Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

Filing exhibits

Related financial report

Astoria Financial similar filings

- 20 Jul 06 Astoria Financial Corporation Announces Second Quarter EPS of $0.49

- 22 Jun 06 Other Events

- 17 May 06 Amendments to the Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics

- 9 May 06 Results of Operations and Financial Condition

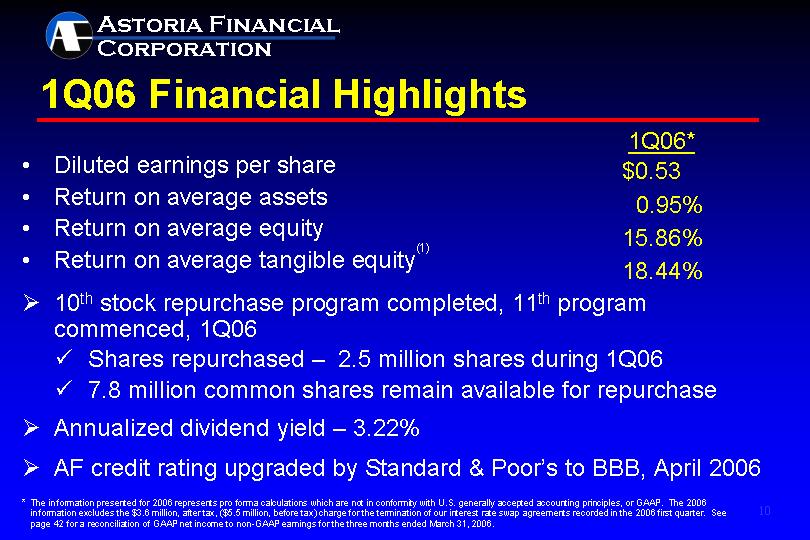

- 20 Apr 06 Astoria Financial Corporation Announces First Quarter EPS of $0.49

- 19 Apr 06 Entry into a Material Definitive Agreement

- 27 Mar 06 Other Events

Filing view

External links