SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

| Filed by the Registrant: | | o |

| Filed by a Party other than the Registrant: | | X |

| Check the appropriate box: |

| | o | Preliminary Proxy Statement |

| | o | Confidential, for Use of the Commission only (as permitted by Rule 14a-6(e)(2)) |

| | o | Definitive Proxy Statement |

| | X | Definitive Additional Materials |

| | o | Soliciting Material Under Rule 14a-12 |

CROWN CRAFTS, INC.

(Name of Registrant as Specified in its Charter)

WYNNEFIELD PARTNERS SMALL CAP VALUE, L.P.

WYNNEFIELD PARTNERS SMALL CAP VALUE, L.P. I

WYNNEFIELD SMALL CAP VALUE OFFSHORE FUND, LTD.

WYNNEFIELD CAPITAL MANAGEMENT, LLC

WYNNEFIELD CAPITAL, INC.

CHANNEL PARTNERSHIP II, L.P.

WYNNEFIELD CAPITAL, INC. PROFIT SHARING & MONEY PURCHASE PLAN

NELSON OBUS

JOSHUA H. LANDES

JON C. BIRO

MELVIN L. KEATING

(Name of Person(s) Filing Proxy Statement if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box)

| | X | | No fee required. |

| | o | | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| | | | (1) | Title of each class of securities to which transaction applies: |

| | | | (2) | Aggregate number of securities to which transaction applies: |

| | | | (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act |

| | | | | Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was |

| | | | | determined): |

| | | | (4) | Proposed maximum aggregate value of transaction: |

| | | | (5) | Total fee paid: |

| | o | | Fee paid previously with preliminary materials. |

| | o | | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify |

| | | | the filing for which the offsetting fee was paid previously. Identify the previous filing by |

| | | | registration statement number, or the Form or Schedule and the date of its filing. |

| | | | (1) | Amount Previously Paid: |

| | | | (2) | Form, Schedule or Registration Statement No.: |

| | | | (3) | Filing Party: |

| | | | (4) | Date Filed: |

The Wynnefield Group

Investor Presentation

Regarding Crown Crafts, Inc.

(Nasdaq: CRWS)

I.

Who is the Wynnefield Group?

II.

Change Needed to Create Stockholder Value

A.

Background of Election Contest

B.

Wynnefield Warned About This in 2007

C.

Years of Underperformance and Entrenchment

D.

Board has No Articulated Strategic Plan; Product Line

Extension Does Not Qualify

III.

Deficiencies of the Current Management-Endorsed

Board Majority

A.

Misaligned Interests Lead to Pursuit of Status Quo

B.

Current Board Not Acting in Stockholders’ Best Interests;

Reinstated “Poison Pill” Without Stockholder Approval

IV.

Wynnefield’s Nominees

A.

Expertise to Address Company’s Challenges

B.

Focus on Increasing Value for All Stockholders

Overview

2

Value investor in small & micro-cap stocks

Largest stockholder of Crown Crafts

Currently own about 17% of outstanding stock

Long-term investor

Invested in Crown Crafts since 1996 and have

increased holdings at a variety of price points to

protect ownership during this period

Who Is The Wynnefield Group?

3

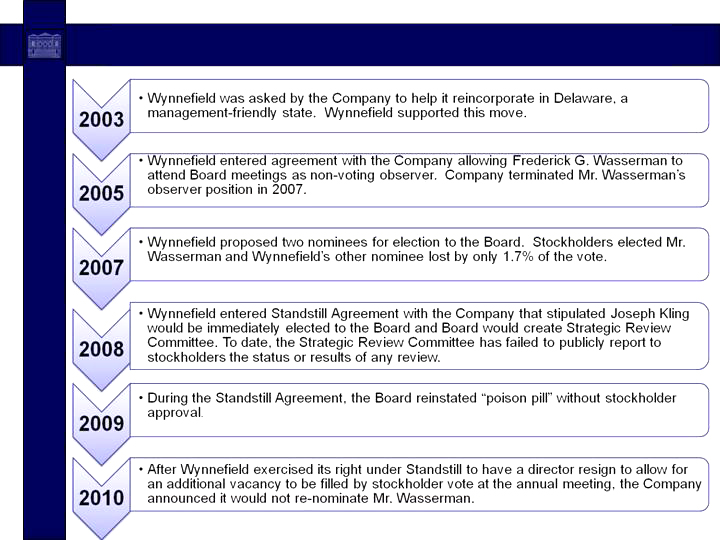

Background of Election Contest

4

CRWS’ Unfulfilled 2007 Promises: Share Price

Pointing to share price of $4.65, Crown Crafts wrote: “In many respects, fiscal year 2007

marked the successful completion of our efforts that began in 2001 to turn the Company

around and reestablish a solid foundation for growth and success…” [Letter to

stockholders, 7/24/07]

Fact: CRWS stock has never again achieved that level – down more than 16% since

then (as of July 20, 2010).

CRWS’ Unfulfilled 2007 Promise: Creating Value

Describing a company “more nimble and poised for growth,” it promised “strategic

acquisitions that will build long-term stockholder value” and enhancing stockholder value

through “achieving organic growth,” among other objectives. [Letter to stockholders,

7/16/07]

Fact: Over the past three years, CRWS has instead completed three small tuck-in

acquisitions while revenue and operating income remain flat.

Fact: CRWS’ net sales decreased by $1.3 million (1.5%) in FY 2010, despite the

Company’s assertions in its earnings release that it was a “banner year.”

5

Wynnefield Warned About This in 2007

6

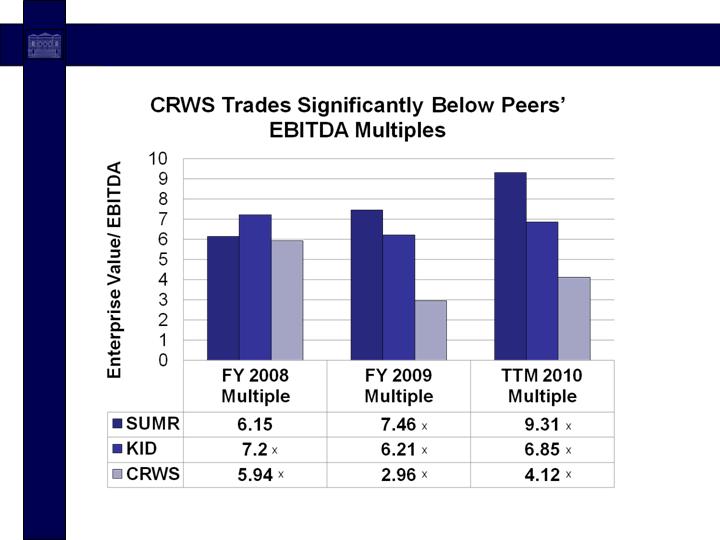

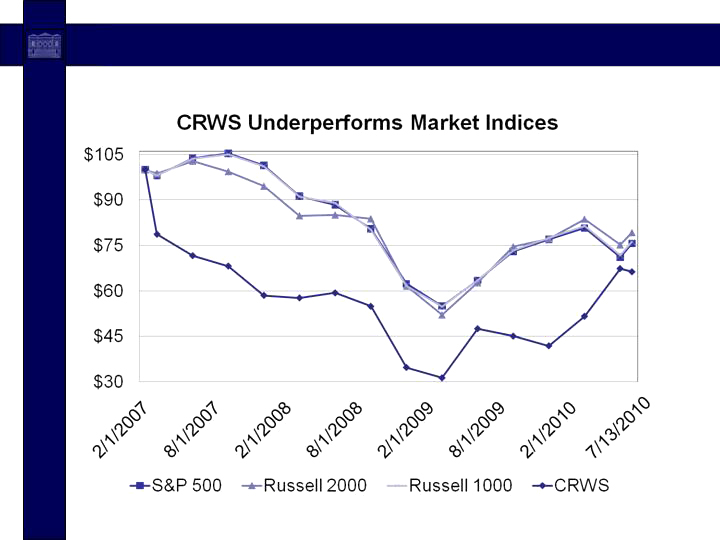

Years of Underperformance and Entrenchment

x

Source: Bloomberg as of July 21, 2010

* TTM = Trailing Twelve Months

*

7

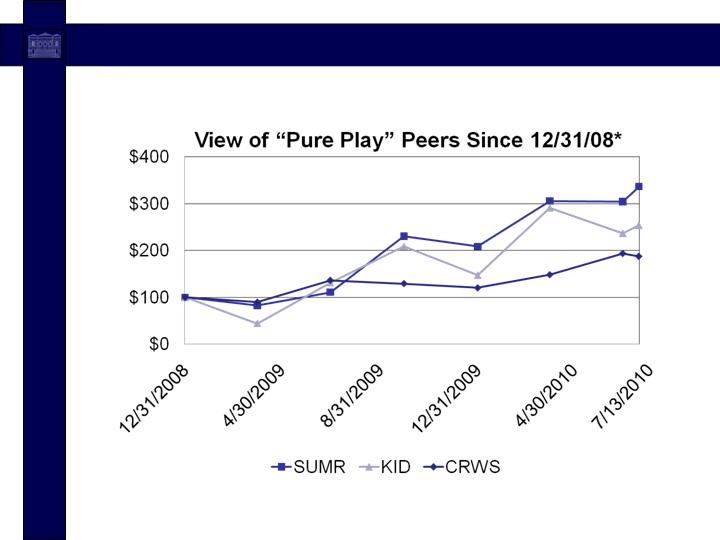

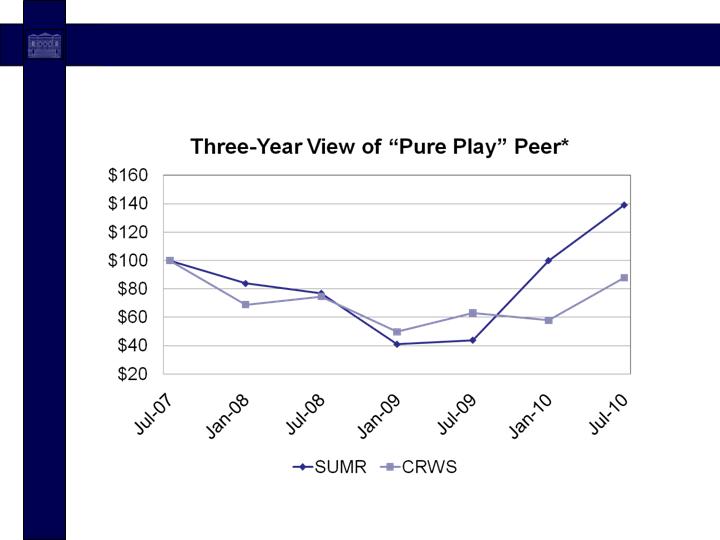

Years of Underperformance and Entrenchment

8

Years of Underperformance and Entrenchment

*Pure Play - Infant and Juvenile Industry Company

9

Years of Underperformance and Entrenchment

* As of 12/23/08, KID became a “Pure Play” Peer after divestiture of giftware business

10

Years of Underperformance and Entrenchment

*Excludes KID, which did not become a “Pure Play” Peer until divestiture of giftware business on 12/23/08

Strategic Review Committee Never Publicly Disclosed

Findings or Even that it had Deliberations

Only After Wynnefield’s 2010 Proxy Announcement Did

Board Proclaim Adoption of “Strategic Plan”

This is first stockholders have heard of this

Still, nothing else disclosed about “plan”

Only thing known about “plan” – if there even is one – is

that it has failed to create stockholder value

This recent announcement is only a product line

extension

The Company’s Micro-Acquisitions Merely Mask

Declining Core Business to Maintain Status Quo

No Stockholder Value Created by the Board or

Management’s Actions in Recent Times

11

Board Has No Articulated Strategic Plan

Lavish Board and Management Pay Incentivize Status Quo Rather

Than Creating Stockholder Value

Management:

Board-approved lavish executive compensation and severance

packages – significant amounts of cash; little long-term equity

compensation despite policy statement to the contrary

Board-approved golden parachute payments and tax gross-ups that

could cost more than $5 million – exceeding CRWS’ annual net income

Board-approved incentive plan rewards management with approximately

3.7% of Company if over five years they match the EBITDA multiple at

which peers are currently trading, a handsome reward for average

performance

Board:

Over past three years, total Board compensation was over $1.3 million

while market value declined by $10.6 million (-22%)

In 2008, Board retainers doubled while operating income remained flat

In 2009, one director’s total compensation was $104,126

Majority of Board retainer paid in cash

Current non-employee directors hold only 2% of outstanding voting stock

12

Misaligned Interests Lead to Pursuit of Status Quo

13

Board Not Acting in Stockholders’ Best Interests

Jon C. Biro

Executive Officer

CFO – Consolidated Graphics, Inc.

CFO, Interim CEO – ICO, Inc.

Corporate Director

Aspect Medical Systems Inc.

ICO, Inc.

Public Accounting & Finance

Certified Public Accountant (CPA)

Price Waterhouse LLP

*Current

Melvin L. Keating

Executive Officer

CEO – Alliance Semiconductor

Corp.

CEO – Sunbelt Management

EVP, CFO & Treasurer –

Quovadx Inc.

Corporate Director

Bitstream Inc.*

Infologix, Inc.*

Red Lion Hotels, Corp.*

Aspect Medical Systems Inc.

Integrated Silicon Solutions Inc.

Plymouth Rubber Co.

Price Legacy Corp.

White Electronic Designs Corp.

Strategic Consultant

Warburg Pincus Equity Partners

BTI Systems, Inc.

14

Wynnefield Nominees’ Expertise

Our Nominees are committed to working

constructively with Board to create stockholder value

and address significant corporate governance

deficiencies

Strategic Plan

Form standing Strategic Review

Committee

Hire qualified independent

consultant to help determine

future path

Communicate to stockholders

nature and extent of review

Cause Company to participate in

investor or industry conferences

Corporate Governance

Eliminate staggered Board

Adopt real CEO succession plan

Terminate “poison pill”

Link executive compensation to

Company performance

Split Chairman/CEO roles

Amend non-employee director

compensation; our Nominees will

only take 50% of cash

compensation or donate balance

to American SIDS Institute

Modify change-in-control

agreements

15

Focus to Increase Value for All Stockholders