Exhibit 99.5

| SUZANO S.A. AP-00778/23 |

| August 16, 2023 Business Contact: Renata Lopes | renata.lopes@apsis.com.br Proposal AP-00778/23 16.404.287/0033-32 – SUZANO S.A. |

| Tax and Accounting Advisory Scope Presentation of Services and Deadlines Fees General Conditions |

| Tax and Accounting Advisory Scope |

| Understanding of the Situation Pursuant to the understandings held, Suzano S.A. (“Suzano”, “Company” or “Client”) contacted Apsis Consultoria e Avaliação Ltda. (“APSIS”) to prepare a Business Proposal, for the issuance of accounting reports in accordance with articles 226, 227 and 252 of Law No. 6,404/76 or in accordance with articles 1,116 and 1,117 of the Civil Code (incorporation), referring to the accounting information of MMC Brasil Indústria e Comércio Ltda. (“Target Company”), related to the corporate transaction to be carried out. The aforementioned corporate transaction, as informed by the Company, consists of the incorporation of the Target Company by their direct shareholders and, in this context, one report will be issued at book value referring to the corporate transaction, in Reais and in Portuguese. This same report will also be issued at book value referring to the corporate transaction, in the version in Reais and in English. Based on Brazilian Law No. 6,404/76, the following corporate transactions require the issuance of accounting reports: ▪ Merger operations: operations whereby one or more companies are absorbed by another, which succeeds them in all their rights and obligations. For this operation, the issuance of a report is required based on articles 226, 227, and 252 of Law No. 6,404/76 or articles 1,116 and 1,117 of the Civil Code, where the value of the shareholders' equity to be merged is evaluated at its book value on the chosen closing date. |

| Project Description Under the terms and for the purposes of the articles mentioned above, the accounting reports will be conducted in compliance with the guidelines established by the Brazilian Accounting Standards. The issuance of an appraisal report at book value presupposes, as a mandatory requirement, the examination of the amounts of the assets, rights and obligations, which make up the shareholders' equity or net assets of the Target Company to appraisal. APSIS's professional responsibility will be to issue accounting reports for corporate reorganization purposes. The Company's Management will be responsible for preparing the balance sheet and all relevant statements for its preparation on the selected base date. The responsibility for the corporate reorganization rests exclusively with the Company and its legal advisors. It is not part of the scope proposed here to issue any type of opinion on the corporate reorganization process, limiting APSIS only to the assessment of the book values of the Target Company. The present proposal assumes that the information, records, and documents necessary for the review will be available to us promptly. This proposal assumes that the information, records, and documents necessary for the review will be made available to us promptly. Our work will be exclusively based on the information provided by the Company about the Target Company, and the information will be made available through a digital platform provided by the Company or by email. |

| Project Description Reports will be issued under CTG 2002 - Valuation Report Issued by an Accountant, of November 22, 2019, as approved by the Federal Accounting Council ("CTG 2002"), and with Law 6,404/76, which provides for the joint-stock companies or under the Civil Code which provides for limited companies, in reais, and Portuguese language, as they are national regulatory documents. The execution of the procedures described in this proposal cannot be taken as a guarantee of the absence of errors (unintentional errors) or irregularities or frauds (intentional errors). Based on the provisions of CTG 2002, the Client has responsibilities that include (i) preparation of accounting information in accordance with Brazilian accounting practices and in accordance with guidelines from specific bodies, (ii) maintenance of internal controls that allow the preparation of accounting information free from material misstatement, whether caused by fraud or error, (iii) provision of accounting information, such as records and documentation for carrying out the work, (iv) asset protection and fraud prevention and detection, and (v) reliable bookkeeping of transactions through records that support accounting information. The Client must formally represent to APSIS that these responsibilities have been observed. |

| Project Description The Client is aware that a report to be issued may contain paragraphs of emphasis related to uncertainties and explanatory paragraphs using measurable adjustments identified in the execution of the works. Any specified adjustments must be confirmed by the Client in the formal representation to be issued before the issuance of the accounting report. Additionally, the Client is aware that APSIS may refrain from issuing an accounting report if restrictions or limitations are found in the scope of the work that prevents the issuance of a conclusive report, such as the identification of potential adjustments that are not subject to measurement on the chosen closing date and/or absence of supporting documentation of the accounting balances of the Target Company. If APSIS abstains from issuing a report, a formal communication will be sent to the Client with the justifications for the aforementioned impossibility of issuing the report and the fees will be due in the extension of the work carried out until that date. |

| Documentation Required The following is a non-exhaustive list of the initial documentation required by the Target Company. The complete list with the necessary analyzes will be sent in due course (after approval of the referred proposal), in what applies to the situation of the Target Company of our works. For each selected valuation date by the Client - (Documentation to be provided by the Target Company): ▪ Balance sheet of the Target Company; ▪ Signed balance sheet of the Target Company (in Reais, with decimal); ▪ Corporate acts and last updated social contract; ▪ Analytical trial balance calculation memory for the Balance Sheet table; ▪ Most recent audited financial statements, if applicable; ▪ Latest revised interim financial information, if applicable; ▪ Representation letter to be signed by representatives of the Target Company and the Client (template to be provided by APSIS and signed by the Target Company's CEO, CFO and accountant); ▪ Accounting policies adopted; ▪ Bank statament from current accounts and financial investments; |

| Documentation Required For each selected valuation date by the Client - (Documentation to be provided by the Target Company): ▪ Aging list of customers, containing invoice information, customer name, value, date of issuance, and due date; ▪ Composition of the allowance for doubtful accounts recognized for accounts receivable from customers and rationale used for measurement of this allowance; ▪ Evidence of the most recent physical inventory of the fixed assets, if any; ▪ Detailed composition of the fixed assets, including asset identification, acquisition date, useful life, cost, and accumulated depreciation; ▪ Detailed movement of fixed asset items from the last physical inventory until the cut-off date of the appraisal; ▪ Accessory obligations on taxes to be recovered and collected, reconciled with accounting (analytical composition and calculation log of tax obligations); ▪ Current lease agreements; ▪ Calculation log of right-of-use assets and lease liabilities; ▪ Aging list of suppliers, containing invoice information, supplier's corporate name, value, issue date and expiration date; |

| Documentation Required For each selected valuation date by the Client - (Documentation to be provided by the Target Company): ▪ Map of transactions between related parties with the position of outstanding asset and liability balances on the selected base date; and ▪ Calculation logs and loan agreements entered into between related parties, if any. If the documentation and/or information necessary for the development of the work are not provided by the Client and obtaining or preparing them results in additional hours of work for the APSIS team involved in the project, the respective hours will be calculated and charged according to the current hourly rate table presented in this proposal. This will also occur when the documentation or information is replaced after the start of the project execution. |

| It is not part of the scope of the services proposed in this proposal: ▪ Execution of works outside the scope of this proposal; ▪ Review, issue of opinion or manifest on the proposed corporate reorganization; ▪ Assessment if the operation meets plausible economic aspects and justifications to be carried out; ▪ Making accounting entries or any modification in management reports, which are the responsibility of the Client or the entities involved in the corporate reorganization, except when detailed as part of this proposal; ▪ Assessment of the competence of the people of the Client and the Target Company, in their current and/or future functions; ▪ Issuance of a report by the independent auditors on the financial statements, quarterly information and pro forma financial information; ▪ Issuance of an accounting or legal opinion; ▪ Sanitation of databases; ▪ Directly extracting from the Entity's systems the databases necessary for carrying out the proposed works; ▪ Fiscal/tax planning or improvement; ▪ Reviews and/or definition of strategic planning; Additional Considerations |

| It is not part of the scope of the services proposed in this proposal: ▪ Alterations and/or elaboration of manuals of norms and procedures; ▪ Elaboration of policies and/or documentation of adopted accounting practices; ▪ Measurement of the impacts of adopting accounting standards; and ▪ Elaboration/implementation of processes and controls. Additional Considerations |

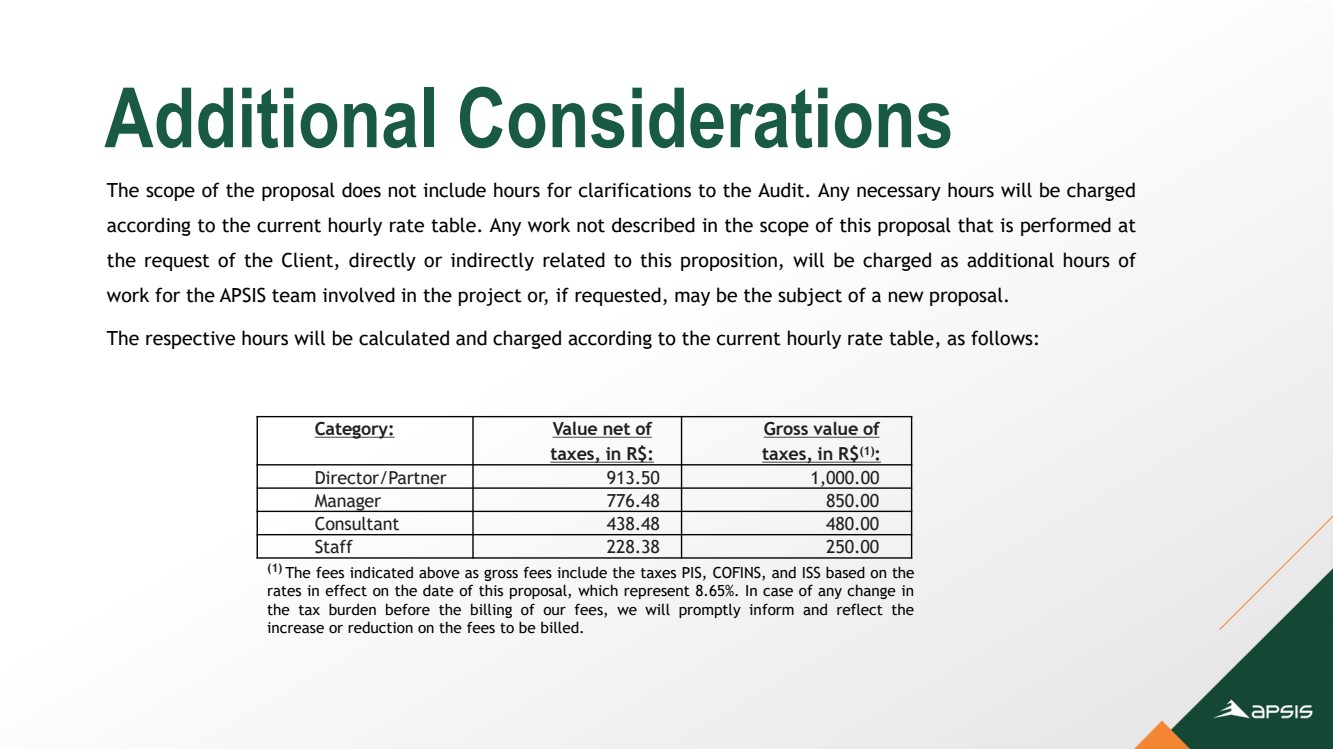

| Additional Considerations The scope of the proposal does not include hours for clarifications to the Audit. Any necessary hours will be charged according to the current hourly rate table. Any work not described in the scope of this proposal that is performed at the request of the Client, directly or indirectly related to this proposition, will be charged as additional hours of work for the APSIS team involved in the project or, if requested, may be the subject of a new proposal. The respective hours will be calculated and charged according to the current hourly rate table, as follows: Category: Value net of taxes, in R$: Gross value of taxes, in R$(1): Director/Partner 913.50 1,000.00 Manager 776.48 850.00 Consultant 438.48 480.00 Staff 228.38 250.00 (1) The fees indicated above as gross fees include the taxes PIS, COFINS, and ISS based on the rates in effect on the date of this proposal, which represent 8.65%. In case of any change in the tax burden before the billing of our fees, we will promptly inform and reflect the increase or reduction on the fees to be billed. |

| Presentation of Services and Deadlines Tax and Accounting Advisory |

| PRESENTATION OF SERVICES The final report will be presented in digital format, that is, an electronic document in Portable Document Format (PDF), and will be available in an exclusive environment on our extranet for a period of 90 (ninety) days. The report can be made available in digital format with electronic signatures or in physical format, to be sent to the Client. If requested, APSIS can provide a physical copy of the report, free of charge, within 05 (five) business days, in a single copy printed document. DEADLINES APSIS estimates to present a draft of the report within 15 (fifteen) business days, considering that the Entity's Administration and/or those involved will provide, at the beginning of the work, all necessary information for the execution of the work, as evidenced in the Scope section of this proposal. Upon receiving the draft of the report, the Client will have a period of up to 20 (twenty) days to request clarifications and approve the final issuance of the document. After the approval of the draft, APSIS will have a period of 02 (two) business days to issue the final report. After the aforementioned time, APSIS may consider the work completed and is authorized to issue the final invoice, regardless of the issuance of the final report, as well as being able to issue the latest draft of the report provided in final form. The services will commence with the express acceptance of this proposal, the payment of the advance and the receipt of the complete documentation necessary for the execution of the work, listed in this proposal. Changes requested after the delivery of the digital report will be subject to a new budget. |

| Fees Tax and Accounting Advisory |

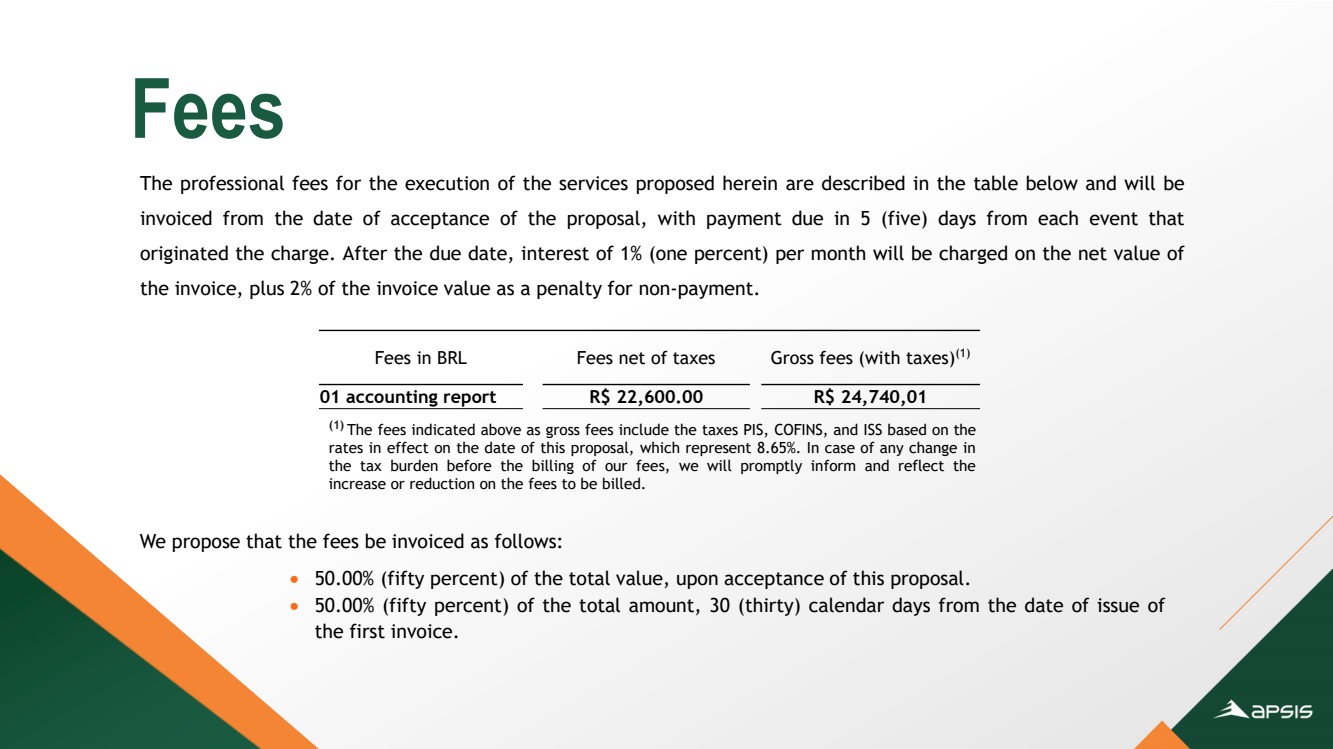

| The professional fees for the execution of the services proposed herein are described in the table below and will be invoiced from the date of acceptance of the proposal, with payment due in 5 (five) days from each event that originated the charge. After the due date, interest of 1% (one percent) per month will be charged on the net value of the invoice, plus 2% of the invoice value as a penalty for non-payment. Fees We propose that the fees be invoiced as follows: • 50.00% (fifty percent) of the total value, upon acceptance of this proposal. • 50.00% (fifty percent) of the total amount, 30 (thirty) calendar days from the date of issue of the first invoice. Fees in BRL Fees net of taxes Gross fees (with taxes)(1) 01 accounting report R$ 22,600.00 R$ 24,740,01 (1) The fees indicated above as gross fees include the taxes PIS, COFINS, and ISS based on the rates in effect on the date of this proposal, which represent 8.65%. In case of any change in the tax burden before the billing of our fees, we will promptly inform and reflect the increase or reduction on the fees to be billed. |

| If there is a need to change the valuation date of the report after the start of the work, additional fees to be applied will be discussed. Considering the limited information received for the preparation of this technical proposal, it was adopted as a premise for measuring the term and the fees presented, the fact that the accounting balances of the Target Company were not shared and those presented as relevant in the meeting should not present relevant variations (greater than to 15%). In addition, during the execution of the work, any services that exceed the initially agreed scope will be informed to the Client and charged through the issuance of a report by APSIS, containing the date, description of the work, and time used. Fees |

| General Conditions Tax and Accounting Advisory |

| CONFIDENTIALITY The present proposal is valid for a period of 30 (thirty) days, counting from the date of its presentation. APSIS is responsible for maintaining the utmost confidentiality regarding confidential information that it may become aware of during the execution of its services. For the purposes of this proposal, any information that APSIS may directly or indirectly access in connection with the services to be provided shall be considered confidential. Confidential information includes all types of oral, written, recorded, and computerized documentation disclosed by the contracting party in any form or obtained through observations, interviews, or analyses, properly and without limitation, including all machinery, compositions, equipment, records, reports, sketches, use of patents and documents, as well as all data, compilations, specifications, strategies, projections, processes, procedures, techniques, models, and tangible and intangible incorporations of any nature. APSIS, its consultants, and employees have no interest, directly or indirectly, in the company involved or in the operation described in this proposal. VALIDITY OF PROPOSAL |

| The basic parameters relevant to the scope of the service will be defined immediately after acceptance of this proposal, to allow for the planning of the work to be performed. Any changes to the data referenced in the Scope section of this proposal may result in a complementary proposal. If during the development of the work the Entity decides to interrupt/cancel the restructuring operation, the execution of our services will be immediately suspended, the already settled paid installments will not be subject to refund/return, and the Client must pay APSIS the fees related to work already performed and not invoiced, if applicable. If the draft report has been presented to the Administration, the work will be considered completed and the entire fees must be paid. If, after acceptance of the proposal, the need for modification or expansion of the initially planned project scope is identified, such that it is necessary to extend the work execution deadline, the situation will be promptly communicated to the Entity, with the impacts of additional work and new deadlines jointly analyzed, as well as the need to invoice additional fees to those originally proposed. GENERAL CONDITIONS |

| In case of force majeure, neither party shall be responsible for non-performance or delays arising from circumstances that, reasonably, can demonstrate that they are beyond their control. Once this circumstance occurs, the affected party shall inform the other party of the manner and duration in which it may affect the project. Upon such notification, the committed execution dates shall be suspended for the duration of such force majeure. Upon the conclusion of the force majeure, the parties shall agree on the corresponding adjustments to the work plan and the economic conditions to be applied, if these are affected. Non-compliance with any item of this proposal during the execution of the services by the Client shall result in the suspension of the work until the requirements of the non-compliant item are met. The execution period shall be extended by the number of days of suspension, plus any necessary time for the new mobilization of the APSIS team. Any eventuality under the responsibility of the Client that causes the interruption of the services, delaying the pre-established schedule, may result in additional fees that will be passed on to the Client through an amendment to this proposal. GENERAL CONDITIONS |

| GENERAL CONDITIONS Our work does not represent an audit, review, or assurance of financial statements performed in accordance with Brazilian and international auditing, review, and assurance standards. Consequently, our work cannot be considered as an opinion, conclusion, or assurance regarding such aspect. This proposal may be terminated by mutual agreement between the Parties. In this case, the Client shall pay APSIS the fees for work already performed, if they exceed the portion billed upon acceptance of the proposal. The forum of the Capital of the State of Rio de Janeiro is elected, to the exclusion of any other, no matter how privileged, to settle any possible doubts during the implementation of this proposal, as well as all cases not provided for in this document. |

| The proposal, once accepted, shall be signed by the legal representative of the requesting company and returned to APSIS, along with all necessary documentation for the commencement of the work. Once the proposal has been returned to APSIS, it will become a formal contract between APSIS and its client according to the current civil legislation. Therefore, the legal representatives of both parties sign this proposal, which shall be automatically converted into a service agreement, in 02 (two) copies. Awaiting your response, we remain. Sincerely, LUIZ PAULO CESAR SILVEIRA AMILCAR DE CASTRO Technical Vice President Director Acceptance: ______________________________ ___________________________ (Location/Date) Legal Representative Company Registration Number (CRN): Witness 01: Witness 02: Identification number: Identification number: |

| +55 21 2212-6850 apsis.rj@apsis.com.br Rio de Janeiro +55 11 4550-2701 apsis.sp@apsis.com.br São Paulo apsis.com.br +55 31 98299-6678 apsis.bh@apsis.com.br Belo Horizonte |