| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | October 31, 2006 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .19.3 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-7978 |

|

ING Mayflower Trust |

(Exact name of registrant as specified in charter) |

|

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

|

CT Corporation System, 101 Federal Street, Boston, MA 02110 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-992-0180 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | November 1, 2005 to April 30, 2006 | |

| | | | | | | | | |

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

| | Funds |

Semi-Annual Report

April 30, 2006

Classes A, B, C, I, M and Q

Global Equity Funds

ING Global Equity Dividend Fund

ING Global Equity Dividend Fund

ING Global Real Estate Fund

ING Global Value Choice Fund

International Equity Funds

ING Emerging Countries Fund

ING Foreign Fund

ING Greater China Fund

ING Index Plus International Equity Fund

ING International Fund

ING International Capital Appreciation Fund

ING International Real Estate Fund

ING International SmallCap Fund

ING International Value Fund

ING International Value Choice Fund

ING Precious Metals Fund

ING Russia Fund

International Fixed-Income Fund

ING Emerging Markets Fixed Income Fund

International Fund-of-Funds

ING Diversified International Fund

E-Delivery Sign-up – details inside

E-Delivery Sign-up – details inside

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. | |

|

| Go Paperless with E-Delivery! |

|

| Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs. |

|

| Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll. |

|

| You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail. |

| | | |

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Dear Shareholder, |

|

As you may recall in my last letter, I described the enthusiasm that we were experiencing here at ING Funds as we worked to bring more of the world’s investment opportunities to you, the investor. |

|

I am happy to report that that enthusiasm is continuing to thrive. With the New Year, we have launched a series of new international mutual funds, each created to bring more of the world’s opportunities to you. |

|

Meanwhile, we have also heard you loud and clear. Our research tells us that many investors report that they find investing an intimidating and overly-complex endeavor. That is why ING is committed to |

helping investors across the country cut through the confusion and clutter. “Your future. Made easier.SM” are more than words, they represent our promise to you. |

|

Those two objectives — bringing you more of the world’s opportunities and doing it in a way that is easier for you — are behind the development of the ING Diversified International Fund. The new Fund is among those that we launched in January but it is unique in that it is a fund-of-funds. It is also, we believe, simply an easier way to invest internationally. |

|

The ING Diversified International Fund brings together six distinct, international mutual funds, each managed by well-known asset managers who specialize in key international sub-asset classes. What’s more, the Fund is periodically reviewed by a seasoned team of ING asset allocation experts who re-adjust the Fund’s allocation based on prevailing market conditions. |

|

Best of all: we’ve made it easy. With just one investment, investors can now acquire a broadly diversified, actively managed international equity portfolio. |

|

The ING Diversified International Fund marks one more way that we at ING Funds are continuing to offer you the global expertise, product innovation and world-class service that you have come to expect from us. |

|

On behalf of everyone at ING Funds, I thank you for your continued support and loyalty. We look forward to serving you in the future. |

Sincerely,

James M. Hennessy

President

ING Funds

June 23, 2006

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

International investing does pose special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

For more complete information, or to obtain a prospectus on any ING fund, please call your Investment Professional or ING Fund Distributor, LLC at (800) 992-0180 or log on to www.ingfunds.com. The prospectus should be read carefully before investing. Consider the fund’s investment objectives, risks, charges and expenses. The prospectus contains this information and other information about the fund. Check with your Investment Professional to determine which funds are available for sale within their firm. Not all funds are available for sale at all firms.

1

MARKET PERSPECTIVE: SIX MONTH ENDED APRIL 30, 2006

Global equities ended up with strong gains for the half-year period ended April 30, 2006 with the foreign markets leading the way. The Morgan Stanley Capital International (“MSCI”) World Index(1) calculated in dollars, including net reinvested dividends rose 16.3%. Indeed, the first quarter of 2006 was the best first quarter since 1998 and the busiest quarter for merger and acquisition activity since 2000. As for currencies, the U.S. dollar at first extended its run of the first ten months of 2005. Few had expected such dollar strength in 2005. Relatively high U.S. interest rates explained part of it, especially the re-cycling of oil exporters’ burgeoning wealth into dollar denominated securities. The yen’s particular weakness was connected with the sharp rise in Japanese stock prices, fueled by outside investors who were hedging their currency risk. Also material was the tax-related “repatriation” into dollars of U.S. corporations’ foreign currency balances. However, by year-end 2005 each of these dynamics was losing steam. A January 2006 correction was partially reversed before resuming in earnest and the dollar ended the April 30, 2006 six-month period weaker than it started, by 5.1% against the euro, 2.2% against the yen and 3.1% against the pound.

Equities investors kept a wary eye on the U.S. fixed-income markets where for over a year, the main issue had been the unexpected flattening of the yield curve. Between June 2004 and October 31, 2005 the Federal Open Market Committee (“FOMC”) had raised the federal funds rate by 25 basis points eleven times, pulling other short-term rates up. However, the yield on the ten-year U.S. Treasury Note had actually fallen by 14 basis points over the same period. By the time Federal Reserve Chairman Alan Greenspan had chaired his final FOMC meeting on the last day of January 2006, rates had been raised three more times. Incoming Chairman Ben Bernanke quickly confirmed that he would maintain the focus of his predecessor. February 2006 ended with the yield curve slightly inverted along much of its range. This largely disappeared in March 2006 as fourth quarter core inflation was reported at an uncomfortable 2.4% and Mr Bernanke’s FOMC raised rates for the fifteenth time. The curve steepened further in April as commodity prices soared on expectations of rising global demand and China’s insatiable appetite. The price of a barrel of oil reached a new record, elevated in addition by political concerns in Iran, Venezuela and Nigeria. For the six-month period the yield on the ten-year U.S. Treasury Note rose 51 basis points to 5.07%, a near four-year high, while the yield on the three-month U.S. Treasury Bill added 84 basis points to 4.65%.

The U.S. equities market in the form of the Standard and Poor’s 500® Composite Stock Price (“S&P 500®”) Index(2), gained 9.6% including dividends during the half year ended April 30, 2006. Boosting sentiment was the continued growth of corporate profits, which looked set in the first quarter of 2006, to record the 11th straight double-digit increase. In the same quarter economic growth roared back to 4.8% after a hurricane affected 1.7% previously. For most of the period investors warmed to the feeling that an end to rising short-term interest rates was drawing near, although the chill could be instantly restored by a single piece of economic data or loose comment by a Federal Reserve official. And latterly, as commodity prices surged ever higher, the market, while still rising, was nonetheless getting increasingly nervous.

Japan equities had been soaring since the middle of 2005 and they kept up the pace in the six-month period April 30, 2006 leaping 24.4% in dollars according to the MSCI Japan® Index(3) plus net dividends. Investors cheered Japan’s re-emergence as a balanced economy, less dependent on exports. Japanese corporations and banks have repaired their balance sheets. At last, core consumer prices started rising in November 2005. Higher wages are supporting domestic demand, leading the rate of fourth quarter gross domestic product (“GDP”) growth to a healthy 4.4%. The long-feared announcement, that the Bank of Japan would end its zero-interest rate policy, thereby reducing liquidity, came on March 9, 2006. However, the Bank of Japan also signaled that it was in no rush, and a relieved market completed the last 9% of its remarkable rise.

European ex UK markets matched Japan’s with a 24.9% return, according to the MSCI Europe ex UK Index(4) including net dividends, despite the first interest rate increase in over five years, followed by another, to 2.5%. Evidence of recovery continued to mount, if not entirely convincingly. Fourth quarter Eurozone GDP growth was only 0.3%, with Germany flat. Unemployment barely edged down to 8.2%. Yet business confidence continued to improve; in Germany’s case to a 15-year high. The key is that tepid macro-economic reports believe the strong profitability of European companies, which are increasingly producing and selling outside developed Europe. This and merger and acquisition activity, in businesses from tobacco to banking to insurance to power to frozen food to drugs, kept stocks buoyant.

2

MARKET PERSPECTIVE: SIX MONTH ENDED APRIL 30, 2006

UK equities jumped 18.5% in the half year, based on the MSCI UK® Index(5) including net dividends. The economic reports were mostly miserable, with manufacturing in decline, GDP growth in 2005 finalized at 1.8%, the weakest since 1992 and unemployment claims up in 13 out of the last 14 months. Yet the market advanced. The comparatively large energy and materials sectors benefited as commodities prices exploded, while the sizeable financials sector contained a number of companies close to the rampant merger and acquisition action (or thought to be). Further support came from rebounding house prices, first quarter GDP growth at 0.6%, within which industrial production outpaced services for the first time since 1999, and in the last few days an unexpectedly strong retail sales report.

(1) The MSCI World® Index is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

(2) The Standard & Poor’s 500® Composite Stock Price (“S&P 500®”) Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the United States.

(3) The MSCI Japan® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(4) The MSCI Europe ex UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(5) The MSCI UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

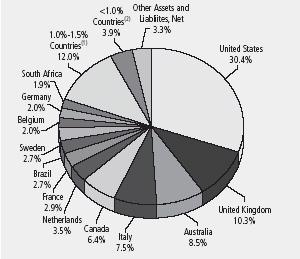

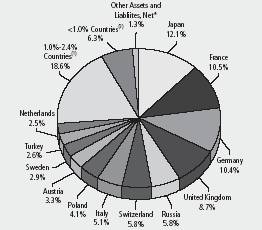

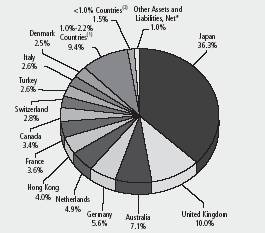

ING GLOBAL EQUITY DIVIDEND FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

(1) Includes eleven countries, which each represents 1.0%-1.5% of net assets.

(2) Includes six countries, which each represents < 1.0% of net assets.

Portfolio holdings are subject to change daily.

ING Global Equity Dividend Fund (the “Fund”) seeks growth of capital with dividend income as a secondary consideration. The Fund is managed by Portfolio Managers, Nicolas Simar and Moudy El Khodr of ING Investment Management Advisors B.V — the Sub-Adviser.

Performance: For the six months ended April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 18.30% compared to the Morgan Stanley Capital International (“MSCI”) World IndexSM, which returned 16.29% for the same period.

Portfolio Specifics: During the reporting period, the Fund had strong performance. Buoyed by the positive economic data and supported by good earnings results the markets performed strongly over the period. Cyclical sectors such as Basic Materials and Industrials performed strongly. Basic Materials were strong on the back of further rises in commodity prices. Industrials did well on a better outlook for the global economy. The Energy sector also had a solid positive performance as oil prices rose further. The defensive and high dividend paying sectors such as Telecoms and Utilities lagged as the market favored the growth oriented sectors. Financials, including Real Estate, were also strong. The sectors were boosted by good earnings results, rising markets and market demand.

The Fund benefited from its positioning in Financials (especially in Real Estate) and Energy. However, the strong positioning in the high dividend paying sectors of Telecoms and Utilities were a drag on the performance as these sectors lagged. As the Fund is underrepresented in the cyclical sectors, their strong performance was also a drag on the Fund.

The Fund profited from its regional positioning. We have a large position in Emerging Markets, which performed strongly especially Brazil. Emerging Markets offer many investment opportunities with very attractive dividend yields, sound fundamentals and above average growth prospects. Our strong position in Europe also performed well as the economic outlook and business sentiment for the region improved. The strong performance of Japan was a drag on the performance as the Fund has no representation in the region because companies do not meet the strategy’s criteria.

In general, stock selection clearly had a positive contribution. The Fund benefited from the strong performance of the UK home builders. Our key bet in Persimmon sold as of April 30, 2006, an England based home builder, plans to save as much as $87 million in costs from its proposed takeover of rival homebuilder Westbury Plc. We sold this stock in December once it reached our dividend threshold. The market was positive regarding the acquisition and the stock performed strongly. Investments in emerging markets — Petroleo Brasileiro and Petrochina, Brazilian and Chinese oil companies respectively — were also amongst our best performers as oil prices rose.

Current Strategy and Outlook: The outlook for the Global Equity Dividend strategy remains positive. Investments in defensive sectors like utilities, real estate, telecommunication services and consumer staples give the strategy downside protection. These sectors are relatively cheap, less dependent on the economic environment and offer stable, high dividend yields. This strategy should perform well on a relative basis in a down market. If the equity markets move sideways, the Fund’s performance will be dependent on stock selection and the application of our disciplined strategy which looks for good value opportunities in countries, sectors or individual stocks.

4

PORTFOLIO MANAGERS’ REPORT | | ING GLOBAL EQUITY DIVIDEND FUND |

| | | | | | | | | | | |

| Average Annual Total Returns for the Periods Ended April 30, 2006 | |

| | | | | | | | | | | |

| | | 1 Year | Since Inception

of Class A

September 17, 2003 | | Since Inception

of Class B

October 24, 2003 | | Since Inception

of Class C

October 29, 2003 | | |

| | | | | | | | | | | |

| Including Sales Charge: | | | | | | | | | | |

| Class A(1) | | 15.29 | % | 19.60 | % | — | | — | | |

| Class B(2) | | 16.43 | % | — | | 20.15 | % | — | | |

| Class C(3) | | 20.47 | % | — | | — | | 20.54 | % | |

| Excluding Sales Charge: | | | | | | | | | | |

| Class A | | 22.29 | % | 22.33 | % | — | | — | | |

| Class B | | 21.43 | % | — | | 21.05 | % | — | | |

| Class C | | 21.47 | % | — | | — | | 20.54 | % | |

| MSCI World IndexSM(4) | | 24.91 | % | 19.82 | %(5) | 17.79 | %(6) | 17.79 | %(6) | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING Global Equity Dividend Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| |

(2) | Reflects deduction of the Class B deferred sales charge of 5% and 3%, respectively, for the 1 year and since inception returns. |

| |

(3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| |

(4) | The MSCI World IndexSM is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. |

| |

(5) | Since inception performance for the index is shown from October 1, 2003. |

| |

(6) | Since inception performance for the index is shown from November 1, 2003. |

5

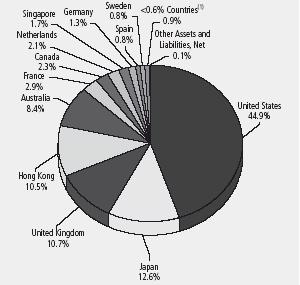

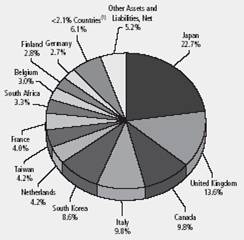

ING GLOBAL REAL ESTATE FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

(1) Includes three countries, which each represents < 0.6% of net assets.

Portfolio holdings are subject to change daily.

ING Global Real Estate Fund (the “Fund”) seeks high total return. T. Ritson Ferguson, CFA, and Steven D. Burton, CFA have been jointly responsible for the day-to-day management of the Fund, ING Clarion Real Estate Securities L.P.—the Sub-Adviser.

Performance: For the six months ended April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 22.90% compared to the S&P/Citigroup World Property Index, which returned 21.13% for the same period.

Portfolio Specifics: Overall performance for the six months ended April 30, 2006 was driven by the European and Asia-Pacific regions. European property stocks garnered the best performance by major region of the world with total return of 30.1% (in USD) over this time period. The Asia-Pacific region followed with total return of 25.3%, driven by Japan 35.6% and Hong Kong 25.6% both of which continue to exhibit signs of sustainable economic expansion. North America total return for the six months ended April 30 was 15.1%.

Thematically, some of the more significant events among world property stocks over the past six months have been: 1) final details regarding the Real Estate Investment Trust (“REIT”) structure in the U.K., 2) continued improving fundamentals in Japan and 3) continued syndicate activity with the formation of new property companies worldwide. In the U.K., the Treasury issued in March, 2006 critical details on the structure of REITs which surprised the market to the upside and should contribute to the healthy conversion and expansion of real estate securities in the U.K., beginning January 1, 2007. The details included a conversion tax of 2% of total assets (at the lower end of expectations), a payout requirement on net income of 90% (versus 95% previously stated) and a recurring net income to interest expense ratio of 1.5X (versus 2.5X previously stated).

In Japan, vacancy and rent trends continue to improve. Vacancies in the Tokyo central five wards declined for the ninth straight month to 3.41% in March from 3.67% in February. Average office rent rose to 18,095 yen per tsubo, the Japanese standard of land measurement that is equivalent to 35.6 square feet, or 3.3 square meters, from 18,038 yen. Separately, the annual land price survey conducted by the Ministry of Land, Infrastructure, and Transport indicated in March an increase in land prices in urban areas for the first time since 1991. The price surge was even more evident in the city centers, as the Tokyo central 5 wards average commercial land price increased 7%. Property stocks generally reacted favorably to the survey.

Syndicate activity was robust during the six months as the global property stock sector continues to expand. Hong Kong now has three REITs with an active pipeline (up from no REITs six months ago) and the Japanese REIT market is approaching USD$30 billion in aggregate size with several new IPO’s, including the first hotel REIT. Europe has seen several billions of equity market cap created among the property companies over the past six months via IPO’s with a bias toward the German markets, Eastern Europe and France.

The Fund achieved its outperformance versus the benchmark over the six months ended April 30 primarily via stock selection in Japan, the U.S. and Hong Kong. Overweights in Tokyo-focused companies Mitsubishi Estate and Sumitomo Realty contributed to the relative outperformance in Japan. In the U.S., companies with significant investments in Manhattan, including SL Green Realty and Boston Properties, contributed to relative outperformance. Hong Kong picks were bolstered by investments in the homebuilding sector in China as well as Hong Kong’s first REIT, The Link REIT, which has performed well since the IPO.

The U.S. dollar generally weakened during the six months against other major currencies, most notably versus the Euro 5.1%, followed by the British pound 3.1%, the Japanese Yen 2.2% and the Australian dollar 0.6%. A weakening U.S. dollar benefits an investor in the Fund as returns translated from the strengthening currency convert to more U.S. dollars once converted back.

Current Strategy and Outlook: The Fund, while maintaining a core of higher dividend yielding, defensively positioned stocks, is positioned to take advantage of the higher growth countries and sectors which will likely respond better to sustained economic recovery. The Fund has reduced its overall weight in continental Europe over the past six months and added to the recovering economies of the Asia-Pacific region, particularly Japan and Hong Kong both of which are exhibiting improving property fundamentals. By property type, the Fund is shifting its weighting towards sectors which have further to respond to improving economies, such as the office, apartment and lodging sectors. Through an average 3-4% dividend yield plus 5-8% prospective annual earnings growth, global property stocks continue to be well-positioned to conservatively deliver attractive total returns over the next several years.

6

PORTFOLIO MANAGERS’ REPORT | | ING GLOBAL REAL ESTATE FUND |

| | | | | | | | | | | | | |

| Average Annual Total Returns for the Periods Ended April 30, 2006 | |

| | | | | | | | | | | | | |

| | | 1 Year | Since Inception

of Class A

November 5, 2001 | | Since Inception

of Class B

March 15, 2002 | | Since Inception

of Class C

January 8, 2002 | | Since Inception

of Class I

June 3, 2005 | | |

| | | | | | | | | | | | |

| Including Sales Charge: | | | | | | | | | | | | |

| Class A(1) | | 25.43 | % | 23.98 | % | — | | — | | — | | |

| Class B(2) | | 27.06 | % | — | | 23.49 | % | — | | — | | |

| Class C(3) | | 30.94 | % | — | | — | | 23.56 | % | — | | |

| Class I | | — | | | | | | | | 30.61 | % | |

| Excluding Sales Charge: | | | | | | | | | | | | |

| Class A | | 33.04 | % | 25.58 | % | — | | — | | — | | |

| Class B | | 32.06 | % | — | | 23.47 | % | — | | — | | |

| Class C | | 31.94 | % | — | | — | | 23.56 | % | — | | |

| Class I | | — | | | | | | | | 30.61 | % | |

| S&P/Citigroup World Property Index(4) | | 31.99 | % | 24.85 | %(5) | 25.36 | %(6) | 24.33 | %(7) | 33.10 | %(8) | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING Global Real Estate Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| |

(2) | Reflects deduction of the Class B deferred sales charge of 5% and 3%, respectively, for the 1 year and since inception returns. |

| |

(3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| |

(4) | The S&P/Citigroup World Property Index is an unmanaged market-weighted total return index which consists of many companies from developed markets whose floats are larger than $100 million and derive more than half of their revenue from property-related activities. |

| |

(5) | Since inception performance for index is shown from November 1, 2001. |

| |

(6) | Since inception performance for index is shown from March 1, 2002. |

| |

(7) | Since inception performance for index is shown from January 1, 2002. |

| |

(8) | Since inception performance for index is shown from June 1, 2005. |

7

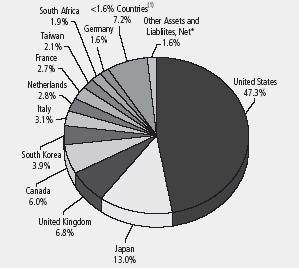

ING GLOBAL VALUE CHOICE FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

(1) | Includes six countries, which each represents < 1.6% of net assets. |

* | Includes securities lending collateral. |

Portfolio holdings are subject to change daily.

ING Global Value Choice Fund (the “Fund”) focuses on long-term capital appreciation by investing primarily in equity securities throughout the world, including the United States. The Fund is managed by Paul S. Hechmer, Managing Director and Institutional Portfolio Manager, and David B. Iben, Managing Director and Chief Investment Officer, Tradewinds NWQ Global Investors, LLC. — the Sub-Adviser*

Performance: For the six months ended April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 18.09% compared to the Morgan Stanley Capital International (“MSCI”) World IndexSM which returned 16.29% for the same period.

Portfolio Specifics: The Fund outperformed the benchmark during the period as a result of strong stock selection across most countries and sectors. Markets around the world performed strongly, with non-US markets in aggregate outperforming the US, with a weaker US dollar adding to overall returns in the global Fund. During the period most commodities performed strongly, with many individual commodities reaching multi year highs. The companies we held in this sector, including Lonmin, Lihir Gold and Impala Platinum, outperformed the benchmark and our overweight exposure to the sector also aided returns. Strong returns in our holdings in the Healthcare sector, including Daiichi Sankyo in Japan also contributed to our strong performance. Individual securities in the Consumer Discretionary sector, including Premiere Ag the German pay TV company detracted from returns, as the company lost the right to broadcast key programming in Germany. We continue to hold the name, believing that the share price has fallen well below the intrinsic value of this market leading company. We were also hurt by our underweight exposure to the Financials sector, and exposure to poorly performing names such as Takefuji in Japan and Citigroup in the US.

Japan was one of the best performing major markets, as investor optimism grew regarding the end of deflation and Japan emerging from a fifteen year economic slump. Our holdings in Japan, while performing strongly from an absolute perspective underperformed relative to the benchmark, as investors focused on higher beta more highly leveraged companies. In the US our overall returns were stronger than that of the market, as names such as Kerr McGee and International Paper rallied strongly significantly outperforming the benchmark return.

Current Strategy and Outlook: Overall on a global basis we believe that market performance would appear to have outpaced the fundamental underlying improvement in business conditions. Further, interest rates appear to be on a northward trend in most major markets around the world. Either or both of these forces could present headwinds to further strong performance in the equity markets. Never the less, our investment universe is extremely broad, and comprised of economies in varied stages of the economic cycle. Japan continues to rebound from 15 years of recession, Europe continues to react positively to the increased competitive environment that the European Union brought with it, and the emerging markets continue to grow very rapidly and the US has significantly lagged other markets throughout the world. In such an environment we continue to be optimistic that good opportunities can still be found.

* The Fund was previously sub-advised by NWQ Investment Management Company.

8

PORTFOLIO MANAGERS’ REPORT | | ING GLOBAL VALUE CHOICE FUND |

| | | | | | | | | |

| Average Annual Total Returns for the Periods Ended April 30, 2006 | |

| | | | | | | | | |

| | | 1 Year | | 5 Year | | 10 Year | | |

| | | | | | | | | |

| Including Sales Charge: | | | | | | | | |

| Class A(1) | | 21.03 | % | 0.26 | % | 7.70 | % | |

| Class B(2) | | 22.67 | % | 0.40 | % | 7.65 | % | |

| Class C(3) | | 26.65 | % | 0.79 | % | 7.65 | % | |

| Class Q | | 28.90 | % | 1.79 | % | 8.65 | % | |

| Excluding Sales Charge: | | | | | | | | |

| Class A | | 28.42 | % | 1.46 | % | 8.34 | % | |

| Class B | | 27.67 | % | 0.79 | % | 7.65 | % | |

| Class C | | 27.65 | % | 0.79 | % | 7.65 | % | |

| Class Q | | 28.90 | % | 1.79 | % | 8.65 | % | |

| MSCI World IndexSM(4) | | 24.91 | % | 5.99 | % | 7.81 | % | |

| | | | | | | | | |

| | | | | | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING Global Value Choice Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| |

(2) | Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and 5 year returns. |

| |

(3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| |

(4) | The MSCI World IndexSM is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. |

Prior to April 24, 2006, the Fund was advised by a different sub-adviser.

9

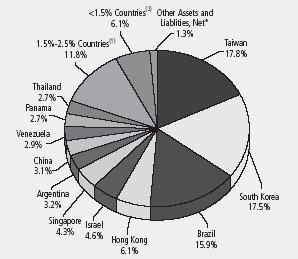

ING EMERGING COUNTRIES FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

(1) | Includes six countries, which each represents 1.5%-2.5% of net assets. |

(2) | Includes six countries, which each represents < 1.5% of net assets. |

* | Includes securities lending collateral. |

Portfolio holdings are subject to change daily.

ING Emerging Countries Fund (the “Fund”) seeks long-term capital appreciation by normally investing at least 80% of its assets in a number of different countries with emerging securities markets. The Fund is managed by Brandes Investment Partners, L.P. — the Sub-Adviser.

Performance: For the six-month period ended April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 27.00% compared to the Morgan Stanley Capital International Emerging Markets IndexSM, (“MSCI EM IndexSM”) which returned 37.77% for the same period.

Portfolio Specifics: On an industry basis, gains for positions in wireless telecom services, commercial banking, and diversified telecom services had the most substantial impact on performance. Among the holdings from these industries posting gains were TIM Participacoes (Brazil — wireless telecom services), Turkiye Vakiflar Bank (Turkey — commercial banking), and CANTV (Venezuela — diversified telecom services).

The Fund’s holdings in Brazil, South Korea, and Taiwan, such as CIA Saneamento Basico (Brazil — water utilities), Korea Electric Power (South Korea — electric utilities), and Yageo (Taiwan — electronic equipment & instruments), also tended to advance in the six-month period.

Relative to the index, some of the recent portfolio underperformance can be attributed at the industry level to underexposure to stocks in the oil, gas & consumable fuels and metals and mining industries, and overexposure to diversified telecom stocks. Within industries, our holdings in commercial banks, capital markets and semiconductors & semiconductor equipment underperformed their industries, as represented in the MSCI Emerging Market Index.

During the period, we sold select positions as their market prices advanced toward our estimates of their intrinsic values, including Sinopec Yizheng Chemical (China — chemicals), Lukoil (Russia — oil, gas, & consumable fuels), and CIA Parananese de Energia (Brazil — independent power producers & energy traders). We purchased shares of companies at prices that we considered attractive, including Taishin Financial Holdings (Taiwan — commercial banking), Wan Hai Lines (Taiwan — marine), and Far EasTone Telecom (Taiwan — wireless telecom services).

Current Strategy and Outlook: Note that our industry exposure is a result of our focus on the fundamentals and valuations of individual companies. We invest in firms that we believe offer a “margin of safety” — companies selling at a price below our estimate of fair value. This often involves investing in unpopular firms and industries. Industry exposures are substantially driven by stock selection, and not by any “industry allocation” decision. Many companies in the oil gas & consumable fuels and metals & mining industries are selling at what we believe to be overly optimistic prices. For the six-month period ending April 30, 2006, both the oil gas & consumable fuels and metals & mining industry components of the Index climbed by more than 50%, or more than 100% on an annualized basis. We do not believe current valuations support the prices for many firms in these industries; in other words, we find firms in these industries expensive. We believe quality businesses with attractive margins of safety represent compelling opportunities for long-term gains.

While we monitor short-term events in emerging markets, our investment philosophy focuses on company-by-company analysis. We take a long-term perspective and believe that none or very little of the short-term “market news” provides useful information to investors.

10

PORTFOLIO MANAGERS’ REPORT | | ING EMERGING COUNTRIES FUND |

| | |

| Average Annual Total Returns for the Periods Ended April 30, 2006 | |

| | | |

| | | | | | | | | Since Inception | | Since Inception | |

| | | | | | | | | of Class I | | of Class M | |

| | | 1 Year | | 5 Year | | 10 Year | | December 21, 2005 | | August 5, 2002 | |

| | | | | | | | | | | | |

| Including Sales Charge: | | | | | | | | | | | |

| Class A(1) | | 30.83 | % | | 14.82 | % | | 7.62 | % | | — | | | — | | |

| Class B(2) | | 32.83 | % | | 15.28 | % | | 7.67 | % | | — | | | — | | |

| Class C(3) | | 36.82 | % | | 15.22 | % | | 7.53 | % | | — | | | — | | |

| Class I | | — | | | — | | | — | | | 17.05 | % | | — | | |

| Class M(4) | | 33.32 | % | | — | | | — | | | — | | | 24.88 | % | |

| Class Q | | 39.03 | % | | 16.34 | % | | 8.56 | % | | — | | | — | | |

| Excluding Sales Charge: | | | | | | | | | | | | | | | | |

| Class A | | 38.83 | % | | 16.19 | % | | 8.26 | % | | — | | | — | | |

| Class B | | 37.83 | % | | 15.51 | % | | 7.67 | % | | — | | | — | | |

| Class C | | 37.82 | % | | 15.22 | % | | 7.53 | % | | — | | | — | | |

| Class I | | — | | | — | | | — | | | 17.05 | % | | — | | |

| Class M | | 38.14 | % | | — | | | — | | | — | | | 26.07 | % | |

| Class Q | | 39.03 | % | | 16.34 | % | | 8.56 | % | | — | | | — | | |

| MSCI EM IndexSM(5) | | 62.89 | % | | 24.09 | % | | 7.88 | % | | 20.12 | %(6) | | 36.03 | %(7) | |

| | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING Emerging Countries Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| | |

(2) | | Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and 5 year returns. |

| | |

(3) | | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| | |

(4) | | Reflects deduction of the maximum Class M sales charge of 3.50%. |

| | |

(5) | | The MSCI EM IndexSM is an unmanaged index that measures the performance of securities listed on exchanges in developing nations throughout the world. |

| | |

(6) | | Since inception performance for index is shown from January 1, 2006. |

| | |

(7) | | Since inception performance for index is shown from August 1, 2002. |

Prior to March 1, 2005, the Fund was advised by a different sub-adviser.

11

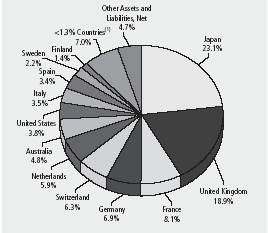

ING FOREIGN FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

* Includes securities lending collateral.

(1) Includes eleven countries, which each represents 1.0%-2.4% of net assets.

(2) Includes twenty-two countries, which each represents < 1.0% of net assets.

Portfolio holdings are subject to change daily.

ING Foreign Fund (the “Fund”) seeks long-term growth of capital by investing primarily in equity securities tied economically to countries outside the United States. The Fund is managed by Rudolph-Riad Younes, CFA, Senior Vice President and Head of International Equity and Richard Pell, Senior Vice President and Chief Investment Officer, both with Julius Baer Investment Management LLC, — the Sub-Adviser.

Performance: For the six months ended April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 26.87% compared to the Morgan Stanley Capital International — Europe, Australasia and Far East® Index (“MSCI EAFE® Index”), which returned 23.10% for the same period.

Portfolio Specifics: Emerging European markets positively impacted results. Specifically, Russia, Turkey, Poland and Romania were all solid performers, although the Czech Republic and Hungary were exceptions. Our decision to underweight the United Kingdom also supported results. Stock selection within Germany, Italy, France and Norway was also a positive contributor. However, the small liquidity position held by the Fund proved to be a detractor to performance amid such a strong backdrop for equities.

From a sector perspective, banks in Eastern and Central Europe as well as Italian banks supported results. Stock selection within the energy sector also had a positive impact given positions in Russia and Norway in particular. Stock selection within utilities, telecommunication services and industrials also had a positive impact on performance. However, our underweight to information technology detracted from results as this sector was strong for the period.

In terms of stock selection, several positions within Russia contributed to results. Specifically, Sberbank, the country’s largest lender, provided strong results over the period. Also, within the energy sector, shares of Gazprom ADR and Lukoil ADR (Russia) were strong performers. In addition, positions held in P.K.O. Bank Polski (Poland) and Akbank T.A.S. (Turkey) were also supportive of results, and reflect our optimism toward the region. Within Germany, Fraport, the German airport operator whose properties include the European hub in Frankfurt, positively contributed to results.

Within the emerging markets, shares of Komercni Banka A.S., the third-largest Czech bank, RAO Unified Energy System (Russia), OTP Bank (Hungary), Eastern Europe’s largest lender by market value, and Magyar Telekom Communications, Hungary’s largest phone company, underperformed the Index over the period.

Shares of Aiful Corp. Japan’s largest consumer lender, detracted from results. Aiful reported a drop in third quarter net income, negatively impacting performance. Additionally, within the spirits industry, our overweight to Pernod Ricard (France) and Diageo (UK) detracted from results.

Current Strategy and Outlook: Our bottom-up approach to security selection within developed markets has continued to support investments in several areas. Infrastructure-related companies such as airport and seaport operators are likely beneficiaries given the increase in global travel and trade. We believe construction companies are also attractive. With funding-related challenges, public authorities are engaging private companies for the construction of toll roads. Another area of interest is the cement industry, which has been slowly consolidating leading to more pricing discipline and additional capacity.

We anticipate the luxury goods industry will enjoy strong growth driven by the expected increase in purchasing power of consumers from emerging economies. The global spirits industry is also likely to benefit as consumers in emerging economies grow in wealth and increase consumption of top brands as a show of status. Italian banks are another area of interest where we anticipate a wave of consolidations over the next few years.

From a regional perspective, we are comfortable with our underweight to Japan. While the economy has certainly improved, we find the market already reflects these positive developments, and find valuations to be demanding versus Europe. Finally, within emerging markets, we remain constructive toward Eastern and Central Europe as beneficiaries of the drive to reunite Europe.

12

PORTFOLIO MANAGERS’ REPORT | | ING FOREIGN FUND |

| | |

| Average Annual Total Returns for the Periods Ended April 30, 2006 | |

| | | | | | | | | | | | | |

| | | | Since Inception | | Since Inception | | Since Inception | | Since Inception | | Since Inception | |

| | | | of Class A | | of Class B | | of Class C | | of Class I | | of Class Q | |

| | 1 Year | | July 1, 2003 | | July 8, 2003 | | July 7, 2003 | | September 8, 2003 | | July 10, 2003 | |

| | | | | | | | | | | | | |

| Including Sales Charge: | | | | | | | | | | | | | |

| Class A(1) | | 32.80 | % | | 22.99 | % | | — | | | — | | | — | | | — | | |

| Class B(2) | | 34.87 | % | | — | | | 22.88 | % | | — | | | — | | | — | | |

| Class C(3) | | 38.81 | % | | — | | | — | | | 23.72 | % | | — | | | — | | |

| Class I | | 41.21 | % | | — | | | — | | | — | | | 25.25 | % | | — | | |

| Class Q | | 40.93 | % | | — | | | — | | | — | | | — | | | 25.27 | % | |

| Excluding Sales Charge: | | | | | | | | | | | | | | | | | | | |

| Class A | | 40.87 | % | | 25.58 | % | | — | | | — | | | — | | | — | | |

| Class B | | 39.87 | % | | — | | | 23.61 | % | | — | | | — | | | — | | |

| Class C | | 39.81 | % | | — | | | — | | | 23.72 | % | | — | | | — | | |

| Class I | | 41.21 | % | | — | | | — | | | — | | | 25.25 | % | | — | | |

| Class Q | | 40.93 | % | | — | | | — | | | — | | | — | | | 25.27 | % | |

| MSCI EAFE® Index(4) | | 34.00 | % | | 27.74 | %(5) | | 27.39 | %(5) | | 27.74 | %(5) | | 27.39 | %(6) | | 27.74 | %(5) | |

| | | | | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING Foreign Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| | |

(2) | | Reflects deduction of the Class B deferred sales charge of 5% and 3%, respectively, for the 1 year and since inception returns. |

| | |

(3) | | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| | |

(4) | | The MSCI EAFE® Index is an unmanaged index that measures the performance of securities listed on exchanges in Europe, Australasia and the Far East. |

| | |

(5) | | Since inception performance for index is shown from July 1, 2003. |

| | |

(6) | | Since inception performance for index is shown from September 1, 2003. |

13

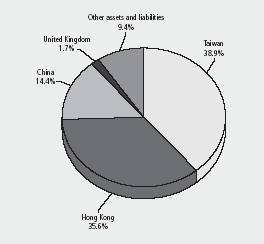

ING GREATER CHINA FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

Portfolio holdings are subject to change daily.

ING Greater China Fund (the “Fund”) seeks long-term capital appreciation. The Fund is managed by Nick Toovey, CFA, Bratain Sanyal, Oscar Leung Kin Fai, CFA, and Michael Hon Lung Chiu, CFA, ING Investment Management Asia/Pacific (Hong Kong) Limited — the Sub-Adviser.

Performance: From December 21, 2005, the inception of the Fund, to April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 21.30% compared to the MSCI All Countries Golden Dragon Net Dividend Reinvested Index, which returned 16.50% for the same period.

Portfolio Specifics: The Fund launched at the end of 2005 under fairly positive economic conditions. The macroeconomic figures announced by China during the 6 months period ended April 30, 2006 were broadly positive. Fourth quarter 2005 gross domestic product (“GDP”) growth of China surprised the market on the upside, rising 9.9% Year-on-Year (“YoY”), up from the 9.8% YoY growth in the previous quarter. For the full year 2005, China reported 9.9% growth in GDP, placing the country as the fourth largest economy in the world. First quarter 2006 GDP growth was 10.2% YoY in China. Fixed asset investment as well as money supply growth also remained strong in first quarter 2006. To avoid potential overheating, Peoples Bank of China, (the central bank of China) took a pre-emptive move by announcing a 27 basis points increase in bank lending rate in April. The Chinese government finally came up with a policy to allow local Chinese money to invest in overseas markets through the Qualified Domestic Institutional Investor (QDII) scheme. Economic growth in Hong Kong remained on track during the period with stable inflation and employment trends. GDP growth in fourth quarter 2005 came in at 7.6% YoY, following the stellar growth of 8.3% YoY in third quarter 2005. First quarter 2006 GDP growth was 8.2% YoY in Hong Kong. However, due to the continuous rise in interest rates, the property sector suffered in the period after its strong run since third quarter 2003. In Taiwan GDP growth in fourth quarter 2005 came in higher than forecast at 6.4% YoY up from 4.4% YoY in the previous quarter. First quarter 2006 GDP growth was 4.9% YoY in Taiwan. On the corporate front, technology companies such as AU Optronics and Siliconware Precision reported better than expected numbers for fourth quarter 2005 with higher capacity utilization and stabilization in product prices. Performance of the Taiwan banking sector was choppy during the period, with negative surprises coming from higher delinquencies of consumer lending while hopes of industry consolidation remained in place.

The Fund’s outperformance against the benchmark was mainly due to stock selection, which added substantial value in each territory.

In terms of performance attribution, our overweight in China and relative underweight in Hong Kong and Taiwan worked well for the Fund from a country selection perspective. Our overweight in the property sectors in China and Taiwan have also contributed positively to performance. In Taiwan, stock selection in the Computer Hardware sub-sector was particularly beneficial. Selected technology names with a focus on mobile communications performed well and have added value, while our overweight in some of the computer manufacturing companies detracted value as they underperformed. In Hong Kong favorable selection among the banks, (partially offset by an allocation to non-benchmark HSBC) and the underweight of a major industrial conglomerate helped relative performance. In China, stock selection gains arose mostly from overweighting Real Estate Management and Development companies and a Metals company which more than doubled in value during the period. Export oriented companies in China also underperformed a rising market due to concerns over Chinese RMB appreciation and higher raw material costs and have contributed negatively.

Current Strategy and Outlook: The Fund continues to favor China because of its strong macroeconomic outlook. The recently announced first quarter 2006 GDP growth and the fixed asset investment growth surprised the market on the upside. As a result, the market widely believes that the recent increase in Chinese interest rate would help cool down the vibrant economy. Nevertheless, we remain bullish on the medium-term outlook for the Chinese markets from a liquidity standpoint. Hong Kong may continue to struggle in the near term due to concerns over a prolonged period of U.S. interest rate hikes. Real estate related stocks in Taiwan are gaining more traction recently thanks to the appreciation of Taiwan dollar as well as hopes of an improvement in cross strait relationship. Technology stocks in Taiwan were hampered by the worse than expected results from the U.S. heavyweights such as Intel. Insurance companies look more promising on a relative basis due to their real asset holdings and improvement in interest rates. Overall, we remain neutral in Taiwan as a market with a preference for domestic plays.

14

PORTFOLIO MANAGERS’ REPORT | | ING GREATER CHINA FUND |

| | |

| Cumulative Total Returns for the Periods Ended April 30, 2006 | |

| | | | | | | |

| | Since Inception | | Since Inception | | Since Inception | |

| | of Class A | | of Class B | | of Class C | |

| | December 21, 2005 | | January 6, 2006 | | January 11, 2006 | |

| | | | | | | |

| Including Sales Charge: | | | | | | | |

| Class A(1) | | 14.33 | % | | — | | | — | | |

| Class B(2) | | — | | | 9.25 | % | | — | | |

| Class C(3) | | — | | | — | | | 12.59 | % | |

| Excluding Sales Charge: | | | | | | | | | | |

| Class A | | 21.30 | % | | — | | | — | | |

| Class B | | — | | | 14.25 | % | | — | | |

| Class C | | — | | | — | | | 13.50 | % | |

| MSCI All Countries Golden Dragon Index | | 16.50 | %(5) | | 16.50 | %(5) | | 16.50 | %(5) | |

| | | | | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING International SmallCap Fund against the Indicies indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| | |

(2) | | Reflects deduction of the Class B deferred sales charge of 5%. |

| | |

(3) | | Reflects deduction of the Class C deferred sales charge of 1%. |

| | |

(4) | | The MSCI All Countries Golden Dragon Index is a broad-based, unmanaged index of common stocks traded in China, Hong Kong and Taiwan. |

| | |

(5) | | Since inception performance for the index is shown from January 1, 2006. |

15

ING INDEX PLUS INTERNATIONAL EQUITY FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

(1) Includes twelve industries, which each represents < 1.3% of net assets.

Portfolio holdings are subject to change daily.

ING Index Plus International Equity Fund (the “Fund”) seeks to exceed the benchmark for developed markets outside the United States (the MSCI EAFE) while maintaining a market level of risk and characteristics comparable to the index. The Fund is managed by Carl Ghielen and Martin Jansen, ING Investment Management Advisors B.V. — the Sub-Adviser.

Performance: From December 21, 2005, the inception of the Fund, to April 30, 2006 the Fund’s Class A shares, excluding sales charges, provided a total return of 12.20% compared to the MSCI EAFE Index, which returned 14.78% for the same period.

Portfolio Specifics: The Fund’s strategy is designed to add value to the MSCI EAFE benchmark through bottom-up security selection on the basis of customized sector models while maintaining approximate benchmark weights of countries, sectors and industries represented in the benchmark. The active risk is substantially controlled by the relatively large number of securities in the Fund (between 340 and 430). As a first step, the best ranked 200 stocks are selected for inclusion across countries, sectors and industries. To ensure that appropriate index weights and an index-like profile are maintained, an additional 140-230 of the next most attractive securities are added. The Fund is rebalanced monthly to maintain the desired tilt to stocks ranking well in the individual sectors and industries represented in the benchmark.

The Fund’s return underperformed the benchmark in the six months ended April 30, 2006. Apart from the negative impact of residual cash in a strongly rising market, this shortfall was attributable almost entirely to value lost within the sectors, as by design the country and sector neutral construction of the portfolio does not add value.

The predictive power of the individual factors included in each of the international sector models for a particular reporting period substantially determines the stock selection result in each sector. For this reporting period, our positioning in the financials had the largest negative impact, due largely to adverse ranking outcomes of the change in return on invested capital and historic price/earnings ratio factors used in the sector model. The earnings and cash flow variables used in the health care and industrial sectors also detracted from the outcome, as did the earnings momentum and price reversal factors in the consumer discretionary sector. On the positive side, our ranking model in materials proved especially effective as earnings, cash flow and dividend yield factors combined to select stocks successfully. The change in return on invested capital and EBITDA/price factors drove successful stock selection in the energy sector. The selection results from the utilities, telecommunication services, and consumer staples sectors also contributed marginally.

Current Strategy and Outlook: By design, the Fund maintains approximate benchmark weights of the countries, economic sectors and industries constituting the MSCI EAFE, and is expected to track the benchmark relatively closely. Stock selection flows from the in-sector/industry ranking models. Fund construction and risk control seek to ensure the characteristics of the Fund remain within an acceptable band around the benchmark. Our most attractively ranked stocks may have individual overweights of up to 100 basis points, while for risk control purposes the maximum allowable underweight per security is 50 basis points. Within this context, the Fund currently has a modest tilt towards lower valuation and smaller capitalization stocks and has a resultant modest focus on stocks linked primarily to local economies. The current portfolio of stocks has generated an historic earnings growth slightly higher than the index, and carries a dividend yield similar to the index.

16

PORTFOLIO MANAGERS’ REPORT | | ING INDEX PLUS INTERNATIONAL EQUITY FUND |

| | | | | |

| Cumulative Total Returns for the Periods Ended April 30, 2006 | |

| | | | | |

| | Since Inception | | Since Inception | |

| | of Class A & I | | of Class B & C | |

| | December 21, 2005 | | January 12, 2006 | |

| | | | | |

| Including Sales Charge: | | | | | |

| Class A(1) | | 5.75 | % | | — | | |

| Class B(2) | | — | | | 2.38 | % | |

| Class C(3) | | — | | | 6.29 | % | |

| Class I | | 12.20 | % | | — | | |

| Excluding Sales Charge: | | | | | | | |

| Class A | | 12.20 | % | | — | | |

| Class B | | — | | | 7.38 | % | |

| Class C | | — | | | 7.29 | % | |

| Class I | | 12.20 | % | | — | | |

| MSCI EAFE® Index(4) | | 14.78 | %(5) | | 14.78 | %(5) | |

| | | | | | | | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING International SmallCap Fund against the Index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in the index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) | | Reflects deduction of the maximum Class A sales charge of 5.75%. |

| | |

(2) | | Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and 5 year returns. |

| | |

(3) | | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| | |

(4) | | The MSCI EAFE® Index is an unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East. |

| | |

(5) | | Since inception performance for the index is shown from January 1, 2006. |

17

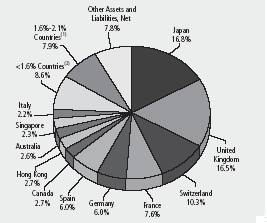

ING INTERNATIONAL FUND | | PORTFOLIO MANAGERS’ REPORT |

Country Allocation

as of April 30, 2006

(as a percent of net assets)

Japan | | 22.6 | % |

United Kingdom | | 18.4 | % |

Germany | | 8.8 | % |

United States | | 8.1 | % |

Switzerland | | 7.4 | % |

France | | 7.2 | % |

Australia | | 3.9 | % |

Netherlands | | 3.5 | % |

Belgium | | 2.5 | % |

Finland | | 2.3 | % |

Hong Kong | | 2.3 | % |

1.3%-2.1% Industries(1) | | 10.6 | % |

<1.3% Industries(2) | | 4.3 | % |

Other Assets and Liabliites, Net* | | (1.9 | )% |

* Includes securities lending collateral.

(1) Includes seven countries, which each represents 1.3%-2.1% of net assets.

(2) Includes five countries, which each represents <1.3% of net assets.

Portfolio holdings are subject to change daily.

ING International Fund (the “Fund”) seeks long-term growth of capital through investment in equity securities and equity equivalents of companies outside the U.S. Before April 28, 2006, Philip Schwartz, CFA and Richard Saler managed the Fund, ING Investment Management Co. — the Sub-Adviser.*

Performance: For the six-month period ended April 30, 2006, the Fund’s Class A shares, excluding sales charges, provided a total return of 22.48% compared to the MSCI EAFE Index, which returned 23.10% for the same period.

Portfolio Specifics: Rising investor confidence and an improving economic outlook in Europe and Japan led to a strong advance of the cyclically sensitive sectors.

Our regional positioning proved successful during the period as the Fund benefitted from our allocation to emerging market stocks. Our move from an underweight of developed Asia to a modest overweight position added to performance. We remained underweight Europe as well, which also proved effective. Stock selection was particularly beneficial within developed Asia and Japan during this period but it was weak in European Markets.

However, our sector strategy reacted negatively while we obtained positive results from successful stock selection. The positive contributions from our overweight of the financials and underweight of the telecom services sectors were offset by our underweight of the strong industrials sector. Positive selection outcome came mainly from stocks within the materials, telecom services and financials sectors. The sectors that detracted most from value were the health care, energy and utilities sectors.

At the security level, one of our largest contributions came from our holding in Nordea Bank AB, a Swedish bank, following announcements of higher profits and an increased dividend. Another positive contributor was Amada Co. Ltd., a Japanese industrial company, following increased income due to higher orders as both domestic and overseas capital expenditures hit higher levels. Another significant individual contributor was NHN Corp., a Korean web search engine, due mostly to rumors that Google was going to initiate a hostile takeover of the firm. Among the major detractors were Cadbury Schweppes, and British telecom company, Vodafone Group PLC, after a decrease in profits. Another negative contributor was Acom Co. Ltd., a Japanese consumer finance firm after the Japanese government announced plans to limit consumer lending.

Current Strategy and Outlook: Uri Landesman assumed responsibility for management of the Fund on May 1, 2006, the day following the last day of the period covered by this report. As portfolio manager he intends to reshape the Fund profile toward large cap growth stocks. Accordingly, we expect that the fundamental characteristics of the portfolio will be consistent with an emphasis on companies with earnings growth rates that are faster than the average for companies in broad international benchmarks such as the MSCI EAFE International Index. Further, stock selection screens will rank stocks on the basis of free cash flow generation, earnings momentum and price momentum to determine a shorter list of purchase candidates for more intensive analysis. Ultimately, the portfolio will differ from its starting point in several ways. For instance, faster rates of growth suggest that price-to-book value, price-to-cash flow and price-to-earnings ratios will be higher, and dividend yield will be lower, features that are consistent with a growth-biased portfolio. We also expect average market capitalization to be lower than that of the original portfolio. Generally the Fund will assume a regionally neutral stance, but we expect to maintain overweight positions in growth-oriented sectors such as consumer discretionary, health care and information technology. Conversely, we intend to maintain underweight positions in more value-oriented sectors such as energy, financials and utilities.

Over very long periods, the outlook for an international growth strategy is not materially different from a core strategy. However, over shorter periods, the growth strategy tends to be favored when investors prefer high quality companies and when international economies and markets are healthy and the portfolio benefits from expanding stock valuations and reported growth rates that exceed analyst estimates. In any event, we believe the emphasis on growth stocks will provide dependable opportunities to provide good performance in most market environments.

* As of May 1, 2006 Uri Landesman, head of international equity, is managing the Fund.

18

PORTFOLIO MANAGERS’ REPORT | | ING INTERNATIONAL FUND |

| | | | | | | | | | | | | | | |

| Average Annual Total Returns for the Periods Ended April 30, 2006 | |

| | | | | | | | | | | | | | | |

| | | | | | | | Since Inception | | Since Inception | | Since Inception | | Since Inception | |

| | | | | | | | of Class B | | of Class C | | of Class Q | | of Class I | |

| | 1 Year | | 5 Year | | 10 Year | | August 22, 2000 | | September 15, 2000 | | February 26, 2001 | | January 15, 2002 | |

| | | | | | | | | | | | | | | |

| Including Sales Charge: | | | | | | | | | | | | | | | |

| Class A(1) | | 24.18 | % | | 5.61 | % | | 7.50 | % | | — | | | — | | | — | | | — | | |

| Class B(2) | | 25.66 | % | | 5.53 | % | | — | | | 2.31 | % | | — | | | — | | | — | | |

| Class C(3) | | 29.56 | % | | 5.85 | % | | — | | | — | | | 3.42 | % | | — | | | — | | |

| Class I | | 32.07 | % | | — | | | — | | | — | | | — | | | — | | | 12.67 | % | |

| Class Q | | 31.76 | % | | 6.91 | % | | — | | | — | | | — | | | 6.40 | % | | — | | |

| Excluding Sales Charge: | | | | | | | | | | | | | | | | | | | | | | |

| Class A | | 31.73 | % | | 6.88 | % | | 8.14 | % | | — | | | — | | | — | | | — | | |

| Class B | | 30.66 | % | | 5.85 | % | | — | | | 2.46 | % | | — | | | — | | | — | | |

| Class C | | 30.56 | % | | 5.85 | % | | — | | | — | | | 3.42 | % | | — | | | — | | |

| Class I | | 32.07 | % | | — | | | — | | | — | | | — | | | — | | | 12.67 | % | |

| Class Q | | 31.76 | % | | 6.91 | % | | — | | | — | | | — | | | 6.40 | % | | — | | |

| MSCI EAFE® Index(4) | | 34.00 | % | | 9.59 | % | | 7.03 | % | | 5.49 | %(5) | | 5.49 | %(5) | | 9.26 | %(6) | | 15.31 | %(7) | |