Exhibit 13

FINANCIAL PERFORMANCE

FINANCIAL TABLE OF CONTENTS

|

| |

| Financial Summary | |

| | |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| | |

| Reports of Management and the Independent Registered Public Accounting Firm | |

| | |

| Consolidated Financial Statements and Notes | |

| | |

| Cautionary Statement Regarding Forward-Looking Information | |

| | |

| Shareholder Information | |

| | |

| Corporate Officers and Operating Management | |

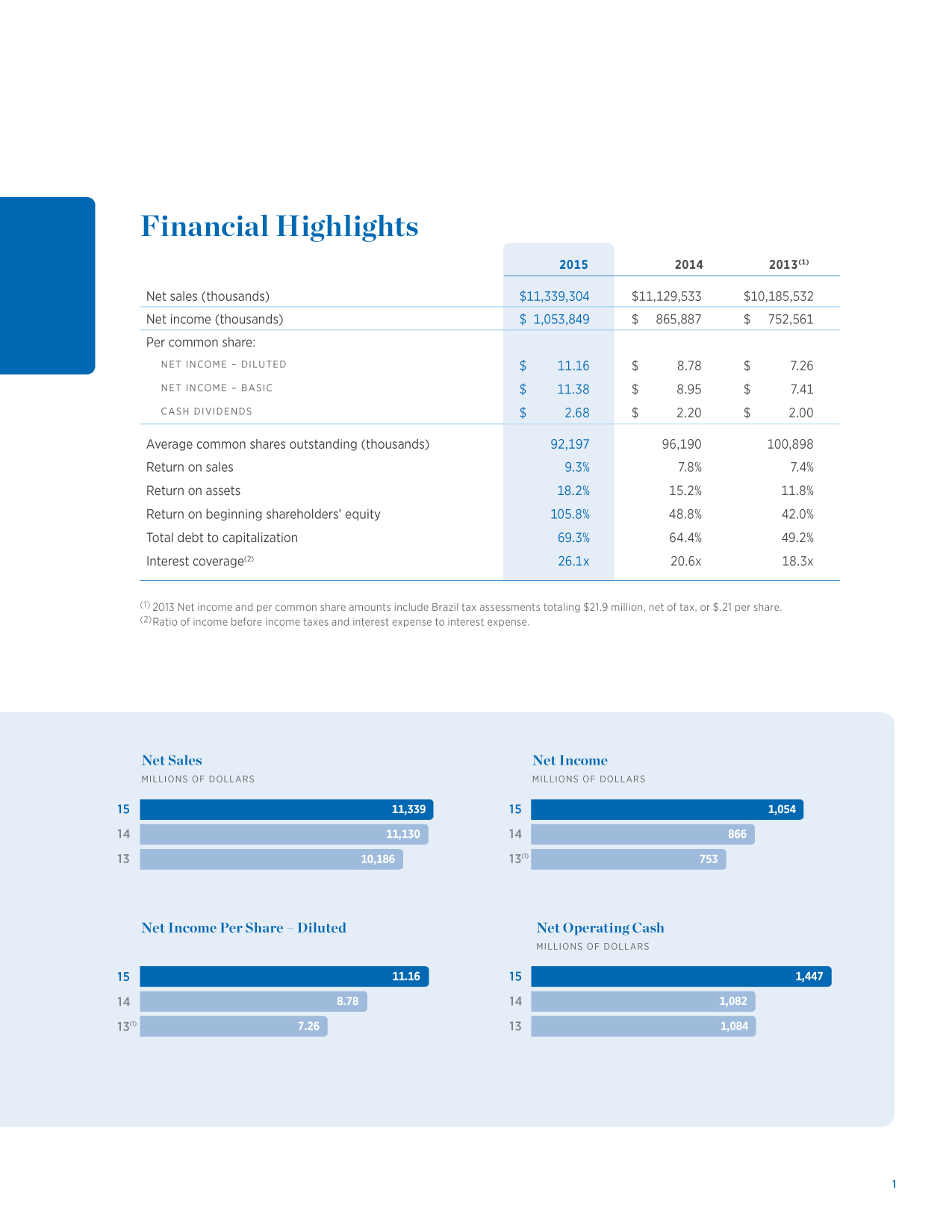

FINANCIAL SUMMARY

(millions of dollars except as noted and per share data)

|

| | | | | | | | | | | | | | | | | | | |

| | 2015 | | 2014 | | 2013 | | 2012 | | 2011 |

| Operations | | | | | | | | | |

| Net sales | $ | 11,339 |

| | $ | 11,130 |

| | $ | 10,186 |

| | $ | 9,534 |

| | $ | 8,766 |

|

| Cost of goods sold | 5,780 |

| | 5,965 |

| | 5,569 |

| | 5,328 |

| | 5,021 |

|

| Selling, general and administrative expenses | 3,914 |

| | 3,823 |

| | 3,468 |

| | 3,260 |

| | 2,961 |

|

| Impairments and dissolution | | | | | | | 4 |

| | 5 |

|

| Interest expense | 62 |

| | 64 |

| | 63 |

| | 43 |

| | 42 |

|

| Income before income taxes | 1,549 |

| | 1,258 |

| | 1,086 |

| | 907 |

| | 742 |

|

| Net income | 1,054 |

| | 866 |

| | 753 |

| | 631 |

| | 442 |

|

| Financial Position | | | | | | | | | |

| Accounts receivable - net | $ | 1,114 |

| | $ | 1,131 |

| | $ | 1,098 |

| | $ | 1,033 |

| | $ | 990 |

|

| Inventories | 1,019 |

| | 1,034 |

| | 971 |

| | 920 |

| | 927 |

|

| Working capital - net | 517 |

| | (114 | ) | | 630 |

| | 1,273 |

| | 99 |

|

| Property, plant and equipment - net | 1,042 |

| | 1,021 |

| | 1,021 |

| | 966 |

| | 957 |

|

| Total assets | 5,792 |

| | 5,706 |

| | 6,383 |

| | 6,235 |

| | 5,229 |

|

| Long-term debt | 1,920 |

| | 1,123 |

| | 1,122 |

| | 1,632 |

| | 639 |

|

| Total debt | 1,963 |

| | 1,805 |

| | 1,722 |

| | 1,705 |

| | 993 |

|

| Shareholders’ equity | 868 |

| | 996 |

| | 1,775 |

| | 1,792 |

| | 1,517 |

|

| Per Common Share Information | | | | | | | | | |

| Average shares outstanding (thousands) | 92,197 |

| | 96,190 |

| | 100,898 |

| | 101,715 |

| | 103,471 |

|

| Book value | $ | 9.41 |

| | $ | 10.52 |

| | $ | 17.72 |

| | $ | 17.35 |

| | $ | 14.61 |

|

| Net income - diluted (1) | 11.16 |

| | 8.78 |

| | 7.26 |

| | 6.02 |

| | 4.14 |

|

| Net income - basic (1) | 11.38 |

| | 8.95 |

| | 7.41 |

| | 6.15 |

| | 4.22 |

|

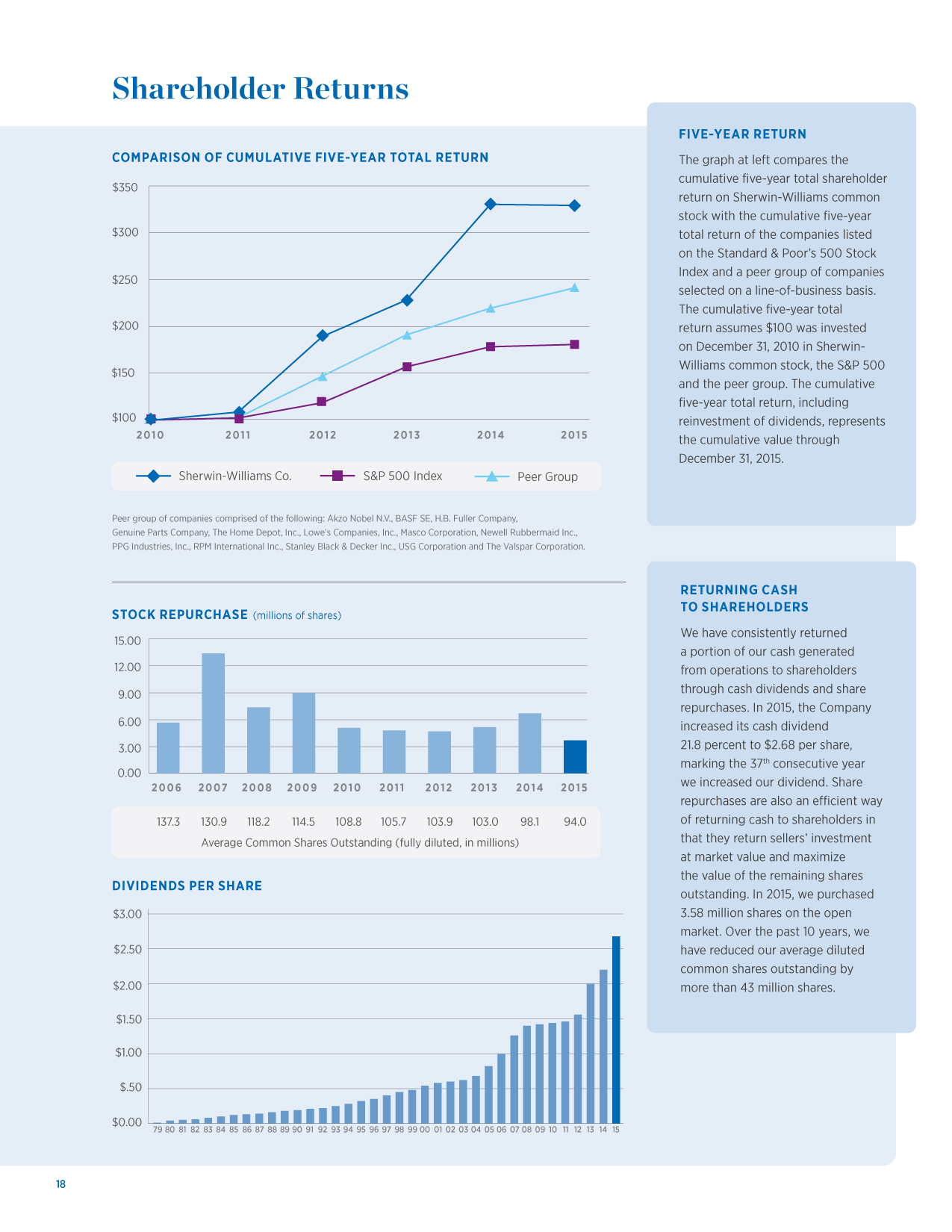

| Cash dividends | 2.68 |

| | 2.20 |

| | 2.00 |

| | 1.56 |

| | 1.46 |

|

| Financial Ratios | | | | | | | | | |

| Return on sales | 9.3 | % | | 7.8 | % | | 7.4 | % | | 6.6 | % | | 5.0 | % |

| Asset turnover | 2.0 | x | | 2.0 | x | | 1.6 | x | | 1.5 | x | | 1.7 | x |

| Return on assets | 18.2 | % | | 15.2 | % | | 11.8 | % | | 10.1 | % | | 8.4 | % |

| Return on equity (2) | 105.8 | % | | 48.8 | % | | 42.0 | % | | 41.6 | % | | 27.5 | % |

| Dividend payout ratio (3) | 30.5 | % | | 30.3 | % | | 33.2 | % | | 37.7 | % | | 34.7 | % |

| Total debt to capitalization | 69.3 | % | | 64.4 | % | | 49.2 | % | | 48.8 | % | | 39.6 | % |

| Current ratio | 1.2 |

| | 1.0 |

| | 1.2 |

| | 1.7 |

| | 1.0 |

|

| Interest coverage (4) | 26.1 | x | | 20.6 | x | | 18.3 | x | | 22.2 | x | | 18.4 | x |

| Net working capital to sales | 4.6 | % | | (1.0 | )% | | 6.2 | % | | 13.3 | % | | 1.1 | % |

| Effective income tax rate (5) | 32.0 | % | | 31.2 | % | | 30.7 | % | | 30.4 | % | | 40.4 | % |

| General | | | | | | | | | |

| Capital expenditures | $ | 234 |

| | $ | 201 |

| | $ | 167 |

| | $ | 157 |

| | $ | 154 |

|

| Total technical expenditures (6) | 150 |

| | 155 |

| | 144 |

| | 140 |

| | 130 |

|

| Advertising expenditures | 338 |

| | 299 |

| | 263 |

| | 247 |

| | 227 |

|

| Repairs and maintenance | 99 |

| | 96 |

| | 87 |

| | 83 |

| | 78 |

|

| Depreciation | 170 |

| | 169 |

| | 159 |

| | 152 |

| | 151 |

|

| Amortization of intangible assets | 28 |

| | 30 |

| | 29 |

| | 27 |

| | 30 |

|

| Shareholders of record (total count) | 6,987 |

| | 7,250 |

| | 7,555 |

| | 7,954 |

| | 8,360 |

|

| Number of employees (total count) | 40,706 |

| | 39,674 |

| | 37,633 |

| | 34,154 |

| | 32,988 |

|

| Sales per employee (thousands of dollars) | $ | 279 |

| | $ | 281 |

| | $ | 271 |

| | $ | 279 |

| | $ | 266 |

|

| Sales per dollar of assets | 1.96 |

| | 1.95 |

| | 1.60 |

| | 1.53 |

| | 1.68 |

|

| |

| (1) | All earnings per share amounts are presented using the two-class method. See Note 15. |

| |

| (2) | Based on net income and shareholders’ equity at beginning of year. |

| |

| (3) | Based on cash dividends per common share and prior year’s diluted net income per common share. |

| |

| (4) | Ratio of income before income taxes and interest expense to interest expense. |

| |

| (5) | Based on income before income taxes. |

| |

| (6) | See Note 1, page 49 of this report, for a description of technical expenditures. |

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

SUMMARY

The Sherwin-Williams Company, founded in 1866, and its consolidated wholly owned subsidiaries (collectively, the “Company”) are engaged in the development, manufacture, distribution and sale of paint, coatings and related products to professional, industrial, commercial and retail customers primarily in North and South America with additional operations in the Caribbean region, Europe and Asia. The Company is structured into four reportable segments – Paint Stores Group, Consumer Group, Global Finishes Group and Latin America Coatings Group (collectively, the “Reportable Segments”) – and an Administrative Segment in the same way it is internally organized for assessing performance and making decisions regarding allocation of resources. See pages 8 through 17 of this report and Note 18, on pages 72 through 75 of this report, for more information concerning the Reportable Segments.

The Company’s financial condition, liquidity and cash flow continued to be strong in 2015 as net operating cash topped $1.000 billion for the third straight year primarily due to improved operating results in our Paint Stores and Consumer Groups. Net working capital increased $630.9 million at December 31, 2015 compared to 2014 due to a significant decrease in current liabilities and an increase in current assets. Cash and cash equivalents along with cash flow from operations were used primarily to purchase $1.035 billion in treasury stock. Short-term borrowings decreased $640.0 million due to strong cash flow and issuance of long-term debt. On July 28, 2015, the Company issued $400.0 million of 3.45% Senior Notes due 2025 and $400.0 million of 4.55% Senior Notes due 2045. The proceeds will be used for general corporate purposes, including repayment of a portion of the Company’s outstanding short-term borrowings. The Company has been able to arrange sufficient short-term borrowing capacity at reasonable rates, and the Company has sufficient total available borrowing capacity to fund its current operating needs. Net operating cash increased $365.9 million to $1.447 billion in 2015 from $1.082 billion in 2014. Strong net operating cash provided the funds necessary to invest in new stores, manufacturing and distribution facilities, renovate and convert acquired stores, and return cash to shareholders through dividends and treasury stock purchases.

Results of operations for the Company were strong and improved in many areas in 2015, primarily due to an improving domestic architectural paint market. Consolidated net sales increased 1.9 percent in 2015 to $11.339 billion from $11.130 billion in 2014 due primarily to higher paint sales volume in the Paint Stores and Consumer Groups. Consolidated gross profit as a percent of consolidated net sales increased to 49.0 percent in 2015 from 46.4 percent in 2014 due primarily to increased paint sales volume and improved operating efficiency. Gross profit in

2014 included a titanium dioxide suppliers antitrust class action lawsuit settlement of $21.4 million received by the Company in the fourth quarter of 2014 (the "2014 TiO2 settlement"). Selling, general and administrative expenses (SG&A) increased $90.6 million in 2015 compared to 2014 and increased as a percent of consolidated net sales to 34.5 percent in 2015 as compared to 34.3 percent in 2014 due primarily due to new stores openings and expenses related to the launch of a new paint program at a national retailer partially offset by foreign currency translation rate fluctuations. Lower average borrowing rates more than offset higher average borrowing levels on total debt throughout 2015 resulting in decreased interest expense of $2.4 million in 2015. The effective income tax rate was 32.0 percent for 2015 and 31.2 percent for 2014. Diluted net income per common share increased 27.1 percent to $11.16 per share for 2015 from $8.78 per share a year ago.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation and fair presentation of the consolidated financial statements, accompanying notes and related financial information included in this report are the responsibility of management. The consolidated financial statements, accompanying notes and related financial information included in this report have been prepared in accordance with U.S. generally accepted accounting principles. The consolidated financial statements contain certain amounts that were based upon management’s best estimates, judgments and assumptions. Management utilized certain outside economic sources of information when developing the bases for their estimates and assumptions. Management used assumptions based on historical results, considering the current economic trends, and other assumptions to form the basis for determining appropriate carrying values of assets and liabilities that were not readily available from other sources. Actual results could differ from those estimates. Also, materially different amounts may result under materially different conditions, materially different economic trends or from using materially different assumptions. However, management believes that any materially different amounts resulting from materially different conditions or material changes in facts or circumstances are unlikely to significantly impact the current valuation of assets and liabilities that were not readily available from other sources.

All of the significant accounting policies that were followed in the preparation of the consolidated financial statements are disclosed in Note 1, on pages 46 through 49, of this report. The following procedures and assumptions utilized by management directly impacted many of the reported amounts in the consolidated financial statements.

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

Non-Traded Investments

The Company has investments in the U.S. affordable housing and historic renovation real estate markets and certain other investments that have been identified as variable interest entities. The Company does not have the power to direct the day-to-day operations of the investments and the risk of loss is limited to the amount of contributed capital, and therefore, the Company is not considered the primary beneficiary. In accordance with the Consolidation Topic of the ASC, the investments are not consolidated. For affordable housing investments entered into prior to the January 1, 2015 adoption of ASU No. 2014-01, the Company uses the effective yield method to determine the carrying value of the investments. Under the effective yield method, the initial cost of the investments is amortized to income tax expense over the period that the tax credits are recognized. For affordable housing investments entered into on or after the January 1, 2015 adoption of ASU No. 2014-01, the Company uses the proportional amortization method. Under the proportional amortization method, the initial cost of the investments is amortized to income tax expense in proportion to the tax credits and other tax benefits received. The Company has no ongoing capital commitments, loan requirements or guarantees with the general partners that would require any future cash contributions other than the contractually committed capital contributions that are disclosed in the contractual obligations table on page 29 of this report. See Note 1, on page 46 of this report, for more information on non-traded investments.

Accounts Receivable

Accounts receivable were recorded at the time of credit sales net of provisions for sales returns and allowances. All provisions for allowances for doubtful collection of accounts are included in Selling, general and administrative expenses and were based on management’s best judgment and assessment, including an analysis of historical bad debts, a review of the aging of Accounts receivable and a review of the current creditworthiness of customers. Management recorded allowances for such accounts which were believed to be uncollectible, including amounts for the resolution of potential credit and other collection issues such as disputed invoices, customer satisfaction claims and pricing discrepancies. However, depending on how such potential issues are resolved, or if the financial condition of any of the Company’s customers were to deteriorate and their ability to make required payments became impaired, increases in these allowances may be required. At December 31, 2015, no individual customer constituted more than 5 percent of Accounts receivable.

Inventories

Inventories were stated at the lower of cost or market with cost determined principally on the last-in, first-out (LIFO) method based on inventory quantities and costs determined during the fourth quarter. Inventory quantities were adjusted during the fourth quarter as a result of annual physical inventory counts taken at all locations. If inventories accounted for on the LIFO method are reduced on a year-over-year basis, then liquidation of certain quantities carried at costs prevailing in prior years occurs. Management recorded the best estimate of net realizable value for obsolete and discontinued inventories based on historical experience and current trends through reductions to inventory cost by recording a provision included in Cost of goods sold. Where management estimated that the reasonable market value was below cost or determined that future demand was lower than current inventory levels, based on historical experience, current and projected market demand, current and projected volume trends and other relevant current and projected factors associated with the current economic conditions, a reduction in inventory cost to estimated net realizable value was made. See Note 3, on page 50 of this report, for more information regarding the impact of the LIFO inventory valuation.

Purchase Accounting, Goodwill and Intangible Assets

In accordance with the Business Combinations Topic of the ASC, the Company used the purchase method of accounting to allocate costs of acquired businesses to the assets acquired and liabilities assumed based on their estimated fair values at the dates of acquisition. The excess costs of acquired businesses over the fair values of the assets acquired and liabilities assumed were recognized as Goodwill. The valuations of the acquired assets and liabilities will impact the determination of future operating results. In addition to using management estimates and negotiated amounts, the Company used a variety of information sources to determine the estimated fair values of acquired assets and liabilities including: third-party appraisals for the estimated value and lives of identifiable intangible assets and property, plant and equipment; third-party actuaries for the estimated obligations of defined benefit pension plans and similar benefit obligations; and legal counsel or other experts to assess the obligations associated with legal, environmental and other contingent liabilities. The business and technical judgment of management was used in determining which intangible assets have indefinite lives and in determining the useful lives of finite-lived intangible assets in accordance with the Goodwill and Other Intangibles Topic of the ASC.

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

As required by the Goodwill and Other Intangibles Topic of the ASC, management performs impairment tests of goodwill and indefinite-lived intangible assets on an annual basis, as well as whenever an event occurs or circumstances change that indicate impairment has more likely than not occurred. The qualitative assessment allows companies to skip the annual two-step quantitative test if it is not more likely than not that impairment has occurred based on monitoring key Company financial performance metrics and macroeconomic conditions. The optional qualitative assessment is performed when deemed appropriate.

In accordance with the Goodwill and Other Intangibles Topic of the ASC, management tests goodwill for impairment at the reporting unit level. A reporting unit is an operating segment per the Segment Reporting Topic of the ASC or one level below the operating segment (component level) as determined by the availability of discrete financial information that is regularly reviewed by operating segment management or an aggregate of component levels of an operating segment having similar economic characteristics. At the time of goodwill impairment testing (if performing a quantitative assessment), management determines fair value through the use of a discounted cash flow valuation model incorporating discount rates commensurate with the risks involved for each reporting unit. If the calculated fair value is less than the current carrying value, impairment of the reporting unit may exist. The use of a discounted cash flow valuation model to determine estimated fair value is common practice in impairment testing. The key assumptions used in the discounted cash flow valuation model for impairment testing include discount rates, growth rates, cash flow projections and terminal value rates. Discount rates are set by using the Weighted Average Cost of Capital (“WACC”) methodology. The WACC methodology considers market and industry data as well as Company-specific risk factors for each reporting unit in determining the appropriate discount rates to be used. The discount rate utilized for each reporting unit is indicative of the return an investor would expect to receive for investing in such a business. Operational management, considering industry and Company-specific historical and projected data, develops growth rates, sales projections and cash flow projections for each reporting unit. Terminal value rate determination follows common methodology of capturing the present value of perpetual cash flow estimates beyond the last projected period assuming a constant WACC and low long-term growth rates. As an indicator that each reporting unit has been valued appropriately through the use of the discounted cash flow valuation model, the aggregate of all reporting units fair value is reconciled to the total market capitalization of the Company.

The Company had six reporting units with goodwill as of October 1, 2015, the date of the annual impairment test. The fair values of each of the reporting units exceeded their respective carrying values by more than ten percent and no goodwill impairment was recorded in 2015. The Company performed a sensitivity analysis on the discount rate, which is a significant assumption in the calculation of the fair values. With a one percentage point increase in the discount rate, the reporting units would continue to have fair values in excess of their respective carrying values.

In accordance with the Goodwill and Other Intangibles Topic of the ASC, management tests indefinite-lived intangible assets for impairment at the asset level, as determined by appropriate asset valuations at acquisition. Management utilizes the royalty savings method and valuation model to determine the estimated fair value for each indefinite-lived intangible asset or trademark. In this method, management estimates the royalty savings arising from the ownership of the intangible asset. The key assumptions used in estimating the royalty savings for impairment testing include discount rates, royalty rates, growth rates, sales projections and terminal value rates. Discount rates used are similar to the rates developed by the WACC methodology considering any differences in Company-specific risk factors between reporting units and trademarks. Royalty rates are established by management and valuation experts and periodically substantiated by valuation experts. Operational management, considering industry and Company-specific historical and projected data, develops growth rates and sales projections for each significant trademark. Terminal value rate determination follows common methodology of capturing the present value of perpetual sales estimates beyond the last projected period assuming a constant WACC and low long-term growth rates. The royalty savings valuation methodology and calculations used in 2015 impairment testing are consistent with prior years.

The discounted cash flow and royalty savings valuation methodologies require management to make certain assumptions based upon information available at the time the valuations are performed. Actual results could differ from these assumptions. Management believes the assumptions used are reflective of what a market participant would have used in calculating fair value considering the current economic conditions. See Notes 2 and 4, on pages 50 through 51 of this report, for a discussion of businesses acquired, the estimated fair values of goodwill and identifiable intangible assets recorded at acquisition date and reductions in carrying value of goodwill and indefinite-lived intangible assets recorded as a result of impairment tests in accordance with the Goodwill and Other Intangibles Topic of the ASC.

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

Property, Plant and Equipment and Impairment of Long-Lived Assets

Property, plant and equipment was stated on the basis of cost and depreciated principally on a straight-line basis using industry standards and historical experience to estimate useful lives. In accordance with the Property, Plant and Equipment Topic of the ASC, if events or changes in circumstances indicated that the carrying value of long-lived assets may not be recoverable or the useful life had changed, impairment tests were performed or the useful life was adjusted. Undiscounted future cash flows were used to calculate the recoverable value of long-lived assets to determine if such assets were impaired. Where impairment was identified, management determined fair values for assets using a discounted cash flow valuation model, incorporating discount rates commensurate with the risks involved for each group of assets. Growth models were developed using both industry and company historical results and forecasts. If the usefulness of an asset was determined to be impaired, then management estimated a new useful life based on the period of time for projected uses of the asset. Such models and changes in useful life required management to make certain assumptions based upon information available at the time the valuation or determination was performed. Actual results could differ from these assumptions. Management believes the assumptions used are reflective of what a market participant would have used in calculating fair value or useful life considering the current economic conditions. All tested long-lived assets or groups of long-lived assets had undiscounted cash flows that were substantially in excess of their carrying value, except as noted in Note 4. See Notes 4 and 5, on pages 50 through 53 of this report, for a discussion of the reductions in carrying value or useful life of long-lived assets in accordance with the Property, Plant and Equipment Topic of the ASC.

Exit or Disposal Activities

Management is continually re-evaluating the Company’s operating facilities against its long-term strategic goals. Liabilities associated with exit or disposal activities are recognized as incurred in accordance with the Exit or Disposal Cost Obligations Topic of the ASC and property, plant and equipment is tested for impairment in accordance with the Property, Plant and Equipment Topic of the ASC. Provisions for qualified exit costs are made at the time a facility is no longer operational, include amounts estimated by management and primarily include post-closure rent expenses or costs to terminate the contract before the end of its term and costs of employee terminations. Adjustments may be made to liabilities accrued for qualified exit costs if information becomes available upon which more accurate amounts can be reasonably estimated. If impairment of property,

plant and equipment exists, then the carrying value is reduced to fair value estimated by management. Additional impairment may be recorded for subsequent revisions in estimated fair value. See Note 5, on pages 51 through 53 of this report, for information concerning impairment of property, plant and equipment and accrued qualified exit costs.

Other Liabilities

The Company retains risk for certain liabilities, primarily worker’s compensation claims, employee medical benefits, and automobile, property, general and product liability claims. Estimated amounts were accrued for certain worker’s compensation, employee medical and disability benefits, automobile and property claims filed but unsettled and estimated claims incurred but not reported based upon management’s estimated aggregate liability for claims incurred using historical experience, actuarial assumptions followed in the insurance industry and actuarially-developed models for estimating certain liabilities. Certain estimated general and product liability claims filed but unsettled were accrued based on management’s best estimate of ultimate settlement or actuarial calculations of potential liability using industry experience and actuarial assumptions developed for similar types of claims.

Defined Benefit Pension and Other Postretirement Benefit Plans

To determine the Company’s ultimate obligation under its defined benefit pension plans and postretirement benefit plans other than pensions, management must estimate the future cost of benefits and attribute that cost to the time period during which each covered employee works. To determine the obligations of such benefit plans, management uses actuaries to calculate such amounts using key assumptions such as discount rates, inflation, long-term investment returns, mortality, employee turnover, rate of compensation increases and medical and prescription drug costs. Management reviews all of these assumptions on an ongoing basis to ensure that the most current information available is being considered. An increase or decrease in the assumptions or economic events outside management’s control could have a direct impact on the Company’s results of operations or financial condition.

In accordance with the Retirement Benefits Topic of the ASC, the Company recognizes each plan’s funded status as an asset for overfunded plans and as a liability for unfunded or underfunded plans. Actuarial gains and losses and prior service costs are recognized and recorded in Cumulative other comprehensive loss, a component of Shareholders’ equity. The amounts recorded in Cumulative other comprehensive loss will continue to be modified as actuarial assumptions and service

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

costs change, and all such amounts will be amortized to expense over a period of years through the net pension and net periodic benefit costs.

Effective July 1, 2009, the domestic salaried defined benefit pension plan was revised. Prior to July 1, 2009, the contribution was based on six percent of compensation for certain covered employees. Under the revised plan, such participants are credited with certain contribution credits that range from two percent to seven percent of compensation based on an age and service formula.

A reduction in the over-funded status of the Company’s defined benefit pension plans at December 31, 2008 due to the decrease in market value of equity securities held by the plans increased the future amortization of actuarial losses recognized in Cumulative comprehensive loss. This amortization increased net pension costs in 2013, 2014 and 2015. An increase in market value of equity securities held by the plans during 2013 and 2014 will decrease the future amortization of actuarial losses recognized in Cumulative comprehensive loss. The deficit in market value of equity securities held by the plans versus the expected returns in 2015 will increase the future amortization of actuarial losses. The amortization of actuarial losses on plan assets, only partially offset by an increase in discount rates on projected benefit obligations, will increase net pension costs in 2016. See Note 6, on pages 54 through 59 of this report, for information concerning the Company’s defined benefit pension plans and postretirement benefit plans other than pensions.

Debt

The fair values of the Company’s publicly traded long-term debt were based on quoted market prices. The fair values of the Company’s non-traded long-term debt were estimated using discounted cash flow analyses, based on the Company’s current incremental borrowing rates for similar types of borrowing arrangements. See Note 1, on page 46 of this report, for the carrying amounts and fair values of the Company’s long-term debt, and Note 7, on page 60 of this report, for a description of the Company’s long-term debt arrangements.

Environmental Matters

The Company is involved with environmental investigation and remediation activities at some of its currently and formerly owned sites and at a number of third-party sites. The Company accrues for environmental-related activities for which commitments or clean-up plans have been developed and for which costs can be reasonably estimated based on industry standards and professional judgment. All accrued amounts were recorded on an undiscounted basis. Environmental-related expenses included direct costs of investigation and remediation

and indirect costs such as compensation and benefits for employees directly involved in the investigation and remediation activities and fees paid to outside engineering, actuarial, consulting and law firms. Due to uncertainties surrounding environmental investigations and remediation activities, the Company’s ultimate liability may result in costs that are significantly higher than currently accrued. See page 29 and Note 8, on pages 60 through 62 of this report, for information concerning the accrual for extended environmental-related activities and a discussion concerning unaccrued future loss contingencies.

Litigation and Other Contingent Liabilities

In the course of its business, the Company is subject to a variety of claims and lawsuits, including, but not limited to, litigation relating to product liability and warranty, personal injury, environmental, intellectual property, commercial, contractual and antitrust claims. Management believes that the Company has properly accrued for all known liabilities that existed and those where a loss was deemed probable for which a fair value was available or an amount could be reasonably estimated in accordance with all present U.S. generally accepted accounting principles. However, because litigation is inherently subject to many uncertainties and the ultimate result of any present or future litigation is unpredictable, the Company’s ultimate liability may result in costs that are significantly higher than currently accrued. In the event that the Company’s loss contingency is ultimately determined to be significantly higher than currently accrued, the recording of the liability may result in a material impact on net income for the annual or interim period during which such liability is accrued. Additionally, due to the uncertainties involved, any potential liability determined to be attributable to the Company arising out of such litigation may have a material adverse effect on the Company’s results of operations, liquidity or financial condition. See Note 9 on pages 62 through 65 of this report for information concerning litigation.

Income Taxes

The Company estimated income taxes in each jurisdiction that it operated. This involved estimating taxable earnings, specific taxable and deductible items, the likelihood of generating sufficient future taxable income to utilize deferred tax assets and possible exposures related to future tax audits. To the extent these estimates change, adjustments to deferred and accrued income taxes will be made in the period in which the changes occur.

See Note 14, on pages 69 and 70 of this report, for information concerning the Company’s unrecognized tax benefits, interest and penalties and current and deferred tax expense.

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

Stock-Based Compensation

The cost of the Company’s stock-based compensation is recorded in accordance with the Stock Compensation Topic of the ASC. The Company follows the “modified prospective” method as described in the Topic whereby compensation cost is recognized for all share-based payments granted after December 31, 2005.

The Company estimates the fair value of option rights using a Black-Scholes-Merton option pricing model which requires management to make estimates for certain assumptions. Management and a consultant continuously review the following significant assumptions: risk-free interest rate, expected life of options, expected volatility of stock and expected dividend yield of stock. An increase or decrease in the assumptions or economic events outside management’s control could have a direct impact on the Company’s results of operations. See Note 12, on pages 67 and 68 of this report, for more information on stock-based compensation.

Revenue Recognition

The Company’s revenue was primarily generated from the sale of products. All sales of products were recognized when shipped and title had passed to unaffiliated customers. Collectibility of amounts recorded as revenue is reasonably assured at time of sale. Discounts were recorded as a reduction to sales in the same period as the sale resulting in an appropriate net sales amount for the period. Standard sales terms are final and returns or exchanges are not permitted unless expressly stated. Estimated provisions for returns or exchanges, recorded as a reduction resulting in net sales, were established in cases where the right of return existed. The Company offered a variety of programs, primarily to its retail customers, designed to promote sales of its products. Such programs required periodic payments and allowances based on estimated results of specific programs and were recorded as a reduction resulting in net sales. The Company accrued the estimated total payments and allowances associated with each transaction at the time of sale. Additionally, the Company offered programs directly to consumers to promote the sale of its products. Promotions that reduced the ultimate consumer sale prices were recorded as a reduction resulting in net sales at the time the promotional offer was made, generally using estimated redemption and participation levels. The Company continually assesses the adequacy of accruals for customer and consumer promotional program costs earned but not yet paid. To the extent total program payments differ from estimates, adjustments may be necessary. Historically, these total program payments and adjustments have not been material.

FINANCIAL CONDITION, LIQUIDITY AND CASH FLOW

Overview

The Company’s financial condition, liquidity and cash flow continued to be strong in 2015 as net operating cash topped $1.000 billion for the third straight year primarily due to improved operating results in our Paint Stores and Consumer Groups. Net working capital increased $630.9 million at December 31, 2015 compared to 2014 due to a significant decrease in current liabilities and an increase in current assets. Cash and cash equivalents along with cash flow from operations were used primarily to purchase $1.035 billion in treasury stock. Short-term borrowings decreased $640.0 million due to strong cash flow and issuance of long-term debt. On July 28, 2015, the Company issued $400.0 million of 3.45% Senior Notes due 2025 and $400.0 million of 4.55% Senior Notes due 2045. See the section that follows for more information regarding Net Working Capital. Total debt at December 31, 2015 increased $157.4 million to $1.963 billion from $1.805 billion at December 31, 2014 due primarily to the debt issuance on July 28, 2015. Total debt increased as a percentage of total capitalization to 69.3 percent from 64.4 percent at the end of 2014. At December 31, 2015, the Company had remaining borrowing ability of $2.078 billion.

Net operating cash increased $365.9 million to $1.447 billion in 2015 from $1.082 billion in 2014 due primarily to an increase in net income of $188.0 million and a reduction in working capital of $188.9 million due to timing of payments. Net operating cash increased as a percent to sales to 12.8 percent in 2015 compared to 9.7 percent in 2014. Strong Net operating cash provided the funds necessary to invest in new stores, manufacturing and distribution facilities, renovate and convert acquired stores and return cash to shareholders through dividends and treasury stock purchases. In 2015, the Company used Net operating cash and Cash and cash equivalents on hand to purchase $1.035 billion in treasury stock, spend $234.3 million in capital additions and improvements and pay $249.6 million in cash dividends to its shareholders of common stock.

Net Working Capital

Total current assets less Total current liabilities (net working capital) increased $630.9 million to a surplus of $517.0 million at December 31, 2015 from a deficit of $113.9 million at December 31, 2014. The net working capital increase is due to a significant decrease in current liabilities and an increase in current assets. Cash and cash equivalents increased $165.0 million. Short-term borrowings decreased $640.0 million. Accounts payable increased $115.4 million while Accrued taxes decreased $5.6 million and all other current liabilities, excluding current portion of long-term debt, decreased $8.5 million. Accounts receivable were

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

down $16.3 million, Inventories were down $15.0 million and Deferred tax net assets were down $21.2 million while the remaining current assets decreased $20.4 million. The Company has sufficient total available borrowing capacity to fund its current operating needs. The significant decrease in Short-term borrowings and significant increase in Cash and cash equivalents caused the Company’s current ratio to improve to 1.24 at December 31, 2015 from 0.96 at December 31, 2014. Accounts receivable as a percent of Net sales decreased to 9.8 percent in 2015 from 10.2 percent in 2014. Accounts receivable days outstanding decreased to 54 days in 2015 from 55 days in 2014. In 2015, provisions for allowance for doubtful collection of accounts decreased $4.3 million, or 8.1 percent. Inventories decreased slightly as a percent of Net sales to 9.0 percent in 2015 from 9.3 percent in 2014 due primarily to tighter inventory management. Inventory days outstanding was down at 83 days in 2015 versus 86 days in 2014. Accounts payable increased in 2015 to $1.158 billion compared to $1.042 billion last year due primarily to increased purchases to service higher sales levels and timing of payments.

Goodwill and Intangible Assets

Goodwill, which represents the excess of cost over the fair value of net assets acquired in purchase business combinations, decreased $15.0 million in 2015 due primarily to foreign currency translation rate fluctuations.

Intangible assets decreased $33.8 million in 2015. Decreases from amortization of finite-lived intangible assets of $28.2 million and foreign currency translation rate fluctuations of $7.9 million were partially offset by $2.4 million of capitalized software costs. Acquired finite-lived intangible assets included assets such as covenants not to compete, customer lists and product formulations. Costs related to designing, developing, obtaining and implementing internal use software are capitalized and amortized in accordance with the Goodwill and Other Intangibles Topic of the ASC. See Notes 2 and 4, on pages 50 through 51 of this report, for a description of acquired goodwill, identifiable intangible assets and asset impairments recorded in accordance with the Goodwill and Other Intangibles Topic of the ASC and summaries of the remaining carrying values of goodwill and intangible assets.

Deferred Pension and Other Assets

Deferred pension assets of $244.9 million at December 31, 2015 represent the excess of the fair value of assets over the actuarially determined projected benefit obligations, primarily of the domestic salaried defined benefit pension plan. The decrease in Deferred pension assets during 2015 of $5.3 million, from $250.1 million last year, was due primarily to a decrease in the fair

value of equity securities held by the salaried defined benefit pension plan partially offset by a decrease in the projected benefit obligations resulting from changes in actuarial assumptions. In accordance with the accounting prescribed by the Retirement Benefits Topic of the ASC, the decrease in the value of the Deferred pension assets is offset in Cumulative other comprehensive loss and is amortized as a component of Net pension costs over a defined period of pension service. See Note 6, on pages 54 through 59 of this report, for more information concerning the excess fair value of assets over projected benefit obligations of the salaried defined benefit pension plan and the amortization of actuarial gains or losses relating to changes in the excess assets and other actuarial assumptions.

Other assets increased $26.9 million to $447.5 million at December 31, 2015 due primarily to long-term deposits and net increases in other investments.

Property, Plant and Equipment

Net property, plant and equipment increased $20.8 million to $1.042 billion at December 31, 2015 due primarily to capital expenditures of $234.3 million partially offset by depreciation expense of $170.3 million, sale or disposition of assets with remaining net book value of $10.5 million and currency translation adjustments of $32.6 million. Capital expenditures during 2015 in the Paint Stores Group were primarily attributable to the opening of new paint stores, renovation and conversion of acquired stores and improvements in existing stores. In the Consumer Group, capital expenditures during 2015 were primarily attributable to improvements and normal equipment replacements in manufacturing and distribution facilities. Capital expenditures in the Global Finishes Group were primarily attributable to improvements in existing manufacturing and distribution facilities. The Administrative Segment incurred capital expenditures primarily for information systems hardware. In 2016, the Company expects to spend more than 2015 for capital expenditures. The predominant share of the capital expenditures in 2016 is expected to be for various productivity improvement and maintenance projects at existing manufacturing, distribution and research and development facilities, new store openings and new or upgraded information systems hardware. The Company does not anticipate the need for any specific long-term external financing to support these capital expenditures.

Debt

There were no borrowings outstanding under the domestic commercial paper program at December 31, 2015 and 2013, respectively. There were $625.9 million in borrowings outstanding under this program at December 31, 2014 with a weighted-average interest rate of 0.3 percent. Borrowings outstanding

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

under various foreign programs at December 31, 2015 were $39.5 million with a weighted-average interest rate of 7.0 percent. At December 31, 2014 and December 31, 2013, foreign borrowings were $53.6 million and $96.6 million with weighted-average interest rates of 6.0 percent and 7.8 percent, respectively. Long-term debt, including the current portion, increased $797.4 million during 2015 resulting primarily from long-term debt issued in 2015. On July 28, 2015, the Company issued $400.0 million of 3.45% Senior Notes due 2025 and $400.0 million of 4.55% Senior Notes due 2045. The notes are covered under a shelf registration filed with the Securities and Exchange Commission on July 28, 2015. The proceeds will be used for general corporate purposes, including repayment of a portion of the Company’s outstanding short-term borrowings.

On July 16, 2015, the Company and three of its wholly-owned subsidiaries, Sherwin-Williams Canada, Inc. (SW Canada), Sherwin-Williams Luxembourg S.à r.l. (SW Lux) and Sherwin-Williams UK Holding Limited, entered into a new five-year $1.350 billion credit agreement. The credit agreement is being used for general corporate purposes, including the financing of working capital requirements. The credit agreement replaced the previous credit agreements for each of the Company, SW Canada and SW Lux, dated July 8, 2011, June 29, 2012 and September 19, 2012, as amended, respectively. The credit agreement allows the Company to extend the maturity of the facility with two one-year extension options and to increase the aggregate amount of the facility to $1.850 billion, both of which are subject to the discretion of each lender. At December 31, 2015, there was $21.7 million of borrowings outstanding under this credit agreement.

On July 8, 2011, the Company entered into a five-year $1.050 billion revolving credit agreement, which replaced the existing three-year $500.0 million credit agreement. The credit agreement allows the Company to extend the maturity of the facility with two one-year extension options and to increase the aggregate amount of the facility to $1.300 billion, both of which are subject to the discretion of each lender.

See Note 7, on page 60 of this report, for a detailed description of the Company’s debt outstanding and other available financing programs.

Defined Benefit Pension and Other Postretirement Benefit Plans

In accordance with the accounting prescribed by the Retirement Benefits Topic of the ASC, the Company’s total liability for unfunded or underfunded defined benefit pension plans decreased $3.6 million to $50.6 million primarily due to changes in the actuarial assumptions of the Company's foreign plans. Postretirement benefits other than pensions decreased

$31.8 million to $263.4 million at December 31, 2015 due primarily to changes in the actuarial assumptions.

Effective July 1, 2009, the domestic salaried defined benefit pension plan was revised. Prior to July 1, 2009, the contribution was based on six percent of compensation for covered employees. Under the revised plan, such participants are credited with certain contribution credits that range from two percent to seven percent of compensation based on an age and service formula. Amounts previously recorded in Cumulative other comprehensive loss in accordance with the provisions of the Retirement Benefits Topic of the ASC were modified in 2009 resulting in a decrease in comprehensive loss due primarily to the change in the domestic salaried defined benefit pension plan and an increase in the excess plan assets over the actuarially calculated projected benefit obligation in the domestic defined benefit pension plans. Partially offsetting this decreased loss were modifications to actuarial assumptions used to calculate projected benefit obligations.

Effective October 1, 2011, the domestic salaried defined benefit pension plan was frozen for new hires, and all newly hired U.S. non-collectively bargained employees are eligible to participate in the Company’s domestic defined contribution plan.

The assumed discount rate used to determine the actuarial present value of projected defined benefit pension and other postretirement benefit obligations for domestic plans was increased from 3.95 percent to 4.40 percent at December 31, 2015 due to increased rates of high-quality, long-term investments and foreign defined benefit pension plans had similar discount rate increases for the same reasons. The rate of compensation increases used to determine the projected benefit obligations decreased to 3.1 percent in 2015 from 4.0 percent for domestic pension plans and was slightly higher on most foreign plans. In deciding on the rate of compensation increases, management considered historical Company increases as well as expectations for future increases. The expected long-term rate of return on assets remained at 6.0 percent for 2015 for domestic pension plans and was slightly lower for most foreign plans. In establishing the expected long-term rate of return on plan assets for 2015, management considered the historical rates of return, the nature of investments and an expectation for future investment strategies. The assumed health care cost trend rates used to determine the net periodic benefit cost of postretirement benefits other than pensions for 2015 were 6.5 percent for medical and prescription drug cost increases, both decreasing gradually to 4.5 percent in 2024. The assumed health care cost trend rates used to determine the benefit obligation at December 31, 2015 were between 11.5 percent and 5.0 percent for medical and prescription drug cost increases. In developing the

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

assumed health care cost trend rates, management considered industry data, historical Company experience and expectations for future health care costs.

For 2016 Net pension cost and Net periodic benefit cost recognition for domestic plans, the Company will use a discount rate of 4.40 percent, an expected long-term rate of return on assets of 6.0 percent, a rate of compensation increase of 3.1 percent and cost trend rates between 5.0 percent and 11.5 percent for health care and prescription drug cost increases. Slightly lower discount rates, rates of compensation increases and expected long-term rates of return on plan assets will be used for most foreign plans. Use of these assumptions and amortization of actuarial gains will result in a domestic Net pension cost in 2016 that is expected to be approximately $7.2 million higher than in 2015 and a Net periodic benefit cost for postretirement benefits other than pensions that is expected to decrease $3.5 million in 2016 compared to 2015. See Note 6, on pages 54 through 59 of this report, for more information on the Company’s obligations and funded status of its defined benefit pension plans and postretirement benefits other than pensions.

Other Long-Term Liabilities

Other long-term liabilities decreased $14.9 million during 2015 due primarily to a decrease in long-term commitments related to the affordable housing and historic renovation real estate properties of $30.1 million, a decrease in non-current deferred tax liabilities of $5.7 million, and a decrease in long-term pension liabilities of $4.3 million partially offset by an increase in accruals for extended environmental-related liabilities of $15.6 million.

Environmental-Related Liabilities

The operations of the Company, like those of other companies in the same industry, are subject to various federal, state and local environmental laws and regulations. These laws and regulations not only govern current operations and products, but also impose potential liability on the Company for past operations. Management expects environmental laws and regulations to impose increasingly stringent requirements upon the Company and the industry in the future. Management believes that the Company conducts its operations in compliance with applicable environmental laws and regulations and has implemented various programs designed to protect the environment and promote continued compliance.

Depreciation of capital expenditures and other expenses related to ongoing environmental compliance measures were included in the normal operating expenses of conducting business. The Company’s capital expenditures, depreciation and other expenses related to ongoing environmental compliance measures were not material to the Company’s financial condition, liquidity, cash flow or results of operations during 2015. Management does not expect that such capital expenditures, depreciation and other expenses will be material to the Company’s financial condition, liquidity, cash flow or results of operations in 2016. See Note 8, on pages 60 through 62 of this report, for further information on environmental-related long-term liabilities.

Contractual Obligations and Commercial Commitments

The Company has certain obligations and commitments to make future payments under contractual obligations and commercial commitments. The following table summarizes such obligations and commitments as of December 31, 2015:

|

| | | | | | | | | | | | | | | | | | | | |

| (thousands of dollars) | | Payments Due by Period |

| Contractual Obligations | | Total | | Less than 1 Year | | 1–3 Years | | 3–5 Years | | More than 5 Years |

| Long-term debt | | $ | 1,927,688 |

| | $ | 3,154 |

| | $ | 700,818 |

| | $ | 315 |

| | $ | 1,223,401 |

|

| Operating leases | | 1,420,549 |

| | 317,843 |

| | 501,728 |

| | 318,078 |

| | 282,900 |

|

| Short-term borrowings | | 39,462 |

| | 39,462 |

| | | | | | |

| Interest on Long-term debt | | 1,147,842 |

| | 62,828 |

| | 115,652 |

| | 106,160 |

| | 863,202 |

|

Purchase obligations (a) | | 52,052 |

| | 52,052 |

| | | | | | |

Other contractual obligations (b) | | 212,965 |

| | 93,572 |

| | 52,072 |

| | 44,956 |

| | 22,365 |

|

| Total contractual cash obligations | | $ | 4,800,558 |

| | $ | 568,911 |

| | $ | 1,370,270 |

| | $ | 469,509 |

| | $ | 2,391,868 |

|

| |

(a) | Relate to open purchase orders for raw materials at December 31, 2015. |

| |

(b) | Relate primarily to estimated future capital contributions to investments in the U.S. affordable housing and historic renovation real estate partnerships and various other contractual obligations. |

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

|

| | | | | | | | | | | | | | | | | | | | |

| | | Amount of Commitment Expiration Per Period |

| Commercial Commitments | | Total | | Less than 1 Year | | 1–3 Years | | 3–5 Years | | More than 5 Years |

| Standby letters of credit | | $ | 45,407 |

| | $ | 45,407 |

| | | | | | |

| Surety bonds | | 64,470 |

| | 64,470 |

| | | | | | |

| Other commercial commitments | | 17,747 |

| | 17,747 |

| | | | | | |

| Total commercial commitments | | $ | 127,624 |

| | $ | 127,624 |

| | $ | — |

| | $ | — |

| | $ | — |

|

Warranties

The Company offers product warranties for certain products. The specific terms and conditions of such warranties vary depending on the product or customer contract requirements. Management estimated the costs of unsettled product warranty claims based on historical results and experience. Management periodically assesses the adequacy of the accrual for product warranty claims and adjusts the accrual as necessary. Changes in the Company’s accrual for product warranty claims during 2015, 2014 and 2013, including customer satisfaction settlements during the year, were as follows:

|

| | | | | | | | | | | |

| (thousands of dollars) | 2015 | | 2014 | | 2013 |

| Balance at January 1 | $ | 27,723 |

| | $ | 26,755 |

| | $ | 22,710 |

|

| Charges to expense | 43,484 |

| | 37,879 |

| | 33,265 |

|

| Settlements | (39,329 | ) | | (36,911 | ) | | (29,220 | ) |

| Balance at December 31 | $ | 31,878 |

| | $ | 27,723 |

| | $ | 26,755 |

|

Shareholders’ Equity

Shareholders’ equity decreased $128.6 million to $867.9 million at December 31, 2015 from $996.5 million last year. The decrease in Shareholders’ equity resulted primarily from the purchase of treasury stock for $1.035 billion, treasury stock received from stock option exercises of $34.4 million and an increase in Cumulative other comprehensive loss of $115.1 million partially offset by an increase in retained earnings of $804.2 million and an increase in Other capital of $250.8 million, due primarily to stock options exercised. The Company purchased 3.58 million shares of its common stock during 2015 for treasury. The Company acquires its common stock for general corporate purposes and, depending on its cash position and market conditions, it may acquire additional shares in the future. On October 21, 2015, the Board of Directors of the Company authorized the Company to purchase an additional 10.0 million shares of its common stock. The Company had remaining authorization from its Board of Directors at December 31, 2015 to purchase 11.65 million shares of its common stock. The increase of $115.1 million in Cumulative other comprehensive loss was due primarily to unfavorable foreign currency translation effects of $128.2 million attributable to the weakening of most foreign

operations’ functional currencies against the U.S. dollar partially offset by $13.8 million in net actuarial gains and prior service costs of defined benefit pension and other postretirement benefit plans net of amortization.

The increase in Other capital of $250.8 million was due primarily to the recognition of stock-based compensation expense, stock option exercises and related income tax effect. Retained earnings increased $804.2 million during 2015 due to net income of $1.054 billion partially offset by $249.6 million in cash dividends paid. The Company’s cash dividend per common share payout target is 30.0 percent of the prior year’s diluted net income per common share. The 2015 annual cash dividend of $2.68 per common share represented 30.5 percent of 2014 diluted net income per common share. The 2015 annual dividend represented the thirty-sixth consecutive year of dividend payments since the dividend was suspended in 1978. At a meeting held on February 17, 2016, the Board of Directors increased the quarterly cash dividend to $.84 per common share. This quarterly dividend, if approved in each of the remaining quarters of 2016, would result in an annual dividend for 2016 of $3.36 per common share or a 30.1 percent payout of 2015 diluted net income per common share. See the Statements of Consolidated Shareholders’ Equity, on page 45 of this report, and Notes 10, 11 and 12, on pages 65 through 68 of this report, for more information concerning Shareholders’ equity.

Cash Flow

Net operating cash increased $365.9 million to $1.447 billion in 2015 from $1.082 billion in 2014 due primarily to an increase in net income of $188.0 million and a reduction in working capital of $188.9 million due to timing of payments. Strong Net operating cash provided the funds necessary to invest in new stores, manufacturing and distribution facilities, renovate and convert acquired stores, pay down debt and return cash to shareholders through dividends and treasury stock purchases. Net investing cash improved $21.4 million to a usage of $288.6 million in 2015 from a usage of $310.1 million in 2014 due primarily due to reduced cash used for other investments of $45.4 million partially offset by increased capital expenditures of $33.8 million. Net financing cash improved $486.7 million to a usage of $980.4 million in 2015 from a usage of $1.467 billion in 2014 due primarily

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

to increased net proceeds of long-term debt of $1.297 billion, decreased treasury stock purchases of $453.4 million partially offset by net decreases in short-term borrowings of $1.222 billion and increased payments of cash dividends of $34.4 million. In 2015, the Company used Net operating cash and Cash and cash equivalents on hand to purchase $1.035 billion in treasury stock, spend $234.3 million in capital additions and improvements and pay $249.6 million in cash dividends to its shareholders of common stock.

Management considers a measurement of cash flow that is not in accordance with U.S. generally accepted accounting principles to be a useful tool in its determination of appropriate uses of the Company’s Net operating cash. Management reduces Net operating cash, as shown in the Statements of Consolidated Cash Flows, by the amount reinvested in the business for Capital expenditures and the return of investment to its shareholders by the payments of cash dividends. The resulting value is referred to by management as “Free Cash Flow” which may not be comparable to values considered by other entities using the same terminology. The reader is cautioned that the Free Cash Flow measure should not be compared to other entities unknowingly, and it does not consider certain non-discretionary cash flows, such as mandatory debt and interest payments. The amount shown below should not be considered an alternative to Net operating cash or other cash flow amounts provided in accordance with U.S. generally accepted accounting principles disclosed in the Statements of Consolidated Cash Flows, on page 44 of this report. Free Cash Flow as defined and used by management is determined as follows:

|

| | | | | | | | | | | |

| | Year Ended December 31, |

| (thousands of dollars) | 2015 | | 2014 | | 2013 |

| Net operating cash | $ | 1,447,463 |

| | $ | 1,081,528 |

| | $ | 1,083,766 |

|

| Capital expenditures | (234,340 | ) | | (200,545 | ) | | (166,680 | ) |

| Cash dividends | (249,647 | ) | | (215,263 | ) | | (204,978 | ) |

| Free cash flow | $ | 963,476 |

| | $ | 665,720 |

| | $ | 712,108 |

|

Litigation

DOL leveraged ESOP settlement. On February 20, 2013, the Company reached a settlement with the DOL of the DOL's investigation of transactions related to the Company's ESOP that were implemented on August 1, 2006 and August 27, 2003. The DOL had notified the Company, among others, of potential enforcement claims asserting breaches of fiduciary obligations and sought compensatory and equitable remedies. The Company resolved all ESOP related claims with the DOL by agreeing, in part, to make a one-time payment of $80.0 million to the ESOP,

resulting in a $49.2 million after tax charge to earnings in the fourth quarter of 2012. The Company made this required $80.0 million payment to the ESOP during the first quarter of 2013.

Government tax assessment settlements related to Brazilian operations. Charges totaling $28.7 million and $2.9 million were recorded to Cost of goods sold and SG&A, respectively, during the second and third quarters of 2013. The

charges were primarily related to import duty taxes paid to the Brazilian government related to the handling of import duties on products brought into the country for the years 2006 through 2012. The Company elected to pay the taxes through an existing voluntary amnesty program offered by the government to resolve these issues rather than contest them in court. The after-tax charges were $21.9 million for the full year 2013. The Company's import duty process in Brazil was changed to reach a final resolution of this matter with the Brazilian government.

Titanium dioxide suppliers antitrust class action lawsuit. The Company is a member of the plaintiff class related to Titanium Dioxide Antitrust Litigation that was initiated in 2010 against certain suppliers alleging various theories of relief arising from purchases of titanium dioxide made from 2003 through 2012. The Court approved a settlement less attorney fees and expense, and the Company timely submitted claims to recover its pro-rata portion of the settlement. There was no specified deadline for the claims administrator to complete the review of all claims submitted. In October 2014, the Company was notified that it would receive a disbursement of settlement funds, and the Company received a pro-rata disbursement net of all fees of approximately $21.4 million. The Company recorded this settlement gain in the fourth quarter of 2014.

See page 25 of this report and Note 9 on pages 62 through 65 for more information concerning litigation.

Market Risk

The Company is exposed to market risk associated with interest rate, foreign currency and commodity fluctuations. The Company occasionally utilizes derivative instruments as part of its overall financial risk management policy, but does not use derivative instruments for speculative or trading purposes. The Company entered into foreign currency option and forward currency exchange contracts with maturity dates of less than twelve months in 2015, 2014 and 2013, primarily to hedge against value changes in foreign currency. There were no material derivative contracts outstanding at December 31, 2015, 2014 and 2013. The Company believes it may be exposed to continuing market risk from foreign currency exchange rate and commodity price fluctuations. However, the Company does not expect that foreign currency exchange rate and commodity price fluctuations or hedging contract losses will have a material adverse effect on

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

the Company’s financial condition, results of operations or cash flows. See Notes 1 and 13 on pages 47 and 69 of this report.

Financial Covenant

Certain borrowings contain a consolidated leverage covenant. The covenant states the Company’s leverage ratio is not to exceed 3.50 to 1.00. The leverage ratio is defined as the ratio of total indebtedness (the sum of Short-term borrowings, Current portion of long-term debt and Long-term debt) at the reporting date to consolidated “Earnings Before Interest, Taxes, Depreciation and Amortization” (EBITDA) for the 12-month period ended on the same date. Refer to the “Results of Operations” caption below for a reconciliation of EBITDA to Net income. At December 31, 2015, the Company was in compliance with the covenant. The Company’s Notes, Debentures and revolving credit agreement contain various default and cross-default provisions. In the event of default under any one of these arrangements, acceleration of

the maturity of any one or more of these borrowings may result. See Note 7 on page 60 of this report.

Employee Stock Ownership Plan (ESOP)

Participants in the Company’s ESOP are allowed to contribute up to the lesser of twenty percent of their annual compensation or the maximum dollar amount allowed under the Internal Revenue Code. The Company matches six percent of eligible employee contributions. The Company’s matching contributions to the ESOP charged to operations were $80.4 million in 2015 compared to $74.6 million in 2014. At December 31, 2015, there were 11,333,455 shares of the Company’s common stock being held by the ESOP, representing 12.3 percent of the total number of voting shares outstanding. See Note 11, on pages 66 and 67 of this report, for more information concerning the Company’s ESOP and preferred stock.

|

| |

| | MANAGEMENT’S DISCUSSION AND ANALYSIS OF |

| | FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

RESULTS OF OPERATIONS - 2015 vs. 2014

Shown below are net sales and segment profit and the percentage change for the current period by segment for 2015 and 2014:

|

| | | | | | | | | | |

| | Year Ended December 31, |

| (thousands of dollars) | 2015 | | 2014 | | Change |

| Net Sales: | | | | | |

| Paint Stores Group | $ | 7,208,951 |

| | $ | 6,851,581 |

| | 5.2 | % |

| Consumer Group | 1,577,955 |

| | 1,420,757 |

| | 11.1 | % |

| Global Finishes Group | 1,916,300 |

| | 2,080,854 |

| | -7.9 | % |

| Latin America Coatings Group | 631,015 |

| | 771,378 |

| | -18.2 | % |

| Administrative | 5,083 |

| | 4,963 |

| | 2.4 | % |

| Net sales | $ | 11,339,304 |

| | $ | 11,129,533 |

| | 1.9 | % |

| | | | | | |

| | Year Ended December 31, |

| (thousands of dollars) | 2015 | | 2014 | | Change |

| Income Before Income Taxes: | | | | | |

| Paint Stores Group | $ | 1,433,504 |

| | $ | 1,201,420 |

| | 19.3 | % |

| Consumer Group | 308,833 |

| | 252,859 |

| | 22.1 | % |

| Global Finishes Group | 201,881 |

| | 201,129 |

| | 0.4 | % |

| Latin America Coatings Group | 18,494 |

| | 40,469 |

| | -54.3 | % |

| Administrative | (413,746 | ) | | (437,651 | ) | | 5.5 | % |

Income before income taxes | $ | 1,548,966 |

| | $ | 1,258,226 |

| | 23.1 | % |

Consolidated net sales for 2015 increased due primarily to higher paint sales volume in the Paint Stores and Consumer Groups. Unfavorable currency translation rate changes decreased 2015 consolidated net sales 3.3 percent. Net sales of all consolidated foreign subsidiaries were down 18.8 percent to $1.789 billion for 2015 versus $2.204 billion for 2014 due primarily to unfavorable foreign currency translation rates. Net sales of all operations other than consolidated foreign subsidiaries were up 7.0 percent to $9.550 billion for 2015 versus $8.926 billion for 2014.

Net sales in the Paint Stores Group in 2015 increased primarily due to higher architectural paint sales volume across all end market segments. Net sales from stores open for more than twelve calendar months increased 4.2 percent for the full year. During 2015, the Paint Stores Group opened 113 new stores and closed 30 redundant locations for a net increase of 83 stores, increasing the total number of stores in operation at December 31, 2015 to 4,086 in the United States, Canada and the Caribbean. The Paint Stores Group’s objective is to expand its

store base an average of two and a half percent each year, primarily through internal growth. Sales of products other than paint increased approximately 8.0 percent for the year over 2014. A discussion of changes in volume versus pricing for sales of products other than paint is not pertinent due to the wide assortment of general merchandise sold.

Net sales of the Consumer Group increased due primarily to a new agreement to sell architectural paint under the HGTV HOME® by Sherwin-Williams brand through a large U.S. national retailer's stores network. Sales of wood care coatings, brushes, rollers, caulk and other paint related products, were all up at least mid to high-single digits as compared to 2014 while sales of aerosol products were down slightly. A discussion of changes in volume versus pricing for sales of products other than paint is not pertinent due to the wide assortment of paint-related merchandise sold. The Consumer Group plans to continue its promotions of new and existing products in 2016 and continue expanding its customer base and product assortment at existing customers.

The Global Finishes Group’s net sales in 2015, when stated in U.S. dollars, decreased due primarily to unfavorable currency translation rate changes. Paint sales volume percentage increased slightly as compared to 2014. Unfavorable currency translation rate changes in the year decreased net sales by 7.5 percent for 2015. In 2015, the Global Finishes Group opened 3 new branches and closed 7 locations decreasing the total from 300 to 296 branches open in the United States, Canada, Mexico, South America, Europe and Asia at year-end. In 2016, the Global Finishes Group expects to continue expanding its worldwide presence and improving its customer base.

The Latin America Coatings Group’s net sales in 2015, when stated in U.S. dollars, decreased due primarily to unfavorable currency translation rate changes and lower paint sales volume partially offset by selling price increases. Paint sales volume percentage decreased in the mid-single digits as compared to 2014. Unfavorable currency translation rate changes in the year decreased net sales by 19.3 percent for 2015. In 2015, the Latin America Coatings Group opened 17 new stores and closed 2 locations for a net increase of 15 stores, increasing the total to 291 stores open in North and South America at year-end. In 2016, the Latin America Coatings Group expects to continue expanding its regional presence and improving its customer base.

Net sales in the Administrative segment, which primarily consist of external leasing revenue of excess headquarters space and leasing of facilities no longer used by the Company in its primary business, increased by an insignificant amount in 2015.

Consolidated gross profit increased $394.7 million in 2015 and improved as a percent to net sales to 49.0 percent from

|

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF | |

| FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

46.4 percent in 2014 due primarily to higher paint sales volume, improved operating efficiencies, and decreasing raw material costs partially offset by unfavorable currency translation rate changes. Gross profit for 2014 included the 2014 TiO2 settlement of $21.4 million received by the Company in the fourth quarter of 2014. The Paint Stores Group’s gross profit for 2015 increased $329.3 million compared to 2014 due primarily to higher paint sales volume. The Paint Stores Group's gross profit margins increased for that same reason. The Consumer Group’s gross profit increased $133.6 million due primarily to improved operating efficiency and increased paint sales volume. The Consumer Group’s gross profit margins increased for those same reasons. The Global Finishes Group’s gross profit for 2015 decreased $29.0 million due primarily unfavorable currency translation rate changes partially offset by improved operating efficiencies and decreasing raw material costs. The Global Finishes Group’s gross profit increased as a percent of sales due primarily to improved operating efficiencies and decreasing raw material costs. Foreign currency translation rate fluctuations decreased Global Finishes Group’s gross profit by $51.4 million for 2015. The Latin America Coatings Group’s gross profit for 2015 decreased $43.9 million and decreased as a percent of sales, when stated in U.S. dollars, primarily due to unfavorable currency translation rate changes and increasing raw material costs. Unfavorable currency translation rate changes and lower volume sales were only partially offset by selling price increases in 2015 compared to 2014. Foreign currency translation rate fluctuations decreased gross profit by $41.5 million for 2015. The Administrative segment’s gross profit increased by $4.8 million.

SG&A increased by $90.6 million due primarily to increased expenses to support higher sales levels and net new store openings as well as the impact from a new paint program launch at a national retailer. SG&A increased as a percent of sales to 34.5 percent in 2015 from 34.3 percent in 2014 primarily due to those same reasons. In the Paint Stores Group, SG&A increased $95.4 million for the year due primarily to increased spending due to the number of new store openings and general comparable store expenses to support higher sales levels. The Consumer Group’s SG&A increased by $79.7 million for the year due to a new paint program launch at a national retailer. The Global Finishes Group’s SG&A decreased by $37.4 million for the year relating primarily to foreign currency translation rate fluctuations reducing SG&A by $44.2 million. The Latin America Coatings Group’s SG&A decreased by $22.0 million for the year relating primarily to foreign currency translation rate fluctuations of $27.9 million. The Administrative segment’s SG&A decreased $25.2 million primarily due to incentive compensation.

Other general expense - net decreased $7.2 million in 2015 compared to 2014. The decrease was mainly caused by a decrease of $6.1 million of expense in the Administrative segment, primarily due to a year-over-year decrease in provisions for environmental matters of $5.0 million. See Note 13, on pages 68 and 69 of this report, for more information concerning Other general expense - net.