OMB APPROVAL

OMB Number: 3235-0570

Expires: Nov. 30, 2005

Estimated average burden

hours per response: 5.0

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

REGISTRATION NO.

811-07696

IOWA PUBLIC AGENCY INVESTMENT TRUST

(EXACT NAME OF REGISTRANT AS SPECIFIED IN CHARTER)

1415 28th STREET, SUITE 200

WEST DES MOINES, IOWA 50266

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES) (ZIP CODE)

Elizabeth Grob, Esq.

Ahlers & Cooney, P.C.

100 Court Avenue, Suite 600, Des Moines, Iowa 50309

(NAME AND ADDRESS OF AGENT FOR SERVICE)

COPIES OF ALL COMMUNICATIONS TO:

Vera Lichtenberger | | JOHN C. MILES, ESQ. |

IOWA PUBLIC AGENCY INVESTMENT TRUST | | DONALD F. BURT, ESQ. |

1415 28th STREET, SUITE 200 | | CLINE, WILLIAMS, WRIGHT, JOHNSON & OLDFATHER |

WEST DES MOINES, IOWA 50266 | | 1900 U.S. BANK BUILDING, 233 S. 13TH STREET |

| | LINCOLN, NEBRASKA 68508 |

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (515) 244-5426

DATE OF FISCAL YEAR END: 06/30/2004

DATE OF REPORTING PERIOD: 06/30/2004

ITEM 1. REPORTS TO UNITHOLDERS.

IOWA PUBLIC AGENCY INVESTMENT TRUST

DIVERSIFIED FUND

COMPREHENSIVE ANNUAL FINANCIAL REPORT

DIRECT GOVERNMENT OBLIGATION FUND

COMPREHENSIVE ANNUAL FINANCIAL REPORT

JUNE 30, 2004

IPAIT - www.ipait.org

IOWA PUBLIC AGENCY INVESTMENT TRUST

DIVERSIFIED FUND

COMPREHENSIVE ANNUAL FINANCIAL REPORT

IOWA PUBLIC AGENCY INVESTMENT TRUST

DIRECT GOVERNMENT OBLIGATION FUND

COMPREHENSIVE ANNUAL FINANCIAL REPORT

For the Fiscal Year

Ended June 30, 2004 | | www.ipait.org |

Prepared by the

Iowa Public Agency Investment Trust

Board of Trustees

TABLE OF CONTENTS

1

This page left intentionally blank.

2

| | INTRODUCTORY SECTION |

3

IOWA PUBLIC AGENCY

INVESTMENT TRUST

DIVERSIFIED FUND |

|

IOWA PUBLIC AGENCY

INVESTMENT TRUST

DIRECT GOVERNMENT

OBLIGATION FUND |

|

|

|

1415 28th Street, Suite 200

West Des Moines, IA 50266 |

August 25, 2004

Dear Fellow IPAIT Participants:

The Iowa Pubic Agency Investment Trust (IPAIT) is pleased to submit to you the Diversified Fund and Direct Government Obligation

Fund (DGO) Annual Financial Report for the fiscal year ended June 30, 2004.

IPAIT has been serving participants’ needs since 1987. Fiscal year 2003-2004 provided many challenges for our participants amidst this low rate environment. The IPAIT Diversified and DGO Funds maintained rates comparable to other money market funds during this time while being an educational resource for IPAIT participants. For a detailed review of the Funds, please refer to the Management’s Discussion and Analysis of each Fund located in the Financial Section. IPAIT appreciates the efforts of the individuals involved in the preparation of this report.

Iowa Economy

Iowa’s economy has historically been characterized as slower growth in new jobs and lower personal income levels than the nation. However, the state’s economic stability has served as a source of strength over the course of economic cycles. Iowa has one of the lowest unemployment rates in the Midwest at 4.3 percent versus the nation at 5.6 percent. A natural cause is the dramatically lower level of historical population growth in Iowa at 5.3 percent versus the nation at 13.1 percent. Over the course of the year the unemployment rate has moved lower from 4.5 percent in June of 2003 to 4.4 percent in June of 2004. Most of the improvement in the unemployment rate has come in the finance sector of the economy.

Inflation across the Midwest remains in check. June 2004 year-over-year CPI – Urban figures indicate Midwest inflation growing at 2.7 percent versus the nation at 3.3 percent. An active Fed will assure inflation will stay in check.

Home construction is off this year in Iowa with respect to last year, primarily due to higher mortgage rates. New residential building permits rose three-fold from 2002 to 2003. However from 2003 to 2004, permits have declined by 60 percent, but still much higher than previous highs of 2002.

Commercial construction remains quite healthy in large urban areas across the state. This additional tax revenue will support future spending needs.

Overall, the Iowa economy is healthy. Budget woes from the recent recession have been muted as tax revenues have risen with the economic recovery. Smaller communities will continue to feel the pain of consolidating businesses and lower tax revenues. Job growth will remain spotty across the state as business prospects remain mixed.

Investment Policies and Strategies

IPAIT was created pursuant to Iowa Code Chapter 28E in 1987 to enable eligible Iowa public agencies to invest their available operating and reserve funds in a competitive rate environment, safely and effectively. Both the Diversified and DGO Funds have followed established money market mutual fund investment parameters designed to maintain a $1 per unit net asset value since inception.

Investment Safeguards

Both Funds continue to be focused on their investment objectives as stated in the IPAIT Investment Policy. These goals, in order of priority are safety of invested principal, maintenance of adequate liquidity, and maximum yield. Within these objectives, each Fund strives to provide participants with the best available rates of return for legally authorized investments. All security settlements within either Fund are settled on a delivery-versus-payment (DVP) basis. DVP settlements greatly reduce the possibility of inappropriate transmission of funds or securities.

Reliability of Investment Section

All commentary and displays in the Investment Section were prepared by IPAIT’s service provider, IMG, the program’s Investment Advisor, Administrative Services Provider and Program Support Provider, and reviewed by KPMG LLP. IMG has provided services to the IPAIT program since the program’s inception in 1987. All services provided by IPAIT to participants are subject to rigorous and regular verification.

4

Schedule of Operations

For fiscal year 2003-2004 (FY 03/04) and fiscal year 2002-2003 (FY 02/03) total interest earned, total operating expenses and net investment income for the IPAIT Diversified and the DGO Funds were as follows:

| | Interest Earned | | Expenses | | Net Investment Income | |

| | | | | | | |

Diversified Fund | | | | | | | |

FY 03/04 | | $ | 2,680,795 | | $ | 1,202,977 | | $ | 1,477,818 | |

FY 02/03 | | $ | 4,035,199 | | $ | 1,503,506 | | $ | 2,531,693 | |

| | | | | | | |

DGO Fund | | | | | | | |

FY 03/04 | | $ | 520,560 | | $ | 255,306 | | $ | 265,254 | |

FY 02/03 | | $ | 1,074,831 | | $ | 416,758 | | $ | 658,073 | |

The decrease in the year-over-year interest income for both Funds is attributed to the low interest rate environment and fewer assets invested in the program. Expenses were less in FY 04 versus FY 03 due to a voluntary reduction in fees charged by the investment advisor and administrator. Each program operates pursuant to Service Provider agreements for all aspects of program operation. Every agreement specifies the fees to be charged for each component of IPAIT services.

Financial and operating highlights from this past year include:

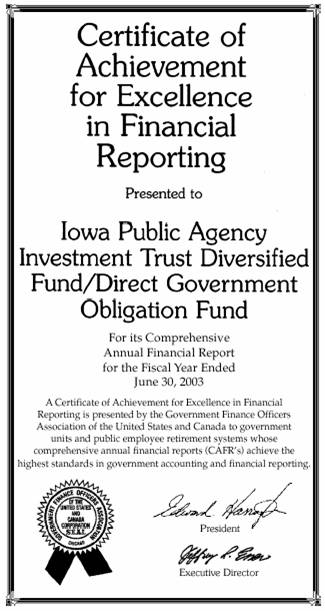

• Receipt of a seventh consecutive Certificate of Achievement for Excellence in Financial Reporting by the Government Finance Officers Association (GFOA).

• Average combined daily investments in the Diversified and DGO Funds of $299,261,038 down from $340,627,139.68 in the last fiscal year.

• Placement of 39 portfolio certificates of deposit in Iowa financial institutions by the Diversified Fund representing over $22,250,000.

• An authorized membership total of 400 public bodies representing 182 municipalities, 78 counties, 81 municipal utilities, and 59 other eligible public agencies.

Total funds invested in the program’s investment alternatives peaked for the fiscal year at $429,059,131 on April 15, 2004.

Comprehensive Annual Financial Report Format and Contents

The report is presented in four sections as follows:

Introduction - contains the Letter of Transmittal, Management Report, a listing of the IPAIT Board of Trustees and service providers and the IPAIT Organizational Chart.

Financial - contains the report of independent auditors, KPMG LLP, the Management Discussions and Analysis for the Diversified Fund and DGO Fund, and the Diversified Fund and DGO Fund financial statements.

Investment - contains a comprehensive discussion of each Fund’s investment performance and operations including the following:

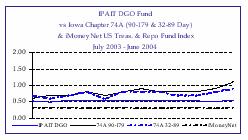

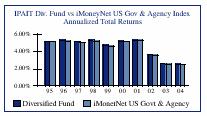

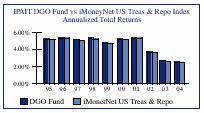

• Fund Facts - a summary of IPAIT’s Diversified Fund and DGO Fund investment strategy, individual fund performance comparison to other registered money market fund performance benchmarks including the iMoneyNet Financial Data Money Fund Index and an Economic Environment Overview for the past fiscal year;

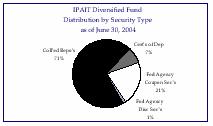

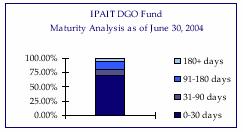

• Complete Portfolio Characteristics portfolio composition and summaries for each Fund to include portfolio ownership analysis, weighted average maturity illustrations and comparisons, maturity analysis, portfolio distribution by security type, historical portfolio asset growth; and

• The IPAIT Diversified Fund and DGO Fund Investment Policy.

Statistical - includes trend data for the past five years for various program-operating components, including total net asset value for each Fund by type of participant, monthly and annual yield highlights and comparisons, Summary of Operations, and a glossary of investment terms.

5

The GFOA awarded a seventh consecutive Certificate of Achievement for Excellence in Financial Reporting to the Iowa Public Agency Investment Trust for its comprehensive annual financial report (CAFR) for the fiscal year ended June 30, 2003. The Certificate of Achievement is a prestigious national award, recognizing conformance with the highest standards for preparation of state and local government financial reports.

In order to be awarded a Certificate of Achievement, a government unit must publish an easily readable and efficiently organized CAFR, whose contents conform to program standards. The CAFR must satisfy both generally accepted accounting principles and applicable legal requirements.

A Certificate of Achievement is valid for a period of one year only. We believe our current report continues to conform to the Certificate of Achievement program requirements, and we are submitting it to the GFOA. IPAIT has adopted GASB Statement No. 34, Basis Financial Statements – and Management’s Discussion and Analysis – for State and Local Governments: Omnibus, as amended by Statement No. 37, Basic Financial Statements – and Management’s Discussion and Analysis – for State and Local Governments: Omnibus, and modified by Statement No. 38, Certain Financial Statement Note Disclosures, (Statements Nos. 34, 37, and 38) effective July 1, 2002. Adoption of Statement Nos., 34, 37, and 38 had no impact on the net assets of the Diversified and the DGO Funds of IPAIT. IPAIT’s annual report has added a section for Management’s Discussion and Analysis as required.

Participant Meeting

IPAIT registered with the Securities and Exchange Commission (SEC) as an open end management investment company and money market fund under the Investment Company Act of 1940 (1940 Act) in May of 1993 in order to comply with Iowa laws relating to investments of public agencies. IPAIT is routinely examined by the SEC. At the July 12, 2004 Board of Trustees meeting, the Trustees determined to change the way in which they are elected to more closely track the requirements of the 1940 Act and called a meeting of the Participants. At this meeting the Participants were asked to elect the Trustees, approve KPMG as IPAIT’s independent auditors, approve a small change to IPAIT’s investment policies, approve the Advisor Agreement with IMG and approve IPAIT’s Rule 12b-1 Distribution Plan which pays fees to the sponsoring associations. We thank all Participants which took the time to return their proxy cards.

The Diversified and DGO Funds were among the first local government investment pools in the country to do so and have been formally regulated by the SEC since that time. In 2004, the SEC conducted an exam of the Diversified and DGO Funds. Upon the SEC findings, the IPAIT Board voted to hold a proxy vote for: 1) Election of Directors, 2) Ratification of Selection of Auditors, 3) Approve Advisor Agreement with Investors Management Group (IMG), 4) Approve the IPAIT Plan under SEC Rule 12B-1, and 5) Change the Investment Policy to change the maximum maturity of securities held in the portfolio from 365 days to 397 days to be consistent with SEC Rule 2a-7 and Iowa statute. The annual shareholder meeting was held on August 24, 2004 and the Trustees’ ratified the proxy statement at the annual IPAIT board meeting on August 25, 2004. IPAIT's Investment Policy (enclosed on page 41) outlines the guidelines and requirements for investment decisions.

On behalf of IPAIT’s Board of Trustees, sponsoring associations and service providers, we thank you for your continued support of the Iowa Public Agency Investment Trust. We encourage you to contact us with comments and suggestions regarding any improvements to the operation of the Program. Your involvement in the Program is essential in IPAIT’s ability to provide competitive investment alternatives and ongoing education for our members.

As we begin fiscal year 2004-2005, IPAIT will continue to expand services within IPASonline, the Internet-based Participant Accounting System utilized by IPAIT. We strive to be a resource for you and your entities through our quarterly newsletters and webcasts. The www.IPAIT.org website provides monthly updates on the Program as well as access to the secure IPASonline system. We collectively pledge to continue working together to provide a safe source of interest income for every participant and to provide helpful, convenient cash management related information.

/s/ Donald W. Kerker | |

|

Respectfully, |

Donald W. Kerker |

Chair, Board of Trustees |

IOWA PUBLIC AGENCY INVESTMENT TRUST |

6

MANAGEMENT REPORT

TO IPAIT PARTICIPANTS:

While IPAIT’s Diversified Fund and DGO Fund financial statements and the related financial data contained in these CAFR have been prepared in conformity with generally accepted accounting principles and have been audited by IPAIT’s Independent Auditor, KPMG LLP, the ultimate accuracy and validity of this information is the responsibility of the management of the Iowa Public Agency Investment Trust Board of Trustees. To carry out this responsibility, the Board of Trustees maintains financial policies, procedures, accounting systems and internal controls which the Board believes provide reasonable, but not absolute, assurance that accurate financial records are maintained and investment assets are safeguarded.

In addition, the three ex-officio trustees meet with the Program’s service providers and legal counsel to review all aspects of IPAIT performance each month. The Board of Trustees meets quarterly to similarly review Program performance and compliance. In addition, IPAIT is regularly subjected to a comprehensive review of all services and costs of operation by the IPAIT Board of Trustees. In September 2003, the investment advisory and administration fee was voluntarily reduced by our service provider. In addition, the Board authorized waiving 2.5 basis points of administrative fees to help improve yield during this low interest rate environment. This year’s CAFR will be submitted to the GFOA for consideration for a Certificate of Achievement for Excellence in Financial Reporting following receipt of a seventh consecutive Certificate of Achievement for the fiscal year ended June 2003 CAFR.

In the Board’s opinion, IPAIT’s internal controls are adequate to ensure that the financial information in this report presents fairly the IPAIT Diversified and DGO Fund operations and financial condition.

Sincerely, |

|

/s/ Robert Haug | |

|

Robert Haug |

Secretary, Board of Trustees |

IOWA PUBLIC AGENCY INVESTMENT TRUST |

7

BOARD OF TRUSTEES

| |

| |

| |

Mr. Thomas Bredweg

Executive Director,

Iowa League of Cities,

IPAIT Treasurer to the Board | | Mr. William Peterson

Executive Director,

Iowa State Association of Counties

IPAIT Assistant Secretary to the Board | | Mr. Robert Haug

Executive Director,

Iowa Association of Municipal Utilities,

IPAIT Secretary to the Board | |

| | | | | |

| |

| |

| |

Mr. Jody Smith

Director of Administrative Services

City of West Des Moines | | Mr. Donald Kerker

Director of Finance

Muscatine Power and Water | | Mr. Floyd Magnusson

Supervisor

Webster County | |

| | | | | |

| |

| |

| |

Mr. Tom Hanafan

Mayor

Council Bluffs | | Ms. Dianne Kiefer

County Treasurer

Wapello County | | Mr. Leon Rodas

General Manager

Spencer Municipal Utility | |

| | | | | |

| |

| |

| |

Ms. Susan Vavroch

City Treasurer

City of Cedar Rapids | | Mr. Robert Hagey

County Treasurer

Sioux County | | Mr. Craig Hall

Superintendent

Brooklyn Municipal Utility | |

The trustees are not compensated for Board service.

Expenses incurred in attending meetings are paid by the Trust.

8

Name, Contact,

Address and Age | | Position

held with

IPAIT | | Term of Office

and Length of

Time Served | | Principal Occupations

During Past Five Years | | Number of

Portfolios

Overseen by

Director | | Other

Directorships

held Outside of

IPAIT | |

| | | | | | | | | | | |

Robert Hagey | | Trustee | | Term ending 2005 | | Sioux County Treasurer | | 2 | | None | |

| | | | | | | | | | | |

210 Central Ave. SW | | | | | | | | | | | |

Orange City, IA 51041 | | | | Served since 1993 | | | | | | | |

| | | | | | | | | | | |

Age 53 | | | | | | | | | | | |

| | | | | | | | | | | |

Thomas Hanafan | | Trustee, Vice Chair | | Term ending 2006 | | Council Bluffs Mayor | | 2 | | None | |

| | | | | | | | | | | |

209 Pearl Street | | | | | | | | | | | |

Council Bluffs, IA | | | | Served since 1992 | | | | | | | |

51503 | | | | | | | | | | | |

| | | | | | | | | | | |

Age 56 | | | | | | | | | | | |

| | | | | | | | | | | |

Donald Kerker | | Trustee, Chair | | Term ending 2005 | | Director of Finance, | | 2 | | None | |

| | | | Served since 1999 | | Muscatine Power and | | | | | |

3205 Cedar Street | | | | | | Water | | | | | |

Muscatine, IA 52761 | | | | | | | | | | | |

| | | | | | | | | | | |

Age 53 | | | | | | | | | | | |

| | | | | | | | | | | |

Dianne Kiefer | | Trustee, | | Term ending 2007 | | Wapello County | | 2 | | None | |

| | Second | | | | Treasurer | | | | | |

101 W. Fourth Street, | | Vice Chair | | | | | | | | | |

Ottumwa, IA 52501 | | | | Served since 2000 | | College Instructor, Buena | | | | | |

| | | | | | Vista University | | | | | |

Age 54 | | | | | | | | | | | |

| | | | | | | | | | | |

Floyd Magnusson | | Trustee | | Term ending 2006 | | Webster County | | 2 | | None | |

| | | | | | Supervisor | | | | | |

703 Central Avenue | | | | | | | | | | | |

Fort Dodge, Iowa | | | | Served since 2000 | | | | | | | |

50501 | | | | | | | | | | | |

| | | | | | | | | | | |

Age 78 | | | | | | | | | | | |

| | | | | | | | | | | |

Craig Hall | | Trustee | | Term ending 2007 | | Manager, Brooklyn | | 2 | | None | |

| | | | | | Municipal Utilities | | | | | |

138 Jackson St. | | | | | | | | | | | |

Brooklyn, Iowa | | | | Served since 2004 | | | | | | | |

| | | | | | | | | | | |

Age 52 | | | | | | | | | | | |

9

Leon Rodas | | Trustee | | Term ending 2006 | | General Manager, | | 2 | | None | |

| | | | | | Spencer Municipal Utility | | | | | |

712 North Grand | | | | | | | | | | | |

Avenue P.O. Box 222 | | | | Served since 2003 | | | | | | | |

Spencer, IA 51301 | | | | | | | | | | | |

| | | | | | | | | | | |

Age 51 | | | | | | | | | | | |

| | | | | | | | | | | |

Jody Smith | | Trustee | | Term ending 2007 | | Director of | | 2 | | None | |

| | | | | | Administrative Services, | | | | | |

P.O. Box 65320 | | | | | | West Des Moines City | | | | | |

West Des Moines, IA | | | | Served since 1994 | | Clerk | | | | | |

50266 | | | | | | | | | | | |

| | | | | | | | | | | |

Age 51 | | | | | | | | | | | |

| | | | | | | | | | | |

Susan Vavroch | | Trustee | | Term ending 2005 | | Cedar Rapids City | | 2 | | None | |

| | | | | | Treasurer | | | | | |

50 Second Ave. Bridge | | | | | | | | | | | |

Cedar Rapids, IA | | | | Served since 2003 | | | | | | | |

52401 | | | | | | | | | | | |

| | | | | | | | | | | |

Age 46 | | | | | | | | | | | |

| | | | | | | | | | | |

Thomas Bredeweg | | Trustee | | Served since 1992 | | Iowa League of Cities | | 2 | | None | |

| | | | | | | | | | | |

317 Sixth Avenue, Ste | | | | | | Executive Director | | | | | |

1400 | | | | | | | | | | | |

Des Moines, IA 50309 | | | | | | IPAIT Treasurer | | | | | |

| | | | | | | | | | | |

Age 56 | | | | | | | | | | | |

| | | | | | | | | | | |

William Peterson | | Trustee | | Served since 1979 | | Iowa State Association of | | 2 | | None | |

| | | | | | Counties | | | | | |

501 SW Seventh St, | | | | | | | | | | | |

Ste Q | | | | | | Executive Director | | | | | |

Des Moines, IA 50309 | | | | | | | | | | | |

| | | | | | IPAIT Assistant Secretary | | | | | |

Age 54 | | | | | | | | | | | |

| | | | | | | | | | | |

Robert Haug | | Trustee | | Served since 1986 | | Iowa Association of | | 2 | | None | |

| | | | | | Municipal Utilities | | | | | |

1735 NE 70th Avenue | | | | | | | | | | | |

Ankeny, IA 50021 | | | | | | Executive Director | | | | | |

| | | | | | | | | | | |

Age 57 | | | | | | IPAIT Secretary | | | | | |

10

SERVICE PROVIDERS

Sponsoring Associations

IOWA

ASSOCIATION OF MUNICIPAL

UTILITIES

Iowa Association of Municipal Utilities

1735 NE 70th Avenue

Ankeny, IA 50021-9353

Robert Haug, Executive Director

bhaug@iamu.org

515-289-1999

Iowa League of Cities

317 Sixth Avenue

Suite 800

Des Moines, IA 50309

Thomas G. Bredeweg, Executive Director

tombredeweg@iowaleague.org

515-244-7282

Iowa State Association of Counties

501 SW 7th Street, Suite Q

Des Moines, IA 50309

William R. Peterson, Executive Director

bpeterson@iowacounties.org

515-244-7181

11

Investment Adviser - Administrator - Program Support

Investors Management Group

1415 28th Street, Suite 200

West Des Moines, IA 50266-1461

Lynn Maaske 515-224-2759

lynn.maaske@amcore.com

Jeff Lorenzen 515-224-2718

jeff.lorenzen@amcore.com

Ron Shortenhaus 515-224-2724

ron.shortenhaus@amcore.com

Anita Tracy 515-224-2725

anita.tracy@amcore.com

Custodian

Wells Fargo Bank, N.A.

MAC N8200-034

666 Walnut Street, P.O. Box 837

Des Moines, IA 50304-0837

MJ Dolan 515-244-8326

m.j.dolan@wellsfargo.com

Teresa Smith 515-245-3245

teresa.a.smith@wellsfargo.com

Legal Counsel

AHLERS & COONEY, P.C.

Ahlers & Cooney, P.C.

100 Court Avenue, Suite 600

Des Moines, IA 50309

Edgar Bittle 515-246-0312

ebittle@ahlerslaw.com

Elizabeth Grob 515-246-0305

egrob@ahlerslaw.com

Independent Auditor

KPMG LLP

2500 Ruan Center

Des Moines, IA 50309

12

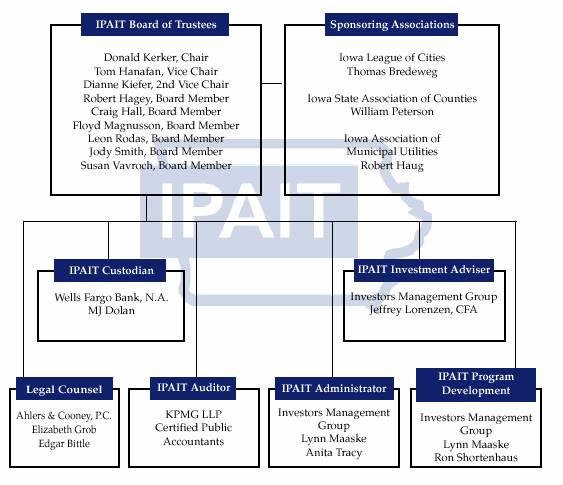

ORGANIZATION CHART

IOWA PUBLIC AGENCY INVESTMENT TRUST (IPAIT)

Diversified Fund and

Direct Government Obligation Fund

Administration Flow Chart

13

14

| | FINANCIAL SECTION |

15

|

KPMG LLP

2500 Ruan Center

666 Grand Avenue

Des Moines, IA 50309

|

Report of Independent Registered Public Accounting Firm

The Board of Trustees and Unitholders

Iowa Public Agency Investment Trust:

We have audited the accompanying statement of net assets of the Diversified Portfolio of the Iowa Public Agency Investment Trust (the Portfolio) as of June 30, 2004, and the related statements of operations for each of the years in the five-year period then ended, statements of changes in net assets for each of the years in the two-year period then ended, and financial highlights for each of the years in the five-year period then ended. These financial statements and the financial highlights are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on these financial statements and the financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board. Those standards require that we plan and perform our audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Investment securities held in custody are confirmed to us by the Custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

As discussed in note 1 to the financial statements, effective July 1, 2002, the Diversified Portfolio of the Trust adopted the provisions of Governmental Accounting Standards Board (GASB) Statement No. 34, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments, GASB Statement No. 37, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments: Omnibus, and GASB Statement No. 38, Certain Financial Statement Disclosures.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Diversified Portfolio of the Iowa Public Agency Investment Trust at June 30, 2004, and the results of its operations for each of the years in the five-year period then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years presented, in conformity with accounting principles generally accepted in the United States of America.

The management’s discussion and analysis on pages 17 to 18 is not a required part of the basic financial statements but is supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the supplementary information. However, we did not audit the information and express no opinion on it.

July 16, 2004

KPMG LLP, a U.S. limited liability partnership, is the U.S.

member firm of KPMG International, a Swiss Cooperative.

16

MANAGEMENT’S DISCUSSION & ANALYSIS

This section of the IPAIT Diversified Portfolio’s annual Financial Statements presents Management’s Discussion and Analysis of the financial position and results of operations for the fiscal year ended June 30, 2004 (FY 04). This information is being presented to provide additional information regarding the activities of the Authority, pursuant to the requirements of Governmental Accounting Standards Board Statement No. 34, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments, Statement No. 37, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments: Omnibus, and Statement No. 38, Certain Financial Statement Note Disclosures (Statements Nos. 34, 37, and 38). This discussion and analysis should be read in conjunction with the Independent Auditor’s Report of KPMG LLP, the Financial Statements, and the accompanying notes.

In addition to the historical information, the Management’s Discussion and Analysis includes certain forward-looking statements that involve certain risks and uncertainties. The actual results of IPAIT’s Diversified Portfolio may differ materially from the results expressed or implied in such forward-looking statements due to a wide range of factors including changes in general economic conditions, fluctuations in interest rates, and legislative changes.

Overview of the Financial Statements

The Management’s Discussion and Analysis provides an introduction to and overview of the basic financial statements of IPAIT’s Diversified Portfolio. The following components comprise the financial statements: 1) Statement of Net Assets, 2) Statements of Operations, 3) Statements of Changes in Net Assets, 4) Financial Highlights, and 5) Notes to Financial Statements.

• The Statement of Net Assets shows the financial position (assets and liabilities) of the portfolio as of the date of the current fiscal year end.

• The Statements of Operations displays the results of operations (income and expenses) of the portfolio for the five most recent fiscal years.

• The Statements of Changes in Net Assets portray participant/unitholder activity (distributions, sales, reinvestments, redemptions) of the portfolio for the two most recent fiscal years.

• The Financial Highlights depict per share/per unit information (net investment income, dividends distributed, net asset value, total return, ratios of expenses and net investment income to average net assets) and summary total net assets of the portfolio for the five most recent fiscal years.

• The Notes to Financial Statements describe significant accounting policies and disclose summary security transaction amounts of the portfolio.

Condensed Financial Information and Financial Analysis

Year-to-year variances in most financial statement amounts reported in IPAIT’s Diversified Portfolio are most significantly impacted by the level of average net assets (which fluctuates based on the overall levels of participant/unitholder invested balances). Additionally, changes in the short-term interest rate environment (which follows the general trend established by monetary policy set by the Federal Reserve) contribute to year-over-year variances in the amount of investment income earned by the portfolio.

During FY 04, average net assets decreased 7.44 percent to $248,770,769 from average net assets of $268,772,324 during the fiscal year ended June 30, 2003 (FY 03) for the Diversified Portfolio. While overnight rates remained stable at 1.00 percent through most of FY 04, one-year rates rose dramatically as the economic recovery became reality. The Federal Reserve raised the overnight rate in late June 2004 to 1.25 percent. The one-year rate gradually drifted upward during the first part of the year from 1.12 percent and shifted upward dramatically during the months of April, May and June to 2.33 percent, once the employment numbers began to firm up.

17

Condensed financial information and variance explanations for FY 04 and FY 03 follows.

Diversified Portfolio:

| | Balances as of June 30, 2004 | | Balances as of June 30, 2003 | | Percent Change | |

Total Investments | | $ | 254,078,254 | | $ | 244,859,425 | | 3.76 | % |

Net Assets | | $ | 254,818,110 | | $ | 245,025,051 | | 4.00 | % |

Investment Income | | $ | 2,680,795 | | $ | 4,035,199 | | -33.56 | % |

Total Expenses | | $ | 1,202,977 | | $ | 1,503,506 | | -19.99 | % |

Net Investment Income | | $ | 1,477,818 | | $ | 2,531,693 | | -41.63 | % |

Units Sold | | 941,862,304 | | 912,307,966 | | 3.24 | % |

Units Redeemed | | 933,547,063 | | 923,762,855 | | 1.06 | % |

Total investments and net assets increased 3.76 percent and 4.00 percent, respectively, comparing June 30, 2004 and June 30, 2003 amounts, due to excess of units sold versus units redeemed in FY 04 and the reinvestment of investment income that resulted in higher aggregate participant balances at FY 04. Investment income and net investment income decreased 33.56 percent and 41.63 percent, respectively, during FY 04 compared to FY 03 primarily due to the lower interest rate environment. Total expenses decreased 19.99 percent during FY 04 compared to FY 03 due to a reduction of both investment advisory and administrative fees. During FY 04 compared to FY 03, units sold and redeemed increased 3.24 percent and 1.06 percent, respectively, caused by an increase in participant transactions. Participant transactions increased due to the participants depositing money in the portfolio until they were able to determine their cash flow needs.

18

FINANCIAL STATEMENTS

Iowa Public Agency Investment Trust — Diversified Portfolio

Statement of Net Assets — June 30, 2004

(Showing Percentage of Net Assets)

PAR

VALUE | | DESCRIPTION | | YIELD AT

TIME OF

PURCHASE | | DUE DATE | | AMORTIZED

COST | |

DISCOUNTED GOVERNMENT SECURITIES — 1.17% | | | | | | | |

$ | 3,000,000 | | Federal Home Loan Mortgage Corporation, Discount Note | | 1.11 | % | 10/05/04 | | $ | 2,991,280 | |

TOTAL (cost — $2,991,280) | | | | | | $ | 2,991,280 | |

| | | | | | | | | |

COUPON SECURITIES — 21.01% | | | | | | | |

$ | 5,000,000 | | Tennessee Valley Authority, 4.75% | | 1.19 | % | 07/15/04 | | $ | 5,006,776 | |

2,000,000 | | Student Loan Marketing Association, 3.375% | | 1.06 | % | 07/15/04 | | 2,001,766 | |

3,000,000 | | Federal National Mortgage Association, 6.50% | | 1.23 | % | 08/15/04 | | 3,019,640 | |

1,000,000 | | Federal National Mortgage Association, 6.50% | | 1.14 | % | 08/15/04 | | 1,006,602 | |

2,530,000 | | Federal Home Loan Mortgage Corporation, 4.50% | | 1.07 | % | 08/15/04 | | 2,540,742 | |

3,000,000 | | Federal National Mortgage Association, 3.50% | | 1.40 | % | 09/15/04 | | 3,012,928 | |

3,000,000 | | Federal National Mortgage Association, 3.50% | | 1.07 | % | 09/15/04 | | 3,014,945 | |

3,500,000 | | Federal Home Loan Bank, 3.625% | | 1.28 | % | 10/15/04 | | 3,523,551 | |

2,095,000 | | Federal Home Loan Bank, 3.625% | | 1.08 | % | 10/15/04 | | 2,110,290 | |

3,000,000 | | Federal Home Loan Mortgage Corporation, 3.25% | | 1.50 | % | 11/15/04 | | 3,019,398 | |

3,000,000 | | Federal Home Loan Bank, 4.125% | | 1.05 | % | 11/15/04 | | 3,034,090 | |

2,245,000 | | Federal Home Loan Bank, 2.00% | | 1.23 | % | 11/15/04 | | 2,251,382 | |

3,000,000 | | Federal Home Loan Bank, 2.125% | | 1.12 | % | 12/15/04 | | 3,013,645 | |

3,000,000 | | Federal National Mortgage Association, 1.875% | | 1.11 | % | 12/15/04 | | 3,010,396 | |

3,217,000 | | Federal Home Loan Mortgage Corporation, 6.875% | | 1.17 | % | 01/15/05 | | 3,315,571 | |

5,000,000 | | Federal Home Loan Mortgage Corporation, 6.875% | | 1.35 | % | 01/15/05 | | 5,148,545 | |

2,325,000 | | Federal National Mortgage Association, 7.125% | | 1.52 | % | 02/15/05 | | 2,405,295 | |

3,000,000 | | Federal National Mortgage Association, 7.125% | | 1.73 | % | 02/15/05 | | 3,099,412 | |

TOTAL (cost — $53,534,974) | | | | | | $ | 53,534,974 | |

| | | | | | | | | |

CERTIFICATES OF DEPOSIT — 7.36% | | | | | | | |

$ | 1,000,000 | | Premier Bank, Dubuque | | 1.40 | % | 08/03/04 | | $ | 1,000,000 | |

250,000 | | Citizens Bank, Sac City | | 1.40 | % | 08/13/04 | | 250,000 | |

1,000,000 | | Peoples Savings Bank, Charles City | | 1.45 | % | 08/16/04 | | 1,000,000 | |

500,000 | | Premier Bank, Rock Valley | | 1.40 | % | 08/25/04 | | 500,000 | |

500,000 | | Premier Bank, Rock Valley | | 1.40 | % | 08/30/04 | | 500,000 | |

500,000 | | Farmers State Bank, Hawarden | | 1.45 | % | 08/31/04 | | 500,000 | |

1,500,000 | | Union State Bank, Winterset | | 1.55 | % | 09/07/04 | | 1,500,000 | |

500,000 | | First American Bank, Ames | | 1.55 | % | 09/14/04 | | 500,000 | |

500,000 | | Tri County Bank & Trust, Cascade | | 1.55 | % | 10/18/04 | | 500,000 | |

500,000 | | Great River Bank & Trust, Princeton | | 1.35 | % | 10/18/04 | | 500,000 | |

900,000 | | First State Bank, Ida Grove | | 1.60 | % | 11/25/04 | | 900,000 | |

500,000 | | Farmers State Bank, Hawarden | | 1.75 | % | 11/29/04 | | 500,000 | |

1,000,000 | | Liberty Bank, West Des Moines | | 1.60 | % | 12/08/04 | | 1,000,000 | |

500,000 | | First Central State Bank, DeWitt | | 2.10 | % | 12/20/04 | | 500,000 | |

800,000 | | Exchange Bank, Collins | | 1.60 | % | 01/07/05 | | 800,000 | |

250,000 | | Ft. Madison Bank & Trust, Ft. Madison | | 1.60 | % | 01/14/05 | | 250,000 | |

250,000 | | Ft. Madison Bank & Trust, Ft. Madison | | 1.60 | % | 01/21/05 | | 250,000 | |

500,000 | | Ft. Madison Bank & Trust, Ft. Madison | | 1.60 | % | 01/27/05 | | 500,000 | |

1,000,000 | | Liberty Bank, West Des Moines | | 1.60 | % | 02/03/05 | | 1,000,000 | |

1,000,000 | | Premier Bank, Dubuque | | 1.60 | % | 02/04/05 | | 1,000,000 | |

250,000 | | Citizens Bank, Sac City | | 1.60 | % | 02/10/05 | | 250,000 | |

See accompanying notes to financial statements.

19

PAR

VALUE | | DESCRIPTION | | YIELD AT

TIME OF

PURCHASE | | DUE DATE | | AMORTIZED

COST | |

| | | | | | | | | |

1,000,000 | | St. Ansgar State Bank, St. Ansgar | | 1.60 | % | 03/04/05 | | 1,000,000 | |

100,000 | | Maxwell State Bank, Maxwell | | 1.60 | % | 03/22/05 | | 100,000 | |

1,000,000 | | First American Bank, Ames | | 2.45 | % | 03/30/05 | | 1,000,000 | |

250,000 | | Citizens Bank, Sac City | | 1.65 | % | 04/01/05 | | 250,000 | |

500,000 | | Ft. Madison Bank & Trust, Ft. Madison | | 1.75 | % | 04/19/05 | | 500,000 | |

250,000 | | Maquoketa State Bank, Maquoketa | | 1.75 | % | 04/21/05 | | 250,000 | |

200,000 | | Maxwell State Bank, Maxwell | | 1.75 | % | 04/22/05 | | 200,000 | |

500,000 | | Ft. Madison Bank & Trust, Ft. Madison | | 1.75 | % | 04/29/05 | | 500,000 | |

250,000 | | Citizens Bank, Sac City | | 2.45 | % | 06/14/05 | | 250,000 | |

1,000,000 | | American Bank, LeMars | | 2.50 | % | 06/14/05 | | 1,000,000 | |

TOTAL (cost — $18,750,000) | | | | | | $ | 18,750,000 | |

| | | | | | | | | |

REPURCHASE AGREEMENTS (collateralized by U.S. Govt. Securities) — 70.17% | | | | | |

$ | 63,500,000 | | Bear, Stearns & Company, Repurchase Agreement | | 1.40 | % | 07/01/04 | | $ | 63,500,000 | |

51,802,000 | | Merrill Lynch, Repurchase Agreement | | 1.25 | % | 07/01/04 | | 51,802,000 | |

63,500,000 | | UBS Securities, Repurchase Agreement | | 1.47 | % | 07/01/04 | | 63,500,000 | |

TOTAL (cost — $178,802,000) | | | | | | $ | 178,802,000 | |

| | | | | | | | | |

TOTAL INVESTMENTS — 99.71% (cost — $254,078,254) | | | | | | $ | 254,078,254 | |

| | | | | | | | | |

EXCESS OF OTHER ASSETS OVER TOTAL LIABILITIES — .29%

(Includes $63,210 payable to IMG and $124,571 dividends payable to unitholders) | | | | | | $ | 739,856 | |

| | | | | | | | | |

NET ASSETS — 100% | | | | | | | |

| | Applicable to 254,818,110 outstanding units | | | | | | $ | 254,818,110 | |

| | | | | | | | | |

NET ASSET VALUE: | | | | | | $ | 1.00 | |

| | Offering and redemption price per unit ($254,818,110 divided by 254,818,110 units outstanding) | | | | | | | |

| | | | | | | | | | | |

See accompanying notes to financial statements.

20

FINANCIAL STATEMENTS

Iowa Public Agency Investment Trust

Statements of Operations — Diversified Portfolio

For the Years Ended June 30,

| | 2004 | | 2003 | | 2002 | | 2001 | | 2000 | |

| | | | | | | | | | | |

INVESTMENT INCOME: | | | | | | | | | | | |

Interest | | $ | 2,680,795 | | $ | 4,035,199 | | $ | 7,432,829 | | $ | 14,889,152 | | $ | 12,205,834 | |

| | | | | | | | | | | |

EXPENSES: | | | | | | | | | | | |

Investment advisory, administrative, and program support fees | | 824,382 | | 1,039,192 | | 878,974 | | 799,428 | | 675,117 | |

Custody fees | | 119,774 | | 128,349 | | 346,055 | | 314,294 | | 263,064 | |

Distribution fees | | 249,452 | | 268,772 | | 282,276 | | 255,831 | | 212,952 | |

Other fees and expenses | | 9,369 | | 67,193 | | 70,569 | | 63,958 | | 53,238 | |

| | | | | | | | | | | |

Total Expenses | | 1,202,977 | | 1,503,506 | | 1,577,874 | | 1,433,511 | | 1,204,371 | |

| | | | | | | | | | | |

NET INVESTMENT INCOME | | $ | 1,477,818 | | $ | 2,531,693 | | $ | 5,854,955 | | $ | 13,455,641 | | $ | 11,001,463 | |

Iowa Public Agency Investment Trust

Statements of Changes in Net Assets — Diversified Portfolio

For the Years Ended June 30,

| | 2004 | | 2003 | |

| | | | | |

From Investment Activities: | | | | | |

Net investment income distributed to unitholders | | $ | 1,447,818 | | $ | 2,531,693 | |

| | | | | |

From Unit Transactions:

(at constant net asset value of $1 per unit) | | | | | |

Units sold | | $ | 941,862,304 | | $ | 912,307,966 | |

Units issued in reinvestment of dividends from net investment income | | $ | 1,447,818 | | $ | 2,531,693 | |

Units redeemed | | (933,547,063 | ) | (923,762,855 | ) |

Net increase (decrease) in net assets derived from unit transactions | | 9,793,059 | | (8,923,196 | ) |

| | | | | |

Net assets at beginning of year | | 245,025,051 | | 253,948,247 | |

| | | | | |

Net assets at end of year | | $ | 254,818,110 | | $ | 245,025,051 | |

See accompanying notes to financial statements.

21

FINANCIAL HIGHLIGHTS

Iowa Public Agency Investment Trust - Diversified Portfolio

Selected Data for Each Unit of Portfolio

Outstanding Through Each Year Ended

June 30, | | 2004 | | 2003 | | 2002 | | 2001 | | 2000 | |

| | | | | | | | | | | |

Net Asset Value, Beginning of Year | | $ | 1,000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | |

Net Investment Income | | 0.006 | | 0.009 | | 0.021 | | 0.053 | | 0.051 | |

Dividends Distributed | | (0.006 | ) | (0.009 | ) | (0.021 | ) | (0.053 | ) | (0.051 | ) |

Net Asset Value, End of Year | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | |

| | | | | | | | | | | |

Total Return | | 0.60 | % | 0.95 | % | 2.14 | % | 5.34 | % | 5.13 | % |

Ratio of Expenses to Average Net Assets | | 0.48 | % | 0.56 | % | 0.56 | % | 0.56 | % | 0.57 | % |

Ratio of Net Investment Income to Average Net Assets | | 0.59 | % | 0.94 | % | 2.07 | % | 5.34 | % | 5.13 | % |

Net Assets, End of Year (000 Omitted) | | $ | 254,818 | | $ | 245,025 | | $ | 253,948 | | $ | 265,091 | | $ | 216,460 | |

See accompanying notes to financial statements.

22

NOTES TO FINANCIAL STATEMENTS

(1) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Iowa Public Agency Investment Trust (IPAIT) is a common law trust established under Iowa law pursuant to Chapter 28E and Sections 331.555 and 384.21, Iowa Code (1987), as amended, which authorizes Iowa public agencies to jointly invest monies pursuant to a joint investment agreement. IPAIT is registered under the Investment Company Act of 1940. IPAIT was established by the adoption of a Joint Powers Agreement and Declaration of Trust as of October 1, 1987, and commenced operations on November 13, 1987. The Joint Powers Agreement and Declaration of Trust was amended September 1, 1988, and again on May 1, 1993. As amended, IPAIT is authorized to operate and now operates investment programs, one of which is the Diversified Portfolio. The accompanying financial statements include activities of the Diversified Portfolio. The objective of the portfolio is to maintain a high degree of liquidity and safety of principal through investment in short-term securities as permitted for Iowa public agencies under Iowa law. Wells Fargo Bank, N.A. (Wells Fargo), serves as the Custodian, and Investors Management Group (IMG) serves as the Investment Adviser, Administrator and Program Support Provider.

The preparation of financial statements, in conformity with accounting principles generally accepted in the United States of America, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of net investment income during the year. Actual results could differ from those estimates.

In reporting financial activity, IPAIT applies applicable Governmental Accounting Standards Board (GASB) pronouncements, as well as all Financial Accounting Standards Board and predecessor statements and interpretations not in conflict with GASB pronouncements.

IPAIT has adopted GASB Statement No. 34, Basic Financial Statements - - and Management’s Discussion and Analysis - for State and Local Governments, as amended by Statement No. 37, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments: Omnibus, and modified by Statement No. 38, Certain Financial Statement Note Disclosures, (Statements Nos. 34, 37, and 38) effective July 1, 2002. Adoption of Statements Nos. 34, 37, and 38 had no impact on the net assets of the Diversified Portfolio of IPAIT. The Statements require IPAIT to add a section for Management’s Discussion and Analysis as supplementary information to precede the financial statements and can be located on page 17.

IPAIT is exposed to various risks in connection with operation of the Diversified Portfolio and adheres to policies which mitigate market risk in the portfolio and maintains insurance coverage for fidelity and errors and omissions exposures. IPAIT has had no claims or settlements under its insurance coverage since its organization in 1987.

Investments in Securities

The Diversified Portfolio consists of cash and short-term investments valued at amortized cost, which approximates market value, pursuant to Rule 2a-7 under the Investment Company Act of 1940. This involves valuing a portfolio security at its original cost on the date of purchase, and thereafter amortizing any premium or discount on a straight-line basis to maturity. The amount of premium or discount amortized to income under the straight-line method does not differ materially from the amount which would be amortized to income under the interest method. Procedures are followed to maintain a constant net asset value of $1.00 per unit for the portfolio.

Security transactions are accounted for on the trade date. Interest income, including the accretion of discount and amortization of premium, is recorded daily on the accrual basis.

23

IPAIT is authorized by investment policy and statute to invest public funds in obligations of the U.S. government, its agencies and instrumentalities; certificates of deposit and other evidences of deposit at federally insured Iowa depository institutions approved and secured pursuant to Chapter 12 of the Code of Iowa; and repurchase agreements, provided that the underlying collateral consists of obligations of the U.S. government, its agencies and instrumentalities and that IPAIT’s custodian takes delivery of the collateral either directly or through an authorized custodian.

In connection with transactions in repurchase agreements, it is IPAIT’s policy that its Custodian take possession of the underlying collateral securities, the value of which exceeds the principal amount of the repurchase transaction, including accrued interest at all times. If the seller defaults and the value of the collateral declines, realization of the collateral by IPAIT may be delayed or limited. At June 30, 2004, the securities purchased under overnight agreements to resell were collateralized by government agency securities with a market value of $182,448,435.

Certificate of deposit amounts up to $100,000 are insured by the Federal Depository Insurance Company (FDIC). For public funds deposited in Iowa financial institutions in excess of the $100,000 FDIC insurance, the local financial institution must comply with Iowa Code Section 12c.22 to insure appropriate collateralization. Public funds not covered by FDIC or collateralization are covered by the state sinking fund in accordance with Chapter 12C of the Code of Iowa, which provides for additional assessments against depositories to ensure there will be no loss of public funds.

Under Governmental Accounting Standards as to custodial credit risk, IPAIT’s investments in securities are classified as category one. Category one consists of insured or registered securities or securities held by IPAIT or its agent in IPAIT’s name and is the most secure investment category description.

Unit Issues, Redemptions and Distributions

IPAIT determines the net asset value of the Diversified Portfolio daily. Units are issued and redeemed daily at the daily net asset value. Dividends from net investment income are declared daily and distributed monthly.

Income Taxes

IPAIT is exempt from both federal income taxes pursuant to Section 115 of the internal revenue code and state income taxes.

Fees and Expenses

Under separate agreements with IPAIT, IMG, the Investment Adviser, Administrator and Program Support Provider, and Wells Fargo, the Custodian, are paid an annual fee for operating the investment program.

From July 1, 2003 to August 27, 2003, IMG received .305 percent of the average daily net asset value up to $150 million, .260 percent from $150 to $300 million, and .215 percent exceeding $300 million for investment advisory and administrative fees. In addition, IMG received .100 percent of the average daily net asset value up to $250 million and .125 percent exceeding $250 million for program support fees. Beginning August 28, 2003, the investment advisory and administrative fees were reduced to .260 percent of the average daily net asset value up to $150 million, .215 percent from $150 to $250 million, and .170 percent exceeding $250 million. Beginning August 28, 2003, the program support fee was reduced to .080 percent of the average daily net asset value. For the year ended June 30, 2004 the Diversified Portfolio paid $824,382 to IMG for services provided.

Wells Fargo receives .050 percent of the average daily net asset value up to $150 million, .045 percent from $150 to $300 million, and .040 percent exceeding $300 million for custodial services. For the year ended June 30, 2004, the Diversified Portfolio paid $119,774 to Wells Fargo for services provided.

Under a distribution plan the public agency associations collectively receive an annual fee of .100 percent of the daily net asset value of the portfolio. For the year ended June 30, 2004, the Diversified Portfolio paid $157,587 to the Iowa League of Cities, $58,908 to the Iowa State Association of Counties, and $32,957 to the Iowa Association of Municipal Utilities.

IPAIT is responsible for other fees and expenses incurred directly by IPAIT. Other fees and expenses were accrued daily at a rate of .025 percent of the average daily net asset value through August 28, 2003, and amounted to $9,369 for the year ended June 30, 2004. The accrual of .025 percent has been temporarily suspended through December 31, 2004. All fees are computed daily and paid monthly.

(2) SECURITIES TRANSACTIONS

Purchases of portfolio securities for the Diversified Portfolio aggregated $45,997,369,189 for the year ended June 30, 2004. Proceeds from maturities of securities for the Diversified Portfolio aggregated $45,986,810,060 for the year ended June 30, 2004.

24

|

KPMG LLP

2500 Ruan Center

666 Grand Avenue

Des Moines, IA 50309

|

Report of Independent Registered Public Accounting Firm

The Board of Trustees and Unitholders

Iowa Public Agency Investment Trust:

We have audited the accompanying statement of net assets of the Direct Government Obligation Portfolio of the Iowa Public Agency Investment Trust (the Portfolio) as of June 30, 2004, and the related statements of operations for each of the years in the five-year period then ended, statements of changes in net assets for each of the years in the two-year period then ended, and financial highlights for each of the years in the five-year period then ended. These financial statements and the financial highlights are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on these financial statements and the financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board. Those standards require that we plan and perform our audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Investment securities held in custody are confirmed to us by the Custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

As discussed in note 1 to the financial statements, effective July 1, 2002, the Direct Government Obligation Portfolio of the Trust adopted the provisions of Governmental Accounting Standards Board (GASB) Statement No. 34, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments, GASB Statement No. 37, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments: Omnibus, and GASB Statement No. 38, Certain Financial Statement Disclosures.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Direct Government Obligation Portfolio of the Iowa Public Agency Investment Trust at June 30, 2004, and the results of its operations for each of the years in the five-year period then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years presented, in conformity with accounting principles generally accepted in the United States of America.

The management’s discussion and analysis on pages 26 to 27 is not a required part of the basic financial statements but is supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the supplementary information. However, we did not audit the information and express no opinion on it.

July 16, 2004

KPMG LLP, a U.S. limited liability partnership, is the U.S.

member firm of KPMG International, a Swiss Cooperative.

25

MANAGEMENT’S DISCUSSION & ANALYSIS

This section of the IPAIT DGO Portfolio’s annual Financial Statements presents Management’s Discussion and Analysis of the financial position and results of operations for the fiscal year ended June 30, 2004 (FY 04). This information is being presented to provide additional information regarding the activities of the Authority, pursuant to the requirements of Governmental Accounting Standards Board Statement No. 34, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments, Statement No. 37, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments: Omnibus, and Statement No. 38, Certain Financial Statement Note Disclosures (Statements Nos. 34, 37, and 38). This discussion and analysis should be read in conjunction with the Independent Auditor’s Report of KPMG LLP, the Financial Statements, and the accompanying notes.

In addition to the historical information, the Management’s Discussion and Analysis includes certain forward-looking statements that involve certain risks and uncertainties. The actual results of IPAIT’s DGO Portfolio may differ materially from the results expressed or implied in such forward-looking statements due to a wide range of factors including changes in general economic conditions, fluctuations in interest rates, and legislative changes.

Overview of the Financial Statements

The Management’s Discussion and Analysis provides an introduction to and overview of the basic financial statements of IPAIT’s DGO Portfolio. The following components comprise the financial statements: 1) Statement of Net Assets, 2) Statements of Operations, 3) Statements of Changes in Net Assets, 4) Financial Highlights, and 5) Notes to Financial Statements.

• The Statement of Net Assets shows the financial position (assets and liabilities) of the portfolio as of the date of the current fiscal year-end.

• The Statements of Operations displays the results of operations (income and expenses) of the portfolio for the five most recent fiscal years.

• The Statements of Changes in Net Assets portray participant/unitholder activity (distributions, sales, reinvestments, redemptions) of the portfolio for the two most recent fiscal years.

• The Financial Highlights depict per share/per unit information (net investment income, dividends distributed, net asset value, total return, ratios of expenses and net investment income to average net assets) and summary total net assets of the portfolio for the five most recent fiscal years.

• The Notes to Financial Statements describe significant accounting policies and disclose summary security transaction amounts of the portfolio.

Condensed Financial Information and Financial Analysis

Year-to-year variances in most financial statement amounts reported in IPAIT’s DGO Portfolio are most significantly impacted by the level of average net assets (which fluctuates based on the overall levels of participant/unitholder invested balances). Additionally, changes in the short-term interest rate environment (which follows the general trend established by monetary policy set by the Federal Reserve) contribute to year-over-year variances in the amount of investment income earned by the portfolio.

During FY 04, average net assets decreased 29.73 percent to $50,490,269 from average net assets of $71,854,148 during the fiscal year ended June 30, 2003 (FY 03) for the DGO Portfolio. While overnight rates remained stable at 1.00 percent through most of FY 04, one-year rates rose dramatically as the economic recovery became reality. The Federal Reserve raised the overnight rate in late June 2004 to 1.25 percent. The one-year rate gradually drifted upward during the first part of the year from 1.12 percent and shifted upward dramatically during the months of April, May and June to 2.33 percent, once the employment numbers began to firm up.

26

Condensed financial information and variance explanations for FY 04 and FY 03 follows.

Direct Government Obligation Portfolio:

| | Balances as of June 30, 2004 | | Balances as of June 30, 2003 | | Percent Change | |

Total Investments | | $ | 37,465,472 | | $ | 52,216,865 | | -28.25 | % |

Net Assets | | $ | 37,532,248 | | $ | 52,291,241 | | -28.22 | % |

Investment Income | | $ | 520,560 | | $ | 1,074,831 | | -51.57 | % |

Total Expenses | | $ | 255,306 | | $ | 416,758 | | -38.74 | % |

Net Investment Income | | $ | 265,254 | | $ | 658,073 | | -59.69 | % |

Units Sold | | 30,120,495 | | 43,658,241 | | -31.01 | % |

Units Redeemed | | 45,144,742 | | 58,486,403 | | -22.81 | % |

Total investments and net assets declined 28.25 percent and 28.22 percent, respectively, comparing June 30, 2004 and June 30, 2003 amounts, due to scheduled withdrawals causing a decrease of participant balances at FY 04. Investment income and net investment income decreased 51.57 percent and 59.69 percent, respectively, during FY 04 compared to FY 03 primarily due to the lower interest rate environment and partially due to lower average net assets. Total expenses decreased 38.74 percent during FY 04 compared to FY 03 due to a reduction both in investment advisory and administrative fees as well as lower average net assets. Both units sold and units redeemed decreased 31.01 percent and 22.81 percent respectively due to limited money movement within the portfolio. The DGO portfolio is for use of restricted funds with specific payout schedules. In FY 04, there was less of a need for funds so money movement decreased from FY 03.

27

FINANCIAL STATEMENTS

Iowa Public Agency Investment Trust — Direct Government Obligation Portfolio

Statement of Net Assets — June 30, 2004

(Showing Percentage of Net Assets)

PAR

VALUE | | DESCRIPTION | | YIELD AT

TIME OF

PURCHASE | | DUE DATE | | AMORTIZED

COST | |

| | | | | | | | | |

DISCOUNTED GOVERNMENT SECURITIES — 6.17% | | | | | | | |

$ | 1,000,000 | | United States Treasury Bill | | 1.03 | % | 10/07/04 | | $ | 997,251 | |

325,000 | | Israel Government Trust Certificate | | 1.45 | % | 11/15/04 | | 323,254 | |

1,000,000 | | Israel Government Trust Certificate | | 1.22 | % | 11/15/04 | | 995,459 | |

TOTAL (cost — $2,315,964) | | | | | | $ | 2,315,964 | |

| | | | | | | | | |

COUPON SECURITIES — 26.62% | | | | | | | |

$ | 1,000,000 | | United States Treasury, 2.25% | | 0.91 | % | 07/31/04 | | $ | 1,001,151 | |

1,000,000 | | Housing and Urban Development, 2.36% | | 1.07 | % | 08/01/04 | | 1,001,114 | |

1,500,000 | | Private Export Funding, 6.31% | | 1.20 | % | 09/30/04 | | 1,518,901 | |

400,000 | | Private Export Funding, 6.31% | | 1.37 | % | 09/30/04 | | 404,872 | |

1,000,000 | | United States Treasury, 1.875% | | 1.24 | % | 09/30/04 | | 1,001,564 | |

1,000,000 | | United States Treasury, 2.125% | | 1.05 | % | 10/31/04 | | 1,003,577 | |

1,000,000 | | United States Treasury, 5.875% | | 1.40 | % | 11/15/04 | | 1,016,581 | |

1,000,000 | | United States Treasury, 1.75% | | 1.03 | % | 12/31/04 | | 1,003,574 | |

1,000,000 | | United States Treasury, 1.625% | | 1.20 | % | 01/31/05 | | 1,002,479 | |

1,000,000 | | United States Treasury, 7.50% | | 1.56 | % | 02/15/05 | | 1,036,695 | |

TOTAL (cost — $9,990,508) | | | | | | $ | 9,990,508 | |

| | | | | | | | | |

REPURCHASE AGREEMENTS (collateralized by U.S. Govt. Securities) — 67.03% | | | | | |

$ | 9,300,000 | | Bear, Stearns & Company, Repurchase Agreement | | 1.20 | % | 07/01/04 | | $ | 9,300,000 | |

6,559,000 | | Merrill Lynch, Repurchase Agreement | | 1.05 | % | 07/01/04 | | 6,559,000 | |

9,300,000 | | UBS Securities, Repurchase Agreement | | 1.23 | % | 07/01/04 | | 9,300,000 | |

TOTAL (cost — $25,159,000) | | | | | | $ | 25,159,000 | |

| | | | | | | | | |

TOTAL INVESTMENTS — 99.82% (cost — $37,465,472) | | | | | | $ | 37,465,472 | |

| | | | | | | | | |

EXCESS OF OTHER ASSETS OVER TOTAL LIABILITIES — .18% | | | | | |

(Includes $11,299 payable to IMG and $18,148 dividends payable to unitholders) | | | | | | $ | 66,776 | |

| | | | | | | | | |

NET ASSETS — 100% | | | | | | | |

Applicable to 37,532,248 outstanding units | | | | | | $ | 37,532,248 | |

| | | | | | | | | |

NET ASSET VALUE: | | | | | | $ | 1.00 | |

Offering and redemption price per unit ($37,532,248 divided by 37,532,248 units outstanding) | | | | | | | |

| | | | | | | | | | | | | |

See accompanying notes to financial statements.

28

Iowa Public Agency Investment Trust

Statements of Operations - Direct Government Obligation Portfolio

For the Years Ended June 30,

| | 2004 | | 2003 | | 2002 | | 2001 | | 2000 | |

INVESTMENT INCOME: | | | | | | | | | | | |

Interest | | $ | 520,560 | | $ | 1,074,831 | | $ | 1,827,701 | | $ | 3,578,957 | | $ | 3,577,873 | |

| | | | | | | | | | | |

EXPENSES: | | | | | | | | | | | |

Investment advisory, administrative, and program support fees | | 177,379 | | 291,012 | | 254,067 | | 206,391 | | 215,189 | |

Custody fees | | 25,314 | | 35,927 | | 96,238 | | 78,179 | | 81,511 | |

Distribution fees | | 50,629 | | 71,855 | | 76,990 | | 62,543 | | 65,209 | |

Other fees and expenses | | 1,984 | | 17,964 | | 19,247 | | 15,635 | | 16,302 | |

| | | | | | | | | | | |

Total Expenses | | 255,306 | | 416,758 | | 446,542 | | 362,748 | | 378,211 | |

| | | | | | | | | | | |

NET INVESTMENT INCOME | | $ | 265,254 | | $ | 658,073 | | $ | 1,381,159 | | $ | 3,216,209 | | $ | 3,199,662 | |

Iowa Public Agency Investment Trust

Statements of Changes in Net Assets — Direct Government Obligation Portfolio

For the Years Ended June 30,

| | 2004 | | 2003 | |

From Investment Activities: | | | | | |

Net investment income distributed to unitholders | | $ | 265,254 | | $ | 658,073 | |

| | | | | |

From Unit Transactions: | | | | | |

(at constant net asset value of $1 per unit) | | | | | |

Units sold | | $ | 30,120,495 | | $ | 43,658,241 | |

Units issued in reinvestment of dividends from net investment income | | 265,254 | | 658,073 | |

Units redeemed | | (45,144,742 | ) | (58,486,403 | ) |

Net increase (decrease) in net assets derived from unit transactions | | (14,758,993 | ) | (14,170,089 | ) |

| | | | | |

Net assets at beginning of year | | 52,291,241 | | 66,461,330 | |

| | | | | |

Net assets at end of year | | $ | 37,532,248 | | $ | 52,291,241 | |

See accompanying notes to financial statements.

29

FINANCIAL HIGHLIGHTS

Iowa Public Agency Investment Trust – Direct Government Obligation Portfolio

Selected Data for Each Unit of Portfolio

Outstanding Through Each Year Ended

June 30, | | 2004 | | 2003 | | 2002 | | 2001 | | 2000 | |

| | | | | | | | | | | |

Net Asset Value, Beginning of Year | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | |

Net Investment Income | | 0.005 | | 0.009 | | 0.018 | | 0.052 | | 0.050 | |

Dividends Distributed | | (0.005 | ) | (0.009 | ) | (0.018 | ) | (0.052 | ) | (0.050 | ) |

Net Asset Value, End of Year | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | | $ | 1.000 | |

| | | | | | | | | | | |

Total Return | | 0.53 | % | 0.91 | % | 1.85 | % | 5.16 | % | 4.98 | % |

Ratio of Expenses to Average Net Assets | | 0.51 | % | 0.58 | % | 0.58 | % | 0.58 | % | 0.58 | % |

Ratio of Net Investment Income to Average Net Assets | | 0.53 | % | 0.92 | % | 1.79 | % | 5.16 | % | 4.98 | % |

Net Assets, End of Year (000 Omitted) | | $ | 37,532 | | $ | 52,291 | | $ | 66,461 | | $ | 59,976 | | $ | 45,366 | |

See accompanying notes to financial statements.

30

NOTES TO FINANCIAL STATEMENTS

(1) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Iowa Public Agency Investment Trust (IPAIT) is a common law trust established under Iowa law pursuant to Chapter 28E and Sections 331.555 and 384.21, Iowa Code (1987), as amended, which authorizes Iowa public agencies to jointly invest monies pursuant to a joint investment agreement. IPAIT is registered under the Investment Company Act of 1940. IPAIT was established by the adoption of a Joint Powers Agreement and Declaration of Trust as of October 1, 1987, and commenced operations on November 13, 1987. The Joint Powers Agreement and Declaration of Trust was amended September 1, 1988, and again on May 1, 1993. As amended, IPAIT is authorized to operate and now operates investment programs, one of which is the Direct Government Obligation Portfolio. The accompanying financial statements include activities of the Direct Government Obligation Portfolio. The objective of the portfolio is to maintain a high degree of liquidity and safety of principal through investment in short-term securities as permitted for Iowa public agencies under Iowa law. Wells Fargo Bank, N.A. (Wells Fargo), serves as the Custodian, and Investors Management Group (IMG) serves as the Investment Adviser, Administrator, and Program Support Provider.

The preparation of financial statements, in conformity with accounting principles generally accepted in the United States of America, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of net investment income during the year. Actual results could differ from those estimates.

In reporting financial activity, IPAIT applies applicable Governmental Accounting Standards Board (GASB) pronouncements, as well as all Financial Accounting Standards Board and predecessor statements and interpretations not in conflict with GASB pronouncements.

IPAIT has adopted GASB Statement No. 34, Basic Financial Statements - - and Management’s Discussion and Analysis - for State and Local Governments, as amended by Statement No. 37, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments: Omnibus, and modified by Statement No. 38, Certain Financial Statement Note Disclosures, (Statements Nos. 34, 37, and 38) effective July 1, 2002. Adoption of Statements Nos. 34, 37, and 38 had no impact on the net assets of the Direct Government Obligation Portfolio of IPAIT. The Statements require IPAIT to add a section for Management’s Discussion and Analysis as supplementary information to precede the financial statements and can be located on page 26.

IPAIT is exposed to various risks in connection with operation of the Direct Government Obligation Portfolio and adheres to policies which mitigate market risk in the portfolio and maintains insurance coverage for fidelity and errors and omissions exposures. IPAIT has had no claims or settlements under its insurance coverage since its organization in 1987.

Investments in Securities

The Direct Government Obligation Portfolio consists of cash and short-term investments valued at amortized cost, which approximates market value, pursuant to Rule 2a-7 under the Investment Company Act of 1940. This involves valuing a portfolio security at its original cost on the date of purchase, and thereafter amortizing any premium or discount on a straight-line basis to maturity. The amount of premium or discount amortized to income under the straight-line method does not differ materially from the amount which would be amortized to income under the interest method. Procedures are followed to maintain a constant net asset value of $1.00 per unit for the portfolio.

Security transactions are accounted for on the trade date. Interest income, including the accretion of discount and amortization of premium, is recorded daily on the accrual basis.

31

IPAIT is authorized by investment policy and statute to invest public funds in obligations of the U.S. government, its agencies and instrumentalities; and repurchase agreements, provided that the underlying collateral consists of obligations of the U.S. government, its agencies and instrumentalities and that IPAIT’s custodian takes delivery of the collateral either directly or through an authorized custodian.

In connection with transactions in repurchase agreements, it is IPAIT’s policy that its Custodian take possession of the underlying collateral securities, the value of which exceeds the principal amount of the repurchase transaction, including accrued interest at all times. If the seller defaults and the value of the collateral declines, realization of the collateral by IPAIT may be delayed or limited. At June 30, 2004, the security purchased under an overnight agreement to resell was collateralized by government securities with a market value of $25,694,292.

Under Governmental Accounting Standards as to custodial credit risk, IPAIT’s investments in securities are classified as category one. Category one consists of insured or registered securities or securities held by IPAIT or its agent in IPAIT’s name and is the most secure investment category description.

Unit Issues, Redemptions and Distributions

IPAIT determines the net asset value of the DGO Portfolio daily. Units are issued and redeemed daily at the daily net asset value. Dividends from net investment income are declared daily and distributed monthly.

Income Taxes

IPAIT is exempt from both federal income taxes pursuant to Section 115 of the internal revenue code and state income taxes.

Fees and Expenses

Under separate agreements with IPAIT, IMG, the Investment Adviser, Administrator and Program Support Provider, and Wells Fargo, the Custodian, are paid an annual fee for operating the investment programs.

From July 1, 2003 to August 27, 2003, IMG received .305 percent of the average daily net asset value up to $150 million, .260 percent from $150 to $300 million, and .215 percent exceeding $300 million for investment advisory and administrative fees. In addition, IMG received .100 percent of the average daily net asset value up to $250 million and .125 percent exceeding $250 million for program support fees. Beginning August 28, 2003, the investment advisory and administrative fees were reduced to .260 percent of the average daily net asset value up to $150 million, .215 percent from $150 to $250 million, and .170 percent exceeding $250 million. Beginning August 28, 2003, the program support fee was reduced to .080 percent of the average daily net asset value. For the year ended June 30, 2004 the DGO Portfolio paid $177,379 to IMG for services provided.

Wells Fargo receives .050 percent of the average daily net asset value up to $150 million, .045 percent from $150 to $300 million, and .040 percent exceeding $300 million for custodial services. For the year ended June 30, 2004, the DGO Portfolio paid $25,314 to Wells Fargo for services provided.

Under a distribution plan the public agency associations collectively receive an annual fee of .100 percent of the daily net asset value of the portfolio. For the year ended June 30, 2004, the DGO Portfolio paid $46,777 to the Iowa League of Cities and $3,852 to the Iowa Association of Municipal Utilities.

IPAIT is responsible for other fees and expenses incurred directly by IPAIT. Other fees and expenses were accrued daily at a rate of .025 percent of the average daily net asset value through August 28, 2003, and amounted to $1,984 for the year ended June 30, 2004. The other fees and expenses accrual of .025 percent has been temporarily suspended through December 31, 2004. All fees are computed daily and paid monthly.

(2) SECURITIES TRANSACTIONS

Purchases of portfolio securities for the DGO Portfolio aggregated $10,307,089,148 for the year ended June 30, 2004. Proceeds from maturities of securities for the DGO Portfolio aggregated $10,321,597,129 for the year ended June 30, 2004.

32

| | INVESTMENT SECTION |

33

FUND FACTS SUMMARY

DIVERSIFIED FUND FACTS

as of June 30, 2004

Investment Strategy/Goals: To provide a safe, liquid, effective investment alternative for the operating and reserve funds for Iowa’s municipalities, counties, municipal utilities and other eligible public agencies by jointly investing participant funds in a professionally managed portfolio of short-term, high-quality, legally authorized marketable securities.

Date of Inception: November 13, 1987

Total Net Assets: $255 million

Benchmarks: iMoneyNet U.S. Government & Agencies Money Fund Report Index, Iowa Code Chapter 74A 32-89 day Public Fund Rates, and Iowa Code Chapter 74A 90-179 day Public Fund Rates.

Performance Objective: To provide the highest level of current income from investment in a portfolio of U.S. government and agency securities, certificates of deposit in Iowa financial institutions, and other authorized securities collateralized by U.S. government and agency securities as is consistent with, in order of priority, preservation of principal and provision of necessary liquidity.

Investment Adviser:

Investors Management Group

Management Fees:

Sliding scale from twelve basis points (0.12%) to seven basis points (0.07%)

Total Expense Ratio:

Sliding scale from forty-one and one-half basis points (0.415%) to fifty-one and one-half basis points (0.515%)

DIRECT GOVERNMENT OBLIGATION (DGO) FUND FACTS

as of June 30, 2004

Investment Strategy/Goals: To provide a safe, liquid, effective investment alternative for the bond proceeds, operating and reserve funds for Iowa’s municipalities, counties, municipal utilities and other eligible public agencies that are limited to investment in only direct obligations of the U.S. government by jointly investing participant funds into a professionally managed portfolio of short-term, eligible marketable securities.

Date of Inception: September 1, 1988

Total Net Assets: $38 million

Benchmarks: iMoneyNet U.S. Treasury & Repo Money Fund Report Index, Iowa Code Chapter 74A 32-89 day Public Fund Rates, and Iowa Code Chapter 74A 90-179 day Public Fund Rates.

Performance Objective: To provide the highest level of income from investment in a portfolio of U.S. government securities as is consistent with, in order of priority, preservation of principal and provision of necessary liquidity.

Investment Adviser: Investors Management Group

Management Fees: Sliding scale from twelve basis points (0.12%) to seven basis points (0.07%)