UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended January 31, 2009

Commission file number: 0-21968

BRAZAURO RESOURCES CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

British Columbia (State or Other Jurisdiction of Incorporation or Organization) | 76-0195574 (I.R.S. Employer Identification No.) |

|

|

16360 Park Ten Place, Suite 217

Houston, TX 77084

(Address of Principal Executive Offices, including Zip Code)

Brian C. Irwin, (281) 579-3400, bcirwin@shaw.ca / (281) 579-9799,

771 Mariner Way, Parksville, B.C., Canada V9P 1S4

(Name, Telephone, E-mail and /or Facsimile number and Address of Company Contact Person)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class None | Name of Exchange on Which Registered None |

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class

COMMON STOCK

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as January 31, 2009: 85,237,621 Common Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o | No x |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o | No x |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x | No o |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site , if any, every Interactive Data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T ( 232.405 of this chapter) during the preceding 12 months (or for such shorter period the the resgistrant was required to submit and post such files).

Yes o | No o |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer x |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP o | International Financial Reporting Standards as issued | Other x |

| by the International Accounting Standards Board | o |

Indicate by check mark which financial statement item the registrant has elected to follow: | x Item 17 | o Item 18 |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes | Yes o No x |

BRAZAURO RESOURCES CORPORATION

FORM 20-F

TABLE OF CONTENTS

Item | Page |

Number | Number |

Item 1. | Identity of Directors, Senior Management and Advisers | 1 |

Item 2. | Offer Statistics and Expected Timetable | 1 |

Item 3. | Key Information | 1 |

Item 4. | Information on the Company | 5 |

Item 4A. | Unresolved Staff Comments | 11 |

Item 5. | Operating and Financial Review and Prospects | 11 |

Item 6. | Directors, Senior Management and Employees | 17 |

Item 7. | Major Shareholders and Related Party Transactions | 26 |

Item 8. | Financial Information | 28 |

Item 9. | The Offer and Listing | 28 |

Item 10. | Additional Information | 30 |

Item 11. | Quantitative and Qualitative Disclosures About Market Risk | 40 |

Item 12. | Descriptions of Securities Other than Equity Securities | 41 |

PART II

Item 13. | Defaults, Dividend Arrearages and Delinquencies | 42 |

Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 42 |

Item 15T. | Controls and Procedures | 42 |

Item 16A. | Audit Committee Financial Expert | 43 |

Item 16B. | Code of Ethics | 43 |

Item 16C. | Principal Accountant Fees and Services | 43 |

Item 16D. | Exemptions from the Listing Standards for Audit Committees | 44 |

Item 16E. | Purchase of Equity Securities by the Issuer and Affiliated Purchasers | 44 |

Item 16F. | Change in Registrant’s Certifying Account | 44 |

Item 16G. | Corporate Governance | 44 |

PART III

Item 17. | Financial Statements | 44 |

Item 18. | Financial Statements | 45 |

Item 19. | Exhibits | 45 |

Signatures | 46 |

i

Item 1. | Identity of Directors, Senior Management and Advisors |

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934, and as such, there is no requirement to provide any information under this item.

Item 2. | Offer Statistics and Expected Timetable |

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934, and as such, there is no requirement to provide any information under this item.

Item 3. | Key Information |

A. Selected Financial Data

The selected consolidated financial information set forth below for each of the five years ended January 31, 2005, 2006, 2007, 2008 and 2009 has been derived from the consolidated financial statements of Brazauro Resources Corporation (“the Company”) for the years indicated and is expressed in Canadian dollars. The selected consolidated financial information should be read in conjunction with the discussion in “Item 5. Operating and Financial Review and Prospects” and the Consolidated Financial Statements and related notes thereto included on pages 47 to 79 herein. References in this Annual Report on Form 20-F to “Notes” are intended to refer to the Notes to the consolidated financial statements included herein.

In this Annual Report on Form 20-F all currency refers to Canadian Dollars (Cdn$) unless indicated otherwise.

Since its formation, the Company’s activities have consisted primarily of acquiring interests in mineral properties, exploration of those properties and acquiring financing for such purposes. Consequently, the selected consolidated financial data may not indicate the Company’s future financial performance.

Selected Consolidated Financial Data

| Fiscal Year Ended January 31 | ||||

| 2009 | 2008 | 2007 | 2006 | 2005 |

| (000’s except for net loss per common share data) | ||||

Operating revenues | - | - | - | - | - |

Write-down of mineral properties | 21 | 685 | 795 | 907 | - |

Net loss for the year | (3,280) | (4,481) | (5,193) | (8,259) | (3,741) |

Basic and diluted net loss per share | (0.04) | (0.06) | (0.10) | (0.17) | (0.10) |

Working capital | 4,586 | 3,005 | 4,518 | 8,611 | 3,296 |

Total assets | 35,315 | 30,640 | 11,330 | 13,498 | 6,482 |

Total liabilities | 1,853 | 2,671 | 412 | 354 | 349 |

Net assets | 33,462 | 27,969 | 10,918 | 13,144 | 6,133 |

Common share capital | 82,106 | 74,807 | 53,729 | 53,433 | 41,536 |

Dividends per share | - | - | - | - | - |

Weighted average shares outstanding | 81,054 | 74,837 | 53,063 | 49,112 | 38,950 |

The consolidated financial statements have been prepared in accordance with generally accepted accounting principles in Canada (“Canadian GAAP”), which differ in certain respects from the principles the Company would have followed had its consolidated financial statements been prepared in accordance with generally accepted accounting principles in the United States (“United States GAAP”). A discussion of differences between Canadian GAAP and United States GAAP is contained in Note 20 to the consolidated financial statements.

1

If the Company had followed United States GAAP, certain items in the consolidated financial statements would have been reported as follow:

Selected Consolidated Financial Data (United States GAAP)

| Fiscal Year Ended January 31 | ||||

| 2009 | 2008 | 2007 | 2006 | 2005 |

| (000’s except for net loss per common share data) | ||||

Operating revenues | - | - | - | - | - |

Write-down of mineral properties |

| 115 | 31 | 109 | - |

Net loss for the year | (6,033) | (6,106) | (6,174) | (9,289) | (5,290) |

Basic and diluted net loss per common share | (0.07) | (0.08) | (0.12) | (0.19) | (0.14) |

Working capital | 4,586 | 3,005 | 4,518 | 8,611 | 3,296 |

Total assets | 27,234 | 25,284 | 7,598 | 10,747 | 4,759 |

Total liabilities | 1,853 | 2,671 | 412 | 354 | 349 |

Net assets | 25,381 | 22,613 | 7,186 | 10,393 | 4,410 |

Common share capital | 82,106 | 74,807 | 53,729 | 53,433 | 41,536 |

Dividends per share | - | - | - | - | - |

Weighted average common shares outstanding | 81,054 | 74,837 | 53,063 | 49,112 | 38,950 |

Exchange Rates

On May 22, 2009, the noon exchange rate for the Canadian dollar against the U.S. dollar according to the Bank of Canada, was $1.00 (Canadian) = U.S. $0.8902. Bank of Canada exchange rates are nominal quotations, not buying or selling rates, and are intended for statistical or analytical purposes. Rates available from financial institutions will differ.

The following table sets forth, for each of the years between 2005 and 2008, additional information with respect to the noon buying rate for $1.00 (Canadian). Such rates are set forth as U.S. dollars per Canadian $1.00 and are based upon the rates quoted by the Federal Reserve Bank of New York. For year 2009 was used the information with respect the noon exchange rate for the Canadian dollar against the U.S. dollar according to the Bank of Canada nominal quote.

Rate | 2009 | 2008 | 2007 | 2006 | 2005 |

Average (1) | 0.9239 | 0.9508 | 0.9419 | 0.8844 | 0.8276 |

(1) The average rate means the average of the exchange rates on the last day of each month during the year.

Canadian/United States Dollar Exchange Rates for the Previous Six Months

| November, 2008 | December, 2008 | January, 2009 | February, 2009 | March, 2009 | April, 2009 |

High | 0.8713 | 0.8423 | 0.8503 | 0.8224 | 0.8202 | 0.8421 |

Low | 0.7721 | 0.7688 | 0.7834 | 0.7855 | 0.7653 | 0.7870 |

2

B. Capitalization and Indebtedness

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934, and as such, there is no requirement to provide any information under this item.

C. Reason for the Offer and Use of Proceeds

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934, and as such, there is no requirement to provide any information under this item.

D. Risk Factors

An investment in the Company’s common shares is highly speculative and subject to a number of risks. Only those investors who can bear the risk of the entire loss of their investment should participate, and an investor should carefully consider the risks described below and the other information that we file with the Securities and Exchange Commission and with Canadian securities regulators before investing in the Company’s common shares. Additional risks that the Company is unaware of or that are currently believed to be immaterial may become important factors that affect the Company’s business. If any of the following risks occur, or if others occur, the Company’s business, operating results and financial condition could be adversely impacted.

The Company’s business plan to acquire additional exploration prospects, continue exploration activities on its current projects, and, if warranted, undertake development and mining operations, is subject to numerous risks and uncertainties, including the following:

Lack of Proven Properties and Development Funds. At this point, all of the Company’s exploration prospects and property interests (collectively the “Properties”) are gold prospects in Brazil, and the Company has no income from operations. While the Company has sufficient funds to complete the exploration phase currently underway, additional funds will likely be necessary in order for the Company to pursue further exploration on its existing properties and to acquire and develop additional exploration prospects. Certain of the Company’s planned expenditures are discretionary and may be increased or decreased based upon funds available to the Company.

As of May 22, 2009, the Company had sufficient cash to fund general and administrative expenses and to complete planned exploration payments during fiscal 2010. As discussed above, the Company will likely be required to raise additional capital for additional exploration activity on its existing properties and acquisition of new exploration prospects subsequent to fiscal 2010. There can be no assurance that additional funds can be raised. See “Item 5. Operating and Financial Review and Prospects”.

Limited Exploration Prospects. The Company’s existing properties are all gold prospects in Brazil. Accordingly, the Company does not have a diversified portfolio of exploration prospects either geographically or by mineral targets. The Company’s operations could be significantly affected by changes in the market price of gold, as the economic viability of the Company’s projects is heavily dependent upon the market price of gold. Additionally, the Company’s projects are subject to the laws of Brazil and can be negatively impacted by the existing laws and regulations of that country, as they apply to mineral exploration, land ownership, royalty interests and taxation, and by any potential changes of such laws and regulations.

Title to Properties. The Company cannot guarantee title to all of its Properties as the Properties may be subject to prior mineral rights applications with priority, prior unregistered agreements or transfers or native land claims, and title may be affected by undetected defects. Certain of the mineral rights held by the Company are held under applications for mineral rights and, until final approval of such applications is received, the Company’s rights to such mineral rights may not materialize and the exact boundaries of the Company’s properties may be subject to adjustment. The Company does not maintain title insurance on its properties.

Environmental Laws. The exploration programs conducted by the Company are subject to national, state and/or local regulations regarding environmental considerations in the jurisdiction where they are located. Most operations involving exploration or production activities are subject to existing laws and regulations relating to exploration and

3

mining procedures, reclamation, safety precautions, employee health and safety, air quality standards, pollution of stream and fresh water sources, odor, noise, dust, and other environmental protection controls adopted by federal, state and local governmental authorities as well as the rights of adjoining property owners. The Company may be required to prepare and present to federal, state or local authorities data pertaining to the effect or impact that any proposed exploration or production of minerals may have upon the environment. All requirements imposed by any such authorities may be costly, time consuming, and may delay commencement or continuation of exploration or production operations. However, at this time, the Company is exploring its Properties and does not anticipate preparing environmental impact statements or assessments until such time as the Company believes one or more of its Properties will prove to be commercially feasible.

Exploration and Development Risks. The business of exploring for minerals and mining involves a high degree of risk. Few properties that are explored are ultimately developed into producing mines. At present, the Company has prepared a preliminary economic assessment of one of the Company’s properties, the Tocantinzinho Property. The remaining property is an early stage exploration prospect and the Company has formed no estimate of a potential ore body. The grade of any ore ultimately mined may differ from that indicated by drilling results. Major expenses may be required to establish ore reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. It is impossible to ensure that the current development programs planned by the Company will result in a profitable commercial mining operation. Mineral deposits and production costs are affected by such factors as environmental permitting regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations and work interruptions.

Competition. The mineral industry is intensely competitive in all its phases. The Company competes with many companies possessing greater financial resources and technical facilities than itself for the acquisition of mineral concessions, claims, leases and other mineral interests as well as for the recruitment and retention of qualified employees.

Political Risk. Properties in which the Company has an interest are located in the Amazon basin in Brazil, which may be of particular interest or sensitivity to one or more interest groups. Consequently, mineral exploration and mining activities in those areas may be affected in varying degrees by political uncertainty, expropriations of property and changes in applicable government policies and regulation such as business laws, environmental laws, native land claims entitlements or procedures and mineral rights and mining laws, affecting the Company’s business in that area. Any changes in regulations or shifts in political conditions are beyond the control or influence of the Company and may adversely affect its business, or if significant enough, may result in the impairment or loss of mineral concessions or other mineral rights, or may make it impossible to continue its mineral exploration and mining activities in such areas.

Potential Dilution to Existing Shareholders. The Company will require additional financing in order to complete full exploration of its mineral properties. The Company anticipates that it will have to sell additional equity securities including, but not limited to, its common stock, share purchase warrants or some form of convertible security. The effect of additional issuances of equity securities will result in dilution to existing shareholders.

Limited Market for Common Shares. The liquidity of the common shares of the Company, or ability of the shareholder to buy or sell the Company’s common stock, may be significantly limited for various unforeseeable periods. The average daily volume of the Company’s shares traded on the TSX Venture Exchange during fiscal 2009 was approximately 115,000 shares. The market price of the Company’s shares has historically fluctuated in a large range, as disclosed in “Item 9 - The Offer and Listing”. The price of the Company’s common shares may be affected by many factors, including adverse change in the Company’s business, a decline in gold price and general economic trends.

Insurance Coverage. Mineral exploration is subject to risks of human injury, environmental and legal liability and loss of assets. The Company may elect not to have insurance for certain risks because of the high premiums associated with insuring those risks or, in some cases, insurance may not be available for certain risks. Occurrence of events for which we are not insured could have a material adverse effect on the Company’s financial position or results of operations.

4

Key Executives. The Company is dependent on the services of key executives, including its Chairman, Mark E. Jones, III, its Director and retired President, Leendert G. Krol, and its Vice President of Exploration, Elton L. S. Pereira. Each of the above individuals has many years of background in the mining industry. The Company may not be able to replace that experience and knowledge with other individuals.

Fluctuations in Foreign Currency Exchange Rates. The Company raises its equity in Canadian dollars and its exploration expenditures are generally denominated in United States dollars. As a result, the Company’s expenditures are subject to foreign currency fluctuations. Foreign currency fluctuations may materially and adversely increase the Company’s operating expenditures and reduce the amount exploration activities that the Company is able to complete with its current capital. The Company does not engage in any hedging or other transactions to protect itself against such currency fluctuations.

Enforcement of Judgments against the Company. The Company is incorporated in the Province of British Columbia, Canada. Certain of our directors and officers live in Canada, and many of the Company’s assets are located in Brazil and Canada. As a result, it may be difficult for investors to effect service of legal process within the United States upon directors and officers who are not United States residents. Also, there is uncertainty as to the enforceability in Canada, in original actions or for enforcement of judgments of U.S. courts, of civil liabilities predicated upon U.S. federal or state securities laws.

Item 4. | Information on the Company |

A. History and Development of the Company

The Company was incorporated under the Company Act (British Columbia) on March 12, 1986 under the name Texas Star Resources Corporation. The Company became a public company in January 1988 when it undertook an initial public offering of its Common Stock in British Columbia, Canada and became listed on the Vancouver Stock Exchange, a predecessor to the TSX Venture Exchange. The Company’s name was amended to Star Resources Corp. in October 1996 and was further amended to Jaguar Resources Corporation in July 2003. In September 2004, the Company’s name was changed to Brazauro Resources Corporation.

The authorized capital of the Company consists of an unlimited amount of shares of common stock without par value (the “Common Stock”), of which 85,237,621 shares were issued and outstanding as of May 22, 2009. The Common Stock of the Company ranks equally as to dividends, voting rights and participation in assets and is traded under the symbol “BZO” on the TSX Venture Exchange.

The Company’s principal office is located at 16360 Park Ten Place, Suite 217, Houston, Texas, U.S.A. 77084, and its phone number is (281) 579-3400. The Company’s website may be found at www.brazauroresources.com.

The Company is engaged in the business of exploring for and, if warranted, developing mineral properties and is concentrating its current acquisition and exploration efforts on those properties which the Company believes have large scale gold potential. From inception and prior to 1988 the Company had limited business activities and through 1993 explored and abandoned several mineral properties. During fiscal 1993, the Company elected to pursue prospects with the potential for commercial diamond production.

The Company completed three acquisitions in fiscal 1993 consistent with its focus on diamond exploration prospects in the United States. During fiscal 1995 through 2003, the Company completed additional acquisitions in the United States and directly managed and funded exploration efforts on certain properties. In fiscal 2003 the Company decided to cease exploration efforts in Arkansas due to disappointing exploration results, and began to pursue mineral exploration prospects, particularly gold prospects in South America.

From fiscal 2003 through the present, the Company has concentrated its efforts on gold prospects in Brazil and currently holds interests in properties located in the Tapajós Gold District of Brazil’s northerly Pará State.

5

Principal Capital Expenditures During The Three Most Recent Fiscal Years

In fiscal 2007, the Company acquired three additional properties in the Tapajós Gold District of Brazil, the Circulo, the Crepori and the Sucuri Properties. Significant exploration activities were conducted at the Company’s Tocantinzinho and Sucuri Properties during fiscal 2007, resulting in the capitalization of acquisition and exploration costs of approximately $930,000 and $1,740,000, respectively. Based on the exploration results to date on the Sucuri Property, the Company has ceased exploration on the project in fiscal 2008. Accordingly, the capitalized exploration costs totaling approximately $710,000 were written off in fiscal 2007. Additionally, the Company conducted limited exploration activities on the Batalha Property in fiscal 2007 prior to abandoning the project and writing off the capitalized costs totaling approximately $70,000.

In February 2007, the Company completed the acquisition of certain mineral rights to the Tocantinzinho Property via the acquisition of the following three corporations. The Company acquired Resource Holdings 2004 Inc. (“RH 2004”, a British Virgin Islands corporation), and its subsidiary, Empresa Internacional de Mineração do Brasil Ltda. (“EIMB”, a Brazil corporation), in exchange for the issuance of 13,150,000 common shares of the Company and the payment of $50,000 (U.S.) to a third party. Additionally, the Company acquired Mineração Cachambix Ltda. (“Cachambix”, a Brazil corporation) from third parties upon payment of $850,000 (U.S.) and two future payments of $1,000,000 (U.S.) each, due and paid in February 2008 and 2009.

In fiscal 2008, the Company performed additional exploration activities at the Tocantinzinho Properties, resulting in the capitalization of approximately $1,623,000 in exploration expenditures in addition to the capitalization of acquisition costs totaling approximately $17,902,000 and primarily related to the acquisition discussed in the preceding paragraph. At the Company’s Crepori Property, exploration activities including soil sampling and a diamond drilling program were completed. Based upon the results of the exploration, the Company elected to terminate the option agreement at Crepori in April 2008. Accordingly, the capitalized acquisition and exploration costs totaling approximately $577,000 were written off in fiscal 2008.

In fiscal 2009, the Company performed additional exploration activities at the Tocantinzinho and Circulo Properties, resulting in the capitalization of approximately $2,122,000 and $520,000, respectively, in exploration expenditures in addition to the capitalization of acquisition costs totaling approximately $154,000 and $38,000, respectively. At the Company’s Crepori Property, additional exploration costs totaling approximately $21,000 were written off in fiscal 2009.

In July 2008, the Company entered into an option agreement under which it may acquire the mineral rights to the 20,688 hectare Piranha Property, located in Pará State. The Company has an option to earn 100% of the Piranha Property, with no residual production royalty obligations, by payment of a total of $1,800,000 (Brazilian Reals) over three years. Exploration activities were conducted at the Company’s Piranha Property during fiscal 2009, resulting in the capitalization of acquisition and exploration costs of approximately $12,000 and $83,000, respectively

6

B. Business Overview

The Company is engaged in the business of exploring for and, if warranted, developing mineral properties and is concentrating its current acquisition and exploration efforts on those properties which the Company believes have large scale gold potential. The Company holds interests in properties located in the Tapajós Gold District of Brazil’s northerly Pará State.

The Company’s mission is to discover and outline significant gold mineralization at its projects to bring on a major mining partner for development of its Properties. Upon acquisition of an exploration property, the Company typically performs geologic evaluation and exploration efforts to determine if the project warrants further work including, but not limited to geologic mapping and sampling, geophysical surveys, and drilling. The Company will continue to pursue mineral exploration prospects, focusing on the Tapajós and on a worldwide basis as opportunities arise, subject to adequate acquisition and exploration funding.

The Tapajós Gold District has a rich history of alluvial gold production. During the 1970’s and 1980’s, the Tapajós area annually produced approximately 30% to 40% of Brazil’s total gold output. Geologically, the Tapajós region is situated within the gold-productive, Archaean to Middle Proterozoic-aged Brazilian Shield that extends from Brazil through Guyana and into Venezuela. In the immediate area of the Company’s projects, granitic basement rocks are intruded by subvolcanic andesitic and rhyolitic bodies, all of lower Proterozoic age. The widespread alluvial gold deposits point to the area’s strong bedrock exploration potential.

The Company is subject to regulation by the Federal mineral land agency in Brazil, the Departamento Nacional de Produção Mineral (“DNPM”). The Company’s holds exploration licenses or applications for exploration licenses granted by the DNPM for the Tocantinzinho and the Circulo Properties. Certain of the licenses for the Tocantinzinho Property are subject to periodic requirements for renewal, and the Company anticipates receiving the renewals in the 2009 calendar year.

Since its inception, the Company has had limited revenues from operations other than interest income on invested cash balances and gains on sales of equipment.

C. | Organizational Structure |

As of January 31, 2009, the Company had four wholly-owned subsidiaries; Brazauro Holdings (Brazil) Ltd., a British Columbia corporation (“Brazauro Holdings”), Star U.S. Inc., a Delaware corporation (“Star”), Brazauro Holdings (BVI) Ltd., and RH 2004. Star in turn owns 100% of the stock of three corporations, Diamond Exploration, Inc. and Continental Diamonds, Inc., both of which are Arkansas corporations (“DEI” and “CDI”, respectively), and Diamond Operations, Inc., a Delaware corporation (“DOI”). The Company and Brazauro Holdings own 98% and 2%, respectively, of Brazauro Recursos Minerais Ltda. (formerly Jaguar Resources do Brasil Ltda.), a Brazilian corporation, which in turn owns 100% of Cachambix. RH 2004 and Brazauro Holdings own 99% and 1%, respectively, of EIMB, a Brazilian corporation. All references to the Company herein include its subsidiaries unless otherwise noted. The Company’s Consolidated Financial Statements referred to herein also include its subsidiaries. The Company’s fiscal year ends January 31.

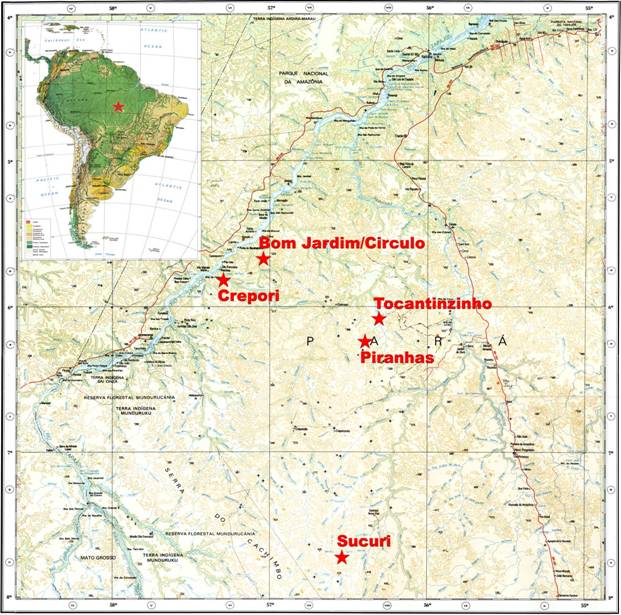

D. Properties

Currently, all of the Company’s Properties are located in the Tapajós Gold District of Brazil’s northerly Pará State. The general location of the Company’s Brazilian Properties is shown on the map provided below. The map is followed by a description of the Company’s rights and interests in each of the Properties.

7

Tocantinzinho Properties

In August 2003, the Company entered into an option to acquire exploration rights to a total of 28,275 hectares in the Tapajós gold district in Pará State, Brazil under an option agreement with two individuals (herein referred to as “optionors”). The option agreement entitled the Company to acquire a 100% interest in the exploration rights to such area (referred to herein as the “Tocantinzinho Properties”) over a four-year period in consideration for the staged payment of $465,000 (U.S.), the staged issuance of 2,600,000 shares of the Company and the expenditure of $1,000,000 (U.S.) on exploration. As of January 31, 2009, the Company has made all payments due under the option agreement and has met the requirement to expend $1,000,000 (U.S.) on exploration.

Additionally, the option agreement required the Company to assume all existing obligations of the optionors to certain Brazilian residents in respect of the mineral rights to the Tocantinzinho Properties (the “Underlying

8

Agreements”) totaling $1,600,000 (U.S.) over a four-year period. As of January 31, 2009, the Company has made all payments due under the Underlying Agreements.

In fiscal 2006, the Company received exploration licenses in respect of the central 4,000 hectare area of the Tocantinzinho Properties on which it has been focusing its exploration efforts as well as for a 9,315 hectare area forming the north eastern and eastern boundary of the Tocantinzinho Properties. Under the option agreement, the Company also holds rights to acquire two other applications for exploration licenses filed with the regulatory authorities in Brazil: one covering 4,275 hectares that lies to the south of the central 4,000 hectare area and one (the “Extension Area”) covering 10,000 hectares that lies immediately to the east but continues well south of the central 4,000 hectare area. The mineralized zone discovered by the Company on the Tocantinzinho Properties starts on the central 4,000 hectare area and extends eastward beyond the boundary of the central 4,000 hectare area into the Extension Area. The Company is subject under DNPM regulations related to periodic renewal requirements for its exploration licenses, and certain of those exploration licenses’ initial three year terms expired during fiscal 2009. The Company has complied with the renewal requirements on the Extension Area and the 4,275 hectare area, and expects to receive extensions of those licenses during the calendar year 2009. In February 2009, the Company received the renovation on the exploration license in respect of the central 4,000 hectare area.

During fiscal year 2006, the Company became aware that Talon Metals Corp. (“Talon”, formerly BrazMin Corp.) also had applied for exploration licenses to areas of the Tocantinzinho Properties, including all of the area of the mineralized zone discovered by the Company that lies within the Extension Area. In response, the Company undertook an extensive review of its title position.

At the end of fiscal 2006, as a result of a title review by the Company, it came to the Company’s attention that a long dormant application for a mining license that covered the Extension Area had never been processed by the Departamento Nacional de Produção Mineral (“DNPM”) and was still valid. According to advice from Brazilian counsel, the dormant application carried paramount title to the Extension Area. The Company, through its subsidiary, Brazauro Recursos Minerais Ltda. (formerly Jaguar Resources do Brasil Ltda.), reached an agreement (“the Extension Area Agreement”) with the holder of such application, Mineração Cachambix Ltda. (“Cachambix”) to acquire its rights to obtain a mining license over the Extension Area, subject to receipt of confirmation from the DNPM of the continued validity of the application for the mining license and the completion of the assignment of the mining license to Brazauro Recursos Minerais Ltda. The Company made a payment of $150,000 (U.S.) to Cachambix in fiscal 2007 upon execution of the Extension Area Agreement.

In September 2006, the Company entered into an agreement (“the Title Consolidation Agreement”) with Talon whereby the Company would acquire the shares of Talon’s subsidiaries with interests in the area of the Tocantinzinho Properties, being Resource Holdings 2004 Inc. and its subsidiary, Empresa Internacional de Mineração do Brasil Ltda., in exchange for 13,150,000 shares of the Company.

In December 2006, the Company was informed by the DNPM that the application to which the Extension Area Agreement relates had been confirmed as the paramount title. The Company and Cachambix reached an agreement to modify the Extension Area Agreement in February 2007. Under this modified agreement, the Company acquired all of the outstanding shares of Cachambix by payment of $850,000 (U.S.) plus its agreement to make two future payments of $1,000,000 (U.S.) each to be made to the former shareholders of Cachambix in February 2008 and 2009. The Company’s obligation to make the future payments was secured by the Cachambix shares. As of February 2009, the Company has made all the payments under the agreement.

In February 2007, under the terms of the Title Consolidation Agreement, the Company acquired Resource Holdings 2004 Inc. and its wholly-owned subsidiary, Empresa Internacional de Mineração do Brasil Ltda., from Talon in exchange for 13,150,000 common shares of the Company and payment of $50,000 (U.S.). Upon issuance of the common shares, the Company and Talon entered into a Voting Trust and Placement Rights Agreement (the “Voting Agreement”) pursuant to which the Company had the right to direct the voting of the shares issued to Talon except in certain conditions, including but not limited to a merger, amalgamation or a sale of all or substantially all of the Company’s assets. Further, the Company had the right to find purchasers for the shares if Talon wished to sell. The Voting Agreement terminated on the earliest of: (i) the day following the second shareholders meeting after the Voting Agreement is entered into, (ii) eighteen months after the Voting Agreement is entered into, and (iii) the date

9

on which the shares held by Talon and its affiliates represent in the aggregate less than 10% of the then outstanding shares. In February 2007, the shares issued to Talon represented approximately 19.8% of the issued shares of the Company. Prior to the closing of the transaction, Talon did not own beneficially, directly or indirectly, any shares of the Company.

In September 2007, Talon sold 8,214,500 common shares of the Company to several third parties. After the sale, Talon holds 4,935,500 shares or approximately 6.5% of the outstanding shares. The Voting Agreement terminated when the holdings of Company common shares by Talon became less than 10% of the Company’s outstanding common shares. The Company and Talon entered into an agreement whereby Talon agreed that it will not sell any of its remaining common shares of the Company for six months without the prior consent of the Company.

The option agreement provides that the optionors may be entitled to a sliding scale gross revenues royalty ranging from 2.5% for gold prices below $400 (U.S.) per ounce to 3.5% for gold prices in excess of $500 (U.S.) per ounce from production in respect of the mineral rights relating to the applications subject to the option agreement. Since the application for the license subject to the option agreement covering the Extension Area (the eastern portion of the deposit) will not be successful due to the presence of a prior owner with mineral rights to that area (being Cachambix, now owned by the Company), the 3.5% NSR is not payable on the Extension Area. The Company estimates that approximately 60 to 65% of the deposit lies within the Extension Area.

Under a separate option agreement, the Company held exploration permits for an additional 16,052 hectares adjacent to the western border of the above Tocantinzinho Properties. The Company agreed to make payments totaling $300,000 (U.S.) over a period of approximately four years to an individual as a finder’s fee related to this 16,000 hectare property. This additional property is not subject to the option agreement and therefore is not subject to the royalty. The Company received an exploration license from the Brazilian regulatory authority with respect to the additional 16,052 hectares in fiscal year 2005, which expired in October 2007. The Company has applied for a new exploration license.

In July 2008, the Company reached an agreement with Eldorado Gold Corporation (“Eldorado”) and completed a private placement required as part of Eldorado’s earn-in on an option to acquire an initial 60% interest in the Tocantinzinho Properties. The private placement consisted of the issuance of 8,800,000 units of the Company (the “Units”) to Eldorado at the price of $0.95 per Unit for proceeds of $8,360,000.

To complete its earn-in of the option to acquire an initial 60% interest in the Company’s Tocantinzinho Properties, Eldorado is required to incur $9.5 million in expenditures on the Tocantinzinho Properties within 24 months or pay the cash equivalent to the Company. Subject to completing the earn-in, Eldorado will be entitled to exercise the option to acquire an initial 60% in the Tocantinzinho Properties by paying $40 million to the Company. Conditional upon exercise of the first option, Eldorado will have a second option to acquire a further 10% interest exercisable after a construction decision has been made on the Tocantinzinho Properties by paying an additional $30 million, subject to increase to up to $40 million based on the proven and probable reserves outlined in the feasibility study, and a third option to acquire within two years of the construction decision a further 5% interest (for a total of 75%) by paying a further $20 million.

Crepori Property

In July 2006, the Company entered into an option agreement under which it could acquire the exploration license to the 8,175 hectare Crepori Property, located in Pará State, approximately 220 kilometers from Itaituba. The Company had an option to earn 100% of the Crepori Property, with no residual production royalty obligations, by payment of a total of $800,000 (Brazilian Reals) over three years. During fiscal 2008, the Company conducted exploration activities at the Crepori Property, and based upon the results of the exploration results, elected to terminate the option agreement in April 2008. Accordingly, the capitalized acquisition and exploration costs totaling $576,694 and $20,922 were written off in fiscal 2008 and 2009, respectively, and the Company has no further obligations under the option agreement.

10

Circulo/ Bom Jardim Property

In fiscal 2007, the Company applied for exploration licenses with the DNPM for a total of approximately 38,096 hectares in Pará State located approximately 190 kilometers southwest from the city of Itaituba. The exploration licenses were granted by the DNPM in September 2007.

On May 9, 2008, the Company and a third party entered into a letter of intent (“the LOI”) whereby the Company was to acquire, subject to certain conditions including the execution of a definitive agreement, the Bom Jardim property consisting of approximately 22,700 hectares of concessions and application areas in the Tapajós region of Pará State, Brazil. The Company was to issue $1,000,000 in common shares for the Bom Jardim Property.

The parties agreed to negotiate a definitive agreement governing the terms of the transaction in detail. In January 2009, after efforts to reach a definite agreement were not successful, the Company notified the third party that as contemplate in the LOI, both parties’ obligations were terminated.

Piranha Property

In July 2008, the Company entered into an option agreement under which it may acquire the mineral rights to the 20,688 hectare Piranha Property, located in Pará State, Brazil. The Company has an option to earn 100% of the Piranha Property, with no residual production royalty obligations, by payment of a total of $1,800,000 (Brazilian Reals) over three years. An initial payment of approximately $11,000 (U.S.) was made in July 2008. The remaining payments under the option agreement total approximately $952,000 and are due as follows (all amounts are in Canadian dollars based on the exchange rate as of January 31, 2009): $35,000, $59,000, $86,000 and $772,000, due in fiscal years 2010, 2011, 2012 and 2013, respectively. The Company can terminate the option agreement at any time without further obligation.

Sucuri Property

In July 2006, the Company entered into an option agreement under which it could acquire the exploration license to the 5,400 hectare Sucuri Property, located in Pará State, approximately 390 kilometers from the city of Itaituba, the city nearest to the Company’s Tocantinzinho Properties. The Company had an option to earn 100% of the Sucuri Property by payment of a total of $1,000,000 (Brazilian Reals) over three years. The Company could terminate the option agreement at any time without further obligation. There are no production royalties in the option agreement.

In fiscal 2007, the Company reviewed its exploration results related to the Sucuri property and determined that exploration activities would be suspended during fiscal 2008. Accordingly, the capitalized exploration costs totaling $707,863 were written off in fiscal 2007. In fiscal 2008, after additional review of the viability of the property, the Company advised the optionor that the Company would release the Sucuri property and no further payments would be made under the agreement. The accumulated acquisition and exploration costs totaling $107,888 were written off in fiscal 2008.

Item 4A. Unresolved Staff Comments

Not applicable.

Item 5. | Operating and Financial Review and Prospects |

A. Operating Results

For the Years Ended January 31, 2009, 2008 and 2007

The following discussion should be read in conjunction with the information contained in the consolidated financial statements and notes thereto included in “Item 17. Financial Statements.”

11

Mineral Properties and Deferred Expenditures

The Company is engaged in the business of exploring for and, if warranted, developing mineral properties and is concentrating its current acquisition and exploration efforts on those properties which the Company believes have large scale gold potential. The Company has been focusing on its Properties located in the Tapajós Gold District of Brazil’s northerly Pará State.

The Company’s current Properties are in the exploration stage and have not been proven to be commercially developable to date. The Company’s existing Properties are gold prospects in Brazil which were acquired during fiscal years 2004 through 2007. The Company capitalizes expenditures associated with the direct acquisition, evaluation and exploration of mineral properties. When an area is disproved or abandoned, the acquisition costs and related deferred expenditures are written-off. The net capitalized cost of each mineral property is periodically compared to management’s estimation of the net realizable value and a write-down is recorded if the net realizable value is less than the cumulative net capitalized costs.

The Company’s mineral properties and deferred expenditures increased to $28,809,952 at January 31, 2009 from $25,872,047 at January 31, 2008 as a result of acquisition costs totaling $231,571 and exploration costs totaling $2,745,256 related to the activities on the Company’s Brazilian properties, less the write-off of the exploration costs related to the Crepori Property of $20,922. As of January 31, 2009, the capitalized costs related to the Company’s primary exploration target, the Tocantinzinho Properties, totaled $28,111,113. The capitalized costs related to the Company’s property, the Circulo/ Bom Jardim Property, totaled approximately $594,000 as of January 31, 2009. The capitalized costs related to the Company’s remaining two properties, the Piranha and Andorinhas Properties, totaled approximately $105,000 as of January 31, 2009.

In July 2008, the Company reached an agreement with Eldorado Gold Corporation (“Eldorado”) and completed a private placement required as part of Eldorado’s earn-in on an option to acquire an initial 60% interest in the Tocantinzinho Properties. The private placement consisted of the issuance of 8,800,000 units of the Company (the “Units”) to Eldorado at the price of $0.95 per Unit for proceeds of $8,360,000.

To complete its earn-in of the option to acquire an initial 60% interest in the Company’s Tocantinzinho Properties, Eldorado is required to incur $9.5 million in expenditures on the Tocantinzinho Properties within 24 months or pay the cash equivalent to the Company. Subject to completing the earn-in Eldorado will be entitled to exercise the option to acquire an initial 60% in the Project by paying $40 million dollars to the Company. Conditional upon exercise of the first option, Eldorado will have a second option to acquire a further 10% interest exercisable after a construction decision has been made on the Tocantinzinho Properties by paying an additional $30 million dollars, subject to increase to up to $40 million dollars based on the proven and probable reserves outlined in the feasibility study, and a third option to acquire within two years of the construction decision a further 5% interest (for a total of 75%) by paying a further $20 million dollars.

In February 2007, the Company completed its acquisition of the mineral rights to the Extension Area within the Tocantinzinho Property as a result of the acquisition of the following three corporations. The Company acquired Resource Holdings 2004 Inc. (“RH 2004”, a British Virgin Islands corporation), and its wholly-owned subsidiary, Empresa Internacional de Mineração do Brasil Ltda. (“EIMB”, a Brazil corporation), in exchange for the issuance of 13,150,000 common shares of the Company and payment of $50,000 (U.S.) to a third party. Additionally, the Company acquired Mineração Cachambix Ltda. (“Cachambix”, a Brazil corporation) from third parties by payment of $850,000 (U.S.) and its agreement to make two future payments of $1,000,000 (U.S.) each, which were paid on the due dates in February 2008 and 2009.

During fiscal 2008 the Company made the final option payment of $150,000 (U.S.) and 700,000 common shares of the Company due under the Option Agreement to acquire the Tocantinzinho Properties dated August 2003. Additionally, in fiscal 2008 the Company incurred acquisition costs totaling approximately $1,290,000 (U.S.) related to the Tocantinzinho Properties, which primarily represent payments for mineral rights under the Underlying Agreements discussed in Note 6 to the Consolidated Financial Statements.

In July 2008, the Company entered into an option agreement under which it may acquire the mineral rights to the 20,688 hectare Piranha Property, located in Pará State. The Company has an option to earn 100% of the Piranha

12

Property, with no residual production royalty obligations, by payment of a total of $1,800,000 (Brazilian Reals) over three years.

During fiscal 2008, the Company conducted exploration activities at the Crepori Property, and based upon the results of the exploration results elected to terminate the option agreement in April 2008. Accordingly, the capitalized acquisition and exploration costs totaling $576,694 and $ 20,922 were written off in fiscal 2008 and 2009, respectively, and the Company has no further obligations under the option agreement.

On May 9, 2008, the Company and Gold Fields Holdings Company BVI Ltd. (“Gold Fields”) entered into a letter of intent (“the LOI”) whereby the Company was to acquire, subject to certain conditions including the execution of a definitive agreement, the Bom Jardim property consisting of approximately 22,700 hectares of concessions and application areas in the Tapajós region of Pará State, Brazil. In January 2009, after efforts to reach a definite agreement were not successful, the Company notified Gold Fields that as contemplated in the LOI, both parties’ obligations were terminated.

The Company’s mineral properties and deferred expenditures increased to $25,872,047 at January 31, 2008 from $6,368,126 at January 31, 2007 as a result of acquisition costs totaling $17,993,741 and exploration costs totaling $2,194,762 related to the activities on the Company’s Brazilian properties, less the write-off of the exploration costs related to the Sucuri and Crepori Properties of $684,582. As of January 31, 2008, the capitalized costs related to the Company’s primary exploration target, the Tocantinzinho Properties, totaled $25,835,276. The capitalized costs related to the Company’s remaining property, the Circulo/ Bom Jardim Property, totaled approximately $36,000 as of January 31, 2008.

In fiscal 2007, the Company reviewed its exploration results related to the Sucuri property and determined that exploration activities would be suspended during fiscal 2008. Accordingly, the capitalized exploration costs totaling approximately $708,000 were written off in fiscal 2007. In fiscal 2008, after additional review of the viability of the property, the Company advised the optionor that the Company would release the Sucuri Property and no further payments would be made under the agreement. The accumulated acquisition and exploration costs totaling $107,888 were written off in fiscal 2008.

The Company completed the Phase I and Phase II diamond drilling programs consisting of twenty holes (4,700 meters) at the Tocantinzinho Properties during fiscal 2005 in which 18 of 20 holes encountered mineralization. The Company completed a follow-up fourteen-hole Phase III drilling program at the Tocantinzinho Properties in fiscal 2006. In fiscal 2007 the Company completed the Phase IV diamond drilling campaign consisting of twelve core holes. In fiscal 2008, the Company completed the Phase V diamond drilling campaign, consisting of twenty five core holes for a total of 5,763 meters, at the Tocantinzinho Properties.

In December 2006, the Company received a NI 43-101 qualified estimate of the gold resource at the Tocantinzinho Properties, and another two, in August 2007 and December 2007. The Company commenced Phase VI, an 26-hole drilling campaign at the Tocantinzinho Properties in the first quarter of fiscal 2008 which was completed in the second quarter of fiscal 2008. Bulk flotation and cyanidation tests were conducted on ore from the Tocantinzinho Properties during August 2007. Additionally, the Company commissioned an independent, preliminary scoping study at the Tocantinzinho Properties, and results from the study were released in the third fiscal quarter of 2008. In the fourth quarter of fiscal 2008, the Company commissioned and received an additional preliminary scoping study at the Tocantinzinho Properties, and results from that study were released in December 2007.

During fiscal 2009 the Company completed an 8,500 meter core drilling campaign on the Tocantinzinho Property that was designed to upgrade inferred resources to the indicated category and to probe deeper into the mineralized zone with a view to increasing the total resources down to the level of 300 meters below surface. Results of the 26 drill holes completed in the fiscal 2009 drilling campaign were released in October, 2008.

13

Income from Operations

The Company has not received any revenues from mining operations since inception. During the years ended January 31, 2009, 2008 and 2007 the Company’s revenues were comprised primarily of interest income on proceeds received from prior financings.

General and administrative expenses totaled approximately $3,727,000 during fiscal 2009 as compared to approximately $2,912,000 during fiscal 2008, representing an increase of approximately $815,000 or 28%. The increase is due primarily to the following: (i) the Company incurred consulting fees during fiscal 2009 totaling approximately $156,000 related to the Eldorado transaction; (ii) directors’ fees totaling $93,500 were awarded in fiscal 2009 and no directors’ fees were awarded during the similar period in 2008; (iii) an increase in professional fees totaling approximately $302,000 related to the increased activity in the Company during fiscal 2009, primarily legal fees related to the Eldorado transaction and the proposed Circulo/Bom Jardim transaction and geology consulting fees incurred in evaluating prospective property acquisitions in Brazil; and (iv) a promotional campaign to investors conducted during fiscal 2009 costing approximately $250,000.

General and administrative expenses totaled approximately $2,912,000 during fiscal 2008 as compared to approximately $4,759,000 during fiscal 2007, representing a decrease of approximately $1,847,000 or 39%. Included in general and administrative expenses during fiscal 2008 and 2007 were approximately $466,000 and $2,700,000, respectively, of stock compensation expense recorded using the fair value method. The Company’s common stock options vest over a period of 18 months, with 25% of the common stock options vesting upon the date of issuance and 12.5% of the common stock options vesting each quarter thereafter. The decrease in the stock compensation expense from fiscal 2007 to fiscal 2008 is due to the decrease in the numbers of options granted over the past three fiscal years. A total of 4,100,000, 250,000 and 1,900,000 options were granted in fiscal 2006, 2007, and 2008, respectively, and as the options issued in fiscal 2006 became fully vested in fiscal 2007, a significant decrease in stock compensation expense resulted.

After adjusting for the effects of stock compensation expense on general and administrative expenses, the remaining general and administrative expenses totaled approximately $2,446,000 and $2,059,000 for the fiscal years of 2008 and 2007, respectively, which represents an increase of 19%. Consulting and salary expenses (exclusive of stock compensation expense) increased by approximately $241,000 in fiscal 2008 as compared to fiscal 2007. The increase was primarily due to bonuses granted in fiscal 2008 to directors, officers, employees and consultants of approximately $160,000. Shareholder relations expense increased from approximately $93,000 for fiscal 2007 to approximately $229,000 for fiscal 2008, an increase of 146%, as a result of the Company’s increased promotional efforts following its successful resolution of the title issues on the Tocantinzinho Properties.

The Company anticipates that general and administrative expenses during fiscal 2010 will increase from the level experienced in fiscal 2009 as the Company incurs additional consulting and exploration expenditures related to the Brazilian Properties

Differences Between Canadian and United States Generally Accepted Accounting Principles

At the present stage of the Company’s business development, there are no significant differences between Canadian and United States generally accepted accounting principles that impact the Consolidated Balance Sheets, the Consolidated Statements of Operations, the Consolidated Statements of Shareholders’ Equity and the Consolidated Statements of Cash Flows except for the capitalization of mineral properties and deferred expenditures as discussed in Note 20 to Notes to Consolidated Financial Statements.

14

Fluctuations in Foreign Currency Exchange Rates.

The Company raises its equity in Canadian dollars and its exploration expenditures are generally denominated in United States dollars. As a result, the Company’s expenditures are subject to foreign currency fluctuations. Foreign currency fluctuations may materially and adversely increase the Company’s operating expenditures and reduce the amount of exploration activities that the Company is able to complete with its current capital. The Company does not engage in any hedging or other transactions to protect itself against such currency fluctuations.

Impact of Inflation.

As the Company is not anticipating recording sales and revenues from operations in the short term, a discussion of the effect of inflation and changing prices on its operations is not relevant.

B. Financial Condition; Liquidity and Capital Resources.

As of January 31, 2009, the Company had working capital of $4,586,023 as compared to working capital of $3,005,013 at January 31, 2008. At January 31, 2009, the Company had current assets of $6,438,840, including $6,021,592 in cash and cash equivalents and $417,248 in other current assets compared to total current liabilities of $1,852,817.

In July 2008, the Company closed a private placement with Eldorado Gold Corporation (“Eldorado”) by the issuance of 8,800,000 units of the Company (the “Units”) at the price of $0.95 per Unit for gross proceeds of $8,360,000. The Company paid stock issuance costs totaling $38,200. Each Unit consists of one common share and one-half of one non-transferable share purchase warrant. Each full warrant would entitle the holder to acquire one additional share at a price of $1.30 per share until January 24, 2010. In the first quarter of 2009, the Company received approval from the TSX Venture Exchange to amend the 4,400,000 warrants to extend the expiry date to January 24, 2011 and to reduce the exercise price to $1.00. The shares, warrants and any shares issued upon exercise of the warrants are subject to a four month hold period during which the securities may not be traded except as permitted by the Securities Act and the Rules made thereunder and the TSX Venture Exchange.

To complete its earn-in of the option to acquire an initial 60% interest in the Company’s Tocantinzinho Properties, Eldorado is required to incur $9.5 million in expenditures on the Tocantinzinho Properties within 24 months or pay the cash equivalent to the Company. Subject to completing the earn-in Eldorado will be entitled to exercise the option to acquire an initial 60% in the Project by paying $40 million dollars to the Company. Conditional upon exercise of the first option, Eldorado will have a second option to acquire a further 10% interest exercisable after a construction decision has been made on the Tocantinzinho Properties by paying an additional $30 million dollars, subject to increase to up to $40 million dollars based on the proven and probable reserves outlined in the feasibility study, and a third option to acquire within two years of the construction decision a further 5% interest (for a total of 75%) by paying a further $20 million dollars.

In March 2007 the Company closed a private placement of 9,253,333 units at $0.90 per unit for gross proceeds of $8,328,000. The Company paid a brokerage commission on the placement of $372,960. Each unit consisted of one common share and one half of one share purchase warrant. Each whole warrant would entitle the holder to purchase one additional share of the Company at $1.60 for one year. Subsequent to January 31, 2008, the Company received approval from the TSX Venture Exchange to amend the warrants to extend the expiry date to March 22, 2009 and to reduce the exercise price to $1.25 per share. In the first quarter of 2009, the Company received approval from the TSX Venture Exchange to amend the 4,626,666 warrants to extend the expiry date to March 22, 2010 and to reduce the exercise price to $1.00.

During fiscal 2009 no stock options were exercised. During fiscal 2008, and 2007 the Company received cash proceeds of $13,500 and $46,900 representing the exercise of 75,000 and 127,643, stock options, respectively, by officers, directors, employees and consultants at exercise prices from $0.10 to $1.30.

In February 2007, the Company completed its acquisition of the mineral rights to the Extension Area within the Tocantinzinho Property as a result of the acquisition of the following three corporations. The Company acquired

15

Resource Holdings 2004 Inc. (“RH 2004”, a British Virgin Islands corporation), and its wholly-owned subsidiary, Empresa Internacional de Mineração do Brasil Ltda. (“EIMB”, a Brazil corporation), in exchange for the issuance of 13,150,000 common shares of the Company and payment of $50,000 (U.S.) to a third party. Additionally, the Company acquired Mineração Cachambix Ltda. (“Cachambix”, a Brazil corporation) from third parties by payment of $850,000 (U.S.) and its agreement to make two future payments of $1,000,000 (U.S.) each, which were due and paid in February 2008 and 2009.

All financings described herein were private placements and were made pursuant to the private placement laws of Canada and pursuant to the exemptions provided by Section 4(2) and Regulation S under the United States Securities Act of 1933.

The Company has no properties that have proven to be commercially developable and has no significant revenues from mining operations. The rights and interests in the Tocantinzinho, Piranha and Circulo/ Bom Jardim Properties in Brazil constitute the Company’s current mineral holdings. While the Company believes its has sufficient working capital as of this date to meet its commitments during fiscal 2010, the Company cannot estimate with any degree of certainty either the time or the amount of funds that will be required to acquire and conduct additional exploration activities on new prospects. Certain of the Company’s planned expenditures are discretionary and may be increased or decreased based upon funds available to the Company. The Company may seek additional equity financing during fiscal 2010, including the potential exercise of outstanding options and warrants. The inability of the Company to raise further equity financing could adversely affect the Company’s business plan, including its ability to acquire additional properties and perform exploration activities on existing properties. If additional equity is not available, the Company may seek exploration partners to assist in funding acquisition or exploration efforts. Historically, the Company has been able to successfully raise capital as required for its business needs; however, no assurances are made by the Company that it can continue to raise debt or equity capital for a number of reasons including its history of losses and property writedowns, the fluctuation in the price of its common stock, the number of shares outstanding and the Company’s limited and speculative asset base of exploration properties and prospects.

C. Research and Development, Patents and Licenses

The Company is a mineral exploration company with no producing properties, so the information required by this item is not applicable.

D. Trend Information

The cyclical nature of the prices of metals, particularly the price of gold, is reasonably likely to have an effect on the Company’s liquidity and capital resources. If the price of gold or the worldwide demand for gold decreases, there would likely be an adverse effect on the Company’s ability to raise additional funding and attract exploration partners for its Properties.

E. Off-Balance Sheet Arrangements.

As of May 22, 2008, the Company has no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company’s financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

F. Contractual Obligations

As of January 31, 2009, the Company’s long-term debt and operating lease obligations were as follows (in US Dollars):

16

| Payments due by period | ||||

| Less |

|

| More | |

|

|

|

|

|

|

Operating Lease Obligations |

|

|

|

|

|

|

|

|

|

$ - |

|

The long-term debt represents the discounted value of the remaining payment due under the agreement to acquire the common shares of Cachambix described in “B. Selected Annual Information” above. The obligation of $1,000,000 (U.S.) was due and paid in February 2009 and is recorded in Canadian dollars on the consolidated balance sheet of the Company as a note payable less unamortized discount based on an imputed interest rate of 7.6%

G. Safe Harbor

Certain statements in this Form 20-F under “Item 3. Risk Factors”, “Item 4. Properties”, “Item 5. Operating and Financial Review and Prospects”, and “Item 8. Financial Information” constitute “forward-looking statements”. These forward-looking statements are subject to various risks and uncertainties that may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, the following: general economic and business conditions; competition; success of operating initiatives; the success of the Company’s exploration and development operations on its Properties; the Company’s ability to raise capital and the terms thereof; the acquisition of additional properties; the continuity, experience and quality of the Company’s management; changes in or failure to comply with government regulations or the lack of government authorization to continue the Company’s projects; and other factors referenced in this Form 20-F. The use in this Form 20-F of such words as “believes”, “plans”, “anticipates”, “expects”, “intends” and similar expressions are intended to identify forward-looking statements, but are not the exclusive means of identifying such statements. The success of the Company is dependent on the efforts of the Company, its employees and many other factors including, primarily, its ability to raise additional capital and establishing the economic viability of its exploration Properties.

Item 6. Directors, Senior Management and Employees

A. Directors and senior management

The directors and executive officers of the Company, their ages and term of continuous service are as follows:

17

|

| Position with | Served As a Director |

D. Harry W. Dobson | 60 | Director | May 27, 2005 (1) |

Patrick L. Glazier | 51 | Director | July 8, 1998 |

Brian C. Irwin | 69 | Director, CFO | October 3, 1995 |

Mark E. Jones, III | 69 | Director, Chairman & CEO | March 12, 1986 |

Leendert G. Krol | 69 | Director | March 6, 2003 |

Dr. Roger David Morton | 73 | Director | June 14, 1993 |

Gregory Chorny | 59 | Director | August 8, 2008 |

Elton L. S. Pereira | 48 | Vice President - Exploration | April 30, 2007 |

Daniel B. Leonard | 72 | Director | October 20, 1999 (2) |

Dr. Roger Howard Mitchell | 67 | Director | June 14, 1993 (2) |

(1) Mr. Dobson resigned effective February April 20, 2009. (2) Mr. Leonard and Mr. Mitchell retired in August, 2008. | |||

D. Harry W. Dobson. Mr. Dobson has served as the Chairman of Kirkland Lake Gold Inc. for the past five years. Mr. Dobson also serves as a Director of Mountain Province Diamonds, Inc, Belvedere Resources Ltd., Navan Capital Corp., Western Uranium Corporation and Suroco Energy Inc.

Patrick L. Glazier. Mr. Glazier has served as the President of East Fraser Fiber Co. Ltd. based in Prince George, British Columbia for the past six years.

Brian C. Irwin. Mr. Irwin’s principal occupation was the practice of law as a partner of DuMoulin Black in Vancouver, British Columbia, until his retirement in June 2005. On May 29, 2008, Mr. Irwin was appointed the Chief Financial Officer of the Company. Mr. Irwin serves as a Director of Callinan Mines Ltd., Carlin Gold Corporation, Constantine Metal Resources Ltd., and International Northair Mines Ltd.

Mark E. Jones, III. Mr. Jones has served as Chairman of the Company from 1986 to the present. In his capacity as Chairman of the Board of Directors, Mr. Jones is the chief executive officer of the Company. Additionally, Mr. Jones served as the President of the Company from 1986 to June 1990, from July 2001 to March 2003, and from May 2005 until the present. Mr. Jones has served as a Director of Crown Resources Corporation (“Crown”) from 1987 to 2006, when Crown was sold to Kinross Gold Corp. Mr. Jones is also a director of Solitario Exploration & Royalty Corporation, where he has served since 1992 and is currently Vice-Chairman of the Board of Directors.

Leendert G. Krol. Until his retirement in April 2001, Mr. Krol had spent 13 years with Newmont Mining Corporation including the last 10 years, successively, as Director of Foreign Operation, Vice President Exploration and Vice President International Exploration. Mr. Krol served as the Company’s president from March 2003 until May 2005. Mr. Krol also serves as a Director of Romarco Minerals Inc and StrataGold Corporation.

Dr. Roger David Morton. Dr. Morton has been Professor Emeritus in Geology with the Department of Earth and Atmospheric Sciences at the University of Alberta since 1996. He is a member of the Board of Directors of Diamond Hawk Mining Corporation and Sola Resource Corporation. Dr. Morton obtained his B.Sc. (Hons. 1st class) in Geology and his Ph.D. in Geology from the University of Nottingham, England.

Gregory Chorny. Mr. Chorny, a Retired Barrister, has been involved in finance in the junior resources sector as an independent venture capitalist for the past fifteen years.

18

Mr. Elton L. S. Pereira. Mr. Pereira began serving as the Company’s Chief Vice President - Exploration on April 30, 2007. Prior to his appointment as Vice President of Exploration of the Company, Mr. Pereira served as the Company’s Manager of Exploration for two years. Mr. Pereira has over twenty years of experience in mineral exploration in Brazil, mainly with the Rio Tinto Group. Mr. Pereira is a graduate geologist of Universidade do Vale do Rio dos Sinos of Rio Grande do Sul State and has a M.Sc degree from Universidade Federal do Ouro Preto of Minas Gerais State.

Dan Leonard. Mr. Leonard served as Senior Vice President of INVESCO for twenty-four years until his retirement in January 1999. Mr. Leonard also serves as a Director of Solitario Exploration & Royalty Corporation.

Dr. Roger Howard Mitchell. For the past five years, Dr. Mitchell has served as a Professor of Geology at Lakehead University, Thunder Bay, Ontario. Dr. Mitchell received his B.Sc. from the University of Manchester, 1964; M.Sc. from Manchester, 1966; Ph.D from McMaster University, 1969; and a D.Sc in 1978 from the University of Manchester. He was elected a Fellow of the Royal Society of Canada in 1994.

No director or officer of the Company has any family relationship with any other officer or director of the Company. The Company has no arrangement or understanding with major shareholders, customers, suppliers or others, pursuant to which any person referred to above was selected as a director.

B. Compensation

Officers

During the financial year ended January 31, 2009, the Company had three (3) Named Executive Officers: Mark E. Jones III, President and Chief Executive Officer, Brian C. Irwin, Chief Financial Officer, and Elton L.S. Pereira, Vice President Exploration. The Company has no long-term incentive plans. However stock options are awarded from time-to-time at the discretion of the Board of Directors and the Compensation Committee. The following tables set forth all annual and long-term compensation for services in all capacities to the Company and its subsidiaries for the last full financial years, including information regarding stock option awards made under the Company’s Stock Option Plan, in respect of the President and Chief Executive Officer, the Chief Financial Officer and the Vice President Exploration

Summary Compensation Table

| Annual Compensation | Long Term Compensation |

| ||||

|

|

|

| Awards | Payouts |

| |

Name |

|

|

US ($) | Securities Under Options |

|

| All other |

Mark E. Jones, III, | 200,000 | 6,000 | 17,079 | - | - | - | 7,800 |

Brian C. Irwin, | 110,619 | 4,411 | 18,897 | - | - | - | - |

Elton L. S. Pereira VP Exploration | 191,770 | 10,000 | - | - | - | - | - |

(1) Mr. Irwin provides consulting services to the Company under month-to-month contracts and a monthly fee of Can$10,000.

(2) Such other compensation includes Director’s fees paid for each Director’s meeting or committee meeting attended

(3) Car allowance.

19

Long Term Incentive Plan (“LTIP”) Awards

The Company does not have a LTIP, pursuant to which cash or non-cash compensation intended to serve as an incentive for performance over a period greater than one financial year (whereby performance is measured by reference to financial performance or the price of the Company’s securities) was paid to the officers during the most recently completed financial year.

Option/Stock Appreciation Rights (“SAR”) Grants During the Most Recently Completed Financial Year

The following table sets forth stock options granted under the Company’s stock option plan or otherwise during the most recently completed financial year to each of the officers.

Option Grants During the Most Recently Completed Fiscal Year

Individual Grants (1) | ||||

| Securities | % of Total Options | (2) |

|

Mark E. Jones, III |

Nil |

Nil |

Nil |

N/A |

Brian C. Irwin |

Nil |

Nil |

Nil |

N/A |

|

Nil |

Nil |

Nil |

N/A |

(1) The options are subject to vesting requirements (25% on the date of grant and 12.5% on each quarter end thereafter).

(2) The exercise price of stock options is determined by the Board of Directors but shall in no event be less than the trading price of the common shares of the Corporation on the TSX Venture Exchange (“the Exchange”) at the time of the grant of the option.

The following table sets forth details of all exercises of stock options during the most recently completed financial year by each of the Named Executive Officer of the Corporation, and as of January 31, 2009, the number of unexercised options held by the Named Executive Officers, and the financial year-end value of unexercised in-the-money options on an aggregated basis.

Option Exercises in Last Fiscal Year

|

|

| Unexercised | Value of Unexercised |

Mark E. Jones, III | Nil | Nil | 1,500,000 – Exercisable | Nil – Exercisable |

Brian C. Irwin | Nil | Nil | 650,000 – Exercisable | Nil – Exercisable |

Elton L. S. Pereira | Nil | Nil | 762,500 – Exercisable | Nil – Exercisable |

20

Directors

The Company currently has six Directors, two of which Mark E. Jones III and Brian C. Irwin are also Named Executive Officers. For a description of the compensation paid to the Company’s Named Executive Officers who also act as Directors, see “Summary Compensation Table” above.

The Company compensates all Directors for their services in their capacity as Directors as follows: Directors are paid an annual fee of Can$15,000 and Can$1,000 for each Directors meeting or committee meeting they attend, with the Chairman receiving Can$1,500.

The Company maintains no pension, profit sharing, retirement or other plan providing benefits to its Directors.