0000895421 srt:ArithmeticAverageMember us-gaap:FairValueInputsLevel3Member us-gaap:FairValueMeasurementsRecurringMember us-gaap:InterestRateContractMember ms:MeasurementInputInterestRateCurveCorrelationMember us-gaap:ValuationTechniqueOptionPricingModelMember 2020-03-31

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2020

Commission File Number 1-11758

(Exact name of Registrant as specified in its charter)

|

| | | | | | | |

| | | | | | | | |

| Delaware | 1585 Broadway | 36-3145972 | (212) | 761-4000 | |

(State or other jurisdiction of incorporation or organization) | New York, | NY | 10036 | (I.R.S. Employer Identification No.) | (Registrant’s telephone number, including area code) |

| (Address of principal executive offices, including zip code) |

|

| | |

Securities registered pursuant to Section 12(b) of the Act: | | |

| Title of each class | Trading Symbol(s) | Name of exchange on which registered |

| Common Stock, $0.01 par value | MS | New York Stock Exchange |

| Depositary Shares, each representing 1/1,000th interest in a share of Floating Rate | MS/PA | New York Stock Exchange |

| Non-Cumulative Preferred Stock, Series A, $0.01 par value |

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate | MS/PE | New York Stock Exchange |

| Non-Cumulative Preferred Stock, Series E, $0.01 par value |

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate | MS/PF | New York Stock Exchange |

| Non-Cumulative Preferred Stock, Series F, $0.01 par value |

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate | MS/PI | New York Stock Exchange |

| Non-Cumulative Preferred Stock, Series I, $0.01 par value |

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate | MS/PK | New York Stock Exchange |

| Non-Cumulative Preferred Stock, Series K, $0.01 par value |

| Depository Shares, each representing 1/1000th interest in a share of 4.875% | MS/PL | New York Stock Exchange |

| Non-Cumulative Preferred Stock, Series L, $0.01 par value |

| Global Medium-Term Notes, Series A, Fixed Rate Step-Up Senior Notes Due 2026 | MS/26C | New York Stock Exchange |

| of Morgan Stanley Finance LLC (and Registrant’s guarantee with respect thereto) |

| Morgan Stanley Cushing® MLP High Income Index ETNs due March 21, 2031 | MLPY | NYSE Arca, Inc. |

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of April 30, 2020, there were 1,575,656,380 shares of the Registrant’s Common Stock, par value $0.01 per share, outstanding.

QUARTERLY REPORT ON FORM 10-Q

For the quarter ended March 31, 2020

|

| | | | | |

| Table of Contents | Part | Item | Page |

| II | 1A |

| |

| I | | |

| I | 2 |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| I | 3 |

| |

| | | |

| | | |

| | | |

| | | |

| I | 1 |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | |

| | | |

| II | | |

| II | 1 |

| |

| II | 2 |

| |

| I | 4 |

| |

| II | 6 |

| |

| | | |

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the SEC. The SEC maintains a website, www.sec.gov, that contains annual, quarterly and current reports, proxy and information statements and other information that issuers file electronically with the SEC. Our electronic SEC filings are available to the public at the SEC’s website.

Our website is www.morganstanley.com. You can access our Investor Relations webpage at www.morganstanley.com/about-us-ir. We make available free of charge, on or through our Investor Relations webpage, our proxy statements, annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934, as amended (“Exchange Act”), as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. We also make available, through our Investor Relations webpage, via a link to the SEC’s website, statements of beneficial ownership of our equity securities filed by our directors, officers, 10% or greater shareholders and others under Section 16 of the Exchange Act.

You can access information about our corporate governance at www.morganstanley.com/about-us-governance and our sustainability initiatives at www.morganstanley.com/about-us/sustainability-at-morgan-stanley. Our webpages include:

| |

| • | Amended and Restated Certificate of Incorporation; |

| |

| • | Amended and Restated Bylaws; |

| |

| • | Charters for our Audit Committee, Compensation, Management Development and Succession Committee, Nominating and Governance Committee, Operations and Technology Committee, and Risk Committee; |

| |

| • | Corporate Governance Policies; |

| |

| • | Policy Regarding Corporate Political Activities; |

| |

| • | Policy Regarding Shareholder Rights Plan; |

| |

| • | Equity Ownership Commitment; |

| |

| • | Code of Ethics and Business Conduct; |

| |

| • | Integrity Hotline Information; |

| |

| • | Environmental and Social Policies; and |

Our Code of Ethics and Business Conduct applies to all directors, officers and employees, including our Chief Executive Officer, Chief Financial Officer and Deputy Chief Financial Officer. We will post any amendments to the Code of Ethics and Business Conduct and any waivers that are required to be disclosed by the rules of either the SEC or the New York Stock Exchange LLC (“NYSE”) on our website. You can request a copy of these documents, excluding exhibits, at no cost, by contacting Investor Relations, 1585 Broadway, New York, NY 10036 (212-761-4000). The information on our website is not incorporated by reference into this report.

Risk Factors

In addition to “Risk Factors” in Part I, Item 1A of the 2019 Form 10-K, please refer to the risk factor under Item 8.01. “Other Matters,” in the Current Report on Form 8-K filed with the SEC on April 16, 2020 and the additional risk factors under “Risk Factors” in the Registration Statement on Form S-4 filed with the SEC on April 17, 2020.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Introduction

Morgan Stanley is a global financial services firm that maintains significant market positions in each of its business segments—Institutional Securities, Wealth Management and Investment Management. Morgan Stanley, through its subsidiaries and affiliates, provides a wide variety of products and services to a large and diversified group of clients and customers, including corporations, governments, financial institutions and individuals. Unless the context otherwise requires, the terms “Morgan Stanley,” “Firm,” “us,” “we” or “our” mean Morgan Stanley (the “Parent Company”) together with its consolidated subsidiaries. See the “Glossary of Common Terms and Acronyms” for the definition of certain terms and acronyms used throughout this Form 10-Q.

A description of the clients and principal products and services of each of our business segments is as follows:

Institutional Securities provides investment banking, sales and trading, lending and other services to corporations, governments, financial institutions and high to ultra-high net worth clients. Investment banking services consist of capital raising and financial advisory services, including services relating to the underwriting of debt, equity and other securities, as well as advice on mergers and acquisitions, restructurings, real estate and project finance. Sales and trading services include sales, financing, prime brokerage and market-making activities in equity and fixed income products, including foreign exchange and commodities. Lending activities include originating corporate loans and commercial real estate loans, providing secured lending facilities, and extending financing to sales and trading customers. Other activities include Asia wealth management services, investments and research.

Wealth Management provides a comprehensive array of financial services and solutions to individual investors and small to medium-sized businesses and institutions covering: brokerage and investment advisory services; financial and wealth planning services; stock plan administration services; annuity and insurance products; securities-based lending, residential real estate loans and other lending products; banking; and retirement plan services.

Investment Management provides a broad range of investment strategies and products that span geographies, asset classes, and public and private markets to a diverse group of clients across institutional and intermediary channels. Strategies and products, which are offered through a variety of investment vehicles, include equity, fixed income, liquidity and alternative/other products. Institutional clients include defined benefit/defined contribution plans, foundations, endowments, government entities, sovereign wealth funds, insurance companies, third-party fund sponsors and corporations. Individual clients are generally served through intermediaries, including affiliated and non-affiliated distributors.

Management’s Discussion and Analysis includes certain metrics which we believe to be useful to us, investors, analysts and other stakeholders by providing further transparency about, or an additional means of assessing, our financial condition and operating results. Such metrics, when used, are defined and may be different from or inconsistent with metrics used by other companies.

The results of operations in the past have been, and in the future may continue to be, materially affected by: competition; risk factors; legislative, legal and regulatory developments; and other factors. These factors also may have an adverse impact on our ability to achieve our strategic objectives. Additionally, the discussion of our results of operations herein may contain forward-looking statements. These statements, which reflect management’s beliefs and expectations, are subject to risks and uncertainties that may cause actual results to differ materially. For a discussion of the risks and uncertainties that may affect our future results, see “Forward-Looking Statements,” “Business—Competition,” “Business—Supervision and Regulation,” and “Risk Factors” in the 2019 Form 10-K, and “Liquidity and Capital Resources—Regulatory Requirements” herein. In addition, see “Executive Summary” herein and “Risk Factors” for information on the current and possible future effects of the COVID-19 pandemic on our results.

|

| |

| |

| Management’s Discussion and Analysis | |

Executive Summary

Overview of Financial Results

Consolidated Results

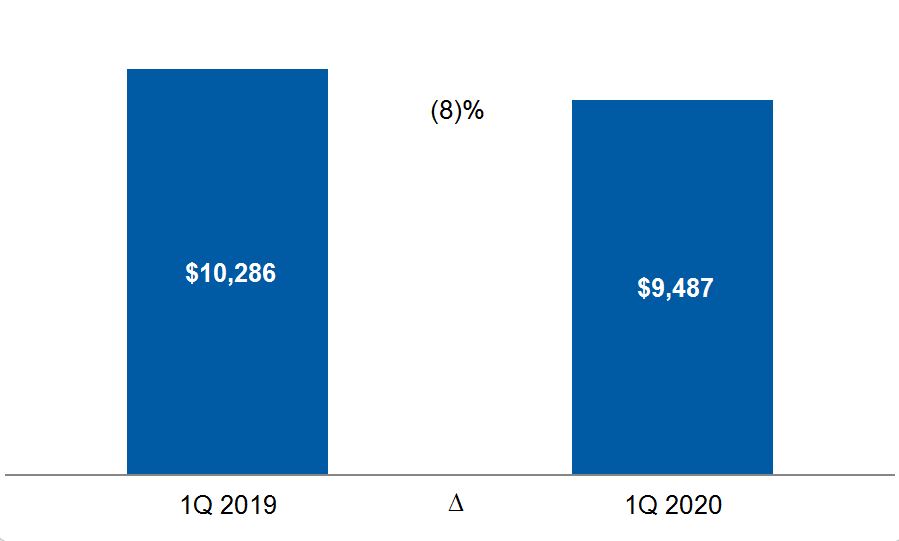

Net Revenues

($ in millions)

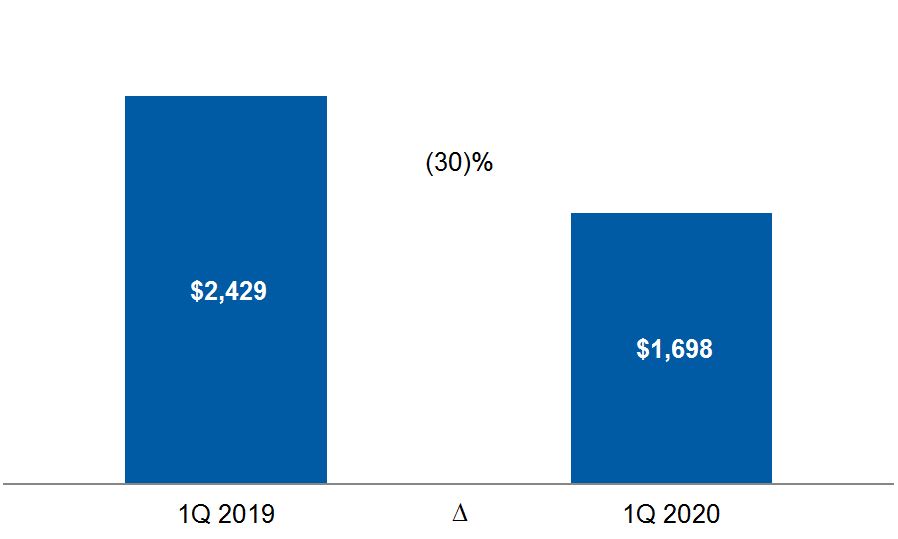

Net Income Applicable to Morgan Stanley

($ in millions)

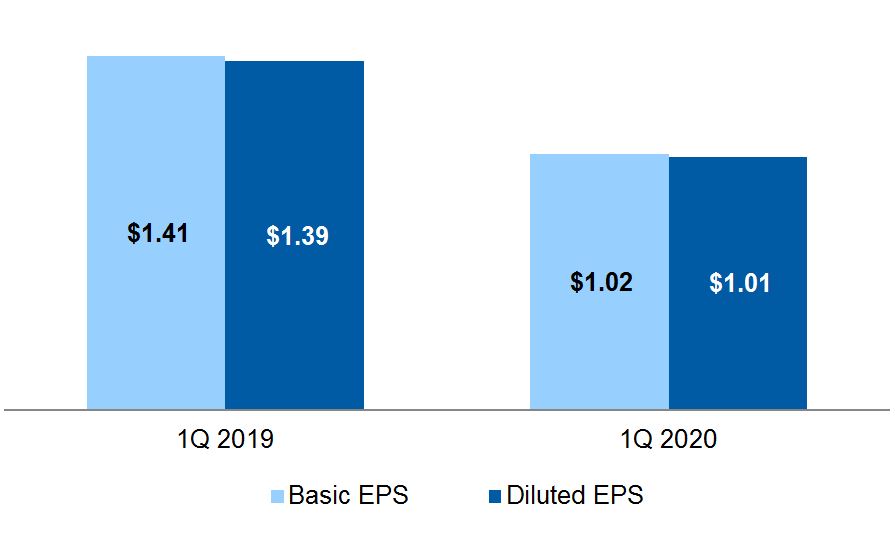

Earnings per Common Share1

| |

| 1. | For further information on basic and diluted EPS, see Note 16 to the financial statements. |

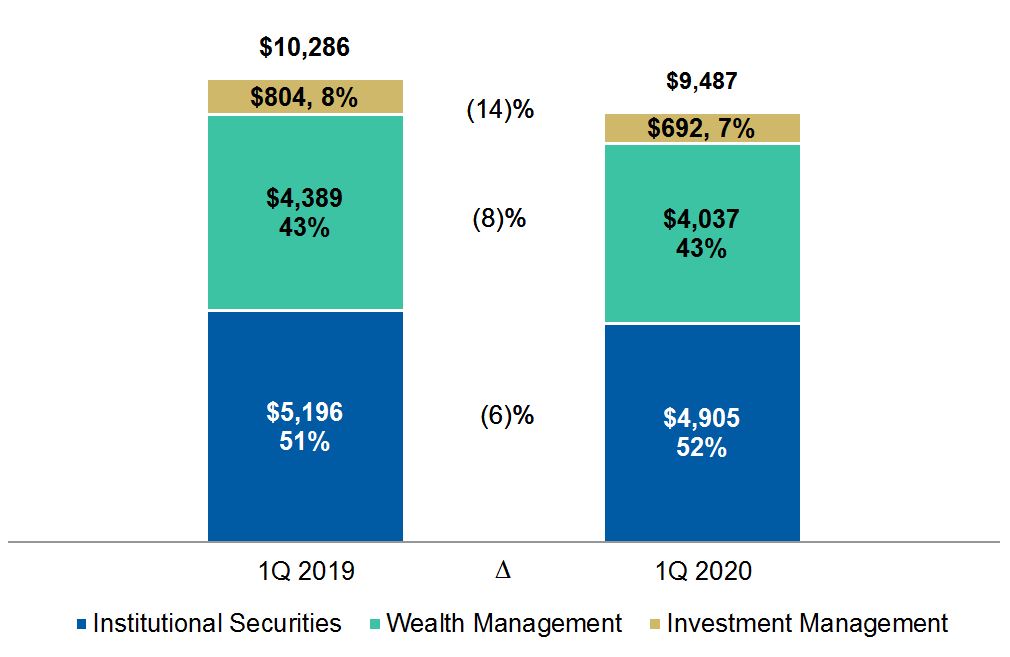

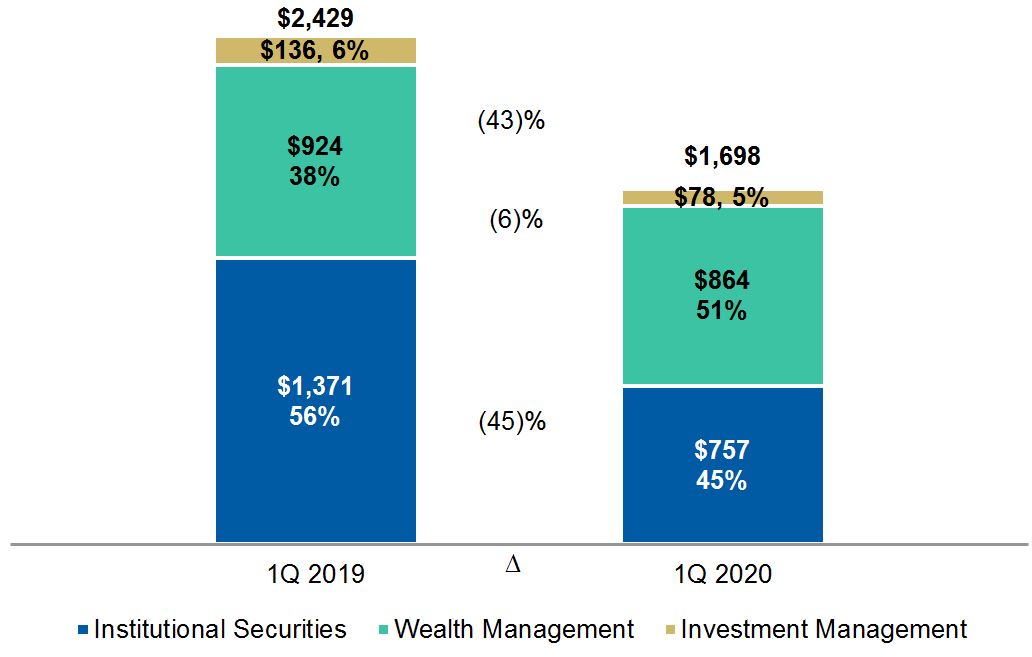

We reported net revenues of $9,487 million in the quarter ended March 31, 2020 (“current quarter,” or “1Q 2020”), compared with $10,286 million in the quarter ended March 31, 2019 (“prior year quarter,” or “1Q 2019”). For the current quarter, net income applicable to Morgan Stanley was $1,698 million, or $1.01 per diluted common share, compared with $2,429 million or $1.39 per diluted common share, in the prior year quarter.

See “Coronavirus Disease (COVID-19) Pandemic” herein for information on the current and possible future effects of the COVID-19 pandemic on our results.

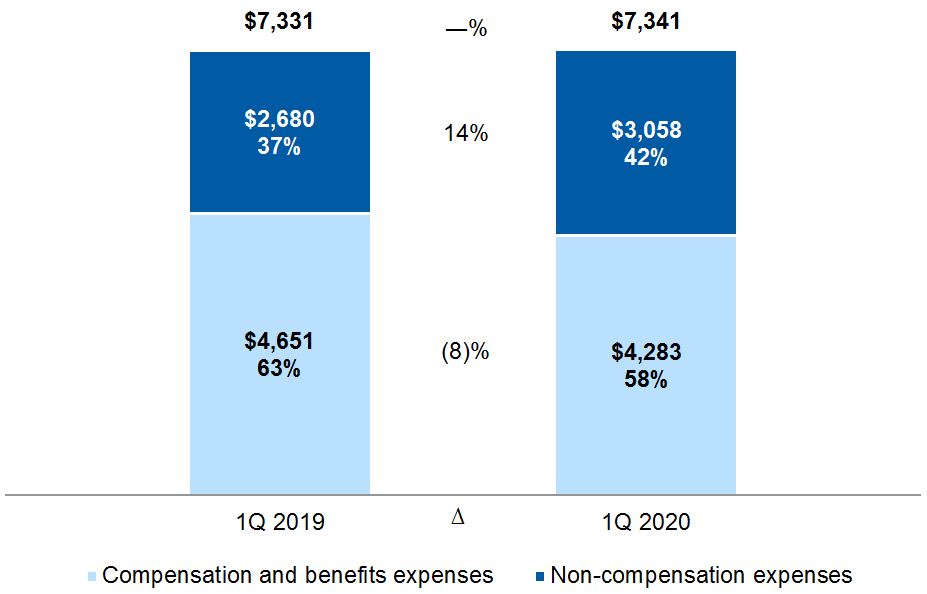

Non-interest Expenses1

($ in millions)

| |

| 1. | The percentages on the bars in the chart represent the contribution of compensation and benefits expenses and non-compensation expenses to the total. |

| |

| • | Compensation and benefits expenses of $4,283 million in the current quarter decreased 8% from $4,651 million in the prior year quarter. The decrease was primarily due to decreases in the fair value of investments to which certain deferred compensation plans are referenced and compensation associated with carried interest, partially offset by increases in discretionary incentive compensation, and the formulaic payout to Wealth Management representatives driven by the mix of revenues. |

| |

| • | Non-compensation expenses of $3,058 million in the current quarter increased 14% from $2,680 million in the prior year quarter. The increase was primarily due to higher volume-related expenses and an increase in the provision for credit losses for lending commitments. |

Income Taxes

The prior year quarter included intermittent net discrete tax benefits of $101 million, primarily associated with remeasurement of reserves and related interest as a result of new information pertaining to the resolution of multi-jurisdiction tax examinations. For further information, see “Supplemental Financial Information—Income Tax Matters” herein.

|

| |

| |

| Management’s Discussion and Analysis | |

Selected Financial Information and Other Statistical Data |

| | | | | | |

| | Three Months Ended March 31, |

| $ in millions | 2020 | 2019 |

| Net income applicable to Morgan Stanley | $ | 1,698 |

| $ | 2,429 |

|

| Preferred stock dividends | 108 |

| 93 |

|

| Earnings applicable to Morgan Stanley common shareholders | $ | 1,590 |

| $ | 2,336 |

|

| | | |

Expense efficiency ratio1 | 77.4 | % | 71.3 | % |

ROE2 | 8.5 | % | 13.1 | % |

Adjusted ROE3 | 8.3 | % | 12.5 | % |

ROTCE2,3 | 9.7 | % | 14.9 | % |

Adjusted ROTCE3 | 9.5 | % | 14.2 | % |

Pretax margin4 | 22.6 | % | 28.7 | % |

Pre-tax margin by segment4 | | |

| Institutional Securities | 19 | % | 31 | % |

| Wealth Management | 26 | % | 27 | % |

| Investment Management | 21 | % | 22 | % |

|

| | | | | | |

| in millions, except per share and employee data | At

March 31,

2020 | At

December 31,

2019 |

Liquidity resources5 | $ | 255,134 |

| $ | 215,868 |

|

Loans6 | $ | 148,697 |

| $ | 130,637 |

|

| Total assets | $ | 947,795 |

| $ | 895,429 |

|

| Deposits | $ | 235,239 |

| $ | 190,356 |

|

| Borrowings | $ | 194,856 |

| $ | 192,627 |

|

| Common shares outstanding | 1,576 |

| 1,594 |

|

| Common shareholders' equity | $ | 77,340 |

| $ | 73,029 |

|

Tangible common shareholders’ equity3 | $ | 68,194 |

| $ | 63,780 |

|

Book value per common share7 | $ | 49.09 |

| $ | 45.82 |

|

Tangible book value per common share3,7 | $ | 43.28 |

| $ | 40.01 |

|

| Worldwide employees | 60,670 |

| 60,431 |

|

|

| | | | |

| | At

March 31,

2020 | At

December 31,

2019 |

Capital ratios8 | | |

| Common Equity Tier 1 capital | 15.2 | % | 16.4 | % |

| Tier 1 capital | 17.3 | % | 18.6 | % |

| Total capital | 19.6 | % | 21.0 | % |

| Tier 1 leverage | 8.1 | % | 8.3 | % |

| SLR | 6.2 | % | 6.4 | % |

| |

| 1. | The expense efficiency ratio represents total non-interest expenses as a percentage of net revenues. |

| |

| 2. | ROE and ROTCE represent annualized earnings applicable to Morgan Stanley common shareholders as a percentage of average common equity and average tangible common equity, respectively. |

| |

| 3. | Represents a non-GAAP measure. See “Selected Non-GAAP Financial Information” herein. |

| |

| 4. | Pre-tax margin represents income from continuing operations before income taxes as a percentage of net revenues. |

| |

| 5. | For a discussion of Liquidity resources, see “Liquidity and Capital Resources—Liquidity Risk Management Framework—Liquidity Resources” herein. |

| |

| 6. | Amounts include loans held for investment (net of allowance) and loans held for sale but exclude loans at fair value, which are included in Trading assets in the balance sheets (see Note 9 to the financial statements). |

| |

| 7. | Book value per common share and tangible book value per common share equal common shareholders’ equity and tangible common shareholders’ equity, respectively, divided by common shares outstanding. |

| |

| 8. | At March 31, 2020 and December 31, 2019, our risk-based capital ratios are based on the Advanced Approach and the Standardized Approach rules, respectively. For a discussion of our capital ratios, see “Liquidity and Capital Resources—Regulatory Requirements” herein. |

Business Segment Results

Net Revenues by Segment1

($ in millions)

Net Income Applicable to Morgan Stanley by Segment1

($ in millions)

| |

| 1. | The percentages on the bars in the charts represent the contribution of each business segment to the total of the applicable financial category and may not total to 100% due to intersegment eliminations. See Note 19 to the financial statements for details of intersegment eliminations. |

| |

| • | Institutional Securities net revenues of $4,905 million in the current quarter decreased 6% from $5,196 million in the prior year quarter primarily reflecting losses on loans and lending commitments held for sale and an increase in the provision for credit losses on loans and lending commitments held for investment, as well as losses related to investments associated with certain employee deferred cash-based compensation plans, partially offset by increases in Fixed Income and Equity sales and trading revenues driven by increased volumes and volatility. |

| |

| • | Wealth Management net revenues of $4,037 million in the current quarter decreased 8% from $4,389 million in the prior year quarter, primarily reflecting losses related to investments associated with certain employee deferred cash-based compensation plans, partially offset by higher Asset management revenues and higher commissions driven by market volatility. |

|

| |

| |

| Management’s Discussion and Analysis | |

| |

| • | Investment Management net revenues of $692 million in the current quarter decreased 14% from $804 million in the prior year quarter, primarily reflecting lower Investments revenues, partially offset by higher Asset management revenues. |

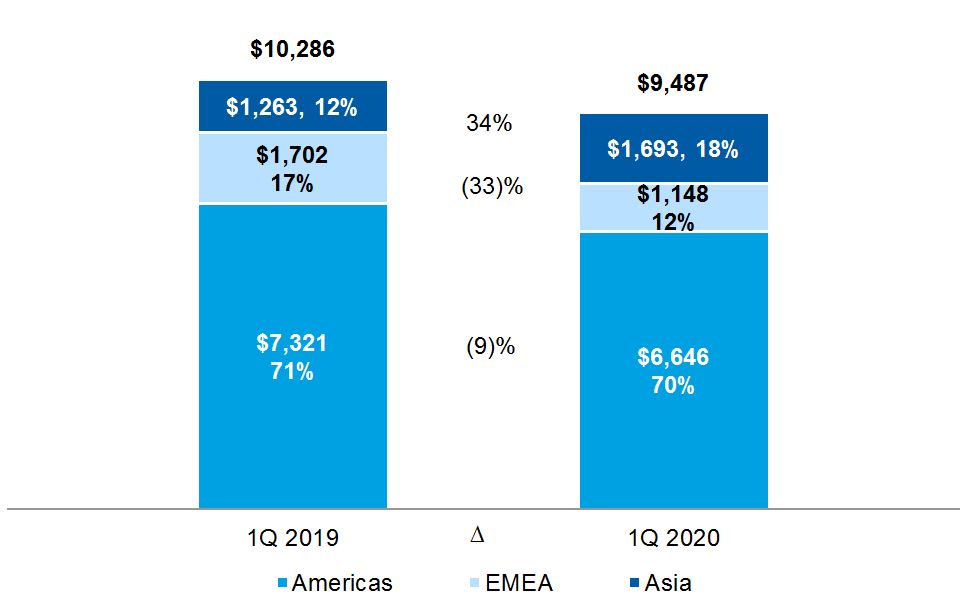

Net Revenues by Region1, 2

($ in millions)

| |

| 1. | The percentages on the bars in the charts represent the contribution of each region to the total. |

| |

| 2. | For a discussion of how the geographic breakdown of net revenues is determined, see Note 19 to the financial statements. |

Both the 34% increase in revenues in Asia and the 33% decrease in revenues in EMEA were primarily attributable to Equity sales and trading within the Institutional Securities business segment. The Equity sales and trading revenues increase in Asia reflects higher client volumes, while in EMEA market volatility and reduced dividend expectations weighed on revenues in the derivatives and financing businesses. Additionally, EMEA results reflected markdowns of held-for-sale loans and lending commitments.

Coronavirus Disease (COVID-19) Pandemic

The coronavirus disease (“COVID-19”) pandemic and related government-imposed shelter-in-place restrictions have had, and will likely continue to have, a severe impact on global economic conditions and the environment in which we operate our businesses.

In responding to this unprecedented situation, we have taken measures to prioritize the health of our employees and their families, and to be prepared operationally to serve our clients, leveraging our business continuity planning and historical investments in technology. More than 90% of our employees are currently working from home, and to date, we have not experienced any significant loss of operational capability, as we have implemented our pandemic-related responses. We believe we are prepared to continue to operate with the vast majority of our workforce working remotely for as long as health guidelines and prudence require, with limited impact to our operational capabilities.

The coronavirus disease has impacted many people’s health around the world, including many of our employees. Our

Chairman and CEO was diagnosed with the coronavirus in March, but has fully recovered. The rest of the Firm’s Operating Committee remain healthy and are sheltering in place.

With the COVID-19 impacts on individuals, communities and organizations continuing to evolve, governments around the world have reacted to the health crisis caused by the pandemic, and central banks have taken steps to proactively address market disruptions by cutting interest rates and providing liquidity sources and other stimulus programs. See “Regulatory Developments in Response to COVID-19” herein for further details.

We also have taken several direct steps to provide assistance. Our balance sheet has increased as we: support market and client activity; take in increased deposits from our Wealth Management clients; extend credit to our institutional and retail clients to provide them with additional liquidity; and provide financing to support COVID-19 impacted clients across multiple sectors. Along with the seven other U.S. Banks comprising the Financial Services Forum, we voluntarily ceased our Share Repurchase Program to keep this capital available to help clients and took action on the Federal Reserve's encouragement to use its discount window by borrowing from it. We have also taken steps to participate in other Federal Reserve programs, notably the Primary Dealer Credit Facility (“PDCF”).

Our financial condition, balance sheet, capital and liquidity have remained strong. In March 2020, we saw deposit inflows of $38 billion as customers sought relative safety away from volatile markets, and we raised more than $5 billion in new long-term debt supplementing our liquidity position.

As further discussed in “Business Segments” herein, towards the end of the current quarter, we observed the impact of the pandemic on our business. The decline of asset prices, reduction in interest rates, widening of credit spreads, borrower and counterparty credit deterioration, market volatility and reduced investment banking activity had the most immediate negative impacts on our current quarter performance. Related to these effects, the Firm experienced mark-to-market losses, net of economic hedges of $610 million on loans and lending commitments held for sale, provisions of $407 million for credit losses on loans and lending commitments held for investment, and losses of $384 million on fund and business-related investments, net of hedges. At the same time, high levels of client trading activity, related to market volatility, significantly increased revenues for global macro products and Commodities in Institutional Securities, and the transactional businesses in Wealth Management.

Though we are unable to estimate the extent of the impact, the continuing pandemic and related global economic crisis will adversely impact our future operating results. Additionally, with the continuance of many of the same negative impacts, without the benefit of higher client trading activity experienced in the

|

| |

| |

| Management’s Discussion and Analysis | |

current quarter, it is uncertain that our financial objectives will be attained within the originally stated two year time frame.

We continue to use the elements of our Enterprise Risk Management framework manage the significant uncertainty in the present economic and market conditions. See “Quantitative and Qualitative Disclosures about Risk” in the 2019 Form 10-K for further information about our Enterprise Risk Management Framework.

In addition, refer to “Risk Factors” herein and Forward Looking Statements in the 2019 Form 10-K.

Selected Non-GAAP Financial Information

We prepare our financial statements using U.S. GAAP. From time to time, we may disclose certain “non-GAAP financial measures” in this document or in the course of our earnings releases, earnings and other conference calls, financial presentations, definitive proxy statement and otherwise. A “non-GAAP financial measure” excludes, or includes, amounts from the most directly comparable measure calculated and presented in accordance with U.S. GAAP. We consider the non-GAAP financial measures we disclose to be useful to us, investors, analysts and other stakeholders by providing further transparency about, or an alternate means of assessing, our financial condition, operating results, prospective regulatory capital requirements or capital adequacy.

These measures are not in accordance with, or a substitute for, U.S. GAAP and may be different from or inconsistent with non-GAAP financial measures used by other companies. Whenever we refer to a non-GAAP financial measure, we will also generally define it or present the most directly comparable financial measure calculated and presented in accordance with U.S. GAAP, along with a reconciliation of the differences between the U.S. GAAP financial measure and the non-GAAP financial measure.

The principal non-GAAP financial measures presented in this document are set forth in the following tables.

Reconciliations from U.S. GAAP to Non-GAAP Consolidated Financial Measures

|

| | | | | | |

| | Three Months Ended

March 31, |

| $ in millions, except per share data | 2020 | 2019 |

| Net income applicable to Morgan Stanley | $ | 1,698 |

| $ | 2,429 |

|

| Impact of adjustments | (31 | ) | (101 | ) |

Adjusted net income applicable to Morgan Stanley—non-GAAP1 | $ | 1,667 |

| $ | 2,328 |

|

| Earnings per diluted common share | $ | 1.01 |

| $ | 1.39 |

|

| Impact of adjustments | (0.02 | ) | (0.06 | ) |

Adjusted earnings per diluted common share—non-GAAP1 | $ | 0.99 |

| $ | 1.33 |

|

| Effective income tax rate | 17.1 | % | 16.5 | % |

| Impact of adjustments | 1.4 | % | 3.4 | % |

Adjusted effective income tax rate— non-GAAP1 | 18.5 | % | 19.9 | % |

|

| | | | | | |

| | Average Monthly Balance |

| | Three Months Ended March 31, |

| $ in millions | 2020 | 2019 |

| Tangible equity | | |

| Morgan Stanley shareholders' equity | $ | 83,244 |

| $ | 80,115 |

|

| Less: Goodwill and net intangible assets | (9,200 | ) | (8,806 | ) |

| Tangible Morgan Stanley shareholders' equity—Non-GAAP | $ | 74,044 |

| $ | 71,309 |

|

| Common shareholders' equity | $ | 74,724 |

| $ | 71,595 |

|

| Less: Goodwill and net intangible assets | (9,200 | ) | (8,806 | ) |

| Tangible common shareholders' equity—Non-GAAP | $ | 65,524 |

| $ | 62,789 |

|

|

| | | | | | |

| | Three Months Ended

March 31, |

| $ in billions | 2020 | 2019 |

| Average common equity | | |

| Unadjusted—GAAP | $ | 74.7 |

| $ | 71.6 |

|

Adjusted1—Non-GAAP | 74.7 |

| 71.5 |

|

ROE2 | | |

| Unadjusted—GAAP | 8.5 | % | 13.1 | % |

Adjusted—Non-GAAP1, 3 | 8.3 | % | 12.5 | % |

| Average tangible common equity—Non-GAAP |

| Unadjusted | $ | 65.5 |

| $ | 62.8 |

|

Adjusted1 | 65.5 |

| 62.7 |

|

ROTCE2—Non-GAAP | | |

| Unadjusted | 9.7 | % | 14.9 | % |

Adjusted1, 3 | 9.5 | % | 14.2 | % |

|

| |

| |

| Management’s Discussion and Analysis | |

Non-GAAP Financial Measures by Business Segment

|

| | | | | | |

| | Three Months Ended

March 31, |

| $ in billions | 2020 | 2019 |

Average common equity4, 5 | | |

| Institutional Securities | $ | 42.8 |

| $ | 40.4 |

|

| Wealth Management | 18.2 |

| 18.2 |

|

| Investment Management | 2.6 |

| 2.5 |

|

Average tangible common equity4, 5 | | |

| Institutional Securities | $ | 42.3 |

| $ | 39.9 |

|

| Wealth Management | 10.4 |

| 10.2 |

|

| Investment Management | 1.7 |

| 1.5 |

|

ROE6 | | |

| Institutional Securities | 6.3 | % | 12.9 | % |

| Wealth Management | 18.5 | % | 19.8 | % |

| Investment Management | 11.7 | % | 21.9 | % |

ROTCE6 | | |

| Institutional Securities | 6.4 | % | 13.0 | % |

| Wealth Management | 32.3 | % | 35.6 | % |

| Investment Management | 18.1 | % | 35.3 | % |

| |

| 1. | Adjusted amounts exclude net discrete tax provisions (benefits) that are intermittent and include those that are recurring. Provisions (benefits) related to conversion of employee share-based awards are expected to occur every year and, as such, are considered recurring discrete tax items. For further information on the net discrete tax provisions (benefits), see “Supplemental Financial Information—Income Tax Matters” herein. |

| |

| 2. | ROE and ROTCE represent annualized earnings applicable to Morgan Stanley common shareholders as a percentage of average common equity and average tangible common equity, respectively. When excluding intermittent net discrete tax provisions (benefits), both the numerator and average denominator are adjusted. |

| |

| 3. | The calculations used in determining our “ROE and ROTCE Targets” referred to in the following section are the Adjusted ROE and Adjusted ROTCE amounts shown in this table. |

| |

| 4. | Average common equity and average tangible common equity for each business segment is determined using our Required Capital framework (see "Liquidity and Capital Resources—Regulatory Requirements—Attribution of Average Common Equity According to the Required Capital Framework” herein). |

| |

| 5. | The sums of the segments' Average common equity and Average tangible common equity do not equal the Consolidated measures due to Parent equity. |

| |

| 6. | The calculation of ROE and ROTCE by segment uses annualized net income applicable to Morgan Stanley by segment less preferred dividends allocated to each segment as a percentage of average common equity and average tangible common equity, respectively, allocated to each segment. |

Return on Tangible Common Equity Target

In January 2020, we established an ROTCE Target of 13% to 15% to be achieved over the next two years.

Our ROTCE Target is a forward-looking statement that was based on a normal market environment and may be materially affected by many factors, including, among other things: macroeconomic and market conditions; legislative and regulatory developments; industry trading and investment banking volumes; equity market levels; interest rate environment; outsized legal expenses or penalties; the ability to maintain a reduced level of expenses; and capital levels.

With the COVID–19 pandemic, and the current global economic crisis that includes negative impacts from many of the aforementioned factors, it is uncertain that the ROTCE Target will be met within the originally stated time frame. See “Coronavirus Disease (COVID–19) Pandemic” herein and “Risk Factors” for further information on market and economic conditions and their effects on our financial results.

For further information on non-GAAP measures (ROTCE excluding intermittent net discrete tax items), see “Selected Non-GAAP Financial Information” herein. For information on the impact of intermittent net discrete tax items, see “Supplemental Financial Information—Income Tax Matters” herein.

Business Segments

Substantially all of our operating revenues and operating expenses are directly attributable to our business segments. Certain revenues and expenses have been allocated to each business segment, generally in proportion to its respective net revenues, non-interest expenses or other relevant measures.

For an overview of the components of our business segments, net revenues, compensation expense and income taxes, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Business Segments” in the 2019 Form 10-K.

|

| |

| |

| Management’s Discussion and Analysis | |

Institutional Securities

Income Statement Information

|

| | | | | | | | |

| | Three Months Ended

March 31, | |

| $ in millions | 2020 | 2019 | % Change |

| Revenues | | | |

| Investment banking | $ | 1,144 |

| $ | 1,151 |

| (1 | )% |

| Trading | 3,416 |

| 3,130 |

| 9 | % |

| Investments | (25 | ) | 81 |

| (131 | )% |

| Commissions and fees | 874 |

| 621 |

| 41 | % |

| Asset management | 113 |

| 107 |

| 6 | % |

| Other | (1,079 | ) | 222 |

| N/M |

|

| Total non-interest revenues | 4,443 |

| 5,312 |

| (16 | )% |

| Interest income | 2,423 |

| 3,056 |

| (21 | )% |

| Interest expense | 1,961 |

| 3,172 |

| (38 | )% |

| Net interest | 462 |

| (116 | ) | N/M |

|

| Net revenues | 4,905 |

| 5,196 |

| (6 | )% |

| Compensation and benefits | 1,814 |

| 1,819 |

| — | % |

| Non-compensation expenses | 2,141 |

| 1,782 |

| 20 | % |

| Total non-interest expenses | 3,955 |

| 3,601 |

| 10 | % |

| Income before provision for income taxes | 950 |

| 1,595 |

| (40 | )% |

| Provision for income taxes | 151 |

| 190 |

| (21 | )% |

| Net income | 799 |

| 1,405 |

| (43 | )% |

| Net income applicable to noncontrolling interests | 42 |

| 34 |

| 24 | % |

| Net income applicable to Morgan Stanley | $ | 757 |

| $ | 1,371 |

| (45 | )% |

Results in the Institutional Securities business segment reflect constructive markets in January and February 2020 and the significant effects of COVID-19 on markets in March. In particular, in March:

| |

| • | Uncertainty, driven by market volatility and the overall environment, resulted in lower activity in Advisory and Equity underwriting. |

| |

| • | Market volumes and volatility were significantly higher than in the prior year quarter resulting in increased client activity across the Sales and Trading businesses and widened bid-offer spreads. Valuations were negatively impacted, and client balances declined significantly in the Equity Financing business. |

| |

| • | Credit deteriorated rapidly, the results of which are reflected in losses on held-for-sale loans and lending commitments recorded in Other revenues, partially offset by positive hedge results in Other Sales and Trading, aggregating to $610 million for the current quarter; provisions for loan losses recorded in Other revenues, and lending commitments shown in Non-compensation expenses, aggregating to $388 million for the current quarter; Trading losses in certain Credit |

products within Fixed Income; and losses on certain counterparties’ failure to meet margin requirements in Equity sales and trading.

These effects, in the context of the full quarter’s results, are further discussed herein.

Investment Banking

Investment Banking Revenues |

| | | | | | | | |

| | Three Months Ended

March 31, | |

| $ in millions | 2020 | 2019 | % Change |

| Advisory | $ | 362 |

| $ | 406 |

| (11 | )% |

| Underwriting: |

|

| |

| Equity | 336 |

| 339 |

| (1 | )% |

| Fixed income | 446 |

| 406 |

| 10 | % |

| Total Underwriting | 782 |

| 745 |

| 5 | % |

| Total Investment banking | $ | 1,144 |

| $ | 1,151 |

| (1 | )% |

Investment Banking Volumes

|

| | | | | | |

| | Three Months Ended

March 31, |

| $ in billions | 2020 | 2019 |

Completed mergers and acquisitions1 | $ | 109 |

| $ | 195 |

|

Equity and equity-related offerings2, 3 | 13 |

| 14 |

|

Fixed income offerings2, 4 | 82 |

| 58 |

|

Source: Refinitiv data as of April 1, 2020. Transaction volumes may not be indicative of net revenues in a given period. In addition, transaction volumes for prior periods may vary from amounts previously reported due to the subsequent withdrawal, change in value or change in timing of certain transactions.

| |

| 1. | Includes transactions of $100 million or more. Based on full credit to each of the advisors in a transaction. |

| |

| 2. | Based on full credit for single book managers and equal credit for joint book managers. |

| |

| 3. | Includes Rule 144A issuances and registered public offerings of common stock, convertible securities and rights offerings. |

| |

| 4. | Includes Rule 144A and publicly registered issuances, non-convertible preferred stock, mortgage-backed and asset-backed securities, and taxable municipal debt. Excludes leveraged loans and self-led issuances. |

Investment banking revenues of $1,144 million in the current quarter were relatively unchanged from the prior year quarter, reflecting lower results in our advisory business offset by higher results in our fixed income underwriting business.

| |

| • | Advisory revenues decreased in the current quarter primarily as a result of lower volumes of completed M&A activity, particularly large transactions. |

| |

| • | Equity underwriting revenues were relatively unchanged compared with subdued results in the prior year quarter as lower revenues in secondary block share trades were offset by higher revenues in initial public offerings and follow-on offerings. |

|

| |

| |

| Management’s Discussion and Analysis | |

| |

| • | Fixed income underwriting revenues increased in the current quarter primarily due to higher overall volumes compared to the prior year quarter, with higher revenues in investment grade bond and non-investment grade loan issuances, partially offset by lower revenues from investment grade loan issuances. |

See “Investment Banking Volumes” herein.

Sales and Trading Net Revenues

By Income Statement Line Item

|

| | | | | | | | |

| | Three Months Ended

March 31, | |

| $ in millions | 2020 | 2019 | % Change |

| Trading | $ | 3,416 |

| $ | 3,130 |

| 9 | % |

| Commissions and fees | 874 |

| 621 |

| 41 | % |

| Asset management | 113 |

| 107 |

| 6 | % |

| Net interest | 462 |

| (116 | ) | N/M |

|

| Total | $ | 4,865 |

| $ | 3,742 |

| 30 | % |

By Business

|

| | | | | | | | |

| | Three Months Ended

March 31, | |

| | |

| $ in millions | 2020 | 2019 | % Change |

| Equity | $ | 2,422 |

| $ | 2,015 |

| 20 | % |

| Fixed Income | 2,203 |

| 1,710 |

| 29 | % |

| Other | 240 |

| 17 |

| N/M |

|

| Total | $ | 4,865 |

| $ | 3,742 |

| 30 | % |

Sales and Trading Revenues—Equity and Fixed Income

|

| | | | | | | | | | | | |

| | Three Months Ended

March 31, 2020 |

| | | | Net | |

| $ in millions | Trading | Fees1 | Interest2 | Total |

| Financing | $ | 1,034 |

| $ | 101 |

| $ | (37 | ) | $ | 1,098 |

|

| Execution services | 579 |

| 783 |

| (38 | ) | 1,324 |

|

| Total Equity | $ | 1,613 |

| $ | 884 |

| $ | (75 | ) | $ | 2,422 |

|

| Total Fixed Income | $ | 1,773 |

| $ | 102 |

| $ | 328 |

| $ | 2,203 |

|

|

| | | | | | | | | | | | |

| | Three Months Ended

March 31, 2019 |

| | | | Net | |

| $ in millions | Trading | Fees1 | Interest2 | Total |

| Financing | $ | 1,115 |

| $ | 98 |

| $ | (258 | ) | $ | 955 |

|

| Execution services | 551 |

| 553 |

| (44 | ) | 1,060 |

|

| Total Equity | $ | 1,666 |

| $ | 651 |

| $ | (302 | ) | $ | 2,015 |

|

| Total Fixed Income | $ | 1,727 |

| $ | 78 |

| $ | (95 | ) | $ | 1,710 |

|

| |

| 1. | Includes Commissions and fees and Asset management revenues. |

| |

| 2. | Includes funding costs, which are allocated to the businesses based on funding usage. |

Equity

Equity sales and trading net revenues of $2,422 million in the current quarter increased 20% from the prior year quarter, reflecting higher results in both our financing and execution services businesses.

| |

| • | Financing increased from the prior year quarter, primarily due to higher average client balances, partially offset by the impact of reduced dividend expectations on the valuation of certain hedges. Net interest increased reflecting a reduction in funding costs. |

| |

| • | Execution services increased from the prior year quarter, reflecting an increase in market volumes in cash equities resulting in higher Commissions and fees, and higher client trading activity in derivatives products, which was partially offset by the impact of losses on certain counterparties’ failure to meet margin requirements and the impact of reduced dividend expectations on derivative valuations. |

Fixed Income

Fixed Income sales and trading net revenues of $2,203 million in the current quarter were 29% higher than the prior year quarter, primarily driven by higher results in global macro products, partially offset by lower results in credit products.

| |

| • | Global macro products Trading revenues increased primarily due to higher client activity in both foreign exchange and rates products, and the widening of bid-offer spreads from higher market volatility. Higher average balances and lower funding costs contributed to an increase in Net interest revenues. |

| |

| • | Credit products Trading revenues decreased primarily due to the widening of credit spreads which resulted in losses in securitized products and municipal securities, partially offset by increased revenues from client activity in corporate credit products from higher volumes and widening bid-offer spreads. Net interest revenues increased, primarily driven by higher spreads on Agency products and higher average balances in secured lending facilities. |

| |

| • | Trading revenues from Commodities products and Other decreased as a result of lower client structuring activity within derivatives counterparty credit risk management, partially offset by improved inventory management in commodities due to higher market volatility in energy and metals. Net interest revenues increased, reflecting lower funding costs. |

Other

| |

| • | Other sales and trading revenues of $240 million in the current quarter increased from the prior year quarter reflecting gains on hedges associated with loans and lending commitments compared with losses in the prior year quarter, partially offset by losses related to investments associated with certain employee deferred cash-based compensation plans. |

|

| |

| |

| Management’s Discussion and Analysis | |

Investments, Other Revenues, Non-interest Expenses, and Income Tax Items

Investments

| |

| • | Net investment losses of $25 million in the current quarter compared to gains in the prior year quarter, were primarily driven by losses in the current quarter on an energy-related investment and lower revenues from fund-related distributions. |

Other Revenues

| |

| • | Other net losses of $1,079 million in the current quarter were primarily as a result of mark-to-market losses on loans and lending commitments held for sale due to the widening of credit spreads, compared with gains in the prior year quarter, as well as an increase in the provision for credit losses on loans held for investment. |

Non-interest Expenses

Non-interest expenses of $3,955 million in the current quarter increased from the prior year quarter, primarily reflecting a 20% increase in Non-compensation expenses.

| |

| • | Compensation and benefits expenses remained relatively unchanged in the current quarter as the benefit from a decrease in the fair value of investments to which certain deferred compensation plans are referenced was offset by an increase in discretionary incentive compensation reflecting baseline annual compensation estimates, exclusive of the benefit noted. |

| |

| • | Non-compensation expenses increased in the current quarter primarily due to higher volume-related expenses as well as an increase in the provision for credit losses for lending commitments held for investment. |

Income Tax Items

Intermittent net discrete tax benefits of $101 million were recognized in Provision for income taxes in the prior year quarter. For further information, see “Supplemental Financial Information—Income Tax Matters” herein.

|

| |

| |

| Management’s Discussion and Analysis | |

Income Statement Information

|

| | | | | | | | |

| | Three Months Ended

March 31, | |

| $ in millions | 2020 | 2019 | % Change |

| Revenues | | | |

| Investment banking | $ | 158 |

| $ | 109 |

| 45 | % |

| Trading | (347 | ) | 302 |

| N/M |

|

| Investments | — |

| 1 |

| (100 | )% |

| Commissions and fees | 588 |

| 406 |

| 45 | % |

| Asset management | 2,680 |

| 2,361 |

| 14 | % |

| Other | 62 |

| 80 |

| (23 | )% |

| Total non-interest revenues | 3,141 |

| 3,259 |

| (4 | )% |

| Interest income | 1,193 |

| 1,413 |

| (16 | )% |

| Interest expense | 297 |

| 283 |

| 5 | % |

| Net interest | 896 |

| 1,130 |

| (21 | )% |

| Net revenues | 4,037 |

| 4,389 |

| (8 | )% |

| Compensation and benefits | 2,212 |

| 2,462 |

| (10 | )% |

| Non-compensation expenses | 770 |

| 739 |

| 4 | % |

| Total non-interest expenses | 2,982 |

| 3,201 |

| (7 | )% |

| Income before provision for income taxes | $ | 1,055 |

| $ | 1,188 |

| (11 | )% |

| Provision for income taxes | 191 |

| 264 |

| (28 | )% |

| Net income applicable to Morgan Stanley | $ | 864 |

| $ | 924 |

| (6 | )% |

Results in the Wealth Management business segment reflect the significant effects of COVID-19 on the economy and markets in March 2020. In particular, in March:

| |

| • | The decline in global asset prices contributed to losses on investments associated with certain employee deferred cash-based compensation plans of $426 million in the current quarter. |

| |

| • | Already elevated market volumes and volatility compared to the prior year quarter increased further, resulting in increased commissions from client activity. |

These effects, in the context of the full quarter’s results, are further discussed herein.

Financial Information and Statistical Data

|

| | | | | | |

| | At

March 31,

2020 | At

December 31,

2019 |

| $ in billions, except employee data |

| Client assets | $ | 2,397 |

| $ | 2,700 |

|

Fee-based client assets1 | $ | 1,134 |

| $ | 1,267 |

|

| Fee-based client assets as a percentage of total client assets | 47 | % | 47 | % |

Client liabilities2 | $ | 92 |

| $ | 90 |

|

| Investment securities portfolio | $ | 75.5 |

| $ | 67.2 |

|

| Loans and lending commitments | $ | 95.9 |

| $ | 93.2 |

|

| Wealth Management representatives | 15,432 |

| 15,468 |

|

|

| | | | | | |

| | Three Months Ended

March 31, |

| | 2020 | 2019 |

| Per representative: | | |

Annualized revenues ($ in thousands)3 | $ | 1,045 |

| $ | 1,118 |

|

Client assets ($ in millions)4 | $ | 155 |

| $ | 158 |

|

Fee-based asset flows ($ in billions)5 | $ | 18.4 |

| $ | 14.8 |

|

| |

| 1. | Fee-based client assets represent the amount of assets in client accounts where the fee for services is calculated based on those assets. |

| |

| 2. | Client liabilities include securities-based and tailored lending, residential real estate loans and margin lending. |

| |

| 3. | Revenues per representative equal Wealth Management’s annualized net revenues divided by the average number of representatives. |

| |

| 4. | Client assets per representative equal total period-end client assets divided by period-end number of representatives. |

| |

| 5. | For a description of the Inflows and Outflows included within Fee-based asset flows, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Business Segments—Wealth Management—Fee-Based Client Assets” in the 2019 Form 10-K. Excludes institutional cash management-related activity. |

Transactional Revenues

|

| | | | | | | | |

| | Three Months Ended

March 31, | |

| $ in millions | 2020 | 2019 | % Change |

| Investment banking | $ | 158 |

| $ | 109 |

| 45 | % |

| Trading | (347 | ) | 302 |

| N/M |

|

| Commissions and fees | 588 |

| 406 |

| 45 | % |

| Total | $ | 399 |

| $ | 817 |

| (51 | )% |

| Transactional revenues as a % of Net revenues | 10 | % | 19 | % | |

|

| |

| |

| Management’s Discussion and Analysis | |

Net Revenues

Transactional Revenues

Transactional revenues of $399 million in the current quarter decreased 51% from the prior year quarter as negative Trading revenues were partially offset by higher Commissions and fees and Investment banking revenues.

| |

| • | Investment banking revenues increased in the current quarter primarily due to higher revenues from structured products and closed-end fund issuances. |

| |

| • | Trading revenues decreased in the current quarter principally due to losses related to investments associated with certain employee deferred cash-based compensation plans, compared with gains in the prior year quarter. |

| |

| • | Commissions and fees increased in the current quarter primarily due to increased client activity in equities. |

Asset Management

Asset management revenues of $2,680 million in the current quarter increased 14% from the prior year quarter primarily due to higher fee-based assets levels at the beginning of the monthly billing cycles in 2020 due to market appreciation and positive net flows, partially offset by lower average fee rates.

See “Fee-Based Client Assets—Rollforwards” herein.

Other

Other revenues of $62 million in the current quarter decreased 23% from the prior year quarter primarily due to an increase in the provision for credit losses.

Net Interest

Net interest of $896 million in the current quarter decreased 21% from the prior year quarter primarily due to lower interest rates on Loans and the investment portfolio, changes in our funding mix, and higher prepayment amortization expense related to mortgage-backed securities. These decreases were partially offset by the impact of lower rates paid on brokerage sweep deposits and higher Loan balances.

Non-interest Expenses

Non-interest expenses of $2,982 million in the current quarter decreased 7% from the prior year quarter primarily as a result of lower Compensation and benefits expenses, partially offset by higher Non-compensation expenses.

| |

| • | Compensation and benefits expenses decreased in the current quarter, primarily due to decreases in the fair value of investments to which certain deferred compensation plans are referenced, partially offset by an increase in the formulaic |

payout to Wealth Management representatives driven by the mix of revenues.

| |

| • | Non-compensation expenses increased in the current quarter primarily due to incremental expenses related to Solium Capital, Inc., which was acquired in the second quarter of 2019. |

Fee-Based Client Assets

Rollforwards

|

| | | | | | | | | | | | | | | |

| $ in billions | At

December 31,

2019 | Inflows | Outflows | Market Impact | At

March 31,

2020 |

Separately managed1 | $ | 322 |

| $ | 12 |

| $ | (7 | ) | $ | 2 |

| $ | 329 |

|

| Unified managed | 313 |

| 16 |

| (13 | ) | (53 | ) | 263 |

|

| Advisor | 155 |

| 10 |

| (9 | ) | (25 | ) | 131 |

|

| Portfolio manager | 435 |

| 27 |

| (18 | ) | (65 | ) | 379 |

|

| Subtotal | $ | 1,225 |

| $ | 65 |

| $ | (47 | ) | $ | (141 | ) | $ | 1,102 |

|

| Cash management | 42 |

| 4 |

| (14 | ) | — |

| 32 |

|

| Total fee-based client assets | $ | 1,267 |

| $ | 69 |

| $ | (61 | ) | $ | (141 | ) | $ | 1,134 |

|

|

| | | | | | | | | | | | | | | |

| $ in billions | At

December 31,

2018 | Inflows | Outflows | Market Impact | At

March 31,

2019 |

Separately managed1 | $ | 279 |

| $ | 14 |

| $ | (5 | ) | $ | (12 | ) | $ | 276 |

|

| Unified managed | 257 |

| 13 |

| (11 | ) | 24 |

| 283 |

|

| Advisor | 137 |

| 8 |

| (9 | ) | 11 |

| 147 |

|

| Portfolio manager | 353 |

| 19 |

| (14 | ) | 33 |

| 391 |

|

| Subtotal | $ | 1,026 |

| $ | 54 |

| $ | (39 | ) | $ | 56 |

| $ | 1,097 |

|

| Cash management | 20 |

| 4 |

| (5 | ) | — |

| 19 |

|

| Total fee-based client assets | $ | 1,046 |

| $ | 58 |

| $ | (44 | ) | $ | 56 |

| $ | 1,116 |

|

Average Fee Rates

|

| | | | |

| | Three Months Ended

March 31, |

| Fee rate in bps | 2020 | 2019 |

| Separately managed | 14 |

| 14 |

|

| Unified managed | 99 |

| 101 |

|

| Advisor | 85 |

| 88 |

|

| Portfolio manager | 94 |

| 96 |

|

| Subtotal | 72 |

| 74 |

|

| Cash management | 5 |

| 6 |

|

| Total fee-based client assets | 71 |

| 73 |

|

| |

| 1. | Includes non-custody account values reflecting prior quarter-end balances due to a lag in the reporting of asset values by third-party custodians. |

For a description of fee-based client assets and rollforward items in the previous tables, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Business Segments—Wealth Management—Fee-Based Client Assets” in the 2019 Form 10-K.

|

| |

| |

| Management’s Discussion and Analysis | |

Investment Management

Income Statement Information

|

| | | | | | | | |

| | Three Months Ended

March 31, | |

| $ in millions | 2020 | 2019 | % Change |

| Revenues | | |

|

| Trading | $ | (37 | ) | $ | (3 | ) | N/M |

|

| Investments | 63 |

| 191 |

| (67 | )% |

| Asset management | 665 |

| 617 |

| 8 | % |

| Other | 7 |

| 3 |

| 133 | % |

| Total non-interest revenues | 698 |

| 808 |

| (14 | )% |

| Interest income | 8 |

| 4 |

| 100 | % |

| Interest expense | 14 |

| 8 |

| 75 | % |

| Net interest | (6 | ) | (4 | ) | (50 | )% |

| Net revenues | 692 |

| 804 |

| (14 | )% |

| Compensation and benefits | 257 |

| 370 |

| (31 | )% |

| Non-compensation expenses | 292 |

| 260 |

| 12 | % |

| Total non-interest expenses | 549 |

| 630 |

| (13 | )% |

| Income before provision for income taxes | 143 |

| 174 |

| (18 | )% |

| Provision for income taxes | 25 |

| 33 |

| (24 | )% |

| Net income | 118 |

| 141 |

| (16 | )% |

| Net income applicable to noncontrolling interests | 40 |

| 5 |

| N/M |

|

| Net income applicable to Morgan Stanley | $ | 78 |

| $ | 136 |

| (43 | )% |

Results in the Investment Management business segment reflect the significant effects of COVID-19 on the economy and markets in March 2020. In particular, in March:

| |

| • | The decline in global asset prices led to losses of $326 million in the current quarter related to the reversal of accrued carried interest, and losses on investments in certain of our funds, net of economic hedges, and net losses in Trading revenues. |

These effects, in the context of the full quarter’s results, are further discussed herein.

Net Revenues

Investments

Investments revenues of $63 million in the current quarter decreased 67% from the prior year quarter primarily as a result of the reversal of accrued carried interest and investment losses in certain private equity, real estate, and infrastructure funds and losses on seed investments in certain funds. Partially offsetting these decreases were higher carried interest and investment gains in an Asia private equity fund, principally driven by gains from an underlying investment, which is subject to certain sales restrictions.

Asset Management

Asset management revenues of $665 million in the current quarter increased 8% from the prior year quarter primarily as a result of higher average AUM.

See “Assets Under Management or Supervision” herein.

Non-interest Expenses

Non-interest expenses of $549 million in the current quarter decreased 13% from the prior year quarter primarily as a result of lower compensation and benefits expenses, partially offset by higher non-compensation expenses.

| |

| • | Compensation and benefits expenses decreased in the current quarter primarily due to lower compensation associated with carried interest and a decrease in the fair value of investments to which certain deferred compensation plans are referenced. |

| |

| • | Non-compensation expenses in the current quarter increased from the prior year quarter primarily as a result of higher fee sharing paid to intermediaries driven by higher average AUM. |

|

| |

| |

| Management’s Discussion and Analysis | |

Assets Under Management or Supervision

Rollforwards

|

| | | | | | | | | | | | | | | | | | |

| $ in billions | At

December 31, 2019 | Inflows | Outflows | Market Impact | Other | At

March 31,

2020 |

| Equity | $ | 138 |

| $ | 14 |

| $ | (12 | ) | $ | (18 | ) | $ | (1 | ) | $ | 121 |

|

| Fixed income | 79 |

| 10 |

| (9 | ) | (4 | ) | (1 | ) | 75 |

|

| Alternative/Other | 139 |

| 8 |

| (4 | ) | (7 | ) | 5 |

| 141 |

|

| Long-term AUM subtotal | 356 |

| 32 |

| (25 | ) | (29 | ) | 3 |

| 337 |

|

| Liquidity | 196 |

| 446 |

| (395 | ) | 1 |

| (1 | ) | 247 |

|

| Total AUM | $ | 552 |

| $ | 478 |

| $ | (420 | ) | $ | (28 | ) | $ | 2 |

| $ | 584 |

|

| Shares of minority stake assets | 6 |

| | | | | 6 |

|

|

| | | | | | | | | | | | | | | | | | |

| $ in billions | At

December 31, 2018 | Inflows | Outflows | Market Impact | Other | At

March 31,

2019 |

| Equity | $ | 103 |

| $ | 9 |

| $ | (8 | ) | $ | 16 |

| $ | — |

| $ | 120 |

|

| Fixed income | 68 |

| 6 |

| (7 | ) | 1 |

| — |

| 68 |

|

| Alternative/Other | 128 |

| 5 |

| (4 | ) | 5 |

| (1 | ) | 133 |

|

| Long-term AUM subtotal | 299 |

| 20 |

| (19 | ) | 22 |

| (1 | ) | 321 |

|

| Liquidity | 164 |

| 343 |

| (348 | ) | 1 |

| (1 | ) | 159 |

|

| Total AUM | $ | 463 |

| $ | 363 |

| $ | (367 | ) | $ | 23 |

| $ | (2 | ) | $ | 480 |

|

| Shares of minority stake assets | 7 |

| | | | | 6 |

|

Average AUM

|

| | | | | | |

| | Three Months Ended

March 31, |

| $ in billions | 2020 | 2019 |

| Equity | $ | 133 |

| $ | 113 |

|

| Fixed income | 79 |

| 68 |

|

| Alternative/Other | 139 |

| 131 |

|

| Long-term AUM subtotal | 351 |

| 312 |

|

| Liquidity | 206 |

| 163 |

|

| Total AUM | $ | 557 |

| $ | 475 |

|

| Shares of minority stake assets | 6 |

| 6 |

|

Average Fee Rates

|

| | | |

| | Three Months Ended

March 31, |

| Fee rate in bps | 2020 | 2019 |

| Equity | 77 |

| 76 |

| Fixed income | 31 |

| 32 |

| Alternative/Other | 60 |

| 68 |

| Long-term AUM | 60 |

| 63 |

| Liquidity | 17 |

| 17 |

| Total AUM | 44 |

| 47 |

For a description of the asset classes and rollforward items in the previous tables, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Business Segments—Investment Management—Assets Under Management or Supervision” in the 2019 Form 10-K.

|

| |

| |

| Management’s Discussion and Analysis | |

Supplemental Financial Information

Income Tax Matters

Effective Tax Rate from Continuing Operations

|

| | | | | | |

| | Three Months Ended

March 31, |

| $ in millions | 2020 | 2019 |

| U.S. GAAP | 17.1 | % | 16.5 | % |

Adjusted effective income tax rate—non-GAAP1 | 18.5 | % | 19.9 | % |

| Net discrete tax provisions/(benefits) | | |

Recurring2 | $ | (99 | ) | $ | (107 | ) |

Intermittent3 | $ | (31 | ) | $ | (101 | ) |

| |

| 1. | The adjusted effective income tax rate is a non-GAAP measure that excludes net discrete tax provisions (benefits) that are intermittent and includes those that are recurring. For further information on non-GAAP measures, see “Selected Non-GAAP Financial Information” herein. |

| |

| 2. | Provisions (benefits) related to conversion of employee share-based awards are expected to occur every year and, as such, are considered recurring discrete tax items. |

| |

| 3. | Includes all tax provisions (benefits) that have been determined to be discrete, other than Recurring items as defined above. |

The current quarter includes intermittent net discrete tax benefits associated with the remeasurement of prior years’ tax liabilities. The prior year quarter includes intermittent net discrete tax benefits primarily associated with remeasurement of reserves and related interest as a result of new information pertaining to the resolution of multi-jurisdiction tax examinations. See Note 18 to the financial statements for further information.

U.S. Bank Subsidiaries

Our U.S. bank subsidiaries, Morgan Stanley Bank N.A. (“MSBNA”) and Morgan Stanley Private Bank, National Association (“MSPBNA”) (collectively, “U.S. Bank Subsidiaries”) accept deposits; provide loans to a variety of customers, from large corporate and institutional clients to high net worth individuals; and invest in securities. Lending activity recorded in the U.S. Bank subsidiaries from the Institutional Securities business segment primarily includes loans and lending commitments to corporate clients. Lending activity recorded in the U.S. Bank subsidiaries from the Wealth Management business segment primarily includes securities-based lending, which allows clients to borrow money against the value of qualifying securities, and residential real estate loans.

For a further discussion of our credit risks, see “Quantitative and Qualitative Disclosures about Risk—Credit Risk.” For a further discussion about loans and lending commitments, see Notes 9 and 13 to the financial statements.

U.S. Bank Subsidiaries’ Supplemental Financial Information1

|

| | | | | | |

| $ in billions | At

March 31,

2020 | At

December 31,

2019 |

| Assets | $ | 265.4 |

| $ | 219.6 |

|

| Investment securities portfolio: | | |

| Investment securities—AFS | 49.0 |

| 42.4 |

|

| Investment securities—HTM | 28.7 |

| 26.1 |

|

| Total investment securities | $ | 77.7 |

| $ | 68.5 |

|

Deposits2 | $ | 234.1 |

| $ | 189.3 |

|

| Wealth Management Loans |

Securities-based lending and other3 | $ | 51.4 |

| $ | 49.9 |

|

| Residential real estate | 31.1 |

| 30.2 |

|

| Total | $ | 82.5 |

| $ | 80.1 |

|

| Institutional Securities Loans |

Corporate4: | | |

| Corporate relationship and event-driven lending | $ | 15.4 |

| $ | 5.6 |

|

| Secured lending facilities | 28.4 |

| 26.8 |

|

| Securities-based lending and other | 5.1 |

| 5.4 |

|

| Commercial and residential real estate | 10.3 |

| 12.0 |

|

| Total | $ | 59.2 |

| $ | 49.8 |

|

| |

| 1. | Amounts exclude transactions between the bank subsidiaries, as well as deposits from the Parent Company and affiliates. |

| |

| 2. | For further information on deposits, see “Liquidity and Capital Resources—Funding Management—Unsecured Financing” herein. |

| |

| 3. | Other loans primarily include tailored lending. |

| |

| 4. | For a further discussion of corporate loans in the Institutional Securities business segment, see “Credit Risk—Institutional Securities Corporate Loans” herein. |

Other Matters

Planned Acquisition of E*TRADE

On February 20, 2020, we entered into a definitive agreement under which we will acquire E*TRADE Financial Corporation (“E*TRADE”) in an all-stock transaction. In the current quarter, we filed our application with the Federal Reserve and in early April the Hart-Scott-Rodino Antitrust waiting period expired. The acquisition is subject to customary closing conditions, including regulatory approvals and approval by E*TRADE shareholders, and we continue to expect the acquisition to close in the fourth quarter of 2020.

Accounting Development Updates

The Financial Accounting Standards Board has issued certain accounting updates that apply to us. Accounting updates not listed below were assessed and either determined to be not applicable or are not expected to have a significant impact on our financial statements.

|

| |

| |

| Management’s Discussion and Analysis | |

The following accounting update is currently being evaluated to determine the potential impact of adoption:

| |

| • | Reference Rate Reform. This accounting update provides optional accounting relief to entities with contracts, hedge accounting relationships or other transactions that reference LIBOR or other interest rate benchmarks for which the referenced rate is expected to be discontinued or replaced. This optional relief generally allows for contract modifications solely related to the replacement of the reference rate to be accounted for as a continuation of the existing contract instead of as an extinguishment of the contract, and would therefore not trigger certain accounting impacts that would otherwise be required. The relief also allows entities to change certain critical terms of existing hedge accounting relationships that are affected by reference rate reform, and these changes would not require de-designating the hedge accounting relationship. The optional relief can be applied beginning January 1, 2020, and ending December 31, 2022. We plan to apply the accounting relief as relevant contract and hedge accounting relationship modifications are made during the course of the reference rate reform transition period. |

Critical Accounting Policies

Our financial statements are prepared in accordance with U.S. GAAP, which requires us to make estimates and assumptions (see Note 1 to the financial statements). We believe that of our significant accounting policies (see Note 2 to the financial statements in the 2019 Form 10-K and Note 2 to the financial statements), the fair value, goodwill and intangible assets, legal and regulatory contingencies and income taxes policies involve a higher degree of judgment and complexity. For a further discussion about our critical accounting policies, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies” in the 2019 Form 10-K.

Liquidity and Capital Resources

Senior management, with oversight by the Asset/Liability Management Committee and the Board of Directors (“Board”), establishes and maintains our liquidity and capital policies. Through various risk and control committees, senior management reviews business performance relative to these policies, monitors the availability of alternative sources of financing, and oversees the liquidity, interest rate and currency sensitivity of our asset and liability position. Our Treasury department, Firm Risk Committee, Asset/Liability Management Committee, and other committees and control groups assist in evaluating, monitoring and controlling the impact that our business activities have on our balance sheet, liquidity and capital structure. Liquidity and capital matters are reported regularly to the Board and the Risk Committee of the Board.

Balance Sheet

We monitor and evaluate the composition and size of our balance sheet on a regular basis. Our balance sheet management process includes quarterly planning, business-specific thresholds, monitoring of business-specific usage versus key performance metrics and new business impact assessments.

We establish balance sheet thresholds at the consolidated and business segment levels. We monitor balance sheet utilization and review variances resulting from business activity and market fluctuations. On a regular basis, we review current performance versus established thresholds and assess the need to re-allocate our balance sheet based on business unit needs. We also monitor key metrics, including asset and liability size and capital usage.

Total Assets by Business Segment

|

| | | | | | | | | | | | |

| | At March 31, 2020 |

| $ in millions | IS | WM | IM | Total |

| Assets |

|

|

|

|

| Cash and cash equivalents | $ | 101,615 |

| $ | 29,803 |

| $ | 91 |

| $ | 131,509 |

|

| Trading assets at fair value | 266,781 |

| 389 |

| 3,746 |

| 270,916 |

|

| Investment securities | 40,662 |

| 75,495 |

| — |

| 116,157 |

|

| Securities purchased under agreements to resell | 88,008 |

| 16,792 |

| — |

| 104,800 |

|

| Securities borrowed | 71,826 |

| 474 |

| — |

| 72,300 |

|

| Customer and other receivables | 58,523 |

| 15,216 |

| 685 |

| 74,424 |

|

Loans1 | 66,171 |

| 82,516 |

| 10 |

| 148,697 |

|

Other assets2 | 13,903 |

| 13,139 |

| 1,950 |

| 28,992 |

|

| Total assets | $ | 707,489 |

| $ | 233,824 |

| $ | 6,482 |

| $ | 947,795 |

|

|

| | | | | | | | | | | | |

| | At December 31, 2019 |

| $ in millions | IS | WM | IM | Total |

| Assets | | | | |

| Cash and cash equivalents | $ | 67,657 |

| $ | 14,247 |

| $ | 267 |

| $ | 82,171 |

|

| Trading assets at fair value | 293,477 |

| 47 |

| 3,586 |

| 297,110 |

|

| Investment securities | 38,524 |

| 67,201 |

| — |

| 105,725 |

|

| Securities purchased under agreements to resell | 80,744 |

| 7,480 |

| — |

| 88,224 |

|

| Securities borrowed | 106,199 |

| 350 |

| — |

| 106,549 |

|

| Customer and other receivables | 39,743 |

| 15,190 |

| 713 |

| 55,646 |

|

Loans1 | 50,557 |

| 80,075 |

| 5 |

| 130,637 |

|

Other assets2 | 14,300 |

| 13,092 |

| 1,975 |

| 29,367 |

|

| Total assets | $ | 691,201 |

| $ | 197,682 |

| $ | 6,546 |

| $ | 895,429 |

|

IS—Institutional Securities

WM—Wealth Management

IM—Investment Management

| |

| 1. | Amounts include loans held for investment, net of allowance, and loans held for sale but exclude loans at fair value, which are included in Trading assets in the balance sheets (see Note 9 to the financial statements). |

| |

| 2. | Other assets primarily includes Goodwill and Intangible assets, premises, equipment and software, ROU assets related to leases, other investments, and deferred tax assets. |

A substantial portion of total assets consists of liquid marketable securities and short-term receivables arising principally from sales and trading activities in the Institutional Securities

|

| |

| |

| Management’s Discussion and Analysis | |

business segment. Total assets increased to $948 billion at March 31, 2020 from $895 billion at December 31, 2019.

Within Wealth Management, assets increased in the investment portfolio comprising Cash and cash equivalents, Investment securities and Securities purchased under agreements to resell, as a result of significantly higher deposits in this segment, and loans continued to grow.

Institutional Securities’ assets were also higher reflecting increases within Cash and cash equivalents, primarily due to higher initial margin related to derivatives; Customer and other receivables, resulting from higher volumes of unsettled transactions in line with market conditions; and loan growth in March in support of client needs. Additionally, within Institutional Securities, Trading assets and Securities borrowed decreased, predominantly driven by corporate equities as the markets declined. The decrease in Trading assets includes a partial offset related to increased derivative exposures related to market volatility.

Liquidity Risk Management Framework

The core components of our Liquidity Risk Management Framework are the Required Liquidity Framework, Liquidity Stress Tests and Liquidity Resources, which support our target liquidity profile. For a further discussion about the Firm’s Required Liquidity Framework and Liquidity Stress Tests, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Liquidity Risk Management Framework” in the 2019 Form 10-K.

At March 31, 2020 and December 31, 2019, we maintained sufficient liquidity to meet current and contingent funding obligations as modeled in our Liquidity Stress Tests.

Liquidity Resources