Included in the above total are contracts related to certain product purchase and licence agreements with deferred consideration obligations, the amounts of which are variable depending upon particular ‘milestone’ achievements. Sales of the products to which these ‘milestones’ relate could give rise to additional payments, contingent upon the sales levels achieved. Guarantees and contingencies arising in the ordinary course of business, for which no security has been given, are not expected to result in any material financial loss.

In 1998, Astra and Merck & Co., Inc restructured their joint venture (the “restructuring”) which had been established some years earlier for the purpose of selling and marketing certain Astra products in the US.

Under the terms of the 1998 restructuring, the merger between Astra and Zeneca in 1999 triggered two one-time payments from AstraZeneca to Merck:

Back to Contents

| 102 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | |

Notes to the Financial Statements continued

34 Assets pledged, commitments and contingent liabilities (continued)

In addition, in 2008 there will be a true up of the Advance Payment. The calculation of this will be based on a multiple of the previous three years’ contingent payments in respect of all the agreement products with the exception of Prilosec and Nexium, plus other defined amounts, which are then reduced by the Appraised Value (whether paid or not), the Partial Redemption and the Advance Payment. This could result in a further payment by AstraZeneca to Merck or a payment by Merck to AstraZeneca.

The precise amount of settlements with Merck under the Partial Redemption and the First Option cannot be determined at this time, as some of the payments are based on calculations based on sales between 2005 and 2007, and another is contingent upon Merck exercising the First Option. However, if Merck does exercise this option, the combined effect will involve a minimum amount payable to Merck in 2008 of approximately $4.7bn. If AstraZeneca exercises this option in 2010, the combined effect will involve a minimum aggregate payable to Merck in 2008 and 2010 of approximately $4.7bn.

Finally, in 2008 Merck will repay to AstraZeneca a loan in the amount of $1.4bn made at the time of the restructuring.

Second Option

A Second Option exists whereby AstraZeneca has the option to re-purchase Merck’s interests in Prilosec and Nexium in the US. This option is exercisable by AstraZeneca two years after the exercise of the First Option in either 2008 or 2010. Exercise of the Second Option by AstraZeneca at a later date is also provided for in 2017 or if combined annual sales of the two products fall below a minimum amount provided, in each case only so long as the First Option has been exercised. The exercise price for the Second Option is the fair value of these product rights as determined at the time of exercise. If the Second Option is exercised, Merck will have no further rights to contingent payments from AstraZeneca.

Environmental costs and liabilities

The Group’s expenditure on environmental protection, including both capital and revenue items, relates to costs which are necessary for meeting current good practice standards and regulatory requirements for processes and products.

They are an integral part of normal ongoing expenditure for maintaining the Group’s manufacturing capacity and product ranges and are not separated from overall operating and development costs. There are no known changes in environmental, regulatory or other requirements resulting in material changes to the levels of expenditure for 2000, 2001 or 2002.

In addition to expenditure for meeting current and foreseen environmental protection requirements, the Group incurs substantial costs in investigating and cleaning up land and groundwater contamination. In particular, AstraZeneca has environmental liabilities at some currently or formerly owned, leased and third party sites in the US and Europe. AstraZeneca, or its indemnitees, have been named under US legislation (the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended) as potentially responsible parties (PRP) in respect of 32 sites (although AstraZeneca expects to be indemnified against liabilities associated with nine of these sites by the seller or owner of the businesses associated with such sites) and, where appropriate, actively participates in or monitors the clean-up activities at sites in respect of which it is a PRP. Stauffer Management Company, a subsidiary of AstraZeneca established in 1987 to own and manage certain assets of Stauffer Chemical Company which was acquired that year, has identified 28 sites (including 18 for which an AstraZeneca indemnitee has been named a PRP) for which it may have responsibility that will, in aggregate, require significant expenditure on clean-up and monitoring.

Liabilities are generally more likely to crystallise where a contaminated site is to be sold, its use changed or where a regulatory authority imposes a particular remedial measure. Costs of these liabilities may be offset by amounts recovered from third parties, such as previous owners of the sites in question or through insurance.

The future level of investigation and clean up costs will depend on a number of factors, including the nature and extent of any contamination that may ultimately be found to exist, the need for and type of any remedial work to be undertaken and the standards required by applicable current and future environmental laws and regulations and the number and financial viability of other PRPs. The relative importance of these factors varies significantly from site to site. Many sites are at different stages in the regulatory process or at different stages in the process of evaluating environmental damage or alternative remediation methods. It is therefore difficult to form meaningful ranges of estimates for such costs.

AstraZeneca had provisions at 31 December 2002 in respect of such costs in accordance with the accounting policies on page 64. Although there can be no assurance, management believes that, taking account of these provisions, the costs of addressing currently identified environmental obligations, as AstraZeneca currently views those obligations, is unlikely to impair materially AstraZeneca’s financial position.

Such contingent costs, to the extent that they exceed applicable provisions, could have a material adverse effect on AstraZeneca’s results of operations for the relevant period.

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | 103 |

Legal proceedings

Losec/Prilosec (omeprazole)

In June 1997, the German Federal Patent Court declared invalid a previously granted supplementary protection certificate which extended protection for omeprazole, the active ingredient contained in Losec, from 1999 to 2003. The decision was appealed and on 1 February 2000, at AstraZeneca’s request, the German Supreme Court decided to refer the case to the European Court of Justice for a preliminary ruling. The court heard the case on 8 November 2001 and its decision is pending. The case does not involve any financial claims.

In March 2000, the German Federal Patent Court declared that AstraZeneca’s formulation patent for omeprazole was invalid. The decision has been appealed to the German Supreme Court. As a consequence, all pending infringement actions in Germany have been stayed awaiting the outcome of the appeal. There is one interlocutory injunction in force against ratiopharm GmbH based on the formulation patent. If the final decision on the validity of the formulation patent goes against AstraZeneca, ratiopharm may claim damages for lost sales due to the interlocutory injunction.

In 1998, Astra filed suits in the US against Andrx Pharmaceuticals, Inc. and Genpharm, Inc. This followed the filing of abbreviated new drug applications by Andrx and Genpharm with the US Food and Drug Administration (FDA) concerning the two companies’ intention to market generic omeprazole products in the US. During 1999, Astra also filed suits against Kremers Urban Development Company and Schwarz Pharma, Inc., and against Cheminor Drugs Ltd., Reddy-Cheminor Inc. and Schein Pharmaceuticals, Inc. During 2000, AstraZeneca filed further suits against Lek Pharmaceutical and Chemical Company d.d, Impax Laboratories Inc., Eon Labs Manufacturing Inc. and Mylan Pharmaceuticals Inc. During 2001, AstraZeneca filed further suits against Torpharm, Inc. and Zenith Goldline Pharmaceuticals, Inc. (Ivax). The basis for the proceedings is that the actions of all the companies infringe several patents relating to omeprazole (Prilosec in the US). The cases are proceeding under the US Hatch-Waxman legislation. AstraZeneca filed additional patent infringement suits during 2001 against Andrx and Genpharm in respect of one other omeprazole patent outside the Hatch-Waxman legislation. The trial against Andrx, Genpharm, Kremers Urban Development Company and Cheminor started in December 2001 and ended in July 2002.

In October 2002, the US District Court for the Southern District of New York ruled that two AstraZeneca patents (‘230 and ‘505) relating to the formulation of omeprazole are valid until 2007, that Andrx, Genpharm and Cheminor all infringed both patents but that Kremers Urban Development Company did not infringe either patent. The court did not rule on the ‘281 patent relating to a manufacturing process for omeprazole formulations in respect of which AstraZeneca has sued Andrx only. AstraZeneca has appealed the judgement with regard to non-infringement and Kremers Urban Development Company. Andrx, Genpharm and Cheminor have appealed the decision with regard to infringement and validity of the patents.

In April 2001, Andrx filed a case in the US District Court for the Southern District of New York against AstraZeneca, Merck & Co., Inc. and the FDA alleging that the listing of certain patents in the FDA’s Orange Book was improper and constituted violations of certain provisions of the Sherman Act, the US federal anti-trust legislation, and a state statute analogous to the federal anti-trust laws. Andrx seeks injunctive relief compelling the parties to delist omeprazole-related patents it claims were improperly listed in the Orange Book and prohibiting the defendants from using patents to delay the effective date of the FDA’s approval of Andrx’s ANDA for omeprazole. AstraZeneca and Merck have filed motions to dismiss the case, which are pending.

AstraZeneca and Merck & Co., Inc. were named as defendants in three class actions; two in the US District Court for the Southern District of New York and one in the US District Court for the District of New Jersey. The plaintiffs are consumers and third party payers who have alleged that they and others who are similarly situated have been forced to pay higher prices for omeprazole as a result of agreements that AstraZeneca and Merck entered into that resulted in ‘unreasonable restraints of trade and competition’. Furthermore, the plaintiffs have alleged that AstraZeneca and Merck engaged in conduct designed to extend their monopoly power ‘beyond the lawful boundaries of their patents’. The plaintiffs are seeking declarative, equitable and injunctive relief enjoining AstraZeneca and Merck from continuing their alleged illegal activities, costs of suit, reasonable attorney’s fees and expenses and any other relief determined by the court. AstraZeneca filed a motion in March 2002 to dismiss the two class actions before the US District Court for the Southern District of New York, which was granted in June 2002. The plaintiffs did not appeal. The plaintiffs voluntarily dismissed the New Jersey case also in June 2002.

In October 2000, the Federal Court of Australia (Full Court) handed down a patent ruling pertaining to omeprazole in connection with a dispute between AstraZeneca and the generic company, Alphapharm Pty Ltd. The court declared that AstraZeneca’s formulation patent was invalid. In November 2001, AstraZeneca applied for special leave to appeal the decision to the High Court of Australia and this application was granted in December 2001. The appeal was heard by the High Court in May 2002 and in December 2002 the High Court reversed the judgement of the lower court. The High Court ruled that AstraZeneca’s formulation patent is valid and that the case should be returned to the lower court for determination of the remaining issues.

During 2000, AstraZeneca was granted interlocutory injunctions based on certain of AstraZeneca’s omeprazole patents and supplementary protection certificates against the generic company, Scandinavian Pharmaceuticals-Generics AB (Scand Pharm), in Sweden, Denmark and Norway. In October 2000, the District Court of Stockholm ruled that Scand Pharm had infringed one of AstraZeneca’s supplementary protection certificates for omeprazole. Scand Pharm has appealed this decision. In October 2001, Oslo City Court in Norway found that Scand Pharm had infringed AstraZeneca’s formulation patent for omeprazole. At the same time, the court declared AstraZeneca’s formulation patent valid. As a result of the Norwegian case, Scand Pharm cannot sell its omeprazole product in Norway, nor can it do so in Sweden or Denmark pending the outcome of the main actions in the cases in these countries. If the final decisions in these cases are against AstraZeneca, Scand Pharm may claim damages for lost sales due to the interlocutory injunctions.

Back to Contents

| 104 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | |

Notes to the Financial Statements continued

34 Assets pledged, commitments and contingent liabilities (continued)

In March 2002, the Patents Court in the UK handed down a ruling invalidating certain of AstraZeneca’s formulation patents for omeprazole. AstraZeneca applied for leave to appeal the decision to the Court of Appeal and this application was granted. The appeal was heard by the Court of Appeal in October 2002 and the court affirmed the original decision of the Patents Court invalidating the formulation patents.

In the Netherlands, Pharmachemie BV has filed a claim against two AstraZeneca companies alleging that AstraZeneca has misused its exclusive rights in the Netherlands in relation to the expiration date for AstraZeneca’s supplementary protection certificate for omeprazole. AstraZeneca denies the allegations and is defending the case.

Other court cases relating to omeprazole patents are pending worldwide. However, the financial impact if AstraZeneca loses is not considered to be material.

In February 2000, the European Commission commenced an investigation relating to certain omeprazole intellectual property rights, and associated regulatory and patent infringement litigation. The investigation is pursuant to Article 82 of the EC Treaty, which prohibits an abuse of a dominant position. The investigation was precipitated by a complaint by a party to a number of patent and other proceedings involving AstraZeneca and relates to a limited number of European countries. AstraZeneca has, in accordance with its corporate policy, co-operated with the Commission. AstraZeneca remains of the view that the complaint is unfounded and that it has complied with all relevant competition laws. In particular, it considers that the matters raised by the complaint are more properly dealt with by the courts in the context of the litigation in which the complainant is involved. The Commission has recently requested certain factual patent and regulatory information from AstraZeneca and AstraZeneca will continue to co-operate with the Commission.

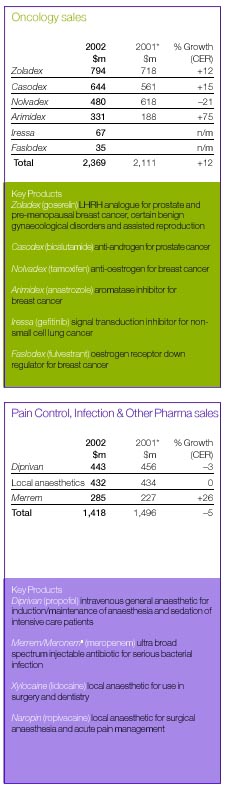

Zoladex (goserelin acetate implant) investigation

The US Department of Justice has been conducting a civil and criminal investigation into the sale and marketing of Zoladex (goserelin acetate implant). The investigation was prompted by the filing of a qui tam complaint by a private party in 1997 and involves allegations of improper submissions of claims to the Medicare and Medicaid programmes. The Company and federal and state authorities are in the process of negotiating a potential settlement of the civil and criminal claims at issue in the investigation. As a result, although no final agreement has been concluded, the Company believes it appropriate to accrue $350m to cover estimated settlement costs.

Plendil (felodipine)

In August 2000, AstraZeneca LP received a letter from Mutual Pharmaceutical Co., Inc. informing AstraZeneca of Mutual’s intention to market a generic version of AstraZeneca’s felodipine extended release tablets (Plendil) prior to the expiration of AstraZeneca’s patent covering the extended release formulation. AstraZeneca filed a patent infringement action against Mutual in the US District Court for the Eastern District of Pennsylvania. Mutual responded and filed counterclaims alleging non-infringement and invalidity. Expert discovery is due to close in March 2003. A trial date has not yet been set.

In May 2001, AstraZeneca Pharmaceuticals LP received a similar letter from Zenith Goldline Pharmaceuticals, Inc. and in July 2001, AstraZeneca filed a patent infringement action against Zenith in the US District Court for the District of New Jersey. Zenith responded and filed counterclaims alleging non-infringement. Fact discovery is due to close in May 2003. A trial date has not yet been set.

Nolvadex (tamoxifen)

AstraZeneca is a co-defendant with Barr Laboratories, Inc. in numerous purported class actions filed in federal and state courts throughout the US. All of the state court actions were removed to federal court and have been consolidated, along with all of the cases originally filed in federal court, in a federal multi-district litigation proceeding pending in the US District Court for the Eastern District of New York. Some of the cases were filed by plaintiffs representing a putative class of consumers who purchased tamoxifen. The other cases were filed on behalf of a putative class of ‘third party payers’ (including health maintenance organisations, insurers and other managed care providers and health plans) that have reimbursed or otherwise paid for prescriptions of tamoxifen. The plaintiffs allege that they paid ‘supra-competitive and monopolistic prices’ for tamoxifen as a result of the settlement of patent litigation between Zeneca and Barr in 1993. The plaintiffs seek injunctive relief, treble damages under the anti-trust laws, disgorgement and restitution. In April 2002, AstraZeneca filed a motion to dismiss the cases for failure to state a cause of action. The court’s decision is awaited.

In August 2002, AstraZeneca’s US distribution agreement with Barr Laboratories, Inc. for non-branded tamoxifen expired, as did AstraZeneca’s patent for Nolvadex (tamoxifen). At the same time, a six month period of market exclusivity, awarded by the US Food and Drug Administration in connection with the successful completion of certain paediatric testing with the product, commenced. Barr thereafter commenced litigation against the FDA in the US District Court for the District of Columbia, challenging the FDA’s refusal to grant Barr final approval for its own generic tamoxifen prior to expiration of AstraZeneca’s exclusivity period. Barr also declined AstraZeneca’s offer to extend the distribution agreement through the end of the exclusivity period. Therefore, in October 2002, AstraZeneca began shipping its own non-branded tamoxifen to customers to ensure an uninterrupted supply to patients. In December 2002, the Court held that Barr could not obtain final FDA approval for its own generic tamoxifen prior to the expiration of AstraZeneca’s paediatric exclusivity for Nolvadex. In January 2003, Barr made a claim that AstraZeneca improperly thwarted Barr’s entry into the tamoxifen market and caused Barr monetary damages. AstraZeneca disputes the claim.

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | 105 |

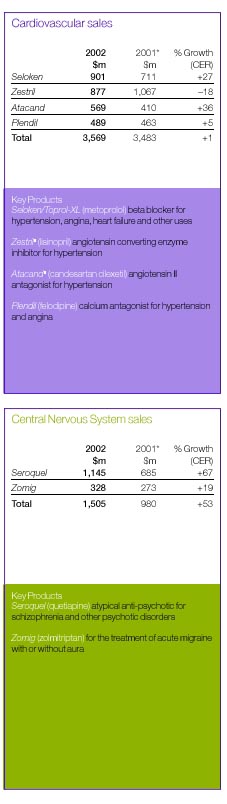

Zestril (lisinopril)

In 1986, AstraZeneca’s predecessor company and Merck & Co., Inc. entered into licence agreements under which AstraZeneca was granted the right to make, use and sell lisinopril (Zestril), in return for which AstraZeneca agreed to pay royalties to Merck. In April 2002, AstraZeneca commenced arbitration proceedings against Merck under one of the licence agreements. In the arbitration, AstraZeneca is seeking repayment of approximately $38m of prior royalty amounts and a prospective reduction in the royalty rate going forward, based on a provision of the licence agreement which reduces the royalty rate if sales of lisinopril by third parties exceed a certain level. The case is currently progressing under the arbitration rules of the International Chamber of Commerce.

Retail pharmacies’/drug purchasers’ actions

Since October 1993, several thousand retail pharmacies and certain retail drug purchasers have commenced purported class actions and individual actions in various federal and state courts throughout the US alleging that, with respect to brand name prescription drugs, manufacturers and wholesalers engaged in discriminatory pricing practices, discriminatory discounting and rebate practices, and/or conspired with one another to fix prices and artificially maintain high prices to the plaintiffs in restraint of trade and commerce. More than 20 brand name prescription drug manufacturers and eight wholesalers have been named defendants in some or all of these suits.

AstraZeneca entered into a settlement agreement with the retail class plaintiffs whose anti-trust claims were consolidated in a federal multi-district litigation proceeding pending in the US District Court for the Northern District of Illinois. AstraZeneca also reached settlements with numerous independent and chain pharmacies that opted out of the federal class action, although there are still actions brought by certain chain and independent pharmacies pending in federal court. AstraZeneca has settled or been dismissed from all of the state cases except for a consumer case pending in state court in Alabama. AstraZeneca has consistently denied liability and continues to believe it has meritorious defences to all of these claims. However, it believes that entering into these settlements is the prudent course of action given the inherent risks and costs of litigation and to avoid further business disruption.

Average wholesale price class action litigation

In January 2002, AstraZeneca was named as a defendant along with 24 other pharmaceutical manufacturers in a class action suit, in Massachusetts, brought on behalf of a putative class of plaintiffs alleged to have overpaid for prescription drugs as a result of inflated wholesale list prices. The suit seeks to recover unspecified damages. AstraZeneca has also been named as a co-defendant with various other pharmaceutical manufacturers in similar class action suits filed in five other states. Most of these suits have been consolidated with the Massachusetts action for pre-trial purposes pursuant to federal multi-district litigation procedures. AstraZeneca believes that it has meritorious defences to all of these claims.

Additional government investigations into drug marketing practices

As is true for most, if not all, major prescription pharmaceutical companies operating in the US, AstraZeneca is currently involved in multiple additional US federal and state criminal and civil investigations into drug marketing and pricing practices. AstraZeneca has received subpoenas from the US Attorney’s Office in Boston requesting production of documents relating to the sale and promotion of Prilosec to the New England Medical Center in Boston. A separate subpoena from the same office requests documents relating to Prilosec purchasing and services agreements with AdvancePCS, the pharmacy benefits management company. AstraZeneca has also received a subpoena from the Massachusetts Attorney General’s Office seeking documents relating to the sale and promotion of five products (Prilosec, Seroquel, Rhinocort Aqua, Toprol-XL and Zestril) within Massachusetts. AstraZeneca has received an investigative demand from the Missouri Attorney General’s Office seeking documents and information relating to agreements with drug retailers doing business within Missouri. Most recently, AstraZeneca has received a Civil Investigative Demand from the US Federal Trade Commission for certain information concerning AstraZeneca’s advertising and marketing of Nexium. AstraZeneca is cooperating with these investigations. It is not possible to predict the outcome of any of these investigations, which could include the payment of damages and the imposition of fines, penalties and administrative remedies.

General

AstraZeneca is also involved in various other legal proceedings considered typical to its businesses, including some remaining US retail pharmacy anti-trust class and individual actions outside the scope of the settlements described above and litigation relating to employment, product liability, commercial disputes, infringement of intellectual property rights and the validity of certain patents. Although there can be no assurance regarding the outcome of any of the legal proceedings or investigations referred to in this Note 34 to the Financial Statements, AstraZeneca does not expect them to have a materially adverse effect on AstraZeneca’s financial position or profitability.

Back to Contents

| 106 | AstraZeneca Annual Report and Form 20-F 2002 www.astrazeneca.com | Financial Statements | |

Notes to the Financial Statements continued

35 Leases

Total rentals under operating leases charged to profit and loss account were as follows:

| | 2002

$m | | 2001

$m | | 2000

$m | |

|

|

|

|

|

| |

| Hire of plant and machinery | 23 | | 25 | | 15 | |

|

|

|

|

|

| |

| Other | 96 | | 76 | | 74 | |

|

|

|

|

|

| |

| | 119 | | 101 | | 89 | |

|

|

|

|

|

| |

Commitments under operating leases to pay rentals during the year following the year of these Financial Statements analysed according to the period in which each lease expires were as follows:

| | Land and buildings

| | Other assets

| |

| | 2002

$m | | 2001

$m | | 2002

$m | | 2001

$m | |

|

|

|

|

|

|

|

| |

| Expiring within one year | 5 | | 5 | | 11 | | 12 | |

|

|

|

|

|

|

|

| |

| Expiring in years two to five | 25 | | 37 | | 15 | | 13 | |

|

|

|

|

|

|

|

| |

| Expiring thereafter | 32 | | 25 | | 2 | | 2 | |

|

|

|

|

|

|

|

| |

| | 62 | | 67 | | 28 | | 27 | |

|

|

|

|

|

|

|

| |

The future minimum lease payments under operating leases that have initial or remaining terms in excess of one year at 31 December 2002 were as follows:

| | Operating leases

| |

| | 2002

$m | | 2001

$m | |

|

|

|

| |

Obligations under leases comprise | | | | |

| Rentals due within one year | 90 | | 94 | |

|

|

|

| |

| Rentals due after more than one year | | | | |

| After five years from balance sheet date | 94 | | 97 | |

|

|

|

| |

| From four to five years | 21 | | 20 | |

|

|

|

| |

| From three to four years | 27 | | 21 | |

|

|

|

| |

| From two to three years | 38 | | 25 | |

|

|

|

| |

| From one to two years | 47 | | 35 | |

|

|

|

| |

| | 227 | | 198 | |

|

|

|

| |

| | 317 | | 292 | |

|

|

|

| |

The Group had no commitments (2001 $nil) under finance leases at the balance sheet date which were due to commence thereafter.

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002 www.astrazeneca.com | Financial Statements | 107 |

36 Statutory and other information

| | | | 2002

$m | | 2001

$m | | 2000

$m | |

|

|

|

|

|

|

|

| |

| Statutory audit fees | | | | | | | | |

| KPMG Audit Plc | | | 3.5 | | 2.5 | | 3.2 | |

|

|

|

|

|

|

|

| |

| Others | | | 0.1 | | 0.1 | | – | |

|

|

|

|

|

|

|

| |

| | | | 3.6 | | 2.6 | | 3.2 | |

|

|

|

|

|

|

|

| |

| | | | | | | | | |

| Fees for other services | | | | | | | | |

| KPMG Audit Plc and associates | – UK | | 0.4 | | 3.2 | | 8.9 | |

|

|

|

|

|

|

|

| |

| | – Worldwide | | 3.1 | | 2.0 | | 5.0 | |

|

|

|

|

|

|

|

| |

| | | | 3.5 | | 5.2 | | 13.9 | |

|

|

|

|

|

|

|

| |

Non statutory audit fees paid to KPMG Audit Plc and its associates were in relation to other assurance services $1.5m (2001 $1.8m); taxation $1.8m (2001 $2.1m); and other non audit services $0.2m (2001 $1.3m).

In addition to the above, in 2000 KPMG Audit Plc and its associates charged fees for other services of $8.0m that were borne by Syngenta AG in relation to its demerger from AstraZeneca.

The charge for the statutory audit of the Company, AstraZeneca PLC, was $1,600 (2001 $1,600, 2000 $1,600). KPMG Audit Plc were sole auditors to AstraZeneca in 2002 and 2001.

The bulk of fees for other services charged by KPMG Audit Plc and its associates (aside from the Zeneca Agrochemicals demerger and associated restructuring work) were incurred in the early months of 2000, completing 1999 integration projects.

Related party transactions

The Group had no material related party transactions which might reasonably be expected to influence decisions made by the users of these Financial Statements.

Subsequent events

No significant change has occurred since the date of the annual Financial Statements.

Back to Contents

| 108 | AstraZeneca Annual Report and Form 20-F 2002 www.astrazeneca.com | Financial Statements | |

Notes to the Financial Statements continued

37 Company information

Company Balance Sheet

| At 31 December | Notes | | 2002

$m | | 2001

$m | |

|

|

|

|

|

| |

| Fixed assets | | | | | | |

| Fixed asset investments | 37 | | 7,236 | | 6,736 | |

|

|

|

|

|

| |

| | | | 7,236 | | 6,736 | |

|

|

|

|

|

| |

| | | | | | | |

| Current assets | | | | | | |

| Debtors – amounts owed by subsidiaries | | | 27,104 | | 27,998 | |

|

|

|

|

|

| |

| Total assets | | | 34,340 | | 34,734 | |

|

|

|

|

|

| |

| | | | | | | |

| Creditors due within one year | | | | | | |

| Non-trade creditors | 37 | | (2,961 | ) | (835 | ) |

|

|

|

|

|

| |

| | | | (2,961 | ) | (835 | ) |

|

|

|

|

|

| |

| Net current assets | | | 24,143 | | 27,163 | |

|

|

|

|

|

| |

| Total assets less current liabilities | | | 31,379 | | 33,899 | |

|

|

|

|

|

| |

| | | | | | | |

| Creditors due after more than one year | | | | | | |

| Loans – owed to subsidiaries | 37 | | (295 | ) | (590 | ) |

|

|

|

|

|

| |

| Net assets | | | 31,084 | | 33,309 | |

|

|

|

|

|

| |

| | | | | | | |

| Capital and reserves | | | | | | |

| Called-up share capital | 38 | | 429 | | 436 | |

|

|

|

|

|

| |

| Share premium account | 37 | | 403 | | 334 | |

|

|

|

|

|

| |

| Capital redemption reserve | 37 | | 16 | | 9 | |

|

|

|

|

|

| |

| Other reserves | 37 | | 1,841 | | 2,239 | |

|

|

|

|

|

| |

| Profit and loss account | 37 | | 28,395 | | 30,291 | |

|

|

|

|

|

| |

| Shareholders’ funds – equity interests | | | 31,084 | | 33,309 | |

|

|

|

|

|

| |

The financial statements on pages 58 to 122 were approved by the Board of Directors on 30 January 2003 and were signed on its behalf by:

| Sir Tom McKillop | Jonathan Symonds |

| Director | Director |

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | 109 |

37 Company information (continued)

Deferred taxationThe parent company had no deferred tax assets or liabilities (actual or potential) at 31 December 2002.

| | Investments in subsidiaries | |

| |

| |

| Fixed asset investments | Shares

$m | | Loans

$m | | Total

$m | |

|

|

|

|

|

| |

| Cost at beginning of year | 6,145 | | 591 | | 6,736 | |

|

|

|

|

|

| |

| Additions | 500 | | – | | 500 | |

|

|

|

|

|

| |

| Net book value at 31 December 2002 | 6,645 | | 591 | | 7,236 | |

|

|

|

|

|

| |

| Net book value at 31 December 2001 | 6,145 | | 591 | | 6,736 | |

|

|

|

|

|

| |

| | | | | | | |

| Non-trade creditors | | | 2002

$m | | 2001

$m | |

|

|

|

|

|

| |

| Amounts due within one year | | | | | | |

| Short term borrowings (unsecured) | | | 3 | | 3 | |

|

|

|

|

|

| |

| Other creditors | | | 50 | | 4 | |

|

|

|

|

|

| |

| Amounts owed to subsidiaries | | | 2,100 | | 8 | |

|

|

|

|

|

| |

| Dividends to Shareholders | | | 808 | | 820 | |

|

|

|

|

|

| |

| | | | 2,961 | | 835 | |

|

|

|

|

|

| |

| | | | | | | |

| Loans – owed to subsidiaries | Repayment

Dates | | 2002

$m | | 2001

$m | |

|

|

|

|

|

| |

| Loans (unsecured) | | | | | | |

| US dollars | | | | | | |

| 6.58% loan | 2003 | | 295 | | 295 | |

|

|

|

|

|

| |

| 7.2% loan | 2023 | | 295 | | 295 | |

|

|

|

|

|

| |

| Total loans | | | 590 | | 590 | |

|

|

|

|

|

| |

| | | | | | | |

| Loans or instalments thereof are repayable | | | | | | |

| After five years from balance sheet date | | | 295 | | 295 | |

|

|

|

|

|

| |

| From two to five years | | | – | | – | |

|

|

|

|

|

| |

| From one to two years | | | – | | 295 | |

|

|

|

|

|

| |

| Total unsecured | | | 295 | | 590 | |

|

|

|

|

|

| |

| Total due within one year | | | 295 | | – | |

|

|

|

|

|

| |

| Total loans | | | 590 | | 590 | |

|

|

|

|

|

| |

Back to Contents

| 110 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | |

Notes to the Financial Statements continued

37 Company information (continued)Reserves

| Share

premium

account

$m | | Capital

redemption

reserve

$m | | Other

reserves

$m | | Profit

and loss

account

$m | | 2002

Total

$m | | 2001

Total

$m | |

|

|

|

|

|

|

|

|

|

|

|

| |

| At beginning of year | 334 | | 9 | | 2,239 | | 30,291 | | 32,873 | | 32,759 | |

|

|

|

|

|

|

|

|

|

|

|

| |

| Net profit for the year | – | | – | | – | | 102 | | 102 | | 2,314 | |

|

|

|

|

|

|

|

|

|

|

|

| |

| Dividends | – | | – | | (398 | ) | (808 | ) | (1,206 | ) | (1,225 | ) |

|

|

|

|

|

|

|

|

|

|

|

| |

| Share re-purchase | – | | 7 | | – | | (1,190 | ) | (1,183 | ) | (1,074 | ) |

|

|

|

|

|

|

|

|

|

|

|

| |

| Share premiums | 69 | | – | | – | | – | | 69 | | 99 | |

|

|

|

|

|

|

|

|

|

|

|

| |

| At end of year | 403 | | 16 | | 1,841 | | 28,395 | | 30,655 | | 32,873 | |

|

|

|

|

|

|

|

|

|

|

|

| |

| Distributable reserves at end of year | – | | – | | 443 | | 1,614 | | 2,057 | | 1,623 | |

|

|

|

|

|

|

|

|

|

|

|

| |

As permitted by section 230 of the Companies Act 1985, the Company has not presented its profit and loss account.

At 31 December 2002 $26,781m (31 December 2001 $29,440m) of the profit and loss account reserve was not available for distribution. The majority of this non-distributable amount relates to profit arising on the sale of Astra AB to a subsidiary in 1999, which becomes distributable as the underlying receivable is settled in cash. During 2002, $2,659m of the profit was realised by repayment. Subsequent to the year end a further $825m was repaid on 23 January 2003 resulting in additional distributable reserves not included in the figures above. Included in other reserves is a special reserve of $157m, arising on the redenomination of share capital in 1999.

| Reconciliation of movement in shareholders’ funds | 2002

$m | | 2001

$m | |

|

|

|

| |

| Shareholders’ funds at beginning of year | 33,309 | | 33,201 | |

|

|

|

| |

| Net profit for the financial year | 102 | | 2,314 | |

|

|

|

| |

| Dividends | (1,206 | ) | (1,225 | ) |

|

|

|

| |

| Issues of AstraZeneca PLC Ordinary Shares | 69 | | 99 | |

|

|

|

| |

| Re-purchase of AstraZeneca PLC Ordinary Shares | (1,190 | ) | (1,080 | ) |

|

|

|

| |

| Net (reduction in)/addition to shareholders’ funds | (2,225 | ) | 108 | |

|

|

|

| |

| Shareholders’ funds at end of year | 31,084 | | 33,309 | |

|

|

|

| |

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | 111 |

38 Called-up share capital of parent company

| | Authorised | | Allotted, called-up

and fully paid | |

| |

| |

| |

| | 2002

$m | | 2002

$m | | 2001

$m | |

|

|

|

|

|

| |

| Ordinary Shares ($0.25 each) | 429 | | 429 | | 436 | |

|

|

|

|

|

| |

| Unissued Ordinary Shares ($0.25 each) | 171 | | – | | – | |

|

|

|

|

|

| |

| Redeemable Preference Shares (£50,000) | – | | – | | – | |

|

|

|

|

|

| |

| | 600 | | 429 | | 436 | |

|

|

|

|

|

| |

The Redeemable Preference Shares carry limited class voting rights and no dividend rights. This class of shares is capable of redemption at par at the option of the Company on the giving of seven days’ written notice to the registered holder of the shares.

The movements in share capital during the year can be summarised as follows:

| | No. of shares

(million) | | $m | |

|

|

|

| |

| At beginning of year | 1,745 | | 436 | |

|

|

|

| |

| Issues of shares | 2 | | – | |

|

|

|

| |

| Re-purchase of shares | (28 | ) | (7 | ) |

|

|

|

| |

| At 31 December 2002 | 1,719 | | 429 | |

|

|

|

| |

Share buy-back

During the year the Company purchased, and subsequently cancelled, 28,386,560 Ordinary Shares at an average price of 2785 pence per share for a consideration, including expenses, of $1,190m. The excess of the consideration over the nominal value has been charged against the profit and loss account reserve.

Share schemes

A total of 1,737,401 shares were issued during the year in respect of share schemes. Details of movements in the number of shares under option are shown in Note 33; details of options granted to Directors are shown in the Directors’ Remuneration Report.

Back to Contents

| 112 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Financial Statements | |

Principal Subsidiaries, Joint Ventures and Associates

| | | Percentage of voting | | |

| At 31 December 2002 | Country | share capital held | | Principal activity |

|

| UK | | | | |

| AstraZeneca UK Limited | England | 100 | # | Research, production, marketing |

|

| AstraZeneca Insurance Company Limited | England | 100 | | Insurance and reinsurance underwriting |

|

| AstraZeneca Treasury Limited | England | 100 | | Treasury |

|

| | | | | |

| Continental Europe | | | | |

| NV AstraZeneca SA | Belgium | 100 | | Marketing |

|

| ASP SA | France | 100 | | Production |

|

| AstraZeneca Pharma SA | France | 100 | | Research, production, marketing |

|

| AstraZeneca GmbH | Germany | 100 | | Development, production, marketing |

|

| AstraZeneca Holding GmbH | Germany | 100 | | Production, marketing |

|

| AstraZeneca SpA | Italy | 100 | | Production, marketing |

|

| AstraZeneca Farmaceutica Spain SA | Spain | 100 | | Production, marketing |

|

| AstraZeneca AB | Sweden | 100 | | Research and development, |

| | | | | production, marketing |

|

| Astra Tech AB | Sweden | 100 | | Research and development, |

| | | | | production, marketing |

|

| AstraZeneca BV | The Netherlands | 100 | | Marketing |

|

| | | | | |

| The Americas | | | | |

| AstraZeneca do Brasil Ltda. | Brazil | 100 | | Production, marketing |

|

| AstraZeneca Canada Inc. | Canada | 100 | | Research, production, marketing |

|

| IPR Pharmaceuticals Inc. | Puerto Rico | 100 | | Development, production, marketing |

|

| AstraZeneca LP | US | 99 | | Development, production, marketing |

|

| AstraZeneca Pharmaceuticals LP | US | 100 | | Development, production, marketing |

|

| Salick Health Care, Inc. | US | 100 | | Provision of disease-specific |

| | | | | healthcare services |

|

| Zeneca Holdings Inc. | US | 100 | | Production, marketing |

|

| | | | | |

| Asia, Africa & Australasia | | | | |

| AstraZeneca Pty Limited | Australia | 100 | | Research, production, marketing |

|

| AstraZeneca Pharmaceutical Co., Limited | China | 100 | | Production, marketing |

|

| AstraZeneca Hong Kong Limited | Hong Kong | 100 | | Production |

|

| AstraZeneca KK | Japan | 80 | | Production, marketing |

|

| # shares held directly |

The companies and other entities listed above are those whose results or financial position principally affected the figures shown in the Group’s annual financial statements. A full list of subsidiaries, joint ventures and associates will be annexed to the Company’s next annual return filed with the Registrar of Companies. The country of registration or incorporation is stated alongside each company. The accounting dates of principal subsidiaries and associates are 31 December, except for Salick Health Care, Inc. which is 30 November. AstraZeneca operates through 235 subsidiary companies worldwide. Products are manufactured in some 20 countries worldwide and are sold in over 100 countries.

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | 113 |

Additional Information for US Investors

Differences between UK and US accounting principles

The accompanying consolidated financial statements included in this Annual Report are prepared in accordance with UK GAAP. Certain significant differences between UK GAAP and US GAAP which affect AstraZeneca’s net income and shareholders’ equity are set out below.

Purchase accounting adjustments

Under UK GAAP the merger of Astra and Zeneca was accounted for as a ‘merger of equals’ (pooling-of-interests). Under US GAAP the merger was accounted for as the acquisition of Astra by Zeneca using ‘purchase accounting’. Under purchase accounting, the cost of the investment is calculated at the market value of the shares issued together with other incidental costs and the assets and liabilities of the acquired entity are recorded at fair value. As a result of the fair value exercise, increases in the values of Astra’s tangible fixed assets and inventory were recognised and values attributed to their in-process research and development, existing products and assembled work force, together with appropriate deferred taxation effects. The difference between the cost of investment and the fair value of the assets and liabilities of Astra was recorded as goodwill. The amount allocated to in-process research and development was, as required by US GAAP, expensed immediately in the first reporting period after the business combination. Fair value adjustments to the recorded amount of inventory were expensed in the period the inventory was utilised. Additional amortisation and depreciation have also been recorded in respect of the fair value adjustments to tangible and intangible assets and the resulting goodwill.

In the consolidated financial statements prepared under UK GAAP, goodwill arising on acquisitions made prior to 1 January 1998 accounted for under the purchase method has been eliminated against shareholders’equity. Under the requirements of UK Financial Reporting Standard 10 ‘Goodwill and Intangible Assets’, goodwill on acquisitions made after 1 January 1998 is capitalised and amortised over its estimated useful life which is generally presumed not to exceed 20 years. UK GAAP requires that on subsequent disposal or termination of a previously acquired business, any goodwill previously taken directly to shareholders’equity is then charged in the income statement against the profit or loss on disposal or termination. Up until 1 January

2002, under US GAAP, goodwill was required to be capitalised and amortised. Now, instead of being amortised, goodwill is tested annually for impairment. Amortisation charged under UK GAAP is added back in the reconciliation of net income. The intangible recognised as assembled workforce has been reclassified as goodwill.

Identifiable intangible assets, which principally include patents, ‘know-how’ and product registrations, are amortised over their estimated useful lives which vary between 5 years and 20 years with a weighted average life of approximately 13 years.

At 31 December 2002 and 2001, shareholders’ equity includes capitalised goodwill of $13,600m and $12,169m respectively (net of amortisation and impairment of $2,383m and $2,180m) and capitalised identifiable intangible assets of $9,433m and $9,789m respectively (net of amortisation and impairment of $4,566m and $3,475m). Goodwill on businesses disposed of is charged to the gain or loss on disposal.

On disposal of a business, the gain or loss under US GAAP may differ from that under UK GAAP due principally to goodwill capitalised and amortised, together with the appropriate share of other differences between UK and US accounting principles recognised previously.

Capitalisation of interest

AstraZeneca does not capitalise interest in its financial statements. US GAAP requires interest incurred as part of the cost of constructing fixed assets to be capitalised and amortised over the life of the asset.

Dividends

Under UK GAAP Ordinary Share dividends proposed are provided for in the year in respect of which they are recommended by the Board of Directors for approval by the shareholders. Under US GAAP such dividends are not provided for until declared by the Board.

Deferred taxation

Deferred taxation is provided on a full liability basis under US GAAP, which permits deferred tax assets to be recognised if their realisation is considered to be more likely than not. Under current UK GAAP, full provision is also made although there are a number of different bases on which this calculation is made, eg rolled over capital gains.

Pension and post-retirement benefits

There are four main differences between current UK GAAP and US GAAP in accounting for pension costs:

| (i) | US GAAP requires measurements of plan assets and obligations to be made as at the date of the financial statements or a date not more than three months prior to that date. Under UK GAAP, calculations may be based on the results of the latest actuarial valuation; |

| | |

| (ii) | US GAAP mandates a particular actuarial method – the projected unit credit method – and requires that each significant assumption necessary to determine annual pension cost reflects best estimates solely with regard to that individual assumption. UK GAAP does not mandate a particular method, but requires that the method and assumptions taken as a whole should be compatible and lead to the actuary’s best estimate of the cost of providing the benefits promised; |

| | |

| (iii) | under US GAAP, a negative pension cost may arise where a significant unrecognised net asset or gain exists at the time of implementation. This is required to be amortised on a straight-line basis over the average remaining service period of employees. Under UK GAAP, AstraZeneca’s policy is not to recognise pension credits in its financial statements unless a refund of, or reduction in, contributions is likely; and |

| | |

| (iv) | under US GAAP, a minimum pension liability is recognised through other comprehensive income in certain circumstances when there is a deficit of plan assets relative to the projected benefits obligation. Under UK GAAP, there is no such requirement. |

Back to Contents

| 114 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | |

Additional Information for US Investors continued

Differences between UK and US accounting principles (continued)

Restructuring costs

Under UK GAAP, provisions are made for restructuring costs once a detailed formal plan is in place and valid expectations have been raised in those affected that the restructuring will be carried out. US GAAP requires a number of specific criteria to be met before such costs can be recognised as an expense. Among these are the requirements that the costs incurred are incremental to other costs incurred by the company, or represent amounts to be incurred under contractual obligations which are not associated with or do not benefit activities that will be continued. Also, all significant actions arising from a restructuring and their completion dates must be identified by the balance sheet date. To the extent that restructuring costs are related to the activities of the acquired company, US GAAP allows them to be recognised as a liability upon acquisition.

Software costs

Under UK GAAP, AstraZeneca capitalises certain defined software costs. Under US GAAP software costs are generally capitalised and amortised over three to five years.

Foreign exchange

Under UK GAAP, unrealised gains and losses on foreign currency transactions to hedge anticipated, but not firmly committed, foreign currency transactions may be deferred and accounted for at the same time as the anticipated transactions. Under US GAAP such deferral is not permitted except in certain defined circumstances.

Derivative instruments and hedging activities

Under US GAAP, all derivative instruments should be recognised as assets or liabilities in the balance sheet at fair value. Gains and losses are recognised in net income unless they are regarded as hedges. Under UK GAAP, these instruments are measured at cost and gains or losses deferred until the underlying transactions occur.

Deferred income

Under UK GAAP, profits or losses from the sale of product related intangible assets are classified in other operating income and are stated after taking account of product disposal costs and costs of minor outstanding obligations. Under US GAAP, such profits are deferred and recognised in

the income statement in subsequent periods until all disposal obligations and commitments have been completed.

Current assets and liabilities

In the Group’s financial statements prepared under UK GAAP, no cost is accrued for the share options awarded to employees under the Zeneca 1994 Executive Share Option Scheme, the AstraZeneca Share Option Plan, and the AstraZeneca Savings-Related Share Option Scheme as the exercise price is equivalent to the market value at the date of grant. Under US GAAP the cost is calculated as the difference between the option price and the market price at the date of grant or, for variable plans, at the end of the reporting period (until measurement date). Under the requirements of APB Opinion No. 25 any compensation cost would be amortised over the period from the date the options are granted to the date they are first exercisable. Under US GAAP in the net income reconciliation, the Group has adjusted for stock compensation costs and calculated under APB Opinion No. 25.

Statement of cash flows: Basis of preparation

AstraZeneca’s Statement of Group Cash Flow is prepared in accordance with United Kingdom Financial Reporting Standard 1 (Revised 1996) (‘FRS 1’), whose objective and principles are similar to those set out in SFAS No. 95, ‘Statement of Cash Flows’. The principal differences between the standards relate to classification. Under FRS 1, the Company presents its cash flows for (a) operating activities; (b) dividends received from joint ventures and associates; (c) returns on investments and servicing of finance; (d) tax paid; (e) capital expenditure and financial investment; (f) acquisitions and disposals; (g) dividends paid to shareholders; (h) management of liquid resources; and (i) financing. SFAS No. 95 requires only three categories of cash flow activity being (a) operating; (b) investing; and (c) financing.

Cash flows from taxation, returns on investments and servicing of finance and dividends received from joint ventures and associates under FRS 1 would be included as operating activities under SFAS No. 95; capital expenditure and financial investment and acquisitions and disposals would be included as investing activities; and distributions would be included as a financing activity under SFAS No. 95. Under FRS 1 cash comprises cash in hand and deposits repayable on demand, less overdrafts repayable on demand; and liquid resources

comprise current asset investments held as readily disposable stores of value. Under SFAS No. 95 cash equivalents, comprising short term highly liquid investments, generally with original maturities of three months or less, are grouped together with cash; short term borrowings repayable on demand would not be included within cash and cash equivalents and movements on those borrowings would be included in financing activities.

New accounting standards adopted

Statement of Financial Accounting Standards SFAS No. 141 ‘Business Combinations’ and SFAS No. 142 ‘Goodwill and Other Intangible Assets’ were issued in July 2001 and are effective for accounting periods commencing on or after 15 December 2001. Under SFAS No. 141, all business combinations initiated after 30 June 2001 must be accounted for using the purchase method. The pooling of interest method is no longer permitted. Intangible assets arising on acquisitions are required to be amortised to residual values over their estimated useful lives unless they are regarded as having indefinite useful lives, in which case they are tested annually for impairment. Goodwill, arising on a combination of business, is tested for impairment annually in lieu of amortisation. SFAS No. 142 requires that goodwill and intangible assets acquired prior to 1 July 2001 should continue to be amortised and tested for impairment until the adoption of the standard. Upon adoption of SFAS No. 142 an impairment test must be carried out on all intangible assets with indefinite useful lives and goodwill. Any impairment loss identified on the date of adoption of SFAS No. 142 should be accounted for as a cumulative effect of a change in accounting principle. At the same time, the estimated useful lives of amortised intangible assets must be reviewed.

Adoption of these new accounting standards has resulted in an estimated increase in net income of $755m (including amortisation charged under UK GAAP of $55m). Initial adoption of SFAS No. 142 did not result in an impairment charge, nor was there any impairment at the subsequent annual test. Had goodwill not been amortised in 2001, net income would have increased from $1,397m to $2,125m (2000 $865m to $1,716m) with a corresponding increase in basic and diluted earnings per share from $0.77 to $1.21 (2000 $0.49 to $0.97). No changes were made to estimated useful lives of intangible assets.

SFAS No. 144 ‘Accounting for the Impairment or Disposal of Long-Lived Assets’

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | 115 |

addresses financial accounting and reporting for the impairment or disposal of long-lived assets and supersedes SFAS No. 121, ‘Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to be Disposed of’ and the accounting and reporting provisions of APB Opinion No. 30, ‘Reporting the Results of Operations – Reporting the Effects of Disposal of a Segment of a Business, and Extraordinary, Unusual and Infrequently Occurring Events and Transactions’, for the disposal of a segment of a business. It is effective for accounting periods beginning on or after 15 December 2001. The adoption of SFAS No. 144 did not have a material effect.

New accounting standards not yet adopted

SFAS No. 143 ‘Accounting for Asset Retirement Obligation’ addresses the accounting and reporting for obligations associated with the retirement of long-lived assets and the associated asset retirement costs. It is effective for accounting periods beginning on or after 15 June 2002. The adoption of SFAS No. 143 is not expected to have a material effect.

SFAS No.146 ‘Accounting for Costs Associated with Exit or Disposal Activities’, issued on 30 July 2002 requires costs associated with exit or disposal activities to be recognised when the costs are incurred rather than at the date of commitment to an exit or disposal plan. The provisions are effective for disposals initialised after 31 December 2002 and restatement of prior periods is not required. As SFAS No. 146 may apply to future activities which are not currently envisaged it is not possible to assess the impact of SFAS No. 146.

SFAS No. 148 ‘Accounting for Stock Based Compensation – Transition and Disclosure – an amendment of FASB Statement No. 123’ permits two additional transition methods for entities that adopt the fair value based method of accounting for stock-based employee compensation. The Statement also requires new disclosures about the ramp-up effect of stock-based employee compensation on reported results and that those effects be disclosed more prominently by specifying the form, content and location of those disclosures. The transition guidance and annual disclosure provisions of SFAS No. 148 are effective for fiscal years ending after 15 December 2002. AstraZeneca has not yet determined whether it will adopt the transition provisions of SFAS No. 148.

Back to Contents

| 116 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | |

Additional Information for US Investors continued

Differences between UK and US accounting principles (continued)Introduction

As a result of the significant difference between the UK GAAP and US GAAP treatment of the combination of Astra and Zeneca in the year of acquisition, and in the results of preceding periods, condensed statements of operations and cash flow under US GAAP have been prepared for the benefit of US investors.

The following is a summary of the material adjustments to net income and shareholders’ equity which would have been required if US GAAP had been applied instead of UK GAAP. As noted on page 62, 2001 and 2000 net income and shareholders’ equity under UK GAAP have been restated under FRS19 – Deferred Tax. On this basis the deferred tax adjustment below as been restated for those years.

| Net income | 2002

$m | | 2001

$m | | 2000

$m | |

|

|

|

|

|

| |

| Net income, as shown in the consolidated statements | | | | | | |

| of income before exceptional items (restated) | 3,186 | | 3,044 | | 2,858 | |

|

|

|

|

|

| |

| Exceptional items after tax | (350 | ) | (138 | ) | (581 | ) |

|

|

|

|

|

| |

| Net income for the period under UK GAAP (restated) | 2,836 | | 2,906 | | 2,277 | |

|

|

|

|

|

| |

| | | | | | | |

| Adjustments to conform to US GAAP | | | | | | |

Purchase accounting adjustments (including goodwill and intangibles)

Deemed acquisition of Astra

Amortisation and other acquisition adjustments | (864 | ) | (1,514 | ) | (1,756 | ) |

|

|

|

|

|

| |

| Others | 55 | | – | | (20 | ) |

|

|

|

|

|

| |

| Capitalisation, less disposals and amortisation of interest | 46 | | 57 | | 45 | |

|

|

|

|

|

| |

| Deferred taxation | | | | | | |

| On fair values of Astra | 239 | | 249 | | 284 | |

|

|

|

|

|

| |

| Others (restated) | (99 | ) | (198 | ) | 115 | |

|

|

|

|

|

| |

| Pension expense | (50 | ) | (33 | ) | (50 | ) |

|

|

|

|

|

| |

| Post-retirement benefits/plan amendment | 4 | | 4 | | 4 | |

|

|

|

|

|

| |

| Software costs | (46 | ) | (10 | ) | 98 | |

|

|

|

|

|

| |

| Restructuring costs | – | | (22 | ) | (97 | ) |

|

|

|

|

|

| |

| Share based compensation | 33 | | (7 | ) | (33 | ) |

|

|

|

|

|

| |

| Fair value of derivative financial instruments | 93 | | 18 | | – | |

|

|

|

|

|

| |

| Deferred income recognition | 61 | | (75 | ) | – | |

|

|

|

|

|

| |

| Unrealised losses on foreign exchange and others | (1 | ) | (10 | ) | (2 | ) |

|

|

|

|

|

| |

| Net income before cumulative effect of change in accounting policy | 2,307 | | 1,365 | | 865 | |

|

|

|

|

|

| |

| Cumulative effect of change in accounting policy, net of tax, on adoption of SFAS No 133 | – | | 32 | | – | |

|

|

|

|

|

| |

| Net income in accordance with US GAAP | 2,307 | | 1,397 | | 865 | |

|

|

|

|

|

| |

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | 117 |

Differences between UK and US accounting principles (continued)US GAAP Condensed Consolidated Statement of Operations

| For the years ended 31 December | | 2002

$m | | 2001

$m | | 2000

$m | |

|

|

|

|

|

|

| |

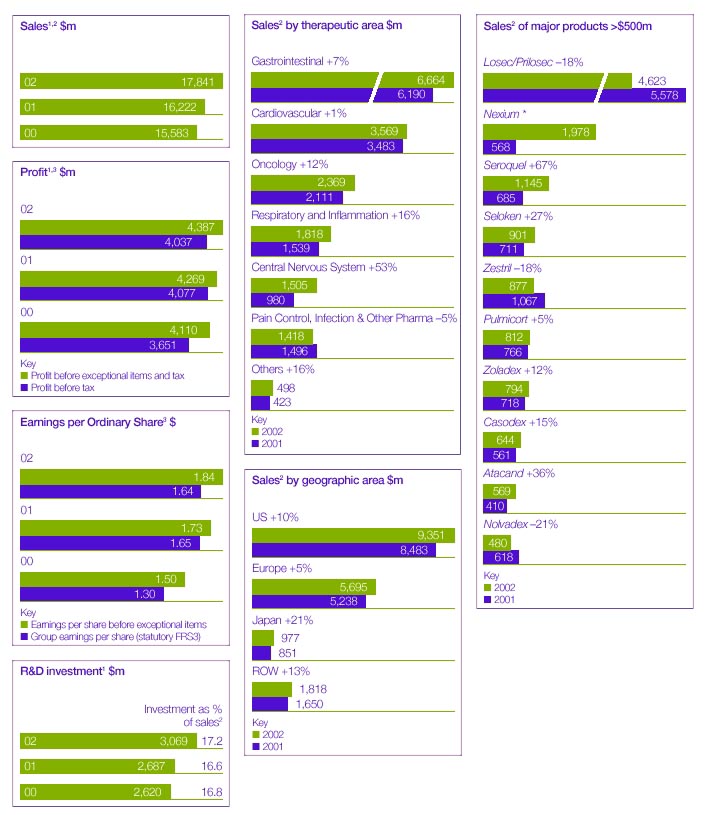

| Sales | | 17,841 | | 16,222 | | 15,583 | |

|

|

|

|

|

|

| |

| Cost of sales | | (4,520 | ) | (4,198 | ) | (3,960 | ) |

|

|

|

|

|

|

| |

| Distribution costs | | (141 | ) | (122 | ) | (210 | ) |

|

|

|

|

|

|

| |

| Research and development | | (3,069 | ) | (2,687 | ) | (2,620 | ) |

|

|

|

|

|

|

| |

| Selling, general and administrative expenses | | (6,165 | ) | (5,219 | ) | (4,861 | ) |

|

|

|

|

|

|

| |

| Acquisition related costs | | – | | (224 | ) | (419 | ) |

|

|

|

|

|

|

| |

| Amortisation of intangibles and goodwill | | (1,052 | ) | (1,769 | ) | (2,043 | ) |

|

|

|

|

|

|

| |

| Other income | | 308 | | 283 | | 223 | |

|

|

|

|

|

|

| |

| Operating income | | 3,202 | | 2,286 | | 1,693 | |

|

|

|

|

|

|

| |

| Net interest income | | 140 | | 188 | | 183 | |

|

|

|

|

|

|

| |

| Income from continuing operations before taxation | | 3,342 | | 2,474 | | 1,876 | |

|

|

|

|

|

|

| |

| Taxes on income from continuing operations | | (1,035 | ) | (1,109 | ) | (969 | ) |

|

|

|

|

|

|

| |

| Net income from continuing operations | | 2,307 | | 1,365 | | 907 | |

|

|

|

|

|

|

| |

Discontinued operations:

Net income from discontinued operations | | – | | – | | (42 | ) |

|

|

|

|

|

|

| |

| Net income before cumulative effect of change in accounting policy | | 2,307 | | 1,365 | | 865 | |

|

|

|

|

|

|

| |

| Cumulative effect of change in accounting policy on adoption of SFAS No 133 | | – | | 32 | | – | |

|

|

|

|

|

|

| |

| Net income for the year | | 2,307 | | 1,397 | | 865 | |

|

|

|

|

|

|

| |

| | | | | | | | |

Weighted average number of $0.25 Ordinary Shares

in issue (millions of shares) | | 1,733 | | 1,758 | | 1,768 | |

|

|

|

|

|

|

| |

| Dilutive impact of share options outstanding (millions of shares) | | 2 | | 3 | | 2 | |

|

|

|

|

|

|

| |

Diluted weighted average number of $0.25 Ordinary Shares

in accordance with US GAAP (millions of shares) | | 1,735 | | 1,761 | | 1,770 | |

|

|

|

|

|

|

| |

Net income per $0.25 Ordinary Share and ADS before change

in accounting policy in accordance with US GAAP – basic and diluted ($) | | $1.33 | | $0.77 | | $0.49 | |

|

|

|

|

|

|

| |

Net income per $0.25 Ordinary Share and ADS after change in

accounting policy in accordance with US GAAP – basic and diluted ($) | | $1.33 | | $0.79 | | $0.49 | |

|

|

|

|

|

|

| |

| | | | | | | | |

| | | | | | | | |

| | | 2002 | | 2001 | | 2000 | |

|

|

|

|

|

|

| |

Net income from continuing operations per $0.25 Ordinary Share and ADS

in accordance with US GAAP – basic and diluted ($) | | $1.33 | | $0.79 | | $0.51 | |

|

|

|

|

|

|

| |

Net loss from discontinued operations per $0.25 Ordinary Share and ADS

in accordance with US GAAP – basic and diluted ($) | | – | | – | | ($0.02 | ) |

|

|

|

|

|

|

| |

The dividend in specie in 2000 in respect of the demerger of Zeneca Agrochemicals under US GAAP amounted to $836m, after realised exchange gains on the translation of foreign currency financial statements of $297m.

As noted on page 62, cash settlement discounts have been reclassified from cost of sales to sales. Comparative information for 2001 and 2000 has also been reclassified for consistency of presentation.

Back to Contents

| 118 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information or US Investors | |

Additional Information for US Investors continued

Differences between UK and US accounting principles (continued)| | | | | | | |

| US GAAP Statement of Comprehensive Income | | | | | | |

| For the years ended 31 December | 2002

$m | | 2001

$m | | 2000

$m | |

| |

| Net income for the year | 2,307 | | 1,397 | | 865 | |

| |

| Exchange gains/(losses) net of tax | 2,919 | | (1,473 | ) | (2,184 | ) |

| |

| Exchange realised on demerger of Zeneca Agrochemicals | – | | – | | (297 | ) |

| |

| Other movements | (73 | ) | – | | (2 | ) |

| |

| Total Comprehensive Income | 5,153 | | (76 | ) | (1,618 | ) |

| |

Other movements in 2002 include the recognition of a minimum liability under SFAS 87 of $45m.

The cumulative exchange gains and losses (net of tax) on the translation of foreign currency financial statements under US GAAP are set out in the following note:

| For the years ended 31 December | 2002

$m | | 2001

$m | | 2000

$m | |

| |

| Balance at 1 January | (4,318 | ) | (2,845 | ) | (364 | ) |

| |

| Movement in year | 2,919 | | (1,473 | ) | (2,481 | ) |

| |

| Balance at 31 December | (1,399 | ) | (4,318 | ) | (2,845 | ) |

| |

Stock compensation

In the Group’s financial statements prepared under UK GAAP, no cost is accrued for the share options awarded to employees under the Zeneca 1994 Executive Share Option Scheme, the AstraZeneca Share Option Plan, and the AstraZeneca Savings-Related Share Option Scheme as the exercise price is equivalent to the market value at the date of grant. Under US GAAP the cost is calculated as the difference between the option price and the market price at the date of grant or, for variable plans, at the end of the reporting period (until measurement date). Under the requirements of APB Opinion No. 25 any compensation cost would be amortised over the period from the date the options are granted to the date they are first exercisable. Under US GAAP in the net income reconciliation, the Group has adjusted for stock compensation costs as calculated under APB Opinion No 25, SFAS No.123 sets out an alternative methodology for recognising the compensation cost based on the fair value at grant date. Had the Group adopted this methodology, the incremental effect on net income under US GAAP is shown below:

| | 2002 | | 2001 | | 2000 | |

| $m | $m | $m |

| |

| Net income under US GAAP as reported | 2,307 | | 1,397 | | 865 | |

| |

| Compensation cost (after adjusting for APB 25 credit of $33m) | (155 | ) | (76 | ) | (46 | ) |

| |

| Pro forma net income | 2,152 | | 1,321 | | 819 | |

| |

| Pro forma net income per $0.25 Ordinary Share and ADS in accordance with US GAAP (basic and diluted): | | | | | | |

| |

| As reported ($) | $1.33 | | $0.79 | | $0.49 | |

| |

| Pro forma ($) | $1.24 | | $0.75 | | $0.46 | |

| |

The fair value of options granted is estimated, based on the stock price at the grant date, using the Black-Scholes option pricing model with the following assumptions:

| | 2002 | | 2001 | | 2000 | |

| |

| Dividend yield | 1.6% | | 1.5% | | 2.0% | |

| |

| Expected volatility | 30.0% | | 20.0% | | 20.0% | |

| |

| Risk-free interest rate | 5.2% | | 4.2% | | 5.9% | |

| |

| Expected lives: 1994 Scheme | – | | – | | 6.0 years | |

| |

| Expected lives: AstraZeneca Share Option Plan | 6.0 years | | 6.0 years | | 6.0 years | |

| |

| Expected lives: SAYE Scheme | 4.3 years | | 4.3 years | | 4.6 years | |

| |

In the initial phase-in period, the effects of applying SFAS No.123 for disclosing compensation cost may not be representative of the effects on pro forma net income and earnings per share for future years.

Back to Contents

| | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | 119 |

Differences between UK and US accounting principles (continued)Pension and post-retirement benefits

For the purposes of US GAAP, the pension costs of the major UK retirement plan and of the retirement plans of the major non-UK subsidiaries have been restated in the following tables in accordance with the requirements of SFAS No. 132. These plans comprise a substantial portion of the actuarial liabilities of all AstraZeneca retirement plans. The changes in projected benefit obligations, plan assets and details of the funded status of these retirement plans, together with the changes in the accumulated other post-retirement benefit obligations, under SFAS No. 132 are as follows:

| | Pension benefits | | Other post-retirement benefits | |

| |

| |

| |

| Change in projected benefit obligation | 2002 | | 2001 | | 2002 | | 2001 | |

| | $m | | $m | | $m | | $m | |

| |

| Benefit obligation at beginning of year | 4,337 | | 4,188 | | 205 | | 197 | |

| |

| Service cost | 114 | | 102 | | 8 | | 7 | |

| |

| Interest cost | 263 | | 243 | | 14 | | 14 | |

| |

| Participant contributions | 18 | | 17 | | – | | – | |

| |

| Plan amendments | – | | (11 | ) | – | | – | |

| |

| Actuarial (gain)/loss | 80 | | 75 | | 23 | | (1 | ) |

| |

| Special termination benefits | 12 | | 19 | | – | | – | |

| |

| Settlement and curtailment | – | | – | | (24 | ) | – | |

| |

| Benefits paid | (206 | ) | (198 | ) | (19 | ) | (14 | ) |

| |

| Exchange | 408 | | (98 | ) | 3 | | 2 | |

| |

| Benefit obligation at end of year | 5,026 | | 4,337 | | 210 | | 205 | |

| |

| | Pension benefits | | Other post-retirement benefits | |

| |

| |

| |

| Change in plan assets | 2002 | | 2001 | | 2002 | | 2001 | |

| | $m | | $m | | $m | | $m | |

| |

| Fair value at 1 January | 3,753 | | 3,803 | | – | | – | |

| |

| Actual return on plan assets | (142 | ) | 45 | | (16 | ) | – | |

| |

| Group contribution | 284 | | 170 | | 161 | | – | |

| |

| Participant contributions | 18 | | 17 | | – | | – | |

| |

| Settlement and curtailment | – | | – | | – | | – | |

| |

| Benefits paid | (205 | ) | (198 | ) | (12 | ) | – | |

| |

| Exchange | 330 | | (84 | ) | – | | – | |

| |

| Fair value of plan assets at end of year | 4,038 | | 3,753 | | 133 | | – | |

| |

| Funded status of plans | (988 | ) | (584 | ) | (77 | ) | (205 | ) |

| |

| Unrecognised net loss/(profit) | 938 | | 396 | | – | | – | |

| |

| Prior service cost not recognised | 29 | | 35 | | – | | – | |

| |

| Unrecognised net obligation on implementation | 3 | | 6 | | – | | – | |

| |

| | (18 | ) | (147 | ) | (77 | ) | (205 | ) |

| |

| Adjustments to recognise minimum liability | | | | | | | | |

| Intangible assets | (45 | ) | – | | – | | – | |

| |

| Accumulated other comprehensive income | (45 | ) | – | | – | | – | |

| |

| Accrued benefit liability | (108 | ) | (147 | ) | (77 | ) | (205 | ) |

| |

Back to Contents

| 120 | AstraZeneca Annual Report and Form 20-F 2002

www.astrazeneca.com | Additional Information for US Investors | |

Additional Information for US Investors continued

Differences between UK and US accounting principles (continued)At 31 December 2002, the projected benefit obligation, accumulated benefit obligation and fair value of the plan assets in respect of the retirement plans above with accumulated benefit obligations in excess of plan assets were $4,249m, $3,557m and $3,296m, (2001 $97m, $73m and $nil) respectively.

Assumed discount rates and rates of increase in remuneration used in calculating the projected benefit obligations together with long term rates of return on plan assets vary according to the economic conditions of the country in which the retirement plans are situated. The weighted average rates used for calculation of year end benefit obligations and forecast benefits cost in the main retirement plans and other benefit obligations for SFAS No. 132 purposes were as follows:

| | Pension benefits | | Other post-retirement benefits | |

| |

| |

| |

| | 2002

% | | 2001

% | | 2000

% | | 2002

% | | 2001

% | | 2000

% | |

|

|

|

|

|

|

|

|

|

|

|

| |

| Discount rate | 5.8 | | 6.0 | | 5.6 | | 6.6 | | 7.1 | | 7.1 | |

|

|

|

|

|