SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D)OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended January 31, 2006 |

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D)OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ____________ to ____________ |

Commission file number: 0-21968

_________________

BRAZAURO RESOURCES CORPORATION

(formerly Jaguar Resources Corporation)

(Exact Name of Registrant as Specified in Its Charter)

| British Columbia (State or Other Jurisdiction of Incorporation or Organization) | 76-0195574 (I.R.S. Employer Identification No.) |

800 Bering, Suite 208

Houston, TX 77057

(Address of Principal Executive Offices, including Zip Code)

(713) 785-1278

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class None | Name of Exchange on Which Registered None |

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class

COMMON STOCK

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

As of July 29, 2005, the aggregate market value of voting stock held by non-affiliates of the Registrant, based on the closing price of the Common Stock of the Registrant quoted on the TSX Venture Exchange was $88,202,856 (Canadian) or $71,961,211 (U.S.). For purposes of calculating this amount, only directors, officers and beneficial owners of 5% or more of the capital stock of the Registrant have been deemed affiliates.

Number of shares of Registrant’s Common Stock outstanding as of April 17, 2006: 52,931,645

Documents incorporated by reference: Portions of Item 10 in an Amended Form 10-K, which is expected to be filed by May 31, 2006, have been incorporated by reference into Part III of this Annual Report on Form 10-K.

BRAZAURO RESOURCES CORPORATION

FORM 10-K

TABLE OF CONTENTS

| Page | ||||||

PART I | ||||||

| Item 1. | Business | 1 | ||||

| Item 1A. | Risk Factors | 2 | ||||

| Item 1B. | Unresolved Staff Comments | 3 | ||||

| Item 2. | Properties | 4 | ||||

| Item 3. | Legal Proceedings | 8 | ||||

| Item 4. | Submission of Matters to a Vote of Security Holders | 8 | ||||

PART II | ||||||

| Item 5. | Market for Registrant’s Common Stock, Related Stockholder Matters and Issuer Purchases of Equity Securities | 8 | ||||

| Item 6. | Selected Consolidated Financial Information | 19 | ||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 20 | ||||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 25 | ||||

| Item 8. | Financial Statements and Supplementary Data | 25 | ||||

| Item 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | 25 | ||||

| Item 9A. | Controls and Procedures | 25 | ||||

PART III | ||||||

| Item 10. | Directors and Executive Officers of the Registrant | 26 | ||||

| Item 11. | Executive Compensation | 28 | ||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 30 | ||||

| Item 13. | Certain Relationships and Related Transactions | 31 | ||||

| Item 14. | Principal Accountant Fees and Services | 32 | ||||

PART IV | ||||||

| Item 15. | Exhibits and Financial Statement Schedules | 33 | ||||

| Signatures | 33 | |||||

i

Item 1. BUSINESS

General Information

Brazauro Resources Corporation (“the Company”) is engaged in the business of exploring for and, if warranted, developing mineral properties and is concentrating its current acquisition and exploration efforts on those properties which the Company believes have large scale gold potential. The Company holds interests in properties located in the Tapajós Gold District of Brazil’s northerly Pará State (collectively the “Properties”).

The Company has two wholly-owned subsidiaries; Brazauro Holdings (Brazil) Ltd., a British Columbia corporation (“Brazauro Holdings”), and Star U.S. Inc., a Delaware corporation (“Star”). Star in turn owns 100% of the stock of three corporations, Diamond Exploration, Inc. and Continental Diamonds, Inc., both of which are Arkansas corporations (“DEI” and “CDI”, respectively), and Diamond Operations, Inc., a Delaware corporation (“DOI”). The Company and Brazauro Holdings own 98% and 2%, respectively, of Jaguar Resources do Brasil Ltda., a Brazilian corporation. All references to the Company herein include its subsidiaries unless otherwise noted. The Company’s Consolidated Financial Statements referred to herein also include its subsidiaries. The Company’s fiscal year ends January 31.

The Company’s principal office is located at 800 Bering, Suite 208, Houston, Texas, U.S.A. 77057. The Company had three (3) full-time employees at January 31, 2006; however, the Company retains consultants, independent contractors and part-time employees on an as-needed basis in connection with its exploration and development activities.

The Company was incorporated under the Company Act (British Columbia) on March 12, 1986. The authorized capital of the Company consists of an unlimited amount of shares of common stock without par value (the “Common Stock”), of which 52,931,645 shares were issued and outstanding as of April 17, 2006. The Common Stock of the Company ranks equally as to dividends, voting rights and participation in assets and is traded under the symbol “BZO” on the TSX Venture Exchange.

Unless otherwise stated herein, all monetary amounts are expressed in Canadian dollars. At April 17, 2006, the exchange rate for conversion to United States dollars was $1.00 (Canadian) = U.S. $ 0.8732. Historical exchange rates for the last five years are set forth in Item 6 at page 19. The Company’s Consolidated Financial Statements in Item 15 are prepared in accordance with Canadian generally accepted accounting principles.

The Company is subject to substantial risks with respect to exploration activities and will seek additional capital during fiscal 2007 to conduct additional property exploration activities and to fund general and administrative expenses. See “Certain Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

Operating History and Development

The Company became a public company in January 1988 when it undertook an initial public offering of its Common Stock in British Columbia, Canada and became listed on the Vancouver Stock Exchange, a predecessor to the TSX Venture Exchange. From inception and prior to 1988 the Company had limited business activities and through 1993 explored and abandoned several mineral properties. During fiscal 1993, the Company elected to pursue prospects with the potential for commercial diamond production.

The Company completed three acquisitions in fiscal 1993 consistent with its focus on diamond exploration prospects, including acquisitions of the “Arkansas Properties” (defined below). During fiscal 1995 through 2003, the Company completed additional acquisitions in Arkansas and directly managed and funded exploration efforts on certain Arkansas Properties. In fiscal 2003 the Company decided to cease exploration efforts in Arkansas due to disappointing exploration results, and began to pursue mineral exploration prospects, particularly gold prospects in South America.

1

During fiscal 2004 the Company acquired the mineral rights to two properties in Brazil, the Tocantinzinho and Mamoal Properties, as described below. In fiscal 2005, the Company extended its holdings in the Tocantinzinho Properties and conducted exploration activities on both the Tocantinzinho and Mamoal Properties. Additionally, the Company acquired the Batalha Property, a gold prospect also located in Pará State, Brazil. During fiscal 2006, the Company conducted further exploration activities on the Tocantinzinho and Mamoal Properties. Based upon the disappointing exploration results at the Mamoal Property, the Company determined that it was likely further exploration activities would not be conducted at the project. Accordingly, the net capitalized costs related to the Mamoal Property totaling $906,535 were written off during the fourth quarter of fiscal 2006.

Upon acquisition of an exploration property, the Company typically performs geologic evaluation and exploration efforts to determine if the project warrants further work including, but not limited to geologic mapping and sampling, geophysical surveys, and drilling. The Company will continue to pursue mineral exploration prospects, focusing on the Tapajós and on a worldwide basis as opportunities arise, subject to adequate acquisition and exploration funding.

Included in the consolidated balance sheets at January 31, 2006 and 2005 are total assets of approximately $4,698,000 and $2,939,000, respectively, related to the Company’s operations in Brazil. The mineral properties and deferred expenditures totaling approximately $4,493,000 and $2,818,000 at January 31, 2006 and 2005, respectively, are net capitalized costs related to the Company’s Brazilian properties.

Since its inception, the Company has no revenues from operations other than interest income on invested cash balances and rental income from the Company’s Diamond Recovery Plant (“the Plant”) totaling $1,079,000. The rental income was received during the three fiscal years ended January 31, 1999. In March 2003 the Company sold the Plant to a third party for $350,000 (U.S.).

Item 1A. RISK FACTORS

The Company’s business plan to acquire additional exploration prospects, continue exploration activities on its current projects, and, if warranted, undertake development and mining operations is subject to numerous risks and uncertainties, including the following:

Lack of Proven Properties and Insufficient Exploration and Development Funds. At this point, all of the Company’s exploration prospects and property interests (collectively the “Properties”) are gold prospects in Brazil. While the Company has sufficient funds to complete the exploration phase currently underway, additional funds may be necessary in order for the Company to pursue further exploration on its existing properties and to acquire and develop additional exploration prospects. Certain of the Company’s planned expenditures are discretionary and may be increased or decreased based upon funds available to the Company.

As of January 31, 2006, the Company had sufficient cash to fund general and administrative expenses anticipated during fiscal 2007. As discussed above, the Company may be required to raise additional capital for additional exploration activity on its existing properties and acquisition of new exploration prospects during fiscal 2007. There can be no assurance that additional funds can be raised. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” (hereinafter referred to as “MD & A”).

Environmental Laws. The exploration programs conducted by the Company are subject to national, state and/or local regulations regarding environmental considerations in the jurisdiction where they are located. Most operations involving exploration or production activities are subject to existing laws and regulations relating to exploration and mining procedures, reclamation, safety precautions, employee health and safety, air quality standards, pollution of stream and fresh water sources, odor, noise, dust, and other environmental protection controls adopted by federal, state and local governmental authorities as well as the rights of adjoining property owners. The Company may be required to prepare and present to federal, state or local authorities data pertaining to the effect or impact that any proposed exploration or production of minerals may have upon the environment. All requirements imposed by any such authorities may be costly, time consuming, and may delay commencement or continuation of exploration or production operations. However, at this time, the Company is exploring its Properties and does not

2

anticipate preparing environmental impact statements or assessments until such time as the Company believes one or more of its Properties will prove to be commercially feasible.

Limited Exploration Prospects. The Company’s existing properties are all gold prospects in Brazil. Accordingly, the Company does not have a diversified portfolio of exploration prospects either geographically or by mineral targets. The Company’s operations could be significantly affected by changes in the market price of gold, as the economic viability of the Company’s projects is heavily dependent upon the market price of gold. Additionally, the Company’s projects are subject to the laws of Brazil and can be negatively impacted by the existing laws and regulations of that country, as they apply to mineral exploration, land ownership, royalty interests and taxation, and by any potential changes of such laws and regulations. Due to the Company’s exploration activities in Brazil, the Company is also subject to economic risks due to currency fluctuation and foreign exchange controls.

Title to Properties. The Company cannot guarantee title to all of its Properties as the Properties may be subject to prior mineral rights applications with priorty, prior unregistered agreements or transfers or native land claims, and title may be affected by undetected defects. Certain of the mineral rights held by the Company are held under applications for mineral rights and, until final approval of such applications is received, the Company’s rights to such mineral rights may not materialize and the exact boundaries of the Company’s properties may be subject to adjustment. The Company does not maintain title insurance on its properties.

Limited Market for Common Shares. The liquidity of the common shares of the Company, or ability of the shareholder to buy or sell the Company’s common stock, may be significantly limited for various unforeseeable periods. The average daily volume of the Company’s shares traded on the TSX Venture Exchange during fiscal 2006 was under 65,000 shares. The market price of the Company’s shares has historically fluctuated in a large range, as disclosed in Item 5 — Market for Registrant’s Common Stock and Related Stockholder Matters on page 6. The price of the Company’s common shares may be affected by many factors, including adverse change in the Company’s business, a decline in gold price and general economic trends.

Insurance Coverage. Mineral exploration is subject to risks of human injury, environmental and legal liability and loss of assets. The Company may elect not to have insurance for certain risks because of the high premiums associated with insuring those risks or, in some cases, insurance may not be available for certain risks. Occurrence of events for which we are not insured could have a material adverse effect on our financial position or results of operations.

Key Executives. The Company is dependent on the services of key executives, including its Chairman, Mark E. Jones, III, its Director and retired President, Leendert G. Krol, and its Vice President of Exploration, Stephen Zahony. All of the above individuals have many years of background in the mining industry. The Company may not be able to replace that experience and knowledge with other individuals.

Enforcement of Judgements against the Company. The Company is incorporated in the Province of British Columbia, Canada. Certain of our directors and officers live in Canada, and most of our assets are located in Brazil and Canada. As a result, it may be difficult for investors to effect service of legal process within the United States upon directors and officers who are not United States residents. Also, there is uncertainty as to the enforceability in Canada, in original actions or for enforcement of judgments of U.S. courts, of civil liabilities predicated upon U.S. federal or state securities laws.

Item 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this Form 10-K under “Item 1. Business”, “Item 2. Properties”, “Item 3. Legal Proceedings”, and “Item 7. MD & A” and other factors may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or

3

implied by such forward-looking statements. Such factors include, among others, the following: general economic and business conditions; competition; success of operating initiatives; the success of the Company’s exploration and development operations on its Properties; the Company’s ability to raise capital and the terms thereof; the acquisition of additional properties; the continuity, experience and quality of the Company’s management; changes in or failure to comply with government regulations or the lack of government authorization to continue the Company’s projects; and other factors referenced in this Form 10-K. The use in this Form 10-K of such words as “believes”, “plans”, “anticipates”, “expects”, “intends” and similar expressions are intended to identify forward-looking statements, but are not the exclusive means of identifying such statements. The success of the Company is dependent on the efforts of the Company, its employees and many other factors including, primarily, its ability to raise additional capital and establishing the economic viability of its exploration Properties.

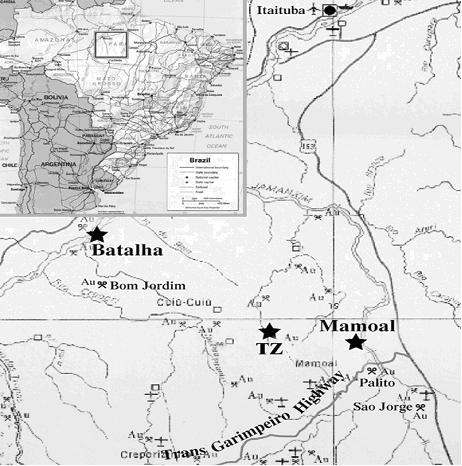

Item 2. PROPERTIES

Currently, all of the Company’s Properties are located in the Tapajós Gold District of Brazil’s northerly Pará State. The general location of the Company’s Brazilian Properties is shown on the map provided below. The map is followed by a description of the Company’s rights and interests in each of the Properties, including those Properties in the State of Arkansas where the Company’s rights and interests have expired.

4

Brazilian Properties

Tocantinzinho Properties

In August 2003 the Company entered into an option to acquire exploration rights to a total of 28,275 hectares in the Tapajós gold district in Para State, Brazil under an option agreement with two individuals (herein referred to as “optionors”). The option agreement entitles the Company to acquire a 100% interest in the exploration rights to such area (referred to herein as the “Tocantinzinho Properties”) over a four-year period in consideration for the staged payment of US$465,000, the staged issuance of 2,600,000 shares of the Company and the expenditure of $1,000,000 (U.S.) on exploration ($300,000 (U.S.) by July 31, 2004). The Company received approval for the acquisition from the TSX Venture Exchange in August 2003 and made the initial payment required by the option agreement to the optionors, consisting of 1,100,000 common shares of the Company and $75,000 (U.S.). The Company made the second option payment, consisting of 200,000 common shares of the Company and $30,000 (U.S.), in February 2004. In August 2004 and July 2005, the Company made the third and fourth option payments, each consisting of 200,000 common shares of the Company and $40,000 (U.S.).

As of January 31, 2006, the total commitment remaining under the option agreement is as follows (all amounts are in U.S. dollars): $130,000 and 200,000 common shares of the Company, and $150,000 and 700,000 common shares of the Company for the 2007 and 2008 fiscal years, respectively.

Additionally, the option agreement requires the Company to assume all existing obligations of the optionors to certain Brazilian residents in respect of the mineral rights to the Tocantinzinho Properties (the “Underlying Agreements”) totaling $1,600,000 (U.S.) over a four-year period. At January 31, 2006, the remaining payment commitments under the Underlying Agreements are as follows (all amounts are in U.S. dollars): $160,000 and $1,205,000 in fiscal years 2007 and 2008, respectively. The Company made payments totaling $35,000 (U.S.), $80,000 (U.S.) and $120,000 (U.S.) in respect of the Underlying Agreements during fiscal 2004, 2005 and 2006, respectively. One of the optionors entered into a consulting agreement with the Company for an 18-month period at a rate of $7,000 (U.S.) per month which expired during fiscal 2005. The payments under the option agreement, the Underlying Agreements and the consulting agreement are considered expenditures for purposes of meeting the required total and initial annual expenditures of $1,000,000 (U.S.) and $300,000 (U.S.), respectively, discussed above. During fiscal 2005 the Company completed the requirement under the option agreement to expend a total of $300,000 (U.S.) and met the requirement to expend $1,000,000 (U.S.) on exploration. The Company has met its commitments under the option agreement to January 31, 2006, and the option agreement is cancelable by the Company without further obligations.

The optionors are entitled to a sliding scale gross revenues royalty ranging from 2.5% for gold prices below $400 (U.S.) per ounce to 3.5% for gold prices in excess of $500 (U.S.) per ounce.

The Company has received exploration licenses in respect of the central 4,000 hectare area of the Tocantinzinho Properties on which it has been focusing its exploration efforts as well as for a 9,315 hectare area forming the north eastern and eastern boundary of the Tocantinzinho Properties. Under the option agreement the Company also holds rights to acquire two other applications for exploration licenses filed with the regulatory authorities in Brazil: one covering 4,275 hectares that lies to the south of the central 4,000 hectare area and one (the “Extension Area”) covering 10,000 hectares that lies immediately to the east but continues well south of the central 4,000 hectare area. The mineralized zone discovered by the Company (see “Drilling and Exploration” below) on the Tocantinzinho Properties starts on the central 4,000 hectare area and extends eastward beyond the boundary of the central 4,000 hectare area into the Extension Area.

At the end of fiscal 2006, as a result of further title reviews by the Company, it came to the Company’s attention that a long dormant application for a mining license that covered the Extension Area had never been processed by the Departamento Nacional de Produção Mineral (“DNPM”) and was still valid. According to advice from Brazilian counsel, the dormant application carried paramount title to the Extension Area. The Company, through its subsidiary, Jaguar Resources do Brasil Ltda., reached an agreement with the holder of such application to acquire its rights to obtain a mining license over the Extension Area, subject to receipt of confirmation from the DNPM of the

5

granting of the mining license. In the event the DNPM does not grant the mining license, the Company’s rights to the Extension Area will be in doubt. To date, the Company has made a payment of $150,000 (U.S.) to the holder of the application.

The Company is aware that another entity has asserted that it holds prior mineral rights to areas of the Tocantinzinho Properties, including areas of the mineralized zone discovered by the Company. The Company is presently undertaking an extensive review of its title position and has found inconsistencies in its title documentation relating to license boundaries. The Company is working with its Brazilian counsel and the DNPM to resolve these inconsistencies. These inconsistencies may adversely affect the Company’s rights to a portion of the mineralized zone. The Company has been advised of the laws governing these matters and considers that these inconsistencies should be resolved such that the Company will retain rights to all of the mineralized zone. However, the resolution of these inconsistencies will require the DNPM to concur with the Company’s interpretation of these laws. An adverse interpretation of Brazilian mining laws may result in another party receiving rights to some portion of the mineralized zone.

Under a separate agreement, the Company holds exploration licenses for an additional 16,052 hectares adjacent to the western border of the above central 4,000 hectares of the Tocantinzinho Properties. The Company has agreed to make payments totaling $300,000 (U.S.) over a period of approximately four years to an individual as a finder’s fee related to this 16,052 hectare property. As of January 31, 2006, the remaining commitment under this agreement is $215,000 (U.S.). This additional property is not subject to the option agreement and therefore is not subject to the royalty. The Company received an exploration license from the Brazilian regulatory authority with respect to the additional 16,052 hectares in fiscal year 2005.

Mamoal Property

The Company entered into an option agreement under which it may acquire the exploration license to the 10,000 hectare Mamoal Property, located 30 kilometers southeast of the Company’s Tocantinzinho Properties, in December 2003. The Company has an option to earn 100% of the Mamoal Property by payment of a total of $300,000 (U.S.) over three and one half years. The Company may terminate the option agreement at any time without further obligation. An initial $10,000 (U.S.) payment was made by the Company in December 2003, and the exploration research license has been transferred to Jaguar Resources do Brasil Ltda. During fiscal 2005 and 2006, the Company made payments under the option agreement totaling $25,000 (U.S.) and $45,000 (U.S.), respectively. The remaining option payments are as follows (all amounts are in U.S. dollars): $65,000 and $155,000 in fiscal years ending January 31, 2007 and 2008, respectively. The Company may acquire the Mamoal Property at any time by accelerating the option payments. The Company has received the exploration license from the Brazilian regulatory authority.

Batalha Property

In September, 2004 the Company applied for an exploration license to the 9800 hectare Batalha Property, located in the Tapajós gold province in northern Brazil. The property, host to a well known and extensive “garimpo” or artisanal mine, lies at the western end of the Tocantinzinho trend.

The Company has agreed to pay the original holder of artisanal mining rights of Batalha, who controls over 1,700 hectares lying within the exploration license and directly over the Batalha zone, the equivalent of approximately $91,000 Canadian dollars in Brazilian reals over a 42 month period with a buyout after 4 years of $250,000 (U.S.) (if the project is deemed economic by the Company) and an additional sum based on the number of ounces of gold in the proven and probable (or measured and indicated) categories at Batalha as set out in a pre-feasibility or feasibility study. The per ounce payment amount ranges in a sliding scale from $1 (U.S.) per ounce for the first one million ounces up to $10 (U.S.) per ounce for each ounce over four million ounces. The 9,800 hectare exploration license lies over top of this area, covering extensions to north, south and west. If after four years the Company, in its sole opinion, has not found an economic ore body, the area and all collected data will be returned to the vendor.

6

Drilling and Exploration

The Company completed a diamond drill program consisting of twenty holes (approximately 4000 meters) at the Tocantinzinho Properties during fiscal 2005 in which 19 of 20 holes encountered mineralization. The Company completed a follow-up fourteen-hole Phase III drilling program at the Tocantinzinho Properties in the third quarter of fiscal 2006. A total of thirty four (34) core holes have now been completed on the property. Drill results to date indicate an extended strike length of mineralization of greater than 650 meters in length and confirm the earlier reported intercepts of continuous lower grade mineralization with several zones of high grade from 26.82 to 374.40 grams of gold per ton over widths of 2.5 to 0.85 meters. Additionally, the Company completed both a ground magnetic survey and metallurgical testing of drill core samples of the Tocantinzinho Properties during fiscal 2005 and 2006 and was encouraged by the results.

In October, 2005 the Company reported results of extensive fixed-wing airborne magnetic and radioactive surveys completed over the Tocantinzinho and Mamoal Properties. These geophysical surveys have located several significant additional magnetic low areas which will now be the subject of further exploration and drilling.

In fiscal 2005 the Company carried out a regional soil auger sampling program on its Mamoal Property, in conjunction with channel-sampling of old pits and rock-chip sampling. At the Mamoal Property, core drilling commenced in November 2005 and was completed in January 2006.

An extensive grid soil geochemical survey was conducted at Mamoal during fiscal 2006. Hand-augered soil samples were collected over two specific areas identified in previous soil sampling programs as being gold anomalous. One area is called Itapecoim, where 544 augered soil samples were collected and chemically analyzed for gold in fiscal 2006. The second area is called Agua Limpa, where 426 augered soil samples were collected in fiscal 2006. Following the geochemical results, seven core holes were drilled for a total of 1,342.7 meters, with 394 core samples assayed. The best intersection returned 0.30 meter at 6.49 grams Au per tonne. The results of the above testing were not encouraging, and the Company may cease exploration of this project or seek a joint venture partner. Accordingly, the net capitalized costs related to the Mamoal Property totaling $906,535 were written off during the fourth quarter of fiscal 2006.

At the Company’s Batalha property a detailed geological survey was followed by an auger geochemical survey. These programs were conducted between February and April 2006 and results are being reviewed and analyzed at the present time.

The Company has signed a 3,000-meter drilling contract for continued drilling at the Tocantinzinho Properties, and work has commenced as of April 17, 2006. Detailed results of the above testing at the Tocantinzinho Properties, including initial results of the April, 2006 drill program, maps of the ground magnetic results and mineralization found by the core drilling program, are located at the Company’s website, www.brazauroresources.com.

Arkansas Properties

The Company maintained interests in several Arkansas Properties during the period from fiscal 1993 through fiscal 2003. In December 2002, based upon the cumulative exploration results obtained on the Arkansas Properties, the Company made the decision to cease operations in Arkansas.

American Mine Property

Pursuant to an agreement dated November 4, 1992, DEI was granted a permit to explore a mineral property located in Pike County, Arkansas. The Company’s Plant was located on this leased property. The Company leased the property and conducted exploration activities during certain periods from 1992 to 2002. The lease payment of $47,500 (U.S.) on the American Property, due November 1, 2002, was not made by the Company.

In March 2003 the Company sold the Plant to a third party for $350,000 (U.S.). In conjunction with the sale, the third party paid the lessor of the American Mine Property $47,500 (U.S.) on behalf of the Company in order to extend the Company’s lease on the property through October 31, 2003. The Company recorded a retirement

7

obligation for leasehold reclamation costs during fiscal year 2004 of approximately $150,000, representing the estimated costs of the Company’s obligation to restore the Arkansas properties to their original condition prior to lease expiration and to perform reclamation activities as required by Arkansas regulatory authorities. The Company allowed the lease to expire effective November 1, 2003.

Item 3. LEGAL PROCEEDINGS

Except as described in Note 11 of the Notes to the Company’s Consolidated Financial Statements incorporated by reference into Part II, Item 8 hereof, there are no material pending legal proceedings to which the Company or any of its subsidiaries is a party or to which any of their property is subject. The Company is involved from time to time in claims arising in the normal course of business.

Item 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

Item 5. MARKET FOR REGISTRANT’S COMMON STOCK, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company’s Common Stock is listed on the TSX Venture Exchange (“the TSX”) in British Columbia, Canada under the symbol “BZO” (“JRS” through September 3, 2004). The Company’s Common Stock is not traded on an exchange or market in the United States. The high and low sales prices (in Canadian dollars) as quoted on the TSX for the below referenced quarterly periods were as follows:

| Price Range of Common Stock Fiscal Year Ended January 31 | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 2006 | 2005 | ||||||||

| Fiscal Quarter Ended | High | Low | High | Low | |||||

| April 30 | 1 | .55 | 0 | .80 | 1 | .80 | 0 | .35 | |

| July 31 | 2 | .15 | 1 | .01 | 1 | .58 | 0 | .73 | |

| October 31 | 2 | .50 | 1 | .60 | 1 | .05 | 0 | .78 | |

| January 31 | 1 | .74 | 1 | .02 | 1 | .39 | 0 | .80 | |

The closing price of the Company’s Common Stock was $1.51 (Canadian) as of April 17, 2006 on the TSX Venture Exchange.

At March 31, 2006, there were 196 holders of record of the Company’s Common Stock including 160 in the United States who collectively held 28,583,087 shares representing 54% of the total number of issued and outstanding shares. The Company believes it has in excess of 300 beneficial owners of its Common Stock residing in the United States and Canada based on the number of record holders and individual participants in security position listings.

Dividend Policy

The Company has never declared or paid cash dividends on its Common Stock. The Company presently intends to retain cash for the operation and development of its business and does not anticipate paying cash dividends in the foreseeable future. A future determination as to the payment of dividends will depend on a number

8

of factors, including future earnings, capital requirements, the financial condition and prospects of the Company and such other factors as the Board of Directors of the Company deems relevant.

Shares Subject to Options

In July 2001 the Company adopted the 2001 Stock Option Plan (“the Plan”) that authorized the issuance of up to 1,142,857 (8,000,000 prior to the November 2001 7-for-1 consolidation of the Company’s common shares) of common shares under the Plan. The shareholders approved subsequent amendments to increase the authorized shares under the Plan, including the July 2005 amendment of the Plan to increase the number of shares reserved for issuance from 7,000,000 to 9,000,000. As of January 31, 2006, the Company has outstanding options to purchase 7,954,643 common shares at prices from $0.18 to $2.00.

| Equity Compensation Plan Information as of January 31, 2006 | |||||||

Plan Category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | ||||

|---|---|---|---|---|---|---|---|

| (a) | (b) | (c) | |||||

| Equity compensation | |||||||

| plans approved by | |||||||

| security holders | 7,954,643 | $1.33 | 1,045,357 | ||||

| Equity compensation | |||||||

| plans not approved by | |||||||

| security holders | -0- | N/A | -0- | ||||

| Total | 7,954,643 | $1.33 | 1,045,357 | ||||

Foreign Controls

The Company is not aware of governmental laws, decrees or regulations in Canada restricting the import or export of capital or affecting the remittance to the United States of interest, dividends or other payments to non-resident holders of the Company’s Common Stock. However, the payment or crediting of interest or dividends to United States residents may be subject to applicable withholding taxes at a rate prescribed by the Income Tax Act (Canada) as modified by the provisions of the Canada-United States Income Tax Act (Canada) and as further modified by the provisions of the Canada-United States Income Tax Convention, 1980 (see “Taxation” below).

Except as provided in the Investment Canada Act (the “ICA”), there are no limitations under the laws of Canada, the Province of British Columbia or in the charter and organizational documents of the Company on the right of nonresident or foreigner owners to hold and/or vote the shares of the Company.

The ICA applies when a “non-Canadian” individual or entity or controlled group of entities as defined in the ICA proposes to make an investment to acquire control of a Canadian business enterprise, either directly or indirectly, and by way of purchase of voting shares of a corporation or of substantially all of the assets used in the Canadian business enterprise. An investment in voting shares of a corporation is deemed to be an acquisition of control where more than 50% of the voting shares are acquired. An acquisition of less than one-third of the voting shares of a corporation is deemed not to be an acquisition of control and an acquisition of between one-third and one-half of the voting shares of a corporation is presumed to be an acquisition of control unless it can be established that the acquisition does not in fact result in control of the corporation by the investor.

An investment to acquire control of a Canadian business enterprise, the gross assets of which exceed certain thresholds, must be reviewed and approved under the ICA before implementation. An investment to acquire

9

control of a Canadian business enterprise, the gross asset value of which falls below these threshold amounts, is one in respect of which notification must be given under the ICA although approval is not required prior to implementation of the investment. NAFTA Investors, (i.e.) investors who are nationals, other than Canadian, as defined in the North American Free Trade Agreement, are not considered for the purposes of the ICA to be “non-Canadian”.

Taxation

Dividends. Generally, dividends paid by a Canadian corporation to non-resident shareholders are, under the Income Tax Act (Canada) (the “ITA”), subject to a withholding tax of 25%. However, paragraph 2 of Article X of the Canada-United States Income Tax Convention (1980) (the “Treaty”) provides for the following maximum withholding tax rates:

| a) | 10% of the gross amount of the dividends if the beneficial owner of such dividends is a U.S. resident company which owns at least 10% of the voting stock of the corporation paying the dividends; and |

| b) | 15% of the gross amount of the dividends in all other cases. |

Subject to certain limitations and exceptions, U.S. resident shareholders of a Canadian corporation may be entitled to a credit for all or a portion of such withholding taxes in computing their U.S. federal and possibly their state income tax liability.

Dividends paid by a Canadian corporation to shareholders resident in Canada will not be subject to withholding tax. Any dividends received by a Canadian resident on shares of the Company will be treated for tax purposes as dividends from a taxable Canadian corporation. Accordingly, where a dividend is received by an individual resident in Canada, the individual will be entitled to claim a federal dividend tax credit, equal to 16 2/3% of the dividend. Where the dividend is received by a corporation resident in Canada, the dividend will normally be free of tax under Part I of the ITA but may be subject to refundable tax under Part IV of the ITA.

Disposition of Capital Property. If shares of a Canadian public corporation held by a non-resident shareholder constitute capital property to that shareholder, the disposition of such shares will not be subject to tax under the ITA unless the shares constitute “taxable Canadian property” to the vendor. Where a non-resident shareholder or persons with whom the non-resident shareholder does not deal at arm’s length have, at any time during the five year period immediately preceding the disposition, owned not less than 25% of the issued shares of any class of the capital stock of the public corporation, the shares so disposed of will constitute “taxable Canadian property”. Under the ITA, a disposition of shares that constitute taxable Canadian property will give rise to a capital gain (or a capital loss) equal to the amount by which the proceeds of disposition of such shares, net of any cost of disposition, exceeds (or is less than) the adjusted cost basis of such shares to that investor. Generally, one-half of any capital gain realized by an investor on a disposition or a deemed disposition of such a shares must be included in computing his Canadian income for that year as a taxable capital gain. One-half of any capital loss realized by an investor on a disposition or deemed disposition of such a share in a taxable year may generally be deducted from his Canadian taxable capital gains for that year.

Any gains realized by a non-resident shareholder from the disposition of shares which are taxable Canadian property may be exempt from tax under the ITA by virtue of Article XIII of the Treaty if, at the time of the disposition of the subject shares, the value thereof was derived principally from something other than direct or indirect real property interests situated in Canada.

Under the ITA, the disposition of a share by an investor may occur or be deemed to occur in a number of circumstances including on a sale or gift of such share or upon the death of that investor.

The initial adjusted cost base of a share to an investor will be the cost to him of that share. Under the ITA, certain addition or reduction adjustments may be required to be made to the cost base of a share. The adjusted cost base of each common share of a corporation owned by an investor at any particular time will be the average adjusted cost base to him of all common shares of that corporation owned at that time.

10

Subject to certain limitations and exceptions, U.S. resident shareholders of a Canadian corporation may be entitled to a credit for all or a portion of any capital gain taxation in computing their U.S. federal and possibly their state income tax liability.

In general, the disposition by a shareholder resident in Canada of the capital stock in a Canadian corporation will be subject to Canadian income taxation in the same manner as rules described above relating to a disposition of share which constitutes taxable Canadian property. A shareholder resident in Canada may, however, be entitled to a capital gains exemption. The ITA provides, for residents of Canada, a cumulative lifetime exemption from income tax of $100,000 of qualifying net capital gains.

Disposition of Non-Capital Property. If the shares of a Canadian public corporation held by a non-resident do not constitute capital property to that shareholder, any gains realized from the disposition thereof will be fully taxable under the ITA if their disposition arises in the course of a business carried on by the shareholder in Canada. Under the ITA, a shareholder will be deemed to carry on business in Canada in respect of particular shares if he offers them for sale in Canada through an agent, including the TSX Venture Exchange. Under the Treaty, any business profits derived by a U.S. resident shareholder of a Canadian public corporation from the disposition of the subject corporation’s shares will only be taxable in Canada to the extent that such profits are attributable to a permanent establishment of the shareholder in Canada.

The foregoing discussion is a summary of certain tax considerations which may be relevant to stockholders of the Company, but it is not intended as a substitute for personal tax planning and professional tax advice.

U.S. Federal Income Tax Consequences

The following is a summary of certain material U.S. federal income tax consequences to a U.S. Holder (as defined below) arising from and relating to the acquisition, ownership, and disposition of Common Stock.

This summary is for general information purposes only and does not purport to be a complete analysis or listing of all potential U.S. federal income tax consequences that may apply to a U.S. Holder as a result of the acquisition, ownership, and disposition of Common Stock. In addition, this summary does not take into account the individual facts and circumstances of any particular U.S. Holder that may affect the U.S. federal income tax consequences of the acquisition, ownership, and disposition of Common Stock. Accordingly, this summary is not intended to be, and should not be construed as, legal or U.S. federal income tax advice with respect to any U.S. Holder. Each U.S. Holder should consult its own tax advisor regarding the U.S. federal income, U.S. state and local, and foreign tax consequences of the acquisition, ownership, and disposition of Common Stock.

Scope of this Summary

Authorities

This summary is based on the Internal Revenue Code of 1986, as amended (the “Code”), Treasury Regulations (whether final, temporary, or proposed), published rulings of the Internal Revenue Service (the “IRS”), published administrative positions of the IRS, the Convention Between Canada and the United States of America with Respect to Taxes on Income and on Capital, signed September 26, 1980, as amended (the “Canada-U.S. Tax Convention”), and U.S. court decisions that are applicable and, in each case, as in effect and available, as of the date of this Annual Report. Any of the authorities on which this summary is based could be changed in a material and adverse manner at any time, and any such change could be applied on a retroactive basis. This summary does not discuss the potential effects, whether adverse or beneficial, of any proposed legislation that, if enacted, could be applied on a retroactive basis.

11

U.S. Holders

For purposes of this summary, a “U.S. Holder” is a beneficial owner of Common Stock that, for U.S. federal income tax purposes, is (a) an individual who is a citizen or resident of the U.S., (b) a corporation, or any other entity classified as a corporation for U.S. federal income tax purposes, that is created or organized in or under the laws of the U.S., any state in the U.S., or the District of Columbia, (c) an estate if the income of such estate is subject to U.S. federal income tax regardless of the source of such income, or (d) a trust if (i) such trust has validly elected to be treated as a U.S. person for U.S. federal income tax purposes or (ii) a U.S. court is able to exercise primary supervision over the administration of such trust and one or more U.S. persons have the authority to control all substantial decisions of such trust.

Non-U.S. Holders

For purposes of this summary, a “non-U.S. Holder” is a beneficial owner of Common Stock other than a U.S. Holder. This summary does not address the U.S. federal income tax consequences of the acquisition, ownership, and disposition of Common Stock to non-U.S. Holders. Accordingly, a non-U.S. Holder should consult its own tax advisor regarding the U.S. federal income, U.S. state and local, and foreign tax consequences (including the potential application of and operation of any income tax treaties) of the acquisition, ownership, and disposition of Common Stock.

U.S. Holders Subject to Special U.S. Federal Income Tax Rules Not Addressed

This summary does not address the U.S. federal income tax consequences of the acquisition, ownership, and disposition of Common Stock to U.S. Holders that are subject to special provisions under the Code, including the following U.S. Holders: (a) U.S. Holders that are tax-exempt organizations, qualified retirement plans, individual retirement accounts, or other tax-deferred accounts; (b) U.S. Holders that are financial institutions, insurance companies, real estate investment trusts, or regulated investment companies; (c) U.S. Holders that are dealers in securities or currencies or U.S. Holders that are traders in securities that elect to apply a mark-to-market accounting method; (d) U.S. Holders that have a “functional currency” other than the U.S. dollar; (e) U.S. Holders that are liable for the alternative minimum tax under the Code; (f) U.S. Holders that own Common Stock as part of a straddle, hedging transaction, conversion transaction, constructive sale, or other arrangement involving more than one position; (g) U.S. Holders that acquired Common Stock in connection with the exercise of employee stock options or otherwise as compensation for services; (h) U.S. Holders that hold Common Stock other than as a capital asset within the meaning of Section 1221 of the Code; or (i) U.S. Holders that own (directly, indirectly, or constructively) 10% or more of the total combined voting power of all classes of shares of the Company entitled to vote. U.S. Holders that are subject to special provisions under the Code, including U.S. Holders described immediately above, should consult their own tax advisors regarding the U.S. federal income tax consequences of the acquisition, ownership, and disposition of Common Stock.

If an entity that is classified as a partnership for U.S. federal income tax purposes holds Common Stock, the U.S. federal income tax consequences of the acquisition, ownership, and disposition of Common Stock to such partnership and the partners of such partnership generally will depend on the activities of the partnership and the status of such partners. Partners of entities that are classified as partnerships for U.S. federal income tax purposes should consult their own tax advisors regarding the U.S. federal income tax consequences of the acquisition, ownership, and disposition of Common Stock.

Tax Consequences Other than U.S. Federal Income Tax Consequences Not Addressed

This summary does not address the U.S. state and local, U.S. federal estate and gift, or foreign tax consequences to U.S. Holders of the acquisition, ownership, and disposition of Common Stock. Each U.S. Holder should consult its own tax advisor regarding the U.S. state and local, U.S. federal estate and gift, and foreign tax consequences of the acquisition, ownership, and disposition of Common Stock.

12

U.S. Federal Income Tax Consequences of the Acquisition, Ownership, and Disposition of Common Stock

Distributions on Common Stock

| General Taxation of Distributions |

Subject to the “passive foreign investment company” rules discussed below, a U.S. Holder that receives a distribution, including a constructive distribution, with respect to the Common Stock will be required to include the amount of such distribution in gross income as a dividend (without reduction for any Canadian income tax withheld from such distribution) to the extent of the current or accumulated “earnings and profits” of the Company. To the extent that a distribution exceeds the current and accumulated “earnings and profits” of the Company, such distribution will be treated (a) first, as a tax-free return of capital to the extent of a U.S. Holder’s tax basis in the Common Stock and, (b) thereafter, as gain from the sale or exchange of such Common Stock. (See “Disposition of Common Stock” below).

| Reduced Tax Rates for Certain Dividends |

For taxable years beginning after December 31, 2002 and before January 1, 2009, a dividend paid by the Company generally will be taxed at the preferential tax rates applicable to long-term capital gains if (a) the Company is a “qualified foreign corporation” (as defined below), (b) the U.S. Holder receiving such dividend is an individual, estate, or trust, and (c) such dividend is paid on Common Stock that have been held by such U.S. Holder for at least 61 days during the 121-day period beginning 60 days before the “ex-dividend date.”

The Company generally will be a “qualified foreign corporation” under Section 1(h)(11) of the Code (a “QFC”) if (a) the Company is incorporated in a possession of the U.S., (b) the Company is eligible for the benefits of the Canada-U.S. Tax Convention, or (c) the Common Stock is readily tradable on an established securities market in the U.S. However, even if the Company satisfies one or more of such requirements, the Company will not be treated as a QFC if the Company is a “passive foreign investment company” (as defined below) for the taxable year during which the Company pays a dividend or for the preceding taxable year. In 2003, the U.S. Department of the Treasury (the “Treasury”) and the IRS announced that they intended to issue Treasury Regulations providing procedures for a foreign corporation to certify that it is a QFC. Although these Treasury Regulations have not yet been issued, the Treasury and the IRS have confirmed their intention to issue these Treasury Regulations. It is expected that these Treasury Regulations will obligate persons required to file information returns to report a dividend paid by a foreign corporation as a dividend from a QFC if the foreign corporation has, among other things, certified under penalties of perjury that the foreign corporation was not a “passive foreign investment company” for the taxable year during which the foreign corporation paid the dividend or for the preceding taxable year.

As discussed below, the Company believes that it was a “passive foreign investment company” for the taxable year ended January 31, 2006, and expects that it will be a “passive foreign investment company” for the taxable year ending January 31, 2007. (See “Additional Rules that May Apply to U.S. Holders—Passive Foreign Investment Company” below). Accordingly, the Company does not expect to be a QFC for the taxable year ending January 31, 2007.

If the Company is not a QFC, a dividend paid by the Company to a U.S. Holder, including a U.S. Holder that is an individual, estate, or trust, generally will be taxed at ordinary income tax rates (and not at the preferential tax rates applicable to long-term capital gains). The dividend rules are complex, and each U.S. Holder should consult its own tax advisor regarding the dividend rules.

| Distributions Paid in Foreign Currency |

The amount of a distribution received on the Common Stock in foreign currency generally will be equal to the U.S. dollar value of such distribution based on the exchange rate applicable on the date of receipt. A U.S. Holder that does not convert foreign currency received as a distribution into U.S. dollars on the date of receipt generally will have a tax basis in such foreign currency equal to the U.S. dollar value of such foreign currency on the

13

date of receipt. Such a U.S. Holder generally will recognize ordinary income or loss on the subsequent sale or other taxable disposition of such foreign currency (including an exchange for U.S. dollars).

| Dividends Received Deduction |

Dividends received on the Common Stock generally will not be eligible for the “dividends received deduction.” The availability of the dividends received deduction is subject to complex limitations that are beyond the scope of this summary, and a U.S. Holder that is a corporation should consult its own tax advisor regarding the dividends received deduction.

Disposition of Common Stock

A U.S. Holder will recognize gain or loss on the sale or other taxable disposition of Common Stock in an amount equal to the difference, if any, between (a) the amount of cash plus the fair market value of any property received and (b) such U.S. Holder’s adjusted tax basis in the Common Stock sold or otherwise disposed of. Subject to the “passive foreign investment company” rules discussed below, any such gain or loss generally will be capital gain or loss, which will be long-term capital gain or loss if the Common Stock is held for more than one year.

Preferential tax rates apply to long-term capital gains of a U.S. Holder that is an individual, estate, or trust. There are currently no preferential tax rates for long-term capital gains of a U.S. Holder that is a corporation. Deductions for capital losses are subject to significant limitations under the Code.

Foreign Tax Credit

A U.S. Holder that pays (whether directly or through withholding) Canadian income tax with respect to dividends received on the Common Stock generally will be entitled, at the election of such U.S. Holder, to receive either a deduction or a credit for such Canadian income tax paid. Generally, a credit will reduce a U.S. Holder’s U.S. federal income tax liability on a dollar-for-dollar basis, whereas a deduction will reduce a U.S. Holder’s income subject to U.S. federal income tax. This election is made on a year-by-year basis and applies to all foreign taxes paid (whether directly or through withholding) by a U.S. Holder during a taxable year.

Complex limitations apply to the foreign tax credit, including the general limitation that the credit cannot exceed the proportionate share of a U.S. Holder’s U.S. federal income tax liability that such U.S. Holder’s “foreign source” taxable income bears to such U.S. Holder’s worldwide taxable income. In applying this limitation, a U.S. Holder’s various items of income and deduction must be classified, under complex rules, as either “foreign source” or “U.S. source.” In addition, this limitation is calculated separately with respect to specific categories of income (including “passive income,” “high withholding tax interest,” “financial services income,” “general income,” and certain other categories of income). Gain or loss recognized by a U.S. Holder on the sale or other taxable disposition of Common Stock generally will be treated as “U.S. source” for purposes of applying the foreign tax credit rules. Dividends received on the Common Stock generally will be treated as “foreign source” and generally will be categorized as “passive income” or, in the case of certain U.S. Holders, “financial services income” for purposes of applying the foreign tax credit rules. However, for taxable years beginning after December 31, 2006, the foreign tax credit limitation categories are reduced to “passive category income” and “general category income” (and the other categories of income, including “financial services income,” are eliminated). The foreign tax credit rules are complex, and each U.S. Holder should consult its own tax advisor regarding the foreign tax credit rules.

Information Reporting; Backup Withholding Tax

Payments made within the U.S., or by a U.S. payor or U.S. middleman, of dividends on, or proceeds arising from the sale or other taxable disposition of, Common Stock generally will be subject to information reporting and backup withholding tax, at the rate of 28%, if a U.S. Holder (a) fails to furnish such U.S. Holder’s correct U.S. taxpayer identification number (generally on Form W-9), (b) furnishes an incorrect U.S. taxpayer identification number, (c) is notified by the IRS that such U.S. Holder has previously failed to properly report items subject to backup withholding tax, or (d) fails to certify, under penalty of perjury, that such U.S. Holder has furnished its

14

correct U.S. taxpayer identification number and that the IRS has not notified such U.S. Holder that it is subject to backup withholding tax. However, U.S. Holders that are corporations generally are excluded from these information reporting and backup withholding tax rules. Any amounts withheld under the U.S. backup withholding tax rules will be allowed as a credit against a U.S. Holder’s U.S. federal income tax liability, if any, or will be refunded, if such U.S. Holder furnishes required information to the IRS. Each U.S. Holder should consult its own tax advisor regarding the information reporting and backup withholding tax rules.

Additional Rules that May Apply to U.S. Holders

If the Company is a “controlled foreign corporation” or a “passive foreign investment company” (each as defined below), the preceding sections of this summary may not describe the U.S. federal income tax consequences to a U.S. Holder of the acquisition, ownership, and disposition of Common Stock.

Controlled Foreign Corporation

The Company generally will be a “controlled foreign corporation” under Section 957(a) of the Code (a “CFC”) if more than 50% of the total voting power or the total value of the outstanding shares of the Company is owned, directly or indirectly, by citizens or residents of the U.S., domestic partnerships, domestic corporations, domestic estates, or domestic trusts (each as defined in Section 7701(a)(30) of the Code), each of which own, directly or indirectly, 10% or more of the total voting power of the outstanding shares of the Company (a “10% Shareholder”).

If the Company is a CFC, a 10% Shareholder generally will be subject to current U.S. federal income tax with respect to (a) such 10% Shareholder’s pro rata share of the “subpart F income” (as defined in Section 952 of the Code) of the Company and (b) such 10% Shareholder’s pro rata share of the earnings of the Company invested in “United States property” (as defined in Section 956 of the Code). In addition, under Section 1248 of the Code, any gain recognized on the sale or other taxable disposition of Common Stock by a U.S. Holder that was a 10% Shareholder at any time during the five-year period ending with such sale or other taxable disposition generally will be treated as a dividend to the extent of the “earnings and profits” of the Company that are attributable to such Common Stock. If the Company is both a CFC and a “passive foreign investment company” (as defined below), the Company generally will be treated as a CFC (and not as a “passive foreign investment company”) with respect to any 10% Shareholder.

The Company does not believe that it has previously been, or currently is, a CFC. However, there can be no assurance that the Company will not be a CFC for the current or any subsequent taxable year.

Passive Foreign Investment Company

The Company generally will be a “passive foreign investment company” under Section 1297(a) of the Code (a “PFIC”) if, for a taxable year, (a) 75% or more of the gross income of the Company for such taxable year is passive income or (b) on average, 50% or more of the assets held by the Company either produce passive income or are held for the production of passive income, based on the fair market value of such assets (or on the adjusted tax basis of such assets, if the Company is not publicly traded and either is a “controlled foreign corporation” or makes an election). “Passive income” includes, for example, dividends, interest, certain rents and royalties, certain gains from the sale of stock and securities, and certain gains from commodities transactions. However, for transactions entered into after December 31, 2004, active business gains arising from the sale or exchange of commodities by the Company generally are excluded from “passive income” if substantially all of the Company’s commodities are (a) stock in trade of the Company or other property of a kind that would properly be included in inventory of the Company, or property held by the Company primarily for sale to customers in the ordinary course of business, (b) property used in the trade or business of the Company that would be subject to the allowance for depreciation under section 167 of the Code, or (c) supplies of a type regularly used or consumed by the Company in the ordinary course of its trade or business.

15

For purposes of the PFIC income test and asset test described above, if the Company owns, directly or indirectly, 25% or more of the total value of the outstanding shares of another foreign corporation, the Company will be treated as if it (a) held a proportionate share of the assets of such other foreign corporation and (b) received directly a proportionate share of the income of such other foreign corporation. In addition, for purposes of the PFIC income test and asset test described above, “passive income” does not include any interest, dividends, rents, or royalties that are received or accrued by the Company from a “related person” (as defined in Section 954(d)(3) of the Code), to the extent such items are properly allocable to the income of such related person that is not passive income.

The Company believes that it was a PFIC for the taxable year ended January 31, 2006, and expects that it will be a PFIC for the taxable year ending January 31, 2007. The determination of whether the Company was, or will be, a PFIC for a taxable year depends, in part, on the application of complex U.S. federal income tax rules, which are subject to various interpretations. In addition, whether the Company will be a PFIC for the taxable year ending January 31, 2007 and each subsequent taxable year depends on the assets and income of the Company over the course of each such taxable year and, as a result, cannot be predicted with certainty as of the date of this Annual Report. Accordingly, there can be no assurance that the IRS will not challenge the determination made by the Company concerning its PFIC status or that the Company was not, or will not be, a PFIC for any taxable year.

| Default PFIC Rules Under Section 1291 of the Code |

If the Company is a PFIC, the U.S. federal income tax consequences to a U.S. Holder of the acquisition, ownership, and disposition of Common Stock will depend on whether such U.S. Holder makes an election to treat the Company as a “qualified electing fund” or “QEF” under Section 1295 of the Code (a “QEF Election”) or a mark-to-market election under Section 1296 of the Code (a “Mark-to-Market Election”). A U.S. Holder that does not make either a QEF Election or a Mark-to-Market Election will be referred to in this summary as a “Non-Electing U.S. Holder.”

A Non-Electing U.S. Holder will be subject to the rules of Section 1291 of the Code with respect to (a) any gain recognized on the sale or other taxable disposition of Common Stock and (b) any excess distribution received on the Common Stock. A distribution generally will be an “excess distribution” to the extent that such distribution (together with all other distributions received in the current taxable year) exceeds 125% of the average distributions received during the three preceding taxable years (or during a U.S. Holder’s holding period for the Common Stock, if shorter).

Under Section 1291 of the Code, any gain recognized on the sale or other taxable disposition of Common Stock, and any excess distribution received on the Common Stock, must be ratably allocated to each day in a Non-Electing U.S. Holder’s holding period for the Common Stock. The amount of any such gain or excess distribution allocated to prior years of such Non-Electing U.S. Holder’s holding period for the Common Stock (other than years prior to the first taxable year of the Company beginning after December 31, 1986 for which the Company was not a PFIC) will be subject to U.S. federal income tax at the highest tax rate applicable to ordinary income in each such prior year. A Non-Electing U.S. Holder will be required to pay interest on the resulting tax liability for each such prior year, calculated as if such tax liability had been due in each such prior year. Such a Non-Electing U.S. Holder that is not a corporation must treat any such interest paid as “personal interest,” which is not deductible. The amount of any such gain or excess distribution allocated to the current year of such Non-Electing U.S. Holder’s holding period for the Common Stock will be treated as ordinary income in the current year, and no interest charge will be incurred with respect to the resulting tax liability for the current year.

If the Company is a PFIC for any taxable year during which a Non-Electing U.S. Holder holds Common Stock, the Company will continue to be treated as a PFIC with respect to such Non-Electing U.S. Holder, regardless of whether the Company ceases to be a PFIC in one or more subsequent taxable years. A Non-Electing U.S. Holder may terminate this deemed PFIC status by electing to recognize gain (which will be taxed under the rules of Section 1291 of the Code discussed above) as if such Common Stock were sold on the last day of the last taxable year for which the Company was a PFIC.

16

| QEF Election |

The procedure for making a QEF Election, and the U.S. federal income tax consequences of making a QEF Election, will depend on whether such QEF Election is timely. A QEF Election generally will be “timely” if it is made for the first year in a U.S. Holder’s holding period for the Common Stock in which the Company is a PFIC. In this case, a U.S. Holder may make a timely QEF Election by filing the appropriate QEF Election documents with such U.S. Holder’s U.S. federal income tax return for such first year. However, if the Company was a PFIC in a prior year in a U.S. Holder’s holding period for the Common Stock, then in order to be treated as making a “timely” QEF Election, such U.S. Holder must elect to recognize gain (which will be taxed under the rules of Section 1291 of the Code discussed above) as if the Common Stock were sold on the qualification date for an amount equal to the fair market value of the Common Stock on the qualification date. The “qualification date” is the first day of the first taxable year in which the Company was a QEF with respect to such U.S. Holder. In addition, under very limited circumstances, a U.S. Holder may make a retroactive QEF Election if such U.S. Holder failed to file the QEF Election documents in a timely manner.

A QEF Election will apply to the taxable year for which such QEF Election is made and to all subsequent taxable years, unless such QEF Election is invalidated or terminated or the IRS consents to revocation of such QEF Election. If a U.S. Holder makes a QEF Election and, in a subsequent taxable year, the Company ceases to be a PFIC, the QEF Election will remain in effect (although it will not be applicable) during those taxable years in which the Company is not a PFIC. Accordingly, if the Company becomes a PFIC in another subsequent taxable year, the QEF Election will be effective and the U.S. Holder will be subject to the QEF rules described above during any such subsequent taxable year in which the Company qualifies as a PFIC. In addition, the QEF Election will remain in effect (although it will not be applicable) with respect to a U.S. Holder even after such U.S. Holder disposes of all of such U.S. Holder’s direct and indirect interest in the Common Stock. Accordingly, if such U.S. Holder reacquires an interest in the Company, such U.S. Holder will be subject to the QEF rules described above for each taxable year in which the Company is a PFIC.

A U.S. Holder that makes a timely QEF Election generally will not be subject to the rules of Section 1291 of the Code discussed above. For example, a U.S. Holder that makes a timely QEF Election generally will recognize capital gain or loss on the sale or other taxable disposition of Common Stock.

However, for each taxable year in which the Company is a PFIC, a U.S. Holder that makes a QEF Election will be subject to U.S. federal income tax on such U.S. Holder’s pro rata share of (a) the net capital gain of the Company, which will be taxed as long-term capital gain to such U.S. Holder, and (b) and the ordinary earnings of the Company, which will be taxed as ordinary income to such U.S. Holder. Generally, “net capital gain” is the excess of (a) net long-term capital gain over (b) net short-term capital loss, and “ordinary earnings” are the excess of (a) “earnings and profits” over (b) net capital gain. A U.S. Holder that makes a QEF Election will be subject to U.S. federal income tax on such amounts for each taxable year in which the Company is a PFIC, regardless of whether such amounts are actually distributed to such U.S. Holder by the Company. However, a U.S. Holder that makes a QEF Election may, subject to certain limitations, elect to defer payment of current U.S. federal income tax on such amounts, subject to an interest charge. If such U.S. Holder is not a corporation, any such interest paid will be treated as “personal interest,” which is not deductible.

A U.S. Holder that makes a QEF Election generally (a) may receive a tax-free distribution from the Company to the extent that such distribution represents “earnings and profits” of the Company that were previously included in income by the U.S. Holder because of such QEF Election and (b) will adjust such U.S. Holder’s tax basis in the Common Stock to reflect the amount included in income or allowed as a tax-free distribution because of such QEF Election.

Each U.S. Holder should consult its own tax advisor regarding the availability of, and procedure for making, a QEF Election. U.S. Holders should be aware that there can be no assurance that the Company will satisfy record keeping requirements that apply to a QEF, or that the Company will supply U.S. Holders with information that such U.S. Holders require to report under the QEF rules, in the event that the Company is a PFIC and a U.S. Holder wishes to make a QEF Election.

17

| Mark-to-Market Election |

A U.S. Holder may make a Mark-to-Market Election only if the Common Stock is marketable stock. The Common Stock generally will be “marketable stock” if the Common Stock is regularly traded on a qualified exchange or other market. For this purpose, a “qualified exchange or other market” includes (a) a national securities exchange that is registered with the Securities and Exchange Commission, (b) the national market system established pursuant to section 11A of the Securities and Exchange Act of 1934, or (c) a foreign securities exchange that is regulated or supervised by a governmental authority of the country in which the market is located, provided that (i) such foreign exchange has trading volume, listing, financial disclosure, surveillance, and other requirements designed to prevent fraudulent and manipulative acts and practices, remove impediments to and perfect the mechanism of a free, open, fair, and orderly market, and protect investors (and the laws of the country in which the foreign exchange is located and the rules of the foreign exchange ensure that such requirements are actually enforced) and (ii) the rules of such foreign exchange effectively promote active trading of listed stocks. If the Common Stock is traded on such a qualified exchange or other market, the Common Stock generally will be “regularly traded” for any calendar year during which the Common Stock is traded, other than in de minimis quantities, on at least 15 days during each calendar quarter.

A Mark-to-Market Election applies to the taxable year in which such Mark-to-Market Election is made and to each subsequent taxable year, unless the Common Stock cease to be “marketable stock” or the IRS consents to revocation of such election. Each U.S. Holder should consult its own tax advisor regarding the availability of, and procedure for making, a Mark-to-Market Election.

A U.S. Holder that makes a Mark-to-Market Election generally will not be subject to the rules of Section 1291 of the Code discussed above. However, if a U.S. Holder makes a Mark-to-Market Election after the beginning of such U.S. Holder’s holding period for the Common Stock and such U.S. Holder has not made a timely QEF Election, the rules of Section 1291 of the Code discussed above will apply to certain dispositions of, and distributions on, the Common Stock.

A U.S. Holder that makes a Mark-to-Market Election will include in ordinary income, for each taxable year in which the Company is a PFIC, an amount equal to the excess, if any, of (a) the fair market value of the Common Stock as of the close of such taxable year over (b) such U.S. Holder’s adjusted tax basis in such Common Stock. A U.S. Holder that makes a Mark-to-Market Election will be allowed a deduction in an amount equal to the lesser of (a) the excess, if any, of (i) such U.S. Holder’s adjusted tax basis in the Common Stock over (ii) the fair market value of such Common Stock as of the close of such taxable year or (b) the excess, if any, of (i) the amount included in ordinary income because of such Mark-to-Market Election for prior taxable years over (ii) the amount allowed as a deduction because of such Mark-to-Market Election for prior taxable years.