Table of Contents

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF

THE SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant: [X]

Filed by a Party other than the Registrant: [ ]

Check the appropriate box:

[ ] Preliminary Proxy Statement

[ ] Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

[X] Definitive Proxy Statement

[ ] Definitive Additional Materials

[ ] Soliciting Material Under Rule 14a-12

PERRY ELLIS INTERNATIONAL, INC.

(Name of Registrant as Specified in its Charter)

N/A

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

[ ] No fee required.

[ ] $125 per Exchange Act Rules 0-11(c)(1)(ii), 14a-6(i)(2) or Item 22(a)(2) of Schedule 14A.

[ ] Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) | Title of each class of securities to which transaction applies: | |||

(2) | Aggregate number of securities to which transaction applies: | |||

(3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | |||

(4) | Proposed maximum aggregate value of transaction: | |||

(5) | Total fee paid: | |||

[ ] Fee paid previously with preliminary materials.

[X] Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2)

and identify the filing for which the offsetting fee was paid previously. Identify the

| previous | filing by registration statement number, or the Form or Schedule and the date of its filing. |

(1) | Amount previously paid: | |||

$2,825.81 | ||||

(2) | Form, schedule or registration statement no.: | |||

Registration No. 333-103848 | ||||

(3) | Filing party: | |||

Perry Ellis International, Inc. | ||||

(4) | Date filed: | |||

March 17, 2003. | ||||

Table of Contents

May 19, 2003

3000 N.W. 107th Avenue

Miami, Florida 33172

Dear Perry Ellis Shareholder:

You are cordially invited to attend the 2003 annual meeting of shareholders of Perry Ellis International, Inc., to be held at Le Parker Meridien Hotel, 119 West 56th Street, New York, New York 10019, on Tuesday, June 17, 2003, at 11:00 a.m., New York City time.

As you know, on February 3, 2003 we entered into a merger agreement with Salant Corporation which provides for the merger of a wholly owned Perry Ellis subsidiary into Salant. If the merger is completed, Salant will become a wholly owned subsidiary of Perry Ellis. We are very excited about this transaction. We believe the merger enables us to consolidate control of the Perry Ellis brands’ major product categories. We also expect the merger to be accretive from an earnings perspective, add significant revenue and earnings growth and strengthen our balance sheet. The merger is subject to customary closing conditions, including the adoption of the merger agreement by the holders of a majority of the outstanding shares of Salant’s common stock. If all of the conditions to the merger are satisfied, we anticipate completing the merger within two business days after the annual meeting.

The aggregate consideration to be paid by Perry Ellis in the merger will be $91.0 million, comprised of approximately $52.0 million in cash and approximately $39.0 million worth of Perry Ellis’ common stock. The precise fraction of a share of Perry Ellis’ common stock that we will issue in the merger for each Salant share will be determined by dividing $39.0 million by the average closing price of our common stock for the 20-trading day period ending three trading days before the merger closing date. The maximum number of shares of Perry Ellis’ common stock that we will issue is limited to 3,250,000. Assuming that all 3,250,000 shares of Perry Ellis’ common stock are issued, following the merger former holders of Salant’s common stock and Salant’s stock options will own approximately 33.6% of the outstanding shares of Perry Ellis’ common stock. This will have the effect of reducing your percentage ownership of our common stock. Of such 3,250,000 newly issued shares of Perry Ellis’ common stock, a maximum of 2,238,548 shares also are being registered for resale by certain selling shareholders of Salant named in the accompanying joint proxy statement-prospectus.

At the annual meeting, you will be asked to vote on a proposal to approve the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger. You are not being asked to approve the merger agreement. At the annual meeting, you will also be asked to vote on certain other separate and independent proposals set forth in the accompanying notice of annual meeting and described in detail in the accompanying joint proxy statement-prospectus.

In considering the proposed merger your board of directors consulted with our senior management team and Perry Ellis’ legal and financial advisors. In addition, the board received the written opinion of Sawaya Segalas & Co., LLC stating that, as of February 1, 2003, the proposed cash and stock consideration to be paid by us to Salant’s shareholders in the merger was fair to Perry Ellis, from a financial point of view. A copy of Sawaya Segalas’ opinion is included asAnnex C to the accompanying joint proxy statement-prospectus and we encourage you to read it carefully and in its entirety.

After careful consideration, your board of directors unanimously determined that the merger is in the best interests of Perry Ellis and its shareholders and adopted the merger agreement. Your board unanimously recommends that you vote “FOR” approval of Perry Ellis’ issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger and “FOR” each of the other separate proposals to be voted on at the annual meeting.

The accompanying joint proxy statement-prospectus describes in detail information about Perry Ellis, Salant, the merger and other important separate proposals you are being asked to vote on at the annual meeting. We encourage you to read the entire joint proxy statement-prospectus and the annexes thereto carefully.In particular, you should read and consider carefully the risks discussed under the caption titled“Risk Factors” beginning on page I-18 of the accompanying joint proxy statement-prospectus before completing your proxy card. In addition, you may obtain additional information about Perry Ellis and Salant from documents filed with the Securities and Exchange Commission at the locations and in the manner described in the accompanying joint proxy statement-prospectus.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of the merger or the shares of Perry Ellis’ common stock to be issued in the merger or determined whether the joint proxy statement-prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

You should know that your chairman and chief executive officer, your president and chief operating officer, and certain of their affiliates, have agreed with Salant to vote all of their Perry Ellis shares, representing 49.6% of the outstanding shares of Perry Ellis’ common stock, in favor of the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger. In addition, each of Perry Ellis’ directors and executive officers has indicated his or her intention to vote all shares of Perry Ellis’ common stock he or she owns in favor of each of the proposals to be voted on at the annual meeting . On May 14, 2003, the record date established for the annual meeting, Perry Ellis’ directors and executive officers beneficially owned in the aggregate approximately 56.0% of Perry Ellis’ outstanding common stock.

Perry Ellis’ common stock is listed on The Nasdaq Stock Market under the symbol “PERY”. On May 16, 2003, the last trading day prior to the date of the accompanying joint proxy statement–prospectus, the closing sale price of a share of Perry Ellis’ common stock was $20.07.

Whether or not you plan to attend the annual meeting, please complete, sign and date the enclosed proxy card and return it to us in the enclosed envelope. Your prompt cooperation will be greatly appreciated. Your proxy may be revoked at any time, before votes at the annual meeting are tabulated, by delivering to Perry Ellis’ corporate secretary a written revocation or a proxy bearing a later date or by oral revocation in person to Perry Ellis’ corporate secretary at the annual meeting.

Thank you very much for your continued support.

Sincerely,

George Feldenkreis

Chairman of the Board and

Chief Executive Officer

The accompanying joint proxy statement-prospectus is dated May 19, 2003 and is first being mailed to shareholders of Perry Ellis and Salant on or about May 20, 2003.

Table of Contents

3000 N.W. 107th Avenue

Miami, Florida 33172

NOTICE OF ANNUAL MEETING

OF

PERRY ELLIS SHAREHOLDERS

TO BE HELD ON JUNE 17, 2003

To All Shareholders of Perry Ellis International, Inc.:

NOTICE IS HEREBY GIVEN that the 2003 annual meeting of shareholders of Perry Ellis International, Inc. will be held on Tuesday, June 17, 2003, at 11:00 a.m., New York City time, at Le Parker Meridien Hotel, 119 West 56th Street, New York, New York 10019, for the following important purposes:

| 1. | To consider and vote on a proposal to approve the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders under the agreement and plan of merger dated February 3, 2003, among Perry Ellis, Salant Corporation and Connor Acquisition Corp., a wholly owned subsidiary of Perry Ellis. |

In the merger, Salant will become a direct wholly owned subsidiary of Perry Ellis and all outstanding shares of Salant’s common stock, other than shares held by shareholders who perfect their statutory appraisal rights under Delaware law, will be converted into the right to receive cash and a fraction of a share of Perry Ellis’ common stock. The fraction will be determined based on the average closing sale price of Perry Ellis’ common stock reported on The Nasdaq Stock Market for the 20-consecutive trading day period ending three trading days before the merger closing date.

| 2. | To elect three directors of Perry Ellis to serve for a three-year term expiring in 2006. |

| 3. | To consider and vote on a proposal to approve an amendment to Perry Ellis’ articles of incorporation to increase the shares of common stock which Perry Ellis is authorized to issue from 30,000,000 to 100,000,000. |

| 4. | To consider and vote on a proposal to approve an amendment to Perry Ellis’ articles of incorporation to increase the shares of preferred stock which Perry Ellis is authorized to issue from 1,000,000 to 5,000,000. |

| 5. | To consider and vote on a proposal to approve an amendment to Perry Ellis’ articles of incorporation to eliminate the ability to take shareholder action by written consent in lieu of a shareholder meeting. |

| 6. | To consider and vote on a proposal to approve an amendment to Perry Ellis’ articles of incorporation to require advance notice and disclosure procedures for shareholders seeking to nominate Perry Ellis’ directors. |

| 7. | To consider and vote on a proposal to approve an amendment to Perry Ellis’ articles of incorporation to require the affirmative vote of 66- 2/3% of the outstanding common stock of Perry Ellis to effect certain future amendments to the articles. |

| 8. | To consider and vote on a proposal to approve an amendment to Perry Ellis’ 2002 stock option plan to allow restricted stock awards to be granted to participants in the plan and to increase the shares of common stock reserved for issuance under the plan from 1,000,000 to 1,500,000. |

| 9. | To consider and vote on a proposal to ratify the appointment by our audit committee of Deloitte & Touche LLP to serve as Perry Ellis’ independent auditors for the fiscal year ending January 31, 2004. |

| 10. | To consider and act on any other matters that properly may be presented at the annual meeting or any adjournment or postponement of the annual meeting, including proposals to adjourn the annual meeting to permit further solicitation of proxies by the board of directors of Perry Ellis if there are insufficient votes to approve any of the proposals above at the time of the annual meeting; provided that no proxy which is voted against Proposal 1 above will be voted in favor of adjournment to solicit further proxies for that proposal. |

Table of Contents

Each of the proposals below are entirely independent of each other and will be voted on separately, and the effectiveness of any one of these proposals is not conditioned upon the approval by Perry Ellis’ shareholders of any of the other proposals to be voted on at the annual meeting.

These proposals, as well as information about the proposed merger, Perry Ellis and Salant, are described in detail in the accompanying joint proxy statement-prospectus. We urge you to read these materials very carefully and in their entirety before deciding how to vote. Only Perry Ellis’ shareholders of record on May 14, 2003 are entitled to notice of and to vote at the annual meeting or at any postponements or adjournments of the annual meeting. A list of shareholders entitled to vote at the annual meeting will be available for inspection during normal business hours for 10 days prior to the annual meeting at Perry Ellis’ executive offices at 3000 N.W. 107th Avenue, Miami, Florida 33172.

Your vote is very important, regardless of the number of shares of Perry Ellis’ common stock you own! Please vote as soon as possible to ensure that your shares are represented at the annual meeting. To vote your shares, you must complete and return the enclosed proxy card. If you are a record holder, you may also cast your vote in person at the annual meeting. If your shares are held in an account at a brokerage firm or bank, you must instruct them on how to vote your shares.

Even if you plan to attend the annual meeting in person, please sign, date and return the accompanying proxy in the enclosed addressed envelope, which requires no postage if mailed in the United States. If you chose to approve a proposal, you will need to check the box indicating a vote “FOR” the proposal by following the instructions contained in the enclosed proxy card. If you properly sign and return your proxy card with no voting instructions, you will be deemed to have voted “FOR” the approval of Proposals 1-9 above. Your proxy may be revoked at any time before votes at the annual meeting are tabulated by delivering to Perry Ellis’ corporate secretary a written revocation or a proxy bearing a later date or by revoking your proxy in person by delivering oral revocation to Perry Ellis’ corporate secretary at the annual meeting.

After careful consideration, your board of directors unanimously determined that the merger is in the best interests of Perry Ellis and its shareholders and adopted the merger agreement. Your board of directors unanimously recommends that you vote “FOR” approval of the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger and “FOR” each of the other separate proposals to be considered and voted on at the annual meeting.

By Order of the Board of Directors,

Fanny Hanono

Secretary

Miami, Florida

May 19, 2003

Please do not send us any of your stock certificates with your proxy card.

Table of Contents

I-1 | ||

I-1 | ||

I-1 | ||

I-5 | ||

The Companies | I-5 | |

Historical Business Relationship of Perry Ellis and Salant | I-6 | |

I-6 | ||

The Merger | I-6 | |

Consideration to be Received by Salant’s Shareholders in the Merger | I-6 | |

Treatment of Salant Stock Options | I-7 | |

Market Price and Dividend Information | I-7 | |

Perry Ellis’ Annual Meeting | I-7 | |

Vote Required for Perry Ellis’ Shareholders to Approve Issuance of Perry Ellis’ Common Stock in the Merger | I-8 | |

Perry Ellis’ Reasons for the Merger | I-8 | |

Recommendation of Perry Ellis’ Directors | I-8 | |

Opinion of Perry Ellis’ Financial Advisor | I-8 | |

Salant’s Special Meeting | I-8 | |

Vote Required for Salant’s Shareholders to Adopt the Merger Agreement | I-9 | |

Salant’s Reasons for the Merger | I-9 | |

Recommendation of Salant’s Directors | I-9 | |

Opinion of Stone Ridge Partners LLC | I-9 | |

Appraisal Rights | I-9 | |

Interests of a Certain Director and Salant’s Executive Officers in the Merger | I-9 | |

Limitations on Salant’s Ability to Consider and Enter Into Other Acquisition Proposals | I-10 | |

Conditions to the Merger | I-11 | |

Termination of the Merger Agreement | I-11 | |

Termination Fee | I-12 | |

Representations and Warranties | I-12 | |

U.S. Federal Income Tax Consequences to Salant’s Shareholders | I-12 | |

Regulatory Approvals | I-12 | |

Financing of the Cash Portion of Merger Consideration | I-12 | |

Effective Time of the Merger | I-13 | |

Comparison of Rights of Perry Ellis’ and Salant’s Shareholders | I-13 | |

Accounting Treatment | I-13 | |

I-14 | ||

Election of Directors of Perry Ellis | I-14 | |

Amendment of Perry Ellis’ Articles of Incorporation to Increase | I-14 | |

Amendment of Perry Ellis’ Articles of Incorporation to Increase | I-15 | |

Amendment of Perry Ellis’ Articles of Incorporation to Eliminate Shareholder | I-15 | |

Amendment of Perry Ellis’ Articles of Incorporation to Require Advance Notice and Disclosure Procedures for Nomination of Perry Ellis’ Directors | I-15 | |

Amendment of Perry Ellis’ Articles of Incorporation to Provide for 66 2/3% Voting Requirements | I-15 |

(i)

Table of Contents

Amendment of Perry Ellis’ 2002 Stock Option Plan | I-16 | |

Ratification of Appointment of Independent Auditors | I-16 | |

Risk Factors | I-17 | |

Where You Can Find More Information | I-17 | |

I-18 | ||

Salant’s Shareholders | I-18 | |

Risks Related to the Merger | I-18 | |

Risks Related to Perry Ellis | I-20 | |

Perry Ellis’ Shareholders | I-24 | |

Risks Related to the Merger | I-24 | |

Risks Related to Perry Ellis | I-26 | |

I-27 | ||

Comparative Market Price Information | I-28 | |

I-29 | ||

I-31 | ||

SELECTED UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL DATA | I-33 | |

I-34 | ||

II-1 | ||

II-1 | ||

II-1 | ||

General | II-1 | |

Date, Time and Place of the Annual Meeting | II-1 | |

Purpose of the Annual Meeting | II-1 | |

Record Date For The Annual Meeting | II-2 | |

Vote Required For Adoption of Proposals | II-2 | |

Proxies | II-3 | |

Solicitation of Proxies | II-4 | |

People with Disabilities | II-5 | |

Stock Certificates | II-5 | |

II-5 | ||

Approval of the Issuance of up to 3,250,000 Shares of Perry Ellis’ Common Stock to Salant’s | II-5 | |

II-6 | ||

General | II-6 | |

Date, Time and Place of the Special Meeting | II-6 | |

Purpose of the Special Meeting | II-6 | |

Recommendation of Salant’s Directors | II-6 | |

Record Date For the Special Meeting | II-6 | |

Vote Required | II-6 | |

Proxies | II-7 | |

Solicitation of Proxies | II-8 | |

People with Disabilities | II-8 | |

Stock Certificates | II-8 | |

III-1 | ||

III-1 | ||

History | III-1 | |

The Perry Ellis License | III-2 |

(ii)

Table of Contents

Background of the Merger | III-3 | |

Perry Ellis’ Reasons for the Merger and Factors Considered by Perry Ellis’ Board | III-17 | |

Recommendation of the Perry Ellis Board of Directors | III-18 | |

Opinion of Sawaya Segalas & Co., LLC | III-19 | |

Salant’s Reasons for the Merger and Factors Considered by Salant’s Board | III-28 | |

Recommendation of Salant’s Board of Directors | III-31 | |

Opinion of Stone Ridge Partners LLC | III-31 | |

Certain Financial Forecasts | III-40 | |

Shareholder Approval in Connection With the Merger | III-42 | |

Interests of a Certain Director and Executive Officers of Salant in the Merger | III-42 | |

Effective Time of the Merger | III-50 | |

Structure of the Merger and Conversion of Salant’s Common Stock | III-50 | |

Fractional Shares | III-52 | |

Certain Adjustments | III-52 | |

Exchange of Salant Stock Certificates for Perry Ellis Stock Certificates | III-53 | |

Treatment of Salant Stock Options | III-53 | |

Material U.S. Federal Income Tax Consequences of the Merger | III-54 | |

Accounting Treatment | III-55 | |

Appraisal Rights | III-56 | |

Financing of Cash Portion of Merger Consideration | III-59 | |

Management of Perry Ellis after the Merger | III-59 | |

Conduct of Salant’s Business if the Merger is not Completed | III-59 | |

Regulatory Approvals | III-60 | |

Antitrust | III-60 | |

Relationships between Perry Ellis and Salant | IIII-60 | |

Other Effects of the Merger | IIII-60 | |

Shares Eligible for Future Sale | IIII-61 | |

IV-1 | ||

IV-1 | ||

IV-1 | ||

General | IV-1 | |

Representations and Warranties | IV-1 | |

Certain Covenants | IV-4 | |

Limitations on Salant’s Ability to Consider and Enter Into Other Acquisition Proposals | IV-6 | |

Additional Covenants | IV-9 | |

Indemnification and Insurance | IV-10 | |

Conditions to Completion of the Merger | IV-10 | |

Termination of the Merger Agreement | IV-11 | |

Termination Fee | IV-12 | |

Amendment, Extension and Waiver | IV-12 | |

Related Matters After the Merger | IV-13 | |

IV-14 | ||

IV-15 | ||

Affiliate Agreements | IV-15 | |

No-Solicitation/No-Hire Agreements | IV-15 | |

Letter Agreements | IV-16 | |

Rights Agreement Amendment | IV-16 |

(iii)

Table of Contents

V-1 | ||

V-1 | ||

V-2 | ||

UNAUDITED PRO FORMA CONDENSED COMBINED STATEMENT OF OPERATIONS | V-3 | |

NOTES TO UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL DATA | V-4 | |

VI-1 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | VI-1 | |

VI-1 | ||

Overview | VI-1 | |

Recent Developments | VI-2 | |

Recent Accounting Pronouncements | VI-3 | |

Critical Accounting Policies | VI-6 | |

Items Affecting Comparability of Fiscal 2002 Period | VI-7 | |

Results of Operations | VI-8 | |

Liquidity and Capital Resources | VI-10 | |

Contractual Obligations and Commercial Commitments | VI-14 | |

Derivatives Financial Instruments | VI-14 | |

Effects of Inflation and Foreign Currency Fluctuations | VI-15 | |

Forward Looking Statements | VI-15 | |

Quantitative and Qualitative Disclosures About Market Risk | VI-15 | |

VI-18 | ||

Overview | VI-18 | |

Results of Operations | VI-18 | |

Liquidity and Capital Resources | VI-21 | |

Critical Accounting Policies and Estimates | VI-25 | |

New Accounting Standards | VI-26 | |

Seasonality | VI-27 | |

Backlog | VI-28 | |

Factors that May Affect Future Results and Financial Condition | VI-28 | |

Quantitative and Qualitative Disclosures About Market Risk | VI-29 | |

VII-1 | ||

VII-1 | ||

VII-1 | ||

Overview | VII-1 | |

Recent Developments | VII-2 | |

Competitive Strengths | VII-3 | |

Business Strategy | VII-5 | |

Brands | VII-8 | |

Other Markets | VII-9 | |

Products and Product Design | VII-10 | |

Marketing and Distribution | VII-11 | |

Licensing Operations | VII-12 | |

Customers | VII-13 | |

Seasonality and Backlog | VII-13 | |

Supply of Products and Quality Control | VII-14 | |

Import and Import Restrictions | VII-15 | |

Competition | VII-15 | |

Trademarks | VII-16 | |

Employees | VII-16 |

(iv)

Table of Contents

Properties | VII-16 | |

Legal Proceedings | VII-17 | |

Management | VII-17 | |

Corporate Governance | VII-18 | |

Meetings and Committees of the Board of Directors | VII-19 | |

Executive Compensation | VII-20 | |

Summary Compensation Table | VII-20 | |

Option Grants in Last Fiscal Year | VII-21 | |

Stock Options Held at End of Fiscal 2003 | VII-21 | |

Equity Compensation Plan Information for Fiscal 2003 | VII-22 | |

Compensation of Directors | VII-22 | |

Employment Agreements | VII-23 | |

Compensation Committee Report on Executive Compensation | VII-23 | |

Compensation Committee Interlocks and Insider Participation | VII-24 | |

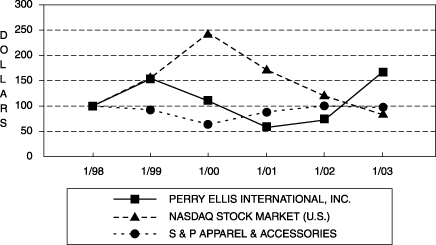

Performance Graph | VII-25 | |

Report of the Audit Committee of the Board of Directors | VII-25 | |

Audit and Non-Audit Fees | VII-26 | |

Certain Transactions | VII-26 | |

Compliance with Section 16(a) of the Securities Exchange Act of 1934 | VII-27 | |

VII-27 | ||

Introduction | VII-27 | |

Men’s Apparel—Wholesale | VII-28 | |

Retail Outlet Operations | VII-28 | |

Significant Customers | VII-28 | |

Trademarks | VII-28 | |

Trademarks Licensed to Salant | VII-29 | |

Design and Production | VII-29 | |

Raw Materials | VII-29 | |

Working Capital | VII-30 | |

Competition | VII-30 | |

Environmental Regulations | VII-30 | |

Seasonality of Business and Backlog of Orders | VII-30 | |

Employees | VII-30 | |

Properties | VII-30 | |

Legal Proceedings | VII-31 | |

Management | VII-31 | |

Executive Compensation | VII-32 | |

Employment Contracts; Termination of Employment and Change-of-Control Arrangements | VII-32 | |

VIII-1 | ||

SECURITY OWNERSHIP OF PRINCIPAL BENEFICIAL OWNERS AND MANAGEMENT | VIII-1 | |

Perry Ellis | VIII-1 | |

Salant | VIII-4 | |

Perry Ellis (Immediately Following the Merger) | VIII-6 | |

IX-1 | ||

IX-1 | ||

Florida Statutory Anti-Takeover Provisions | IX-2 | |

Anti-Takeover Provisions of Perry Ellis’ Articles of Incorporation | IX-4 | |

Indemnification Provisions | IX-5 | |

X-1 | ||

X-1 |

(v)

Table of Contents

XI-1 | ||

COMPARISON OF RIGHTS OF PERRY ELLIS’ AND SALANT’S SHAREHOLDERS | XI-1 | |

XII-1 | ||

XII-1 | ||

XII-1 | ||

Election of Directors | XII-1 | |

Proposed Amendments to Perry Ellis’ Articles of Incorporation | XII-2 | |

XII-3 | ||

Amendment of Perry Ellis’ Articles of Incorporation to Increase Authorized Common Stock | XII-3 | |

XII-4 | ||

Amendment of Perry Ellis’ Articles of Incorporation to Increase Authorized Preferred Stock | XII-4 | |

XII-5 | ||

Amendment of Perry Ellis’ Articles of Incorporation to Eliminate Shareholder Action By Written Consent | XII-5 | |

XII-6 | ||

Amendment of Perry Ellis’ Articles of Incorporation to Require Advance Notice and Disclosure Procedures for Nomination of Directors | XII-6 | |

XII-8 | ||

Amendment of Perry Ellis’ Articles of Incorporation to Provide for 66 2/3% Voting Requirements to Effect Certain Future Article Amendments | XII-8 | |

XII-9 | ||

Amendment of Perry Ellis’ 2002 Stock Option Plan | XII-9 | |

XII-15 | ||

Ratification Appointment of Independent Auditors | XII-15 | |

Other Matters | XII-15 | |

XIII-1 | ||

CERTAIN LEGAL INFORMATION AND ADDITIONAL INFORMATION FOR SHAREHOLDERS | XIII-1 | |

Legal Matters | XIII-1 | |

Experts | XIII-1 | |

Shareholder Proposals | XIII-1 | |

Where You Can Find More Information | XIII-2 | |

Special Note Regarding Forward-Looking Statements | XIII-2 | |

F-1 |

Agreement and Plan of Merger, dated as of February 3, 2003, by and among Perry Ellis, Connor Acquisition Corp. and Salant | A-1 | |||||

Voting Agreement | B-1 | |||||

Opinion of Sawaya Segalas & Co., LLC | C-1 | |||||

Opinion of Stone Ridge Partners LLC | D-1 | |||||

DGCL Appraisal Rights Statute | E-1 | |||||

Articles of Amendment to Articles of Incorporation of Perry Ellis International, Inc. | F-1 | |||||

Amended and Restated Perry Ellis International, Inc. 2002 Stock Option Plan | G-1 | |||||

Perry Ellis International, Inc. Audit Committee Charter | H-1 |

(vi)

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE MEETINGS

| 1. Q: | What is the proposed merger? |

| A: | On February 3, 2003, Perry Ellis and Salant signed a merger agreement which provides for the merger of a wholly owned Perry Ellis subsidiary into Salant. Upon completion of the merger Salant will become a direct wholly owned subsidiary of Perry Ellis. In the merger, Perry Ellis will issue a combination of cash and shares of Perry Ellis’ common stock in exchange for all outstanding shares of Salant’s common stock and options to purchase Salant’s common stock. |

| 2. Q: | Can Salant’s shareholders elect the form of merger consideration they receive in the merger? |

| A: | No, you will receive a fixed amount of cash and shares of Perry Ellis’ common stock having a total value of approximately $9.37 as provided in the merger agreement. |

| 3. Q: | How and when will Salant’s shareholders find out how many shares of Perry Ellis’ common stock and how much cash they will receive in the merger? |

| A: | Perry Ellis and Salant intend to hold their respective shareholder meetings on June 17, 2003, and intend to close the proposed merger within two business days after that date. Accordingly, Perry Ellis and Salant intend to calculate and publicly announce the exchange ratio as of the close of business on June 16, 2003, the trading day immediately prior to the date of Perry Ellis’ and Salant’s shareholder meetings. Perry Ellis and Salant also intend to announce the exchange ratio at their respective shareholder meetings prior to the taking of any votes—to enable you to determine how many shares of Perry Ellis’ common stock and how much cash you will receive in the merger. |

| Therefore, if you submit a proxy before June 16, 2003, you may not know the precise number of shares of Perry Ellis’ common stock you will receive in the merger at the time you vote. |

| 4. Q: | What steps must I follow to vote? |

| A: | Perry Ellis’ shareholders. You may vote in person at Perry Ellis’ annual meeting or by proxy without attending the annual meeting. |

| Salant’s shareholders. You may vote in person at Salant’s special meeting or by proxy without attending the special meeting. |

| 5. Q: | What should I do now? |

| A: | Perry Ellis’ shareholders. After you have carefully read this document and whether or not you plan to attend Perry Ellis’ annual meeting, complete, sign, date and mail your proxy card in the enclosed return envelope as soon as possible. That way, your shares can be represented at Perry Ellis’ annual meeting. |

| Salant’s shareholders. After you have carefully read this document and whether or not you plan to attend Salant’s special meeting, complete, sign, date and mail your proxy card in the enclosed return envelope as soon as possible. That way, your shares can be represented at Salant’s special meeting. |

| 6. Q: | What if my shares are held in “street name”? |

| A: | Shares held in “street name” are shares held in brokerage accounts or held by other nominees on your behalf. If your shares are held in “street name”, you will receive a voter information form from your broker or nominee. You should follow the instructions |

I-1

Table of Contents

provided on the voter information form regarding how to instruct your broker or nominee to vote your shares. |

| 7. Q: | Can I change my vote after I mail my signed proxy? |

| A: | Perry Ellis’ shareholders. Yes, you can revoke your proxy at any time before votes at the annual meeting are tabulated by sending a written notice revoking the proxy or completing and submitting a new proxy having a later date to Perry Ellis at its address set forth in question 17 below, or by attending Perry Ellis’ annual meeting and voting in person. |

| Attendance at Perry Ellis’ annual meeting will not in and of itself constitute revocation of a proxy. |

| Salant’s shareholders. Yes, you can revoke your proxy at any time before votes at the special meeting are tabulated by sending a written notice revoking the proxy or completing and submitting a new proxy having a later date to Salant at its address set forth in question 17 below, or attending Salant’s special meeting and voting in person. |

| Attendance at Salant’s special meeting will not in and of itself constitute revocation of a proxy. |

| 8. Q: | How will votes be counted at Perry Ellis’ annual meeting? |

| A: | Votes cast by proxy or in person at the annual meetingwill be counted by the persons appointed by Perry Ellis to act as inspectors of election. The attendance, in person or by proxy, of the holders of a majority of the outstanding shares of Perry Ellis’ common stock entitled to vote at the annual meeting is necessary to constitute a quorum. |

| If you send back a proxy card but withhold authority to vote for a nominee for election as a director by marking the appropriate box, your shareswill be counted for purposes of determining whether a quorum is present, butwill not be counted as votescast“FOR” the election of such nominee. If you send back a proxy card but abstain from voting on any proposal by marking the abstention box, your shareswill be counted in determining whether a quorum is present, butwill not be counted as votes cast“FOR” or“AGAINST”such proposal. |

| If your shares are held in “street name”, and you do not instruct your broker or nominee how to vote your shares, your broker or nominee has discretionary authority to vote only on matters that are determined to be “routine,” such as the election of directors and ratification of independent auditors,but not on any other proposal (so-called “broker non-votes”). Broker non-voteswill be counted in determining whether a quorum is present, butwould not be considered entitled to vote on any of the proposals to be voted on at Perry Ellis’ annual meeting except the election of Perry Ellis’ three directors and the ratification of the appointment of Deloitte & Touche LLP as Perry Ellis’ independent auditors. |

| Abstentions and broker non-votes will have no effect for purposes of determining whether the separate proposals to be voted on at Perry Ellis’ annual meeting have received sufficient votes for approval with one exception: both abstentions and broker-non voteswill have the same effect as votes cast“AGAINST” the proposal to amend Perry Ellis’ articles of incorporation to require the affirmative vote of the holders of 66 2/3% of Perry Ellis’ outstanding common stock to effect certain future potential amendments to the articles. |

| 9. Q: | How will votes be counted at Salant’s special meeting? |

| A: | Votes cast by proxy or in person at the special meetingwill be counted by the persons appointed by Salant to act as inspectors of election. The attendance, in person or by proxy, of the holders of a majority of the outstanding shares of Salant’s common stock entitled to vote at the special meeting is necessary to constitute a quorum. |

I-2

Table of Contents

| Abstentions and broker non-voteswill have the same effect as a vote“AGAINST” the proposal to adopt the merger agreement. |

| 10. Q: | What if I do not vote at all? |

| A: | Perry Ellis’ shareholders. If you fail to send back a proxy card or vote at the annual meeting, your shareswill not be counted for any purpose, including in determining whether a quorum is present. |

| If you send back a proxy card and do not check any of the voting choice boxes, your shareswill be voted “FOR” the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger and “FOR” each of the other separate proposals to be voted on at the annual meeting. |

| Salant’s shareholders. If you fail to send back a proxy card or vote at the special meeting, your shareswill not be counted for any purpose, including in determining whether a quorum is present. |

| If you send back a proxy card and do not check any of the voting choice boxes, your proxywill be counted as a vote “FOR” adoption of the merger agreement. |

| 11. Q: | Should Salant’s shareholders send in their stock certificates now? |

| A: | No, please do not send us your stock certificates now. Perry Ellis’ exchange agent, Continental Stock Transfer & Trust Company, will send you written instructions on how to surrender your stock certificates for exchange after the merger is completed. |

| 12. Q: | Will Perry Ellis’ common stock received by Salant’s shareholders be listed? |

| A: | Yes. The shares of Perry Ellis’ common stock received by Salant’s shareholders will be listed on The Nasdaq Stock Market under the symbol “PERY”. |

| 13. Q: | I am a shareholder of Salant. If the merger occurs, when will I receive my cash and shares of Perry Ellis’ common stock? |

| A: | If the merger is completed, you will receive cash and shares of Perry Ellis’ common stock promptly after Continental Stock Transfer & Trust Company receives from you a properly completed letter of transmittal together with your Salant stock certificates or, if you do not own any physical Salant stock certificates, promptly after Perry Ellis receives your completed letter of transmittal and electronic transfer of your shares of Salant’s common stock to Perry Ellis’ account. |

| 14. Q: | How and when will I know whether the merger has been completed? |

| A: | If the merger is completed, Perry Ellis and Salant will issue a press release immediately after the closing indicating this and you will receive notice by mail. |

| Perry Ellis and Salant anticipate that if the required shareholder approvals are obtained and the other conditions to the merger are satisfied or, where legally permitted, waived, the merger will close within two business days after June 17, 2003, the date of Perry Ellis’ annual meeting and Salant’s special meeting. |

| 15. Q: | Who is paying for the costs of this solicitation and the preparation of this document? |

| A: | Perry Ellis and Salant are paying the costs of this solicitation, and Salant and Perry Ellis are sharing equally the fees and expenses associated with the preparation, filing and mailing of this document. |

| 16. Q: | Are there any important risks about the merger transaction that we should be aware of? |

| A: | Yes. There are very important risks involved. Before making any decision on |

I-3

Table of Contents

whether and how to vote, we urge you to read very carefully and in its entirety “Chapter I—Risk Factors” beginning on page I-18. |

| 17. Q: | Who should I contact if I have more questions about the merger? |

| A: | Shareholders of both Perry Ellis and Salant may contact: |

| D.F. King & Co., Inc. |

| 48 Wall Street |

| New York, New York 10005 |

| Call toll free: 800-769-7666 |

| Fax: 212-809-8839 |

| Attention: Richard Grubaugh |

| Please refer to the “Perry Ellis-Salant merger” when making any oral or written request to D.F. King. |

| Additionally, shareholders of Perry Ellis may contact: |

| Perry Ellis International, Inc. |

| 3000 N.W. 107th Avenue |

| Miami, Florida 33172 |

| (305) 592-2830 (phone) |

| (305) 406-0505 (fax) |

| Attention: Rosemary Trudeau |

| Shareholders of Salant may contact: |

| Salant Corporation |

| 1114 Avenue of the Americas |

| New York, New York 10036 |

| (212) 221-7500 (phone) |

| (212) 536-5870 (fax) |

| Attention: Awadhesh K. Sinha |

| 18. Q: | Where can I learn more information about Perry Ellis and Salant? |

| A: | To learn more information about Perry Ellis and Salant see “Chapter XIII—Certain Legal Information and Additional Information for Shareholders—Where You Can Find More Information,” on page XIII-2 of this document. |

I-4

Table of Contents

This summary highlights the information contained elsewhere in this document but may not contain in this section all of the information that is important to you. Therefore, you should read this entire document and the other documents referred to herein very carefully to understand fully the proposed merger transaction and all of the other important matters described in this document.

The merger agreement is attached asAnnex A to this document. Perry Ellis and Salant encourage you to read the merger agreement carefully and in its entirety because it is the document that contains and governs all of the legal terms and conditions of the merger and the transactions contemplated thereby.

Page references included in the parentheses below refer you to the more detailed descriptions of topics presented in this summary which are contained elsewhere in this document.

References in this document to Perry Ellis include its consolidated subsidiaries, and references in this document to Salant include its consolidated subsidiaries.

Unless otherwise stated, certain information concerning beneficial ownership of Perry Ellis’ shareholders after completion of the merger gives effect to the issuance of a maximum of 3,250,000 shares of Perry Ellis’ common stock in the merger, and assumes that the 20-consecutive trading day average closing price of Perry Ellis’ common stock will be $12.00 per share and that the exchange ratio in the merger will be 0.3346.

The Companies (Page VII-1)

Perry Ellis International, Inc.

3000 N.W. 107th Avenue

Miami, Florida 33172

(305) 592-2830

Perry Ellis is a leading designer, marketer and licensor of a broad line of high quality men’s sportswear, including casual and dress casual shirts, golf sportswear, sweaters, casual dress pants and shorts, jeanswear, activewear and swimwear to all levels of retail distribution. In fiscal 2003, Perry Ellis began designing, marketing and licensing women’sand junior’s swimwear. Perry Ellis licenses its trademark portfolio domestically and internationally to third parties for apparel and various other products that it does not sell, including men’s and women’s footwear and men’s suits, underwear, loungewear, activewear, outerwear, fragrances and accessories. Perry Ellis has built its broad portfolio of brands through selective acquisitions and establishing its own brands over its 36-year operating history. Its distribution channels include regional, national and international upscale department stores, national and regional chain stores, mass merchants, specialty stores and corporate wear distributors throughout the U.S., Puerto Rico and Canada.

Salant Corporation

1114 Avenue of the Americas

New York, New York 10036

(212) 221-7500

Salant was incorporated in Delaware in 1987, is the successor to a business founded in 1893 and was incorporated in New York in 1919. Salant designs, produces, imports and markets to retailers throughout the U.S. brand name and private label menswear apparel products. Salant currently sells its products to department stores, specialty stores, major discounters and national chains throughout the U.S. Salant also operates 38 retail outlet stores in various parts of the U.S. Salant operates in the men’s apparel wholesale and the retail outlet operations segments.

On May 11, 1999, the U.S. Bankruptcy Court confirmed Salant’s plan of reorganization under Chapter 11 of the U.S. Bankruptcy Code to implement the restructuring of Salant’s 10 1/2% senior secured notes due December 31, 1998 and to establish the capitalization, management structure and equity ownership of Salant.

Previously, Salant had filed two voluntary petitions for relief under Chapter 11 of the U.S. Bankruptcy Code: one in February 1985, with a plan of reorganization confirmed by the U.S. Bankruptcy Court in March 1987, and the other in June 1990, with a plan of reorganization confirmed by the U.S. Bankruptcy Court in July 1993.

I-5

Table of Contents

Connor Acquisition Corp.

c/o Perry Ellis International, Inc.

3000 N.W. 107th Avenue

Miami, Florida 33172

(305) 592-2830

Connor Acquisition Corp. is a direct wholly owned subsidiary of Perry Ellis that was incorporated in Delaware on December 16, 2002 for the sole purpose of effecting the proposed merger with Salant. Connor Acquisition Corp. has not conducted any operations other than in connection with the proposed merger. Because of this, when we discuss the merger in this document, we generally refer only to Perry Ellis.

Historical Business Relationship of Perry Ellis and Salant (Page III-1)

Perry Ellis licenses the Perry Ellis trademarks to Salant covering men’s sportswear, dress shirts, bottoms, belts, suspenders and outlet stores in the U.S. under exclusive license agreements expiring on December 31, 2015, if the licenses are effective for their maximum terms (collectively, the “Perry Ellis Licenses”). Approximately 65% of Salant’s net sales for its 2002 fiscal year, and approximately 55% of Salant’s net sales for its fiscal quarter ended March 29, 2003, were attributable to products sold under the licensed Perry Ellis trademarks. Approximately 19.9% of Perry Ellis’ licensing revenue for its 2003 fiscal year was attributable to royalty payments made by Salant under the Perry Ellis Licenses. Salant is Perry Ellis’ largest licensee.

This section of the summary highlights all of the important information relating to the merger. It also describes the proposals relating to the merger to be voted on at Perry Ellis’ annual meeting and Salant’s special meeting. The other separate and independent proposals to be voted on at Perry Ellis’ annual meeting are described in a separate section of this summary under the heading “Important Non-Merger Proposals Which Perry Ellis’ Shareholders Will be Asked to Vote on at Perry Ellis’ Annual Meeting.”

The Merger (Page III-1)

Perry Ellis, Salant and Connor Acquisition Corp. signed a merger agreement on February 3, 2003 providing for the merger. In the merger, Connor Acquisition Corp. will merge into Salant, Salant will become a direct wholly owned subsidiary of Perry Ellis, and Salant’s shareholders will become shareholders of Perry Ellis.

Consideration to be Received by Salant’s Shareholders in the Merger (Page III-50)

The aggregate consideration to be paid by Perry Ellis in the merger will be $91.0 million, comprised of approximately $52.0 million in cash and approximately $39.0 million worth of Perry Ellis’ common stock.

Each share of Salant’s common stock will be converted in the merger into the right to receive approximately $9.37 in total value, comprised of not less than $5.35 in cash and not more than approximately $4.02 worth of Perry Ellis’ common stock.

The precise fraction of a share of Perry Ellis’ common stock that you will receive in the merger for each share of Salant’s common stock that you own will be determined based on the average closing price of Perry Ellis’ common stock reported on The Nasdaq Stock Market for the 20-consecutive trading days ending on the third full trading day prior to the merger closing date.

If you submit a proxy before that time, you may not know the precise number of shares of Perry Ellis’ common stock you will receive in the merger at the time you vote. However, you will always receive approximately $9.37 in total value for each share of Salant’s common stock you own, no matter what the 20-day average closing price of the Perry Ellis common stock is and irrespective of the fraction of a share of Perry Ellis’ common stock issued to you.

Salant’s shareholders are urged to calculate the 20-day average closing price of Perry Ellis’ common stock by obtaining current market quotations of Perry Ellis’ common stock on Nasdaq prior to making any decision whether and how to vote their shares to determine the number of shares that would be issued in the merger as of the time you submit your proxy.

I-6

Table of Contents

If Perry Ellis’ 20-day average price is $12.00 or less, you will receive 0.3346 of a share of Perry Ellis’ common stock, and if such average price is less than $12.00, the cash portion of the merger consideration will be increased as necessary to provide the approximately $9.37 total per share value you are entitled to receive in the merger.

On May 16, 2003, the last trading day before the date of this joint proxy statement–prospectus, Perry Ellis’ common stock closed at $20.07 per share on The Nasdaq Stock Market. If, hypothetically, this were the average closing price of Perry Ellis’ common stock for the 20-day period described above, you would be entitled to receive 0.2001 of a share of Perry Ellis’ common stock plus approximately $5.35 in cash for each share of Salant’s common stock you own.

Please see “Chapter III—The Merger—Structure of the Merger and Conversion of Salant’s Common Stock” on page III-50 of this document for a table that illustrates how the merger consideration would be issued assuming various hypothetical Perry Ellis 20-day average closing prices. Please see “Chapter II—Information About the Meetings—Perry Ellis’Annual Meeting—Proxies”and “—Salant’s Special Meeting—Proxies” for a discussion on how to revoke your proxies.

Treatment of Salant Stock Options (Page III-53)

Salant has obtained option cancellation agreements from each holder of outstanding “in-the-money” options to purchase Salant’s common stock under which, at the effective time of the merger, (a) all such options will vest and become immediately exercisable, (b) the options will be surrendered for cancellation, and (c) such holder will receive for each surrendered option an amount equal to the excess of approximately $9.37 over the then applicable exercise price of the surrendered options, multiplied by the number of shares of Salant’s common stock subject to each surrendered option. This amount will be paid in cash and shares of Perry Ellis’ common stock ratably and in the same proportion in which the merger consideration is paid to Salant’s shareholders in the merger.

In addition, each optionholder will have the option to pay withholding taxes payable with respect to the surrender and cancellation of his or her options by surrendering shares of Perry Ellis’ common stock of a value equal to the withholding tax.

As of May 14, 2003, options to purchase 915,277 shares of Salant’s common stock were outstanding under Salant’s 1999 Stock Award and Incentive Plan, exercisable at prices ranging from $1.64 per share to $4.125 per share. Accordingly, all of these options were “in the money” in relation to the approximately $9.37 per share of merger consideration.

Market Price and Dividend Information (Page I-28)

Perry Ellis’ common stock is listed on The Nasdaq Stock Market under the symbol “PERY”, and Salant’s common stock is traded on the Over-the-Counter Bulletin Board under the symbol “SLNT.” On May 16, 2003, the closing price of Perry Ellis’ common stock was $20.07, and the closing price of Salant’s common stock was $9.22. Neither Perry Ellis nor Salant pays dividends and neither contemplate doing so in the near future. Each of Perry Ellis’ and Salant’s existing credit facilities prohibit each from paying cash dividends.

Perry Ellis’ Annual Meeting (Page II-1)

Perry Ellis’ annual meeting will be held at Le Parker Meridien Hotel, 119 W. 56th Street, New York, New York 10019, on June 17, 2003, at 11:00 a.m., New York City time. The record date for Perry Ellis’ annual meeting is the close of business on May 14, 2003. Only Perry Ellis’ shareholders of record on that date are entitled to notice of and to vote at Perry Ellis’ annual meeting.

At the annual meeting, Perry Ellis’ shareholders will be asked to vote to approve the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger.

See“Important Non-Merger Proposals Which Perry Ellis’ Shareholders Will be Asked to Vote on at Perry Ellis’ Annual Meeting” below in this summary for a description of the other important separate proposals to be voted on at Perry Ellis’ annual meeting.

Perry Ellis’ annual meeting may be adjourned or postponed to another time and/or place for the purpose of, among other things, permitting dissemination of information regarding material developments relating to the merger, or permitting further solicitation of proxies by Perry Ellis’ board of

I-7

Table of Contents

directors. If Perry Ellis’ shareholders are asked to vote on a proposal to adjourn or postpone the annual meeting to permit solicitation of additional proxies, approval of that proposal will require the affirmative vote of holders of a majority of the votes cast at Perry Ellis’ annual meeting in person or by proxy. However, no proxy which is voted against the proposal to approve the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger will be voted to adjourn or postpone the annual meeting to permit further solicitation of proxies for that proposal.

Vote Required for Perry Ellis’ Shareholders to Approve Issuance of Perry Ellis’ Common Stock in the Merger (Page III-42)

Approval of the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger requires the affirmative vote of a majority of the votes cast on that proposal at Perry Ellis’ annual meeting in person or by proxy.

Perry Ellis’ chairman and chief executive officer, its president and chief operating officer, and certain of their affiliates, have agreed with Salant to vote all of their shares of Perry Ellis’ common stock in favor of the issuance of Perry Ellis’ common stock in the merger. On May 14, 2003, these shares represented in the aggregate approximately 49.6% of Perry Ellis’ outstanding common stock.

In addition, each of the other directors and executive officers of Perry Ellis has indicated his or her intent to vote all shares of Perry Ellis’ common stock he or she holds in favor of the issuance of Perry Ellis’ common stock in the merger. On May 14, 2003, Perry Ellis’ directors and executive officers collectively beneficially owned approximately 56.0% of Perry Ellis’ outstanding common stock.

Perry Ellis’ Reasons for the Merger (Page III-17)

As described in“Chapter III—The Merger—Perry Ellis’ Reasons for the Merger and Factors Considered by Perry Ellis’ Board,”beginning on page III-17 of this document, Perry Ellis’ board of directors considered a variety of factors in determining whether to adopt the merger agreement. No particular weight or rank was assigned to any one of these factors, and Perry Ellis’ board considered all factors as an entirety.

Recommendation of Perry Ellis’ Directors

(Page III-18)

After careful consideration, Perry Ellis’ board unanimously determined that the merger is in the best interests of Perry Ellis and its shareholders, adopted the merger agreement and unanimously recommends that Perry Ellis’ shareholders vote “FOR” approval of the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger.

Opinion of Perry Ellis’ Financial Advisor

(Page III-19)

On December 17, 2002, Perry Ellis’ board engaged Sawaya Segalas & Co., LLC as its financial advisor to evaluate the financial terms of the merger. Sawaya Segalas delivered its written opinion to Perry Ellis’ board stating that, as of February 1, 2003, the proposed consideration to be paid by Perry Ellis in the merger was fair to Perry Ellis, from a financial point of view.

The full text of the written opinion of Sawaya Segalas dated February 1, 2003 is attached as Annex C to this document. You are encouraged to read this opinion carefully and in its entirety.

Salant’s Special Meeting (Page II-6)

Salant’s special meeting will be held at Salant’s executive offices located at 1114 Avenue of the Americas, 36th Floor, New York, New York 10036, on Tuesday, June 17, 2003, at 9:30 a.m., New York City time. The record date for Salant’s special meeting is the close of business on May 14, 2003. Only Salant’s shareholders of record on that date are entitled to notice of and to vote at Salant’s special meeting.

At the special meeting, Salant’s shareholders will be asked to vote to adopt the merger agreement.

Salant’s special meeting may be adjourned or postponed to another time and/or place for the purpose of, among other things, permitting dissemination of information regarding material developments relating to the merger, or permitting further solicitation of proxies by Salant’s board of

I-8

Table of Contents

directors. If Salant’s shareholders are asked to vote on a proposal to adjourn or postpone the special meeting to permit solicitation of additional proxies, approval of that proposal will require the affirmative vote of holders of a majority of the shares of Salant’s common stock present in person or represented by proxy at the special meeting. However, no proxy which is voted against the proposal to adopt the merger agreement will be voted to adjourn or postpone the special meeting to permit further solicitation of proxies for that proposal.

Vote Required for Salant’s Shareholders to Adopt the Merger Agreement (Page III-42)

The affirmative vote of the holders of a majority of the outstanding shares of Salant’s common stock is required for Salant’s shareholders to adopt the merger agreement.

On May 14, 2003, Salant’s directors and executive officers beneficially owned in the aggregate approximately 6.9% of Salant’s outstanding common stock, and they have indicated their intention to vote all of their shares for adoption of the merger agreement.

Salant’s Reasons for the Merger (Page III-28)

As described in“Chapter III—The Merger—Salant’s Reasons for the Merger and Factors

Considered by Salant’s Board,” beginning on page III-28 of this document, Salant’s board of directors considered a variety of factors in determining whether to approve the merger agreement. No particular weight or rank was assigned to any one of these factors, and Salant’s board considered all factors as an entirety.

Recommendation of Salant’s Directors (Page III-31)

After careful consideration, Salant’s board unanimously determined that the merger is fair to and in the best interests of Salant and its shareholders and that the merger agreement is advisable, approved the merger agreement, and unanimously recommends that Salant’s shareholders vote “FOR” adoption of the merger agreement.

Opinion of Stone Ridge Partners LLC (Page III-31)

On October 8, 2002, Salant’s board engaged Stone Ridge Partners LLC as its financial advisor to provide certain financial advisory services and evaluate the financial terms of the merger. Stone Ridge delivered its written opinion to Salant’s board stating that, as of February 3, 2003, the consideration to be received in the merger by the holders of Salant’s common stock, was fair to Salant and such holders, from a financial point of view.

The full text of the written opinion of Stone Ridge Partners LLC dated February 3, 2003 is attached asAnnex D to this document. You are encouraged to read this opinion carefully and in its entirety.

Salant has paid $100,000 to Stone Ridge to date and has agreed to pay Stone Ridge a “success fee” of $1,261,100 upon completion of the merger.

Appraisal Rights (Page III-56)

Perry Ellis’ shareholders have no appraisal rights in the merger.

Under Delaware law, if a Salant shareholder complies with certain statutory procedures he or she will be entitled to appraisal rights and to receive a judicially determined payment in cash for the fair value of his or her shares. A Salant shareholder must vote against or abstain from voting on adoption of the merger agreement to be entitled to appraisal rights.

Please seeAnnex E for the full text of Section 262 of the Delaware General Corporation Law, as amended, which governs the appraisal rights of Salant’s shareholders in the merger.

Interests of a Certain Director and Salant’s Executive Officers in the Merger (Page III-42)

When considering the recommendation of Salant’s board, Salant’s shareholders should be aware that a certain director and Salant’s executive officers have interests in the transaction that are materially

I-9

Table of Contents

different from, or that are in addition to, the interests of Salant’s shareholders. These interests include the following:

| Ÿ | Michael J. Setola, Salant’s chairman and chief executive officer, and Awadhesh K. Sinha, Salant’s chief operating officer and chief financial officer, will receive a cash change-in-control payment of approximately $2.5 million and $630,000, respectively, at the effective time of the merger under the terms of amendments to their respective employment agreements entered into on November 25, 2002 and December 27, 2002, respectively. |

| Ÿ | Certain officers and other employees of Salant, including its chief financial officer, are eligible to receive certain retention bonuses aggregating approximately $1.5 million if they remain employed by Salant for, or if their employment is terminated under certain circumstances within, six months after the closing of the merger. |

| Ÿ | Certain officers and other employees of Salant also may become entitled to receive “enhanced” severance payments aggregating approximately $1.2 million if their employment is terminated under certain circumstances within six months after the closing of the merger. |

| Ÿ | Certain officers and other employees of Salant also may become entitled to receive contractual severance payments aggregating up to approximately $3.7 million if their employment is terminated under certain circumstances either before or after the merger. |

| Ÿ | Unvested options to purchase an aggregate of 30,831 shares of Salant’s common stock held by directors and executive officers of Salant (as well as all other outstanding unvested options) will become fully vested and immediately exercisable at the closing of the merger. |

| Ÿ | Each of Salant’s directors and executive officers will be entitled to continued indemnification by Perry Ellis for five years after completion of the merger to the extent provided in Salant’s existing charter, by-lawsand other contractual arrangements. Perry Ellis has agreed to pay for continued directors’ and officers’ liability insurance for three years after completion of the merger for these persons as well. |

The non-management directors of Salant will not receive any change-in-control, retention, “enhanced” severance or other severance payments by virtue of the merger, and they do not hold any unvested options.

Upon completion of the merger, the non-competition covenants contained in Mr. Setola’s current employment agreement with Salant will terminate and the non-solicitation covenants contained therein will become effective. In addition, Perry Ellis entered into a no-solicitation/no-hire agreement with each of Messrs. Setola and Sinha under which:

| Ÿ | Mr. Setola has agreed, among other things, not to (a) solicit or hire certain employees of Salant in connection with any wholesale or retail manufacturing, distribution, sale or licensing of apparel goods or services for a period of 21 months beginning on the closing date of the merger and (b) take certain actions that may negatively affect Salant’s licensee-licensor relationship with Ocean Pacific Apparel Corp. |

| Ÿ | Mr. Sinha has agreed not to solicit or hire certain employees of Salant in connection with any wholesale or retail manufacturing, distribution, sale or licensing of apparel goods or services for a period of nine months beginning on the closing date of the merger. |

Limitations on Salant’s Ability to Consider and Enter Into Other Acquisition Proposals (Page IV-6)

The merger agreement prohibits Salant from initiating, soliciting or facilitating the receipt or submission of an alternative acquisition proposal. Salant, however, can provide non-public information and enter into discussions and negotiations in response to unsolicited acquisition proposals from third parties who sign a confidentiality agreement, if Salant’s board, in good faith after consultation with

I-10

Table of Contents

its outside counsel and financial advisor, reasonably believes that failing to do so would violate the board’s fiduciary duties under applicable law, and that by doing so there would be a substantial likelihood that Salant would obtain an alternative acquisition proposal having terms superior to the merger with Perry Ellis.

Prior to Salant’s special meeting, Salant’s board can change or withdraw its recommendation that Salant’s shareholders vote to adopt the merger agreement if Salant receives an unsolicited third party acquisition proposal which the board determines, in good faith after consultation with its outside counsel and financial advisor, is financially superior to the merger with Perry Ellis. However, Salant’s directors may do this only if Perry Ellis does not match the terms of the superior deal within seven business days. If Salant’s board changes or withdraws its recommendation and, as a result, Perry Ellis elects to terminate the merger agreement, Salant must pay Perry Ellis the $3,680,000 termination fee described below in “Termination Fee.”

After, and only after, Salant’s special meeting, Salant can terminate the merger agreement and enter into a definitive agreement for an unsolicited third party acquisition proposal that Salant’s board determines, in good faith after consultation with its outside counsel and financial advisor, is financially superior to the merger with Perry Ellis. However, Salant’s directors may do this only if Perry Ellis does not match the terms of the superior deal within seven business days and provided that Salant first pays Perry Ellis the $3,680,000 termination fee described below in “Termination Fee.”

The merger agreement also provides that notwithstanding any change or withdrawal of Salant’s recommendation under the circumstances permitted by the merger agreement, Salant must submit the merger agreement to Salant’s shareholders for their adoption at Salant’s special meeting and cannot terminate the merger agreement because of such changed or withdrawn recommendation.

Conditions to the Merger (Page IV-10)

The obligations of Perry Ellis and Salant to complete the merger are subject to the satisfaction ofa number of mutual and unilateral conditions which are customary for cash and stock acquisitions of public companies such as the merger. Neither Perry Ellis nor Salant presently anticipates waiving any of the conditions to the merger.

Termination of the Merger Agreement (Page IV-11)

The merger may be terminated at any time prior to the completion of the merger, whether or not Salant’s shareholders have adopted the merger agreement or Perry Ellis’ shareholders have approved the issuance of Perry Ellis’ common stock in the merger:

| Ÿ | by the mutual written consent of Perry Ellis and Salant, |

| Ÿ | by either Perry Ellis or Salant, if: |

| — | the merger is not completed by July 31, 2003 (other than because of a breach of the merger agreement caused by the terminating party), |

| — | the merger agreement is not adopted by Salant’s shareholders, |

| — | the issuance of up to 3,250,000 shares of Perry Ellis’ common stock to Salant’s shareholders in the merger is not approved by Perry Ellis’ shareholders, |

| — | a final and nonappealable legal restraint on consummation of the merger is issued, or |

| — | the consent to the merger of a required governmental entity is denied on a final and nonappealable basis, |

| Ÿ | by Perry Ellis, if Salant’s board changes or withdraws its recommendation or Salant fails to call or convene Salant’s special meeting, |

| Ÿ | by Perry Ellis, if Salant breaches any of its representations, warranties, covenants or other agreements in the merger agreement and the breach would result in the failure of a closing condition to be satisfied and is not remedied within 15 days of notice of the breach, |

I-11

Table of Contents

| Ÿ | by Salant after, and only after, its special meeting, if it previously received an unsolicited third party acquisition proposal that Salant’s board determines, in good faith after consultation with its outside counsel and financial advisor, is financially superior to the merger with Perry Ellis, provided Perry Ellis does not match the terms of the superior proposal within seven business days and Salant first pays Perry Ellis the $3,680,000 termination fee described below in “Termination Fee”, or |

| Ÿ | by Salant, if Perry Ellis breaches any of its representations, warranties, covenants or other agreements in the merger agreement and the breach would result in the failure of a closing condition to be satisfied and is not remedied within 15 days of notice of the breach. |

Termination Fee (Page IV-12)

Salant must pay Perry Ellis a $3,680,000 termination fee if any of the following events occurs:

| Ÿ | Perry Ellis terminates the merger agreement because, prior to Salant’s special meeting and under the circumstances permitted by the merger agreement, Salant’s board changes or withdraws its recommendation for Salant’s shareholders to adopt the merger agreement after receiving an unsolicited third party acquisition proposal which Salant’s board determines, in good faith after consultation with its outside counsel and financial advisor, is financially superior to the merger with Perry Ellis, and Perry Ellis does not match within seven business days the terms of the superior proposal, |

| Ÿ | an unsolicited third party acquisition proposal is made or publicly announced prior to Salant’s special meeting and either Salant or Perry Ellis terminates the merger agreement because Salant’s shareholders do not adopt the merger agreement at the special meeting and, within 12 months after the merger agreement is terminated, such third party consummates a takeover proposal for Salant or Salant enters into or publicly announces anagreement to consummate a takeover proposal, or |

| Ÿ | after, and only after, Salant’s special meeting has occurred, Salant terminates the merger agreement with Perry Ellis and enters into or announces a third party acquisition agreement after previously receiving an unsolicited proposal from such third party which Salant’s board determines, in good faith after consultation with its outside counsel and financial advisor, is financially superior to the merger with Perry Ellis, and Perry Ellis does not match within seven business days the terms of the superior proposal. |

If the events described in either the first or third bullet-point above occur, the $3,680,000 termination fee is payable by Salant upon termination of the merger agreement. If the event described in the second bullet-point above occurs, the $3,680,000 termination fee is payable on the earliest to occur of the date the third party takeover proposal is consummated or the date the agreement to consummate a takeover proposal is entered into or publicly announced.

In addition, Salant must pay Perry Ellis a termination fee of $1,840,000, without duplication of the event described in the second bullet-point above, if either Salant or Perry Ellis terminates the merger agreement because Salant’s shareholders do not adopt the merger agreement for any reason whatsoever. In this case, the $1,840,000 termination fee is payable not later than the second business day after termination of the merger agreement.

Representations and Warranties (Page IV-1)

The merger agreement contains various representations, warranties and covenants of the parties customary for cash and stock acquisitions of public companies such as the merger.

U.S. Federal Income Tax Consequences to Salant’s Shareholders (Page III-55)

In general, for U.S. federal income tax purposes:

| Ÿ | You will recognize gain or loss equal to the difference between the fair market value of |

I-12

Table of Contents

the shares of Perry Ellis’ common stock at the time of the merger plus the amount of cash you receive, and your aggregate adjusted tax basis in the shares of Salant’s common stock surrendered in exchange for the merger consideration. |

| Ÿ | Your tax basis of the shares of Perry Ellis’ common stock you receive in the merger will be equal to the fair market value of Perry Ellis’ common stock at the time of the merger. |

| Ÿ | Your holding period of the shares of Perry Ellis’ common stock you receive in the merger will begin at the time of the merger. |

The U.S. federal income tax consequences of the merger to you will depend on your own situation. You should consult your own tax advisors for a full understanding of the tax consequences of the merger to you.

Regulatory Approvals (Page III-60)

Perry Ellis and Salant each filed the required information and forms with the Antitrust Division of the U.S. Department of Justice and the U.S. Federal Trade Commission under the Hart-Scott-Rodino Act on March 14, 2003 and requested an early termination of the statutory waiting period.

On April 1, 2003, Perry Ellis and Salant received notification of early termination of the 30-day statutory waiting period from the U.S. Federal Trade Commission.

Financing of the Cash Portion of Merger Consideration (Page III-59)

Perry Ellis anticipates that the cash portion of the merger consideration to be paid in the merger will be funded from its existing cash reserves and through borrowings under an amended senior credit facility.

Perry Ellis obtained a commitment letter from Congress Financial Corp., a senior lender participant in Perry Ellis’ senior credit facility, to increase the facility to $110.0 million, subject to inventory and accounts receivable borrowing base limitations.

Effective Time of the Merger (Page III-50)

The merger will be completed only if and when all the conditions to completion of the merger are satisfied or, if allowed by law, waived. The merger will become effective when a certificate of merger is filed with the Delaware Secretary of State. Perry Ellis and Salant intend that if the required shareholder approvals are obtained and the other conditions to the merger are satisfied or, where legally permitted, waived, the merger will close within two business days after June 17, 2003, the date on which Perry Ellis’ annual meeting and Salant’s special meeting are held.

Comparison of Rights of Perry Ellis’ and Salant’s Shareholders (Page XI-1)

There are very important differences between the rights of Perry Ellis’ shareholders under Florida corporate law and Perry Ellis’ articles of incorporation and by-laws, and the rights of Salant’s shareholders under Delaware corporate law and Salant’s certificate of incorporation and by-laws. When the merger is completed, Salant’s shareholders will become shareholders of Perry Ellis, and their rights will be governed by Florida corporate law and Perry Ellis’ articles of incorporation and by-laws (instead of Delaware corporate law and Salant’s certificate of incorporation and by-laws).

Accounting Treatment (Page III-55)

For financial reporting purposes, the merger will be accounted for by Perry Ellis as a purchase of Salant.

I-13

Table of Contents

IMPORTANT NON-MERGER PROPOSALS WHICH PERRY ELLIS’ SHAREHOLDERS WILL BE ASKED TO VOTE ON AT PERRY ELLIS’ ANNUAL MEETING

This section discusses the non-merger proposals to be voted on at Perry Ellis’ annual meeting. These proposals are being submitted only to Perry Ellis’ shareholders at Perry Ellis’ annual meting and do not apply to Salant’s shareholders or Salant’s special meeting.

As discussed above, because Perry Ellis’ meeting is an annual meeting, Perry Ellis’ shareholders are also being asked to vote upon the following important additional proposals.

Each of the proposals discussed below will be presented and voted on separately, and the effectiveness of any one of these proposals is not conditioned upon the approval by Perry Ellis’ shareholders of any of the other proposals.

Each of Perry Ellis’ directors and executive officers has indicated his or her intent to vote all shares of Perry Ellis’ common stock he or she holds in favor of each of the proposals discussed below. On May 14, 2003, Perry Ellis’ directors and executive officers beneficially owned in the aggregate approximately 56.0% of the outstanding shares of Perry Ellis’ common stock.

After careful consideration, Perry Ellis’ board of directors has unanimously approved each of the separate proposals discussed below and recommends that Perry Ellis’ shareholders vote “FOR” each of these separate proposals.

Election of Directors of Perry Ellis (Page XII-1)

Perry Ellis’ shareholders are being asked to vote to elect three directors of Perry Ellis, each to serve for a term expiring at Perry Ellis’ 2006 annual meeting of shareholders. Your board of directors has nominated for election: Messrs. Oscar Feldenkreis, Joseph P. Lacher and Allan Zwerner.

A plurality of the votes cast at Perry Ellis’ annual meeting in person or by proxy is required to elect each of the nominees above for election as directors of Perry Ellis.

By “plurality” we mean that the directors who receive the most votes cast “FOR” election to fill the available director seats, even if not a majority of all votes cast, will be elected.

Proposed Amendments to Perry Ellis’

Articles of Incorporation