UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07390 |

|

Boulder Total Return Fund, Inc. |

(Exact name of registrant as specified in charter) |

|

Fund Administrative Services 2344 Spruce Street, Suite A Boulder, CO | | 80302 |

(Address of principal executive offices) | | (Zip code) |

|

Fund Administrative Services 2344 Spruce Street, Suite A Boulder, CO 80302 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (303) 444-5483 | |

|

Date of fiscal year end: | November 30, 2009 | |

|

Date of reporting period: | May 31, 2009 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The Report to Stockholders is attached herewith.

BOULDER TOTAL RETURN FUND, INC.

TABLE OF CONTENTS

LETTER FROM THE ADVISERS |

|

Dear Shareholder:

The Boulder Total Return Fund (BTF) had a total return of -1.1% based on its net asset value (NAV) for the 6-months ending 05/31/2009. The total return based on BTF’s market price for the same period was 4.0%. The S&P 500 Index was up 4.1% over the same period.

| | 3 Months | | 6 Months | | One Year | | Three Years* | | Five Years* | | Since | |

| | Ended | | Ended | | Ended | | Ended | | Ended | | August | |

Cumulative Returns | | 5/31/09 | | 5/31/09 | | 5/31/09 | | 5/31/09 | | 5/31/09 | | 1999** | |

Boulder Total Return Fund (NAV) | | 31.2 | % | (1.1 | )% | (37.6 | )% | (10.0 | )% | (3.5 | )% | 2.5 | % |

S&P 500 Index | | 25.8 | % | 4.1 | % | (32.6 | )% | (8.3 | )% | (1.9 | )% | (1.9 | )% |

Dow Jones Industrial Average | | 21.3 | % | (2.0 | )% | (30.4 | )% | (6.2 | )% | (1.1 | )% | (0.3 | )% |

NASDAQ Composite | | 29.1 | % | 16.2 | % | (28.9 | )% | (5.8 | )% | (1.4 | )% | (3.8 | )% |

The total returns for BTF in the table above do not include the affect of dilution from the 7/2003 rights offering. If the affect of dilution is included, the annualized return since August 1999 would be 1.7%.

* | Annualized |

** | Annualized since August 1999, when the current Advisers became investment advisers to the Fund. |

You can see in the table above that BTF had a big return in the latest fiscal quarter. This good quarter made up for nearly all of the losses that it incurred in the 1st quarter of this fiscal year. In the first quarter ended 2/28/09, BTF had a total return on NAV of -24.7%. If you’ve done the simple arithmetic, you may be scratching your head saying, “why wasn’t the return for the 6 months positive since the Fund was up 31.2% in the second three month period while it was only down 24.7% in the first three months?” The simple answer is that it’s not simple arithmetic. Returns are compounded. That is why our first rule of investing “Don’t lose what you already have” is so important. Think about it this way: If you have $1.00 and you lose $.50, your return is -50%. But in order to get back to where you started, you’re going to need a return of 100%.

These huge swings in returns give an indication of the huge volatility in the markets. Obviously we suffered with the rest of the market. We wish we could have avoided the downturn and kept what we had in tact, but we’re not smart enough to know when the market will rise and fall. We try to find long-term investments that will: 1) survive in even the most severe economic downturns such as the one we had, and are currently witnessing, and 2) provide good returns when the economy is on cruise control.

5.31.09  SEMI-ANNUAL REPORT

SEMI-ANNUAL REPORT

1

A $10,000 investment in BTF at NAV when BIA and SIA became co-advisers to the Fund in August, 1999 would be worth $12,780 on May 31, 2009. Had the investor purchased the S&P 500 Index at the same time, he’d have less than he started with— only $8,270. So after expenses (and assuming no expenses on the S&P), an investor would have 54% more money having purchased BTF.

Looking at the Fund’s investments, its largest one, Berkshire Hathaway, was down (11.9%) in the 6 months ending 5/31/09. But leading the pack performance-wise was BTF’s second largest position, YUM! Brands, up 30.2% during the 6 months. YUM has grown to be over 16% of the Fund’s assets due to capital appreciation; when we bought YUM back in 2000 it was less than 5% of BTF’s assets. We’re still quite happy to hold on to this fast food restaurant gem. Some other significant positions in the Fund are WalMart, down (9.6%), Eaton Corp, down (4%), and Cheung Kong Holdings, up 31%.

We are finding some places to put your money to work at what we believe are good prices. Yet, we’re not convinced that we’ve seen the bottom, so we continue to be very cautious before making new commitments or adding to some good companies we already own. At this point, we do not anticipate a quick end to the worldwide economic crisis and the cash we hold makes us feel quite comfortable.

When making additional equity investments, we continue to try to estimate what effect inflation will have on them. With the U.S. Treasury issuing debt at an unprecedented rate, and the Federal Reserve continuing to monetize it, we think there is a high probability of increasing inflation; but we have no idea how soon such inflation will occur. What we can tell you for certain is we won’t pay a price we don’t think is reasonable. We’d rather be patient with your money. This economy is by no means out of the woods yet; there are potential dark clouds on the horizon. The State of California is in a sorry state. How would you like to get an IOU for your State income tax refund? Try taking that to the grocery store. Other state and local governments across the nation are also hurting.

But there are still bargains to be found. We have been buying other closed-end funds trading at discounts to their NAV’s which more than offsets the expenses and provides us with income through a diversified portfolio. For the most part, the funds we bought specialize in REITs, utilities and/or preferreds. All of the funds we bought pay a regular monthly or quarterly dividend. If the underlying assets in these funds recover, we may have the chance to double-dip in our returns if the discounts narrow at the same time.

BOULDER TOTAL RETURN FUND, INC. www.boulderfunds.net

2

The Fund holds cash and “cash-equivalents” totaling about $24 million, or about 10% of the Fund’s assets as of 5/31/09. Included in the cash-equivalents are Auction Rate Preferreds (“ARPs”) issued by other closed-end funds. The Fund holds a total of $2.1 million par value of these preferred instruments (which are currently fair valued at 98% of par). One year ago, the Fund held $12.2 million of these securities. Since then, many funds have redeemed their ARPs at their full stated par value. We consider these somewhat frozen assets (the auctions continue to fail) to be good assets – that is to say, they are still rated “AAA” and continue paying dividends. In fact, we recently read that we can expect another $1.9 million in redemptions this July, which would leave BTF holding only $200,000 worth of ARPs.

Our website at www.boulderfunds.net is an excellent source for information on the Fund. One of the features on the website is the ability to sign up for electronic delivery of stockholder information. Through electronic delivery, you can enjoy the convenience of receiving and viewing stockholder communications, such as annual reports, managed distribution information, and proxy statements online in addition to, but more quickly than, the hard copies you currently receive in the mail. To enroll, simply go to www.boulderfunds.net/enotify.htm. You will also find information about the Boulder Total Return Fund’s sister fund – the Boulder Growth & Income Fund – on the website.

Sincerely, | | |

| |

|

Stewart R. Horejsi | | Carl D. Johns |

Stewart Investment Advisers | | Boulder Investment Advisers, LLC |

Barbados, W.I. | | Boulder, Colorado |

3

| FINANCIAL DATA [Unaudited] |

| | Per Share of Common Stock | |

| | Net Asset | | NYSE | | Dividend | |

| | Value | | Closing Price | | Paid | |

12/31/2008 | | $ | 12.71 | | $ | 9.86 | | $ | 0.000 | |

1/31/2009 | | 11.21 | | 9.30 | | 0.000 | |

2/28/2009 | | 9.57 | | 7.75 | | 0.000 | |

3/31/2009 | | 10.68 | | 8.07 | | 0.000 | |

4/30/2009 | | 12.27 | | 9.40 | | 0.000 | |

5/31/2009 | | 12.56 | | 9.54 | | 0.000 | |

| | | | | | | | | | |

The Boulder Total Return Fund was ranked #1 in Lipper Closed-End Equity Fund Performance for the year ended December 31, 2000 by Lipper Inc.

LIPPER and the LIPPER Corporate Marks are propriety trademarks of Lipper, a Reuters Company. Used by permission.

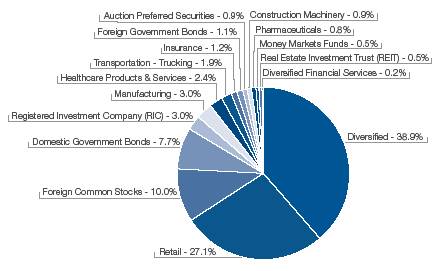

INVESTMENTS AS A % OF NET ASSETS AVAILABLE TO COMMON AND PREFERRED STOCK

4

PORTFOLIO OF INVESTMENTS [Unaudited] |

|

May 31, 2009 | |

Shares | | Description | | Value (Note 1) | |

| | | | | |

LONG TERM INVESTMENTS 90.8% | | | |

DOMESTIC COMMON STOCKS 79.9% | | | |

Construction Machinery 0.9% | | | |

60,000 | | Caterpillar, Inc. | | $ | 2,127,600 | |

| | | | | |

Diversified 38.9% | | | |

690 | | Berkshire Hathaway, Inc., Class A* | | 63,203,999 | |

9,200 | | Berkshire Hathaway, Inc., Class B* | | 27,342,400 | |

| | | | 90,546,399 | |

Diversified Financial Services 0.2% | | | |

5,700 | | Franklin Resources, Inc. | | 381,045 | |

| | | | | |

Healthcare Products & Services 2.4% | | | |

100,000 | | Johnson & Johnson | | 5,516,000 | |

| | | | | |

Insurance 1.2% | | | |

120,000 | | First American Corp. | | 2,737,200 | |

| | | | | |

Manufacturing 3.0% | | | |

8,000 | | 3M Co. | | 456,800 | |

150,500 | | Eaton Corp. | | 6,546,750 | |

| | | | 7,003,550 | |

Pharmaceuticals 0.8% | | | |

123,300 | | Pfizer, Inc. | | 1,872,927 | |

| | | | | |

Real Estate Investment Trust (REIT) 0.5% | | | |

75,000 | | Redwood Trust, Inc. | | 1,194,000 | |

| | | | | |

Registered Investment Company (RIC) 3.0% | | | |

151,250 | | Cohen & Steers REIT and Utility Income Fund, Inc. | | 983,125 | |

92,940 | | Cohen & Steers Select Utility Fund, Inc. | | 1,029,775 | |

549,200 | | Flaherty & Crumrine/Claymore Preferred Securities Income Fund, Inc. | | 4,970,260 | |

4,600 | | Flaherty & Crumrine/Claymore Total Return Fund, Inc. | | 41,676 | |

| | | | 7,024,836 | |

Retail 27.1% | | | |

72,500 | | The Home Depot, Inc. | | 1,679,100 | |

177,000 | | Walgreen Co. | | 5,272,830 | |

370,000 | | Wal-Mart Stores, Inc. | | 18,403,800 | |

1,085,000 | | Yum! Brands, Inc. | | 37,573,550 | |

| | | | 62,929,280 | |

| | | | | | |

See accompanying notes to financial statements.

5

Shares | | Description | | Value (Note 1) | |

| | | | | |

Transportation - Trucking 1.9% | | | |

60,000 | | Burlington Northern Santa Fe Corp. | | $ | 4,346,400 | |

63,100 | | YRC Worldwide, Inc.* | | 162,798 | |

| | | | 4,509,198 | |

| | | |

TOTAL DOMESTIC COMMON STOCKS

(Cost $135,534,515) | | 185,842,035 | |

| | | | | |

FOREIGN COMMON STOCKS 10.0% | | | |

Canada 0.1% | | | |

123,000 | | Canfor Pulp Income Fund | | 233,213 | |

| | | | | |

Hong Kong 4.8% | | | |

515,000 | | Cheung Kong Holdings, Ltd. | | 6,364,217 | |

500,000 | | Henderson Investment, Ltd. | | 39,343 | |

104,500 | | Henderson Land Development Co., Ltd. | | 630,862 | |

6,156,000 | | Midland Holdings, Ltd. | | 4,113,397 | |

| | | | 11,147,819 | |

Japan 0.0%(1) | | | |

340 | | New City Residence Investment Corp.*(2)(3) | | 14,809 | |

| | | | | |

Netherlands 2.2% | | | |

60,000 | | Heineken Holding NV | | 1,801,629 | |

95,117 | | Heineken NV | | 3,385,894 | |

| | | | 5,187,523 | |

New Zealand 1.1% | | | |

4,177,436 | | Kiwi Income Property Trust | | 2,461,975 | |

| | | | | |

Turkey 0.0%(1) | | | |

57,183 | | Dogus GE Gayrimenkul Yatirim Ortakligi A.S.* | | 29,449 | |

| | | | | |

United Kingdom 1.8% | | | |

75,000 | | Diageo PLC, Sponsored ADR | | 4,092,000 | |

| | | | | |

TOTAL FOREIGN COMMON STOCKS

(Cost $24,813,737) | | 23,166,788 | |

| | | | | | |

See accompanying notes to financial statements.

6

Shares/ | | | | | |

Principal | | | | | |

Amount | | Description | | Value (Note 1) | |

| | | | | |

AUCTION PREFERRED SECURITIES 0.9% | | | |

20 | | Cohen & Steers Quality Income Realty Fund, Inc., Series M7(3) | | $ | 490,000 | |

56 | | Cohen & Steers REIT and Utility Income Fund, Inc., Series T7(3) | | 1,372,000 | |

8 | | Neuberger Berman Real Estate Securities Income Fund, Inc., Series C(3) | | 196,000 | |

| | | | | |

TOTAL AUCTION PREFERRED SECURITIES

(Cost $2,100,021) | | 2,058,000 | |

| | | | | |

TOTAL LONG TERM INVESTMENTS

(Cost $162,448,273) | | 211,066,823 | |

| | | | | |

SHORT TERM INVESTMENTS 9.3% | | | |

DOMESTIC GOVERNMENT BONDS 7.7% | | | |

United States Treasury Bills | | | |

$ | 8,000,000 | | 0.110% due 6/18/2009 | | 7,999,584 | |

10,000,000 | | 0.120% due 6/25/2009 | | 9,999,200 | |

| | | | | |

TOTAL DOMESTIC GOVERNMENT BONDS

(Amortized Cost $17,998,784) | | 17,998,784 | |

| | | | | |

FOREIGN GOVERNMENT BONDS 1.1% | | | |

New Zealand 1.0% | | | |

3,800,000 | | New Zealand Treasury Bills, Discount Notes, 2.260% due 07/29/2009 NZD | | 2,424,441 | |

| | | | | |

TOTAL FOREIGN GOVERNMENT BONDS

(Amortized Cost $2,213,474) | | 2,424,441 | |

| | | | | |

MONEY MARKET FUNDS 0.5% | | | |

1,220,906 | | Dreyfus Treasury Cash Management Money Market Fund, Institutional Class, 7 Day Yield - 0.122% | | 1,220,906 | |

| | | | | |

TOTAL MONEY MARKET FUNDS

(Cost $1,220,906) | | 1,220,906 | |

| | | | | |

TOTAL SHORT TERM INVESTMENTS

(Amortized Cost $21,433,164) | | 21,644,131 | |

| | | | | | | |

See accompanying notes to financial statements.

7

| | Value (Note 1) | |

| | | |

TOTAL INVESTMENTS 100.1%

(Cost $183,881,437) | | $ | 232,710,954 | |

| | | |

OTHER ASSETS AND LIABILITIES -0.1% | | (185,913 | ) |

| | | |

TOTAL NET ASSETS AVAILABLE TO COMMON STOCK AND PREFERRED STOCK 100.0% | | 232,525,041 | |

| | | |

AUCTION MARKET PREFERRED STOCK (AMPS) REDEMPTION VALUE | | (77,500,000 | ) |

| | | |

TOTAL NET ASSETS AVAILABLE TO COMMON STOCK | | $ | 155,025,041 | |

* | Non-income producing security. |

(1) | Less than 0.05% of Total Net Assets Available to Common and Preferred Stock. |

(2) | On October 9, 2008, the company declared bankruptcy. |

(3) | Fair valued security under procedures established by the Fund’s Board of Directors. Total market value of fair valued securities as of May 31, 2009 is $2,072,809, or 0.9% of total net assets available to common and preferred stock. |

Percentages are stated as a percent of Total Net Assets Available to Common and Preferred Stock.

Common Abbreviations:

ADR - American Depositary Receipt

A.S. - Anonim Sirketi (Turkish: Joint Stock Company)

Ltd. - Limited

NV - Naamloze Vennootchap is the Dutch term for a public limited liability corporation

NZD - New Zealand Dollar

PLC - Public Limited Company

REIT - Real Estate Investment Trust

For Fund compliance purposes, the Fund’s industry and/or geography classifications refer to any one of the industry/geography sub-classifications used by one or more widely recognized market indexes, and/or as defined by Fund Management. This definition may not apply for purposes of this report, which may combine industry/geography sub-classifications for reporting ease. Industries/geographies are shown as a percent of net assets available to common and preferred shares. These industry/geography classifications are unaudited.

See accompanying notes to financial statements.

8

STATEMENT OF ASSETS AND LIABILITIES [Unaudited] |

|

May 31, 2009 | |

ASSETS: | | | |

Investments, at value (Cost $183,881,437) (Note 1) | | $ | 232,710,954 | |

Foreign currency, at value (Cost $13,600) | | 16,555 | |

Dividends and interest receivable | | 187,053 | |

Prepaid expenses and other assets | | 54,862 | |

Total Assets | | 232,969,424 | |

| | | |

LIABILITIES: | | | |

Payable for investments purchased | | 15,833 | |

Investment co-advisory fees payable (Note 2) | | 242,075 | |

Accumulated undeclared dividends on Taxable Auction Market Preferred Stock (Note 5) | | 65,610 | |

Administration and co-administration fees payable (Note 2) | | 52,513 | |

Legal and audit fees payable | | 41,984 | |

Directors’ fees and expenses payable (Note 2) | | 3,380 | |

Printing fees payable | | 255 | |

Accrued expenses and other payables | | 22,733 | |

Total Liabilities | | 444,383 | |

FUND TOTAL NET ASSETS | | $ | 232,525,041 | |

| | | |

TAXABLE AUCTION MARKET PREFERRED STOCK: | | | |

$0.01 par value, 10,000,000 shares authorized, 775 shares outstanding, liquidation preference of $100,000 per share (Note 5) | | 77,500,000 | |

TOTAL NET ASSETS (APPLICABLE TO COMMON STOCKHOLDERS) | | $ | 155,025,041 | |

| | | |

NET ASSETS (APPLICABLE TO COMMON STOCKHOLDERS) CONSIST OF: | | | |

Par value of common shares (Note 4) | | $ | 123,387 | |

Paid-in capital in excess of par value of common stock | | 124,495,248 | |

Overdistributed net investment income | | (493,941 | ) |

Accumulated net realized loss on investments sold and foreign currency related transactions | | (17,931,707 | ) |

Net unrealized appreciation on investments and foreign currency translation | | 48,832,054 | |

NET ASSETS (APPLICABLE TO COMMON STOCKHOLDERS) | | $ | 155,025,041 | |

| | | |

Net Asset Value, $155,025,041/12,338,660 common stock outstanding | | $ | 12.56 | |

See accompanying notes to financial statements.

9

| STATEMENT OF OPERATIONS [Unaudited] |

| For the Six Months Ended May 31, 2009 |

INVESTMENT INCOME: | | | |

Dividends (net of foreign withholding tax of $4,060) | | $ | 2,090,529 | |

Interest and other income | | 45,593 | |

Total Investment Income | | 2,136,122 | |

| | | |

EXPENSES: | | | |

Investment co-advisory fee (Note 2) | | 1,357,492 | |

Administration and co-administration fees (Note 2) | | 296,634 | |

Preferred stock broker commissions and auction agent fees | | 71,762 | |

Directors’ fees and expenses (Note 2) | | 48,979 | |

Legal and audit fees | | 34,493 | |

Insurance expense | | 22,191 | |

Printing fees | | 18,919 | |

Custody fees | | 10,234 | |

Transfer agency fees | | 9,418 | |

Other | | 47,918 | |

Total Expenses | | 1,918,040 | |

Net Investment Income | | 218,082 | |

| | | |

REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | | | |

Net realized loss on: | | | |

Investment securities | | (7,447,432 | ) |

Foreign currency related transactions | | (1,170,446 | ) |

| | (8,617,878 | ) |

Net change in unrealized appreciation of: | | | |

Investment securities | | 7,404,007 | |

Foreign currency related transactions | | 156 | |

| | 7,404,163 | |

| | | |

NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS: | | (1,213,715 | ) |

LESS: PREFERRED STOCK DISTRIBUTIONS (NOTE 9) | | | |

From net investment income | | (712,023 | ) |

Total Distributions: Preferred Stock | | (712,023 | ) |

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (1,707,656 | ) |

See accompanying notes to financial statements.

10

STATEMENTS OF CHANGES IN NET ASSETS |

|

| | For the

Six Months Ended

May 31, 2009 (Unaudited) | | For the

Year Ended

November 30, 2008 | |

OPERATIONS: | | | | | |

Net investment income | | $ | 218,082 | | $ | 1,683,670 | |

Net realized loss on investments sold | | (8,617,878 | ) | (10,172,497 | ) |

Net change in unrealized appreciation/ (depreciation) on investments during the year | | 7,404,163 | | (103,024,638 | ) |

Net Decrease in Net Assets Resulting from Operations | | (995,633 | ) | (111,513,465 | ) |

| | | | | |

DISTRIBUTIONS: PREFERRED STOCK (NOTE 9) | | | | | |

From net investment income | | (712,023 | ) | (822,246 | ) |

From tax return of capital | | — | | (2,568,738 | ) |

Total Distributions: Preferred Stock | | (712,023 | ) | (3,390,984 | ) |

| | | | | |

Net Decrease in Net Assets Resulting from Operations Applicable to Common Stockholders | | (1,707,656 | ) | (114,904,449 | ) |

| | | | | |

DISTRIBUTIONS: COMMON STOCK (NOTE 9) | | | | | |

From net investment income | | — | | (1,303,416 | ) |

From net realized capital gains | | — | | (448,908 | ) |

From tax return of capital | | — | | (34,486,321 | ) |

Total Distributions: Common Stock | | — | | (36,238,645 | ) |

Net Decrease in Net Assets | | (1,707,656 | ) | (151,143,094 | ) |

| | | | | |

NET ASSETS: | | | | | |

Beginning of period | | 234,232,697 | | 385,375,791 | |

End of period (including overdistributed net investment income of $(493,941) and $0, respectively) | | 232,525,041 | | 234,232,697 | |

Auction Market Preferred Stock (AMPS) Redemption Value | | (77,500,000 | ) | (77,500,000 | ) |

Net Assets Applicable to Common Stockholders | | $ | 155,025,041 | | $ | 156,732,697 | |

See accompanying notes to financial statements.

11

Contained below is selected data for a share of common stock outstanding, total investment return, ratios to average net assets and other supplemental data for the period indicated. This information has been determined based upon information provided in the financial statements and market price data for the Fund’s shares.

| | For the Six Months

Ended May 31,

2009 (Unaudited) | |

OPERATING PERFORMANCE: | | | |

Net Asset Value - Beginning of Period | | $ | 12.70 | |

Income/(Loss) From Investment Operations | | | |

Net investment income(a) | | 0.02 | |

Net realized and unrealized gain/(loss) on investments | | (0.10 | ) |

Total from Investment Operations | | (0.08 | ) |

Distributions: Preferred Stock | | | |

Dividends paid from net investment income(a) | | (0.06 | ) |

Distributions paid from net realized capital gains(a) | | — | |

Distributions paid from tax return of capital(a) | | — | |

Change in accumulated undeclared dividend on AMPS* | | — | |

Total Dividends Paid to AMPS* | | (0.06 | ) |

Net Increase/(Decrease) from Operations Applicable to Common Stock | | (0.14 | ) |

Distribtions: Common Stock | | | |

Dividends paid from net investment income | | — | |

Distributions paid from net realized capital gains | | — | |

Distributions paid from tax return of capital | | — | |

Total Distributions Paid to Common Stockholders | | — | |

Net Increase/(Decrease) in Net Asset Value | | (0.14 | ) |

Common Share Net Asset Value - End of Period | | $ | 12.56 | |

Common Share Market Value - End of Period | | $ | 9.54 | |

Total Return, Common Share Net Asset Value(b) | | (1.1 | )% |

Total Return, Common Share Market Value(b) | | 4.0 | % |

RATIOS TO AVERAGE NET ASSETS AVAILABLE TO COMMON STOCKHOLDERS:(c) | | | |

Net Operating Expenses | | 2.70 | %(d) |

Net Investment Income | | 0.31 | %(d) |

SUPPLEMENTAL DATA: | | | |

Portfolio Turnover Rate | | 3 | % |

Net Assets Applicable to Common Stockholders, End of Period (000s) | | $ | 155,025 | |

Number of Common Shares Outstanding - End of Period (000s) | | 12,339 | |

Ratio of operating expenses to Total Average Net Assets including AMPS* | | 1.75 | %(d) |

* | Taxable Auction Market Preferred Stock (“AMPS”). |

(a) | Calculated based on the average number of common shares outstanding during each fiscal period. |

(b) | Total return based on per share net asset value reflects the effects of changes in net assets value on the performance of the Fund during each fiscal period. Total return based on per share market value assumes the purchase of common shares at the market price on the first day and sales of common shares at the market price on the last day of the period indicated. Dividends and distributions, if any, are assumed to be reinvested at prices obtained under the |

12

FINANCIAL HIGHLIGHTS

For a Common Share Outstanding Throughout Each Period.

| | For the Years Ended November 30, | |

| | 2008 | | 2007 | | 2006 | | 2005 | | 2004 | |

OPERATING PERFORMANCE: | | | | | | | | | | | |

Net Asset Value - Beginning of Period | | $ | 24.95 | | $ | 23.64 | | $ | 21.02 | | $ | 19.91 | | $ | 17.61 | |

Income/(Loss) From Investment Operations | | | | | | | | | | | |

Net investment income(a) | | 0.14 | | 0.35 | | 0.30 | | 0.15 | | 0.03 | |

Net realized and unrealized gain/(loss) on investments | | (9.18 | ) | 2.34 | | 3.37 | | 1.17 | | 2.35 | |

Total from Investment Operations | | (9.04 | ) | 2.69 | | 3.67 | | 1.32 | | 2.38 | |

Distributions: Preferred Stock | | | | | | | | | | | |

Dividends paid from net investment income(a) | | (0.06 | ) | (0.26 | ) | (0.04 | ) | (0.05 | ) | (0.09 | ) |

Distributions paid from net realized capital gains(a) | | — | | (0.09 | ) | (0.27 | ) | (0.15 | ) | — | |

Distributions paid from tax return of capital(a) | | (0.21 | ) | — | | — | | — | | — | |

Change in accumulated undeclared dividend on AMPS* | | — | | — | | — | | (0.01 | ) | 0.01 | |

Total Dividends Paid to AMPS* | | (0.27 | ) | (0.35 | ) | (0.31 | ) | (0.21 | ) | (0.08 | ) |

Net Increase/(Decrease) from Operations Applicable to Common Stock | | (9.31 | ) | 2.34 | | 3.36 | | 1.11 | | 2.30 | |

Distribtions: Common Stock | | (0.11 | ) | (0.19 | ) | (0.17 | ) | — | | — | |

Dividends paid from net investment income | | (0.04 | ) | (0.84 | ) | (0.57 | ) | — | | — | |

Distributions paid from net realized capital gains | | (2.79 | ) | — | | — | | — | | — | |

Distributions paid from tax return of capital | | (2.94 | ) | (1.03 | ) | (0.74 | ) | — | | — | |

Total Distributions Paid to Common Stockholders | | (12.25 | ) | 1.31 | | 2.62 | | 1.11 | | 2.30 | |

Net Increase/(Decrease) in Net Asset Value | | $ | 12.70 | | $ | 24.95 | | $ | 23.64 | | $ | 21.02 | | $ | 19.91 | |

Common Share Net Asset Value - End of Period | | $ | 9.17 | | $ | 22.70 | | $ | 21.59 | | $ | 17.57 | | $ | 17.45 | |

Common Share Market Value - End of Period | | (40.3 | )% | 10.4 | % | 17.4 | % | 5.6 | % | 13.1 | % |

Total Return, Common Share Net Asset Value(b) | | (52.6 | )% | 10.0 | % | 28.2 | % | 0.7 | % | 19.6 | % |

Total Return, Common Share Market Value(b) | | | | | | | | | | | |

RATIOS TO AVERAGE NET ASSETS AVAILABLE TO COMMON STOCKHOLDERS:(c) | | | | | | | | | | | |

Net Operating Expenses | | 2.22 | % | 2.07 | % | 2.21 | % | 2.24 | % | 2.30 | % |

Net Investment Income | | (0.70 | )% | 0.04 | % | 1.06 | % | 0.71 | % | 0.66 | % |

SUPPLEMENTAL DATA: | | | | | | | | | | | |

Portfolio Turnover Rate | | 6 | % | 28 | % | 23 | % | 32 | % | 25 | % |

Net Assets Applicable to Common Stockholders, End of Period (000s) | | $ | 156,733 | | $ | 307,876 | | $ | 291,662 | | $ | 259,363 | | $ | 245,626 | |

Number of Common Shares Outstanding - End of Period (000s) | | 12,339 | | 12,339 | | 12,339 | | 12,339 | | 12,339 | |

Ratio of operating expenses to Total Average Net Assets including AMPS* | | 1.69 | % | 1.65 | % | 1.71 | % | 1.72 | % | 1.73 | % |

| Fund’s distribution reinvestment plan. Results represent past performance and do not guarantee future results. Current returns may be lower or higher than the performance data quoted. |

(c) | Expense ratios do not include the effect of distributions to preferred stockholders. The net investment income ratios reflect income net of operating expenses and payments and change in undeclared dividends to AMPS Stockholders. |

(d) | Annualized. |

See accompanying notes to financial statements.

13

The table below sets out information with respect to Taxable Auction Market Preferred Stock currently outstanding.(1)

| | | | | | | | Involuntary | | | |

| | | | Total Shares | | Asset | | Liquidating | | Average | |

| | Liquidation | | Outstanding | | Coverage | | Preference | | Market Value | |

| | Value (000) | | (000) | | Per Share(2) | | Per Share(3) | | Per Share(3) | |

05/31/09 | | $ | 77,500 | | 0.775 | | $ | 300,117 | | $ | 100,000 | | $ | 100,000 | |

11/30/08 | | 77,500 | | 0.775 | | 302,273 | | 100,000 | | 100,000 | |

11/30/07 | | 77,500 | | 0.775 | | 497,949 | | 100,000 | | 100,000 | |

11/30/06 | | 77,500 | | 0.775 | | 476,367 | | 100,000 | | 100,000 | |

11/30/05 | | 77,500 | | 0.775 | | 434,662 | | 100,000 | | 100,000 | |

11/30/04 | | 77,500 | | 0.775 | | 416,937 | | 100,000 | | 100,000 | |

| | | | | | | | | | | | | | | |

(1) See Note 5 in Notes to Financial Statements.

(2) Calculated by subtracting the Fund’s total liabilities (excluding accumulated unpaid distributions on Preferred Shares) from the Fund’s total assets and dividing by the number of AMPS outstanding.

(3) Excludes accumulated undeclared dividends.

See accompanying notes to financial statements.

14

NOTES TO FINANCIAL STATEMENTS [Unaudited] May 31, 2009 |

|

NOTE 1. | SIGNIFICANT ACCOUNTING POLICIES |

Boulder Total Return Fund, Inc. (the “Fund), is a diversified, closed-end management company organized as a Maryland corporation and is registered with the Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). The policies described below are followed consistently by the Fund in the preparation of its financial statements in conformity with accounting principles generally accepted in the United States of America.

Portfolio Valuation: The net asset value of the Fund’s Common Shares is determined by the Fund’s co-administrator no less frequently than on the last business day of each week and month. It is determined by dividing the value of the Fund’s net assets attributable to common stock by the number of Common Shares outstanding. The value of the Fund’s net assets attributable to Common Shares is deemed to equal the value of the Fund’s total assets less (i) the Fund’s liabilities and (ii) the aggregate liquidation value of the outstanding Taxable Auction Market Preferred Stock. Securities listed on a national securities exchange are valued on the basis of the last sale on such exchange or the NASDAQ Official Close Price on the day of valuation. In the absence of sales of listed securities and with respect to securities for which the most recent sale prices are not deemed to represent fair market value, and unlisted securities (other than money market instruments), securities are valued at the mean between the closing bid and asked prices, or based on a matrix system which utilizes information (such as credit ratings, yields and maturities) from independent sources. Investments for which market quotations are not readily available or do not otherwise accurately reflect the fair value of the investment are valued at fair value as determined in good faith by or under the direction of the Board of Directors of the Fund, including reference to valuations of other securities which are considered comparable in quality, maturity and type. Investments in money market instruments, which mature in 60 days or less at the time of purchase, are valued at amortized cost.

The Fund follows Financial Accounting Standards Board (“FASB”) Statement of Financial Accounting Standards No. 157, “Fair Value Measurements” (“FAS 157). In accordance with FAS 157, fair value is defined as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. Under certain circumstances, fair value may equal the mean between the bid and asked prices. FAS 157 established a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including such a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed

15

| NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

· Level 1—quoted prices in active markets for identical investments

· Level 2—significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

· Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The valuation techniques used by the Fund to measure fair value during the six months ended May 31, 2009 maximized the use of observable inputs and minimized the use of unobservable inputs. The Fund utilized the following fair value techniques: discounted future cash flow models, weighted average of last available trade prices and multi-dimensional relational pricing model.

The following is a summary of the inputs used as of May 31, 2009 in valuing the Fund’s investments carried at fair value:

Valuation Inputs | | Investments in Securities | |

Level 1—Quoted Prices | | $ | 210,214,920 | |

Level 2—Significant Observable Inputs | | 22,481,225 | |

Level 3—Significant Unobservable Inputs | | 14,809 | |

Total | | $ | 232,710,954 | |

The following is a reconciliation of assets in which significant unobservable inputs (Level 3) were used in determining fair value:

| | Investments in Securities | |

Balance as of 11/30/08 | | $ | 14,764 | |

Realized gain/(loss) | | — | |

Change in unrealized appreciation | | 45 | |

Net purchases/(sales) | | — | |

Transfer in and/or out of Level 3 | | — | |

Balance as of 5/31/09 | | $ | 14,809 | |

Securities Transactions and Investment Income: Securities transactions are recorded as of the trade date. Realized gains and losses from securities sold are recorded on the identified cost basis. Dividend income is recorded on ex-dividend dates. Interest income is recorded using the interest method.

16

NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

|

The actual amounts of dividend income and return of capital received from investments in real estate investment trusts (“REITS”) and registered investment companies (“RICS”) at calendar year-end are determined after the end of the fiscal year. The Fund therefore estimates these amounts for accounting purposes until the actual characterization of REIT and RIC distributions is known. Distributions received in excess of the estimate are recorded as a reduction of the cost of investments.

Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Foreign currencies, investments and other assets and liabilities denominated in foreign currencies are translated in U.S. dollars at the exchange rate prevailing at the end of the period, and purchases and sales of investment securities, income and expenses transacted in foreign currencies are translated at the exchange rate on the dates of such transactions.

Foreign currency gains and losses result from fluctuations in exchange rates between trade date and settlement date on securities transactions, foreign currency transactions and the difference between amounts of interest and dividends recorded on the books of the Fund and the amounts actually received. The portion of foreign currency gains and losses related to fluctuation in exchange rates between the initial purchase trade date and the subsequent sale trade date is included in gains and losses as stated in the Statement of Operations under Foreign currency related transactions.

Repurchase Agreements: The Fund may engage in repurchase agreement transactions. The Fund’s Management reviews and approves periodically the eligibility of the banks and dealers with which the Fund enters into repurchase agreement transactions. The value of the collateral underlying such transactions is at least equal at all times to the total amount of the repurchase obligations, including interest. The Fund maintains possession of the collateral and, in the event of counterparty default, the Fund has the right to use the collateral to offset losses incurred. There is the possibility of loss to the Fund in the event the Fund is delayed or prevented from exercising its rights to dispose of the collateral securities. The Fund had no outstanding repurchase agreements as of May 31, 2009.

Lending of Portfolio Securities: The Fund may participate in securities lending arrangements. To do so, the Fund would engage a lending agent to loan securities to qualified brokers and dealers in exchange for negotiated lenders’ fees. As of May 31, 2009, the Fund was not participating in any securities lending arrangements.

Dividends and Distributions to Stockholders: Dividends to common stockholders will be declared in such a manner as to avoid the imposition of the 4% excise tax described in “Federal Income Taxes” below. The stockholders of Taxable Auction Market Preferred Stock (“AMPS”) are entitled to receive cumulative cash dividends as declared by the Fund’s Board of Directors. Distributions to stockholders are recorded on the ex-dividend date. Any net realized short-term capital gains will be distributed to stockholders at least annually. Any net realized long-term capital gains may be distributed to stockholders at least annually or may be retained by the Fund as determined by the

17

| NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

Fund’s Board of Directors. Capital gains retained by the Fund are subject to tax at the corporate tax rate. Subject to the Fund qualifying as a registered investment company, any taxes paid by the Fund on such net realized long-term gains may be used by the Fund’s stockholders as a credit against their own tax liabilities.

Prior to November 10, 2008, it was the policy of the Fund to declare quarterly and pay monthly distributions to common stockholders (the “Policy”). In an effort to maintain a stable distribution amount, the Fund could have paid distributions consisting of net investment income, realized gains and return of paid-in capital. Return of paid-in capital should not be considered yield by investors in the Fund. To the extent stockholders receive a return of paid-in capital they will be required to adjust their cost basis by the same amount upon the sale of their Fund shares. The composition of the Fund’s distributions, if any, for the calendar year 2009 will be reported to Fund stockholders on IRS Form 1099-DIV. The Fund may pay distributions in excess of those required to avoid excise tax or to satisfy the requirements of Subchapter M of the Internal Revenue Code. Distributions to common stockholders are recorded on the ex-date. Net realized capital gains, if any, will be offset to the extent of any available capital loss carryforwards.

The Fund’s Policy was suspended, as approved by the Board of Directors, at the regular meeting held November 10, 2008. The Fund’s Board of Directors considered continuation of the Policy and a number of alternatives and other factors before coming to the conclusion to suspend the Policy.

Use of Estimates: The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Indemnifications: Like many other companies, the Fund’s organizational documents provide that its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, both in some of its principal service contracts and in the normal course of its business, the Fund enters into contracts that provide indemnifications to other parties for certain types of losses or liabilities. The Fund’s maximum exposure under these arrangements is unknown as this could involve future claims against the Fund.

Federal Income Taxes: For federal income tax purposes, the Fund currently qualifies, and intends to remain qualified, as a regulated investment company under the provisions of the Internal Revenue Code by distributing substantially all of its investment company taxable net income including realized gain not offset by capital loss carryforwards, if any, to its stockholders. Accordingly, no provision for federal income or excise taxes has been made.

Income and capital gain distributions are determined and characterized in accordance with income tax regulations, which may differ from generally accepted accounting

18

NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

|

principles. These differences are primarily due to (1) differing treatments of income and gains on various investment securities held by the Fund, including temporary differences, (2) the attribution of expenses against certain components of taxable investment income, and (3) federal regulations requiring proportional allocation of income and gains to all classes of stockholders. The Code imposes a 4% nondeductible excise tax on the Fund to the extent the Fund does not distribute by the end of any calendar year at least (1) 98% of the sum of its net investment income for that year and its capital gains (both long-term and short-term) for its fiscal year and (2) certain undistributed amounts from previous years.

The Fund follows FASB Interpretation No. 48 (“FIN 48”) “Accounting for Uncertainty in Income Taxes,” which requires that the financial statement effects of a tax position taken or expected to be taken in a tax return be recognized in the financial statements when it is more likely than not, based on the technical merits, that the position will be sustained upon examination. Management has concluded that the Fund has taken no uncertain tax positions that require adjustment to the financial statements to comply with the provisions of FIN 48. The Fund files income tax returns in the U.S. federal jurisdiction and Colorado. The statue of limitations on the Fund’s federal tax filings remains open for the fiscal years ended November 30, 2008, November 30, 2007, November 30, 2006 and November 30, 2005. The statute of limitation on the Fund’s state tax filings remains open for the fiscal years ended November 30, 2008, November 30, 2007, November 30, 2006, November 30, 2005 and November 30, 2004.

NOTE 2. | INVESTMENT CO-ADVISORY FEES, DIRECTORS’ FEES, CO-ADMINISTRATION FEE, CUSTODY FEE AND TRANSFER AGENT FEE |

Boulder Investment Advisers, L.L.C. (“BIA”) and Stewart Investment Advisers (“SIA”) serve as the Fund’s co-investment advisers (the “Advisers”). The Fund pays the Advisers a monthly fee at an annual rate of 1.25% of the value of the Fund’s average monthly total assets under management (including the principal amount of leverage, if any). At the Feburary 9, 2009 Board of Directors meeting, the Advisers agreed to a waiver of advisory fees such that, in the future, the advisory fees would be calculated at the annual rate of 1.25% on assets up to $400 million, 1.10% on assets between $400-$600 million and 1.00% on assets exceeding $600 million. This fee waiver has a one year term and is renewable annually at the option of the Advisers. The waiver is not subject to recapture. The equity owners of BIA are Evergreen Atlantic, LLC, a Colorado limited liability company (“EALLC”), and the Lola Brown Trust No. 1B (the “Lola Trust”), each of which is considered to be an “affiliated person” of the Fund as that term is defined in the 1940 Act. Stewart West Indies Trading Company, Ltd. is a Barbados international business company doing business as Stewart Investment Advisers. SIA receives a monthly fee equal to 75% of the fees earned by the Advisers, and BIA receives 25% of the fees earned by the Advisers. The equity owner of SIA is the Stewart West Indies Trust, considered to be an “affiliated person” of the Fund as that term is defined in the 1940 Act.

19

| NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

Fund Administrative Services, LLC (“FAS”) serves as the Fund’s co-administrator. Under the Administration Agreement, FAS provides certain administrative and executive management services to the Fund. The Fund pays FAS a monthly fee calculated at an annual rate of 0.20% of the value of the Fund’s average monthly total assets (including leverage) up to $250 million; 0.18% of the Fund’s average monthly total assets (including leverage) on the next $150 million; and, 0.15% on the value of the Fund’s average monthly total assets (including leverage) over $400 million. The equity owners of FAS are EALLC and the Lola Trust.

ALPS Fund Services, Inc. (“ALPS”) serves as the Fund’s co-administrator. As compensation for its services, ALPS receives certain out-of-pocket expenses and asset-based fees, which are accrued daily and paid monthly. Fees paid to ALPS are calculated based on combined assets of the Fund, the Boulder Growth & Income Fund, Inc., The Denali Fund Inc., and First Opportunity Fund, Inc. (the “Fund Group”). ALPS receives the greater of the following, based on combined assets of the Fund Complex: an annual minimum of $460,000, or an annualized fee of 0.045% on assets up to $1 billion, an annualized fee of 0.03% on assets between $1 and $3 billion, and an annualized fee of 0.02% on assets above $3 billion.

The Fund pays each Director who is not a director, officer, employee, or affiliate of the Advisers or FAS a fee of $8,000 per annum, plus $4,000 for each in-person meeting of the Board of Directors and $500 for each telephone meeting. In addition, the Chairman of the Board and the Chairman of the Audit Committee receive $1,000 per meeting and each member of the Audit Committee receives $500 per meeting. The Fund will also reimburse all non-interested Directors for travel and out-of-pocket expenses incurred in connection with such meetings.

Bank of New York Mellon (“BNY Mellon”) serves as the Fund’s custodian and as compensation for BNY Mellon’s services the Fund pays BNY Mellon a monthly fee plus certain out-of-pocket expenses.

PNC Global Investment Servicing (“PNC GIS”) serves as the Fund’s Common Stock Servicing Agent (transfer agent), dividend-paying agent and registrar, and as compensation for PNC GIS’s services as such, the Fund pays PNC GIS a monthly fee plus certain out-of-pocket expenses.

Deutsche Bank Trust Company Americas (“Auction Agent”), a wholly owned subsidiary of Deutsche Bank AG, serves as the Fund’s Preferred Stock transfer agent, registrar, dividend disbursing agent and redemption agent.

NOTE 3. | SECURITIES TRANSACTIONS |

Purchases and sales of securities, excluding short term securities, during the six months ended May 31, 2009 were $5,587,847 and $9,392,829, respectively.

20

NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

|

On May 31, 2009, based on cost of $183,875,189 for federal income tax purposes, aggregate gross unrealized appreciation for all securities in which there is an excess of value over tax cost was $68,671,934 and aggregate gross unrealized depreciation for all securities in which there is an excess of tax cost over value was $19,836,169, resulting in net unrealized appreciation of $48,835,765.

At May 31, 2009, 240,000,000 of $0.01 par value Common Stock were authorized, of which 12,338,660 were outstanding.

Transactions in common stock were as follows:

| | Six Months Ended | | Year Ended | |

| | May 31, 2009 | | November 30, 2008 | |

Common Shares outstanding – beginning of period | | 12,338,660 | | 12,338,660 | |

Common Shares issued as reinvestment of dividends | | — | | — | |

Common Shares outstanding – end of period | | 12,338,660 | | 12,338,660 | |

NOTE 5. | TAXABLE AUCTION MARKET PREFERRED STOCK |

The Fund’s Articles of Incorporation authorize the issuance of up to 10,000,000 shares of $0.01 par value preferred stock. On August 15, 2000, the Fund’s 775 shares of Money Market Cumulative Preferred StockTM were retired and 775 shares of Taxable Auction Market Preferred Stock (“AMPS”) were issued. AMPS is senior to the Common Stock and results in the financial leveraging of the Common Stock. Such leveraging tends to magnify both the risks and opportunities to Common Stockholders. Dividends on shares of AMPS are cumulative. The Fund’s AMPS have a liquidation preference of $100,000 per share, plus any accumulated unpaid distributions, whether or not earned or declared by the Fund but excluding interest thereon (“Liquidation Value”) and have no set retirement date. An auction of the AMPS is generally held every 28 days. Existing stockholders may submit an order to hold, bid or sell shares on each auction date. AMPS stockholders may also trade shares in the secondary market.

In February 2008, the auction market across almost all closed-end funds became illiquid resulting in failed auctions for the Fund’s AMPS. A failed auction is not an event of default for the Fund but it has a negative impact on the liquidity of the AMPS. A failed auction occurs when there are more sellers of a fund’s AMPS than buyers. It is impossible to predict how long this imbalance will last. A successful auction for the Fund’s AMPS may not occur for some time, if ever, and even if liquidity does resume, holders of AMPS may not have the ability to sell the AMPS at their liquidation preference. As such, the Fund continues to pay dividends on the AMPS at the maximum rate, set forth in the Fund’s Articles Supplementary, the governing document for the AMPS. The Fund’s maximum rate is set at the greater of 1.25% of 30-day LIBOR or 30-day LIBOR plus 125 basis points.

21

| NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

The Fund may redeem its AMPS, in whole or in part, on the second business day preceding any distribution payment date at Liquidation Value. The Fund is also subject to certain restrictions relating to the AMPS. Specifically, the Fund is required under the 1940 Act to maintain an asset coverage with respect to the AMPS of 200% or greater. The Fund is also required to maintain certain coverage amounts for Standard & Poor’s and Moody’s (“rating agencies”). Failure to comply with these restrictions could preclude the Fund from declaring any distributions to common stockholders or repurchasing common shares and/or could trigger the mandatory redemption of AMPS at Liquidation Value. The Fund was in compliance with these requirements as of May 31, 2009. The holders of AMPS are entitled to one vote per share and will vote with holders of common shares as a single class, except that the AMPS holders will vote separately as a class on certain matters, as required by law or the Fund’s charter. The holders of the AMPS, voting as a separate class, are entitled at all times to elect two Directors of the Fund, and to elect a majority of the Directors of the Fund if the Fund fails to pay distributions on AMPS for two consecutive years.

In connection with the settlement of each AMPS auction, the Fund pays, through the auction agent, a service fee to each participating broker-dealer based upon the aggregate liquidation preference of the AMPS held by the broker-dealer’s customers. Prior to February 19, 2009 the Fund paid at an annual rate of 0.25% and upon this date the annual rate was reduced to 0.05% until further notice from the Fund. These fees are paid for failed auctions as well.

On May 31, 2009, 775 shares of AMPS were outstanding at the annual rate of 1.60%. The dividend rate, as set by the auction process, is generally expected to vary with short-term interest rates. These rates may vary in a manner unrelated to the income received on the Fund’s assets, which could have either a beneficial or detrimental impact on net investment income and gains available to common stockholders. While the Fund expects to earn a higher return on its assets than the cost associated with the AMPS, including expenses, there can be no assurance that such results will be attained.

NOTE 6. | PORTFOLIO INVESTMENTS, CONCENTRATION AND INVESTMENT QUALITY |

The Fund operates as a “diversified” management investment company, as defined in the 1940 Act. Under this definition, at least 75% of the value of the Fund’s total assets must at the time of investment consist of cash and cash items (including receivables), U.S. Government securities, securities of other investment companies, and other securities limited in respect of any one issuer to an amount not greater in value than 5% of the value of the Fund’s total assets (at the time of purchase) and to not more than 10% of the voting securities of a single issuer. This limit does not apply, however, to 25% of the Fund’s assets, which may be invested in a single issuer. A more concentrated portfolio may cause the Fund’s net asset value to be more volatile and thus may subject stockholders to more risk. The Fund may hold a substantial position (up to 25% of its assets) in the common stock of a single issuer. As of May 31, 2009, the Fund held more than 25% of its assets in Berkshire Hathaway, Inc., as a direct result of the market appreciation of

22

NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

|

the issuer since the time of purchase. Thus, the volatility of the Fund’s common stock, and the Fund’s net assets value and its performance in general, depends disproportionately more on the performance of this single issuer than that of a more diversified fund.

The Fund intends to concentrate its common stock investments in a few issuers and to take large positions in those issuers. As a result, the Fund is subject to a greater risk of loss than a fund that diversifies its investments more broadly. Taking larger positions is also likely to increase the volatility of the Fund’s net asset value reflecting fluctuation in the value of its large holdings. Under normal market conditions, the Fund intends to invest in a portfolio of common stocks. The portion of the Fund’s assets invested in each can vary depending on market conditions. The term “common stocks” includes both stocks acquired primarily for their appreciation potential and stocks acquired for their income potential, such as dividend-paying RICs and REITs. The term “income securities” includes bonds, U.S. Government securities, notes, bills, debentures, preferred stocks, convertible securities, bank debt obligations, repurchase agreements and short-term money market obligations.

NOTE 7. | SIGNIFICANT STOCKHOLDERS |

On May 31, 2009, trusts and other entities affiliated with Stewart R. Horejsi and the Horejsi family owned 4,956,149 shares of Common Stock of the Fund, representing approximately 40.17% of the total Fund shares. Stewart R. Horejsi is the primary portfolio manager for SIA and is the Fund’s primary portfolio manager. He is responsible for the day-to-day strategic management of the Fund.

NOTE 8. | SHARE REPURCHASE PROGRAM |

In accordance with Section 23(c) of the 1940 Act, the Fund may from time to time effect redemptions and/or repurchases of its AMPS and/or its Common Stock, in the open market or through private transactions; at the option of the Board of Directors and upon such terms as the Directors shall determine.

For the six months ended May 31, 2009 and the year ended November 30, 2008, the Fund did not repurchase any of its own stock.

NOTE 9. | TAX BASIS DISTRIBUTIONS |

As determined on November 30, 2008, permanent differences resulting primarily from different book and tax accounting for gains and losses on foreign currency and certain other investments were reclassified at fiscal year-end. These reclassifications had no effect on net income, net asset value applicable to common stockholders or net asset value per common share of the Fund.

Ordinary income and long-term capital gains are allocated to common stockholders after payment of the available amounts on any outstanding AMPS. To the extent that the

23

| NOTES TO FINANCIAL STATEMENTS [Unaudited]

May 31, 2009 |

amount distributed to common stockholders exceeds the amount of available ordinary income and long-term capital gains after allocation to any outstanding AMPS, these distributions are treated as a tax return of capital. Additionally, to the extent that the amount distributed on any outstanding AMPS exceeds the amount of available ordinary income and long-term capital gains, these distributions are treated as a tax return of capital.

Permanent book and tax basis differences of $(858,668) and $858,668 were reclassified at November 30, 2008 among distributions in excess of net investment income and accumulated net realized losses on investments, respectively, for the Fund.

The tax character of distributions paid during the years ended November 30, 2008 and November 30, 2007 was as follows:

| | Year Ended | | Year Ended | |

| | November 2008 | | November 2007 | |

Distributions paid from: | | | | | |

Ordinary Income | | $ | 2,125,662 | | $ | 5,501,573 | |

Long-Term Capital Gain | | 448,908 | | 11,440,578 | |

Tax Return of Capital | | 37,055,059 | | — | |

| | $ | 39,629,629 | | $ | 16,942,151 | |

As of November 30, 2008, the Fund had available for tax purposes unused capital loss carryovers of $9,313,829 expiring November 30, 2016.

As of November 30, 2008, the components of distributable earnings (accumulated losses) on a U.S. federal income tax basis were as follows:

Accumulated Capital Losses | | $ | (9,313,829 | ) |

Unrealized Appreciation | | 41,427,891 | |

| | $ | 32,114,062 | |

NOTE 10. | OTHER INFORMATION |

Rights Offerings: The Fund, like other closed-end funds, may at times raise cash for investment by issuing a fixed number of shares through one or more public offerings, including rights offerings. Proceeds from any such offerings will be used to further the investment objectives of the Fund.

NOTE 11. | RECENTLY ISSUED ACCOUNTING PRONOUNCEMENT |

In March 2008, FASB issued Statement of Financial Accounting Standards No. 161 (“SFAS 161”) “Disclosures about Derivative Instruments and Hedging Activities”—an amendment of FASB Statement No. 133 (“SFAS 133”), expands the disclosure requirements in SFAS 133 about an entity’s derivative instruments and hedging activities. SFAS 161 is effective for fiscal years and interim periods beginning after November 15, 2008. Management has concluded that the adoption of SFAS 161, as adopted by the Fund December 1, 2008, has no impact on the Fund’s financial statements for the six months ended May 31, 2009.

24

SUMMARY OF DIVIDEND REINVESTMENT PLAN [Unaudited] May 31, 2009 |

|

Registered holders (“Common Stockholders”) of common shares (the “Common Shares”) are automatically enrolled (the “Participants”) in the Fund’s Dividend Reinvestment Plan (the “Plan”) whereupon all distributions of income, capital gains or managed distributions (“Distributions”) are automatically reinvested in additional Common Shares. Common Stockholders who elect to not participate in the Plan will receive all distributions in cash paid by check in U.S. dollars mailed directly to the stockholders of record (or if the shares are held in street name or other nominee name, then the nominee) by the custodian, as dividend disbursing agent.

PNC Global Investment Servicing (the “Agent”) serves as Agent for each Participant in administering the Plan. After the Fund declares a Distribution, if (1) the net asset value per Common Share is equal to or less than the market price per Common Share plus estimated brokerage commissions on the payment date for a Distribution, Participants will be issued Common Shares at the higher of net asset value per Common Share or 95% of the market price per Common Share on the payment date; or if (2) the net asset value per Common Share exceeds the market price plus estimated brokerage commissions on the payment date for a Distribution, the Agent shall apply the amount of such Distribution to purchase Common Shares on the open market and Participants will receive the equivalent in Common Shares valued at the weighted average market price (including brokerage commissions) determined as of the time of the purchase (generally, following the payment date of the Distribution). If, before the Agent has completed its purchases, the market price plus estimated brokerage commissions exceeds the net asset value of the Common Shares as of the payment date, the purchase price paid by the Agent may exceed the net asset value of the Common Shares, resulting in the acquisition of fewer Common Shares than if such Distribution had been paid in Common Shares issued by the Fund. If the Agent is unable to invest the full Distribution amount in purchases in the open market or if the market discount shifts to a market premium during the purchase period than the Agent may cease making purchases in the open market the instant the Agent is notified of a market premium and may invest the uninvested portion portion of the Distribution in newly issued Common Shares at the net asset value per Common Share at the close of business provided that, if the net asset value is less than or equal to 95% of the then current market price per Common Share, the dollar amount of the Distribution will be divided by 95% of the market price on the payment date. The Fund will not issue Common Shares under the Plan below net asset value.

There is no charge to Participants for reinvesting Distributions, except for certain brokerage commissions, as described below. The Agent’s fees for the handling of the reinvestment of Distributions will be paid by the Fund. There will be no brokerage commissions charged with respect to shares issued directly by the Fund. However, each Participant will pay a pro rata share of brokerage commissions incurred with respect to the Agent’s open market purchase in connection with the reinvestment of Distributions. The automatic reinvestment of Distributions will not relieve Participants of any federal income tax that may be payable on such Distributions.

25

The Fund reserves the right to amend or terminate the Plan upon 90 days’ written notice to Common Stockholders of the Fund.

Participants in the Plan may (i) request a certificate, (ii) request to sell their shares, or (iii) withdraw from the Plan upon written notice to the Agent or by telephone in accordance with the specific procedures and will receive certificates for whole Common Shares and cash for fractional Common Shares.

All correspondence concerning the Plan should be directed to the Agent, PNC Global Investment Servicing, P.O. Box 43027, Providence, RI 02940-3027. To receive a full copy of the Fund’s Dividend Reinvestment Plan, please contact the Agent at 1-800-331-1710.

26

ADDITIONAL INFORMATION [Unaudited] May 31, 2009 |

|

Portfolio Information. The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available (1) on the Fund’s website located at http://www.boulderfunds. net; (2) on the SEC’s website at http://www.sec.gov; or (3) for review and copying at the SEC’s Public Reference Room (“PRR”) in Washington, DC. Information regarding the operation of the PRR may be obtained by calling 1-800-SEC-0330.

Proxy Information. The policies and procedures used to determine how to vote proxies relating to portfolio securities held by the Fund are available on the Fund’s website located at http://www.boulderfunds.net. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent twelve-month period ended June 30 is available at http://www.sec.gov.

Senior Officer Code of Ethics. The Fund files a copy of its code of ethics that applies to the registrant’s principal executive officer, principal financial officer or controller, or persons performing similar functions (the “Senior Officer Code of Ethics”), with the SEC as an exhibit to its annual report on Form N-CSR. The Fund’s Senior Officer Code of Ethics is available on the Fund’s website located at http://www.boulderfunds.net.

Privacy Statement. Pursuant to SEC Regulation S-P (Privacy of Consumer Financial Information) the Directors of the Fund have established the following policy regarding information about the Fund’s stockholders. We consider all stockholder data to be private and confidential, and we hold ourselves to the highest standards in its safekeeping and use.

General Statement. The Fund may collect nonpublic information (e.g., your name, address, email address, Social Security Number, Fund holdings (collectively, “Personal Information”)) about stockholders from transactions in Fund shares. The Fund will not release Personal Information about current or former stockholders (except as permitted by law) unless one of the following conditions is met: (i) we receive your prior written consent; (ii) we believe the recipient to be you or your authorized representative; (iii) to service or support the business functions of the Fund (as explained in more detail below), or (iv) we are required by law to release Personal Information to the recipient. The Fund has not and will not in the future give or sell Personal Information about its current or former stockholders to any company, individual, or group (except as permitted by law) and as otherwise provided in this policy.

In the future, the Fund may make certain electronic services available to its stockholders and may solicit your email address and contact you by email, telephone or US mail regarding the availability of such services. The Fund may also contact stockholders by email, telephone or US mail in connection with these services, such as to confirm enrollment in electronic stockholders communications or to update your Personal Information. In no event will the Fund transmit your Personal Information via email without your consent.

27

Use of Personal Information. The Fund will only use Personal Information (i) as necessary to service or maintain stockholder accounts in the ordinary course of business and (ii) to support business functions of the Fund and its affiliated businesses. This means that the Fund may share certain Personal Information, only as permitted by law, with affiliated businesses of the Fund, and that such information may be used for non-Fund-related solicitation. When Personal Information is shared with the Fund’s business affiliates, the Fund may do so without providing you the option of preventing these types of disclosures as permitted by law.

Safeguards regarding Personal Information. Internally, we also restrict access to Personal Information to those who have a specific need for the records. We maintain physical, electronic, and procedural safeguards that comply with Federal standards to guard Personal Information. Any doubts about the confidentiality of Personal Information, as required by law, are resolved in favor of confidentiality.

Meeting of Stockholders - Voting Results

On April 24, 2009, the Fund held its Annual Meeting of Stockholders to consider an amendment to the Fund’s Charter and the election of Directors of the Fund. The results of voting were as follows:

Proposal 1: Amendment to the Charter classifying the Board of Directors into three separate classes and making related changes to the Charter (both common and preferred stockholders vote)

| | # of Votes Cast | | % of Votes Cast | |

Affirmative | | 6,878,143 | | 90.67 | % |

Against | | 684,220 | | 9.02 | % |

Abstained | | 23,268 | | 0.31 | % |

TOTAL | | 7,585,631 | | 100.00 | % |

Proposal 2: Election of Directors of the Fund

Election of Joel W. Looney as a Class II Director of the Fund

(both common and preferred stockholders vote)

| | # of Votes Cast | | % of Votes Cast | |

Affirmative | | 11,087,571 | | 93.49 | % |

Withheld | | 772,237 | | 6.51 | % |

TOTAL | | 11,859,808 | | 100.00 | % |

28

Election of Richard I. Barr as a Class III Director of the Fund

(both common and preferred stockholders vote)

| | # of Votes Cast | | % of Votes Cast | |

Affirmative | | 11,079,510 | | 93.42 | % |

Withheld | | 780,298 | | 6.58 | % |

TOTAL | | 11,859,808 | | 100.00 | % |

Election of Dr. Dean L. Jacobson as a Class I Director of the Fund

(both common and preferred stockholders vote)

| | # of Votes Cast | | % of Votes Cast | |

Affirmative | | 11,079,199 | | 93.42 | % |

Withheld | | 780,609 | | 6.58 | % |

TOTAL | | 11,859,808 | | 100.00 | % |

Election of John S. Horejsi as a Class I Director of the Fund

(only preferred stockholders vote)

| | # of Votes Cast | | % of Votes Cast | |

Affirmative | | 713 | | 98.48 | % |

Withheld | | 11 | | 1.52 | % |

TOTAL | | 724 | | 100.00 | % |

Election of Susan L. Ciciora as a Class III Director of the Fund

(only preferred stockholders vote)

| | # of Votes Cast | | % of Votes Cast | |

Affirmative | | 713 | | 98.48 | % |

Withheld | | 11 | | 0.02 | |

TOTAL | | 724 | | 100.00 | % |

29

| DISCUSSION REGARDING THE BOARD OF DIRECTORS’ APPROVAL

OF THE INVESTMENT ADVISORY AGREEMENTS [Unaudited] |

May 31, 2009 |

Each of the Advisers has entered into an Investment Advisory Agreement with the Fund (the “Agreements”) pursuant to which the Advisers are jointly responsible for managing the Fund’s assets in accordance with its investment objectives, policies and limitations. The 1940 Act requires that the Board of Directors (the “Board”), including a majority of the Independent Directors, annually approve the terms of the Agreements. At a regularly scheduled meeting held on February 9, 2009, the Directors, by a unanimous vote (including a separate vote of the Independent Directors), approved the renewal of the Agreements.

Factors Considered

Generally, the Board considered a number of factors in renewing the Agreements including, among other things, (i) the nature, extent and quality of services to be furnished by the Advisers to the Fund; (ii) the investment performance of the Fund compared to relevant market indices and the performance of comparable funds; (iii) the advisory fees and other expenses paid by the Fund; (iv) the profitability to the Advisers of their investment advisory relationship with the Fund; (v) the extent to which economies of scale would be realized as the Fund grows and whether fee levels reflect any economies of scale; (vi) support of the Advisers by the Fund’s principal stockholders; (vii) the historical relationship between the Fund and the Advisers, and (viii) the relationship between the Advisers and its affiliated service provider, Fund Administrative Services, LLC (“FAS”). The Board also reviewed the ability of the Advisers to provide investment management and supervision services to the Fund, including the background, education and experience of the key portfolio management and operational personnel, the investment philosophy and decision-making process of those professionals, and the ethical standards maintained by the Advisers.

Deliberative Process

To assist the Board in its evaluation of the quality of the Advisers’ services and the reasonableness of the Advisers’ fees under the Agreements, the Board received a memorandum from independent legal counsel to the Independent Directors discussing the factors generally regarded as appropriate to consider in evaluating investment advisory arrangements and the duties of directors in approving such arrangements. In connection with its evaluation, the Board also requested, and received, various materials relating to the Advisers’ investment services under the Agreements. These materials included reports and presentations from the Advisers that described, among other things, the Advisers’ organizational structure, financial condition, internal controls, policies and procedures on brokerage practices, soft-dollar commissions and trade allocation, comparative investment performance results, comparative sub-advisory fees, and compliance policies and procedures. The Board also received a report prepared by an independent consultant, Lipper Analytical Services, Inc. (“Lipper”), comparing the Fund’s performance, advisory fees and expenses to a group of leveraged closed-end funds determined to be most similar to the Fund in each case as determined by Lipper. The Board also considered information received from the

30

Advisers throughout the year, including investment performance and expense ratio reports for the Fund.

In advance of the February 9, 2009 meeting, the Independent Directors held a special telephonic meeting with counsel to the Fund and the Independent Directors. The principal purpose of the meeting was to discuss the renewal of the Agreements and review the materials provided to the Board by the Advisers in connection with the annual review process. The Board held additional discussions at the February 9, 2009 Board meeting, which included a private session among the Independent Directors and their independent legal counsel at which no employees or representatives of the Advisers were present.

The information below summarizes the Board’s considerations in connection with its approval of the Agreements. In deciding to approve the Agreements, the Board did not identify a single factor as controlling and this summary does not describe all of the matters considered. However, the Board concluded that each of the various factors referred to below favored such approval.

Nature, Extent and Quality of the Services Provided; Ability to Provide Services

The Board received and considered various data and information regarding the nature, extent and quality of services provided to the Fund by the Advisers under the Agreements. Each Adviser’s most recent investment adviser registration form on the Securities and Exchange Commission’s Form ADV was provided to the Board, as were the responses of the Advisers to information requests submitted to the Advisers by the Independent Directors through their independent legal counsel. The Board reviewed and analyzed the materials, which included information about the background, education and experience of the Advisers’ key portfolio management and operational personnel and the amount of attention devoted to the Fund by the Advisers’ portfolio management personnel. In this regard, it was noted that the Advisers’ only clients are the Fund, two other registered investment companies (Boulder Growth & Income Fund, Inc. and The Denali Fund Inc.) and a charitable foundation affiliated with the Horejsi family. Based on its evaluation, the Board was satisfied that the Advisers’ investment personnel, including Stewart Horejsi, the Fund’s principal portfolio manager, would continue to devote a significant portion of their time and attention to the success of the Fund and its investment strategy. The Board also considered the Advisers’ policies and procedures for ensuring compliance with applicable laws and regulations, as well as the results of a recently completed routine examination of the Advisers and the Fund by the staff of the Securities and Exchange Commission. Based on the above factors, the Board concluded that it was generally satisfied with nature, extent and quality of the investment advisory services provided to the Fund by the Advisers, and that the Advisers possessed the ability to continue to provide these services to the Fund in the future.

31

Investment Performance

The Board considered the investment performance of the Fund since August 1999, when the Advisers became the investment managers for the Fund, as compared to both relevant indices and the performance of the Fund’s Peer Group and Universe. The Board noted that for the one-year period ended December 31, 2008, the Fund underperformed the S&P 500 Index (the “S&P”), the Fund’s primary benchmark and the Dow Jones Industrial Average (“Dow”), however it outperformed the NASDAQ Composite “NASDAQ”). For the 3 year-period ended December 31, 2008, the Board noted that the Fund outperformed the S&P and NASDAQ but underperformed the Dow. The Board further noted for the five-year period ended December 31, 2008, the Fund performed comparably to the S&P, outperformed the NASDAQ and underperformed the Dow Jones. In evaluating the Fund’s performance, the Board placed greater weight on the three- and five-year time periods.