Exhibit 99.2

|

TEEKAY CORPORATION Q4-2015 EARNINGS AND BUSINESS OUTLOOK PRESENTATION

February 18, 2016

|

Forward Looking Statements

This presentation contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934, as amended) which reflect management’s current views with respect to certain future events and performance, including statements regarding: Teekay Offshore’s and Teekay LNG’s use of internally generated cash flow to contribute to the funding of growth projects, including the impact on their future available distributable cash flow per unit; the potential for future dividend and distribution changes by Teekay Parent or any of the Daughter Entities; the impact of growth projects on Teekay Offshore’s and Teekay LNG’s future cash flows; the pending sale of Teekay Offshore’s two conventional tankers, including the impact on future liquidity; Teekay Group’s expected fixed future revenues and weighted average remaining contract lengths; the expected redelivery date and potential redeployment of the Varg FPSO; the timing of newbuilding, conversion and upgrade vessel or offshore unit deliveries and commencement of their respective charter contracts; the timing of the Bahrain project start-up and timing of commencement of related contracts; the capacity, total cost and financing for the Bahrain project; any recovery of deferred charter amounts relating to Teekay LNG’s two 52 percent-owned LNG carriers on charter to the Yemen LNG project, and any recommencement of such project; Teekay Tankers’ future dividend payout ratio; the impact on Teekay Tankers’ debt maturity profile and financial flexibility as a result of the new $900 million long-term debt facility; potential access to bank, bond and preferred equity; the value of Teekay Parent’s FPSO units, VLCC tanker, and joint ventures and other investments. The following factors are among those that could cause actual results to differ materially from the forward-looking statements, which involve risks and uncertainties, and that should be considered in evaluating any such statement: changes in production of, or demand for oil, petroleum products, LNG and LPG, either generally or in particular regions; greater or less than anticipated levels of newbuilding orders or greater or less than anticipated rates of vessel scrapping; changes in trading patterns significantly affecting overall vessel tonnage requirements; changes in applicable industry laws and regulations and the timing of implementation of new laws and regulations; changes in the typical seasonal variations in tanker charter rates; changes in the offshore production of oil or demand for shuttle tankers, FSOs, FPSOs, UMS, and towage vessels; changes in oil production and the impact on the Company’s tankers and offshore units; fluctuations in global oil prices; trends in prevailing charter rates for the Company’s vessels and offshore unit contract renewals; the potential for early termination of long-term contracts and inability of the Company to renew or replace long-term contracts; the inability of charterers to make future charter payments; potential shipyard and project construction delays, newbuilding specification changes or cost overruns; costs relating to projects; potential delays in the sale of Teekay Offshore’s two conventional tankers; failure by Teekay Offshore to secure a contract for the Varg FPSO; delays in commencement of operations of FPSO and FSO units at designated fields; changes in the Company’s expenses; factors affecting the resumption of the LNG plant in Yemen; the inability of Teekay LNG to collect the deferred charter payments from the Yemen LNG project; the Company and its publicly-traded subsidiaries’ ability to raise adequate financing for existing growth projects, to refinance future debt maturities and for other financing requirements; the amount of future cash distributions by the Company’s Daughter Entities to the Company, including any failure of the respective Board of Directors of the general partners of Teekay Offshore and Teekay LNG to approve future cash distribution increases; failure by the Company’s Board of Directors to approve future dividend increases; Teekay Tankers actual dividend payout ratio determined by its Board of Directors; conditions in the United States capital markets; and other factors discussed in Teekay’s filings from time to time with the SEC, including its Report on Form 20-F for the fiscal year ended December 31, 2014 and Form 6-K for the quarters ended March 31, 2015, June 30, 2015 and September 30, 2015. The Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any such statement is based.

2

|

Recent Highlights

Generated consolidated CFVO1 of $401.4 million in Q4-15, an increase of 30 percent from Q4-14

Generated consolidated CFVO of $1.4 billion in fiscal 2015, up 35 percent over 2014

Reported adjusted net income attributable to shareholders1 of $29.8 million, or $0.41 per share, in Q4-15 and $68.1 million, or $0.94 per share, in fiscal year 2015

In December 2015, announced quarterly cash dividends temporarily reduced to $0.055 per share (previously $0.55 per share), concurrent with temporary reduction in distribution payments received from its two MLPs

o MLPs reallocating internally generated cash flows to fund profitable growth projects

1) See the Q4-15 earnings release for explanations and reconciliations of these non-GAAP financial measures to the most directly comparable financial measures under GAAP.

3

|

Recent Daughter Highlights

Teekay LNG Partners

Generated CFVO1 of $121.1 million in Q4-15, an increase of 6% from Q3-15 Declared Q4-15 distribution of $0.14 per unit – $3.8M to Teekay Parent

Secured first LNG regasification project utilizing an existing MEGI LNG newbuilding and a 30% interest in an LNG regasification plant in Bahrain under 20-year contracts

Teekay Offshore Partners

Generated CFVO1 of $172.9 million in Q4-15, an increase of 20% from Q3-15 Declared Q4-15 distribution of $0.11 per unit – $4.4M to Teekay Parent

Completed the sale of two conventional tankers and agreed to sell the two remaining conventional tankers creating approximately $60M of liquidity

Teekay Tankers

Generated free cash flow1 of $74.0 million, or $0.48 per share, in Q4-15, up 25% from Q3-15 Implemented new variable dividend policy in December 2015, under which Teekay Tankers intends to pay out 30 to 50 percent of its quarterly adjusted net income1 Declared Q4-15 dividend of $0.12 per share, an increase of 300% from Q3-15 – $4.8M to Teekay Parent Refinanced majority of fleet through new five-year $900 million debt facility Acquired two purpose-built lightering Aframaxes for en bloc price of $80 million to bolster strategic U.S. Gulf presence

1) See Teekay Offshore’s, Teekay LNG’s and Teekay Tankers’ Q4-15 earnings releases for explanations and reconciliations of these non-GAAP financial measures to the most directly comparable financial measures under GAAP.

4

|

Strategic Rationale for Dividend Reductions

In December 2015, Teekay Parent dividend reduced by 90% to reflect temporary distribution decreases at two MLPs (TGP and TOO)

Disconnect between capital markets (high correlation to weak oil prices) and the relative stability/growth profile of TGP and TOO cash flows made equity capital uneconomical

Significant decline in MLP equity values made capital markets prohibitively expensive

Internally generated cash flows the lowest cost source of equity capital for TGP and TOO

Distribution reductions enable TGP and TOO to retain ~$450M of cash flow per annum

Avoids permanently dilutive equity issuances

Provides greater funding certainty for growth capex and deleveraging

Facilitates access to bank, bond and preferred equity markets

Will result in higher DCF per unit in the future as projects deliver

Creates greater capacity to increase distributions in the future

5

|

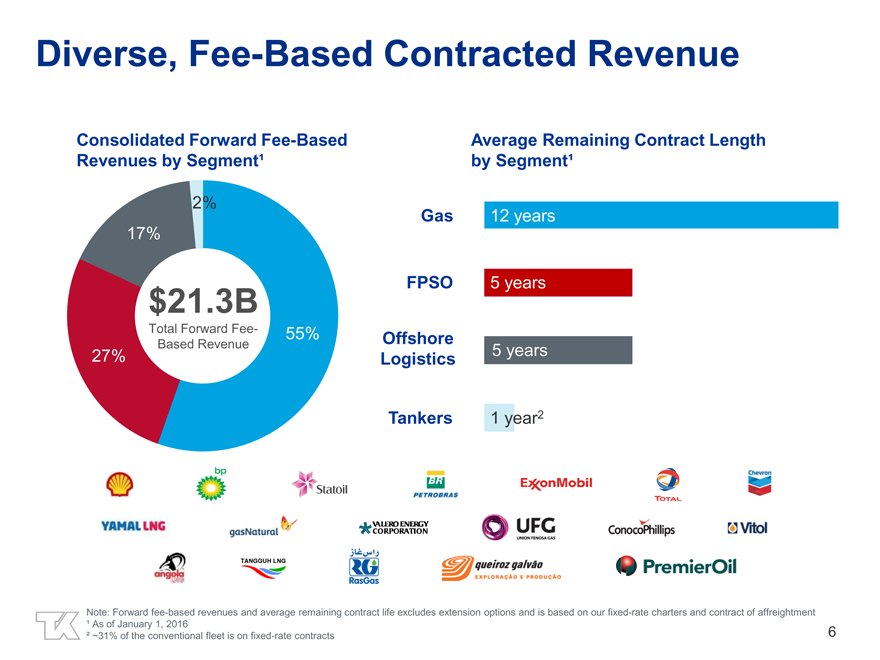

Diverse, Fee-Based Contracted Revenue

Consolidated Forward Fee-Based Revenues by Segment¹

2% 17%

$21.3B

Total Forward Fee- 55% Based Revenue

27%

Average Remaining Contract Length by Segment¹

Gas 12 years

FPSO 5 5 years

Offshore

5 years

Logistics

Tankers 1 year2

Note: Forward fee-based revenues and average remaining contract life excludes extension options and is based on our fixed-rate charters and contract of affreightment

¹ As of January 1, 2016

² ~31% of the conventional fleet is on fixed-rate contracts

6

|

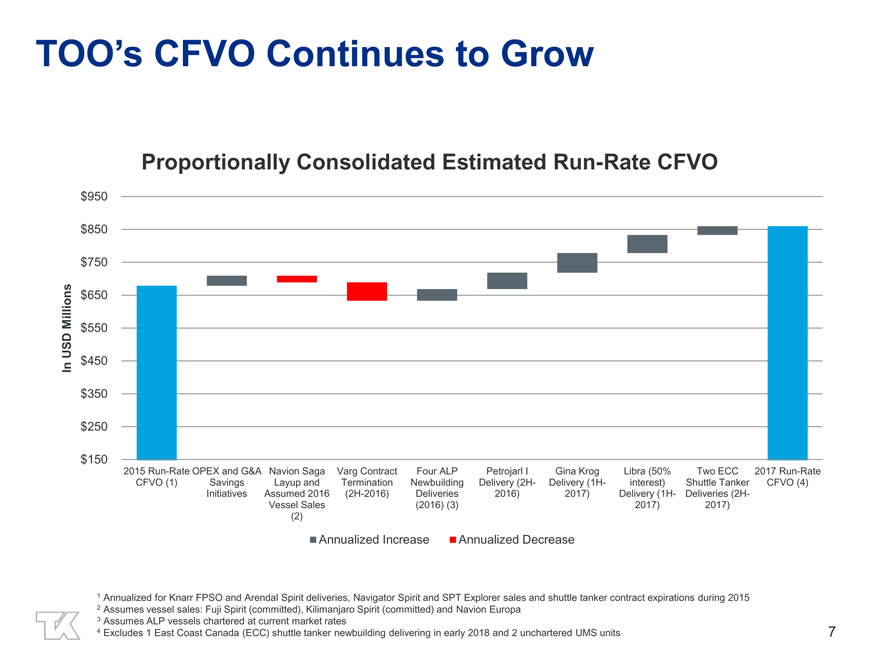

TOO’s CFVO Continues to Grow

Proportionally Consolidated Estimated Run-Rate CFVO

$950

$850

$750

Millions $650 $550

USD $450

In

$350

$250

$150

2015 Run-Rate OPEX and G&A Navion Saga Varg Contract Four ALP Petrojarl I Gina Krog Libra (50% Two ECC 2017 Run-Rate CFVO (1) Savings Layup and Termination Newbuilding Delivery (2H- Delivery (1H- interest) Shuttle Tanker CFVO (4) Initiatives Assumed 2016 (2H-2016) Deliveries 2016) 2017) Delivery (1H- Deliveries (2H-Vessel Sales (2016) (3) 2017) 2017) (2)

Annualized Increase Annualized Decrease

1 Annualized for Knarr FPSO and Arendal Spirit deliveries, Navigator Spirit and SPT Explorer sales and shuttle tanker contract expirations during 2015

2 Assumes vessel sales: Fuji Spirit (committed), Kilimanjaro Spirit (committed) and Navion Europa

3 Assumes ALP vessels chartered at current market rates

4 Excludes 1 East Coast Canada (ECC) shuttle tanker newbuilding delivering in early 2018 and 2 unchartered UMS units

7

|

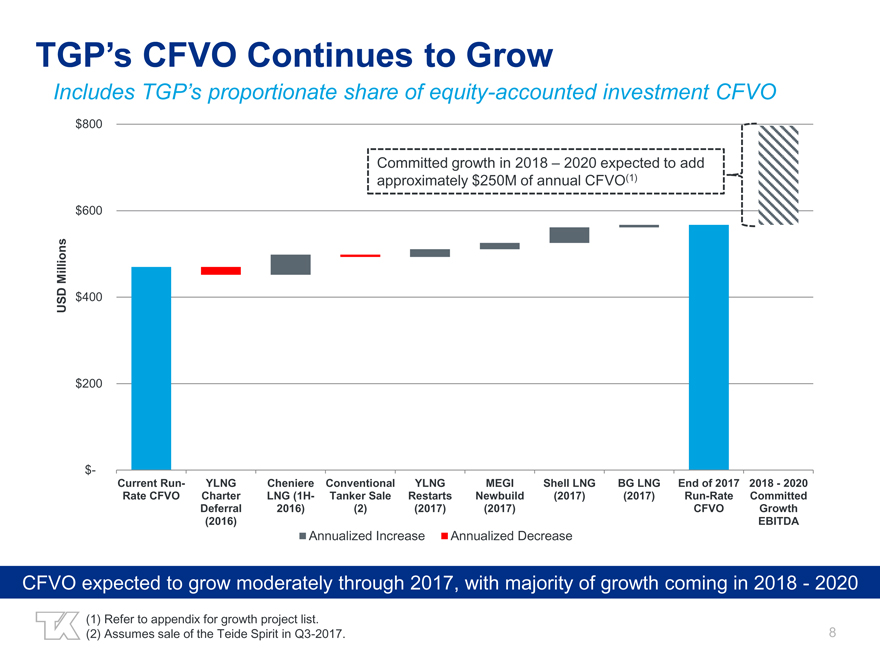

TGP’s CFVO Continues to Grow

Includes TGP’s proportionate share of equity-accounted investment CFVO

$800

Committed growth in 2018 – 2020 expected to add approximately $250M of annual CFVO(1)

$600

Millions

USD $400

$200

$-

Current Run- YLNG Cheniere Conventional YLNG MEGI Shell LNG BG LNG End of 2017 2018—2020 Rate CFVO Charter LNG (1H- Tanker Sale Restarts Newbuild (2017) (2017) Run-Rate Committed Deferral 2016) (2) (2017) (2017) CFVO Growth (2016) EBITDA

Annualized Increase Annualized Decrease

CFVO expected to grow moderately through 2017, with majority of growth coming in 2018—2020

(1) Refer to appendix for growth project list.

(2) Assumes sale of the Teide Spirit in Q3-2017. 8

|

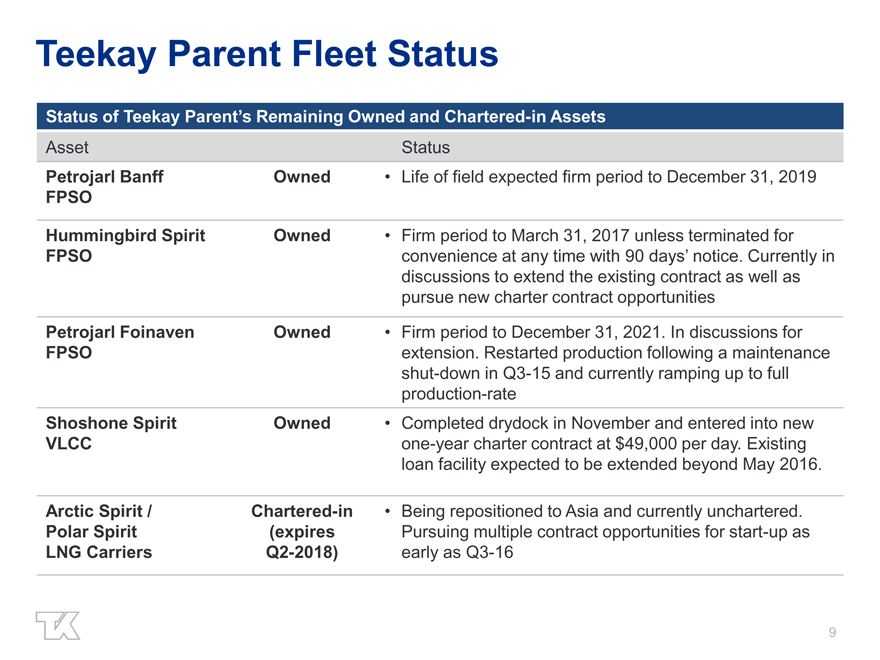

Teekay Parent Fleet Status

Status of Teekay Parent’s Remaining Owned and Chartered-in Assets

Asset Status

Petrojarl Banff Owned • Life of field expected firm period to December 31, 2019

FPSO

Hummingbird Spirit Owned • Firm period to March 31, 2017 unless terminated for

FPSO convenience at any time with 90 days’ notice. Currently in

discussions to extend the existing contract as well as

pursue new charter contract opportunities

Petrojarl Foinaven Owned • Firm period to December 31, 2021. In discussions for

FPSO extension. Restarted production following a maintenance

shut-down in Q3-15 and currently ramping up to full

production-rate

Shoshone Spirit Owned • Completed drydock in November and entered into new

VLCC one-year charter contract at $49,000 per day. Existing

loan facility expected to be extended beyond May 2016.

Arctic Spirit / Chartered-in • Being repositioned to Asia and currently unchartered.

Polar Spirit(expires Pursuing multiple contract opportunities for start-up as

LNG Carriers Q2-2018) early as Q3-16

9

|

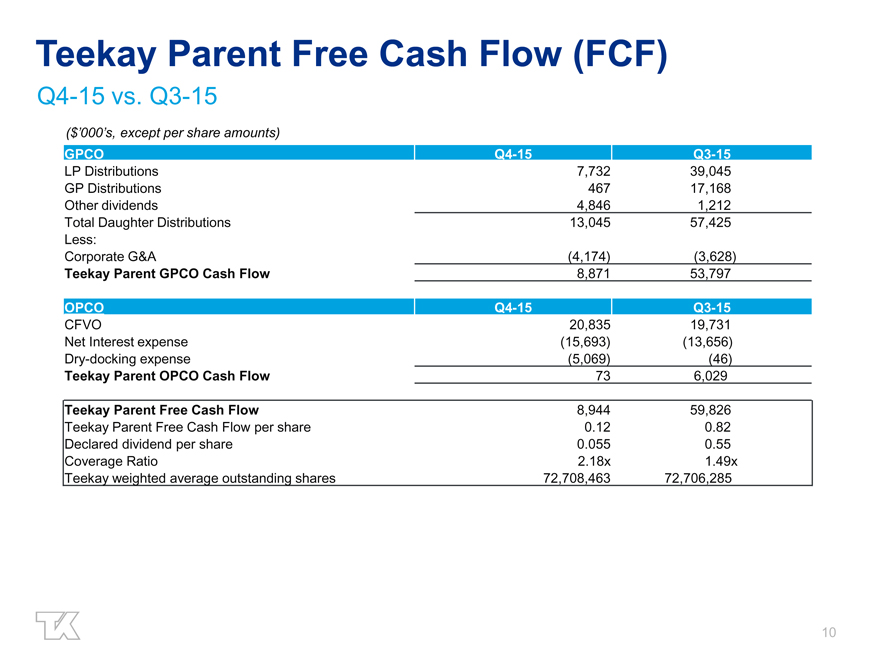

Teekay Parent Free Cash Flow (FCF)

Q4-15 vs. Q3-15

($’000’s, except per share amounts)

GPCO Q4-15 Q3-15

LP Distributions 7,732 39,045

GP Distributions 467 17,168

Other dividends 4,846 1,212

Total Daughter Distributions 13,045 57,425

Less:

Corporate G&A(4,174)(3,628)

Teekay Parent GPCO Cash Flow 8,871 53,797

OPCO Q4-15 Q3-15

CFVO 20,835 19,731

Net Interest expense(15,693)(13,656)

Dry-docking expense(5,069)(46)

Teekay Parent OPCO Cash Flow 73 6,029

Teekay Parent Free Cash Flow 8,944 59,826

Teekay Parent Free Cash Flow per share 0.12 0.82

Declared dividend per share 0.055 0.55

Coverage Ratio 2.18x 1.49x

Teekay weighted average outstanding shares 72,708,463 72,706,285

10

|

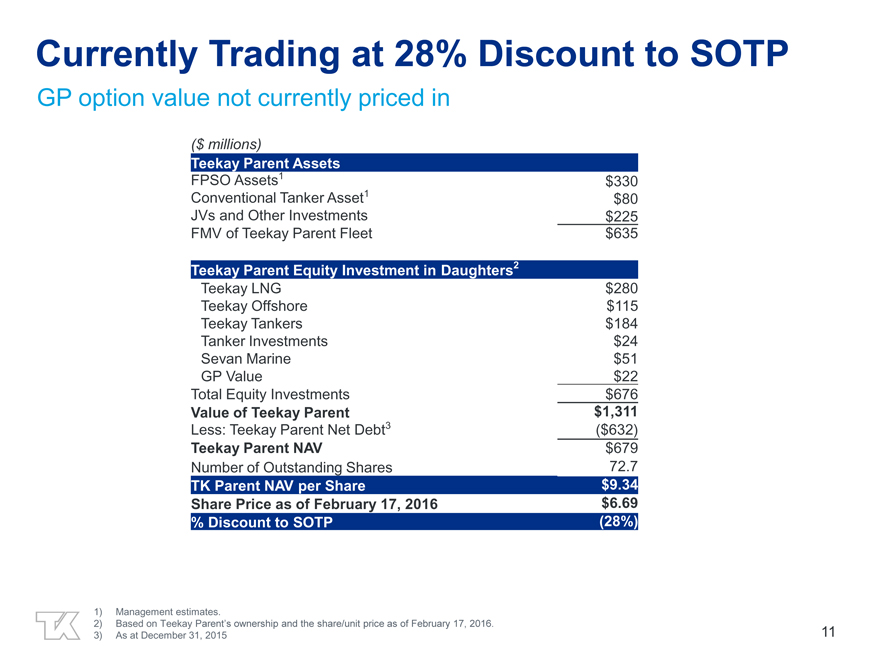

Currently Trading at 28% Discount to SOTP

GP option value not currently priced in

($ millions)

Teekay Parent Assets

FPSO Assets1 $330

Conventional Tanker Asset1 $80

JVs and Other Investments $225

FMV of Teekay Parent Fleet $635

Teekay Parent Equity Investment in Daughters2

Teekay LNG $280

Teekay Offshore $115

Teekay Tankers $184

Tanker Investments $24

Sevan Marine $51

GP Value $22

Total Equity Investments $676

Value of Teekay Parent $1,311

Less: Teekay Parent Net Debt3($632)

Teekay Parent NAV $679

Number of Outstanding Shares 72.7

TK Parent NAV per Share $9.34

Share Price as of February 17, 2016 $6.69

% Discount to SOTP(28%)

1) Management estimates.

2) Based on Teekay Parent’s ownership and the share/unit price as of February 17, 2016.

3) As at December 31, 2015

11

|

Appendix

|

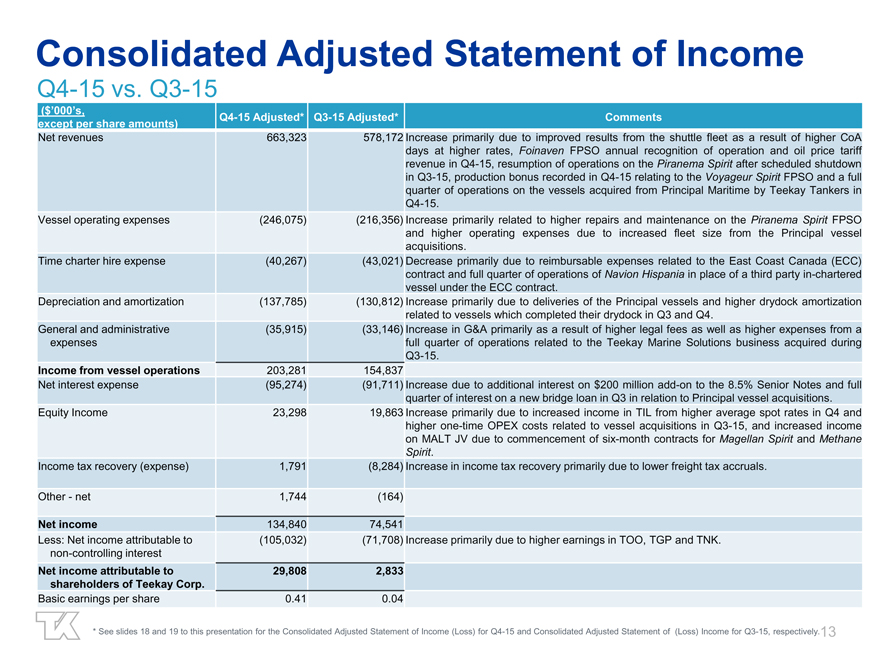

Consolidated Adjusted Statement of Income

Q4-15 vs. Q3-15

($’000’s,

except per share amounts) Q4-15 Adjusted* Q3-15 Adjusted* Comments

Net revenues 663,323 578,172 Increase primarily due to improved results from the shuttle fleet as a result of higher CoA

days at higher rates, Foinaven FPSO annual recognition of operation and oil price tariff

revenue in Q4-15, resumption of operations on the Piranema Spirit after scheduled shutdown

in Q3-15, production bonus recorded in Q4-15 relating to the Voyageur Spirit FPSO and a full

quarter of operations on the vessels acquired from Principal Maritime by Teekay Tankers in

Q4-15.

Vessel operating expenses(246,075)(216,356) Increase primarily related to higher repairs and maintenance on the Piranema Spirit FPSO

and higher operating expenses due to increased fleet size from the Principal vessel

acquisitions.

Time charter hire expense(40,267)(43,021) Decrease primarily due to reimbursable expenses related to the East Coast Canada (ECC)

contract and full quarter of operations of Navion Hispania in place of a third party in-chartered

vessel under the ECC contract.

Depreciation and amortization(137,785)(130,812) Increase primarily due to deliveries of the Principal vessels and higher drydock amortization

related to vessels which completed their drydock in Q3 and Q4.

General and administrative(35,915)(33,146) Increase in G&A primarily as a result of higher legal fees as well as higher expenses from a

expenses full quarter of operations related to the Teekay Marine Solutions business acquired during

Q3-15.

Income from vessel operations 203,281 154,837

Net interest expense(95,274)(91,711) Increase due to additional interest on $200 million add-on to the 8.5% Senior Notes and full

quarter of interest on a new bridge loan in Q3 in relation to Principal vessel acquisitions.

Equity Income 23,298 19,863 Increase primarily due to increased income in TIL from higher average spot rates in Q4 and

higher one-time OPEX costs related to vessel acquisitions in Q3-15, and increased income

on MALT JV due to commencement of six-month contracts for Magellan Spirit and Methane

Spirit.

Income tax recovery (expense) 1,791(8,284) Increase in income tax recovery primarily due to lower freight tax accruals.

Other—net 1,744(164)

Net income 134,840 74,541

Less: Net income attributable to(105,032)(71,708) Increase primarily due to higher earnings in TOO, TGP and TNK.

non-controlling interest

Net income attributable to 29,808 2,833

shareholders of Teekay Corp.

Basic earnings per share 0.41 0.04

* See slides 18 and 19 to this presentation for the Consolidated Adjusted Statement of Income (Loss) for Q4-15 and Consolidated Adjusted Statement of (Loss) Income for Q3-15, respectively.13

|

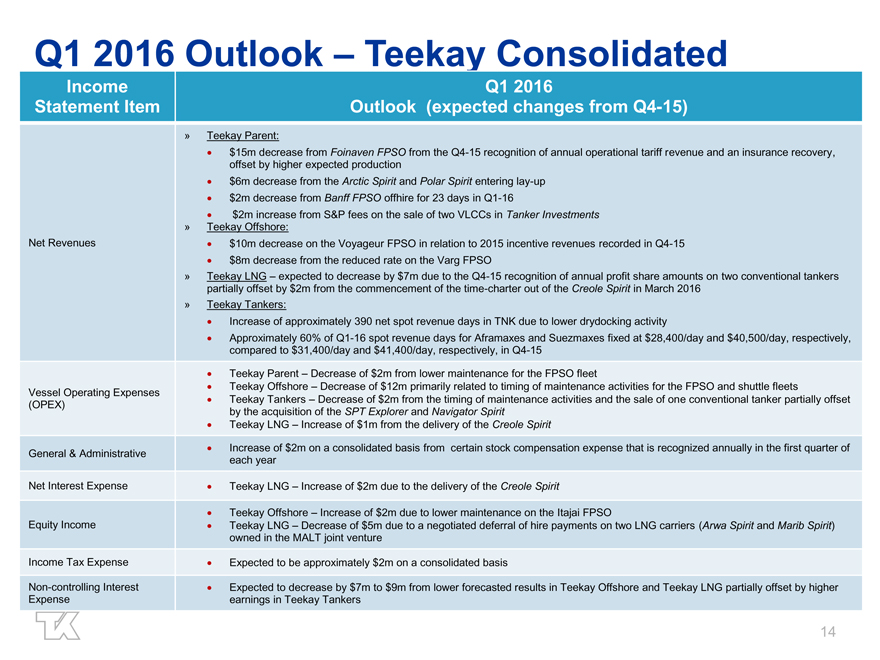

Q1 2016 Outlook – Teekay Consolidated

Income Q1 2016

Statement Item Outlook (expected changes from Q4-15)

» Teekay Parent:

• $15m decrease from Foinaven FPSO from the Q4-15 recognition of annual operational tariff revenue and an insurance recovery,

offset by higher expected production

• $6m decrease from the Arctic Spirit and Polar Spirit entering lay-up

• $2m decrease from Banff FPSO offhire for 23 days in Q1-16

• $2m increase from S&P fees on the sale of two VLCCs in Tanker Investments

» Teekay Offshore:

Net Revenues • $10m decrease on the Voyageur FPSO in relation to 2015 incentive revenues recorded in Q4-15

• $8m decrease from the reduced rate on the Varg FPSO

» Teekay LNG – expected to decrease by $7m due to the Q4-15 recognition of annual profit share amounts on two conventional tankers

partially offset by $2m from the commencement of the time-charter out of the Creole Spirit in March 2016

» Teekay Tankers:

• Increase of approximately 390 net spot revenue days in TNK due to lower drydocking activity

• Approximately 60% of Q1-16 spot revenue days for Aframaxes and Suezmaxes fixed at $28,400/day and $40,500/day, respectively,

compared to $31,400/day and $41,400/day, respectively, in Q4-15

• Teekay Parent – Decrease of $2m from lower maintenance for the FPSO fleet

• Teekay Offshore – Decrease of $12m primarily related to timing of maintenance activities for the FPSO and shuttle fleets

Vessel Operating Expenses • Teekay Tankers – Decrease of $2m from the timing of maintenance activities and the sale of one conventional tanker partially offset

(OPEX) by the acquisition of the SPT Explorer and Navigator Spirit

• Teekay LNG – Increase of $1m from the delivery of the Creole Spirit

General & Administrative • Increase of $2m on a consolidated basis from certain stock compensation expense that is recognized annually in the first quarter of

each year

Net Interest Expense • Teekay LNG – Increase of $2m due to the delivery of the Creole Spirit

• Teekay Offshore – Increase of $2m due to lower maintenance on the Itajai FPSO

Equity Income • Teekay LNG – Decrease of $5m due to a negotiated deferral of hire payments on two LNG carriers (Arwa Spirit and Marib Spirit)

owned in the MALT joint venture

Income Tax Expense • Expected to be approximately $2m on a consolidated basis

Non-controlling Interest • Expected to decrease by $7m to $9m from lower forecasted results in Teekay Offshore and Teekay LNG partially offset by higher

Expense earnings in Teekay Tankers

14

|

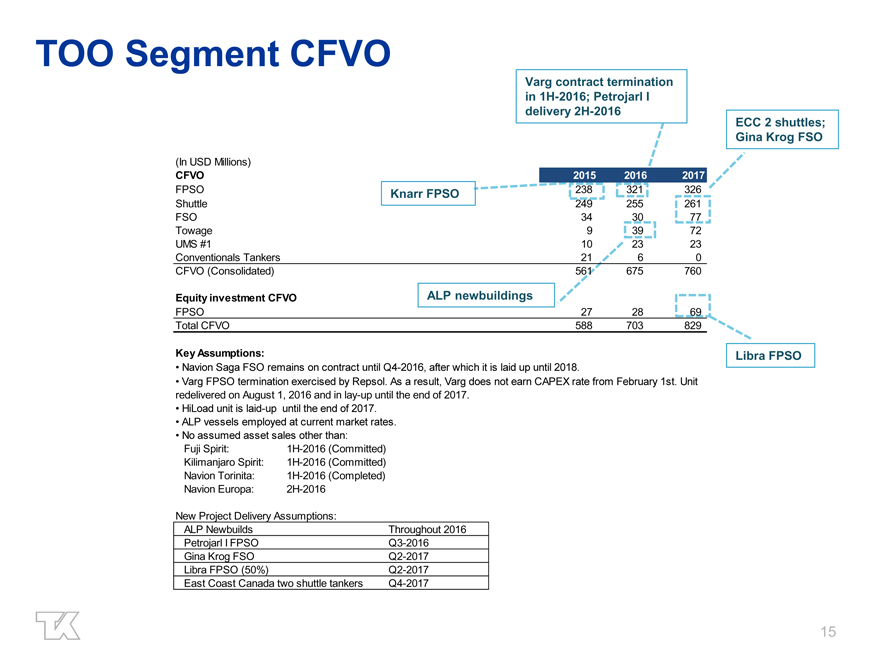

TOO Segment CFVO

Varg contract termination

in 1H-2016; Petrojarl I

delivery 2H-2016

ECC 2 shuttles;

Gina Krog FSO

(In USD Millions)

CFVO 2015 2016 2017

FPSO Knarr FPSO 238 321 326

Shuttle 249 255 261

FSO 34 30 77

Towage 9 39 72

UMS #1 10 23 23

Conventionals Tankers 21 6 0

CFVO (Consolidated) 561 675 760

Equity investment CFVO ALP newbuildings

FPSO 27 28 69

Total CFVO 588 703 829

Key Assumptions: Libra FPSO

Navion Saga FSO remains on contract until Q4-2016, after which it is laid up until 2018.

• Varg FPSO termination exercised by Repsol. As a result, Varg does not earn CAPEX rate from February 1st. Unit

redelivered on August 1, 2016 and in lay-up until the end of 2017.

• HiLoad unit is laid-up until the end of 2017.

• ALP vessels employed at current market rates.

• No assumed asset sales other than:

Fuji Spirit: 1H-2016 (Committed)

Kilimanjaro Spirit: 1H-2016 (Committed)

Navion Torinita: 1H-2016 (Completed)

Navion Europa: 2H-2016

New Project Delivery Assumptions:

ALP Newbuilds Throughout 2016

Petrojarl I FPSO Q3-2016

Gina Krog FSO Q2-2017

Libra FPSO (50%) Q2-2017

East Coast Canada two shuttle tankers Q4-2017

15

|

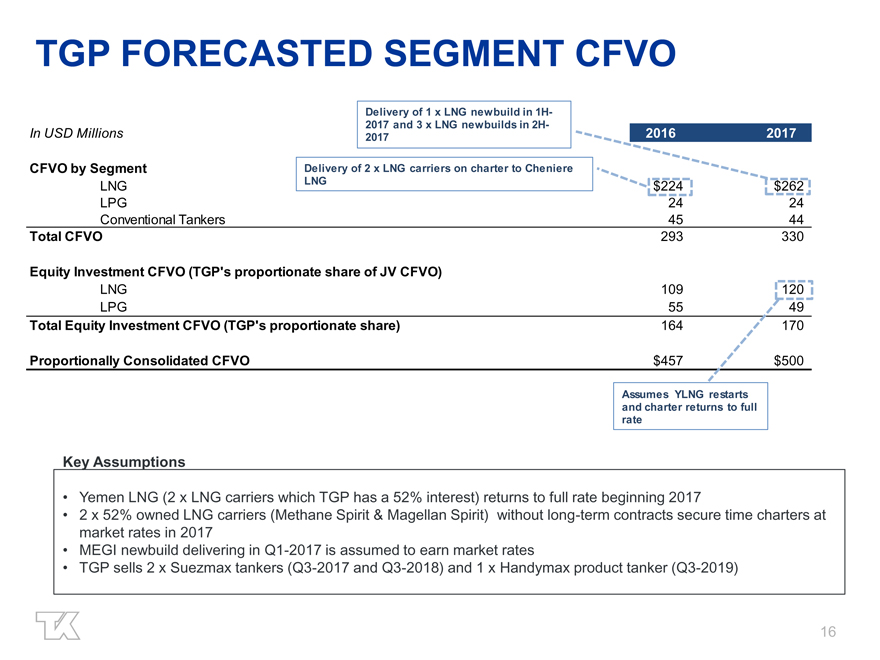

TGP FORECASTED SEGMENT CFVO

Delivery of 1 x LNG newbuild in 1H-

2017 and 3 x LNG newbuilds in 2H-

In USD Millions 2017 2016 2017

CFVO by Segment Delivery of 2 x LNG carriers on charter to Cheniere

LNG LNG $ 224 $ 262

LPG 24 24

Conventional Tankers 45 44

Total CFVO 293 330

Equity Investment CFVO (TGP’s proportionate share of JV CFVO)

LNG 109 120

LPG 55 49

Total Equity Investment CFVO (TGP’s proportionate share) 164 170

Proportionally Consolidated CFVO $ 457 $ 500

Assumes YLNG restarts

and charter returns to full

rate

Key Assumptions

• Yemen LNG (2 x LNG carriers which TGP has a 52% interest) returns to full rate beginning 2017

• 2 x 52% owned LNG carriers (Methane Spirit & Magellan Spirit) without long-term contracts secure time charters at

market rates in 2017

• MEGI newbuild delivering in Q1-2017 is assumed to earn market rates

• TGP sells 2 x Suezmax tankers (Q3-2017 and Q3-2018) and 1 x Handymax product tanker (Q3-2019)

16

|

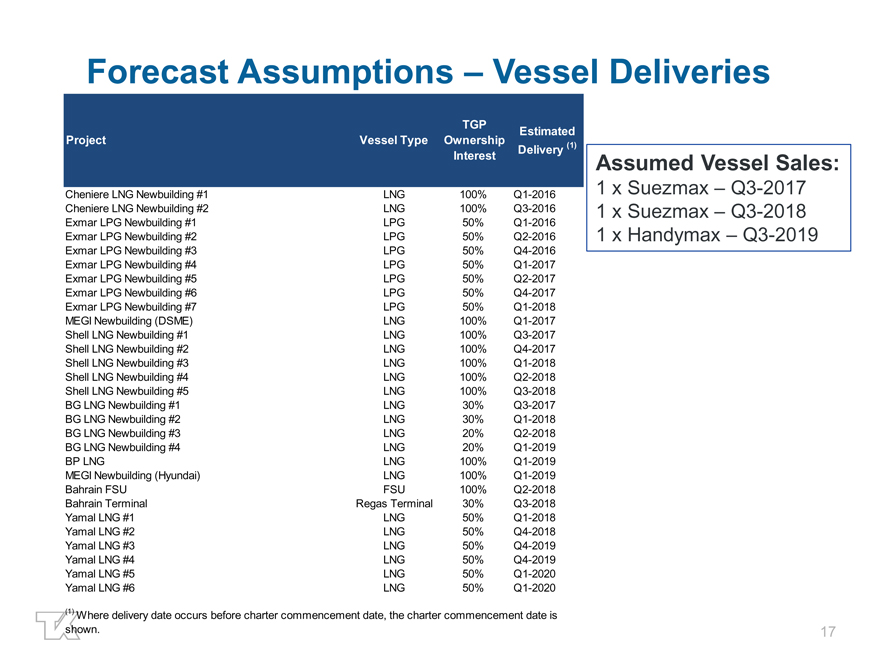

Forecast Assumptions – Vessel Deliveries

TGP Estimated

Project Vessel Type Ownership

Interest Delivery (1)

Cheniere LNG Newbuilding #1 LNG 100% Q1-2016

Cheniere LNG Newbuilding #2 LNG 100% Q3-2016

Exmar LPG Newbuilding #1 LPG 50% Q1-2016

Exmar LPG Newbuilding #2 LPG 50% Q2-2016

Exmar LPG Newbuilding #3 LPG 50% Q4-2016

Exmar LPG Newbuilding #4 LPG 50% Q1-2017

Exmar LPG Newbuilding #5 LPG 50% Q2-2017

Exmar LPG Newbuilding #6 LPG 50% Q4-2017

Exmar LPG Newbuilding #7 LPG 50% Q1-2018

MEGI Newbuilding (DSME) LNG 100% Q1-2017

Shell LNG Newbuilding #1 LNG 100% Q3-2017

Shell LNG Newbuilding #2 LNG 100% Q4-2017

Shell LNG Newbuilding #3 LNG 100% Q1-2018

Shell LNG Newbuilding #4 LNG 100% Q2-2018

Shell LNG Newbuilding #5 LNG 100% Q3-2018

BG LNG Newbuilding #1 LNG 30% Q3-2017

BG LNG Newbuilding #2 LNG 30% Q1-2018

BG LNG Newbuilding #3 LNG 20% Q2-2018

BG LNG Newbuilding #4 LNG 20% Q1-2019

BP LNG LNG 100% Q1-2019

MEGI Newbuilding (Hyundai) LNG 100% Q1-2019

Bahrain FSU FSU 100% Q2-2018

Bahrain Terminal Regas Terminal 30% Q3-2018

Yamal LNG #1 LNG 50% Q1-2018

Yamal LNG #2 LNG 50% Q4-2018

Yamal LNG #3 LNG 50% Q4-2019

Yamal LNG #4 LNG 50% Q4-2019

Yamal LNG #5 LNG 50% Q1-2020

Yamal LNG #6 LNG 50% Q1-2020

(1) Where delivery date occurs before charter commencement date, the charter commencement date is

shown.

Assumed Vessel Sales:

1 x Suezmax – Q3-2017 1 x Suezmax – Q3-2018 1 x Handymax – Q3-2019

17

|

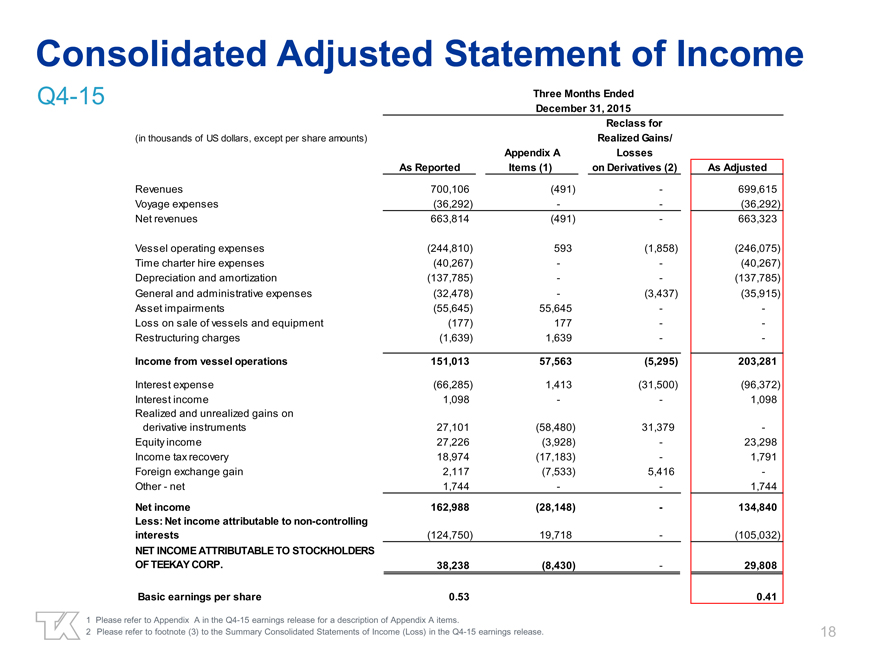

Consolidated Adjusted Statement of Income

Q4-15 Three Months Ended

December 31, 2015

Reclass for

(in thousands of US dollars, except per share amounts) Realized Gains/

Appendix A Losses

As Reported Items (1) on Derivatives (2) As Adjusted

Revenues 700,106(491)—699,615

Voyage expenses(36,292) —(36,292)

Net revenues 663,814(491)—663,323

Vessel operating expenses(244,810) 593(1,858)(246,075)

Time charter hire expenses(40,267) —(40,267)

Depreciation and amortization(137,785) —(137,785)

General and administrative expenses(32,478) -(3,437)(35,915)

Asset impairments(55,645) 55,645 —

Loss on sale of vessels and equipment(177) 177 —

Restructuring charges(1,639) 1,639 —

Income from vessel operations 151,013 57,563(5,295) 203,281

Interest expense(66,285) 1,413(31,500)(96,372)

Interest income 1,098 — 1,098

Realized and unrealized gains on

derivative instruments 27,101(58,480) 31,379 -

Equity income 27,226(3,928)—23,298

Income tax recovery 18,974(17,183)—1,791

Foreign exchange gain 2,117(7,533) 5,416 -

Other—net 1,744 — 1,744

Net income 162,988(28,148)—134,840

Less: Net income attributable to non-controlling

interests(124,750) 19,718 -(105,032)

NET INCOME ATTRIBUTABLE TO STOCKHOLDERS

OF TEEKAY CORP. 38,238(8,430) - 29,808

Basic earnings per share 0.53 0.41

1 Please refer to Appendix A in the Q4-15 earnings release for a description of Appendix A items.

2 Please refer to footnote (3) to the Summary Consolidated Statements of Income (Loss) in the Q4-15 earnings release.

18

|

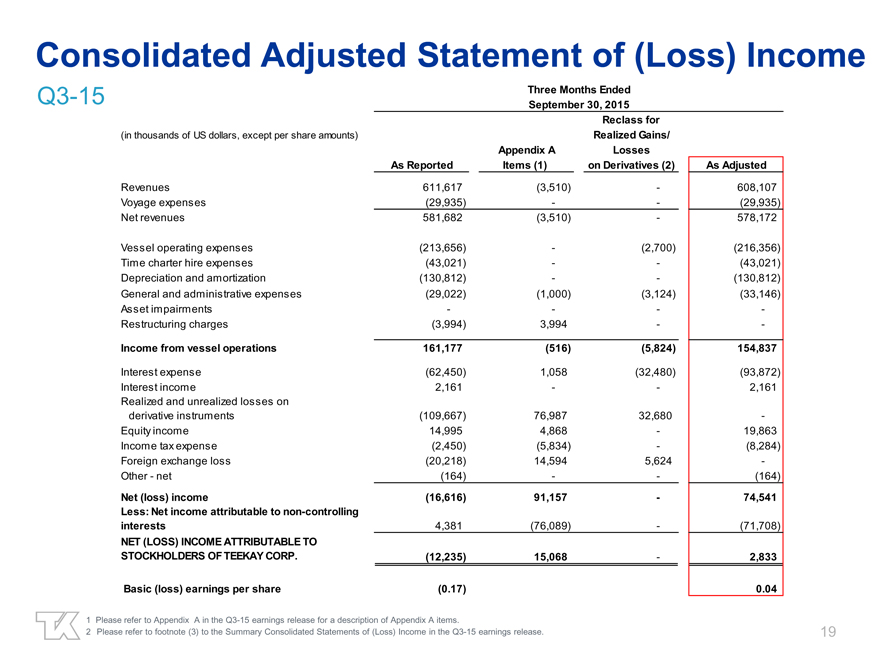

Consolidated Adjusted Statement of (Loss) Income

Q3-15 Three Months Ended

September 30, 2015

Reclass for

(in thousands of US dollars, except per share amounts) Realized Gains/

Appendix A Losses

As Reported Items (1) on Derivatives (2) As Adjusted

Revenues 611,617(3,510)—608,107

Voyage expenses(29,935) —(29,935)

Net revenues 581,682(3,510)—578,172

Vessel operating expenses(213,656) -(2,700)(216,356)

Time charter hire expenses(43,021) —(43,021)

Depreciation and amortization(130,812) —(130,812)

General and administrative expenses(29,022)(1,000)(3,124)(33,146)

Asset impairments — —

Restructuring charges(3,994) 3,994 —

Income from vessel operations 161,177(516)(5,824) 154,837

Interest expense(62,450) 1,058(32,480)(93,872)

Interest income 2,161 — 2,161

Realized and unrealized losses on

derivative instruments(109,667) 76,987 32,680 -

Equity income 14,995 4,868—19,863

Income tax expense(2,450)(5,834) -(8,284)

Foreign exchange loss(20,218) 14,594 5,624 -

Other—net(164) —(164)

Net (loss) income(16,616) 91,157—74,541

Less: Net income attributable to non-controlling

interests 4,381(76,089) -(71,708)

NET (LOSS) INCOME ATTRIBUTABLE TO

STOCKHOLDERS OF TEEKAY CORP.(12,235) 15,068 - 2,833

Basic (loss) earnings per share(0.17) 0.04

1 Please refer to Appendix A in the Q3-15 earnings release for a description of Appendix A items.

2 Please refer to footnote (3) to the Summary Consolidated Statements of (Loss) Income in the Q3-15 earnings release. 19

|

BRINGING ENERGY TO THE WORLD