UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of |

| May 2005 |

|

|

|

Commission File Number |

| 0-24096 |

QUEENSTAKE RESOURCES LTD.

999 18th Street, Suite 2940, Denver, CO 80202

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40 F.

Form 20-F ý Form 40 F o

Indicate by check mark whether by furnishing the information contained in this Form the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes o No ý

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b):

DOCUMENTS FILED: | 2004 Annual Report | |

DESCRIPTION: | Queenstake Resources 2004 Annual Report |

2

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

| QUEENSTAKE RESOURCES LTD. | ||||

|

| (Registrant) | ||||

|

|

| ||||

Date | May 19, 2005 |

| By | “Dorian L. Nicol” (signed) | ||

|

| (Signature) | ||||

|

|

| ||||

|

|

| Dorian L. Nicol, President & CEO |

| ||

3

Queenstake

|

|

|

|

|

Producing Gold, Growth and Value

2004 Annual Report

Resources

In Brief

• Acquired Jerritt Canyon Mine in northern Nevada, July 2003

• Queenstake at one stroke became a mid-tier gold company

• Now sixth largest U.S. gold producer

• Long-term production of 275,000 ounces or more per year

• Five-year mine life – and growing

• Highly prospective 100-square-mile exploration district

• Historical exploration success: 18 deposits found in 24 years

• All mines in northern half: southern half hardly explored

• Established significant southern deposit in 2004

• Unhedged

• Trades on TSX: QRL; Amex: QEE

• Important Milestones

• Jerritt Canyon produced its seven millionth ounce after 24 years of operation

• Worked more than 1.4 million man hours since September 2003 without a lost-time accident

• Mine Development Now Well Ahead of Early 2004

• Development footage increased 93% over 2003

• Two new deposits developed

• Collared Steer Mine portal and tunneled 2,250 feet to reach reserves and resources

• Tunneled 1,500 feet to Mahala deposit, accessed via the Smith Mine portal

• Constructed surface support facilities at Steer in preparation for full scale mining

• Disappointing Production Results

• Produced 243,300 ounces of gold vs. planned 300,000 ounces

• Total cash operating costs were $336 per ounce, vs. planned $275

• Development now sufficiently advanced to forecast increased production of 275,000 ounces for 2005

• Aggressive and Successful Exploration Program

• Completed 300,000 feet (57 miles) of drilling in more than 400 holes

• Increased reserves 54%, after depletion, to 875,000 ounces of gold

• Established a new gold deposit at Starvation Canyon

• Fourth largest gold exploration program in Nevada: $10.4 million

• Successful Financing to Support Mine Development, Reduce Debt

• Completed equity financing of $12.2 million, net of commissions

• Eliminated $20.0 million long-term debt and $9.0 million in royalties

• Reclamation liability remains fully funded

• Sold Magistral property in Mexico for $9 million

• Listed on the American Stock Exchange, symbol QEE

1

The reliability of the equipment we acquired mid 2003 was much lower than we anticipated. Overdue maintenance and new equipment is steadily improving availability.

|

| 2004 |

| 2003(1) |

| 2002(2) |

|

Gold production (000 ounces) |

| 243.3 |

| 150.0 |

| — |

|

Gold sales (000 ounces) |

| 245.7 |

| 146.8 |

| — |

|

Average realized gold price ($/ounce) |

| 398 |

| 377 |

| — |

|

Cash operating costs (3) ($/ounce) |

| 336 |

| 270 |

| — |

|

Revenue ($ millions) |

| 97.8 |

| 54.9 |

| — |

|

Net loss ($ millions) |

| (22.1 | ) | (7.8 | ) | (1.1 | ) |

Per common share, basic and diluted ($) |

| (0.06 | ) | (0.04 | ) | (0.02 | ) |

Net cash provided by (used in) operations ($ millions) |

| 15.2 |

| 13.5 |

| (0.8 | ) |

Market capitalization at year-end ($ millions) |

| 164 |

| 205.7 |

| 13.4 |

|

Share price at year-end (C $) |

| 0.475 |

| 0.740 |

| 0.310 |

|

Total assets ($ millions) |

| 87.9 |

| 97.9 |

| 4.6 |

|

All dollar amounts used in this annual report are in U.S. dollars unless otherwise specified.

(1) Six months of operations, July to December 2003

(2) Queenstake had no commercial production in 2002

(3) See reconciliation of cash operating costs per ounce to GAAP operating costs on page 28

Forward-Looking Statements - This Annual Report contains “Forward-Looking Statements” within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended and the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, included in this annual report about Queenstake’s future plans, are forward-looking statements that involve various risks and uncertainties. There can be no assurance that such statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements are based on the estimates and opinions of management on the date the statements are made, and Queenstake does not undertake any obligation to update forward-looking statements should conditions or management’s estimates or opinions change.

2

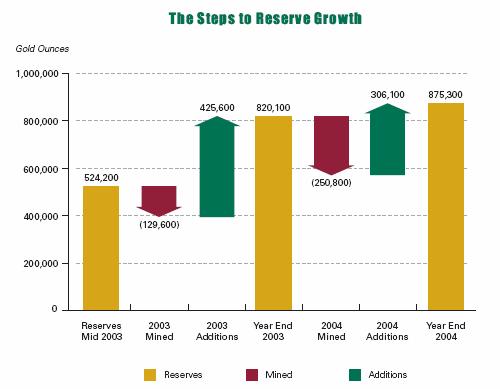

(Mined ounces do not equal gold production due to recovery process losses and estimations.)

Since mid 2003, when Queenstake acquired Jerritt Canyon, over 730,000 ounces have

been added to reserves and about 380,000 ounces mined or depleted.

This is an increase in reserves of 67% in 18 months, after replacing ounces mined.

Table of Contents

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

3

Dorian L. (Dusty) Nicol

President & Chief Executive Officer

Dear Fellow Shareholder,

A Year of Mixed Results

The past year has had its ups and downs for the management team at Queenstake. The production disappointments masked our considerable achievements which confirmed the underlying value of the Jerritt Canyon Mine and our reasons for acquiring it.

We acquired the mine mid 2003, several years after the previous owners had made the decision to mine out and close the property by the end of 2004. Understandably with making this decision, they invested no money in the mine beyond the short term operating requirements. Equipment was maintained, but long-overdue overhauls were not done, and development to access the immediate underground mining areas was carried out on a limited basis, but the search for and development of new areas to mine was not.

Learning from Our Mistakes

We knew that a major investment had to be made in developing access to the mineral resources in order to continue mining, and that we had to add new reserves to extend the limited mine-life we inherited. We made the investment and continue to do so, and we are beginning to see the benefits. However, we made two basic mistakes in the first 18 months after acquiring Jerritt Canyon:

First, we did not realize that we would not be able to develop new mining areas fast enough while still mining other areas – logistics limited the work we could do. Hence, production was constrained by the lower tonnage mined and we missed our 300,000-ounce gold production target by nearly 57,000 ounces. Consequently, our cash operating cost was $336 per ounce versus a planned $275 per ounce, principally because of the mine’s fixed costs being spread over fewer ounces produced.

Second, we met production and cost targets for the second half of 2003, the first six months that we operated Jerritt Canyon. This gave us a false sense of optimism when making our forecast for 2004. We did not recognize that our targets were unrealistic. Also, we did not include sufficient contingency for the setbacks all mines can face. Our setbacks came by way of an exceptional winter snowfall, equipment failures well beyond what we anticipated due to lack of long-term maintenance by the previous owners, difficulties in efficiently developing and accessing new mining areas, and a number of smaller events that were significant on a cumulative basis.

We should have foreseen and planned for the main issues. We should have been more realistic as these issues unfolded. We should have better managed investor expectations. That is the bad news.

4

In 2003, we acquired an operating mine, its resources and all the infrastructure for approximately $50 million. The mill alone would cost well over $100 million to replace today. Here, tailings pond water is being evaporated at the mill.

The Good News

The good news is that we believe the turnaround is underway, based on our considerable successes in 2004:

• Mining equipment and mill availability has improved.

• Developed mining areas have increased 25% and we continue to develop more.

• The new Steer Mine has been developed, as has the Mahala extension to the Smith Mine.

• Jerritt Canyon had estimated reserves of 875,000 ounces at the end of 2004, representing an addition of 730,000 ounces (including what we have mined) since our purchase of the mine.

• The mine had measured and indicated resources estimated at 2.4 million ounces (including reserves) at the end of 2004, indicating a minimum five-year mine life. There are additional inferred resources of 0.9 million ounces and many exploration opportunities to further extend that life.

• Our exploration team discovered high-grade gold mineralization at Starvation Canyon, reinforcing our belief that the underexplored southern half of the property is highly prospective.

• Employees of the Jerritt Canyon Mine worked 1.4 million man-hours without a lost-time accident since September 2003.

• We completed the $20 million repayment of an acquisition loan ahead of schedule.

• We eliminated production royalties for $9 million.

The Best Place to Find a Mine ...

We believe there are more orebodies to be found on our property. Jerritt has hosted 18 mines in its 24-year life, accounting for over seven million ounces of production, and there are many other mines nearby in the world-renowned Carlin Trend. The old saying that “the best place to find a mine is near a mine” is based on the fact that the mineralizing fluids that created one orebody often find other faults to create nearby deposits. Our property has many such faults as evidenced by the broken nature of the topography (see the photograph on the inside front cover). It is our job to find where else the gold has been deposited, such as at Starvation Canyon.

In searching for that gold, we have the advantage of over 24 years of geological data. We also have an increasing knowledge of what controls the formation of ore deposits on our property and how to explore for them more effectively. More importantly, we have a superb exploration team with a phenomenal track record of discovery at Jerritt Canyon and elsewhere. That team will continue to discover more gold at our mine.

5

Ore is hauled from the mine portals to the mill in 150-ton trucks. While mined tonnage fell short of target in 2004 due to the logistical constraints of essential development work, we are now catching up and expect to meet our forecast in 2005.

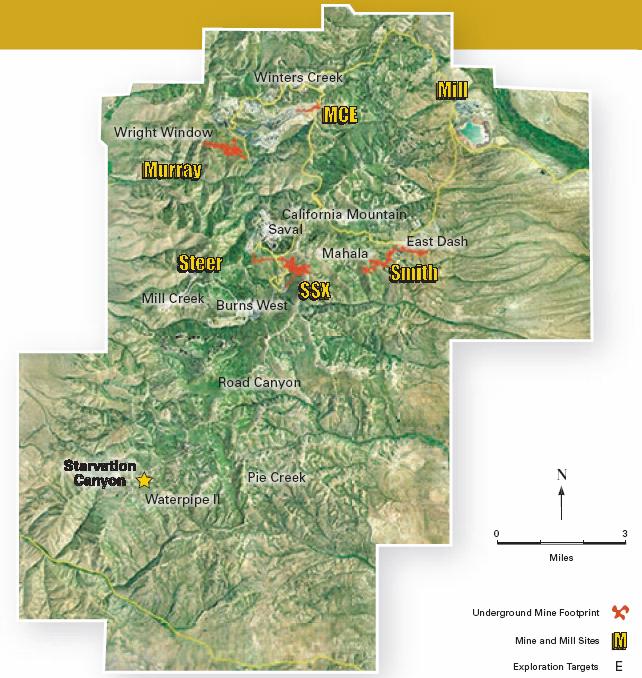

Starvation Canyon

Historically, there has been much less exploration in the southern half of the Jerritt Canyon District than the northern half, which hosts the deposits that have produced over seven million ounces of gold to date. Previous owners did identify a number of mineralized areas in the southern half, but their exploration programs consisted principally of wide-spaced drilling focused on potential open-pit targets. When none were recognized, exploration in that part of the District essentially ceased and was not pursued until Queenstake’s acquisition and our aggressive program.

One of the mineralized areas recognized by previous owners was Starvation Canyon, about 17 miles southwest of our mill. Gold mineralization was discovered that was geologically similar to other Jerritt Canyon deposits, but when it did not appear amenable to open pit mining, it was not followed up.

Using the results of the previous work in the Starvation Canyon area, we began the search for high-grade deposits that could be mined from underground. Drilling in 2004 found significant thicknesses of high-grade gold mineralization and the mineralization was expanded. We have now demonstrated an indicated resource currently estimated at 156,000 ounces; this is not yet included in our reserves. The mineralized zones that host this deposit have not been fully delineated and have the potential for significant expansion. The deposit should be readily accessible by a horizontal ramp from the nearby canyon wall.

Drilling in 2005 is expected to increase and upgrade the resource at Starvation Canyon, as well as begin testing other parts of the exciting 4 1/2 -mile mineralized trend, which includes this deposit.

The Underexplored Half of the Property

This discovery of high-grade gold mineralization validates one of our reasons for the acquisition: There is gold to be found in the underexplored southern half of the property. And why shouldn’t it be there? It has the same geology as the northern half where seven million ounces have been produced, and where there is still more to be mined.

At the time of acquiring Jerritt Canyon, our optimism for its potential was mirrored by the enthusiasm of the mining and exploration people at site and not just for the sake of their continued employment. (They are of such a high caliber that they would have been welcomed at almost any mine in Nevada). Like us, they knew there was much more gold to be found.

The Next Stage of Evolution

I was asked to take over as CEO in March 2005. My past role as Vice President and a Director of the Company since 1999, together with my exploration background, will allow me to help guide Queenstake through the next stage of its evolution, namely, to turn Jerritt Canyon into a profitable operation and to find other orebodies within our highly prospective 100-square-mile property.

6

As this annual report goes to press, our projection for 2005 is that we will produce 275,000 ounces of gold. However, we are currently updating the mine plan and budget in order to reflect a review of our forecasting procedures as well as recent drill data. Because of seasonal slowness during winter, we expect to produce 45% of the ounces in the first half of the year, biased towards the second quarter, and 55% in the second half. At the moment we do not want to forecast a total cash operating cost per ounce until we have a better feel for the timing of operational improvements, but it should be below 2004’s cost of $336 an ounce. On a longer-term basis, our projection is that we will produce 275,000 ounces or more per year.

I realize the disappointments in 2004 have undermined our credibility with investors. However, I believe our achievements during the year reinforce the underlying value of Jerritt Canyon and Queenstake. Unfortunately, it will take several quarters of performing to expectations before the market will give us credit for our reserves and resources, our ability to be profitable, the upside potential for discoveries on the property, and our mid-tier producer status. We will work hard to meet our targets.

2004 Achievements

• Significantly increased access to mining areas

• Developed two new orebodies near existing mines

• Increased reserves nearly 7%, after depletion

• Improved mill and equipment availability

• Discovered high-grade deposit in southern section of property

• Worked safely for 18 months

• Repaid $20 million acquisition loan

• Eliminated royalties for $9 million

2005 Objectives

• Produce 275,000 ounces gold, subject to updated information

• Total cash costs to be less than 2004

• Lower corporate overhead

• Continue exploration of high priority targets

• Expand and upgrade the Starvation Canyon resource

• Plan for long-term production of over 275,000 ounces per year

Our Thanks

My thanks and that of the Board goes to the people at Queenstake for their continued hard work and support. They experienced the difficulties of 2004 and together we got through them. Of greater importance, they brought about the achievements during the year that are helping to turn the Company around.

And our thanks to you, our shareholders, for your support. Queenstake has come a long way in the 18 months since we acquired Jerritt Canyon and became a mid-tier gold producer. As you can see by 2004’s achievements, we are demonstrating that the potential and the value are there to be realized.

In Jerritt Canyon, we believe we have a mine with a long and profitable life.

Yours Sincerely, |

|

|

Dorain L. (Dusty) Nicol |

President and Chief Executive Officer |

|

April 6, 2005 |

7

Ore awaits being hauled from the SSX Mine to the mill. Three of the four underground mines are accessed by ramps from the bottom of mined-out open pits. We follow the mineralization below the economic depths of the pits and elsewhere underground.

Jerritt Canyon

The Jerritt Canyon Mine consists of four separate ramp-accessed underground mines: the Murray, SSX, Steer, and Smith. None of the mines exceed 1,000 feet in depth measured from the elevations at their portals. Underground mining is trackless, using low profile 6-cubic-yard load/haul/dump tractors (LHD) loading 35- and 40-ton trucks for ore removal. Ground support is typically rock bolts and shotcrete, with cemented back-fill in mined areas.

All underground ore is stacked near the mine portals for grade sampling. It is then transported in 150-ton trucks to the central processing facility for drying, grinding, roasting, carbon-in-leach (CIL) processing, and refining. High quality doré bars are shipped for commercial refining to fine gold.

Total Production: 24-Year History

|

| Tons |

| Ounces(1) |

| Grade |

|

|

| (000) |

| (000) |

| (oz/t) |

|

|

|

|

|

|

|

|

|

Open-Pit Production – 12 Mines (mined out) |

| 35,554.3 |

| 5,393.1 |

| 0.152 |

|

|

|

|

|

|

|

|

|

Underground Mine Production |

|

|

|

|

|

|

|

SSX |

| 2,903.2 |

| 894.3 |

| 0.308 |

|

Murray |

| 3,575.6 |

| 1,197.5 |

| 0.335 |

|

Smith (including new Mahala deposit) |

| 653.2 |

| 186.3 |

| 0.285 |

|

Steer (new) |

| 29.9 |

| 5.6 |

| 0.187 |

|

West Generator (previously mined out) |

| 460.1 |

| 108.1 |

| 0.235 |

|

MCE (mined out in 2004) |

| 258.3 |

| 95.4 |

| 0.369 |

|

|

|

|

|

|

|

|

|

Underground Production – 6 Mines |

| 7,622.0 |

| 2,391.9 |

| 0.314 |

|

|

|

|

|

|

|

|

|

TOTAL – 18 Mines |

| 43,176.3 |

| 7,785.0 |

| 0.180 |

|

(1) Before process recovery losses

8

The Jerritt Canyon Property

Four mines supplied feed to the mill in 2004. MCE was mined-out in the year as the Steer Mine and the Mahala deposit at Smith were being developed for production. In all, 18 mines – 12 open-pit – have been operated over the past 24 years. Many targets await exploration.

9

2004: Major Changes and Improvements

During 2004 we mined over 1.1 million tons from the underground mines and recovered and sold 243,300 ounces of gold.

Production in 2004 fell well short of plan and we have identified and addressed the critical operating issues. We have gained considerable knowledge in how best to develop our new mines while continuing to extract ore from the existing ones, and we are improving key areas on a continuing basis. An impending mine-closing situation was inherited from the previous owners in July 2003 – the operation was being prepared for shutdown in December 2004. In the past 18 months we have been running hard to catch up on the development of mining areas, or stopes, and to provide ore beyond 2004 at a higher-grade mill feed than using the low-grade stockpile.

In the fall of 2003 when we were compiling our operating plan for 2004, we underestimated two key elements of the plan:

• Availability of the mining fleet and the mill due to the cost-saving approach to maintenance as the mine neared closure; and

• The logistical constraints of a major underground development program working in tandem with normal mining operations – such as the volume of mine traffic.

Our results for the year, though disappointing, benefited from the skills and resources of the mine personnel who are Jerritt Canyon. With their commitment and hard work we accomplished major changes and improvements. The benefits were felt in 2004 and are being realized more fully in 2005. We have done and continue to do the following:

• Strengthen the operating and management teams

• Upgrade and replace older mining equipment to improve productivity and operating costs

• Upgrade site communications and computer systems

• Began construction of the new Steer Mine’s support facilities, such as the maintenance building

• Aggressively explore around the mine areas, including:

• Resource-to-reserve conversion drilling

• Development at each of the operating mines, nearly doubling the footage of 2003.

Ore mined in 2004 exceeded the combined 2003 tonnage of the previous owners and Queenstake. However, the ore grade was lower than anticipated, yielding 8% less ounces mined.

In 2005, underground ore production is targeted at 2004 production levels. Ore grade mined in 2004 averaged 0.253 oz/ton, which is below 2003 levels, and grades for 2005 are targeted to be slightly above 2004.

10

Drilling is underway to define reserves at the Smith Mine where the recently discovered Mahala deposit was developed in 2004. Mahala already contains over 80,000 ounces of reserves and there is more gold to be discovered.

Production Statistics

|

| Jan – June 2003 |

| July – Dec 2003 |

| 2003 |

| 2004 |

| 2005 |

|

|

| (pre Queenstake) |

| (Queenstake) |

|

|

|

|

|

|

|

Ore mined (tons) |

| 551,187 |

| 544,341 |

| 1,095,528 |

| 1,144,214 |

| 1,140,000 |

|

Waste mined (tons) |

| 185,015 |

| 206,423 |

| 391,438 |

| 495,998 |

| 385,000 |

|

Total tons mined |

| 736,202 |

| 750,764 |

| 1,486,966 |

| 1,640,212 |

| 1,525,000 |

|

Average grade mined (oz/t) |

| 0.285 |

| 0.288 |

| 0.287 |

| 0.253 |

| 0.259 |

|

Gold mined (oz) |

| 157,193 |

| 156,982 |

| 314,175 |

| 289,436 |

| 295,000 |

|

Stockpile used (tons) |

| 178,126 |

| 222,787 |

| 400,913 |

| 161,619 |

| 310,000 |

|

Process throughput (tons) |

| 729,313 |

| 767,128 |

| 1,496,441 |

| 1,305,833 |

| 1,450,000 |

|

Grade processed (oz/t) |

| 0.230 |

| 0.221 |

| 0.225 |

| 0.214 |

| 0.217 |

|

Process recovery (%) |

| 88.2 |

| 88.5 |

| 88.3 |

| 86.6 |

| 86.9 |

|

Gold produced (oz) |

| 152,095 |

| 150,001 |

| 302,096 |

| 243,333 |

| 275,000 |

|

Mine development (feet) |

| 3,221 |

| 4,207 |

| 7,428 |

| 14,302 |

| 11,300 |

|

(1) Subject to ongoing review

Safety and the Environment: Two Milestones

Queenstake’s and Jerritt Canyon’s commitment to safety are reflected in our ongoing high standard of safety performance. In October 2004, Jerritt surpassed the milestone of one million man-hours worked since September 2003 with no lost time accidents, a record that continues to grow.

An environmental milestone was reached in 2004 with the five-year renewal of major environmental permits.

Mine Development

As planned, mine development footage in 2004 was nearly double 2003’s footage. We knew we had to catch up on development to continue operating the mine after the previously planned December 2004 closure target. The 2004 development program is already providing improved access to mining areas. Unfortunately, this high level of development impeded mining operations, and was in part the cause of the year’s disappointing results.

Mine development footage targeted for 2005, though less than 2004, is 50 percent over 2003’s level. We believe 2005’s planned footage will allow efficient mining operations while still adding to developed tonnage for future mining.

11

Two New Production Areas: Steer and Mahala

Two new production areas were developed in 2004: the new Steer Mine adjacent to the SSX Mine, and the Mahala extension – a new area within the Smith Mine underground complex. Both areas provide access to new ore for 2005, as well as to opportunities for the discovery of new reserves. The Steer Mine construction includes a four-bay maintenance shop, an office and change house, and a fuel depot, which will be completed in 2005.

Developmental production from the new Steer Mine replaced production from the depleted MCE Mine in the second half of 2004. Although Steer is currently accessed from its own portal, ongoing development in 2005 will join the Steer and SSX mines. This connection will:

• Provide required ventilation and emergency escapeway;

• Improve operating efficiency;

• Improve access for drilling;

• Facilitate ongoing development and mining of the SSX and Steer ore bodies; and

• Facilitate the conversion of mineral resources to reserves for both mines.

Gold Reserves (1),(2)

|

| PROVEN |

| PROBABLE |

| TOTAL |

| ||||||||||||

MINE |

| Tons |

| Grade |

| Gold |

| Tons |

| Grade |

| Gold |

| Tons |

| Grade |

| Gold |

|

|

| (000) |

| (oz/t) |

| (000 oz) |

| (000) |

| (oz/t) |

| (000 oz) |

| (000) |

| (oz/t) |

| (000 oz) |

|

SSX |

| 470.7 |

| 0.268 |

| 126.3 |

| 1,090.7 |

| 0.253 |

| 275.9 |

| 1,561.4 |

| 0.258 |

| 402.2 |

|

Smith |

| 98.7 |

| 0.312 |

| 30.8 |

| 742.2 |

| 0.300 |

| 222.5 |

| 840.9 |

| 0.301 |

| 253.2 |

|

Steer |

| 31.3 |

| 0.250 |

| 7.8 |

| 393.2 |

| 0.279 |

| 109.6 |

| 424.4 |

| 0.277 |

| 117.4 |

|

Murray |

| 90.6 |

| 0.315 |

| 28.5 |

| 57.6 |

| 0.276 |

| 15.9 |

| 148.2 |

| 0.300 |

| 44.4 |

|

Wright Window |

| — |

| — |

| — |

| 32.6 |

| 0.226 |

| 7.4 |

| 32.6 |

| 0.226 |

| 7.4 |

|

Low-grade stockpiles |

| 69.3 |

| 0.186 |

| 12.9 |

| 433.8 |

| 0.087 |

| 37.9 |

| 503.1 |

| 0.101 |

| 50.7 |

|

TOTAL 2004 |

| 760.5 |

| 0.271 |

| 206.3 |

| 2,750.1 |

| 0.243 |

| 669.1 |

| 3,510.6 |

| 0.249 |

| 875.3 |

|

Total 2003 |

| 932.8 |

| 0.299 |

| 279.0 |

| 2,132.4 |

| 0.254 |

| 541.1 |

| 3,065.3 |

| 0.268 |

| 820.1 |

|

(1) Reserves were estimated in accordance with Canada’s National Instrument 43-101 using a price of $360 an ounce at December 31, 2004, and $325 an ounce at December 31, 2003. The estimates are based on contained ounces of gold before processing losses. Definitions of Reserves are given on page 20. Additional information on estimating reserves, including qualified persons and quality control and assurance procedures, can be found in the Company’s Technical Report and the Annual Information Form, which can be examined on the Company’s web site or at sedar.com.

(2) U.S. investors should read the cautionary statements relating to Reserves on page 20.

12

An exploration priority in 2005 will be to explore the exciting 4 1/2 -mile mineralized trend that appears to connect Starvation Canyon with the Waterpipe II and Pie Creek prospects (see map, page 9).

A Very Successful Year By Any Measure

The 2004 exploration program at Jerritt Canyon was, by any measure, a very successful one. The Company once again more than replaced depleted reserves while making additions to measured and indicated resources, both adjacent to existing mines and in new target areas. (The 2004 year-end reserves and resources estimates appear as tables on pages 12 and 14).

Surface and underground drill programs added over 300,000 ounces of gold during the year, after depletion, to the Company’s mineral reserves at the Murray, SSX, Smith and Steer mines. At year-end 2004, proven and probable reserves at Jerritt Canyon stood at 875,300 ounces of gold. Significantly, reserve replacement was not at the expense of resources. Measured and indicated resources increased to 2.4 million ounces of gold, while an additional 0.9 million ounces were also reported in the year-end estimates as an inferred resource. Resources were increased both adjacent to operating mines and in new exploration targets, most significantly Starvation Canyon.

Since acquiring Jerritt Canyon in June 2003 through to year-end 2004, Queenstake added over 730,000 ounces of gold to proven and probable reserves. In other words, during the first 18 months of ownership, Queenstake added over 40,000 ounces per month. This translates to over 1.5 ounces per foot drilled as part of the near-mine exploration program.

The Most Intensive Drill Program in 10 Years

During 2004, the Company drilled more than 400 surface core and reverse circulation holes, totaling over 300,000 feet – the most intensive drill program carried out at Jerritt Canyon since 1994. Underground core drilling, designed to explore for and delineate reserves and resources close to operating mines, totaled a further 126,000 feet.

13

We inherited an invaluable asset with Jerritt Canyon: 24 years of geological data. This is providing the knowledge as to how the deposits were formed and clues where to search. We have identified many targets for follow-up in the years to come.

Total Gold Resources (1),(2) (including Reserves)

|

| MEASURED |

| INDICATED |

| MEASURED & INDICATED |

| INFERRED |

| ||||||||||||||||

MINE/AREA |

| Tons |

| Grade |

| Gold |

| Tons |

| Grade |

| Gold |

| Tons |

| Grade |

| Gold |

| Tons |

| Grade |

| Gold |

|

|

| (000) |

| (oz/t) |

| (000 oz) |

| (000) |

| (oz/t) |

| (000 oz) |

| (000) |

| (oz/t) |

| (000 oz) |

| (000) |

| (oz/t) |

| (000 oz) |

|

SSX |

| 1,080.0 |

| 0.298 |

| 322.1 |

| 1,865.8 |

| 0.282 |

| 527.0 |

| 2,945.7 |

| 0.288 |

| 849.1 |

| 943.0 |

| 0.242 |

| 228.1 |

|

Smith |

| 514.6 |

| 0.282 |

| 145.0 |

| 1,418.0 |

| 0.292 |

| 413.7 |

| 1,932.6 |

| 0.289 |

| 558.7 |

| 948.8 |

| 0.230 |

| 218.6 |

|

Steer |

| 81.3 |

| 0.246 |

| 20.0 |

| 901.9 |

| 0.266 |

| 240.4 |

| 983.2 |

| 0.265 |

| 260.4 |

| 649.0 |

| 0.255 |

| 165.6 |

|

Murray |

| 517.9 |

| 0.290 |

| 150.2 |

| 173.7 |

| 0.264 |

| 45.8 |

| 691.7 |

| 0.283 |

| 196.0 |

| 362.9 |

| 0.270 |

| 98.0 |

|

Wright Window |

| — |

| — |

| — |

| 114.2 |

| 0.147 |

| 16.8 |

| 114.2 |

| 0.147 |

| 16.8 |

| 278.0 |

| 0.105 |

| 29.1 |

|

Stockpiles |

| 69.3 |

| 0.186 |

| 12.9 |

| 1,239.7 |

| 0.059 |

| 73.1 |

| 1,309.0 |

| 0.066 |

| 85.9 |

| — |

| — |

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Active mines |

| 2,263.0 |

| 0.287 |

| 650.1 |

| 5,713.4 |

| 0.230 |

| 1,316.8 |

| 7,976.4 |

| 0.247 |

| 1,966.9 |

| 3,181.8 |

| 0.232 |

| 739.3 |

|

Underground resources |

| — |

| — |

| — |

| 1,508.9 |

| 0.251 |

| 378.7 |

| 1,508.9 |

| 0.251 |

| 378.7 |

| 513.3 |

| 0.221 |

| 113.4 |

|

Open pit resources |

| — |

| — |

| — |

| 502.5 |

| 0.127 |

| 64.0 |

| 502.5 |

| 0.127 |

| 64.0 |

| 363.6 |

| 0.098 |

| 35.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2004 Total Resources (including Reserves) |

| 2,263.0 |

| 0.287 |

| 650.1 |

| 7,724.8 |

| 0.228 |

| 1,759.5 |

| 9,987.8 |

| 0.241 |

| 2,409.6 |

| 4,058.7 |

| 0.219 |

| 888.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2003 Total Resources (including Reserves) |

| 2,219.3 |

| 0.306 |

| 679.7 |

| 7,277.6 |

| 0.222 |

| 1,615.7 |

| 9,496.9 |

| 0.242 |

| 2,295.3 |

| 5,415.4 |

| 0.191 |

| 1,034.0 |

|

(1) Measured and Indicated Resources and Inferred Resources were estimated in accordance with Canada’s National Instrument 43-101. The estimates are based on contained ounces of gold before mining dilution and process losses. Definitions of Resources are given on page 20. Additional information on estimating Resources, including qualified persons and quality control and assurance procedures, can be found in the Company’s Technical Report and the Annual Information Form, which can be examined on the Company’s web site or at sedar.com.

(2) U.S. investors should read the cautionary statements relating to Resources on page 20.

14

At Starvation Canyon, one drill hole in 2004 intercepted 95 feet grading 0.405 ounces of gold per ton.

Five Areas of Success

The most significant exploration accomplishments in 2004 were:

• Increased reserves by 55,000 ounces, net of depletion, and measured and indicated resources by 115,000 ounces;

• Discovered the Starvation Canyon high-grade mineralization in the southwestern part of the Jerritt Canyon property;

• Tripled the size of Steer Mine;

• Substantially increased the size of the Mahala deposit; and

• Added the B-pit underground deposit.

We are very pleased with the results of the underground exploration drilling program at the Smith Mine, where a major expansion of the Mahala deposit was achieved, and the B-pit underground deposit was added to the mineral reserve category. Both underground deposits will significantly contribute to the life of Smith. As development continues at Steer towards the SSX mine, we expect our exploration success to continue along the trend between the two mines.

The First Deposit in the Southern Part of the District

The discovery of high-grade mineralization at Starvation Canyon has been particularly exciting for us, as this is the first substantial gold deposit found in 24 years in the southern part of the district – an area that we have always considered to have high mineral potential. Based on our current level of work, the Indicated Resource is estimated at 577,000 tons with an average grade of 0.271 ounces of gold per ton, containing 156,000 ounces. The mineralized zones that host this deposit have not been fully delineated and have the potential for significant expansion. The thickness and grade of mineralization are comparable to the mineralization at the Company’s mines elsewhere at Jerritt Canyon.

15

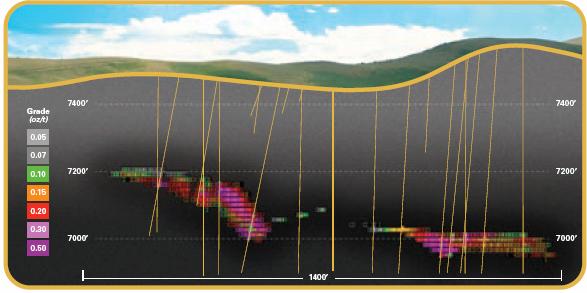

Starvation Canyon - Longitudinal Diagram

To date, the exciting new Starvation Canyon deposit has a resource of 577,000 tons grading 0.271 ounces per ton, for contained gold of 156,000 ounces. Data from 58 drill holes was used to establish this resource, only 16 are shown on this section. Exploration will continue in 2005 after the winter snow clears, subject to available funding.

An Extensive Mineralized Trend

Starvation Canyon has demonstrated that the mineral potential of this part of the district is real, and it has highlighted several other targets in the area, which will be assessed during the 2005 field season. These include a prospective 4 1/2 -mile mineralized trend that includes Starvation Canyon and mineralized targets at Waterpipe II and Pie Creek (see map, page 9).

In addition to various drill programs, our exploration team undertook geologic mapping in several important parts of the Jerritt Canyon district. We also continued with a district-wide soil-sampling program. Mapping and soil sampling have proved to be critical tools to identify new exploration targets on the property.

The successes achieved by our exploration efforts have validated our 2003 decision to acquire Jerritt Canyon. There is much more gold to be found.

16

Commitment to Elko County, Nevada

Queenstake’s success is firmly entrenched in the concept of multiple use of lands, which integrates land use for mining, agriculture, ranching, wildlife and sustainable public development. We are committed to land use that strengthens and enhances the social and environmental quality of northern Nevada.

Regulatory approvals and permits for the Jerritt Canyon mines were seamlessly transferred to Queenstake on July 1, 2003. In the ensuing 18 months Queenstake has vigorously sought to communicate to the public and to the regulatory agencies that all of the high standards of environmental performance at Jerritt Canyon are being continued and expanded under Queenstake’s leadership.

Major Permits Renewed for Five Years

Pursuant to changing permitting strategies from one of closure planning, made by the previous owners, to ours of sustaining and increasing production for the foreseeable future, all three major operating permits were renewed or reissued in 2004. The Nevada mining permit which regulates water pollution control was renewed in September 2004 for five years. A site-wide Air Quality Permit was issued in March 2004 for a five year term. In April, 2004 a site-wide Reclamation Permit was reissued to include all ongoing activities at Jerritt Canyon. In addition, Queenstake also permitted the Steer Portal and its surface facilities area in January 2004, and initiated the U.S. Forest Service permitting process for the next five-year exploration plan.

Award for Ongoing Reclamation

The Company maintained active participation in the Nevada Voluntary Mercury Emission Reduction Program and exceeded all 2004 goals. It was also honored by the State of Nevada when it received the 2004 Nevada Reclamation Award for closure and reclamation work at the Burns Basin open-pit mine area.

A large portion of the Jerritt Canyon Mine is located on public land administered by the U.S. Forest Service. The Jerritt Canyon staff maintains a proactive relationship with the service administrators. A majority of the Jerritt Canyon mining district has undergone formal National Environmental Policy Act (NEPA) review as part of the 25-year mining and exploration history of the district. Environmental areas of risk are well defined in this documentation and appropriate mitigation strategies are in place to support and expand operations.

Fully Funded Reclamation Liability

Reclamation projects are scheduled annually and are completed concurrent with the completion of mining activities. To date, over 1,500 acres of mined lands have been reclaimed. Reclamation and closure activitiesare defined ahead of any project and associated costs are bonded with the Federal Government and the State of Nevada. These bonded activities are also insured by a reclamation and closure insurance policy independently administered by AIG. As reclamation is completed, payment for completing the insured activity is made to Queenstake from a pre-funded commutation account administered by AIG.

17

Reclamation is an ongoing program at Jerritt Canyon – in the background is the reclaimed California Mountain open pit.

Support of Local Communities and Organizations

Queenstake has a strong commitment to its employees and to the communities in which they live. Projects are supported based on their social, economic or environmental value as well as on the impact a contribution from Queenstake will make. We strive to improve the communities with our support.

The McCaw School of Mines in Henderson, Nevada, was a beneficiary of Jerritt Canyon’s support in 2004. The McCaw School, located on an elementary school campus, provides tours to elementary age children throughout Nevada. The children are introduced not only to the history of mining but also the importance of modern mining. Over 25,000 children toured since project inception.

Jerritt Canyon continued its support of local youth programs and athletic teams, becoming a major sponsor for the youth football league in Elko. Support has continued for educational programs, including Teacher’s Mining Workshops held throughout Nevada, The Close-Up program (which sends high school children to Washington, DC), and drug and alcohol-free high school events, to name some. Jerritt Canyon also maintains a scholarship program, providing financial support for employees’ children to further their education. Summer employment is also provided to these college students whenever jobs are available.

The 450 employees at Jerritt Canyon are very active in the community, the schools and youth activities. The Company encourages and supports their participation and leadership roles in many civic and youth programs.

|

|

|

|

|

|

| ||||

The Company will therefore: |

|

|

|

| ||||||

|

|

|

|

|

|

| ||||

• |

| Comply with applicable laws, regulations, and permit conditions and, where appropriate, exceed their minimum requirements; |

|

| ||||||

• |

| Establish and maintain management systems to monitor environmental aspects of its activities; |

|

| ||||||

• |

| Review these management systems regularly to evaluate their effectiveness and modify them as appropriate to o optimize their effectiveness; | ||||||||

• |

| Proactively pursue and evaluate engineering alternatives to best address closure and reclamation issues; |

|

| ||||||

• |

| Ensure that financial resources are available to meet environmental and reclamation obligations; |

|

| ||||||

• |

| Ensure that the Company’s employees and contractors are aware of this policy and understand their relevant responsibilities; | ||||||||

• |

| Participate in the ongoing public and private sector debate on environmental and social matters that relate to the mining industry. | ||||||||

|

|

|

|

|

|

| ||||

Queenstake Resources Ltd. will continually strive to improve its environmental performance. |

| |||||||||

|

|

|

|

|

|

| ||||

18

Good corporate governance ensures that the interests of the Board of Directors and Management are aligned with those of the shareholders. In short, good governance is good business. The Board of Directors periodically monitors its governance policies to ensure that they reflect integrity, high ethical values and evolving regulatory requirements.

Board Mission

The mission of the Board of Directors is to oversee the affairs of the Company in order to ensure its long-term financial strength and the creation of enduring shareholder value.

Board Constitution

The Queenstake Board of Directors is constituted with a majority of independent directors, currently four out of five directors.

Board Operations

The Board of Directors currently has three committees: Audit, Corporate Governance and Compensation. The composition of committees is designed to take advantage of each director’s experience and expertise.

Audit Committee

(Mike Smith, Chairman, Peter Bojtos and Hugh Mogensen) Responsible for overseeing the integrity of the financial reporting process and for ensuring that the financial statements and management’s discussion andanalysis adequately represent the Company’s financial condition, results of operations and cash flows. TheCommittee is also responsible for overseeing the Company’s compliance with corporate policies and provides processes, procedures and standards to accomplish the Company’s goals and objectives.

Compensation Committee

(Hugh Mogensen, Chairman, and Robert L. Zerga) Responsible for compensation policies and practices, and reviewing and recommending to the Board the remuneration for directors and senior management of the Company. The Committee also administers the Company’s stock option plan.

Corporate Governance Committee

(Peter Bojtos, Chairman, and Robert L. Zerga) Responsible for corporate governance policies and practices and evaluating the effectiveness of the Board. The Committee annually recommends to the Board the slate ofDirector nominees for election to the Board by the shareholders and recommends nominees to fill vacancies.

19

Reserves and Resources

Canadian definitions in accordance with National Instrument 43-101

Reserves: Combined proven and probable mineral reserves.

Reserves, Probable: The economically mineable part of an indicated and in some circumstances a measured mineral resource, demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified.

Reserves, Proven: The economically mineable part of a measured mineral resource demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate at the time of reporting, that economic extraction is justified.

Resource, Measured: That part of a mineral resource for which quantity, grade or quality, densities, shape andphysical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity.

Resource, Indicated: That part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed.

Resource, Inferred: That part of a mineral resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes.

Mineral Reserve and Resource Terminology: Canadian and U.S. Differences

The Company is organized under the laws of the Yukon Territory, Canada. The mineral reserves and resources described in this Annual Report are estimates and have been prepared in compliance with National Instrument 43-101 of the Canadian Securities Administrators. The definitions of proven and probable reserves used in National Instrument 43-101 differ from the definitions in the United States Securities and Exchange Commission (“SEC”) Industry Guide 7. In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by National Instrument 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and normally are not permitted to be used in reports and registration statements filed with the SEC. Accordingly, information contained in this Annual Report containing descriptions of the Company’s mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Cautionary Note to U.S. Investors concerning estimates of Measured and Indicated Resources

This document uses the terms “measured and indicated resources”. The Company advises U.S. investors that while these terms are recognized and required by Canadian regulations, the SEC does not recognize them. U.S. investors are cautioned not to assume that any part or all of mineral deposits in this category will ever be converted into reserves.

Cautionary Note to U.S. Investors concerning estimates of Inferred Resources

This document uses the term “inferred resources”. The Company advises U.S. investors that while this term is recognized and required by Canadian regulations, the SEC does not recognize it. “Inferred resources” have a greatamount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannotbe assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. UnderCanadian rules, estimates of inferred mineral resources may not form the basis of a feasibility or other economicstudy. U.S. investors are cautioned not to assume that any part or all of an inferred resource exists or is economically or legally minable.

20

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Queenstake Resources Ltd.

This discussion and analysis has been prepared as at March 29, 2005 unless otherwise indicated, and it should be read in conjunction with the audited consolidated financial statements of Queenstake ResourcesLtd. (“Queenstake” or the “Company”) as at December 31, 2004 and the notes thereto, which have been prepared in accordance with accounting principles generally accepted in Canada (“Canadian GAAP”). Differences from generally accepted accounting principles in the United States (“U.S. GAAP”) and Canadian GAAP are described in Note 27 to the consolidated financial statements. All dollar figures are in U.S. dollars, unless otherwise indicated.

Overview

The Company engages in the mining, processing, production and sale of gold, as well as related activities including development and exploration. The Company’s principal asset and only current source of revenue is its 100% owned Jerritt Canyon Mine, 50 miles north of Elko, Nevada. The Jerritt Canyon Mine complex consists of four underground mines, which together with ore stockpiles, feeds ore to a 1.5 million ton per year capacity ore processing plant. Jerritt Canyon has extensive exploration potential, comprised of an approximately 100 square mile land position, together with a geological database compiled over the past 25 years.

The Company acquired the Jerritt Canyon Mine on June 30, 2003; prior to that date the Company was an exploration company and did not have commercial scale gold production. Consequently, comparisons of production and operating results to periods prior to June 30, 2003 are not meaningful.

Highlights of the Company’s activity in the year ended December 31, 2004 are as follows:

In February 2004 the Company completed the sale of Pangea Resources Inc. (“Pangea”) and all of its related assets, including the Magistral Mine, to Nevada Pacific Gold (“NPG”) for an initial payment of $4.0 million in cash, a note receivable of $3.0 million due in the current year and 2,000,000 common shares of NPG.

Subsequently to the sale during 2004, the Company collected $2.5 million in cash and agreed to accept an additional 669,485 shares of NPG with a fair value of $0.5 million to settle the balance of the note receivable. The Company sold 2,000,000 of the 2,669,485 shares of NPG for proceeds of $1.5 million. The cash proceeds from the sale of Pangea and cash realized from the sale of the 2,000,000 common shares were used to reduce the balance of an existing term loan and support exploration and underground activities at the Jerritt Canyon Mine.

In August 2004, the Company successfully completed the closing of a private placement for aggregate cash proceeds of approximately $12.9 million and reached agreements to settle all material obligations connected with the Company’s June 2003 acquisition of the Jerritt Canyon Mine. From the proceeds of the offering the Company paid approximately $11.9 million to settle deferred production payments, a net smelter royalty, notes payable and the remaining balance of a term loan.

During 2004, the Company’s mining activities resulted in the depletion of estimated proven and probable reserves from production by 243,000 ounces. Total additions to the estimated reserve during 2004 were 298,000 ounces exceeding the ounces depleted during the year by approximately 55,000 ounces. Estimated proven and probable reserves as at December 31, 2004 are reported to be 875,000 contained ounces as compared to 820,000 at December 31, 2003.

The Company initiated a district-scale exploration program during 2004. Expenditures during the year were $6.6 million. Promising targets were explored throughout the 100 square mile Jerritt Canyon district. The most significant results were obtained at Starvation Canyon, where high-grade gold mineralization was located in a system that remains open in all directions. Management believes Starvation Canyon to be a part of a larger mineralized trend with a strike length of at least 4.5 miles.

During December 2004, the Company’s common shares were approved for listing on the American Stock Exchange (“AMEX”) and commenced trading under the ticker symbol “QEE”.

21

Material changes in the management structure of the Company occurring after December 31, 2004 include the resignations of Christopher Davie as President, Chief Executive Officer and as a member of the Board of Directors, and John “Jack” Engele, Vice-President of Finance and Chief Financial Officer.

On March 9, 2005, Mr. Davie resigned from his position with the Company as a result of certain health issues. In connection with the resignation of Mr. Davie, the Company has agreed to pay Mr. Davie a $1.0 million payment and reimbursement of certain expenses. Dorian “Dusty” Nicol was appointed President and Chief Executive Officer in addition to his current duties as Executive Vice President, Director of Exploration and a member of the Company’s Board of Directors.

On February 25, 2005, Mr. Engele resigned his position with the Company to accept an opportunity with a major mining company in a senior position. Eric H. Edwards joined the Company on March 14, 2005 accepting the position of Vice President of Finance and Chief Financial Officer. Mr. Edwards has more than 25 years of experience in gold mining as a financial executive and specific experience with the Jerritt Canyon Mine as an Operations Controller.

On March 23, 2005, the Company successfully closed an equity financing at the maximum offering amount (the “Offering”) through a syndicate of agents (the “Agents”) for aggregate cash proceeds of Cdn $30.0 million. The aggregate cash proceeds, included Cdn $10.0 million issued and sold pursuant to exercise by the Agents of an over-allotment option. The total Offering consisted of 100 million units (the “Units”),including those issued pursuant to the Agents’ over-allotment option, with each Unit consisting of one common share and one half of one common share purchase warrant at a price of Cdn $0.30 per Unit. Each whole common share purchase warrant (50 million warrants in total) can be exercised to acquire one additional common share at a price of Cdn $0.40 for a period of 24 months. If at any time after six months from the March 23, 2005 closing date of this Offering, the weighted average trading price of the Common Shares on the Toronto Stock Exchange (the “TSX”) (or such other exchange or trading market on which the Common Shares principally trade) is Cdn $0.52 or more per Common Share for a period of thirty consecutive trading days then, upon notice by the Company, the holders of such warrants must exercise their warrants within thirty days or they will expire and will no longer be valid. The Agents received a 5% commission on the gross proceeds of the offering. The net proceeds of the Offering will be used to fund the Company’s planned capital expenditures, district exploration, and general working capital for its Jerritt Canyon mine operations. Any additional net proceeds will be used for general corporate working capital.

Outlook

Reserves and Resources

The December 31, 2004 Jerritt Canyon year-end reserves and resource estimate demonstrates that fiscal 2004 work to increase and replace the mined reserves has been successful. The Company has established 298,000 ounces of new reserves during 2004, which exceeds the current year production of 243,000 for a net increase in reserves of approximately 55,000 ounces.

Reserves were increased in and around existing work areas at the Smith and SSX Mines. Development at Steer and Mahala, which were added to reserves in 2003, provided locations for underground drilling which increased reserves at Steer to 95,000 contained ounces and increased the Mahala reserves by 62% to 81,000 contained ounces. New reserve areas include Zone 5 (B-Pit) of Smith, Saval 4, and Murray Zone 7. Additional drilling into Zone 5 of Smith resulted in upgrading the resource to a reserve of 38,000 ounces. Surface drilling in the Saval mineralization northwest of SSX resulted in increasing and upgrading the resource at Saval 4 to reserve status. At Murray, Zone 7 was added to reserve and development will allow underground drilling to commence in March. Surface drilling at Murray Zone 9 significantly increased the resource and additional drilling is planned for 2005. Further development and the preparation of secondary escape ways will be completed at Mahala and Steer during early 2005, resulting in expected increases in both mined tons and mill feed grade during the latter part of the year.

22

Development and Exploration

Drilling results since the completion of the December 31, 2004 reserve estimate continue to be encouraging, with significant grade and width intercepts outside the current resource envelope, but near current workings. Management believes these results are indicative of additional mineral inventory which it anticipates converting to reserves and/or mining during the next year. Management believes that measured and indicated resources and proven and probable reserves can be generated in the immediate mine areas at a rate that will keep pace with mining depletion for the foreseeable future.

Development of two new reserve areas, Steer and Mahala, at Jerritt Canyon is well underway. Mineralization for the Steer and Mahala reserves are accessed via a new portal collared in April 2004 and from the Smith Mine, respectively. Both Steer and Mahala reserve development have progressed to the proximity of the underground ore zones and underground drilling has both expanded and added continuity to oreshapes. Results received for 2004 underground drilling were incorporated in the December 31, 2004 reserve estimate.

The 2005 development and exploration program will continue to focus on both near-mine exploration, with the objective of short-term reserve replacement, and district-scale exploration with the objective of discovery of new ore bodies. A priority of district-scale exploration during 2005 will be the Starvation Canyon deposit, where the Company announced a discoveryduring 2004.

New Mine Production

Major development of the new Steer Mine commenced in April 2004 with development of the Steer decline and subsequent definition drilling of the known ore shapes. Shop and office construction was initiated and electrical and communications infrastructure was installed in 2004. Prior to starting commercial production from this mine, a second escape way must be provided by a connection to the existing SSX Mine. This connection is scheduled for completion early in the second half of 2005. The Company has estimated completion costs of approximately $2.1 million prior to the commencement of commercial production.

Major access development to the Mahala reserve was largely completed from the existing Smith Mine in 2004. Completion of a ventilation and escape raise to surface is underway and will allow production from this high-grade ore body to commence in the later part of 2005. The Company has estimated completion costs of approximately $2.9 million prior to commencement of commercial production from the Mahala reserve. The average grade at Mahala is expected to be 0.371opt and this will have a positive effect on mill grade as production starts in the later part of 2005.

At Zone 5 of the SSX Mine new pods of ore were discovered and have been developed for 2005 production. Development was also carried out in Zone 1 to the east for production during 2005.

Capital mine development costs for Steer, Smith and SSX are estimated to total $8.6 million during 2005. The Company currently expects to finance this development with cash flows generated from operations.

Other Mines

As expected, the MCE Mine was depleted during 2004 and mining operations have been discontinued. The equipment used at the MCE Mine has been redeployed to other mining operations. The Murray Mine, which in the past was a major component of production, is nearing the end of its life with the main ore body to be depleted this year. However, Zone 7 at Murray was added to reserves, and drilling significantly increased the resource at Zone 9. Replacement of the Murray ore mill feed will be provided by Steer and Mahala in the near term and from the area to the north of SSX known as Saval in later years.

2005 Production

The operating practice since the year 2000 at the Jerritt Canyon Mine has been to blend ore mined from underground with ore stockpiled from earlier open pit operations. The resulting mill feed averaged 1.4 million tons per year.

The primary focus of production during 2005 and succeeding years will be to increase the rate at which underground ore is mined and fed to the mill. Additional

23

underground ore will reduce the component of low grade stockpile fed to the mill resulting in an increase of mill feed grade during 2005, which is anticipated to have the effect of reducing unit operating costs. This is expected to result in a increase in gold production by approximately 13% during 2005, with no additional costs to the mill plant nor any increase in mill operating costs.

The Company expects 2005 gold production to be approximately 275,000 ounces with approximately 45% of the production occurring in the first half of 2005 and 55% in the latter half of 2005. The Company’s expected 2005 gold production represents an increase of 13% over 2004 production. Gold production in 2005 will primarily occur from the SSX Mine with additional contributions from the Murray, Smith, Mahala and Steer Mines. Mill capacity during the summer and fall is typically 20% to 40% higher than winter, largely because the dry mill capacity is adversely affected byhigh moisture in the feed, due to snowfall and ice. In an effort to minimize the seasonal impacts on mining and processing, the Company plans to continue concentrating on underground development during the winter months to ensure sufficient ore availability to maximize production in the summer months.

As discussed above, 2005 production will largely be achieved by introducing new mill feed in the latter part of the year from the Steer and Mahala Mines.

Life of Mine Plan

A life of mine plan has been prepared based on management’s expectation of the future conversion of resources to reserves at a rate commensurate with that achieved during 2004 and the second half of 2003. The discovery of additional resources, should it occur, would provide the potential for additional mine life.

The life-of-mine plan envisages that underground ore production will increase to approximately 1.4 million tons per year by mid 2005 and continue at this rate through 2009. The plan is predicated on the continuing conversion of measured and indicated resources to proven and probable reserves at rates achieved in the past, but does not assume additional exploration success. Management believes that these assumptions are reasonable.

The SSX Mine is expected to continue to produce at a rate of 500,000 to 600,000 tons of ore per year, while Smith production, with the addition of Mahala ore, is expected to continue to produce at a rate of 300,000 tons per year. Initially, Steer production is expected to be initially 150,000 tons per year rising to approximately 300,000 to 350,000 tons per year. Additional ore tons of approximately 150,000 per year will be provided by other target zones and low grade stock piles.

Results of Operations

Gold production

The Company began commercial scale gold production from the Jerritt Canyon Mine, its only producing gold mine, on June 30, 2003. Gold production during the year ended December 31, 2004 was 243,333 ounces, while gold production for the year ended December 31, 2003 was 302,096 ounces, of which 152,095 ounces were to the account of the former owners and 150,001 ounces were to the Company’s account. Key quarterly production statistics are illustrated in Table 1 below.

Table 1 – Jerritt Canyon Production Statistics

|

| Three months ended |

| ||||||||||||||||

|

| December 31, |

| September 30, |

| June 30, |

| March 31, |

| December 31, |

| September 30, |

| ||||||

|

| 2004 |

| 2004 |

| 2004 |

| 2004 |

| 2003 |

| 2003 |

| ||||||

Gold ounces produced |

| 60,384 |

| 73,070 |

| 61,247 |

| 48,632 |

| 68,411 |

| 81,590 |

| ||||||

Gold ounces sold |

| 64,723 |

| 71,210 |

| 63,983 |

| 45,735 |

| 72,932 |

| 73,891 |

| ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Average sales price per ounce |

| $ | 432 |

| $ | 402 |

| $ | 395 |

| $ | 406 |

| $ | 391 |

| $ | 365 |

|

Cash operating costs per ounce(1) |

| $ | 336 |

| $ | 303 |

| $ | 337 |

| $ | 388 |

| $ | 298 |

| $ | 247 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Ore tons mined |

| 320,505 |

| 296,474 |

| 284,737 |

| 242,498 |

| 248,036 |

| 296,305 |

| ||||||

Tons processed |

| 331,619 |

| 358,600 |

| 323,782 |

| 291,832 |

| 369,465 |

| 397,663 |

| ||||||

Grade processed (opt) |

| 0.214 |

| 0.224 |

| 0.208 |

| 0.209 |

| 0.212 |

| 0.229 |

| ||||||

Process recovery |

| 85.0 | % | 91.1 | % | 91.0 | % | 79.7 | % | 87.3 | % | 90.0 | % | ||||||

(1) The Company has adopted the Gold Institute Production Cost Standard (the “Standard”) to calculate and report cash operating costs per ounce of gold produced. This is a non-GAAP measure, intended to complement conventional GAAP reporting; accordingly these data should not be considered a substitute for GAAP measures. Management believes that cash operating costs per ounce is a useful indicator of a mine’s performance. Where GAAP operating costs are adjusted to calculate per ounce data consistent with the Standard, reconciliations to GAAP measures are provided, see Table 5 on page 28.

24

Ounces of gold produced decreased 11% in the final two quarters of 2004 as compared to the same period in 2003. The decrease was attributable to a decline in the grade of ore mined in the period and a decrease in process recovery in the fourth quarter of 2004. The Company believes that the decline in the grade of mined ore resulted from a lack of available working faces caused by a prolonged decline in development work over the past years.

Gold production for 2004 was approximately 13% below expectations. Weather conditions affected gold production early in the year, and some difficulties were experienced in mining dilution and in maintaining mine development sequencing during the secondquarter of 2004. Process recoveries were also affected by characteristics of some of the ores milled, a transient situation, and by variations in mill feed rates. Several factors that affect production levels, such as the number of available working faces in the mines, equipment availability and productivity improved during the third and fourth quarters of 2004.

Total cash operating costs for the twelve months ended December 31, 2004 were $336 per ounce compared to $270 per ounce for the six months of Company mining operations during the year ended December 31, 2003. Increased costs including electricity and commodity prices, together with one-time processing plant maintenance costs resulted in approximately a 10% increasein total cash operating costs through the twelve-month period ended December 31, 2004. The remaining unit cost increase is attributed to lower gold production and the decrease in the average grade of ore mined during 2004.

Statements of loss

The Company reported a net loss of $22.1 million ($0.06 per share) and $8.1 million ($0.04 per share) for the twelve-month periods ended December 31, 2004 and 2003, respectively. The principal components of the loss for the year ended December 31, 2004 are: a loss from operations of $17.1 million, interest expense of $4.9 million and stock-based compensation expense of $0.5 million which are offset by net other income of $0.5 million, including the $0.7 million gain from the disposition of Pangea Resources Inc. in February 2004. The principal components of the loss for the year ended December 31, 2003 are: interest expense of $4.9 million and a $6.2 million write-down of the Company’s investment in the Magistral Joint Venture, offset by income from operations of $3.1 million.

Income (loss) from operations in 2004, 2003 and 2002 are illustrated in the Table 2 below.

Table 2

(In millions of U.S. Dollars) |

| 2004 |

| 2003 |

| 2002 |

| |||

Gold sales |

| $ | 97.8 |

| $ | 54.9 |

| $ | — |

|

Costs and expenses |

|

|

|

|

|

|

| |||

Operating costs |

| 85.3 |

| 40.7 |

| — |

| |||

Depreciation, depletion and amortization |

| 19.6 |

| 9.2 |

| — |

| |||

Exploration |

| 6.6 |

| — |

| — |

| |||

General and administrative |

| 3.4 |

| 1.9 |

| 1.0 |

| |||

|

| 114.9 |

| 51.8 |

| 1.0 |

| |||

Income (loss) from operations |

| $ | (17.1 | ) | $ | 3.1 |

| $ | (1.0 | ) |

During the year ended December 31, 2004, revenues were generated from the sale of 245,651 ounces of gold compared to 146,823 during the six months of mine operations during the year ended December 31,2003. Average gold sale prices increased $24 per ounce during the twelve-month period ended December 31, 2004 to $398 per ounce compared to $374 per ounce for the six months of mine operations during the year ended December 31, 2003.

Operating costs and depreciation, depletion and amortization costs are substantially all associated with the Jerritt Canyon Mine. Operating costs were substantially as expected for the year ended December 31, 2004 with the exception of increased electricity and commodity prices. The increases in electricity and commodity costs and lower gold production contributed to the increase in cash cost per ounce during 2004. A reconciliation of operating costs to cash operating costs per ounce is provided in Table 5 on page 28 below.

Depreciation, depletion and amortization expense are substantially all attributed to the Jerritt Canyon mineral property, plant and equipment. Depreciation of the processing plant and mining equipment comprises $4.4 million and $1.7 million of the totals for the year ended December 31, 2004 and the six months of Company mine operations during the period ended December 31, 2003, respectively; amortization and depletion expenses comprise the remaining $15.2 million and $7.5 million for the same periods. Reference should be made to Note 3 of the financial statements where accounting policies for depreciation, depletion and amortization are discussed.

25

Exploration expense for the year ended December 31, 2004 was incurred for target generation and follow-up within the Jerritt Canyon District. The Jerritt Canyon District exploration program was not in process during the six months of Company mine operations during the year ended December 31, 2003.

General and administrative costs are associated with the Company’s executive offices in Denver, Colorado and are substantially as expected and comparable for the years ended December 31, 2004 and December 31,2003, respectively. General and administrative costs include wages and salaries of $1.2 million, facilities expense of $0.2 million, legal and professional fees of $0.9 million and general operating expenses of $1.3 million, which includes supplies, travel and entertainment, corporate filing fees and other miscellaneous operating expenses.

The principal remaining components of the Company’s net loss, other income, net of other expense and interest expense, are illustrated in Table 3 below.

Table 3

(In millions of U.S. Dollars) |

| 2004 |

| 2003 |

| 2002 |

| |||

Other (income) expense, net |

| $ | (0.5 | ) | $ | (0.2 | ) | $ | (0.4 | ) |

Stock-based compensation |

| 0.5 |

| 0.3 |

| — |

| |||

Interest expense |

| 4.9 |

| 4.9 |

| — |

| |||

Foreign exchange (gain) loss |

| 0.1 |

| (0.2 | ) | 0.1 |

| |||

Non-cash loss on early debt conversion |

| — |

| — |

| 0.4 |

| |||

Provision for impairment of Magistral Joint Venture |

| — |

| 6.2 |

| — |

| |||

|

| $ | 5.0 |

| $ | 11.0 |

| $ | 0.1 |

|