Exhibit 13

2007 ANNUAL REPORT

Meta means change.

Change is not merely necessary to life — it is life.

ALVIN TOFFLER

LET’S FACE IT. LIFE CHANGES. AND SO DOES BUSINESS. THAT IS WHY META FINANCIAL GROUP IS DEDICATED TO CHANGE. CHANGING THE WAY PEOPLE PAY. CHANGING THE WAY BUSINESSES MANAGE MONEY. CHANGING THE WAY PEOPLE BANK. CHANGE FOR THE BETTER. THAT IS WHAT META IS ABOUT.

COMPANY STRUCTURE

COMPANY PROFILE

Headquartered in Storm Lake, Iowa, Meta Financial Group, Inc. (Meta) (trading symbol: “CASH”) is a $686 million bank holding company for MetaBank, MetaBank West Central, and Meta Trust Company. Its primary businesses are providing payment solutions nationally through its Meta Payment Systems (MPS) division and marketing deposits, loans and other financial services and products to meet the needs of its commercial, agricultural and retail customers in its bank markets. Meta shares are traded on the NASDAQ Global Market.SM

MPS is a recognized leader in the prepaid card industry and provides innovative payment solutions delivered nationally in collaboration with market-leading partners. MPS focuses on offering specific product solutions in the following areas: (i) prepaid cards, (ii) credit cards and lending solutions, and (iii) ATM sponsorship.

Meta operates its bank branches under a super-community banking philosophy with an emphasis on business banking that allows the Company to grow while maintaining its community bank roots, with local decision making and customer service. Administrative functions, transparent to the customer, are centralized to enhance the banks’ operational efficiencies and to improve customer service capabilities. MetaBank is a federally-chartered savings bank with four market areas: Brookings, Central Iowa, Northwest Iowa and Sioux Empire. MetaBank West Central is a state-chartered commercial bank located in West Central Iowa. Seventeen bank offices and two MPS/administrative offices support customers in Iowa, Nebraska, South Dakota and Tennessee and MPS clients across the country. Meta Trust provides professional trust services.

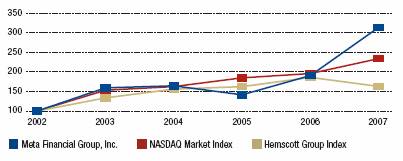

COMPARISON OF CUMULATIVE TOTAL RETURN OF CASH, INDUSTRY AND BROAD MARKET INDEXES

Banks are Members FDIC and Equal Housing Lenders. The Company and its subsidiaries exceed regulatory capital requirements.

CONTENTS | |

| |

Company Structure & Profile | i |

| |

Letter to Shareholders | ii-iii |

| |

Financials | 1-34 |

| |

Directors & Senior Officers | 35 |

| |

Investor Information | 36 |

| |

Locations | 37 |

i

To Fellow Shareholders

L TO R: J. TYLER HAAHR, JAMES S. HAAHR

ON BEHALF OF OUR LEADERSHIP TEAM AND META ASSOCIATES, WE ARE PLEASED TO SHARE ANOTHER YEAR OF PROGRESSION WITH YOU. META CONTINUES TO POSITION ITSELF AS A COMPANY THAT EMBRACES CHANGE—CHANGING THE WAY PEOPLE PAY, CHANGING THE WAY BUSINESSES MANAGE MONEY, AND CHANGING THE WAY PEOPLE BANK.

As a principal member of MasterCard,® Visa,® Discover® and the regional debit networks, Meta Payment Systems (MPS) expands the Company’s opportunity and reach in the growing payments industry. It serves banks, card processors, and third-party marketing companies nationwide. MPS focuses on offering specific product solutions in the following areas: (i) prepaid cards, (ii) credit cards and lending solutions, and (iii) ATM sponsorship.

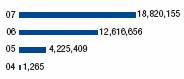

Annual consumer spending on prepaid cards is estimated to reach $260 billion by 2009.(1) As of fiscal year end, MPS supported clients by implementing more than 1,110 prepaid programs and issuing 35.7 million cards, up 94 percent and 49 percent from 2006 year end respectively. The success of its prepaid sponsorship program and launch of its new SimplexusTM prepaid card product suite has contributed to exponential growth since its inception in 2004. Additionally, MPS’s ATM Services unit now sponsors more than 44 percent of the white-label ATMs placed nationwide, up from 28 percent a year ago.

MPS FISCAL YEAR

CARDS ISSUED

MPS’s focus on leadership, innovation and change is evident by several noteworthy accomplishments in 2007:

· Founding member of the National Branded Prepaid Card Association (NBPCA) Board of Directors;

· Successful launch of SimplexusTM product suite;

· Market leader in ATM sponsorship;

· Rebate card programs issued for several Fortune 500 companies; and

· Successful pilot of contactless payment devices with MasterCard® and Visa.®

Meta understands the responsibility associated with being a recognized leader in the prepaid card industry. It respects its collaboration with market-leading partners in its efforts to deliver innovative payment solutions to improve the lives of its customers. Meta is bringing money to life.

FINANCIAL HIGHLIGHTS(2)

While Meta made strides in 2007, the Company’s constant emphasis on long-term, profitable growth over short-term gains is becoming increasingly important as Meta prepares for its next opportunities—in both payment solutions and traditional banking.

Meta reported net income of $1.2 million or $0.45 per diluted share for fiscal year 2007. This compares to net income of $3.7 million or $1.46 per diluted share for fiscal year 2006. Earnings for 2007 were impacted by a large provision for loan losses related primarily to an impairment on a commercial loan relationship offset, in part, by a gain on the sale of four Northwest Iowa bank branches. 2006 earnings were impacted by non-recurring fee income associated with a portfolio of purchased prepaid debit cards.

An important highlight for Meta is its growth in total revenues. Total revenue for fiscal year 2007 rose to a record $62.1 million, an increase of $7.8 million or 14 percent over fiscal year 2006. Total revenue from MPS, a separate reportable business unit of the

Company, was $26.3 million for fiscal 2007, up 90 percent or $12.5 million from fiscal 2006.

Net interest income for fiscal year 2007 was $21.7 million, up $2.1 million from fiscal year 2006. The 11 percent increase was driven by a higher net interest margin offset, in part, by a smaller earning asset base. Net interest margin continues its widening trend with a spread of 3.38 percent in fiscal year 2007, compared to 2.85 percent in 2006.

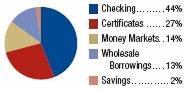

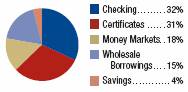

Contributing directly to Meta’s revenue and net interest income growth is a deliberate shift in its funding mix. Meta is replacing higher cost certificates of deposit, public funds deposits, and wholesale borrowings with low- and no-cost deposits that include checking, money market accounts and prepaid card product deposits.

FUNDING SOURCES 2007

FUNDING SOURCES 2006

ii

Total low- and no-cost deposits rose 15 percent during fiscal year 2007 to $356 million at September 30, 2007.(3) As of September 30, 2007, these deposits represented 58 percent of total funding liabilities, compared to 50 percent one year earlier. A significant portion of this growth came from deposits generated by MPS. The Company used these deposit increases to pay down wholesale borrowing sources. Total wholesale borrowings at September 30, 2007 were $78.5 million, down 36 percent from $114.8 million at September 30, 2006.

LOW-COST

DEPOSIT BALANCES(3)

In millions

Low-cost deposits include checking and money market accounts.

Meta’s non-interest income also exhibited dramatic growth in fiscal year 2007, reaching a record $22.1 million. The $8.3 million or 61 percent increase from fiscal year 2006 can be attributed, in part, to MPS card fee income growth of $4.6 million, or 42 percent, over 2006 and increases in loan fee and deposit fee income totaling $150,000.

On the lending side, total loans, net of allowance for loan losses, fell $23.4 million or 6 percent during fiscal year 2007. This includes $2.2 million related to the branch sales. However, during the fourth quarter of fiscal 2007 there was an increase of $1.9 million. The Company believes

the pay downs and payoffs primarily in its originated and purchased commercial operating and commercial real estate portfolios are driven, in part, by a decrease in overall demand for credit and increased competition from secondary market investors.

Meta’s credit quality continues to exhibit positive trends. Non-performing loans at September 30, 2007 were 0.47 percent of total loans compared to 1.41 percent one year earlier. The Company’s underlying credit trends are very strong, and the Company continues to foster a conservative credit culture while it reduces its classified and nonperforming assets. Meta does not have any direct exposure to subprime mortgage loans.

Non-interest expense grew $10.2 million or 37 percent during fiscal 2007. The primary contributors, compensation and card processing expenses, rose as a result of MPS’s significant growth and Meta’s proactive efforts to support future growth and product development.

Meta has hired executive level management, client relations, compliance and operations support staff within MPS, as well as software developers, IT support staff, and other administrative support within the Company to secure the necessary infrastructure needed to support growth in the Company’s fast-growing MPS and its larger bank markets. For example, Meta’s information technology staff has grown from five to 35 full-time employees within two years in order to maintain Meta’s systems and support research and development initiatives.

Additionally, the Company invested in card processing settlement functions for value loading, card sales and other items to support new product development and anticipated growth of existing products. Meta’s occupancy and equipment expenses also rose during fiscal year 2007. The Company added administrative office space for MPS in Sioux Falls, SD and Omaha, NE and invested in computer hardware and software. Meta believes these investments will actively support growth at MPS.

Bank branch structure is also changing in the Company. In November 2007, Meta announced an agreement to sell its MetaBank West Central subsidiary with its three offices located in Stuart, Casey and Menlo, Iowa. The transaction will involve the sale of MetaBank West Central stock for approximately $8.3 million, which is dependent on the satisfaction of routine contractual terms by the date of the sale. The sale is anticipated to close on or before March 30, 2008.

Meta also sold four branches in Northwest Iowa for a $3.33 million gain recorded during the third quarter of fiscal 2007. The premium received from the sale of Meta’s seven branches has been and will be utilized for MPS and traditional banking expansion in markets with greater growth potential. MetaBank opened a new administrative office and retail branch in downtown Des Moines, Iowa this year and opened six new bank offices in Sioux Falls, South Dakota and the Des Moines metro area within the last five years. The Company believes that additional offices in higher-growth markets will lead to further loan and deposit growth. Its ATM network, online offerings and other technological services also support the distribution of Meta services.

CHANGE FOR THE FUTURE

The Company is committed to profitable growth for its customers, employees and shareholders. Meta associates are working to execute three key initiatives that we believe will enhance long-term performance and earnings:

· Actively pursue MPS growth,

· Build commercial banking business, and

· Manage infrastructure and risk to support growth.

Thank you for your interest and investment in our company

JAMES S. HAAHR, Chairman of the Board

(1) Mitchell, Richard. “Meeting the demand with rosy forecasts ahead, payment processors are tuned to servicing prepaid products,” www.intelecard.com, May 7, 2006.

(2) Information presented herein is qualified in its entirety by the Company’s audited financial statements presented elsewhere herein.

(3) 2007 low-cost deposit numbers exclude deposits from branches sold during the year and those related to the pending sale of MetaBank West Central.

iii

FINANCIAL HIGHLIGHTS

(Dollars in Thousands except Per Share Data) | | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

| | | | (Restated) | | | | | | | |

AT SEPTEMBER 30 | | | | | | | | | | | |

Total assets | | $ | 686,080 | | $ | 740,921 | | $ | 775,839 | | $ | 780,799 | | $ | 772,285 | |

Total loans, net | | 355,612 | | 368,959 | | 415,568 | | 381,406 | | 332,062 | |

Total deposits | | 522,978 | | 538,169 | | 510,258 | | 433,928 | | 408,558 | |

Shareholder’s equity | | 48,098 | | 45,099 | | 42,959 | | 47,274 | | 43,031 | |

Book value per common share | | $ | 18.57 | | $ | 17.79 | | $ | 17.16 | | $ | 18.98 | | $ | 17.25 | |

Total equity to assets | | 7.01 | % | 6.09 | % | 5.54 | % | 6.05 | % | 5.57 | % |

| | | | | | | | | | | |

FOR THE FISCAL YEAR | | | | | | | | | | | |

Total interest income and non-interest income-continuing operations | | $ | 59,632 | | $ | 51,607 | | $ | 41,870 | | $ | 36,729 | | $ | 35,543 | |

Net interest income-continuing operations | | 20,807 | | 18,501 | | 18,063 | | 16,539 | | 14,647 | |

Income(loss)from continuing operations, net of tax | | 1,312 | | 3,379 | | (652 | ) | 3,662 | | 3,091 | |

Income (loss) from discontinued operations, net of tax | | (141 | ) | 309 | | (272 | ) | 325 | | 306 | |

Net income(loss) | | 1,171 | | 3,688 | | (924 | ) | 3,987 | | 3,397 | |

| | | | | | | | | | | |

Diluted earnings (loss) per share: | | | | | | | | | | | |

Income (loss) from continuing operations | | $ | 0.50 | | $ | 1.34 | | $ | (0.27 | ) | $ | 1.44 | | $ | 1.24 | |

Income (loss) from discontinued operations | | (0.05 | ) | 0.12 | | (0.11 | ) | 0.13 | | 0.12 | |

Net income (loss) | | 0.45 | | 1.46 | | (0.38 | ) | 1.57 | | 1.36 | |

| | | | | | | | | | | |

Return on average assets | | 0.17 | % | 0.49 | % | -0.12 | % | 0.51 | % | 0.47 | % |

Return on average assets-continuing operations | | 0.19 | % | 0.45 | % | -0.08 | % | 0.47 | % | 0.43 | % |

Return on average equity | | 2.69 | % | 8.55 | % | -2.04 | % | 8.69 | % | 7.57 | % |

Return on average equity-continuing operations | | 3.01 | % | 7.83 | % | -1.44 | % | 7.98 | % | 6.89 | % |

Net yield on interest-earning assets-continuing operations | | 3.38 | % | 2.85 | % | 2.59 | % | 2.44 | % | 2.35 | % |

TOTAL ASSETS | | TOTAL LOANS, NET | | TOTAL DEPOSITS | | TOTAL REVENUES | | TOTAL NET INCOME |

In thousands | | In thousands | | In thousands | | In thousands | | n thousands |

| | | | | | | | |

| |

| |

| |

| |

|

FINANCIAL CONTENTS | | |

| | |

Financial Highlights | | 1 |

Selected Consolidated Financial Information | | 2 |

Management’s Discussion and Analysis | | 3 |

Report of Independent Registered Public Accounting Firm | | 11 |

Consolidated Statements of Financial Condition at September 30, 2007 and 2006 | | 12 |

Consolidated Statements of Operations for the Years Ended September 30, 2007, 2006 and 2005 | | 13 |

Consolidated Statements of Comprehensive Income (Loss) for the Years Ended September 30, 2007, 2006 and 2005 | | 14 |

Consolidated Statements of Changes in Shareholders’ Equity for the Years Ended September 30, 2007, 2006 and 2005 | | 14 |

Consolidated Statements of Cash Flows for the Years Ended September 30, 2007, 2006 and 2005. | | 15 |

Notes to Consolidated Financial Statements | | 16 |

1

Meta Financial Group, Inc. and Subsidiaries

SELECTED CONSOLIDATED FINANCIAL INFORMATION

SEPTEMBER 30, | | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

| | | | (Restated) | | | | | | | |

SELECTED FINANCIAL CONDITION DATA

(In Thousands) | | | | | | | | | | | |

| | | | | | | | | | | |

Total assets | | $ | 686,080 | | $ | 740,921 | | $ | 775,839 | | $ | 780,799 | | $ | 772,285 | |

Loans receivable, net | | 355,612 | | 368,959 | | 415,568 | | 381,406 | | 332,062 | |

Securities available for sale | | 158,701 | | 172,444 | | 213,245 | | 290,186 | | 324,915 | |

Goodwill | | 1,508 | | 1,508 | | 1,508 | | 1,508 | | 1,508 | |

Deposits | | 522,978 | | 538,169 | | 510,258 | | 433,928 | | 408,558 | |

Total borrowings | | 78,534 | | 114,789 | | 176,857 | | 241,354 | | 258,082 | |

Shareholders’ equity | | 48,098 | | 45,099 | | 42,959 | | 47,274 | | 43,031 | |

| | | | | | | | | | | | | | | | |

YEAR ENDED SEPTEMBER 30, | | | | | | | | | | | |

| | | | | | | | | | | |

SELECTED OPERATIONS DATA | | | | | | | | | | | |

(In Thousands, Except Per Share Data) | | | | | | | | | | | |

| | | | | | | | | | | |

Total interest income | | $ | 37,774 | | 38,112 | | $ | 38,368 | | $ | 33,433 | | $ | 32,390 | |

Total interest expense | | 16,967 | | 19,611 | | 20,305 | | 16,894 | | 17,743 | |

Net interest income | | 20,807 | | 18,501 | | 18,063 | | 16,539 | | 14,647 | |

Provision for loan losses | | 3,168 | | 311 | | 4,713 | | 473 | | 381 | |

Net interest income after provision for loan losses | | 17,639 | | 18,190 | | 13,350 | | 16,066 | | 14,266 | |

Total non-interest income | | 21,858 | | 13,495 | | 3,502 | | 3,296 | | 3,153 | |

Total non-interest expense | | 36,958 | | 26,640 | | 17,995 | | 13,797 | | 12,778 | |

Income (loss) from continuing operations before income tax expense (benefit) | | 2,539 | | 5,045 | | (1,143 | ) | 5,565 | | 4,641 | |

Income tax expense (benefit) | | 1,227 | | 1,666 | | (491 | ) | 1,903 | | 1,550 | |

Income (loss) from continuing operations | | 1,312 | | 3,379 | | (652 | ) | 3,662 | | 3,091 | |

Income (loss) from discontinued operations, net of tax | | (141 | ) | 309 | | (272 | ) | 325 | | 306 | |

Net income (loss) | | 1,171 | | 3,688 | | (924 | ) | 3,987 | | 3,397 | |

| | | | | | | | | | | | | | | |

Basic earnings (loss) per common share: | | | | | | | | | | | |

Income (loss) from continuing operations | | $ | 0.52 | | $ | 1.36 | | $ | (0.27 | ) | $ | 1.48 | | $ | 1.25 | |

Income (loss) from discontinued operations | | (0.06 | ) | 0.12 | | (0.11 | ) | 0.13 | | 0.12 | |

Net income (loss) | | $ | 0.46 | | $ | 1.48 | | $ | (0.38 | ) | $ | 1.61 | | $ | 1.37 | |

| | | | | | | | | | | |

Diluted earnings (loss) per common share: | | | | | | | | | | | |

Income (loss) from continuing operations | | $ | 0.50 | | $ | 1.34 | | $ | (0.27 | ) | $ | 1.44 | | $ | 1.23 | |

Income (loss) from discontinued operations | | (0.05 | ) | 0.12 | | (0.11 | ) | 0.13 | | 0.12 | |

Net income (loss) | | $ | 0.45 | | $ | 1.46 | | $ | (0.38 | ) | $ | 1.57 | | $ | 1.36 | |

YEAR ENDED SEPTEMBER 30, | | | | | | | | | | | |

| | | | | | | | | | | |

SELECTED FINANCIAL RATIOS AND OTHER DATA PERFORMANCE RATIOS | | | | | | | | | | | |

Return on average assets | | 0.17 | % | 0.49 | % | -0.12 | % | 0.51 | % | 0.47 | % |

Return on average assets-continuing operations | | 0.19 | % | 0.45 | % | -0.08 | % | 0.47 | % | 0.43 | % |

Return on average equity | | 2.69 | % | 8.55 | % | -2.04 | % | 8.69 | % | 7.57 | % |

Return on average equity-continuing operations | | 3.01 | % | 7.83 | % | -1.44 | % | 7.98 | % | 6.89 | % |

Net interest margin-continuing operations | | 3.38 | % | 2.85 | % | 2.59 | % | 2.44 | % | 2.35 | % |

Operating expense to average assets-continuing operations | | 5.26 | % | 3.55 | % | 2.29 | % | 1.78 | % | 1.78 | % |

| | | | | | | | | | | |

QUALITY RATIOS—CONTINUING OPERATIONS | | | | | | | | | | | |

Non-performing assets to total assets at end of year | | 0.38 | % | 0.72 | % | 0.92 | % | 0.09 | % | 0.27 | % |

Allowance for loan losses to non-performing loans | | 196 | % | 121 | % | 280 | % | 706 | % | 475 | % |

| | | | | | | | | | | |

CAPITAL RATIOS | | | | | | | | | | | |

Shareholders’ equity to total assets at end of period | | 7.01 | % | 6.09 | % | 5.54 | % | 6.05 | % | 5.57 | % |

Average shareholders’ equity to average assets | | 6.20 | % | 5.76 | % | 5.77 | % | 5.91 | % | 6.25 | % |

| | | | | | | | | | | |

OTHER DATA | | | | | | | | | | | |

Book value per common share outstanding | | $ | 18.57 | | $ | 17.79 | | $ | 17.16 | | $ | 18.98 | | $ | 17.25 | |

Dividends declared per share | | 0.52 | | 0.52 | | 0.52 | | 0.52 | | 0.52 | |

Number of full-service offices | | 17 | | 19 | | 17 | | 16 | | 16 | |

| | | | | | | | | | | | | | | | |

2

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

MANAGEMENT’S DISCUSSION AND ANALYSIS

GENERAL

Meta Financial Group, Inc.® (the “Company”) is a bank holding company whose primary subsidiaries are MetaBank (the “Bank”) and MetaBank West Central (“MetaBank WC”). The Company focuses on two core businesses, its regional retail banking business and a national payments business, conducted through its Meta Payment Systems® (“MPS”) division. The Company’s retail bank business is focused on establishing and maintaining long-term relationships with customers, and is committed to serving the financial service needs of the communities in its market area. The retail bank’s primary market area includes the following counties: Adair, Buena Vista, Dallas, Guthrie, and Polk located in central and northwestern Iowa, and Brookings, Lincoln, and Minnehaha located in east central South Dakota. The traditional bank segment attracts retail deposits from the general public and uses those deposits, together with other borrowed funds, to originate and purchase residential and commercial mortgage loans, and to originate consumer, agricultural and other commercial loans.

MPS, a division of the Bank, is an industry leader in the issuance of prepaid debit cards and is also a provider of a wide range of payment-related products and services, including prepaid debit cards, ATMs, credit cards and rebate cards. MPS pursues a strategy of working with industry-leading companies in a variety of industries to help them introduce new payment products to their customers. In addition, MPS partners with emerging companies to develop and introduce new payment products. MPS earns revenues from fees as well as being a significant provider of low- and no-cost demand deposits.

OVERVIEW OF CORPORATE DEVELOPMENTS

The Company continues to experience significant growth in its MPS division and is investing for further growth in this business unit. MPS continued to exhibit rapid growth during fiscal year 2007. On a business segment basis, its revenues (interest income plus non-interest income) grew by 58% over the previous year and now comprise 44% of the Company’s total revenue from continuing operations compared to 32% in the prior year. The division was created in May 2004 to take advantage of opportunities in the growing area of prepaid debit cards, ATM sponsorship, and other payment products and services. MPS is now recognized as an industry leader in a number of different areas within the payment systems industry including prepaid debit cards and ATMs.

The Bank continues to emphasize expansion in the growing metropolitan areas of Sioux Falls, South Dakota and Des Moines, Iowa. The Company focuses primarily on establishing lending and deposit relationships with commercial businesses and commercial real estate developers in these communities. In March 2007, the Company also opened an administrative support office in Omaha, Nebraska. During the third quarter of fiscal 2007, the Company divested four of its branches in rural Northwest Iowa. The Company also has signed a definitive agreement to sell MetaBank WC, which includes three branches in rural West-Central Iowa, with an expectation that the transaction will close in the second quarter of fiscal 2008. After the transaction closes the Company will be a unitary thrift holding company, subject to the jurisdiction of the Office of Thrift Supervision (“OTS”). These transactions allow the Company to increase its focus on higher growth markets and business lines. The Company now operates 17 branches: in Brookings (1) and Sioux Falls (4), South Dakota, in Des Moines (6), Northwest (2), and West-Central (3), Iowa, as well as a non-retail service branch in Memphis, Tennessee.

The Company discovered in September 2007 that maintenance fees charged to and collected from holders of prepaid gift cards, which were issued through the Company’s network of agent financial institutions, were not recognized as income in the appropriate periods. The impact to income from continuing operations before income tax expense for the fiscal year ended September 30, 2006 amounted to $322,000.

In addition, during the quarter ended December 31, 2006, the Company determined that a material impairment of its assets related to a certain loan had occurred and recorded an additional $690,000 provision for loan losses. The Company was subsequently informed by its independent accountants that, as a result of their consultation with their regulatory authorities, the additional provision should have been recorded in the quarter ended September 30, 2006 instead of the quarter ended December 31, 2006.

As a result of the above, the Company has restated its financial statements for the year ended September 30, 2006 to reflect an additional $322,000 of card fee revenue, an additional provision for loan losses of $690,000 and additional income tax benefit of $135,000, resulting in a decrease to net income of $233,000. The statement of financial condition for the year ending September 30, 2006 reflects a decrease in net loans of $690,000, a decrease to deposits of $322,000, a decrease to accrued expenses of $135,000, and a decrease to retained earnings of $233,000.

In November 2007, the Company also amended its Quarterly Reports on Form 10-Q for the quarterly periods ended December 31, 2006, March 31, 2007, and June 30, 2007 for the above restatements. Net income, as restated for the three months ended December 31, 2006, increased $550,000 due to additional prepaid card fee income of $178,000 and reduction in the provision for loan losses of $690,000. Net income, as restated for the three months ended March 31, 2007 and June 30, 2007, increased $132,000 and $152,000, respectively, due to additional prepaid card fee income.

The Company’s stock trades on the NASDAQ Global Market under the symbol “CASH.”

FINANCIAL CONDITION

The following discussion of the Company’s consolidated financial condition should be read in conjunction with the Selected Consolidated Financial Information and Consolidated Financial Statements and the related notes included in this Annual Report.

The Company’s total assets at September 30, 2007 were $686.1 million, a decrease of $54.8 million, or 7.4%, from $740.9 million at September 30, 2006. The decrease in assets of $54.8 million resulted primarily from decreases in the Company’s cash, securities, and loan portfolios.

Total cash and cash equivalents and federal funds sold were $86.3 million at September 30, 2007, a decrease of $21.2 million, or 19.7%, from $107.5 million at September 30, 2006. The decrease was primarily the result of the Company’s sale of four branches in northwest Iowa. Cash and short term investments were used to fund the assumption of deposit liabilities by the acquiring institutions.

In general, the Company maintains its cash investments in interest-bearing overnight deposits with various correspondent banks. Federal funds sold deposits are maintained at various large commercial banks.

The Company’s portfolio of securities purchased under agreements to resell and available for sale decreased $5.9 million, or 100%, to none at September 30, 2007. The Company’s portfolio of investment securities available for sale consists primarily of mortgage-backed securities, most with balloon maturities, which have relatively short expected average lives and limited maturity extension risk. During fiscal year 2007, the Company purchased securities for its available for sale portfolio totaling $13.2 million and sold securities available for sale in the amount of $1.1 million. See Note 5 to the Notes to Consolidated Financial Statements.

The Company’s portfolio of net loans receivable decreased by $13.4 million, or 3.6%, to $355.6 million at September 30, 2007 from $369.0 million at September 30, 2006. The decrease was mainly the result of pay offs and pay downs in the Company’s purchased loan participation portfolio, which is concentrated in commercial real estate and commercial operating credits. The Company experienced slight growth in its agricultural real estate and agricultural operating portfolios. See Note 6 to the Notes to Consolidated Financial Statements.

The Company owns stock in the Federal Home Loan Bank (“FHLB”) of Des Moines as well as in the Federal Reserve Bank due to its membership and participation in these banking systems. The Company’s investment in such stock decreased $1.1 million, or 20.5%, to $4.0 million at September 30, 2007 from $5.1 million at September 30, 2006. The decrease was due to a decrease in the level of borrowings from the FHLB, which require a calculated level of stock investment based on a formula determined by the FHLB.

Total deposits decreased by $15.2 million, or 2.8%, to $523.0 million at September 30, 2007 from $538.2 million at September 30, 2006. The majority of this net decrease was related to the sale of four branches in northwest Iowa. Additionally, however, the Company’s deposit mix shifted away from higher costing certificates of deposit and money market deposits toward low- and no-cost checking deposits. Most of the increase in checking deposits was the result of prepaid card deposit growth at the Bank’s MPS

3

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

division. Total checking deposits increased by $64.0 million, or 30.4%, to $274.7 million at September 30, 2007 from $210.7 million at September 30, 2006. Total savings and certificates of deposit declined $61.8 million, or 27.0%, to $167.0 million at September 30, 2007 from $228.8 million at September 30, 2006. The decrease in savings and certificates resulted primarily from the sale of four branches and runoff of higher costing public funds deposits. Money market account balances also decreased during fiscal year 2007, decreasing $17.4 million, or 17.6%, to $81.3 million at September 30, 2007 from $98.7 million at September 30, 2006. Money market deposits decreased primarily due to the sale of branches and fluctuations in several large accounts.

The Company’s wholesale borrowings portfolio decreased $36.3 million, or 31.6%, to $78.5 million at September 30, 2007 from $114.8 million at September 30, 2006. The Company continues to de-emphasize these high cost funding sources in an effort to decrease overall liability costs and to de-lever the Company’s balance sheet. See Notes 10, 11, and 12 to the Notes to Consolidated Financial Statements.

Shareholders’ equity increased $3.0 million, or 6.6%, to $48.1 million at September 30, 2007 from $45.1 million at September 30, 2006. The increase was primarily the result of a favorable change in the accumulated other comprehensive loss on the Company’s securities available for sale portfolio and by the reported fiscal 2007 net income (see “Results of Operations” below) offset by the payment of dividends on common stock. At September 30, 2007, the Company and both of its banking subsidiaries, MetaBank and MetaBankWC, continue to meet regulatory requirements for classification as well capitalized institutions. See Note 16 to the Notes to Consolidated Financial Statements.

RESULTS OF OPERATIONS

The following discussion of the Company’s Results of Operations should be read in conjunction with the Selected Consolidated Financial Information and Consolidated Financial Statements and the related notes included in this Annual Report.

Of increasing importance, the Company’s Results of Operations are dependent on net interest income, non-interest income, non-interest expense, and income tax expense. Net interest income is the difference, or spread, between the average yield on interest earning assets and the average rate paid on interest-bearing liabilities. The interest rate spread is affected by regulatory, economic, and competitive factors that influence interest rates, loan demand, and deposit flows. The Company, like other financial institutions, is subject to interest rate risk to the extent that its interest-earning assets mature or reprice at different times, or on a different basis, than its interest-bearing liabilities.

The Company’s non-interest income is derived primarily from card and ATM fees attributable to MPS and fees charged on loans and transaction accounts. The Company’s fiscal year 2007 non-interest income was also impacted by a gain on sale of four branches in the amount of $3.3 million. This income is offset, in part, by expenses, such as compensation and occupancy expenses associated with additional personnel and office locations as well as card processing expenses attributable to MPS. To a lesser extent, non-interest income is derived from gains or losses on the sale of securities available for sale as well as the Company’s holdings of bank-owned life insurance. Additionally, non-interest income has been derived from the activities of Meta Trust Company® (“Meta Trust”), a wholly-owned subsidiary of Meta Financial Group, which provides a variety of professional trust services. Non-interest expense is also impacted by occupancy and equipment expenses and legal and consulting expenses.

COMPARISON OF OPERATING RESULTS FOR THE YEARS ENDED SEPTEMBER 30, 2007 AND SEPTEMBER 30, 2006

GENERAL

The Company’s income from continuing operations was $1.3 million, or $0.50 per diluted share, for the year ended September 30, 2007 compared to $3.4 million, or $1.34 per diluted share, for the year ended September 30, 2006. Net income was $1.2 million, or $0.45 per diluted share, for the year ended September 30, 2007 compared to $3.7 million, or $1.46 per diluted share, for the year ended September 30, 2006. Earnings in fiscal year 2007 were impacted by a large provision for loan losses related primarily to an impairment on a commercial loan relationship of $5.0 million related to fraud by the borrower and a gain on the sale of four branches in northwest Iowa of $3.3 million. Earnings in fiscal year 2006 were impacted by non-recurring fee income of $2.6 million associated with a portfolio of purchased prepaid debit cards.

NET INTEREST INCOME

Net interest income from continuing operations for the year ended September 30, 2007 increased by $2.3 million, or 12.5%, to $20.8 million from $18.5 million for the year ended September 30, 2006. The increase in net interest income reflects a higher net interest margin, offset in part by a smaller average earning asset base. Net interest margin increased 53 basis points to 3.38% in fiscal year 2007 from 2.85% in fiscal year 2006. The improvement resulted primarily from the shift in the Company’s funding mix attributable to growth in non-interest-bearing deposits and decreases in higher costing certificates, public funds deposits, and wholesale borrowings.

The Company’s average earning assets decreased $33.1 million, or 5.1%, to $616.3 million during fiscal year 2007 from $649.5 million during fiscal year 2006. The decrease is primarily the result of the decrease in the loan portfolio. The Company’s yield on earning assets rose 26 basis points to 6.13% during fiscal year 2007 from 5.87% during fiscal year 2006. The increase is the result primarily of increasing yields on the Company’s other investments.

The Company’s average total deposits and interest-bearing liabilities decreased $40.7 million, or 6.2%, to $616.7 million during fiscal year 2007 from $657.4 million during fiscal year 2006. The decrease resulted mainly from a decrease in the Company’s interest- bearing deposits and wholesale borrowings. Decreases in public funds deposits were more than offset by growth in non-interest bearing checking accounts. The Company’s cost of total deposits and interest-bearing liabilities decreased 23 basis points during fiscal year 2007 to 2.75% during fiscal year 2007 from 2.98% during fiscal year 2006. Despite an increasing interest rate environment in 2007, which drove the costs of certificates and money market deposits higher, the Company was able to limit the increase in its overall cost of funds by shifting its portfolio mix away from higher costing certificates, public funds deposits, and wholesale borrowings, into lower costing demand deposits.

PROVISION FOR LOAN LOSSES

In fiscal year 2007, the Company recorded a provision for loan losses of $3.2 million, compared to $311,000 for fiscal year 2006. The reduction in the provision in 2006 relates in part to the Company’s settlement agreement with one of several participants in an auto-dealership related lending relationship. Additionally, shrinkage in the Company’s loan portfolio during the year reduced the level of required loan loss allowances on the portfolio. The relatively large provision in fiscal year 2007 is the primary reason that net interest income after provision for loan losses decreased by $551,000, from $18.2 million in fiscal 2006 to $17.6 million in fiscal year 2007. For fiscal year 2007, the Company’s provision for loan losses of $3.2 million consisted of the impairment of a commercial lending relationship due to the fraud by the borrower partially offset by a decrease in loans, a decrease in impaired loans and a $500,000 recovery of a fidelity bond claim payment by the Company’s insurance carrier.

Management closely monitors economic developments both regionally and nationwide, and considers these factors when assessing the adequacy of its allowance for loan losses. While the Company has no direct exposure to sub-prime loans, management is concerned that recent developments in the sub-prime mortgage market may have a ripple effect on residential real estate prices. In addition, the potential for an economic slowdown and recent increase in energy prices may strain the financial condition of some borrowers. Management therefore believes that future losses in the residential portfolio may be somewhat higher than historical experience. Over the past six years, loss rates in the commercial and multi-family real estate market have remained moderate. Management recognizes that low charge-off rates over the past several years reflect the strong economic environment and are not indicative of likely losses over a full business cycle. This observation, as well as the aforementioned concerns regarding an economic slowdown, has led management to the conclusion that future losses in this portfolio may be somewhat higher than recent historical experience, excluding loan losses related to fraud by borrowers. On the other hand, current trends in agricultural

4

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

AVERAGE BALANCES, INTEREST RATES AND YIELDS

The following table presents, for the periods indicated, the total dollar amount of interest income from average interest-earning assets and the resulting yields, as well as the interest expense on average interest-bearing liabilities, expressed both in dollars and rates. No tax equivalent adjustments have been made. Non-accruing loans have been included in the table as loans carrying a zero yield. Balances related to discontinued operations have been reclassified to non-interest earning assets and non-interest bearing liabilities for all periods presented.

YEAR ENDED SEPTEMBER 30,

| | | | 2007 | | | | | | 2006 | | | | | | 2005 | | | |

| | | | | | | | | | | | | | | | | | | |

| | Average | | Interest | | | | Average | | Interest | | | | Average | | Interest | | | |

| | Outstanding | | Earned | | Yield | | Outstanding | | Earned | | Yield | | Outstanding | | Earned | | Yield | |

(Dollars in Thousands) | | Balance | | /Paid | | /Rate | | Balance | | /Paid | | /Rate | | Balance | | /Paid | | /Rate | |

INTEREST-EARNING ASSETS | | | | | | | | | | | | | | | | | | | |

Interest-earning assets: | | | | | | | | | | | | | | | | | | | |

Loans receivable | | $ | 354,465 | | $ | 25,584 | | 7.22 | % | $ | 390,002 | | $ | 27,948 | | 7.17 | % | $ | 409,783 | | $ | 28,103 | | 6.86 | % |

Mortgage-backed securities | | 135,007 | | 5,500 | | 4.07 | % | 163,032 | | 6,185 | | 3.79 | % | 239,514 | | 8,688 | | 3.63 | % |

Other investments | | 126,853 | | 6,690 | | 5.27 | % | 96,416 | | 3,979 | | 4.13 | % | 47,730 | | 1,577 | | 3.30 | % |

Total interest-earning assets | | 616,325 | | $ | 37,774 | | 6.1 3 | % | 649,450 | | $ | 38,112 | | 5.87 | % | 697,027 | | $ | 38,368 | | 5.50 | % |

Non-interest-earning assets | | 86,502 | | | | | | 99,960 | | | | | | 89 ,171 | | | | | |

Total assets | | $ | 702,827 | | | | | | $ | 749,410 | | | | | | $ | 786,198 | | | | | |

| | | | | | | | | | | | | | | | | | | |

Non-interest bearing deposits | | $ | 230,930 | | $ | –– | | 0.00 | % | $ | 147,520 | | $ | –– | | 0.00 | % | $ | 31,896 | | $ | –– | | 0.00 | % |

INTEREST-BEARING LIABILITIES | | | | | | | | | | | | | | | | | | | |

Interest-bearing checking | | $ | 22,004 | | $ | 538 | | 2.45 | % | $ | 21,852 | | $ | 789 | | 3.61 | % | $ | 54,154 | | $ | 872 | | 1.61 | % |

Savings | | 17,586 | | 471 | | 2.68 | % | 46,822 | | 1,388 | | 2.96 | % | 55,541 | | 1,306 | | 2.35 | % |

Money markets | | 67,087 | | 2,301 | | 3.43 | % | 83,486 | | 2,354 | | 2.82 | % | 50,269 | | 895 | | 1.78 | % |

Time deposits | | 183,505 | | 8,355 | | 4.55 | % | 215,815 | | 8,225 | | 3.81 | % | 268,198 | | 8,427 | | 3.14 | % |

FHLB advances | | 77,433 | | 4,091 | | 5.28 | % | 115,102 | | 7,237 | | 4.77 | % | 194,960 | | 7,530 | | 3.86 | % |

Other borrowings | | 18,172 | | 1,211 | | 6.66 | % | 26,846 | | 1,367 | | 5.09 | % | 31,802 | | 1,275 | | 4.01 | % |

Total interest-bearing liabilities | | 385,787 | | 16,967 | | 4.4 0 | % | 509,923 | | 19,611 | | 3.85 | % | 654,924 | | 20,305 | | 3.10 | % |

Total deposits and interest-bearing liabilities | | 616,717 | | $ | 16,967 | | 2.7 5 | % | 657,443 | | $ | 19,611 | | 2.98 | % | 686,820 | | $ | 20,305 | | 2.96 | % |

Other non-interest bearing liabilities | | 42,557 | | | | | | 48,831 | | | | | | 54,027 | | | | | |

Total liabilities | | 659,274 | | | | | | 706,274 | | | | | | 740,847 | | | | | |

Shareholders’ equity | | 43,553 | | | | | | 43,136 | | | | | | 45,351 | | | | | |

Total liabilities and shareholders’ equity | | $ | 702,827 | | | | | | $ | 749,410 | | | | | | $ | 786,198 | | | | | |

Net interest income and net interest rate spread including non-interest bearing deposits | | | | $ | 20,807 | | 3.38 | % | | | $ | 18,501 | | 2.89 | % | | | $ | 18,063 | | 2.54 | % |

Net interest margin | | | | | | 3.38 | % | | | | | 2.85 | % | | | | | 2.59 | % |

markets are very favorable. Higher commodity prices as well as higher yields have created positive economic conditions for most farmers. Nonetheless, management still expects that future losses in this portfolio, which have been very low, could be higher than recent historical experience. Management believes that the aforementioned possibility for a slowdown in economic growth during the next fiscal year may also negatively impact consumers’ repayment capacities. Additionally, a sizable portion of the Company’s consumer loan portfolio is secured by residential real estate, as discussed above, is an area to be closely monitored by management in view of its stated concerns.

Management believes that, based on a detailed review of the loan portfolio, historic loan losses, current economic conditions, the size of the loan portfolio, and other factors, the current level of the allowance for loan losses at September 30, 2007 reflects an adequate allowance against probable losses from the loan portfolio. Although the Company maintains its allowance for loan losses at a level that it considers to be adequate, investors and others are cautioned that there can be no assurance that future losses will not exceed estimated amounts, or that additional provisions for loan losses will not be required in future periods. In addition, the Company’s determination of the allowance for loan losses is subject to review by its regulatory agencies, which can require the establishment of additional general or specific allowances.

NON-INTEREST INCOME

Non-interest income increased by $8.4 million, or 62.0%, to $21.9 million for the fiscal year 2007 from $13.5 million for fiscal year 2006. Non-interest income in fiscal year 2007 was impacted by a gain on the sale of four branches in northwest Iowa of $3.3 million. Non-interest income in the 2006 period was impacted by non-recurring pre-tax fee income of $2.6 million related to a purchased portfolio of prepaid debit cards. Adjusting for these non-recurring items, non-interest income for fiscal year 2007 rose $7.6 million, or 69.4%, over the same period in the prior fiscal year primarily due to an increase in card fee income. The majority of this growth is related to higher fee income earned on prepaid debit cards and other products and services offered by MPS.

Management performed an evaluation of whether the sale of the branches constituted discontinued operations, and concluded that the operations and cash flows of the branches sold were not discontinued operations. Revenue and expenses of the entity, including the gain on sale, are, therefore, included in the appropriate income statement line items for all periods presented.

NON-INTEREST EXPENSE

Non-interest expense increased by $10.4 million, or 38.7%, to $37.0 million for fiscal year 2007 from $26.6 million for fiscal year 2006. Several factors contributed to this increase. Compensation expense rose $5.4 million during the year, from $12.8 million in fiscal year 2006 to $18.2 million in fiscal year 2007. The increase represents the addition of executive level management, client relations, compliance and operations support staff within MPS, as well as software developers, Information Technology (“IT”) support staff, and other administrative support within the Company. Many of the new employees at MPS and in IT will be focused on developing new product lines and increasing market penetration of our payments systems products and services.

Costs associated with the processing of card-related products at MPS also increased during fiscal year 2007. Card processing expense rose $3.4 million from $3.0 million in fiscal year 2006 to $6.4 million in fiscal year 2007 as a result of the significant growth

in

5

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

RATE/VOLUME ANALYSIS

The following schedule presents the dollar amount of changes in interest income and interest expense for major components of interest-earning assets and interest-bearing liabilities. It distinguishes between the increase related to higher outstanding balances and that due to the levels and volatility of interest rates. For each category of interest-earning assets and interest-bearing liabilities, information is provided on changes attributable to (i) changes in volume (i.e. changes in volume multiplied by old rate) and (ii) changes in rate (i.e. changes in rate multiplied by old volume). For purposes of this table, changes attributable to both rate and volume that cannot be segregated have been allocated proportionately to the change due to volume and the change due to rate.

YEAR ENDED SEPTEMBER 30,

| | 2007 VS. 2006 | | 2006 VS. 2005 | |

| | Increase | | Increase | | Total | | Increase | | Increase | | Total | |

| | (Decrease) | | (Decrease) | | Increase | | (Decrease) | | (Decrease) | | Increase | |

(in Thousands) | | Due to Volume | | Due to Rate | | (Decrease) | | Due to Volume | | Due to Rate | | (Decrease) | |

| | | | | | | | | | | | | |

INTEREST-EARNING ASSETS | | | | | | | | | | | | | |

Loans Receivable | | $ | (2,567 | ) | $ | 203 | | $ | (2,364 | ) | $ | (2,236 | ) | $ | 2,081 | | $ | (155 | ) |

Mortgage-backed securities | | (1,203 | ) | 518 | | (685 | ) | (2,921 | ) | 418 | | (2,503 | ) |

Other investments | | 1,444 | | 1,267 | | 2,711 | | 1,930 | | 472 | | 2,402 | |

Total interest - earning asset s | | $ | (2,326 | ) | $ | 1,988 | | $ | (338 | ) | $ | (3,227 | ) | $ | 2,971 | | (256 | ) |

| | | | | | | | | | | | | |

INTEREST-BEARING LIABILITIES | | | | | | | | | | | | | |

Interest-bearing checking | | $ | 6 | | $ | (257 | ) | $ | (251 | ) | $ | 76 | | $ | (159 | ) | $ | (83 | ) |

Savings | | (794 | ) | (123 | ) | (917 | ) | (124 | ) | 206 | | 82 | |

Money markets | | 521 | | (574 | ) | (53 | ) | 775 | | 684 | | 1,459 | |

Time deposits | | (433 | ) | 563 | | 130 | | 2,239 | | (2,441 | ) | (202 | ) |

FHLB advances | | (2,086 | ) | 689 | | (1,397 | ) | (4,776 | ) | 2,734 | | (2,042 | ) |

Other borrowings | | (3,510 | ) | 3,354 | | (156 | ) | (125 | ) | 217 | | 92 | |

Total interest-bearing liabilities | | $ | (6,296 | ) | $ | 3,652 | | $ | (2,644 | ) | $ | (1,935 | ) | $ | 1,241 | | $ | (694 | ) |

| | | | | | | | | | | | | |

Net effect on net interest income | | $ | 3,970 | | $ | (1,664 | ) | $ | 2,306 | | $ | (1,292 | ) | $ | 1,730 | | $ | 438 | |

the division’s product lines. These expenses stem primarily from MPS’ Simplexus® prepaid card product and other prepaid card programs managed by MPS. Other card processing expense increases are attributable to settlement functions for value loading, card sales and anticipated growth of existing products. Management expects that these costs will continue to increase as MPS issues more cards; however, it is anticipated that overall costs will increase less than revenues associated with these cards.

The Company’s occupancy and equipment expense also rose during fiscal year 2007, driven primarily by the addition of administrative office space in Sioux Falls and Omaha, as well as investment in computer hardware and software, primarily to support growth at MPS. Occupancy and equipment expense for fiscal year 2007 was $4.0 million compared to $2.9 million in fiscal year 2006.

INCOME TAX EXPENSE

Income tax expense from continuing operations for fiscal year 2007 was $1.2 million, or an effective tax rate of 48.3%, compared to $1.7 million, or an effective tax rate of 33.0%, in fiscal year 2006. The change is due primarily to the decrease in net income before income tax expense. The Company’s recorded income tax expense was also impacted primarily by permanent differences between book and taxable income.

DISCONTINUED OPERATIONS

Income (loss) from discontinued operations was a loss of $141,000 for fiscal year 2007 compared to income of $309,000 for fiscal year 2006. The decrease was primarily related to an increase in provision for loan losses in the amount of $703,000 as compared to the prior fiscal year. See Note 3 to the Notes to Consolidated Financial Statements for further discussion on discontinued operations.

COMPARISON OF OPERATING RESULTS FOR THE YEARS ENDED SEPTEMBER 30, 2006 AND SEPTEMBER 30, 2005

GENERAL

The Company’s income from continuing operations was $3.4 million, or $1.34 per diluted share, for the year ended September 30, 2006, compared to a net loss of $652,000, or $0.27 per diluted share, for the year ended September 30, 2005. Net income was $3.7 million, or $1.46 per diluted share, for the year ended September 30, 2006 compared to a net loss of $924,000, or $0.38 per diluted share, for the year ended September 30, 2005. Earnings in fiscal year 2006 were primarily impacted by card fees and non-recurring fee income, partially offset by higher compensation, occupancy, legal and consulting, and card processing expenses. Earnings in fiscal year 2005 were impacted by the provision for loan loss.

NET INTEREST INCOME

Net interest income from continuing operations for the year ended September 30, 2006 increased by $438,000, or 2.4%, to $18.5 million from $18.1 million for the year ended September 30, 2005. The increase in net interest income reflects a higher net interest margin, offset in part by a smaller average earning asset base. Net interest margin increased 26 basis points to 2.85% in fiscal year 2006 from 2.59% in fiscal year 2005. The improvement resulted primarily from the shift in the Company’s funding mix attributable to growth in non-interest-bearing and money market deposits and decreases in higher costing certificates, public funds deposits, and wholesale borrowings.

The Company’s average earning assets decreased $47.5 million, or 6.8%, to $649.5 million during fiscal year 2006 from $697.0 million during fiscal year 2005. The decrease is primarily the result of a smaller portfolio of mortgage-backed securities and loans. The Company’s yield on earning assets rose 37 basis points to 5.87% during fiscal year 2006 from 5.50% during fiscal year 2005. The increase is the result primarily of increasing yields on the Company’s adjustable rate loan portfolio due to an increasing interest rate environment during 2006.

The Company’s average total deposits and interest-bearing liabilities decreased $29.4 million, or 4.3%, to $657.4 million during fiscal year 2006 from $686.8 million during fiscal year 2005. The decrease resulted mainly from a decrease in the Company’s portfolio of advances from the FHLB and other wholesale borrowings. Decreases in public funds deposits were more than offset by growth in non-interest bearing checking accounts. The Company’s cost of total deposits and interest-bearing liabilities rose 2 basis points during fiscal year 2006 to 2.98% during fiscal year 2006 from 2.96%

6

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

during fiscal year 2005. Despite an increasing interest rate environment in 2006, which drove the costs of certificates and money market deposits higher, the Company was able to limit the increase in its overall cost of funds by shifting its portfolio mix away from higher costing certificates, public funds deposits, and wholesale borrowings, into lower costing demand deposits.

PROVISION FOR LOAN LOSSES

In fiscal year 2006, the Company recorded a provision for loan losses of $311,000 compared to $4.7 million for fiscal year 2005. The provision in 2006 relates in part to the Company’s settlement agreement with one of several participants in an auto-dealership related lending relationship. Additionally, shrinkage in the Company’s loan portfolio during the year reduced the level of required loan loss allowances on the portfolio. The large provision for loan losses in fiscal year 2005 stemmed primarily from provisions related to losses in the aforementioned auto-dealership related loans. The relatively large provision in fiscal year 2005 and the provision in fiscal year 2006 is the primary reason that net interest income from continuing operations after provision for loan losses increased by $4.8 million, from $13.4 million in fiscal 2005 to $18.2 million in fiscal year 2006.

Management closely monitors economic developments both regionally and nationwide, and considers these factors when assessing the adequacy of its allowance for loan losses. Although current economic conditions are relatively strong, management is aware that many economists have forecasted a slowdown in economic growth during calendar year 2007. Additionally, management has monitored the disinflationary trend in residential and commercial real estate prices in recent quarters. Economic conditions in the agricultural sector of the Company’s market area are relatively strong. Recent rises in agricultural commodity prices will serve to offset more modest yields this year. The agricultural economy is accustomed to commodity price fluctuations and is generally able to handle such fluctuations without significant problems. The recent decrease in energy prices should also help to improve cash flows of consumers and businesses alike if the decrease persists during 2007.

Management believes that, based on a detailed review of the loan portfolio, historic loan losses, current economic conditions, the size of the loan portfolio, and other factors, the current level of the allowance for loan losses reflects an adequate allowance against probable losses from the loan portfolio. Although the Company maintains its allowance for loan losses at a level that it considers to be adequate, investors and others are cautioned that there can be no assurance that future losses will not exceed estimated amounts, or that additional provisions for loan losses will not be required in future periods. In addition, the Company’s determination of the allowance for loan losses is subject to review by its regulatory agencies, which can require the establishment of additional general or specific allowances.

NON-INTEREST INCOME

Non-interest income increased by $10.0 million, or 285.4%, to $13.5 million for the fiscal year 2006 from $3.5 million from fiscal year 2005. The majority of this growth is related to higher card fee income earned on prepaid debit cards and other products and services offered by MPS. The increase also includes $2.6 million of non-recurring fee income related to a purchased portfolio of prepaid debit cards.

NON-INTEREST EXPENSE

Non-interest expense increased by $8.6 million, or 48.0%, to $26.6 million for fiscal year 2006 from $18.0 million for fiscal year 2005. Several factors contributed to this increase. Compensation expense rose $1.9 million during the year, from $10.9 million in fiscal year 2005 to $12.8 million in fiscal year 2006. The increase stems primarily from staff acquisition costs related to growth at MPS and the staffing of two de novo branch facilities in the Sioux Falls market. The new branch in Des Moines did not significantly impact non-interest expense for the year, due to its opening late in the fiscal year.

Costs associated with the processing of card-related products at MPS also increased during fiscal year 2006. Card processing expense rose $2.6 million from $337,000 in fiscal year 2005 to $3.0 million in fiscal year 2006 as a result of the significant growth in the division’s product lines. These expenses stem primarily from fees charged by third party card and network transaction processors as well as costs associated with issuing MetaBank branded prepaid debit cards. Management expects that these costs will continue to rise as MPS issues more cards; however, it is anticipated that overall costs will rise less than revenues associated with these cards.

Legal and consulting expense increased $2.2 million in fiscal year 2006, from $815,000 in fiscal year 2005 to $3.0 million in fiscal year 2006. Several factors contributed to this increase. The Company incurred expenses related to the aforementioned auto dealership-related loans during the course of foreclosing on and liquidating the remaining assets of the borrowers. Additionally, the Company has been named in several lawsuits by banks that participated with MetaBank in these lending relationships. The Company has also incurred expenses related to its retention of an outside consulting firm to complete implementation work related to section 404 of the Sarbanes-Oxley Act. At this time, the Company does not anticipate that expenses associated with this implementation work will continue at present levels over the long term. Finally, the Company outsourced a significant portion of its internal audit work to an outside consulting firm during fiscal year 2006.

INCOME TAX EXPENSE

Income tax expense from continuing operations for fiscal year 2006 was $1.7 million, or an effective tax rate of 33.0%. In fiscal year 2005, the Company recorded an income tax benefit of $491,000, or an effective tax rate of 43.0%, due to the net loss recorded that year. The increase in income taxes is primarily the result of the positive change in operating results between the comparable periods.

DISCONTINUED OPERATIONS

Income from discontinued operations was $309,000 for fiscal year 2006 compared to a loss of $272,000 for fiscal year 2005. The increase was primarily related to a decrease in provision for loan losses in the amount of $845,000 as compared to the prior fiscal year. See Note 3 to the Notes to Consolidated Financial Statements for further discussion on discontinued operations.

CRITICAL ACCOUNTING POLICY

The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States of America. The financial information contained within these statements is, to a significant extent, financial information that is based on approximate measures of the financial effects of transactions and events that have already occurred. Based on its consideration of accounting policies that involve the most complex and subjective decisions and assessments, management has identified its most critical accounting policies to be those related to the allowance for loan losses and asset impairment judgments including the recoverability of goodwill.

The Company’s allowance for loan loss methodology incorporates a variety of risk considerations, both quantitative and qualitative, in establishing an allowance for loan loss that management believes is appropriate at each reporting date. Quantitative factors include the Company’s historical loss experience, delinquency and charge-off trends, collateral values, changes in nonperforming loans, and other factors. Quantitative factors also incorporate known information about individual loans, including borrowers’ sensitivity to interest rate movements. Qualitative factors include the general economic environment in the Company’s markets, including economic conditions throughout the Midwest and, in particular, the state of certain industries. Size and complexity of individual credits in relation to loan structure, existing loan policies, and pace of portfolio growth are other qualitative factors that are considered in the methodology. As the Company adds new products and increases the complexity of its loan portfolio, it will enhance its methodology accordingly. Management may have reported a materially different amount for the provision for loan losses in the statement of operations to change the allowance for loan losses if its assessment of the above factors were different. This discussion and analysis should be read in conjunction with the Company’s financial statements and the accompanying notes presented in this Annual Report, as well as the portion of this

7

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

Management’s Discussion and Analysis section entitled “Asset Quality.” Although management believes the levels of the allowance as of both September 30, 2007 and September 30, 2006 were adequate to absorb probable losses inherent in the loan portfolio, a decline in local economic conditions or other factors could result in increasing losses. See Notes 1 and 6 to the Notes to Consolidated Financial Statements.

Goodwill represents the excess of acquisition costs over the fair value of the net assets acquired in a purchase acquisition. Goodwill is tested annually for impairment.

ASSET/LIABILITY MANAGEMENT AND MARKET RISK

QUALITATIVE ASPECTS OF MARKET RISK

As stated above, the Company derives a portion of its income from the excess of interest collected over interest paid. The rates of interest the Company earns on assets and pays on liabilities generally are established contractually for a period of time. Market interest rates change over time. Accordingly, the Company’s results of operations, like those of most financial institutions, are impacted by changes in interest rates and the interest rate sensitivity of its assets and liabilities. The risk associated with changes in interest rates and the Company’s ability to adapt to these changes is known as interest rate risk and is the Company’s only significant “market” risk.

QUANTITATIVE ASPECTS OF MARKET RISK

The Company monitors and measures its exposure to changes in interest rates in order to comply with applicable government regulations and risk policies established by the Board of Directors, and in order to preserve shareholder value. In monitoring interest rate risk, the Company analyzes assets and liabilities based on characteristics including size, coupon rate, repricing frequency, maturity date, and likelihood of prepayment.

If the Company’s assets mature or reprice more rapidly or to a greater extent than its liabilities, then net portfolio value and net interest income would tend to increase during periods of rising rates and decrease during periods of falling interest rates. Conversely, if the Company’s assets mature or reprice more slowly or to a lesser extent than its liabilities, then net portfolio value and net interest income would tend to decrease during periods of rising interest rates and increase during periods of falling interest rates.

The Company currently focuses lending efforts toward originating and purchasing competitively priced adjustable-rate and fixed-rate loan products with short to intermediate terms to maturity, generally 5 years or less. This theoretically allows the Company to maintain a portfolio of loans that will have relatively little sensitivity to changes in the level of interest rates, while providing a reasonable spread to the cost of liabilities used to fund the loans.

The Company’s primary objective for its investment portfolio is to provide a source of liquidity for the Company. In addition, the investment portfolio may be used in the management of the Company’s interest rate risk profile. The investment policy generally calls for funds to be invested among various categories of security types and maturities based upon the Company’s need for liquidity, desire to achieve a proper balance between minimizing risk while maximizing yield, the need to provide collateral for borrowings, and to fulfill the Company’s asset/liability management goals.

The Company’s cost of funds responds to changes in interest rates due to the relatively short-term nature of its deposit portfolio, and due to the relatively short-term nature of its borrowed funds. The Company’s growing portfolio of low- or no-cost deposits provides a stable and profitable funding vehicle, but also subjects the Company to greater risk in a falling interest rate environment than it would otherwise have without this portfolio. This risk is due to the fact that, while asset yields may decrease in a falling interest rate environment, the Company cannot significantly reduce interest costs associated with these deposits, which thereby compresses the Company’s net interest margin. As a result of the Company’s new interest rate risk exposure in this regard, the Company has elected not to enter in to any new longer term wholesale borrowings, and generally has not emphasized longer term time deposit products.

The Board of Directors and relevant government regulations establish limits on the level of acceptable interest rate risk at the Company, to which management adheres. There can be no assurance, however, that in the event of an adverse change in interest rates, the Company’s efforts to limit interest rate risk will be successful.

NET PORTFOLIO VALUE

The Company uses a net portfolio value (“NPV”) approach to the quantification of interest rate risk. This approach calculates the difference between the present value of expected cash flows from assets and the present value of expected cash flows from liabilities, as well as cash flows from any off balance-sheet contracts. Management of the Company’s assets and liabilities is performed within the context of the marketplace, but also within limits established by the Board of Directors on the amount of change in NPV that is acceptable given certain interest rate changes.

Presented below (including discontinued operations), as of September 30, 2007 and 2006, is an analysis of the Company’s interest rate risk as measured by changes in NPV for an instantaneous and sustained parallel shift in the yield curve, in 100 basis point increments, up and down 200 basis points. As illustrated in the table below, the Company’s NPV at September 30, 2007 was relatively balanced. Growth in the Company’s portfolio of non-interest bearing deposits during fiscal year 2007 has contributed to a balance sheet that is slightly less asset sensitive, i.e. exhibits more favorable changes in a rising rate environment, as of September 30, 2007, than was the case at September 30, 2006.

Certain shortcomings are inherent in the method of analysis presented in the table. For example, although certain assets and liabilities may have similar maturities or periods to repricing, they may react in different degrees to changes in market interest rates. Also, the interest rates on certain types of assets and liabilities may fluctuate in advance of changes in market interest rates, while interest rates on other types may lag behind changes in market rates. Additionally, certain assets, such as adjustable rate mortgage loans, have features that restrict changes in interest rates on a short term basis and over the life of the asset. Furthermore, although management has estimated changes in the levels of prepayments and early withdrawal in these rate environments, such levels would likely deviate from those assumed in calculating the table. Finally, the ability of some borrowers to service their debt may decrease in the event of an interest rate increase.

In addition to the NPV approach, the Company also reviews gap reports, which measure the differences in assets and liabilities repricing in given time periods, and net income simulations to assess its interest rate risk profile. Management reviews its interest rate risk profile on a quarterly basis.

ASSET QUALITY

It is management’s belief, based on information available at fiscal year end, that the Company’s current asset quality is satisfactory. At September 30, 2007, nonperforming assets, consisting of impaired/non-accruing loans, accruing loans delinquent 90 days or more, restructured loans, foreclosed real estate, and repossessed consumer property,

Change in Interest Rate | | Board Limit | | | | At September 30, 2007 | | | | At September 30, 2006 | |

(Basis Points) | | % Change | | $ Change | | % Change | | $ Change | | % Change | |

Dollars In Thousands | | | | | | | | | | | | |

+200 bp | | (20 | )% | $ | 606 | | (1 | )% | $ | 548 | | 1 | % |

+100 bp | | (10 | ) | (221 | ) | (1 | ) | 562 | | 1 | |

0 | | — | | — | | — | | — | | — | |

-100 bp | | (10 | ) | (545 | ) | (1 | ) | (907 | ) | (1 | ) |

-200 bp | | (20 | ) | (3,226 | ) | (4 | ) | (4,139 | ) | (6 | ) |

| | | | | | | | | | | | | | |

8

Meta Financial Group, Inc. and Subsidiaries

MANAGEMENT’S DISCUSSION AND ANALYSIS

totaled $2.6 million, or 0.38% of total assets, compared to $5.3 million, or 0.72% of total assets, at September 30, 2006.

Impaired/non-accruing and restructured loans at September 30, 2007 totaled $1.7 million. Foreclosed real estate and repossessed assets at September 30, 2007 totaled $318,000.

The Company maintains an allowance for loan losses because of the potential that some loans may not be repaid in full. See Note 1 to the Notes to Consolidated Financial Statements. At September 30, 2007, the Company had an allowance for loan losses in the amount of $4.5 million as compared to $6.4 million at September 30, 2006. Management’s periodic review of the adequacy of the allowance for loan losses is based on various subjective and objective factors including the Company’s past loss experience, known and inherent risks in the portfolio, adverse situations that may affect the borrower’s ability to repay, the estimated value of any underlying collateral, and current economic conditions. While management may allocate portions of the allowance for specifically identified problem loan situations, the majority of the allowance is based on judgmental factors related to the overall loan portfolio and is available for any loan charge-offs that may occur. As stated previously, there can be no assurance that future losses will not exceed estimated amounts, or that additional provisions for loan losses will not be required in future periods. In addition, the Company’s banks are subject to review by banking regulatory bodies, which have the authority to require management to make changes to the allowance for loan losses.

In determining the allowance for loan losses, the Company specifically identifies loans that it considers to have potential collectibility problems. Based on criteria established by Statement of Financial Accounting Standards (SFAS) No. 114, some of these loans are considered to be “impaired” while others are not considered to be impaired, but possess weaknesses that the Company believes merit additional analysis in establishing the allowance for loan losses. All other loans are evaluated by applying estimated loss ratios to various pools of loans. The Company then analyzes other factors (such as economic conditions) in determining the aggregate amount of the allowance needed.

At September 30, 2007, $1.5 million of the allowance for loan losses was allocated to impaired loans, representing 65.1% of the related loan balances. See Note 6 to the Notes to Consolidated Financial Statements. $639,000 of the allowance was allocated to other identified problem loan situations, representing 3.0% of the related loan balances, and $2.4 million, representing 0.7% of the related loan balances, was allocated to the remaining overall loan portfolio based on historical loss experience and general economic conditions. At September 30, 2006, $2.7 million of the allowance for loan losses was allocated to impaired loans, representing 51.5% of the related loan balances. $1.1 million was allocated to other identified problem loan situations, and $2.5 million was allocated against losses from the overall loan portfolio based on historical loss experience and general economic conditions.

LIQUIDITY AND CAPITAL RESOURCES

The Company’s primary sources of funds are deposits, borrowings, principal and interest payments on loans and mortgage backed securities, and maturing investment securities. While scheduled loan repayments and maturing investments are relatively predictable, deposit flows and early loan repayments are influenced by the level of interest rates, general economic conditions, and competition.

The Company relies on advertising, quality customer service, convenient locations, and competitive pricing to attract and retain its deposits and only solicits these deposits from its primary market area. Based on its experience, the Company believes that its consumer checking, savings, and money market accounts are relatively stable sources of deposits. The Company’s ability to attract and retain time deposits has been, and will continue to be, affected by market conditions. However, the Company does not foresee any significant funding issues resulting from the sensitivity of time deposits to such market factors.

The Company is aware that, due to higher levels of concentration risk, the low- and no-cost checking deposits generated through MPS may carry a greater degree of liquidity risk than traditional consumer checking deposits. As a result, the Company closely monitors balances in these accounts, and maintains a portfolio of highly liquid assets to fund potential deposit outflows. To date, the Company has not experienced any inordinate or unusual outflows related to MPS, though no assurance can be given that this will continue to be the case.

MetaBank and MetaBank WC are required by regulation to maintain sufficient liquidity to assure their safe and sound operation. In the opinion of management, both MetaBank and MetaBank WC are in compliance with this requirement.

Liquidity management is both a daily and long term function of the Company’s management strategy. The Company adjusts its investments in liquid assets based upon management’s assessment of (i) expected loan demand, (ii) the projected availability of purchased loan products, (iii) expected deposit flows, (iv) yields available on interest bearing deposits, and (v) the objectives of its asset/liability management program. Excess liquidity is generally invested in interest earning overnight deposits and other short term government agency obligations. If the Company requires funds beyond its ability to generate them internally, it has additional borrowing capacity with the FHLB and other wholesale funding sources. The Company is not aware of any significant trends in the Company’s liquidity or its ability to borrow additional funds if needed.

The primary investing activities of the Company are the origination and purchase of loans and the purchase of securities. During the years ended September 30, 2007, 2006 and 2005, the Company originated loans totaling $274.5 million, $306.6 million, and $311.7 million, respectively. Purchases of loans totaled $44.9 million, $58.9 million, and $29.7 million during the years ended September 30, 2007, 2006 and 2005, respectively. During the years ended September 30, 2007, 2006 and 2005, the Company purchased mortgage-backed securities and other securities available for sale in the amount of $13.2 million, $109,000 and $17.6 million, respectively.

At September 30, 2007, the Company had unfunded loan commitments of $50.3 million. See Note 17 to the Notes to Consolidated Financial Statements. Certificates of deposit scheduled to mature in one year or less from September 30, 2007 totaled $107.3 million. Based on its historical experience, management believes that a significant portion of such deposits will remain with the Company; however, there can be no assurance that the Company can retain all such deposits. Management believes that loan repayment and other sources of funds will be adequate to meet the Company’s foreseeable short and long-term liquidity needs.

During July 2001, the Company’s unconsolidated trust subsidiary, First Midwest Financial Capital Trust I, sold $10.0 million in floating rate cumulative preferred securities. Proceeds from the sale were used to purchase subordinated debentures of Meta Financial