Table of Contents

Filed Pursuant to Rule 424(b)(5)

Registration Number 333-221806

Registration Number 333-231003

PROSPECTUS SUPPLEMENT

(To Prospectus dated January 12, 2018)

Teekay Corporation

Common Stock

Having an Aggregate Offering Price of Up to $63,000,000

We have entered into an equity distribution agreement with Citigroup Global Markets Inc., or the “Agent,” relating to the shares of common stock of Teekay Corporation offered by this prospectus supplement and the accompanying prospectus. In accordance with the terms of the equity distribution agreement, we may offer and sell shares of common stock having an aggregate offering price of up to $63,000,000 from time to time through the Agent, as our sales agent, or directly to the Agent acting as principal.

Sales of the common stock, if any, made by the Agent, as our sales agent, as contemplated by this prospectus supplement and the accompanying prospectus, may be made by means of ordinary brokers’ transactions on the New York Stock Exchange at market prices, in block transactions, or as otherwise agreed between us and the Agent. We will pay the Agent a commission of up to 2.0% of the gross sales price per share of common stock sold through the Agent, as our sales agent, under the equity distribution agreement.

Under the terms of the equity distribution agreement, we also may sell shares of common stock to the Agent as principal at a price to be agreed upon at the time of sale. If we sell shares of common stock to the Agent as principal, we will enter into a separate terms agreement with the Agent, and we will describe the public offering price, underwriting discount (which may exceed 2.0% of the public offering price) and other terms of the offering of those shares of common stock in a separate prospectus supplement or pricing supplement.

The Agent is not required to sell any specific number of shares or dollar amount of our common stock but will use its reasonable efforts, as our sales agent, and on the terms and subject to the conditions of the equity distribution agreement, to sell the common stock offered on terms agreed by the Agent and us. The offering of shares of our common stock pursuant to the equity distribution agreement will terminate upon the earlier of (1) the sale of all of the common stock subject to the equity distribution agreement and (2) the termination of the equity distribution agreement by either the Agent or us.

Our common stock trades on the New York Stock Exchange (orNYSE) under the symbol “TK.” The last reported sale price of our common stock on the New York Stock Exchange on April 23, 2019 was $4.62 per share.

Investing in our common stock involves a high degree of risk. You should carefully consider each of the factors described or referred to under “Risk Factors” onpage S-8 of this prospectus supplement, page 4 of the accompanying prospectus and in the documents incorporated by reference into this prospectus supplement and accompanying prospectus before you make an investment in our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Citigroup

The date of this prospectus supplement is April 24, 2019.

Table of Contents

ABOUT THIS PROSPECTUS SUPPLEMENT

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering of shares of our common stock. The second part is the accompanying prospectus, which gives more general information, some of which may not apply to this offering of common stock. Generally, when we refer to the “prospectus,” we refer to both parts combined. If information varies between this prospectus supplement and the accompanying prospectus, you should rely on the information in this prospectus supplement.

Any statement made in this prospectus or in a document incorporated or deemed to be incorporated by reference into this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in this prospectus or in any other subsequently filed document that is also incorporated by reference into this prospectus modifies or supersedes that statement. Any statement so modified or superseded will not be deemed, except as so modified or superseded, to constitute a part of this prospectus.

You should rely only on the information contained or incorporated by reference in this prospectus or any “free writing prospectus” we may authorize to be delivered to you. We have not authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. You should not assume that the information contained in this prospectus or any “free writing prospectus” we may authorize to be delivered to you, as well as the information we previously filed with the Securities and Exchange Commission (or theSEC) that is incorporated by reference into this prospectus, is accurate as of any date other than its respective date. Our business, financial condition, results of operations and prospects may have changed since such dates.

We are offering to sell shares of our common stock, and are seeking offers to buy shares of our common stock, only in jurisdictions where offers and sales are permitted. The distribution of this prospectus and the offering of shares of our common stock in certain jurisdictions may be restricted by law. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of the common stock and the distribution of this prospectus outside the United States. This prospectus does not constitute, and may not be used in connection with, an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so or to any person to whom it is unlawful to make such offer or solicitation.

S-i

Table of Contents

TABLE OF CONTENTS

Prospectus Supplement

| S-i | ||||

| S-1 | ||||

| S-2 | ||||

| S-8 | ||||

| S-10 | ||||

| S-11 | ||||

| S-12 | ||||

| S-16 | ||||

| S-23 | ||||

| S-24 | ||||

| S-26 | ||||

| S-26 | ||||

| S-26 | ||||

| S-28 |

Prospectus

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 12 | ||||

| 20 | ||||

| 26 | ||||

| 27 | ||||

| 29 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 31 |

S-ii

Table of Contents

All statements, other than statements of historical fact, included in or incorporated by reference into this prospectus are forward-looking statements. In addition, we and our representatives may from time to time make other oral or written statements that are also forward-looking statements. Such statements include, in particular, statements about our future or anticipated operations, cash flows, financial position, plans, strategies, business prospects, changes and trends in our business, and the markets in which we operate. In some cases, you can identify the forward-looking statements by the use of words such as “may,” “will,” “could,” “should,” “would,” “expect,” “plan,” “anticipate,” “intend,” “forecast,” “believe,” “estimate,” “predict,” “propose,” “potential,” “continue” or the negative of these terms or other comparable terminology.

These and other forward-looking statements reflect management’s current plans, expectations, estimates, assumptions and beliefs concerning future events affecting us. Forward-looking statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond our control. We caution that forward- looking statements are not guarantees and that actual results may differ materially from those expressed or implied by such forward-looking statements. Important factors that could cause actual results to differ materially include, but are not limited to, those factors discussed under the heading “Risk Factors” set forth in this prospectus and those factors discussed in our most recent Annual Report on Form20-F and other reports we file with or furnish to the SEC and that are incorporated into this prospectus by reference.

We undertake no obligation to update any forward-looking statement to reflect any change in our expectations or events or circumstances that may arise after the date on which such statement is made. New factors emerge from time to time, and it is not possible for us to predict all of these factors. In addition, we cannot assess the effect of each such factor on our business or the extent to which any factor, or combination of factors, may cause actual results to be materially different from those contained in any forward-looking statement.

Forward-looking statements in this prospectus or incorporated by reference herein include, among others, statements about the following matters:

| • | the timing and amount of sales of our common stock pursuant to the equity distribution agreement, and the expected use of any sales proceeds; |

| • | our plans for Teekay Parent (as defined below) not to have a direct ownership in any conventional tankers or floating production, storage andoff-loading (orFPSO) units, and increase its free cash flow, reduce its net debt and delever its balance sheet; |

| • | our dividend policy and our payment of or our ability to pay any cash dividends on our shares of common stock, and the distribution and dividend policies of the Daughter Entities (as defined below), including the ability to increase the distribution levels of the Daughter Entities in the future; |

| • | the completion, terms and pricing of the Note Offering (as defined below), and the collateral used to secure the Notes; |

| • | commencement and results of the Tender Offer (as defined below), and the results of the Consent Solicitation (as defined below); |

| • | our intent to cure the Teekay Tankers $1.00 per share deficiency and regain compliance with the NYSE continued listing requirement; |

| • | our expectations regarding tax liabilities and classifications; and |

| • | the realization of contracted, forward fixed-rate revenues. |

S-1

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus and the documents incorporated by reference in this prospectus and does not contain all the information you will need in making an investment decision. You should carefully read this entire prospectus supplement, the accompanying prospectus, and the documents incorporated by reference into this prospectus.

Unless otherwise indicated, references in this prospectus to “Teekay,” the “Company,” “we,” “us” and “our” and similar terms refer to Teekay Corporation and/or its subsidiaries, except that those terms, when used in this prospectus in connection with the common stock described herein, shall mean specifically Teekay Corporation. References in this prospectus supplement to (a) “Teekay LNG” refer to Teekay LNG Partners L.P. (NYSE: TGP), a subsidiary of Teekay Corporation, (b) “Teekay Tankers” refer to Teekay Tankers Ltd. (NYSE: TNK), a subsidiary of Teekay Corporation, (c) “Teekay Parent” refer to Teekay Corporation and its remaining subsidiaries and (d) “Teekay Offshore” refer to Teekay Offshore Partners L.P. (NYSE: TOO), an entity which since September 25, 2017 is no longer consolidated with Teekay Corporation and for which Teekay Corporation now accounts using the equity method. In this prospectus supplement, we refer to Teekay LNG and Teekay Tankers as the “Controlled Daughter Entities” and the Controlled Daughter Entities and Teekay Offshore collectively as the “Daughter Entities,” and references to the “Teekay group” include Teekay Parent and the Daughter Entities.

Unless otherwise indicated, certain information in this prospectus supplement about the vessels and fleets, segment market positions, employees, contracted revenues and related matters of the Teekay group or a particular group member refer in the aggregate to 100% of such items for (a) in the case of the Teekay group, Teekay Corporation, Teekay LNG, Teekay Tankers, Teekay Offshore and their subsidiaries and equity-accounted vessels and investments and (b) in the case of a particular Teekay group member, such member and its subsidiaries and equity-accounted vessels and investments.

Unless otherwise indicated, all references in this prospectus supplement to “dollars” and “$” are to, and amounts are presented in, U.S. Dollars. Teekay prepares its financial statements in accordance with United States generally accepted accounting principles (or GAAP). References to “independent” fleet owners or operators mean companies other than private or state-controlled entities that operate their own fleets. Unless otherwise indicated, we include as long-term contracts those with an initial term of at least three years.

Overview

The Teekay group is a leading provider of international crude oil and gas marine transportation services and offshore production and logistics with offices in 14 countries and approximately 8,000 seagoing and shore-based employees. The Teekay group provides these services primarily through:

| • | Teekay LNG – the world’s third largest independent owner and operator of LNG carriers; |

| �� | Teekay Tankers – one of the world’s largest owners and operators ofmid-sized crude tankers; and |

| • | Teekay Offshore – the world’s largest operator of shuttle tankers and fourth largest independent provider of leased FPSO unit solutions.1 |

As of December 31, 2018, the Teekay group operated total assets under management of approximately $16 billion, comprised of approximately 205 liquefied gas, offshore, and conventional tanker assets (excluding vessels managed for third parties). The Teekay group generates revenue primarily under long-term, fixed-rate

| 1 | Teekay Offshore is controlled by Brookfield Business Partners L.P. and certain of its affiliates (collectively,Brookfield) |

S-2

Table of Contents

contracts with a diverse customer base of major energy and utility companies. As of January 1, 2019, the Teekay group had approximately $16 billion of contracted, forward fixed-rate revenues. The revenue-weighted average remaining term of the Teekay group’s contracts was approximately 8.4 years as of January 1, 2019, excluding spot market contracts and extension options. “Revenue-weighted average” represents the average remaining fixed contract duration of the applicable contracts, weighted on the basis of aggregate fixed forward payments to be received from each operating segment, excluding extension options. Fixed forward payments for Teekay Offshore are on a 100% basis and our equity accounted investments and joint ventures are proportionately adjusted in the calculation to reflect our ownership interests in such investments and joint ventures.

Background

Over the last two decades, we have undergone a major transformation from being primarily an owner of ships in the cyclical spot tanker business to being an asset manager and project developer in the “Marine Midstream” sector. This transformation has included the continuation and expansion of our liquefied natural gas (orLNG) business and our expansion into the liquefied petroleum gas (orLPG) shipping sector through Teekay LNG, the continuation and expansion of our conventional tanker business through Teekay Tankers, and expansion of our operations in the offshore production, storage and transportation sector primarily through our investment in Teekay Offshore.

Recent Developments

Teekay Parent

Concurrently with our signing of the equity distribution agreement, we separately announced:

| • | a proposed offering (theNote Offering) of $300,000,000 in aggregate principal amount of senior secured notes due 2024 (theNotes) in a private placement to eligible purchasers under Rule 144A and Regulation S of the U.S. Securities Act of 1933, as amended (theSecurities Act), which Notes will be guaranteed on a senior secured basis by certain of the Company’s subsidiaries and will initially be secured by first-priority liens, subject to permitted liens, on (i) two FPSO units (and related assets) owned by Company subsidiaries, (ii) all shares of common stock of the Company’s subsidiary that owns all of the Company’s common units of Teekay LNG and Teekay Offshore and all of the Company’s Class A common shares of Teekay Tankers and (iii) all equity interests in the Teekay subsidiaries that own two FPSO units; |

| • | a proposed cash tender offer (theTender Offer) to purchase any and all of the Company’s outstanding 8.5% Senior Unsecured Notes due 2020 (the2020 Notes). Concurrently with the Tender Offer, the Company is soliciting (theConsent Solicitation) from the holders representing at least a majority of the aggregate principal amount of the 2020 Notes then outstanding a consent to certain proposed amendments that will eliminate substantially all of the restrictive covenants and certain events of default and related provisions from the indenture governing the 2020 Notes, including the covenant restricting the Company from granting liens on its assets for issuances of other debt securities unless the Company grants apari passulien on such assets in favor of the 2020 Notes; and |

| • | that in connection with the Note Offering and the Tender Offer, Teekay’s Board of Directors has approved the elimination of the quarterly dividend on Teekay’s common stock, commencing with the dividend payable for the quarter ended March 31, 2019, in order to retain cash to further strengthen its balance sheet. |

Teekay Tankers

In April 2019, Teekay Tankers received notice from the NYSE that Teekay Tankers is not in compliance with the NYSE continued listing standards because the average closing price of Teekay Tankers’ shares of

S-3

Table of Contents

Class A common stock fell below $1.00 per share over a period of 30 consecutive trading days. In accordance with NYSE procedures, Teekay Tankers intends to cure the $1.00 per share deficiency and has six months following receipt of the noncompliance notice to regain compliance with the NYSE continued listing requirement.

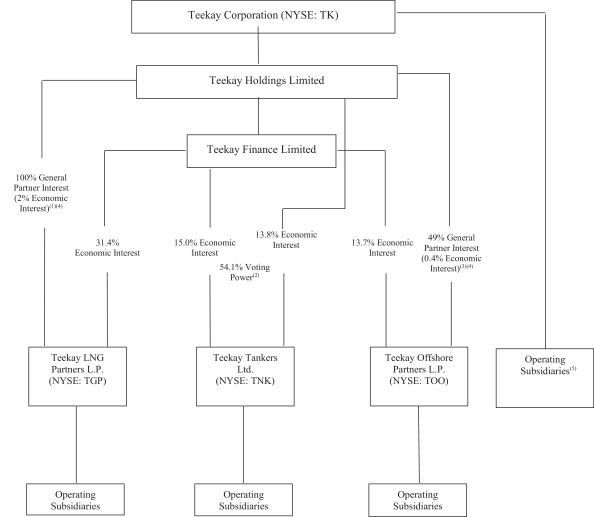

Organizational structure and ownership in Daughter Entities

Our organizational structure can be divided into (a) our controlling interests in our publicly-listed subsidiaries, Teekay LNG and Teekay Tankers, (b) our equity-accounted investment in Teekay Offshore and (c) Teekay Parent.

The following chart provides an overview of our organizational structure as of April 1, 2019:

| (1) | Teekay LNG is controlled by its general partner. We indirectly own a 100% beneficial ownership in the general partner. However, in limited cases, approval of a majority of the unitholders of Teekay LNG is required to approve certain actions. Teekay LNG’s general partner owns its incentive distribution rights. |

S-4

Table of Contents

| (2) | Teekay Tankers has two classes of shares: Class A common stock and Class B common stock. We indirectly own 100% of the Class B shares through Teekay Holdings Limited, which have five votes each but aggregate voting power capped at 49%. As a result of our ownership of Class A and Class B shares, we hold aggregate voting power of 54.1% as of April 1, 2019. |

| (3) | Teekay Offshore is controlled by its general partner. Brookfield and we indirectly have ownership interests of 51% and 49% of the general partner, respectively. However, in limited cases, approval of a majority of the unitholders of Teekay Offshore is required to approve certain actions. As a result of a transaction with Brookfield, since September 25, 2017, Teekay Offshore is no longer a consolidated subsidiary of ours, but is instead accounted for under the equity method. Teekay Offshore’s general partner owns its incentive distribution rights. |

| (4) | Economic interests in Teekay LNG and Teekay Offshore are based on outstanding common units and common-unit equivalents represented by the general partner interests. |

| (5) | Includes, among others, subsidiaries owning Teekay Parent’s three FPSO units. |

Teekay Parent

Teekay Parent currently owns three FPSO units, two of which are on firm contracts to August and September 2020 and one of which is on alife-of-field contract. Teekay Parent is currently in discussions regarding and expects to obtain aone-year contract extension on thePetrojarl BanffFPSO unit to August 2020 and is currently in discussions with the charterers of the other two FPSO units on potential contract extensions and amendments or dispositions.

Our long-term vision is for Teekay Parent to be primarily a portfolio manager and project developer with the Teekay group’s fixed assets primarily owned directly by the Controlled Daughter Entities. Our primary financial objectives for Teekay Parent are to increase the value of the contracts for our three FPSO units and the value of our investments in Teekay LNG, Teekay Tankers and Teekay Offshore, increase Teekay Parent’s free cash flow and, as a service provider to the Daughter Entities, provide scale and other benefits across the Teekay group. We intend to (a) continue to reduce net debt of Teekay Parent, including by using the net proceeds from the potential sale of the three FPSO units or other assets in the future to repay debt and (b) seek to increase the distributions of Teekay LNG in a sustainable manner and the dividends of Teekay Tankers as the tanker market recovers.

Teekay LNG

Teekay LNG primarily provides LNG transportation services and includes all of our LNG andmid-size LPG carriers. LNG carriers are usually chartered to carry LNG pursuant to time-charter contracts, where a vessel is hired for a fixed period of time under atake-or-pay structure. LPG carriers are mainly chartered to carry LPG and ammonia ontake-or-pay time charter contracts, on contracts of affreightment or on spot voyage charters. As of April 1, 2019, Teekay LNG’s fleet of LNG carriers, including newbuildings on order, had a total cargo carrying capacity of approximately 8.0 million cubic meters.

Teekay LNG has a fleet of 79 vessels, including four newbuildings on order, and an interest in a regasification project in Bahrain. These four newbuildings and the regasification project are scheduled to commence operations under their respective long-term contracts in 2019. As of April 1, 2019, Teekay LNG had ownership interests ranging from 20% to 100% in 49 LNG carriers, including four newbuilding LNG carriers on order. In addition, Teekay LNG has 99% ownership interests in sevenmulti-gas carriers and 50% ownership interests, through its joint venture agreement with Exmar NV, in 22mid-size LPG carriers. Teekay LNG’s large and diverse portfolio of long-term contracts represented $10.1 billion of contracted, forward fixed-rate revenues with a revenue-weighted average remaining contract duration of approximately 11.5 years as of January 1, 2019 (excluding options to extend). Teekay’s LNG and LPG segments generated total consolidated revenues of $454.5 million and $23.9 million, respectively, in 2018 (which excludes revenue generated by vessels that are owned in equity-accounted joint ventures).

S-5

Table of Contents

Teekay Tankers

Teekay Tankers provides oil transportation services and includes a substantial majority of our conventional crude oil tankers and all of our product carriers. Teekay Tankers’ conventional crude oil tankers and product tankers primarily operate in the spot-tanker market under contracts that are priced on a spot-market basis or under short-term, fixed-rate contracts. Teekay Tankers considers contracts that have an original term of less than one year in duration to be short-term. Certain of Teekay Tankers’ conventional crude oil tankers and product tankers are on fixed-ratetake-or-pay time-charter contracts with an initial duration of at least one year.

Teekay Tankers’ vessels compete primarily in the Aframax and Suezmax tanker markets. Many major oil companies and other oil trading companies, the primary charterers of our vessels, also operate their own vessels and transport their own oil and oil for third-party charterers in direct competition with us and other independent owners and operators. Teekay Tankers competes principally in the global spot-charter market.

As of April 1, 2019, Teekay Tankers’ fleet included 62 owned andchartered-in tankers (excluding sixship-to-ship transfer support vessels). Teekay Tankers also owns aship-to-ship transfer business that primarily provides lightering and reverse lightering services for crude oil imports into, and exports out of, the United States. As of April 1, 2019, Teekay Tankers’ fleet had a total cargo carrying capacity of approximately 8.5 million deadweight tonnes (ordwt).

Teekay Offshore

Teekay Offshore provides oil production and logistics services to the offshore oil production industry in the North Sea, Brazil and the East Coast of Canada and includes FPSO units, shuttle tankers, floating storage and offtake (orFSO) units, a unit for maintenance and safety (orUMS), and long-distance towing and offshore installation vessels. Teekay Offshore primarily provides FPSO and shuttle tanker services. Shuttle tankers generally operate under long-term, fixed-rate time-charter contracts or bareboat charter contracts for a specific offshore oil field (where a vessel is hired for a fixed period of time) or under contracts of affreightment to service various fields. FPSO units generally operate under long-term contracts — often where the contract’s duration is for the useful life of the oil field — and with a fixed charter rate and, in some cases, a variable component based on oil prices or production by the unit.

As of April 1, 2019, Teekay Offshore had interests in eight FPSO units, 35 shuttle tankers (including six newbuilding shuttle tankers on order), six FSO units, one UMS and 10 long-distance towing and offshore installation vessels. Teekay Offshore’s ownership interests in these vessels range from 50% to 100%. Teekay Offshore’s large and diverse portfolio of long-term contracts represented $5.7 billion of contracted, forward fixed-rate revenues with a revenue-weighted average remaining contract duration of approximately four years as of January 1, 2019 (excluding options to extend). Teekay Offshore has approximately 2,000 seagoing and shore-based employees.

S-6

Table of Contents

The Offering

Issuer | Teekay Corporation |

Common stock offered by us | Shares of common stock having an aggregate offering price of up to $63,000,000. |

Use of proceeds | We intend to use the net proceeds from this offering, if any, after deducting the Agent’s commission and our offering expenses, for general corporate purposes, which may include, among other things, repaying a portion of our outstanding indebtedness. Please read “Use of Proceeds.” |

New York Stock Exchange Symbol | TK |

Risk factors | Investing in our common stock involves risks. You should carefully consider each of the factors described or referred to under “Risk Factors” beginning on pageS-8 of this prospectus supplement, page 4 of the accompanying prospectus and in the documents incorporated by reference into this prospectus supplement and accompanying prospectus before you make an investment in our common stock. |

S-7

Table of Contents

An investment in our common stock involves risk. Before investing in our common stock, you should carefully consider the following risk factors, together with all the information included or incorporated by reference in this prospectus, including the risks discussed under the heading “Risk Factors” in the accompanying prospectus, in our latest Annual Report on Form20-F filed with the SEC and incorporated by reference into this prospectus supplement. For more information, please read “Where You Can Find More Information” in the prospectus and “Incorporation of Documents by Reference” in this prospectus supplement. In addition, you should read “Material United States Federal Income Tax Considerations” in this prospectus supplement and in the accompanying prospectus for a more complete discussion of expected material U.S. federal income tax consequences of owning and disposing of our securities.

If any of these risks were to occur, our business, financial condition, operating results or cash flows could be materially adversely affected. The risks and uncertainties we have described are not the only ones we face.

Additional risks and uncertainties that are not yet identified may also materially harm our business, financial condition, operating results and cash flows. In that case, the trading price of our common stock could decline, you could lose all or part of your investment and our ability to pay dividends on shares of our common stock may be reduced or restricted.

U.S. tax authorities could treat us as a “passive foreign investment company,” which could have adverse U.S. federal income tax consequences to U.S. shareholders.

Anon-U.S. entity treated as a corporation for U.S. federal income tax purposes will be treated as a “passive foreign investment company” (orPFIC) for such purposes in any taxable year for which either (a) at least 75% of its gross income consists of “passive income,” or (b) at least 50% of the average value of the entity’s assets is attributable to assets that produce or are held for the production of “passive income.” For purposes of these tests, “passive income” includes dividends, interest, gains from the sale or exchange of investment property and rents and royalties other than rents and royalties that are received from unrelated parties in connection with the active conduct of a trade or business. By contrast, income derived from the performance of services does not constitute “passive income.”

There are legal uncertainties involved in determining whether the income derived from our time-chartering activities constitutes rental income or income derived from the performance of services, including the decision in Tidewater Inc. v. United States, 565 F.3d 299 (5th Cir. 2009), which held that income derived from certain time-chartering activities should be treated as rental income rather than services income for purposes of a foreign sales corporation provision of the Internal Revenue Code of 1986, as amended (or theCode). However, the Internal Revenue Service (or theIRS) stated in an Action on Decision (AOD2010-01) that it disagrees with, and will not acquiesce to, the way that the rental versus services framework was applied to the facts in the Tidewater decision, and in its discussion stated that the time charters at issue in Tidewater would be treated as producing services income for PFIC purposes. The IRS’s statement with respect to Tidewater cannot be relied upon or otherwise cited as precedent by taxpayers. Consequently, in the absence of any binding legal authority specifically relating to the statutory provisions governing PFICs, there can be no assurance that the IRS or a court would not follow the Tidewater decision in interpreting the PFIC provisions of the Code. Nevertheless, based on the current composition of our assets and operations (and those of our look-through subsidiaries), we intend to take the position that we are not now and have never been a PFIC, and our counsel, Perkins Coie LLP, is of the opinion that it is more likely than not we are not a PFIC based on representations we have made to them regarding the composition of our and our look-through subsidiaries’ assets, source of income and nature of activities and operations. No assurance can be given, however, that the opinion of Perkins Coie LLP would be sustained by a court if contested by the IRS, or that we would not constitute a PFIC for any future taxable year if there were to be changes in our assets, income or operations.

S-8

Table of Contents

If the IRS were to determine that we are or have been a PFIC for any taxable year during which a U.S. Holder (as defined below under “Material United States Federal Income Tax Considerations”) held stock, such U.S. Holder would face adverse U.S. federal income tax consequences. For a more comprehensive discussion regarding our status as a PFIC and the tax consequences to U.S. Holders if we are treated as a PFIC, please read “Material United States Federal Income Tax Considerations — United States Federal Income Taxation of U.S. Holders — Consequences of Possible PFIC Classification.”

We may be subject to taxes, which reduces our cash available for distribution to our shareholders.

We or some of our subsidiaries may be subject to tax in the jurisdictions in which we or our subsidiaries are organized or operate, reducing the amount of our cash available for distribution. In computing our tax obligation in these jurisdictions, we are required to take various tax accounting and reporting positions on matters that are not entirely free from doubt and for which we have not received rulings from the governing authorities. We cannot assure you that upon review of these positions the applicable authorities will agree with our positions. A successful challenge by a tax authority could result in additional tax imposed on us or our subsidiaries in jurisdictions in which operations are conducted. For example, if Teekay Corporation was not able to meet the criteria specified by Section 883 of the Code, our U.S. source income may become subject to taxation.

Teekay Tankers currently is not in compliance with the NYSE’s requirements for the continued listing of its Class A common stock on the exchange, which may adversely affect the value of shares of such stock owned by us.

Teekay Tankers’ Class A common stock is listed on the NYSE under the symbol “TNK”. On April 10, 2019, Teekay Tankers received written notice from the NYSE that Teekay Tankers is not in compliance with the NYSE continued listing standards because the average closing price of Teekay Tankers’ shares of Class A common stock fell below $1.00 per share over a period of 30 consecutive trading days. Teekay Tankers intends to cure the $1.00 per share deficiency and has six months following receipt of the noncompliance notice to regain compliance with the NYSE continued listing requirement. If Teekay Tankers fails to timely cure the noncompliance, the NYSE would delist the Class A common stock from the NYSE. Any such delisting would negatively impact Teekay Tankers and holders of the Class A common stock, including due to the resulting decreased price, liquidity and trading of the Class A common stock, limited availability of price quotations and reduced news and analyst coverage. These developments may also require brokers trading in the Class A common stock to adhere to more stringent rules and may limit Teekay Tankers’ ability to raise capital by issuing additional shares of Class A common stock in the future. Delisting may adversely impact the perception of Teekay Tankers’ financial condition and harm its reputation with investors and other third parties. In addition, any perceived decrease in value of employee equity incentive awards may reduce their effectiveness in encouraging performance and retention.

S-9

Table of Contents

We intend to use the net proceeds from this offering of shares of our common stock, if any, after deducting the Agent’s commission and our offering expenses, for general corporate purposes, which may include, among other things, repaying a portion of our outstanding indebtedness.

S-10

Table of Contents

The following table sets forth our historical capitalization on a consolidated basis as of December 31, 2018, and does not reflect the Note Offering or the Tender Offer.

The data in the table is derived from, and should be read in conjunction with, our historical financial statements, including accompanying notes, and the section entitled “Operating and Financial Review and Prospects — Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited consolidated financial statements as of and for the year ended December 31, 2018, and the notes thereto included in our latest Annual Report on Form20-F filed with the SEC and incorporated by reference herein.

| As of December 31, 2018 | ||||

| (in thousands) | ||||

Cash and cash equivalents(1) | $ | 424,169 | ||

Restricted cash | 81,470 | |||

|

| |||

Total cash and restricted cash | $ | 505,639 | ||

Debt(including current portion) | ||||

8.50% Senior Notes due 2020(2) | �� | 508,577 | ||

5.00% Convertible Senior Notes Due 2023 | 125,000 | |||

Obligations related to capital leases(3) | 1,673,845 | |||

Other long-term secured debt(3) | 2,153,277 | |||

Other long-term unsecured debt(3) | 576,273 | |||

Unamortized discount and debt issuance costs | (43,604 | ) | ||

|

| |||

Total debt(1) | $ | 4,993,368 | ||

Equity | ||||

Common stock and additionalpaid-in capital | 1,045,659 | |||

Accumulated deficit | (234,395 | ) | ||

Non-controlling interest | 2,058,037 | |||

Accumulated other comprehensive (loss) | (2,273 | ) | ||

Total equity | $ | 2,867,028 | ||

Total capitalization | $ | 7,354,757 | ||

|

| |||

| (1) | The following table reconciles our consolidated and Teekay Parent’s cash and cash equivalents and total debt, respectively, as of December 31, 2018. |

| As of December 31, 2018 | ||||||||||||

| (in thousands) | Teekay consolidated | Controlled Daughter Entities | Teekay Parent | |||||||||

Cash and cash equivalents | $ | 424,169 | $ | 203,931 | $ | 220,238 | ||||||

Total debt | 4,993,368 | 4,379,027 | 614,341 | |||||||||

|

|

|

|

|

| |||||||

| (2) | As of April 1, 2019, there was approximately $497.7 million in aggregate principal amount of 8.50% Senior Notes due 2020 outstanding. |

| (3) | Amounts do not reflect borrowings and repayments subsequent to December 31, 2018. From December 31, 2018 to April 22, 2019, we repaid, on a net basis, approximately $22 million of other long-term secured debt, entered into a sale and leaseback arrangement for an LNG carrier newbuilding that delivered in January 2019 which increased our obligations related to capital leases by approximately $159 million and extinguished $24 million of obligations related to capital leases related to the redelivery of theToledo Spirit to its owner. |

S-11

Table of Contents

General

We may issue common stock or preferred stock, in one or more distinct series, from time to time. This section summarizes the material terms of our common stock and material terms that would be common to all series of our preferred stock. The following description of our common stock, preferred stock and provisions of our Amended and Restated Articles of Incorporation, as amended (or Articles) and our Amended and Restated Bylaws (or Bylaws), are summaries and are qualified by reference to our Articles and our Bylaws, copies of which have been filed as exhibits to our Annual Report on Form 20-F for the year ended December 31, 2018, which is incorporated by reference herein.

Our authorized capital stock consists of 725 million shares of common stock, with a par value of $0.001 per share, and 25 million shares of preferred stock, with a par value of $1 per share. As of April 22, 2019, there were 100,684,489 shares of our common stock outstanding and no shares of preferred stock outstanding.

Exchange Listing

Shares of our common stock are listed on the New York Stock Exchange, where they trade under the symbol “TK.”

Transfer Agent and Registrar

Computershare Inc. serves as registrar and transfer agent for our common stock.

Common Stock

Each outstanding share of our common stock entitles the holder to one vote on all matters submitted to a vote of shareholders. Subject to preferences that may be applicable to any outstanding shares of our preferred stock, holders of common stock are entitled to receive ratably any dividends declared from time to time by our Board of Directors out of funds legally available therefor. Holders of our common stock generally do not have conversion, redemption or preemptive rights to subscribe for any of our securities. All outstanding shares of common stock are fully paid and nonassessable. The rights, preferences and privileges of holders of our common stock are subject to the rights of the holders of any shares of preferred stock that we may issue.

Preferred Stock

Our Board of Directors may from time to time, and without further action by our shareholders, direct the issuance of shares of preferred stock in one or more series and may, at the time of issuance, determine the rights, preference and limitations of each such series. Satisfaction of any dividend preferences of outstanding shares of preferred stock would reduce the amount of funds available for the payment of dividends on shares of common stock. Holders of shares of our preferred stock may be entitled to receive a preference payment in the event of any liquidation, dissolution or winding-up of Teekay Corporation before any payment is made to the holders of shares of our common stock. The voting, dividend, liquidation, redemption, conversion or other rights of any preferred stock we may issue could adversely affect the voting power and other rights of the holders of our common stock and may have the effect of decreasing the market price of our common stock. Under certain circumstances, the issuance of shares of our preferred stock may render more difficult or tend to discourage a merger, tender offer, proxy contest, the assumption of control by a holder of a large block of our securities or the removal of incumbent management.

S-12

Table of Contents

Anti-Takeover Provisions

Preferred Stock Authorization

As noted above, our Board of Directors, without shareholder approval, has the authority under our Articles to issue preferred stock with rights superior to the rights of the holders of common stock. As a result, preferred stock could be issued quickly and easily, could adversely affect the rights of holders of common stock and could be issued with terms calculated or which have a tendency to delay or prevent a change of control of Teekay Corporation or make removal of management more difficult.

Shareholder Rights Plan

We have an amended and restated shareholders rights agreement pursuant to which holders of our common stock have been granted one purchase right on each outstanding share of common stock. Each purchase right, when exercisable, initially entitles its registered holder to purchase from us one share of our common stock at a price of $200 per share, subject to certain anti-dilution adjustments. The purchase rights are not currently exercisable and will become exercisable only upon the earlier of:

| • | Ten days following a public announcement that a person became an “acquiring person,” which refers to a person who either (a) did not beneficially own 15% or more of our outstanding common stock on July 2, 2010 (the effective date of the amended and restated shareholder rights plan), and subsequently acquires beneficial ownership of 20% or more of our outstanding common stock, or (b) did beneficially own 15% or more of our outstanding common stock on July 2, 2010, and subsequently acquires beneficial ownership of an additional 5% or more of our outstanding common stock; or |

| • | Ten business days (or such later date as may be determined by action of the Board of Directors prior to such time as any person or group of affiliated persons becomes an acquiring person) following the commencement of, or announcement of an intention to make, a tender offer or exchange offer the consummation of which would result in a person or group becoming an acquiring person. |

Unless otherwise approved by our Board of Directors, if a person becomes an acquiring person, the purchase rights held at any time by the acquiring person and its affiliates will become null and void and nontransferable, and the remaining purchase rights will entitle each other right holder to purchase, for the purchase price, the number of shares of our common stock which at the time of the transaction would have a market value equal to twice the purchase price. Additionally, at any time prior to an acquiring person’s becoming the holder of 50% or more of our outstanding shares of common stock, our Board of Directors may exchange the purchase rights (other than the purchase rights owned by the acquiring person and its affiliates), at an exchange ratio of one share of our common stock per purchase right.

After a person becomes an acquiring person, each of the following events would entitle each holder of a purchase right (other than the acquiring person and its affiliates) to purchase, for the purchase price, that number of shares of common stock of another corporation which at the time of the event would have a market value equal to twice the purchase price:

| • | the acquisition of us in a merger by such other corporation; |

| • | a business combination between us and such other corporation; or |

| • | the sale, lease, exchange or transfer of 50% or more of our assets or assets accounting for 50% or more of our net income or revenues, in one or more transactions. |

At any time prior to the earlier of a triggering offer or any person becoming an acquiring person, our Board of Directors may redeem the purchase rights in whole, but not in part, at a price of $0.0001 per purchase right. In addition, the Board of Directors may also waive, within a specified period, the effect of such triggering event or a person being an acquiring person.

S-13

Table of Contents

The purchase rights have certain anti-takeover effects and will cause substantial dilution to a person or group that attempts to acquire us on terms not approved by our Board of Directors. The purchase rights will not interfere with any merger or other business combination approved by our Board of Directors, since the Board of Directors may, at its option, authorize Teekay Corporation to redeem all of the then-outstanding purchase rights or waive the application of the shareholder rights plan in connection with a specific transaction. The shareholder rights plan and the rights expire in July 2020. The description and terms of the purchase rights are set forth in our Amended and Restated Rights Agreement that is filed as an exhibit to the Registration Statement onForm 8-A/A filed on July 2, 2010, which is incorporated by reference into this prospectus.

Shareholder Meetings, Quorum, and Voting

Our Bylaws establish advance notice procedures with respect to business brought before an annual meeting by a shareholder and the nomination of candidates for election as directors, other than nominations made by or at the direction of our Board of Directors. Under our Bylaws, special meetings of the shareholders may be called only by our Board of Directors. No business other than that stated in the notice of meeting may be transacted at any special meeting. Our Articles provide that a majority of the shares entitled to vote on any matter shall constitute a quorum at a meeting of shareholders, unless the matter has been submitted to the shareholders at any meeting and recommended by a majority of our Continuing Directors (as defined in our Articles), in which case one-third of the shares entitled to vote on the matter shall constitute a quorum.

Election of Directors

Our Bylaws provide for a “staggered board,” with our Board of Directors divided into three classes, as nearly equal in number as possible, and the directors in each class serving three-year terms and one class being elected each year by our shareholders. Vacancies on the Board of Directors are filled by our Board of Directors. Because this system of electing directors and filling vacancies generally makes it more difficult for shareholders to replace a majority of the Board of Directors, it may tend to discourage a third party from making a tender offer or otherwise attempting to gain control of us.

Other Matters

Sales of Assets, Mergers and Dissolution

Under the Marshall Islands Business Corporations Act, the sale, lease, exchange or other disposition of all or substantially all of Teekay Corporation’s assets not made in the usual or regular course of Teekay Corporation’s business or the non-judicial dissolution and liquidation of Teekay Corporation are required to be approved by the holders of two-thirds of the outstanding shares of our capital stock entitled to vote on such matter; in addition, non-judicial dissolution approved, if approved by written consent, must be approved by a unanimous written consent of all holders of capital stock entitled to vote on the matter. In addition, the holders of one-half of the outstanding shares of capital stock entitled to vote in an election of directors may institute judicial dissolution proceedings in specified circumstances in accordance with the Marshall Islands Business Corporations Act. In the event of the dissolution of Teekay Corporation, the holders of our common stock will be entitled to share pro rata in our net assets available for distribution to them, after payment to all creditors and the liquidation preferences of any of our outstanding preferred stock.

Under the Marshall Islands Business Corporations Act, a merger or consolidation involving Teekay Corporation (other than with certain subsidiaries at least 90% of whose shares of each class are owned by Teekay Corporation) is required to be approved by the holders of a majority of the outstanding shares of our capital stock entitled to vote on the matter.

A class of shares may be entitled to vote separately as a class on various corporate activities. The vote for such class will be determined by the Marshall Islands Business Corporations Act and, if applicable, our articles of incorporation and bylaws.

S-14

Table of Contents

Dissenters’ Rights of Appraisal and Payment

Under the Marshall Islands Business Corporations Act, shareholders have the right to dissent from various corporate actions, including certain mergers or sales, leases, exchanges or other dispositions of all or substantially all of our assets not made in the usual course of our business, and receive payment of the fair value of their shares. The right of a dissenting shareholder to receive payment of the fair value of such shareholder’s shares shall not be available for the shares of any class or series of stock, which shares, at the record date fixed to determine the shareholders entitled to receive notice of and to vote at the meeting of shareholders to act upon the agreement of merger or consolidation or any sale or exchange of all or substantially all of the property and assets of the corporation not made in the usual course of its business, were either (i) listed on a securities exchange or admitted for trading on an interdealer quotation system or (ii) held of record by more than 2,000 holders. In the event of any further amendment of our articles of incorporation, a shareholder also has the right to dissent and receive payment for his or her shares if the amendment alters, creates or abolishes certain rights in respect of those shares. A condition for such payment is that the dissenting shareholders follow the procedures set forth in the Marshall Islands Business Corporations Act. In the event that we (or the surviving entity in a merger) fail to agree with any dissenting shareholder on a price for the shares, such procedures involve, among other things, the institution of court proceedings in either the Republic of the Marshall Islands or the country where our shares are primarily traded, which is the United States. The value of the shares of a dissenting shareholder is fixed by the court after reference, if the court so elects, to the recommendations of a court-appointed appraiser.

Amendment of Articles of Incorporation

Under the Marshall Islands Business Corporations Act, amendments to the articles of incorporation of a Republic of the Marshall Islands corporation generally may be authorized upon approval of the holders of a majority of all outstanding shares entitled to vote. The approval of the holders of a majority of the outstanding shares of an adversely affected class or series of stock is also required for certain amendments.

Limitations on Ownership and Dividends

Neither Republic of the Marshall Islands law nor our Articles or Bylaws limit the right to own our securities, including the rights of non-resident or foreign shareholders to hold or exercise voting rights on the securities. Certain of our debt facilities, and Republic of the Marshall Islands law, impose limitations on our ability to pay dividends.

S-15

Table of Contents

MATERIAL UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS

The following is a discussion of the material U.S. federal income tax considerations that may be relevant to prospective shareholders and, unless otherwise noted in the following discussion, is the opinion of Perkins Coie LLP, our U.S. counsel, insofar as it relates to matters of U.S. federal income tax law and legal conclusions with respect to those matters. The opinion of our counsel is dependent on the accuracy of representations made by us to them, including descriptions of our operations contained herein. This discussion is based upon the provisions of the Code, legislative history, applicable U.S. Treasury Regulations (orTreasury Regulations), judicial authority and administrative interpretations, all as in effect on the date of this prospectus, and which are subject to change, possibly with retroactive effect, or are subject to different interpretations. Changes in these authorities may cause the tax consequences to vary substantially from the consequences described below. Unless the context otherwise requires, references in this section to “we,” “our” or “us” are references to Teekay Corporation.

This discussion is limited to shareholders who hold their common stock as a capital asset for tax purposes. This discussion does not address all tax considerations that may be important to a particular shareholder in light of the shareholder’s circumstances, or to certain categories of shareholders that may be subject to special tax rules, such as:

| • | dealers in securities or currencies; |

| • | traders in securities that have elected themark-to-market method of accounting for their securities; |

| • | persons whose functional currency is not the U.S. dollar; |

| • | persons holding our common stock as part of a hedge, straddle, conversion or other “synthetic security” or integrated transaction; |

| • | certain U.S. expatriates; |

| • | financial institutions; |

| • | insurance companies; |

| • | persons subject to the alternative minimum tax; |

| • | persons that actually or under applicable constructive ownership rules own 10% or more of our stock (by vote or value); and |

| • | entities that aretax-exempt for U.S. federal income tax purposes. |

If a partnership (including any entity or arrangement treated as a partnership for U.S. federal income tax purposes) holds our common stock, the tax treatment of a partner generally will depend upon the status of the partner and the activities of the partnership. Partners in partnerships holding our common stock should consult their tax advisors to determine the appropriate tax treatment of the partnership’s ownership of our common stock.

No ruling has been or will be requested from the IRS regarding any matter affecting us or our shareholders. Instead, we will rely on the opinion of Perkins Coie LLP. Unlike a ruling, an opinion of counsel represents only that counsel’s legal judgment and does not bind the IRS or the courts. Accordingly, the opinions and statements made herein may not be sustained by a court if contested by the IRS.

This discussion does not address any U.S. estate tax considerations or tax considerations arising under the laws of any state, local ornon-U.S. jurisdiction. Each shareholder is urged to consult its tax advisor regarding the U.S. federal, state, local,non-U.S. and other tax consequences of the ownership or disposition of our common stock.

United States Federal Income Taxation of U.S. Holders

As used herein, the termU.S. Holder means a beneficial owner of our common stock that is, for U.S. federal income tax purposes: (a) a U.S. citizen or U.S. resident alien (or aU.S. Individual Holder), (b) a corporation or

S-16

Table of Contents

other entity taxable as a corporation that was created or organized under the laws of the United States, any state thereof or the District of Columbia, (c) an estate whose income is subject to U.S. federal income taxation regardless of its source, or (d) a trust that either is subject to the supervision of a court within the United States and has one or more U.S. persons with authority to control all of its substantial decisions or has a valid election in effect under applicable Treasury Regulations to be treated as a U.S. person.

Distributions

Subject to the discussion of passive foreign investment companies (orPFICs) below, any distributions made by us to a U.S. Holder generally will constitute dividends, which may be taxable as ordinary income or “qualified dividend income” as described in more detail below, to the extent of our current and accumulated earnings and profits, as determined under U.S. federal income tax principles. Distributions in excess of our current and accumulated earnings and profits will be treated first as a nontaxable return of capital to the extent of the U.S. Holder’s tax basis in our common stock and thereafter as capital gain, which will be either long term or short term capital gain depending upon whether the U.S. Holder has held the common stock for more than one year. U.S. Holders that are corporations for U.S. federal income tax purposes generally will not be entitled to claim a dividends received deduction with respect to any distributions they receive from us. For purposes of computing allowable foreign tax credits for U.S. federal income tax purposes, dividends received with respect to our common stock will be treated as foreign source income and generally will be treated as “passive category income”.

Subject to holding period requirements and certain other limitations, dividends received with respect to our common stock by a U.S. Holder who is an individual, trust or estate (aNon-Corporate U.S. Holder) will be treated as “qualified dividend income” that is taxable to suchNon-Corporate U.S. Holder at preferential capital gain tax rates provided that we are not classified as a PFIC for the taxable year during which the dividend is paid or the immediately preceding taxable year (we intend to take the position that we are not now and have never been classified as a PFIC, as discussed below). Any dividends received with respect to our common stock not eligible for these preferential rates will be taxed as ordinary income to aNon-Corporate U.S. Holder.

Special rules may apply to any “extraordinary dividend” paid by us. Generally, an extraordinary dividend is a dividend with respect to a share of common stock if the amount of the dividend is equal to or in excess of 10% of a common stockholder’s adjusted tax basis (or fair market value in certain circumstances) in such common stock. In addition, extraordinary dividends include dividends received within a one year period that, in the aggregate, equal or exceed 20% of a stockholder’s adjusted tax basis (or fair market value in certain circumstances). If we pay an “extraordinary dividend” on our common stock that is treated as “qualified dividend income,” then any loss recognized by aNon-Corporate U.S. Holder from the sale or exchange of such common stock will be treated as long-term capital loss to the extent of the amount of such dividend.

CertainNon-Corporate U.S. Holders are subject to a 3.8% tax on certain investment income, including dividends.Non-Corporate U.S. Holders should consult their tax advisors regarding the effect, if any, of this tax on their ownership of our common stock.

Sale, Exchange or Other Disposition of Common Stock

Subject to the discussion of PFICs below, a U.S. Holder generally will recognize capital gain or loss upon a sale, exchange or other disposition of our common stock in an amount equal to the difference between the amount realized by the U.S. Holder from such sale, exchange or other disposition and the U.S. Holder’s tax basis in such stock. Subject to the discussion of extraordinary dividends above, such gain or loss generally will be treated as (a) long-term capital gain or loss if the U.S. Holder’s holding period is greater than one year at the time of the sale, exchange or other disposition, or short term capital gain or loss otherwise and (b) U.S. source gain or loss, as applicable, for foreign tax credit purposes.Non-Corporate U.S. Holders may be eligible for preferential

S-17

Table of Contents

rates of U.S. federal income tax in respect of long-term capital gains. A U.S. Holder’s ability to deduct capital losses is subject to certain limitations.

CertainNon-Corporate U.S. Holders are subject to a 3.8% tax on certain investment income, including capital gains from the sale or other disposition of stock.Non-Corporate U.S. Holders should consult their tax advisors regarding the effect, if any, of this tax on their disposition of our common stock.

Consequences of Possible PFIC Classification

Anon-U.S. entity treated as a corporation for U.S. federal income tax purposes will be treated as a PFIC in any taxable year in which, after taking into account the income and assets of the corporation and, pursuant to a “look through” rule, any other corporation in which the corporation directly or indirectly owns at least 25% of the stock (by value), either: (a) at least 75% of its gross income is “passive” income; or (b) at least 50% of the average value of its assets is attributable to assets that produce or are held for the production of passive income. For purposes of these tests, “passive income” includes dividends, interest, gains from the sale or exchange of investment property and rents and royalties (other than rents and royalties that are received from unrelated parties in connection with the active conduct of a trade or business). By contrast, income derived from the performance of services does not constitute “passive income.”

There are legal uncertainties involved in determining whether the income derived from our time-chartering activities constitutes rental income or income derived from the performance of services, including legal uncertainties arising from the decision inTidewater Inc. v. United States, 565 F.3d 299 (5th Cir. 2009), which held that income derived from certain time-chartering activities should be treated as rental income rather than services income for purposes of a foreign sales corporation provision of the Code. However, the IRS stated in an Action on Decision (AOD2010-01) that it disagrees with, and will not acquiesce to, the way that the rental versus services framework was applied to the facts in theTidewaterdecision, and in its discussion stated that the time charters at issue inTidewaterwould be treated as producing services income for PFIC purposes. The IRS’s statement with respect toTidewatercannot be relied upon or otherwise cited as precedent by taxpayers. Consequently, in the absence of any binding legal authority specifically relating to the statutory provisions governing PFICs, there can be no assurance that the IRS or a court would not follow theTidewaterdecision in interpreting the PFIC provisions of the Code. Moreover, the market value of our common stock and our publicly traded subsidiaries may be treated as reflecting the value of our assets, and our publicly traded subsidiaries’ assets, respectively, at any given time. Therefore, a decline in the market value of our common stock, or our publicly traded subsidiaries, which is not within our control, may impact the determination of whether we are a PFIC. Nevertheless, based on our and our look-through subsidiaries’ current assets and operations, we intend to take the position that we are not now and have never been a PFIC, and our counsel, Perkins Coie LLP, is of the opinion that it is more likely than not that we are not a PFIC based on applicable law, including the Code, legislative history, published revenue rulings and court decisions, and representations we have made to them regarding the composition of our and our look-through subsidiaries’ assets, source of income and nature of activities and other operations, including:

the total payments due to us under each of our time charters are substantially in excess of the current bareboat charter rate for comparable vessels;

the income derived from our participation in pooling arrangements and from our other time and voyage charters will be greater than 25% of our total gross income at all relevant times; and

the gross value of our vessels participating in pooling arrangements and servicing our other time and voyage charters will exceed the gross value of all other assets we own at all relevant times.

An opinion of counsel represents only that counsel’s best legal judgment and does not bind the IRS or the courts. Accordingly, the opinion of Perkins Coie LLP may not be sustained by a court if contested by the IRS. Further, no assurance can be given that we would not constitute a PFIC for any future taxable year if there were to be changes in our or our subsidiaries’ assets, income or operations.

S-18

Table of Contents

As discussed more fully below, if we were to be treated as a PFIC for any taxable year, a U.S. Holder generally would be subject to different taxation rules depending on whether the U.S. Holder makes a timely and effective election to treat us as a “Qualified Electing Fund” (or aQEF election). As an alternative to making a QEF election, a U.S. Holder should be able to make a“mark-to-market” election with respect to our common stock, as discussed below.

Taxation of U.S. Holders Making a Timely QEF Election

A U.S. Holder who makes a timely QEF election (anElecting Holder) must report the Electing Holder’s pro rata share of our ordinary earnings and net capital gain, if any, for each taxable year for which we are a PFIC that ends with or within the Electing Holder’s taxable year, regardless of whether or not the Electing Holder received distributions from us in that year. Such income inclusions would not be eligible for the preferential tax rates applicable to qualified dividend income. The Electing Holder’s adjusted tax basis in our common stock will be increased to reflect taxed but undistributed earnings and profits. Distributions of earnings and profits that were previously taxed will result in a corresponding reduction in the Electing Holder’s adjusted tax basis in our common stock and will not be taxed again once distributed. An Electing Holder generally will recognize capital gain or loss on the sale, exchange or other disposition of our common stock. A U.S. Holder makes a QEF election with respect to any year that we are a PFIC by filing IRS Form 8621 with the U.S. Holder’s timely filed U.S. federal income tax return (including extensions).

If a U.S. Holder has not made a timely QEF election with respect to the first year in the U.S. Holder’s holding period of our common stock during which we qualified as a PFIC, the U.S. Holder may be treated as having made a timely QEF election by filing a QEF election with the U.S. Holder’s timely filed U.S. federal income tax return (including extensions) and, under the rules of Section 1291 of the Code, a “deemed sale election” to include in income as an “excess distribution” (described below) the amount of any gain that the U.S. Holder would otherwise recognize if the U.S. Holder sold the U.S. Holder’s common stock on the “qualification date.” The qualification date is the first day of our taxable year in which we qualified as a “qualified electing fund” with respect to such U.S. Holder. In addition to the above rules, under very limited circumstances, a U.S. Holder may make a retroactive QEF election if the U.S. Holder failed to file the QEF election documents in a timely manner. If a U.S. Holder makes a timely QEF election for one of our taxable years, but did not make such election with respect to the first year in the U.S. Holder’s holding period of our common stock during which we qualified as a PFIC and the U.S. Holder did not make the deemed sale election described above, the U.S. Holder also will be subject to the more adverse rules described below.

A U.S. Holder’s QEF election will not be effective unless we annually provide the U.S. Holder with certain information concerning our income and gain, calculated in accordance with the Code, to be included with the U.S. Holder’s U.S. federal income tax return. We have not provided our U.S. Holders with such information in prior taxable years and do not intend to provide such information in the current taxable year. Accordingly, U.S. Holders will not be able to make an effective QEF election at this time. If, contrary to our expectations, we determine that we are or will be a PFIC for any taxable year, we will provide U.S. Holders with the information necessary to make an effective QEF election with respect to our common stock.

Taxation of U.S. Holders Making a“Mark-to-Market” Election

If we were to be treated as a PFIC for any taxable year and, as we anticipate, our common stock was treated as “marketable stock,” then, as an alternative to making a QEF election, a U.S. Holder would be allowed to make a“mark-to-market” election with respect to our common stock, provided the U.S. Holder completes and files IRS Form 8621 in accordance with the relevant instructions and related Treasury Regulations. If that election is made for the first year a U.S. Holder holds or is deemed to hold our common stock and for which we are a PFIC, the U.S. Holder generally would include as ordinary income in each taxable year that we are a PFIC the excess, if any, of the fair market value of the U.S. Holder’s common stock at the end of the taxable year over the U.S. Holder’s adjusted tax basis in the common stock. The U.S. Holder also would be permitted an ordinary loss in

S-19

Table of Contents

respect of the excess, if any, of the U.S. Holder’s adjusted tax basis in the common stock over the fair market value thereof at the end of the taxable year that we are a PFIC, but only to the extent of the net amount previously included in income as a result of themark-to-market election. A U.S. Holder’s tax basis in our common stock would be adjusted to reflect any such income or loss recognized. Gain recognized on the sale, exchange or other disposition of our common stock in taxable years that we are a PFIC would be treated as ordinary income, and any loss recognized on the sale, exchange or other disposition of our common stock in taxable years that we are a PFIC would be treated as ordinary loss to the extent that such loss does not exceed the netmark-to-market gains previously included in income by the U.S. Holder. Because themark-to-market election only applies to marketable stock, however, it would not apply to a U.S. Holder’s indirect interest in any of our subsidiaries that were also determined to be PFICs.

If a U.S. Holder makes amark-to-market election for one of our taxable years and we were a PFIC for a prior taxable year during which such U.S. Holder held our common stock and for which (a) we were not a QEF with respect to such U.S. Holder and (b) such U.S. Holder did not make a timelymark-to-market election, such U.S. Holder would also be subject to the more adverse rules described below in the first taxable year for which themark-to-market election is in effect and also to the extent the fair market value of the U.S. Holder’s common stock exceeds the U.S. Holder’s adjusted tax basis in the common stock at the end of the first taxable year for which themark-to-market election is in effect.

Taxation of U.S. Holders Not Making a Timely QEF orMark-to-Market Election

If we were to be treated as a PFIC for any taxable year, a U.S. Holder who does not make either a QEF election or a“mark-to-market” election for that year (aNon-Electing Holder) would be subject to special rules resulting in increased tax liability with respect to (a) any “excess distribution” (i.e., the portion of any distributions received by theNon-Electing Holder on our common stock in a taxable year in excess of 125% of the average annual distributions received by theNon-Electing Holder in the three preceding taxable years, or, if shorter, theNon-Electing Holder’s holding period for our common stock), and (b) any gain realized on the sale, exchange or other disposition of our common stock. Under these special rules:

the excess distribution or gain would be allocated ratably over theNon-Electing Holder’s aggregate holding period for our common stock;

the amount allocated to the current taxable year and any taxable year prior to the taxable year we were first treated as a PFIC with respect to theNon-Electing Holder would be taxed as ordinary income in the current taxable year;

the amount allocated to each of the other taxable years would be subject to U.S. federal income tax at the highest rate of tax in effect for the applicable class of taxpayer for that year; and

an interest charge for the deemed deferral benefit would be imposed with respect to the resulting tax attributable to each such other taxable year.

Additionally, for each year during which a U.S. Holder holds our common stock, we are a PFIC, and the total value of all PFIC stock that such U.S. Holder directly or indirectly holds exceeds certain thresholds, such U.S. Holder will be required to file IRS Form 8621 with its annual U.S. federal income tax return to report its ownership of our common stock. In addition, if aNon-Electing Holder who is an individual dies while owning our common stock, suchNon-Electing Holder’s successor generally would not receive astep-up in tax basis with respect to such common stock.

S-20

Table of Contents

U.S. Holders are urged to consult their tax advisors regarding the PFIC rules, including the PFIC annual reporting requirements, as well as the applicability, availability and advisability of, and procedure for, making QEF,mark-to-market and other available elections with respect to us and our subsidiaries, and the U.S. federal income tax consequences of making such elections.

U.S. Return Disclosure Requirements for U.S. Individual Holders

U.S. Individual Holders who hold certain specified foreign financial assets, including stock in a foreign corporation that is not held in an account maintained by a financial institution, with an aggregate value in excess of $50,000 on the last day of a taxable year, or $75,000 at any time during that taxable year, may be required to report such assets on IRS Form 8938 with their U.S. federal income tax return for that taxable year. This reporting requirement does not apply to U.S. Individual Holders who report their ownership of our common stock under the PFIC annual reporting rules described above. Penalties apply for failure to properly complete and file IRS Form 8938. U.S. Individual Holders are encouraged to consult with their tax advisors regarding the possible application of this disclosure requirement to their investment in our common stock.

United States Federal Income Taxation ofNon-U.S. Holders

A beneficial owner of our common stock (other than a partnership, including any entity or arrangement treated as a partnership for U.S. federal income tax purposes) that is not a U.S. Holder is aNon-U.S. Holder.

Distributions

In general, aNon-U.S. Holder will not be subject to U.S. federal income tax on distributions received from us with respect to our common stock unless the distributions are effectively connected with theNon-U.S. Holder’s conduct of a trade or business within the United States (and, if required by an applicable income tax treaty, are attributable to a permanent establishment that theNon-U.S. Holder maintains in the United States). If aNon-U.S. Holder is engaged in a trade or business within the United States and the distributions are deemed to be effectively connected to that trade or business (and, if required by an applicable income tax treaty, are attributable to a permanent establishment that theNon-U.S. Holder maintains in the United States), theNon-U.S. Holder generally will be subject to U.S. federal income tax on those distributions in the same manner as if it were a U.S. Holder. In addition, aNon-U.S. Holder that is a foreign corporation for U.S. federal income tax purposes may be subject to branch profits tax at a rate of 30% (or lower applicable treaty rate) on theafter-tax earnings and profits attributable to such distributions.

Sale, Exchange or Other Disposition of Common Stock