Investor Presentation

First Quarter Ended

March 31, 2009

www.astoriafederal.com

LONG ISLAND’S PREMIER COMMUNITY BANK

Forward Looking Statement

This presentation may contain a number of forward-looking statements within the meaning of Section 27A of

the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as

amended. Forward-looking statements are based on various assumptions and analyses made by us in light

of our management’s experience and perception of historical trends, current conditions and expected future

developments, as well as other factors we believe are appropriate under the circumstances. These

statements are not guarantees of future performance and are subject to risks, uncertainties and other factors

(many of which are beyond our control) that could cause actual results to differ materially from future results

expressed or implied by such forward-looking statements. These factors include, without limitation, the

following: the timing and occurrence or non-occurrence of events may be subject to circumstances beyond

our control; there may be increases in competitive pressure among financial institutions or from non-financial

institutions; changes in the interest rate environment may reduce interest margins or affect the value of our

investments; changes in deposit flows, loan demand or real estate values may adversely affect our business;

changes in accounting principles, policies or guidelines may cause our financial condition to be perceived

differently; general economic conditions, either nationally or locally in some or all areas in which we do

business, or conditions in the real estate or securities markets or the banking industry may be less favorable

than we currently anticipate; legislative or regulatory changes may adversely affect our business; applicable

technological changes may be more difficult or expensive than we anticipate; success or consummation of

new business initiatives may be more difficult or expensive than we anticipate; or litigation or matters before

regulatory agencies, whether currently existing or commencing in the future, may be determined adverse to us

or may delay occurrence or non-occurrence of events longer than we anticipate. We assume no obligation to

update any forward-looking statements to reflect events or circumstances after the date of this document.

2

NYSE: AF

Corporate Profile

$21.4 billion in assets

$16.4 billion in loans

$13.6 billion in deposits

8.0% deposit market share in Long Island market

– Largest thrift depository

Insider & ESOP stock ownership: 23%

Well capitalized

– Bank regulatory capital: target > 6%

Core and tangible capital: 6.55%

Risk-based capital: 12.45%

Tier 1 risk-based capital: 11.24%

All figures in this presentation are as of March 31, 2009, except as noted.

3

• 1-4 Family loan portfolio increased $881.8 million, or 7.8%, from March 31, 2008,

to $12.2 billion with a weighted average rate of 5.61% at March 31, 2009

• Deposits increased $625.6 million, or 4.8%, from March 31, 2008, to $13.6 billion

at March 31, 2009; weighted average rate of deposits declined 67 bp from

March 31, 2008, to 2.57% at March 31, 2009

• Net interest income increased $30.9 million, or 38.2% from 1Q08, to $111.7

million for 1Q09

• Net interest margin increased 59 basis points from 1Q08, or 37.6%, to 2.16% for

1Q09

• Pre-tax, pre-provision operating income, 1Q09 $69.0 million; $276 million,

annualized*

• Tangible book value at March 31, 2009: $11.02 per share

Financial Highlights

For the twelve months ended March 31, 2009

* Excludes $5.3 million 1Q09 OTTI charge. For a reconciliation of operating income and operating EPS to GAAP net income and EPS, please

refer to table on page 35.

4

EFFICIENCY

MORTGAGE LENDING

• Portfolio lender,

• 1-4 Family, Multi-Family and CRE

expertise

• Solid asset quality

RETAIL BANKING

• Premier community bank on

Long Island

• Dominant deposit market share

• #1 thrift depository in core market

Same Simple Business Model

NOT A MTGE. BANKER

5

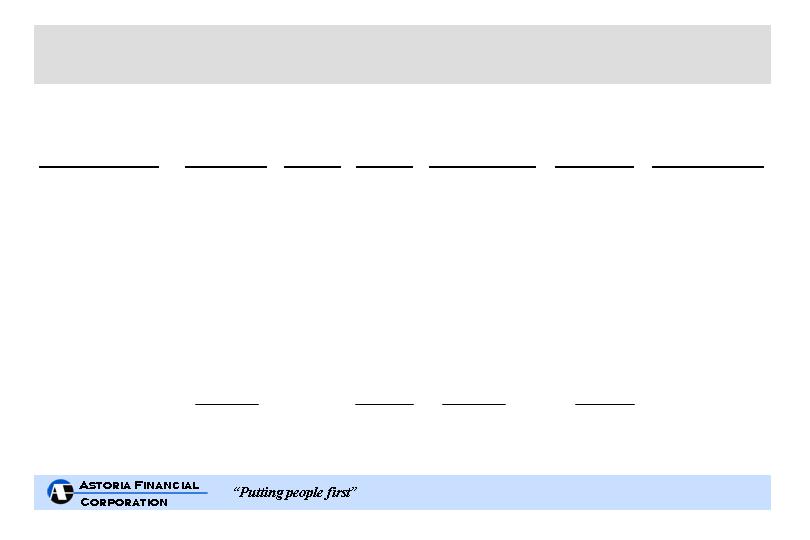

6%

Other

17%

Securities

77%

Loans

Other

8%

Loans

45%

Securities

47%

2%

Other

5%

Equity

42%

Deposits

51%

Borrowings

Total Assets: $22,696,536

($ in thousands)

($ in thousands)

Improving Balance Sheet Quality

At March 31, 2009

Total Assets: $21,404,781

Liabilities & Shareholders’ Equity

Liabilities & Shareholders’ Equity

Assets

Assets

At December 31, 1999

Equity

6%

Borrowings

29%

Deposits

64%

Other

1%

6

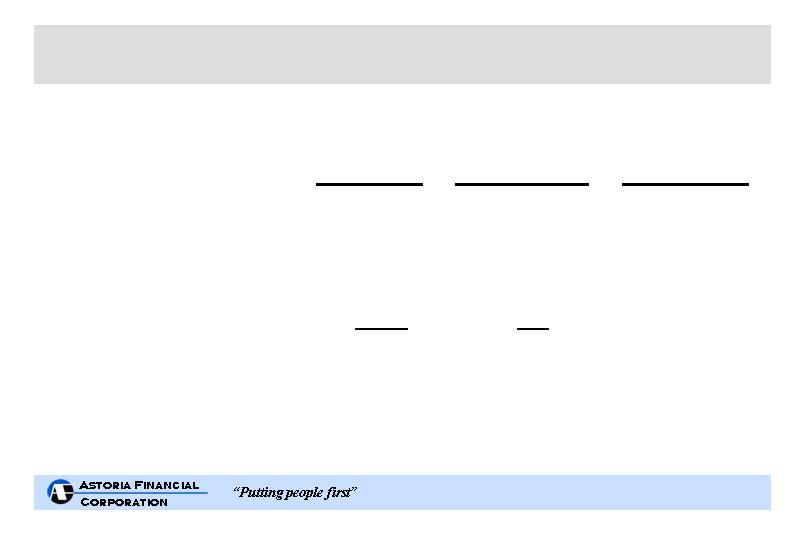

Low Expense Ratio(1)

* Data for All US Thrifts and NY Thrifts is not available for the quarter ended March 31, 2009. AF data is for the quarter ended March 31, 2009.

Source: SNL Financial – Median Ratios

(1) G&A expense ratio represents general and administrative expense divided by average assets.

0.0

0.5

1.0

1.5

2.0

2.5

2004

2005

2006

2007

2008

1Q09*

All U.S. Thrifts

NY Thrifts

AF

7

Primarily short-term, 5/1 jumbo prime hybrid ARMs for portfolio

Retain jumbo 15 year fixed-rate loans for portfolio

No sub-prime, negative amortization or payment option ARM lending

Average loan amount for first quarter 2009 production = $730,000

Average LTV on first quarter 2009 production = 55% at origination

Average LTV on total 1-4 family loan portfolio < 63%*

Multiple delivery channels provide flexibility & efficiency

Retail

Commissioned brokers covering 19 states**

Third party originators – correspondents covering 20 states**

Secondary marketing capability

Sale of 15 year and 30 year fixed rate conforming loans

Geographically diversified portfolio

Reduces lending concentrations

1-4 Family Mortgage Lending

* Based on current principal balances and original appraised values.

** All loans underwritten to Astoria’s stringent standards. Includes Washington, D.C.

8

By Product Type

$5.6 B

$0.46 B

$3.8 B

Other

Other ARM

5/1 ARM

3/1 ARM

1Q09

2008

2007

2006

2005

2004

2003

$6.0

$5.0

$4.0

$3.0

$2.0

$1.0

$0.0

$3.2 B

$3.3 B

$2.7 B

$3.8 B

1-4 Family Mortgage Loan Originations

Net portfolio growth:

($238.3 ) M

+$83.7 M

+$703.2 M

+$456.2 M

+$1.4 B

+$721.3 M

($192.3) M

Weighted Avg. Portfolio

Coupon at Period End

5.26%

5.05%

5.19%

5.48%

5.70%

5.65%

5.61%

9

Solid Multi-family/CRE portfolio

$3.8 billion in portfolio

Weighted Average Coupon at March 31, 2009: 5.96%

Weighted average LTV < 61%*

Average loan < $1 million

Approximately 70% of multi-family portfolio is

subject to rent control or rent stabilization

Limit originations in current economic environment

Multi-family/Commercial Real Estate Lending

* Based on current principal balances and original appraised values.

10

• Limited credit risk

Conservative underwriting, top quality loans, low LTVs

No sub-prime, negative amortization or payment option ARM lending

Non-performing assets: $367 million or 1.71% of total assets

No geographic concentration of NPLs

Net charge-offs to average loans outstanding:

48 basis points, 1Q09 annualized

• Top quality MBS portfolio

95% GSE/agency, balance ‘AAA’ rated

CMOs, seasoned collateral, well structured with minimal extension

risk

Average life 1.7 years

Asset Quality Focus

11

LI Savings Bank

Acquisition

09/30/98

Outsourced

Mtge. Servicing

12/31/05

1-4 Family Delinquency Ratios: AF vs. MBA

Source: MBA National Delinquency Survey.

0

1

2

3

4

5

6

7

8

9

10

11

12

MBA - NY

MBA - US

AF

12

Geographic Composition of 1- 4 Family NPLs

(1)

Based on current principal balances and original appraised values.

(2)

Includes 30 states and Washington, D.C.

(3)

Does not foot due to rounding.

At March 31, 2009

($ in millions)

Total

% of

% of

1-4 Family

1-4 Family

Non-Performing

Average

1-4 Family

Non-Performing

Non-Performing

Loans as a %

State

LTV

(1)

Loans

Loans

Loans

of State Totals

New York

$

2,875.8

55

%

24

%

$21.9

9

%

0.76

%

Illinois

1,309.5

66

11

29.0

12

2.21

California

1,304.9

65

11

38.4

16

2.94

Connecticut

1,276.8

56

11

16.8

7

1.32

New Jersey

996.6

67

8

27.7

11

2.78

Virginia

905.4

70

7

24.6

10

2.72

Maryland

854.5

67

7

30.0

12

3.51

Massachusetts

838.9

62

7

12.4

5

1.48

Washington

322.7

62

3

0.0

0

0.00

Florida

305.3

66

3

22.6

9

7.40

All other states

(2)

1,166.9

66

10

22.1

9

1.89

TOTAL

$

12,157.3

62

%

100

%

(3)

$245.5

100

%

2.02

%

Total

1-4 Family

Loans

13

Note: LTVs are based on current principal balances and original appraised values.

At March 31, 2009

($ in millions)

1- 4 Family Loan Portfolio Stratification

Non-Performing

Non-Performing

Loans as a %

Loans

of Total Loans

Full income portfolio

$

9,782.4

$

98.9

1.01

%

Alt A < 70% LTV

1,333.1

48.7

3.65

%

Alt A between 70% - 80% LTV

1,041.8

97.9

9.40

%

Total 1-4 family loans

$

12,157.3

$

245.5

2.02

%

Total

Loans

14

Asset Quality

(1)

Includes construction loans of $57.6 million and consumer and other loans of $333.9 million.

(2)

Includes $115.0 million of net unamortized premiums and deferred loan costs.

(3)

Includes construction loans of $7.2 million and consumer and other loans of $2.4 million.

($ in millions)

For the Three Months Ended March 31, 2009

Multi-family

Loan portfolio balance

$

12,157.3

$

2,837.4

$

920.7

$

391.5

(1)

$

16,421.9

(2)

Non-performing loans

$

245.5

$

66.2

$

15.3

$

9.6

(3)

$

336.6

% of total loans

1.49

%

0.41

%

0.09

%

0.06

%

2.05

%

Net charge-offs

$

11.2

$

7.9

$

0

$

0.7

$

19.8

Net charge-offs to avg. loans

27

bp

19

bp

0

bp

2

bp

48

bp

(annualized)

Other

1-4

Family

Total

CRE

15

Organic growth vs. de-novo branching

Differentiation from competition

– Maintain pricing discipline

– Pro-active sales culture – PEAK Process

– Focus on customer service – High customer satisfaction

– Community involvement – Support over 575 local

organizations and not-for-profit agencies in our markets

Astoria Federal is an integral part of the fabric of the communities we serve

Retail Banking Philosophy

16

• $13.6 billion in deposits, 85 banking office network

Serving the Long Island market since 1888

• Low cost/stable source of funds – weighted average rate: 2.57%*

• $12.7 billion, or 93%, of total deposits emanate from within

5 miles of a branch – no broker or municipal deposits

• Banking offices with high average deposits contribute to

efficiency

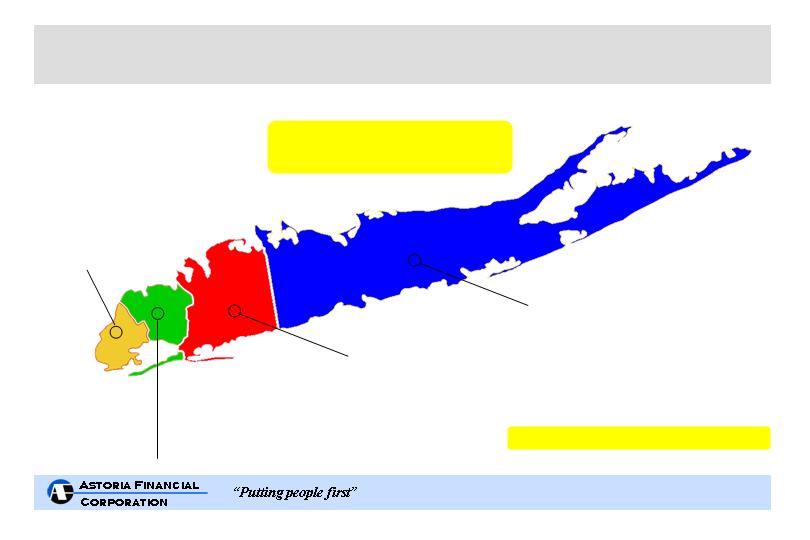

Long Island Offices (82) – Nassau (28), Queens (17), Suffolk (25),

Brooklyn (12) – Average Deposits of $159 Million

Westchester Offices (3) – Average Deposits of $202 Million

• Alternative delivery channels

ATM’s, telephone and Internet banking

* At March 31, 2009

Leading Retail Banking Franchise

17

TOTAL 4 COUNTY POPULATION: 7,661,593

Source: FDIC Summary of Deposits (as of June 30, 2008)

Kings County (Brooklyn)

Population: 2,548,982

Median household income: $43,514

Deposits: $1.6 billion

Branches: 12

Market share: 5%

Rank: #2 thrift, #6 all banks

Queens County

Population: 2,279,742

Median household income: $57,409

Deposits: $3.1 billion

Branches: 17

Market share: 8%

Rank: #1 thrift, #4 all banks

Nassau County

Population: 1,334,459

Median household income: $100,150

Deposits: $5.1 billion

Branches: 28

Market share: 10%

Rank: #1 thrift, #4 all banks

Suffolk County

Population: 1,498,410

Median household income: $86,495

Deposits: $3.1 billion

Branches: 25

Market share: 8%

Rank: #1 thrift, #3 all banks

Long Island Powerhouse

Well Positioned in Key Markets

Overall LI Deposit Share Ranking:

#1- all thrifts, #4- all banks

18

Brooklyn, Queens, Nassau and Suffolk

Market Share Trend 1999 - 2008

Note: Data adjusted to include the effect of merger and acquisition activity.

19

* Astoria’s deposits highlighted above are comprised of retail community deposits. Astoria does not solicit broker or municipal deposits.

Reflects one branch closed in 3Q08

Source: FDIC Summary of Deposits. Data as of June 30, 2008. Top 8 represents institutions with deposits exceeding $5 Billion.

($ in millions)

June 08

June 99-08

June 99-08

June 2008

June 99-08

Market

Market Share

Change in #

Institution

Deposits

$

Growth

%

Share

Gain/(Loss)

of Branches

1

TD Bank

$

7,233

$

7,233

100.0

%

4.5

%

4.5

%

60

2

Citibank

19,818

5,977

43.2

12.4

(0.1)

(18)

3

ASTORIA*

12,802

3,608

39.2

8.0

(0.3)

(2)

4

NY Community

10,069

2,026

25.2

6.3

(0.9)

29

5

HSBC

10,461

1,930

22.6

6.5

(1.1)

(6)

6

Capital One

22,800

5,423

31.2

14.2

(1.4)

7

7

Chase

38,034

9,914

35.3

23.7

(1.5)

46

8

Bank of America

5,360

(2,578)

(32.5)

3.3

(3.8)

(2)

Total - Top 8

$

126,577

$

33,533

36.0

%

79.0

%

(4.6)

%

+ 114

Total - Core Market

$

160,225

$

48,882

43.9

%

100.0

%

+ 306

* Note: 59% of the households that have a retail CD or Liquid CD account also have a low

cost checking, savings or money market account relationship.

At March 31, 2009

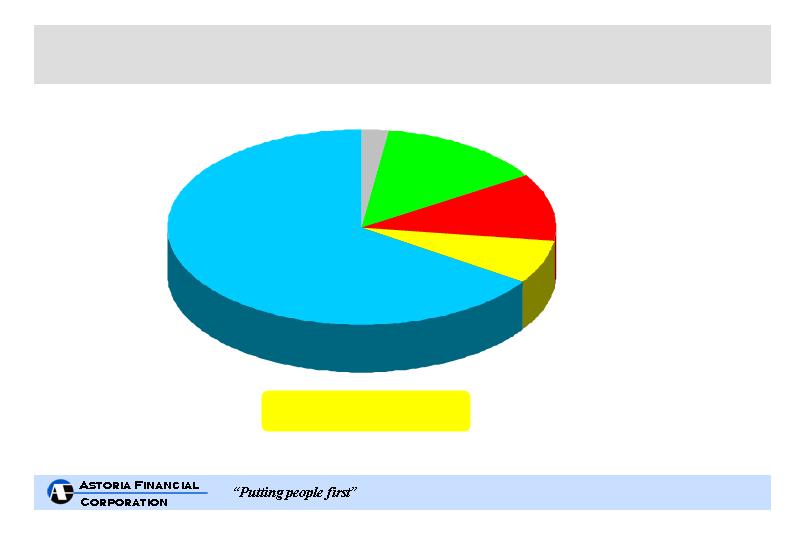

Core Community Deposits

Now/Demand: $1.5B

Rate: 0.06%

*Liquid CDs: $1.0B

Rate: 1.69%

Savings: $1.9B

Rate: 0.40%

Money Market: $0.3B

Rate: 0.82%

*Retail CDs: $8.9B

Rate: 3.61%

Total - $13.6 Billion

Retail CD's

47%

20

We expect, beginning in the 2Q09, to realize the benefit from the repricing

of maturing CDs that have interest rates considerably above recently

issued or repriced CDs.

CDs were either issued or repriced during March 2009 with a weighted

average rate of 1.88%.

CDs scheduled to mature during the remainder of 2009:

2Q09: $1.8 billion with a weighted rate of 3.49%

2H09: $2.9 billion with a weighted average rate of 3.59%

Margin Expansion Opportunities

* CDs referenced herein exclude Liquid CDs

21

• Loan and deposit growth

• Modest margin expansion

• Internal tangible capital generation

• Maintain bank core and tangible regulatory capital > 6%

° At March 31, 2009:

Core and tangible capital: 6.55%

Risk-based capital: 12.45%

Tier 1 risk-based capital: 11.24%

Outlook for the remainder of 2009

22

www.astoriafederal.com

LONG ISLAND’S PREMIER COMMUNITY BANK

Addendum

23

Ownership Profile

Shares Outstanding: 97,058,454

At March 31, 2009

ESOP & Other

Benefit Plans

12%

Officers &

Directors

11%

Retail

14%

Institutions

63%

24

37

68

Support Services

Arnold K. Greenberg

Executive Vice President

29

55

Legal

Alan P. Eggleston

EVP, Secretary & General Counsel

32

56

Mortgage Lending

Gary T. McCann

Executive Vice President

38

62

Retail Banking

Gerard C. Keegan

Vice Chairman & CAO

19

46

Chief Financial Officer

Frank E. Fusco

EVP, Treasurer & CFO

35

58

Chief Operating Officer

Monte N. Redman

President & COO

38

70

Chief Executive Officer

George L. Engelke, Jr.

Chairman & CEO

Yrs. in

Banking

Age

Responsibility

Solid and Seasoned Management Team

25

$0.46 B

$3.8 B

$3.8 B

1-4 Family Mortgage Loan Originations

$2.7 B

$3.3 B

$3.2 B

By Delivery Channel

$0.0

$1.0

$2.0

$3.0

$4.0

2004

2005

2006

2007

2008

1Q09

Retail

Broker

Correspondent

26

For the quarter ended March 31, 2009

Total 1-4 Family Loan Originations

$463.3 Million

Geographic Composition of 1-4 Family Originations

Maryland

5%

New Jersey

5%

Connecticut

8%

Other < 5%

15%

Illinois

15%

New York

34%

Washington

8%

Massachusetts

10%

27

Percentages do not foot to 100% due to rounding

Total 1-4 Family Loan Portfolio

$12.2 Billion

At March 31, 2009

Geographic Composition of 1-4 Family Loan Portfolio

California

11%

Virginia

7%

New York

24%

Connecticut

11%

Massachusetts

7%

Illinois

11%

New Jersey

8%

Maryland

7%

Other < 5%

16%

28

Geographic Composition of Multi-family/CRE Portfolio Loans

New York,

New Jersey,

Connecticut

93%

Total Multifamily/CRE Portfolio

$3.8 Billion

At March 31, 2009

Florida

3%

Other

4%

29

At March 31, 2009

* Astoria Federal Savings

12.45%

Bank Regulatory Capital*

6.55%

6.55%

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Core

Tangible

Risk-Based

Regulatory Requirement

Excess Capital

30

(1) Branches sold in 1999

(2) One satellite office closed in 1997

$11,590

86

TOTAL

6,600

35

Long Island Bancorp, Inc.

1998

2,400

14

The Greater NY Savings Bank

1997

1,800

18

Fidelity New York (2)

1995

280

4

Whitestone Savings (RTC)

1990

205

4

Oneonta Federal (1)

1987

25

1

Chenango Federal (1)

1984

100

3

Hastings-on-Hudson Federal

1982

130

5

Citizens Savings (FSLIC)

1979

$ 50

2

Metropolitan Federal

1973

Assets

# Branches

Thrift

Year

(in millions)

Acquisition History

31

Performance based on Enthusiasm, A ctions and Knowledge

“Sales Oriented and Service Obsessed”

A “needs” based approach to sales rather than “product”

based approach

Highly interactive program – daily and weekly meetings

create a focus that is shared throughout the branch network

Incentives for strong performance, both individual and team

Sales – PEAK Process

32

Key Findings : Favorably Positioned Against Competitors

• 74% of Astoria customers are highly satisfied

• 72% of Astoria customers are highly likely to recommend

Astoria to friend/family member

• Astoria customers are 25% more likely to net increase their

deposit relationship than are competitor customers

• Satisfaction with the branch is by far the strongest driver of

overall satisfaction – 83% of Astoria customers are highly

satisfied with quality of branch service

Customer Satisfaction

33

• Education First

Supports lifelong learning, promotes savings and provides meaningful

financial solutions to improve the way our customers live

• Neighborhood Outreach

Supports local organizations that enrich the communities within our market

area

Over 575 community-based organizations and not-for-profit agencies

supported in our markets

• Results/Recognition

Six consecutive “Outstanding” Community Reinvestment Act ratings by OTS

Astoria Federal is an integral part of the fabric of the communities we serve

Community Involvement

Key Initiatives

34

Reconciliation of GAAP Net Income to Non-GAAP Net Income(1)

(In Thousands, Except Per Share Data)

GAAP

Adjustments (2)

Non-GAAP

Net interest income

$111,677

$ -

$111,677

Provision for loan losses

50,000

-

50,000

Net interest income after provision for loan losses

61,677

-

61,677

Non-interest income

15,942

5,300

21,242

Non-interest expense

63,961

-

63,961

Income before income tax expense

13,658

5,300

18,958

Income tax expense

4,862

1,855

6,717

Net income

$ 8,796

$ 3,445

$ 12,241

Basic earnings per common share

$0.10

$0.04

$0.14

Diluted earnings per common share

$0.10

$0.04

$0.14

(1) Non-GAAP net income is also referred to as operating income and operating EPS in this presentation.

(2) Adjustments relate to the other-than-temporary impairment write-down of securities charge and the related tax effects.

Non-GAAP net income, non-GAAP earnings per share and non-GAAP returns, representing net income and earnings per share determined in

accordance with GAAP excluding the effects of the after-tax charges noted below, provide a meaningful comparison for effectively evaluating

Astoria's operating results.

March 31, 2009

For the Three Months Ended

35

Other Than Temporary Impairment

-

OTTI

Mortgage Bankers Association

-

MBA

Mortgage-Backed Securities

-

MBS

Office of Thrift Supervision

-

OTS

Earnings Per Share

-

EPS

Non-Performing Loan

-

NPL

Loan-To-Value Ratio

-

LTV

Government Sponsored Enterprise

-

GSE

Generally Accepted Accounting Principles

-

GAAP

Collateralized Mortgage Obligation

-

CMO

Employee Stock Ownership Plan

-

ESOP

Commercial Real Estate

-

CRE

Adjustable Rate Mortgage

-

ARM

Glossary

36

Contact Information

Astoria Financial Corporation

Attn: Investor Relations

One Astoria Federal Plaza

Lake Success, NY 11042

Address:

ir@astoriafederal.com

Email:

(516) 327-7869

Telephone:

www.astoriafederal.com

Web site:

37