Exhibit 99.1

Amedisys, Inc.

NASDAQ: AMED

May 2005

Forward Looking Statements

Statements contained in this presentation which are not historical facts are forward-looking statements. These forward-looking statements and all other statements that may be contained in this presentation that are not historical facts are subject to a number of risks and uncertainties, and actual results may differ materially than those forecasted. Such forward-looking statements are estimates reflecting the best judgment of Amedisys, Inc. management based upon currently available information. Certain factors which could affect the accuracy of such forward-looking statements are identified in the public filings made by Amedisys, Inc. with the Securities and Exchange Commission, and forward-looking statements contained herein, or other public statements of Amedisys, Inc. or its management should be considered in light of those factors.

1

Investment Highlights

Large, growing, and fragmented industry

Focus on Medicare home nursing

Strong internal growth

Demonstrated ability to identify and integrate acquisitions

Proven operating model

Experienced management team

2

Management Team

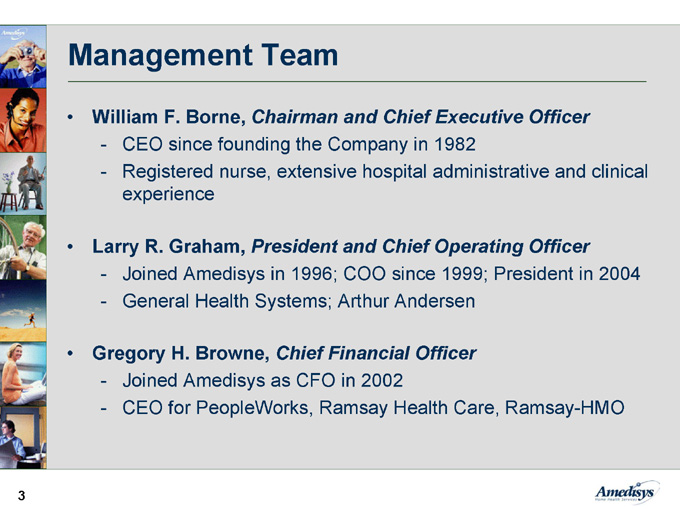

William F. Borne, Chairman and Chief Executive Officer

CEO since founding the Company in 1982

Registered nurse, extensive hospital administrative and clinical experience

Larry R. Graham, President and Chief Operating Officer

Joined Amedisys in 1996; COO since 1999; President in 2004

General Health Systems; Arthur Andersen

Gregory H. Browne, Chief Financial Officer

Joined Amedisys as CFO in 2002

CEO for PeopleWorks, Ramsay Health Care, Ramsay-HMO

3

Corporate Overview

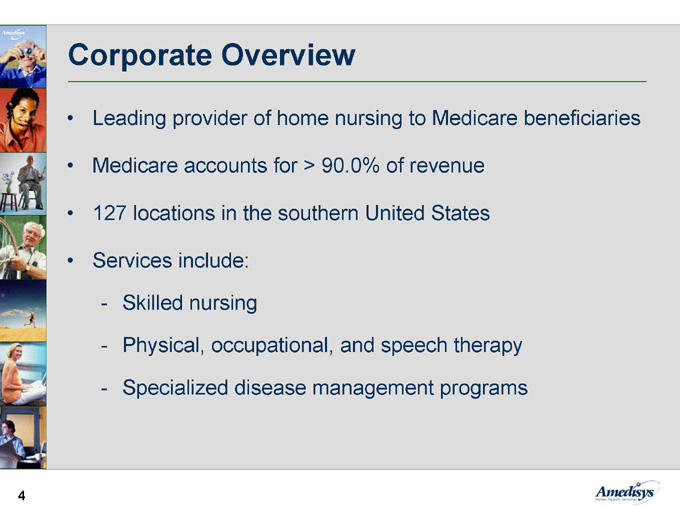

Leading provider of home nursing to Medicare beneficiaries

Medicare accounts for > 90.0% of revenue

127 locations in the southern United States

Services include:

Skilled nursing

Physical, occupational, and speech therapy

Specialized disease management programs

4

Our Locations

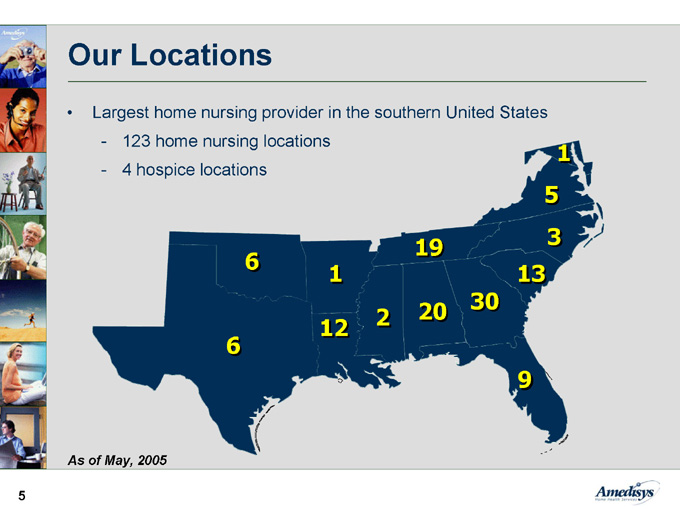

Largest home nursing provider in the southern United States

123 home nursing locations

4 hospice locations

1

5

3

19

6

13

1

30

2

20

12

6

9

As of May, 2005

5

Our Strategy

Focus on Medicare-eligible patients

Prioritize internal growth

Develop and deploy specialized nursing programs

Leverage cost-efficient operating structure

Grow through strategic acquisitions

6

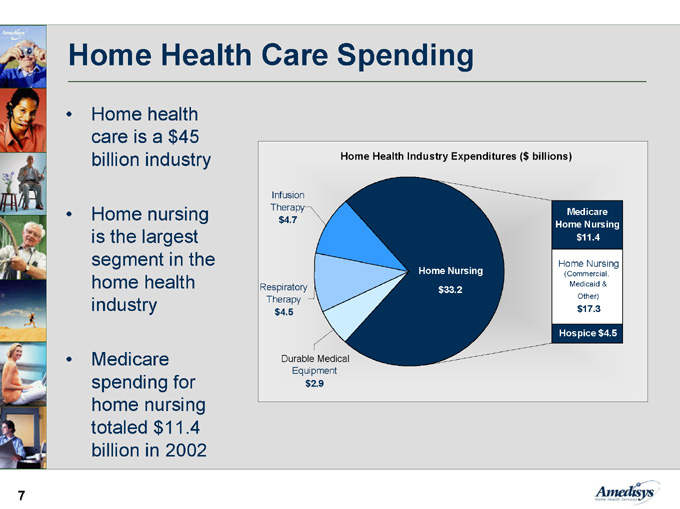

Home Health Care Spending

Home health care is a $45 billion industry

Home nursing is the largest segment in the home health industry

Medicare spending for home nursing totaled $11.4 billion in 2002

Home Health Industry Expenditures ($ billions)

Infusion

Therapy

Medicare

Home Nursing

$4.7

$11.4

Home Nursing

Home Nursing

(Commercial,

Respiratory

$33.2

Medicaid &

Therapy

Other)

$4.5

$17.3

Hospice $4.5

Durable Medical

Equipment

$2.9

7

Home Nursing Market

Industry is highly fragmented

7,000 Medicare-certified nursing agencies

Most are single site or small regional providers:

Independently-owned agencies

Visiting nurse associations

Facility- and hospital-based agencies

Publicly-owned providers account for less than 5.0% of the home nursing market

8

Industry Growth Drivers

Trend from inpatient to home-based care:

Patient preference

Payor incentives

Technology advancements

Demographics – aging population

Increased prevalence of chronic and co-morbid conditions

9

Internal Growth

Strong recent internal growth in Medicare admissions

- Approximately 21% for 1Q 2005

Internal growth being driven by:

Overall industry growth

Expanded and more effective sales force

Comprehensive range of clinical programs

Enhanced referral source education efforts

Increased focus on start-ups

10

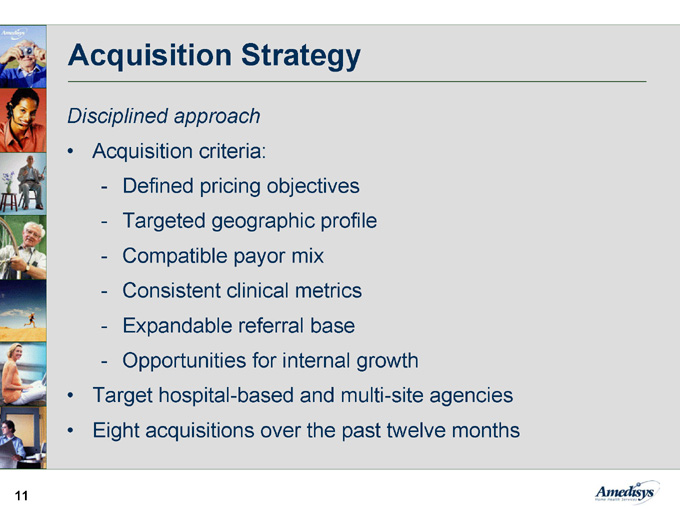

Acquisition Strategy

Disciplined approach

Acquisition criteria:

Defined pricing objectives

Targeted geographic profile

Compatible payor mix

Consistent clinical metrics

Expandable referral base

Opportunities for internal growth

Target hospital-based and multi-site agencies

Eight acquisitions over the past twelve months

11

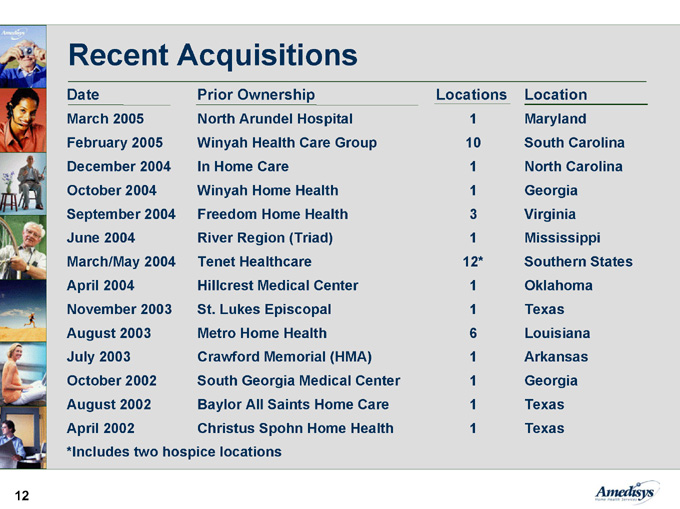

Recent Acquisitions

Date

Prior Ownership

Locations

Location

March 2005

North Arundel Hospital

1

Maryland

Winyah Health Care Group

10

South Carolina February 2005 In Home Care 1 North Carolina December 2004

October 2004

Winyah Home Health

1

Georgia

September 2004

Freedom Home Health 3 Virginia June 2004 River Region (Triad) 1 Mississippi

March/May 2004

Tenet Healthcare 12*

Southern States

April 2004

Hillcrest Medical Center 1 Oklahoma November 2003 St. Lukes Episcopal 1 Texas August 2003 Metro Home Health 6

Louisiana

July 2003 Crawford Memorial (HMA) 1 Arkansas October 2002 South Georgia Medical Center 1 Georgia August 2002

Baylor All Saints Home Care 1 Texas April 2002 Christus Spohn Home Health 1 Texas

*Includes two hospice locations

12

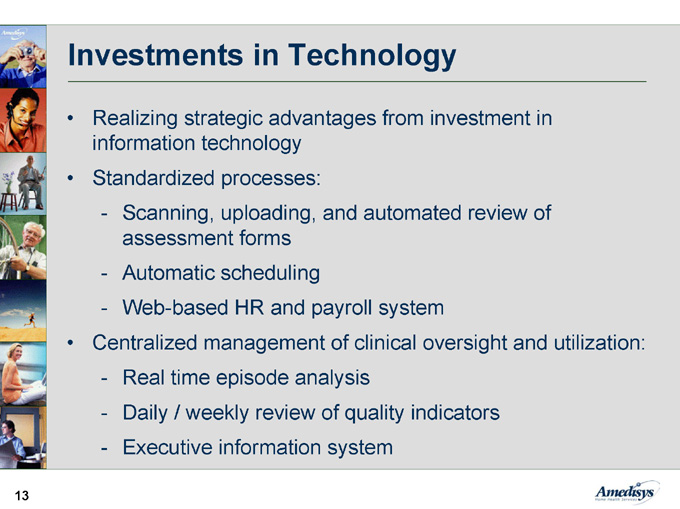

Investments in Technology

Realizing strategic advantages from investment in information technology

Standardized processes:

Scanning, uploading, and automated review of assessment forms

Automatic scheduling

Web-based HR and payroll system

Centralized management of clinical oversight and utilization:

Real time episode analysis

Daily / weekly review of quality indicators

Executive information system

13

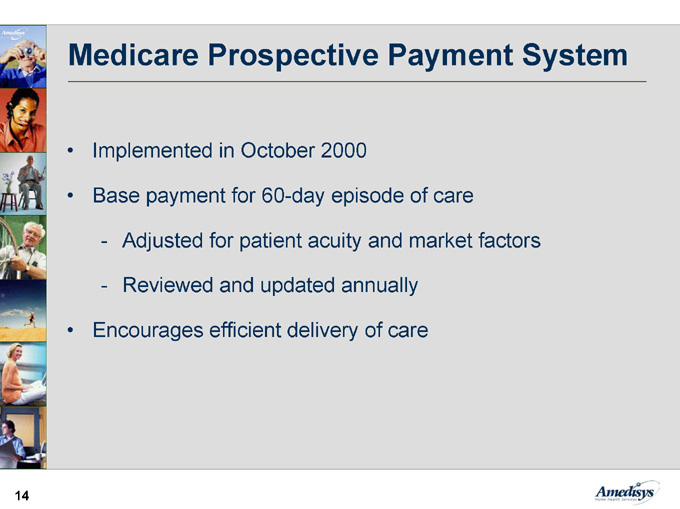

Medicare Prospective Payment System

Implemented in October 2000

Base payment for 60-day episode of care

Adjusted for patient acuity and market factors

Reviewed and updated annually

Encourages efficient delivery of care

14

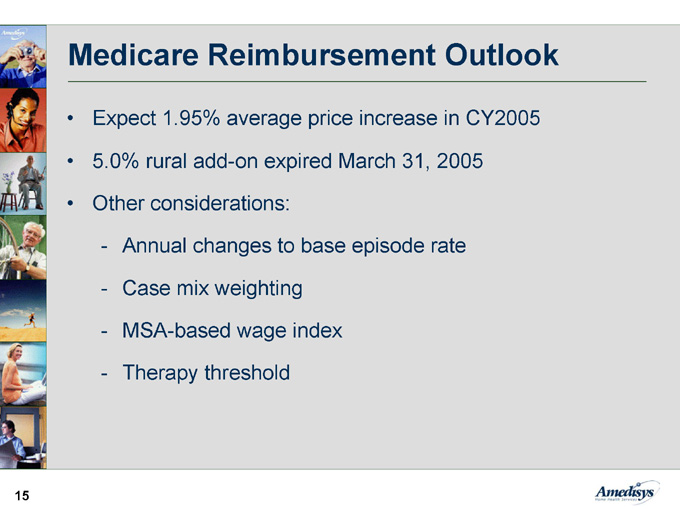

Medicare Reimbursement Outlook

Expect 1.95% average price increase in CY2005

5.0% rural add-on expired March 31, 2005

Other considerations:

Annual changes to base episode rate

Case mix weighting

MSA-based wage index

Therapy threshold

15

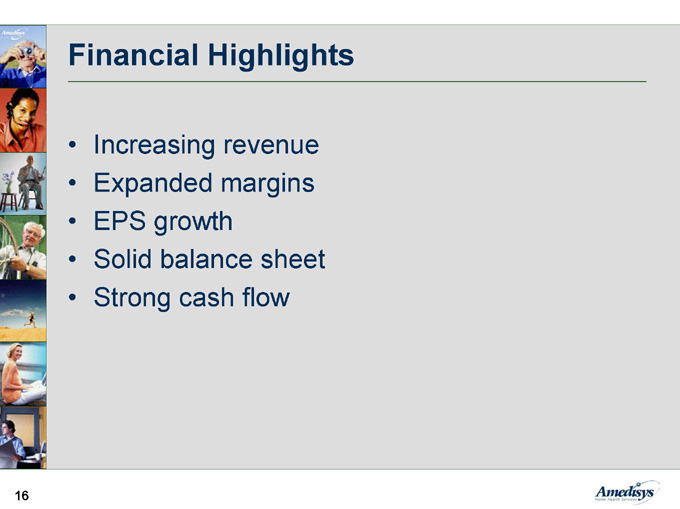

Financial Highlights

Increasing revenue

Expanded margins

EPS growth

Solid balance sheet

Strong cash flow

16

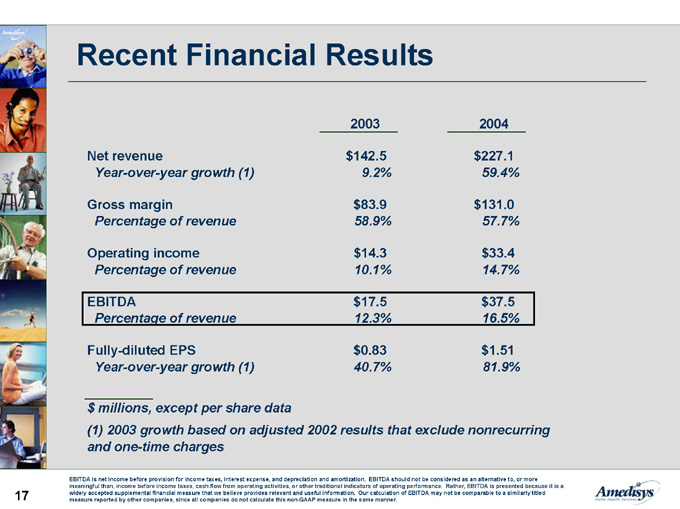

Recent Financial Results

2003 2004 $142.5 Net revenue

$227.1 9.2% Year-over-year growth (1) 59.4% $83.9 Gross margin $131.0 58.9% Percentage of revenue 57.7% $14.3

Operating income $33.4 10.1% Percentage of revenue 14.7%

$37.5

$17.5

EBITDA

12.3%

Percentage of revenue

16.5%

$0.83

Fully-diluted EPS

$1.51

40.7%

Year-over-year growth (1)

81.9%

$ millions, except per share data

(1) 2003 growth based on adjusted 2002 results that exclude nonrecurring

and one-time charges

EBITDA is net income before provision for income taxes, interest expense, and depreciation and amortization. EBITDA should not be considered as an alternative to, or more meaningful than, income before income taxes, cash flow from operating activities, or other traditional indicators of operating performance. Rather, EBITDA is presented because it is a widely accepted supplemental financial measure that we believe provides relevant and useful information. Our calculation of EBITDA may not be comparable to a similarly titled measure reported by other companies, since all companies do not calculate this non-GAAP measure in the same manner.

17

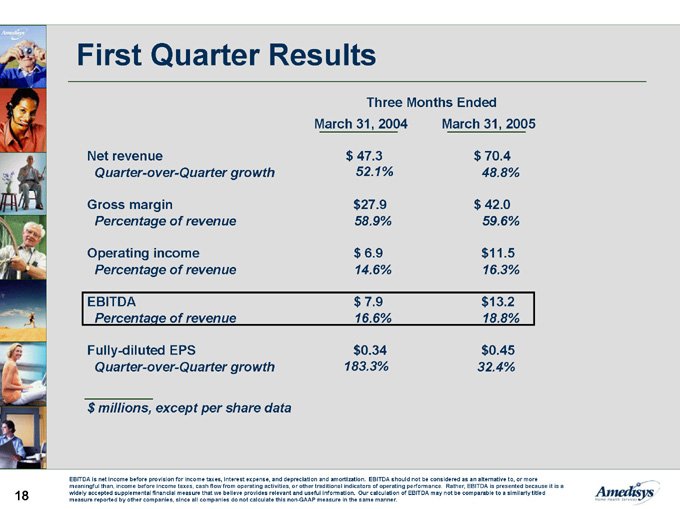

First Quarter Results

Three Months Ended

March 31, 2004

March 31, 2005

$ 47.3 Net revenue $ 70.4 48.8%

Quarter-over-Quarter growth

52.1% $27.9 Gross margin $ 42.0 58.9% Percentage of revenue 59.6% $ 6.9 Operating income

$11.5

14.6%

Percentage of revenue

16.3%

$13.2

$ 7.9

EBITDA

16.6%

Percentage of revenue

18.8%

$0.34

Fully-diluted EPS

$0.45

32.4%

Quarter-over-Quarter growth

183.3%

$ millions, except per share data

EBITDA is net income before provision for income taxes, interest expense, and depreciation and amortization. EBITDA should not be considered as an alternative to, or more meaningful than, income before income taxes, cash flow from operating activities, or other traditional indicators of operating performance. Rather, EBITDA is presented because it is a widely accepted supplemental financial measure that we believe provides relevant and useful information. Our calculation of EBITDA may not be comparable to a similarly titled measure reported by other companies, since all companies do not calculate this non-GAAP measure in the same manner.

18

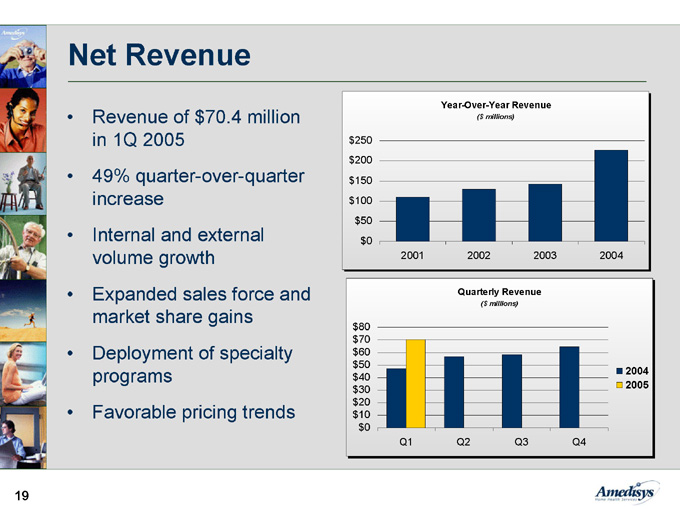

Net Revenue

Revenue of $70.4 million in 1Q 2005

49% quarter-over-quarter increase

Internal and external volume growth

Expanded sales force and market share gains

Deployment of specialty programs

Favorable pricing trends

Year-Over-Year Revenue

($ millions)

$250 $200 $150 $100 $50 $0 2003 2002 2001 2004

Quarterly Revenue

($ millions)

$80 $70 $60 $50 $40 2004

2005

$30

$20

$10

$0

Q3

Q4

Q1

Q2

19

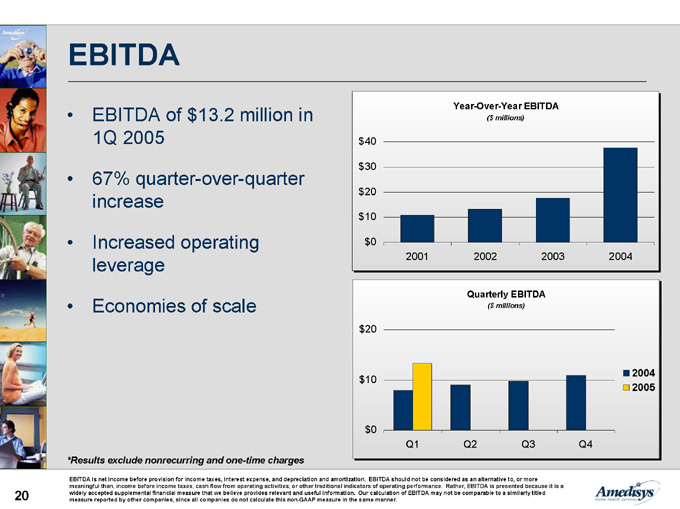

EBITDA

Year-Over-Year EBITDA

EBITDA of $13.2 million in 1Q 2005 67% quarter-over-quarter increase

Increased operating leverage

Economies of scale

($ millions)

$40 $30 $20 $10 $0 2004 2003 2002 2001

Quarterly EBITDA

($ millions)

$20 2004 $10 2005 $0 Q4 Q3 Q2 Q1

*Results exclude nonrecurring and one-time charges

EBITDA is net income before provision for income taxes, interest expense, and depreciation and amortization. EBITDA should not be considered as an alternative to, or more meaningful than, income before income taxes, cash flow from operating activities, or other traditional indicators of operating performance. Rather, EBITDA is presented because it is a widely accepted supplemental financial measure that we believe provides relevant and useful information. Our calculation of EBITDA may not be comparable to a similarly titled measure reported by other companies, since all companies do not calculate this non-GAAP measure in the same manner.

20

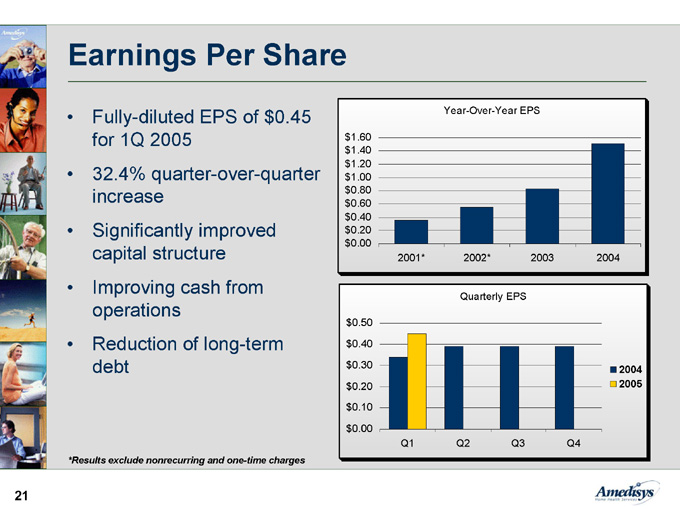

Earnings Per Share

Fully-diluted EPS of $0.45 for 1Q 2005

32.4% quarter-over-quarter increase

Significantly improved capital structure

Improving cash from operations

Reduction of long-term debt

Year-Over-Year EPS

$1.60 $1.40 $1.20 $1.00 $0.80 $0.60 $0.40 $0.20 $0.00 2003 2002* 2001* 2004

Quarterly EPS

$0.50 $0.40 $0.30 2004 $0.20 2005 $0.10 $0.00 Q3 Q2 Q1 Q4

*Results exclude nonrecurring and one-time charges

21

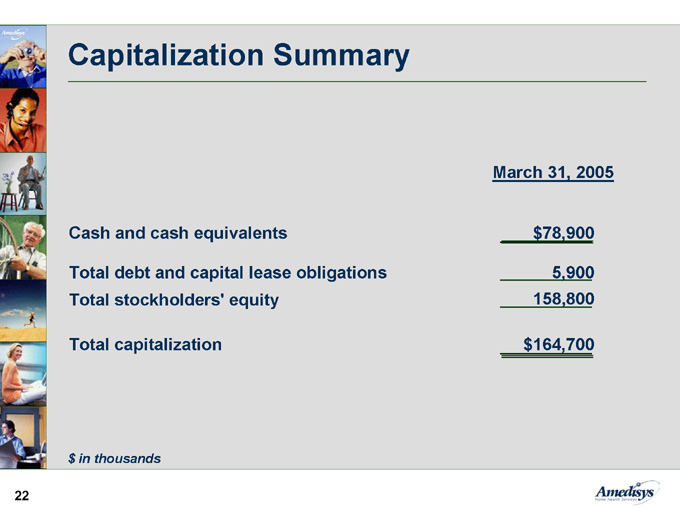

Capitalization Summary

March 31, 2005

Cash and cash equivalents

$78,900

Total debt and capital lease obligations

5,900

Total stockholders’ equity

158,800

Total capitalization

$164,700

$ in thousands

22

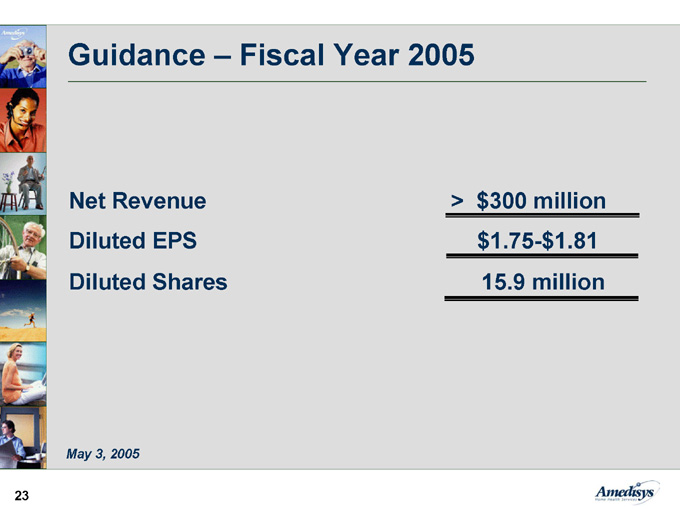

Guidance – Fiscal Year 2005

> $300 million

Net Revenue

$1.75-$1.81

Diluted EPS

15.9 million

Diluted Shares

May 3, 2005

23

Investment Highlights

Large, growing, and fragmented industry

Focus on Medicare home nursing

Strong internal growth

Demonstrated ability to identify and integrate acquisitions

Proven operating model

Experienced management team

24