Item 1. Reports to Stockholders

Annual report

Closed-end fund

Delaware Investments® Dividend and Income Fund, Inc.

November 30, 2019

|

Beginning on or about June 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your Fund’s shareholder reports will no longer be sent to you by mail, unless you specifically request them from the Fund or from your financial intermediary, such as a broker/dealer, bank, or insurance company. Instead, you will be notified by mail each time a report is posted on the website and provided with a link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you do not need to take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by logging into your Investor Center account at computershare.com/investor and going to “Communication Preferences” or by calling Computershare and speaking to a representative. You may elect to receive paper copies of all future shareholder reports free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting us at 866437-0252. If you own these shares through a financial intermediary, you may contact your financial intermediary to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the Delaware Funds®by Macquarie or your financial intermediary. |

The figures in the annual report for Delaware Investments Dividend and Income Fund, Inc. represent past results, which are not a guarantee of future results. A rise or fall in interest rates can have a significant impact on bond prices. Funds that invest in bonds can lose their value as interest rates rise.

Table of contents

Delaware Investments® Dividend and Income Fund, Inc. (“DDF” or the “Fund”), acting pursuant to a Securities and Exchange Commission (“SEC”) exemptive order and with the approval of the Fund’s Board of Trustees (the “Board”), has adopted a managed distribution policy (the “Plan”). Effective as of March 29, 2018, the Fund makes monthly distributions to common shareholders at a targeted annual distribution rate of 10% of the Fund’s average net asset value (“NAV”) per share. The Fund will calculate the average NAV per share from the previous three full months immediately prior to the distribution based on the number of business days in those three months on which the NAV is calculated. The distribution will be calculated as 10% of the prior three months’ average NAV per share, divided by 12. This distribution methodology is intended to provide shareholders with a consistent, but not guaranteed, income stream and a targeted annual distribution rate and is intended to narrow any discount between the market price and the NAV of the Fund’s common shares, but there is no assurance that the policy will be successful in doing so.

Under the Plan, the Fund is managed with a goal of generating as much of the distribution as possible from net investment income and short-term capital gains. The balance of the distribution will then come from long-term capital gains to the extent permitted, and if necessary, a return of capital. The Fund will generally distribute amounts necessary to satisfy the terms of the Fund’s Plan and the requirements prescribed by excise tax rules and Subchapter M of the Internal Revenue Code (the “Code”). Each monthly distribution to shareholders is expected to be at the fixed percentage described above, except for extraordinary distributions and potential distribution rate increases or decreases to enable the Fund to comply with the distribution requirements imposed by the Code.

The Board may amend, suspend, or terminate the Fund’s Plan at any time without prior notice if it deems such action to be in the best interest of the Fund or its shareholders. The methodology for determining monthly distributions under the Plan will be reviewed at least annually by the Fund’s Board, and the Fund will continue to evaluate its distribution in light of ongoing market conditions. The suspension or termination of the Plan could have the effect of creating a trading discount (if the Fund’s stock is trading at or above NAV) or widening an existing trading discount. The Fund is subject to risks that could have an adverse impact on its ability to maintain distributions under the Plan. Examples of potential risks include, but are not limited to, economic downturns impacting the markets, increased market volatility, portfolio companies suspending or decreasing corporate dividend distributions, and changes in the Code.

Shareholders should not draw any conclusions about the Fund’s investment performance from the amounts of these distributions or from the terms of the Plan. The Fund’s total investment return on NAV is presented in its financial highlights table.

A cumulative summary of the Section 19(a) notices for the Fund’s current fiscal period, if applicable, is included in Other Fund Information. Section 19(a) notices for the Fund, as applicable, are available on the Fund’s website atdelawarefunds.com/closed-end/performance/fund-distributions.

Macquarie Asset Management (MAM) offers a diverse range of products including securities investment management, infrastructure and real asset management, and fund and equity-based structured products. Macquarie Investment Management (MIM) is the marketing name for certain companies comprising the asset management division of Macquarie Group. These include the following investment advisors: Macquarie Investment Management Business Trust (MIMBT), Macquarie Funds Management Hong Kong Limited, Macquarie Investment Management Austria Kapitalanlage AG, Macquarie Investment Management Global Limited, Macquarie Investment Management Europe Limited, Macquarie Capital Investment Management LLC, and Macquarie Investment Management Europe S.A. For more information, including press releases, please visitdelawarefunds.com/closed-end.

Unless otherwise noted, views expressed herein are current as of Nov. 30, 2019, and subject to change for events occurring after such date.

The Fund is not FDIC insured and is not guaranteed. It is possible to lose the principal amount invested.

Advisory services provided by Delaware Management Company, a series of MIMBT, a US registered investment advisor. Other than Macquarie Bank Limited (MBL), none of the entities noted are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise. The Fund is governed by US laws and regulations.

All third-party marks cited are the property of their respective owners.

© 2020 Macquarie Management Holdings, Inc.

Portfolio management review (Unaudited)

Delaware Investments®Dividend and Income Fund, Inc.

December 10, 2019

Performance preview (for the year ended November 30, 2019)

| | | | | | | | |

| | | |

Delaware Investments Dividend and Income Fund, Inc. @ market price | | | 1-year return | | | | +23.07 | % |

| | |

Delaware Investments Dividend and Income Fund, Inc. @ NAV | | | 1-year return | | | | +7.51 | % |

| | |

LipperClosed-end Income and Preferred Stock Funds Average @ market price | | | 1-year return | | | | +21.98 | % |

| | |

LipperClosed-end Income and Preferred Stock Funds Average @ NAV | | | 1-year return | | | | +12.79 | % |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Investments Dividend and Income Fund, Inc., please see the table on page 3.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

For the fiscal year ended Nov. 30, 2019, Delaware Investments Dividend and Income Fund, Inc. returned +7.51% at net asset value (NAV) and +23.07% at market price (both figures reflect all distributions reinvested). Complete annualized performance for the Fund is shown in the table on page 3.

A shifting monetary backdrop

The Fund’s fiscal year ended Nov. 30, 2019, began with a sharp downturn, with most financial assets experiencing steep valuation drops. These asset-price declines primarily reflected investors’ worries about rising interest rates amid mounting global economic uncertainty.

By the first quarter of 2019, however, conditions for most asset classes had turned significantly positive and generally remained that way for the rest of the fiscal year. Global financial markets marched ahead, as central banks globally signaled their intent to provide monetary support for their respective economies.

These central banks included the US Federal Reserve, which gradually shifted from a policy of raising interest rates to one of cutting them. The shift took place against a backdrop of consistent US economic growth with few signs of inflation. In December 2018, the Fed raised its benchmark short-term interest rate by 0.25 percentage points – it was the central bank’s seventh such rate increase in the previous two years. The Fed then kept the federal funds rate steady until late July, when it initiated its first of three successive0.25-percentage-point rate cuts. By fiscal year end, the federal funds rate was within a range of 1.50% to 1.75%, where it had been inmid-2018.

The Fed’s monetary policy shift came amid the US economy’s weakest quarterly performance of the fiscal year. US gross domestic product (GDP), a measure of national economic output, grew by an annualized rate of just 1.1% in the final three months of 2018. By the first quarter of 2019, however, US annual GDP growth accelerated to 3.1%. The national economy subsequently expanded by 2.0% and an estimated 2.1% in the year’s second and third quarters, respectively. Meanwhile, the US unemployment rate declined further, reaching 3.5% in November 2019 – the lowest

since 1969. (Sources: US Bureau of Economic Analysis and US Bureau of Labor Statistics.)

Favorable market conditions

The shift in Fed interest rate policy was the main driver behind the favorable results seen across all of the Fund’s asset classes, as financial markets benefited strongly from the increase in global liquidity.

For the fiscal year ended Nov. 30, 2019, USlarge-cap value stocks, as measured by the Russell 1000® Value Index, gained 11.33%, as the equity market recovered from a December 2018 market correction to produce steady gains throughout the rest of the12-month period.

High yield corporate bonds gained 9.68%, as reflected in the performance of the Bloomberg Barclays US Corporate High-Yield Index. During the fiscal year, high yield bonds benefited from narrowing credit spreads, indicating that investors were willing to accept gradually less income in exchange for taking on credit risk.

Meanwhile, convertible securities, as measured by the ICE BofA US Convertible Index, gained 14.53%, while US real estate securities, as indicated by the FTSE Nareit Equity REITs Index, gained 16.33%.

Individual contributors and detractors

Within the USlarge-cap value equity subportfolio, we saw subpar results from several energy stocks, especiallyHalliburton Co.,an energy-services provider, andMarathon Oil Corp.andOccidental Petroleum Corp.,both exploration and production (E&P) companies.

Halliburton continued to face difficult business conditions, as the company has had to adjust to declining North American investment activity and its increasingly returns-focused business model. Marathon Oil struggled due to its sensitivity to changes in the price of oil, which often leads to exaggerated moves in the company’s stock price. Finally, shares of Occidental Petroleum came under pressure following its decision to acquire Anadarko Petroleum at what investors viewed was too high a price. Investors also appeared to dislike the terms of the deal’s financing.

Portfolio management review (Unaudited)

Delaware Investments® Dividend and Income Fund, Inc.

In contrast, several defense-related companies within the industrials sector contributed to the Fund’s relative performance, especiallyNorthrop Grumman Corp.andRaytheon Co.We believe defense-company stocks generally fared well due to rising geopolitical tensions and potentially weaker fundamentals weighing on stocks in many other areas of the industrials sector.

Sticking to our strategy

We regularly invest across multiple asset classes, searching for securities that offer a competitive yield and the opportunity for dividend growth. We also prioritize managing downside risk while seeking to limit potential capital losses.

Throughout the fiscal year, consistent with our income-oriented focus, we maintained a relatively consistent asset mix. The Fund’s largest allocation remained inlarge-cap value equities, which expanded incrementally from 59% of the portfolio in December 2018 to 60% at fiscal year end. USlarge-cap stocks remained the largest allocation in the Fund’s portfolio, reflecting our view that the asset class offered investors a favorable combination of yield and upside potential following the market’s sharp correction in late 2018.

The Fund’s largest asset shift reflected an increase in exposure to convertible securities, which moved from 1% of the portfolio at the start of the12-month period to about 4% at fiscal year end. This corresponded to a three-percentage-point decrease in the Fund’s exposure to high yield bonds, which moved from 31% to 28% of the Fund. Meanwhile, the Fund’s weighting in real estate investment trusts (REITs) declined minimally, from about 9% to about 8%.

During the fiscal year, the Fund used foreign currency exchange contracts to facilitate the purchase and sale of securities, and written option contracts to manage the Fund’s exposure to changes in securities prices caused by interest rates or market conditions. These derivative securities did not have a material effect on performance during the fiscal year.

A final note: The Fund’s use of leverage – a portfolio management tool designed to obtain a potentially higher return on the Fund’s investments – added to performance in light of the stock market’s increase. Leverage magnifies the effect of gains and losses. As a result, leverage added to the Fund’s results in what was a positive market environment.

Monitoring market conditions

We continue to believe that income-generating securities, such aslarge-cap value equities, REITs, convertibles, and high yield bonds, have the potential to perform well as markets remain uneven and volatile.

We will continue to closely monitor market conditions as we seek to provide a favorable total return to investors while managing downside risk and seeking potential upside via income-generating securities across multiple asset classes and regions. We also may seek to take advantage of market shifts to increase or decrease exposure to certain asset classes as relative value opportunities emerge.

Unless otherwise noted, views expressed herein are current as of Nov. 30, 2019, and subject to change.

2

Performance summary (Unaudited)

Delaware Investments® Dividend and Income Fund, Inc.

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Please obtain the most recent performance data by calling 866437-0252 or visiting our website atdelawarefunds.com/closed-end.

Fund performance

| | | | | | | | |

Average annual total returns through November 30, 2019 | | 1 year | | 5 years | | 10 years | | Lifetime |

At market price (inception date March 26, 1993) | | +23.07% | | +15.15% | | +16.50% | | +9.78% |

At net asset value (inception date March 26, 1993) | | +7.51% | | +7.34% | | +12.91% | | +9.03% |

Diversification may not protect against market risk.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a bond that is held by a portfolio will be prepaid prior to maturity, at the time when interest rates are lower than what the bond was paying. A portfolio may then have to reinvest that money at a lower interest rate.

High yielding,non-investment-grade bonds (junk bonds) involve higher risk than investment grade bonds.

Narrowly focused investments may exhibit higher volatility than investments in multiple industry sectors.

REIT investments are subject to many of the risks associated with direct real estate ownership, including changes in economic conditions, credit risk, and interest rate fluctuations.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivatives transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

If and when the Fund invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund borrows through a line of credit for purposes of leveraging. Leveraging may result in higher degrees of volatility because the Fund’s net asset value could be subject to fluctuations in short-term interest rates and changes in market value of portfolio securities attributable to leverage. Leverage magnifies the potential for gain and the risk of loss. As a result, a relatively small decline in the value of the underlying investments could result in a relatively large loss. In addition, the leverage through the line of credit is dependent on the credit provider’s ability to fulfill its contractual obligations.

Closed-end fund shares do not represent a deposit or obligation of, and are not guaranteed or endorsed by, any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation or any other government agency.Closed-end funds, unlikeopen-end funds, are not continuously offered. After being issued during aone-time-only public offering, shares ofclosed-end funds are sold in the open market through a securities exchange. Net asset value (NAV) is calculated by subtracting total liabilities by total assets, then dividing by the number of shares outstanding. At the time of sale, your shares may have a market price that is above or below NAV, and may be worth more or less than your original investment.

The Fund may make distributions of ordinary income and capital gains at calendar year end. Those distributions may temporarily cause extraordinarily high yields. There is no assurance that a Fund will repeat that yield in the future. Subsequent monthly distributions that do not include ordinary income or capital gains in the form of dividends will likely be lower.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Returns reflect the reinvestment of all distributions. Dividends and distributions, if any, are assumed, for the purpose of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment policy. Shares of the Fund were initially offered with a sales charge of 6%. Performance since inception does not include the sales charge or any other brokerage commission for purchases made since inception.

Past performance is not a guarantee of future results.

Performance summary (Unaudited)

Delaware Investments® Dividend and Income Fund, Inc.

Fund basics

As of November 30, 2019

| | |

| Fund objectives | | Fund start date |

| The Fund’s primary investment objective is to seek high current income; capital appreciation is a secondary objective. | | March 26, 1993 |

| | |

| Total Fund net assets | | NYSE symbol |

| $84 million | | DDF |

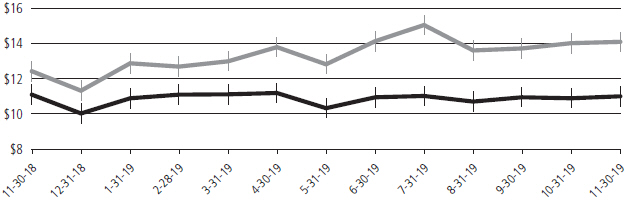

Market price versus net asset value(see notes below and on next page)

November 30, 2018 through November 30, 2019

| | | | | | |

Starting value (Nov. 30, 2018) | | Ending value (Nov. 30, 2019) |

| | | |

| | Delaware Investments Dividend and Income Fund, Inc. @ market price | | $12.42 | | $14.09 |

| | | |

| | Delaware Investments Dividend and Income Fund, Inc. @ NAV | | $11.09 | | $10.99 |

Past performance is not a guarantee of future results.

4

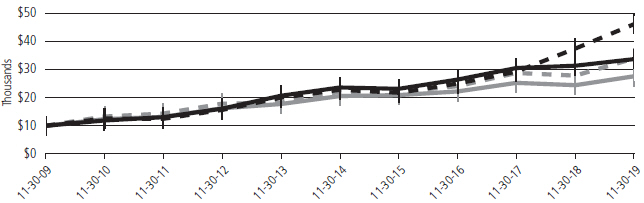

Performance of a $10,000 investment

Average annual total returns from November 30, 2009 through November 30, 2019

| | | | | | | | |

| Starting value (Nov. 30, 2009) Ending value (Nov. 30, 2019) |

| | | |

| | Delaware Investments®Dividend and Income Fund, Inc. @ market price | | $ | 10,000 | | | $46,054 |

| | | |

| | LipperClosed-end Income and Preferred Stock Funds Average @ market price | | $ | 10,000 | | | $33,931 |

| | | |

| | Delaware Investments Dividend and Income Fund, Inc. @ NAV | | $ | 10,000 | | | $33,676 |

| | | |

| | LipperClosed-end Income and Preferred Stock Funds Average @ NAV | | $ | 10,000 | | | $27,580 |

The “Performance of a $10,000 investment” graph assumes $10,000 invested in the Fund on Nov. 30, 2009, and includes the reinvestment of all distributions at market value. The graph assumes $10,000 in the LipperClosed-end Income and Preferred Stock Funds Average at market price and at NAV. Performance of the Fund and the Lipper class at market value is based on market performance during the period. Performance of the Fund and Lipper class at NAV is based on the fluctuations in NAV during the period. Delaware Investments Dividend and Income Fund, Inc. was initially offered with a sales charge of 6%. For market price, performance shown in both graphs above does not include fees, the initial sales charge, or any brokerage commissions on purchases. For NAV, performance shown in both graphs above includes fees, but does not include the initial sales charge or any brokerage commissions for purchases. Investments in the Fund are not available at NAV.

The LipperClosed-end Income and Preferred Stock Funds Average represents the average return ofclosed-end funds that normally seek a high level of current income through investing in income-producing stocks, bonds, and money market instruments, or funds that invest primarily in preferred securities, often considering tax code implications (source: Lipper).

The Russell 1000 Value Index, mentioned on page 1, measures the performance of thelarge-cap value segment of the US equity universe. It includes those Russell 1000 companies with lowerprice-to-book ratios and lower forecasted growth values.

The Bloomberg Barclays US Corporate High-Yield Index, mentioned on page 1, is composed of US dollar-denominated, noninvestment-grade corporate bonds for which the middle rating among Moody’s Investors Service, Inc., Fitch, Inc., and Standard & Poor’s is Ba1/BB+/BB+ or below.

The ICE BofA US Convertible Index, mentioned on page 1, tracks the performance of publicly issued US dollar-denominated convertible securities of US companies. Qualifying securities must have at least $50 million face amount outstanding and at least one month remaining to the final conversion date.

The FTSE Nareit Equity REITs Index, mentioned on page 1, contains alltax-qualified real estate investment trusts (REITs) traded on US exchanges excluding timber and infrastructure REITs, with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria.

Frank Russell Company is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company.

Performance summary (Unaudited)

Delaware Investments® Dividend and Income Fund, Inc.

Gross domestic product is a measure of all goods and services produced by a nation in a year.

Market price is the price an investor would pay for shares of the Fund on the secondary market.

NAV is the total value of one fund share, generally equal to a fund’s net assets divided by the number of shares outstanding.

Past performance is not a guarantee of future results.

6

Security type / sector allocations and

top 10 equity holdings

Delaware Investments® Dividend and Income Fund, Inc.

As of November 30, 2019 (Unaudited)

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications.

| | | | |

| Security type / sector | | Percentage

of net assets | |

Common Stock | | | 91.47% | |

Communication Services | | | 5.03% | |

Consumer Discretionary | | | 4.89% | |

Consumer Staples | | | 8.05% | |

Energy | | | 5.78% | |

Financials | | | 13.99% | |

Healthcare | | | 21.99% | |

Industrials | | | 7.94% | |

Information Technology | | | 10.27% | |

Materials | | | 2.13% | |

REIT Diversified | | | 0.16% | |

REIT Healthcare | | | 0.92% | |

REIT Hotel | | | 0.81% | |

REIT Industrial | | | 0.20% | |

REIT Mall | | | 0.21% | |

REIT Manufactured Housing | | | 0.33% | |

REIT Mortgage | | | 0.43% | |

REIT Multifamily | | | 4.05% | |

REIT Office | | | 0.83% | |

REIT Self-Storage | | | 0.21% | |

REIT Shopping Center | | | 0.47% | |

REIT Single Tenant | | | 0.43% | |

Utilities | | | 2.35% | |

Convertible Preferred Stock | | | 1.07% | |

Convertible Bonds | | | 5.18% | |

Capital Goods | | | 0.32% | |

Communications | | | 0.69% | |

Consumer Cyclical | | | 0.27% | |

ConsumerNon-Cyclical | | | 0.86% | |

Electric | | | 0.17% | |

Energy | | | 0.69% | |

Financials | | | 0.29% | |

Industrials | | | 0.21% | |

REIT | | | 0.17% | |

Technology | | | 1.51% | |

| | | | |

| Security type / sector | | Percentage

of net assets | |

Corporate Bonds | | | 36.59% | |

Automotive | | | 0.55% | |

Banking | | | 1.69% | |

Basic Industry | | | 4.42% | |

Capital Goods | | | 2.57% | |

Communications | | | 2.62% | |

Consumer Cyclical | | | 2.34% | |

ConsumerNon-Cyclical | | | 2.24% | |

Energy | | | 4.13% | |

Financials | | | 0.92% | |

Healthcare | | | 3.35% | |

Insurance | | | 0.96% | |

Media | | | 4.40% | |

Real Estate Investment Trusts | | | 0.94% | |

Services | | | 1.18% | |

Technology & Electronics | | | 2.31% | |

Transportation | | | 0.33% | |

Utilities | | | 1.64% | |

Preferred Stock | | | 0.50% | |

Exchange-Traded Fund | | | 1.92% | |

Rights | | | 0.00% | |

Short-Term Investments | | | 7.32% | |

Total Value of Securities | | | 144.05% | |

Borrowing Under Line of Credit | | | (41.43%) | |

Liabilities Net of Receivables and Other Assets | | | (2.62%) | |

Total Net Assets | | | 100.00% | |

Security type / sector allocations and

top 10 equity holdings

Delaware Investments® Dividend and Income Fund, Inc.

Holdings are for informational purposes only and are subject to change at any time. They are not a recommendation to buy, sell, or hold any security.

| | |

| Top 10 Equity Holdings | | Percentage of net assets |

CVS Health | | 3.26% |

ConocoPhillips | | 3.01% |

Cigna | | 3.01% |

Allstate | | 2.95% |

Brookdale Senior Living | | 2.92% |

BB&T | | 2.89% |

Marsh & McLennan | | 2.87% |

Lowe’s | | 2.83% |

Intel | | 2.81% |

Occidental Petroleum | | 2.78% |

8

Schedule of investments

Delaware Investments® Dividend and Income Fund, Inc.

November 30, 2019

| | | | | | | | |

| | | Number of

shares | | | Value (US $) | |

| |

Common Stock – 91.47% | | | | | | | | |

| |

Communication Services – 5.03% | | | | | |

AT&T | | | 58,000 | | | $ | 2,168,040 | |

Century Communications =† | | | 500,000 | | | | 0 | |

Verizon Communications | | | 34,600 | | | | 2,084,304 | |

| | | | | | | | |

| | | | | | | 4,252,344 | |

| | | | | | | | |

Consumer Discretionary – 4.89% | | | | | |

Dollar Tree † | | | 19,000 | | | | 1,737,740 | |

Lowe’s | | | 20,400 | | | | 2,393,124 | |

| | | | | | | | |

| | | | | | | 4,130,864 | |

| | | | | | | | |

Consumer Staples – 8.05% | | | | | |

Archer-Daniels-Midland | | | 46,700 | | | | 2,004,831 | |

Coca-Cola | | | 14,546 | | | | 776,756 | |

Conagra Brands | | | 69,763 | | | | 2,014,058 | |

Mondelez International Class A | | | 38,100 | | | | 2,001,774 | |

| | | | | | | | |

| | | | | | | 6,797,419 | |

| | | | | | | | |

Energy – 5.78% | | | | | |

ConocoPhillips | | | 42,400 | | | | 2,541,456 | |

Occidental Petroleum | | | 60,800 | | | | 2,345,056 | |

| | | | | | | | |

| | | | | | | 4,886,512 | |

| | | | | | | | |

Financials – 13.99% | | | | | |

Allstate | | | 22,400 | | | | 2,494,240 | |

American International Group | | | 39,900 | | | | 2,101,134 | |

Bank of New York Mellon | | | 46,200 | | | | 2,262,414 | |

BB&T | | | 44,600 | | | | 2,440,512 | |

Hercules Capital | | | 7,218 | | | | 103,434 | |

Marsh & McLennan | | | 22,400 | | | | 2,420,768 | |

| | | | | | | | |

| | | | | | | 11,822,502 | |

| | | | | | | | |

Healthcare – 21.99% | | | | | |

Abbott Laboratories | | | 24,700 | | | | 2,110,615 | |

Brookdale Senior Living † | | | 345,252 | | | | 2,465,099 | |

Cardinal Health | | | 40,400 | | | | 2,223,212 | |

Cigna | | | 12,708 | | | | 2,540,583 | |

CVS Health | | | 36,600 | | | | 2,754,882 | |

Johnson & Johnson | | | 15,000 | | | | 2,062,350 | |

Merck & Co. | | | 25,500 | | | | 2,223,090 | |

Pfizer | | | 57,089 | | | | 2,199,068 | |

| | | | | | | | |

| | | | | | | 18,578,899 | |

| | | | | | | | |

Industrials – 7.94% | | | | | |

Northrop Grumman | | | 6,200 | | | | 2,180,974 | |

Raytheon | | | 10,600 | | | | 2,304,652 | |

| | | | | | | | |

| | | Number of

shares | | | Value (US $) | |

| |

Common Stock (continued) | | | | | | | | |

| |

Industrials (continued) | | | | | | | | |

Waste Management | | | 19,700 | | | $ | 2,224,327 | |

| | | | | | | | |

| | | | | | | 6,709,953 | |

| | | | | | | | |

Information Technology – 10.27% | | | | | |

Broadcom | | | 7,100 | | | | 2,245,091 | |

Cisco Systems | | | 39,200 | | | | 1,776,152 | |

Intel | | | 40,900 | | | | 2,374,245 | |

Oracle | | | 40,700 | | | | 2,284,898 | |

| | | | | | | | |

| | | | | | | 8,680,386 | |

| | | | | | | | |

Materials – 2.13% | | | | | |

DuPont de Nemours | | | 27,732 | | | | 1,797,311 | |

| | | | | | | | |

| | | | | | | 1,797,311 | |

| | | | | | | | |

REIT Diversified – 0.16% | | | | | |

Fibra Uno Administracion | | | 88,100 | | | | 135,161 | |

| | | | | | | | |

| | | | | | | 135,161 | |

| | | | | | | | |

REIT Healthcare – 0.92% | | | | | |

Assura | | | 269,626 | | | | 264,330 | |

Healthpeak Properties | | | 6,400 | | | | 223,232 | |

Sabra Health Care REIT | | | 3,000 | | | | 66,840 | |

Welltower | | | 2,592 | | | | 219,205 | |

| | | | | | | | |

| | | | | | | 773,607 | |

| | | | | | | | |

REIT Hotel – 0.81% | | | | | |

MGM Growth Properties Class A | | | 6,299 | | | | 195,206 | |

Service Properties Trust | | | 4,700 | | | | 109,463 | |

Summit Hotel Properties | | | 14,547 | | | | 176,310 | |

VICI Properties | | | 8,069 | | | | 199,546 | |

| | | | | | | | |

| | | | | | | 680,525 | |

| | | | | | | | |

REIT Industrial – 0.20% | | | | | |

Liberty Property Trust | | | 2,700 | | | | 166,374 | |

| | | | | | | | |

| | | | | | | 166,374 | |

| | | | | | | | |

REIT Mall – 0.21% | | | | | |

Simon Property Group | | | 1,193 | | | | 180,394 | |

| | | | | | | | |

| | | | | | | 180,394 | |

| | | | | | | | |

REIT Manufactured Housing – 0.33% | | | | | |

Sun Communities | | | 1,689 | | | | 278,195 | |

| | | | | | | | |

| | | | | | | 278,195 | |

| | | | | | | | |

REIT Mortgage – 0.43% | | | | | |

Annaly Capital Management | | | 38,832 | | | | 362,303 | |

| | | | | | | | |

| | | | | | | 362,303 | |

| | | | | | | | |

REIT Multifamily – 4.05% | | | | | |

Bluerock Residential Growth REIT | | | 11,500 | | | | 140,990 | |

Brookfield Property Partners | | | 2 | | | | 38 | |

Schedule of investments

Delaware Investments® Dividend and Income Fund, Inc.

| | | | | | | | |

| | | Number of

shares | | | Value (US $) | |

| |

Common Stock (continued) | | | | | | | | |

| |

REIT Multifamily (continued) | | | | | | | | |

Equity Residential | | | 26,557 | | | $ | 2,260,001 | |

Essential Properties Realty Trust | | | 23,600 | | | | 615,724 | |

Grainger | | | 34,875 | | | | 127,919 | |

Invitation Homes | | | 4,300 | | | | 131,279 | |

NexPoint Residential Trust | | | 3,000 | | | | 143,550 | |

| | | | | | | | |

| | | | | | | 3,419,501 | |

| | | | | | | | |

REIT Office – 0.83% | | | | | | | | |

Alpine Income Property Trust † | | | 13,727 | | | | 257,656 | |

Postal Realty Trust Class A | | | 12,497 | | | | 198,202 | |

VEREIT | | | 25,000 | | | | 244,000 | |

| | | | | | | | |

| | | | | | | 699,858 | |

| | | | | | | | |

REIT Self-Storage – 0.21% | | | | | | | | |

National Storage Affiliates Trust | | | 5,361 | | | | 179,594 | |

| | | | | | | | |

| | | | | | | 179,594 | |

| | | | | | | | |

REIT Shopping Center – 0.47% | | | | | |

Brixmor Property Group | | | 10,282 | | | | 225,587 | |

First Capital Realty | | | 5,504 | | | | 89,420 | |

SITE Centers | | | 5,722 | | | | 82,912 | |

| | | | | | | | |

| | | | | | | 397,919 | |

| | | | | | | | |

REIT Single Tenant – 0.43% | | | | | | | | |

Spirit Realty Capital | | | 2,140 | | | | 112,136 | |

STORE Capital | | | 6,200 | | | | 252,402 | |

| | | | | | | | |

| | | | | | | 364,538 | |

| | | | | | | | |

Utilities – 2.35% | | | | | | | | |

Edison International | | | 28,700 | | | | 1,983,170 | |

| | | | | | | | |

| | | | | | | 1,983,170 | |

| | | | | | | | |

Total Common Stock

(cost $59,299,522) | | | | | | | 77,277,329 | |

| | | | | | | | |

| | | | | | | | |

| |

Convertible Preferred Stock – 1.07% | | | | | |

| |

A Schulman 6.00% exercise price $52.33y | | | 199 | | | | 204,451 | |

AMG Capital Trust II 5.15% exercise price $195.47, maturity date 10/15/37 | | | 2,953 | | | | 143,350 | |

Bank of America 7.25% exercise price $50.00y | | | 118 | | | | 174,640 | |

El Paso Energy Capital Trust I 4.75% exercise price $34.49, maturity date 3/31/28 | | | 4,121 | | | | 203,619 | |

| | | | | | | | |

| | | Number of

shares | | | Value (US $) | |

| |

Convertible Preferred Stock (continued) | |

| |

QTS Realty Trust 6.50% exercise price $46.99y | | | 1,420 | | | $ | 179,247 | |

| | | | | | | | |

| |

Total Convertible Preferred Stock

(cost $764,060) | | | | 905,307 | |

| | | | | | | | |

| | |

| | | Principal

amount° | | | | |

| |

Convertible Bonds – 5.18% | | | | | | | | |

| |

Capital Goods – 0.32% | | | | | | | | |

Aerojet Rocketdyne Holdings 2.25% exercise price $26.00, maturity date 12/15/23 | | | 51,000 | | | | 90,113 | |

Cemex 3.72% exercise price $10.88, maturity date 3/15/20 | | | 180,000 | | | | 180,678 | |

| | | | | | | | |

| | | | | | | 270,791 | |

| | | | | | | | |

Communications – 0.69% | | | | | | | | |

DISH Network 2.375% exercise price $82.22, maturity date 3/15/24 | | | 181,000 | | | | 164,088 | |

GCI Liberty 144A 1.75% exercise price $370.52, maturity date 9/30/46 # | | | 146,000 | | | | 196,286 | |

InterDigital 144A 2.00% exercise price $81.29, maturity date 6/1/24 # | | | 126,000 | | | | 126,905 | |

Liberty Media 2.25% exercise price $34.28, maturity date 9/30/46 | | | 170,000 | | | | 96,178 | |

| | | | | | | | |

| | | | | | | 583,457 | |

| | | | | | | | |

Consumer Cyclical – 0.27% | | | | | | | | |

Meritor 3.25% exercise price $39.92, maturity date 10/15/37 | | | 75,000 | | | | 80,353 | |

Team 5.00% exercise price $21.70, maturity date 8/1/23 | | | 140,000 | | | | 146,745 | |

| | | | | | | | |

| | | | | | | 227,098 | |

| | | | | | | | |

ConsumerNon-Cyclical – 0.86% | |

BioMarin Pharmaceutical 0.599% exercise price $124.67, maturity date 8/1/24 | | | 105,000 | | | | 108,273 | |

Chefs’ Warehouse 144A 1.875% exercise price $44.20, maturity date 12/1/24 # | | | 61,000 | | | | 63,474 | |

Medicines 2.75% exercise price $48.97, maturity date 7/15/23 | | | 100,000 | | | | 173,254 | |

Paratek Pharmaceuticals 4.75% exercise price $15.90, maturity date 5/1/24 | | | 177,000 | | | | 109,233 | |

Vector Group 1.75% exercise price $20.27, maturity date 4/15/20● | | | 262,000 | | | | 272,316 | |

| | | | | | | | |

| | | | | | | 726,550 | |

| | | | | | | | |

10

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Convertible Bonds (continued) | | | | | |

| |

Electric – 0.17% | | | | | | | | |

NRG Energy 2.75% exercise price $47.74, maturity date 6/1/48 | | | 128,000 | | | $ | 144,522 | |

| | | | | | | | |

| | | | | | | 144,522 | |

| | | | | | | | |

Energy – 0.69% | | | | | |

Cheniere Energy 4.25% exercise price $138.38, maturity date 3/15/45 | | | 259,000 | | | | 204,616 | |

Helix Energy Solutions Group 4.25% exercise price $13.89, maturity date 5/1/22 | | | 218,000 | | | | 223,698 | |

PDC Energy 1.125% exercise price $85.39, maturity date 9/15/21 | | | 172,000 | | | | 158,646 | |

| | | | | | | | |

| | | | | | | 586,960 | |

| | | | | | | | |

Financials – 0.29% | | | | | |

FTI Consulting 2.00% exercise price $101.38, maturity date 8/15/23 | | | 89,000 | | | | 111,028 | |

GAIN Capital Holdings 5.00% exercise price $8.20, maturity date 8/15/22 | | | 154,000 | | | | 135,005 | |

| | | | | | | | |

| | | | | | | 246,033 | |

| | | | | | | | |

Industrials – 0.21% | | | | | |

Chart Industries 144A 1.00% exercise price $58.73, maturity date 11/15/24 # | | | 85,000 | | | | 98,285 | |

Dycom Industries 0.75% exercise price $96.89, maturity date 9/15/21 | | | 80,000 | | | | 77,959 | |

| | | | | | | | |

| | | | | | | 176,244 | |

| | | | | | | | |

REIT – 0.17% | | | | | |

Blackstone Mortgage Trust 4.75% exercise price $36.23, maturity date 3/15/23 | | | 134,000 | | | | 142,215 | |

| | | | | | | | |

| | | | | | | 142,215 | |

| | | | | | | | |

Technology – 1.51% | | | | | |

Boingo Wireless 1.00% exercise price $42.32, maturity date 10/1/23 | | | 169,000 | | | | 148,951 | |

CSG Systems International 4.25% exercise price $56.87, maturity date 3/15/36 | | | 139,000 | | | | 164,045 | |

Knowles 3.25% exercise price $18.43, maturity date 11/1/21 | | | 103,000 | | | | 137,659 | |

Ligand Pharmaceuticals 0.75% exercise price $248.48, maturity date 5/15/23 | | | 87,000 | | | | 75,977 | |

Pluralsight 144A 0.375% exercise price $38.76, maturity date 3/1/24 # | | | 163,000 | | | | 141,052 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Convertible Bonds (continued) | | | | | | | | |

| |

Technology (continued) | | | | | | | | |

Quotient Technology 1.75% exercise price $17.36, maturity date 12/1/22 | | | 127,000 | | | $ | 124,897 | |

Retrophin 2.50% exercise price $38.80, maturity date 9/15/25 | | | 129,000 | | | | 100,830 | |

Synaptics 0.50% exercise price $73.02, maturity date 6/15/22 | | | 120,000 | | | | 124,967 | |

Verint Systems 1.50% exercise price $64.46, maturity date 6/1/21 | | | 140,000 | | | | 144,275 | |

Vishay Intertechnology 2.25% exercise price $31.45, maturity date 6/15/25 | | | 113,000 | | | | 110,659 | |

| | | | | | | | |

| | | | | | | 1,273,312 | |

| | | | | | | | |

| |

Total Convertible Bonds

(cost $4,198,645) | | | | 4,377,182 | |

| | | | | | | | |

|

| |

Corporate Bonds – 36.59% | | | | | | | | |

| |

Automotive – 0.55% | | | | | | | | |

Allison Transmission 144A 5.875% 6/1/29 # | | | 430,000 | | | | 464,861 | |

| | | | | | | | |

| | | | | | | 464,861 | |

| | | | | | | | |

Banking – 1.69% | | | | | |

Ally Financial 5.75% 11/20/25 | | | 435,000 | | | | 480,131 | |

Credit Suisse Group 144A 6.25% #µy | | | 200,000 | | | | 216,289 | |

Popular 6.125% 9/14/23 | | | 280,000 | | | | 301,116 | |

Royal Bank of Scotland Group 8.625% µy | | | 400,000 | | | | 432,792 | |

| | | | | | | | |

| | | | | | | 1,430,328 | |

| | | | | | | | |

Basic Industry – 4.42% | | | | | |

BMC East 144A 5.50% 10/1/24 # | | | 125,000 | | | | 130,208 | |

Boise Cascade 144A 5.625% 9/1/24 # | | | 275,000 | | | | 286,802 | |

Builders FirstSource 144A 5.625% 9/1/24 # | | | 148,000 | | | | 154,289 | |

Chemours 5.375% 5/15/27 | | | 190,000 | | | | 160,080 | |

FMG Resources August 2006 | | | | | | | | |

144A 4.75% 5/15/22 # | | | 105,000 | | | | 107,887 | |

144A 5.125% 5/15/24 # | | | 180,000 | | | | 189,299 | |

Freeport-McMoRan | | | | | | | | |

4.55% 11/14/24 | | | 170,000 | | | | 179,088 | |

5.45% 3/15/43 | | | 185,000 | | | | 178,081 | |

HD Supply 144A 5.375% 10/15/26 # | | | 170,000 | | | | 180,595 | |

Hudbay Minerals 144A 7.625% 1/15/25 # | | | 180,000 | | | | 180,898 | |

Joseph T Ryerson & Son 144A 11.00% 5/15/22 # | | | 110,000 | | | | 116,544 | |

Schedule of investments

Delaware Investments® Dividend and Income Fund, Inc.

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Corporate Bonds (continued) | | | | | |

| |

Basic Industry (continued) | | | | | |

Koppers 144A 6.00% 2/15/25 # | | | 215,000 | | | $ | 218,223 | |

Lennar | | | | | | | | |

4.50% 4/30/24 | | | 195,000 | | | | 207,318 | |

4.75% 5/30/25 | | | 95,000 | | | | 102,271 | |

5.875% 11/15/24 | | | 80,000 | | | | 89,433 | |

M/I Homes 5.625% 8/1/25 | | | 20,000 | | | | 20,808 | |

NOVA Chemicals 144A 5.00% 5/1/25 # | | | 130,000 | | | | 130,974 | |

Novelis 144A 6.25%

8/15/24 # | | | 116,000 | | | | 122,267 | |

Olin | | | | | | | | |

5.00% 2/1/30 | | | 175,000 | | | | 174,129 | |

5.125% 9/15/27 | | | 195,000 | | | | 202,765 | |

PulteGroup 5.00% 1/15/27 | | | 100,000 | | | | 109,232 | |

Standard Industries 144A 6.00% 10/15/25 # | | | 50,000 | | | | 52,437 | |

Steel Dynamics 5.00% 12/15/26 | | | 280,000 | | | | 298,101 | |

Univar Solutions USA 144A 5.125% 12/1/27 # | | | 140,000 | | | | 143,528 | |

| | | | | | | | |

| | | | | | | 3,735,257 | |

| | | | | | | | |

Capital Goods – 2.57% | | | | | | | | |

Ardagh Packaging Finance 144A 6.00% 2/15/25 # | | | 240,000 | | | | 252,600 | |

Ashtead Capital 144A 5.25% 8/1/26 # | | | 530,000 | | | | 567,613 | |

Bombardier 144A 6.00% 10/15/22 # | | | 325,000 | | | | 326,625 | |

Crown Americas 4.75% 2/1/26 | | | 285,000 | | | | 299,705 | |

Mauser Packaging Solutions Holding | | | | | | | | |

144A 5.50% 4/15/24 # | | | 310,000 | | | | 317,747 | |

144A 7.25% 4/15/25 # | | | 105,000 | | | | 99,749 | |

TransDigm 144A 6.25% 3/15/26 # | | | 125,000 | | | | 134,453 | |

Zekelman Industries 144A 9.875% 6/15/23 # | | | 165,000 | | | | 174,178 | |

| | | | | | | | |

| | | | | | | 2,172,670 | |

| | | | | | | | |

Communications – 2.62% | | | | | | | | |

Altice France 144A 7.375% 5/1/26 # | | | 420,000 | | | | 449,412 | |

Level 3 Financing 144A 3.875% 11/15/29 # | | | 267,000 | | | | 269,213 | |

SBA Communications 4.875% 9/1/24 | | | 345,000 | | | | 358,688 | |

Sprint | | | | | | | | |

7.125% 6/15/24 | | | 190,000 | | | | 205,200 | |

7.625% 3/1/26 | | | 10,000 | | | | 10,937 | |

7.875% 9/15/23 | | | 103,000 | | | | 113,493 | |

Sprint Communications 7.00% 8/15/20 | | | 136,000 | | | | 139,468 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Corporate Bonds (continued) | | | | | |

| |

Communications (continued) | | | | | |

T-Mobile USA | | | | | | | | |

6.375% 3/1/25 = | | | 85,000 | | | $ | 0 | |

6.50% 1/15/26 | | | 305,000 | | | | 327,120 | |

6.50% 1/15/26 = | | | 220,000 | | | | 0 | |

Zayo Group | | | | | | | | |

144A 5.75% 1/15/27 # | | | 75,000 | | | | 76,714 | |

6.375% 5/15/25 | | | 250,000 | | | | 257,810 | |

| | | | | | | | |

| | | | | | | 2,208,055 | |

| | | | | | | | |

Consumer Cyclical – 2.34% | | | | | |

AMC Entertainment Holdings 6.125% 5/15/27 | | | 290,000 | | | | 261,732 | |

KAR Auction Services 144A 5.125% 6/1/25 # | | | 95,000 | | | | 96,780 | |

Levi Strauss & Co. 5.00% 5/1/25 | | | 190,000 | | | | 196,254 | |

MGM Resorts International 5.75% 6/15/25 | | | 180,000 | | | | 201,373 | |

Penn National Gaming 144A 5.625% 1/15/27 # | | | 215,000 | | | | 223,675 | |

Scientific Games International | | | | | | | | |

144A 8.25% 3/15/26 # | | | 290,000 | | | | 314,497 | |

10.00% 12/1/22 | | | 290,000 | | | | 297,975 | |

Yum! Brands 144A 4.75% 1/15/30 # | | | 370,000 | | | | 383,884 | |

| | | | | | | | |

| | | | | | | 1,976,170 | |

| | | | | | | | |

ConsumerNon-Cyclical – 2.24% | | | | | |

Aramark Services 144A 5.00% 2/1/28 # | | | 345,000 | | | | 363,121 | |

Cott Holdings 144A 5.50% 4/1/25 # | | | 260,000 | | | | 272,997 | |

JBS USA | | | | | | | | |

144A 5.75% 6/15/25 # | | | 170,000 | | | | 176,871 | |

144A 6.50% 4/15/29 # | | | 160,000 | | | | 177,656 | |

144A 6.75% 2/15/28 # | | | 20,000 | | | | 22,130 | |

Pilgrim’s Pride | | | | | | | | |

144A 5.75% 3/15/25 # | | | 315,000 | | | | 327,597 | |

144A 5.875% 9/30/27 # | | | 65,000 | | | | 70,351 | |

Post Holdings | | | | | | | | |

144A 5.00% 8/15/26 # | | | 100,000 | | | | 105,230 | |

144A 5.625% 1/15/28 # | | | 180,000 | | | | 192,568 | |

144A 5.75% 3/1/27 # | | | 170,000 | | | | 182,511 | |

| | | | | | | | |

| | | | | | | 1,891,032 | |

| | | | | | | | |

Energy – 4.13% | | | | | | | | |

AmeriGas Partners | | | | | | | | |

5.625% 5/20/24 | | | 10,000 | | | | 10,700 | |

5.875% 8/20/26 | | | 160,000 | | | | 175,972 | |

12

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Corporate Bonds (continued) | | | | | |

| |

Energy (continued) | | | | | | | | |

Cheniere Corpus Christi Holdings | | | | | | | | |

5.125% 6/30/27 | | | 40,000 | | | $ | 43,921 | |

5.875% 3/31/25 | | | 80,000 | | | | 89,616 | |

7.00% 6/30/24 | | | 200,000 | | | | 229,968 | |

Cheniere Energy Partners 5.25% 10/1/25 | | | 175,000 | | | | 180,686 | |

Crestwood Midstream Partners 6.25% 4/1/23 | | | 225,000 | | | | 226,123 | |

Energy Transfer Operating 5.50% 6/1/27 | | | 115,000 | | | | 127,288 | |

Genesis Energy | | | | | | | | |

6.50% 10/1/25 | | | 40,000 | | | | 36,299 | |

6.75% 8/1/22 | | | 174,000 | | | | 170,410 | |

Hilcorp Energy I 144A 5.00% 12/1/24 # | | | 97,000 | | | | 86,651 | |

Murphy Oil | | | | | | | | |

5.875% 12/1/27 | | | 214,000 | | | | 215,382 | |

6.875% 8/15/24 | | | 145,000 | | | | 152,125 | |

Murphy Oil USA 5.625% 5/1/27 | | | 415,000 | | | | 448,604 | |

Newfield Exploration 5.375% 1/1/26 | | | 275,000 | | | | 295,326 | |

NuStar Logistics 5.625% 4/28/27 | | | 160,000 | | | | 165,572 | |

Precision Drilling 144A 7.125% 1/15/26 # | | | 40,000 | | | | 35,086 | |

Southwestern Energy 7.75% 10/1/27 | | | 220,000 | | | | 191,681 | |

Summit Midstream Holdings 5.75% 4/15/25 | | | 10,000 | | | | 7,579 | |

Targa Resources Partners | | | | | | | | |

5.375% 2/1/27 | | | 300,000 | | | | 305,947 | |

5.875% 4/15/26 | | | 20,000 | | | | 21,081 | |

Transocean 144A 9.00% 7/15/23 # | | | 200,000 | | | | 204,560 | |

Transocean Proteus 144A 6.25% 12/1/24 # | | | 67,500 | | | | 68,372 | |

| | | | | | | | |

| | | | | | | 3,488,949 | |

| | | | | | | | |

Financials – 0.92% | | | | | |

AerCap Global Aviation Trust 144A 6.50% 6/15/45 #µ | | | 200,000 | | | | 220,020 | |

DAE Funding 144A 5.75% 11/15/23 # | | | 350,000 | | | | 369,395 | |

E*TRADE Financial

5.875% µy | | | 180,000 | | | | 188,718 | |

| | | | | | | | |

| | | | | | | 778,133 | |

| | | | | | | | |

Healthcare – 3.35% | | | | | |

Bausch Health 144A 5.50% 11/1/25 # | | | 465,000 | | | | 487,088 | |

Charles River Laboratories International | | | | | | | | |

144A 4.25% 5/1/28 # | | | 140,000 | | | | 141,400 | |

144A 5.50% 4/1/26 # | | | 330,000 | | | | 352,216 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Corporate Bonds (continued) | | | | | |

| |

Healthcare (continued) | | | | | | | | |

Encompass Health | | | | | | | | |

5.75% 11/1/24 | | | 173,000 | | | $ | 175,810 | |

5.75% 9/15/25 | | | 120,000 | | | | 126,350 | |

HCA | | | | | | | | |

5.375% 2/1/25 | | | 405,000 | | | | 448,533 | |

5.875% 2/15/26 | | | 165,000 | | | | 186,660 | |

7.58% 9/15/25 | | | 80,000 | | | | 95,900 | |

Hill-Rom Holdings 144A 5.00% 2/15/25 # | | | 180,000 | | | | 188,175 | |

Hologic 144A 4.625% 2/1/28 # | | | 160,000 | | | | 169,256 | |

Tenet Healthcare | | | | | | | | |

5.125% 5/1/25 | | | 175,000 | | | | 180,250 | |

8.125% 4/1/22 | | | 255,000 | | | | 279,225 | |

| | | | | | | | |

| | | | | | | 2,830,863 | |

| | | | | | | | |

Insurance – 0.96% | | | | | |

HUB International 144A 7.00% 5/1/26 # | | | 210,000 | | | | 215,780 | |

USI 144A 6.875% 5/1/25 # | | | 295,000 | | | | 297,210 | |

WellCare Health Plans 144A 5.375% 8/15/26 # | | | 275,000 | | | | 293,514 | |

| | | | | | | | |

| | | | | | | 806,504 | |

| | | | | | | | |

Media – 4.40% | | | | | |

AMC Networks 4.75% 8/1/25 | | | 370,000 | | | | 368,150 | |

CCO Holdings | | | | | | | | |

144A 5.125% 5/1/27 # | | | 120,000 | | | | 127,503 | |

144A 5.375% 6/1/29 # | | | 170,000 | | | | 182,542 | |

144A 5.50% 5/1/26 # | | | 30,000 | | | | 31,720 | |

144A 5.75% 2/15/26 # | | | 160,000 | | | | 169,365 | |

144A 5.875% 5/1/27 # | | | 190,000 | | | | 202,791 | |

CSC Holdings | | | | | | | | |

6.75% 11/15/21 | | | 230,000 | | | | 248,055 | |

144A 7.75% 7/15/25 # | | | 200,000 | | | | 215,000 | |

Gray Television | | | | | | | | |

144A 5.875% 7/15/26 # | | | 290,000 | | | | 308,176 | |

144A 7.00% 5/15/27 # | | | 55,000 | | | | 61,040 | |

Lamar Media | | | | | | | | |

5.375% 1/15/24 | | | 190,000 | | | | 194,748 | |

5.75% 2/1/26 | | | 167,000 | | | | 177,984 | |

Netflix 5.875% 11/15/28 | | | 365,000 | | | | 399,684 | |

Sinclair Television Group 144A 5.125% 2/15/27 # | | | 195,000 | | | | 197,505 | |

Sirius XM Radio | | | | | | | | |

144A 5.00% 8/1/27 # | | | 395,000 | | | | 416,735 | |

144A 5.375% 4/15/25 # | | | 205,000 | | | | 212,685 | |

VTR Finance 144A 6.875% 1/15/24 # | | | 200,000 | | | | 205,333 | |

| | | | | | | | |

| | | | | | | 3,719,016 | |

| | | | | | | | |

Schedule of investments

Delaware Investments® Dividend and Income Fund, Inc.

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Corporate Bonds (continued) | |

| |

Real Estate Investment Trusts – 0.94% | |

CyrusOne 5.375% 3/15/27 | | | 170,000 | | | $ | 187,484 | |

ESH Hospitality | | | | | | | | |

144A 4.625% 10/1/27 # | | | 90,000 | | | | 90,659 | |

144A 5.25% 5/1/25 # | | | 290,000 | | | | 300,150 | |

GLP Capital 5.375% 4/15/26 | | | 110,000 | | | | 121,468 | |

MGM Growth Properties Operating Partnership 144A 5.75% 2/1/27 # | | | 85,000 | | | | 95,306 | |

| | | | | | | | |

| | | | | | | 795,067 | |

| | | | | | | | |

Services – 1.18% | | | | | |

Advanced Disposal Services 144A 5.625% 11/15/24 # | | | 215,000 | | | | 225,033 | |

Covanta Holding 5.875% 7/1/25 | | | 210,000 | | | | 220,062 | |

Prime Security Services Borrower | | | | | | | | |

144A 5.75% 4/15/26 # | | | 220,000 | | | | 230,207 | |

144A 9.25% 5/15/23 # | | | 146,000 | | | | 153,756 | |

Service Corp. International 4.625% 12/15/27 | | | 159,000 | | | | 165,332 | |

| | | | | | | | |

| | | | | | | 994,390 | |

| | | | | | | | |

Technology & Electronics – 2.31% | | | | | |

CDK Global | | | | | | | | |

5.00% 10/15/24 | | | 175,000 | | | | 189,656 | |

5.875% 6/15/26 | | | 236,000 | | | | 252,773 | |

CDW Finance 5.00% 9/1/25 | | | 95,000 | | | | 99,274 | |

CommScope Technologies 144A 5.00% 3/15/27 # | | | 100,000 | | | | 88,006 | |

Infor US 6.50% 5/15/22 | | | 185,000 | | | | 188,939 | |

Iron Mountain US Holdings 144A 5.375% 6/1/26 # | | | 357,000 | | | | 372,297 | |

RP Crown Parent 144A 7.375% 10/15/24 # | | | 20,000 | | | | 20,758 | |

Sensata Technologies UK Financing 144A 6.25% 2/15/26 # | | | 200,000 | | | | 215,339 | |

SS&C Technologies 144A 5.50% 9/30/27 # | | | 490,000 | | | | 525,194 | |

| | | | | | | | |

| | | | | | | 1,952,236 | |

| | | | | | | | |

Transportation – 0.33% | | | | | |

Avis Budget Car Rental 144A 6.375% 4/1/24 # | | | 65,000 | | | | 67,871 | |

XPO Logistics 144A 6.125%

9/1/23 # | | | 201,000 | | | | 208,033 | |

| | | | | | | | |

| | | | | | | 275,904 | |

| | | | | | | | |

Utilities – 1.64% | | | | | |

AES | | | | | | | | |

5.50% 4/15/25 | | | 160,000 | | | | 166,190 | |

6.00% 5/15/26 | | | 25,000 | | | | 26,745 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (US $) | |

| |

Corporate Bonds (continued) | |

| |

Utilities (continued) | |

Calpine | | | | | | | | |

144A 5.25% 6/1/26 # | | | 190,000 | | | $ | 199,016 | |

144A 5.875% 1/15/24 # | | | 85,000 | | | | 86,948 | |

Emera 6.75% 6/15/76 µ | | | 180,000 | | | | 202,774 | |

Enel 144A 8.75% 9/24/73 #µ | | | 200,000 | | | | 234,520 | |

Vistra Energy 144A 8.00% 1/15/25 # | | | 158,000 | | | | 165,505 | |

Vistra Operations | | | | | | | | |

144A 5.50% 9/1/26 # | | | 205,000 | | | | 216,239 | |

144A 5.625% 2/15/27 # | | | 85,000 | | | | 89,464 | |

| | | | | | | | |

| | | | | | | 1,387,401 | |

| | | | | | | | |

Total Corporate Bonds

(cost $29,752,664) | | | | | | | 30,906,836 | |

| | | | | | | | |

| | |

| | | Number of shares | | | | |

| |

Preferred Stock – 0.50% | | | | | |

| |

Bank of America 6.50% µ | | | 220,000 | | | | 249,307 | |

GMAC Capital Trust I 7.695% (LIBOR03M + 5.785%) 2/15/40● | | | 2,000 | | | | 51,860 | |

Washington Prime Group 6.875% | | | 5,800 | | | | 120,125 | |

| | | | | | | | |

Total Preferred Stock

(cost $401,122) | | | | | | | 421,292 | |

| | | | | | | | |

|

| |

Exchange-Traded Fund – 1.92% | |

| |

VanEck Vectors Oil Services ETF | | | 138,800 | | | | 1,622,572 | |

| | | | | | | | |

Total Exchange-Traded Fund

(cost $1,648,208) | | | | 1,622,572 | |

| | | | | | | | |

|

| |

Rights – 0.00% | | | | | |

| |

DISH Network† | | | 119 | | | | 81 | |

| | | | | | | | |

Total Right(cost $0) | | | | | | | 81 | |

| | | | | | | | |

|

| |

Short-Term Investments – 7.32% | |

| |

Money Market Mutual Funds – 7.32% | |

BlackRock FedFund – Institutional Shares(seven-day effective yield 1.55%) | | | 1,236,558 | | | | 1,236,558 | |

Fidelity Investments Money Market Government Portfolio – Class I(seven-day effective yield 1.53%) | | | 1,236,558 | | | | 1,236,558 | |

14

| | | | | | | | |

| | | Number of

shares | | | Value

(US $) | |

| |

Short-Term Investments (continued) | | | | | |

| |

Money Market Mutual Funds (continued) | |

GS Financial Square Government Fund

– Institutional Shares(seven-day effective yield 1.54%) | | | 1,236,558 | | | $ | 1,236,558 | |

Morgan Stanley Government Portfolio – Institutional Share Class(seven-day effective yield 1.52%) | | | 1,236,558 | | | | 1,236,558 | |

State Street Institutional US Government Money Market Fund – Investor Class(seven-day effective yield 1.51%) | | | 1,236,558 | | | | 1,236,558 | |

| | | | | | | | |

Total Short-Term Investments

(cost $6,182,790) | | | | | | | 6,182,790 | |

| | | | | | | | |

Total Value of Securities – 144.05% (cost $102,247,011) | | | | | | $ | 121,693,389 | |

| | | | | | | | |

| # | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. At Nov. 30, 2019, the aggregate value of Rule 144A securities was $17,942,694, which represents 21.24% of the Fund’s net assets. See Note 10 in “Notes to financial statements.” |

| = | The value of this security was determined using significant unobservable inputs and is reported as a Level 3 security in the disclosure table located in Note 3 in “Notes to financial statements.” |

| ° | Principal amount shown is stated in USD unless noted that the security is denominated in another currency. |

| µ | Fixed to variable rate investment. The rate shown reflects the fixed rate in effect at Nov. 30, 2019. Rate will reset at a future date. |

| y | No contractual maturity date. |

| † | Non-income producing security. |

| ● | Variable rate investment. Rates reset periodically. Rate shown reflects the rate in effect at Nov. 30, 2019. For securities based on a published reference rate and spread, the reference rate and spread are indicated in their description above. The reference rate descriptions (i.e. LIBOR03M, LIBOR06M, etc.) used in this report are identical for different securities, but the underlying reference rates may differ due to the timing of the reset period. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions, or for mortgage-backed securities, are impacted by the individual mortgages which are paying off over time. These securities do not indicate a reference rate and spread in their description above. |

Summary of abbreviations:

ETF – Exchange-Traded Fund

GS – Goldman Sachs

ICE – Intercontinental Exchange

LIBOR – London Interbank Offered Rate

LIBOR03M – ICE LIBOR USD 3 Month

LIBOR06M – ICE LIBOR USD 6 Month

REIT – Real Estate Investment Trust

USD – US Dollar

See accompanying notes, which are an integral part of the financial statements.

Statement of assets and liabilities

Delaware Investments® Dividend and Income Fund, Inc.

November 30, 2019

| | | | |

Assets: | | | | |

Investments, at value1 | | $ | 121,693,389 | |

Foreign currencies, at value2 | | | 237,751 | |

Receivable for securities sold | | | 863,993 | |

Dividends and interest receivable | | | 685,077 | |

Foreign tax reclaims receivable | | | 4,812 | |

| | | | |

Total assets | | | 123,485,022 | |

| | | | |

Liabilities: | | | | |

Borrowing under line of credit | | | 35,000,000 | |

Payable for securities purchased | | | 3,816,947 | |

Other accrued expenses | | | 104,052 | |

Investment management fees payable to affiliates | | | 54,221 | |

Interest expense payable on line of credit | | | 18,285 | |

Legal fees payable to affiliates | | | 8,890 | |

Accounting and administration expenses payable to affiliates | | | 657 | |

Reports and statements to shareholders expenses payable to affiliates | | | 48 | |

Cash due to custodian | | | 585 | |

Directors’ fees and expenses payable to affiliates | | | 1 | |

| | | | |

Total liabilities | | | 39,003,686 | |

| | | | |

Total Net Assets | | $ | 84,481,336 | |

| | | | |

| |

Net Assets Consist of: | | | | |

Common stock, $0.01 par value, 500,000,000 shares authorized to the Fund | | $ | 65,099,486 | |

Total distributable earnings (loss) | | | 19,381,850 | |

| | | | |

Total Net Assets | | $ | 84,481,336 | |

| | | | |

| |

Net Asset Value | | | | |

| |

Common Shares | | | | |

Net assets | | $ | 84,481,336 | |

Shares of beneficial interest outstanding | | | 7,688,159 | |

Net asset value per share | | $ | 10.99 | |

| | | | |

1Investments, at cost | | $ | 102,247,011 | |

2Foreign currencies, at cost | | | 241,918 | |

See accompanying notes, which are an integral part of the financial statements.

16

Statement of operations

Delaware Investments® Dividend and Income Fund, Inc.

Year ended November 30, 2019

| | | | |

Investment Income: | | | | |

Interest | | $ | 2,739,424 | |

Dividends | | | 2,296,163 | |

Foreign tax withheld | | | (4,074 | ) |

| | | | |

| | | 5,031,513 | |

| | | | |

Expenses: | | | | |

Interest expense | | | 1,126,431 | |

Management fees | | | 652,803 | |

Legal fees | | | 397,029 | |

Reports and statements to shareholders expenses | | | 158,273 | |

Dividend disbursing and transfer agent fees and expenses | | | 86,170 | |

Accounting and administration expenses | | | 64,459 | |

Audit and tax fees | | | 47,221 | |

Custodian fees | | | 5,909 | |

Directors’ fees and expenses | | | 4,919 | |

Registration fees | | | 288 | |

Other expenses | | | 83,130 | |

| | | | |

| | | 2,626,632 | |

Less expenses paid indirectly | | | (522 | ) |

| | | | |

Total operating expenses | | | 2,626,110 | |

| | | | |

Net Investment Income | | | 2,405,403 | |

| | | | |

| |

Net Realized and Unrealized Gain (Loss): | | | | |

Net realized gain (loss) on: | | | | |

Investments* | | | 4,860,667 | |

Foreign currencies | | | (8,263 | ) |

Foreign currency exchange contracts | | | (1,177 | ) |

Options written | | | 589,991 | |

| | | | |

Net realized gain | | | 5,441,218 | |

| | | | |

| |

Net change in unrealized appreciation (depreciation) of: | | | | |

Investments | | | (223,163 | ) |

Foreign currencies | | | 5,801 | |

| | | | |

Net change in unrealized appreciation (depreciation) | | | (217,362 | ) |

| | | | |

Net Realized and Unrealized Gain | | | 5,223,856 | |

| | | | |

| |

Net Increase in Net Assets Resulting from Operations | | $ | 7,629,259 | |

| | | | |

*Includes $151,801 related to General Motors term loan litigation. See Note 12 in “Notes to financial statements.”

See accompanying notes, which are an integral part of the financial statements.

Statements of changes in net assets

Delaware Investments® Dividend and Income Fund, Inc.

| | | | | | | | |

| | | Year ended | |

| | | 11/30/19 | | | 11/30/18 | |

Increase (Decrease) in Net Assets from Operations: | | | | | | | | |

Net investment income | | $ | 2,405,403 | | | $ | 2,117,294 | |

Net realized gain | | | 5,441,218 | | | | 6,206,741 | |

Net change in unrealized appreciation (depreciation) | | | (217,362 | ) | | | (6,079,580 | ) |

| | | | | | | | |

Net increase in net assets resulting from operations | | | 7,629,259 | | | | 2,244,455 | |

| | | | | | | | |

| | |

Dividends and Distributions to Shareholders from: | | | | | | | | |

Distributable earnings | | | (8,391,625 | ) | | | (9,916,955 | ) |

| | | | | | | | |

| | | (8,391,625 | ) | | | (9,916,955 | ) |

| | | | | | | | |

| | |

Net Decrease in Net Assets | | | (762,366 | ) | | | (7,672,500 | ) |

| | |

Net Assets: | | | | | | | | |

Beginning of year | | | 85,243,702 | | | | 92,916,202 | |

| | | | | | | | |

End of year | | $ | 84,481,336 | | | $ | 85,243,702 | |

| | | | | | | | |

See accompanying notes, which are an integral part of the financial statements.

18

Statement of cash flows

Delaware Investments® Dividend and Income Fund, Inc.

Year ended November 30, 2019

| | | | |

Net Cash (including Foreign Currency) Provided by (Used for) Operating Activities: | | | | |

Net increase in net assets resulting from operations | | $ | 7,629,259 | |

| | | | |

| |

Adjustments to reconcile net increase (decrease) in net assets from operations to cash provided by (used for) operating activities: | | | | |

Amortization of premium and accretion of discount on investments, net | | | (654,509 | ) |

Proceeds from disposition of investment securities | | | 67,622,029 | |

Purchase of investment securities | | | (60,238,441 | ) |

(Purchase) Proceeds from disposition of short-term investment securities, net | | | (329,221 | ) |

Net realized (gain) loss on investments | | | (4,860,667 | ) |

Net realized (gain) loss on options written | | | (589,991 | ) |

Net change in unrealized (appreciation) depreciation of investments | | | 223,163 | |

Net change in unrealized (appreciation) depreciation of foreign currencies | | | (5,801 | ) |

Purchases in options written | | | 594,410 | |

Sales in options written | | | (4,419 | ) |

(Increase) Decrease in receivable for securities sold | | | (846,061 | ) |

(Increase) Decrease in dividends and interest receivable | | | (6,392 | ) |

Return of capital distributions on investments | | | 298,618 | |

Proceeds from GM litigation | | | 151,801 | |

(Increase) Decrease in foreign tax reclaims receivable | | | 1,532 | |

Increase (Decrease) in payable for securities purchased | | | 3,629,504 | |

Increase (Decrease) in Directors’ fees and expenses payable to affiliates | | | (676 | ) |

Increase (Decrease) in accounting and administration expenses payable to affiliates | | | (62 | ) |

Increase (Decrease) in investment management fees payable to affiliates | | | (2,234 | ) |

Increase (Decrease) in reports and statements to shareholders expenses payable to affiliates | | | (25 | ) |

Increase (Decrease) in legal fees payable to affiliates | | | 163 | |

Increase (Decrease) in other accrued expenses | | | 16,468 | |

Increase (Decrease) in other assets | | | 65,058 | |

Increase (Decrease in other liabilities | | | (216,859 | ) |

Increase (Decrease) in interest expense payable on line of credit | | | (2,715 | ) |

| | | | |

Total adjustments | | | 4,844,673 | |

| | | | |

Net cash provided by (used for) operating activities | | | 12,473,932 | |

| | | | |

| |

Cash provided by (used for) financing activities: | | | | |

Decrease in borrowing under line of credit | | | (5,000,000 | ) |

Cash dividends and distributions paid to shareholders | | | (8,391,625 | ) |

| | | | |

Net cash provided by (used for) financing activities | | | (13,391,625 | ) |

| | | | |

Effect of exchange rates on cash | | | 5,801 | |

| | | | |

Net increase (decrease) in cash | | | (911,892 | ) |

Cash at beginning of year | | | 1,149,058 | |

| | | | |

Cash at end of year | | $ | 237,166 | |

| | | | |

| |

Cash paid for interest expense on line of credit | | $ | 1,129,146 | |

| | | | |

Statement of cash flows

Year ended November 30, 2019

| | | | |

| The following table provides a reconciliation of cash, foreign currencies, and restricted cash reported within the statement of financial position that sum to the total of the same amounts shown on the previous page at November 30, 2019: | | | | |

Cash | | $ | (585 | ) |

Foreign currencies, at value | | | 237,751 | |

| | | | |

Total cash, foreign currencies, and restricted cash at end of year | | $ | 237,166 | |

| | | | |

See accompanying notes, which are an integral part of the financial statements.

20

Financial highlights

Delaware Investments® Dividend and Income Fund, Inc.

Selected data for each share of the Fund outstanding throughout each period were as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended | |

| | | | | |

| | | 11/30/19 | | | 11/30/18 | | | 11/30/17 | | | 11/30/16 | | | 11/30/15 | |

Net asset value, beginning of period | | $ | 11.09 | | | $ | 12.09 | | | $ | 10.96 | | | $ | 10.20 | | | $ | 11.14 | |

| | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income1 | | | 0.31 | | | | 0.28 | | | | 0.34 | | | | 0.38 | | | | 0.44 | |

Net realized and unrealized gain (loss) | | | 0.68 | | | | 0.01 | | | | 1.27 | | | | 0.97 | | | | (0.75 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.99 | | | | 0.29 | | | | 1.61 | | | | 1.35 | | | | (0.31 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Less dividends and distributions from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.09 | ) | | | (0.95 | ) | | | (0.48 | ) | | | (0.59 | ) | | | (0.63 | ) |

Net realized gain | | | — | | | | (0.34 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (1.09 | ) | | | (1.29 | ) | | | (0.48 | ) | | | (0.59 | ) | | | (0.63 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net asset value, end of period | | $ | 10.99 | | | $ | 11.09 | | | $ | 12.09 | | | $ | 10.96 | | | $ | 10.20 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Market value, end of period | | $ | 14.09 | | | $ | 12.42 | | | $ | 10.85 | | | $ | 9.70 | | | $ | 9.00 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total return based on2: | | | | | | | | | | | | | | | | | | | | |

Net asset value | | | 7.51% | 3 | | | 2.55% | | | | 15.49% | | | | 14.50% | | | | (2.26% | ) |

Market value | | | 23.07% | | | | 27.97% | | | | 17.11% | | | | 14.85% | | | | (4.41% | ) |

| | | | | |

Ratios and supplemental data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 84,481 | | | $ | 85,244 | | | $ | 92,916 | | | $ | 88,664 | | | $ | 86,919 | |

Ratio of expenses to average net assets4,5,6 | | | 3.15% | | | | 2.48% | | | | 2.09% | | | | 1.95% | | | | 1.71% | |

Ratio of net investment income to average net assets7 | | | 2.88% | | | | 2.37% | | | | 2.94% | | | | 3.68% | | | | 4.03% | |

Portfolio turnover | | | 52% | | | | 29% | | | | 36% | | | | 47% | | | | 43% | |

| | | | | |

Leverage analysis: | | | | | | | | | | | | | | | | | | | | |

Debt outstanding at end of period at par (000 omitted) | | $ | 35,000 | | | $ | 40,000 | | | $ | 40,000 | | | $ | 40,000 | | | $ | 38,000 | |

Asset coverage per $1,000 of debt outstanding at end of period | | $ | 3,414 | | | $ | 3,131 | | | $ | 3,323 | | | $ | 3,217 | | | $ | 3,287 | |

| 1 | The average shares outstanding method has been applied for per share information. |

| 2 | Total return is calculated assuming a purchase of common stock on the opening of the first day and a sale on the closing of the last day of each period reported. Dividends and distributions, if any, are assumed for the purpose of this calculation, to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Generally, total investment return based on net asset value will be higher than total investment return based on market value in periods where there is an increase in the discount or decrease in the premium of the market value to the net asset value from the beginning to the end of such periods. Conversely, total return based on net asset value will be lower than total return based on market value in periods where there is a decrease in the discount or an increase in the premium of the market value to the net asset value from the beginning to the end of such periods. |

| 3 | General Motors term loan litigation was included in total return. If excluded, the impact on the total return would be 0.18% lower. See Note 12 in “Notes to financial statements.” |

| 4 | The ratio of interest expense to adjusted average net assets (excluding debt outstanding) for the years ended Nov. 30, 2019, 2018, 2017, 2016, and 2015 were 0.95%, 0.85%, 0.58%, 0.41%, and 0.32%, respectively. |

| 5 | The ratio of interest expense to average net assets for the years ended Nov. 30, 2019, 2018, 2017, 2016, and 2015 were 1.35%, 1.23%, 0.84%, 0.59%, and 0.45%, respectively. |

| 6 | The ratio of expenses before interest expense to adjusted average net assets (excluding debt outstanding) for the years ended Nov. 30, 2019, 2018, 2017, 2016, and 2015 were 1.26%, 0.86%, 0.87%, 0.95%, and 0.89%, respectively. |

| 7 | The ratio of net investment income to adjusted average net assets (excluding debt outstanding) for the years ended Nov. 30, 2019, 2018, 2017, 2016, and 2015 were 2.03%, 1.64%, 2.05%, 2.56%, and 2.85%, respectively. |

See accompanying notes, which are an integral part of the financial statements.

Notes to financial statements

Delaware Investments® Dividend and Income Fund, Inc.

November 30, 2019

Delaware Investments Dividend and Income Fund, Inc. (Fund) is organized as a Maryland corporation and is a diversifiedclosed-end management investment company under the Investment Company Act of 1940, as amended (1940 Act). The Fund’s shares trade on the New York Stock Exchange (NYSE) under the symbol DDF.

The Fund’s primary investment objective is to seek high current income; capital appreciation is a secondary objective.

1. Significant Accounting Policies

The Fund follows accounting and reporting guidance under Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946, Financial Services – Investment Companies. The following accounting policies are in accordance with US generally accepted accounting principles (US GAAP) and are consistently followed by the Fund.