|

Exhibit 99.1

|

Exhibit 99.1

Casella Waste Systems, Inc.

KeyBanc Capital Markets’

Industrial, Automotive &

Transportation Conference

May 28, 2015

Safe harbor statement

Certain matters discussed in this presentation are “forward-looking statements” intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can generally be identified as such by the context of the statements, including words such as “believe,” “expect,” “anticipate,” “plan,” “may,” “would,” “intend,” “estimate,” “guidance” and other similar expressions, whether in the negative or affirmative. These forward-looking statements are based on current expectations, estimates, forecasts and projections about the industry and markets in which we operate and management’s beliefs and assumptions. We cannot guarantee that we actually will achieve the plans, intentions, expectations or guidance disclosed in the forward-looking statements made. Such forward-looking statements, and all phases of our operations, involve a number of risks and uncertainties, any one or more of which could cause actual results to differ materially from those described in our forward-looking statements. Such risks and uncertainties include or relate to, among other things: adverse weather conditions that have negatively impacted and may continue to negatively impact our revenues and our operating margin; current economic conditions that have adversely affected and may continue to adversely affect our revenues and our operating margin; we may be unable to increase volumes at our landfills or improve our route profitability; our need to service our indebtedness may limit our ability to invest in our business; we may be unable to reduce costs or increase pricing or volumes sufficiently to achieve estimated Adjusted EBITDA and other targets; landfill operations and permit status may be affected by factors outside our control; we may be required to incur capital expenditures in excess of our estimates; fluctuations in energy pricing or the commodity pricing of our recyclables may make it more difficult for us to predict our results of operations or meet our estimates; actions of activist investors and the cost and disruption of responding to those actions; and we may incur environmental charges or asset impairments in the future. There are a number of other important risks and uncertainties that could cause our actual results to differ materially from those indicated by such forward-looking statements. These additional risks and uncertainties include, without limitation, those detailed in Item 1A, “Risk Factors” in our Form 10-KT for the transition period ended December 31, 2014 and in our Form 10-Q for the quarterly period ended March 31, 2015.

We undertake no obligation to update publicly any forward-looking statements whether as a result of new information, future events or otherwise, except as required by the federal securities laws.

Casella Waste Systems—Overview

Casella provides integrated solid waste, recycling and resource services.

$529.3 mm of revenues for LTM ended 3/31/15.

Integrated solid waste and recycling services in six northeast states.

Strategy focused on delivering customers resource and waste solutions.

Tying economic and environmental models together to create incremental value from traditional waste streams.

Provide customers unique resource solutions through Zero-Sort® recycling, organics, and clean energy programs.

Casella Waste Systems 3

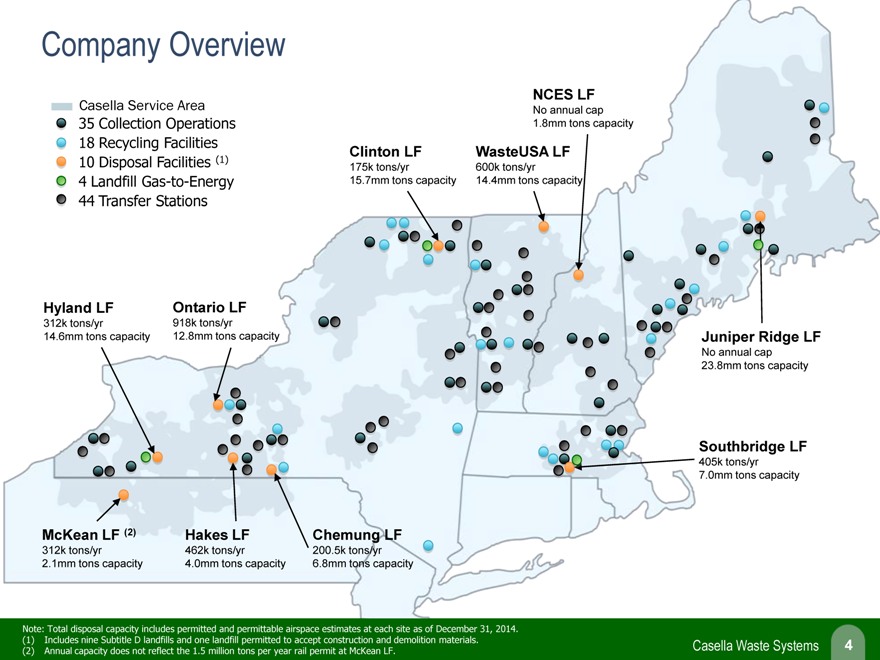

Company Overview

Casella Service Area

35 Collection Operations

18 Recycling Facilities

10 Disposal Facilities (1)

44 Transfer Stations

Clinton LF

175k tons/yr

15.7mm tons capacity

WasteUSA LF

600k tons/yr

14.4mm tons capacity

NCES LF

No annual cap 1.8mm tons capacity

Hyland LF

312k tons/yr

14.6mm tons capacity

Ontario LF

918k tons/yr

12.8mm tons capacity

Juniper Ridge LF

No annual cap 23.8mm tons capacity

Juniper Ridge LF

No annual cap 23.8mm tons capacity

McKean LF (2)

312k tons/yr

2.1mm tons capacity

Hakes LF

462k tons/yr

4.0mm tons capacity

Chemung LF

200.5k tons/yr 6.8mm tons capacity

Southbridge LF

405k tons/yr

7.0mm tons capacity

Note: Total disposal capacity includes permitted and permittable airspace estimates at each site as of December 31, 2014.

(1) | | Includes nine Subtitle D landfills and one landfill permitted to accept construction and demolition materials. |

(2) | | Annual capacity does not reflect the 1.5 million tons per year rail permit at McKean LF. |

Casella Waste Systems 4

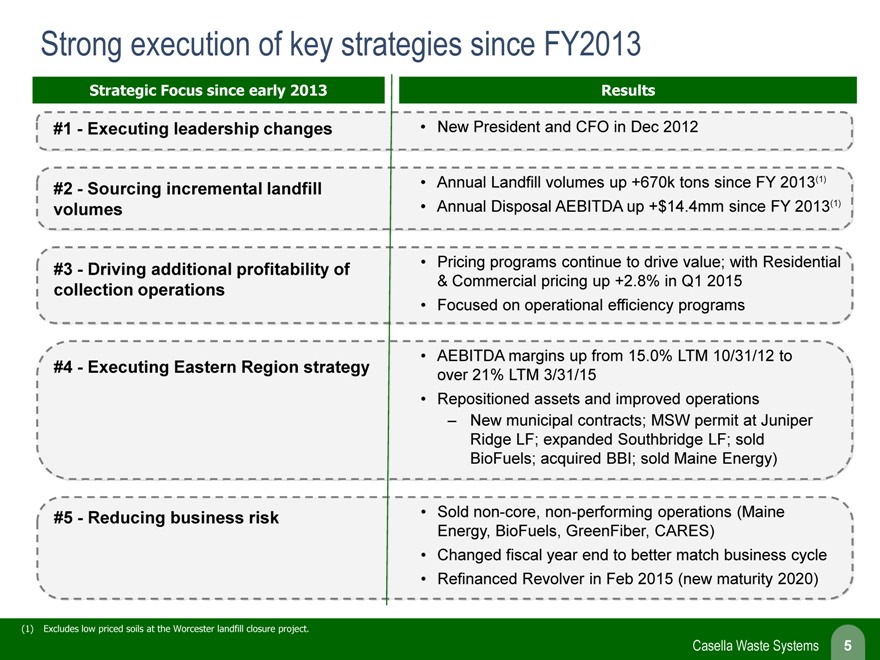

Strong execution of key strategies since FY2013

Strategic Focus since early 2013

#1—Executing leadership changes

#2—Sourcing incremental landfill volumes

#3—Driving additional profitability of collection operations

#4—Executing Eastern Region strategy

#5—Reducing business risk

Results

New President and CFO in Dec 2012

Annual Landfill volumes up +670k tons since FY 2013(1)

Annual Disposal AEBITDA up +$14.4mm since FY 2013(1)

Pricing programs continue to drive value; with Residential

& Commercial pricing up +2.8% in Q1 2015

Focused on operational efficiency programs

AEBITDA margins up from 15.0% LTM 10/31/12 to over 21% LTM 3/31/15

Repositioned assets and improved operations

New municipal contracts; MSW permit at Juniper Ridge LF; expanded Southbridge LF; sold BioFuels; acquired BBI; sold Maine Energy)

Sold non-core, non-performing operations (Maine Energy, BioFuels, GreenFiber, CARES)

Changed fiscal year end to better match business cycle

Refinanced Revolver in Feb 2015 (new maturity 2020)

(1) | | Excludes low priced soils at the Worcester landfill closure project. |

Casella Waste Systems 5

Results up significantly on strategic execution

Revenue ($mm)

$ 529.3

$ 497.6

$ 530

to

$ 455.3

$ 520

FYE

FYE

LTM

2015

4/30/13

4/30/14

3/31/15

Guidance

Adj EBITDA ($mm) & Margin (1)

19.3% 20.0% 19.1% 18.5%

$97.9 $107 $95.1 to $87.8 $103

FYE FYE LTM 2015 4/30/13 4/30/14 3/31/15 Guidance

(1) | | Please refer to the appendix for a reconciliation of Adjusted EBITDA to the comparable GAAP numbers. |

(2) | | Disposal Revenue includes Worcester landfill. |

(3) | | Excludes low-priced soils at the Worcester landfill closure project. |

Results since FY 2013:

Revenue growth +$74.0mm (or +16.3%) mainly driven by Disposal (+$26.6mm)(2), Collection (+$21.4mm), and Customer Solutions (+$17.9mm).

Adj. EBITDA up +$10.1mm (or +11.5%) mainly driven by higher landfill volumes and strategic execution.

Landfill tons up +670k annually (or +18.8%).(3)

Residential and Commercial collection price increases accelerating (up +2.8% in Q1 2015).

Casella Waste Systems 6

Strategic Focus in 2015 and beyond

Management focused in key areas to increase free cash flow and to reduce debt leverage:

1 | | Increasing landfill returns |

2 | | Driving additional profitability in collection operations |

3 | | Creating incremental value through Resource Solutions |

4 | | Improving balance sheet and reducing risk |

Casella Waste Systems 7

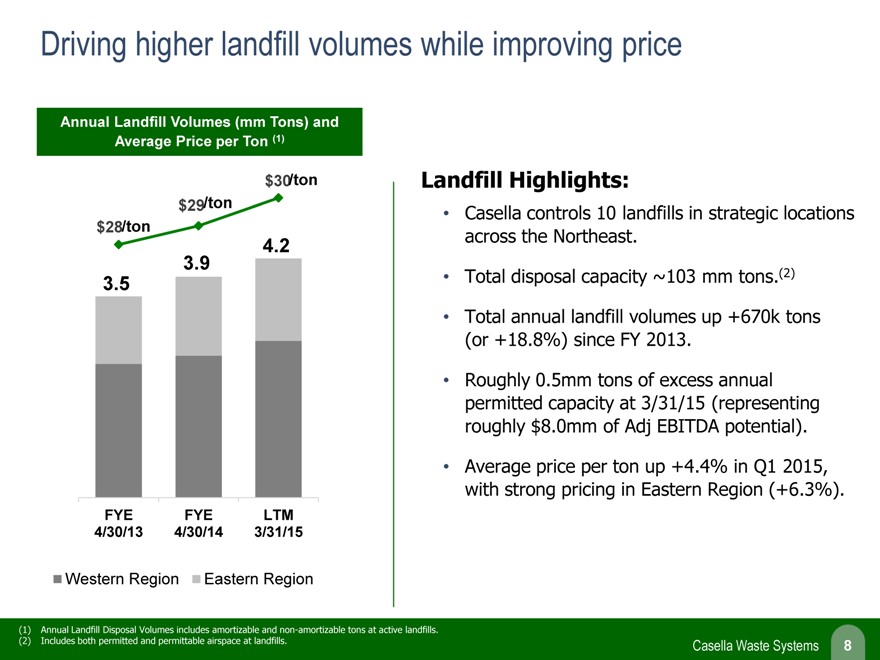

Driving higher landfill volumes while improving price

Annual Landfill Volumes (mm Tons) and Average Price per Ton (1)

$30/ton

$29/ton

$28/ton

3.9 4.2 35 .

FYE FYE LTM 4/30/13 4/30/14 3/31/15

Western Region Eastern Region

(1) | | Annual Landfill Disposal Volumes includes amortizable and non-amortizable tons at active landfills. |

(2) | | Includes both permitted and permittable airspace at landfills. |

Landfill Highlights:

Casella controls 10 landfills in strategic locations across the Northeast.

Total disposal capacity ~103 mm tons.(2)

Total annual landfill volumes up +670k tons (or +18.8%) since FY 2013.

Roughly 0.5mm tons of excess annual permitted capacity at 3/31/15 (representing roughly $8.0mm of Adj EBITDA potential).

Average price per ton up +4.4% in Q1 2015, with strong pricing in Eastern Region (+6.3%).

Casella Waste Systems 8

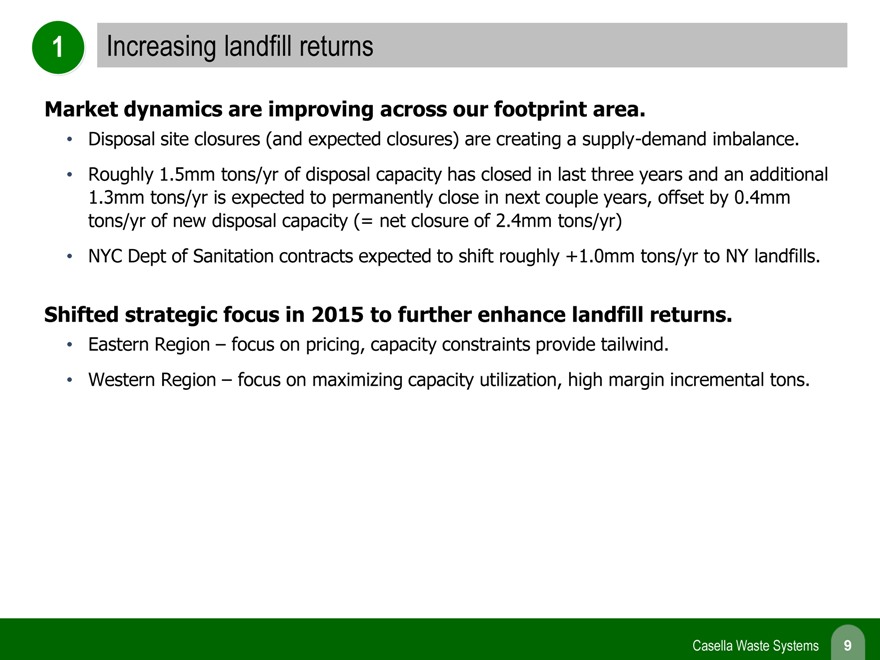

1 Increasing landfill returns

Market dynamics are improving across our footprint area.

Disposal site closures (and expected closures) are creating a supply-demand imbalance.

Roughly 1.5mm tons/yr of disposal capacity has closed in last three years and an additional 1.3mm tons/yr is expected to permanently close in next couple years, offset by 0.4mm tons/yr of new disposal capacity (= net closure of 2.4mm tons/yr)

NYC Dept of Sanitation contracts expected to shift roughly +1.0mm tons/yr to NY landfills.

Shifted strategic focus in 2015 to further enhance landfill returns.

Eastern Region – focus on pricing, capacity constraints provide tailwind.

Western Region focus on maximizing capacity utilization, high margin incremental tons.

Casella Waste Systems 9

Disposal market in dynamics Northeast are isshifting contracting

10 Disposal Facilities

4 | | Landfill Gas-to-Energy Facilities |

Other18 disposal Recycling sites ( closed Facilities or potential 10 to Disposal close) Facilities

2 | | New Disposal Facilities online Expected 35 Collection NYC waste Operations flows |

Clinton LF

175k tons/yr

15.7mm tons capacity

WasteUSA LF

600k tons/yr

14.4mm tons capacity

NCES LF

No annual cap

1.8mm tons capacity

Juniper Ridge LF

No annual cap 23.8mm tons capacity

Hyland LF

312k tons/yr

14.6mm tons capacity

Ontario LF

918k tons/yr

12.8mm tons capacity

Finch LF

130k tons/yr New 2014

Moretown LF

286k tons/yr, Closed 2013

MERC WTE

300k tons/yr, Closed 2012

PERC WTE

300k tons/yr

Rockland

45k tons/yr, Closing 2015

Claremont WTE

73k tons/yr, Closed 2013

Albany LF

275k tons/yr Closing 2016

Dunn LF

~300k tons/yr New 2015

Southbridge LF

405k tons/yr

7.0mm tons capacity

McKean LF (1)

312k tons/yr

2.1mm tons capacity

Hakes LF

462k tons/yr

4.0mm tons capacity

Chemung LF

200.5k tons/yr 6.8mm tons capacity

Wallingford

130k tons/yr Closing 2015

Fall River LF

376k tons/yr, Closed 2014

Taunton LF

120k tons/yr Closing 2018

1 | | Granby LF—235k tons/yr, Closed 2014 |

2 | | S. Hadley LF – 156k tons/yr, Closed 2014 |

3 | | Barre LF—94k tons/yr, Closing 2015 |

4 | | Northampton LF – 50k tons/yr, Closed 2013 |

5 | | Chicopee LF—365k tons/yr, Closing 2018 |

NYC Dept of Sanitation

10k – 12k tons per day.

Building 4 marine transfer stations to transload waste to rail (expect 2 built by early 2015).

Expect an additional 1.0m tons/yr to be disposed in NY.

Note: Total disposal capacity includes permitted and permittable airspace estimates at each site as of December 31, 2014.

(1) | | Annual capacity does not reflect the 1.5mm tons per year rail permit at McKean LF. |

Casella Waste Systems 10

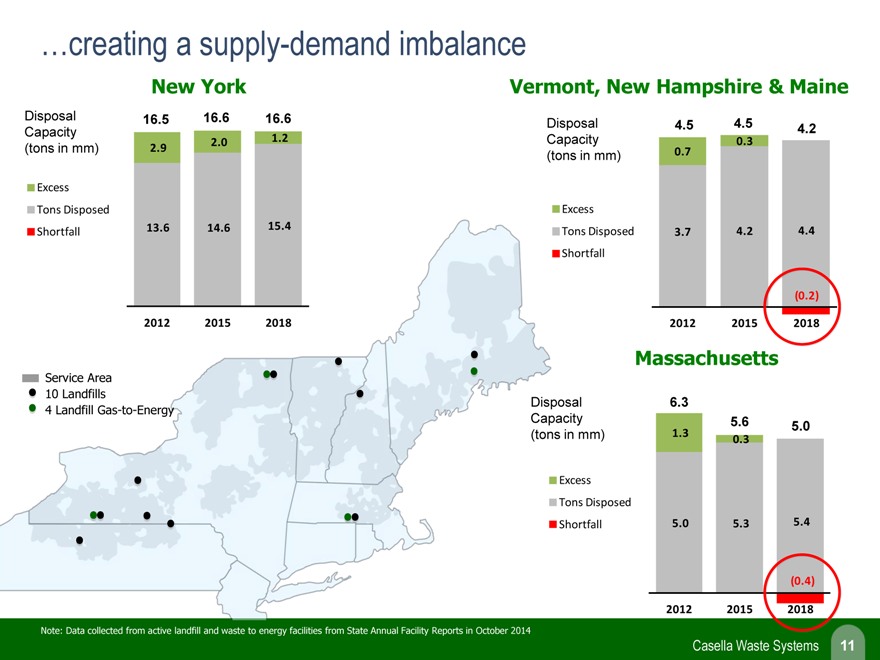

creating a supply-demand imbalance

New York

Disposal Capacity (tons in mm)

Excess

Tons Disposed

Shortfall

16.5 16.6 16.6

2.0 1.2

2.9 13.6 14.6 15.4

2012 2015 2018

Service Area

10 Landfills

Vermont, New Hampshire & Maine

Disposal Capacity (tons in mm)

Excess

Tons Disposed

Shortfall

4.5 4.5 4.2

0.3

0.7

3.7 4.2 4.4

(0.2) 2012 2015 2018

Massachusetts

Disposal Capacity (tons in mm)

Excess

Tons Disposed

Shortfall

6.3

5.6 5.0

1.3

0.3

5.0 5.3 5.4

(0.4) 2012 2015 2018

Note: Data collected from active landfill and waste to energy facilities from State Annual Facility Reports in October 2014

Casella Waste Systems 11

2 Driving additional profitability in collection operations

Team working to further improve collection profitability.

Pricing – continued focus on pricing discipline.

Route profitability – eliminating route days to reduce cost and improve asset utilization.

Fleet optimization – upgrading fleet for route applications and solving lingering fleet issues.

Collection pricing programs continue to drive value.

Residential and commercial pricing up +2.8% YOY in Q1 2015.

Launched an SRA fee in Q2 2015 to offset lower recycling commodity values.

The roll-off market has shown early signs of rebounding, with growth in select markets.

Reducing cost of operations is key to improving profitability.

Working to improve routing efficiency through customer selection, new routing tools, and on-route marketing to improve density.

Implementing fleet plan to standardize fleet selection, optimize truck selection, reduce maintenance costs, and reduce spare ratios.

Reducing volatility by locking in roughly 45% of fuel at fixed prices for 12 months.

Casella Waste Systems 12

3 Creating incremental value through Resource Solutions

Customer Solutions

Focus on creating resource solutions for Industrial, Municipal, Institutional, and multi-location Retail customers.

Experiencing strong growth in the Industrial segment (lower margins with high FCF).

CS revenues up +28% YOY for LTM ended 3/31/15.

Zero-Sort® Recycling

Casella operates 6 Zero-Sort MRFs in our integrated footprint.

Mature facilities operating at ~95% of capacity; new Lewiston, ME MRF online in Q2 2015.

Recycling volumes up +10% YOY for LTM ended 3/31/15.(1)

Reshaping business model to reduce commodity risk and improve returns (e.g., SRA fee).

Casella Organics

Business model is primarily focused on transforming Biosolids into renewable products for fertilization and landscaping.

Working with partners to transform Source Separated Organics into energy or compost.

(1) | | Shipped tons from MRFs on a “same store basis” . |

Casella Waste Systems 13

4 Improving balance sheet and reducing risk

Focused over last 2 1/2 years on reducing risk, improving the balance sheet, and increasing cash flows:

Dec 2012 – sold Maine Energy for $6.7mm; eliminated negative cash flow operation.

July 2013 – sold BioFuels for $2.0mm; eliminated negative cash flow operation.

Dec 2013 – sold 50% stake in US GreenFiber resulting in $3.4mm net cash proceeds; eliminated non-integrated, negative cash flow operation.(1)

Dec 2014 – completed environmental remediation and closure at three sites.

Feb 2015 – refinanced Senior Secured Revolver with new ABL Revolver; moved out maturities 5-yrs, minimized cash interest costs, and increased financial flexibility.

Mar 2015 – sold CARES assets and wholly-owned assets/real estate for $3.1mm net cash proceeds; eliminated non-integrated, negative cash flow operation.

Focused on improving Free Cash Flow, with excess cash primarily used to repay indebtedness and for tuck-in acquisitions.

Focus on improving operating cash flows, maintaining strict capital discipline, and selectively improving asset mix.

(1) | | US GreenFiber sold for $18.0mm gross proceeds, with $3.4mm net proceeds for Casella’s 50% equity interest. |

Casella Waste Systems 14

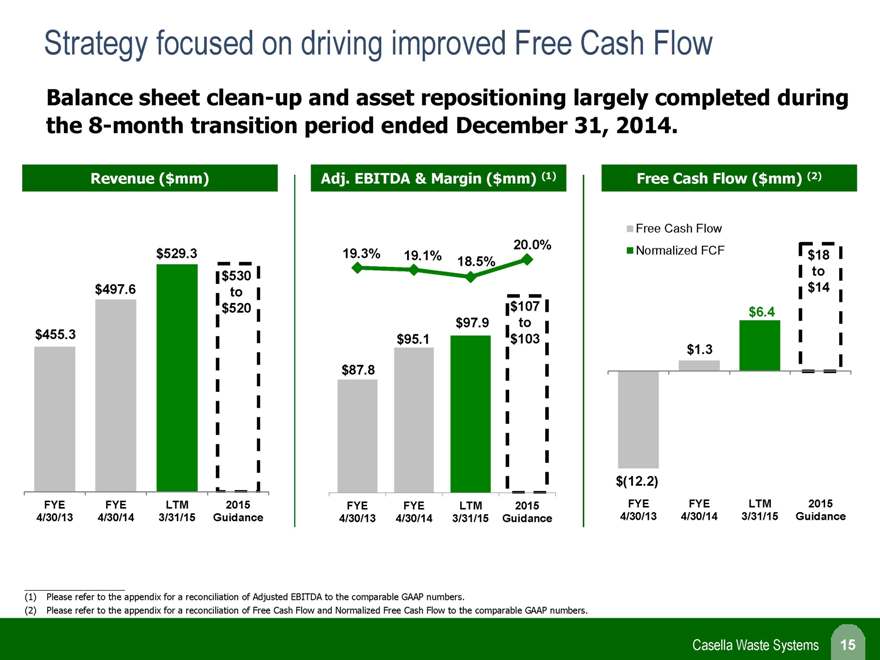

Strategy focused on driving improved Free Cash Flow

Balance sheet heet clean-up and asset sset repositioning epositioning largely completed ompleted during the 8-month transition period ended December 31, 2014.

Revenue ($mm) Adj. EBITDA & Margin ($mm) (1) Free Cash Flow ($mm) (2)

Free Cash Flow

20.0% Normalized FCF $529.3 19.3% 19.1% $18

18.5% $530 to $497.6 to $14 $520 $107 $6.4 $455.3 $97.9 to

$95.1 $103

$1.3

$87.8

$(12.2)

FYE FYE LTM 2015 FYE FYE LTM 2015 FYE FYE LTM 2015 4/30/13 4/30/14 3/31/15 Guidance 4/30/13 4/30/14 3/31/15 Guidance 4/30/13 4/30/14 3/31/15 Guidance

(1) Please refer to the appendix for a reconciliation of Adjusted EBITDA to the comparable GAAP numbers.

(2) Please refer to the appendix for a reconciliation of Free Cash Flow and Normalized Free Cash Flow to the comparable GAAP numbers.

Casella Waste Systems 15

Casella’s value drivers

Valuable integrated solid waste assets in disposal limited Northeast markets.

Management focused on increasing Free Cash Flow and reducing debt.

Results demonstrate strong execution of plan.

Near term focus of team:

Improving landfill returns;

Driving profitability of collection operations;

Creating value through Resource Solutions;

Improving balance sheet & reducing risk.

Casella Waste Systems 16

Additional Information

This presentation may be deemed to be soliciting material in respect of the solicitation of proxies from stockholders in connection with Casella Waste Systems, Inc.’s 2015 Annual Meeting of Stockholders. Casella, its directors and certain of its executive officers are deemed to be participants in the solicitation of proxies from the Company’s stockholders in connection with the matters to be considered at the Company’s 2015 Annual Meeting of Stockholders. Information regarding the names of the Company’s directors and executive officers and their respective interests in the Company by security holdings or otherwise can be found in the Company’s proxy statement for its 2014 Annual Meeting of Stockholders, filed with the SEC on August 19, 2014. To the extent holdings of the Company’s securities have changed since the amounts set forth in the Company’s proxy statement for the 2014 Annual Meeting of Stockholders, such changes have been reflected on Initial Statements of Beneficial Ownership on Form 3 or Statements of Change in Ownership on Form 4 filed with the SEC. These documents are available free of charge at the SEC’s website at www.sec.gov. Casella intends to file a proxy statement and accompanying WHITE proxy card with the SEC in connection with the solicitation of proxies from Casella stockholders in connection with the matters to be considered at the Company’s 2015 Annual Meeting. Additional information regarding the identity of participants, and their direct or indirect interests, by security holdings or otherwise, will be set forth in the Company’s proxy statement for its 2015 Annual Meeting, including the schedules and appendices thereto. INVESTORS AND STOCKHOLDERS ARE STRONGLY ENCOURAGED TO READ ANY SUCH PROXY STATEMENT AND THE

ACCOMPANYING PROXY CARD AND OTHER DOCUMENTS FILED BY CASELLA WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE AS THEY WILL CONTAIN IMPORTANT INFORMATION. Stockholders will be able to obtain the Proxy Statement, any amendments or supplements to the Proxy Statement, the accompanying WHITE proxy card, and other documents filed by Casella with the SEC for no charge at the SEC’s website at www.sec.gov. Copies will also be available at no charge at the Investor Relations section of the Company’s corporate website at www.casella.com, by writing to the Company’s Corporate Secretary at Casella Waste Systems, Inc., 25 Greens Hill Lane, Rutland, VT 05701, or by calling the Company’s Corporate Secretary at (802) 772-2257.

Casella Waste Systems 17

Appendix

Casella Waste Systems 18

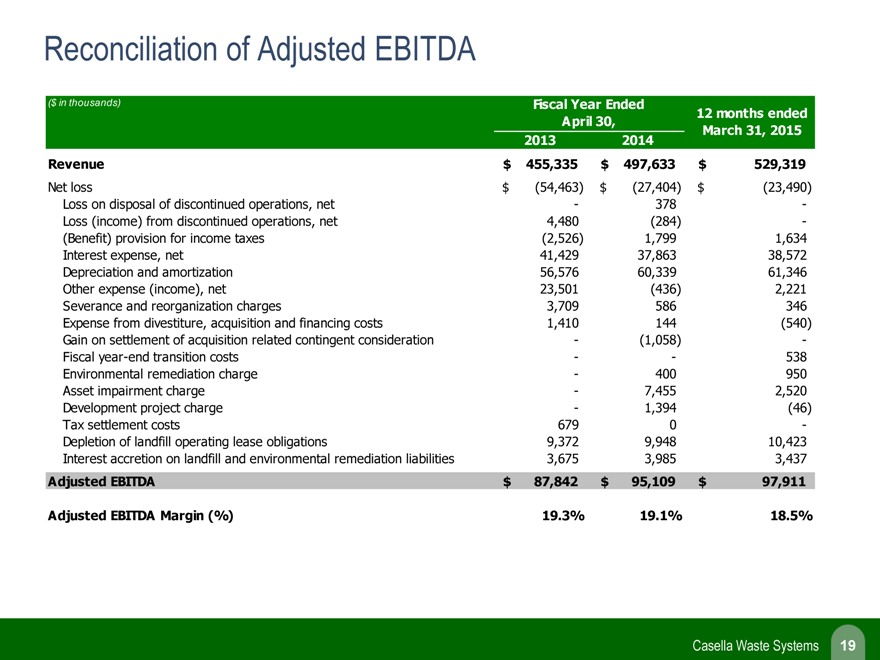

Reconciliation of Adjusted EBITDA

($ in thousands)

Revenue

Net loss

Loss on disposal of discontinued operations, net

Loss (income) from discontinued operations, net

(Benefit) provision for income taxes

Interest expense, net

Depreciation and amortization

Other expense (income), net

Severance and reorganization charges

Expense from divestiture, acquisition and financing costs

Gain on settlement of acquisition related contingent consideration

Fiscal year-end transition costs

Environmental remediation charge

Asset impairment charge

Development project charge

Tax settlement costs

Depletion of landfill operating lease obligations

Interest accretion on landfill and environmental remediation liabilities

Adjusted EBITDA

Adjusted EBITDA Margin (%)

Fiscal Year Ended

April 30, 12 months ended

March 31, 2015

2013 2014

$ 455,335 $ 497,633 $ 529,319

$ (54,463) $ (27,404) $ (23,490)

- 378 -

4,480 (284) -

(2,526) 1,799 1,634

41,429 37,863 38,572

56,576 60,339 61,346

23,501 (436) 2,221

3,709 586 346

1,410 144 (540)

- (1,058) -

- — 538

- 400 950

- 7,455 2,520

- 1,394 (46)

679 0 -

9,372 9,948 10,423

3,675 3,985 3,437

$ 87,842 $ 95,109 $ 97,911

19.3% 19.1% 18.5%

Casella Waste Systems 19

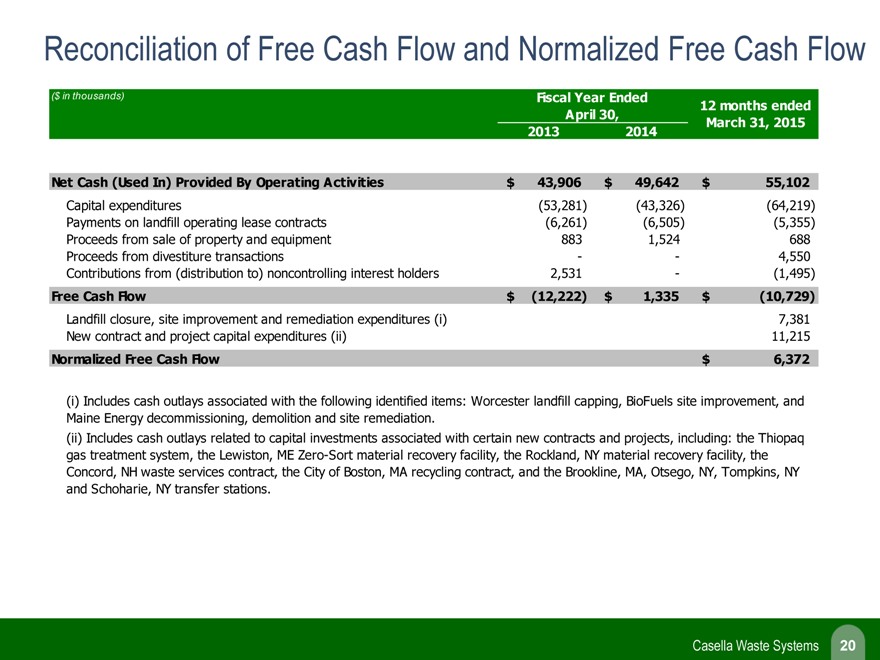

Reconciliation of Free Cash Flow and Normalized Free Cash Flow

($ in thousands)

Net Cash (Used In) Provided By Operating Activities

Capital expenditures

Payments on landfill operating lease contracts

Proceeds from sale of property and equipment

Proceeds from divestiture transactions

Contributions from (distribution to) noncontrolling interest holders

Free Cash Flow

Landfill closure, site improvement and remediation expenditures (i)

New contract and project capital expenditures (ii)

Normalized Free Cash Flow

Fiscal Year Ended 12 months ended

April 30, March 31, 2015

2013 2014

$ 43,906 $ 49,642 $ 55,102

(53,281) (43,326) (64,219)

(6,261) (6,505) (5,355)

883 1,524 688

- — 4,550

2,531 — (1,495)

$ (12,222) $ 1,335 $ (10,729)

7,381

11,215

$ 6,372

(i) Includes cash outlays associated with the following identified items: Worcester landfill capping, BioFuels site improvement, and Maine Energy decommissioning, demolition and site remediation.

(ii) Includes cash outlays related to capital investments associated with certain new contracts and projects, including: the Thiopaq gas treatment system, the Lewiston, ME Zero-Sort material recovery facility, the Rockland, NY material recovery facility, the Concord, NH waste services contract, the City of Boston, MA recycling contract, and the Brookline, MA, Otsego, NY, Tompkins, NY and Schoharie, NY transfer stations.

Casella Waste Systems 20