In fact, RGA is the second largest North American life reinsurer, number one in terms of new business written. An important part of our business is facultative. We're the industry leaders in facultative business. These are the difficult cases to underwrite. They're high value-added services provided to the life insurance industry. There are no official statistics, but we feel very confident in claiming we're the largest, because nobody's really even that close to us.

We view that RGA has lots of opportunities. We've been growing at double-digit rates. We have a track record over a long period of time that generates consistent earnings throughout. Quarter-to-quarter you see volatility from mortality experience: who dies in the given quarter. But the track record is strong over time.

Our separation from MetLife will be a net benefit to RGA. We think that independence from MetLife will enhance the ability of RGA stock to take its own course. And we also have a leading management team in the industry.

[Slide 9] You can see the rankings in North America and worldwide. On a couple of different bases in North America, what we collect is life reinsurance and inforce in volume. So, you can see we have about $1.4 trillion of life reinsurance inforce, second to Swiss Re. On a worldwide basis, what you see is premiums and RGA is the third largest, with about $4.7 billion of gross life premium.

[Slide 10] If you take a look at our position in the marketplace that we serve, in North America, as I said, we've been the leading life reinsurer in new business in both the U.S. and Canada last year and the leader in the U.S. in the last couple of years. We are the largest facultative reinsurer by a fair margin.

This is a mature market. Its growth has subsided a bit. We're talking about high single digit growth, sort of like 7% to 8% at this point. And again, this is a market that we have operated in for a long time and the business on our books has generated consistent profit over that period of time.

Profits that we experienced in 2008 come from business written in all prior years. So, all of the past record is relevant here.

The most rapidly growing part of the world for life reinsurance as a growth industry is Asia. And in Asian markets we're the region-wide leader in new business, with about a 26% market share. That's according to NMG surveys that were done. We're the second largest reinsurer of new group business to Swiss Re and we're the market leader in terms of the number of new treaties entered into.

In Europe, we are probably a little bit underrepresented at this point. It provides opportunities for us to expand into Continental Europe in particular. We have established operations in the UK and Spain and everywhere else is fairly early on at this state. With all of the regulatory changes in Europe, there are a lot of opportunities in that market as well.

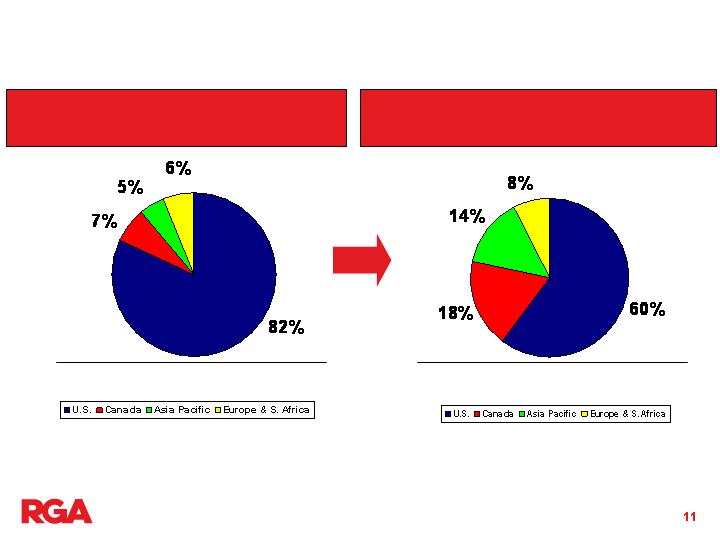

[Slide 11] You can see in this pie chart the breakdown of our business by geography and how it has evolved over time. The U.S. share of the pie is decreasing as a result of the growth in Asia and Europe.

[Slide 12] We mentioned our facultative business as an important feature. We have been recognized as the leader in this field for some time. We review over 100,000 facultative applications a year, averaging over $1 million per policy. We place a sizeable proportion of these cases. In this part of the market the victories are one case at a time, so there are significant barriers to entry. It is difficult for other reinsurers to encroach upon our position here.

But in addition, it also provides a lot of extra leverage for us in the regular automatic business. In much of the regular automatic life reinsurance business we are able to leverage our facultative position into better shares or better prices.

[Slide 13] There are a lot of growth opportunities left in the life reinsurance business. In North America we are talking, as I said, about high single digit growth, sort of 8% growth. There are not a lot of new entrants into our business. The ones that have entered have not been very effective in making an impact. We also see a changeover into increasing amounts of annuities and

other types of products being written and reinsured. In addition, the stresses in the macro environment are creating a lot of opportunities for reinsurers, who provide a fast, flexible source of capital to companies as well in the life insurance space.

Internationally, Asia, as I said, is a place where life insurance is a growth industry and we're growing along with that. In many of these markets you're talking about high teens in terms of growth rates on an annual recurring basis.

Most of these markets, in particular some of the more developed ones like Japan and Korea, have very low penetration rates. And these have been our largest growth stories for the last several years, because we're not only seeing sizeable opportunities, but we're penetrating the market farther. And companies are reinsuring more than they have in the past.

Other markets, like China and India, are for really the intermediate future. It's not something that's going to make an impact in the near term.

[Slide 14] Here's a chart that shows the growth rate of the life reinsurance inforce in the United States and Canada. You can see in the United States it's slowed down considerably. In the last couple of years, it's been quite level. In fact, new business cession rates have been decreasing somewhat. But remember, our profits come from all the inforce in place and not just from new business. And so, it's really the inforce growth that's important here.

Canada's been growing a little bit faster, continued on high penetration rates and a lot of reasons structurally for companies in Canada to reinsure. Some of

those may change and you might see this fall back more towards the United States level.

[Slide 15] We went public in 1993 and you can see some selected compound growth rate numbers for RGA parameters here. All of them have increased substantially on a compound basis.

[Slide 16] We expect that the independence from MetLife will have a positive effect for RGA stock in particular. We will increase the float available in the marketplace and eliminate the overhang that's always been present when MetLife has owned more than 50% of the stock. They've been generally very good owners for RGA, but we are looking forward to independence and separation in this transaction.

[Slide 17] In the life reinsurance business the scarcest resource tends to be the people and the quality of experience that is warehoused within an organization and RGA has a lot of people that not only have deep experience, but long experience with RGA as well.

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

ROE** was 14% last year. That's ex AOCI. Book value per share** growth has been 14% over the last five years or so.

And in terms of goals, we articulate an operating EPS* growth rate target of 14%. We're still comfortable with that number. And an ROE** percentage so to speak of 14%. That's our expectation over the intermediate term, which we typically define as the next two- to three-year period.

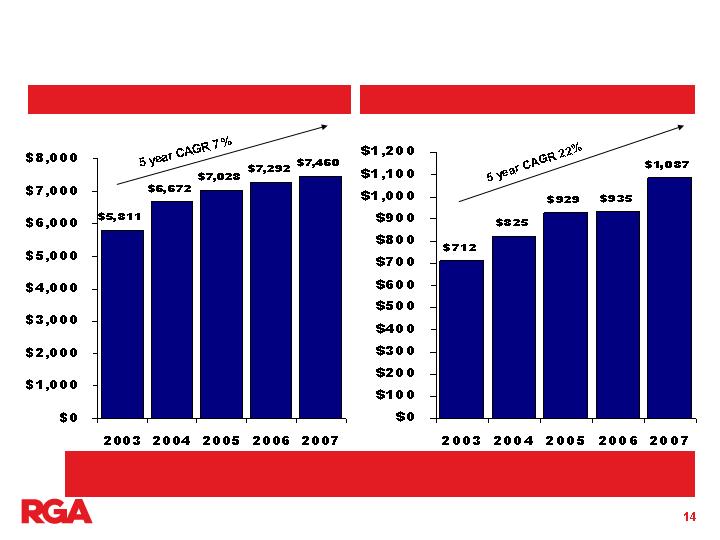

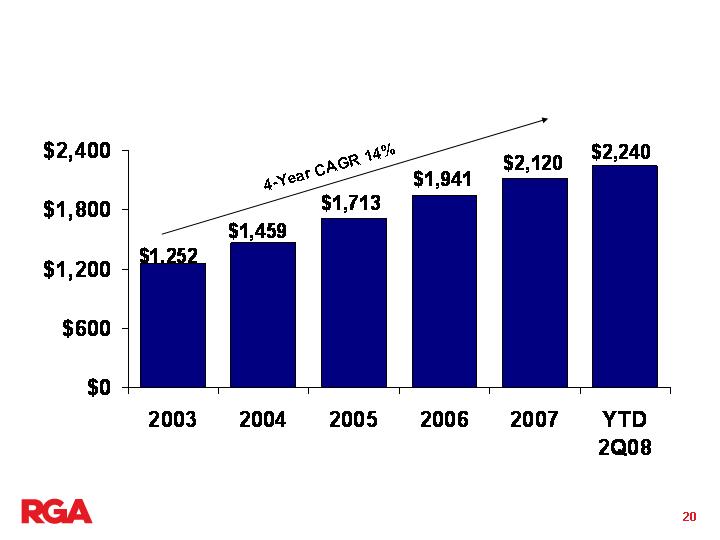

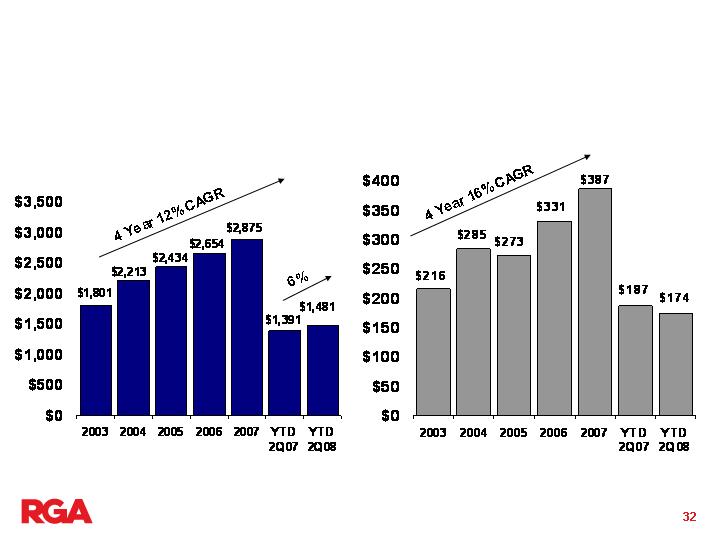

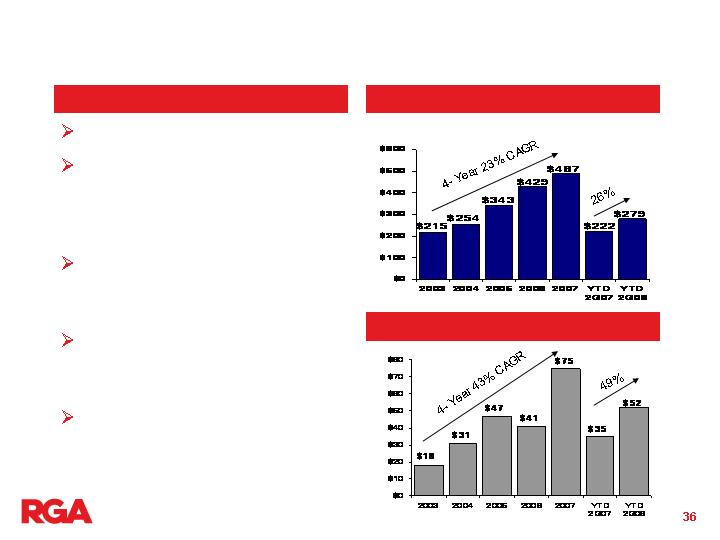

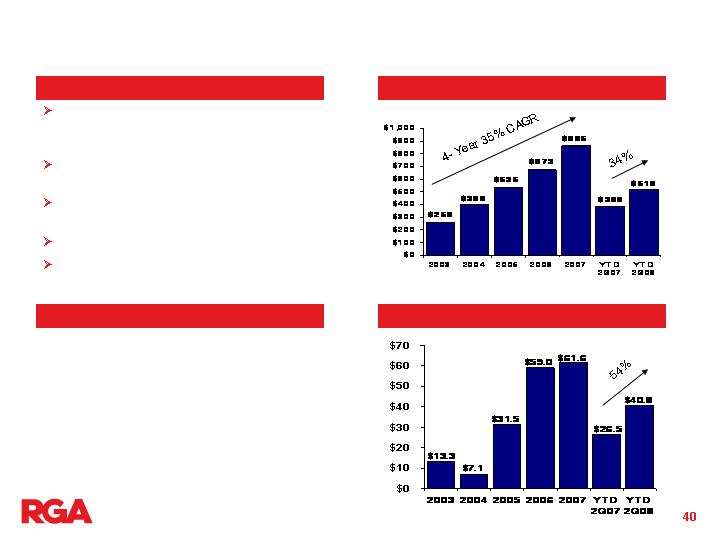

[Slide 20] Our next slide represents life reinsurance inforce. And you can see a 14% growth rate over that period of time. This is not a perfect metric in terms of determining the business vitality, but it's one of several that we monitor. And as you can see, we're over $2 trillion, $2.2 trillion at the end of the second quarter of 2008.

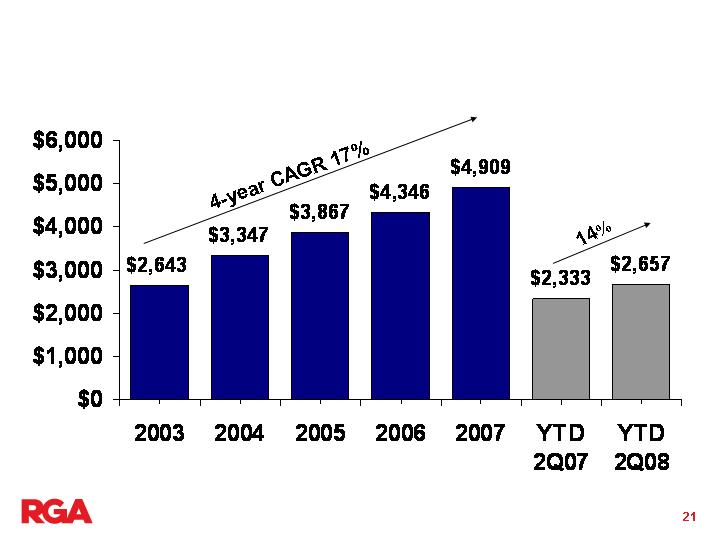

[Slide 21] Our premium growth rate, you see here a compound annual growth rate of 17% over the last four years. You can see about 14% growth rate, 2Q, year-to-date, 2Q '08 versus '07. We expect that to be in the 12 to 14% range for the year. So, that's obviously a little bit towards the high end of that range currently. That's an enterprise-wide growth rate.

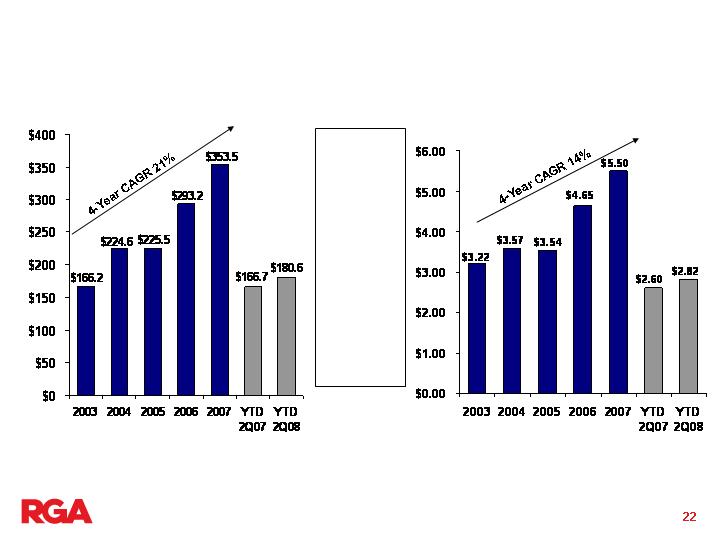

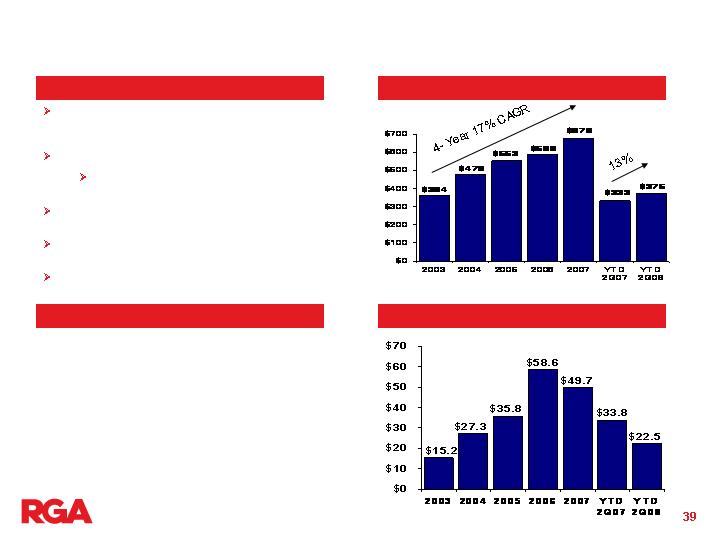

[Slide 22] We reflect consolidated operating income* on this slide. You can see gross dollars on the left and on the right operating income per share.* Also on the right, you see in terms of per share a four-year growth rate of 14%. I commented on our expectations in terms of the intermediate term.

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

**Excludes accumulated other comprehensive income. See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

You see we're at $2.82 for the first six months versus $2.60 for the first six months of last year. We had a difficult first quarter in terms of mortality. We expect to have some mortality fluctuations and we did sustain that in the first quarter this year. Mortality was back on track in the second quarter. So, we're still at a point where, in terms of the guidance for the year, it remains to be seen. We have to follow on with a couple more strong quarters, but may still be in that guidance range that we articulated in January, which was $6.00 to $6.50 per share.

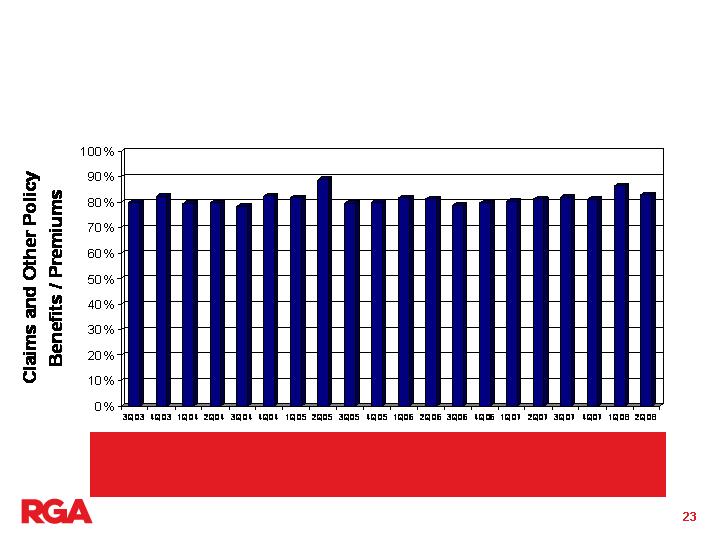

[Slide 23] This page reflects, over a five-year period, quarterly mortality volatility. And the takeaway here is even when we have difficult quarters—and I described one earlier—we're not like a P&C reinsurer, even a P&C primary company, where it can wipe out earnings if you do have a difficult quarter in terms of mortality expectations. It's merely a blip for us. And you can see relative, fairly consistent pattern here, that we don't have a lot of volatility, either up or down, as you can see.

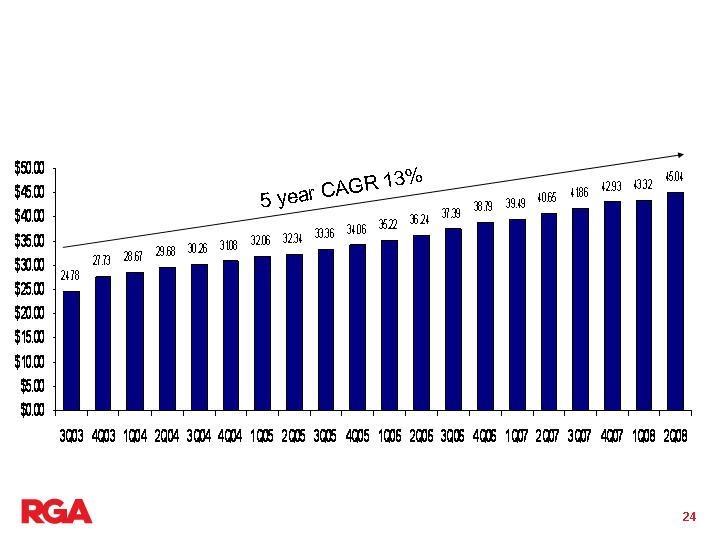

[Slide 24] Book value per share***, you see an upward trend there. Five-year compound annual growth rate of 13% or $45.00, ex AOCI at June 30th of 2008. And, as you can see from the slide, we add about a dollar or so per share each quarter, if we have a representative quarter.

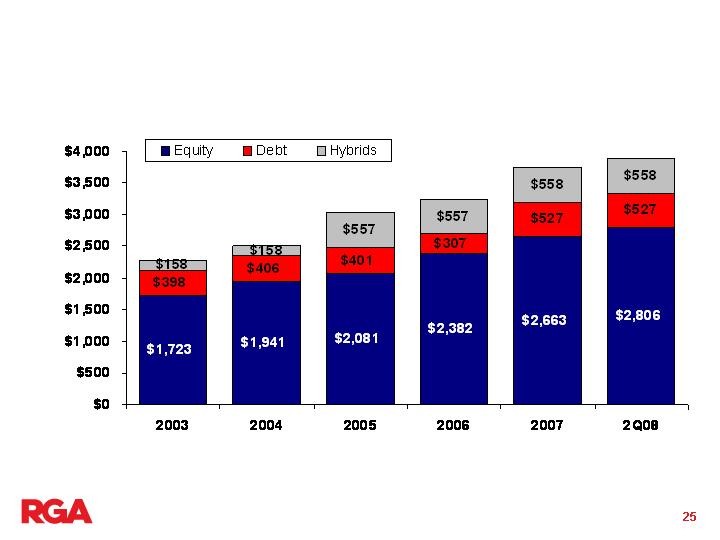

[Slide 25] In terms of our capitalization, you can see equity versus debt and hybrids here. We feel we have a little bit of leveragability with respect to the rating agencies currently, several hundred million. Not a whole lot, but at

*** Book value excludes other comprehensive income. See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

least some flexibility with respect to leverage associated with the current capitalization levels.

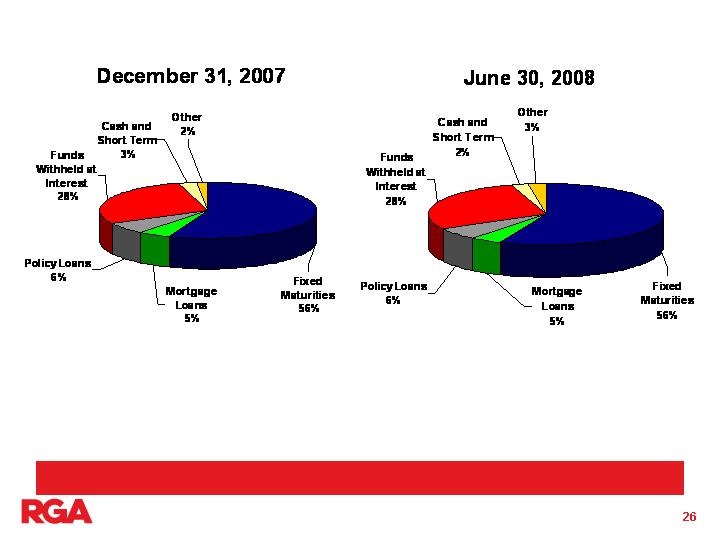

[Slide 26] Pie charts of our consolidated asset composition. At the end of last year, as well as at the end of the first six months, I would characterize our portfolio as relatively conservative. That is, compared to the typical life insurance company, ours probably is a little more conservative. Not a lot, but a little. It's an A quality, on average, portfolio, with the asset classes that you would normally see in an insurance company. And you can see the breakdown on this page reflecting pretty much the different types of asset classes.

You'll see one called funds withheld at interest. That represents asset portfolios that are on the books of some of our client companies. And because of the treaty structure, they maintain legal ownership of those securities, but the economics pass through to the reinsurer, in this case, RGA.

You can see a reference at the bottom, roughly 3% of our securities are below investment grade.

[Slide 27] With that, Greig, maybe you want to take the conclusion.

We have multiple opportunities to grow because of the nature of our business and the nature of our operations around the world, in particular our strong position in Asia and our growing position in Continental Europe, we have a strong team in place that's delivered impressive results over a long period of time. And we believe that the separation from MetLife will be nothing but beneficial to RGA and RGA's stock price going forward.

Reinsurance Group of America

____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

RGA / MET Exchange Offer

September 2008

CAUTIONARY STATEMENT REGARDING

FORWARD-LOOKING STATEMENTS

This presentation contains both historical and forward-looking statements. Forward-looking statements are not based on historical facts, but rather reflect the

Company’s current expectations, estimates and projections concerning future results and events. Forward-looking statements generally can be identified by

the fact that they do not relate strictly to historical or current facts and include, without limitation, words such as “believe,” “expect,” “anticipate,” “may,”

“could,” “intend,” “intent,” “belief,” “estimate,” “plan,” “foresee,” “likely,” “will” or other similar words or phrases. These forward-looking statements are not

guarantees of future performance and involve known and unknown risks, uncertainties, assumptions and other factors that are difficult to predict and that

may cause the Company’s actual results, performance or achievements to vary materially from what is expressed in or indicated by such forward-looking

statements. The Company cannot make any assurance that projected results or events will be achieved.

The risk factors set forth in the Company’s prospectus dated August 11, 2008 and proxy statement/prospectus dated August 4, 2008 in the respective

sections entitled “Risk Factors,” and the matters discussed in RGA’s SEC filings, including the “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” sections of RGA’s Annual Report on Form 10-K for the fiscal year ended December 31, 2007 and RGA’s Quarterly

Reports on Form 10-Q for the fiscal quarters ended March 31, 2008 and June 30, 2008, could affect future results, causing these results to differ materially

from those expressed in RGA’s forward-looking statements.

The forward-looking statements included in this document are only made as of the date of this document and RGA has no obligation to publicly update any

forward-looking statement to reflect subsequent events or circumstances.

Numerous important factors could cause actual results and events to differ materially from those expressed or implied by forward-looking statements

including, without limitation, (1) adverse changes in mortality, morbidity, lapsation or claims experience, (2) changes in our financial strength and credit

ratings or those of MetLife, Inc. ("MetLife"), the beneficial owner of a majority of our common shares, or its subsidiaries, and the effect of such changes on

our future results of operations and financial condition, (3) inadequate risk analysis and underwriting, (4) general economic conditions or a prolonged

economic downturn affecting the demand for insurance and reinsurance in our current and planned markets, (5) the availability and cost of collateral

necessary for regulatory reserves and capital, (6) market or economic conditions that adversely affect our ability to make timely sales of investment

securities, (7) risks inherent in our risk management and investment strategy, including changes in investment portfolio yields due to interest rate or credit

quality changes, (8) fluctuations in U.S. or foreign currency exchange rates, interest rates, or securities and real estate markets, (9) adverse litigation or

arbitration results, (10) the adequacy of reserves, resources and accurate information relating to settlements, awards and terminated and discontinued lines

of business, (11) the stability of and actions by governments and economies in the markets in which we operate, (12) competitive factors and competitors'

responses to our initiatives, (13) the success of our clients, (14) successful execution of our entry into new markets, (15) successful development and

introduction of new products and distribution opportunities, (16) our ability to successfully integrate and operate reinsurance business that we acquire, (17)

regulatory action that may be taken by state Departments of Insurance with respect to us, MetLife, or its subsidiaries, (18) our dependence on third parties,

including those insurance companies and reinsurers to which we cede some reinsurance, third-party investment managers and others, (19) the threat of

natural disasters, catastrophes, terrorist attacks, epidemics or pandemics anywhere in the world where we or our clients do business, (20) changes in laws,

regulations, and accounting standards applicable to us, our subsidiaries, or our business, (21) the effect of our status as an insurance holding company and

regulatory restrictions on our ability to pay principal of and interest on our debt obligations, and (22) other risks and uncertainties described in this document

and in our other filings with the Securities and Exchange Commission.

Additional Information and Where You Can Find It

In connection with MetLife’s proposed divestiture of its stake in RGA, on August 11, 2008, RGA filed with the Securities and Exchange Commission (the

“SEC”) a registration statement on Form S-4 (No. 333-152828), as amended, which includes a form of prospectus relating to the exchange offer. On August

14, 2008, MetLife filed with the SEC a statement on Schedule TO. In addition, RGA has filed with the SEC a registration statement on Form S-4 (File No.

333-151390), as amended, which includes a final proxy statement/prospectus dated August 4, 2008 related to the recapitalization. Investors and holders of

RGA and MetLife securities are strongly encouraged to read the registration statements and any other relevant documents filed with the SEC,

including the prospectus dated August 11, 2008 relating to the exchange offer and related exchange offer materials, the tender offer statement on

Schedule TO, and the proxy statement/prospectus dated August 4, 2008 relating to the recapitalization, as well as any amendments and

supplements to those documents, because they contain important information about RGA, MetLife, and the proposed transactions. The

prospectus relating to the exchange offer and related exchange offer materials have been mailed to stockholders of MetLife. The proxy statement/prospectus

relating to the recapitalization and related transactions has been mailed to shareholders of RGA. Investors and security holders can obtain free copies of the

registration statements, the prospectus relating to the exchange offer and related exchange offer materials and the tender offer statement on Schedule TO,

and the proxy statement/prospectus relating to the recapitalization, as well as other filed documents containing information about MetLife and RGA, without

charge, at the SEC’s web site (www.sec.gov). Free copies of RGA’s filings also may be obtained by directing a request to RGA, Investor Relations, by phone

to (636) 736-7243, in writing to Mr. John Hayden, Vice President-Investor Relations, Reinsurance Group of America, Incorporated, 1370 Timberlake Manor

Parkway, Chesterfield, Missouri, 63017, or by email to investrelations@rgare.com. Free copies of MetLife’s filings may be obtained by directing a request to

MetLife, Investor Relations, by phone to (212) 578-2211, in writing to MetLife, Inc., 1 MetLife Plaza, Long Island City, NY 11101, or by email to

metir@metlife.com. Neither RGA, MetLife nor any of their respective directors or executive officers or the dealer managers, with respect to the exchange

offer makes any recommendation as to whether you should participate in the exchange offer.

This communication shall not constitute an offer to sell or the solicitation of an offer to buy securities, nor shall there be any sale of securities in any

jurisdiction in which such solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. Such an offer

may be made solely by a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended. The distribution of this

communication may, in some countries, be restricted by law or regulation. Accordingly, persons who come into possession of this document should inform

themselves of and observe these restrictions.

RGA, MetLife and their respective directors and executive officers may be deemed, under SEC rules, to be participants in the solicitation of proxies from RGA’s

shareholders with respect to the proposed recapitalization. Information regarding the directors and executive officers of RGA is included in its definitive proxy

statement for its 2008 Annual Meeting of Shareholders filed with the SEC on April 9, 2008. Information regarding the directors and officers of MetLife is

included in the definitive proxy statement for MetLife’s 2008 Annual Meeting of Shareholders filed with the SEC on March 18, 2008. More detailed information

regarding the identity of potential participants, and their direct or indirect interests, by securities holdings or otherwise, is set forth in the proxy

statement/prospectus dated August 4, 2008 and the prospectus dated August 11, 2008 relating to the exchange offer, each as may be amended from time to

time, and other materials to be filed with the SEC in connection with the proposed transactions.

Participants in the Solicitation

Non-GAAP Measures

RGA uses a non-GAAP financial measure called “operating income” as a basis for analyzing financial results. This measure also serves as

a basis for establishing target levels and awards under RGA’s management incentive programs. Management believes that operating

income, on a pre-tax and after-tax basis, better measures the ongoing profitability and underlying trends of the company’s continuing

operations because that measure excludes the effect of net realized capital gains and losses, changes in the fair value of certain embedded

derivatives and related deferred acquisition costs. These items tend to be highly variable primarily due to the credit market and interest rate

environment and are not necessarily indicative of the performance of our underlying businesses. Additionally, operating income excludes

any net gain or loss from discontinued operations, which management believes is not indicative of the company’s ongoing operations. The

definition of operating income can vary by company and is not considered a substitute for GAAP net income.

Additionally, the Company evaluates its stockholder equity position excluding the impact of “Other Comprehensive Income”. This is also

considered a non-GAAP measure. The Company believes it is important to evaluate its stockholders’ equity position to exclude the effect of

Other Comprehensive Income since the net unrealized gains or losses included in Other Comprehensive Income primarily relate to changes

in interest rates, credit spreads on its investment securities and foreign currency fluctuations that are not permanent and can fluctuate

significantly from period to period.

Reconciliations of non-GAAP measures to the nearest GAAP measures are provided at the end of this presentation.

Effective in 1Q 2006, the Company changed its capital allocation methodology from a regulatory-based approach to an economic-based

approach. To enhance comparability, all prior period segment results in this presentation have been adjusted to reflect the new methodology.

This change in capital allocation does not affect the Company’s reported consolidated financial results.

Capital Allocation

Transaction Summary

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Transaction Summary

(1) Expiration of split-off may be extended to September 15, 2008, if exchange ratio limit is in effect at the end of the

originally contemplated split-off period.

Recapitalization

RGA recapitalizes its single class of stock into two classes of stock (Class

A

–

“low” vote; Class B

–

“high” vote)

Results in 29,243,539 MET

-

owned shares of “High” Vote Class B Common

Stock

RGA Shareholder Vote

September 5, 2008

Shares

to Be

Exchanged (Split

-

Off)

29,243,539 RGA Class B Shares owned by MET

for

outstanding MET

Common Stock

Split

-

Off Fixed Discount

Mechanism

RGA Class B shares offered at a 10% discount to MET shareholders

subject to a limit of 1.3071 shares of RGA Class B

Common Stock per

share of MET

Split

-

Off Expiration

September 11, 2008

(1)

Potential

Conversion of

RGA Dual Class Stock

RGA currently expects that, following the transactions, the RGA

Board of

D

irectors

will consider submitting a proposal to RGA’s sharehol

ders to

convert the dual

-

class structure into a single

-

class st

r

ucture. However,

there is no binding commitment by the RGA B

oard of

D

irectors

to

, and

there can be no assurance that the RGA Board of Directors will, consider

proposing a conversion or resolv

e to

submit such a proposal

to the RGA

shareholders

, and if submitted, there can be no

assurance

that the RGA

shareholders would approve

such a

conversion

Dealer Managers

Goldman Sachs

Merrill Lynch

Information Agent

D.F. King

Split

-

Off Website

http://www.dfking.com/metlife

RGA Investment Highlights

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

A. Greig Woodring (CEO)

RGA Investment Highlights

Second largest North American life reinsurer with

established and expanding global presence

A leading facultative reinsurer with high degree of

mortality expertise; provides competitive advantage

Multiple growth opportunities stemming from

on-going industry consolidation and international

expansion

Proven track record of delivering strong top and

bottom-line growth

Increased independence post-separation from

MetLife

Industry-leading management team

A Leading Life Reinsurer

Top Five Life Reinsurers Now Account for 76% of Market, Up From 48% in 1997

Source: 2007 Munich American / Society of Actuaries Reinsurance Survey

1.8

156.2

General Re Life

10

2.3

195.2

Canada Life

9

3.2

274.8

SCOR

8

4.3

362.4

Generali

7

4.8

406.4

ERC

6

9.9

850.0

Transamerica Re

5

11.4

970.0

Scottish Re

4

13.2

1,132.4

Munich American Re

3

16.7

1,429.1

RGA

2

24.5

$2,090.8

Swiss Re

1

($ in billions)

Share

Market

Force

Reinsurance In

Life

Reinsurer

Rank

North America In 2007

Worldwide in 2006

Rank

Reinsurer

Gross Life

Reinsurance

Premiums

($ in millions)

1

Swiss Re

$

10,378

2

Munich Re Group

10,114

3

RGA

4,732

4

Hannover Re

3,686

5

Scor

3,039

6

Berkshire Hathaway

2,476

7

Transamerica Re (Aegon)

2,259

8

Scottish Re Group, Ltd.

1,842

9

Reliastar

675

10

XL Re

597

Source: Standard & Poor's

Operational Strength

Leading new business

market share (23%) in

U.S.(1)

Leading new business

market share (35%) in

Canada(1)

Largest facultative

reinsurer(2)

High single-digit

premium growth

Long track record of

profitability

Region-wide leader in

individual new

business (26%)(3)

Second largest

reinsurer of new group

life (20%) market

share(3)

Market leader in new

treaty line acquisition(3)

Strong North American

Market Positions

Third-largest life &

health reinsurer in

the UK&I(4)

Well-established in

Spain

New Offices in Italy,

Germany, France,

and Poland

Changes in

regulation and

solvency measures

expected to provide

opportunities for new

market entrants

Well Positioned in

Rapidly Growing Asian

Markets

Continued Expansion

into Europe Offers

Growth Opportunities

(1) 2007 Munich American / Society of Actuaries Reinsurance Survey

(2) Based on Company estimate

(3) NMG Financial Services Consulting – 2008 Programme (March)

(4) NMG Financial Services Consulting – Risk Premium Monitor 2006

Expanding Global Presence

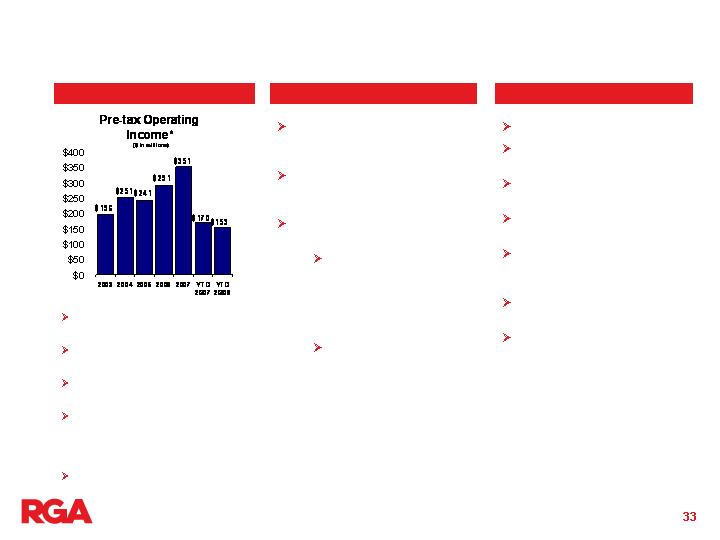

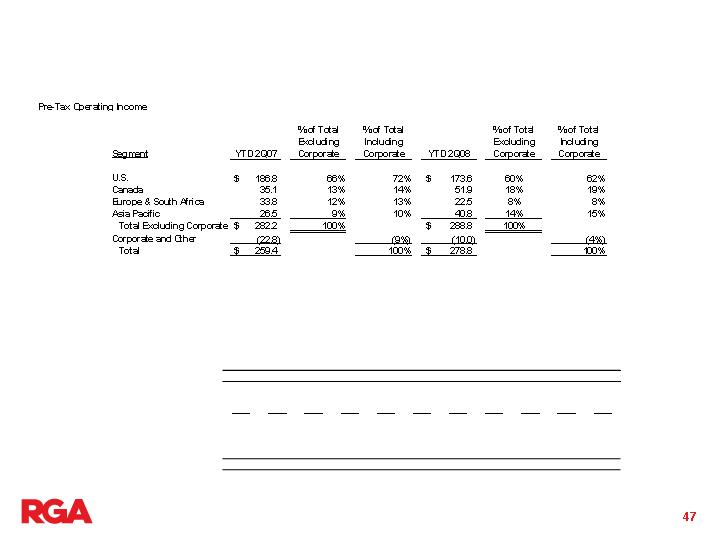

Total 2003 Pre-tax Operating Income = $263M

2003 Pre-tax Operating Income

by Operating Segment

YTD June 30, 2008 Pre-tax Operating

Income by Operating Segment

Note: Figures include results from the U.S., Canada, Asia Pacific and Europe & South

Africa operating segments; exclude Corporate segment. See “Reconciliations of Non-

GAAP Measures” at the end of this presentation.

Total YTD June 30, 2008 Pre-tax

Operating Income = $289M

Leading Facultative

Franchise

Recognized facultative expertise

Provide a market for non-conforming risks

Significant barriers to entry

Fosters closer relationships with cedants

Leverage for additional business opportunities

Provides some pricing power for automatic

business

Frequent entry point for international business

development

Significant Growth

Opportunities

Expect intermediate

growth of 8%-10% in

traditional market going

forward

Limited number of

competitors; good

pricing environment

expected to continue

Little impact from start-

ups

Some direct companies

retaining more business

Highest growth rates likely to

come from Asia Pacific (primarily

Japan and South Korea)

Penetration rates in most of Asia

Pacific are very low; Australia is

the exception

UK growth is moderating;

increase in number of

competitors

India and China represent

longer-term significant

opportunities

EU solvency and other

regulatory risk based capital

initiatives will likely be a catalyst

for additional reinsurance

opportunities

North America

International

North America Market

Continues to Grow

Source: Munich American / Society of Actuaries Reinsurance Surveys

($ in billions)

+8%

+15%

+5%

+4%

+2%

+76%

+12%

+16%

+1%

+16%

($ in billions)

Although cession rates in the U.S. market have fallen over the past several

years, RGA has continued to grow through market share increases.

United States

Life Reinsurance Inforce

Life Reinsurance Inforce

Canada

Strong Track Record of Growth

Share Price $12.28* $52.48 10.9%

Market Cap $480M $3.3B 14.8%

Assets $1.2B $21.6B 22.9%

Net Income $34.1M $293.8M 16.6%

Premiums $380M 4.9B 20.0%

Employees 198 1,066 12.8%

* Split-adjusted

December 31,

1993

December 31,

2007

CAGR

Increased Independence

Post-Separation from MetLife

Expected to eliminate overhang and increase liquidity and public

float for RGA common stock

Expected to result in wider following by equity research community

Expected to facilitate use of RGA common stock as acquisition

currency and source of capital and enhance the attractiveness of

RGA’s equity-based compensation plans

Expected to allow RGA to pursue future business initiatives free

from constraint of a controlling corporate shareholder

Expected to eliminate potential customer conflicts, given that some

key customers of RGA directly compete with MetLife

Expected to permit RGA shareholders to share in any premium

associated with any subsequent change in control of RGA

For a broader discussion of the potential advantages and

disadvantages of the separation from MetLife, see "RGA's Reasons

for the Recapitalization" in the prospectus dated August 11, 2008

Industry-Leading

Management Team

(1)

Includes experience in life insurance and life reinsurance industries

(2)

Includes experience with RGA’s predecessor, the reinsurance division of General American Life Insurance Company

Years Experience

Name

Position

In Industry

(1)

With RGA

(2)

A. Greig Woodring

President, Chief Executive Officer, and Director

33

29

Jack B. Lay

Senior E.V.P. and Chief Financial Officer

17

14

Paul A. Schuster

Senior E.V.P., U.S. Operations

32

17

Graham S. Watson

Senior E.V.P., International and Chief Marketing Officer

38

12

David B. Atkinson

E.V.P.

33

22

Brendan J. Galligan

E.V.P., Asia Pacific

30

18

John P. Laughlin

E.V.P., U.S. Financial Markets

24

13

Robert M. Musen

E.V.P.

32

8

Paul Nitsou

E.V.P., International

23

12

Alain P. Neemeh

President and Chief Executive Officer, RGA Canada

11

11

A. David Pelletier

E.V.P.

24

13

Michael S. Stein

E.V.P., U.S. Operations

27

10

Overview of Financial

Performance

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Jack B. Lay (CFO)

Financial Highlights

Operating EPS Growth 14% (5-year CAGR, 2003-2007)

Premium Growth 13% (2007 compared to 2006)

Return on Equity* 14% (2007)

BV/Share Growth* 14% (5-year and 14-year CAGR)

Operating EPS Growth 14%

Return on Equity* 14%

Historical Performance

Intermediate Goals

RGA targets debt leverage of 25% or less, commensurate with various rating agency guidelines for

existing ratings.

* Excludes accumulated other comprehensive income. See “Reconciliations of Non-GAAP

Measures” at the end of this presentation.

Life Reinsurance In Force

($ in billions)

Consolidated Net Premiums

($ in millions)

Consolidated Operating Income

Operating

Return on

Equity(1)

2003…13%

2004…12%

2005…11%

2006…13%

2007…14%

Operating Income

($ in millions)

Operating Income Per Share

(1)

Operating ROE is computed excluding accumulated other comprehensive income,

using quarterly average for equity amounts. See “Reconciliations of Non-GAAP

Measures” at the end of this presentation.

Quarterly Mortality Volatility

5 Year Average = 81.4%

RGA’s results can exhibit quarterly volatility in mortality experience,

but when measured over longer periods of time, mortality experience is

more predictable and stable.

Book Value Per Share*

5 Year Trend

* Book value excludes other comprehensive income. See “Reconciliations of Non-GAAP Measures”

at the end of this presentation.

Total Capitalization Levels

(Excluding Other Comprehensive Income)*

($ in millions)

Debt & Hybrids/

Total Capitalization 24.4% 22.5% 31.5% 26.6% 28.9% 27.9%

$2,279

$2,505

$3,039

$3,246

$3,748

$3,891

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

Consolidated Asset Composition

($ in millions) Carrying Value Carrying Value YTD

Asset Type Dec. 31, 2007 June 30, 2008 Change

Fixed Maturities $ 9,398 $ 9,668 $ 270

Mortgage Loans 832 799 (33)

Policy Loans 1,059 1,048 (11)

Funds Withheld at Interest 4,749 4,825 76

Cash and Short Term 479 410 (69)

Other 284 419 135

$ 16,801 $ 17,169 $ 368

Well-diversified fixed maturity portfolio; 97% investment grade as of June 30, 2008

Conclusion

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

A. Greig Woodring (CEO)

RGA Investment Highlights

Second largest North American life reinsurer with

established and expanding global presence

A leading facultative reinsurer with high degree of

mortality expertise; provides competitive advantage

Multiple growth opportunities stemming from on-

going industry consolidation and international

expansion

Proven track record of delivering strong top and

bottom-line growth

Increased independence post-separation from

MetLife

Industry-leading management team

Appendix:

RGA’s Operating Segments

Transaction Diagram

Reconciliations of Non-

GAAP Measures

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

RGA’s Operating Segments

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

U.S. Operations

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Total U.S. Operations

Pre-tax Operating Income*

($ in millions)

Net Premiums

($ in millions)

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

U.S. Traditional Operations

RGA’s goal is to be

among those 3-5 with

very favorable terms

Automatic reinsurance

programs are placed

with 3-5 reinsurers

RGA’s differentiator is

our facultative services

Companies cannot

access these

services unless RGA

is participating

automatically in their

reinsurance

In order to maintain

our industry-leading

facultative position,

we focus on

continually refining

and improving these

services

Competitive offers

Industry-leading time

service

Solid, individual life

capacity

Facultative Application

Console (FAC)

AURA technology-

based rules engine

(ASAP)

Underwriting

“Connection”

Yearly seminars,

newsletters

Approach to the Market

Facultative Excellence

$1.3 trillion of life

reinsurance inforce

Largest source of revenue

and earnings

Quality, long-term, client

base

Recognized leader in

facultative underwriting;

over 100,000 applications in

2007

Adverse claim levels in 1Q

2008

Overview

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

U.S. Asset Intensive and Financial

Reinsurance Sub-segments

Primarily annuities and COLI/BOLI; a

spread business

Some volatility in operating income due

to treatment of realized gains/losses for

funds withheld treaties

RGA shares in asset risk for general

account annuity transactions

Opportunistic growth; provides

meaningful diversification from mortality

risk

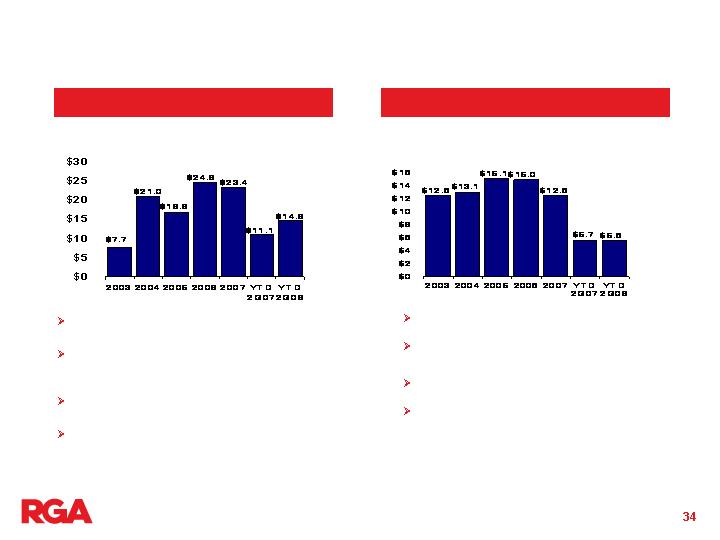

Pre-tax Operating Income*

($ in millions)

Asset Intensive

Financial Reinsurance

A recognized leader in this highly

specialized market

Limited new opportunities currently

in U.S.; stronger opportunities in

Asia Pacific

Intellectual capital is essential due

to complexity of transactions

Generally a fee-based business for

RGA; rely on retrocession capacity

Pre-tax Operating Income*

($ in millions)

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

Canada Operations

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Canada Operations

Established in 1992

Traditional individual life

reinsurance, including

preferred classes; some

creditor business

Most of the life insurance

companies in Canada are

clients

A market leader; primary

competitors are Munich

Re and Swiss Re

Strong results and

favorable mortality in 2007

and first half of 2008

Overview

Premiums

$ in millions

Pre-tax Operating Income*

$ in millions

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

International Operations

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

International Operations Overview

Have demonstrated success

Built green-field operations across the globe;

centrally managed by dedicated team in Toronto

Developed divisional infrastructure and culture

Established as a leading reinsurer in key

markets

Focused on multi-nationals and larger

local companies

Reinsurance products include life and

critical illness

Europe & South Africa Operations

Spain 1995

England 1999

South Africa 1999

India 2002

Ireland 2003

Poland 2006

Germany 2006

France 2007

Italy 2007

UK market has fueled past growth; 12%-

15% premium growth expected going

forward

Increasing continental Europe presence

Offices recently established in France,

Germany, Italy and Poland

Reinsurance products include life YRT and

coinsurance, accelerated critical illness

India viewed as providing long-term

growth opportunities

Adverse claim levels in UK and South

Africa in Q1 2008

Overview

Markets and Date of Entry

Net Premiums

Pre-tax Operating Income*

$ in millions

$ in millions

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

Asia Pacific Operations

Hong Kong 1994

Japan 1995

Australia/New Zealand 1996

Malaysia 1997

Taiwan 1999

South Korea 2002

China 2005

Overview

Markets and Date of Entry

Net Premiums

Pre-tax Operating Income*

$ in millions

$ in millions

Strong results in 2006, 2007 and first

half of 2008 lead by Australia, Japan

and South Korea

A recognized leader in the Asia

Pacific region based on NMG survey

Japan and South Korea should lead

growth in near term

Strong facultative market in Japan

Opened office in China in 2005;

longer-term growth opportunity

* See “Reconciliations of Non-GAAP Measures” at the end of this presentation.

Transaction Diagram

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Transaction Diagram

Status Quo

Step 1: Recapitalization of

RGA Stock

RGA recapitalizes its single class of stock into

two classes of stock (Class A – “low” vote;

Class B – “high” vote)

MET exchanges substantially all of its stake for

all Class B shares(1)

RGA

Class A

Shares

(<20% Vote)

RGA

Class A & B

Shares(1)(2)

(>80% Vote)

(1) In addition to the Class B shares, MET will also own 3 million Class A shares which it will dispose of within 60

months of the completion of the split-off.

(2) Class B shares carry “high” vote, having the right to elect at least 80% of the board of directors.

RGA

Other MET

Businesses

MET

Existing MET

Shareholders

48%

Vote

52%

Vote

Existing RGA

Shareholders

RGA

Other MET

Businesses

MET

Existing MET

Shareholders

Existing RGA

Shareholders

Transaction Diagram (Cont’d)

Step 2: Split-Off

(Exchange Offer)

RGA

Other MET

Businesses

MET

Existing MET

Shareholders

Existing RGA

Shareholders

MET splits-off all of its RGA Class B shares in exchange for MET shares

RGA Class B shares offered at a 10% discount subject to a limit of 1.3071 shares of RGA Class B

Common Stock per share of MET

RGA

Class A

Shares

RGA

Class B

Shares

MET

Shares

RGA

Class A

Shares

Reconciliations of Non-

GAAP Measures

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Financial Performance

(1) Net of DAC offset

14.8

11.1

23.4

24.6

16.8

21.0

7.7

Pre-tax Operating Income

47.5

0.9

37.5

(2.8)

(0.5)

2.0

(12.9)

Change in MV of Embedded Derivatives(1)

(1.5)

1.6

8.2

7.2

1.0

7.3

1.4

Realized Capital (Gains) / Losses (1)

(31.2)

8.6

(22.3)

20.2

16.3

11.7

19.2

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

U.S. ASSET-INTENSIVE

153.2

170.0

351.4

291.2

241.0

251.2

195.7

Pre-tax Operating Income

3.1

4.9

13.8

4.1

8.6

(18.1)

6.6

Realized Capital (Gains) / Losses

150.1

165.1

337.6

287.1

232.4

269.3

189.1

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

U.S. TRADITIONAL OPERATIONS

(10.0)

(22.8)

(29.6)

(37.6)

(41.8)

(9.0)

(9.3)

Pre-tax Operating Income

0.1

11.8

12.5

(4.0)

(17.4)

(7.8)

(0.9)

Realized Capital (Gains) / Losses

(10.1)

(34.6)

(42.1)

(33.6)

(24.4)

(1.2)

(8.4)

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

CORPORATE & OTHER SEGMENT

40.8

26.5

61.6

59.0

31.5

7.1

13.3

Pre-tax Operating Income

1.0

0.6

1.5

0.4

0.3

(0.3)

0.1

Realized Capital (Gains) / Losses

39.8

25.9

60.1

58.6

31.2

7.4

13.2

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

ASIA-PACIFIC OPERATIONS

($ in millions)

Reconciliation of Pre-Tax Income to Pre-Tax Operating Income

22.5

33.8

49.7

58.6

35.8

27.3

15.2

Pre-tax Operating Income

(0.6)

0.8

2.2

0.3

0.3

(2.3)

(2.6)

Realized Capital (Gains) / Losses

23.1

33.0

47.5

58.3

35.5

29.6

17.8

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

EUROPE & SOUTH AFRICA OPERATIONS

51.9

35.1

74.9

40.6

46.8

31.2

18.2

Pre-tax Operating Income

1.5

(4.1)

(6.6)

(5.2)

(3.4)

(8.1)

(9.9)

Realized Capital (Gains) / Losses

50.4

39.2

81.5

45.8

50.2

39.3

28.1

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

CANADA OPERATIONS

U.S. FINANCIAL REINSURANCE

2003

2004

2005

2006

2007

YTD 2Q07

YTD 2Q08

GAAP Pre-Tax Income - Cont Ops

12.6

13.1

15.1

15.0

12.6

5.7

5.6

Realized Capital (Gains) / Losses

-

-

-

-

-

-

-

Pre-tax Operating Income

12.6

13.1

15.1

15.0

12.6

5.7

5.6

TOTAL US OPERATIONS SEGMENT

2003

2004

2005

2006

2007

YTD 2Q07

YTD 2Q08

GAAP Pre-Tax Income - Cont Ops

220.9

294.1

263.8

322.3

327.9

179.4

124.5

Realized Capital (Gains) / Losses(1)

8.0

(10.8)

9.6

11.3

22.0

6.5

1.6

Change in MV of Embedded Derivatives(1)

(12.9)

2.0

(0.5)

(2.8)

37.5

0.9

47.5

Pre-tax Operating Income

216.0

285.3

272.9

330.8

387.4

186.8

173.6

(1) Net of DAC offset

Financial Performance

(1) Net of DAC offset

278.8

259.4

544.0

451.4

345.2

341.9

253.4

Pre-tax Operating Income

47.5

0.9

46.5

(2.8)

(0.5)

2.0

(12.9)

Change in MV of Embedded Derivatives(1)

3.6

15.6

22.6

2.8

(10.6)

(29.3)

(5.3)

Realized Capital (Gains) / Losses(1)

227.7

242.9

474.9

451.4

356.3

369.2

271.6

GAAP Pre-Tax Income - Cont Ops

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

RGA CONSOLIDATED

$

2.82

$

2.60

$

5.50

$

4.65

$

3.54

$

3.57

$

3.22

Operating EPS from Cont. Operations

0.08

0.04

0.22

0.08

0.18

0.37

0.11

Loss from Discontinued Operations

0.48

0.01

0.47

(0.03)

(0.01)

0.02

(0.16)

Change in MV of Embedded Derivatives

0.04

0.16

0.23

0.03

(0.15)

(0.34)

(0.09)

Realized Capital (Gains) / Losses

$

2.22

$

2.39

$

4.57

$

4.57

$

3.52

$

3.52

$

3.36

GAAP Net Income

YTD 2Q08

YTD 2Q07

2007

2006

2005

2004

2003

Per Diluted Share Basis

CONSOLIDATED EPS RECONCILIATION

Stockholders’ Equity Reconciliation

Consolidated EPS Reconciliation

($ in millions)

Reconciliation of Pre-Tax Income to

Pre-Tax Operating Income

2003

2004

2005

2006

2007

YTD 2Q07

YTD 2Q08

GAAP Stockholders' Equity

1,947.7

$

2,279.0

$

2,527.5

$

2,815.4

$

3,189.8

$

2,894.6

$

3,061.4

$

FAS 115 Equity Adjustment

170.6

244.7

361.8

335.6

313.2

204.1

47.5

Foreign Currency Adjustment

53.6

93.7

85.1

109.1

222.0

182.0

215.6

Unrealized Pension

0.0

0.0

0.0

(11.3)

(8.4)

(11.6)

(8.1)

Equity Excluding OCI

1,723.5

$

1,940.6

$

2,080.6

$

2,382.0

$

2,663.0

$

2,520.1

$

2,806.4

$

GAAP Stockholders' Average Equity

1,460.8

$

2,071.7

$

2,423.4

$

2,613.8

$

2,965.8

$

2,866.4

$

3,103.4

$

FAS 115 Average Equity Adjustment

148.5

180.0

310.5

287.9

282.2

293.3

175.9

Foreign Currency Adjustment

26.9

54.6

84.1

102.3

174.9

138.0

213.7

Unrealized Pension

-

-

-

(2.3)

(10.9)

(11.4)

(8.2)

Average Equity Excluding OCI

1,285.4

$

1,837.0

$

2,028.8

$

2,225.8

$

2,519.6

$

2,446.5

$

2,721.9

$

Operating ROE - GAAP Stockholders' Equity

11%

11%

9%

11%

12%

6%

6%

Operating ROE - Excluding OCI

13%

12%

11%

13%

14%

7%

7%

Financial Performance

Pre-Tax Operating Earnings YTD

($ in millions)

Book Value per Share Reconciliation

2Q08

1Q08

4Q07

3Q07

2Q07

1Q07

4Q06

3Q06

2Q06

1Q06

4Q05

Book value per share

49.13

$

49.15

$

51.42

$

49.03

$

46.69

$

46.81

$

45.85

$

45.22

$

40.30

$

40.62

$

41.38

$

Less: effect of FAS 115

0.76

2.69

5.04

3.52

3.29

5.51

5.46

5.93

2.14

4.04

5.92

Less: effect of CTA

3.46

3.27

3.58

3.84

2.94

1.99

1.78

1.90

1.92

1.36

1.40

Less: effect of Pension Benefit

(0.13)

(0.13)

(0.13)

(0.19)

(0.19)

(0.18)

(0.18)

-

-

-

-

Book value per share excluding OCI

45.04

$

43.32

$

42.93

$

41.86

$

40.65

$

39.49

$

38.79

$

37.39

$

36.24

$

35.22

$

34.06

$

3Q05

2Q05

1Q05

4Q04

3Q04

2Q04

1Q04

4Q03

3Q03

2Q03

1Q03

Book value per share

40.33

$

39.60

$

36.79

$

36.50

$

33.92

$

31.38

$

33.11

$

31.33

$

28.92

$

28.93

$

25.18

$

Less: effect of FAS 115

5.52

6.22

3.37

3.92

2.91

1.21

3.67

2.74

3.47

4.19

1.76

Less: effect of CTA

1.45

1.04

1.36

1.50

0.75

0.49

0.77

0.86

0.67

0.73

0.21

Less: effect of Pension Benefit

-

-

-

-

-

-

-

-

-

-

-

Book value per share excluding OCI

33.36

$

32.34

$

32.06

$

31.08

$

30.26

$

29.68

$

28.67

$

27.73

$

24.78

$

24.01

$

23.21

$

Reinsurance Group of America

____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

RGA / MET Exchange Offer

September 2008