Item 1. Reports to Stockholders

Annual report

Closed-end fund

Delaware Investments® National Municipal Income Fund

March 31, 2022

Table of Contents

Table of contents

Macquarie Asset Management (MAM) is the asset management division of Macquarie Group. MAM is a full-service asset manager offering a diverse range of products across public and private markets including fixed income, equities, multi-asset solutions, private credit, infrastructure, renewables, natural assets, real estate, and asset finance. The Public Investments business is a part of MAM and includes the following investment advisers: Macquarie Investment Management Business Trust (MIMBT), Macquarie Funds Management Hong Kong Limited, Macquarie Investment Management Austria Kapitalanlage AG, Macquarie Investment Management Global Limited, Macquarie Investment Management Europe Limited, and Macquarie Investment Management Europe S.A.

Unless otherwise noted, views expressed herein are current as of March 31, 2022, and subject to change for events occurring after such date.

The Fund is not FDIC insured and is not guaranteed. It is possible to lose the principal amount invested.

Advisory services provided by Delaware Management Company, a series of MIMBT, a US registered investment advisor.

Other than Macquarie Bank Limited ABN 46 008 583 542 ("Macquarie Bank"), any Macquarie Group entity noted in this document is not an authorized deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these other Macquarie Group entities do not represent deposits or other liabilities of Macquarie Bank. Macquarie Bank does not guarantee or otherwise provide assurance in respect of the obligations of these other Macquarie Group entities. In addition, if this document relates to an investment, (a) the investor is subject to investment risk including possible delays in repayment and loss of income and principal invested and (b) none of Macquarie Bank or any other Macquarie Group entity guarantees any particular rate of return on or the performance of the investment, nor do they guarantee repayment of capital in respect of the investment.

The Fund is governed by US laws and regulations.

All third-party marks cited are the property of their respective owners.

©2022 Macquarie Management Holdings, Inc.

Table of Contents

Portfolio management review

Delaware Investments ® National Municipal Income Fund

March 31, 2022 (Unaudited)

| Performance preview (for the year ended March 31, 2022) | | | |

| Delaware Investments National Municipal Income Fund @ market price | 1-year return | +0.92 | % |

| Delaware Investments National Municipal Income Fund @ NAV | 1-year return | -3.87 | % |

| Lipper Closed-end General and Insured Municipal Debt Funds Average (Leveraged) @ market price | 1-year return | -8.88 | % |

| Lipper Closed-end General and Insured Municipal Debt Funds Average (Leveraged) @ NAV | 1-year return | -5.81 | % |

Past performance does not guarantee future results.

Performance at market price will differ from performance at net asset value (NAV). Although market price returns tend to reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in the Fund’s distribution rate.

For complete, annualized performance for Delaware Investments National Municipal Income Fund, please see the table on page 3.

Economic backdrop

During the Fund’s fiscal year ended March 31, 2022, the US economy continued to bounce back from its sharp decline at the start of the coronavirus pandemic in 2020, benefiting as states and municipalities reopened their economies.

COVID-19 vaccines had promised to lower virus cases and hospitalization rates while boosting economic growth. New variants of the coronavirus, however, complicated the picture. The Delta variant emerged in the summer and fall. Then, in late 2021 and early 2022, the fast-spreading Omicron variant emerged, although it proved less likely than earlier variants to lead to severe health outcomes.

Despite these multiple coronavirus waves, the US economy had strong growth for the fiscal year. In the second quarter of 2021, the country’s gross domestic product (GDP) expanded by an annualized 6.7%. In the third quarter, US GDP growth slowed to 2.3%, as the Delta variant alongside supply-chain concerns weighed on economic activity. By the fourth quarter of 2021, however, national growth reached an estimated 6.9%. Robust consumer and business spending drove the increase, which came despite rising Omicron cases, a sharp pickup in inflation, and expectations for several US Federal Reserve interest rate hikes. The US economy grew by 5.7% in 2021, the country’s strongest growth for any calendar year since 1984.

As the economy continued to expand, the employment situation similarly improved throughout the fiscal year. The US jobless rate, which began the 12-month period at 6.0%, fell steadily and by March had reached 3.6% – the lowest level seen since the start of the pandemic.

As inflation accelerated, the Fed signaled it would raise interest rates off its historic lows. In March 2022, the Fed raised its federal funds short-term interest rate by 0.25 percentage points. This was the central bank’s first rate increase since late 2018. The Fed also signaled that multiple additional interest rate increases were likely to follow in 2022.

Municipal bond market conditions

The municipal bond market, as measured by the Bloomberg Municipal Bond Index, returned -4.47% for the fiscal year. That decline came amid sharply rising interest rates in the first quarter of 2022.

During the fiscal year, investors experienced two different sets of market conditions. For roughly the first three quarters of the fiscal year, municipal bonds benefited from a favorable technical backdrop – robust demand for tax-exempt debt alongside constrained supply. Other factors that boosted the performance of municipal bonds during this time frame included investors’ continued confidence in issuers’ underlying credit quality, ample fiscal stimulus from the federal government, higher-than-anticipated state and local tax collections, and expectations for higher future tax rates. With interest rates remaining low during the 12-month period, longer-dated, lower-rated municipal bonds were especially in demand due to their higher yields.

Starting in late 2021 and persisting through the rest of the fiscal year, market conditions shifted, as the Fed pivoted from seeing inflation as transitory to acting aggressively to slow rising prices. Meanwhile, concern about the Russia-Ukraine war added further uncertainty to the global economic environment. As rates in the US rose and investors expected more Fed rate hikes to come, the demand for municipal bonds steadily declined, leading to a less favorable technical backdrop for the asset class.

Yields on tax-exempt bonds rose for the fiscal year, while the municipal yield curve flattened, indicating that rates on shorter-term bonds rose more than on longer-dated bonds. Bonds with shorter maturities generally outperformed their intermediate- and longer-dated counterparts, while lower-rated bonds tended to outpace higher-quality issues.

These tables show municipal bond returns by maturity length and by credit quality for the fiscal year.

1

Table of Contents

Portfolio management review

Delaware Investments ® National Municipal Income Fund

The following tables show the returns experienced by municipal bonds of varying maturity lengths and credit ratings for the Fund's fiscal year ended March 31, 2022:

| Returns by maturity | | | |

| 1 year | | (1.51 | )% |

| 3 years | | (3.31 | )% |

| 5 years | | (4.48 | )% |

| 10 years | | (4.79 | )% |

| 22+ years | | (5.30 | )% |

| | | | |

| Returns by credit rating | | | |

| AAA | | (4.84 | )% |

| AA | | (4.59 | )% |

| A | | (4.23 | )% |

| BBB | | (3.85 | )% |

Source: Bloomberg.

A consistent management approach

We continue to manage the Fund following the same strategy we use regardless of the market backdrop. We emphasize a bottom-up investment approach, relying on our team’s thorough credit research to choose bonds on an issuer-by-issuer basis. We regularly seek tax-exempt bonds that offer the Fund’s shareholders what we see as an attractive trade-off between return opportunity and risk.

Pursuing this approach, we tend to maintain relatively less exposure to high-rated, lower-yielding bonds. Instead, we prefer to overweight bonds with lower-investment-grade or below-investment-grade credit ratings and solid underlying credit quality. We prefer to own lower-rated issues because we believe they provide the Fund with greater opportunity to add long-term value for shareholders.

For the first three-quarters of this fiscal year in particular, our purchase activity for the Fund was relatively limited. With credit spreads narrowing and interest rates falling, we saw little need to make large portfolio adjustments because the bonds we already owned in the Fund were generally more attractive to us than the new opportunities the market was offering.

When we did have funds available to invest via the proceeds of bond calls, maturities, or income payments, we sought to take advantage of attractive new issues available in the marketplace. When appropriate, we invested in longer-dated bonds in an effort to keep the Fund’s duration (interest-rate sensitivity) at our desired level.

In the first three months of 2022, as interest rates and bond yields rose and credit spreads widened, we engaged in various tax-loss swaps. With this strategy, we took advantage of opportunities to exchange bonds with lower yields for those with similar risk characteristics but higher yields. With this strategy, we improved the Fund’s income profile while also incurring a tax loss that we believe we may be able to apply to future gains.

Many of our swaps reflected a desire to enhance the Fund’s diversification. In February, the Fund acquired the assets of two state-specific tax-exempt bond funds: Delaware Investments® Minnesota Municipal Income Fund II, Inc. and Delaware Investments®Colorado Municipal Income Fund, Inc. As a result of this reorganization, the Fund gained more exposure to the Minnesota and Colorado state marketplaces than we found optimal. Thus, we quickly prioritized efforts to moderate that exposure. We swapped some Minnesota and Colorado holdings with newer ones that allowed us to achieve our diversification objectives while enhancing the Fund’s income profile. During the quarter, we made considerable progress in diversifying the Fund’s assets. We do, however, expect the diversification process to take time, given that the Minnesota and Colorado funds included various older bonds issued in much higher-interest rate environments, making them more difficult to replace in today’s lower-rate environment.

Individual performance effects

The performers for Delaware Investments National Municipal Income Fund were bonds issued for the Brightline high-speed rail project in South Florida. These nonrated bonds gained 14% for the Fund this fiscal year, far outpacing the Fund’s benchmark return. The bonds benefited from their relatively high income and limited interest rate sensitivity, as well as improved investor optimism about Brightline’s expanding market opportunity.

Bonds for the Legacy Cares athletic complex project in Mesa, Arizona also contributed to the Fund performance, gaining 11% for the fiscal year. These bonds gained ground as the issuer saw more credit improvement than investors had apparently expected. A high coupon and near-term call date also provided additional cushion for the bonds in a rising interest rate environment.

In contrast, bonds for the Chiara Communities senior housing project in Waukesha, Wisconsin, hampered results, returning -19% for the fiscal year and significantly lagging the benchmark. These bonds lagged as the issuer faced ongoing credit challenges owing to difficulties ramping up occupancy in its retirement community following the difficult pandemic years.

Other detractors from the Fund’s performance were University of North Carolina hospital bonds (-10%). These high-quality, non-callable issues struggled, largely due to their relatively extended duration, which proved a negative performance factor as interest rates rose.

2

Table of Contents

Performance summary

Delaware Investments® National Municipal Income Fund

March 31, 2022 (Unaudited)

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Please obtain the most recent performance data by calling 866 437-0252 or visiting our website at delawarefunds.com/closed-end.

| Fund performance | | | | | | | | | | | | |

| Average annual total returns through March 31, 2022 | | 1 year | | 5 year | | 10 year | | Lifetime |

| At market price | | +0.92 | % | | +4.31 | % | | +4.65 | % | | +4.69 | %* |

| At net asset value | | -3.87 | %** | | +3.78 | % | | +4.83 | % | | +4.78 | %* |

| * | The inception date of the performance shown is May 14, 1998. The Fund commenced operations on February 26, 1993. |

| ** | Total returns for the report period presented in the table differs from the return in “Financial highlights.” The total returns presented in the above table are calculated based on the net asset value (NAV) at which shareholder transactions were processed. The total returns presented in “Financial highlights” are calculated in the same manner, but also takes into account certain adjustments that are necessary under US generally accepted accounting principles (US GAAP) required in the annual report. |

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a bond that is held by a portfolio will be prepaid prior to maturity, at the time when interest rates are lower than what the bond was paying. A portfolio may then have to reinvest that money at a lower interest rate.

High yielding, non-investment-grade bonds (junk bonds) involve higher risk than investment grade bonds. Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to state or local and/or the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

Funds that have a significant percentage of assets allocated to one state may be more susceptible to the economic, regulatory, regional, and other factors of that state than more geographically diversified funds.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

The Fund’s use of leverage may expose common shareholders to additional volatility, and cause the Fund to incur certain costs. In the event that the Fund is unable to meet certain criteria (including, but not limited to, maintaining certain ratings with Fitch Ratings (Fitch), funding dividend payments or funding redemptions), the Fund will pay additional fees with respect to the leverage.

Duration number will change as market conditions change. Therefore, duration should not be solely relied upon to indicate a municipal bond fund’s potential volatility.

IBOR risk is the risk that changes related to the use of the London interbank offered rate (LIBOR) or similar rates (such as EONIA) could have adverse impacts on financial instruments that reference these rates. The abandonment of these rates and transition to alternative rates could affect the value and liquidity of instruments that reference them and could affect investment strategy performance.

The disruptions caused by natural disasters, pandemics, or similar events could prevent the Fund from executing advantageous investment decisions in a timely manner and could negatively impact the Fund’s ability to achieve its investment objective and the value of the Fund’s investments.

This document may mention bond ratings published by nationally recognized statistical rating organizations (NRSROs) Standard & Poor’s (S&P), Moody’s Investors Service, and Fitch. For securities rated by an NRSRO other than S&P, the rating is converted to the equivalent S&P credit rating. Bonds rated AAA are rated as having the highest quality and are generally considered to have the lowest degree of investment risk. Bonds rated AA are considered to be of high quality, but with a slightly higher degree of risk than bonds rated AAA. Bonds rated A are considered to have many favorable investment qualities, though they are somewhat more susceptible to adverse economic conditions. Bonds

3

Table of Contents

Performance summary

Delaware Investments® National Municipal Income Fund

rated BBB are believed to be of medium-grade quality and generally riskier over the long term. Bonds rated BB, B, and CCC are regarded as having significant speculative characteristics, with BB indicating the least degree of speculation of the three.

Closed-end fund shares do not represent a deposit or obligation of, and are not guaranteed or endorsed by, any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation or any other government agency.

Closed-end funds, unlike open-end funds, are not continuously offered. After being issued during a one-time-only public offering, shares of closed-end funds are sold in the open market through a securities exchange. Net asset value (NAV) is calculated by subtracting total liabilities by total assets, then dividing by the number of shares outstanding. At the time of sale, your shares may have a market price that is above or below NAV, and may be worth more or less than your original investment.

The Bloomberg Municipal Bond Index, mentioned on page 1, measures the total return performance of the long-term investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Returns reflect the reinvestment of all distributions. Dividends and distributions, if any, are assumed, for the purpose of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment policy. Shares of the Fund were initially offered with a sales charge of 7%. Performance since inception does not include the sales charge or any other brokerage commission for purchases made since inception.

Past performance does not guarantee future results.

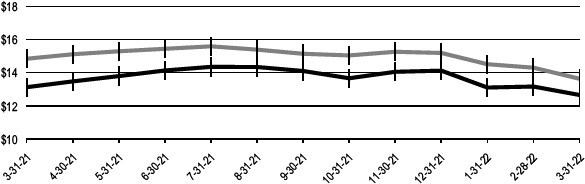

Market price versus net asset value (see notes on next page)

March 31, 2021 through March 31, 2022

| For period beginning March 31, 2012 through March 31, 2022 | | Starting value | | Ending value |

| Delaware Investments National Municipal Income Fund @ NAV | | $14.84 | | $13.63 |

| Delaware Investments National Municipal Income Fund @ market price | | $13.12 | | $12.65 |

Past performance is not a guarantee of future results.

4

Table of Contents

Performance of a $10,000 Investment

Average annual total returns from March 31, 2012 through March 31, 2022

| For period beginning March 31, 2012 through March 31, 2022 | | Starting value | | Ending value |

| Delaware Investments® National Municipal Income Fund @ NAV | | $10,000 | | $16,032 |

| Lipper Closed-end General and Insured Municipal Debt Funds Average (Leveraged) @ NAV | | $10,000 | | $15,808 |

| Delaware Investments National Municipal Income Fund @ market price | | $10,000 | | $15,761 |

| Lipper Closed-end General and Insured Municipal Debt Funds Average (Leveraged) @ market price | | $10,000 | | $15,130 |

The “Performance of a $10,000 investment” graph assumes $10,000 invested in the Fund on March 31, 2011 and includes the reinvestment of all distributions at market value. The graph assumes $10,000 in the Lipper Closed-end General and Insured Municipal Debt Funds Average (Leveraged) at market price and at NAV. Performance of the Fund and the Lipper class at market value is based on market performance during the period. Performance of the Fund and Lipper class at NAV is based on the fluctuations in NAV during the period. Delaware Investments National Municipal Income Fund was initially offered with a sales charge of 7%. For market price, performance shown in both graphs above does not include fees, the initial sales charge, or any brokerage commissions on purchases. For NAV, performance shown in both graphs above includes fees, but does not include the initial sales charge or any brokerage commissions for purchases. Investments in the Fund are not available at NAV.

The Lipper Closed-end General and Insured Municipal Debt Funds Average (Leveraged) compares closed-end funds that either invest primarily in municipal debt issues rated in the top four credit ratings or invest primarily in municipal debt issues insured as to timely payment. These funds can be leveraged via use of debt, preferred equity, and/or reverse purchase agreements (source: Lipper).

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Market price is the price an investor would pay for shares of the Fund on the secondary market. NAV is the total value of one fund share, generally equal to a fund’s net assets divided by the number of shares outstanding.

Past performance does not guarantee future results.

5

Table of Contents

Fund basics

As of March 31, 2022 (Unaudited)

Delaware Investments®

National Municipal Income Fund

Fund objective

The Fund seeks to provide current income exempt from regular

federal income tax, consistent with the preservation of capital.

Total Fund net assets

$285 million

Number of holdings

442

Fund start date

February 26, 1993

NYSE American symbol

VFL

CUSIP number

24610T108

6

Table of Contents

Security type / sector / state / territory allocations

As of March 31, 2022 (Unaudited)

Sector designations may be different from the sector designations presented in other Fund materials.

Delaware Investments® National Municipal Income Fund

| | Percentage |

| Security type / sector | | of net assets |

| Municipal Bonds* | | 146.96 | % |

| Corporate Revenue Bonds | | 6.63 | % |

| Education Revenue Bonds | | 19.16 | % |

| Electric Revenue Bonds | | 10.02 | % |

| Healthcare Revenue Bonds | | 40.06 | % |

| Housing Revenue Bonds | | 0.72 | % |

| Lease Revenue Bonds | | 7.83 | % |

| Local General Obligation Bonds | | 10.98 | % |

| Pre-Refunded/Escrowed to Maturity Bonds | | 9.33 | % |

| Special Tax Revenue Bonds | | 15.47 | % |

| State General Obligation Bonds | | 9.15 | % |

| Transportation Revenue Bonds | | 13.16 | % |

| Water & Sewer Revenue Bonds | | 4.45 | % |

| Short-Term Investments | | 1.51 | % |

| Total Value of Securities | | 148.47 | % |

| Liquidation Value of Preferred** | | (47.42 | %) |

| Liabilities Net of Receivables and Other Assets | | (1.05 | %) |

| Total Net Assets | | 100.00 | % |

| * | As of the date of this report, Delaware Investments National Municipal Income Fund held bonds issued by or on behalf of territories and the states of the US as follows: |

| | Percentage |

| State / territory | | of net assets |

| Alabama | | 0.18 | % |

| Arizona | | 2.09 | % |

| California | | 8.13 | % |

| Colorado | | 26.04 | % |

| District of Columbia | | 0.19 | % |

| Florida | | 2.78 | % |

| Georgia | | 1.33 | % |

| Guam | | 0.46 | % |

| Illinois | | 5.50 | % |

| Indiana | | 0.20 | % |

| Kansas | | 0.07 | % |

| Louisiana | | 0.73 | % |

| Maryland | | 0.27 | % |

| Massachusetts | | 0.19 | % |

| Michigan | | 0.38 | % |

| Minnesota | | 59.61 | % |

| Mississippi | | 0.35 | % |

| Missouri | | 0.53 | % |

| Montana | | 0.26 | % |

| Nebraska | | 0.09 | % |

| New Jersey | | 3.14 | % |

| New York | | 5.27 | % |

| North Carolina | | 0.22 | % |

| Ohio | | 0.87 | % |

| Oregon | | 0.19 | % |

| Pennsylvania | | 6.25 | % |

| Puerto Rico | | 19.16 | % |

| Texas | | 1.66 | % |

| Utah | | 0.24 | % |

| Virginia | | 0.85 | % |

| Washington | | 0.10 | % |

| Wisconsin | | 0.96 | % |

| Wyoming | | 0.18 | % |

| Total Value of Securities | | 148.47 | % |

| ** | More information regarding the Fund’s use of preferred shares as leverage is included in Note 6 in “Notes to financial statements.” The Fund utilizes preferred shares as leverage in an attempt to obtain a higher return for the Fund. There is no assurance that the Fund will achieve its a higher return or its investment objectives through the use of such leverage. |

7

Table of Contents

Schedule of investments

Delaware Investments® National Municipal Income Fund

March 31, 2022

| | | | | Principal | | | |

| | | | | | amount° | | Value (US $) |

| Municipal Bonds — 146.96% | | | | | |

| Corporate Revenue Bonds — 6.63% | | | | | |

| Arizona Industrial Development | | | | | |

| | Authority Revenue | | | | | |

| | (Legacy Cares, Inc. Project) | | | | | |

| | | Series A 144A 7.75% | | | | | |

| | | 7/1/50 # | | 725,000 | | $ | 821,809 |

| Buckeye Tobacco Settlement | | | | | |

| | Financing Authority | | | | | |

| | (Senior) | | | | | |

| | | Series A-2 4.00% 6/1/48 | | 900,000 | | | 903,690 |

| Central Plains Energy Project | | | | | |

| | Revenue, Nebraska | | | | | |

| | (Project No. 3) | | | | | |

| | | Series A 5.00% 9/1/36 | | 225,000 | | | 263,419 |

| Commonwealth Financing | | | | | |

| | Authority Revenue, | | | | | |

| | Pennsylvania | | | | | |

| | (Tobacco Master Settlement | | | | | |

| | | Payment) | | | | | |

| | | 4.00% 6/1/39 (AGM) | | 1,015,000 | | | 1,065,506 |

| Denver City & County | | | | | |

| | (United Airlines Project) | | | | | |

| | | 5.00% 10/1/32 (AMT) | | 215,000 | | | 221,433 |

| Florida Development Finance | | | | | |

| | Surface Transportation | | | | | |

| | Facilities Revenue | | | | | |

| | (Brightline Passenger Rail | | | | | |

| | | Project) | | | | | |

| | | Series B 144A 7.375% | | | | | |

| | | 1/1/49 (AMT) # | | 680,000 | | | 718,427 |

| | (Virgin Trains USA Passenger | | | | | |

| | | Rail Project) | | | | | |

| | | Series A 144A 6.50% | | | | | |

| | | 1/1/49 (AMT) # | | 475,000 | | | 475,879 |

| George L Smith II Congress | | | | | |

| | Center Authority Revenue | | | | | |

| | (Convention Center Hotel) | | | | | |

| | | Series A 4.00% 1/1/54 | | 2,750,000 | | | 2,697,612 |

| M-S-R Energy Authority, California | | | | | |

| | Gas | | | | | |

| | Series B 6.50% 11/1/39 | | 250,000 | | | 339,247 |

| | Series C 7.00% 11/1/34 | | 1,000,000 | | | 1,334,610 |

| New York Transportation | | | | | |

| | Development | | | | | |

| | (Delta Air Lines, Inc. - | | | | | |

| | | LaGuardia Airport Terminals | | | | | |

| | | C&D Redevelopment | | | | | |

| | | Project) | | | | | |

| | | 4.00% 1/1/36 (AMT) | | 750,000 | | | 767,115 |

| Public Authority for Colorado | | | | | |

| | Energy Natural Gas Revenue | | | | | |

| | 6.25% 11/15/28 | | 865,000 | | | 1,002,743 |

| | 6.50% 11/15/38 | | 2,250,000 | | | 3,032,100 |

| Public Finance Authority, | | | | | |

| | Wisconsin Airport Facilities | | | | | |

| | Revenue | | | | | |

| | (Grand Hyatt San Antonio Hotel | | | | | |

| | | Acquisition Project) | | | | | |

| | | 5.00% 2/1/62 | | 1,475,000 | | | 1,546,111 |

| Shoals, Indiana | | | | | |

| | (National Gypsum Project) | | | | | |

| | | 7.25% 11/1/43 (AMT) | | 310,000 | | | 323,767 |

| St. Paul Port Authority Solid Waste | | | | | |

| | Disposal Revenue | | | | | |

| | (Gerdau St. Paul Steel Mill | | | | | |

| | | Project) | | | | | |

| | | Series 7 144A 4.50% | | | | | |

| | | 10/1/37 (AMT) # | | 2,415,000 | | | 2,422,414 |

| Tobacco Settlement Financing | | | | | |

| | Corporation, Louisiana | | | | | |

| | Asset-Backed Note | | | | | |

| | | Series A 5.25% 5/15/35 | | 460,000 | | | 479,131 |

| Tobacco Settlement Financing | | | | | |

| | Corporation, New Jersey | | | | | |

| | Series A 5.00% 6/1/46 | | 130,000 | | | 141,539 |

| TSASC Revenue, New York | | | | | |

| | (Settlement) | | | | | |

| | | Series A 5.00% 6/1/41 | | 60,000 | | | 65,036 |

| Valparaiso, Indiana | | | | | |

| | (Pratt Paper Project) | | | | | |

| | | 7.00% 1/1/44 (AMT) | | 240,000 | | | 254,935 |

| | | | | | | | 18,876,523 |

| Education Revenue Bonds — 19.16% | | | | | |

| Arizona Industrial Development | | | | | |

| | Authority Revenue | | | | | |

| | (American Charter Schools | | | | | |

| | | Foundation Project) | | | | | |

| | | 144A 6.00% 7/1/47 # | | 330,000 | | | 366,066 |

8

Table of Contents

| | | | | | Principal | | | |

| | | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Education Revenue Bonds (continued) | | | | | |

| Bethel Charter School Lease | | | | | |

| | Revenue | | | | | |

| | (Spectrum High School Project) | | | | | |

| | | Series A 4.375% 7/1/52 | | 1,100,000 | | $ | 1,103,762 |

| Board of Trustees For Colorado | | | | | |

| | Mesa University Enterprise | | | | | |

| | Revenue | | | | | |

| | Series B 5.00% 5/15/49 | | 750,000 | | | 861,240 |

| Brooklyn Park Charter School | | | | | |

| | Lease Revenue | | | | | |

| | (Prairie Seeds Academy | | | | | |

| | Project) | | | | | |

| | Series A 5.00% 3/1/34 | | 990,000 | | | 1,005,196 |

| | Series A 5.00% 3/1/39 | | 170,000 | | | 171,639 |

| California Educational Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (Loma Linda University) | | | | | |

| | Series A 5.00% 4/1/47 | | 500,000 | | | 547,980 |

| | (Stanford University) | | | | | |

| | Series V-1 5.00% 5/1/49 | | 900,000 | | | 1,181,295 |

| | Series V-2 2.25% 4/1/51 | | 500,000 | | | 376,650 |

| California School Finance | | | | | |

| | Authority Revenue | | | | | |

| | (Russell Westbrook Why Not? | | | | | |

| | | Academy - Obligated Group) | | | | | |

| | | Series A 144A 4.00% | | | | | |

| | | 6/1/51 # | | 500,000 | | | 440,390 |

| Cologne Charter School Lease | | | | | |

| | Revenue | | | | | |

| | (Cologne Academy Project) | | | | | |

| | Series A 5.00% 7/1/29 | | 270,000 | | | 279,588 |

| | Series A 5.00% 7/1/45 | | 445,000 | | | 453,655 |

| Colorado Educational & Cultural | | | | | |

| | Facilities Authority Revenue | | | | | |

| | 144A 5.00% 7/1/36 # | | 500,000 | | | 517,950 |

| | 5.125% 11/1/49 | | 765,000 | | | 798,316 |

| | 144A 5.25% 7/1/46 # | | 500,000 | | | 516,180 |

| | (Alexander Dawson School- | | | | | |

| | | Nevada Project) | | | | | |

| | | 5.00% 5/15/29 | | 760,000 | | | 829,639 |

| | (Aspen View Academy Project) | | | | | |

| | | 4.00% 5/1/41 | | 175,000 | | | 177,445 |

| | (Charter School - Atlas | | | | | |

| | | Preparatory School) | | | | | |

| | | 144A 5.25% 4/1/45 # | | 700,000 | | | 700,756 |

| | (Charter School - Community | | | | | |

| | | Leadership Academy) | | | | | |

| | | 7.45% 8/1/48 | | 500,000 | | | 524,850 |

| | (Charter School - Peak to Peak | | | | | |

| | | Charter) | | | | | |

| | | 5.00% 8/15/34 | | 1,000,000 | | | 1,051,280 |

| | (Global Village Academy - | | | | | |

| | | Northglenn Project) | | | | | |

| | | 144A 5.00% 12/1/50 # | | 475,000 | | | 465,747 |

| | (Improvement - Charter School | | | | | |

| | | - University Lab School | | | | | |

| | | Building) | | | | | |

| | | 5.00% 12/15/45 | | 500,000 | | | 527,435 |

| | (Liberty Charter School) | | | | | |

| | | Series A 5.00% 1/15/44 | | 1,000,000 | | | 1,026,160 |

| | (Loveland Classical Schools) | | | | | |

| | | 144A 5.00% 7/1/36 # | | 625,000 | | | 654,087 |

| | (Science Technology | | | | | |

| | | Engineering and Math | | | | | |

| | | (Stem) School Project) | | | | | |

| | | 5.00% 11/1/54 | | 700,000 | | | 727,237 |

| | (Skyview Charter School) | | | | | |

| | | 144A 5.50% 7/1/49 # | | 750,000 | | | 772,380 |

| | (Vail Mountain School Project) | | | | | |

| | | 4.00% 5/1/46 | | 25,000 | | | 24,760 |

| Colorado School of Mines | | | | | |

| | Series B 5.00% 12/1/42 | | 270,000 | | | 275,856 |

| Deephaven Charter School | | | | | |

| | (Eagle Ridge Academy Project) | | | | | |

| | Series A 5.25% 7/1/37 | | 590,000 | | | 626,368 |

| | Series A 5.25% 7/1/40 | | 500,000 | | | 528,765 |

| Duluth Housing & Redevelopment | | | | | |

| | Authority | | | | | |

| | (Duluth Public Schools | | | | | |

| | | Academy Project) | | | | | |

| | | Series A 5.00% 11/1/48 | | 1,200,000 | | | 1,232,400 |

| Florida Development Finance | | | | | |

| | Surface Transportation | | | | | |

| | Facilities Revenue | | | | | |

| | (River City Education Services | | | | | |

| | Project) | | | | | |

| | Series A-1 5.00% 7/1/51 | | 395,000 | | | 421,749 |

| | Series A-1 5.00% 7/1/51 | | 1,330,000 | | | 1,356,494 |

| | Series A-1 5.00% 2/1/57 | | 575,000 | | | 607,160 |

| Forest Lake Minnesota Charter | | | | | |

| | School Revenue | | | | | |

| | (Lake International Language | | | | | |

| | Academy) | | | | | |

| | Series A 5.375% 8/1/50 | | 915,000 | | | 979,526 |

| | Series A 5.75% 8/1/44 | | 705,000 | | | 723,555 |

9

Table of Contents

Schedule of investments

Delaware Investments® National Municipal Income Fund

| | | | | | Principal | | | |

| | | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Education Revenue Bonds (continued) | | | | | |

| Health & Educational Facilities | | | | | |

| | Authority of the State of | | | | | |

| | Missouri | | | | | |

| | (St. Louis College of Pharmacy | | | | | |

| | | Project) | | | | | |

| | | 5.25% 5/1/33 | | 500,000 | | $ | 518,545 |

| Hugo Charter School Lease | | | | | |

| | Revenue | | | | | |

| | (Noble Academy Project) | | | | | |

| | Series A 5.00% 7/1/34 | | 255,000 | | | 260,454 |

| | Series A 5.00% 7/1/44 | | 775,000 | | | 784,765 |

| Illinois Finance Authority Revenue | | | | | |

| | (CHF - Chicago, L.L.C. - | | | | | |

| | | University Of Illinois at | | | | | |

| | | Chicago Project) | | | | | |

| | | Series A 5.00% 2/15/50 | | 460,000 | | | 489,983 |

| | (Chicago International Charter | | | | | |

| | | School Project) | | | | | |

| | | 5.00% 12/1/47 | | 535,000 | | | 574,140 |

| Louisiana Public Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (Provident Group-Flagship | | | | | |

| | | Properties) | | | | | |

| | | Series A 5.00% 7/1/56 | | 500,000 | | | 531,730 |

| Massachusetts Development | | | | | |

| | Finance Agency | | | | | |

| | (Umass Boston Student | | | | | |

| | | Housing Project) | | | | | |

| | | 5.00% 10/1/48 | | 285,000 | | | 305,315 |

| Minneapolis Charter School Lease | | | | | |

| | Revenue | | | | | |

| | (Hiawatha Academies Project) | | | | | |

| | Series A 5.00% 7/1/36 | | 750,000 | | | 776,280 |

| | Series A 5.00% 7/1/47 | | 900,000 | | | 922,725 |

| Minneapolis Student Housing | | | | | |

| | Revenue | | | | | |

| | (Riverton Community Housing | | | | | |

| | Project) | | | | | |

| | 5.25% 8/1/39 | | 205,000 | | | 211,312 |

| | 5.50% 8/1/49 | | 990,000 | | | 1,020,819 |

| Minnesota Higher Education | | | | | |

| | Facilities Authority Revenue | | | | | |

| | (Carleton College) | | | | | |

| | 4.00% 3/1/36 | | 485,000 | | | 516,210 |

| | 5.00% 3/1/44 | | 905,000 | | | 1,016,939 |

| | (College of St. Benedict) | | | | | |

| | | 4.00% 3/1/36 | | 410,000 | | | 426,962 |

| | (Gustavus Adolphus College) | | | | | |

| | | 5.00% 10/1/47 | | 2,600,000 | | | 2,879,526 |

| | (Macalester College) | | | | | |

| | 4.00% 3/1/42 | | 900,000 | | | 958,887 |

| | 4.00% 3/1/48 | | 600,000 | | | 638,904 |

| | (St. Catherine University) | | | | | |

| | Series A 4.00% 10/1/38 | | 920,000 | | | 961,529 |

| | Series A 5.00% 10/1/45 | | 785,000 | | | 865,957 |

| | (St. Johns University) | | | | | |

| | Series 8-I 5.00% 10/1/31 | | 235,000 | | | 256,077 |

| | Series 8-I 5.00% 10/1/34 | | 35,000 | | | 38,086 |

| | (St. Olaf College) | | | | | |

| | | Series 8-N 4.00% 10/1/35 | | 590,000 | | | 624,090 |

| | (Trustees Of The Hamline | | | | | |

| | | University Of Minnesota) | | | | | |

| | | Series B 5.00% 10/1/47 | | 1,055,000 | | | 1,094,024 |

| | (University of St. Thomas) | | | | | |

| | 4.00% 10/1/44 | | 645,000 | | | 673,928 |

| | 5.00% 10/1/40 | | 750,000 | | | 857,168 |

| | Series A 4.00% 10/1/37 | | 500,000 | | | 532,135 |

| Otsego Charter School | | | | | |

| | (Kaleidoscope Charter School) | | | | | |

| | Series A 5.00% 9/1/34 | | 230,000 | | | 233,742 |

| | Series A 5.00% 9/1/44 | | 400,000 | | | 402,864 |

| Philadelphia, Pennsylvania | | | | | |

| | Authority for Industrial | | | | | |

| | Development | | | | | |

| | (1st Philadelphia Preparatory | | | | | |

| | | College) | | | | | |

| | | Series A 7.25% 6/15/43 | | 370,000 | | | 401,935 |

| Phoenix, Arizona Industrial | | | | | |

| | Development Authority | | | | | |

| | Revenue | | | | | |

| | (Rowan University Project) | | | | | |

| | | 5.00% 6/1/42 | | 1,000,000 | | | 1,004,870 |

| Pima County, Arizona Industrial | | | | | |

| | Development Authority | | | | | |

| | (Edkey Charter Schools | | | | | |

| | | Project) | | | | | |

| | | 144A 5.00% 7/1/49 # | | 500,000 | | | 507,335 |

| St. Cloud Charter School Lease | | | | | |

| | Revenue | | | | | |

| | (Stride Academy Project) | | | | | |

| | | Series A 5.00% 4/1/46 | | 375,000 | | | 300,938 |

10

Table of Contents

| | | | | Principal | | | |

| | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Education Revenue Bonds (continued) | | | | | |

| St. Paul Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Charter School Lease Revenue | | | | | |

| | (Academia Cesar Chavez | | | | | |

| | School Project) | | | | | |

| | Series A 5.25% 7/1/50 | | 825,000 | | $ | 829,076 |

| | (Great River School Project) | | | | | |

| | Series A 144A 4.75% 7/1/29 # | | 100,000 | | | 103,444 |

| | Series A 144A 5.50% 7/1/38 # | | 240,000 | | | 255,686 |

| | (Twin Cities Academy Project) | | | | | |

| | Series A 5.30% 7/1/45 | | 630,000 | | | 659,503 |

| University of California | | | | | |

| | Series AI 5.00% 5/15/32 | | 1,000,000 | | | 1,036,000 |

| University of Minnesota | | | | | |

| | Series A 5.00% 9/1/40 | | 1,240,000 | | | 1,408,863 |

| | Series A 5.00% 9/1/42 | | 2,000,000 | | | 2,269,620 |

| | Series A 5.00% 4/1/44 | | 1,500,000 | | | 1,739,310 |

| University of Texas System Board | | | | | |

| | of Regents | | | | | |

| | Series B 5.00% 8/15/49 | | 1,000,000 | | | 1,295,260 |

| University of Wyoming | | | | | |

| | Series C 4.00% 6/1/43 (AGM) | | 460,000 | | | 499,132 |

| | | | | | | 54,537,624 |

| Electric Revenue Bonds – 10.02% | | | | | |

| Central Minnesota Municipal | | | | | |

| | Power Agency | | | | | |

| | (Brookings - Southeast Twin | | | | | |

| | Cities Transmission Project) | | | | | |

| | 3.00% 1/1/38 (AGM) | | 300,000 | | | 299,109 |

| Chaska Electric Revenue | | | | | |

| | Series A 5.00% 10/1/28 | | 445,000 | | | 486,260 |

| City of Fort Collins Electric Utility | | | | | |

| | Enterprise Revenue | | | | | |

| | Series A 5.00% 12/1/42 | | 500,000 | | | 573,625 |

| City of Loveland Colorado Electric | | | | | |

| | & Communications Enterprise | | | | | |

| | Revenue | | | | | |

| | Series A 5.00% 12/1/44 | | 1,060,000 | | | 1,213,965 |

| Long Island Power Authority, New | | | | | |

| | York Electric System Revenue | | | | | |

| | 5.00% 9/1/47 | | 305,000 | | | 341,603 |

| | Series A 5.00% 9/1/44 | | 250,000 | | | 265,355 |

| | Series B 5.00% 9/1/46 | | 130,000 | | | 143,350 |

| Minnesota Municipal Power | | | | | |

| | Agency Electric Revenue | | | | | |

| | 5.00% 10/1/25 | | 500,000 | | | 536,965 |

| | 5.00% 10/1/26 | | 500,000 | | | 536,210 |

| | 5.00% 10/1/27 | | 320,000 | | | 343,011 |

| | 5.00% 10/1/47 | | 1,755,000 | | | 1,921,743 |

| Northern Municipal Power Agency | | | | | |

| | Series A 5.00% 1/1/26 | | 100,000 | | | 102,404 |

| | Series A 5.00% 1/1/30 | | 340,000 | | | 348,174 |

| Philadelphia, Pennsylvania Gas | | | | | |

| | Works Revenue | | | | | |

| | (1998 General Ordinance | | | | | |

| | Fifteenth Series) | | | | | |

| | 5.00% 8/1/47 | | 500,000 | | | 547,580 |

| Puerto Rico Electric Power | | | | | |

| | Authority Revenue | | | | | |

| | Series A 5.05% 7/1/42 ‡ | | 320,000 | | | 306,400 |

| | Series AAA 5.25% 7/1/25 ‡ | | 180,000 | | | 173,250 |

| | Series CCC 5.25% 7/1/27 | | 1,450,000 | | | 1,395,625 |

| | Series WW 5.00% 7/1/28 ‡ | | 1,400,000 | | | 1,340,500 |

| | Series WW 5.25% 7/1/33 | | 95,000 | | | 91,438 |

| | Series WW 5.50% 7/1/17 ‡ | | 210,000 | | | 202,387 |

| | Series WW 5.50% 7/1/19 ‡ | | 160,000 | | | 154,200 |

| | Series XX 4.75% 7/1/26 ‡ | | 190,000 | | | 181,213 |

| | Series XX 5.25% 7/1/40 | | 2,305,000 | | | 2,218,562 |

| | Series XX 5.75% 7/1/36 ‡ | | 680,000 | | | 659,600 |

| | Series ZZ 4.75% 7/1/27 ‡ | | 155,000 | | | 147,831 |

| | Series ZZ 5.00% 7/1/19 ‡ | | 280,000 | | | 267,400 |

| | Series ZZ 5.25% 7/1/24 ‡ | | 250,000 | | | 240,625 |

| Rochester Electric Utility Revenue | | | | | |

| | Series A 5.00% 12/1/42 | | 605,000 | | | 669,808 |

| | Series A 5.00% 12/1/47 | | 985,000 | | | 1,082,328 |

| Southern Minnesota Municipal | | | | | |

| | Power Agency Supply Revenue | | | | | |

| | Series A 5.00% 1/1/41 | | 240,000 | | | 261,170 |

| | Series A 5.00% 1/1/47 | | 1,650,000 | | | 1,851,465 |

| St. Paul Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Charter School Lease Revenue | | | | | |

| | Series A 4.00% 10/1/33 | | 285,000 | | | 298,848 |

| | Series B 4.00% 10/1/37 | | 800,000 | | | 834,344 |

| Western Minnesota Municipal | | | | | |

| | Power Agency Supply Revenue | | | | | |

| | Series A 5.00% 1/1/25 | | 3,000,000 | | | 3,076,170 |

| | Series A 5.00% 1/1/26 | | 1,000,000 | | | 1,025,090 |

| | Series A 5.00% 1/1/49 | | 3,860,000 | | | 4,389,360 |

| | | | | | | 28,526,968 |

| Healthcare Revenue Bonds – 40.06% | | | | | |

| Alabama Special Care Facilities | | | | | |

| | Financing Authority- | | | | | |

| | Birmingham Alabama | | | | | |

| | (Methodist Home for the Aging) | | | | | |

| | 6.00% 6/1/50 | | 500,000 | | | 511,580 |

11

Table of Contents

Schedule of investments

Delaware Investments® National Municipal Income Fund

| | | | | Principal | | | |

| | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Healthcare Revenue Bonds (continued) | | | | | |

| Allegheny County Hospital, | | | | | |

| | Pennsylvania Development | | | | | |

| | Authority | | | | | |

| | (Allegheny Health Network | | | | | |

| | Obligated Group Issue) | | | | | |

| | Series A 4.00% 4/1/44 | | 300,000 | | $ | 313,509 |

| Anoka Health Care Facilities | | | | | |

| | Revenue | | | | | |

| | 5.375% 11/1/34 | | 610,000 | | | 629,404 |

| Apple Valley Senior Housing | | | | | |

| | Revenue | | | | | |

| | (PHS Senior Housing, Inc. | | | | | |

| | Orchard Path Project) | | | | | |

| | 4.50% 9/1/53 | | 1,160,000 | | | 1,165,951 |

| | 5.00% 9/1/58 | | 1,605,000 | | | 1,611,404 |

| Apple Valley Senior Living | | | | | |

| | Revenue | | | | | |

| | (Senior Living LLC Project) | | | | | |

| | Series B 5.00% 1/1/47 | | 715,000 | | | 481,881 |

| | 4th Tier | | | | | |

| | Series D 7.00% 1/1/37 | | 685,000 | | | 507,023 |

| | Series D 7.25% 1/1/52 | | 1,035,000 | | | 712,743 |

| Arizona Industrial Development | | | | | |

| | Authority Revenue | | | | | |

| | (Great Lakes Senior Living | | | | | |

| | Communities LLC Project) | | | | | |

| | Series B 5.00% 1/1/49 | | 70,000 | | | 50,227 |

| | Series D-2 144A 7.75% 1/1/54 # | | 50,000 | | | 35,132 |

| | (Phoenix Children's Hospital) | | | | | |

| | Series A 4.00% 2/1/50 | | 755,000 | | | 782,580 |

| Bethel Housing & Health Care | | | | | |

| | Facilities Revenue | | | | | |

| | (Benedictine Health System- | | | | | |

| | St. Peter Communities | | | | | |

| | Project) | | | | | |

| | | Series A 5.50% 12/1/48 | | 500,000 | | | 489,015 |

| Brookhaven Development | | | | | |

| | Authority Revenue, Georgia | | | | | |

| | (Children's Healthcare of | | | | | |

| | Atlanta) | | | | | |

| | Series A 4.00% 7/1/49 | | 30,000 | | | 31,610 |

| California Health Facilities | | | | | |

| | Financing Authority | | | | | |

| | Series A 4.00% 4/1/49 | | 1,000,000 | | | 1,018,200 |

| California Health Facilities | | | | | |

| | Financing Authority Revenue | | | | | |

| | (Kaiser Permanente) | | | | | |

| | Series A-2 5.00% 11/1/47 | | 1,030,000 | | | 1,305,937 |

| Center City Health Care Facilities | | | | | |

| | Revenue | | | | | |

| | (Hazelden Betty Ford | | | | | |

| | Foundation Project) | | | | | |

| | 5.00% 11/1/27 | | 500,000 | | | 532,780 |

| City of Bethel | | | | | |

| | (The Lodge at Lakes at | | | | | |

| | Stillwater Project) | | | | | |

| | 5.25% 6/1/58 | | 1,775,000 | | | 1,741,026 |

| City of Center City, Minnesota | | | | | |

| | Healthcare Facilities Revenue | | | | | |

| | Refunding | | | | | |

| | (Hazelden Betty Ford | | | | | |

| | Foundation Project) | | | | | |

| | 4.00% 11/1/41 | | 200,000 | | | 210,270 |

| City of Crookston, Minnesota | | | | | |

| | Health Care Facilities Revenue | | | | | |

| | (Riverview Health Project) | | | | | |

| | 5.00% 5/1/51 | | 1,390,000 | | | 1,354,597 |

| Colorado Health Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (Aberdeen Ridge) | | | | | |

| | Series A 5.00% 5/15/49 | | 500,000 | | | 478,520 |

| | (AdventHealth Obligated | | | | | |

| | Group) | | | | | |

| | Series A 3.00% 11/15/51 | | 500,000 | | | 441,875 |

| | Series A 4.00% 11/15/43 | | 1,000,000 | | | 1,058,250 |

| | (Adventist Health System/ | | | | | |

| | Sunbelt Obligated Group) | | | | | |

| | Series A 5.00% 11/15/48 | | 1,000,000 | | | 1,122,540 |

| | (Bethesda Project) | | | | | |

| | Series A-1 5.00% 9/15/48 | | 750,000 | | | 798,368 |

| | (Boulder Community Health | | | | | |

| | Project) | | | | | |

| | 4.00% 10/1/38 | | 250,000 | | | 267,385 |

| | 4.00% 10/1/39 | | 250,000 | | | 266,965 |

| | 4.00% 10/1/40 | | 280,000 | | | 298,323 |

| | (Cappella of Grand Junction | | | | | |

| | Project) | | | | | |

| | 144A 5.00% 12/1/54 # | | 695,000 | | | 586,365 |

| | (CommonSpirit Health) | | | | | |

| | Series A-1 4.00% 8/1/39 | | 550,000 | | | 577,209 |

| | Series A-2 4.00% 8/1/49 | | 2,500,000 | | | 2,594,075 |

| | Series A-2 5.00% 8/1/39 | | 1,500,000 | | | 1,698,495 |

| | Series A-2 5.00% 8/1/44 | | 1,500,000 | | | 1,681,365 |

| | (Covenant Living Communities | | | | | |

| | and Services) | | | | | |

| | Series A 4.00% 12/1/40 | | 750,000 | | | 809,355 |

12

Table of Contents

| | | | | | Principal | | | |

| | | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Healthcare Revenue Bonds (continued) | | | | | |

| Colorado Health Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (Covenant Retirement | | | | | |

| | | Communities Inc.) | | | | | |

| | | 5.00% 12/1/35 | | 1,000,000 | | $ | 1,069,090 |

| | (Healthcare Facilities - | | | | | |

| | | American Baptist) | | | | | |

| | | 8.00% 8/1/43 | | 830,000 | | | 861,523 |

| | (Mental Health Center of | | | | | |

| | | Denver Project) | | | | | |

| | | Series A 5.75% 2/1/44 | | 1,500,000 | | | 1,559,880 |

| | (National Jewish Health | | | | | |

| | | Project) | | | | | |

| | | 5.00% 1/1/27 | | 500,000 | | | 501,015 |

| | (Sanford Health) | | | | | |

| | | Series A 5.00% 11/1/44 | | 2,000,000 | | | 2,249,180 |

| | (SCL Health System) | | | | | |

| | Series A 4.00% 1/1/37 | | 575,000 | | | 613,962 |

| | Series A 4.00% 1/1/38 | | 1,950,000 | | | 2,076,301 |

| | Series A 4.00% 1/1/39 | | 465,000 | | | 494,397 |

| | (Sunny Vista Living Center) | | | | | |

| | | Series A 144A 6.25% | | | | | |

| | | 12/1/50 # | | 505,000 | | | 442,355 |

| | (Vail Valley Medical Center | | | | | |

| | | Project) | | | | | |

| | | 5.00% 1/15/35 | | 1,250,000 | | | 1,356,125 |

| Cuyahoga County, Ohio Hospital | | | | | |

| | Revenue | | | | | |

| | (The Metrohealth System) | | | | | |

| | | 5.50% 2/15/57 | | 1,000,000 | | | 1,110,520 |

| Dakota County Community | | | | | |

| | Development Agency Senior | | | | | |

| | Housing Revenue | | | | | |

| | (Walker Highview Hills Project) | | | | | |

| | Series A 144A 5.00% 8/1/46 # | | 370,000 | | | 371,121 |

| | Series A 144A 5.00% 8/1/51 # | | 755,000 | | | 757,159 |

| Deephaven Housing & Healthcare | | | | | |

| | Revenue | | | | | |

| | (St. Therese Senior Living | | | | | |

| | Project) | | | | | |

| | Series A 5.00% 4/1/38 | | 280,000 | | | 270,721 |

| | Series A 5.00% 4/1/40 | | 270,000 | | | 257,963 |

| Denver Health & Hospital | | | | | |

| | Authority Health Care Revenue | | | | | |

| | Series A 4.00% 12/1/40 | | 500,000 | | | 525,335 |

| Duluth Economic Development | | | | | |

| | Authority | | | | | |

| | (Essentia Health Obligated | | | | | |

| | | Group) | | | | | |

| | | Series A 5.00% 2/15/48 | | 810,000 | | | 903,199 |

| | (St. Luke’s Hospital of Duluth | | | | | |

| | | Obligated Group) | | | | | |

| | | Unrefunded Balance 6.00% | | | | | |

| | | 6/15/39 | | 980,000 | | | 989,427 |

| Escambia County Health Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (Healthcare Facilities - Baptist) | | | | | |

| | | Series A 4.00% 8/15/50 | | 1,540,000 | | | 1,565,687 |

| Glendale, Arizona Industrial | | | | | |

| | Development Authority | | | | | |

| | (Royal Oaks - Inspirata Pointe | | | | | |

| | | Project) | | | | | |

| | | Series A 5.00% 5/15/56 | | 500,000 | | | 531,940 |

| Hamilton County, Ohio Hospital | | | | | |

| | Revenue | | | | | |

| | (Cincinnati Children's Hospital | | | | | |

| | | Medical Center Project) | | | | | |

| | | Series CC 5.00% 11/15/49 | | 345,000 | | | 442,297 |

| Hayward | | | | | |

| | (American Baptist Homes | | | | | |

| | | Midwest) | | | | | |

| | | 5.75% 2/1/44 | | 500,000 | | | 459,805 |

| Hayward Health Care Facilities | | | | | |

| | Revenue | | | | | |

| | (St. John's Lutheran Home of | | | | | |

| | | Albert Lea) | | | | | |

| | | 5.375% 10/1/44 | | 260,000 | | | 237,687 |

| Housing & Redevelopment | | | | | |

| | Authority of The City of St Paul | | | | | |

| | Minnesota | | | | | |

| | Series A 5.00% 12/1/30 | | 300,000 | | | 342,981 |

| Illinois Finance Authority Revenue | | | | | |

| | (NorthShore - Edward-Elmhurst | | | | | |

| | | Health Credit Group) | | | | | |

| | | Series A 5.00% 8/15/47 | | 3,355,000 | | | 3,882,775 |

| Kalispell, Montana | | | | | |

| | (Immanuel Lutheran | | | | | |

| | | Corporation Project) | | | | | |

| | | Series A 5.25% 5/15/37 | | 700,000 | | | 731,507 |

13

Table of Contents

Schedule of investments

Delaware Investments® National Municipal Income Fund

| | | | | Principal | | | |

| | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Healthcare Revenue Bonds (continued) | | | | | |

| Lancaster County Hospital | | | | | |

| | Authority | | | | | |

| | (Penn State Health) | | | | | |

| | 5.00% 11/1/51 | | 2,345,000 | | $ | 2,628,628 |

| Maple Grove Health Care | | | | | |

| | Facilities Revenue | | | | | |

| | (Maple Grove Hospital | | | | | |

| | Corporation) | | | | | |

| | 4.00% 5/1/37 | | 1,000,000 | | | 1,058,240 |

| | (North Memorial Health Care) | | | | | |

| | 5.00% 9/1/30 | | 865,000 | | | 935,420 |

| Maple Plain Senior Housing & | | | | | |

| | Health Care Revenue | | | | | |

| | (Haven Homes Project) | | | | | |

| | 5.00% 7/1/54 | | 1,500,000 | | | 1,506,045 |

| Maryland Health & Higher | | | | | |

| | Educational Facilities Authority | | | | | |

| | (University of Maryland Medical | | | | | |

| | System Issue) | | | | | |

| | Series D 4.00% 7/1/48 | | 255,000 | | | 267,737 |

| Miami-Dade County, Florida | | | | | |

| | Health Facilities Authority | | | | | |

| | Revenue | | | | | |

| | (Nicklaus Children's Hospital | | | | | |

| | Project) | | | | | |

| | 5.00% 8/1/47 | | 200,000 | | | 221,520 |

| Michigan Finance Authority | | | | | |

| | Revenue | | | | | |

| | (Beaumont Health Credit | | | | | |

| | Group) | | | | | |

| | 5.00% 11/1/44 | | 1,000,000 | | | 1,083,970 |

| Minneapolis Health Care System | | | | | |

| | Revenue | | | | | |

| | (Fairview Health Services) | | | | | |

| | Series A 4.00% 11/15/48 | | 2,855,000 | | | 2,914,098 |

| | Series A 5.00% 11/15/33 | | 500,000 | | | 543,110 |

| | Series A 5.00% 11/15/34 | | 500,000 | | | 543,110 |

| | Series A 5.00% 11/15/49 | | 2,000,000 | | | 2,254,340 |

| Minneapolis Senior Housing & | | | | | |

| | Healthcare Revenue | | | | | |

| | (Ecumen Mill City Quarter) | | | | | |

| | 5.25% 11/1/45 | | 850,000 | | | 850,221 |

| | 5.375% 11/1/50 | | 200,000 | | | 200,166 |

| | (Ecumen-Abiitan Mill City | | | | | |

| | Project) | | | | | |

| | 5.00% 11/1/35 | | 220,000 | | | 219,776 |

| Minneapolis – St. Paul Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Health Care Revenue | | | | | |

| | (Allina Health System) | | | | | |

| | Series A 5.00% 11/15/29 | | 585,000 | | | 661,910 |

| Monroe County, New York | | | | | |

| | Industrial Development | | | | | |

| | Revenue | | | | | |

| | (Rochester Regional Health | | | | | |

| | Project) | | | | | |

| | Series A 4.00% 12/1/46 | | 440,000 | | | 453,218 |

| Montgomery County Higher | | | | | |

| | Education and Health Authority | | | | | |

| | (Thomas Jefferson University) | | | | | |

| | Series A 4.00% 9/1/49 | | 750,000 | | | 770,715 |

| | Series B 4.00% 5/1/56 | | 1,000,000 | | | 1,017,620 |

| Moon, Pennsylvania Industrial | | | | | |

| | Development Authority | | | | | |

| | (Baptist Homes Society | | | | | |

| | Obligation) | | | | | |

| | 6.125% 7/1/50 | | 750,000 | | | 776,025 |

| New Hope, Texas Cultural | | | | | |

| | Education Facilities | | | | | |

| | (Cardinal Bay Inc.) | | | | | |

| | Series A1 5.00% 7/1/51 ‡ | | 135,000 | | | 102,600 |

| | Series B 4.75% 7/1/51 | | 160,000 | | | 88,000 |

| New Jersey Health Care Facilities | | | | | |

| | Financing Authority Revenue | | | | | |

| | (St. Peters University Hospital) | | | | | |

| | 6.25% 7/1/35 | | 300,000 | | | 300,678 |

| | (Valley Health System | | | | | |

| | Obligated) | | | | | |

| | 4.00% 7/1/44 | | 475,000 | | | 509,570 |

| New York State Dormitory | | | | | |

| | Authority | | | | | |

| | Series A 4.00% 7/1/53 | | 355,000 | | | 367,400 |

| | (Orange Regional Medical | | | | | |

| | Center) | | | | | |

| | 144A 5.00% 12/1/35 # | | 500,000 | | | 557,520 |

| | (Personal Income Tax) | | | | | |

| | 4.00% 3/15/48 | | 4,000,000 | | | 4,182,340 |

| Oregon State Facilities Authority | | | | | |

| | Revenue | | | | | |

| | (Peacehealth Project) | | | | | |

| | Series A 5.00% 11/15/29 | | 500,000 | | | 529,905 |

| Palomar Health, California | | | | | |

| | 5.00% 11/1/39 | | 130,000 | | | 142,401 |

14

Table of Contents

| | | | | | Principal | | | |

| | | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Healthcare Revenue Bonds (continued) | | | | | |

| Pennsylvania Higher Educational | | | | | |

| | Facilities Authority Revenue | | | | | |

| | (University of Pennsylvania | | | | | |

| | | Health System) | | | | | |

| | | Series A 4.00% 8/15/43 | | 1,905,000 | | $ | 2,025,244 |

| Rochester Health Care & Housing | | | | | |

| | Revenue | | | | | |

| | (The Homestead at Rochester | | | | | |

| | | Project) | | | | | |

| | | Series A 6.875% 12/1/48 | | 1,220,000 | | | 1,260,175 |

| Rochester Health Care Facilities | | | | | |

| | Revenue | | | | | |

| | (Mayo Clinic) | | | | | |

| | 4.00% 11/15/41 | | 4,860,000 | | | 4,874,871 |

| | 5.00% 11/15/57 | | 2,175,000 | | | 2,537,551 |

| Sartell Health Care Facilities | | | | | |

| | Revenue | | | | | |

| | (Country Manor Campus | | | | | |

| | Project) | | | | | |

| | Series A 5.25% 9/1/30 | | 1,000,000 | | | 1,001,660 |

| | Series A 5.30% 9/1/37 | | 600,000 | | | 601,500 |

| Shakopee Health Care Facilities | | | | | |

| | Revenue | | | | | |

| | (St. Francis Regional Medical | | | | | |

| | Center) | | | | | |

| | 4.00% 9/1/31 | | 205,000 | | | 213,020 |

| | 5.00% 9/1/34 | | 165,000 | | | 175,441 |

| St. Cloud Health Care Revenue | | | | | |

| | (Centracare Health System | | | | | |

| | Project) | | | | | |

| | 4.00% 5/1/49 | | 1,585,000 | | | 1,673,475 |

| | 5.00% 5/1/48 | | 3,150,000 | | | 3,569,359 |

| | Series A 4.00% 5/1/37 | | 1,295,000 | | | 1,366,614 |

| | Series A 5.00% 5/1/46 | | 4,800,000 | | | 5,247,120 |

| | Series B 5.00% 5/1/24 | | 1,400,000 | | | 1,482,026 |

| St. Paul Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Health Care Facilities Revenue | | | | | |

| | (Fairview Health Services) | | | | | |

| | Series A 4.00% 11/15/43 | | 905,000 | | | 930,476 |

| | Series A 5.00% 11/15/47 | | 680,000 | | | 755,976 |

| | (Health Partners Obligation | | | | | |

| | Group Project) | | | | | |

| | Series A 5.00% 7/1/29 | | 2,000,000 | | | 2,165,960 |

| | Series A 5.00% 7/1/32 | | 1,100,000 | | | 1,189,122 |

| St. Paul Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Housing & Health Care | | | | | |

| | Facilities Revenue | | | | | |

| | Series A 5.00% 12/1/36 | | 750,000 | | | 838,717 |

| | (Senior Episcopal Homes | | | | | |

| | | Project) | | | | | |

| | | 5.125% 5/1/48 | | 1,200,000 | | | 1,206,240 |

| Tarrant County, Texas Cultural | | | | | |

| | Education Facilities Finance | | | | | |

| | (Buckner Senior Living - | | | | | |

| | | Ventana Project) | | | | | |

| | | Series A 6.75% 11/15/47 | | 250,000 | | | 266,725 |

| University of North Carolina Board | | | | | |

| | of Governors | | | | | |

| | 5.00% 2/1/49 | | 500,000 | | | 620,310 |

| Washington Health Care Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (CommonSpirit Health) | | | | | |

| | | Series A-2 5.00% 8/1/38 | | 250,000 | | | 283,465 |

| Westminster, Maryland | | | | | |

| | (Lutheran Village Millers Grant) | | | | | |

| | | Series A 6.00% 7/1/34 | | 500,000 | | | 526,360 |

| Wisconsin Health & Educational | | | | | |

| | Facilities Authority | | | | | |

| | (Covenant Communities, Inc. | | | | | |

| | | Project) | | | | | |

| | | Series B 5.00% 7/1/53 | | 1,000,000 | | | 786,080 |

| Woodbury Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Revenue | | | | | |

| | (St. Therese of Woodbury) | | | | | |

| | | 5.125% 12/1/44 | | 1,250,000 | | | 1,255,912 |

| Yavapai County, Arizona Industrial | | | | | |

| | Development Authority | | | | | |

| | Revenue | | | | | |

| | (Yavapai Regional Medical | | | | | |

| | | Center) | | | | | |

| | | Series A 5.00% 8/1/28 | | 720,000 | | | 749,657 |

| | | | | | | | 114,057,250 |

| Housing Revenue Bonds – 0.72% | | | | | |

| Minnesota Housing Finance | | | | | |

| | Agency | | | | | |

| | (Non Ace - State Appropriated | | | | | |

| | | Housing) | | | | | |

| | | Series C 5.00% 8/1/33 | | 1,390,000 | | | 1,475,902 |

15

Table of Contents

Schedule of investments

Delaware Investments® National Municipal Income Fund

| | | | | | Principal | | | |

| | | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Housing Revenue Bonds (continued) | | | | | |

| Northwest Multi-County Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | (Pooled Housing Program) | | | | | |

| | | 5.50% 7/1/45 | | 560,000 | | $ | 563,298 |

| | | | | | | | 2,039,200 |

| Lease Revenue Bonds – 7.83% | | | | | |

| Denver Health & Hospital | | | | | |

| | Authority | | | | | |

| | (550 ACOMA, Inc.) | | | | | |

| | | 4.00% 12/1/38 | | 500,000 | | | 525,220 |

| Metropolitan Pier & | | | | | |

| | Exposition Authority Illinois | | | | | |

| | Revenue | | | | | |

| | (McCormick Place Expansion) | | | | | |

| | 4.00% 6/15/50 | | 1,375,000 | | | 1,367,066 |

| | 5.00% 6/15/50 | | 290,000 | | | 309,433 |

| | Series B 2.855% 12/15/54 (BAM) ^ | | 990,000 | | | 243,362 |

| Minnesota State General Fund | | | | | |

| | Revenue Appropriations | | | | | |

| | Series A 5.00% 6/1/32 | | 780,000 | | | 807,620 |

| | Series A 5.00% 6/1/38 | | 5,500,000 | | | 5,692,170 |

| | Series A 5.00% 6/1/43 | | 1,750,000 | | | 1,808,905 |

| Minnesota State Housing Finance | | | | | |

| | Agency | | | | | |

| | (Non Ace - State Appropriated | | | | | |

| | | Housing) | | | | | |

| | | Series C 5.00% 8/1/36 | | 1,000,000 | | | 1,060,400 |

| New Jersey Economic | | | | | |

| | Development Authority | | | | | |

| | (Transit Transportation Project) | | | | | |

| | | Series A 4.00% 11/1/44 | | 400,000 | | | 408,984 |

| New Jersey State Transportation | | | | | |

| | Trust Fund Authority | | | | | |

| | (Capital Appreciation) | | | | | |

| | | Series A 3.114% | | | | | |

| | | 12/15/39 (BAM) ^ | | 5,290,000 | | | 2,776,721 |

| | (Transportation Program) | | | | | |

| | | Series B 4.00% 6/15/50 | | 1,000,000 | | | 1,010,650 |

| New York Liberty Development | | | | | |

| | Revenue | | | | | |

| | (4 World Trade Center Project) | | | | | |

| | | Series A 3.00% 11/15/51 | | 3,640,000 | | | 3,149,328 |

| State of Colorado Department of | | | | | |

| | | Transportation | | | | | |

| | | Certificates of Participation | | | | | |

| | | 5.00% 6/15/34 | | 340,000 | | | 374,184 |

| | | 5.00% 6/15/36 | | 545,000 | | | 597,968 |

| Virginia Commonwealth | | | | | |

| | Transportation Board | | | | | |

| | (U.S. Route 58 Corridor | | | | | |

| | | Development Program) | | | | | |

| | | 4.00% 5/15/47 | | 2,000,000 | | | 2,155,140 |

| | | | | | | | 22,287,151 |

| Local General Obligation Bonds – 10.98% | | | |

| Adams & Weld Counties School | | | | | |

| | District No 27J Brighton | | | | | |

| | 4.00% 12/1/30 | | 700,000 | | | 747,579 |

| Arapahoe County School District | | | | | |

| | No. 6 Littleton | | | | | |

| | Series A 5.50% 12/1/38 | | 650,000 | | | 778,876 |

| Beacon Point Metropolitan District | | | | | |

| | 5.00% 12/1/30 (AGM) | | 600,000 | | | 659,370 |

| Boulder Valley School District No | | | | | |

| | RE-2 Boulder | | | | | |

| | Series A 4.00% 12/1/48 | | 500,000 | | | 543,585 |

| Brainerd Independent School | | | | | |

| | District No. 181 | | | | | |

| | (General Obligation School | | | | | |

| | Building Bonds) | | | | | |

| | Series A 4.00% 2/1/38 | | 1,500,000 | | | 1,597,110 |

| | Series A 4.00% 2/1/43 | | 1,500,000 | | | 1,586,625 |

| Chicago Board of Education, | | | | | |

| | Illinois | | | | | |

| | 5.00% 4/1/42 | | 205,000 | | | 218,870 |

| | 5.00% 4/1/46 | | 210,000 | | | 223,526 |

| Chicago, Illinois | | | | | |

| | Series A 5.50% 1/1/34 | | 225,000 | | | 241,090 |

| | Series C 5.00% 1/1/38 | | 500,000 | | | 532,625 |

| Duluth Independent School | | | | | |

| | District No. 709 | | | | | |

| | Series A 4.00% 2/1/27 | | 600,000 | | | 639,924 |

| Duluth, Minnesota | | | | | |

| | (Improvement DECC) | | | | | |

| | | Series A 5.00% 2/1/34 | | 545,000 | | | 600,530 |

| Edina Independent School District | | | | | |

| | No. 273 | | | | | |

| | Series A 5.00% 2/1/27 | | 1,500,000 | | | 1,626,525 |

| Grand River Hospital District | | | | | |

| | 5.25% 12/1/37 (AGM) | | 675,000 | | | 766,814 |

| Hennepin County | | | | | |

| | Series A 5.00% 12/1/36 | | 300,000 | | | 337,896 |

| | Series A 5.00% 12/1/37 | | 1,240,000 | | | 1,421,487 |

| | Series A 5.00% 12/1/41 | | 1,060,000 | | | 1,189,394 |

16

Table of Contents

| | | | | Principal | | | |

| | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Local General Obligation Bonds (continued) | | | |

| Jefferson County School District | | | | | |

| | No. R-1 | | | | | |

| | 5.25% 12/15/24 | | 750,000 | | $ | 816,375 |

| Mahtomedi Independent School | | | | | |

| | District No. 832 | | | | | |

| | (School Building) | | | | | |

| | Series A 5.00% 2/1/28 | | 515,000 | | | 557,554 |

| Mesa County Valley School | | | | | |

| | District No. 51 Grand Junction | | | | | |

| | 4.00% 12/1/41 | | 1,000,000 | | | 1,102,150 |

| Minneapolis Special School | | | | | |

| | District No. 1 | | | | | |

| | Series A 4.00% 2/1/36 | | 190,000 | | | 208,103 |

| | Series A 4.00% 2/1/37 | | 250,000 | | | 273,195 |

| | Series A 4.00% 2/1/38 | | 260,000 | | | 283,408 |

| | Series B 4.00% 2/1/36 | | 400,000 | | | 438,112 |

| | Series B 4.00% 2/1/37 | | 530,000 | | | 579,173 |

| | Series B 4.00% 2/1/38 | | 550,000 | | | 599,517 |

| Mounds View Independent School | | | | | |

| | District No. 621 | | | | | |

| | (School Building) | | | | | |

| | Series A 4.00% 2/1/43 | | 2,000,000 | | | 2,109,000 |

| New York City, New York | | | | | |

| | Series C 5.00% 8/1/43 | | 500,000 | | | 573,020 |

| St. Michael-Albertville | | | | | |

| | Independent School District No. | | | | | |

| | 885 | | | | | |

| | (School Building) | | | | | |

| | Series A 5.00% 2/1/27 | | 1,300,000 | | | 1,446,601 |

| St. Paul Independent School | | | | | |

| | District No. 625 | | | | | |

| | (School Building) | | | | | |

| | Series B 5.00% 2/1/26 | | 1,000,000 | | | 1,028,350 |

| Verve Metropolitan District No 1 | | | | | |

| | 5.00% 12/1/51 | | 1,000,000 | | | 1,009,270 |

| Weld County School District No. | | | | | |

| | RE-1 | | | | | |

| | 5.00% 12/15/30 (AGM) | | 500,000 | | | 559,340 |

| Weld County School District No. | | | | | |

| | RE-2 Eaton | | | | | |

| | Series 2 5.00% 12/1/44 | | 1,250,000 | | | 1,469,512 |

| Weld County School District No. | | | | | |

| | RE-3J | | | | | |

| | 5.00% 12/15/34 (BAM) | | 1,000,000 | | | 1,115,850 |

| Weld County School District No. | | | | | |

| | RE-8 | | | | | |

| | 5.00% 12/1/31 | | 510,000 | | | 573,459 |

| | 5.00% 12/1/32 | | 340,000 | | | 381,987 |

| White Bear Lake Independent | | | | | |

| | School District No. 624 | | | | | |

| | Series A 3.00% 2/1/43 | | 2,595,000 | | | 2,433,591 |

| | | | | | | 31,269,393 |

| Pre-Refunded/Escrowed to Maturity Bonds – 9.33% | | | |

| Colorado Educational & Cultural | | | | |

| | Facilities Authority Revenue | | | | | |

| | (Johnson & Wales University) | | | | |

| | Series A 5.25% 4/1/37-23 § | | 900,000 | | | 930,213 |

| Colorado Health Facilities | | | | | |

| | Authority Revenue | | | | | |

| | (Covenant Retirement | | | | | |

| | Communities Inc.) | | | | | |

| | Series A 5.75% | | | | | |

| | 12/1/36-23 § | | 1,000,000 | | | 1,064,980 |

| | (Evangelical Lutheran Good | | | | | |

| | Samaritan Society) | | | | | |

| | 5.00% 6/1/28-23 § | | 1,250,000 | | | 1,296,750 |

| | 5.50% 6/1/33-23 § | | 2,000,000 | | | 2,086,220 |

| | 5.625% 6/1/43-23 § | | 1,000,000 | | | 1,044,540 |

| | (Frasier Meadows Retirement | | | | |

| | Community Project) | | | | | |

| | Series B 5.00% 5/15/48 | | 340,000 | | | 351,937 |

| Colorado School of Mines | | | | | |

| | Series B 5.00% 12/1/42-22 § | 1,115,000 | | | 1,141,258 |

| Commerce City | | | | | |

| | 5.00% 8/1/44-24 (AGM) § | | 1,000,000 | | | 1,055,970 |

| Deephaven Charter School | | | | | |

| | (Eagle Ridge Academy Project) | | | | |

| | Series A 5.50% 7/1/43-23 § | | 500,000 | | | 522,950 |

| Denver City & County Airport | | | | | |

| | System Revenue | | | | | |

| | Series B 5.00% 11/15/37-22 § | | 1,700,000 | | | 1,738,624 |

| Duluth Economic Development | | | | | |

| | Authority | | | | | |

| | (St. Luke’s Hospital of Duluth | | | | | |

| | Obligated Group) | | | | | |

| | 6.00% 6/15/39-22 | | 20,000 | | | 20,192 |

| East Hempfield Township, | | | | | |

| | Pennsylvania Industrial | | | | | |

| | Development Authority | | | | | |

| | (Student Services Income - | | | | | |

| | Student Housing Project) | | | | | |

| | 5.00% 7/1/35-23 § | | 1,000,000 | | | 1,040,410 |

| Eaton Area Park & Recreation | | | | | |

| | District | | | | | |

| | 5.25% 12/1/34-22 § | | 190,000 | | | 194,849 |

| JEA Electric System Revenue, | | | | | |

| | Florida | | | | | |

| | Series A 5.00% 10/1/33-23 § | 645,000 | | | 675,618 |

17

Table of Contents

Schedule of investments

Delaware Investments® National Municipal Income Fund

| | | | | Principal | | | |

| | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Pre-Refunded/Escrowed to Maturity Bonds (continued) | |

| Minnesota Higher Education | | | | | |

| | Facilities Authority Revenue | | | | | |

| | (St. Catherine University) | | | | | |

| | Series 7-Q 5.00% | | | | | |

| | 10/1/32-22 § | | 700,000 | | $ | 712,971 |

| New Hope, Texas Cultural | | | | | |

| | Education Facilities | | | | | |

| | (Chief-Collegiate Housing- | | | | | |

| | Tarleton St.) | | | | | |

| | Series A 5.00% 4/1/34-24 § | | 1,000,000 | | | 1,059,220 |

| New Jersey Economic | | | | | |

| | Development Authority | | | | | |

| | Series WW 5.25% | | | | | |

| | 6/15/30-25 § | | 1,000,000 | | | 1,099,040 |

| New Jersey Economic | | | | | |

| | Development Authority | | | | | |

| | Revenue | | | | | |

| | (Cigarette Tax) | | | | | |

| | 5.00% 6/15/28-22 § | | 200,000 | | | 201,596 |

| | 5.00% 6/15/29-22 § | | 800,000 | | | 806,384 |

| Palm Beach County Health | | | | | |

| | Facilities Authority, Florida | | | | | |

| | (Sinai Residences Boca Raton | | | | | |

| | Project) | | | | | |

| | Series A 7.50% 6/1/49 | | 105,000 | | | 108,150 |

| Philadelphia, Pennsylvania Water | | | | | |

| | & Wastewater Revenue | | | | | |

| | Series A 5.00% 7/1/45-24 § | | 500,000 | | | 533,620 |

| Rice County Educational Facilities | | | | | |

| | Revenue | | | | | |

| | (Shattuck-St. Mary's School) | | | | | |

| | Series A 144A 5.00% | | | | | |

| | 8/1/22 # | | 900,000 | | | 911,601 |

| Rochester Electric Utility Revenue | | | | | |

| | Series B 5.00% 12/1/30-23 § | | 1,300,000 | | | 1,368,614 |

| | Series B 5.00% 12/1/43-23 § | | 1,000,000 | | | 1,052,780 |

| St. Paul Housing & | | | | | |

| | Redevelopment Authority | | | | | |

| | Hospital Facility | | | | | |

| | (Healtheast Care System | | | | | |

| | Project) | | | | | |

| | Series A 5.00% 11/15/29-25 § | | 395,000 | | | 435,409 |

| | Series A 5.00% 11/15/30-25 § | | 290,000 | | | 319,667 |

| Tallyn's Reach Metropolitan | | | | | |

| | District No. 3 | | | | | |

| | (Limited Tax Convertible) | | | | | |

| | 5.125% 11/1/38-23 § | | 295,000 | | | 309,187 |

| Western Minnesota Municipal | | | | | |

| | Power Agency Supply Revenue | | | | | |

| | Series A 5.00% 1/1/33-24 § | | 1,000,000 | | | 1,054,820 |

| | Series A 5.00% 1/1/40-24 § | | 750,000 | | | 791,115 |

| | Series A 5.00% 1/1/46-24 § | | 2,500,000 | | | 2,637,050 |

| | | | | | | 26,565,735 |

| Special Tax Revenue Bonds – 15.47% | | | | | |

| Central Platte Valley Metropolitan | | | | | |

| | District | | | | | |

| | 5.00% 12/1/43 | | 375,000 | | | 381,758 |

| Fountain Urban Renewal Authority | | | | | |

| | Tax Increment Revenue | | | | | |

| | (Academy Highlands Project) | | | | | |

| | Series A 5.50% 11/1/44 | | 655,000 | | | 659,821 |

| GDB Debt Recovery Authority of | | | | | |

| | Puerto Rico | | | | | |

| | 7.50% 8/20/40 | | 4,542,695 | | | 4,270,133 |

| Lincoln Park Metropolitan District | | | | | |

| | 5.00% 12/1/46 (AGM) | | 500,000 | | | 552,870 |

| Massachusetts Bay Transportation | | | | | |

| | Authority Senior | | | | | |

| | Series A 5.25% 7/1/29 | | 200,000 | | | 239,862 |

| Miami-Dade County | | | | | |

| | (Capital Appreciation) | | | | | |

| | 0.00% 10/1/37 (BAM) ^ | | 3,000,000 | | | 1,723,050 |

| Minneapolis Revenue | | | | | |

| | (YMCA Greater Twin Cities | | | | | |

| | Project) | | | | | |

| | 4.00% 6/1/29 | | 165,000 | | | 168,411 |

| Northampton County, | | | | | |

| | Pennsylvania Industrial | | | | | |

| | Development Authority | | | | | |

| | Revenue | | | | | |

| | (Route 33 Project) | | | | | |

| | 7.00% 7/1/32 | | 205,000 | | | 213,196 |

| Prairie Center Metropolitan District | | | | | |

| | No. 3 | | | | | |

| | Series A 144A 5.00% | | | | | |

| | 12/15/41 # | | 500,000 | | | 510,570 |

| Public Finance Authority, | | | | | |

| | Wisconsin Airport Facilities | | | | | |

| | Revenue | | | | | |

| | (American Dream @ | | | | | |

| | Meadowlands Project) | | | | | |

| | 144A 7.00% 12/1/50 # | | 380,000 | | | 385,069 |

18

Table of Contents

| | | | | Principal | | | |

| | | | amount° | | Value (US $) |

| Municipal Bonds (continued) | | | | | |

| Special Tax Revenue Bonds (continued) | | | | | |