Exhibit 99.1

Exhibit 99.1

STRATEGIES & STRENGTHS

2003 Investor Presentation February 2004

Forward-looking Statements and Risk Factors

This presentation, and other written materials and oral statements made by management, may contain certain forward-looking statements regarding the Company’s prospective performance and strategies within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The Company intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and is including this statement for purposes of said safe harbor provisions.

Forward-looking statements, which are based on certain assumptions and describe future plans, strategies, and expectations of the Company, are generally identified by use of the words “plan,” “believe,” “expect,” “intend,” “anticipate,” “estimate,” “project,” or other similar expressions. The Company’s ability to predict results or the actual effects of its plans and strategies, including the recent merger with Roslyn Bancorp, Inc., is inherently uncertain. Accordingly, actual results may differ materially from anticipated results.

The following factors, among others, could cause the actual results of the merger to differ materially from the expectations stated in this presentation: the ability to successfully integrate the companies following the merger, including the retention of key personnel; the ability to effect the proposed restructuring; the ability to fully realize the expected cost savings and revenues; and the ability to realize the expected cost savings and revenues on a timely basis.

Factors that could have a material adverse effect on the operations of the Company and its subsidiaries include, but are not limited to, changes in general economic conditions; interest rates, deposit flows, loan demand, real estate values, competition, and demand for financial services and loan, deposit, and investment products in the Company’s local markets; changes in the quality or composition of the loan or investment portfolios; changes in accounting principles, policies, or guidelines; changes in legislation and regulation; changes in the monetary and fiscal policies of the U.S. Government, including policies of the U.S. Treasury and the Federal Reserve Board; war or terrorist activities; and other economic, competitive, governmental, regulatory, geopolitical, and technological factors affecting the Company’s operations, pricing, and services.

The Company undertakes no obligation to update these forward-looking statements to reflect events or circumstances that occur after the date on which such statements were made.

2

Strength: Our Mission

Our primary goal is the creation of shareholder value.

The mission of New York Community Bancorp, Inc. is to create shareholder value by consistently delivering the thrift industry’s top financial performance, and by providing those who live and work in the New York metro region with easy access to the full range of financial products and services they seek.

3

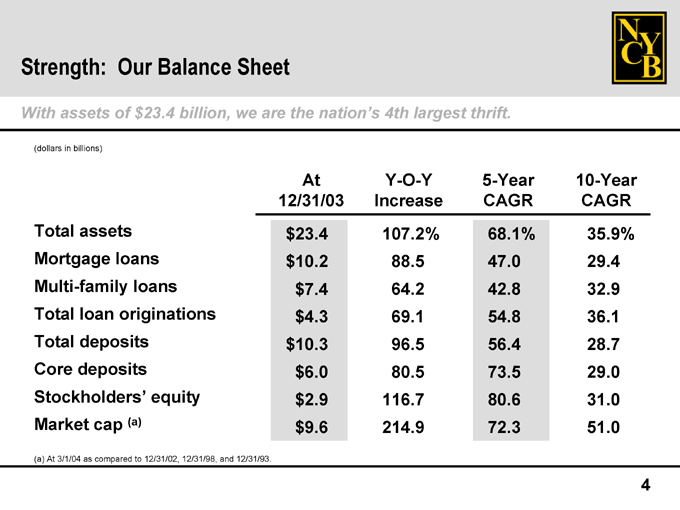

Strength: Our Balance Sheet

With assets of $23.4 billion, we are the nation’s 4th largest thrift.

(dollars in billions)

At Y-O-Y 5-Year 10-Year

12/31/03 Increase CAGR CAGR

Total assets $ 23.4 107.2% 68.1% 35.9%

Mortgage loans $ 10.2 88.5 47.0 29.4

Multi-family loans $ 7.4 64.2 42.8 32.9

Total loan originations $ 4.3 69.1 54.8 36.1

Total deposits $ 10.3 96.5 56.4 28.7

Core deposits $ 6.0 80.5 73.5 29.0

Stockholders’ equity $ 2.9 116.7 80.6 31.0

Market cap (a) $ 9.6 214.9 72.3 51.0

(a) At 3/1/04 as compared to 12/31/02, 12/31/98, and 12/31/93.

4

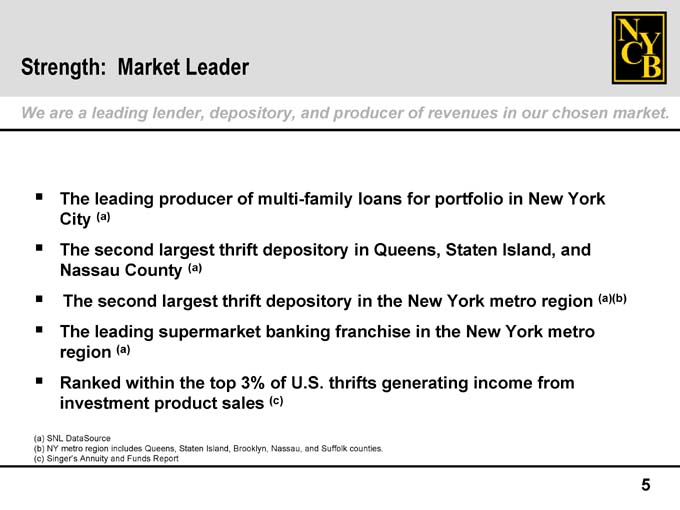

Strength: Market Leader

We are a leading lender, depository, and producer of revenues in our chosen market.

The leading producer of multi-family loans for portfolio in New York City (a) The second largest thrift depository in Queens, Staten Island, and Nassau County (a) The second largest thrift depository in the New York metro region (a)(b) The leading supermarket banking franchise in the New York metro region (a) Ranked within the top 3% of U.S. thrifts generating income from investment product sales (c)

(a) SNL DataSource

(b) NY metro region includes Queens, Staten Island, Brooklyn, Nassau, and Suffolk counties. (c) Singer’s Annuity and Funds Report

5

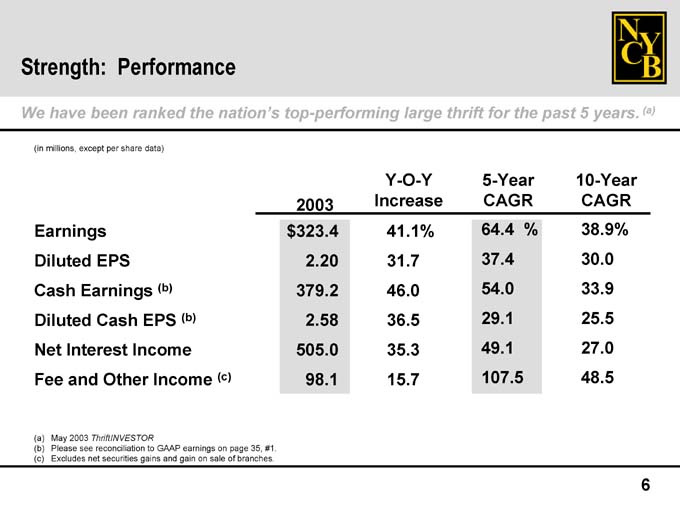

Strength: Performance

We have been ranked the nation’s top-performing large thrift for the past 5 years. (a)

(in millions, except per share data)

Y-O-Y 5-Year 10-Year

2003 Increase CAGR CAGR

Earnings $ 323.4 41.1% 64.4 % 38.9%

Diluted EPS 2.20 31.7 37.4 30.0

Cash Earnings (b) 379.2 46.0 54.0 33.9

Diluted Cash EPS (b) 2.58 36.5 29.1 25.5

Net Interest Income 505.0 35.3 49.1 27.0

Fee and Other Income (c) 98.1 15.7 107.5 48.5

(a) May 2003 ThriftINVESTOR

(b) Please see reconciliation to GAAP earnings on page 35, #1.

(c) Excludes net securities gains and gain on sale of branches.

6

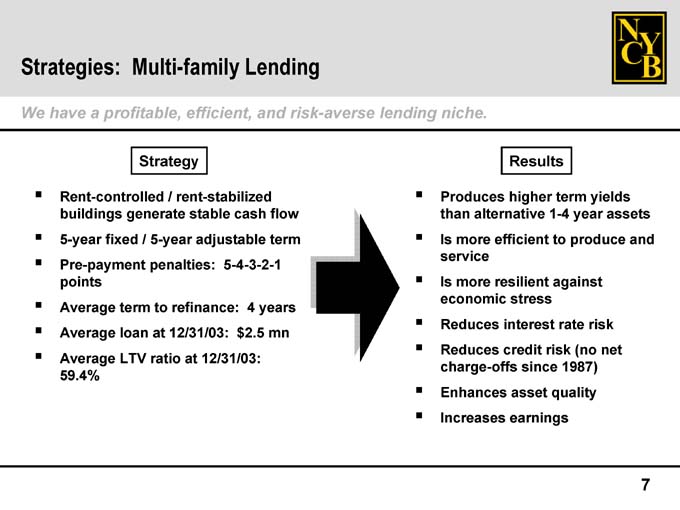

Strategies: Multi-family Lending

We have a profitable, efficient, and risk-averse lending niche.

Strategy Results

Rent-controlled / rent-stabilized Produces higher term yields

buildings generate stable cash flow than alternative 1-4 year assets

5-year fixed / 5-year adjustable term Is more efficient to produce and

service

Pre-payment penalties: 5-4-3-2-1

points Is more resilient against

economic stress

Average term to refinance: 4 years

Reduces interest rate risk

Average loan at 12/31/03: $2.5 mn

Reduces credit risk (no net

Average LTV ratio at 12/31/03:

charge-offs since 1987)

59.4%

Enhances asset quality

Increases earnings

7

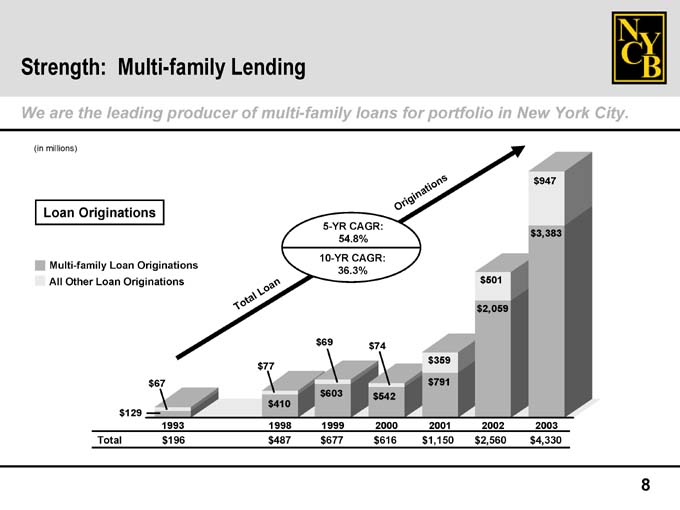

Strength: Multi-family Lending

We are the leading producer of multi-family loans for portfolio in New York City.

(in millions)

Loan Originations

5-YR CAGR:

$ 3,383

54.8%

10-YR CAGR:

Multi-family Loan Originations

36.3%

All Other Loan Originations $ 501

$ 2,059

$ 69 $ 74

$ 359

$ 77

$ 67 $ 791

$ 603 $ 542

$ 410

$ 129

1993 1998 1999 2000 2001 2002 2003

Total $ 196 $ 487 $ 677 $ 616 $ 1,150 $ 2,560 $ 4,330

8

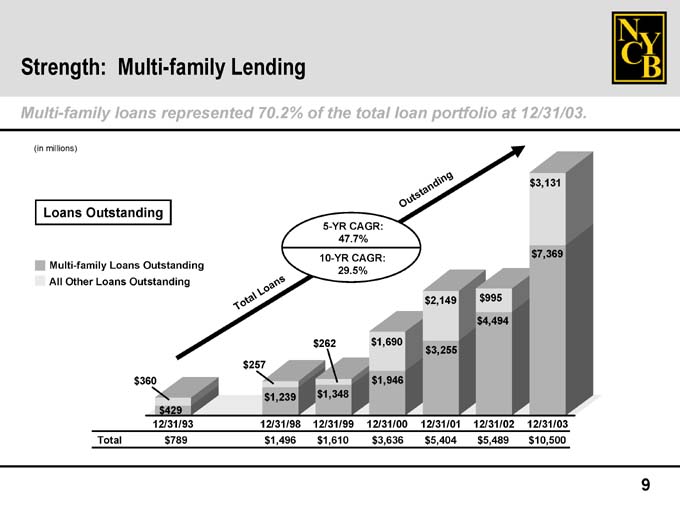

Strength: Multi-family Lending

Multi-family loans represented 70.2% of the total loan portfolio at 12/31/03.

(in millions)

n g $ 3,131

Loans Outstanding

Multi-family Loans Outstanding

All Other Loans Outstanding

Total Loans Outstanding

5-YR CAGR:

47.7%

10-YR CAGR:

29.5%

$3,131

$7,369

$ 995

$ 2,149

$ 4,494

$ 262 $ 1,690

$ 3,255

$ 257

$ 360 $ 1,946

$ 1,239 $ 1,348

$ 429

12/31/93 12/31/98 12/31/99 12/31/00 12/31/01 12/31/02 12/31/03

Total $ 789 $ 1,496 $ 1,610 $ 3,636 $ 5,404 $ 5,489 $ 10,500

9

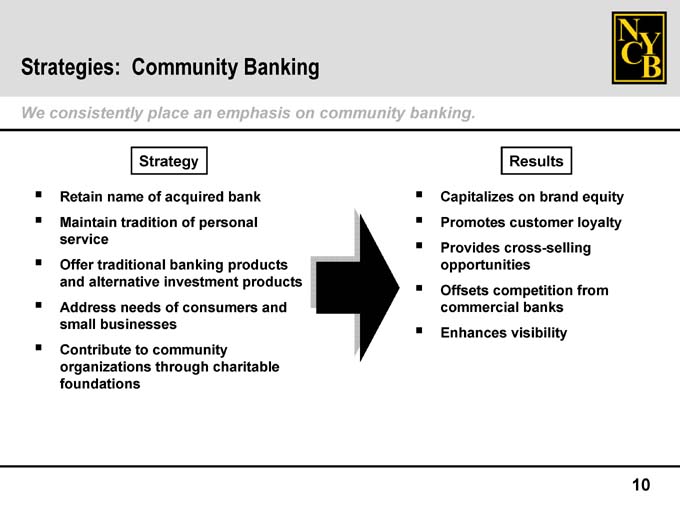

Strategies: Community Banking

We consistently place an emphasis on community banking.

Strategy Results

Retain name of acquired bank Capitalizes on brand equity

Maintain tradition of personal Promotes customer loyalty

service

Provides cross-selling

Offer traditional banking products opportunities

and alternative investment products

Offsets competition from

Address needs of consumers and commercial banks

small businesses

Enhances visibility

Contribute to community

organizations through charitable

foundations

10

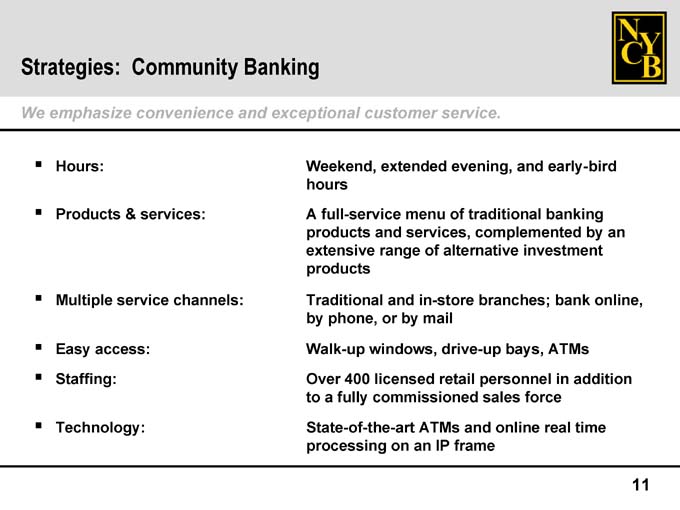

Strategies: Community Banking

We emphasize convenience and exceptional customer service.

Hours: Weekend, extended evening, and early-bird

hours

Products & services: A full-service menu of traditional banking

products and services, complemented by an

extensive range of alternative investment

products

Multiple service channels: Traditional and in-store branches; bank online,

by phone, or by mail

Easy access: Walk-up windows, drive-up bays, ATMs

Staffing: Over 400 licensed retail personnel in addition

to a fully commissioned sales force

Technology: State-of-the-art ATMs and online real time

processing on an IP frame

11

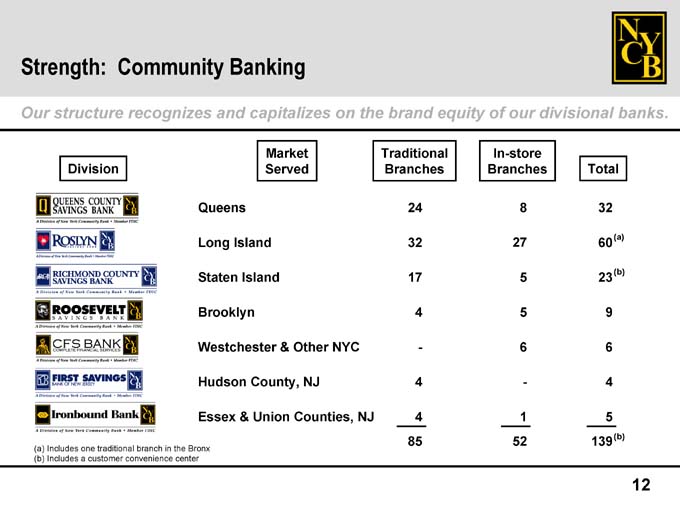

Strength: Community Banking

Our structure recognizes and capitalizes on the brand equity of our divisional banks.

Market Traditional In-store

Division Served Branches Branches Total

Queens 24 8 32

Long Island 32 27 60(a)

Staten Island 17 5 23(b)

Brooklyn 4 5 9

Westchester & Other NYC - 6 6

Hudson County, NJ 4 - 4

Essex & Union Counties, NJ 4 1 5

85 52 139(b)

(a) Includes one traditional branch in the Bronx (b) Includes a customer convenience center

12

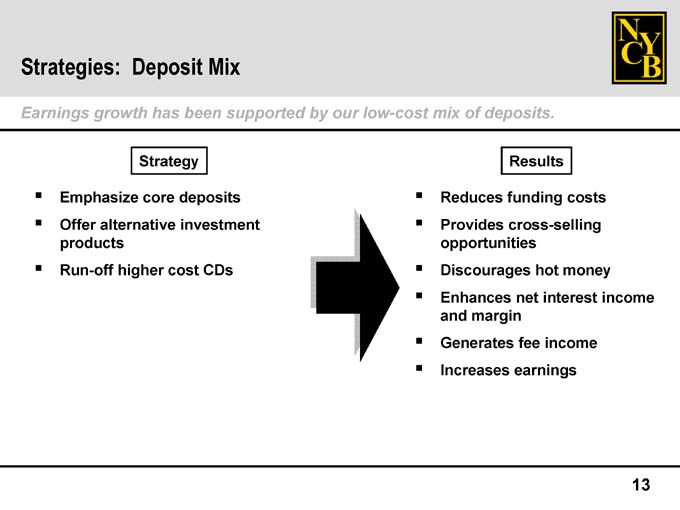

Strategies: Deposit Mix

Earnings growth has been supported by our low-cost mix of deposits.

Strategy Results

Emphasize core deposits Reduces funding costs

Offer alternative investment Provides cross-selling

products opportunities

Run-off higher cost CDs Discourages hot money

Enhances net interest income

and margin

Generates fee income

Increases earnings

13

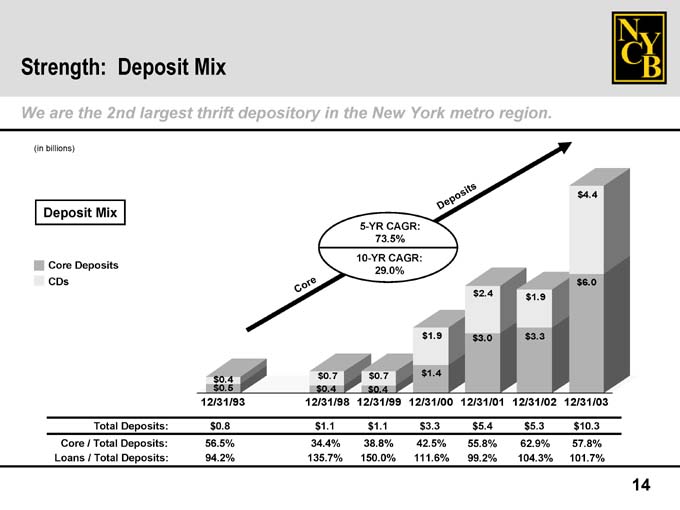

Strength: Deposit Mix

We are the 2nd largest thrift depository in the New York metro region.

(in billions)

Deposit Mix

5-YR CAGR:

73.5%

10-YR CAGR:

Core Deposits

29.0%

CDs

$ 2.4 $ 1.9

$ 1.9 $ 3.0 $ 3.3

$ 0.7 $ 0.7 $ 1.4

$ 0.4

$ 0.5 $ 0.4 $ 0.4

12/31/93 12/31/98 12/31/99 12/31/00 12/31/01 12/31/02 12/31/03

Total Deposits: $ 0.8 $ 1.1 $ 1.1 $ 3.3 $ 5.4 $ 5.3 $ 10.3

Core / Total Deposits: 56.5% 34.4% 38.8% 42.5% 55.8% 62.9% 57.8%

Loans / Total Deposits: 94.2% 135.7% 150.0% 111.6% 99.2% 104.3% 101.7%

14

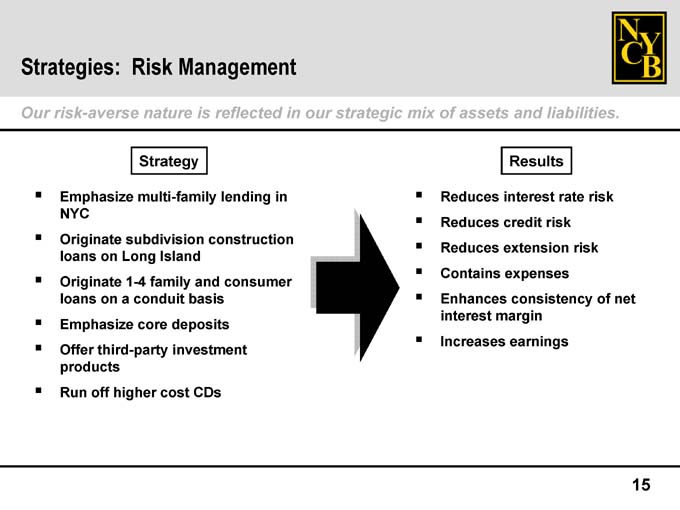

Strategies: Risk Management

Our risk-averse nature is reflected in our strategic mix of assets and liabilities.

Strategy Results

Emphasize multi-family lending in Reduces interest rate risk

NYC

Reduces credit risk

Originate subdivision construction

Reduces extension risk

loans on Long Island

Contains expenses

Originate 1-4 family and consumer

loans on a conduit basis Enhances consistency of net

interest margin

Emphasize core deposits

Increases earnings

Offer third-party investment

products

Run off higher cost CDs

15

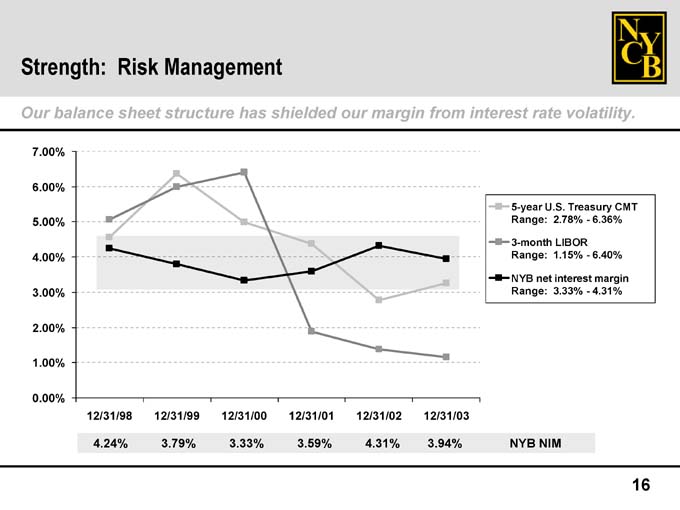

Strength: Risk Management

Our balance sheet structure has shielded our margin from interest rate volatility.

5-year U.S. Treasury CMT Range: 2.78%—6.36%

3-month LIBOR Range: 1.15%—6.40%

NYB net interest margin Range: 3.33%—4.31%

7.00%

6.00%

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

12/31/98 12/31/99 12/31/00 12/31/01 12/31/02 12/31/03

4.24% 3.79% 3.33% 3.59% 4.31% 3.94% NYB NIM

16

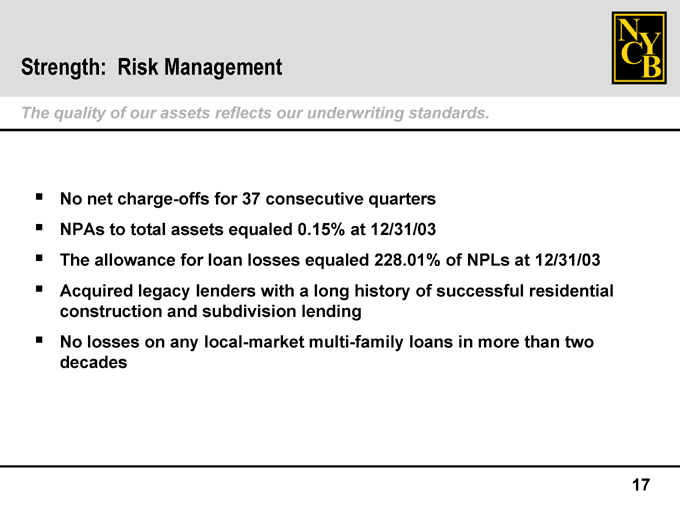

Strength: Risk Management

The quality of our assets reflects our underwriting standards.

No net charge-offs for 37 consecutive quarters

NPAs to total assets equaled 0.15% at 12/31/03

The allowance for loan losses equaled 228.01% of NPLs at 12/31/03

Acquired legacy lenders with a long history of successful residential construction and subdivision lending

No losses on any local-market multi-family loans in more than two decades

17

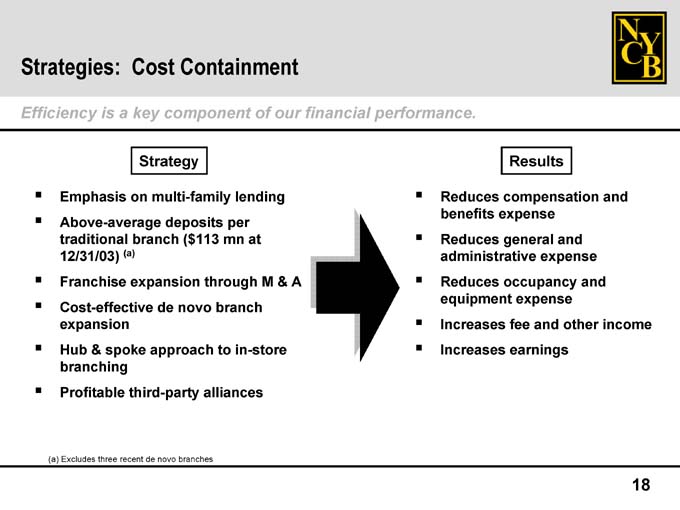

Strategies: Cost Containment

Efficiency is a key component of our financial performance.

Strategy Results

Emphasis on multi-family lending Reduces compensation and

benefits expense

Above-average deposits per

traditional branch ($113 mn at Reduces general and

12/31/03) (a) administrative expense

Franchise expansion through M & A Reduces occupancy and

equipment expense

Cost-effective de novo branch

expansion Increases fee and other income

Hub & spoke approach to in-store Increases earnings

branching

Profitable third-party alliances

(a) Excludes three recent de novo branches

18

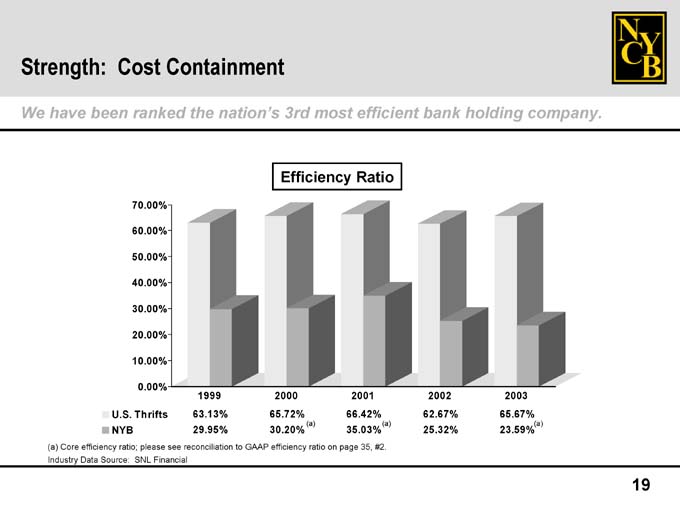

Strength: Cost Containment

We have been ranked the nation’s 3rd most efficient bank holding company.

Efficiency Ratio

70.00%

60.00%

50.00%

40.00%

30.00%

20.00%

10.00%

0.00%

1999 2000 2001 2002 2003

U.S. Thrifts 63.13% 65.72% 66.42% 62.67% 65.67%

(a) (a) (a)

NYB 29.95% 30.20% 35.03% 25.32% 23.59%

(a) Core efficiency ratio; please see reconciliation to GAAP efficiency ratio on page 35, #2. Industry Data Source: SNL Financial

19

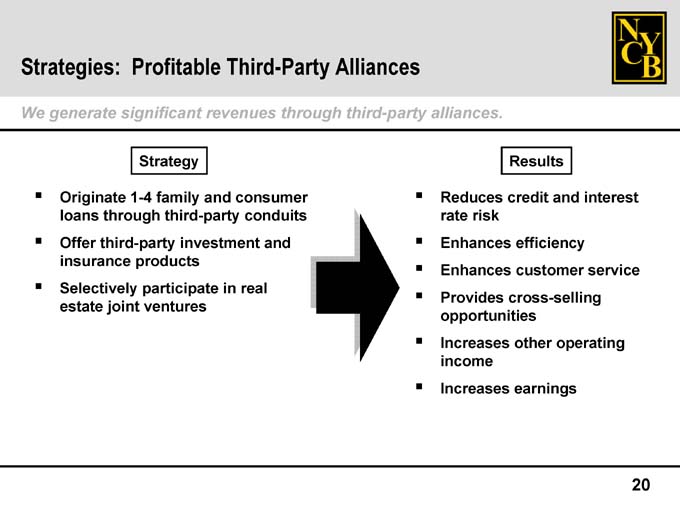

Strategies: Profitable Third-Party Alliances

We generate significant revenues through third-party alliances.

Strategy Results

Originate 1-4 family and consumer Reduces credit and interest

loans through third-party conduits rate risk

Offer third-party investment and Enhances efficiency

insurance products

Enhances customer service

Selectively participate in real

Provides cross-selling

estate joint ventures

opportunities

Increases other operating

income

Increases earnings

20

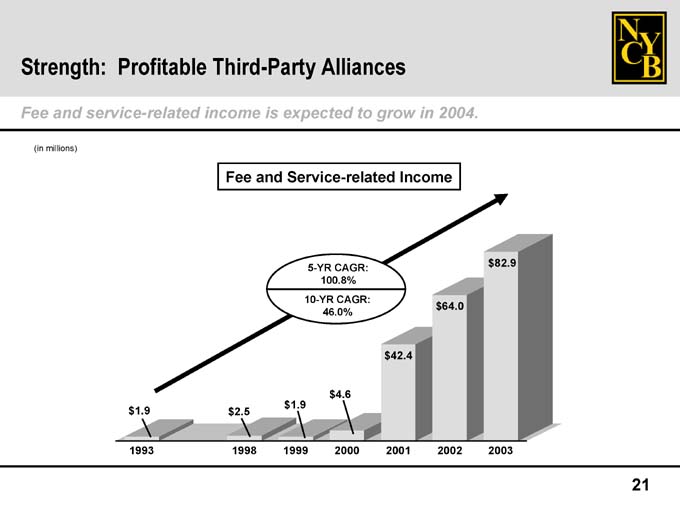

Strength: Profitable Third-Party Alliances

Fee and service-related income is expected to grow in 2004.

(in millions)

Fee and Service-related Income

5-YR CAGR: $ 82.9

100.8%

10-YR CAGR:

$ 64.0

46.0%

$ 42.4

$ 4.6

$ 1.9

$ 1.9 $ 2.5

1993 1998 1999 2000 2001 2002 2003

21

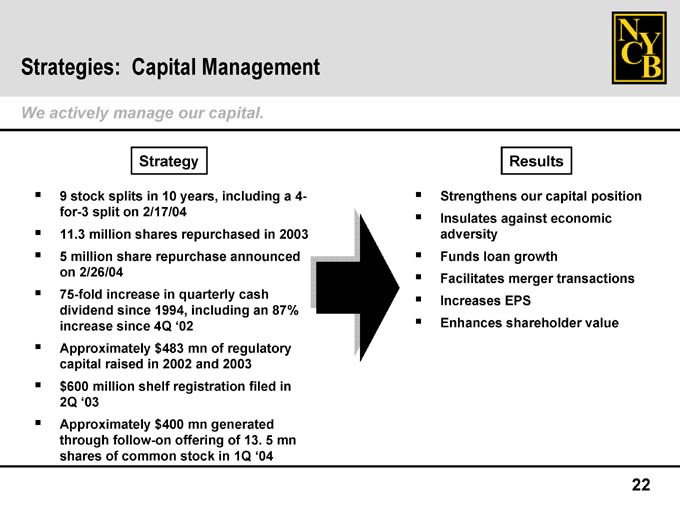

Strategies: Capital Management

We actively manage our capital.

Strategy Results

9 stock splits in 10 years, including a 4- Strengthens our capital position

for-3 split on 2/17/04

Insulates against economic

11.3 million shares repurchased in 2003 adversity

5 million share repurchase announced on 2/26/04

Facilitates merger transactions

75-fold increase in quarterly cash

Increases EPS

dividend since 1994, including an 87%

increase since 4Q ‘02 Enhances shareholder value

Approximately $483 mn of regulatory

capital raised in 2002 and 2003

$ 600 million shelf registration filed in

2Q ‘03

Approximately $400 mn generated

through follow-on offering of 13.5 mn

shares of common stock in 1Q ‘04

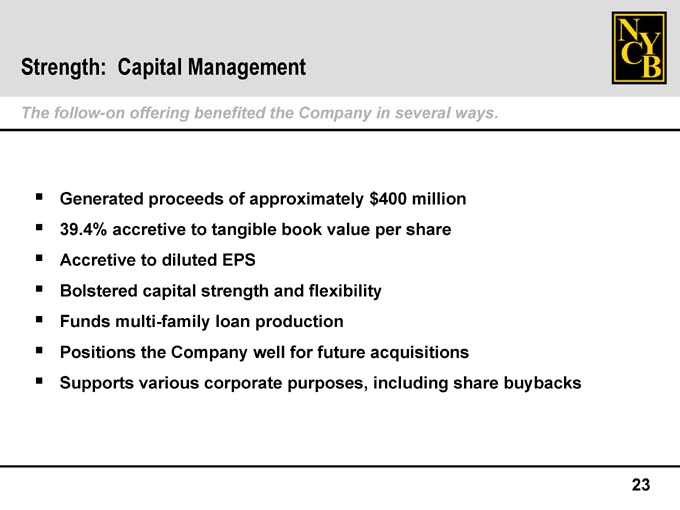

Strength: Capital Management

The follow-on offering benefited the Company in several ways.

Generated proceeds of approximately $400 million 39.4% accretive to tangible book value per share Accretive to diluted EPS

Bolstered capital strength and flexibility Funds multi-family loan production

Positions the Company well for future acquisitions

Supports various corporate purposes, including share buybacks

23

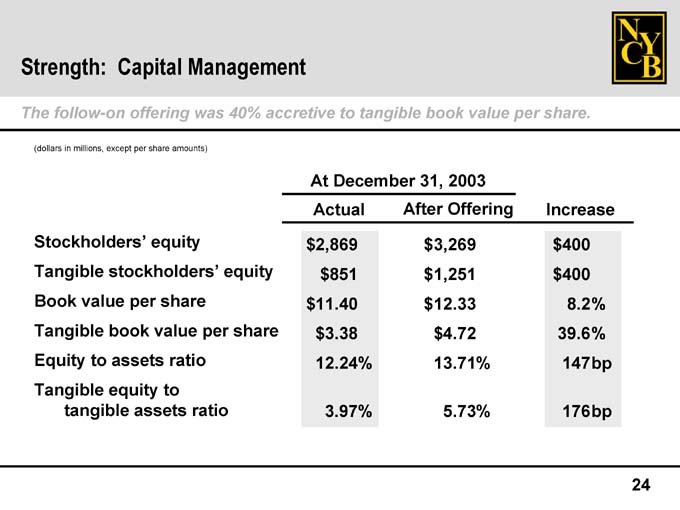

Strength: Capital Management

The follow-on offering was 40% accretive to tangible book value per share.

(dollars in millions, except per share amounts)

At December 31, 2003

Actual After Offering Increase

Stockholders’ equity $2,869 $3,269 $400

Tangible stockholders’ equity $851 $1,251 $400

Book value per share $ 11.40 $12.33 8.2%

Tangible book value per share $3.38 $4.72 39.6%

Equity to assets ratio 12.24% 13.71% 147bp

Tangible equity to

tangible assets ratio 3.97% 5.73% 176bp

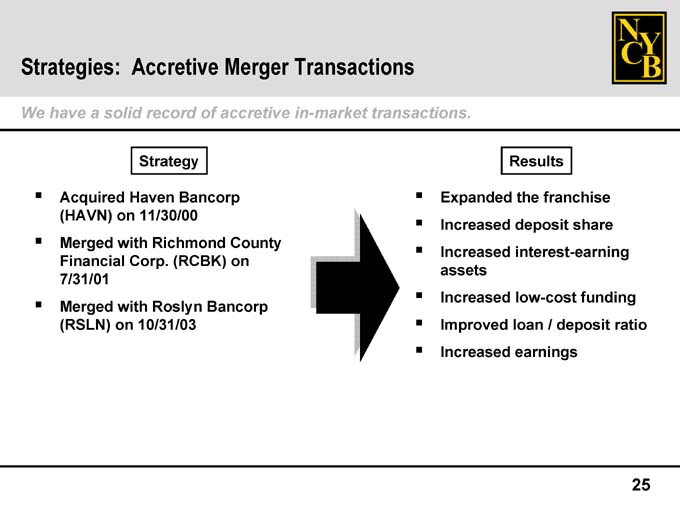

Strategies: Accretive Merger Transactions

We have a solid record of accretive in-market transactions.

Strategy Results

Acquired Haven Bancorp Expanded the franchise

(HAVN) on 11/30/00

Increased deposit share

Merged with Richmond County

Increased interest-earning

Financial Corp. (RCBK) on

assets

7/31/01

Increased low-cost funding

Merged with Roslyn Bancorp

(RSLN) on 10/31/03 Improved loan / deposit ratio

Increased earnings

25

Strength: Accretive Merger Transactions

We have successfully completed three accretive merger transactions in three years.

Earnings Accretion

Original Actual

2002 2002

Completed Projection Results

HAVN 11/30/00

11.8%-16.5% 129.4%

RCBK 7/31/01

Earnings Accretion

Original Revised

2004 2004

Completed Projection Projection

RSLN 10/31/03 10% 28%

26

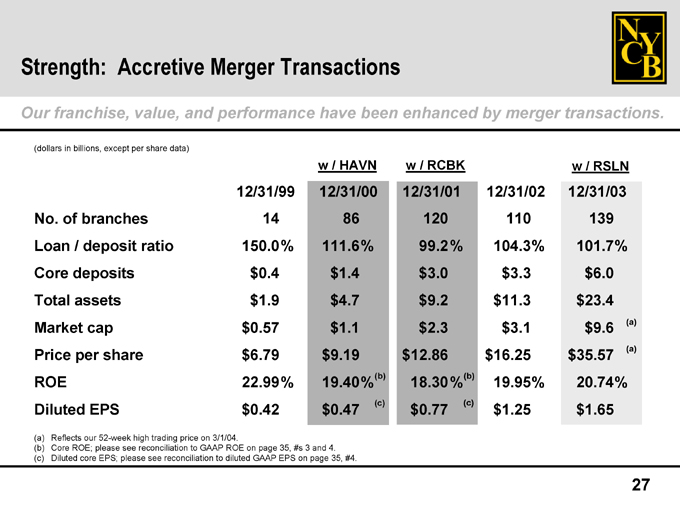

Strength: Accretive Merger Transactions

Our franchise, value, and performance have been enhanced by merger transactions.

(dollars in billions, except per share data)

w / HAVN w / RCBK w / RSLN

12/31/99 12/31/00 12/31/01 12/31/02 12/31/03

No. of branches 14 86 120 110 139

Loan / deposit ratio 150.0% 111.6% 99.2% 104.3% 101.7%

Core deposits $ 0.4 $ 1.4 $ 3.0 $ 3.3 $ 6.0

Total assets $ 1.9 $ 4.7 $ 9.2 $ 11.3 $ 23.4

Market cap $ 0.57 $ 1.1 $ 2.3 $ 3.1 $ 9.6 (a)

Price per share $ 6.79 $ 9.19 $ 12.86 $ 16.25 $ 35.57 (a)

ROE 22.99% 19.40%(b) 18.30%(b) 19.95% 20.74%

Diluted EPS $ 0.42 $ 0.47 (c) $ 0.77 (c) $ 1.25 $ 1.65

(a) Reflects our 52-week high trading price on 3/1/04.

(b) Core ROE; please see reconciliation to GAAP ROE on page 35, #s 3 and 4. (c) Diluted core EPS; please see reconciliation to diluted GAAP EPS on page 35, #4.

27

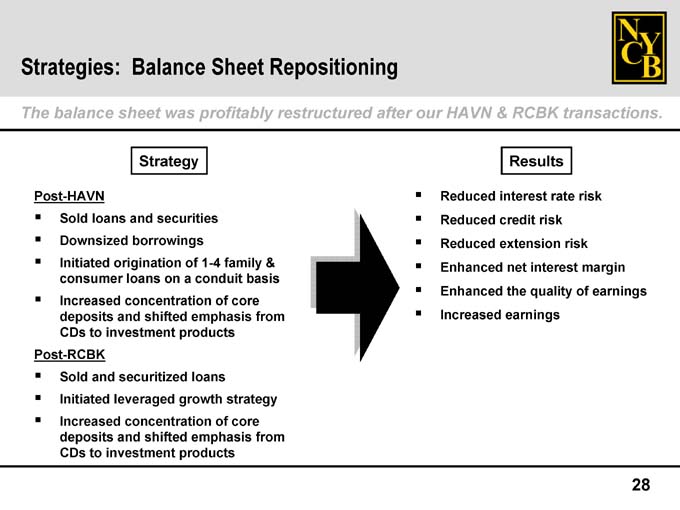

Strategies: Balance Sheet Repositioning

The balance sheet was profitably restructured after our HAVN & RCBK transactions.

Strategy Results

Post-HAVN Reduced interest rate risk

Sold loans and securities Reduced credit risk

Downsized borrowings Reduced extension risk

Initiated origination of 1-4 family & Enhanced net interest margin

consumer loans on a conduit basis

Enhanced the quality of earnings

Increased concentration of core

deposits and shifted emphasis from Increased earnings

CDs to investment products

Post-RCBK

Sold and securitized loans

Initiated leveraged growth strategy

Increased concentration of core

deposits and shifted emphasis from

CDs to investment products

28

Strategies: Balance Sheet Repositioning

We have initiated the process of repositioning the post-RSLN balance sheet.

Strategy Results

Post-RSLN Reduces interest rate risk

Invested liquidity from the Reduces credit risk

securities portfolio into a record

Reduces extension risk

volume of multi-family loans in 4Q ‘03

Sold approximately $130 mn of home Enhances net interest margin

equity and second mortgage loans in Enhances the quality of earnings

1Q ‘04

Increases earnings

Increased core deposits while

reducing concentration of higher-cost

CDs

Replaced FHLB borrowings with

reverse repos with Wall Street firms at

favorable rates

29

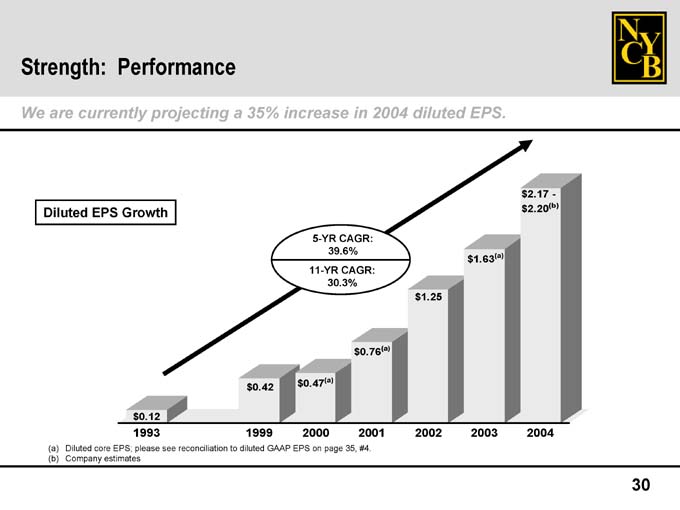

Strength: Performance

We are currently projecting a 35% increase in 2004 diluted EPS.

$2.17 -

Diluted EPS Growth $ 2.20(b)

5-YR CAGR:

39.6%

$ 1.63(a)

11-YR CAGR:

30.3%

$ 1.25

$ 0.76(a)

$ 0.42 $ 0.47(a)

$ 0.12

1993 1999 2000 2001 2002 2003 2004

(a) Diluted core EPS; please see reconciliation to diluted GAAP EPS on page 35, #4.

(b) Company estimates

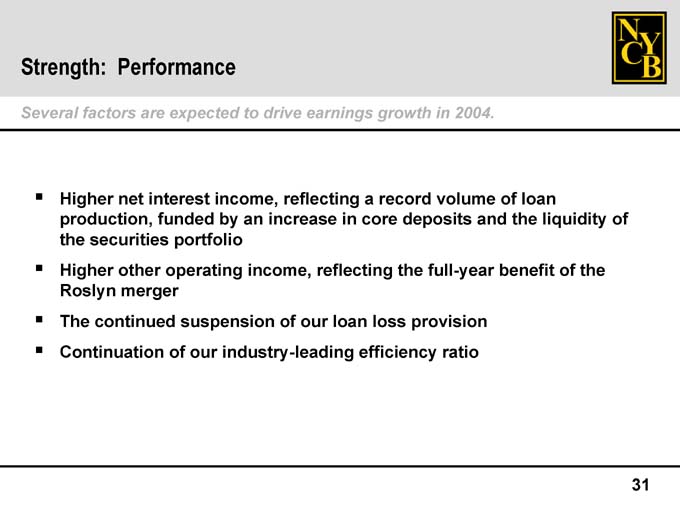

Strength: Performance

Several factors are expected to drive earnings growth in 2004.

Higher net interest income, reflecting a record volume of loan production, funded by an increase in core deposits and the liquidity of the securities portfolio

Higher other operating income, reflecting the full-year benefit of the Roslyn merger

The continued suspension of our loan loss provision

Continuation of our industry-leading efficiency ratio

31

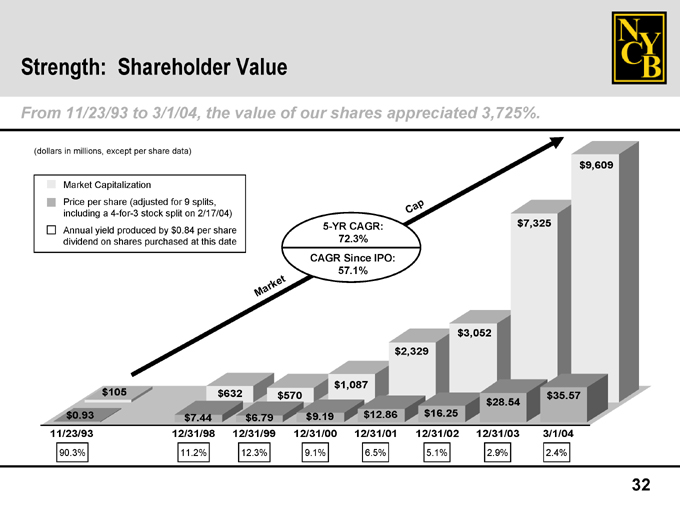

Strength: Shareholder Value

From 11/23/93 to 3/1/04, the value of our shares appreciated 3,725%.

(dollars in millions, except per share data)

Market Capitalization

Price per share (adjusted for 9 splits, including a 4-for-3 stock split on 2/17/04) Annual yield produced by $0.84 per share dividend on shares purchased at this date

57.1%

72.3%

5-YR CAGR: CAGR Since IPO: $0.93

11/23/93 12/31/98 12/31/99 12/31/00 12/31/01 12/31/02 12/31/03 3/1/04

90.3% 11.2% 12.3% 9.1% 6.5% 5.1% 2.9% 2.4%

32

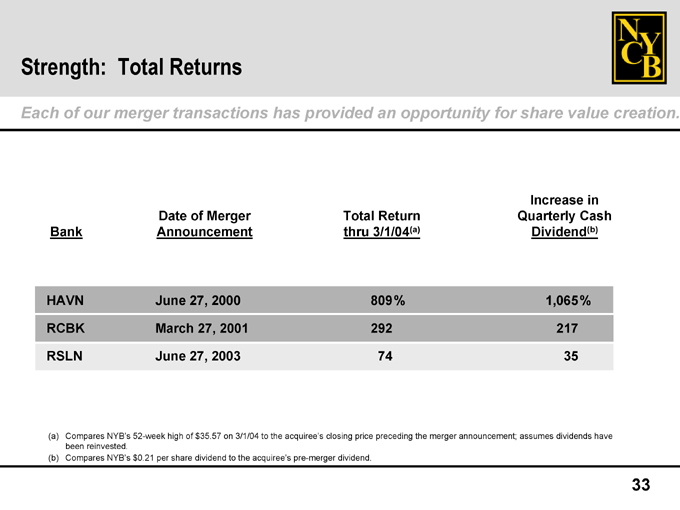

Strength: Total Returns

Each of our merger transactions has provided an opportunity for share value creation.

Increase in

Date of Merger Total Return Quarterly Cash

Bank Announcement thru 3/1/04(a) Dividend(b)

HAVN June 27, 2000 809% 1,065%

RCBK March 27, 2001 292 217

RSLN June 27, 2003 74 35

(a) Compares NYB’s 52-week high of $35.57 on 3/1/04 to the acquiree’s closing price preceding the merger announcement; assumes dividends have been reinvested.

(b) Compares NYB’s $0.21 per share dividend to the acquiree’s pre-merger dividend.

33

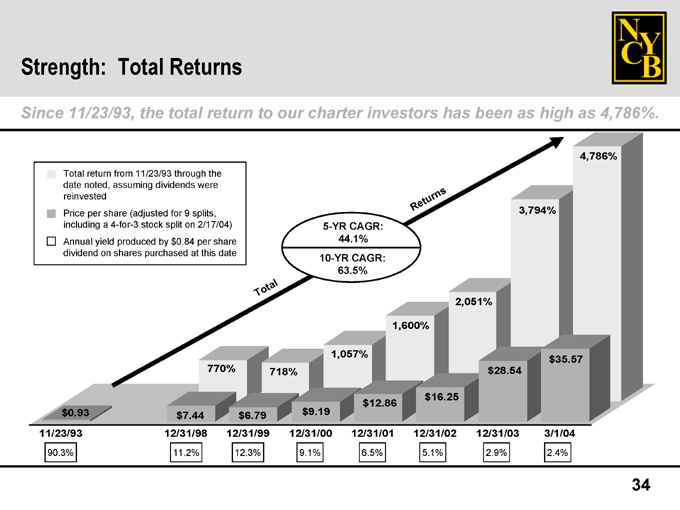

Strength: Total Returns

Since 11/23/93, the total return to our charter investors has been as high as 4,786%.

Total return from 11/23/93 through the date noted, assuming dividends were reinvested Price per share (adjusted for 9 splits, including a 4-for-3 stock split on 2/17/04) Annual yield produced by $0.84 per share dividend on shares purchased at this date

63.5%

44.1%

10-YR CAGR:

5-YR CAGR:

11/23/93 12/31/98 12/31/99 12/31/00 12/31/01 12/31/02 12/31/03 3/1/04

90.3% 11.2% 12.3% 9.1% 6.5% 5.1% 2.9% 2.4%

34

Appendix

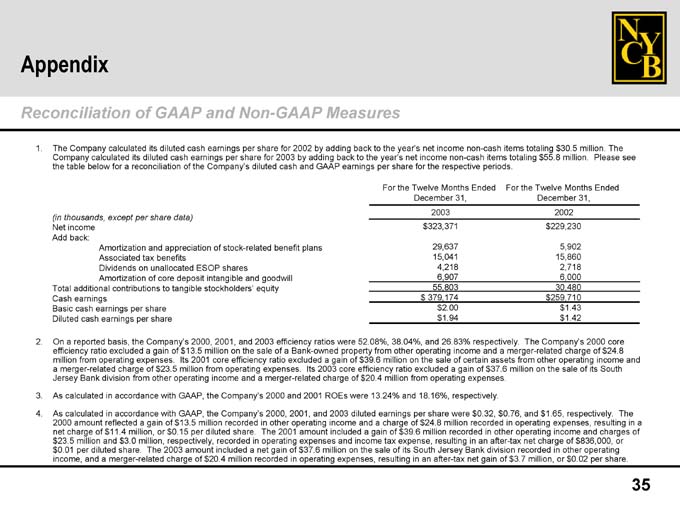

Reconciliation of GAAP and Non-GAAP Measures

1. The Company calculated its diluted cash earnings per share for 2002 by adding back to the year’s net income non-cash items totaling $30.5 million. The Company calculated its diluted cash earnings per share for 2003 by adding back to the year’s net income non-cash items totaling $55.8 million. Please see the table below for a reconciliation of the Company’s diluted cash and GAAP earnings per share for the respective periods.

For the Twelve Months Ended For the Twelve Months Ended

December 31, December 31,

2003

(in thousands, except per share data)

Net income $ 323,371 $ 229,230

Add back:

Amortization and appreciation of stock-related benefit plans 29,637 5,902

Associated tax benefits 15,041 15,860

Dividends on unallocated ESOP shares 4,218 2,718

Amortization of core deposit intangible and goodwill 6,907 6,000

Total additional contributions to tangible stockholders’ equity 55,803 30,480

Cash earnings $ 379,174 $ 259,710

Basic cash earnings per share $2.00 $ 1.43

Diluted cash earnings per share $1.94 $1.42

2. On a reported basis, the Company’s 2000, 2001, and 2003 efficiency ratios were 52.08%, 38.04%, and 26.83% respectively. The Company’s 2000 core efficiency ratio excluded a gain of $13.5 million on the sale of a Bank-owned property from other operating income and a merger-related charge of $24.8 million from operating expenses. Its 2001 core efficiency ratio excluded a gain of $39.6 million on the sale of certain assets from other operating income and a merger-related charge of $23.5 million from operating expenses. Its 2003 core efficiency ratio excluded a gain of $37.6 million on the sale of its South Jersey Bank division from other operating income and a merger-related charge of $20.4 million from operating expenses.

3. As calculated in accordance with GAAP, the Company’s 2000 and 2001 ROEs were 13.24% and 18.16%, respectively.

4. As calculated in accordance with GAAP, the Company’s 2000, 2001, and 2003 diluted earnings per share were $0.32, $0.76, and $1.65, respectively. The 2000 amount reflected a gain of $13.5 million recorded in other operating income and a charge of $24.8 million recorded in operating expenses, resulting in a net charge of $11.4 million, or $0.15 per diluted share. The 2001 amount included a gain of $39.6 million recorded in other operating income and charges of $23.5 million and $3.0 million, respectively, recorded in operating expenses and income tax expense, resulting in an after-tax net charge of $836,000, or $0.01 per diluted share. The 2003 amount included a net gain of $37.6 million on the sale of its South Jersey Bank division recorded in other operating income, and a merger-related charge of $20.4 million recorded in operating expenses, resulting in an after-tax net gain of $3.7 million, or $0.02 per share.

For More Information:

The Company trades on the NYSE under the symbol “NYB”.

Log onto our web site: www.myNYCB.com

E-mail requests to: ir@myNYCB.com

Call Investor Relations at: (516) 683-4420

Write to: New York Community Bancorp, Inc.

615 Merrick Avenue Westbury, NY 11590

2/4/04