Exhibit 99.1 WillScot and Mobile Mini to Combine Creating a North American Leader in Modular Space and Portable Storage March 2, 2020 Exhibit 99.1 WillScot and Mobile Mini to Combine Creating a North American Leader in Modular Space and Portable Storage March 2, 2020

A4 FORMAT Forward-Looking Statements Please don’t change page set up to A3, print to This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to risks and uncertainties and are made pursuant to the A3 paper and fit safe harbor provisions of 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The words “estimates,” “expects,” “anticipates,” “believes,” to scale “forecasts,” “projects,” “plans,” “intends,” “may,” “will,” “should,” “could,” “shall,” “continue,” “outlook” and variations of these words and similar expressions (or the negative thereof) identify forward-looking statements, which are generally not historical in nature. Certain of these forward-looking statements relate to the proposed business combination (the “Proposed Transaction”) involving WillScot Corporation (“WillScot”) and Mobile Mini, Inc. (“Mobile Mini”), including: expected scale; operating efficiency; stockholder, employee and customer benefits; key assumptions; timing of closing; the amount and timing of revenue and expense synergies; future financial benefits and operating results; and integration spend, which reflects management’s beliefs, expectations and objectives as of the date hereof. Achievement of the expressed beliefs, expectations and objectives is subject to risks and uncertainties that could cause actual results to differ materially from those beliefs, expectations or 0 objectives. These forward-looking statements are only estimates, assumptions and projections, and involve known and unknown risks and uncertainties, many of which are beyond the control of WillScot 138 and Mobile Mini. 95 Important Proposed Transaction-related factors that may cause such differences include, but are not limited to: the risk that expected revenue, expense and other synergies from the Proposed Transaction may not be fully realized or may take longer to realize than expected; the parties are unable to successfully implement their integration strategies; the inherent uncertainty associated with financial or other projections; failure of the parties to satisfy the closing conditions in the merger agreement in a timely manner or at all, including stockholder and regulatory approvals; the occurrence of 0 any event, change or other circumstances that could give rise to the termination of the merger agreement; the possibility that the Proposed Transaction may be more expensive to complete than 0 anticipated, including as a result of unexpected factors or events; and disruptions to the parties’ businesses and financial condition as a result of the announcement and pendency of the Proposed 0 Transaction. Other important factors include: the parties’ ability to manage growth and execute their business plan; their estimates of the size of the markets for their products; the rate and degree of market acceptance of their products; the success of other competing modular space and portable storage solutions that exist or may become available; rising costs adversely affecting their profitability (including cost increases resulting from tariffs); general economic and market conditions impacting demand for their products and services; the value of WillScot shares to be issued in the Proposed Transaction; the parties’ capital structure, levels of indebtedness and availability of credit; expected financing transactions undertaken in connection with the Proposed Transaction; third party contracts 115 containing consent and/or other provisions that may be triggered by the Proposed Transaction; the ability to retain and hire key personnel and uncertainties arising from leadership changes; the response 193 of business partners as a result of the announcement and pendency of the Proposed Transaction; the diversion of management attention from business operations to the Proposed Transaction; the ability 103 to implement and maintain an effective system of internal controls; potential litigation and regulatory matters involving the combined company; implementation of tax reform; the intended qualification of the Proposed Transaction as a tax-free reorganization; the changes in political conditions in the U.S. and other countries in which the parties operate, including U.S. trade policies or the U.K.’s withdrawal from the European Union; and such other risks and uncertainties described in the periodic reports WillScot and Mobile Mini file with the SEC from time to time including WillScot’s Annual Report on Form 10-K for the fiscal year ended December 31, 2018, which was filed with the SEC on March 15, 2019, WillScot's Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which will be 95 filed with the SEC today and Mobile Mini’s Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which was filed with the SEC on February 3, 2020, each of which are or will be 96 available through the SEC’s EDGAR system at www.sec.gov. 98 Investors are cautioned not to place undue reliance on these forward-looking statements as the information in this communication speaks only as of March 2, 2020 or such earlier date as specified herein. WillScot and Mobile Mini disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. Investors should not assume that any lack of update to a previously issued “forward-looking statement” constitutes a reaffirmation of that statement. All subsequent written and oral forward-looking 193 statements attributable to WillScot, Mobile Mini or any person acting on behalf of either party are expressly qualified in their entirety by the cautionary statements referenced above. 216 47 This presentation contains certain non-GAAP financial measures, including Adjusted EBITDA, and Adjusted EBITDA Margin, and Free Cash Flow. Adjusted EBITDA of $357 million for the 12 months ended December 31, 2019 at WillScot is defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non-cash items considered non-core to business operations including net currency gains and losses, goodwill and other impairment charges, restructuring costs, costs to integrate acquired companies, costs incurred related to transactions, non-cash charges for stock compensation plans, and other discrete expenses. Adjusted EBITDA of $243 million for the 12 months ended December 31, 2019 at Mobile Mini is defined as net income 158 before discontinued operations, net of tax (if applicable), interest expense, income taxes, depreciation and amortization, and debt restructuring or extinguishment expense (if applicable), including any 159 write off of deferred financing costs, further adjusted to exclude certain non-cash expenses, including share based compensation, as well as transactions that management believes are not indicative of 161 their business. Adjusted EBITDA Margin is defined as Adjusted EBITDA divided by Revenue. Further information and reconciliations for these Non-GAAP measures to the most directly comparable US generally accepted accounting principles (GAAP) financial measures are included in the full Q4 results presentations available at each of the respective company’s websites. Free Cash Flow is defined as Cash Flow from Operations, reduced by Net Capex. Net Capex is defined as purchases of rental equipment and refurbishments and purchases of property, plant and equipment, less proceeds from sale of rental equipment and proceeds from the sale of property, plant and equipment, which are all included in cash flows from investing activities. Information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort. 2 A4 FORMAT Forward-Looking Statements Please don’t change page set up to A3, print to This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to risks and uncertainties and are made pursuant to the A3 paper and fit safe harbor provisions of 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The words “estimates,” “expects,” “anticipates,” “believes,” to scale “forecasts,” “projects,” “plans,” “intends,” “may,” “will,” “should,” “could,” “shall,” “continue,” “outlook” and variations of these words and similar expressions (or the negative thereof) identify forward-looking statements, which are generally not historical in nature. Certain of these forward-looking statements relate to the proposed business combination (the “Proposed Transaction”) involving WillScot Corporation (“WillScot”) and Mobile Mini, Inc. (“Mobile Mini”), including: expected scale; operating efficiency; stockholder, employee and customer benefits; key assumptions; timing of closing; the amount and timing of revenue and expense synergies; future financial benefits and operating results; and integration spend, which reflects management’s beliefs, expectations and objectives as of the date hereof. Achievement of the expressed beliefs, expectations and objectives is subject to risks and uncertainties that could cause actual results to differ materially from those beliefs, expectations or 0 objectives. These forward-looking statements are only estimates, assumptions and projections, and involve known and unknown risks and uncertainties, many of which are beyond the control of WillScot 138 and Mobile Mini. 95 Important Proposed Transaction-related factors that may cause such differences include, but are not limited to: the risk that expected revenue, expense and other synergies from the Proposed Transaction may not be fully realized or may take longer to realize than expected; the parties are unable to successfully implement their integration strategies; the inherent uncertainty associated with financial or other projections; failure of the parties to satisfy the closing conditions in the merger agreement in a timely manner or at all, including stockholder and regulatory approvals; the occurrence of 0 any event, change or other circumstances that could give rise to the termination of the merger agreement; the possibility that the Proposed Transaction may be more expensive to complete than 0 anticipated, including as a result of unexpected factors or events; and disruptions to the parties’ businesses and financial condition as a result of the announcement and pendency of the Proposed 0 Transaction. Other important factors include: the parties’ ability to manage growth and execute their business plan; their estimates of the size of the markets for their products; the rate and degree of market acceptance of their products; the success of other competing modular space and portable storage solutions that exist or may become available; rising costs adversely affecting their profitability (including cost increases resulting from tariffs); general economic and market conditions impacting demand for their products and services; the value of WillScot shares to be issued in the Proposed Transaction; the parties’ capital structure, levels of indebtedness and availability of credit; expected financing transactions undertaken in connection with the Proposed Transaction; third party contracts 115 containing consent and/or other provisions that may be triggered by the Proposed Transaction; the ability to retain and hire key personnel and uncertainties arising from leadership changes; the response 193 of business partners as a result of the announcement and pendency of the Proposed Transaction; the diversion of management attention from business operations to the Proposed Transaction; the ability 103 to implement and maintain an effective system of internal controls; potential litigation and regulatory matters involving the combined company; implementation of tax reform; the intended qualification of the Proposed Transaction as a tax-free reorganization; the changes in political conditions in the U.S. and other countries in which the parties operate, including U.S. trade policies or the U.K.’s withdrawal from the European Union; and such other risks and uncertainties described in the periodic reports WillScot and Mobile Mini file with the SEC from time to time including WillScot’s Annual Report on Form 10-K for the fiscal year ended December 31, 2018, which was filed with the SEC on March 15, 2019, WillScot's Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which will be 95 filed with the SEC today and Mobile Mini’s Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which was filed with the SEC on February 3, 2020, each of which are or will be 96 available through the SEC’s EDGAR system at www.sec.gov. 98 Investors are cautioned not to place undue reliance on these forward-looking statements as the information in this communication speaks only as of March 2, 2020 or such earlier date as specified herein. WillScot and Mobile Mini disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. Investors should not assume that any lack of update to a previously issued “forward-looking statement” constitutes a reaffirmation of that statement. All subsequent written and oral forward-looking 193 statements attributable to WillScot, Mobile Mini or any person acting on behalf of either party are expressly qualified in their entirety by the cautionary statements referenced above. 216 47 This presentation contains certain non-GAAP financial measures, including Adjusted EBITDA, and Adjusted EBITDA Margin, and Free Cash Flow. Adjusted EBITDA of $357 million for the 12 months ended December 31, 2019 at WillScot is defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non-cash items considered non-core to business operations including net currency gains and losses, goodwill and other impairment charges, restructuring costs, costs to integrate acquired companies, costs incurred related to transactions, non-cash charges for stock compensation plans, and other discrete expenses. Adjusted EBITDA of $243 million for the 12 months ended December 31, 2019 at Mobile Mini is defined as net income 158 before discontinued operations, net of tax (if applicable), interest expense, income taxes, depreciation and amortization, and debt restructuring or extinguishment expense (if applicable), including any 159 write off of deferred financing costs, further adjusted to exclude certain non-cash expenses, including share based compensation, as well as transactions that management believes are not indicative of 161 their business. Adjusted EBITDA Margin is defined as Adjusted EBITDA divided by Revenue. Further information and reconciliations for these Non-GAAP measures to the most directly comparable US generally accepted accounting principles (GAAP) financial measures are included in the full Q4 results presentations available at each of the respective company’s websites. Free Cash Flow is defined as Cash Flow from Operations, reduced by Net Capex. Net Capex is defined as purchases of rental equipment and refurbishments and purchases of property, plant and equipment, less proceeds from sale of rental equipment and proceeds from the sale of property, plant and equipment, which are all included in cash flows from investing activities. Information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort. 2

A4 FORMAT Important Information About the Proposed Transaction Please don’t change page set up to A3, print to Additional Information and Where to Find It A3 paper and fit This communication is for informational purposes only and does not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any securities or a solicitation of any vote or approval. This to scale communication relates to the Proposed Transaction. In connection with the Proposed Transaction, WillScot will file a registration statement on Form S-4, which will include a document that serves as a prospectus of WillScot and a joint proxy statement of WillScot and Mobile Mini (the “joint proxy statement/prospectus”), and each party will file other documents regarding the Proposed Transaction with the U.S. Securities and Exchange Commission (the “SEC”). No offering of securities shall be made, except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY, IF AND WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION THAT STOCKHOLDERS SHOULD 0 CONSIDER BEFORE MAKING ANY DECISION REGARDING THE PROPOSED TRANSACTION. A definitive joint proxy statement/prospectus will be sent to WillScot’s stockholders and Mobile Mini’s 138 stockholders. Investors and security holders will be able to obtain these documents (if and when available) free of charge from the SEC’s website at www.sec.gov. The documents filed by WillScot with 95 the SEC may also be obtained free of charge from WillScot by requesting them by mail at WillScot Corporation, 901 S. Bond Street, Suite 600, Baltimore, Maryland 21231. The documents filed by Mobile Mini may also be obtained free of charge from Mobile Mini by requesting them by mail at Mobile Mini, Inc. 4646 E. Van Buren Street, Suite 400, Phoenix, Arizona 85008. Participants in the Solicitation 0 WillScot, Mobile Mini, their respective directors and executive officers and other members of management and employees and certain of their respective significant stockholders may be deemed to be 0 participants in the solicitation of proxies in respect of the Proposed Transaction. Information about WillScot’s directors and executive officers is available in WillScot’s proxy statement, dated April 30, 2019 0 for the 2019 Annual Meeting of Stockholders, WillScot’s Annual Report on Form 10-K for the fiscal year ended December 31, 2018, which was filed with the SEC on March 15, 2019, WillScot's Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which will be filed with the SEC today and WillScot's Current Reports on Form 8-K filed on May 17, 2019 and June 19, 2019. Information about Mobile Mini’s directors and executive officers is available in Mobile Mini’s proxy statement, dated March 12, 2019 for its 2019 Annual Meeting of Stockholders and Mobile Mini’s Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which was filed with the SEC on February 3, 2020. Information regarding the persons who may, under the rules of the SEC, be 115 deemed participants in the proxy solicitation and a description of their direct and indirect interests, by security holding or otherwise, will be contained in the joint proxy statement/prospectus and other 193 relevant materials to be filed with the SEC regarding the Proposed Transaction when they become available. Investors should read the joint proxy statement/prospectus carefully when it becomes 103 available before making any voting or investment decisions. You may obtain free copies of these documents from the SEC, WillScot or Mobile Mini as indicated above. No Offer or Solicitation This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale 95 would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements 96 of Section 10 of the Securities Act of 1933, as amended. 98 193 216 47 158 159 161 3 A4 FORMAT Important Information About the Proposed Transaction Please don’t change page set up to A3, print to Additional Information and Where to Find It A3 paper and fit This communication is for informational purposes only and does not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any securities or a solicitation of any vote or approval. This to scale communication relates to the Proposed Transaction. In connection with the Proposed Transaction, WillScot will file a registration statement on Form S-4, which will include a document that serves as a prospectus of WillScot and a joint proxy statement of WillScot and Mobile Mini (the “joint proxy statement/prospectus”), and each party will file other documents regarding the Proposed Transaction with the U.S. Securities and Exchange Commission (the “SEC”). No offering of securities shall be made, except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY, IF AND WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION THAT STOCKHOLDERS SHOULD 0 CONSIDER BEFORE MAKING ANY DECISION REGARDING THE PROPOSED TRANSACTION. A definitive joint proxy statement/prospectus will be sent to WillScot’s stockholders and Mobile Mini’s 138 stockholders. Investors and security holders will be able to obtain these documents (if and when available) free of charge from the SEC’s website at www.sec.gov. The documents filed by WillScot with 95 the SEC may also be obtained free of charge from WillScot by requesting them by mail at WillScot Corporation, 901 S. Bond Street, Suite 600, Baltimore, Maryland 21231. The documents filed by Mobile Mini may also be obtained free of charge from Mobile Mini by requesting them by mail at Mobile Mini, Inc. 4646 E. Van Buren Street, Suite 400, Phoenix, Arizona 85008. Participants in the Solicitation 0 WillScot, Mobile Mini, their respective directors and executive officers and other members of management and employees and certain of their respective significant stockholders may be deemed to be 0 participants in the solicitation of proxies in respect of the Proposed Transaction. Information about WillScot’s directors and executive officers is available in WillScot’s proxy statement, dated April 30, 2019 0 for the 2019 Annual Meeting of Stockholders, WillScot’s Annual Report on Form 10-K for the fiscal year ended December 31, 2018, which was filed with the SEC on March 15, 2019, WillScot's Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which will be filed with the SEC today and WillScot's Current Reports on Form 8-K filed on May 17, 2019 and June 19, 2019. Information about Mobile Mini’s directors and executive officers is available in Mobile Mini’s proxy statement, dated March 12, 2019 for its 2019 Annual Meeting of Stockholders and Mobile Mini’s Annual Report on Form 10-K for the fiscal year ended December 31, 2019, which was filed with the SEC on February 3, 2020. Information regarding the persons who may, under the rules of the SEC, be 115 deemed participants in the proxy solicitation and a description of their direct and indirect interests, by security holding or otherwise, will be contained in the joint proxy statement/prospectus and other 193 relevant materials to be filed with the SEC regarding the Proposed Transaction when they become available. Investors should read the joint proxy statement/prospectus carefully when it becomes 103 available before making any voting or investment decisions. You may obtain free copies of these documents from the SEC, WillScot or Mobile Mini as indicated above. No Offer or Solicitation This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale 95 would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements 96 of Section 10 of the Securities Act of 1933, as amended. 98 193 216 47 158 159 161 3

A4 FORMAT Today’s Presenters Please don’t change page set up to A3, print to A3 paper and fit to scale 0 138 95 0 0 0 115 193 103 95 96 98 193 Brad Soultz Kelly Williams Tim Boswell 216 President and Chief President and Chief Chief Financial Officer, 47 Executive Officer, WillScot Executive Officer, WillScot 158 Mobile Mini 159 161 4 A4 FORMAT Today’s Presenters Please don’t change page set up to A3, print to A3 paper and fit to scale 0 138 95 0 0 0 115 193 103 95 96 98 193 Brad Soultz Kelly Williams Tim Boswell 216 President and Chief President and Chief Chief Financial Officer, 47 Executive Officer, WillScot Executive Officer, WillScot 158 Mobile Mini 159 161 4

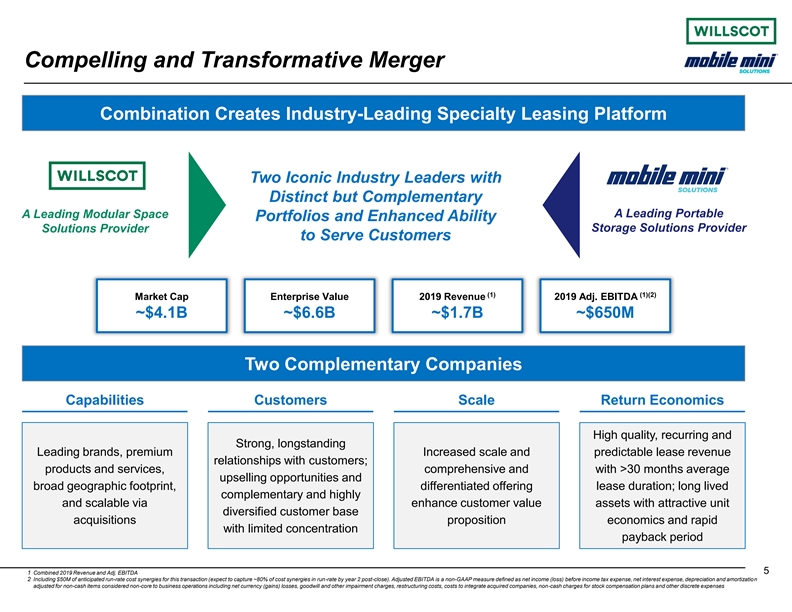

A4 FORMAT Compelling and Transformative Merger Please don’t change page set up to A3, print to A3 paper and fit Combination Creates Industry-Leading Specialty Leasing Platform to scale 0 Two Iconic Industry Leaders with 138 95 Distinct but Complementary A Leading Portable A Leading Modular Space Portfolios and Enhanced Ability 0 Storage Solutions Provider Solutions Provider to Serve Customers 0 0 115 (1) (1)(2) Market Cap Enterprise Value 2019 Revenue 2019 Adj. EBITDA 193 103 ~$4.1B ~$6.6B ~$1.7B ~$650M 95 96 Two Complementary Companies 98 193 Capabilities Customers Scale Return Economics 216 47 High quality, recurring and Strong, longstanding Leading brands, premium Increased scale and predictable lease revenue 158 relationships with customers; products and services, comprehensive and with >30 months average 159 upselling opportunities and 161 broad geographic footprint, differentiated offering lease duration; long lived complementary and highly and scalable via enhance customer value assets with attractive unit diversified customer base acquisitions proposition economics and rapid with limited concentration payback period 5 1 Combined 2019 Revenue and Adj. EBITDA 2 Including $50M of anticipated run-rate cost synergies for this transaction (expect to capture ~80% of cost synergies in run-rate by year 2 post-close). Adjusted EBITDA is a non-GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non-cash items considered non-core to business operations including net currency (gains) losses, goodwill and other impairment charges, restructuring costs, costs to integrate acquired companies, non-cash charges for stock compensation plans and other discrete expenses A4 FORMAT Compelling and Transformative Merger Please don’t change page set up to A3, print to A3 paper and fit Combination Creates Industry-Leading Specialty Leasing Platform to scale 0 Two Iconic Industry Leaders with 138 95 Distinct but Complementary A Leading Portable A Leading Modular Space Portfolios and Enhanced Ability 0 Storage Solutions Provider Solutions Provider to Serve Customers 0 0 115 (1) (1)(2) Market Cap Enterprise Value 2019 Revenue 2019 Adj. EBITDA 193 103 ~$4.1B ~$6.6B ~$1.7B ~$650M 95 96 Two Complementary Companies 98 193 Capabilities Customers Scale Return Economics 216 47 High quality, recurring and Strong, longstanding Leading brands, premium Increased scale and predictable lease revenue 158 relationships with customers; products and services, comprehensive and with >30 months average 159 upselling opportunities and 161 broad geographic footprint, differentiated offering lease duration; long lived complementary and highly and scalable via enhance customer value assets with attractive unit diversified customer base acquisitions proposition economics and rapid with limited concentration payback period 5 1 Combined 2019 Revenue and Adj. EBITDA 2 Including $50M of anticipated run-rate cost synergies for this transaction (expect to capture ~80% of cost synergies in run-rate by year 2 post-close). Adjusted EBITDA is a non-GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non-cash items considered non-core to business operations including net currency (gains) losses, goodwill and other impairment charges, restructuring costs, costs to integrate acquired companies, non-cash charges for stock compensation plans and other discrete expenses

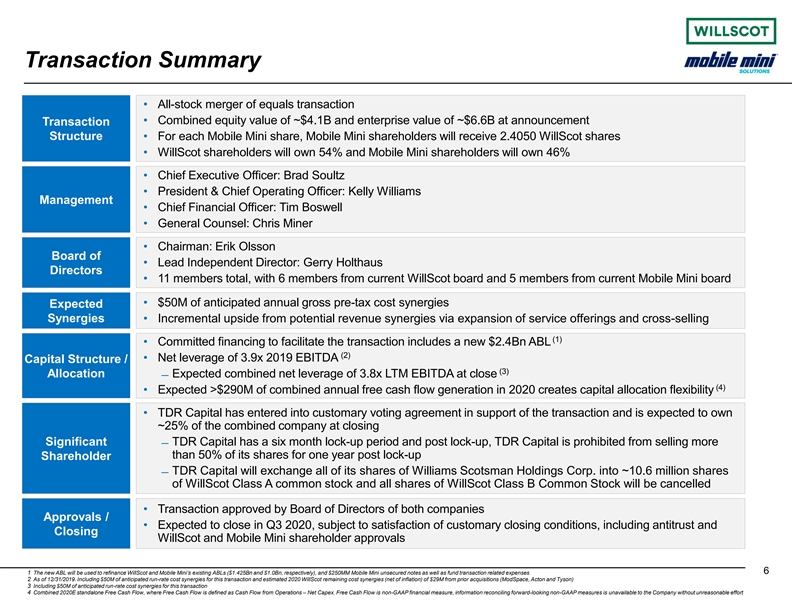

A4 FORMAT Transaction Summary Please don’t change page set up to A3, print to • All-stock merger of equals transaction A3 paper and fit • Combined equity value of ~$4.1B and enterprise value of ~$6.6B at announcement Transaction to scale Structure • For each Mobile Mini share, Mobile Mini shareholders will receive 2.4050 WillScot shares • WillScot shareholders will own 54% and Mobile Mini shareholders will own 46% 0 • Chief Executive Officer: Brad Soultz 138 • President & Chief Operating Officer: Kelly Williams 95 Management • Chief Financial Officer: Tim Boswell • General Counsel: Chris Miner 0 0 • Chairman: Erik Olsson 0 Board of • Lead Independent Director: Gerry Holthaus Directors • 11 members total, with 6 members from current WillScot board and 5 members from current Mobile Mini board 115 193 • $50M of anticipated annual gross pre-tax cost synergies Expected 103 Synergies • Incremental upside from potential revenue synergies via expansion of service offerings and cross-selling (1) 95 • Committed financing to facilitate the transaction includes a new $2.4Bn ABL (2) 96 • Net leverage of 3.9x 2019 EBITDA Capital Structure / 98 (3) Allocation ̶ Expected combined net leverage of 3.8x LTM EBITDA at close (4) • Expected >$290M of combined annual free cash flow generation in 2020 creates capital allocation flexibility 193 216 • TDR Capital has entered into customary voting agreement in support of the transaction and is expected to own 47 ~25% of the combined company at closing Significant ̶ TDR Capital has a six month lock-up period and post lock-up, TDR Capital is prohibited from selling more than 50% of its shares for one year post lock-up Shareholder 158 159 ̶ TDR Capital will exchange all of its shares of Williams Scotsman Holdings Corp. into ~10.6 million shares 161 of WillScot Class A common stock and all shares of WillScot Class B Common Stock will be cancelled • Transaction approved by Board of Directors of both companies Approvals / • Expected to close in Q3 2020, subject to satisfaction of customary closing conditions, including antitrust and Closing WillScot and Mobile Mini shareholder approvals 6 1 The new ABL will be used to refinance WillScot and Mobile Mini’s existing ABLs ($1.425Bn and $1.0Bn, respectively), and $250MM Mobile Mini unsecured notes as well as fund transaction related expenses 2 As of 12/31/2019. Including $50M of anticipated run-rate cost synergies for this transaction and estimated 2020 WillScot remaining cost synergies (net of inflation) of $29M from prior acquisitions (ModSpace, Acton and Tyson) 3 Including $50M of anticipated run-rate cost synergies for this transaction 4 Combined 2020E standalone Free Cash Flow, where Free Cash Flow is defined as Cash Flow from Operations – Net Capex. Free Cash Flow is non-GAAP financial measure, information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort A4 FORMAT Transaction Summary Please don’t change page set up to A3, print to • All-stock merger of equals transaction A3 paper and fit • Combined equity value of ~$4.1B and enterprise value of ~$6.6B at announcement Transaction to scale Structure • For each Mobile Mini share, Mobile Mini shareholders will receive 2.4050 WillScot shares • WillScot shareholders will own 54% and Mobile Mini shareholders will own 46% 0 • Chief Executive Officer: Brad Soultz 138 • President & Chief Operating Officer: Kelly Williams 95 Management • Chief Financial Officer: Tim Boswell • General Counsel: Chris Miner 0 0 • Chairman: Erik Olsson 0 Board of • Lead Independent Director: Gerry Holthaus Directors • 11 members total, with 6 members from current WillScot board and 5 members from current Mobile Mini board 115 193 • $50M of anticipated annual gross pre-tax cost synergies Expected 103 Synergies • Incremental upside from potential revenue synergies via expansion of service offerings and cross-selling (1) 95 • Committed financing to facilitate the transaction includes a new $2.4Bn ABL (2) 96 • Net leverage of 3.9x 2019 EBITDA Capital Structure / 98 (3) Allocation ̶ Expected combined net leverage of 3.8x LTM EBITDA at close (4) • Expected >$290M of combined annual free cash flow generation in 2020 creates capital allocation flexibility 193 216 • TDR Capital has entered into customary voting agreement in support of the transaction and is expected to own 47 ~25% of the combined company at closing Significant ̶ TDR Capital has a six month lock-up period and post lock-up, TDR Capital is prohibited from selling more than 50% of its shares for one year post lock-up Shareholder 158 159 ̶ TDR Capital will exchange all of its shares of Williams Scotsman Holdings Corp. into ~10.6 million shares 161 of WillScot Class A common stock and all shares of WillScot Class B Common Stock will be cancelled • Transaction approved by Board of Directors of both companies Approvals / • Expected to close in Q3 2020, subject to satisfaction of customary closing conditions, including antitrust and Closing WillScot and Mobile Mini shareholder approvals 6 1 The new ABL will be used to refinance WillScot and Mobile Mini’s existing ABLs ($1.425Bn and $1.0Bn, respectively), and $250MM Mobile Mini unsecured notes as well as fund transaction related expenses 2 As of 12/31/2019. Including $50M of anticipated run-rate cost synergies for this transaction and estimated 2020 WillScot remaining cost synergies (net of inflation) of $29M from prior acquisitions (ModSpace, Acton and Tyson) 3 Including $50M of anticipated run-rate cost synergies for this transaction 4 Combined 2020E standalone Free Cash Flow, where Free Cash Flow is defined as Cash Flow from Operations – Net Capex. Free Cash Flow is non-GAAP financial measure, information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort

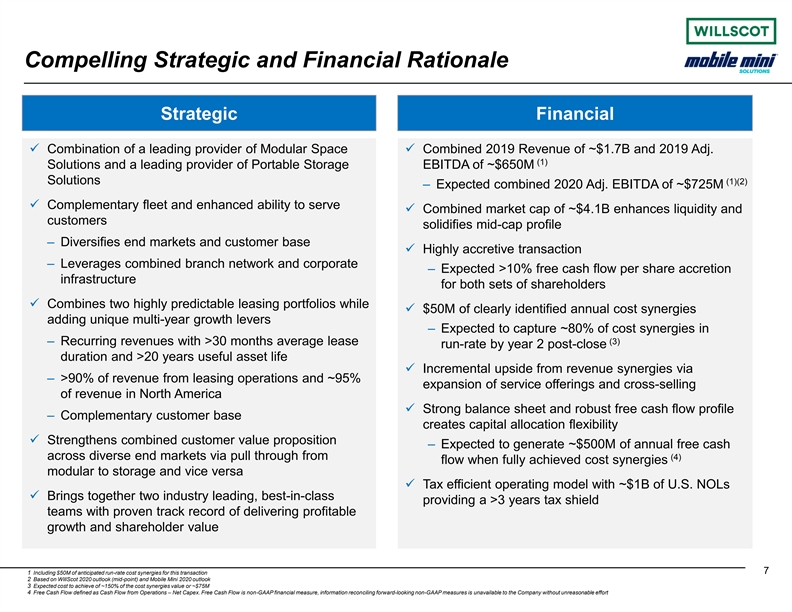

A4 FORMAT Compelling Strategic and Financial Rationale Please don’t change page set up to A3, print to A3 paper and fit Strategic Financial to scale ü Combination of a leading provider of Modular Space ü Combined 2019 Revenue of ~$1.7B and 2019 Adj. (1) Solutions and a leading provider of Portable Storage EBITDA of ~$650M 0 Solutions 138 (1)(2) ‒ Expected combined 2020 Adj. EBITDA of ~$725M 95 ü Complementary fleet and enhanced ability to serve ü Combined market cap of ~$4.1B enhances liquidity and customers solidifies mid-cap profile 0 0 ‒ Diversifies end markets and customer base ü Highly accretive transaction 0 ‒ Leverages combined branch network and corporate ‒ Expected >10% free cash flow per share accretion infrastructure 115 for both sets of shareholders 193 ü Combines two highly predictable leasing portfolios while 103 ü $50M of clearly identified annual cost synergies adding unique multi-year growth levers ‒ Expected to capture ~80% of cost synergies in (3) ‒ Recurring revenues with >30 months average lease 95 run-rate by year 2 post-close 96 duration and >20 years useful asset life 98 ü Incremental upside from revenue synergies via ‒ >90% of revenue from leasing operations and ~95% expansion of service offerings and cross-selling of revenue in North America 193 ü Strong balance sheet and robust free cash flow profile 216 ‒ Complementary customer base 47 creates capital allocation flexibility ü Strengthens combined customer value proposition ‒ Expected to generate ~$500M of annual free cash across diverse end markets via pull through from (4) 158 flow when fully achieved cost synergies 159 modular to storage and vice versa 161 ü Tax efficient operating model with ~$1B of U.S. NOLs ü Brings together two industry leading, best-in-class providing a >3 years tax shield teams with proven track record of delivering profitable growth and shareholder value 7 1 Including $50M of anticipated run-rate cost synergies for this transaction 2 Based on WillScot 2020 outlook (mid-point) and Mobile Mini 2020 outlook 3 Expected cost to achieve of ~150% of the cost synergies value or ~$75M 4 Free Cash Flow defined as Cash Flow from Operations – Net Capex. Free Cash Flow is non-GAAP financial measure, information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort A4 FORMAT Compelling Strategic and Financial Rationale Please don’t change page set up to A3, print to A3 paper and fit Strategic Financial to scale ü Combination of a leading provider of Modular Space ü Combined 2019 Revenue of ~$1.7B and 2019 Adj. (1) Solutions and a leading provider of Portable Storage EBITDA of ~$650M 0 Solutions 138 (1)(2) ‒ Expected combined 2020 Adj. EBITDA of ~$725M 95 ü Complementary fleet and enhanced ability to serve ü Combined market cap of ~$4.1B enhances liquidity and customers solidifies mid-cap profile 0 0 ‒ Diversifies end markets and customer base ü Highly accretive transaction 0 ‒ Leverages combined branch network and corporate ‒ Expected >10% free cash flow per share accretion infrastructure 115 for both sets of shareholders 193 ü Combines two highly predictable leasing portfolios while 103 ü $50M of clearly identified annual cost synergies adding unique multi-year growth levers ‒ Expected to capture ~80% of cost synergies in (3) ‒ Recurring revenues with >30 months average lease 95 run-rate by year 2 post-close 96 duration and >20 years useful asset life 98 ü Incremental upside from revenue synergies via ‒ >90% of revenue from leasing operations and ~95% expansion of service offerings and cross-selling of revenue in North America 193 ü Strong balance sheet and robust free cash flow profile 216 ‒ Complementary customer base 47 creates capital allocation flexibility ü Strengthens combined customer value proposition ‒ Expected to generate ~$500M of annual free cash across diverse end markets via pull through from (4) 158 flow when fully achieved cost synergies 159 modular to storage and vice versa 161 ü Tax efficient operating model with ~$1B of U.S. NOLs ü Brings together two industry leading, best-in-class providing a >3 years tax shield teams with proven track record of delivering profitable growth and shareholder value 7 1 Including $50M of anticipated run-rate cost synergies for this transaction 2 Based on WillScot 2020 outlook (mid-point) and Mobile Mini 2020 outlook 3 Expected cost to achieve of ~150% of the cost synergies value or ~$75M 4 Free Cash Flow defined as Cash Flow from Operations – Net Capex. Free Cash Flow is non-GAAP financial measure, information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort

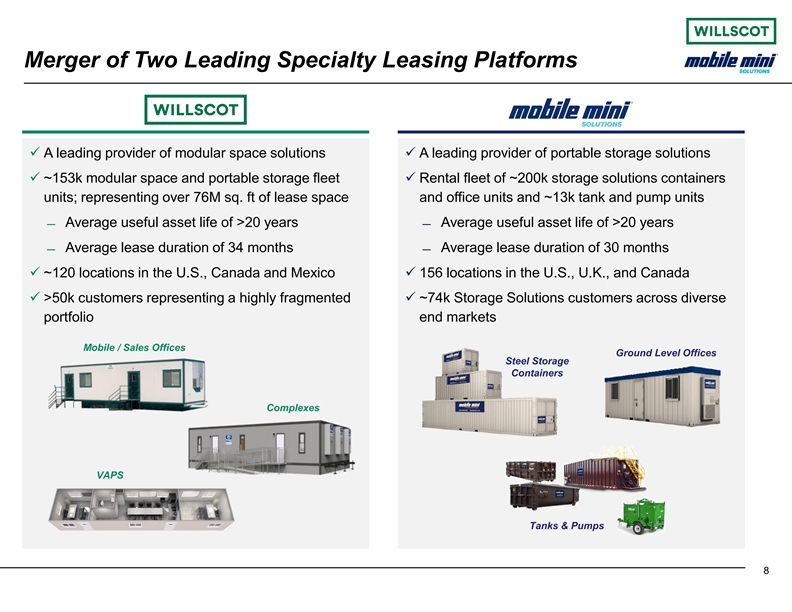

A4 FORMAT Merger of Two Leading Specialty Leasing Platforms Please don’t change page set up to A3, print to A3 paper and fit to scale ü A leading provider of modular space solutions ü A leading provider of portable storage solutions 0 ü ~153k modular space and portable storage fleet ü Rental fleet of ~200k storage solutions containers 138 95 units; representing over 76M sq. ft of lease space and office units and ~13k tank and pump units ̶ Average useful asset life of >20 years ̶ Average useful asset life of >20 years 0 0 ̶ Average lease duration of 34 months ̶ Average lease duration of 30 months 0 ü ~120 locations in the U.S., Canada and Mexico ü 156 locations in the U.S., U.K., and Canada 115 193 ü >50k customers representing a highly fragmented ü ~74k Storage Solutions customers across diverse 103 portfolio end markets 95 Mobile / Sales Offices Ground Level Offices 96 Steel Storage 98 Containers 193 Complexes 216 47 158 159 VAPS 161 Tanks & Pumps 8 A4 FORMAT Merger of Two Leading Specialty Leasing Platforms Please don’t change page set up to A3, print to A3 paper and fit to scale ü A leading provider of modular space solutions ü A leading provider of portable storage solutions 0 ü ~153k modular space and portable storage fleet ü Rental fleet of ~200k storage solutions containers 138 95 units; representing over 76M sq. ft of lease space and office units and ~13k tank and pump units ̶ Average useful asset life of >20 years ̶ Average useful asset life of >20 years 0 0 ̶ Average lease duration of 34 months ̶ Average lease duration of 30 months 0 ü ~120 locations in the U.S., Canada and Mexico ü 156 locations in the U.S., U.K., and Canada 115 193 ü >50k customers representing a highly fragmented ü ~74k Storage Solutions customers across diverse 103 portfolio end markets 95 Mobile / Sales Offices Ground Level Offices 96 Steel Storage 98 Containers 193 Complexes 216 47 158 159 VAPS 161 Tanks & Pumps 8

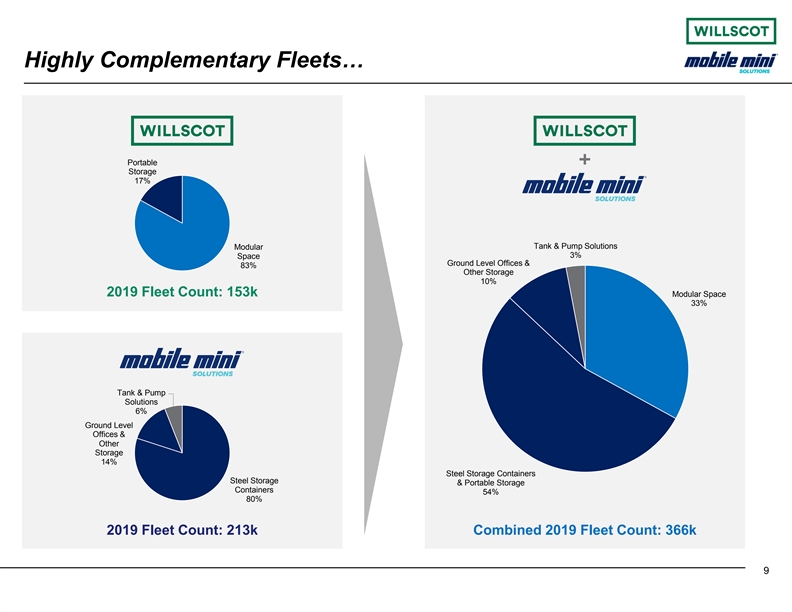

A4 FORMAT Highly Complementary Fleets… Please don’t change page set up to A3, print to A3 paper and fit to scale Portable 0 Storage 17% 138 95 0 0 Tank & Pump Solutions Modular 0 3% Space Ground Level Offices & 83% Other Storage 10% 115 2019 Fleet Count: 153k Modular Space 193 33% 103 95 96 98 Tank & Pump 193 Solutions 6% 216 Ground Level 47 Offices & Other Storage 158 14% 159 Steel Storage Containers Steel Storage & Portable Storage 161 Containers 54% 80% 2019 Fleet Count: 213k Combined 2019 Fleet Count: 366k 9 A4 FORMAT Highly Complementary Fleets… Please don’t change page set up to A3, print to A3 paper and fit to scale Portable 0 Storage 17% 138 95 0 0 Tank & Pump Solutions Modular 0 3% Space Ground Level Offices & 83% Other Storage 10% 115 2019 Fleet Count: 153k Modular Space 193 33% 103 95 96 98 Tank & Pump 193 Solutions 6% 216 Ground Level 47 Offices & Other Storage 158 14% 159 Steel Storage Containers Steel Storage & Portable Storage 161 Containers 54% 80% 2019 Fleet Count: 213k Combined 2019 Fleet Count: 366k 9

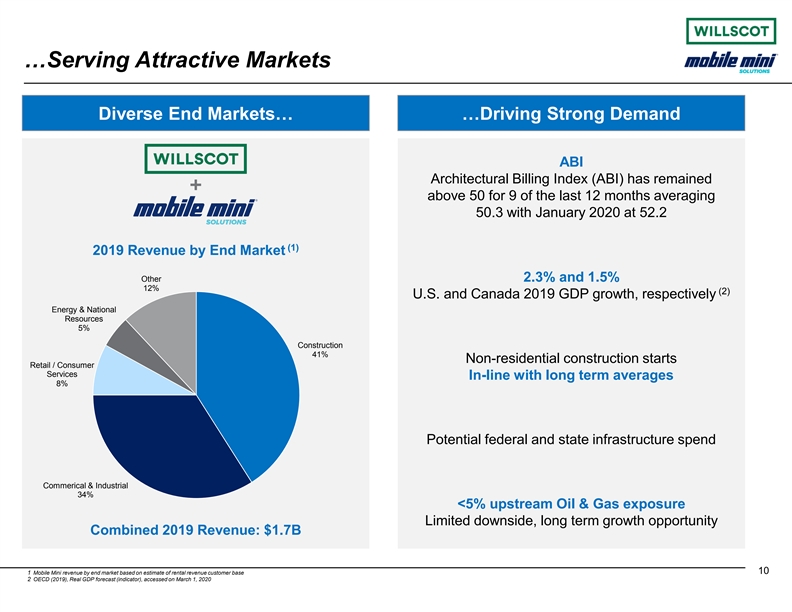

A4 FORMAT …Serving Attractive Markets Please don’t change page set up to A3, print to A3 paper and fit Diverse End Markets… …Driving Strong Demand to scale ABI 0 Architectural Billing Index (ABI) has remained 138 95 above 50 for 9 of the last 12 months averaging 50.3 with January 2020 at 52.2 0 0 (1) 2019 Revenue by End Market 0 Other 2.3% and 1.5% 115 12% (2) U.S. and Canada 2019 GDP growth, respectively 193 Energy & National 103 Resources 5% 95 Construction 41% 96 Non-residential construction starts Retail / Consumer 98 Services In-line with long term averages 8% 193 216 47 Potential federal and state infrastructure spend 158 159 161 Commerical & Industrial 34% <5% upstream Oil & Gas exposure Limited downside, long term growth opportunity Combined 2019 Revenue: $1.7B 10 1 Mobile Mini revenue by end market based on estimate of rental revenue customer base 2 OECD (2019), Real GDP forecast (indicator), accessed on March 1, 2020 A4 FORMAT …Serving Attractive Markets Please don’t change page set up to A3, print to A3 paper and fit Diverse End Markets… …Driving Strong Demand to scale ABI 0 Architectural Billing Index (ABI) has remained 138 95 above 50 for 9 of the last 12 months averaging 50.3 with January 2020 at 52.2 0 0 (1) 2019 Revenue by End Market 0 Other 2.3% and 1.5% 115 12% (2) U.S. and Canada 2019 GDP growth, respectively 193 Energy & National 103 Resources 5% 95 Construction 41% 96 Non-residential construction starts Retail / Consumer 98 Services In-line with long term averages 8% 193 216 47 Potential federal and state infrastructure spend 158 159 161 Commerical & Industrial 34% <5% upstream Oil & Gas exposure Limited downside, long term growth opportunity Combined 2019 Revenue: $1.7B 10 1 Mobile Mini revenue by end market based on estimate of rental revenue customer base 2 OECD (2019), Real GDP forecast (indicator), accessed on March 1, 2020

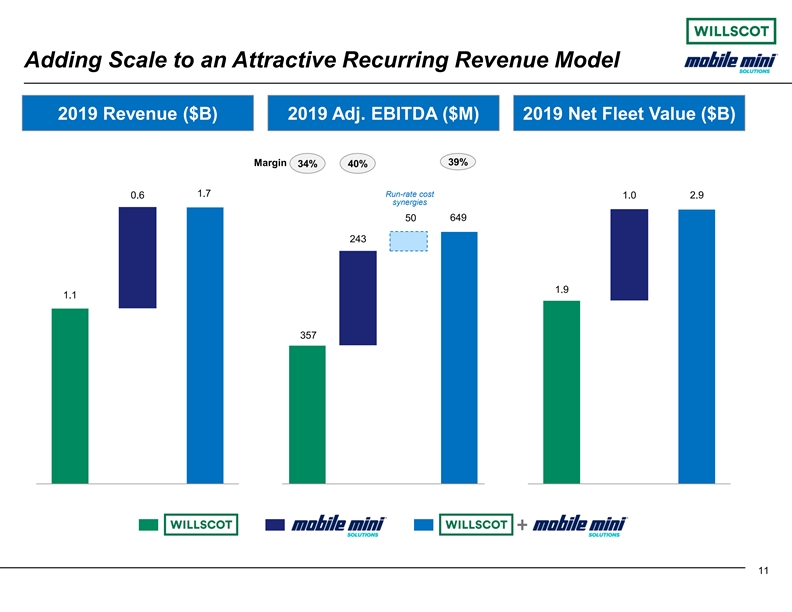

A4 FORMAT Adding Scale to an Attractive Recurring Revenue Model Please don’t change page set up to A3, print to A3 paper and fit 2019 Revenue ($B) 2019 Adj. EBITDA ($M) 2019 Net Fleet Value ($B) to scale 39% Margin 34% 40% 0 138 1.7 Run-rate cost 95 0.6 1.0 2.9 synergies 50 649 0 243 0 0 115 1.9 1.1 193 103 357 95 96 98 193 216 47 158 159 161 11 A4 FORMAT Adding Scale to an Attractive Recurring Revenue Model Please don’t change page set up to A3, print to A3 paper and fit 2019 Revenue ($B) 2019 Adj. EBITDA ($M) 2019 Net Fleet Value ($B) to scale 39% Margin 34% 40% 0 138 1.7 Run-rate cost 95 0.6 1.0 2.9 synergies 50 649 0 243 0 0 115 1.9 1.1 193 103 357 95 96 98 193 216 47 158 159 161 11

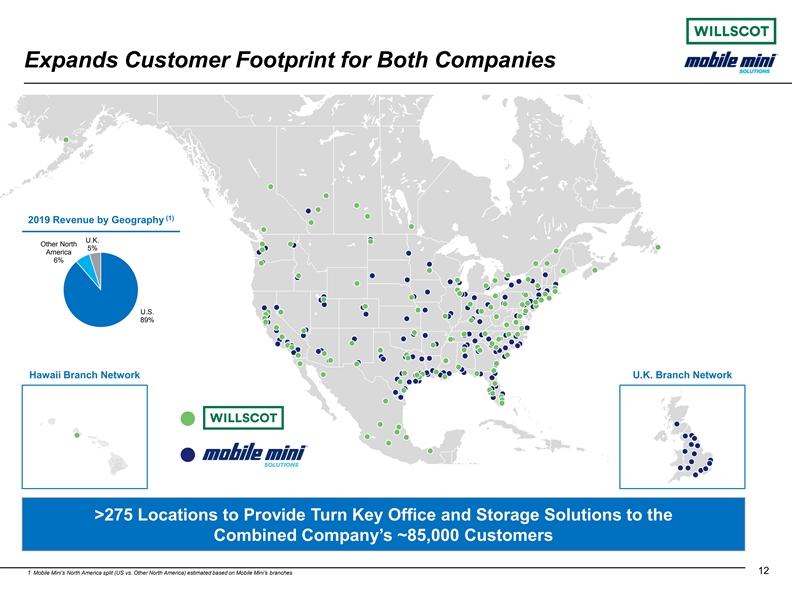

A4 FORMAT Expands Customer Footprint for Both Companies Please don’t change page set up to A3, print to A3 paper and fit to scale 0 138 95 (1) 2019 Revenue by Geography 0 0 U.K. Other North 5% America 0 6% 115 193 103 U.S. 89% 95 96 98 Hawaii Branch Network U.K. Branch Network 193 216 47 158 159 161 >275 Locations to Provide Turn Key Office and Storage Solutions to the Combined Company’s ~85,000 Customers 12 1 Mobile Mini’s North America split (US vs. Other North America) estimated based on Mobile Mini’s branches A4 FORMAT Expands Customer Footprint for Both Companies Please don’t change page set up to A3, print to A3 paper and fit to scale 0 138 95 (1) 2019 Revenue by Geography 0 0 U.K. Other North 5% America 0 6% 115 193 103 U.S. 89% 95 96 98 Hawaii Branch Network U.K. Branch Network 193 216 47 158 159 161 >275 Locations to Provide Turn Key Office and Storage Solutions to the Combined Company’s ~85,000 Customers 12 1 Mobile Mini’s North America split (US vs. Other North America) estimated based on Mobile Mini’s branches

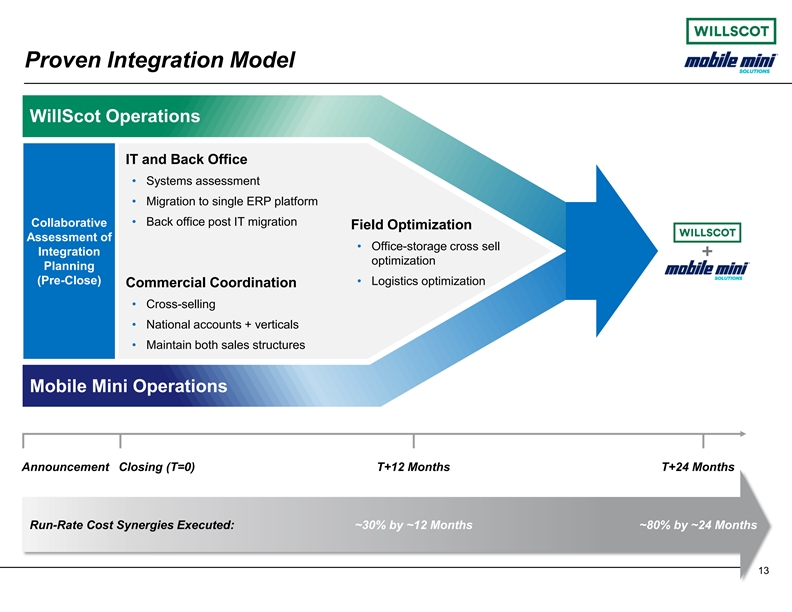

A4 FORMAT Proven Integration Model Please don’t change page set up to A3, WillScot Operations print to A3 paper and fit to scale IT and Back Office #008A5F 0 • Systems assessment 138 95 • Migration to single ERP platform #5D5D5E • Back office post IT migration Collaborative Field Optimization 0 Assessment of 0 • Office-storage cross sell Integration 0 optimization Planning #ACACAC (Pre-Close) • Logistics optimization Commercial Coordination 115 193 • Cross-selling 103 • National accounts + verticals #9BDA44 95 • Maintain both sales structures 96 98 Mobile Mini Operations 193 216 47 158 Announcement Closing (T=0) T+12 Months T+24 Months 159 161 Run-Rate Cost Synergies Executed: ~30% by ~12 Months ~80% by ~24 Months 13 A4 FORMAT Proven Integration Model Please don’t change page set up to A3, WillScot Operations print to A3 paper and fit to scale IT and Back Office #008A5F 0 • Systems assessment 138 95 • Migration to single ERP platform #5D5D5E • Back office post IT migration Collaborative Field Optimization 0 Assessment of 0 • Office-storage cross sell Integration 0 optimization Planning #ACACAC (Pre-Close) • Logistics optimization Commercial Coordination 115 193 • Cross-selling 103 • National accounts + verticals #9BDA44 95 • Maintain both sales structures 96 98 Mobile Mini Operations 193 216 47 158 Announcement Closing (T=0) T+12 Months T+24 Months 159 161 Run-Rate Cost Synergies Executed: ~30% by ~12 Months ~80% by ~24 Months 13

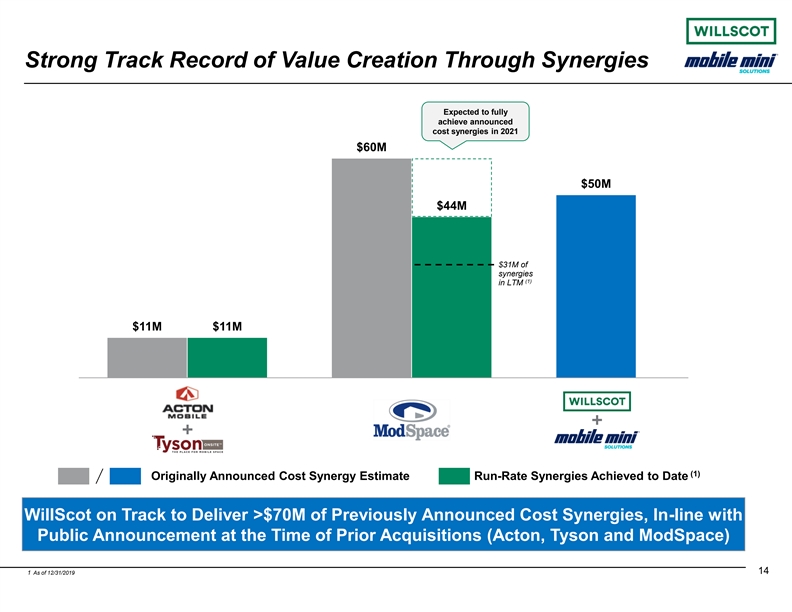

A4 FORMAT Strong Track Record of Value Creation Through Synergies Please don’t change page set up to A3, Expected to fully print to A3 achieve announced cost synergies in 2021 paper and fit to $60M scale 0 138 $50M 95 $44M 0 0 0 $31M of synergies (1) in LTM 115 193 103 $11M $11M 95 96 98 193 216 47 158 (1) 159 Originally Announced Cost Synergy Estimate Run-Rate Synergies Achieved to Date 161 WillScot on Track to Deliver >$70M of Previously Announced Cost Synergies, In-line with Public Announcement at the Time of Prior Acquisitions (Acton, Tyson and ModSpace) 14 1 As of 12/31/2019 A4 FORMAT Strong Track Record of Value Creation Through Synergies Please don’t change page set up to A3, Expected to fully print to A3 achieve announced cost synergies in 2021 paper and fit to $60M scale 0 138 $50M 95 $44M 0 0 0 $31M of synergies (1) in LTM 115 193 103 $11M $11M 95 96 98 193 216 47 158 (1) 159 Originally Announced Cost Synergy Estimate Run-Rate Synergies Achieved to Date 161 WillScot on Track to Deliver >$70M of Previously Announced Cost Synergies, In-line with Public Announcement at the Time of Prior Acquisitions (Acton, Tyson and ModSpace) 14 1 As of 12/31/2019

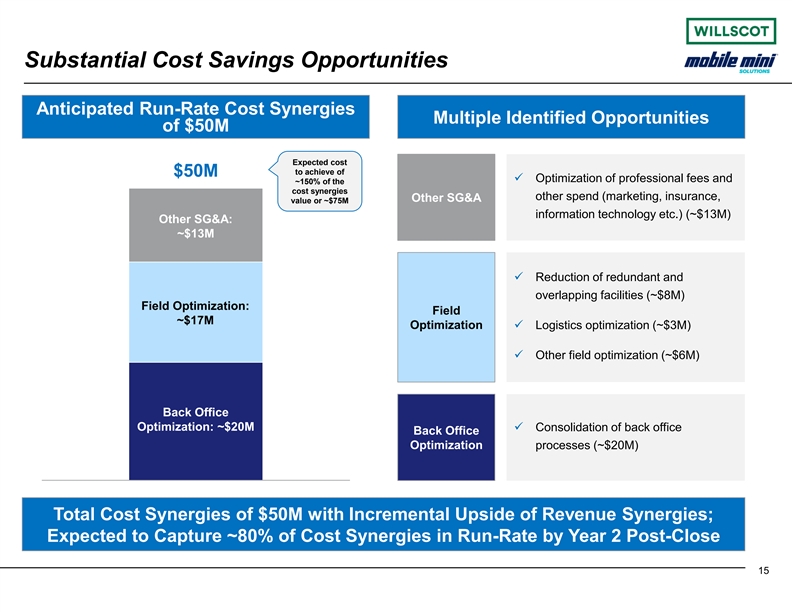

A4 FORMAT Substantial Cost Savings Opportunities Please don’t change page set up to A3, print to Anticipated Run-Rate Cost Synergies A3 paper and fit Multiple Identified Opportunities to scale of $50M Expected cost 0 to achieve of $50M ü Optimization of professional fees and ~150% of the 138 cost synergies 95 other spend (marketing, insurance, Other SG&A value or ~$75M information technology etc.) (~$13M) Other SG&A: 0 ~$13M 0 0 ü Reduction of redundant and 115 overlapping facilities (~$8M) 193 Field Optimization: 103 Field ~$17M Optimization ü Logistics optimization (~$3M) 95 96 ü Other field optimization (~$6M) 98 193 Back Office 216 47 Optimization: ~$20M ü Consolidation of back office Back Office Optimization processes (~$20M) 158 159 Category 1 161 Total Cost Synergies of $50M with Incremental Upside of Revenue Synergies; Expected to Capture ~80% of Cost Synergies in Run-Rate by Year 2 Post-Close 15 A4 FORMAT Substantial Cost Savings Opportunities Please don’t change page set up to A3, print to Anticipated Run-Rate Cost Synergies A3 paper and fit Multiple Identified Opportunities to scale of $50M Expected cost 0 to achieve of $50M ü Optimization of professional fees and ~150% of the 138 cost synergies 95 other spend (marketing, insurance, Other SG&A value or ~$75M information technology etc.) (~$13M) Other SG&A: 0 ~$13M 0 0 ü Reduction of redundant and 115 overlapping facilities (~$8M) 193 Field Optimization: 103 Field ~$17M Optimization ü Logistics optimization (~$3M) 95 96 ü Other field optimization (~$6M) 98 193 Back Office 216 47 Optimization: ~$20M ü Consolidation of back office Back Office Optimization processes (~$20M) 158 159 Category 1 161 Total Cost Synergies of $50M with Incremental Upside of Revenue Synergies; Expected to Capture ~80% of Cost Synergies in Run-Rate by Year 2 Post-Close 15

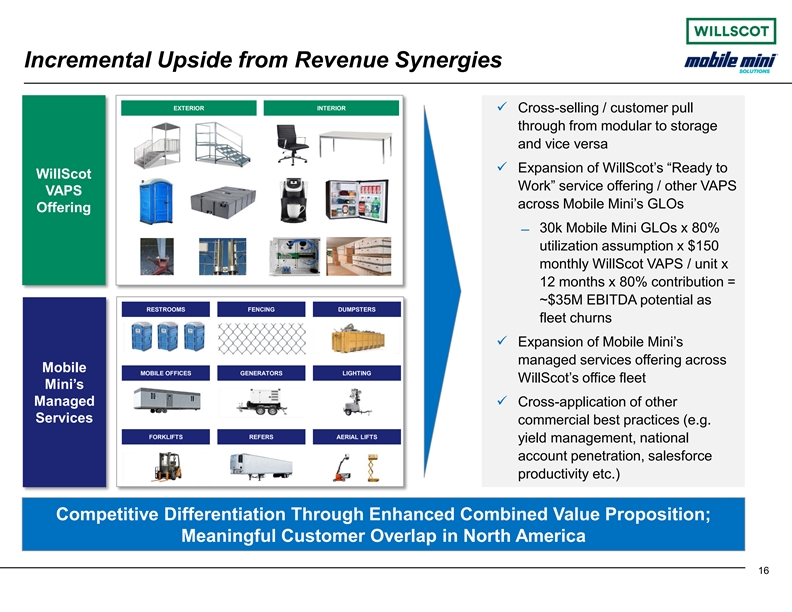

A4 FORMAT Incremental Upside from Revenue Synergies Please don’t change page set up to A3, print to EXTERIOR INTERIOR ü Cross-selling / customer pull A3 paper and fit through from modular to storage to scale and vice versa 0 ü Expansion of WillScot’s “Ready to WillScot 138 Work” service offering / other VAPS VAPS 95 across Mobile Mini’s GLOs Offering 0 ̶ 30k Mobile Mini GLOs x 80% 0 utilization assumption x $150 0 monthly WillScot VAPS / unit x 12 months x 80% contribution = 115 193 ~$35M EBITDA potential as RESTROOMS FENCING DUMPSTERS 103 fleet churns 95 ü Expansion of Mobile Mini’s 96 managed services offering across 98 Mobile MOBILE OFFICES GENERATORS LIGHTING WillScot’s office fleet Mini’s 193 Managed ü Cross-application of other 216 Services commercial best practices (e.g. 47 FORKLIFTS REFERS AERIAL LIFTS yield management, national account penetration, salesforce 158 159 productivity etc.) 161 Competitive Differentiation Through Enhanced Combined Value Proposition; Meaningful Customer Overlap in North America 16 A4 FORMAT Incremental Upside from Revenue Synergies Please don’t change page set up to A3, print to EXTERIOR INTERIOR ü Cross-selling / customer pull A3 paper and fit through from modular to storage to scale and vice versa 0 ü Expansion of WillScot’s “Ready to WillScot 138 Work” service offering / other VAPS VAPS 95 across Mobile Mini’s GLOs Offering 0 ̶ 30k Mobile Mini GLOs x 80% 0 utilization assumption x $150 0 monthly WillScot VAPS / unit x 12 months x 80% contribution = 115 193 ~$35M EBITDA potential as RESTROOMS FENCING DUMPSTERS 103 fleet churns 95 ü Expansion of Mobile Mini’s 96 managed services offering across 98 Mobile MOBILE OFFICES GENERATORS LIGHTING WillScot’s office fleet Mini’s 193 Managed ü Cross-application of other 216 Services commercial best practices (e.g. 47 FORKLIFTS REFERS AERIAL LIFTS yield management, national account penetration, salesforce 158 159 productivity etc.) 161 Competitive Differentiation Through Enhanced Combined Value Proposition; Meaningful Customer Overlap in North America 16

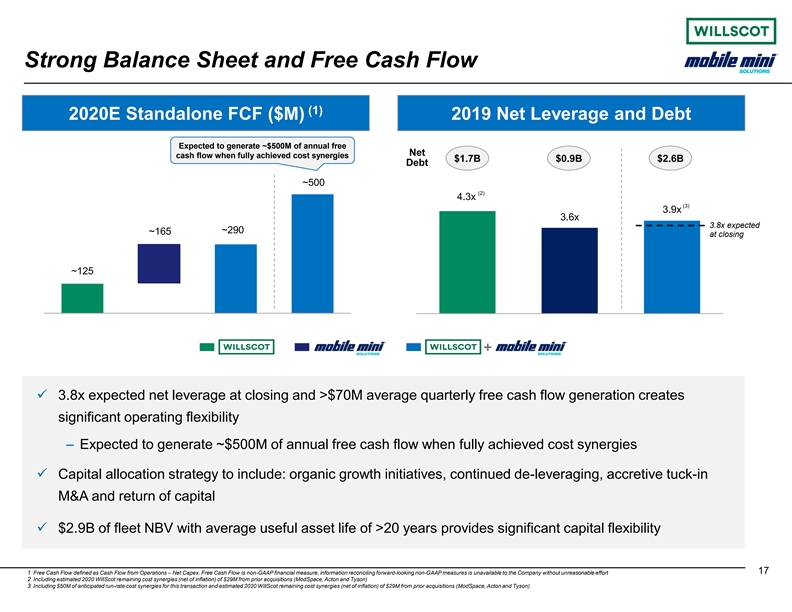

A4 FORMAT Strong Balance Sheet and Free Cash Flow Please don’t change page set up to A3, print to (1) A3 paper and fit 2020E Standalone FCF ($M) 2019 Net Leverage and Debt to scale Expected to generate ~$500M of annual free Net cash flow when fully achieved cost synergies $1.7B $0.9B $2.6B Debt 0 138 ~500 (2) 95 4.3x (3) 3.9x 3.6x 3.8x expected 0 ~290 ~165 at closing 0 0 ~125 115 193 103 95 96 98 ü 3.8x expected net leverage at closing and >$70M average quarterly free cash flow generation creates 193 216 significant operating flexibility 47 ‒ Expected to generate ~$500M of annual free cash flow when fully achieved cost synergies 158 159 ü Capital allocation strategy to include: organic growth initiatives, continued de-leveraging, accretive tuck-in 161 M&A and return of capital ü $2.9B of fleet NBV with average useful asset life of >20 years provides significant capital flexibility 17 1 Free Cash Flow defined as Cash Flow from Operations – Net Capex. Free Cash Flow is non-GAAP financial measure, information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort 2 Including estimated 2020 WillScot remaining cost synergies (net of inflation) of $29M from prior acquisitions (ModSpace, Acton and Tyson) 3 Including $50M of anticipated run-rate cost synergies for this transaction and estimated 2020 WillScot remaining cost synergies (net of inflation) of $29M from prior acquisitions (ModSpace, Acton and Tyson) A4 FORMAT Strong Balance Sheet and Free Cash Flow Please don’t change page set up to A3, print to (1) A3 paper and fit 2020E Standalone FCF ($M) 2019 Net Leverage and Debt to scale Expected to generate ~$500M of annual free Net cash flow when fully achieved cost synergies $1.7B $0.9B $2.6B Debt 0 138 ~500 (2) 95 4.3x (3) 3.9x 3.6x 3.8x expected 0 ~290 ~165 at closing 0 0 ~125 115 193 103 95 96 98 ü 3.8x expected net leverage at closing and >$70M average quarterly free cash flow generation creates 193 216 significant operating flexibility 47 ‒ Expected to generate ~$500M of annual free cash flow when fully achieved cost synergies 158 159 ü Capital allocation strategy to include: organic growth initiatives, continued de-leveraging, accretive tuck-in 161 M&A and return of capital ü $2.9B of fleet NBV with average useful asset life of >20 years provides significant capital flexibility 17 1 Free Cash Flow defined as Cash Flow from Operations – Net Capex. Free Cash Flow is non-GAAP financial measure, information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort 2 Including estimated 2020 WillScot remaining cost synergies (net of inflation) of $29M from prior acquisitions (ModSpace, Acton and Tyson) 3 Including $50M of anticipated run-rate cost synergies for this transaction and estimated 2020 WillScot remaining cost synergies (net of inflation) of $29M from prior acquisitions (ModSpace, Acton and Tyson)

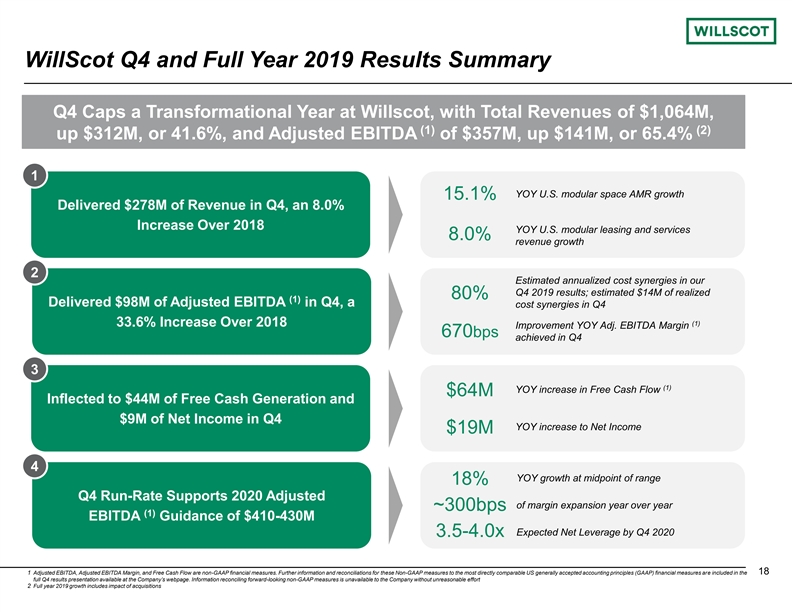

A4 FORMAT WillScot Q4 and Full Year 2019 Results Summary Please don’t change page set up to A3, Q4 Caps a Transformational Year at Willscot, with Total Revenues of $1,064M, print to A3 (1) (2) paper and fit to up $312M, or 41.6%, and Adjusted EBITDA of $357M, up $141M, or 65.4% scale 0 1 138 YOY U.S. modular space AMR growth 15.1% 95 Delivered $278M of Revenue in Q4, an 8.0% Increase Over 2018 0 YOY U.S. modular leasing and services 8.0% revenue growth 0 0 2 Estimated annualized cost synergies in our 115 Q4 2019 results; estimated $14M of realized 80% (1) 193 Delivered $98M of Adjusted EBITDA in Q4, a cost synergies in Q4 103 (1) 33.6% Increase Over 2018 Improvement YOY Adj. EBITDA Margin 670bps achieved in Q4 95 96 98 3 (1) YOY increase in Free Cash Flow $64M Inflected to $44M of Free Cash Generation and 193 216 $9M of Net Income in Q4 YOY increase to Net Income 47 $19M 158 4 159 YOY growth at midpoint of range 18% 161 Q4 Run-Rate Supports 2020 Adjusted of margin expansion year over year ~300bps (1) EBITDA Guidance of $410-430M Expected Net Leverage by Q4 2020 3.5-4.0x 1 Adjusted EBITDA, Adjusted EBITDA Margin, and Free Cash Flow are non-GAAP financial measures. Further information and reconciliations for these Non-GAAP measures to the most directly comparable US generally accepted accounting principles (GAAP) financial measures are included in the 18 full Q4 results presentation available at the Company’s webpage. Information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort 2 Full year 2019 growth includes impact of acquisitions A4 FORMAT WillScot Q4 and Full Year 2019 Results Summary Please don’t change page set up to A3, Q4 Caps a Transformational Year at Willscot, with Total Revenues of $1,064M, print to A3 (1) (2) paper and fit to up $312M, or 41.6%, and Adjusted EBITDA of $357M, up $141M, or 65.4% scale 0 1 138 YOY U.S. modular space AMR growth 15.1% 95 Delivered $278M of Revenue in Q4, an 8.0% Increase Over 2018 0 YOY U.S. modular leasing and services 8.0% revenue growth 0 0 2 Estimated annualized cost synergies in our 115 Q4 2019 results; estimated $14M of realized 80% (1) 193 Delivered $98M of Adjusted EBITDA in Q4, a cost synergies in Q4 103 (1) 33.6% Increase Over 2018 Improvement YOY Adj. EBITDA Margin 670bps achieved in Q4 95 96 98 3 (1) YOY increase in Free Cash Flow $64M Inflected to $44M of Free Cash Generation and 193 216 $9M of Net Income in Q4 YOY increase to Net Income 47 $19M 158 4 159 YOY growth at midpoint of range 18% 161 Q4 Run-Rate Supports 2020 Adjusted of margin expansion year over year ~300bps (1) EBITDA Guidance of $410-430M Expected Net Leverage by Q4 2020 3.5-4.0x 1 Adjusted EBITDA, Adjusted EBITDA Margin, and Free Cash Flow are non-GAAP financial measures. Further information and reconciliations for these Non-GAAP measures to the most directly comparable US generally accepted accounting principles (GAAP) financial measures are included in the 18 full Q4 results presentation available at the Company’s webpage. Information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort 2 Full year 2019 growth includes impact of acquisitions

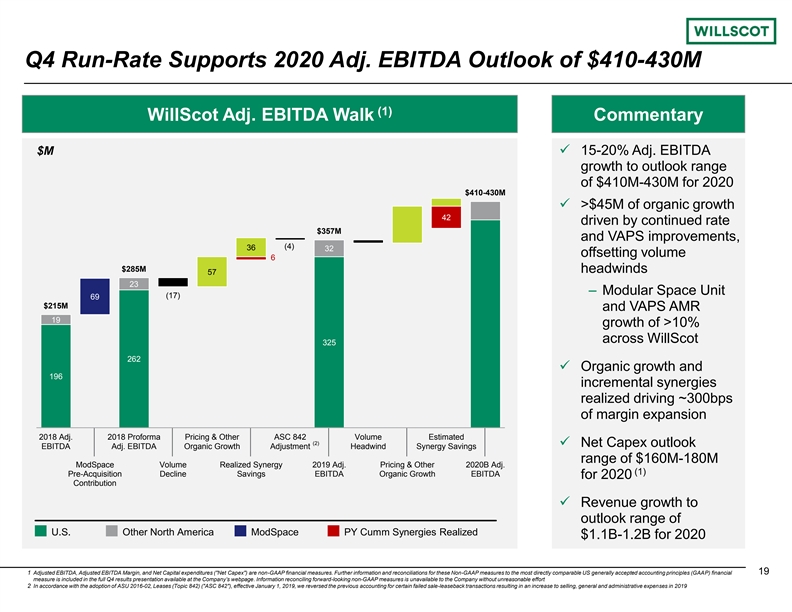

A4 FORMAT Q4 Run-Rate Supports 2020 Adj. EBITDA Outlook of $410-430M Please don’t change page set up to A3, (1) WillScot Adj. EBITDA Walk Commentary print to A3 paper and fit to scale $M ü 15-20% Adj. EBITDA growth to outlook range 0 of $410M-430M for 2020 138 $410-430M 95 ü >$45M of organic growth 42 driven by continued rate 0 $357M and VAPS improvements, 0 (4) 36 32 offsetting volume 0 6 $285M headwinds 57 23 115 ‒ Modular Space Unit (17) 69 193 $215M and VAPS AMR 103 19 growth of >10% across WillScot 325 95 96 262 ü Organic growth and 98 196 incremental synergies realized driving ~300bps 193 216 of margin expansion 47 2018 Adj. 2018 Proforma Pricing & Other ASC 842 Volume Estimated (2) ü Net Capex outlook EBITDA Adj. EBITDA Organic Growth Adjustment Headwind Synergy Savings range of $160M-180M 158 ModSpace Volume Realized Synergy 2019 Adj. Pricing & Other 2020B Adj. (1) 159 Pre-Acquisition Decline Savings EBITDA Organic Growth EBITDA for 2020 Contribution 161 ü Revenue growth to outlook range of U.S. Other North America ModSpace PY Cumm Synergies Realized $1.1B-1.2B for 2020 1 Adjusted EBITDA, Adjusted EBITDA Margin, and Net Capital expenditures ( Net Capex ) are non-GAAP financial measures. Further information and reconciliations for these Non-GAAP measures to the most directly comparable US generally accepted accounting principles (GAAP) financial 19 measure is included in the full Q4 results presentation available at the Company’s webpage. Information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort 2 In accordance with the adoption of ASU 2016-02, Leases (Topic 842) ( ASC 842 ), effective January 1, 2019, we reversed the previous accounting for certain failed sale-leaseback transactions resulting in an increase to selling, general and administrative expenses in 2019 A4 FORMAT Q4 Run-Rate Supports 2020 Adj. EBITDA Outlook of $410-430M Please don’t change page set up to A3, (1) WillScot Adj. EBITDA Walk Commentary print to A3 paper and fit to scale $M ü 15-20% Adj. EBITDA growth to outlook range 0 of $410M-430M for 2020 138 $410-430M 95 ü >$45M of organic growth 42 driven by continued rate 0 $357M and VAPS improvements, 0 (4) 36 32 offsetting volume 0 6 $285M headwinds 57 23 115 ‒ Modular Space Unit (17) 69 193 $215M and VAPS AMR 103 19 growth of >10% across WillScot 325 95 96 262 ü Organic growth and 98 196 incremental synergies realized driving ~300bps 193 216 of margin expansion 47 2018 Adj. 2018 Proforma Pricing & Other ASC 842 Volume Estimated (2) ü Net Capex outlook EBITDA Adj. EBITDA Organic Growth Adjustment Headwind Synergy Savings range of $160M-180M 158 ModSpace Volume Realized Synergy 2019 Adj. Pricing & Other 2020B Adj. (1) 159 Pre-Acquisition Decline Savings EBITDA Organic Growth EBITDA for 2020 Contribution 161 ü Revenue growth to outlook range of U.S. Other North America ModSpace PY Cumm Synergies Realized $1.1B-1.2B for 2020 1 Adjusted EBITDA, Adjusted EBITDA Margin, and Net Capital expenditures ( Net Capex ) are non-GAAP financial measures. Further information and reconciliations for these Non-GAAP measures to the most directly comparable US generally accepted accounting principles (GAAP) financial 19 measure is included in the full Q4 results presentation available at the Company’s webpage. Information reconciling forward-looking non-GAAP measures is unavailable to the Company without unreasonable effort 2 In accordance with the adoption of ASU 2016-02, Leases (Topic 842) ( ASC 842 ), effective January 1, 2019, we reversed the previous accounting for certain failed sale-leaseback transactions resulting in an increase to selling, general and administrative expenses in 2019

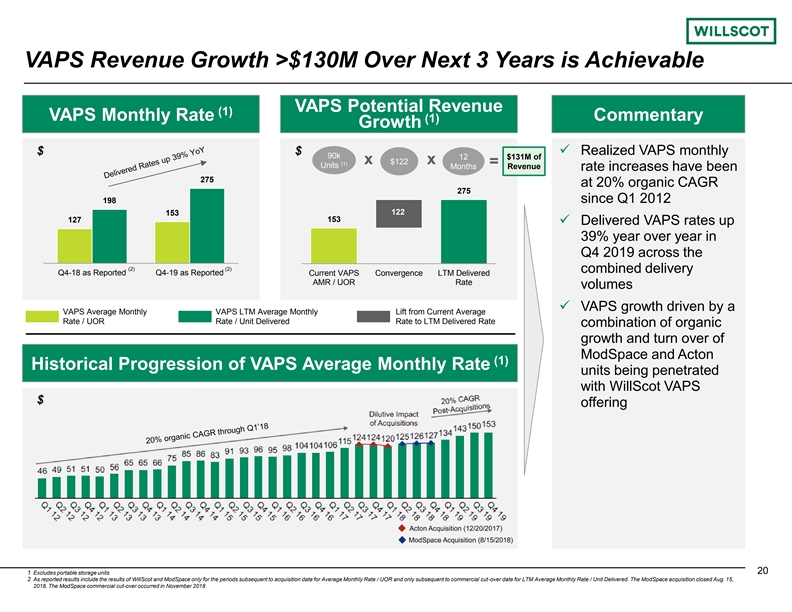

A4 FORMAT VAPS Revenue Growth >$130M Over Next 3 Years is Achievable Please don’t change page set up to A3, print to VAPS Potential Revenue (1) A3 paper and fit VAPS Monthly Rate Commentary (1) Growth to scale $ $ ü Realized VAPS monthly 90k 12 $131M of x $122 x (1) = Units Months Revenue rate increases have been 0 275 138 at 20% organic CAGR 275 95 198 since Q1 2012 122 153 153 127 ü Delivered VAPS rates up 0 39% year over year in 0 0 Q4 2019 across the (2) (2) combined delivery Q4-18 as Reported Q4-19 as Reported Current VAPS Convergence LTM Delivered AMR / UOR Rate 115 volumes 193 ü VAPS growth driven by a 103 VAPS Average Monthly VAPS LTM Average Monthly Lift from Current Average Rate / UOR Rate / Unit Delivered Rate to LTM Delivered Rate combination of organic growth and turn over of 95 96 ModSpace and Acton (1) Historical Progression of VAPS Average Monthly Rate 98 units being penetrated with WillScot VAPS 193 $ offering 216 47 158 159 161 20 1 Excludes portable storage units 2 As reported results include the results of WillScot and ModSpace only for the periods subsequent to acquisition date for Average Monthly Rate / UOR and only subsequent to commercial cut-over date for LTM Average Monthly Rate / Unit Delivered. The ModSpace acquisition closed Aug. 15, 2018. The ModSpace commercial cut-over occurred in November 2018 A4 FORMAT VAPS Revenue Growth >$130M Over Next 3 Years is Achievable Please don’t change page set up to A3, print to VAPS Potential Revenue (1) A3 paper and fit VAPS Monthly Rate Commentary (1) Growth to scale $ $ ü Realized VAPS monthly 90k 12 $131M of x $122 x (1) = Units Months Revenue rate increases have been 0 275 138 at 20% organic CAGR 275 95 198 since Q1 2012 122 153 153 127 ü Delivered VAPS rates up 0 39% year over year in 0 0 Q4 2019 across the (2) (2) combined delivery Q4-18 as Reported Q4-19 as Reported Current VAPS Convergence LTM Delivered AMR / UOR Rate 115 volumes 193 ü VAPS growth driven by a 103 VAPS Average Monthly VAPS LTM Average Monthly Lift from Current Average Rate / UOR Rate / Unit Delivered Rate to LTM Delivered Rate combination of organic growth and turn over of 95 96 ModSpace and Acton (1) Historical Progression of VAPS Average Monthly Rate 98 units being penetrated with WillScot VAPS 193 $ offering 216 47 158 159 161 20 1 Excludes portable storage units 2 As reported results include the results of WillScot and ModSpace only for the periods subsequent to acquisition date for Average Monthly Rate / UOR and only subsequent to commercial cut-over date for LTM Average Monthly Rate / Unit Delivered. The ModSpace acquisition closed Aug. 15, 2018. The ModSpace commercial cut-over occurred in November 2018

A4 FORMAT WillScot and Mobile Mini Are the Right Partners Please don’t change page set up to A3, print to A3 paper and fit to scale ü After a thorough review of the industry prospects and strategic alternatives, the WillScot and Mobile Mini boards concluded the transaction is the best value creation opportunity for both shareholders 0 138 95 ü Key considerations included: 0 0 ̶ Shareholder value creation potential based on strategic and financial profile of combined company 0 ̶ Compelling cost and revenue synergy potential of combination 115 193 103 ̶ Execution and integration capabilities of WillScot and Mobile Mini 95 ̶ Complementary nature of fleets, footprint, strategic vision, and culture 96 98 193 ü Robust review process conducted by both companies: 216 47 ̶ Review included input from independent financial, legal and commercial advisors 158 159 ̶ Jointly and independently concluded that this is the preferred strategic partnership 161 ̶ Board approval for both WillScot and Mobile Mini 21 A4 FORMAT WillScot and Mobile Mini Are the Right Partners Please don’t change page set up to A3, print to A3 paper and fit to scale ü After a thorough review of the industry prospects and strategic alternatives, the WillScot and Mobile Mini boards concluded the transaction is the best value creation opportunity for both shareholders 0 138 95 ü Key considerations included: 0 0 ̶ Shareholder value creation potential based on strategic and financial profile of combined company 0 ̶ Compelling cost and revenue synergy potential of combination 115 193 103 ̶ Execution and integration capabilities of WillScot and Mobile Mini 95 ̶ Complementary nature of fleets, footprint, strategic vision, and culture 96 98 193 ü Robust review process conducted by both companies: 216 47 ̶ Review included input from independent financial, legal and commercial advisors 158 159 ̶ Jointly and independently concluded that this is the preferred strategic partnership 161 ̶ Board approval for both WillScot and Mobile Mini 21

A4 FORMAT Merger Benefits All Stakeholders Please don’t change page set up to A3, print to A3 Combines Two Leading Specialty Leasing Platforms paper and fit to scale #008A5F 0 138 95 Complementary Fleet and Enhanced Ability to Serve Customers #5D5D5E 0 0 0 #ACACAC 115 Creates Scale Platform and Expands Customer Footprint 193 103 #9BDA44 95 $50M of Clearly Identified Cost Synergies with Incremental Upside from 96 98 Potential Revenue Synergies 193 216 47 Brings Together Two Industry Leading, Best-in-Class Teams with Proven Track Record of Delivering Profitable Growth and Shareholder Value 158 159 161 Unique Opportunity to Drive Substantial Value Creation 22 A4 FORMAT Merger Benefits All Stakeholders Please don’t change page set up to A3, print to A3 Combines Two Leading Specialty Leasing Platforms paper and fit to scale #008A5F 0 138 95 Complementary Fleet and Enhanced Ability to Serve Customers #5D5D5E 0 0 0 #ACACAC 115 Creates Scale Platform and Expands Customer Footprint 193 103 #9BDA44 95 $50M of Clearly Identified Cost Synergies with Incremental Upside from 96 98 Potential Revenue Synergies 193 216 47 Brings Together Two Industry Leading, Best-in-Class Teams with Proven Track Record of Delivering Profitable Growth and Shareholder Value 158 159 161 Unique Opportunity to Drive Substantial Value Creation 22