| OMB APPROVAL |

| OMB Number: 3235-0570 |

| Expires: November 30, 2005 |

| Estimated average burden |

| hours per response... 5.0 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07678

American Municipal Income Portfolio Inc.

(Exact name of registrant as specified in charter)

800 Nicollet Mall, Minneapolis, MN | | 55402 |

(Address of principal executive offices) | | (Zip code) |

Charles D. Gariboldi 800 Nicollet Mall, Minneapolis, MN 55402

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-677-3863

Date of fiscal year end: August 31

Date of reporting period: August 31, 2005

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Item 1. Report to Shareholders

AMERICAN MUNICIPAL | |

INCOME PORTFOLIO | |

| |

XAA | |

August 31, 2005

ANNUAL REPORT

AMERICAN MUNICIPAL INCOME PORTFOLIO

Primary Investments

American Municipal Income Portfolio (the “fund”) invests primarily in a wide range of municipal securities that, at the time of purchase, are rated investment-grade or are unrated and deemed to be of comparable quality by U.S. Bancorp Asset Management, Inc. (“USBAM”). The fund may invest up to 5% of its assets in municipal securities that, at the time of purchase, are rated lower than investment-grade or are unrated and deemed to be of comparable quality by USBAM. The fund’s investments may include municipal-derivative securities, such as inverse floating-rate and inverse interest-only municipal securities, which may be more volatile than traditional municipal securities in certain market conditions.

Fund Objective

The fund is a diversified, closed-end management investment company. The investment objective is to provide high current income exempt from regular federal income tax, consistent with preservation of capital. The fund’s income may be subject to state or local tax and the federal alternative minimum tax. Distributions of capital gains will be taxable to shareholders. Investors should consult their tax advisors. As with other investment companies, there can be no assurance the fund will achieve its objective.

| | Table of Contents |

| | |

2 | | Fund Overview |

| | |

7 | | Financial Statements |

| | |

10 | | Notes to Financial Statements |

| | |

15 | | Schedule of Investments |

| | |

20 | | Report of Independent Registered Public Accounting Firm |

| | |

21 | | Notice to Shareholders |

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE

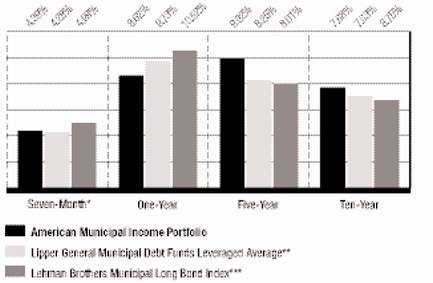

Average Annual Total Returns

Based on net asset value (“NAV”) for the period ended August 31, 2005

*Total return has not been annualized.

**The Lipper General Municipal Debt Funds Leveraged Average represents the average annual total return, with distributions reinvested, of leveraged perpetual national closed-end municipal funds as characterized by Lipper Inc.

***The Lehman Brothers Municipal Long Bond Index is comprised of municipal bonds with more than 22 years to maturity and an average credit quality of Aa. The index is unmanaged and does not include any fees expenses in its total return figures.

The average annual total returns for the fund are based on the change in its NAV and assume reinvestment of distributions at NAV. NAV-based performance is used to measure investment management results.

• Average annual total returns based on the change in market price for the seven-month, one-year, five-year, and ten-year periods ended August 31, 2005, were 2.19%, 0.04%, 10.68%, and 8.67%, respectively. • Market price returns assume that all distributions have been reinvested at actual prices pursuant to the fund’s dividend reinvestment plan. Market price returns reflect any broker commissions or sales charges on dividends reinvested at market price. • Please remember, you could lose money with this investment. Neither safety of principal nor stability of income is guaranteed. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that fund shares, when sold, may be worth more or less than their original cost. Closed-end funds, such as this fund, often trade at discounts to NAV. Therefore, you may be unable to realize the full NAV of your shares when you sell.

1

Fund OVERVIEW

Fund Management

Doug White, CFA is primarily responsible for the management of the fund. He has 22 years of financial experience.

Catherine Stienstra assists with the management of the fund. She has 17 years of financial experience.

American Municipal Income Portfolio’s fiscal year-end has changed from January 31 to August 31, effective with the seven months ended August 31, 2005. In this report, we will discuss the economy and the fund’s performance during this seven-month period. American Municipal Income Portfolio earned a total return of 4.39% based on NAV for the fiscal period ended August 31, 2005. The fund’s market price return was 2.19% during the period. The fund’s competitive group, the Lipper General Municipal Debt Funds Leveraged Average, produced an average return of 4.28% during the period. The Lehman Brothers Municipal Long Bond Index, the benchmark comparison for the fund, which reflects no fees or expenses, returned 4.99%.

The economy continued to expand at a solid pace as corporate earnings remained vigorous and balance sheets strong. Under the watchful eye of the Federal Reserve (the “Fed”), inflation was held in check, with no fewer than four short-term rate hikes by the Fed from February 2005 through August 2005. While this measured approach to tightening monetary policy continued to foster stability in the bond market, there was little the Fed could do – aside from expressions of perplexity – to affect the long-term rates, which remained stubbornly low, largely due to a variety of technical factors in the marketplace.

Year-to-date, the nationwide new municipal bond supply of $275.5 billion is set to break the previous record level issuance in 2003. Heavy refunding volume is the main driver, accounting for more than 60% of total issuance. The current environment of higher short-term rates and lower long-term rates tends to help the mechanics of refunding issues. The smaller the difference in yield between the shorter taxable securities purchased to hold in escrow to pay the refunded issue and the borrowing rate on the new long-term municipal issue, the more attractive the refunding.

Portfolio Allocation

As a percentage of total assets on August 31, 2005

2

The percentage of new issues carrying insurance rose to 60% so far this year. This jump in insurance penetration can be attributed to a variety of factors, including greater nontraditional buyer participation and their desire for bond commoditization, a higher volume of refunding issues that can be underwritten with lower insurance premiums, and increased competition from new insurers entering the marketplace.

Due to the increased insurance sector, lower-rated municipals are becoming more scarce, resulting in their continued outperformance vs. high-grade municipals. The difference, or spread, between yields on lower- and higher-rated issues continued to narrow as it has for the past 14 to 18 months. As such, the fund’s performance also benefited from its holdings of lower-rated bonds, which generally outperformed the Lehman Brothers Municipal Long Bond Index. The yield spread on the Lehman Baa Index vs. its Aaa Index narrowed to 82 basis points at the end of August. This is mildly wider than its long-term average but dramatically lower than the 190-basis-point peak of two years ago.

The municipal yield curve continued its flattening trend, resulting in generally positive price performance for bonds maturing in 15 years and longer. Despite the increase in short and intermediate yields, the longer end of the yield curve dropped, which caused long maturity bonds to produce the best total returns. Long municipal bond yields have now declined by more than 60 basis points in the face of 250 basis points of Fed tightening

Geographical Distribution

As a percentage of total assets on August 31, 2005. Shaded areas without values indicate states in which the fund has invested less than 0.50% of its assets.

3

since June 30, 2004. The fund’s positions in longer maturity holdings were positive contributors to performance relative to investments in short/intermediate issues (eight years and under). During the period, the fund held 26% of its total assets in short/intermediate issues and 47% in longer maturity holdings.

The yield curve may flatten somewhat further if the Fed suggests there is still some distance to go with its tightening program. We expect the most pressure would be on short and intermediate serial bonds. While the municipal yield curve is flatter than its long-term averages, it is not yet at historical extremes. Still, the magnitude of further curve compression seems limited, making certain bond portfolio flattening strategies such as “barbells” less attractive. As such, the fund’s current structure is more laddered than previously but still maintains a component of short-term, variable-rate securities. Duration has also been shortened to slightly longer than the fund’s benchmark. Therefore the fund had less interest-rate risk, relative to the benchmark, than during the previous period.

We continue to emphasize a broad mix of securities, both across the quality spectrum and across sectors. The fund’s performance benefited from its positions in selected healthcare and transportation revenue bonds, as these sectors outperformed the Lehman Brothers Municipal Long Bond Index. The fund held bonds in a variety of municipal sectors as of the end of August. The overall credit outlook by the rating agencies for states is relatively stable. Most state budgets were stronger than in recent years due to increases in state tax revenues, which is a positive trend compared to large deficits experienced in 2001.

Factors that negatively impacted performance included positions in general obligations, electric revenue, and higher-rated bonds as these generally underperformed the Lehman Brothers Municipal Long Bond Index.

Credit Quality Breakdown*

As a percentage of total assets on August 31, 2005

AAA/Aaa | | 43 | % |

AA/Aa | | 6 | % |

A | | 14 | % |

BBB/Baa | | 24 | % |

BB/Ba | | 1 | % |

Nonrated | | 12 | % |

| | 100 | % |

*In the case of split ratings, a security is considered to be rated in the listed category if two of Moody’s Investor Service, Standard & Poor’s, and Fitch rate the security in that category. If ratings are provided by only two of those rating agencies, the lower rating is used. If only one of those rating agencies provides a rating, that rating is used.

4

The fund reduced its common stock dividend during the period. The monthly dividend was lowered from 7.8 to 7.5 cents per share in June. Due to the fund’s reduced duration and increased leverage costs resulting from rising short-term interest rates, income declined and some of the fund’s dividend reserve has been used to pay the common stock dividend. As of August 31, 2005, the dividend reserve, which is included in the fund’s NAV, stood at 15.9 cents per share, down from 20.2 cents per share at the start of February.

We once again wish to express our appreciation for your ongoing investment in the fund. If you have any questions or need assistance with your investments, please call us at 800.677.FUND.

Sincerely,

/s/ Mark Jordahl | |

Mark Jordahl |

Chief Investment Officer |

U.S. Bancorp Asset Management, Inc. |

/s/ Doug White | |

Doug White, CFA |

Head of Tax Exempt Fixed Income |

U.S. Bancorp Asset Management, Inc. |

/s/ Catherine M. Stienstra | |

Catherine M. Stienstra |

Senior Fixed-Income Portfolio Manager |

U.S. Bancorp Asset Management, Inc. |

5

Preferred Shares

The preferred shares issued by the fund pay dividends at a specified rate and have preference over common shares in the payments of dividends and the liquidation of assets. Rates paid on preferred shares are reset every seven days and are based on short-term tax-exempt interest rates. Preferred shareholders accept these short-term rates in exchange for low credit risk (preferred shares are rated AAA by Moody’s and S&P) and high liquidity (preferred shares trade at par and are remarketed every seven days). The proceeds from the sale of preferred shares are invested at intermediate- and long-term tax-exempt rates. Because these intermediate- and long-term rates are normally higher than the short-term rates paid on preferred shares, common shareholders benefit by receiving higher dividends and/or an increase to the dividend reserve. However, the risk of having preferred shares is that if short-term rates rise higher than intermediate- and long-term rates, creating an inverted yield curve, common shareholders may receive a lower rate of return than if their fund did not have any preferred shares outstanding. This type of economic environment is unusual and historically has been short term in nature. Investors should also be aware that the issuance of preferred shares results in the leveraging of common shares, which increases the volatility of both the NAV of the fund and the market value of common shares.

6

Financial STATEMENTS

Statement of Assets and Liabilities August 31, 2005

Assets:

| Investments in unaffiliated securities, at market value (cost: $121,699,354) (note 2) | | $ | 131,482,055 | | |

| Investment in affiliated money market fund, at market value (cost: $2,102,205) (note 5) | | | 2,102,205 | | |

| Receivable for accrued interest | | | 1,541,798 | | |

| Prepaid expenses | | | 43,625 | | |

| Total assets | | | 135,169,683 | | |

Liabilities:

| Payable for preferred share distributions (note 3) | | | 10,041 | | |

| Payable for investment advisory fees (note 5) | | | 40,942 | | |

| Payable for administrative fees (note 5) | | | 22,712 | | |

| Payable for transfer agent fees | | | 39,285 | | |

| Payable for pricing fees | | | 21,633 | | |

| Payable for professional fees | | | 19,318 | | |

| Payable for postage and printing fees | | | 18,182 | | |

| Payable for listing fees | | | 6,507 | | |

| Payable for other expenses | | | 5,187 | | |

| Total liabilities | | | 183,807 | | |

| Preferred shares, at liquidation value | | | 43,500,000 | | |

| Net assets applicable to outstanding common shares | | $ | 91,485,876 | | |

Net assets applicable to outstanding common shares consist of:

| Common shares and additional paid-in capital | | $ | 80,009,100 | | |

| Undistributed net investment income | | | 914,907 | | |

| Accumulated net realized gain on investments | | | 779,168 | | |

| Unrealized appreciation of investments | | | 9,782,701 | | |

| Net assets applicable to outstanding common shares | | $ | 91,485,876 | | |

Net asset value and market price of common shares:

| Net assets applicable to outstanding common shares | | $ | 91,485,876 | | |

| Common shares outstanding (authorized 200 million shares of $0.01 par value) | | | 5,756,267 | | |

| Net asset value per share | | $ | 15.89 | | |

| Market price per share | | $ | 14.70 | | |

Liquidation preference of preferred shares (note 3):

| Net assets applicable to preferred shares | | $ | 43,500,000 | | |

| Preferred shares outstanding (authorized one million shares) | | | 1,740 | | |

| Liquidation preference per share | | $ | 25,000 | | |

See accompanying Notes to Financial Statements.

2005 Annual Report

American Municipal Income Portfolio

7

Financial STATEMENTS continued

Statements of Operations

| | | Seven-Month

Period Ended

8/31/05 | |

Year Ended

1/31/05 | |

| Investment income: | | | |

| Interest from unaffiliated securities | | $ | 3,936,104 | | | $ | 6,623,629 | | |

| Dividends from affiliated money market fund | | | 50,286 | | | | 78,768 | | |

| Total investment income | | | 3,986,390 | | | | 6,702,397 | | |

Expenses (note 5):

| Investment advisory fees | | | 271,257 | | | | 463,371 | | |

| Administrative fees | | | 155,004 | | | | 264,794 | | |

| Remarketing agent fees | | | 56,231 | | | | 108,375 | | |

| Custodian fees | | | 9,351 | | | | 19,828 | | |

| Transfer agent fees | | | 23,614 | | | | 50,636 | | |

| Listing fees | | | 14,371 | | | | 25,000 | | |

| Postage and printing fees | | | 15,944 | | | | 46,302 | | |

| Directors' fees | | | 3,218 | | | | 7,746 | | |

| Professional fees | | | 33,984 | | | | 73,929 | | |

| Other expenses | | | 15,784 | | | | 35,286 | | |

| Total expenses | | | 598,758 | | | | 1,095,267 | | |

| Net investment income | | | 3,387,632 | | | | 5,607,130 | | |

Net realized and unrealized gains on investments:

| Net realized gain on investments (note 4) | | | 906,288 | | | | 434,640 | | |

| Net change in unrealized appreciation or depreciation of investments | | | 188,050 | | | | 357,679 | | |

| Net gain on investments | | | 1,094,338 | | | | 792,319 | | |

Distributions to preferred shareholders (note 2):

| From net investment income | | | (544,394 | ) | | | (515,848 | ) | |

| Net increase in net assets applicable to common shares resulting from operations | | $ | 3,937,576 | | | $ | 5,883,601 | | |

See accompanying Notes to Financial Statements.

2005 Annual Report

American Municipal Income Portfolio

8

Statements of Changes in Net Assets

| | | Seven-Month

Period Ended

8/31/05 | |

Year Ended

1/31/05 | |

Year Ended

1/31/04 | |

| Operations: | | | |

| Net investment income | | $ | 3,387,632 | | | $ | 5,607,130 | | | $ | 5,876,556 | | |

| Net realized gain on investments | | | 906,288 | | | | 434,640 | | | | 955,092 | | |

| Net change in unrealized appreciation or depreciation of investments | | | 188,050 | | | | 357,679 | | | | 2,018,611 | | |

| Distributions to preferred shareholders (note 2): | |

| From net investment income | | | (544,394 | ) | | | (515,848 | ) | | | (419,577 | ) | |

| Net increase in net assets applicable to common shares resulting from operations | | | 3,937,576 | | | | 5,883,601 | | | | 8,430,682 | | |

Distributions to common shareholders (note 2):

| From net investment income | | | (3,091,116 | ) | | | (5,387,866 | ) | | | (5,387,866 | ) | |

| Total increase in net assets in net assets applicable to common shares | | | 846,460 | | | | 495,735 | | | | 3,042,816 | | |

| Net assets applicable to common shares at beginning of period | | | 90,639,416 | | | | 90,143,681 | | | | 87,100,865 | | |

| Net assets applicable to common shares at end of period | | $ | 91,485,876 | | | $ | 90,639,416 | | | $ | 90,143,681 | | |

| Undistributed net investment income | | $ | 914,907 | | | $ | 1,162,785 | | | $ | 1,460,037 | | |

See accompanying Notes to Financial Statements.

2005 Annual Report

American Municipal Income Portfolio

9

Notes to Financial STATEMENTS

(1) Organization

American Municipal Income Portfolio Inc. (the "fund") is registered under the Investment Company Act of 1940 (as amended) as a diversified, closed-end management investment company. The fund invests primarily in a diverse range of municipal securities that, at the time of purchase, are rated investment grade or are unrated and deemed to be of comparable quality by U.S. Bancorp Asset Management, Inc. ("USBAM"). The fund may invest up to 5% of its total assets in municipal securities that, at the time of purchase, are rated lower than investment grade or are unrated and deemed to be of comparable quality by USBAM. The fund will not invest in municipal securities that, at the time of purchase, are rated lower than B or are unrated and deemed to be of comparable quality by USBAM. Municipal securities in which the fund invests may include municipal derivative securities, such as inverse floating rate and inv erse interest-only municipal securities. The fund's investments also may include futures contracts, options on futures contracts, options, and interest rate swaps, caps, and floors. Although the fund is authorized to invest in the financial instruments mentioned in the preceding two sentences, and may do so in the future, the fund did not make any such investments during the seven-month period ended August 31, 2005 (the "fiscal period"). Fund shares are listed on the New York Stock Exchange under the symbol XAA.

On June 22, 2005, the fund's board of directors approved a change in the fund's fiscal year-end from January 31 to August 31, effective with the fiscal period ended August 31, 2005.

(2) Summary of Significant Accounting Policies

Security Valuations

Security valuations for the fund's investments are furnished by one or more independent pricing services that have been approved by the fund's board of directors. Debt obligations exceeding 60 days to maturity are valued by an independent pricing service. The pricing service may employ methodologies that utilize actual market transactions, broker-dealer supplied valuations, or other formula-driven valuation techniques. These techniques generally consider such factors as yields or prices of bonds of comparable quality, type of issue, coupon, maturity, ratings, and general market conditions. Securities for which prices are not available from an independent pricing service but where an active market exists are valued using market quotations obtained from one or more dealers that make markets in the securities or from a widely used quotation system. When market quotations are not readily available, securities are valued at fair value as determined in good faith by procedures established and approved by the fund's board of directors. Some of the factors which may be considered in determining fair value are fundamental analytical data relating to the investment; the nature and duration of any restrictions on disposition; trading in similar securities of the same issuer or comparable companies; information from broker-dealers; and an evaluation of the forces that influence the market in which the securities are purchased or sold. If events occur that materially affect the value of securities between the close of trading in those securities and the close of regular trading on the New York Stock Exchange, the securities will be valued at fair value. Debt obligations with 60 days or less remaining until maturity may be valued at their amortized cost, which approximates market value. Security valuations are performed once a week and at the end of each month.

As of August 31, 2005, the fund had no fair valued securities.

Security Transactions and Investment Income

For financial statement purposes, the fund records security transactions on the trade date of the security purchase or sale. Dividend income is recorded on the ex-dividend date. Interest income, including accretion of bond discounts and amortization of bond premiums, is recorded on an accrual basis. Security gains and losses are determined on the basis of identified cost, which is the same basis used for federal income tax purposes.

2005 Annual Report

American Municipal Income Portfolio

10

Inverse Floaters

As part of its investment strategy, the fund may invest in certain securities for which the potential income return is inversely related to changes in a floating interest rate ("inverse floaters"). In general, income on inverse floaters will decrease when short-term interest rates increase and increase when short-term interest rates decrease. Inverse floaters may be characterized as derivative securities and may subject the fund to the risks of reduced or eliminated interest payments and losses of invested principal. In addition, inverse floaters have the effect of providing investment leverage and, as a result, the market value of such securities will generally be more volatile than that of fixed-rate, tax-exempt securities. To the extent the fund invests in inverse floaters, the net asset value of the fund's shares may be more volatile than if the fund did not invest in such securities. As of August&n bsp;31, 2005, the fund had no outstanding investments in inverse floaters.

Futures Transactions

To gain exposure to or protect itself from changes in the market, the fund may buy and sell interest rate futures contracts. Risks of entering into futures contracts and related options include the possibility there may be an illiquid market and that a change in the value of the contract or option may not correlate with changes in the value of the underlying securities.

Upon entering into a futures contract, the fund is required to deposit, in segregated accounts with its custodian, either cash or securities in an amount (initial margin) equal to a certain percentage of the contract value. Subsequent payments (variation margin) are made or received by the fund each day. The variation margin payments are equal to the daily changes in the contract value and are recorded as unrealized gains and losses. The fund recognizes a realized gain or loss when the contract is closed or expires. As of August 31, 2005, the fund had no outstanding futures contracts.

Securities Purchased on a When-Issued Basis

Delivery and payment for securities that have been purchased by the fund on a when-issued or forward-commitment basis can take place a month or more after the transaction date. During this fiscal period ended August 31, 2005, such securities do not earn interest, are subject to market fluctuation, and may increase or decrease in value prior to their delivery. The fund segregates, with its custodian, assets with a market value equal to the amount of its purchase commitments. The purchase of securities on a when-issued or forward-commitment basis may increase the volatility of the fund's net asset value if the fund makes such purchases while remaining substantially fully invested. As of August 31, 2005, the fund had no outstanding when-issued or forward-commitments securities.

Federal Taxes

The fund intends to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies and not be subject to federal income tax. Therefore, no income tax provision is required. The fund also intends to distribute its taxable net investment income and realized gains, if any, to avoid the payment of any federal excise taxes.

Net investment income and net realized gains and losses may differ for financial statement and tax purposes primarily because of market discount amortization. The character of distributions made during the fiscal period from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. In addition, due to the timing of dividend distributions, the fiscal period in which amounts are distributed may differ from the fiscal period that the income or realized gains or losses were recorded by the fund.

2005 Annual Report

American Municipal Income Portfolio

11

Notes to Financial STATEMENTS continued

The tax character of common and preferred share distributions paid during the fiscal period ended August 31, 2005 and fiscal years ended January 31, 2005 and 2004, were characterized as follows:

| | | 8/31/05 | | 1/31/05 | | 1/31/04 | |

| Distributions paid from: | |

| Tax-exempt income | | $ | 3,636,374 | | | $ | 5,809,265 | | | $ | 5,745,748 | | |

| Ordinary income | | | - | | | | 86,786 | | | | 60,896 | | |

| | | $ | 3,636,374 | | | $ | 5,896,051 | | | $ | 5,806,644 | | |

At August 31, 2005, the components of accumulated earnings on a tax basis were as follows:

| Undistributed ordinary income | | $ | 509,981 | | |

| Undistributed tax-exempt income | | | 834,154 | | |

| Accumulated capital gains | | | 359,981 | | |

| Unrealized appreciation | | | 9,782,701 | | |

| Accumulated earnings | | $ | 11,486,817 | | |

Distributions to Shareholders

Distributions from net investment income are made monthly for common shareholders and weekly for preferred shareholders. Common share distributions are recorded as of the close of business on the ex-dividend date and preferred share dividends are accrued daily. Net realized gains distributions, if any, will be made at least annually. Distributions are payable in cash or, for common shareholders pursuant to the fund's dividend reinvestment plan, reinvested in additional common shares of the fund. Under the dividend reinvestment plan, common shares will be purchased in the open market.

Repurchase Agreements

For repurchase agreements entered into with certain broker-dealers, the fund, along with other affiliated registered investment companies, may transfer uninvested cash balances into a joint trading account, the daily aggregate balance of which is invested in repurchase agreements secured by U.S. government or agency obligations. Securities pledged as collateral for all individual and joint repurchase agreements are held by the fund's custodian bank until maturity of the repurchase agreement. All agreements require that the daily market value of the collateral be in excess of the repurchase amount, including accrued interest, to protect the fund in the event of a default. As of August 31, 2005, the fund had no outstanding repurchase agreements.

Deferred Compensation Plan

Under a Deferred Compensation Plan (the "Plan"), non-interested directors of the First American Fund family may participate and elect to defer receipt of their annual compensation. Deferred amounts are treated as though equivalent dollar amounts had been invested in shares of selected open-end First American Funds as designated by the board of directors. All amounts in the Plan are 100% vested and accounts under the Plan are obligations of the funds. Deferred amounts remain in the funds until distributed in accordance with the Plan.

Use of Estimates in the Preparation of Financial Statements

The preparation of financial statements, in conformity with U.S. generally accepted accounting principles, requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the results of operations during the reporting period. Actual results could differ from these estimates.

2005 Annual Report

American Municipal Income Portfolio

12

Reclassifications

Certain amounts in the 1/31/05 financial statements have been reclassified to confirm to the 8/31/05 presentation.

(3) Remarketed Preferred Shares

As of August 31, 2005, the fund had 1,740 remarketed preferred shares (870 shares in class "T" and 870 shares in class "TH") (RP®) with a liquidation preference of $25,000 per share. The dividend rate on the RP® is adjusted every seven days (on Tuesdays for class "T" and on Thursdays for class "TH"), as determined by the remarketing agent. On August 31, 2005, the dividend rates were 2.45% and 2.40% for class "T" and "TH", respectively.

RP® is a registered trademark of Merrill Lynch & Company ("Merrill Lynch").

(4) Investment Security Transactions

Cost of purchases and proceeds from sales of securities, other than temporary investments in short-term securities, for the fiscal period ended August 31, 2005, aggregated $15,942,023 and $21,733,124, respectively.

(5) Expenses

Investment Advisory Fees

Pursuant to an investment advisory agreement (the "Agreement"), USBAM, a subsidiary of U.S. Bank National Association ("U.S. Bank"), manages the fund's assets and furnishes related office facilities, equipment, research, and personnel. The Agreement provides USBAM with a monthly investment advisory fee in an amount equal to an annualized rate of 0.35% of the fund's average weekly net assets including preferred shares. For its fee, USBAM provides investment advice and, in general, conducts the management and investment activities of the fund.

The fund may invest in related money market funds that are series of First American Funds, Inc. ("FAF"), subject to certain limitations. In order to avoid the payment of duplicative investment advisory fees to USBAM, which acts as the investment advisor to both the fund and the related money market funds, USBAM will reimburse the fund an amount equal to the investment advisory fee received from the related money market funds that is attributable to the assets of the fund. For financial statement purposes, this reimbursement is recorded as investment income.

Administrative Fees

USBAM serves as the fund's administrator pursuant to an administration agreement between USBAM and the fund. Under this administration agreement, USBAM receives a monthly administrative fee in an amount equal to an annualized rate of 0.20% of the fund's average weekly net assets including preferred shares. For its fee, USBAM provides numerous services to the fund including, but not limited to, handling the general business affairs, financial and regulatory reporting, and various other services.

Remarketing Agent Fees

The fund has entered into a remarketing agreement with Merrill Lynch (the "Remarketing Agent"). The remarketing agreement provides the Remarketing Agent with a monthly fee in an amount equal to an annual rate of 0.25% of the fund's average amount of RP® outstanding. For its fee, the Remarketing Agent will remarket shares of RP® tendered to it on behalf of shareholders and will determine the applicable dividend rate for each seven-day dividend period.

Custodian Fees

U.S. Bank serves as the fund's custodian pursuant to a custodian agreement with the fund. Effective July 1, 2005, the custodian fee charged to the fund was reduced from an annual rate of 0.015% of average weekly net assets including preferred shares, to an annual rate of 0.005% of average weekly net assets including preferred shares. These fees are computed weekly and paid monthly.

2005 Annual Report

American Municipal Income Portfolio

13

Notes to Financial STATEMENTS continued

Other Fees and Expenses

In addition to the investment advisory, administrative, remarketing agent, and custodian fees, the fund is responsible for paying most other operating expenses, including: outside directors' fees and expenses, listing fees, postage and printing of shareholder reports, transfer agent fees and expenses, legal, auditing, and accounting services, insurance, interest, taxes, and other miscellaneous expenses.

(6) Indemnifications

The fund enters into contracts that contain a variety of indemnifications. The fund's maximum exposure under these arrangements is unknown. However, the fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

(7) Financial Highlights

Per-share data for an outstanding common share throughout each period and selected information for each period are as follows:

| | | Seven-Month

Period Ended | |

Year Ended January 31, | |

| | | 8/31/05 | | 2005 | | 2004 | | 2003 | | 2002 | | 2001 | |

| Per-Share Data | |

| Net asset value, common shares, beginning of period | | $ | 15.75 | | | $ | 15.66 | | | $ | 15.13 | | | $ | 14.67 | | | $ | 14.50 | | | $ | 13.17 | | |

| Operations: | |

| Net investment income | | | 0.59 | | | | 0.97 | | | | 1.02 | | | | 1.07 | | | | 1.04 | | | | 1.15 | | |

| Net realized and unrealized gains on investments | | | 0.19 | | | | 0.15 | | | | 0.52 | | | | 0.40 | | | | 0.12 | | | | 1.27 | | |

| Distributions to preferred shareholders: | |

| From net investment income | | | (0.10 | ) | | | (0.09 | ) | | | (0.07 | ) | | | (0.10 | ) | | | (0.18 | ) | | | (0.30 | ) | |

| Total from operations | | | 0.68 | | | | 1.03 | | | | 1.47 | | | | 1.37 | | | | 0.98 | | | | 2.12 | | |

| Distributions to common shareholders: | |

| From net investment income | | | (0.54 | ) | | | (0.94 | ) | | | (0.94 | ) | | | (0.91 | ) | | | (0.81 | ) | | | (0.79 | ) | |

| Net asset value, common shares, end of period | | $ | 15.89 | | | $ | 15.75 | | | $ | 15.66 | | | $ | 15.13 | | | $ | 14.67 | | | $ | 14.50 | | |

| Market value, common shares, end of period | | $ | 14.70 | | | $ | 14.92 | | | $ | 14.90 | | | $ | 14.60 | | | $ | 14.02 | | | $ | 13.80 | | |

| Selected Information | |

| Total return, common shares, net asset value (a) | | | 4.39 | % (f) | | | 6.84 | % | | | 9.98 | % | | | 9.58 | % | | | 6.92 | % | | | 16.58 | % | |

| Total return, common shares, market value (b) | | | 2.19 | % (f) | | | 6.83 | % | | | 8.77 | % | | | 11.06 | % | | | 7.77 | % | | | 25.44 | % | |

Net assets applicable to common shares at

end of period (in millions) | | $ | 91 | | | $ | 91 | | | $ | 90 | | | $ | 87 | | | $ | 84 | | | $ | 83 | | |

Ratio of expenses to average weekly net assets

applicable to commons shares (c) | | | 1.15 | % (e) | | | 1.23 | % | | | 1.18 | % | | | 1.23 | % | | | 1.17 | % | | | 1.23 | % | |

Ratio of net investment income to average weekly

net assets applicable to common shares (c) | | | 5.44 | % (e) | | | 5.73 | % | | | 6.65 | % | | | 7.19 | % | | | 7.11 | % | | | 8.00 | % | |

| Portfolio turnover rate | | | 13 | % | | | 36 | % | | | 34 | % | | | 18 | % | | | 9 | % | | | 35 | % | |

Remarketed preferred shares outstanding,

end of period (in millions) | | $ | 44 | | | $ | 44 | | | $ | 44 | | | $ | 44 | | | $ | 44 | | | $ | 44 | | |

Asset coverage per remarketed preferred

share (in thousands) (d) | | $ | 78 | | | $ | 77 | | | $ | 77 | | | $ | 75 | | | $ | 74 | | | $ | 73 | | |

Liquidation preference and market value per

remarketed preferred share (in thousands) | | $ | 25 | | | $ | 25 | | | $ | 25 | | | $ | 25 | | | $ | 25 | | | $ | 25 | | |

(a) Assumes reinvestment of distributions at net asset value.

(b) Assumes reinvestment of distributions at actual prices pursuant to the fund's dividend reinvestment plan.

(c) Ratios do not reflect the effect of dividend payments to preferred shareholders; income ratios reflect income earned on assets attributable to preferred shares, where applicable.

(d) Represents net assets applicable to common shares plus preferred shares at liquidation value divided by preferred shares outstanding.

(e) Annualized.

(f) Total return has not been annualized.

2005 Annual Report

American Municipal Income Portfolio

14

Schedule of INVESTMENTS

American Municipal Income Portfolio August 31, 2005

| Description of Security | | Principal

Amount | | Market

Value (a) | |

| (Percentages of each investment category relate to net assets applicable to outstanding common shares) | | | |

| Municipal Long-Term Securities - 131.3% | | | |

| Alabama - 0.8% | | | |

| Camden Industrial Development Board, Weyerhaeuser, (AMT) (Callable 12/1/13 at 100), 6.38%, 12/1/24 | | $ | 650,000 | | | $ | 715,754 | | |

| Arizona - 7.4% | | | |

| Douglas Community Housing Revenue, Rancho La Perilla (Callable 1/20/10 at 102), 6.13%, 7/20/41 | | | 990,000 | | | | 1,041,183 | | |

| Gilbert Industrial Development Authority, S.W. Student Services (Prerefunded 2/1/09 at 102), 5.85%, 2/1/19 (d) | | | 1,300,000 | | | | 1,433,640 | | |

| Gilbert Wastewater System and Development Revenue (Callable 10/1/09 at 100), 4.90%, 4/1/19 | | | 1,000,000 | | | | 1,007,660 | | |

| Pima County United School District (FGIC), 8.38%, 7/1/13 | | | 2,450,000 | | | | 3,257,985 | | |

| | | | 6,740,468 | | |

| Arkansas - 0.6% | | | |

| Washington County Hospital Revenue, Regional Medical Center (Callable 2/1/15 at 100), 5.00%, 2/1/30 | | | 500,000 | | | | 507,485 | | |

| California - 13.2% | | | |

| Alameda Corridor Transportation Authority, Zero-Coupon Bond (AMBAC), 5.72%, 10/1/30 (b) | | | 7,375,000 | | | | 2,356,829 | | |

California Statewide Communities Development Authority Revenue, L.A. Jewish Home

(Callable 11/1/13 at 100), 5.25%, 11/15/23 | | | 2,000,000 | | | | 2,145,800 | | |

| Golden State Tobacco Settlement (Callable 6/1/13 at 100), 5.50%, 6/1/33 | | | 1,500,000 | | | | 1,702,335 | | |

Pollution Control Financing Authority, Solid Waste Revenue, Waste Management Inc. Project, Series A-2, (AMT)

(Callable 4/1/15 at 101), 5.40%, 4/1/25 | | | 1,000,000 | | | | 1,045,070 | | |

Pollution Control Financing Authority, Solid Waste Revenue, Waste Management Inc. Project, Series B, (AMT)

(Callable 7/1/15 at 101), 5.00%, 7/1/27 | | | 500,000 | | | | 507,705 | | |

| State General Obligation (Callable 2/1/13 at 100), 5.00%, 2/1/21 | | | 1,500,000 | | | | 1,595,400 | | |

| State Public Works, Department of Mental Health - Coalinga (Callable 6/1/14 at 100), 5.50%, 6/1/19 | | | 2,000,000 | | | | 2,239,900 | | |

| Vernon California Electrical System, Malburg Generating System (Prerefunded 4/1/08 at 100), 5.50%, 4/1/23 (d) | | | 500,000 | | | | 532,245 | | |

| | | | 12,125,284 | | |

| Colorado - 12.1% | | | |

| Educational and Cultural Facilities Authority, The Classical Academy (Prerefunded 12/1/11 at 100), 7.25%, 12/1/30 (d) | | | 2,000,000 | | | | 2,425,100 | | |

| Health Facility Revenue Authority, Vail Valley Medical Center Project (Callable 1/15/15 at 100), 5.00%, 1/15/20 | | | 1,000,000 | | | | 1,047,130 | | |

| Northwest Parkway Public Highway Authority, Zero-Coupon Bond (AMBAC) (Callable 6/15/11 at 33.46), 6.29%, 6/15/29 (b) | | | 5,000,000 | | | | 1,318,000 | | |

| State Health Facilities Authority, Covenant Retirement Community (Callable 12/1/12 at 101), 6.13%, 12/1/33 | | | 1,000,000 | | | | 1,095,360 | | |

| State Health Facilities Authority, Evangelical Lutheran (Callable 10/1/12 at 100), 5.90%, 10/1/27 | | | 650,000 | | | | 709,254 | | |

State Housing and Financial Authority, Multifamily Housing Project - Class II, (AMT)

(Callable 4/1/12 at 100), 5.70%, 10/1/42 | | | 2,745,000 | | | | 2,880,246 | | |

| State Housing and Financial Authority, Solid Waste Revenue, Waste Management Inc. Project, (AMT), 5.70%, 7/1/18 | | | 1,000,000 | | | | 1,064,660 | | |

| Water Reserve and Power Development Authority, Clean Water Revenue (Callable 9/1/06 at 101), 5.90%, 9/1/16 | | | 135,000 | | | | 140,114 | | |

| Water Reserve and Power Development Authority, Clean Water Revenue (Prerefunded 9/1/06 at 101), 5.90%, 9/1/16 (d) | | | 365,000 | | | | 379,589 | | |

| | | | 11,059,453 | | |

| Florida - 1.3% | | | |

| Palm Beach County Facilities Authority, Abbey Delray South (Callable 10/1/13 at 100), 5.45%, 10/1/15 | | | 1,100,000 | | | | 1,178,045 | | |

| Georgia - 8.2% | | | |

| Fulton County Development Authority, Maxon Atlantic Station, (AMT) (Callable 3/1/15 at 100), 5.13%, 3/1/26 | | | 700,000 | | | | 702,989 | | |

| Municipal Electrical Authority (FGIC) (Escrowed to maturity), 6.50%, 1/1/12 (c) | | | 6,000,000 | | | | 6,773,160 | | |

| | | | 7,476,149 | | |

| Illinois - 8.8% | | | |

| Finance Authority, Friendship Village Schaumburg (Callable 2/15/15 at 100), 5.38%, 2/15/25 | | | 500,000 | | | | 509,075 | | |

| Health Facility Authority, Condell Medical Center (Callable 5/15/12 at 100), 5.50%, 5/15/32 | | | 500,000 | | | | 521,280 | | |

Health Facility Authority, Lutheran General Hospital,

7.00%, 4/1/08 | | | 775,000 | | | | 818,408 | | |

| 7.00%, 4/1/14 | | | 500,000 | | | | 610,690 | | |

| Health Facility Authority, Villa St. Benedict (Callable 11/15/13 at 101), 6.90%, 11/15/33 | | | 600,000 | | | | 636,000 | | |

| Metropolitan Pier and Exposition Authority, McCormick Place, Convertible, Zero-Coupon Bond (MBIA), 5.32%, 6/15/23 (b) | | | 6,115,000 | | | | 3,895,500 | | |

| Rockford Multifamily Housing Revenue, Rivers Edge Apartments, (AMT) (Callable 1/20/08 at 102), 5.88%, 1/20/38 | | | 1,000,000 | | | | 1,035,170 | | |

| | | | 8,026,123 | | |

| See accompanying Notes to Schedule of Investments. | |

2005 Annual Report

American Municipal Income Portfolio

15

Schedule of INVESTMENTS continued

American Municipal Income Portfolio (Continued)

| Description of Security | | Principal

Amount | | Market

Value (a) | |

| Indiana - 5.8% | | | |

| Health Facility Authority, Columbus Hospital (FSA), 7.00%, 8/15/15 | | $ | 2,670,000 | | | $ | 3,234,865 | | |

| Indianapolis Indiana Airport Authority, Fed Ex Corporation Project, (AMT), 5.10%, 1/15/17 | | | 1,000,000 | | | | 1,057,830 | | |

| St. Joseph County Hospital Facilities, Madison Center Obligated Group Project (Callable 2/15/15 at 100), 5.25%, 2/15/28 | | | 1,000,000 | | | | 1,036,210 | | |

| | | | 5,328,905 | | |

| Iowa - 5.2% | | | |

| Finance Authority, Friendship Haven Project, Series A (Callable 11/15/11 at 100), 6.13%, 11/15/32 | | | 800,000 | | | | 819,216 | | |

| Hospital Facilities Authority (Prerefunded 2/15/10 at 101), 6.75%, 2/15/15 (d) | | | 1,000,000 | | | | 1,153,180 | | |

Sheldon Health Care Facilities, Revenue Refunding Northwest Iowa Health Center

(Callable 3/1/06 at 100), 6.15%, 3/1/16 | | | 1,000,000 | | | | 1,002,260 | | |

State Higher Education Loan Authority, Simpson College (Callable 12/1/10 at 102),

5.00%, 12/1/27 | | | 430,000 | | | | 433,350 | | |

| 5.10%, 12/1/35 | | | 290,000 | | | | 291,337 | | |

| State Higher Education Loan Authority, Wartburg College (ACA) (Callable 10/1/12 at 100), 5.50%, 10/1/33 | | | 1,000,000 | | | | 1,066,280 | | |

| | | | 4,765,623 | | |

| Massachusetts - 1.7% | | | |

Boston Industrial Development Financing Authority, Crosstown Center Project, (AMT) (Callable 9/1/12 at 102),

6.50%, 9/1/35 | | | 500,000 | | | | 504,810 | | |

Health and Education Facility Authority, University of Massachusetts Memorial, Series D (Callable 7/1/15 at 100),

5.00%, 7/1/33 | | | 1,000,000 | | | | 1,011,560 | | |

| | | | 1,516,370 | | |

| Michigan - 12.8% | | | |

| Comstock Park Public Schools (FGIC), 7.88%, 5/1/11 | | | 3,145,000 | | | | 3,769,597 | | |

| Hospital Financing Authority, Daughters of Charity (Escrowed to maturity, callable 11/1/05 at 101), 5.25%, 11/1/15 (c) | | | 1,500,000 | | | | 1,519,140 | | |

| Kent Hospital Financial Authority, Butterworth Hospital (MBIA), 7.25%, 1/15/13 | | | 4,000,000 | | | | 4,672,240 | | |

| State General Obligation, Carrier Creek Michigan, District #326 (AMBAC) (Callable 6/1/15 at 100), 4.25%, 6/1/23 | | | 1,775,000 | | | | 1,780,538 | | |

| | | | 11,741,515 | | |

| Minnesota - 4.8% | | | |

| Glencoe Health Care Facilities, Glencoe Regional Health Services (Prerefunded 4/1/11 at 101), 7.50%, 4/1/31 (d) | | | 900,000 | | | | 1,078,389 | | |

| Maplewood Multifamily Revenue, Carefree Cottages II, (AMT) (FNMA) (Callable 4/15/14 at 100), 4.80%, 4/15/34 | | | 1,000,000 | | | | 1,013,340 | | |

| Marshall Health Care Facility, Weiner Medical Center (Callable 11/1/13 at 100), 6.00%, 11/1/28 | | | 500,000 | | | | 552,905 | | |

| Minneapolis Health Care System, Allina Health System, 6.00%, 11/15/23 | | | 565,000 | | | | 624,302 | | |

| State Agriculture and Economic Board, Health Care System (Callable 11/15/10 at 101), 6.38%, 11/15/29 | | | 30,000 | | | | 32,981 | | |

| State Agriculture and Economic Board, Health Care System (Prerefunded 11/15/10 at 101), 6.38%, 11/15/29 (d) | | | 970,000 | | | | 1,118,711 | | |

| | | | 4,420,628 | | |

| Missouri - 0.6% | | | |

Cape Girardeau County Industrial Development Authority, Southeast Hospital Association (Callable 6/1/12 at 100),

5.75%, 6/1/32 | | | 500,000 | | | | 527,070 | | |

| Nebraska - 0.7% | | | |

Educational Financial Authority Revenue, Midland Lutheran College, Series A (Callable 9/15/13 at 100),

5.60%, 9/15/29 | | | 600,000 | | | | 606,324 | | |

| Nevada - 1.1% | | | |

| State Department of Business and Industry, Las Ventanas Retirement Project (Callable 11/15/08 at 100), 6.00%, 11/15/14 | | | 250,000 | | | | 258,800 | | |

| State Department of Business and Industry, Las Ventanas Retirement Project (Callable 11/15/14 at 100), 6.75%, 11/15/23 | | | 750,000 | | | | 779,047 | | |

| | | | 1,037,847 | | |

| New Hampshire - 0.7% | | | |

| Health and Education Facility Authority, Speare Memorial Hospital (Callable 7/1/15 at 100), 5.88%, 7/1/34 | | | 600,000 | | | | 631,200 | | |

| New Mexico - 2.9% | | | |

Mortgage Finance Authority,

6.88%, 1/1/25 | | | 1,140,000 | | | | 1,149,895 | | |

| 6.50%, 7/1/25 | | | 830,000 | | | | 836,989 | | |

| 6.75%, 7/1/25 | | | 690,000 | | | | 696,776 | | |

| | | | 2,683,660 | | |

| See accompanying Notes to Schedule of Investments. | |

2005 Annual Report

American Municipal Income Portfolio

16

American Municipal Income Portfolio (Continued)

| Description of Security | | Principal

Amount | | Market

Value (a) | |

| New York - 2.9% | |

| New York City, Series B, 5.75%, 8/1/16 | | $ | 1,400,000 | | | $ | 1,565,536 | | |

| New York Water and Sewer System (Crossover refunded to 6/15/10 at 101), 6.00%, 6/15/33 (d) | | | 380,000 | | | | 428,583 | | |

| New York Water and Sewer System (Prerefunded to 6/15/10 at 101), 6.00%, 6/15/33 (d) | | | 620,000 | | | | 704,525 | | |

| | | | 2,698,644 | | |

| North Dakota - 2.1% | | | |

| Fargo Health Systems, Meritcare (Callable 6/1/10 at 101), 5.63%, 6/1/31 | | | 1,750,000 | | | | 1,915,707 | | |

| Ohio - 3.6% | |

Richland County Hospital Facilities, Medcentral Health System (Callable 11/15/10 at 101),

6.13%, 11/15/16 | | | 1,000,000 | | | | 1,098,630 | | |

| 6.38%, 11/15/30 | | | 1,000,000 | | | | 1,093,520 | | |

| Toledo - Lucas County Port Authority, Crocker Park Public Improvement Project (Callable 12/1/13 at 102), 5.25%, 12/1/23 | | | 500,000 | | | | 524,205 | | |

| Toledo - Lucas County Port Authority, St. Mary Woods Project, Series A (Callable 5/15/10 at 100), 6.00%, 5/15/24 | | | 600,000 | | | | 606,006 | | |

| | | | 3,322,361 | | |

| Pennsylvania - 3.0% | | | |

Chartiers Valley Industrial and Commercial Development Authority, Friendship Village South (Callable 8/15/10 at 100),

5.75%, 8/15/20 | | | 1,000,000 | | | | 1,034,750 | | |

Erie County Industrial Development Authority, Environmental Improvement Refunding International Paper Company

Project (AMT) (Callable 11/1/14 at 100), 5.00%, 11/1/18 | | | 650,000 | | | | 661,680 | | |

Montgomery County Industrial Development Authority, Whitemarsh Continuing Care (Callable 2/1/15 at 100),

6.25%, 2/1/35 | | | 1,000,000 | | | | 1,058,260 | | |

| | | | 2,754,690 | | |

| Puerto Rico - 1.2% | | | |

| Puerto Rico Public Finance Corporation (Callable 2/1/12 at 100), 5.75%, 8/1/27 | | | 1,000,000 | | | | 1,109,780 | | |

| South Carolina - 0.8% | |

State Jobs Economic Development Authority, Hospital Facility, Palmetto Health (Callable 8/1/13 at 100),

6.13%, 8/1/23 | | | 250,000 | | | | 277,323 | | |

| 6.38%, 8/1/34 | | | 375,000 | | | | 418,916 | | |

| | | | 696,239 | | |

| South Dakota - 4.1% | | | |

| Souix Falls Health Facilities, Dow Rummel Village Project (Callable 11/15/12 at 100), 6.63%, 11/15/23 | | | 620,000 | | | | 648,036 | | |

State Economic Development Finance Authority, Pooled Loan Program, Davis Family, (AMT) (Callable 4/1/14 at 100),

6.00%, 4/1/29 | | | 1,000,000 | | | | 1,040,730 | | |

State Economic Development Finance Authority, Pooled Loan Program, McEleeg S.D., (AMT) (Callable 4/1/14 at 100),

5.95%, 4/1/24 | | | 2,000,000 | | | | 2,080,500 | | |

| | | | 3,769,266 | | |

| Tennessee - 3.1% | | | |

| Johnson City Health and Education Facilities, Mountain States Health (Callable 7/1/12 at 103), 7.50%, 7/1/33 | | | 1,000,000 | | | | 1,192,580 | | |

| Shelby County Health, Education and Housing Facilities, Methodist Healthcare (Escrowed to maturity), 6.50%, 9/1/21 (c) | | | 240,000 | | | | 284,686 | | |

Shelby County Health, Education and Housing Facilities, Methodist Healthcare (Prerefunded 9/1/12 at 100),

6.50%, 9/1/21 (d) | | | 410,000 | | | | 486,703 | | |

Sullivan County Health, Education and Housing Facilities, Wellmont Health System Project (Callable 9/1/12 at 101),

6.25%, 9/1/32 | | | 750,000 | | | | 827,858 | | |

| | | | 2,791,827 | | |

| Texas - 16.6% | | | |

| Abilene Health Facility Development Revenue, Sears Methodist Retirement (Callable 5/15/09 at 101), 6.00%, 11/15/29 | | | 500,000 | | | | 509,115 | | |

| Abilene Health Facility Development Revenue, Sears Methodist Retirement (Callable 11/15/08 at 101), 5.88%, 11/15/18 | | | 1,150,000 | | | | 1,180,245 | | |

| Brazoria County Environmental Authority, Dow Chemical Project, (AMT) (Callable 5/15/12 at 100), 5.70%, 5/15/33 | | | 500,000 | | | | 544,895 | | |

| Brazos River Pollution Control Authority, Texas Utilities, (AMT) (Callable 4/1/13 at 101), 7.70%, 4/1/33 | | | 500,000 | | | | 601,515 | | |

| Brazos River Pollution Control Authority, TXU Energy, (AMT) (Callable 10/1/13 at 101), 6.75%, 10/1/38 | | | 715,000 | | | | 799,849 | | |

| Fort Bend Independent School District (Escrowed to maturity), 5.00%, 2/15/14 (c) | | | 1,000,000 | | | | 1,105,870 | | |

| Grand Prairie Independent School District (PSF) (Callable 8/15/11 at 100), 5.85%, 2/15/26 | | | 40,000 | | | | 44,762 | | |

| Grand Prairie Independent School District (PSF) (Prerefunded to 8/15/11 at 100), 5.85%, 2/15/26 (d) | | | 2,960,000 | | | | 3,365,046 | | |

| See accompanying Notes to Schedule of Investments. | |

2005 Annual Report

American Municipal Income Portfolio

17

Schedule of INVESTMENTS continued

American Municipal Income Portfolio (Continued)

| Description of Security | | Principal

Amount/

Shares | | Market

Value (a) | |

| Housing Finance Development Community Central, Villa De San Antonio (Callable 5/15/09 at 100), 6.00%, 5/15/25 | | $ | 1,000,000 | | | $ | 1,011,750 | | |

Houston Health Facilities Development Revenue, Retirement Facility, Buckingham Senior Living (Callable 2/15/14 at 101),

7.00%, 2/15/26 | | | 1,500,000 | | | | 1,664,235 | | |

| Richardson Hospital Authority, Richardson Regional Hospital (Callable 12/1/13 at 100), 6.00%, 12/1/34 | | | 2,500,000 | | | | 2,708,375 | | |

| Sam Rayburn Municipal Power Agency (RAAI) (Callable 10/1/12 at 100), 5.75%, 10/1/21 | | | 1,000,000 | | | | 1,114,160 | | |

| Tyler Health Facility, Mother Frances Hospital (Callable 7/1/13 at 100), 5.75%, 7/1/27 | | | 500,000 | | | | 533,025 | | |

| | | | 15,182,842 | | |

| Washington - 1.1% | | | |

| Skagit County Public Hospital District (Callable 12/1/13 at 101), 6.00%, 12/1/23 | | | 900,000 | | | | 984,969 | | |

| Wisconsin - 4.1% | | | |

| State Health and Educational Facility Authority, Attic Angel Obligated Group (Callable 11/15/08 at 102), 5.75%, 11/15/27 | | | 1,800,000 | | | | 1,803,024 | | |

| State Health and Educational Facility Authority, Beloit Hospital (Callable 7/1/06 at 100), 5.90%, 7/1/11 | | | 625,000 | | | | 625,875 | | |

| State Health and Educational Facility Authority, Synergyhealth Inc. (Callable 8/15/13 at 100), 6.00%, 11/15/23 | | | 500,000 | | | | 549,115 | | |

| State Health and Educational Facility Authority, Wheaton Fransiscan Services (Callable 2/15/12 at 101), 5.75%, 8/15/30 | | | 750,000 | | | | 809,813 | | |

| | | | 3,787,827 | | |

Total Municipal Long-Term Securities

(cost: $110,319,354) | | | | | | | 120,102,055 | | |

| Municipal Variable Rate Short-Term Securities (e) - 12.4% | | | |

| Connecticut - 0.5% | | | |

| Connecticut State, 2.35%, 9/1/05 | | | 500,000 | | | | 500,000 | | |

| Minnesota - 4.1% | | | |

| Guthrie Parking Ramp (Callable 10/1/05 at 100), 2.36%, 9/1/05 | | | 3,780,000 | | | | 3,780,000 | | |

| Missouri - 1.0% | | | |

| Missouri Health and Educational Facilities Authority, Cox Health System (AMBAC), 2.45%, 9/1/05 | | | 900,000 | | | | 900,000 | | |

| New York - 2.2% | | | |

| Transportation Authority, New York Dedicated Tax Fund (Callable 11/1/18 at 100), 2.43%, 9/1/05 | | | 2,000,000 | | | | 2,000,000 | | |

| South Carolina - 4.6% | | | |

| Piedmont Municipal Power Agency (MBIA) (Callable 1/1/33 at 100), 2.34%, 9/7/05 | | | 4,200,000 | | | | 4,200,000 | | |

Total Municipal Variable Rate Short-Term Securities

(cost: $11,380,000) | | | | | | | 11,380,000 | | |

Total Investments in Unaffiliated Securities

(cost: $121,699,354) | | | | | | | 131,482,055 | | |

| Affiliated Money Market Fund (f) - 2.3% | | | |

First American Tax Free Obligations Fund, Class Z

(cost: $2,102,205) | | | 2,102,205 | | | | 2,102,205 | | |

Total Investments in Securities (g) - 146.0%

(cost: $123,801,559) | | | | | | $ | 133,584,260 | | |

| See accompanying Notes to Schedule of Investments. | |

2005 Annual Report

American Municipal Income Portfolio

18

Notes to Schedule of Investments:

(a) Securities are valued in accordance with procedures described in note 2 in Notes to Financial Statements.

(b) For zero-coupon investments, the interest rate shown is the effective yield on the date of purchase.

(c) Escrowed to maturity issues are typically backed by U.S. government obligations. If callable, these bonds may still be subject to call at the call date and price indicated.

(d) Prerefunded issues are backed by U.S. government obligations. Crossover refunded issues are backed by the credit of the refunding issuer. In both cases, the bonds mature at the call date and price indicated.

(e) Securities have demand features which qualify them as short-term securities. The date disclosed is the next put date or interest rate reset date.

(f) Investment in affiliated security. This money market fund is advised by U.S. Bancorp Asset Management, Inc., which also serves as advisor for the fund. See note 5 in Notes to Financial Statements.

(g) On August 31, 2005, the cost of investments in securities for federal income tax purposes was $123,801,559. There are currently no material differences between tax cost and book cost of investments. The aggregate gross unrealized appreciation and depreciation of investments in securities, based on this cost were as follows:

| Gross unrealized appreciation | | $ | 9,782,701 | | |

| Gross unrealized depreciation | | | - | | |

| Net unrealized appreciation | | $ | 9,782,701 | | |

Porfolio abbreviations and definitions:

ACA–American Capital Access

AMBAC–American Municipal Bond Assurance Company

AMT–Alternative Minimum Tax. As of August 31, 2005, the aggregate market value of securities subject to the AMT was $16,256,743, which represents 17.8% of net assets applicable to common shares.

FGIC–Financial Guaranty Insurance Corporation

FNMA–Federal National Mortgage Association

FSA–Financial Security Assurance

MBIA–Municipal Bond Insurance Association

PSF–Permanent School Fund

RAAI–Radian Asset Assurance Inc.

2005 Annual Report

American Municipal Income Portfolio

19

Report of INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors and Shareholders

American Municipal Income Portfolio Inc.

We have audited the accompanying statement of assets and liabilities of American Municipal Income Portfolio Inc. (the fund), including the schedule of investments, as of August 31, 2005, and the related statements of operations and changes in net assets and the financial highlights for the periods indicated therein. These financial statements and financial highlights are the responsibility of the fund's management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the fund's internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the fund's internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounti ng principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of August 31, 2005, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of American Municipal Income Portfolio Inc., at August 31, 2005, the results of its operations, the changes in its net assets and the financial highlights for the periods indicated therein, in conformity with U.S. generally accepted accounting principles.

Minneapolis, Minnesota

October 7, 2005

2005 Annual Report

American Municipal Income Portfolio

20

NOTICE TO SHAREHOLDERS (Unaudited)

Annual Meeting Results

An annual meeting of the fund's shareholders was held on September 19, 2005. Each matter voted upon at that meeting, as well as the number of votes cast for, against or withheld, the number of abstentions, and the number of broker non-votes with respect to such matters, are set forth below.

(1) The fund's preferred shareholders elected the following directors:

| | | Shares

Voted "For" | | Shares Withholding

Authority to Vote | |

| Roger A. Gibson | | | 1,668 | | | | 2 | | |

| Leonard W. Kedrowski | | | 1,668 | | | | 2 | | |

(2) The fund's common and preferred shareholders, voting as a single class, elected the following directors:

| | | Shares

Voted "For" | | Shares Withholding

Authority to Vote | |

| Benjamin R. Field III | | | 5,572,977 | | | | 51,142 | | |

| Victoria J. Herget | | | 5,572,095 | | | | 52,024 | | |

| Richard K. Riederer | | | 5,566,445 | | | | 57,674 | | |

| Joseph D. Strauss | | | 5,572,220 | | | | 51,899 | | |

| Virginia L. Stringer | | | 5,563,595 | | | | 60,524 | | |

| James M. Wade | | | 5,572,095 | | | | 52,024 | | |

(3) The fund's common and preferred shareholders, voting as a single class, ratified the selection by the fund's board of directors of Ernst & Young LLP as the independent registered public accounting firm for the fund for the fiscal period ending August 31, 2005. The following votes were cast regarding this matter:

Shares

Voted "For" | | Shares

Voted "Against" | | Abstentions | | Broker

Non-Votes | |

| | 5,568,442 | | | | 20,761 | | | | 34,916 | | | | - | | |

Terms and Conditions of the Dividend Reinvestment Plan

As a shareholder, you may choose to participate in the Dividend Reinvestment Plan. It's a convenient and economical way to buy additional shares of the fund by automatically reinvesting dividends and capital gains. The plan is administered by EquiServe, the plan agent.

Eligibility/Participation

You may join the plan at any time. Reinvestment of distributions will begin with the next distribution paid, provided your request is received at least 10 days before the record date for that distribution.

If your shares are in certificate form, you may join the plan directly and have your distributions reinvested in additional shares of the fund. To enroll in this plan, call EquiServe at 800.426.5523. If your shares are registered in your brokerage firm's name or another name, ask the holder of your shares how you may participate.

Banks, brokers or nominees, on behalf of their beneficial owners who wish to reinvest dividend and capital gains distributions, may participate in the plan by informing EquiServe at least 10 days before the next dividend and/or capital gains distribution.

Plan Administration

Beginning no more than five business days before the dividend payment date, EquiServe will buy shares of the fund on the New York Stock Exchange or elsewhere on the open market.

2005 Annual Report

American Municipal Income Portfolio

21

NOTICE TO SHAREHOLDERS (Unaudited) continued

The fund will not issue any new shares in connection with the plan. All reinvestments will be at a market price plus a pro rata share of any brokerage commissions, which may be more or less than the fund's net asset value per share. The number of shares allocated to you is determined by dividing the amount of the dividend or distribution by the applicable price per share.

There is no direct charge for reinvestment of dividends and capital gains, since EquiServe fees are paid for by the fund. However, each participant pays a pro rata portion of the brokerage commissions. Brokerage charges are expected to be lower than those for individual transactions because shares are purchased for all participants in blocks. As long as you continue to participate in the plan, distributions paid on the shares in your account will be reinvested.

EquiServe maintains accounts for plan participants holding shares in certificate form and will furnish written confirmation of all transactions, including information you need for tax records. Reinvested shares in your account will be held by EquiServe in noncertificated form in your name.

Tax Information

Distributions invested in additional shares of the fund are subject to income tax, to the same extent as if received in cash. Shareholders, as required by the Internal Revenue Service, will receive a Form 1099-DIV regarding the federal tax status of the prior year's distributions.

Plan Withdrawal

If you hold your shares in certificate form, you may terminate your participation in the plan at any time by giving written notice to EquiServe. If your shares are registered in your brokerage firm's name, you may terminate your participation via verbal or written instructions to your investment professional. Written instructions should include your name and address as they appear on the certificate or account.

If notice is received at least 10 days before the record date, all future distributions will be paid directly to the shareholder of record.

If your shares are issued in certificate form and you discontinue your participation in the plan, you (or your nominee) will receive an additional certificate for all full shares and a check for any fractional shares in your account.

Plan Amendment/Termination

The fund reserves the right to amend or terminate the plan. Should the plan be amended or terminated, participants will be notified in writing at least 90 days before the record date for such dividend or distribution. The plan may also be amended or terminated by EquiServe with at least 90 days written notice to participants in the plan.

Any questions about the plan should be directed to your investment professional or to EquiServe Trust Company, N.A., P.O. Box 43010, Providence, RI, 02940-3010, 800.426.5523.

Tax Information

The following per-share information describes the federal tax treatment of distributions made during the fiscal period. Exempt-interest dividends are exempt from federal income tax and should not be included in your gross income, but need to be reported on your income tax return for information purposes. Please consult a tax advisor on how to report these distributions at the state and local levels.

2005 Annual Report

American Municipal Income Portfolio

22

Common Share Income Distributions (income from tax-exempt securities, 100.0% qualifying as exempt-interest dividends)

| Payable Date | | Amount | |

| February 23, 2005 | | $ | 0.0780 | | |

| March 23, 2005 | | | 0.0780 | | |

| April 27, 2005 | | | 0.0780 | | |

| May 25, 2005 | | | 0.0780 | | |

| June 22, 2005 | | | 0.0750 | | |

| July 27, 2005 | | | 0.0750 | | |

| August 24, 2005 | | | 0.0750 | | |

| Total | | $ | 0.5370 | | |

Preferred Share Income Distributions (income from tax-exempt securities, 100.0% qualifying as exempt-interest dividends)

| Payable Date | | Amount | |

| Total class "T" | | $ | 311.50 | | |

| Total class "TH" | | $ | 314.24 | | |

How to Obtain a Copy of the Fund's Proxy Voting Policies and Proxy Voting Record

A description of the policies and procedures that the fund uses to determine how to vote proxies relating to portfolio securities, as well as information regarding how the fund voted proxies relating to portfolio securities during the most recent 12 month period ended June 30, is available (1) without charge upon request by calling 800.677.FUND; (2) at www.firstamericanfunds.com; and (3) on the U.S. Securities and Exchange Commission's website at http://www.sec.gov.

Form N-Q Holdings Information

The fund is required to file its complete schedule of portfolio holdings for the first and third quarters of each fiscal year with the Securities and Exchange Commission on Form N-Q. The fund's Forms N-Q are available (1) without charge upon request by calling 800.677.FUND and (2) on the U.S. Securities and Exchange Commission's website at http://www.sec.gov. In addition, you may review and copy the fund's Forms N-Q at the Commissions Public Reference Room in Washington D.C. You may obtain information on the operation of the Public Reference Room by calling 1-800-SEC-0330.

Certifications

In October 2005, the fund's Chief Executive Officer submitted to the New York Stock Exchange ("NYSE") his annual certification required under Section 303A.12(a) of the NYSE corporate governance rules. The certifications of the fund's Principal Executive Officer and Principal Financial Officer required pursuant to Rule 30a-2 under the 1940 Act are filed with the fund's Form N-CSR filings and are available on the U.S. Securities and Exchange Commission's website at http://www.sec.gov.

2005 Annual Report

American Municipal Income Portfolio

23

NOTICE TO SHAREHOLDERS (Unaudited) continued

Directors and Officers of the Fund

Independent Directors

Name, Address, and

Year of Birth | |

Position(s)

Held with

Fund | |

Term of Office and

Length of Time Served | |

Principal Occupation(s)

During Past 5 Years | |

Number of Portfolios

in Fund Complex

Overseen by Director | | Other

Directorships

Held by

Director† | |

Benjamin R. Field III

P.O. Box 1329

Minneapolis, MN 55440-1329

(1938) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since September 2003. | | Retired; Senior Financial Advisor, Bemis Company, Inc. from May 2002 through March 2003; Senior Vice President, Chief Financial Officer and Treasurer, Bemis, through April 2002. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

Roger A. Gibson

P.O. Box 1329

Minneapolis, MN 55440-1329

(1946) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since August 1998. | | Retired; Vice President, Cargo–United Airlines, from July 2001 through July 2004; Vice President, North America-Mountain Region, United Airlines, prior to July 2001. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

Victoria J. Herget

P.O. Box 1329

Minneapolis, MN 55440-1329

(1951) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since September 2003. | | Investment consultant and non-profit board member since 2001; Managing Director of Zurich Scudder Investments, through 2001. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

Leonard W. Kedrowski

P.O. Box 1329

Minneapolis, MN 55440-1329

(1941) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since August 1998. | | Owner and President, Executive and Management Consulting, Inc., a management consulting firm; Board member, GC McGuiggan Corporation (dba Smyth Companies), a label printer; former Chief Executive Officer, Creative Promotions International, LLC, a promotional award programs and products company, through October 2003; Advisory Board member, Designer Doors, manufacturer of designer doors, through 2002. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

Richard K. Riederer

P.O. Box 1329

Minneapolis, MN 55440-1329

(1944) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since August 2001. | | Retired; Director, President, and Chief Executive Officer, Weirton Steel, through 2001. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | Cleveland-Cliffs Inc (a producer of iron ore pellets) | |

|

Joseph D. Strauss

P.O. Box 1329

Minneapolis, MN 55440-1329

(1940) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since August 1998. | | Owner and President, Strauss Management Company, a Minnesota holding company for various organizational management business ventures; owner, Chairman, and Chief Executive Officer, Community Resource Partnerships, Inc., a company engaged in strategic planning, operations management, government relations, transportation planning, and public relations; attorney at law; Partner and Chairman, ExcensusTM, LLC, a demographic services company. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

Virginia L. Stringer

P.O. Box 1329

Minneapolis, MN 55440-1329

(1944) | | Chair; Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Chair term three years, assuming reelection as a director. Chair of XAA's board since 1998; current term expires September 2006. Director of XAA since August 1998. | | Owner and President, Strategic Management Resources, Inc., a management consulting firm; Executive Consultant for State Farm Insurance Cos. through 2003. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

James M. Wade

P.O. Box 1329

Minneapolis, MN 55440-1329

(1943) | | Director | | Directors serve for a one-year term that expires at the next annual meeting of shareholders. Director of XAA since August 2001. | | Owner and President, Jim Wade Homes, a homebuilding company, since 1999. | | First American Funds Complex: eleven registered investment companies, including fifty-five portfolios | | None | |

|

†Includes only directorships in a company with a class of securities registered pursuant to Section 12 of the Securities Exchange Act or subject to the requirements of Section 15(d) of the Securities Exchange Act, or any company registered as an investment company under the Investment Company Act.

2005 Annual Report

American Municipal Income Portfolio

24

Officers

Name, Address, and

Year of Birth | | Position(s)

Held with

Fund | |

Term of Office and Length of Time Served | |

Principal Occupation(s) During Past 5 Years | |

Thomas S. Schreier, Jr.

U.S. Bancorp Asset

Management, Inc.

800 Nicollet Mall

Minneapolis, MN 55402