UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the fiscal year ended September 26, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period from to

Commission file number 1-12340

GREEN MOUNTAIN COFFEE ROASTERS, INC.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 03-0339228 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

| 33 Coffee Lane, Waterbury, Vermont | | 05676 |

| (Address of principal executive offices) | | (zip code) |

(802) 244-5621

(Registrants’ telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report.)

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, $0.10 par value per share | | The Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act:NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer x Accelerated Filer ¨ Non-Accelerated Filer ¨ Smaller Reporting Company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock of the registrant held by non-affiliates of the registrant on March 28, 2009 was approximately $946,000,000 based upon the closing price of such stock on that date.

As of November 20, 2009, 43,656,266 shares of common stock of the registrant were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the 2010 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Form 10-K, are incorporated by reference in Part III, Items 10-14 of this Form 10-K.

GREEN MOUNTAIN COFFEE ROASTERS, INC,

Annual Report on Form 10-K

For

Fiscal Year Ended September 26, 2009

Table of Contents

PART I

Overview

Green Mountain Coffee Roasters, Inc. (together with its subsidiaries, the “Company” or “GMCR, Inc.”) is a leader in the specialty coffee and coffee maker businesses. We sell over 200 whole bean and ground coffee selections, cocoa, teas and coffees in K-Cup® portion packs, Keurig® single-cup brewers and other accessories. In recent years, a significant driver of the Company’s growth has been the sale of K-Cups and Keurig brewing systems. We manage our operations through two business segments, Specialty Coffee business unit (SCBU) formerly referred to as Green Mountain Coffee (GMC), and Keurig business unit (Keurig). See Note 9 of the Consolidated Financial Statements included in this Form 10-K.

SCBU sells whole bean and ground coffee selections, as well as K-Cups in domestic wholesale and retail channels and directly to consumers. In addition, SCBU sells Keurig single-cup brewing systems and other accessories directly to consumers and more recently to supermarkets.

Keurig is a pioneer and leading manufacturer of gourmet single-cup brewing systems and targets its premium patented single-cup brewing systems for consumers at home (AH) and away-from-home (AFH) mainly in North America. Keurig sells its AFH single-cup brewers to distributors for offices and its AH single-cup brewers to select retailers such as department stores and club stores for at-home use. Keurig sells coffee, tea and cocoa in K-Cups produced by a variety of roasters, including SCBU, and related accessories to select retailers such as department stores and club stores and also directly to consumers. Keurig earns royalty income from the sale of K-Cups shipped by its licensed roasters.

Corporate Information

Green Mountain Coffee Roasters, Inc. is a Delaware corporation formed in July 1993. Our corporate offices are located at 33 Coffee Lane, Waterbury, Vermont 05676. The main telephone number is (802) 244-5621, and our e-mail address for investor information isinvestor.services@gmcr.com. The address of our Company’s website iswww.GMCR.com.

Corporate Objective and Philosophy

Our Company’s objective is to be a leader in the coffee business by selling high-quality, premium coffee and innovative coffee brewing systems that consistently provide a superior coffee experience. Essential elements of our philosophy and approach include:

High-Quality Coffee.From tree to cup. We are passionate about roasting great coffees and are committed to ensuring that our customers have an outstanding coffee experience. We buy some of the highest-quality Arabica beans available from the world's coffee-producing regions and use a roasting process designed to optimize each coffee’s individual taste and aroma.

Single-Cup Brewing Patented Technology. Our patented single-cup brewing technology, embodied in a premium quality machine, provides coffee and tea drinkers with the benefits of convenience, variety and great taste. Single-cup systems are designed to provide consumers consistent taste, convenience and speed with no mess or coffee waste. The Keurig gourmet single-cup system is based on three fundamental elements:

| | • | | Patented and proprietary K-Cup® portion packs, which contain precisely portioned amounts of gourmet coffees, cocoa and teas in a sealed, low oxygen environment to ensure freshness. |

| | • | | Specially designed proprietary high-speed packaging lines that manufacture K-Cups at the coffee roasters’ facilities using freshly-roasted and ground coffee (or tea or cocoa). |

1

| | • | | Premium quality brewers that precisely control the amount, temperature and pressure of water to provide a cup of coffee, tea or cocoa of a consistent high quality in less than a minute when used with K-Cups. |

The Company holds 33 U.S. and 73 international patents covering a range of its portion pack, packaging line and brewing technology innovations, with additional patent applications in process. In 1998, Keurig launched its first single-cup brewers for the AFH channel and partnered with the Company to manufacture and sell Keurig’s patented K-Cups. Since then Keurig has licensed several other coffee roasters to package gourmet coffees and teas into K-Cups, all of whom pay royalties to Keurig based on the number of K-Cups shipped.

Through K-Cups, we offer the industry’s widest selection of gourmet branded coffees and teas in a proprietary single-cup format. Consumers can choose from over a dozen gourmet brands and over 200 varieties of coffees and teas. Brands which are packaged and sold by SCBU include Green Mountain Coffee®, our co-branded Newman’s Own® Organics brands, our licensed Caribou®and Celestial Seasonings™ brands, and as of March 27, 2009, our Tully’s® Coffee brand. Additionally, as of November 13, 2009, the Company acquired the Timothy’s World Coffee® brand and the licensed Emeril’s brand, which will be packaged and sold by the SCBU segment during fiscal 2010. Keurig partners with other North American K-Cup brands that include Diedrich, Gloria Jean’s and Coffee People, Van Houtte, Bigelow and Twinings.

Customer Service and Distribution.The Company seeks to create customers for life. We believe that coffee is a convenience purchase, and we utilize our multi-channel distribution network of wholesale, retail and consumer direct to make our coffee and single-cup Keurig® brewers widely and easily available to both AH and AFH consumers.

Our operations are coordinated from our headquarters in Waterbury, Vermont and supplemented by regional distribution centers located in Maine, Upstate New York, Massachusetts, Connecticut and Tennessee. Distribution facilities are designed to be located within a two-hour radius of most customers to expedite delivery. In recent years, we have added a packaging and warehousing facility in Essex, Vermont, purchased our manufacturing facility in Knoxville, Tennessee, and expanded our manufacturing and distribution facilities to Seattle, Washington. As part of the Timothy’s acquisition on November 13, 2009, we have added a manufacturing facility in Toronto, Canada.

Socially Responsible Business Practices.We have a long history of supporting social and environmental causes, allocating at least 5% of our pretax income towards such projects. These projects typically involve direct or indirect financial support, donations of products or equipment, and employee volunteer efforts.

Corporate Culture. Our Code of Ethics is an important part of our culture and is applicable to all of our employees and our Board of Directors. The Code of Ethics is posted on our website. In addition, we believe the Company has a highly inclusive and collaborative work environment that encourages employees' individual growth and personal awareness through a culture of personal accountability and continuous learning.

The Products

Coffee

The Company offers high-quality Arabica bean coffee including single-origin, Fair Trade Certified™, organic, flavored, limited edition and proprietary blends sold under the Green Mountain Coffee®, Tully’s® Coffee, Newman’s Own® Organics and, since November 13, 2009, the Timothy’s World Coffee® brands. We carefully select our coffee beans andappropriately roast the coffees to optimize their taste and flavor differences. Our coffee comes in a variety of package types including whole bean, fractional packages (for food service and office environments), and single-cup Keurig K-Cup® portion packs. In addition to coffee, we also sell cocoa and teas in K-Cups. The Company has an exclusive licensing agreement with Celestial Seasonings to produce Celestial Seasonings™ branded teas and Perfect Iced Tea in K-Cups.

2

In fiscal 2009, approximately 30% of SCBU’s total consolidated sales volume was from Fair Trade Certified coffee.

Brewers

We are a leader in selling patented and proprietary single-cup coffee and tea brewing systems under the Keurig® brand name to the AFH and AH channels. Keurig offers a brewer line-up that is differentiated by channel and size of customer, for the AFH channel, and by features of the brewer for the AH channel. Keurig also offers a selection of brewers for the hospitality, wholesale club and consumer direct channel, and a brewer specifically designed for travel.

Marketing and Distribution

To better support customer acquisition and existing customer growth, the Company has separate sales organizations for AFH, AH and consumer direct. Consumer direct provides us the opportunity to effectively position our brands by test-marketing new products, building one-on-one relationships, and having direct correspondence with consumers, all of which gives us the ability to illuminate the Company’s points of difference. The Company’s primary geographic region is North America.

SCBU publishes catalogs and maintains a website to market and sell over 200 coffee varieties, coffee-related equipment and accessories, gift assortments, hand-crafted items from coffee-source countries and Vermont, and gourmet food items covering a wide range of price points. We encourage customers to become members of our “Café EXPRESS” service, a continuity program with customized standing orders for automatic re-shipment. Over the past couple of years, a large portion of our efforts in the consumer direct channel has been directed towards increasing traffic on our website (www.GMCR.com) and marketing of the Keurig single-cup brewers. These efforts, along with the catalog and direct mail programs, are intended to build brand awareness nationwide and boost direct sales to consumers in our less mature geographic regions.

In the U.S. and Canada, Keurig operates in both the AFH and AH segments. In AFH, Keurig targets the office coffee channel with a broad offering of single-cup brewing systems which significantly upgrade the quality of the coffee served in the workplace. Keurig promotes its AFH brewing system through a large, selective but non-exclusive network of AFH distributors in the U.S. and Canada ranging in size from local to regional to national. In AH, Keurig targets gourmet coffee drinkers who wish to enjoy the speed and convenience of single-cup brewing but who do not want to compromise on taste. Keurig promotes its AH brewing system through upscale specialty and department store retailers, select wholesale clubs and mass merchants, on its website (www.keurig.com), through select supermarkets, and through its licensed roasters and authorized AFH distributors. Keurig relies on a single order fulfillment company, MBlock & Sons, to process the majority of orders for our AH single-cup business sold through retailers.

Growth Strategy

In recent years, the primary growth in the coffee industry has come from the specialty coffee category, including demand for single-cup specialty coffee. This growth has been driven by the wider availability of high-quality coffee, the emergence of upscale coffee shops throughout the country, and the general level of consumer knowledge of, and appreciation for, coffee quality. The Company has been benefiting from the overall industry trend plus what we believe to be our carefully developed and distinctive advantages over our competitors.

We are focused on building our brands and profitably growing our business. We believe we can continue to grow sales by increasing customer awareness in existing regions, expanding into new geographic regions, expanding sales in high-growth industry segments such as single-cup coffee and tea, and selectively pursuing other opportunities, including strategic acquisitions.

3

Our growth strategy for Keurig involves developing and managing marketing programs to sell as many brewers as possible to generate ongoing demand for K-Cups®. In addition, we are focused on partnering with other gourmet coffee roasters and tea packers with strong national/regional brands to create additional K-Cup products that will help create consumer demand for the Keurig® single-cup brewing system. When used with the Keurig brewers, K-Cups are designed to provide brewed coffee, tea and cocoa that consistently deliver the taste profiles specified by gourmet roasters and tea packers, which we believe creates attractive opportunities for our roaster partners to expand their geographical presence and take advantage of new industry opportunities in both the AFH and AH single-cup industry segments with minimal investment. Only roasters and other vendors licensed by the Company may benefit from Keurig's technology and distribution network.

In March 2009, we completed the acquisition of the Tully’s® Coffee brand and certain assets of its wholesale business. Tully’s wholesale business division distributes handcrafted coffees and related products via office coffee services, food service distributors, and over 5,000 supermarkets located primarily in the western states. The geographic region encompassed by the Tully’s brand creates an advantaged opportunity for the Company to accelerate growth in the west coast region by capitalizing on Tully’s brand recognition and the loyalty of their customer base. On November 13, 2009, we acquired Timothy’s World Coffee® brand and wholesale business. Headquartered in Toronto, Canada, Timothy’s is a premium coffee company that produces specialty coffee, tea and other beverages predominantly in K-Cup portion packs. The acquisition of Timothy’s will enable geographic expansion with a Canadian brand platform that includes manufacturing and distribution synergies. In addition, we have submitted a proposal to acquire Diedrich Coffee, Inc. which, if successful, we believe would enable us to more effectively reach consumers in the southern California region and take advantage of manufacturing and distribution synergies in that region.

Competition

The specialty coffee segment of the coffee industry is highly competitive and fragmented. Within it we compete against larger companies that possess greater marketing and operating resources than our Company. The primary methods of competition in specialty coffee include price, service, product performance and brand differentiation. Our Company competes against all sellers of specialty coffee, including Dunkin’ Donuts®, Peet’s® and Starbucks®. When selling to supermarkets, we also compete with “commercial” coffee roasters, to the extent that we are also trying to “upsell” consumers into the specialty coffee segment. Some multi-national consumer goods companies have divisions or subsidiaries selling specialty coffees. For example, The J.M. Smucker Company distributes both Folgers® and premium Millstone® and Brothers™ brands, as well as Dunkin’ Donuts packaged coffees by license. Nestle S.A. markets the premium Nespresso® single-cup espresso system as well as other less premium coffee brands. When selling direct to consumers, we compete with established roasters such as Gevalia®, a division of Kraft Foods, Inc., as well as with other direct mail companies. In foodservice, we compete against private label roasters, as well as brands such as Seattle’s Best Coffee® and Starbucks®.

Similar to specialty coffee, the coffeemaker industry is also highly competitive and we compete against larger companies that possess greater marketing and operating resources than the Company. The primary methods of competition are essentially the same as in specialty coffee; price, product performance and brand differentiation. Through the Keurig segment, our Company also competes against all sellers of coffeemakers, including companies such as Bunn-O-Matic Corporation and Mars, Inc. (through its FLAVIA® unit) for AFH customers and companies such as Conair, Inc., Jarden Corporation, Phillips Electronics NV and Robert Bosch GmbH for AH customers. Specifically, the Company also competes within the small but growing single-cup segment of the coffeemaker industry with other single-cup coffee and tea delivery systems, including: FLAVIA® Beverage Systems (manufactured and marketed by Mars, Inc.), the TASSIMO beverage system (manufactured and marketed by Robert Bosch GmbH and Kraft Foods, Inc.), the SENSEO® brewing system (manufactured and marketed by Philips Electronics NV and Sara Lee Corporation) and a number of additional single-cup pod brewing systems and brands.

4

SCBU was the first roaster to sell coffee in Keurig’s innovative single-cup brewing system, and we have established a leadership position in the sale of K-Cup® portion packs. Other coffee roasters and specialty tea suppliers also participate in the proprietary Keurig® system, including: Diedrich Coffee, Inc., (which include the Diedrich Coffee, Gloria Jean’s Coffees and Coffee People brands), Timothy’s Coffees of the World, Inc., (which includes the Emeril’s Coffee brand), Van Houtte, Inc., R.C. Bigelow, Inc. and R. Twinings and Company Limited. As of November 13, 2009, the Company acquired the Timothy’s World Coffee® brand and the licensed Emeril’s brand, which will be included in the SCBU family of brands in fiscal 2010. While to some extent these brands compete against our own Green Mountain Coffee®, Tully’s Coffee® and co-branded Newman’s Own® Organics brands or our licensed Caribou® and Celestial Seasonings™ branded K-Cups, they are subject to a royalty, which is paid to us for each K-Cup shipped.

We expect competition in these segments to remain intense, both within our existing customer base and as we expand into new regions. In both business segments, we compete primarily by providing high-quality coffee and single-cup coffeemakers, easy access to our products, superior customer service and a comprehensive approach to customer relationship management. We believe that our ability to provide a convenient and broad network of outlets from which to purchase our products is an important factor in our ability to compete. Through our multi-channel distribution network of wholesale, retail and consumer direct operations, with particular emphasis for SCBU on brand trial through K-Cups, we believe we differentiate ourselves from many of our larger competitors, who specialize in only one primary channel of distribution. We also believe that SCBU’s product offering is distinctive because we offer a wide array of coffees, including flavored, Fair Trade Certified™, and organic coffees. Green Mountain Coffee also offers products that feature licensed brand partnerships, including Newman’s Own Organics, Celestial Seasonings and Caribou. Within Keurig, we believe our constant innovation and focus on quality, all directed to delivering a consistently superior cup of coffee, differentiates us among competitors in the single-cup coffeemaker industry. We also seek to differentiate ourselves through our socially- and environmentally-responsible business practices. While our Company believes we currently compete favorably with respect to all of these factors, there can be no assurance that we will be able to compete successfully in the future.

Green Coffee Cost and Supply

SCBU sold approximately 40 million pounds of coffee in fiscal 2009. We utilize a combination of outside brokers and direct relationships with farms, estates, cooperatives and cooperative groups for our supply of green coffees. Outside brokers provide the largest supply of our green coffee. The supply and price of coffee are subject to high volatility. Supply and price of all coffee grades are affected by multiple factors, such as weather, pest damage, politics and economics in the producing countries.

Cyclical swings in commodity markets are common and the most recent years have been especially volatile for the “c” price of coffee (the price per pound quoted by the Coffee, Sugar and Cocoa Exchange). The “c” price of coffee declined during fiscal 2009, consistent with most other commodity markets, as compared to fiscal 2008 when “c” prices had reached record levels for the 5-year historical period. It is expected that coffee prices will remain volatile in the coming years. In addition to the “c” price, coffee of the quality sought by us tends to trade on a negotiated basis at a substantial premium or “differential” above the “c” price. These differentials also are subject to significant variations and have generally been on the rise in recent years.

For coffees that SCBU purchases with differentials above the “c” price of coffee, we generally fix the price of our coffee contracts for approximately two fiscal quarters, and at times three fiscal quarters, prior to delivery so that we can adjust our sales prices to marketplace conditions. SCBU believes this approach is the best way to provide our customers with a fair price for our coffee. On September 26, 2009, we had approximately $90.8 million in green coffee purchase commitments, of which approximately 46% had a fixed price. In addition, from time to time we purchase coffee futures contracts and coffee options when we are not able to enter into coffee purchase commitments or when the price of a significant portion of committed contracts has not been fixed. On September 26, 2009, we held futures contracts covering approximately 1.1 million pounds of coffee.

5

In fiscal 2009, 33% of our purchases were from Fair Trade certified sources. This provides an assurance that the organized farmer groups are receiving the Fair Trade minimum price and the group is a democratically managed cooperative. In fiscal 2009, 41% of our purchases were from farm-identified sources, which means that we know the farms, estates or coops, and can develop a relationship directly with the farmers. We believe that our “farm-identified” strategy helps us secure long-term supplies of high-quality coffee.

Intellectual Property

The Company owns a number of United States trademarks and service marks that have been registered with the United States Patent and Trademark Office. We anticipate maintaining our trademark and service mark registrations with the United States Patent and Trademark Office. We also own other trademarks and service marks for which we have applications for U.S. registration. The Company has further registered or applied for registration of certain of its trademarks and service marks in the United Kingdom, the European Union, Canada, Japan, the People's Republic of China, South Korea, Taiwan and other foreign countries. The Company has licenses to use other marks, all subject to the terms of the agreements under which such licenses are granted.

The Company holds 33 U.S. patents and 73 international patents related to our Keurig® brewing and portion pack technology. Of these, 86 are utility patents and 20 are design patents. We view these patents as very valuable but do not view any single patent as critical to the Company’s success. We own patents that cover significant aspects of our products and certain patents of ours will expire in the future. The two principal patents associated with our current generation K-Cup® portion packs will expire in 2012, and we have pending patent applications associated with this technology which, if ultimately issued as patents, would have expiration dates extending to 2023. Our agreements with our roasters are more than simple patent licenses. Roasters with agreements with the Company have access to and benefit from Keurig’s technology and distribution network and we believe these benefits will help us to maintain royalty revenue irrespective of our patent status.

We have diligently protected intellectual property through the use of domestic and international patents and trademark registrations. We regularly monitor commercial activity in the countries in which we operate to guard against potential infringement. In January 2007, we filed a patent infringement lawsuit against Kraft Foods, Inc., Kraft Foods Global, Inc. and Tassimo Corporation (collectively “Kraft”) in the United States District Court for the District of Delaware asserting that Kraft’s T DISC single-serve beverage cartridges infringe upon Keurig’s United States Patent number 6,607,762. In October 2008, we entered into a Settlement and License Agreement to completely settle the patent litigation with Kraft. Pursuant to the terms of the Settlement and License Agreement, Kraft paid $17 million on October 31, 2008 to the Company and Keurig has granted to Kraft and its affiliates a limited, non exclusive, perpetual, worldwide, fully paid up license of Keurig’s United States Patents Numbered 6,607,762 (the “762 Patent”) and 7,377,162 (the “162 Patent”), and United States and foreign counterpart patents connected to the 762 Patent or 162 Patent, for use in connection with the manufacture, distribution and sale of beverage brewing machines and certain beverage filter cartridges.

Seasonality

Historically, we have experienced variations in sales from quarter-to-quarter due to the holiday season and a variety of other factors, including, but not limited to, general economic trends, the cost of green coffee, competition, marketing programs and weather. Because of the seasonality of our business, results for any quarter are not necessarily indicative of the results that may be achieved for the full fiscal year.

Employees

As of September 26, 2009, the Company had 1,499 full-time employees and 18 part-time employees. We supplement our workforce with temporary workers from time to time, especially in the first quarter of each fiscal year to service increased customer and consumer demand during the peak November-December holiday season.

6

Available information

Our Company files annual, quarterly, and current reports, proxy statements, and other documents with the Securities and Exchange Commission (SEC) under the Securities Exchange Act of 1934 (the “Exchange Act”). The public may read and copy any materials that the Company files with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet website that contains reports, proxy and information statements, and other information regarding issuers, including GMCR, Inc., that file electronically with the SEC. The public can obtain any documents that we file with the SEC atwww.sec.gov.

Our Company maintains a website atwww.GMCR.com. Our filings with the SEC, including without limitation, our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, are available through a link maintained on our website under the heading “Investor Services—Stock Quotes and Filings.” Information contained on our website is not incorporated by reference into this report.

Risks Related to the Company’s Business

The Company’s business, its future performance and forward-looking statements are affected by general industry and market conditions and growth rates, general U.S. and non-U.S. economic and political conditions (including the global economy), competition, interest rate and currency exchange rate fluctuations and other events. The following items are representative of the risks, uncertainties and other conditions that may impact our business, future performance and the forward-looking statements that we make in this report or that we may make in the future.

Risks Related to Our Operations

Our financial performance is highly dependent upon the sales of K-Cup® portion packs.

A significant and increasing percentage of our total revenue has been attributable to royalties and other revenue from sales of K-Cups for use with our Keurig® single-cup brewing systems. In fiscal 2009, total consolidated net sales of K-Cups, Keurig brewers and royalties earned upon shipment of K-Cups by licensed roasters represent approximately 81% of consolidated net sales. Continued acceptance of Keurig single-cup brewing systems and sales of K-Cups to our installed base of brewers are significant factors in our growth plans. Any substantial or sustained decline in the acceptance of Keurig single-cup brewing systems or sales of our K-Cups would materially adversely affect us. Keurig’s single cup brewing system competes against all sellers of coffeemakers, including companies such as Bunn-O-Matic Corporation, Mars, Inc., Jarden Corporation, Conair, Inc., Phillips Electronics NV and Robert Bosch GmbH. The Company also competes within the small but growing single-cup segment of the coffeemaker industry with other single-cup coffee and tea delivery systems, including: FLAVIA® Beverage Systems (manufactured and marketed by Mars, Inc.), the TASSIMO beverage system (manufactured and marketed by Robert Bosch GmbH and Kraft Foods, Inc.), the SENSEO® brewing system (manufactured and marketed by Philips Electronics NV and Sara Lee Corporation) and a number of additional single-cup pod brewing systems and brands. If we do not succeed in effectively differentiating ourselves from our competitors, based on technology or otherwise, or our competitors adopt our strategies, then our competitive position may be weakened and our sales of Keurig single-cup brewing systems and K-Cups, and accordingly our profitability, may be materially adversely affected.

Our intellectual property may not be valid, enforceable, or commercially valuable.

While we make efforts to develop and protect our intellectual property, the validity, enforceability and commercial value of our intellectual property rights may be reduced or eliminated by the discovery of prior inventions by third parties, the discovery of similar marks previously used by third parties, the successful

7

independent development by third parties of the same or similar confidential or proprietary innovations or changes in the supply or distribution chains that render our rights obsolete.

Many factors bear upon the exclusive ownership and exploitation right to intellectual properties, including, without limitation, prior rights of third parties, nonuse and/or nonenforcement by us, and/or related entities. Our ability to compete effectively depends, in part, on our ability to maintain the proprietary nature of our technologies, which include the ability to obtain, protect and enforce patents and other trade secrets and know how relating to our technology. We own patents that cover significant aspects of our products, and certain patents of ours will expire in the near future. In the United States, we have patents expiring between 2012 and 2017 associated with the K-Cup portion packs presently used in Keurig brewers. We also have pending patent applications associated with current K-Cup® portion packs technology. These applications may not issue, or if they issue, they may not be enforceable, may be challenged, invalidated or circumvented by others. Additionally, we have a number of portion pack patents that extend to 2021 but which we have elected not to commercialize yet and may never commercialize. In addition, Keurig continues to invest in further innovation in portion packs and brewing technology and takes steps it believes are appropriate to protect all such innovation. We are prepared to protect our patents vigorously; however, there can be no assurance that we will prevail in any intellectual property infringement litigation we institute to protect our intellectual property rights given the complex technical issues and inherent uncertainties in litigation. Even if we prevail in litigation, such litigation could result in substantial costs and diversion of resources and could materially adversely affect us. In addition, the validity, enforceability and value of our intellectual property depends in part on the continued maintenance and prosecution of such rights through applications, maintenance documents, and other filings, and rights may be lost through the intentional or inadvertent failure to make such necessary filings. Similarly, third parties may allege that our activities violate their intellectual properties. To the extent we are required to defend our self against such a claim, no assurance can be given that we will prevail. Such defense could be costly and materially adversely affect our business and prospects.

Competition in specialty coffee is intense and could affect our sales and profitability.

The specialty coffee business is highly fragmented. Competition in specialty coffee is increasingly intense as relatively low barriers to entry encourage new competitors to enter the marketplace. In addition, we believe that maintaining and developing our brands, including Green Mountain Coffee®, Keurig® and Tully’s Coffee® and our licensed co-branded Newman’s Own Organic® coffees, are important to our success and that the importance of brand recognition may increase to the extent that competitors offer products similar to ours. Many of our current and potential competitors have substantially greater financial, marketing and operating resources and access to capital than we do. Our primary competitors in specialty coffee include Dunkin’ Donuts, New England Coffee Company, Peet’s Coffee & Tea, Starbucks Corporation, The J.M. Smucker Company (with the Millstone® brand and The Folgers Coffee Company subsidiary) and Kraft Foods, Inc. (with the Gevalia® Kaffe brand). There are numerous smaller, regional brands that also compete in the specialty coffee business. In addition, we compete indirectly against all other coffee brands in the marketplace. A number of nationwide coffee marketers, such as The Folgers Coffee Company (a subsidiary of The J.M Smucker Company), Kraft Foods, Inc., Nestlé USA, Procter & Gamble, Inc., and Sara Lee Corporation are distributing premium coffee brands in supermarkets. These premium coffee brands may serve as substitutes for our coffee. If we do not succeed in effectively differentiating ourselves from our competitors in specialty coffee, including by developing and maintaining our brands, or our competitors adopt our strategies, then our competitive position may be weakened and our sales of specialty coffee, and accordingly our profitability, may be materially adversely affected.

Because all of our single-cup brewers are manufactured by a single manufacturer in China, a significant disruption in the operation of this manufacturer or political unrest in China could materially adversely affect us.

We have only one manufacturer of single-cup brewers. Any disruption in production or inability of our manufacturer to produce adequate quantities to meet our needs, whether as a result of a natural disaster or other

8

causes, could significantly impair our ability to operate our business on a day-to-day basis. Furthermore, our manufacturer is located in China. This exposes us to the possibility of product supply disruption and increased costs in the event of changes in the policies of the Chinese government, political unrest or unstable economic conditions in China, or developments in the U.S. that are adverse to trade, including enactment of protectionist legislation. Any of these matters could materially adversely affect us.

Product recalls and/or product liability may adversely impact us.

We are subject to regulation by a variety of regulatory authorities, including the Consumer Product Safety Commission. In the event our manufacturer of single-cup brewers, which is located in China, does not adhere to product safety requirements or our quality control standards, we might not identify a deficiency before brewers ship to our customers. The failure of our third party manufacturer to produce merchandise that adheres to our quality control standards could damage our reputation and brands and lead to customer litigation against us. If our manufacturer is unable or unwilling to recall products failing to meet our quality standards, we may be required to remove merchandise or recall those products at a substantial cost to us. We may be unable to recover costs related to product recalls.

We may not be able to enter into license agreements with coffee roasters and other third parties to manufacture, distribute and sell K-Cups® or maintain our current license agreements, or it may be expensive to do so. In addition, our current licensees may fail to perform their obligations under existing licensing agreements.

We license the right to manufacture, distribute and sell K-Cups on an exclusive or non-exclusive basis to gourmet coffee roasters and tea packers in return for royalty payments from the licensees when they ship the K-Cups. Although many licensees are willing to enter into such licensing agreements, there can be no assurance that such agreements will be negotiated on terms favorable to us, or at all. In addition, our current licensees may fail to perform their obligations under such licensing agreements due to operational disruptions, economic hardship or bankruptcy. Our failure to enter into similar licensing agreements in the future or the failure of our licensees to perform their obligations under existing license agreements could limit our ability to develop and sell our products and could cause our business to suffer.

We also have an exclusive coffee license agreement with Newman’s Own® Organics. We produce a line of several co-branded Newman’s Own Organics coffees under the Newman’s Own Organics and Green Mountain Coffee® brand names. In addition, from time to time, we enter into licensing agreements to allow for the development, marketing and sale of single-cup brewing systems by other companies. We recently announced license and distribution agreements with Conair Corporation for the Mr. Coffee® brand and Jarden Corporation for the Cuisinart® brand. The failure to maintain these agreements could adversely impact our future growth.

Our increasing reliance on a limited number of specialty farms could impair our ability to maintain or expand our business.

Because an increasing amount of our supply of Arabica coffee beans comes from specifically identified specialty farms, estates, and cooperatives, we are more dependent upon a limited number of suppliers than some of our competitors. In fiscal 2009, approximately 41% of our green coffee purchases were “farm-identified”. The timing of these purchases is dictated by when the coffee becomes available (after the annual crop), which does not always coincide with the period in which we need green coffee to fulfill customer demand. This can lead to higher and more variable inventory levels. Any deterioration of our relationship with these suppliers, or problems experienced by these suppliers, could lead to inventory shortages. In such case, we may not be able to fulfill the demand of existing customers, supply new customers, or expand other channels of distribution. A raw material shortage could result in decreased revenue or could impair our ability to maintain or expand our business.

9

Our business is highly dependent on sales of specialty coffee, and if demand for specialty coffee decreases, our business would suffer.

Substantially all of our revenues are dependent on demand for specialty coffee. In addition, demand for specialty coffee is a driving factor in the sales of our Keurig® single-cup brewing systems. Demand for specialty coffee and demand for our Keurig single-cup brewing systems is affected by many factors, including:

| | • | | Changes in consumer tastes and preferences; |

| | • | | Changes in consumer lifestyles; |

| | • | | National, regional and local economic conditions; |

| | • | | Perceptions or concerns about the environmental impact of our products; |

| | • | | Demographic trends; and |

| | • | | Perceived or actual health benefits or risks. |

Because we are highly dependent on consumer demand for specialty coffee, a shift in consumer preferences away from specialty coffee or our product offerings would harm our business more than if we had more diversified product offerings. If customer demand for our specialty coffee decreases, our sales would decrease and we would be materially adversely affected.

Our roasting methods are not proprietary, so competitors may be able to duplicate them, which could harm our competitive position.

We consider our roasting methods essential to the flavor and richness of our coffee and, therefore, essential to our various brands. Because our roasting methods cannot be patented, we would be unable to prevent competitors from copying our roasting methods if such methods became known. If our competitors copy our roasting methods, the value of our brands could be diminished and we could lose customers to our competitors. In addition, competitors could develop roasting methods that are more advanced than ours, which could also harm our competitive position.

We depend on the expertise of key personnel. If these individuals leave or change their role within the Company without effective replacements, our operations could suffer.

The success of our business is dependent to a large degree on our President and Chief Executive Officer, Lawrence J. Blanford, and the other members of our management team. We have an employment agreement with Mr. Blanford that expires on May 3, 2012. If Mr. Blanford or the other members of our management team leave without effective replacements, our ability to implement our business strategy could be impaired.

We may be able to incur substantial additional indebtedness in the future, which could restrict our ability to operate our business.

We may be able to incur substantial additional indebtedness in the future. In addition, future disruptions in the financial markets, such as have been recently experienced, could affect our ability to obtain new or additional debt financing or to refinance our existing indebtedness on favorable terms (or at all), and have other adverse effects on us. We have a $225 million revolving credit facility. On June 29, 2009, we exercised our increase option in the form of a $50 million term loan, to be amortized at the rate of 10% annually, commencing on September 30, 2009. All borrowings under the credit agreement, including the outstanding balance under the term loan, are due on December 3, 2012. In addition, on June 29, 2009, we amended the credit facility to remove the capital expenditures limitation covenant and adjusted the definition of the fixed charge coverage ratio to modify the capital expenditures captured in the definition to 50% of unfinanced capital expenditures. As of September 26, 2009 approximately $50 million was outstanding under our term loan and $28 million was outstanding on our revolving line of credit under this credit facility. The incurrence of debt under our credit facility could adversely affect our business. Our debt obligations could:

| | • | | Increase our vulnerability to general adverse economic and industry conditions; |

10

| | • | | Require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow for other purposes; |

| | • | | Impair our rights to our intellectual property, which have been pledged as collateral under our credit facility, upon the occurrence of a default; |

| | • | | Limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate, thereby placing us at a competitive disadvantage compared to our competitors that may have less debt; and |

| | • | | Limit, by the financial and other restrictive covenants in our debt agreements, our ability to borrow additional funds and have a material adverse effect on us if we fail to comply with the covenants in our debt agreements because such failure could result in an event of default which, if not cured or waived, could result in a substantial amount of our indebtedness becoming immediately due and payable. |

A significant interruption in the operation of our roasting, manufacturing or distribution capabilities could materially adversely affect us.

We currently roast our coffee at three facilities: Waterbury, Vermont; Knoxville, Tennessee; and Seattle, Washington. In addition, as part of the Timothy’s acquisition on November 13, 2009, we added a fourth manufacturing facility in Toronto, Canada. We expect to be able to meet current and forecasted demand for the near term. However, if demand increases more than we currently forecast, we will need to either expand our current roasting capabilities internally or acquire additional roasting capacity and the failure to do so in a timely or cost effective manner could have a negative impact on our business. Significant interruption in the operation of our current facilities, whether as a result of a natural disaster or other causes, could significantly impair our ability to operate our business on a day-to-day basis.

In addition, we and other licensed coffee roasters manufacture the K-Cups® sold for use with our single-cup brewer systems. We manufacture K-Cups at our Vermont, Tennessee and Washington State facilities, and any significant disruption in our or our licensees ability to manufacture adequate quantities of K-Cups to meet our needs, whether as a result of a natural disaster or other causes, could adversely affect our business and financial results. We currently have three distribution facilities, one located adjacent to our roasting facility in Waterbury, Vermont, another located in Essex, Vermont and a third at our facility in Knoxville, Tennessee. Any disruption to our distribution facilities could significantly impair our ability to operate our business. In addition, because we have our coffee roasting and primary distribution facilities in Vermont, our ability to ship coffee and receive shipments of raw materials could be adversely affected during winter months as a result of severe winter conditions and storms.

Our order processing and fulfillment systems may fail or limit user traffic, which could cause us to lose sales.

We processes all customer orders through an order fulfillment facility in Waterbury, Vermont. We are dependent on our ability to maintain our computer and telecommunications equipment at this facility in effective working order and to protect against damage from fire, natural disaster, power loss, telecommunications failure or similar events. In addition, growth of our customer base may strain or exceed the capacity of our systems and lead to degradations in performance or systems failure. We have experienced capacity constraints in the past that have resulted in decreased levels of customer service, such as increased customer call center wait times and delays in service to customers for limited periods of time. Although we continually review and consider upgrades to our order fulfillment infrastructure and provide for system redundancies to limit the likelihood of systems overload or failure, substantial damage to our systems or a systems failure that causes interruptions for a number of days could adversely affect our business. Additionally, if we are unsuccessful in updating and expanding our order fulfillment infrastructure, our ability to grow may be constrained.

11

Our reliance on a single order fulfillment company for our Keurig subsidiary’s at home business exposes us to significant credit risk.

We rely on a single order fulfillment company, M.Block & Sons, Inc., to process the majority of orders for our At-Home (AH) single-cup business sold through retailers. We sell a significant number of brewers and K-Cups® to this third party fulfillment company for re-sale to certain retailers. Receivables from this company were approximately 51% of our consolidated accounts receivable balance at September 26, 2009. Accordingly, we are subject to significant credit risk regarding the creditworthiness of this company. The inability of this company to perform its obligations to us, whether due to a deterioration in its financial condition or otherwise, could result in significant losses that could materially adversely affect us. If our relationship with this company is terminated, we can provide no assurance that we would be able to contract with another third party to provide these services to use in a timely manner or on favorable terms.

Because we rely heavily on common carriers to deliver our coffee and brewers, any disruption in their services or increase in shipping costs could adversely affect our business.

We rely on a number of common carriers to deliver coffee and brewers to our customers and distribution centers. We have no control over these common carriers and the services provided by them may be interrupted as a result of labor shortages, contract disputes or other factors. If we experience an interruption in these services, we may be unable to ship our products in a timely manner. A delay in shipping could:

| | • | | Have an adverse impact on the quality of the coffee, hot cocoa or tea shipped, and thereby adversely affect our brands and reputation; |

| | • | | Result in the disposal of an amount of coffee, hot cocoa or tea that could not be shipped in a timely manner; and |

| | • | | Require us to contract with alternative, and possibly more expensive, common carriers. |

Any significant increase in shipping costs could lower our profit margins or force us to raise prices, which could cause our revenue and profitability to suffer.

Our acquisition of certain assets from Tully’s Coffee Corporation was completed on March 27, 2009, and our acquisition of the wholesale business of Timothy’s Coffee of the World, Inc., was completed on November 13, 2009 . The failure to successfully integrate Tully’s and Timothy’s wholesale businesses into our business may cause us to fail to realize the expected synergies, cost savings and other benefits expected from these acquisitions, which could significantly affect us.

The integration of these wholesale businesses into our business presents significant challenges and risks to our business, including:

| | • | | Distraction of management from regular business concerns; |

| | • | | Assimilation and retention of employees and customers of Tully’s and Timothy’s; |

| | • | | Managing the West Coast-based Tully’s wholesale operations and employees, both of which are distant from our current headquarters and operation locations; |

| | • | | Managing the Canadian-based Timothy’s wholesale operations and employees, both of which are distant from our current headquarters and operation locations; |

| | • | | Expansion into new geographies; |

| | • | | Integration of technologies, services and products; and |

| | • | | Achievement of appropriate internal control over financial reporting. |

We may fail to successfully complete the integration of these businesses into our business and, as a result, may fail to realize the synergies, cost savings and other benefits expected from these acquisitions. We may fail to

12

grow and build profits in the Tully’s or Timothy’s business lines or achieve sufficient cost savings through the integration of customer service or administrative and other operational activities. Furthermore, we must achieve these objectives without adversely affecting our revenues. If we are not able to successfully achieve these objectives, the anticipated benefits of these acquisitions may not be realized fully or at all, or it may take longer to realize them than expected, and our results of operations could be materially adversely affected.

Tully’s has a history of operating losses, and our ability to achieve and then maintain the profitability of its business lines will depend on our ability to manage and control operating expenses and to generate and sustain increased levels of revenue. Our expectation to achieve profitability from this business may not be realized, and losses on the Tully’s business may continue as we integrate its operations into our business.

Strategic investments or acquisitions may result in additional risks and uncertainties in our business.

We may seek to grow our business through opportunistic strategic investments or acquisitions. From time to time we may be in various stages of negotiation with parties relating to the possible investment in or acquisition of businesses or assets, including our current discussions with Diedrich Coffee, Inc. We are unable to predict whether our negotiations will result in any agreement to invest in or acquire a business or an asset or whether any such transaction will be consummated on favorable terms or at all. Additionally, we may pursue an acquisition that is not accretive initially due to its long term strategic value.

In addition, to the extent we are successful in completing one or more opportunistic strategic investments or acquisitions, we would face numerous risks and uncertainties integrating the relevant businesses and systems, including the need to combine accounting and data processing systems and management controls and to retain relationships with customers and business partners.

Due to the seasonality of many of our products and other factors, our operating results are subject to quarterly fluctuations.

Historically, we have experienced increased sales of our Keurig® single-cup brewing systems in our first fiscal quarter due to the holiday season. Because of the seasonality of our business, results for any quarter are not necessarily indicative of the results that may be achieved for the full fiscal year. The impact on sales volume and operating results due to the timing and extent of these factors can significantly impact our business. For these reasons, quarterly operating results should not be relied upon as indications of our future performance.

Risks Related to our Industry

Increases in the cost of high-quality Arabica coffee beans or cost of materials used to produce our brewers could reduce our gross margin and profit.

We utilize a combination of outside brokers and direct relationships with farms, estates, cooperatives and cooperative groups for our supply of green coffees. Outside brokers provide the largest supply of our green coffee. The supply and price of coffee are subject to high volatility. Although most coffee trades in the commodity market at a price referred to as the “c” price (the price per pound quoted by the Coffee, Sugar and Cocoa Exchange), coffee of the quality we are seeking tends to trade on a negotiated basis at a substantial premium or “differential” above the “c” price, depending upon the supply and demand at the time of purchase. Supply and price can be affected by multiple factors, such as weather, pest damage, politics and economics in the producing countries.

Cyclical swings in commodity markets are common and the most recent years have been especially volatile for the “c” price of coffee. The “c” price of coffee declined during fiscal 2009, consistent with most other commodity markets, as compared to fiscal 2008 when “c” prices had reached record levels for the 5-year historical period. It is expected that coffee prices will remain volatile in the coming years. In addition to the “c”

13

price, coffee of the quality sought by us tends to trade on a negotiated basis at a substantial premium or “differential” above the “c” price. These differentials also are subject to significant variations and have generally been on the rise in recent years.

We generally try to pass on coffee price increases and decreases to our customers. There can be no assurance that we will be successful in passing on these cost increases to customers without losses in sales volume or gross margin. Additionally, even if higher green coffee costs can be offset on a dollar-for-dollar basis by price increases, this still lowers our gross margin as a percentage of sales. Similarly, rapid and sharp decreases in the cost of green coffee could also force us to lower sales prices before realizing cost reductions in our green coffee inventory and purchase commitments.

Significant fluctuations in the cost of other commodities, such as steel, petroleum and copper influence prices of plastic and other components used in manufacturing our coffee brewers. Approximately 96% of Keurig brewers shipped in fiscal 2009, were sold to the AH channel at our cost with essentially no gross margin. With respect to the Keurig single-cup AH system, we are continuing to pursue a model designed to penetrate the marketplace, a component of which is to sell brewers and accessories essentially at cost, and are focused on driving new customers into single serve coffee. Any rapid, sharp increases in our cost of manufacturing AH brewers would be unlikely to lead us to raise sales prices to offset such increased cost as our current strategy is to drive penetration and not risk slowing down the rate of sales growth to competitors or before realizing cost reductions in our purchase commitments. There can be no assurance that we will able to maintain our gross margin when such fluctuations occur.

Decreased availability of high-quality Arabica coffee beans could jeopardize our ability to maintain or expand our business.

We roast over 40 different types of green coffee beans to produce more than 100 coffee selections. If one type of green coffee bean were to become unavailable or prohibitively expensive, we believe we could substitute another type of coffee of equal or better quality meeting a similar taste profile. However, a worldwide supply shortage of the high-quality Arabica coffees we purchase could have a material adverse impact on us.

Worldwide or regional shortages of high-quality Arabica coffees can be caused by multiple factors, such as weather, pest damage and economics in the producing countries. In addition, the political situation in many of the Arabica coffee growing regions, including Africa, Indonesia, and Central and South America, can be unstable, and such instability could affect our ability to purchase coffee from those regions. If Arabica coffee beans from a region become unavailable or prohibitively expensive, we could be forced to discontinue particular coffee types and blends or substitute coffee beans from other regions in our blends. Frequent substitutions and changes in our coffee product lines could lead to cost increases, customer alienation and fluctuations in our gross margins.

While production of commercial grade coffee is generally on the rise, many industry experts are concerned about the ability of specialty coffee production to keep pace with demand. Arabica coffee beans of the quality we purchase are not readily available on the commodity markets. We depend on our relationships with coffee brokers, exporters and growers for the supply of our primary raw material, high-quality Arabica coffee beans. In particular, the supply of Fair Trade Certified™ coffees is limited. We may not be able to purchase enough Fair Trade Certified coffees to satisfy the rapidly increasing demand for such coffees, which could impact our revenue growth.

The recent adverse changes in global and domestic economic conditions or a worsening of the United States economy could materially adversely affect us.

Our revenues and performance depend significantly on consumer confidence and discretionary spending, which have recently deteriorated due to current worldwide economic conditions. This economic downturn and decrease in consumer spending may adversely impact our revenues, ability to market our products, build customer loyalty,

14

or otherwise implement our business strategy and further diversify the geographical concentration of our operations. For example, we are highly dependent on consumer demand for specialty coffee and a shift in consumer demand away from specialty coffee due to economic or other consumer preferences would harm our business. Keurig brewer sales may also decline as a result of the economic environment. We also have exposure to various financial institutions under coffee hedging arrangements and interest rate swaps, and the risk of counterparty default is currently higher in light of existing capital market and economic conditions.

Our products must comply with government regulation.

The USDA adopted regulations with respect to a national organic labeling and certification program which became effective in February 2001, and fully implemented in October 2002. Amendments to Canada’s Organic Products regulations as administered by the Canada Organic Office of the Canadian Food Inspection Agency became effective in December 2008. Although the implementation period has not yet been defined, we will be required to apply for recertification of our organic products under the new regulations and update any affected packaging. In addition, similar regulations and requirements exist in the other countries in which we may market our products. Our organic products are covered by these various regulations. Future developments in the regulation of labeling of organic foods could require us to further modify the labeling of our products, which could affect the sales of our products and thus harm our business.

Furthermore, new government laws and regulations may be introduced in the future that could result in additional compliance costs, seizures, confiscations, recalls or monetary fines, any of which could prevent or inhibit the development, distribution and sale of our products. If we fail to comply with applicable laws and regulations, we may be subject to civil remedies, including fines, injunctions, recalls or seizures, as well as potential criminal sanctions, which could have a material adverse effect on us.

We rely on independent certification for a number of our products, the loss of any of which could harm our business.

We rely on independent certification, such as certifications of our products as “organic” or “fair trade,” to differentiate our products from others. The Newman’s Own® Organics product line, combined with the Specialty Coffee business unit’s own branded Fair Traded Certified™ coffee line, represented a combined 30% of the Specialty Coffee business unit’s total consolidated sales volume in fiscal year 2009. The loss of any independent certifications could adversely affect our marketplace position, which could harm our business.

We must comply with the requirements of independent organizations or certification authorities in order to label our products as certified. For example, we can lose our “organic” certification if a manufacturing plant becomes contaminated with non-organic materials or if it is not properly cleaned after a production run. In addition, all raw materials must be certified organic.

| Item 1B. | Unresolved Staff Comments |

None.

SCBU owns a 72,000 square foot warehousing and distribution facility adjacent to our manufacturing plant in Waterbury, Vermont. The land underneath this facility is leased and the lease for the land expires in 2024.

The Company owns a manufacturing and warehousing facility located in Knoxville, Tennessee. The facility has approximately 334,500 square feet of usable space.

15

Our other facilities, all of which are leased, are as follows:

| | | | | | |

Type | | Location | | Approximate

Square Feet | | Expiration

of Lease |

SCBU Manufacturing Space | | Essex, VT Sumner, WA Waterbury, VT | | 99,000

197,800 98,000 | | 2012

2015 2017 |

| | | |

SCBU Warehouse/Distribution/Service/Retail Space | | Wilmington, MA Southington, CT Demeritt Place (I), Waterbury, VT

112 Main Street, Waterbury, VT

Waterbury, VT (Factory Outlet)

Waterbury, VT (Visitor Center)

Biddeford, ME

Latham, NY

Marshall Avenue, Williston, VT | | 17,500 11,200 12,000

3,000

2,000 2,900 10,000

7,500 70,500 | | 2013

2011

2010

2010

2010

2026 2011 2013 2012 |

| | | |

SCBU Administrative and Corporate Offices | | Coffee Lane, Waterbury, VT

Demeritt Place (II), Waterbury,VT 46 Main Street, Waterbury, VT

152 Main Street, Waterbury, VT

Pilgrim Park II, Waterbury, VT

Pilgrim Park V, Waterbury VT

5 New England, Essex, VT | | 3,000

10,00010,900 9,600 22,900 15,000 10,000 | | 2010

2010

2011

20182011 2016 2013 |

| | | |

Keurig Administrative Offices | | Reading, MA

Woburn, MA | | 72,000

7,600 | | 2015

2010 |

In addition to the locations listed above, the Company has inventory at various locations managed by third party warehouses and order fulfillment companies.

We believe our facilities are generally adequate for our current needs and for the remainder of fiscal 2010.

None.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matters were submitted to a vote of security holders during the fiscal quarter ended September 26, 2009.

16

Executive Officers of the Registrant

Certain biographical information regarding each executive officer of our Company is set forth below:

| | | | | | |

Name | | Age | | Position | | Officer

since |

Lawrence J. Blanford | | 56 | | President, Chief Executive Officer and Director | | 2007 |

Kathryn S. Brooks | | 54 | | Vice President, Human Resources and Organizational Development | | 2001 |

Howard Malovany | | 59 | | Vice President, Corporate General Counsel and Secretary | | 2009 |

R. Scott McCreary | | 50 | | Chief Operating Officer | | 2004 |

Frances G. Rathke | | 49 | | Vice President, Chief Financial Officer, and Treasurer | | 2003 |

Stephen J. Sabol | | 48 | | Vice President of Development | | 1993 |

Michelle V. Stacy | | 53 | | President of Keurig, Incorporated | | 2008 |

Lawrence J. Blanford has served as President, Chief Executive Officer and Director since May 2007. From May 2005 to October 2006, Mr. Blanford held the position of Chief Executive Officer at Royal Group Technologies Ltd., a Canadian building products and home improvements company. From January 2004 to May 2005, Mr. Blanford was Founder and President of Strategic Value Consulting, LLC, a consultancy.

Kathryn S. Brooks has served as Vice President of Human Resources and Organizational Development since April 2001. She was also a Director of the Company from March 2002 to September 2006.

Howard Malovanyhas served as Vice President, Corporate General Counsel and Secretary since February 2009. From 1996 to 2009, Mr. Malovany worked with the Wm. Wrigley Jr. Company, serving most recently as Senior Vice President, Secretary and General Counsel.

R. Scott McCrearyhas served as Chief Operating Officer of the Company since September 2004.

Frances G. Rathke has served as Vice President, Chief Financial Officer and Treasurer of the Company since October 2003.

Stephen J. Sabolhas served as Vice President of Development of the Company since October 2001.

Michelle V. Stacyhas served as President of Keurig, Incorporated since November 2008. From October 2007 to October 2008, Ms. Stacy served as Managing Partner of Archpoint Consulting, a professional services firm. From October 2005 to October 2007, Ms. Stacy was Vice President and General Manager of Global Professional Oral Care with Procter & Gamble. From 1983 to 2005, Ms. Stacy held various executive positions with The Gillette Company.

17

PART II

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Securities |

Price Range of Securities

The Company’s common stock trades on the NASDAQ Global Market under the symbol GMCR. The following table sets forth the high and low closing prices as reported by NASDAQ for the periods indicated as adjusted to reflect the three-for-two stock split effected on June 8, 2009.

| | | | | | |

| | | | | High | | Low |

Fiscal 2008 | | 13 weeks ended December 29, 2007 13 weeks ended March 29, 2008 13 weeks ended June 28, 2008 13 weeks ended September 27, 2008 | | $27.65

$27.75

$29.39

$26.83 | | $19.93

$16.83

$21.10

$21.65 |

Fiscal 2009 | | 13 weeks ended December 27, 2008 13 weeks ended March 28, 2009 13 weeks ended June 27, 2009 13 weeks ended September 26, 2009 | | $27.14

$32.65

$62.57

$70.44 | | $16.24

$22.13

$30.99

$55.61 |

Number of Equity Security Holders

As of November 23, 2009, the number of record holders of the Company’s common stock was 481.

Dividends

The Company has never paid a cash dividend on its common stock and anticipates that for the foreseeable future any earnings will be retained for use in its business and, accordingly, does not anticipate the payment of cash dividends.

Securities Authorized for Issuance Under Equity Compensation Plans

| | | | | | | |

Plan category | | Number of securities

to be issued upon

exercise of

outstanding options,

warrants and rights | | Weighted

average exercise

price of

outstanding

options, warrants

and rights | | Number of securities

remaining available for

future issuance under

equity compensation plans

(excluding securities

reflected in column (a)) |

| | | (a) | | (b) | | (c) |

Equity compensation plans approved by security holders | | 3,300,125 | | $ | 12.83 | | 1,087,028 |

| | | | | | | |

Equity compensation plans not approved by security holders(1) | | 628,475 | | $ | 13.34 | | — |

| | | | | | | |

Total | | 3,928,600 | | $ | 12.91 | | 1,087,028 |

| | | | | | | |

| (1) | Includes compensation plans assumed in the Keurig acquisition and inducement grants to Lawrence Blanford, Howard Malovany and Michelle Stacy. See Note 16 of the Consolidated Financial Statements included in this Form 10-K. |

18

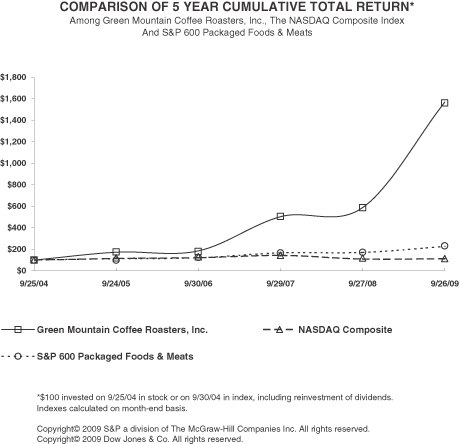

Performance graph

| Item 6. | Selected Financial Data |

The table below shows selected financial data for our last five fiscal years. Our fiscal year is based on a 52-week year for all years presented, except fiscal 2006 which was comprised of 53 weeks. There were no cash dividends paid during the past five fiscal years.

| | | | | | | | | | | | | | | | |

| | | Fiscal Years Ended |

| | | Sept. 26, 2009(1)(3) | | | Sept. 27, 2008(1) | | Sept. 29, 2007(1) | | Sept. 30, 2006(1) | | Sept. 24, 2005 |

| | | In thousands, except per share data |

Net sales | | $ | 803,045 | | | $ | 500,277 | | $ | 341,651 | | $ | 225,323 | | $ | 161,536 |

Income before equity in loss of Keurig, Incorporated | | $ | 55,882 | | | $ | 22,299 | | $ | 12,843 | | $ | 9,406 | | $ | 9,448 |

Net income | | $ | 55,882 | | | $ | 22,299 | | $ | 12,843 | | $ | 8,443 | | $ | 8,956 |

Net income per share—diluted | | $ | 1.39 | | | $ | 0.58 | | $ | 0.35 | | $ | 0.24 | | $ | 0.26 |

Total assets | | $ | 813,839 | | | $ | 357,648 | | $ | 264,527 | | $ | 234,006 | | $ | 91,147 |

Long-term debt | | $ | 73,013 | | | $ | 123,517 | | $ | 90,050 | | $ | 102,871 | | $ | 5,218 |

Stockholders’ equity | | $ | 590,174 | (2) | | $ | 139,520 | | $ | 99,099 | | $ | 74,940 | | $ | 60,392 |

| (1) | Fiscal 2009, 2008, 2007 and 2006 information presented reflects the acquisition of Keurig, Incorporated on June 15, 2006. |

| (2) | The fiscal 2009 stockholders’ equity balance reflects the impact of the August 12, 2009, equity offering. |

| (3) | Fiscal 2009 information presented reflects the acquisition of the wholesale business and certain assets of Tully’s Coffee Corporation. |

19

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion and analysis is intended to help you understand the results of operations and financial condition of Green Mountain Coffee Roasters, Inc. (together with its subsidiaries, the “Company”). You should read the following discussion and analysis in conjunction with our consolidated financial statements and related notes included elsewhere in this report.

Overview

We are a leader in the specialty coffee and the overall coffee maker businesses. We roast premium, high-quality Arabica bean coffees and offer over 100 coffee selections, including single-origins, estates, certified organics, Fair Trade Certified™, proprietary blends, and flavored coffees that sell under the Green Mountain Coffee®,, Newman’s Own® Organics and, as of March 27, 2009, Tully’s® Coffee brands. Additionally, as of November 13, 2009, we acquired the Timothy’s World Coffee® brand. We also sell cocoa, teas and coffees in K-Cup® portion packs, Keurig® single-cup brewers and other accessories. In recent years, a significant driver of the Company’s growth has been the sale of K-Cups and Keurig brewing systems.

Business Segments

The Company manages its operations through two operating segments, Specialty Coffee Business Unit (SCBU) formerly referred to as Green Mountain Coffee (GMC) and Keurig business unit (Keurig). We evaluate performance primarily based on segment income before taxes. Expenses not specifically related to either operating segment are recorded as “Corporate”.

SCBU sells whole bean and ground coffee, as well as K-Cups, and to a lesser extent, Keurig single-cup brewers and other accessories mainly in domestic wholesale and retail channels, and directly to consumers. The majority of SCBU’s revenue is derived from its North American wholesale channels.

Additionally, on March 27, 2009, the Company acquired certain assets of the Tully’s Coffee Corporation (Tully’s) which are included in SCBU. The SCBU began selling whole bean and ground coffee and coffee in K-Cups under the Tully’s brand in the third quarter of fiscal 2009.

Keurig is a pioneer and leading manufacturer of gourmet single-cup brewing systems and targets its premium patented single-cup brewing systems for consumers at home (AH) or away-from-home (AFH) mainly in North America. Keurig sells its AFH single-cup brewers to distributors for offices and its AH single-cup brewers to select retailers such as department stores and club stores and directly to consumers. Keurig sells coffee, tea and cocoa in K-Cups produced by a variety of roasters, including the SCBU, and related accessories to select retailers such as department stores and club stores and also directly to consumers. Keurig earns royalty income from K-Cups shipped by its licensed roasters.