UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

The Alger Institutional Funds

(Exact name of registrant as specified in charter)

100 Pearl Street, New York, New York 10004

Registrant's telephone number, including area code:

Date of reporting period:

Item 1. Report to Stockholders.

(a) The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

Alger Capital Appreciation Institutional Fund

Class I / ALARX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Capital Appreciation Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Capital Appreciation Institutional Fund

(Class I / ALARX) | $160 | 1.24% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Capital Appreciation Institutional Fund Class I returned 57.90% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Amazon.com, Inc.; and Natera, Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Humana Inc.; Snowflake, Inc.; Schlumberger Ltd.; HubSpot, Inc.; and Snap, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

Fund Performance

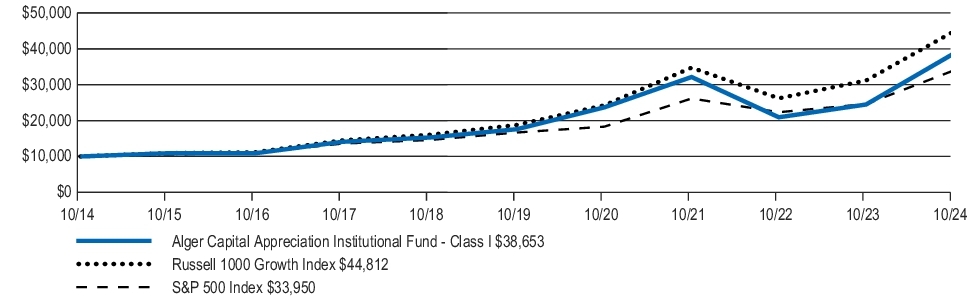

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class I shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Capital Appreciation Institutional Fund Class I | 57.90% | 17.04% | 14.48% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 16.18% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $2,120,603,780 |

| Total number of portfolio holdings1 | 70 |

| Portfolio turnover rate as of the end of the reporting period | 59.80% |

| Total advisory fees paid | $17,002,298 |

1 | Excludes Money Market Funds. |

| Communication Services | 15.2% |

| Consumer Discretionary | 12.8% |

| Energy | 0.5% |

| Financials | 3.9% |

| Healthcare | 9.3% |

| Industrials | 8.4% |

| Information Technology | 47.3% |

| Materials | 0.2% |

| Real Estate | 0.8% |

| Utilities | 1.6% |

| Short-Term Investments and Other Net Assets | 0.0% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Capital Appreciation Institutional Fund

Class R / ACARX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Capital Appreciation Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Capital Appreciation Institutional Fund

(Class R / ACARX) | $217 | 1.69% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Capital Appreciation Institutional Fund Class R returned 57.21% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Amazon.com, Inc.; and Natera, Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Humana Inc.; Snowflake, Inc.; Schlumberger Ltd.; HubSpot, Inc.; and Snap, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

Fund Performance

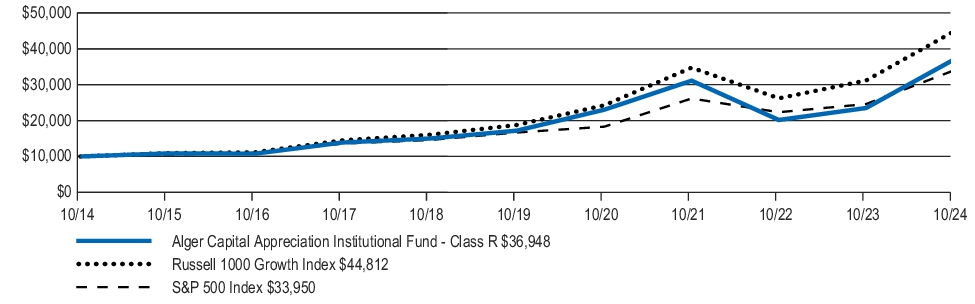

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class R shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Capital Appreciation Institutional Fund Class R | 57.21% | 16.53% | 13.96% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 16.18% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $2,120,603,780 |

| Total number of portfolio holdings1 | 70 |

| Portfolio turnover rate as of the end of the reporting period | 59.80% |

| Total advisory fees paid | $17,002,298 |

1 | Excludes Money Market Funds. |

| Communication Services | 15.2% |

| Consumer Discretionary | 12.8% |

| Energy | 0.5% |

| Financials | 3.9% |

| Healthcare | 9.3% |

| Industrials | 8.4% |

| Information Technology | 47.3% |

| Materials | 0.2% |

| Real Estate | 0.8% |

| Utilities | 1.6% |

| Short-Term Investments and Other Net Assets | 0.0% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Capital Appreciation Institutional Fund

Class Y / ACAYX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Capital Appreciation Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Capital Appreciation Institutional Fund

(Class Y / ACAYX) | $111 | 0.86% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Capital Appreciation Institutional Fund Class Y returned 58.48% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Amazon.com, Inc.; and Natera, Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Humana Inc.; Snowflake, Inc.; Schlumberger Ltd.; HubSpot, Inc.; and Snap, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

Fund Performance

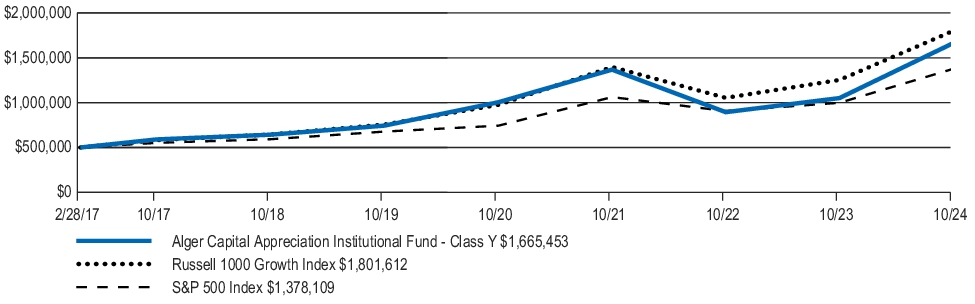

The following graph compares the initial and subsequent account values at the end of each of the most recently completed annual periods for the life of Class Y shares of the Fund since its inception. The graph assumes a $500,000 initial investment at net asset value at the inception date of the Fund in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $500,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | Since Inception

2/28/17 |

| Alger Capital Appreciation Institutional Fund Class Y | 58.48% | 17.51% | 16.98% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 18.19% |

| S&P 500 Index | 38.02% | 15.27% | 14.13% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $2,120,603,780 |

| Total number of portfolio holdings1 | 70 |

| Portfolio turnover rate as of the end of the reporting period | 59.80% |

| Total advisory fees paid | $17,002,298 |

1 | Excludes Money Market Funds. |

| Communication Services | 15.2% |

| Consumer Discretionary | 12.8% |

| Energy | 0.5% |

| Financials | 3.9% |

| Healthcare | 9.3% |

| Industrials | 8.4% |

| Information Technology | 47.3% |

| Materials | 0.2% |

| Real Estate | 0.8% |

| Utilities | 1.6% |

| Short-Term Investments and Other Net Assets | 0.0% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Capital Appreciation Institutional Fund

Class Z-2 / ACIZX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Capital Appreciation Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Capital Appreciation Institutional Fund

(Class Z-2 / ACIZX) | $114 | 0.88% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Capital Appreciation Institutional Fund Class Z-2 returned 58.44% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Amazon.com, Inc.; and Natera, Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Humana Inc.; Snowflake, Inc.; Schlumberger Ltd.; HubSpot, Inc.; and Snap, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

Fund Performance

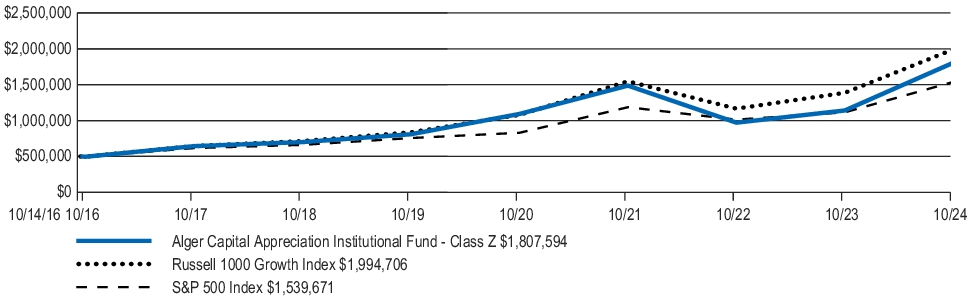

The following graph compares the initial and subsequent account values at the end of each of the most recently completed annual periods for the life of Class Z-2 shares of the Fund since its inception. The graph assumes a $500,000 initial investment at net asset value at the inception date of the Fund in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $500,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | Since Inception

10/14/16 |

| Alger Capital Appreciation Institutional Fund Class Z-2 | 58.44% | 17.44% | 17.32% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 18.19% |

| S&P 500 Index | 38.02% | 15.27% | 14.13% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $2,120,603,780 |

| Total number of portfolio holdings1 | 70 |

| Portfolio turnover rate as of the end of the reporting period | 59.80% |

| Total advisory fees paid | $17,002,298 |

1 | Excludes Money Market Funds. |

| Communication Services | 15.2% |

| Consumer Discretionary | 12.8% |

| Energy | 0.5% |

| Financials | 3.9% |

| Healthcare | 9.3% |

| Industrials | 8.4% |

| Information Technology | 47.3% |

| Materials | 0.2% |

| Real Estate | 0.8% |

| Utilities | 1.6% |

| Short-Term Investments and Other Net Assets | 0.0% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

Effective March 1, 2024, Alger Management has contractually agreed to waive fees or to reimburse Fund expenses (excluding custody fees, acquired fund fees and expenses, dividend expense on short sales, net borrowing costs, interest, taxes, brokerage and extraordinary expenses, to the extent applicable) through October 31, 2025 to the extent necessary to limit the Other Expenses of the Class Z-2 Shares of the Fund to 0.05% of the class’s average daily net assets. On October 22, 2024, the Board approved that any fees incurred as a result of the joint special meeting of shareholders would be excluded from the expense reimbursement.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Focus Equity Fund

Class A / ALAFX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Focus Equity Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Focus Equity Fund

(Class A / ALAFX) | $124 | 0.95% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Focus Equity Fund Class A returned 60.77%, excluding sales load, for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Natera, Inc.; and AppLovin Corp. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Snowflake, Inc.; ASML Holding; Schlumberger Ltd.; EOG Resources, Inc.; and Fluence Energy, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

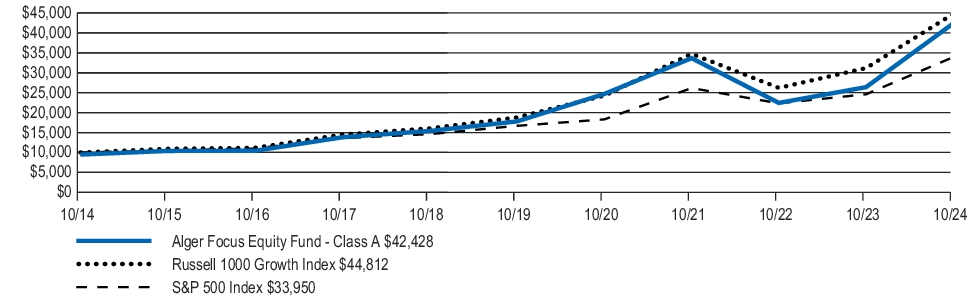

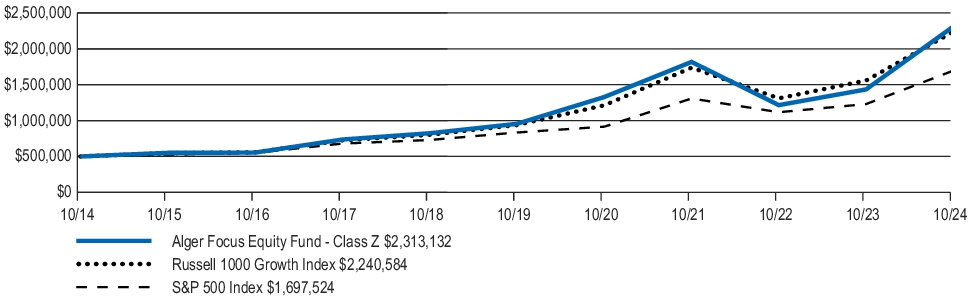

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class A shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Focus Equity Fund Class A | 52.32% | 17.71% | 15.55% |

| Alger Focus Equity Fund Class A—excluding sales load | 60.77% | 18.99% | 16.17% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 16.18% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $1,791,352,839 |

| Total number of portfolio holdings1 | 51 |

| Portfolio turnover rate as of the end of the reporting period | 92.43% |

| Total advisory fees paid | $7,683,585 |

1 | Excludes Money Market Funds. |

| Communication Services | 14.0% |

| Consumer Discretionary | 12.1% |

| Energy | 1.0% |

| Financials | 3.1% |

| Healthcare | 7.4% |

| Industrials | 10.8% |

| Information Technology | 43.7% |

| Materials | 0.3% |

| Real Estate | 0.9% |

| Utilities | 2.3% |

| Short-Term Investments and Other Net Assets | 4.4% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Focus Equity Fund

Class C / ALCFX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Focus Equity Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Focus Equity Fund

(Class C / ALCFX) | $223 | 1.72% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Focus Equity Fund Class C returned 59.55%, excluding contingent deferred sales charge for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Natera, Inc.; and AppLovin Corp. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Snowflake, Inc.; ASML Holding; Schlumberger Ltd.; EOG Resources, Inc.; and Fluence Energy, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

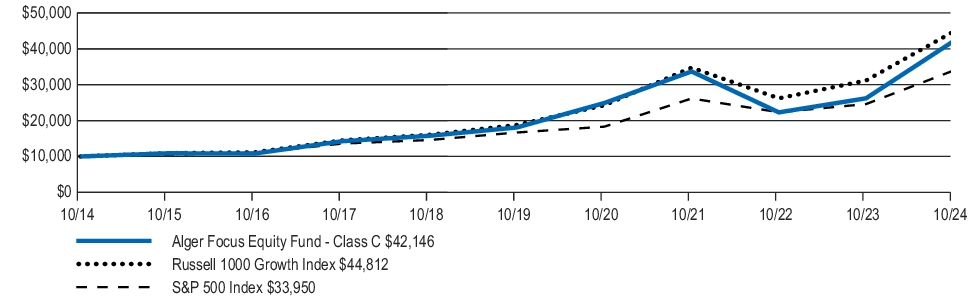

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class C shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Focus Equity Fund Class C | 58.55% | 18.08% | 15.47% |

| Alger Focus Equity Fund Class C—excluding contingent deferred sales charges | 59.55% | 18.08% | 15.47% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 16.18% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $1,791,352,839 |

| Total number of portfolio holdings1 | 51 |

| Portfolio turnover rate as of the end of the reporting period | 92.43% |

| Total advisory fees paid | $7,683,585 |

1 | Excludes Money Market Funds. |

| Communication Services | 14.0% |

| Consumer Discretionary | 12.1% |

| Energy | 1.0% |

| Financials | 3.1% |

| Healthcare | 7.4% |

| Industrials | 10.8% |

| Information Technology | 43.7% |

| Materials | 0.3% |

| Real Estate | 0.9% |

| Utilities | 2.3% |

| Short-Term Investments and Other Net Assets | 4.4% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Focus Equity Fund

Class I / ALGRX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Focus Equity Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Focus Equity Fund

(Class I / ALGRX) | $123 | 0.94% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Focus Equity Fund Class I returned 60.84% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Natera, Inc.; and AppLovin Corp. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Snowflake, Inc.; ASML Holding; Schlumberger Ltd.; EOG Resources, Inc.; and Fluence Energy, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

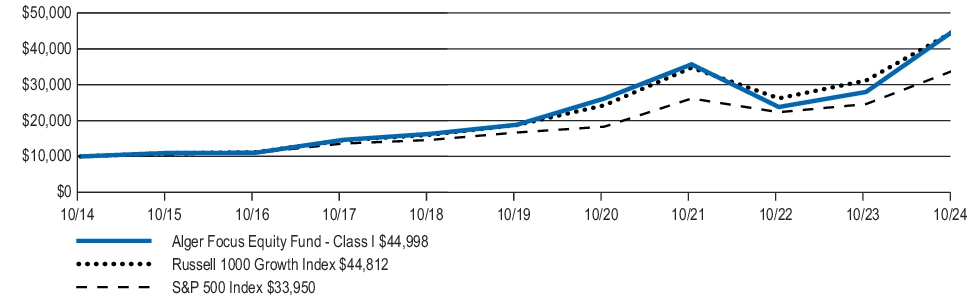

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class I shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Focus Equity Fund Class I | 60.84% | 19.03% | 16.23% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 16.18% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $1,791,352,839 |

| Total number of portfolio holdings1 | 51 |

| Portfolio turnover rate as of the end of the reporting period | 92.43% |

| Total advisory fees paid | $7,683,585 |

1 | Excludes Money Market Funds. |

| Communication Services | 14.0% |

| Consumer Discretionary | 12.1% |

| Energy | 1.0% |

| Financials | 3.1% |

| Healthcare | 7.4% |

| Industrials | 10.8% |

| Information Technology | 43.7% |

| Materials | 0.3% |

| Real Estate | 0.9% |

| Utilities | 2.3% |

| Short-Term Investments and Other Net Assets | 4.4% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Focus Equity Fund

Class Y / ALGYX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Focus Equity Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Focus Equity Fund

(Class Y / ALGYX) | $76 | 0.58% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Focus Equity Fund Class Y returned 61.36% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Natera, Inc.; and AppLovin Corp. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Snowflake, Inc.; ASML Holding; Schlumberger Ltd.; EOG Resources, Inc.; and Fluence Energy, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

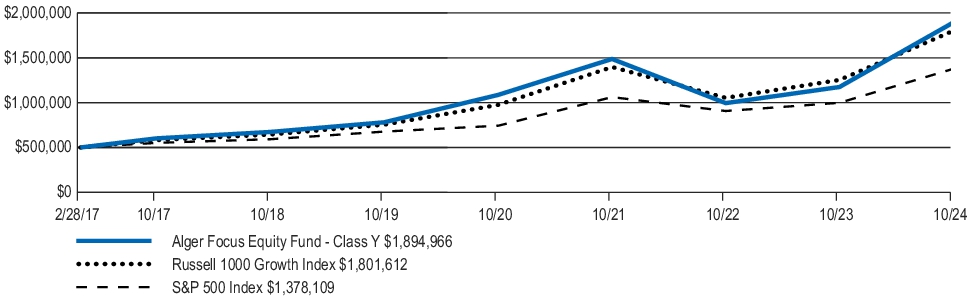

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed annual periods for the life of Class Y shares of the Fund since its inception. The graph assumes a $500,000 initial investment at net asset value at the inception date of the Fund in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $500,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | Since Inception

2/28/17 |

| Alger Focus Equity Fund Class Y | 61.36% | 19.40% | 18.97% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 18.19% |

| S&P 500 Index | 38.02% | 15.27% | 14.13% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $1,791,352,839 |

| Total number of portfolio holdings1 | 51 |

| Portfolio turnover rate as of the end of the reporting period | 92.43% |

| Total advisory fees paid | $7,683,585 |

1 | Excludes Money Market Funds. |

| Communication Services | 14.0% |

| Consumer Discretionary | 12.1% |

| Energy | 1.0% |

| Financials | 3.1% |

| Healthcare | 7.4% |

| Industrials | 10.8% |

| Information Technology | 43.7% |

| Materials | 0.3% |

| Real Estate | 0.9% |

| Utilities | 2.3% |

| Short-Term Investments and Other Net Assets | 4.4% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

Effective March 1, 2024, Alger Management has contractually agreed to waive and/or reimburse Fund expenses (excluding custody fees, acquired fund fees and expenses, dividend expense on short sales, net borrowing costs, interest, taxes, brokerage and extraordinary expenses, to the extent applicable) through October 31, 2025 to the extent necessary to limit other expenses and any other applicable share class-specific expenses of the Class Y Shares of the Fund to 0.06% of the class’s average daily net assets. On October 22, 2024, the Board approved that any fees incurred as a result of the joint special meeting of shareholders would be excluded from the expense reimbursement.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Focus Equity Fund

Class Z / ALZFX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Focus Equity Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Focus Equity Fund

(Class Z / ALZFX) | $82 | 0.63% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Focus Equity Fund Class Z returned 61.29% for the fiscal twelve-month period ended October 31, 2024, compared to the 43.77% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Communication Services. The largest sector overweight was Industrials and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. NVIDIA Corp.; Meta Platforms Inc.; Microsoft Corp.; Natera, Inc.; and AppLovin Corp. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Staples and Financials sectors were the largest detractors from relative performance. Snowflake, Inc.; ASML Holding; Schlumberger Ltd.; EOG Resources, Inc.; and Fluence Energy, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class Z shares of the Fund. The graph assumes a $500,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $500,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Focus Equity Fund Class Z | 61.29% | 19.37% | 16.55% |

| Russell 1000 Growth Index | 43.77% | 19.00% | 16.18% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $1,791,352,839 |

| Total number of portfolio holdings1 | 51 |

| Portfolio turnover rate as of the end of the reporting period | 92.43% |

| Total advisory fees paid | $7,683,585 |

1 | Excludes Money Market Funds. |

| Communication Services | 14.0% |

| Consumer Discretionary | 12.1% |

| Energy | 1.0% |

| Financials | 3.1% |

| Healthcare | 7.4% |

| Industrials | 10.8% |

| Information Technology | 43.7% |

| Materials | 0.3% |

| Real Estate | 0.9% |

| Utilities | 2.3% |

| Short-Term Investments and Other Net Assets | 4.4% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

Effective March 1, 2024, Alger Management has contractually agreed to waive and/or reimburse Fund expenses (excluding custody fees, acquired fund fees and expenses, dividend expense on short sales, net borrowing costs, interest, taxes, brokerage and extraordinary expenses, to the extent applicable) through October 31, 2025 to the extent necessary to limit other expenses and any other applicable share class-specific expenses of the Class Z Shares of the Fund to 0.11% of the class’s average daily net assets. On October 22, 2024, the Board approved that any fees incurred as a result of the joint special meeting of shareholders would be excluded from the expense reimbursement.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Mid Cap Growth Institutional Fund

Class I / ALMRX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Mid Cap Growth Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Mid Cap Growth Institutional Fund

(Class I / ALMRX) | $154 | 1.31% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Mid Cap Growth Institutional Fund Class I returned 35.83% for the fiscal twelve-month period ended October 31, 2024, compared to the 38.67% return of the Russell Midcap Growth Index. During the reporting period, the largest sector weightings were Information Technology and Industrials. The largest sector overweight was Information Technology and the largest sector underweight was Financials.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. Natera, Inc.; Vertiv Holdings Co.; Spotify Technology; AppLovin Corp.; and Constellation Software Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Discretionary and Financials sectors were the largest detractors from relative performance. Super Micro Computer, Inc.; Lattice Semiconductor Corp.; Wayfair, Inc.; Five Below, Inc.; and Paycom Software, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

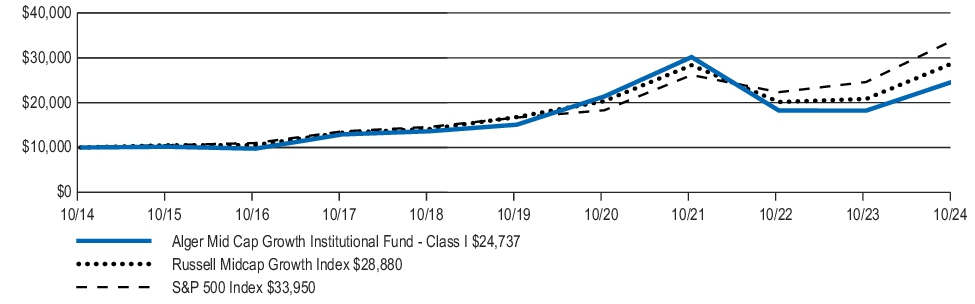

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class I shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Mid Cap Growth Institutional Fund Class I | 35.83% | 10.40% | 9.48% |

| Russell Midcap Growth Index | 38.67% | 11.46% | 11.19% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $65,737,384 |

| Total number of portfolio holdings1 | 64 |

| Portfolio turnover rate as of the end of the reporting period | 56.01% |

| Total advisory fees paid | $491,165 |

1 | Excludes Money Market Funds. |

| Communication Services | 7.8% |

| Consumer Discretionary | 10.8% |

| Consumer Staples | 0.4% |

| Energy | 2.2% |

| Financials | 10.1% |

| Healthcare | 10.8% |

| Industrials | 23.1% |

| Information Technology | 29.9% |

| Materials | 1.8% |

| Real Estate | 3.8% |

| Short-Term Investments and Other Net Assets | (0.7)% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

Effective February 29, 2024, Fred Alger Management, LLC has contractually agreed to waive and/or reimburse Fund expenses (excluding custody fees, acquired fund fees and expenses, dividend expense on short sales, net borrowing costs, interest, taxes, brokerage and extraordinary expenses, to the extent applicable) through October 31, 2025 to the extent necessary to limit other expenses and any other applicable share class-specific expenses of the Class I Shares of the Fund to 0.48% of the class’s average daily net assets.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Mid Cap Growth Institutional Fund

Class R / AGIRX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Mid Cap Growth Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Mid Cap Growth Institutional Fund

(Class R / AGIRX) | $217 | 1.85% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Mid Cap Growth Institutional Fund Class R returned 35.12% for the fiscal twelve-month period ended October 31, 2024, compared to the 38.67% return of the Russell Midcap Growth Index. During the reporting period, the largest sector weightings were Information Technology and Industrials. The largest sector overweight was Information Technology and the largest sector underweight was Financials.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. Natera, Inc.; Vertiv Holdings Co.; Spotify Technology; AppLovin Corp.; and Constellation Software Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Discretionary and Financials sectors were the largest detractors from relative performance. Super Micro Computer, Inc.; Lattice Semiconductor Corp.; Wayfair, Inc.; Five Below, Inc.; and Paycom Software, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |

| Federal Reserve Rate Cuts | Positive | In September 2024, the Federal Reserve initiated a rate-cutting cycle with a 50-basis point reduction, aiming to bolster economic growth amid a strong but softening labor market and easing inflation, creating a favorable backdrop for equities. |

| Rising Geopolitical Tensions | Negative | Geopolitical conflicts and trade disputes created some uncertainty ahead of the 2024 U.S. presidential election. |

| Weakening U.S. Labor Market | Negative | In August 2024, equity markets experienced a brief sell-off due to growth concerns following a weaker-than-expected July payrolls report, which raised fears that the Federal Reserve might be slow to respond to slowing economic conditions. The unemployment rate increased to 4.3%, triggering the Sahm rule—a recession indicator that signals a likely recession when the three-month moving average of the unemployment rate rises by at least 50 basis points from its twelve-month low. |

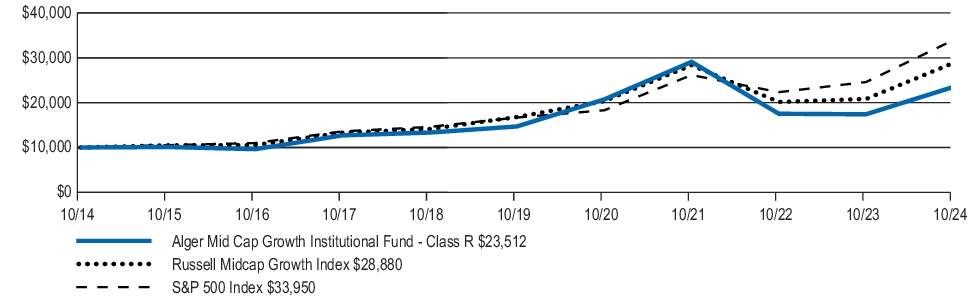

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed ten fiscal years of Class R shares of the Fund. The graph assumes a $10,000 initial investment at the beginning of the first annual period in an appropriate, broad-based securities market index and a more narrowly based index that reflects the market sector in which the Fund invests for the same period.

INITIAL INVESTMENT OF $10,000

| Average Annual Total Returns (As of October 31, 2024) | 1 Year | 5 Years | 10 Years |

| Alger Mid Cap Growth Institutional Fund Class R | 35.12% | 9.86% | 8.93% |

| Russell Midcap Growth Index | 38.67% | 11.46% | 11.19% |

| S&P 500 Index | 38.02% | 15.27% | 13.00% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

Visit https://www.alger.com/Pages/StrategyFinder.aspx?vehicle=mf for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. All performance figures assume reinvestment of distributions.

Key Fund Statistics

The following table outlines key fund statistics as of the fiscal year ended October 31, 2024.

| Fund net assets | $65,737,384 |

| Total number of portfolio holdings1 | 64 |

| Portfolio turnover rate as of the end of the reporting period | 56.01% |

| Total advisory fees paid | $491,165 |

1 | Excludes Money Market Funds. |

| Communication Services | 7.8% |

| Consumer Discretionary | 10.8% |

| Consumer Staples | 0.4% |

| Energy | 2.2% |

| Financials | 10.1% |

| Healthcare | 10.8% |

| Industrials | 23.1% |

| Information Technology | 29.9% |

| Materials | 1.8% |

| Real Estate | 3.8% |

| Short-Term Investments and Other Net Assets | (0.7)% |

| 100.0% |

Material and Other Fund Changes

Effective January 29, 2024, the Fund's custodian and administrator transitioned from Brown Brothers Harriman & Company to The Bank of New York.

On August 16, 2024, at a joint special meeting of shareholders, shareholders of the Fund elected three new trustees and one current trustee to the Board.

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 at https://connect.rightprospectus.com/Alger or upon request at (800) 992-3863.

Availability of Additional Information

Householding

To reduce expenses, only one copy of the most recent financial reports and prospectus may be mailed to households, even if more than one person in a household holds shares of a Fund. Call an Alger Funds Representative at (800) 992-3863 if you need additional copies of financial reports or prospectuses, or download them at https://connect.rightprospectus.com/Alger. If you do not want the mailing of these documents to be combined with those for other members of your household, contact your broker-dealer or other financial intermediary or Alger Institutional Funds in writing at Alger Family of Funds, c/o UMB Fund Services, Inc. 235 W. Galena Street Milwaukee, WI 53212.

Alger Mid Cap Growth Institutional Fund

Class Z-2 / ALMZX

Annual SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about the Alger Mid Cap Growth Institutional Fund (“Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://connect.rightprospectus.com/Alger. You can also request a copy of the annual report by contacting us at (800) 992-3863.

This report describes material changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class/Ticker) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Alger Mid Cap Growth Institutional Fund

(Class Z-2 / ALMZX) | $118 | 1.00% |

Management's Discussion of Fund Performance

What impacted Fund performance over the reporting period?

The Alger Mid Cap Growth Institutional Fund Class Z-2 returned 36.22% for the fiscal twelve-month period ended October 31, 2024, compared to the 38.67% return of the Russell Midcap Growth Index. During the reporting period, the largest sector weightings were Information Technology and Industrials. The largest sector overweight was Information Technology and the largest sector underweight was Financials.

Contributors to Performance

The Information Technology and Health Care sectors provided the largest contributions to relative performance. Natera, Inc.; Vertiv Holdings Co.; Spotify Technology; AppLovin Corp.; and Constellation Software Inc. were the top five contributors to absolute performance.

Detractors from Performance

The Consumer Discretionary and Financials sectors were the largest detractors from relative performance. Super Micro Computer, Inc.; Lattice Semiconductor Corp.; Wayfair, Inc.; Five Below, Inc.; and Paycom Software, Inc. were the top five detractors from absolute performance.

| U.S. FACTOR | IMPACT | SUMMARY |

| Resilient Corporate Earnings | Positive | Strong corporate earnings were driven by profit margin improvement and robust consumer spending. Themes such as AI proliferation, waning cloud optimization pressure, and profit margin expansion from increased productivity and expense control also supported market sentiment. |