| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | August 31, 2010 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . 18.9 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-7986 |

|

The Alger Institutional Funds |

(Exact name of registrant as specified in charter) |

|

111 Fifth Avenue New York, New York | | 10003 |

(Address of principal executive offices) | | (Zip code) |

|

Mr. Hal Liebes

Fred Alger Management, Inc.

111 Fifth Avenue

New York, New York 10003 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-806-8800 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | October 31, 2007 | |

| | | | | | | | |

ITEM 1. REPORTS TO STOCKHOLDERS.

Alger SmallCap Growth Institutional Fund

| Alger MidCap Growth Institutional Fund |

Alger LargeCap Growth Institutional Fund

| Alger Capital Appreciation Institutional Fund |

The Alger

Institutional Funds

ANNUAL REPORT

October 31, 2007

Table Of Contents

THE ALGER INSTITUTIONAL FUNDS

| Letter to Our Shareholders | | | 1 | | |

|

| Fund Highlights (Unaudited) | | | 9 | | |

|

| Portfolio Summary (Unaudited) | | | 13 | | |

|

| Schedules of Investments | | | 14 | | |

|

| Statements of Assets and Liabilities | | | 34 | | |

|

| Statements of Operations | | | 36 | | |

|

| Statements of Changes in Net Assets | | | 38 | | |

|

| Financial Highlights | | | 40 | | |

|

| Notes to Financial Statements | | | 44 | | |

|

| Report of Independent Registered Public Accounting Firm | | | 55 | | |

|

| Additional Information (Unaudited) | | | 56 | | |

|

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we'll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

Dear Shareholders, November 23, 2007

Roller coaster: it's an apt metaphor for the past fiscal year. With the sharp run-up in the stock market through June, followed by the near-meltdown of those parts of the financial sector exposed to housing and mortgages, there were times when the financial markets felt like a long weekend at Six Flags Great Adventure. Even investors with cast-iron stomachs were wondering: why did this happen? How long can it continue? And is there an upside?

Once again, perceptions were more dramatic than realities. For all the agita in the markets, the indices posted solid gains in the United States, not to mention throughout the world, and the day-to-day volatility was ultimately less than the sum of its parts. Economic growth chugged along and most companies showed decent if not downright good earnings growth — with the notable and glaring exception of the financial sector in the third quarter of 2007. In short, there was noise, drama and even smoke, but not much actual fire. Or back to the initial metaphor, the roller coaster ride was full of sharp turns, shrieks, and moments of fear and anticipation, but the car stayed on the tracks, the ride ended safely, and most people even made some progress along the way.

Black Friday Revisited

In the financial markets it was a year of milestones and anniversaries. Both the S&P 500 Indexi and the Dow Jones Industrial Averageii reached new heights during the year, with the Dow breaking 13,000 and then 14,000 twice. But October 19, 2007 was a more somber milestone: the 20th anniversary of Black Friday on Wall Street. In the days before, pundits didn't hesitate to predict a "curse" coming back to haunt the markets. (Sounds ridiculous, but a surprising number of articles had that exact headline the next morning.) Sure enough, the Dow tumbled by 247 points, but that was nothing compared to that one-day 508-point loss in 1987, especially in percentage terms. In today's market the Dow would have had to shed about 3,100 points in one day to be comparable to the cras h of '87.

Three times this past year U.S. markets fell sharply. On February 27, the Dow lost 314 points, with a total decline of 736 points from February 20 to March 5. The sell-off was triggered by rumors of a possible Chinese government squeeze on credit. Then, the Dow climbed a total of 1,910 points over the following four months to register a new record of 14,000 on July 19. Through the end of July, the markets were turbulent as the sub-prime mortgage debacle unfolded. From July 26 through August 6, the Dow roller coaster went up and down with dizzying speed, with some days showing losses as great as 268 points while others showed gains of up to 169 points. But the true second phase of the market sell-off happened during the headiest days of the credit crunch — from August 8 to August 16 — with the Dow experiencing a total loss of 812 points. That was followed by a September rally that recouped most of the lost ground.

The third sell-off period occurred during the final weeks of the fiscal year, and lasted from October 11 through November 12 — when the Dow shed a total of 1,167 points, as the sub-prime mess erupted into a full-blown credit crisis involving banks and financial institutions. Even the tech sector — one of the strongest performers for

-1-

the year — saw a steep pullback at the end of October. However, after each sell-off, the markets rebounded stronger than ever, and in some cases — as in the February drop — the markets moved into a long period of steady uphill climb.

To push our roller coaster metaphor even further – the number of extreme single day swings was even greater than the sell-off periods. In 2007, the Dow saw no less than eight days of single-day losses of more than 200 points (the largest being 314 points) and six days of gains of more than 169 points (with the largest being 319 points). Most telling, perhaps, is that on three separate days (August 16, 17, and November 8) the day's close showed little movement, yet during the day the Dow had swooned more than 442 points. On November 8, for example, the Dow fell 462 points before climbing back to a 64 point loss at day's end.

We believe the year's turbulence emphasizes a trend that has become more noticeable with each passing year: high-levels of short-term volatility and economic concerns unfolding against a backdrop of unusual global economic stability. The fact that so many people felt so unsettled even while the markets remained up for the year should tell us something about the disconnect between how people feel and what has actually been happening.

Global Growth and Earnings

Fifty years ago it was perfectly fair to say "as goes the U.S. economy, so go U.S. companies and their stocks." Today that no longer holds true. Earnings this year indicate that the trajectory of companies is different and more positive than that of countries and that the United States is no longer the sole guide to the health of U.S. firms. While U.S. GDP grew a paltry 0.6% in the first quarter of 2007, the companies of the S&P 500 Index registered nearly 8% growth. And, while economic data still matters, it is no longer a good idea to use the U.S. economy as an automatic proxy for how U.S. companies, or their stock prices, will perform.

The world economy has grown at a 4% annual pace for the past several years; according to BCA research, this has been the strongest expansion phase since 1960. And earnings for many companies — especially innovative growth companies — continue to benefit from very strong international growth, which has begun to "decouple" from dependence on the U.S. economy. One consumer company recently reported 2% growth in the U.S. market and 17% growth abroad with more than 50% growth in China alone. In fact, global equity markets have been on a tear and many U.S.-listed companies are benefiting from the same global growth trends. Especially for the larger companies of the S&P 500, the U.S. is simply one market, albeit a large and vital aspect of their global business model.

The weakness of the U.S. dollar is yet one more factor that has benefited U.S. companies doing business outside of the United States. Corporate profits have been boosted by a continuing weak dollar which inflates the reported dollar profits of U.S.-listed companies.

At the same time, global interest rates have compressed, with both short-term and long-term rates as well as corporate and government rates converging between 4% and 5%. One negative consequence of that compression is that many fixed-income managers have taken oversize risks in an attempt to generate above average returns, and the consequences of those risks has been nothing short of a debacle for many funds and for financial institutions exposed to housing and mortgage-backed securities.

-2-

The Sub-Prime Mortgage Mess

In August, the mortgage mess transmogrified into a global financial panic that seemed on the verge of draining not just excess liquidity out of the system but all liquidity. If that had happened — and there was some risk that it was about to — financial systems would have ground to a halt. Short-term liquidity in the form of commercial paper is to the financial system what water is to the body. Without it, all bets are — literally — off.

What threatened the financial system was that the leveraged exposure was substantially greater than the actual size of defaults or outstanding low-credit loans. Wall Street didn't simply "securitize" loans by slicing and dicing them. It buried them in packages of other loans and then bundled them with higher credit loans. When mortgage defaults began to rise on the lower end of the spectrum, many Wall Street institutions and hedge funds realized that they didn't really know which of these various loan derivatives were good and which were bad. The result was that trading in almost anything mortgage-related froze in the middle of July, creating a domino effect. Lenders and mortgage brokers tightened lending standards and banks demanded more collateral, not just for home loans, but for credit lines to hedge funds and private equity firms. Suddenly, getting a loan of any sort went from incredibly easy to astonishingly difficult.

That crisis was — at least temporarily — averted by the aggressive action of the Federal Reserve which cut the Fed funds rate by 50 basis points (one-half a percentage point) to 4.75% in mid-September. The rate cut was a welcome and perhaps essential step in preventing the mortgage mess from imperiling the financial system. Whether or not the rate cuts (the Fed cut an additional quarter point on the last day of this fiscal year, October 31) will have any lasting impact, or if they were merely a demonstration that the Fed could and would act if necessary, remains to be seen.

Our conclusion: it will continue to be a painful and dislocating period for real estate and for millions of people exposed to its descent. Low-end consumers, and many in the middle, will feel the pain. As adjustable-rate mortgages reset, there will be substantial numbers of foreclosures. Some Wall Street investment firms will lose money; many already have. But we do not believe that the global financial system is in jeopardy, nor do we think that the housing bust will severely dent corporate profits in those sectors of the economy not directly exposed to housing and mortgage-backed financial instruments. One unintended consequence is that stocks may ultimately benefit from the meltdown if investors find themselves turning to equities as a safe haven.

Portfolio Matters

Alger LargeCap Growth Institutional Fund

The Alger LargeCap Growth Institutional Fund returned 27.32% for the fiscal year ended October 31, 2007, compared with a return of 19.22% for the Russell 1000 Growth Indexiii.

Information Technology represented an average weight of 29.82%. The Fund was overweight compared to the benchmark, but outperformed in this sector. Strong performers included MEMC Electronic Materials, Inc., a global supplier of silicon wafers to the semiconductor industry, electronic game manufacturer Nintendo Co. Ltd., and Apple, Inc.

-3-

In the Consumer Discretionary sector, at an average weight of 12.08%, the Fund was underweight but outperformed the benchmark. XM Satellite Radio Holdings Inc., Las Vegas Sands Corp. and Hilton Hotels Corp. were the top performers in this sector.

The Fund was underweight and underperformed the benchmark in the Industrials sector, at an average weight of 11.70%. ITT Corp., a leading U.S. defense contractor and the world's largest supplier of equipment to move and treat water and wastewater, and General Dynamics Corp., a leading defense industry contractor, were solid performers in this sector.

At an average weight of 11.29% the Fund was underweight the benchmark in the Health Care sector and underperformed. Merck & Co. Inc., the international manufacturer and distributor of pharmaceuticals, Intuitive Surgical Inc., a leader in surgical robotics and Health Net Inc., one of the U.S.'s largest managed health care companies, were solid performers in this sector.

During the fiscal year, the Alger LargeCap Growth Institutional Fund saw underperformance in the Industrials sector from FedEx Corp. and United Airlines Corp. Underperformers in the Health Care sector included Amgen, Inc., a human therapeutics company in the biotechnology industry, and Medco Health Solutions, Inc., a leading pharmacy benefit manager.

Alger SmallCap Growth Institutional Fund

The Alger SmallCap Growth Institutional Fund gained 26.36% for the fiscal year ended October 31, 2007, compared to the Russell 2000 Growth Indexiv which returned 16.72%.

In the Information Technology sector, the Fund, at an average weight of 22.76%, was slightly underweight the benchmark, but outperformed. Top performers in this sector were Synchronoss Technologies, Inc., a provider of on-demand transaction management solutions, DealerTrack Holdings, Inc., a leading provider of on-demand software and data solutions for the automotive retail industry in the United States, and Omniture, Inc., a provider of online business optimization services.

At an average weight of 17.43%, the Fund was underweight but outperformed the benchmark in Health Care. Ventana Medical Systems, Inc., one of the world's leading developers and manufacturers of medical diagnostic instruments and technology was the prominent performer in this sector, followed by PAREXEL International Corp., a leading global bio/pharmaceutical services organization and Onyx Pharmaceuticals, Inc.

In the Consumer Discretionary sector, the Fund, at an average weight of 15.62% was marginally underweight the benchmark but outperformed. Top performers in this sector were Deckers Outdoor Corp., a manufacturer of function-oriented, high-performance outdoor footwear, the travel website Priceline.com, Inc., and Bally Technologies, Inc., a manufacturer of gaming machines and computerized monitoring systems for the gaming industry worldwide.

At an average weight of 13.55%, the Fund was underweight, but significantly outperformed the benchmark in the Industrials sector. Top performers in this sector were: BE Aerospace, Inc., the world's leading manufacturer of cabin interior products for commercial aircraft, FTI Consulting, Inc., a global business advisory firm that provides critical legal, financial and reputational advice and Bucyrus International, Inc., a world leader in the manufacture of draglines, drills and shovels for the surface mining industry.

-4-

Key detractors in the Fund during the fiscal year included Coldwater Creek, Inc., a women's apparel and accessories retailer, DSW, Inc., a footwear retailer, American Reprographics Co., the largest reprographics company in the United States, and McCormick & Schmick's Seafood Restaurants.

Alger MidCap Growth Institutional Fund

For the fiscal year ended October 31, 2007, the Alger MidCap Growth Institutional Fund gained 45.45%, compared to the Russell Midcap Growth Indexv with a return of 19.70%.

The Fund, at an average weight of 23.91%, had a significant exposure in Information Technology. This weighting was overweight the benchmark but outperformed. Nintendo Co. Ltd., was the strongest contributor in this sector, followed by Research in Motion Ltd., a leader in wireless communications, Apple, Inc., and MEMC Electronic Materials, Inc.

In the Consumer Discretionary sector, the Fund had an average weight of 20.10%, slightly underweight the benchmark but outperforming. The auction house Sotheby's, Focus Media Holding, Ltd., the largest outdoor TV advertising network in China, and the retail chain GameStop Corp., were the top performers in this sector.

At an average weight of 14.56%, the Fund was slightly overweight the benchmark in the Health Care sector, but underperformed. Notable contributors included Intuitive Surgical, Inc., and Onyx Pharmaceuticals. Medco Health Solutions, Inc. and Zimmer Holdings, Inc. were key detractors.

The Fund was underweight the benchmark, at an average weight of 11.95%, in the Industrials sector but outperformed. Strong contributors included McDermott International, Inc., a leading worldwide energy services company, BE Aerospace, Inc., and Armor Holdings, a manufacturer and provider of specialized security products.

During the fiscal year, the Fund saw outperformanced across most sectors, but did underperform in companies including Isilon Systems, Inc., a Seattle company that designs storage systems and software for digital content, and retailers Starbucks Corp., and Netflix, Inc.

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund gained 41.31% for the fiscal year ended October 31, 2007, outperforming the Russell 3000 Growth Indexvi return of 18.99%.

Information Technology represented an average weight of 32.27% of the Fund's holdings, and outperformed the benchmark with strong contributions from: MEMC Electronic Materials, Inc., ON Semiconductor Corp., a provider of semiconductor components, Apple Inc. and DealerTrack Holdings, Inc.

In the Health Care sector, the Fund, at an average weight of 13.49%, was underweight compared to the benchmark but outperformed. The top performers were Intuitive Surgical, Inc., Hologic, Inc., a developer and manufacturer of proprietary x-ray systems and Onyx Pharmaceuticals Inc.

At an average weight of 10.92%, the Fund was underweight the benchmark in the Consumer Discretionary sector but outperformed. Focus Media Holding, Ltd. was a top performer as was Bally Technologies, Inc., and Hilton Hotels Corp.

In the Industrial sector, the Fund at an average weight of 8.94% was underweight the benchmark but outperformed. Top performers in this sector were: Armor

-5-

Holdings, JA Solar Holdings Inc., a manufacturer or high-performance solar cells and McDermott International Inc.

While the Fund outperformed overall there were detractors across sectors, including the diet plan provider, NutriSystems, Inc., retailer Urban Outfitters, Inc., Rambus, Inc., a provider of high-speed interface technology, Trident Microsystems, Inc., a supplier of processors for flat panel displays, Amgen, Inc., Sepracor, Inc., and Sunoco, Inc.

In Summary

Wall Street tends to react to sudden changes in the status quo with apocalyptic rhetoric. Though we don't take the psychology of the markets lightly, proprietary indicators that we have used for many decades suggest that while these roller coaster movements may continue, the fundamental picture for many growth companies remains positive.

The early fall pullback was steep, with the S&P losing about 10%, but it is still in the realm of normal given recent trends. There have been much steeper corrections in emerging markets over the past three years, followed by equally steep recoveries and subsequent gains. In each of those previous sell-offs, there was no dearth of commentary that some structural weakness in the markets was being exposed yet predictions of doom and gloom proved either premature or simply wrong.

With continued global expansion, the unwinding of the mortgage mess and what likely will be a hectic and turbulent U.S. election season, 2008 looks to be unsettled in the equity markets. Swoons which came fast and furious in 2007 may happen even faster and be even more furious.

But the fundamentals of the economy, of companies in general, and of the domestic and global equity markets, do not seem to us either weak or overvalued. As bottom-up stock pickers, we believe these market sell-offs offer excellent opportunities to add or increase positions in growth companies whose opportunities are, in fact, just beginning.

Respectfully submitted,

| |  | |

|

| Daniel C. Chung | | Zachary Karabell | |

|

| Chief Investment Officer | | Chief Economist | |

|

i Standard & Poor's 500 Index is an index of the 500 largest companies in the United States.

ii The Dow Jones Industrial Average is an index of common stocks comprised of major industrial companies and assumes reinvestment of dividends. It is frequently used as a general measure of stock market performance.

iii The Russell 1000 Growth Index is an unmanaged index designed to measure the performance of the largest 1000 companies in the Russell 3000 Index with higher price-to-book ratios and higher forecasted growth values. The Russell 3000 Index measures the performance of the 3000 largest U.S. companies based on the total market capitalization, which represents 98% of the U.S. Equity Market.

-6-

iv The Russell 2000 Growth Index is an unmanaged index designed to measure the performance of the 2000 smallest companies in the Russell 3000 Index with higher price-to-book ratios and higher forecasted growth values.

v The Russell Midcap Growth Index is an unmanaged index designed to measure the performance of the 800 smallest companies in the Russell 1000 Index with higher price-to-book ratios and higher forecasted growth values.

vi The Russell 3000 Growth Index is an unmanaged index designed to measure the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values.

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Funds unless proceeded or accompanied by an effective prospectus for the Funds. Funds returns represent the fiscal 12 month period return of Class I shares. The performance data quoted represents past performance, which is not an indication or guarantee of future results. Standardized performance results can be found on the following page. The investment return and principal value of an investment in a fund will fluctuate so that an investor's shares when redeemed may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Fo r performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the Funds' management in this report are as of the date of the Shareholders letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable; however, there is no guarantee that such information is accurate. Any securities mentioned should be considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities may be for a variety of reasons, including without limitation, in response to cash flows, inclusion in a benchmark and risk control. Please refer to the Schedules of Investments for each fund which is included in this report for a complete list of fund holdings as of October 31, 2007. Securities mentioned in the Shareholders letter, if not found in the Schedule of Investments, were held by the Fund during the Fund's fiscal year.

A Word About Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends to be higher in relation to their companies' earnings and may be more sensitive to market, political and economic developments. Investing in the stock market involves gains and losses and may not be suitable for all investors. Stocks of small- and mid-sized companies are subject to greater risk than stocks of larger, more established companies owing to such factors as limited liquidity, inexperienced management, and limited financial resources. Funds that participate in leveraging, such as the Capital Appreciation Institutional Fund, are subject to the risk that borrowing money to leverage will exceed the returns for securities purchased or that the securities purchased may actually go down in value; thus, the Funds' net asset value

-7-

can decrease more quickly than if the Funds had not borrowed. For a more detailed discussion of the risks associated with a Funds, please see the Funds' Prospectus.

Before investing, carefully consider a fund's investment objective, risks, charges, and expenses. For a prospectus containing this and other information about The Alger Institutional Funds call us at (800) 992-3863 or visit us at www.alger.com. Read it carefully before investing. Fred Alger & Company, Incorporated, Distributor. Member NYSE, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

-8-

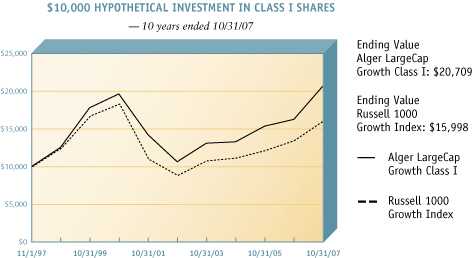

ALGER LARGECAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through October 31, 2007 (Unaudited)

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger LargeCap Growth Institutional Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2007. The figures for the Alger LargeCap Growth Institutional Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Performance for the Alger LargeCap Growth Institutional Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON

AVERAGE ANNUAL TOTAL RETURNS

| | | 1

YEAR | | 5

YEARS | | 10

YEARS | | SINCE

INCEPTION | |

| As of 10/31/07 | |

| Class I (Inception 11/8/93) | | | 27.32 | % | | | 14.23 | % | | | 7.55 | % | | | 10.63 | % | |

| Russell 1000 Growth Index | | | 19.22 | % | | | 12.61 | % | | | 4.81 | % | | | 9.31 | % | |

| Class R (Inception 1/27/03) | | | 26.69 | % | | | N/A | | | | N/A | | | | 16.08 | % | |

| Russell 1000 Growth Index | | | 19.22 | % | | | N/A | | | | N/A | | | | 14.23 | % | |

| As of 9/30/07 | |

| Class I | | | 26.58 | % | | | 14.66 | % | | | 6.57 | % | | | 10.40 | % | |

| Russell 1000 Growth Index | | | 19.36 | % | | | 13.84 | % | | | 4.07 | % | | | 9.11 | % | |

| Class R | | | 25.87 | % | | | N/A | | | | N/A | | | | 15.46 | % | |

| Russell 1000 Growth Index | | | 19.36 | % | | | N/A | | | | N/A | | | | 13.69 | % | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The graph and table above do not reflect the deduction of taxes that a shareholder would have paid on fund distributions or on the redemption of fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

-9-

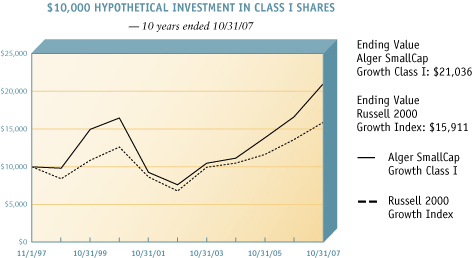

ALGER SMALLCAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through October 31, 2007 (Unaudited)

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger SmallCap Growth Institutional Class I shares and the Russell 2000 Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2007. The figures for the Alger SmallCap Growth Institutional Class I shares and the Russell 2000 Growth Index include reinvestment of dividends. Performance for the Alger SmallCap Growth Institutional Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON

AVERAGE ANNUAL TOTAL RETURNS

| | | 1

YEAR | | 5

YEARS | | 10

YEARS | | SINCE

INCEPTION | |

| As of 10/31/07 | |

| Class I (Inception 11/8/93) | | | 26.36 | % | | | 22.53 | % | | | 7.72 | % | | | 12.07 | % | |

| Russell 2000 Growth Index | | | 16.72 | % | | | 18.57 | % | | | 4.75 | % | | | 7.18 | % | |

| Class R (Inception 1/27/03) | | | 25.70 | % | | | N/A | | | | N/A | | | | 23.80 | % | |

| Russell 2000 Growth Index | | | 16.72 | % | | | N/A | | | | N/A | | | | 19.59 | % | |

| As of 9/30/07 | |

| Class I | | | 27.17 | % | | | 22.30 | % | | | 6.22 | % | | | 11.64 | % | |

| Russell 2000 Growth Index | | | 18.93 | % | | | 18.70 | % | | | 3.65 | % | | | 6.88 | % | |

| Class R | | | 26.52 | % | | | N/A | | | | N/A | | | | 22.64 | % | |

| Russell 2000 Growth Index | | | 18.93 | % | | | N/A | | | | N/A | | | | 18.86 | % | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The graph and table above do not reflect the deduction of taxes that a shareholder would have paid on fund distributions or on the redemption of fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

-10-

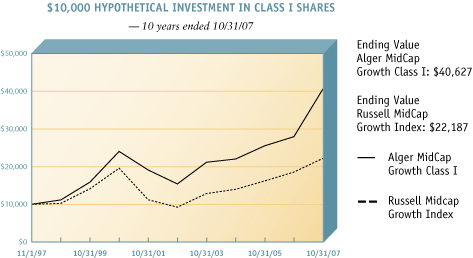

ALGER MIDCAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through October 31, 2007 (Unaudited)

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger MidCap Growth Institutional Class I shares and the Russell Midcap Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2007. Figures for the Alger MidCap Growth Institutional Class I shares and the Russell Midcap Growth Index include reinvestment of dividends. Performance for the Alger MidCap Growth Institutional Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON

AVERAGE ANNUAL TOTAL RETURNS

| | | 1

YEAR | | 5

YEARS | | 10

YEARS | | SINCE

INCEPTION | |

| As of 10/31/07 | |

| Class I (Inception 11/8/93) | | | 45.45 | % | | | 21.42 | % | | | 15.05 | % | | | 17.88 | % | |

| Russell Midcap Growth Index | | | 19.70 | % | | | 19.21 | % | | | 8.30 | % | | | 10.76 | % | |

| Class R (Inception 1/27/03) | | | 44.70 | % | | | N/A | | | | N/A | | | | 23.26 | % | |

| Russell Midcap Growth Index | | | 19.70 | % | | | N/A | | | | N/A | | | | 20.14 | % | |

| As of 9/30/07 | |

| Class I | | | 43.96 | % | | | 21.40 | % | | | 13.86 | % | | | 17.53 | % | |

| Russell MidCap Growth Index | | | 21.22 | % | | | 20.40 | % | | | 7.47 | % | | | 10.63 | % | |

| Class R | | | 43.24 | % | | | N/A | | | | N/A | | | | 22.27 | % | |

| Russell MidCap Growth Index | | | 21.22 | % | | | N/A | | | | N/A | | | | 19.89 | % | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The graph and table above do not reflect the deduction of taxes that a shareholder would have paid on fund distributions or on the redemption of fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

-11-

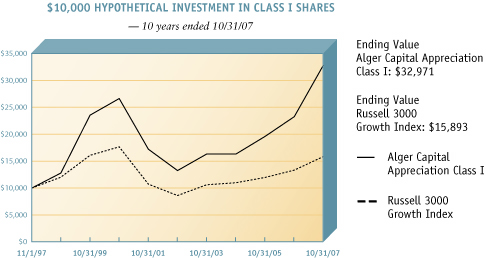

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through October 31, 2007 (Unaudited)

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger Capital Appreciation Institutional Class I shares and the Russell 3000 Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2007. Figures for the Alger Capital Appreciation Institutional Class I shares and the Russell 3000 Growth Index include reinvestment of dividends. Performance for the Alger Capital Appreciation Institutional Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON

AVERAGE ANNUAL TOTAL RETURNS

| | | 1

YEAR | | 5

YEARS | | 10

YEARS | | SINCE

INCEPTION | |

| As of 10/31/07 | |

| Class I shares (Inception 11/8/93) | | | 41.31 | % | | | 19.95 | % | | | 12.67 | % | | | 14.77 | % | |

| Russell 3000 Growth Index | | | 18.99 | % | | | 13.02 | % | | | 4.74 | % | | | 9.07 | % | |

| Class R shares (Inception 1/27/03) | | | 40.59 | % | | | N/A | | | | N/A | | | | 22.22 | % | |

| Russell 3000 Growth Index | | | 18.99 | % | | | N/A | | | | N/A | | | | 14.61 | % | |

| As of 9/30/07 | |

| Class I shares | | | 38.75 | % | | | 19.20 | % | | | 11.23 | % | | | 14.35 | % | |

| Russell 3000 Growth Index | | | 19.30 | % | | | 14.18 | % | | | 3.96 | % | | | 8.86 | % | |

| Class R shares | | | 38.04 | % | | | N/A | | | | N/A | | | | 21.04 | % | |

| Russell 3000 Growth Index | | | 19.30 | % | | | N/A | | | | N/A | | | | 14.05 | % | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The graph and table above do not reflect the deduction of taxes that a shareholder would have paid on fund distributions or on the redemption of fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

-12-

PORTFOLIO SUMMARY*

October 31, 2007 (Unaudited)

| SECTORS | | LARGECAP

GROWTH

INSTITUTIONAL

FUND | | SMALLCAP

GROWTH

INSTITUTIONAL

FUND | | MIDCAP

GROWTH

INSTITUTIONAL

FUND | | CAPITAL

APPRECIATION

INSTITUTIONAL

FUND | |

| Consumer Discretionary | | | 7.2 | % | | | 13.2 | % | | | 16.7 | % | | | 13.1 | % | |

| Consumer Staples | | | 8.7 | | | | 1.4 | | | | 1.5 | | | | 5.6 | | |

| Energy | | | 8.1 | | | | 8.8 | | | | 10.3 | | | | 7.1 | | |

| Financials | | | 8.1 | | | | 7.8 | | | | 10.9 | | | | 10.1 | | |

| Health Care | | | 16.1 | | | | 17.1 | | | | 14.3 | | | | 10.7 | | |

| Industrials | | | 10.4 | | | | 14.0 | | | | 11.5 | | | | 12.4 | | |

| Information Technology | | | 31.7 | | | | 26.4 | | | | 25.6 | | | | 32.9 | | |

| Materials | | | 3.1 | | | | 3.3 | | | | 2.7 | | | | 3.8 | | |

| Telecommunication Services | | | 0.9 | | | | 2.6 | | | | 2.8 | | | | 2.2 | | |

| Utilities | | | 1.0 | | | | 1.4 | | | | 1.3 | | | | 0.0 | | |

| Cash and Net Other Assets | | | 4.7 | | | | 4.0 | | | | 2.4 | | | | 2.1 | | |

| | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | |

* Based on net assets for each Fund.

-13-

THE ALGER INSTITUTIONAL FUNDS | ALGER LARGECAP GROWTH INSTITUTIONAL FUND

Schedule of Investments October 31, 2007

| COMMON STOCKS—95.3% | | SHARES | | VALUE | |

| AEROSPACE & DEFENSE—3.6% | |

| Boeing Company | | | 5,900 | | | $ | 581,681 | | |

| General Dynamics Corporation | | | 17,550 | | | | 1,596,348 | | |

| | | | 2,178,029 | | |

| AUTO EQUIPMENT & SERVICE—1.0% | |

| Cummins Inc. | | | 4,950 | | | | 593,802 | | |

| BEVERAGES—1.8% | |

| PepsiCo, Inc. | | | 14,650 | | | | 1,079,998 | | |

| BIOTECHNOLOGY—1.5% | |

| Celgene Corporation* | | | 5,350 | | | | 353,100 | | |

| Genentech, Inc.* | | | 7,550 | | | | 559,681 | | |

| | | | 912,781 | | |

| CHEMICALS—.7% | |

| Monsanto Company | | | 4,500 | | | | 439,335 | | |

| COMMUNICATION EQUIPMENT—5.2% | |

| Cisco Systems, Inc.* | | | 44,350 | | | | 1,466,211 | | |

| QUALCOMM Inc. | | | 17,550 | | | | 749,912 | | |

| Research In Motion Limited* | | | 7,650 | | | | 952,502 | | |

| | | | 3,168,625 | | |

| COMPUTERS & PERIPHERALS—6.6% | |

| Apple Computer, Inc.* | | | 10,300 | | | | 1,956,485 | | |

| Dell Inc.* | | | 28,600 | | | | 875,160 | | |

| Hewlett-Packard Company | | | 10,000 | | | | 516,800 | | |

| Memc Electronic Materials, Inc.* | | | 9,500 | | | | 695,590 | | |

| | | | 4,044,035 | | |

| COMPUTER SERVICES—.6% | |

| Akamai Technologies, Inc.* | | | 9,150 | | | | 358,588 | | |

| COMPUTER TECHNOLOGY—1.5% | |

| NAVTEQ* | | | 12,050 | | | | 930,260 | | |

| CONGLOMERATE—1.5% | |

| ITT Corporation | | | 13,850 | | | | 926,842 | | |

| DIVERSIFIED FINANCIAL SERVICES—1.2% | |

| Citigroup Inc. | | | 12,200 | | | | 511,180 | | |

| NYSE Euronext Inc. | | | 2,450 | | | | 229,982 | | |

| | | | 741,162 | | |

| ELECTRONICS—1.4% | |

| Nintendo Co., Ltd. ADR# | | | 10,850 | | | | 845,855 | | |

| ENERGY—.8% | |

| First Solar, Inc.* | | | 3,050 | | | | 484,370 | | |

| ENERGY EQUIPMENT & SERVICES—5.0% | |

| Cameron International Corp.* | | | 5,850 | | | | 569,556 | | |

| National-Oilwell Varco Inc.* | | | 10,450 | | | | 765,358 | | |

| Schlumberger Limited | | | 8,350 | | | | 806,360 | | |

| Transocean Inc.* | | | 7,500 | | | | 895,275 | | |

| | | | 3,036,549 | | |

-14-

THE ALGER INSTITUTIONAL FUNDS | ALGER LARGECAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| FINANCE—.8% | |

| IntercontinentalExchange Inc.* | | | 2,700 | | | $ | 481,140 | | |

| FINANCIAL SERVICES—5.2% | |

| Alibaba.com Corporation* | | | 30,400 | | | | 52,949 | | |

| AllianceBernstein Holding LP | | | 3,550 | | | | 303,276 | | |

| Bovespa Holding SA* | | | 8,050 | | | | 152,467 | | |

| CME Group Inc. | | | 1,250 | | | | 832,812 | | |

| Nymex Holdings Inc. | | | 9,250 | | | | 1,188,810 | | |

| UBS AG | | | 11,350 | | | | 609,382 | | |

| | | | 3,139,696 | | |

| FOOD & STAPLES RETAILING—2.7% | |

| Walgreen Co. | | | 29,450 | | | | 1,167,693 | | |

| Whole Foods Market, Inc. | | | 9,155 | | | | 453,539 | | |

| | | | 1,621,232 | | |

| HEALTH CARE EQUIPMENT & SUPPLIES—5.0% | |

| Beckman Coulter, Inc. | | | 5,050 | | | | 357,641 | | |

| Hologic, Inc.* | | | 11,450 | | | | 777,798 | | |

| Intuitive Surgical, Inc.* | | | 1,300 | | | | 424,931 | | |

| St. Jude Medical, Inc.* | | | 16,700 | | | | 680,191 | | |

| Zimmer Holdings, Inc.* | | | 11,200 | | | | 778,288 | | |

| | | | 3,018,849 | | |

| HEALTH CARE PROVIDERS & SERVICES—2.2% | |

| Health Net Inc.* | | | 8,850 | | | | 474,448 | | |

| Quest Diagnostics Incorporated | | | 8,200 | | | | 436,076 | | |

| UnitedHealth Group Incorporated | | | 8,350 | | | | 410,403 | | |

| | | | 1,320,927 | | |

| HOTELS, RESTAURANTS & LEISURE—2.8% | |

| Accor SA | | | 6,250 | | | | 595,613 | | |

| MGM MIRAGE* | | | 4,800 | | | | 439,728 | | |

| Starbucks Corporation* | | | 24,950 | | | | 665,666 | | |

| | | | 1,701,007 | | |

| HOUSEHOLD DURABLES—.7% | |

| Garmin Ltd. | | | 1,000 | | | | 107,400 | | |

| Harman International Industries, Incorporated | | | 3,550 | | | | 298,910 | | |

| | | | 406,310 | | |

| HOUSEHOLD PRODUCTS—2.1% | |

| Procter & Gamble Company | | | 18,650 | | | | 1,296,548 | | |

| INDUSTRIAL CONGLOMERATES—2.8% | |

| 3M Co. | | | 6,700 | | | | 578,612 | | |

| General Electric Company | | | 27,000 | | | | 1,111,320 | | |

| | | | 1,689,932 | | |

| INFORMATION TECHNOLOGY SERVICES—.8% | |

| Cognizant Technology Solutions Corporation Cl. A* | | | 11,450 | | | | 474,717 | | |

-15-

THE ALGER INSTITUTIONAL FUNDS | ALGER LARGECAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| INSURANCE—1.0% | |

| American International Group, Inc. | | | 9,450 | | | $ | 596,484 | | |

| INTERNET & CATALOG RETAIL—2.0% | |

| eBay Inc.* | | | 34,450 | | | | 1,243,645 | | |

| INTERNET SOFTWARE & SERVICES—4.5% | |

| Google Inc. Cl. A* | | | 2,350 | | | | 1,661,450 | | |

| Yahoo! Inc. * | | | 34,750 | | | | 1,080,725 | | |

| | | | 2,742,175 | | |

| MACHINERY—.7% | |

| Terex Corporation* | | | 6,050 | | | | 449,031 | | |

| MEDIA—1.4% | |

| Comcast Corporation Special Cl. A* | | | 15,700 | | | | 327,659 | | |

| Focus Media Holding Limited ADR*# | | | 8,650 | | | | 536,300 | | |

| | | | 863,959 | | |

| MEDICAL PRODUCTS—.9% | |

| Covidien Limited* | | | 13,600 | | | | 565,760 | | |

| METALS—1.8% | |

| Titanium Metals Corporation* | | | 15,500 | | | | 545,600 | | |

| Uranium One, Inc.* | | | 49,300 | | | | 544,489 | | |

| | | | 1,090,089 | | |

| METALS & MINING—2.4% | |

| Freeport-McMoRan Copper & Gold, Inc. Cl. B | | | 7,602 | | | | 894,603 | | |

| Peabody Energy Corporation | | | 10,450 | | | | 582,588 | | |

| | | | 1,477,191 | | |

| MULTILINE RETAIL—1.6% | |

| Kohl's Corporation* | | | 4,750 | | | | 261,108 | | |

| Macy's Inc. | | | 11,700 | | | | 374,751 | | |

| Penny, (JC) Co. Inc. | | | 5,850 | | | | 329,004 | | |

| | | | 964,863 | | |

| OIL & GAS—1.3% | |

| Exxon Mobil Corporation | | | 8,650 | | | | 795,713 | | |

| PHARMACEUTICALS—6.5% | |

| Abbott Laboratories | | | 16,300 | | | | 890,306 | | |

| Allergan, Inc. | | | 8,900 | | | | 601,462 | | |

| Merck & Co. Inc. | | | 14,500 | | | | 844,770 | | |

| Johnson & Johnson | | | 16,000 | | | | 1,042,720 | | |

| Schering-Plough Corporation | | | 19,700 | | | | 601,244 | | |

| | | | 3,980,502 | | |

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—3.6% | |

| Intel Corporation | | | 35,850 | | | | 964,365 | | |

| Lam Research Corporation* | | | 9,300 | | | | 466,860 | | |

| Maxim Integrated Products, Inc. | | | 16,800 | | | | 455,280 | | |

| NVIDIA Corporation* | | | 9,325 | | | | 329,919 | | |

| | | | 2,216,424 | | |

-16-

THE ALGER INSTITUTIONAL FUNDS | ALGER LARGECAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| SOFTWARE—5.3% | |

| Adobe Systems Incorporated* | | | 8,700 | | | $ | 416,730 | | |

| Microsoft Corporation | | | 54,900 | | | | 2,020,869 | | |

| TomTom NV* | | | 9,850 | | | | 784,637 | | |

| | | | 3,222,236 | | |

| SPECIALTY RETAIL—.8% | |

| Urban Outfitters, Inc.* | | | 18,854 | | | | 476,441 | | |

| TOBACCO—2.1% | |

| Altria Group, Inc. | | | 17,750 | | | | 1,294,507 | | |

| UTILITIES—1.0% | |

| Veolia Environnement ADR# | | | 7,100 | | | | 637,083 | | |

| WIRELESS TELECOMMUNICATION SERVICES—.9% | |

| NII Holdings Inc. Cl. B* | | | 9,250 | | | | 536,500 | | |

TOTAL COMMON STOCKS

(Cost $49,778,046) | | | | | | | 58,043,192 | | |

| SHORT-TERM INVESTMENTS—6.0% | | PRINCIPAL

AMOUNT | | | |

| U.S. AGENCY OBLIGATIONS | |

Federal Home Loan Banks, 4.25%, 11/1/07

(Cost $3,646,000) | | $ | 3,646,000 | | | | 3,646,000 | | |

Total Investments

(Cost $53,424,046)(a) | | | 101.3 | % | | | 61,689,192 | | |

| Liabilities in Excess of Other Assets | | | (1.3 | ) | | | (815,429 | ) | |

| NET ASSETS | | | 100.0 | % | | $ | 60,873,763 | | |

* Non-income producing security.

# American Depositary Receipts.

(a) At October 31, 2007, the net unrealized appreciation of investments, based on cost for federal income tax purposes of $53,502,840 amounted to $8,186,352 which consisted of aggregate gross unrealized appreciation of $9,492,013 and aggregate gross unrealized depreciation of $1,305,661.

See Notes to Financial Statements.

-17-

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALLCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments October 31, 2007

| COMMON STOCKS—96.0% | | SHARES | | VALUE | |

| AEROSPACE & DEFENSE—3.3% | |

| BE Aerospace, Inc.* | | | 260,355 | | | $ | 12,942,247 | | |

| Esterline Technologies Corporation* | | | 205,125 | | | | 11,236,747 | | |

| SI International Inc.* | | | 248,780 | | | | 7,018,084 | | |

| | | | 31,197,078 | | |

| AIRLINES—.7% | |

| AirTran Holdings, Inc.* | | | 631,840 | | | | 6,577,454 | | |

| AUTO COMPONENTS—1.2% | |

| LKQ Corporation* | | | 293,570 | | | | 11,320,059 | | |

| AUTO EQUIPMENT & SERVICE—.9% | |

| Tenneco Inc.* | | | 290,905 | | | | 8,904,602 | | |

| BIOTECHNOLOGY—3.9% | |

| BioMarin Pharmaceutical Inc.* | | | 209,700 | | | | 5,814,981 | | |

| InterMune, Inc.* | | | 221,855 | | | | 4,419,352 | | |

| Neurocrine Biosciences, Inc.* | | | 429,000 | | | | 3,968,250 | | |

| Onyx Pharmaceuticals, Inc.* | | | 190,900 | | | | 8,916,939 | | |

| Progenics Pharmaceuticals, Inc.* | | | 296,850 | | | | 6,875,046 | | |

| Regeneron Pharmaceuticals, Inc.* | | | 278,390 | | | | 6,124,580 | | |

| Theravance, Inc.* | | | 28,700 | | | | 718,074 | | |

| | | | 36,837,222 | | |

| BUSINESS SERVICES—.8% | |

| TeleTech Holdings Inc.* | | | 295,250 | | | | 7,360,583 | | |

| CASINOS & RESORTS—1.3% | |

| Bally Technologies Inc.* | | | 303,600 | | | | 12,244,188 | | |

| CAPITAL MARKETS—1.2% | |

| Greenhill & Co., Inc. | | | 149,860 | | | | 11,086,643 | | |

| CHEMICALS—1.0% | |

| Zoltek Companies, Inc.* | | | 203,280 | | | | 8,995,140 | | |

| COMMERCIAL BANKS—2.9% | |

| Boston Private Financial Holdings, Inc. | | | 287,805 | | | | 8,277,272 | | |

| First Midwest Bancorp., Inc. | | | 196,350 | | | | 6,613,068 | | |

| Signature Bank* | | | 251,110 | | | | 8,575,407 | | |

| Wintrust Financial Corporation | | | 108,040 | | | | 3,969,390 | | |

| | | | 27,435,137 | | |

| COMMERCIAL SERVICES & SUPPLIES—1.3% | |

| FTI Consulting, Inc.* | | | 218,510 | | | | 11,865,093 | | |

| COMMUNICATION EQUIPMENT—4.1% | |

| Foundry Networks, Inc.* | | | 375,350 | | | | 7,934,899 | | |

| NICE Systems Ltd. ADR*# | | | 291,100 | | | | 11,478,073 | | |

| Polycom, Inc.* | | | 376,255 | | | | 10,527,615 | | |

| Sonus Networks, Inc.* | | | 1,238,485 | | | | 8,545,547 | | |

| | | | 38,486,134 | | |

-18-

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALLCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| COMMUNICATION TECHNOLOGY—1.5% | |

| Novatel Wireless, Inc.* | | | 372,600 | | | $ | 9,687,600 | | |

| Time Warner Telecom Inc. Cl. A* | | | 194,450 | | | | 4,519,018 | | |

| | | | 14,206,618 | | |

| COMPUTER SERVICES—4.0% | |

| ANSYS, Inc.* | | | 315,150 | | | | 12,230,971 | | |

| Digital River, Inc.* | | | 133,650 | | | | 7,091,469 | | |

| GSI Commerce, Inc.* | | | 407,350 | | | | 11,605,401 | | |

| Internap Network Services Corporation* | | | 380,205 | | | | 6,334,215 | | |

| | | | 37,262,056 | | |

| COMPUTERS & PERIPHERALS—1.2% | |

| Synaptics Incorporated* | | | 215,150 | | | | 11,693,403 | | |

| COMPUTER TECHNOLOGY—1.0% | |

| Atheros Communications* | | | 259,485 | | | | 9,107,923 | | |

| CONSTRUCTION & ENGINEERING—1.2% | |

| URS Corporation* | | | 190,755 | | | | 11,790,567 | | |

| CONTAINERS & PACKAGING—.9% | |

| Clarcor Inc. | | | 236,150 | | | | 8,610,029 | | |

| CORRECTIONAL FACILITIES—1.2% | |

| The Geo Group Inc.* | | | 363,950 | | | | 11,511,738 | | |

| DRUGS & PHARMACEUTICALS—.8% | |

| United Therapeutics Corporation* | | | 113,865 | | | | 7,792,921 | | |

| ELECTRIC SERVICES—1.4% | |

| ITC Holdings Corporation | | | 227,160 | | | | 13,002,638 | | |

| ELECTRONICS: SEMI-CONDUCTORS/COMPONENTS—1.0% | |

| Mellanox Technologies Ltd.* | | | 403,400 | | | | 9,524,274 | | |

| ENERGY—.7% | |

| JA Solar Holdings Co. Ltd. ADR*# | | | 118,350 | | | | 6,816,960 | | |

| ENERGY EQUIPMENT & SERVICES—3.2% | |

| Dril-Quip Inc.* | | | 176,720 | | | | 9,424,478 | | |

| Horizon Offshore, Inc.* | | | 408,855 | | | | 6,582,566 | | |

| North American Energy Partner* | | | 425,450 | | | | 7,896,352 | | |

| T-3 Energy Services, Inc.* | | | 132,450 | | | | 6,294,024 | | |

| | | | 30,197,420 | | |

| ENGINEERING—1.0% | |

| Aecom Technology Corp.* | | | 278,400 | | | | 9,401,568 | | |

| FINANCIAL INFORMATION SERVICES—1.0% | |

| GFI Group Inc.* | | | 108,670 | | | | 9,380,394 | | |

| FINANCIAL SERVICES—1.6% | |

| Cohen & Steers, Inc. | | | 187,700 | | | | 7,057,520 | | |

| Heartland Payment Systems, Inc. | | | 278,100 | | | | 8,343,000 | | |

| | | | 15,400,520 | | |

-19-

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALLCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| FOOD & BEVERAGES—1.4% | |

| Hain Celestial Group Inc. (The)* | | | 370,565 | | | $ | 12,992,009 | | |

| HEALTH CARE EQUIPMENT & SUPPLIES—3.8% | |

| ArthroCare Corporation* | | | 102,250 | | | | 6,629,890 | | |

| Hologic, Inc.* | | | 168,400 | | | | 11,439,412 | | |

| Illumina, Inc.* | | | 184,530 | | | | 10,361,360 | | |

| Thoratec Corporation* | | | 374,400 | | | | 7,476,768 | | |

| | | | 35,907,430 | | |

| HEALTH CARE PROVIDERS & SERVICES—2.5% | |

| Parexel International Corporation* | | | 261,030 | | | | 12,007,380 | | |

| Psychiatric Solutions, Inc.* | | | 286,420 | | | | 11,342,232 | | |

| | | | 23,349,612 | | |

| HOTELS, RESTAURANTS & LEISURE—.6% | |

| Orient-Express Hotels Ltd. Cl. A. | | | 84,550 | | | | 5,478,840 | | |

| INSURANCE—1.0% | |

| First Mercury Financial Corporation* | | | 446,800 | | | | 9,896,620 | | |

| INTERNET & CATALOG RETAIL—1.3% | |

| Priceline.com Incorporated* | | | 127,160 | | | | 11,838,596 | | |

| INTERNET SOFTWARE & SERVICES—3.8% | |

| Acme Packet, Inc.* | | | 451,650 | | | | 6,485,694 | | |

| Allscripts Healthcare Solutions, Inc.* | | | 398,900 | | | | 11,049,530 | | |

| DealerTrack Holdings Inc.* | | | 238,345 | | | | 11,700,356 | | |

| Omniture Inc.* | | | 199,005 | | | | 6,798,011 | | |

| | | | 36,033,591 | | |

| IT SERVICES—1.1% | |

| Wright Express Corp.* | | | 264,285 | | | | 10,227,830 | | |

| LEISURE EQUIPMENT & PRODUCTS—.9% | |

| LIFE TIME FITNESS, Inc.* | | | 144,195 | | | | 8,743,985 | | |

| MACHINERY—2.4% | |

| Actuant Corporation Cl. A | | | 151,180 | | | | 10,428,396 | | |

| Bucyrus International, Inc. Cl. A | | | 147,080 | | | | 12,134,100 | | |

| | | | 22,562,496 | | |

| MANUFACTURING—1.1% | |

| Silgan Holdings Inc. | | | 190,550 | | | | 10,398,314 | | |

| MEDIA—1.0% | |

| NeuStar, Inc. Cl. A* | | | 271,860 | | | | 9,297,612 | | |

| MEDICAL DEVICES—.5% | |

| Dexcom Inc.* | | | 555,350 | | | | 5,164,755 | | |

| MEDICAL PRODUCTS—2.6% | |

| Inverness Medical Innovations, Inc.* | | | 159,900 | | | | 9,608,391 | | |

| Omrix Biopharmaceuticals, Inc.* | | | 265,250 | | | | 9,241,310 | | |

| Savient Pharmaceuticals Inc.* | | | 376,150 | | | | 5,296,192 | | |

| | | | 24,145,893 | | |

-20-

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALLCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| MEDICAL TECHNOLOGY—.8% | |

| Acorda Therapeutics Inc.* | | | 350,950 | | | $ | 7,113,756 | | |

| METALS—3.1% | |

| RBC Bearings, Inc.* | | | 266,990 | | | | 10,730,328 | | |

| Thompson Creek Metals Co.,Inc* | | | 457,750 | | | | 12,038,917 | | |

| Uranium One, Inc.* | | | 617,800 | | | | 6,823,230 | | |

| | | | 29,592,475 | | |

| OIL & GAS—2.2% | |

| Carrizo Oil & Gas, Inc.* | | | 211,060 | | | | 10,846,373 | | |

| Mariner Energy Inc.* | | | 411,000 | | | | 10,275,000 | | |

| | | | 21,121,373 | | |

| OIL AND GAS EXPLORATION SERVICES—1.1% | |

| Petrobank Energy and Resources Ltd.* | | | 209,160 | | | | 10,345,681 | | |

| OIL: CRUDE PRODUCERS—1.5% | |

| Concho Resources Inc.* | | | 395,610 | | | | 7,710,439 | | |

| CVR Energy, Inc.* | | | 280,550 | | | | 6,396,540 | | |

| | | | 14,106,979 | | |

| PHARMACEUTICAL PREPARATIONS—1.1% | |

| Adams Respiratory Therapeutics, Inc.* | | | 231,055 | | | | 10,152,557 | | |

| PRINTING—.9% | |

| VistaPrint Limited* | | | 171,950 | | | | 8,179,662 | | |

| REAL ESTATE—.4% | |

| HFF Inc.* | | | 360,250 | | | | 3,620,512 | | |

| RESTAURANTS—.6% | |

| McCormick & Schmick's Seafood Restaurants, Inc.* | | | 306,000 | | | | 5,195,880 | | |

| RETAIL—1.6% | |

| bebe Stores, Inc. | | | 500,900 | | | | 6,967,519 | | |

| Phillips-Van Heusen Corporation | | | 167,070 | | | | 7,985,946 | | |

| | | | 14,953,465 | | |

| SAVINGS & LOANS—.5% | |

| FirstFed Financial Corp.* | | | 114,150 | | | | 4,883,337 | | |

| SEMICONDUCTOR CAPITAL EQUIPMENT—1.6% | |

| FormFactor Inc.* | | | 179,840 | | | | 7,033,542 | | |

| SiRF Technology Holdings, Inc.* | | | 269,065 | | | | 8,020,828 | | |

| | | | 15,054,370 | | |

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—2.7% | |

| Cirrus Logic, Inc.* | | | 896,350 | | | | 5,512,552 | | |

| ON Semiconductor Corporation* | | | 885,450 | | | | 9,031,590 | | |

| Tessera Technologies Inc.* | | | 269,260 | | | | 10,283,039 | | |

| | | | 24,827,181 | | |

-21-

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALLCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| SOFTWARE—4.9% | |

| Concur Technologies, Inc.* | | | 197,100 | | | $ | 7,103,484 | | |

| Solera Holdings Inc.* | | | 503,500 | | | | 10,830,285 | | |

| Synchronoss Technologies Inc.* | | | 242,450 | | | | 9,698,000 | | |

| Tibco Software Inc.* | | | 598,030 | | | | 5,489,915 | | |

| VeriFone Holdings Inc.* | | | 266,695 | | | | 13,182,734 | | |

| | | | 46,304,418 | | |

| SPECIALTY RETAIL—1.2% | |

| Carter's, Inc.* | | | 298,800 | | | | 6,597,504 | | |

| DSW Inc. Cl. A* | | | 226,840 | | | | 5,103,900 | | |

| | | | 11,701,404 | | |

| TEXTILES & APPAREL—1.1% | |

| Iconix Brand Group, Inc.* | | | 468,025 | | | | 10,694,371 | | |

| TEXTILES, APPAREL & LUXURY GOODS—1.2% | |

| Deckers Outdoor Corporation* | | | 81,350 | | | | 11,371,916 | | |

| WIRELESS TELECOMMUNICATION SERVICES—1.2% | |

| SBA Communications Corporation Cl. A* | | | 312,775 | | | | 11,134,790 | | |

TOTAL COMMON STOCKS

(Cost $761,785,501) | | | | | | | 904,400,072 | | |

| SHORT-TERM INVESTMENTS—5.2% | | PRINCIPAL

AMOUNT | | | |

| U.S. AGENCY OBLIGATIONS | |

Federal Home Loan Banks, 4.25%,11/1/07

(Cost $48,534,000) | | $ | 48,534,000 | | | | 48,534,000 | | |

Total Investments

(Cost $810,319,501)(a) | | | 101.2 | % | | | 952,934,072 | | |

| Liabilities in Excess of Other Assets | | | (1.2 | ) | | | (11,089,717 | ) | |

| NET ASSETS | | | 100.0 | % | | $ | 941,844,355 | | |

* Non-income producing security.

# American Depositary Receipts.

(a) At October 31, 2007, the net unrealized appreciation of investments, based on cost for federal income tax purposes of $811,547,851 amounted to $141,386,221 which consisted of aggregate gross unrealized appreciation of $164,596,926 and aggregate gross unrealized depreciation of $23,210,705.

See Notes to Financial Statements.

-22-

THE ALGER INSTITUTIONAL FUNDS | ALGER MIDCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments October 31, 2007

| COMMON STOCKS—97.6% | | SHARES | | VALUE | |

| AEROSPACE & DEFENSE—1.6% | |

| BE Aerospace, Inc.* | | | 666,090 | | | $ | 33,111,334 | | |

| AGRICULTURE—.8% | |

| Mosaic Co.* | | | 239,000 | | | | 16,682,200 | | |

| APPAREL—.4% | |

| J Crew Group Inc.* | | | 224,700 | | | | 8,403,780 | | |

| AUTO COMPONENTS—1.0% | |

| LKQ Corporation* | | | 573,400 | | | | 22,110,304 | | |

| BIOTECHNOLOGY—2.7% | |

| Affymetrix Inc.* | | | 990,850 | | | | 25,227,041 | | |

| ImClone Systems Incorporated* | | | 433,800 | | | | 18,718,470 | | |

| Neurocrine Biosciences, Inc.* | | | 103,500 | | | | 957,375 | | |

| Onyx Pharmaceuticals, Inc.* | | | 231,200 | | | | 10,799,352 | | |

| | | | 55,702,238 | | |

| BUSINESS SERVICES—.3% | |

| Endeavor Acquisition Corp.* | | | 495,100 | | | | 6,089,730 | | |

| CAPITAL MARKETS—.9% | |

| Affiliated Managers Group, Inc.* | | | 145,975 | | | | 19,203,011 | | |

| CASINOS & RESORTS—1.4% | |

| Bally Technologies Inc.* | | | 717,600 | | | | 28,940,808 | | |

| COMMERCIAL BANKS—.5% | |

| Boston Private Financial Holdings, Inc. | | | 367,100 | | | | 10,557,796 | | |

| COMMERCIAL SERVICES & SUPPLIES—.5% | |

| Monster Worldwide Inc.* | | | 274,200 | | | | 11,127,036 | | |

| COMMUNICATION EQUIPMENT—1.7% | |

| Research In Motion Limited* | | | 170,095 | | | | 21,178,528 | | |

| NICE Systems Ltd. ADR*# | | | 354,400 | | | | 13,973,992 | | |

| | | | 35,152,520 | | |

| COMPUTER TECHNOLOGY—2.6% | |

| Atheros Communications* | | | 860,635 | | | | 30,208,288 | | |

| NAVTEQ* | | | 327,585 | | | | 25,289,562 | | |

| | | | 55,497,850 | | |

| COMPUTERS & PERIPHERALS—4.4% | |

| Apple Computer, Inc.* | | | 329,900 | | | | 62,664,505 | | |

| Memc Electronic Materials, Inc.* | | | 318,165 | | | | 23,296,041 | | |

| SanDisk Corporation* | | | 143,600 | | | | 6,375,840 | | |

| | | | 92,336,386 | | |

| CONGLOMERATE—1.2% | |

| ITT Corporation | | | 377,000 | | | | 25,228,840 | | |

| CONSTRUCTION & ENGINEERING—2.6% | |

| Chicago Bridge & Iron Company N.V. | | | 591,800 | | | | 29,590,000 | | |

| McDermott International, Inc.* | | | 424,080 | | | | 25,894,325 | | |

| | | | 55,484,325 | | |

-23-

THE ALGER INSTITUTIONAL FUNDS | ALGER MIDCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| DRUGS & PHARMACEUTICALS—.8% | |

| United Therapeutics Corporation* | | | 237,055 | | | $ | 16,224,044 | | |

| ELECTRIC SERVICES—.5% | |

| ITC Holdings Corporation | | | 181,600 | | | | 10,394,784 | | |

| ELECTRONICS—2.0% | |

| Nintendo Co., Ltd. ADR# | | | 533,730 | | | | 41,609,057 | | |

| ELECTRONICS: SEMI-CONDUCTORS/COMPONENTS—.3% | |

| Spreadtrum Communications, Inc. ADR*# | | | 487,400 | | | | 6,297,208 | | |

| ENERGY—2.3% | |

| First Solar, Inc.* | | | 116,700 | | | | 18,533,127 | | |

| JA Solar Holdings Co. Ltd. ADR*# | | | 515,000 | | | | 29,664,000 | | |

| | | | 48,197,127 | | |

| ENERGY EQUIPMENT & SERVICES—7.4% | |

| Cameron International Corp.* | | | 375,230 | | | | 36,532,393 | | |

| Diamond Offshore Drilling Inc. | | | 251,600 | | | | 28,488,668 | | |

| FMC Technologies, Inc.* | | | 317,000 | | | | 19,219,710 | | |

| National-Oilwell Varco Inc.* | | | 350,970 | | | | 25,705,043 | | |

| Transocean Inc.* | | | 224,400 | | | | 26,786,628 | | |

| Weatherford International Ltd.* | | | 285,500 | | | | 18,531,805 | | |

| | | | 155,264,247 | | |

| FINANCE—1.5% | |

| IntercontinentalExchange Inc.* | | | 180,300 | | | | 32,129,460 | | |

| FINANCIAL INFORMATION SERVICES—.7% | |

| GFI Group Inc.* | | | 171,100 | | | | 14,769,352 | | |

| FINANCIAL SERVICES—7.6% | |

| Alibaba.com Corporation* | | | 1,037,600 | | | | 1,807,246 | | |

| AllianceBernstein Holding LP | | | 286,300 | | | | 24,458,609 | | |

| Bovespa Holding SA* | | | 823,500 | | | | 15,597,129 | | |

| CME Group Inc. | | | 39,600 | | | | 26,383,500 | | |

| Genpact Limited* | | | 1,315,755 | | | | 21,052,080 | | |

| Lazard Ltd. | | | 397,913 | | | | 19,975,233 | | |

| Nymex Holdings Inc. | | | 398,000 | | | | 51,150,960 | | |

| | | | 160,424,757 | | |

| FOOD & BEVERAGES—1.0% | |

| Yum! Brands, Inc. | | | 526,400 | | | | 21,198,128 | | |

| FOOD & STAPLES RETAILING—1.5% | |

| Whole Foods Market, Inc. | | | 630,900 | | | | 31,254,786 | | |

| HEALTH CARE EQUIPMENT & SUPPLIES—4.3% | |

| Hologic, Inc.* | | | 462,800 | | | | 31,438,004 | | |

| Intuitive Surgical, Inc.* | | | 61,700 | | | | 20,167,879 | | |

| Smith & Nephew Plc. ADR# | | | 79,900 | | | | 5,414,823 | | |

| St. Jude Medical, Inc.* | | | 509,100 | | | | 20,735,643 | | |

| Zimmer Holdings, Inc.* | | | 177,900 | | | | 12,362,271 | | |

| | | | 90,118,620 | | |

-24-

THE ALGER INSTITUTIONAL FUNDS | ALGER MIDCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| HEALTH CARE PROVIDERS & SERVICES—3.7% | |

| Health Net Inc.* | | | 571,900 | | | $ | 30,659,559 | | |

| McKesson Corporation | | | 348,000 | | | | 23,002,800 | | |

| Quest Diagnostics Incorporated | | | 441,300 | | | | 23,468,334 | | |

| | | | 77,130,693 | | |

| HOTELS, RESTAURANTS & LEISURE—4.1% | |

| Accor SA | | | 327,200 | | | | 31,181,516 | | |

| MGM MIRAGE* | | | 203,900 | | | | 18,679,279 | | |

| Orient-Express Hotels Ltd. Cl. A. | | | 323,360 | | | | 20,953,728 | | |

| Scientific Games Corporation* | | | 440,110 | | | | 15,909,977 | | |

| | | | 86,724,500 | | |

| HOUSEHOLD DURABLES—.5% | |

| Harman International Industries, Incorporated | | | 120,800 | | | | 10,171,360 | | |

| INFORMATION TECHNOLOGY SERVICES—1.0% | |

| Cognizant Technology Solutions Corporation Cl. A* | | | 510,900 | | | | 21,181,914 | | |

| INTERNET SOFTWARE & SERVICES—2.9% | |

| Allscripts Healthcare Solutions, Inc.* | | | 1,160,255 | | | | 32,139,063 | | |

| DealerTrack Holdings Inc.* | | | 172,572 | | | | 8,471,559 | | |

| SINA Corp.* | | | 361,600 | | | | 20,730,528 | | |

| | | | 61,341,150 | | |

| LEISURE & ENTERTAINMENT—.5% | |

| Vail Resorts Inc.* | | | 169,900 | | | | 10,311,231 | | |

| LEISURE EQUIPMENT & PRODUCTS—.3% | |

| UbiSoft Entertainment SA* | | | 66,900 | | | | 5,486,923 | | |

| MACHINERY—1.0% | |

| Oshkosh Truck Corporation | | | 376,800 | | | | 20,422,560 | | |

| MEDICAL PRODUCTS—1.0% | |

| Metabolix, Inc.* | | | 705,500 | | | | 20,381,895 | | |

| METALS—2.8% | |

| Thompson Creek Metals Co.,Inc* | | | 383,600 | | | | 10,088,757 | | |

| Titanium Metals Corporation* | | | 829,400 | | | | 29,194,880 | | |

| Uranium One, Inc.* | | | 1,777,175 | | | | 19,627,832 | | |

| | | | 58,911,469 | | |

| METALS & MINING—.6% | |

| Paladin Resources Limited* | | | 1,572,480 | | | | 12,249,619 | | |

| OIL AND GAS EXPLORATION SERVICES—1.1% | |

| Petrobank Energy and Resources Ltd.* | | | 449,400 | | | | 22,228,672 | | |

| OIL: CRUDE PRODUCERS—.3% | |

| Concho Resources Inc.* | | | 377,100 | | | | 7,349,679 | | |

| PHARMACEUTICALS—.5% | |

| Pharmion Corp.* | | | 200,500 | | | | 9,648,060 | | |

-25-

THE ALGER INSTITUTIONAL FUNDS | ALGER MIDCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| PHOTOGRAPHY—.8% | |

| Shutterfly, Inc.* | | | 511,400 | | | $ | 17,065,418 | | |

| REAL ESTATE—.4% | |

| DuPont Fabros Technology Inc.* | | | 427,300 | | | | 9,178,404 | | |

| RETAIL—1.9% | |

| Sothebys Holdings Inc., Cl. A | | | 742,100 | | | | 40,199,557 | | |

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—5.8% | |

| Cree, Inc.* | | | 702,000 | | | | 19,656,000 | | |

| Lam Research Corporation* | | | 397,900 | | | | 19,974,580 | | |

| NVIDIA Corporation* | | | 590,500 | | | | 20,891,890 | | |

| ON Semiconductor Corporation* | | | 1,689,325 | | | | 17,231,115 | | |

| Tessera Technologies Inc.* | | | 510,245 | | | | 19,486,257 | | |

| Varian Semiconductor Equipment Associates, Inc.* | | | 555,200 | | | | 25,550,304 | | |

| | | | 122,790,146 | | |

| SPECIALTY RETAIL—4.2% | |

| DSW Inc. Cl. A* | | | 189,600 | | | | 4,266,000 | | |

| Gamestop Corp. Cl. A* | | | 707,516 | | | | 41,899,098 | | |

| PETSMART, Inc. | | | 689,600 | | | | 20,653,520 | | |

| Urban Outfitters, Inc.* | | | 847,500 | | | | 21,416,325 | | |

| | | | 88,234,943 | | |

| SOFTWARE—5.0% | |

| Activision, Inc.* | | | 842,180 | | | | 19,917,557 | | |

| Net 1 UEPS Technologies, Inc.* | | | 892,517 | | | | 28,578,394 | | |

| Solera Holdings Inc.* | | | 1,204,700 | | | | 25,913,097 | | |

| Synchronoss Technologies Inc.* | | | 223,300 | | | | 8,932,000 | | |

| TomTom NV* | | | 287,600 | | | | 22,909,803 | | |

| | | | 106,250,851 | | |

| TEXTILES & APPAREL—.8% | |

| Iconix Brand Group, Inc.* | | | 763,800 | | | | 17,452,830 | | |

| TRANSPORTATION—2.3% | |

| Norfolk Southern Corporation | | | 246,700 | | | | 12,742,055 | | |

| Textron Inc. | | | 517,500 | | | | 35,816,175 | | |

| | | | 48,558,230 | | |

| UTILITIES—.8% | |

| Veolia Environnement ADR# | | | 192,880 | | | | 17,307,122 | | |

| WIRELESS TELECOMMUNICATION SERVICES—2.8% | |

| NII Holdings Inc. Cl. B* | | | 535,945 | | | | 31,084,810 | | |

| SBA Communications Corporation Cl. A* | | | 773,965 | | | | 27,553,154 | | |

| | | | 58,637,964 | | |

TOTAL COMMON STOCKS

(Cost $1,691,796,938) | | | | | | | 2,052,724,918 | | |

-26-

THE ALGER INSTITUTIONAL FUNDS | ALGER MIDCAP GROWTH INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| SHORT-TERM INVESTMENTS—2.7% | | PRINCIPAL

AMOUNT | | VALUE | |

| U.S. AGENCY OBLIGATIONS | |

Federal Home Loan Banks, 4.25%, 11/1/07

(Cost $56,630,000) | | $ | 56,630,000 | | | $ | 56,630,000 | | |

Total Investments

(Cost $1,748,426,938)(a) | | | 100.3 | % | | | 2,109,354,918 | | |

| Liabilities in Excess of Other Assets | | | (0.3 | ) | | | (7,151,457 | ) | |

| NET ASSETS | | | 100.0 | % | | $ | 2,102,203,461 | | |

* Non-income producing security.

# American Depositary Receipts.

(a) At October 31, 2007, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $1,763,415,328 amounted to $345,939,590 which consisted of aggregate gross unrealized appreciation of $376,126,118 and aggregate gross unrealized depreciation of $30,186,528.

See Notes to Financial Statements.

-27-

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments October 31, 2007

| COMMON STOCKS—97.6% | | SHARES | | VALUE | |

| AEROSPACE & DEFENSE—3.7% | |

| Boeing Company | | | 48,800 | | | $ | 4,811,192 | | |

| General Dynamics Corporation | | | 184,500 | | | | 16,782,120 | | |

| | | | 21,593,312 | | |

| AUTO COMPONENTS—.2% | |

| LKQ Corporation* | | | 28,200 | | | | 1,087,392 | | |

| AUTO EQUIPMENT & SERVICES—3.1% | |

| Cummins Inc. | | | 150,600 | | | | 18,065,976 | | |

| BIOTECHNOLOGY—1.0% | |

| ImClone Systems Incorporated* | | | 46,400 | | | | 2,002,160 | | |

| InterMune, Inc.* | | | 33,000 | | | | 657,360 | | |

| Onyx Pharmaceuticals, Inc.* | | | 72,000 | | | | 3,363,120 | | |

| | | | 6,022,640 | | |

| BUSINESS SERVICES—.6% | |

| Endeavor Acquisition Corp.* | | | 300,500 | | | | 3,696,150 | | |

| CAPITAL MARKETS—.6% | |

| Goldman Sachs Group, Inc. | | | 14,600 | | | | 3,619,632 | | |

| CASINOS & RESORTS—1.8% | |

| Bally Technologies Inc.* | | | 262,400 | | | | 10,582,592 | | |

| CHEMICALS—.6% | |

| Celanese Corp., Series A | | | 82,600 | | | | 3,465,896 | | |

| COMMERCIAL SERVICES & SUPPLIES—.5% | |

| Monster Worldwide Inc.* | | | 74,500 | | | | 3,023,210 | | |

| COMMUNICATION EQUIPMENT—1.3% | |

| Research In Motion Limited* | | | 20,700 | | | | 2,577,357 | | |

| Sonus Networks, Inc.* | | | 677,400 | | | | 4,674,060 | | |

| | | | 7,251,417 | | |

| COMPUTER SERVICES—2.0% | |

| Satyam Computer Services- ADR# | | | 138,700 | | | | 4,209,545 | | |

| Switch and Data Inc.* | | | 22,200 | | | | 436,896 | | |

| Tele Atlas NV* | | | 168,200 | | | | 6,711,453 | | |

| | | | 11,357,894 | | |

| COMPUTER TECHNOLOGY—3.1% | |

| Atheros Communications* | | | 307,180 | | | | 10,782,018 | | |

| NAVTEQ* | | | 92,100 | | | | 7,110,120 | | |

| | | | 17,892,138 | | |

| COMPUTERS & PERIPHERALS—5.1% | |

| Apple Computer, Inc.* | | | 107,200 | | | | 20,362,640 | | |

| Hewlett-Packard Company | | | 25,800 | | | | 1,333,344 | | |

| Memc Electronic Materials, Inc.* | | | 70,400 | | | | 5,154,688 | | |

| Network Appliance, Inc.* | | | 90,600 | | | | 2,852,994 | | |

| | | | 29,703,666 | | |

-28-

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| CONTAINERS & PACKAGING—2.7% | |

| Pactiv Corporation* | | | 571,400 | | | $ | 15,696,358 | | |

| DRUGS & PHARMACEUTICALS—.9% | |

| United Therapeutics Corporation* | | | 75,200 | | | | 5,146,688 | | |

| ENERGY—2.6% | |

| First Solar, Inc.* | | | 5,600 | | | | 889,336 | | |

| JA Solar Holdings Co. Ltd. ADR*# | | | 248,000 | | | | 14,284,800 | | |

| | | | 15,174,136 | | |

| ENERGY EQUIPMENT & SERVICES—4.3% | |

| National-Oilwell Varco Inc.* | | | 26,200 | | | | 1,918,888 | | |

| Transocean Inc.* | | | 121,500 | | | | 14,503,455 | | |

| Weatherford International Ltd.* | | | 131,900 | | | | 8,561,629 | | |

| | | | 24,983,972 | | |

| FINANCE—.4% | |

| IntercontinentalExchange Inc. * | | | 13,800 | | | | 2,459,160 | | |

| FINANCIAL SERVICES—7.5% | |

| Alibaba.com Corporation* | | | 283,100 | | | | 493,091 | | |

| AllianceBernstein Holding LP | | | 58,500 | | | | 4,997,655 | | |

| CME Group Inc. | | | 17,100 | | | | 11,392,875 | | |

| ICICI Bank Limited ADR# | | | 28,200 | | | | 1,958,208 | | |

| Lazard Ltd. | | | 121,600 | | | | 6,104,320 | | |

| Nymex Holdings Inc. | | | 98,900 | | | | 12,710,628 | | |

| UBS AG | | | 105,100 | | | | 5,642,819 | | |

| | | | 43,299,596 | | |

| FOOD & STAPLES RETAILING—1.3% | |

| CVS Caremark Corporation | | | 179,200 | | | | 7,485,184 | | |

| HEALTH CARE EQUIPMENT & SUPPLIES—2.7% | |

| Hologic, Inc.* | | | 129,248 | | | | 8,779,817 | | |

| Illumina, Inc.* | | | 70,100 | | | | 3,936,115 | | |

| Intuitive Surgical, Inc.* | | | 7,750 | | | | 2,533,243 | | |

| | | | 15,249,175 | | |

| HEALTH CARE PROVIDERS & SERVICES—1.3% | |

| Cardinal Health, Inc. | | | 110,200 | | | | 7,496,906 | | |

| HOTELS, RESTAURANTS & LEISURE—5.9% | |

| Accor SA | | | 181,800 | | | | 17,325,182 | | |

| Ctrip.com International Ltd. ADR# | | | 51,100 | | | | 2,879,996 | | |

| MGM MIRAGE * | | | 51,800 | | | | 4,745,398 | | |

| Penn National Gaming, Inc.* | | | 121,100 | | | | 7,477,925 | | |

| Starbucks Corporation* | | | 64,000 | | | | 1,707,520 | | |

| | | | 34,136,021 | | |

| HOUSEHOLD PRODUCTS—.4% | |

| Procter & Gamble Company | | | 35,402 | | | | 2,461,147 | | |

-29-

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| INDUSTRIAL CONGLOMERATES—.9% | |

| General Electric Company | | | 124,100 | | | $ | 5,107,956 | | |

| INFORMATION TECHNOLOGY SERVICES—.9% | |

| Cognizant Technology Solutions Corporation Cl. A* | | | 120,300 | | | | 4,987,638 | | |

| INSURANCE—.7% | |

| American International Group, Inc. | | | 59,200 | | | | 3,736,704 | | |

| INTERNET & CATALOG RETAIL—2.7% | |

| eBay Inc.* | | | 427,900 | | | | 15,447,190 | | |

| INTERNET SOFTWARE & SERVICES—7.2% | |

| DealerTrack Holdings Inc.* | | | 85,475 | | | | 4,195,968 | | |

| Google Inc. Cl. A* | | | 24,100 | | | | 17,038,700 | | |

| SINA Corp.* | | | 166,200 | | | | 9,528,246 | | |

| Yahoo! Inc.* | | | 352,500 | | | | 10,962,750 | | |

| | | | 41,725,664 | | |

| LEISURE EQUIPMENT & PRODUCTS—.2% | |

| Smith & Wesson Holding Corporation* | | | 77,800 | | | | 940,602 | | |

| MACHINERY—1.5% | |

| Oshkosh Truck Corporation | | | 146,400 | | | | 7,934,880 | | |

| Terex Corporation* | | | 12,100 | | | | 898,062 | | |

| | | | 8,832,942 | | |

| MEDIA—2.0% | |

| Dolby Laboratories Inc. Cl. A* | | | 108,700 | | | | 4,506,702 | | |

| DreamWorks Animation SKG, Inc. Cl. A* | | | 73,400 | | | | 2,389,904 | | |

| Focus Media Holding Limited ADR*# | | | 56,300 | | | | 3,490,600 | | |

| NeuStar, Inc. Cl. A* | | | 28,600 | | | | 978,120 | | |

| | | | 11,365,326 | | |

| MEDICAL PRODUCTS—1.7% | |

| Inverness Medical Innovations, Inc.* | | | 142,000 | | | | 8,532,780 | | |

| Northstar Neuroscience, Inc.* | | | 80,610 | | | | 1,068,083 | | |

| | | | 9,600,863 | | |

| METALS—.2% | |

| Uranium One, Inc.* | | | 116,300 | | | | 1,284,464 | | |

| METALS & MINING—1.1% | |

| Freeport-McMoRan Copper & Gold, Inc. Cl. B | | | 24,800 | | | | 2,918,464 | | |

| Paladin Resources Limited* | | | 419,600 | | | | 3,268,684 | | |

| | | | 6,187,148 | | |

| OIL & GAS—1.3% | |

| Exterran Holdings Inc.* | | | 53,583 | | | | 4,511,646 | | |

| Range Resources Corporation | | | 29,300 | | | | 1,316,449 | | |

| Warren Resources Inc.* | | | 91,900 | | | | 1,395,042 | | |

| | | | 7,223,137 | | |

-30-

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments (Continued) October 31, 2007

| COMMON STOCKS—(CONT.) | | SHARES | | VALUE | |

| OIL AND GAS EXPLORATION SERVICES—.8% | |

| Petrobank Energy and Resources Ltd.* | | | 86,700 | | | $ | 4,288,442 | | |

| PHARMACEUTICAL PREPARATIONS—1.0% | |

| Adams Respiratory Therapeutics, Inc.* | | | 129,400 | | | | 5,685,836 | | |

| PHARMACEUTICALS—2.2% | |

| Abbott Laboratories | | | 157,300 | | | | 8,591,726 | | |

| Pharmion Corp.* | | | 82,700 | | | | 3,979,524 | | |

| | | | 12,571,250 | | |

| REAL ESTATE—.3% | |

| Digital Realty Trust, Inc. | | | 41,400 | | | | 1,821,186 | | |

| RETAIL—1.4% | |

| Sothebys Holdings Inc., Cl. A | | | 149,000 | | | | 8,071,330 | | |

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—5.4% | |

| Intel Corporation | | | 381,200 | | | | 10,254,280 | | |

| Lam Research Corporation* | | | 74,300 | | | | 3,729,860 | | |

| ON Semiconductor Corporation* | | | 577,300 | | | | 5,888,460 | | |

| Tessera Technologies Inc.* | | | 214,400 | | | | 8,187,936 | | |

| Varian Semiconductor Equipment Associates, Inc.* | | | 68,900 | | | | 3,170,778 | | |

| | | | 31,231,314 | | |

| SOFTWARE—5.5% | |

| Adobe Systems Incorporated* | | | 92,400 | | | | 4,425,960 | | |

| Microsoft Corporation | | | 136,700 | | | | 5,031,927 | | |

| Net 1 UEPS Technologies, Inc.* | | | 227,600 | | | | 7,287,752 | | |

| Solera Holdings Inc.* | | | 284,900 | | | | 6,128,199 | | |

| TomTom NV* | | | 110,000 | | | | 8,762,442 | | |

| | | | 31,636,280 | | |

| TEXTILES & APPAREL—.8% | |

| Iconix Brand Group, Inc.* | | | 206,200 | | | | 4,711,670 | | |

| TEXTILES, APPAREL & LUXURY GOODS—.3% | |