accounts, and certificates of deposit. Interest-bearing accounts generally earn interest at rates established by management based on competitive market factors and management's desire to increase certain types or alter maturities of deposit liabilities. During times of asset growth, or as liquidity needs arise, the Company utilizes brokered certificates of deposit as a source of funding. The Company strives to establish customer relationships to attract core deposits in non-interest-bearing transactional accounts to reduce its cost of funds.

1

Loan Products. The Company offers a broad range of loan products to retail and business customers. The Company maintains loan underwriting standards with written loan policies and individual lending limits. All new loans and renewals are reported monthly to the Company's Board of Directors. The Board of Directors’ Loan Committee approves particularly large loan commitments. Underwriting standards are designed to achieve a high-quality loan portfolio, compliance with lending regulations and an appropriate mix of loan maturities and industry concentrations. Management seeks to minimize credit losses by closely monitoring the financial condition of its borrowers and the value of collateral.

Commercial Loans. Commercial lending is a focus of the Company's lending activities, and a significant portion of its loan portfolio consists of commercial loans. The Company offers specialized loans for its business and commercial customers. These include operating lines of credit that support accounts receivables and inventory, as well as secured term loans to finance machinery and equipment. The Company has historically reported loans in accordance with Bank regulatory guidelines. As a result, a substantial portion of the Company's commercial loans are designated as real estate loans, as the loans are secured by mortgages or trust deeds on real property, although some of these loans were not made to finance real estate nor does the repayment depend on the sale of or income from the real estate. Lending decisions are based on careful evaluation of the financial strength, management and credit history of the borrower, and the quality of the collateral securing the loan. A second category of commercial lending involves construction or term loans on commercial income producing properties and acquisition and development loans for single family residential development. These loans are secured by real property and are generally limited to 75% of the value of collateral. In most cases, the Company requires personal guarantees and secondary sources of repayment. In competing with major regional and national banks, the Company is limited by lower single borrower lending limits imposed by law.

Real Estate Loans. This category supports single family residential lending. The loans are available for construction, purchase, or refinancing of residential properties. Borrowers can choose from a variety of fixed and adjustable rate options and terms. The Company provides customers access to long-term residential real estate loans through Bay Mortgage and its branch network, focusing on all facets of residential lending from single family homes to small multiplexes, including FHA and VA loans, construction and bridge loans. Real estate loans reflected in the loan portfolio also include loans made to commercial customers that are secured by real property.

Consumer Loans. The Company provides loans to individual borrowers for a variety of purposes, including secured and unsecured personal loans, home equity, personal lines of credit and motor vehicle loans. Consumer loans can carry significantly greater risks than other loan products, even if secured, if the collateral consists of rapidly depreciating assets such as automobiles or recreational equipment. Repossessed collateral securing a defaulted consumer loan may not provide an adequate source of repayment of the loan. Consumer loan collections are dependent on borrowers' continuing financial stability, and are sensitive to job loss, illness and other personal factors. The Company attempts to manage the risks inherent in consumer lending by following conservative credit guidelines and underwriting practices. The Company also offers Visa credit cards to its customers.

Trust Services. Cowlitz Bank is the only bank headquartered in Cowlitz County to offer complete in-house trust services. The trust department, located in the offices of the main branch in Longview, Washington provide trust services to individuals, partnerships, corporations and institutions and acts as fiduciary of living trusts, estates, conservatorships and other plans. The Company believes these services add to the value of the Bank as a community bank by providing local access to services that are offered by out of the area financial institutions.

International Banking.Through its Seattle branch, the Company offers a variety of international banking services. To assist customers with import, export and other trade related needs, the Company provides commercial and standby letters of credit, foreign exchange and foreign collection services, international funds transfer capabilities accounts receivable financing and foreign denominated accounts (euro, pounds, yen).

2

Internet Banking. Internet banking and cash management systems are available to both business and individual customers, providing secure access to information and services from the Company’s website. Business clients can avail themselves of comprehensive cash management program which allows them to easily and securely move money between accounts, wire funds, receive funds, pay bills, and generally manage their financial resources. Retail customers have the ability to access account information, pay bills, and manage their accounts by way of the internet. The Company’s website address iswww.cowlitzbancorporation.com and the Bank’s websites arewww.cowlitzbank.com, www.bay-bank.com andwww.bay-loans.com. The content of these websites is not incorporated into this document or into the Company’s other filings with the SEC.

Other Banking Products and Services. In support of its focus on personalized service, the Company offers additional products and services for the convenience of its customers. These services include a debit card program, automated teller machines at six branches and one off-site location, merchant services and an automated telephone banking service with 24-hour access to accounts that also allows customers to speak directly with a customer service representative during normal banking hours. The Company provides drive-through facilities at three of its branches.

Market Areas and Competition

The Company's primary market areas in which it accepts deposits and makes loans are Cowlitz County, in southwest Washington; King County, Washington; the Portland metropolitan area in Oregon; and the surrounding counties in Washington and northwest Oregon. As a community bank, the Bank has certain competitive advantages due to its local focus, but is also more closely tied to the local community than many of its competitors, which serve a number of geographic markets. Bay Mortgage operations are concentrated in southwestern Washington.

According to the US Department of Labor—Bureau of Labor Statistics website, both Washington (28th at 4.8%) and Oregon (41st at 5.6%) were among the states with relatively high unemployment rates during December 2007. Washington’s December 2007 unemployment rate declined 0.2% from a year ago. The Seattle metropolitan area’s unemployment rate (not seasonally adjusted) was 4.0% and ranked 31 out of 367 metropolitan areas. Washington ranked in the top ten states for year-over-year job growth in 2007 and 2006. Oregon’s December 2007 unemployment rate increased 0.2% from a year ago. The Portland –Vancouver metropolitan area’s unemployment rate was 4.9% and ranked 164. The increase in the unemployment rate reflects the decline in the residential real estate construction industry. The Longview area in Cowlitz County, Washington, continues to experience cyclically higher levels of unemployment than the Seattle metropolitan area. In December 2007, unemployment in Cowlitz County was 6.8%, an increase of 0.6% from a year ago. The increase primarily reflected recent workforce reductions in the forest products industry.

In the first quarter of 2008, the Federal Reserve made a series of interest rate cuts to support a softening national economy. Contributing to concerns about a U.S. recession in 2008 are the significant declines in most residential real estate markets and the increase in mortgage loan delinquencies and foreclosures, increasing unemployment rates, higher energy costs and lower consumer confidence. According to Standard & Poor’s S&P/Case-Shiller quarterly index, for the fourth quarter of 2007, Portland, Oregon and Seattle, Washington, were two of the three major metropolitan areas out of 20 to show year-over-year increases in existing single-family home prices. However, the Company expects the economy in the Pacific Northwest to generally follow the direction of the national economy in 2008.

Commercial banking in the state of Washington and northwest Oregon is highly competitive with respect to providing banking services including making loans and attracting deposits. The Company competes with other banks, as well as with savings and loan associations, savings banks, credit unions, mortgage companies, investment banks, insurance companies, securities brokerages and other financial institutions. Banking in Washington and Oregon is dominated by several significant banking institutions which together account for a majority of the total commercial and savings bank loans and deposits in Washington and Oregon. These

3

competitors have significantly greater financial resources and offer a greater number of branch locations (with statewide branch networks), higher lending limits, and a variety of services not offered by the Bank. The Company has attempted to offset some of the advantages of the large competitors by arranging participations with other banks for loans above its legal lending limits, as well as leveraging technology and third party arrangements to deliver financial products and better compete in targeted customer segments. The Company has positioned itself as a local alternative to larger competitors that may be perceived by customers or potential customers to be impersonal, out-of-touch with the community, or simply not interested in providing banking services to some of the target customers, by offering excellent customer service and investing in the markets it services through its business practices and community service.

In addition to larger institutions, other community banks and credit unions have been formed, expanded, or moved into the Company’s market areas and have developed a similar focus to the Company. This growing number of similar financial institutions and an increased focus by larger institutions on the Company’s market segments has led to intensified competition in all aspects of the Company’s business. Increased competitive pressure and changing customer deposit behaviors could adversely affect the Bank’s market share of deposits.

The adoption of the Gramm-Leach-Bliley Act of 1999 (the “GLB Act”) led to further competition in the financial services industry. The GLB Act eliminated many of the barriers to affiliation among providers of various types of financial services and permitted business combinations among financial service providers such as banks, insurance companies, securities or brokerage firms and other financial service providers. Additionally, the rapid adoption of financial services through the internet has reduced or even eliminated many barriers to entry by financial services providers physically located outside our market areas. For example, remote deposit services allow depository companies physically located in other geographical markets to service local businesses with minimal cost of entry. Although the Company has been able to compete effectively in the financial services business in its markets to date, there can be no assurance that it will be able to continue to do so in the future.

The financial services industry has experienced widespread consolidation over the last decade. The Company anticipates that consolidation among financial institutions in its market areas will continue. As noted the Company may seek acquisition opportunities in markets of strategic importance to it from time to time. However, other financial institutions aggressively compete against the Company in the acquisition market. Some of these institutions may have greater access to capital markets, larger cash reserves and stock for use in acquisitions that is more liquid and more highly valued by the market.

Employees

As of December 31, 2007, the Company employed a total of 142 full-time equivalent employees. None of the employees are subject to a collective bargaining agreement and the Company considers its relationships with its employees to be favorable.

Regulation and Supervision

The Company and the Bank are subject to extensive federal and state regulations that significantly affect the respective activities of the Company and the Bank and the competitive environment in which they operate. These laws and regulations are intended primarily to protect depositors and the deposit insurance fund, rather than shareholders.

The description of the laws and regulations applicable to the Company and the Bank is not a complete description of the laws and regulations mentioned herein or of all such laws and regulations. Any change in applicable laws or regulations may have a material effect on the business and prospects of the Company and the Bank.

The Bank is a state chartered commercial bank, which is not a member of the Federal Reserve System, and is subject to primary regulation and supervision by the Department of Financial Institutions of the State of Washington (“DFI”) and by the Federal Deposit Insurance Corporation (the “FDIC”), which also insures bank deposits. The Company is subject to regulation and supervision by the Board of Governors of the Federal Reserve System (the “Federal Reserve”).

4

Bank Holding Company Regulation. The Company is a bank holding company within the meaning of the Bank Holding Company Act of 1956, as amended (“BHCA”) and, as such, is subject to the regulations of the Federal Reserve. Bank holding companies are required to file periodic reports with, and are subject to periodic examination by, the Federal Reserve. The Federal Reserve has issued regulations under the BHCA requiring bank holding companies to serve as a source of financial and managerial strength to their subsidiary banks. It is the policy of the Federal Reserve that, pursuant to this requirement, a bank holding company should stand ready to use its resources to provide adequate capital to fund its subsidiary banks during periods of financial stress or adversity. Additionally, under the Federal Deposit Insurance Corporation Improvement Act of 1991 (“FDICIA”), a bank holding company is required to guarantee the compliance of any insured depository institution subsidiary that may become “undercapitalized” (as defined in the statute) with the terms of any capital restoration plan filed by such subsidiary with its appropriate federal banking agency up to the lesser of (i) an amount equal to 5% of the institution’s total assets at the time the institution became undercapitalized, or (ii) the amount that is necessary (or would have been necessary) to bring the institution into compliance with all applicable capital standards as of the time the institution fails to comply with such capital restoration plan. Under the BHCA, the Federal Reserve has the authority to require a bank holding company to terminate any activity or relinquish control of a non-bank subsidiary (other than a non-bank subsidiary of a bank) upon the Federal Reserve's determination that such activity or control constitutes a serious risk to the financial soundness and stability of any bank subsidiary of the bank holding company.

Capital Adequacy Guidelines for Bank Holding Companies. The Federal Reserve has adopted capital adequacy guidelines for bank holding companies. These guidelines are similar to, although not identical with, the guidelines applicable to banks. See “FDICIA and Capital Requirements.”

Bank Regulation. The Bank is organized under the laws of the State of Washington and is subject to the supervision of the DFI, whose examiners conduct periodic examinations of state banks. Cowlitz Bank is not a member of the Federal Reserve System, so its principal federal regulator is the FDIC, which also conducts periodic examinations of the Bank. The Bank's deposits are insured, to the maximum extent permitted by law, by the Deposit Insurance Fund (“DIF”) administered by the FDIC and are subject to the FDIC’s rules and regulations respecting the insurance of deposits. See “Deposit Insurance.”

Both federal and state laws extensively regulate various aspects of the banking business such as reserve requirements, truth-in-lending and truth-in-savings disclosures, equal credit opportunity, fair credit reporting, trading in securities and other aspects of banking operations. Current federal law also requires banks, among other things, to make deposited funds available within specified time periods.

Insured state-chartered banks are generally prohibited under FDICIA from engaging as principal in activities that are not permitted for national banks, unless (i) the FDIC determines that the activity would pose no significant risk to the appropriate deposit insurance fund, and (ii) the bank is, and continues to be, in compliance with all applicable capital standards. The Company believes that these restrictions do not have a material adverse effect on its current operations.

FDICIA. FDICIA requires, among other things, federal bank regulatory authorities to take “prompt corrective action” with respect to banks that do not meet minimum capital requirements. For these purposes, FDICIA establishes five capital tiers: well capitalized, adequately capitalized, undercapitalized, significantly undercapitalized, and critically undercapitalized.

The FDIC has adopted regulations to implement the prompt corrective action provisions of FDICIA. Among other things, the regulations define the relevant capital measures for the five capital categories. An institution is deemed to be “well capitalized” if it has a total risk-based capital ratio of 10% or greater, a Tier 1 risk-based capital ratio of 6% or greater, and a leverage ratio of 5% or greater, and is not subject to a regulatory order, agreement or directive to meet and maintain a specific capital level for any capital measure. The Federal Reserve Board classifies a bank holding company as “well capitalized” if it has a total risk-based capital ratio of 10% or greater and a Tier 1 risk-based capital ratio of 6% or greater. The Company and the Bank are both “well-capitalized.”

5

FDICIA further directs that each federal banking agency prescribe standards for depository institutions and depository institution holding companies relating to internal controls, information systems, internal audit systems, loan documentation, credit underwriting, interest rate exposure, asset growth, management compensation, a maximum ratio of classified assets to capital, minimum earnings sufficient to absorb losses, a minimum ratio of market value to book value of publicly traded shares and such other standards as the agency deems appropriate.

Capital Requirements. The FDIC has adopted risk-based capital ratio guidelines to which the Bank is subject. The guidelines establish a systematic analytical framework that makes regulatory capital requirements more sensitive to differences in risk profiles among banking organizations. Risk-based capital ratios are determined by allocating assets and specified off-balance sheet commitments to four risk weighted categories, with higher levels of capital being required for the categories perceived as representing greater risk.

These guidelines divide a bank’s capital into two tiers. Tier 1 includes common equity, certain non-cumulative perpetual preferred stock (excluding auction rate issues) and minority interest in equity accounts of consolidated subsidiaries, less goodwill and certain other intangible assets (except mortgage servicing rights and purchased credit card relationships, subject to certain limitations). Supplementary (Tier 2) capital includes, among other items, preferred stock (cumulative perpetual and long-term, limited-life), mandatory convertible securities, certain hybrid capital instruments, term-subordinated debt and the allowance for loan and lease losses, subject to certain limitations, less required deductions. Banks are required to maintain a total risk-based capital ratio of 8%, of which 4% must be Tier 1 capital. The FDIC may, however, set higher capital requirements when a bank's particular circumstances warrant. Banks experiencing or anticipating significant growth are expected to maintain capital ratios, including tangible capital positions, well above the minimum levels.

In addition, the FDIC has established guidelines prescribing a minimum Tier 1 leverage ratio (Tier 1 capital to adjusted total assets) of 3% for banks that meet certain specified criteria, including that the banks have the highest regulatory rating and are not experiencing or anticipating significant growth. All other banks are required to maintain a Tier 1 leverage ratio of not less than 4%.

At December 31, 2007, the regulatory capital ratios for the Company and the Bank were:

| | | | | | |

| | | December 31, 2007 | |

| | | Company | | | Bank | |

Total risk-based capital to risk-weighted assets | | 14.82 | % | | 14.06 | % |

Tier 1 Capital to risk-weighted assets | | 13.56 | % | | 12.81 | % |

Tier 1 leverage ratio | | 12.51 | % | | 11.78 | % |

Dividends. The principal source of the Company’s cash revenues is dividends from the Bank. Under Washington law, the Bank may not pay dividends in an amount greater than its retained earnings as determined by generally accepted accounting principles. In addition, DFI has the authority to require a state-chartered bank to suspend the payment of dividends. The FDIC has the authority to prohibit a bank from paying dividends if, in its opinion, the payment of dividends would constitute an unsafe or unsound practice in light of the financial condition of the bank or if it would cause a bank to become undercapitalized.

Lending Limits. Under Washington law, the total loans and extensions of credit by a Washington-chartered bank to a borrower outstanding at one time may not exceed 20% of the bank’s Tier 1 capital. However, this limitation does not apply to loans or extensions of credit which are fully secured by readily marketable collateral having market value of at least 115% of the amount of the loan or the extension of credit at all times.

Branches and Affiliates. Establishment of bank branches is subject to approval of the DFI and FDIC and geographic limits established by state laws. Washington's branch banking law permits a bank having its principal place of business in the State of Washington to establish branch offices in any county in Washington without geographic restrictions. A bank may also merge with any national or state chartered bank located anywhere in the State of Washington without geographic restrictions.

6

Under Oregon law, an out-of-state bank or bank holding company may merge with or acquire an Oregon state chartered bank or bank holding company if the Oregon bank, or in the case of a bank holding company, the subsidiary bank, has been in existence for a minimum of three years, and the law of the state in which the acquiring bank is located permits such merger. Branches may not be acquired or opened separately, but once an out-of-state bank has acquired branches in Oregon, either through a merger with or acquisition of substantially all of the assets of an Oregon bank, the bank may open additional branches.

The Bank is subject to provisions of the Federal Reserve Act that restrict financial transactions between banks and affiliated companies. The statute limits credit transactions between a bank and its executive officers and its affiliates, prescribes terms and conditions for bank affiliate transactions deemed to be consistent with safe and sound banking practices, and restricts the types of collateral security permitted in connection with a bank's extension of credit to an affiliate.

Deposit Insurance. The Bank’s deposits are insured by the Deposit Insurance Fund (“DIF”). The Federal Deposit Insurance Reform Act of 2005 (“Reform Act”), enacted in February 2006, increased the deposit insurance limit for certain retirement plan deposit accounts from $100,000 to $250,000. The basic insurance limit for other deposits, including individuals, joint account holders, businesses, government entities, and trusts, remains at $100,000. The Bank’s deposits were previously insured by the Bank Insurance Fund, which was merged with the Savings Association Insurance Fund to form the DIF in March 2006.

As an institution whose deposits are insured by DIF, the Bank is required to pay deposit insurance premiums to DIF. FDIC regulations set deposit insurance premiums based upon the risks a particular bank or savings association poses to the deposit insurance fund. This system bases an institution's risk category partly upon whether the institution is well capitalized, adequately capitalized or less than adequately capitalized. Each insured depository institution is also assigned to one of three “supervisory” categories based on reviews by regulators, statistical analysis of financial statements and other relevant information. An institution's assessment rate depends upon the capital category and supervisory category to which it is assigned.

The Reform Act created a new system and assessment rate schedule to calculate an institution’s assessment. For 2007, the assessment rates ranged from $0.05 to $0.43 per $100 of deposits annually. Assessment rates for well managed, well capitalized institutions ranged from $0.05 to $0.07 per $100 of deposits annually. The Bank’s assessment rate for 2007 fell within this range and is expected to fall within this range for 2008. In 2007, the FDIC issued one-time assessment credits that were used to offset FDIC assessments. The Bank’s credit was fully utilized and covered the majority of the assessment in 2007. The Bank does not have any remaining credit to offset assessments in 2008. The FDIC may increase or decrease the assessment rate schedule on a semi-annual basis in order to manage the DIF to prescribed statutory target levels. Further increases in the assessment rate could have a material adverse affect on the Company’s earnings, depending on the amount of the increase.

Under legislation enacted in 1996 to recapitalize the Savings Association Insurance Fund, the FDIC is authorized to collect assessments against insured deposits to be paid to the Financing Corporation (“FICO”) to service FICO debt incurred in the 1980's. The current FICO assessment rate for DIF insured deposits are $0.0114 per $100 of deposits per year. An increase in deposit or FICO assessments could have an adverse effect on the Bank's earnings, depending upon the amount of the increase.

Gramm-Leach-Bliley Act. On November 12, 1999, the Gramm-Leach-Bliley Act (the “GLB Act”) was signed into law, which significantly reformed various aspects of the financial services business. Among other things, the GLB Act:

| | • | | established a new framework under which bank holding companies and banks can own securities firms, insurance companies and other financial companies; |

| | • | | provided consumers with new protections regarding the transfer and use of their non-public personal information by financial institutions; and |

7

| | • | | changed the Federal Home Loan Bank (“FHLB”) system in numerous ways revising the manner of calculating the Resolution Funding Corporation obligations payable by the FHLB and broadening the purposes for which FHLB advances may be used. |

The GLB Act also includes provisions to protect consumer privacy by prohibiting financial services providers, whether or not affiliated with a bank, from disclosing non-public personal, financial information to unaffiliated parties without the consent of the customer, and by requiring annual disclosure of the provider’s privacy policy.

Community Reinvestment Act. The Community Reinvestment Act (“CRA”) requires financial institutions regulated by the federal financial supervisory agencies to ascertain and help meet the credit needs of their delineated communities, including low-income and moderate-income neighborhoods within those communities, while maintaining safe and sound banking practices. The regulatory agency assigns one of four possible ratings to an institution's CRA performance and is required to make public an institution’s rating and written evaluation. The four possible ratings are “outstanding,” “satisfactory,” “needs to improve” and "substantial non-compliance."

Many factors play a role in assessing a financial institution's CRA performance. The institution’s regulator must consider its financial capacity and size, legal impediments, local economic conditions and demographics and the competitive environment in which it operates. The evaluation does not rely on absolute standards and financial institutions are not required to perform specific activities or to provide specific amounts or types of credit.

The Company’s most recent rating under CRA is “satisfactory.” This rating reflects the Company's commitment to meeting the credit needs of the communities it serves. Although the Company strives to maintain a satisfactory or higher rating, no assurance can be given that the Company will maintain this rating in the future. If the Company’s CRA rating were to fall below “satisfactory” it may inhibit its ability to obtain regulatory approval for acquisitions or expansion.

Sarbanes-Oxley Act of 2002.The Sarbanes-Oxley Act of 2002 addressed public company corporate governance, auditing, accounting, executive compensation, and enhanced and timely disclosure of corporate information. The Sarbanes-Oxley Act represents significant federal involvement in matters traditionally left to state regulatory systems, such as the regulation of the accounting profession, and to state corporate law, such as the relationship between a board of directors and management and between a board of directors and its committees.

The Sarbanes-Oxley Act and related SEC regulations provides for, among other matters:

| | • | | a prohibition on personal loans by Cowlitz to its directors and executive officers except loans in the ordinary course of business made by the Bank; |

| | • | | independence requirements for Board audit committee members and the Company’s auditors; |

| | • | | certification of Exchange Act reports by the chief executive officer and the chief financial officer; |

| | • | | disclosure of off-balance sheet transactions; |

| | • | | expedited reporting of stock transactions by insiders; |

| | • | | internal and disclosure controls and procedures requirements; and |

| | • | | increased criminal penalties for violations of securities laws. |

The Sarbanes-Oxley Act also requires:

| | • | | management to establish, maintain and evaluate disclosure controls and procedures; |

| | • | | report on its annual assessment of the effectiveness of internal controls over financial reporting; and |

| | • | | a company’s auditor to attest to management’s assessment of internal controls. |

8

The SEC has adopted regulations to implement various provisions of the Sarbanes-Oxley Act, including disclosures in periodic filings pursuant to the Exchange Act. Also in response to the Sarbanes-Oxley Act, NASDAQ adopted new standards for listed companies. In 2007, the SEC extended the requirement for a company’s auditor to attest to management’s assessment of internal controls for a small company, as defined by the SEC. For 2007, the Company met the definition of a small company and, therefore, did not have its external auditor attest to management’s assessment of internal controls. In 2007, the Sarbanes-Oxley Act substantially increased the Company’s reporting and compliance expenses.

Anti-Terrorism Legislation. The Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act (“USA Patriot Act”), enacted in 2001:

| | • | | prohibits banks from providing correspondent accounts directly to foreign shell banks; |

| | • | | imposes due diligence requirements on banks opening or holding accounts for foreign financial institutions or wealthy foreign individuals; |

| | • | | requires financial institutions to establish an anti-money-laundering (“AML”) compliance program; and |

| | • | | generally eliminates civil liability for persons who file suspicious activity reports. |

The USA Patriot Act also increases governmental powers to investigate terrorism, including expanded government access to account records. The Department of the Treasury is empowered to administer and make rules to implement the Act, which to some degree, affects the Bank’s record-keeping and reporting expenses. Should the Bank’s AML compliance program be deemed insufficient by federal regulators, the Company would not be able to grow through acquiring other institutions or opening de novo branches.

Additional Matters. The Company and the Bank are subject to additional regulation of their activities, including a variety of consumer protection regulations affecting lending, deposit and collection activities and regulations affecting secondary mortgage market activities. The earnings of financial institutions, including the Company and the Bank, are also affected by general economic conditions and prevailing interest rates, both domestic and foreign and by the monetary and fiscal policies of the U.S. Government and its various agencies, particularly the Federal Reserve.

Additional legislation and administrative actions affecting the banking industry may be considered by the United States Congress, the Washington Legislature and various regulatory agencies, including those referred to above. It cannot be predicted with certainty whether such legislation or administrative action will be enacted or the extent to which the banking industry in general or the Company and the Bank in particular would be affected.

The Company is extremely sensitive to the economy of the Pacific Northwest.

The Company operates primarily in Cowlitz County, Washington, the Seattle/Bellevue metropolitan area, and the Vancouver, Washington and Portland, Oregon metropolitan area. Local economic conditions in these areas have a significant impact on:

| | • | | the ability of the Company’s customers to repay loans; |

| | • | | the value of collateral securing loans; |

| | • | | the demand for the Company’s products and services; and |

| | • | | the stability of deposits that create liquidity to support lending activities. |

A sustained economic downturn could affect these local economies, resulting in an adverse effect on the Company’s financial condition or results of operations.

9

The Company has a concentration of real estate collateral securing loans.

Many of the Company’s loans are secured by real estate located in Washington and Oregon. A decline in the real estate market could lead to a decrease in the value of collateral securing loans to the Company’s customers. The Company’s ability to recover on defaulted loans by foreclosing and selling the real estate collateral would be diminished, and the Company would be more likely to incur losses on defaulted loans.

Interest rates are subject to constant, often unpredictable changes and could have an adverse effect on our earnings.

Interest and fees on loans and securities, net of interest paid on deposits and borrowings, are a large part of the Company’s net income. Interest rates are key drivers of net interest margin and are subject to many factors beyond the control of management. As interest rates change, net interest income is affected. Rapid increases in interest rates in the future could result in interest expense increasing faster than interest income because of mismatches in financial instrument maturities and rapid decreases in interest rates could result in interest income decreasing faster than interest expense, for example, when management is unable to match decreases in market interest rates, lowering earning assets yield, with reduced rates paid on deposits or borrowings. Further, substantially higher interest rates generally reduce loan demand and may result in slower loan growth, particularly in construction lending, an important factor in the Company’s revenue growth over the past two years. Decreases or increases in interest rates could have a negative effect on the spreads between the interest rates earned on assets and the rates of interest paid on liabilities, and therefore decrease net interest income. For more information on this topic see “Quantitative and Qualitative Disclosures about Market Risk.”

Our allowance for credit losses may not be adequate.

The risk of nonpayment of loans is inherent in all lending activities, and nonpayment, if it occurs, may have an adverse effect on the Company’s financial condition or results of operation. The Company maintains a reserve for credit losses to absorb estimated probable loan losses inherent in the loan and commitment portfolios as of the balance sheet date. In determining the level of the reserve, management makes various assumptions and judgments about the loan portfolio. If the Company’s assumptions are incorrect, the reserve for credit losses may not be sufficient to cover losses, which could adversely affect the Company’s financial condition or results of operations. The Company establishes its level of reserve for credit losses as a result of management’s continued evaluation of specific credit risks, loan loss experience, quality of the current loan portfolio, loan concentrations, economic conditions, regulations, political climate, new information about borrowers, additional problem loans and other factors.

We may be subject to environmental liability risk associated with lending activities.

A significant portion of the Bank’s loan portfolio is secured by real property. In the ordinary course of business, the Bank may foreclose on and take title to properties securing loans. There is a risk that hazardous or toxic substances will be found on these properties, in which case the Bank may be liable for remediation costs and related personal injury and property damage. Compliance with environmental laws may require the Bank to incur substantial expenses and may materially reduce the affected property’s value or limit the Bank’s ability to use or sell the affected property. Environmental indemnifications obtained from borrowers and their principals or affiliates may not adequately compensate the Bank for losses related to environmental conditions. The remediation costs and financial liabilities associated with environmental conditions could have a material adverse effect on our financial condition and results of operations.

We rely on our information technology and communications systems to conduct our business.

We depend on uninterrupted and successful functioning of our information technology and communications systems, many of which are provided by third parties. We rely on outsourced systems to provide customer service and complete banking transactions. Disruptions in these systems could affect our ability to deliver products and services to our customers. If a third party service provider experiences operational or financial difficulties that interfere with their ability to serve us, our operations could be harmed.

10

The financial services industry is extremely competitive.

The Company competes with well-established, large banks based outside of the region, community banks, credit unions, thrift institutions, investment banking firms, insurance companies, payday loan offices and mortgage lenders for depositors and borrowers. Management believes the most significant competitive factor is customer service, in addition to competitively priced loans and deposits, for structure, branch locations and the range of banking products and services offered.

Offices of the major financial institutions have competitive advantages over the Company in that they have high public visibility, may offer a wider variety of products and are able to maintain advertising and marketing activities on a much larger scale than the Company can economically maintain. Since single borrower lending limits imposed by law are dependent on the capital of the institution, the branches of larger institutions with substantial capital bases also have an advantage with respect to loan applications that are in excess of the Company’s legal lending limits.

In competing for deposits, the Company is subject to certain limitations not applicable to non-bank financial institution competitors. Previous laws limiting the deposit instruments and lending activities of savings and loan associations have been substantially eliminated, thus increasing the competition from these institutions. In Cowlitz County, the main source of competition for deposits is the relatively large number of credit unions.

Federal and State regulations applicable only to banks and bank holding companies also place banks at a competitive disadvantage compared to less regulated competitors such as finance companies, credit unions, mortgage banking companies and leasing companies. Although the Company has been able to compete effectively in its market area in the past, there can be no assurance that it will be able to continue to do so. With significant competition in the Company’s market areas, there can be no assurance that the Company can continue to attract significant loan and deposit customers. The inability to attract these customers could have an adverse effect on the Company’s financial position and results of operations.

The financial services industry is heavily regulated and additional laws and regulations are often considered at the state and federal level.

Federal and state regulations are designed to protect depositors, federal deposit insurance funds, consumers and the banking system, not our shareholders. Banking regulations can significantly restrict our business. Additional laws and regulations affecting banks and bank holdings companies are often proposed at the state and federal levels, which could affect our ability to compete with non-bank companies. The operations of the Company and the Bank may be adversely affected by legislative and regulatory changes as well as by changes in the policies of various regulatory authorities. The Company cannot accurately predict the nature or the extent of the effects that such changes may have in the future on its business and earnings. Failure to comply with the laws or regulations could result in fines, penalties, sanctions and damage to the Company’s reputation which could have an adverse effect on the Company’s business and financial results.

If we acquire companies in the future, our earnings could be reduced if we are unable to successfully integrate operations.

We explore opportunities to acquire other banks. If we are able to find a suitable acquisition opportunity and negotiate and close a transaction, but we experience difficulty in integrating an acquired company, consequently, we may not realize expected revenue enhancements, cost savings, increases in geographic presence or other projected benefits. Integration could also disturb customer and employee relationships at the acquired company, causing deposit run-off and loss of key employees. Resources spent on integration may also detract from our ability to grow existing business.

11

The Company may not be able to attract or retain key banking employees.

The Company strives to attract and retain key banking professionals, management and staff. Competition to attract the best professionals in the industry can be intense which will limit the Company’s ability to hire new professionals. Banking related revenues and net income could be adversely affected in the event of the unexpected loss of key personnel.

| Item 1B. | Unresolved Staff Comments |

None.

The Company owns its main office space in Longview, Washington, occupying approximately 27,500 square feet. The Company owns branches in Kelso and Kalama, Washington. All other facilities are leased. Six of these banking offices have automated teller machines and three provide drive-up services. The following are all of the Company’s locations at December 31, 2007.

| | | | |

Cowlitz Bancorporation

Cowlitz Bank Main Office

Bay Mortgage—Longview | | Cowlitz Bank—Kalama | | Bay Bank—Portland |

927 Commerce Avenue | | 195 N. 1st Street | | 1001 SW 5th Ave., Suite 250 |

Longview, WA 98632 | | Kalama, WA 98625 | | Portland, OR 97204 |

(360) 423-9800 | | (360) 673-2226 | | (503) 222-9164 |

| | |

Cowlitz Bank—Kelso | | Bay Bank—Bellevue | | Bay Bank

Retirement Center Branch

Springridge at Charbonneau |

1000 South 13th | | 10500 NE 8th St., Suite 1750 | | 32200 SW French Prarie Rd |

Kelso, WA 98626 | | Bellevue, WA 98004 | | Wilsonville, OR 97070 |

(360) 423-7800 | | (425) 452-1543 | | (503) 694-6950 |

| | |

Cowlitz Bank—Castle Rock | | Bay Mortgage—Vancouver

Bay Bank—Vancouver | | Bay Bank—Seattle |

202 Cowlitz St. W. | | 700 Washington St., Suite 105 | | 1505 Westlake Ave N, Suite 125 |

Castle Rock, WA 98611 | | Vancouver, WA 98660 | | Seattle, WA 981093050 |

(360) 274-6685 | | (360) 992-6200 | | (206) 282-4000 |

The Company from time to time enters into routine litigation resulting from the collection of secured and unsecured indebtedness as part of its business of providing financial services. In some cases, such litigation will involve counterclaims or other claims against the Company. Such proceedings against financial institutions sometimes also involve claims for punitive damages in addition to other specific relief. The Company is not a party to any litigation other than in the ordinary course of business. In the opinion of management, the ultimate outcome of all pending legal proceedings will not individually or in the aggregate have a material adverse effect on the financial condition or the results of operations of the Company.

| Item 4. | Submission of Matters to a Vote of Securities Holders |

No matters were presented for a vote of the Company’s shareholders during the fourth quarter of 2007.

12

PART II

| Item 5. | Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities |

Cowlitz Bancorporation stock trades on the NASDAQ Global Market under the symbol “CWLZ”.

| | | | | | | | | | | | | | | | | | |

| | | 2007 | | 2006 |

| | Market Price | | Cash Dividend

Declared | | Market Price | | Cash Dividend

Declared |

| | High | | Low | | | High | | Low | |

1st Quarter | | $ | 17.00 | | $ | 16.10 | | $ | — | | $ | 14.60 | | $ | 13.13 | | $ | — |

2nd Quarter | | | 17.55 | | | 16.25 | | | — | | | 16.20 | | | 13.55 | | | — |

3rd Quarter | | | 16.40 | | | 12.38 | | | — | | | 16.88 | | | 14.94 | | | — |

4th Quarter | | | 15.01 | | | 11.29 | | | — | | | 17.43 | | | 16.25 | | | — |

During 2007 and 2006, the Company neither declared nor paid any dividends to its stockholders. As of February 29, 2008 there were 5,054,507 shares of common stock outstanding and 355 shareholders of record, a number that does not include beneficial owners who hold shares in “street name”.

On September 5, 2007, the Company announced a stock repurchase plan program for up to 500,000 shares. No shares were purchased as of December 31, 2007.

13

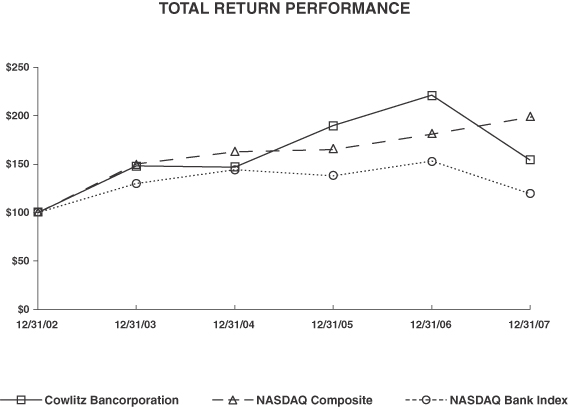

Stock Performance Graph

The following chart, which is furnished not filed, compares the annual percentage change in the cumulative total return of Cowlitz Bancorporation common stock during the period commencing December 31, 2002 and through the fiscal years ended December 31, 2007 with the total return index for the NASDAQ Composite Index and the total return index for the NASDAQ Bank Index. This comparison assumes $100.00 was invested on December 31, 2002, in Cowlitz common stock and in the comparison indices, and assumes reinvestment of all cash dividends prior to any tax effect and retention of all stock dividends. Price information for the chart was obtained using the NASDAQ closing price as of that date.

| | | | | | | | | | | | |

| | | Period Ending |

Index | | 12/31/02 | | 12/31/03 | | 12/31/04 | | 12/31/05 | | 12/31/06 | | 12/31/07 |

Cowlitz Bancorporation | | 100.00 | | 148.22 | | 146.77 | | 189.72 | | 221.08 | | 154.15 |

NASDAQ Composite | | 100.00 | | 150.01 | | 162.89 | | 165.13 | | 180.85 | | 198.60 |

NASDAQ Bank Index | | 100.00 | | 129.93 | | 144.21 | | 137.97 | | 153.15 | | 119.35 |

Cowlitz Bancorporation’s total cumulative return was 54.15% over the five-year period ending December 31, 2007, compared with 98.6% and 19.35% for the NASDAQ Composite and NASDAQ Bank indices, respectively.

14

| Item 6. | Selected Financial Data |

| | | | | | | | | | | | | | | | | | | | |

| | | As of and For the Year Ended December 31, | |

| (dollars in thousands) | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

Interest income | | $ | 36,226 | | | $ | 31,638 | | | $ | 19,698 | | | $ | 15,243 | | | $ | 16,282 | |

Interest expense | | | 13,871 | | | | 9,263 | | | | 4,902 | | | | 3,048 | | | | 4,962 | |

| | | | | | | | | | | | | | | | | | | | |

Net interest income | | | 22,355 | | | | 22,375 | | | | 14,796 | | | | 12,195 | | | | 11,320 | |

Provision for credit losses | | | 7,800 | | | | 2,640 | | | | 870 | | | | 210 | | | | 237 | |

| | | | | | | | | | | | | | | | | | | | |

Net interest income after provision for credit losses | | | 14,555 | | | | 19,735 | | | | 13,926 | | | | 11,985 | | | | 11,083 | |

Non-interest income | | | 3,462 | | | | 2,825 | | | | 2,194 | | | | 2,787 | | | | 9,406 | |

Non-interest expense | | | 18,721 | | | | 16,099 | | | | 12,304 | | | | 12,242 | | | | 20,410 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) before income taxes | | | (704 | ) | | | 6,461 | | | | 3,816 | | | | 2,530 | | | | 79 | |

Income tax (benefit) provision | | | (790 | ) | | | 1,702 | | | | 859 | | | | 590 | | | | (38 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 86 | | | $ | 4,759 | | | $ | 2,957 | | | $ | 1,940 | | | $ | 117 | |

| | | | | | | | | | | | | | | | | | | | |

Per share data: | | | | | | | | | | | | | | | | | | | | |

Diluted earnings per share | | $ | 0.02 | | | $ | 0.93 | | | $ | 0.66 | | | $ | 0.47 | | | $ | 0.03 | |

Cash dividends per share | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

Weighted average diluted shares outstanding | | | 5,175,526 | | | | 5,098,334 | | | | 4,451,466 | | | | 4,094,109 | | | | 4,004,502 | |

Balance Sheet Data (at period end) | | | | | | | | | | | | | | | | | | | | |

Loans, net of deferred fees | | $ | 397,325 | | | $ | 358,390 | | | $ | 270,247 | | | $ | 189,346 | | | $ | 163,490 | |

Allowance for loan losses | | | 5,801 | | | | 4,481 | | | | 4,668 | | | | 3,796 | | | | 3,968 | |

Net loans charged-off during period | | | 6,635 | | | | 2,483 | | | | 1,649 | | | | 382 | | | | 2,419 | |

Total non-performing assets (1) (2) | | | 13,226 | | | | 1,759 | | | | 4,156 | | | | 818 | | | | 3,225 | |

Total assets (1) | | | 514,180 | | | | 468,395 | | | | 370,095 | | | | 273,286 | | | | 268,799 | |

Total deposits | | | 441,179 | | | | 399,450 | | | | 309,195 | | | | 234,610 | | | | 226,480 | |

Total liabilities (1) | | | 458,640 | | | | 417,670 | | | | 325,154 | | | | 237,588 | | | | 236,997 | |

Total shareholders’ equity | | | 55,540 | | | | 50,725 | | | | 44,941 | | | | 35,698 | | | | 31,802 | |

Balance Sheet Data (average for period) | | | | | | | | | | | | | | | | | | | | |

Average loans, net of deferred fees | | $ | 383,477 | | | $ | 319,577 | | | $ | 219,882 | | | $ | 177,064 | | | $ | 173,966 | |

Average interest-earning assets | | | 446,337 | | | | 384,251 | | | | 284,080 | | | | 242,310 | | | | 271,771 | |

Average total assets | | | 489,141 | | | | 422,133 | | | | 308,542 | | | | 265,411 | | | | 292,520 | |

Average shareholders’ equity | | | 53,932 | | | | 47,642 | | | | 36,483 | | | | 33,477 | | | | 32,660 | |

Selected Ratios | | | | | | | | | | | | | | | | | | | | |

Return on average total assets | | | 0.02 | % | | | 1.13 | % | | | 0.96 | % | | | 0.73 | % | | | 0.04 | % |

Return on average shareholders’ equity | | | 0.16 | % | | | 9.99 | % | | | 8.11 | % | | | 5.80 | % | | | 0.36 | % |

Net interest margin (fully tax-equivalent) | | | 5.12 | % | | | 5.90 | % | | | 5.28 | % | | | 5.10 | % | | | 4.18 | % |

Efficiency ratio (3) | | | 72.51 | % | | | 63.88 | % | | | 72.42 | % | | | 81.71 | % | | | 98.48 | % |

Allowance for loan losses to: | | | | | | | | | | | | | | | | | | | | |

Ending total loans | | | 1.46 | % | | | 1.25 | % | | | 1.73 | % | | | 2.00 | % | | | 2.43 | % |

Non-performing loans | | | 54 | % | | | 394 | % | | | 112 | % | | | N/M | | | | 212 | % |

Non-performing assets to ending total assets | | | 2.57 | % | | | 0.38 | % | | | 1.12 | % | | | 0.30 | % | | | 1.20 | % |

Net loans charged-off to average loans | | | 1.73 | % | | | 0.78 | % | | | 0.75 | % | | | 0.22 | % | | | 1.39 | % |

Shareholders’ equity to average assets | | | 11.35 | % | | | 12.02 | % | | | 14.57 | % | | | 13.45 | % | | | 10.87 | % |

Tier 1 capital ratio (4) | | | 13.56 | % | | | 14.63 | % | | | 17.63 | % | | | 16.00 | % | | | 15.12 | % |

Total risk-based capital ratio (5) | | | 14.82 | % | | | 15.79 | % | | | 18.89 | % | | | 17.26 | % | | | 16.38 | % |

| (1) | For purposes of this presentation, immaterial results from discontinued operations have been included in the total. |

| (2) | Non-performing assets consist of non-accrual loans, loans contractually past due 90 days or more, and repossessed assets. |

| (3) | Non-interest expense divided by the sum of net interest income plus non-interest income. |

| (4) | Tier 1 capital divided by risk-weighted assets. |

| (5) | Total risk-based capital divided by risk-weighted assets. |

N/M—Not meaningful.

15

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations includes a discussion of significant business trends and uncertainties as well as certain forward-looking statements and is intended to be read in conjunction with and is qualified in its entirety by reference to the consolidated financial statements of the Company and accompanying notes included elsewhere in this report. For a discussion of important factors that could cause actual results to differ materially from such forward-looking statements, see Item 1A. “Risk Factors” and the risk factors discussed on page 1 immediately following the table of contents.

Results of Operations—Overview

For the year ended December 31, 2007, the Company recorded net income of $86,000, or $0.02 per diluted share. This compares with net income of $4.8 million, or $0.93 per share, and $3.0 million, or $0.66 per share, for the corresponding periods ended December 31, 2006, and 2005, respectively. Average loans in 2007 totaled $383.5 million, an increase of 20% over 2006, and up significantly from $219.9 million in 2005. This loan growth, primarily in commercial and real estate loans, was funded mostly by the growth in deposits, with a significant portion consisting of certificates of deposits.

Net interest income was down slightly compared with 2006 results, and up 51% over 2005 results. The net interest margin (on a fully tax-equivalent basis) was 5.12% in 2007, compared with 5.90% and 5.28% in 2006 and 2005, respectively. The decline in net interest margin in 2007 related to several factors, including recent Federal Reserve rate cuts, competitive loan and deposit pricing, and interest reversals on non-accrual loans, as well as a higher level of non-accrual loans.

The Company’s provision for credit losses was $7.8 million in 2007, compared with $2.6 million in 2006 and $0.9 million in 2005. Net charge-offs of $6.6 million were recorded in 2007, compared with $2.5 million and $1.6 million in 2006 and 2005, respectively. The charge-offs in 2007 primarily related to residential land acquisition and development loans. At December 31, 2007, total non-performing assets were $13.2 million compared with $1.8 million at year-end 2006 and $4.2 million at December 31, 2005. Non-performing assets include nonaccrual loans, loans past due 90 days or more and still accruing, and repossessed assets.

Non-interest income and non-interest expenses in 2007 increased significantly when compared with 2006, reflecting an overall higher level of staffing, occupancy, data processing and branch activities due to loan growth and the expansion of the Company’s international trade finance capabilities. In 2007, the Company incurred higher levels of professional fees related to efforts to comply with Sarbanes-Oxley Act requirements and to higher levels of non-performing assets.

Critical Accounting Policies

The Company’s most critical accounting policy is related to the allowance for credit losses. The Company utilizes both quantitative and qualitative considerations in establishing an allowance for credit losses believed to be appropriate as of each reporting date.

Quantitative factors include:

| | • | | the volume and severity of non-performing loans and adversely classified credits, |

| | • | | the level of net charge-offs experienced on previously classified loans, |

| | • | | the nature and value of collateral securing the loans, |

| | • | | the trend in loan growth and the percentage of change, |

| | • | | the level of geographic and/or industry concentration, |

16

| | • | | the relationship and trend over the past several years of recoveries in relation to charge-offs, and |

| | • | | other known factors regarding specific loans. |

Qualitative factors include:

| | • | | the effectiveness of credit administration, |

| | • | | the adequacy of loan review, |

| | • | | the adequacy of loan operations personnel and processes, |

| | • | | the effect of competitive issues that impact loan underwriting and structure, |

| | • | | the impact of economic conditions including interest rate trends, |

| | • | | the introduction of new loan products or specific marketing efforts, |

| | • | | large credit exposure and trends, and |

| | • | | industry segments that are exhibiting stress. |

Changes in the above factors could significantly affect the determination of the adequacy of the allowance for credit losses. Management performs a full analysis, no less often than quarterly, to ensure that changes in estimated credit loss levels are adjusted on a timely basis. For further discussion of this significant management estimate, see “Allowance for Credit Losses.”

Another critical accounting policy of the Company is that related to the carrying value of goodwill and other intangibles. Under Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (SFAS No. 142), the Company ceased amortization of goodwill on January 1, 2002 and periodically tests intangibles with indefinite lives for impairment. Impairment analysis of the fair value of goodwill involves a substantial amount of judgment, as does establishing and monitoring estimated amounts and lives of other intangible assets.

Net Interest Income

For financial institutions, the primary component of earnings is net interest income. Net interest income is the difference between interest income, principally from loans and investment securities portfolios, and interest expense, principally on customer deposits and other borrowings. Changes in net interest income result from changes in “volume,” “spread” and “margin.” Volume refers to the dollar level of interest-earning assets and interest-bearing liabilities. Spread refers to the difference between the yield on interest-earning assets and the cost of interest-bearing liabilities. Net interest margin is the ratio of net interest income to total interest-earning assets and is influenced by the level and relative mix of interest-earning assets and interest-bearing liabilities.

17

The following table sets forth, for the periods indicated, information with regard to average balances of assets and liabilities, the total dollar amount of interest income on interest-earning assets and interest expense on interest-bearing liabilities, the resulting yields or costs, net interest income, and net interest spread. Non-accrual loans have been included in the table as loans carrying a zero yield. Loan fees are amortized to interest income over the life of the loan.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | As of and For the Year Ended December 31, | |

| | | 2007 | | | 2006 | | | 2005 | |

| (dollars in thousands) | | Average

Outstanding

Balance | | | Interest

Earned/

Paid | | Yield/

Rate | | | Average

Outstanding

Balance | | | Interest

Earned/

Paid | | Yield/

Rate | | | Average

Outstanding

Balance | | | Interest

Earned/

Paid | | Yield/

Rate | |

Assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-Earning Assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Loans (1) (2) (3) | | $ | 383,477 | | | $ | 33,191 | | 8.66 | % | | $ | 319,577 | | | $ | 28,521 | | 8.92 | % | | $ | 219,882 | | | $ | 16,967 | | 7.72 | % |

Taxable securities | | | 34,010 | | | | 1,865 | | 5.48 | % | | | 36,594 | | | | 1,925 | | 5.26 | % | | | 41,004 | | | | 1,884 | | 4.59 | % |

Non-taxable securities (2) | | | 21,747 | | | | 1,383 | | 6.36 | % | | | 19,690 | | | | 1,096 | | 5.57 | % | | | 14,777 | | | | 809 | | 5.47 | % |

Federal funds sold | | | 5,207 | | | | 262 | | 5.03 | % | | | 5,919 | | | | 268 | | 4.53 | % | | | 5,977 | | | | 201 | | 3.36 | % |

Interest-earning balances due from banks and FHLB stock | | | 1,896 | | | | 42 | | 2.22 | % | | | 2,471 | | | | 140 | | 5.67 | % | | | 2,440 | | | | 42 | | 1.72 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest-earning assets (2) | | | 446,337 | | | | 36,743 | | 8.23 | % | | | 384,251 | | | | 31,950 | | 8.31 | % | | | 284,080 | | | | 19,903 | | 7.01 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and due from banks | | | 18,427 | | | | | | | | | | 15,941 | | | | | | | | | | 10,004 | | | | | | | |

Allowance for loan losses | | | (5,141 | ) | | | | | | | | | (5,074 | ) | | | | | | | | | (4,675 | ) | | | | | | |

Other assets | | | 29,518 | | | | | | | | | | 27,015 | | | | | | | | | | 19,133 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 489,141 | | | | | | | | | $ | 422,133 | | | | | | | | | $ | 308,542 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Liabilities and Shareholders Equity | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-Bearing Liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Savings, money market and interest-bearing demand deposits | | $ | 104,310 | | | $ | 2,260 | | 2.17 | % | | $ | 96,101 | | | $ | 1,321 | | 1.37 | % | | $ | 83,498 | | | $ | 846 | | 1.01 | % |

Certificates of deposit | | | 210,174 | | | | 10,602 | | 5.04 | % | | | 156,655 | | | | 7,022 | | 4.48 | % | | | 110,411 | | | | 3,506 | | 3.18 | % |

Federal funds purchased | | | 2,313 | | | | 121 | | 5.23 | % | | | 1,467 | | | | 83 | | 5.66 | % | | | 1,889 | | | | 62 | | 3.28 | % |

Junior subordinated debentures | | | 12,372 | | | | 875 | | 7.07 | % | | | 12,372 | | | | 815 | | 6.59 | % | | | 8,372 | | | | 455 | | 5.43 | % |

FHLB and other borrowings | | | 175 | | | | 13 | | 7.43 | % | | | 297 | | | | 22 | | 7.41 | % | | | 430 | | | | 33 | | 7.67 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest-bearing liabilities | | | 329,344 | | | | 13,871 | | 4.21 | % | | | 266,892 | | | | 9,263 | | 3.47 | % | | | 204,600 | | | | 4,902 | | 2.40 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Non-interest-bearing deposits | | | 100,817 | | | | | | | | | | 102,201 | | | | | | | | | | 64,934 | | | | | | | |

Other liabilities | | | 5,048 | | | | | | | | | | 5,398 | | | | | | | | | | 2,525 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total liabilities | | | 435,209 | | | | | | | | | | 374,491 | | | | | | | | | | 272,059 | | | | | | | |

Shareholders’ Equity | | | 53,932 | | | | | | | | | | 47,642 | | | | | | | | | | 36,483 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 489,141 | | | | | | | | | $ | 422,133 | | | | | | | | | $ | 308,542 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income (2) | | | | | | $ | 22,872 | | | | | | | | | $ | 22,687 | | | | | | | | | $ | 15,001 | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest spread | | | | | | | | | 4.02 | % | | | | | | | | | 4.84 | % | | | | | | | | | 4.61 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Yield on average interest-earning assets | | | | | | | | | 8.23 | % | | | | | | | | | 8.31 | % | | | | | | | | | 7.01 | % |

Interest expense to average interest-earning assets | | | | | | | | | 3.11 | % | | | | | | | | | 2.41 | % | | | | | | | | | 1.73 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income to average interest-earning assets (net interest margin) | | | | | | | | | 5.12 | % | | | | | | | | | 5.90 | % | | | | | | | | | 5.28 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Loans include loans on which the accrual of interest has been discontinued. |

| (2) | Interest earned on non-taxable securities and loans has been computed on a 34 percent tax-equivalent basis. |

| (3) | Loan interest income includes net loan fee amortization of $1.8 million, $1.8 million, and $0.9 million for 2007, 2006, and 2005, respectively. |

18

The following table shows the dollar amount of the increase (decrease) in the Company’s net interest income and expense, on a tax equivalent basis, and attributes such dollar amounts to changes in volume or changes in rates. Rate/volume variances have been allocated to volume changes:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2007 vs. 2006 | | | 2006 vs. 2005 | |

| | | Increase (Decrease)

Due to | | | Total

Increase

(Decrease) | | | Increase (Decrease)

Due to | | | Total

Increase

(Decrease) | |

| | | | | |

| | | Volume | | | Rate | | | | Volume | | | Rate | | |

Interest Income: | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-earning balances due from banks | | $ | (13 | ) | | $ | (85 | ) | | $ | (98 | ) | | $ | 2 | | | $ | 96 | | | $ | 98 | |

Federal funds sold | | | (36 | ) | | | 30 | | | | (6 | ) | | | (3 | ) | | | 70 | | | | 67 | |

Investment security income: | | | | | | | | | | | | | | | | | | | | | | | | |

Taxable securities | | | (142 | ) | | | 82 | | | | (60 | ) | | | (232 | ) | | | 273 | | | | 41 | |

Non-taxable securities | | | 131 | | | | 156 | | | | 287 | | | | 274 | | | | 13 | | | | 287 | |

Loans | | | 5,531 | | | | (861 | ) | | | 4,670 | | | | 8,893 | | | | 2,661 | | | | 11,554 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total interest income | | | 5,471 | | | | (678 | ) | | | 4,793 | | | | 8,934 | | | | 3,113 | | | | 12,047 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Interest Expense: | | | | | | | | | | | | | | | | | | | | | | | | |

Savings, money market and interest-bearing demand deposits | | | 178 | | | | 761 | | | | 939 | | | | 173 | | | | 302 | | | | 475 | |

Certificates of deposit | | | 2,700 | | | | 880 | | | | 3,580 | | | | 2,073 | | | | 1,443 | | | | 3,516 | |

Federal funds purchased | | | 44 | | | | (6 | ) | | | 38 | | | | (24 | ) | | | 45 | | | | 21 | |

Junior subordinated debentures | | | — | | | | 60 | | | | 60 | | | | 263 | | | | 97 | | | | 360 | |

FHLB and other borrowings | | | (9 | ) | | | — | | | | (9 | ) | | | (10 | ) | | | (1 | ) | | | (11 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total interest expense | | | 2,913 | | | | 1,695 | | | | 4,608 | | | | 2,475 | | | | 1,886 | | | | 4,361 | |

| | | | | | | | | | | | | | | | | | | | | | | | |