EXHIBIT 99.2

| TABLE OF | ||||||||

¢¢ | CONTENTS | |||||||

| About CMHC | 7 | |||||||

| ¡ | Message from the Chairperson | 8 | ||||||

| ¡ | Message from the President | 11 | ||||||

| Corporate Governance | 17 | |||||||

| ¡ | Corporate Structure | 18 | ||||||

| ¡ | Board of Directors and its Committees | 18 | ||||||

| ¡ | Corporate Planning and Reporting | 20 | ||||||

| ¡ | Special Examinations and Annual Reviews | 21 | ||||||

| ¡ | Assessing Board Performance | 21 | ||||||

| ¡ | Board Compensation and Attendance | 22 | ||||||

| ¡ | CMHC Pension Fund | 22 | ||||||

| Corporate Responsibility | 23 | |||||||

| Management’s Discussion and Analysis | 37 | |||||||

| ¡ | The Operating Environment in 2012 and Outlook for 2013 | 38 | ||||||

| ¡ | Summary of Financial Results | 42 | ||||||

| ¡ | Performance by Objective | 51 | ||||||

| ¡ | Risk Management | 85 | ||||||

| ¡ | Human Resources and Internal Services | 94 | ||||||

| ¡ | 2008 to 2013 Financial Highlights | 98 | ||||||

| Consolidated Financial Statements | 99 | |||||||

| Other Information | 157 | |||||||

| ¡ | CMHC Board of Directors | 158 | ||||||

| ¡ | CMHC Management | 161 | ||||||

| ¡ | Use of Appropriations | 163 | ||||||

| ¡ | Glossary | 164 | ||||||

| ¡ | Definition of Select Performance Measures | 168 | ||||||

| ¡ | Expected Outcomes and Indicators | 170 | ||||||

| ¡ | CMHC Offices | 174 | ||||||

| For a list of acronyms used in this Annual Report, see Glossary. | ||||||||

| Performance by Objective |  | |||||||||

| ||||||||||

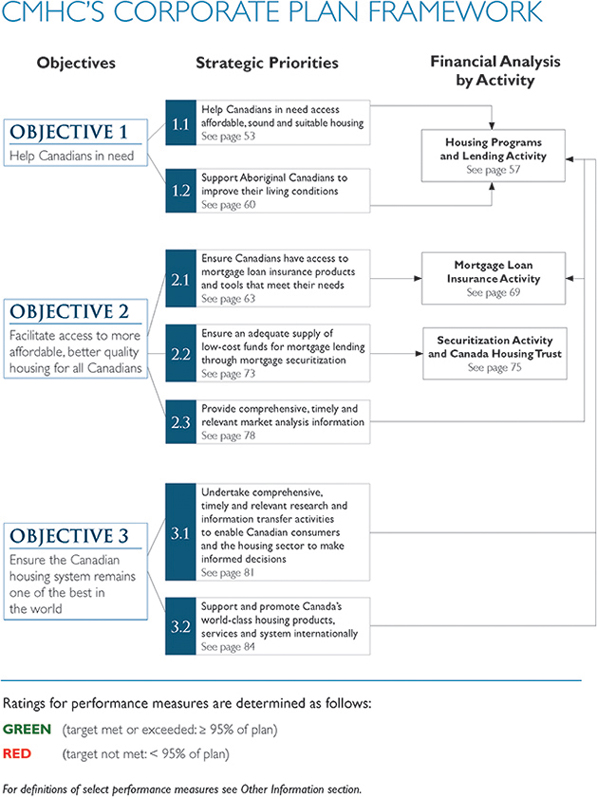

Corporate Plan Framework |

|

52

|

| |||||||

| Objective 1: | ||||||||||

| Help Canadians in need | 53 | |||||||||

Strategic Priority 1.1: | ||||||||||

Help Canadians in need access affordable, sound and suitable housing | ||||||||||

Strategic Priority 1.2: | ||||||||||

Support Aboriginal Canadians to improve their living conditions | ||||||||||

Objective 2: | ||||||||||

| Facilitate access to more affordable, better quality housing for all Canadians |

|

63 |

| |||||||

| Strategic Priority 2.1: | ||||||||||

Ensure Canadians have access to mortgage loan insurance products and tools that meet their needs | ||||||||||

| Strategic Priority 2.2: | ||||||||||

Ensure an adequate supply of low-cost funds for mortgage lending through mortgage securitization | ||||||||||

| Strategic Priority 2.3: | ||||||||||

Provide comprehensive, timely and relevant market analysis information | ||||||||||

| Objective 3: | ||||||||||

Ensure the Canadian housing system remains one of the best in the world | 81 | |||||||||

| Strategic Priority 3.1: | ||||||||||

Undertake comprehensive, timely and relevant research and information transfer activities to enable Canadian consumers and the housing sector to make informed decisions | ||||||||||

| Strategic Priority 3.2: | ||||||||||

Support and promote Canada’s world-class housing products, services and system internationally

| ||||||||||

CORPORATE STRUCTURE | 18 | |||

BOARD OF DIRECTORS AND ITS COMMITTEES | 18 | |||

CORPORATE PLANNING AND REPORTING | 20 | |||

SPECIAL EXAMINATIONS AND ANNUAL REVIEWS | 21 | |||

BOARD PERFORMANCE | 21 | |||

BOARD COMPENSATION AND ATTENDANCE | 22 | |||

CMHC PENSION FUND | 22 | |||

17

CORPORATE STRUCTURE

CMHC is governed by a Board of Directors appointed by the Government of Canada and currently reports to Parliament through the Minister of Human Resources and Skills Development. CMHC Management is comprised of the President and Chief Executive Officer, heads of business areas and support functions and General Managers of regional business centres. (See Other Information section for a list of CMHC Management members.) We have a workforce of approximately 1,900 employees. Our national office is located in Ottawa and our regional business centres are in Halifax, Montréal, Toronto, Calgary and Vancouver. Several smaller communities are served by CMHC employees who reside in these communities.

CMHC provides management, advisory and other services to the Canada Housing Trust (CHT) and to the First Nations Market Housing Fund (FNMHF). It also manages and administers Granville Island on behalf of the Government of Canada. (See Glossary for further information on these organizations.)

BOARD OF DIRECTORS AND ITS COMMITTEES

Pursuant to the CMHC Act, the stewardship of the Corporation is the responsibility of the Board of Directors which is comprised of the Chairperson, the President and Chief Executive Officer (CEO), the Deputy Minister of the Minister for CMHC, the Deputy Minister of Finance, and eight other directors.

The Chairperson and the President and CEO are appointed by the Governor in Council. The Deputy Minister of the Minister of CMHC and the Deputy Minister of Finance are members of the Board of Directors by reason of the office they each hold. The eight other directors are appointed by the Minister designated for the purposes of the CMHC Act and the NHA with the approval of the Governor in Council. With the exception of the President and CEO, all CMHC Board members are independent of CMHC Management.

The Board meets a minimum of five times per year. In order to gain regional perspective, the Board holds two of its regularly scheduled meetings outside

18 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

the National Capital Region. These meetings are opportunities for Board members to visit housing projects and to discuss issues with local stakeholders.

The Corporate Governance and Nominating Committee, the Audit Committee, the Risk Management Committee, and the Human Resources

Committee support the Board in carrying out its stewardship of CMHC. These committees examine matters in their respective areas that come before the Board for consideration. Their respective charters are posted on CMHC’s website and are reviewed on a regular basis by the Board to ensure these committees continue to carry out their responsibilities effectively.

MEETING WITH CANADIANS

Regional Board Meetings

This year, while in Toronto in May, the Board met with local representatives of the real estate development and construction sectors, municipal housing agencies, non-profit housing providers, mortgage lenders and First Nations. Among the housing projects visited by the Board was the historic downtown Toronto neighbourhood of Regent Park which received federal and provincial funding under the Affordable Housing Initiative and is in the midst of a remarkable rejuvenation.

While in Quebec City in August, the Board visited a number of housing developments serving diverse community needs, including a co-operative that receives subsidies from CMHC. The Board also visited a housing development which incorporated sustainable practices. In addition, the Board discussed local housing issues at a roundtable meeting with representatives from provincial and municipal housing agencies, the lending industry and First Nations communities.

The Annual Public Meeting

In conjunction with the Board of Directors meeting in Toronto, CMHC held its fourth Annual Public Meeting on May 24, 2012. CMHC’s Annual Public Meeting provides an opportunity for the general public to learn about CMHC’s achievements and to raise questions or concerns. Presentations by the Chairperson and the President and Chief Executive Officer provided an overview of CMHC’s mandate and highlighted the Corporation’s results and accomplishments.

19

CORPORATE PLANNING

AND REPORTING

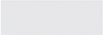

Each year, as required by the Financial Administration Act (FAA), CMHC submits a five-year plan to its Minister for approval by the Government of Canada. The corporate plan is the centrepiece of the accountability regime for Crown corporations and encompasses all of CMHC’s activities, budgets and resource requirements.

Taking into account Government of Canada objectives and priorities, the development of the corporate plan begins with a thorough examination of both the internal and external operating environments of the Corporation. In the development of the 2013-2017 Corporate Plan, the Board of Directors’ planning session in March 2012 examined global and national trends in order to assess their potential impact on CMHC’s operations. The Board determined key directions for the upcoming year and submitted to the Minister for CMHC, the Corporation’s proposed 2013-2017 Corporate Plan, which was subsequently

approved by the Government on December 13, 2012. A Summary of the Plan was tabled in Parliament on March 22, 2013.

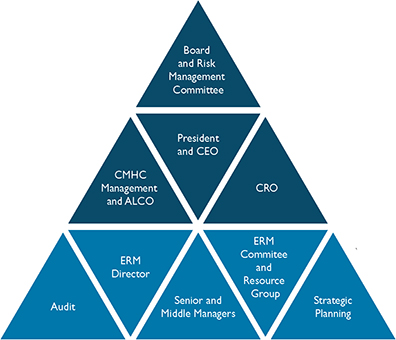

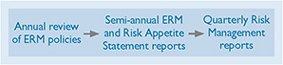

Through the year, the Board reviews Quarterly Performance Reports and adjusts priorities and resources accordingly. Quarterly Financial Reports are published sixty days after the end of each of the first three quarters of the year pursuant to the FAA. The Board, with the support of the Risk Management Committee of the Board, reviews significant risks and mitigating strategies through a variety of mechanisms, including through semi-annual Enterprise Risk Management reports and Quarterly Risk Management Reports. (Also see section on Risk Management in the MD&A.)

An annual report is prepared and submitted to the Minister for CMHC three months following the close of the financial year (December 31) and is tabled in Parliament 15 sitting days after the Minister’s receipt.

20 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

SPECIAL EXAMINATIONS AND ANNUAL REVIEWS

The Financial Administration Act (FAA) requires that a special examination be carried out at least once every ten years and at any additional time that the Governor in Council, the appropriate Minister, the Board of Directors, or the Auditor General may require. In its last special examination report dated August 25, 2008, CMHC received an unqualified opinion, meaning that the examiners found no significant deficiencies in the systems and practices of the Corporation.

Under amendments to the NHA passed in June 2012, the Office of the Superintendent of Financial Institutions is required, at least once in each calendar year, to “make or cause to be made any examination or inquiry that the Superintendent considers to be necessary or expedient to determine if the Corporation is carrying on any or all of its commercial activities in a safe and sound manner with due regard to its exposure to loss”.

BOARD PERFORMANCE

The skills profile of the Board describes the core attributes, competencies, skills, knowledge and experience required of Board members, individually and collectively, and was updated in 2012. This profile assists the Corporate Governance and Nominating Committee of the Board to identify potential new Board members as well as candidates for the positions of Chairperson and President and CEO to be recommended to the Minister for appointment.

Conducting regular assessments of the Board’s performance is integral to best governance practices. Two types of assessments are undertaken on alternate years – a peer assessment, which involves Board members assessing and providing feedback on each other’s contributions, and an overall Board assessment, which examines the effectiveness of the Board in comparison to the boards of other Crown corporations.

In 2012, CMHC completed an overall Board assessment with external professional assistance. The assessment evaluated the performance of CMHC’s Board over the past year. The Board received an overall strong and positive assessment and was slightly higher than the average assessment of CMHC’s peer organizations. The areas where the Board rated the highest were its comprehensive monitoring of the Corporation’s financial results and its effective working relationships with the President and CEO and with senior management.

21

BOARD COMPENSATION AND ATTENDANCE RECORD

CMHC follows federal guidelines for the remuneration of Board members.

The Chairperson and other non-government employee Board members receive an annual retainer for their services to CMHC plus fixed per diems for travel time, for their attendance at committee and Board meetings, and for carrying out other CMHC-related responsibilities as they arise.

Full-time employees of the federal government are not eligible to receive additional remuneration when appointed to a part-time position by Governor in Council. As such, the President and CEO, the Deputy Minister of the Minister for CMHC, and the Deputy Minister of Finance, as members of the Board, do not receive additional remunerations. (See Other Information for Compensation and Attendance Record for Board members.)

CMHC PENSION FUND

The CMHC Pension Fund was established by the Board of Directors pursuant to the CMHC Act. The Board has delegated general management and administrative responsibilities for the Fund to the Pension Fund Trustees. The Board appoints to the Pension Fund Trustees a member of the Board of Directors, the President and CEO, and two other members of CMHC Management. Three other Trustees are elected by the Pension Council (two representing employees and one representing pensioners). The President and CEO is Chair of the Pension Fund Trustees.

Within the framework of the enterprise risk management policies specific to the Pension Fund approved by the Board, the Trustees are responsible for setting investment objectives and policies, periodically reviewing strategic asset allocations and monitoring investment results. The outcomes of Trustees meetings and the performance of the Fund are regularly reported to the Board. The Board also receives an annual report on the Fund’s investment activities.

22 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

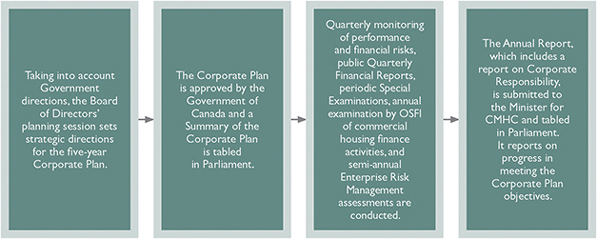

Making a difference in the lives of Canadians is what we do every day in every part of the country and housing has been our focus for more than 66 years.

Our employees are the foundation of our organization. We create a respectful, inclusive and supportive work environment where our employees are valued and encouraged to reach their full potential.

Our activities, including assisted housing programs, mortgage loan insurance, securitization, and research and information transfer, are our building blocks. We strive to perform these activities in a manner that maximizes our economic and social contributions and minimizes our environmental impacts.

Our governance structure provides the roof and ensures that we perform in a responsible, ethical and efficient manner.

23

Corporate responsibility is generally defined and recognized as a corporation’s commitment to take social, environmental and economic considerations into account in its decision-making process and activities. As Canada’s national housing agency, social and economic considerations are at the core of CMHC’s mandate and activities. These activities support and contribute to the well-being of Canadians and the stability of Canada’s economy.

In carrying out its mandate, CMHC strives to conduct its business in a manner that maximizes social and economic contributions and minimizes environmental impacts. CMHC is committed to the highest standards of competence, trustworthiness and prudence in managing the financial, physical and human resources entrusted to its care.

In 2012, CMHC implemented a number of measures to enhance the framework for tracking and reporting its corporate responsibility efforts, including the establishment of a formal Corporate Responsibility Advisory Committee to champion these efforts.

The following is a summary of key accomplishments for 2012:

¡ Responsible Governance:

In addition to enhancements to CMHC’s governance framework described in the Corporate Governance section, CMHC enacted an updated CMHC Code of Conduct.

¡ Social Contributions:

In addition to providing federal assistance to help address the housing needs of low-income Canadians, our employees give personally to their communities through the Government of Canada Workplace Charitable Campaign and other charitable causes.

¡ Environmental Contributions:

Ongoing efforts were made in 2012 to reduce CMHC’s environmental footprint, including the integration of environmental performance considerations into the procurement process.

¡ Economic Contributions:

CMHC was given an enhanced mandate to ensure that its commercial mortgage loan insurance and securitization activities contribute to financial system stability which is important to long-term growth and prosperity.

¡ Employees and Workplace Community:

CMHC has a strong diverse workplace community built on mutual respect, employee wellness and development opportunities. The Corporation was recognized as one of Canada’s 10 Most Admired Corporate CulturesTM in the broader public sector category by Waterstone Human Capital.

25

RESPONSIBLE GOVERNANCE

CMHC promotes a culture of ethical business conduct that is reinforced by a number of policies and guidelines.

CMHC’s updated Code of Conduct, enacted on April 2, 2012, integrates the Values and Ethics Code for the Public Service with CMHC’s longstanding corporate values. CMHC was able to enact its updated code the very same day the federal code was enacted. The Code of Conduct has two components:

| ¡ | Code of Values and Ethical Conduct – |

| This code outlines the principles and standards that guide employees and Board members in all CMHC duties, highlighting CMHC’s three corporate values: |

| ¡ | Serving the Public Interest |

| As stewards of the public trust, we serve with fairness, impartiality and objectivity. All of our activities, including those that are commercial in nature, are carried out in support of our public policy objectives. Our actions are inspired by a respect for human dignity and the value of every person. |

| ¡ | Achieving Business Excellence |

| We exercise the highest standards of competence, trustworthiness and prudence in conducting our business relationships and in managing the financial, physical and human resources entrusted to our care. We encourage learning, innovation and personal initiative to continuously improve the way we do business and achieve the best possible results for the Canadian public. |

| ¡ | Building a Workplace Community |

| We practice mutual respect and honesty in our working relationships. We help each other to achieve the goals of the team and the organization, and to maintain a healthy balance between our CMHC work and the other parts of our lives. We willingly explain our actions so that we may hold ourselves, and each other, accountable for living these values in the workplace. |

| ¡ | Conflict of Interest Policy – This policy serves to outline requirements with respect to the avoidance and, where necessary, disclosure of real, apparent or potential conflicts of interest, together with a process for discussing and disclosing such conflicts of interest. This policy applies to Board members and all employees. CMHC Board members are also subject to federal conflict of interest legislation. Certain CMHC employees are also subject to personal trading guidelines which impose trading restrictions on those who acquire, in the course of their official duties, information that is generally not available to the public. |

The Code of Conduct is also supported by the Disclosure of Wrongdoing in the Workplace Policy, which defines wrongdoing, articulates the role and responsibilities of CMHC’s Senior Officer for Disclosure, and establishes a process for reporting wrongdoing in the workplace.

26 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

SOCIAL CONTRIBUTIONS

Strengthening communities

CMHC contributes to the development of communities through investments in programs and initiatives that improve the quality of life for families and individuals.

27

28 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

29

2012 Charitable Campaigns

CMHC employees have a longstanding reputation of supporting charities and volunteering in the community, demonstrating their spirit of generosity and desire to reach out to those in need. In 2012, CMHC raised a total of $350,000 in contributions to the Government of Canada Workplace Charitable Campaign. The National Capital Regional team surpassed its goal for the 10th year and received the Michael Nurse Award for its creativity, dedication and enthusiasm that were instrumental to the campaign’s success.

In addition to the Government of Canada Workplace Charitable Campaign, CMHC employees continue to be actively engaged in the communities in which they live and work. During the past year, over 70 charitable activities organized by CMHC or by CMHC employees on their own raised over $180,000 in support of a wide range of organizations all across the country.

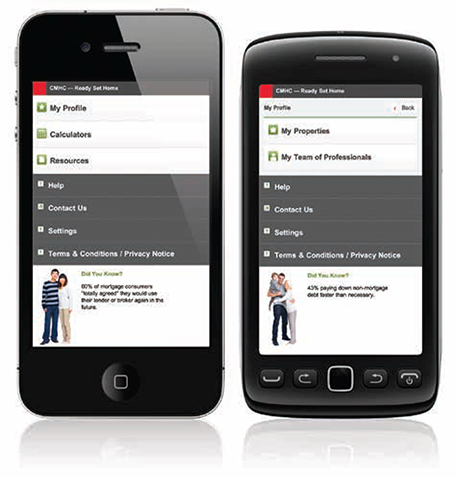

Financial Literacy: Helping Canadians make informed and responsible home-buying decisions

Buying a house is one of the most important financial decisions that most Canadians will make. In 2012, CMHC introduced two new tools to help Canadian home buyers make informed decisions. Ready, Set, Home is a mobile app which provides information and helps home buyers keep track of details throughout the process. An easy-to-use debt service calculator allows home buyers to understand how much they can comfortably afford to spend on a mortgage.

30 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

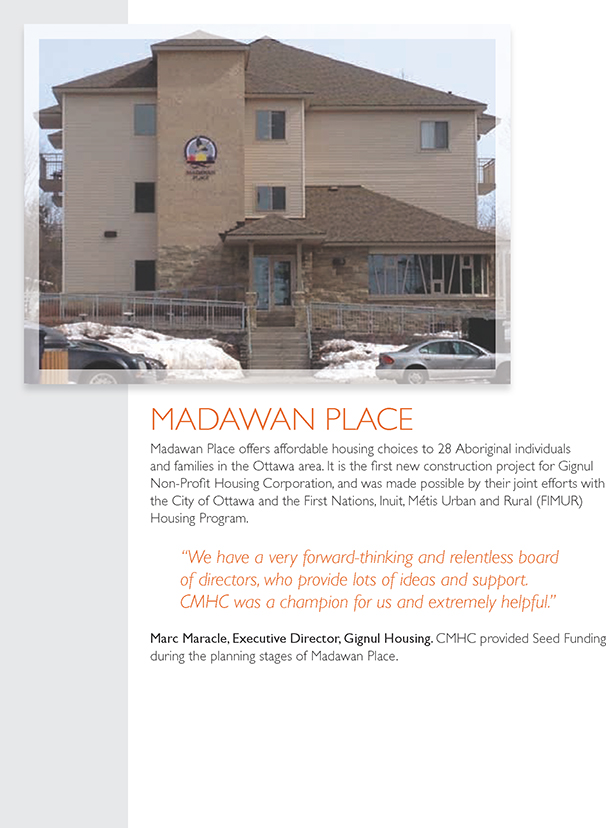

Habitat for Humanity Canada

CMHC and Habitat for Humanity have a long history of working together. The reason is simple – both organizations are motivated by the same basic belief that housing is fundamental to a good quality of life. CMHC is a Gold partner and the founding national

sponsor of the Habitat for Humanity Aboriginal Housing Program which helps make the Habitat homeownership model available to more Aboriginal people. To date, 50 Aboriginal families have moved into their Habitat homes and it is envisioned that many more will benefit from this program in the coming years.

|

FIRST HOUSE PROJECT

First House Project in Takhini River, located 50 kilometres west of Whitehorse, will make homeownership possible for three low-income First Nation families. The project was developed through a partnership between Habitat for Humanity Yukon and the Champagne and Aishihik First Nations (CAFN).

“First House is a milestone project under Habitat Canada’s Aboriginal Housing Program, which promotes homeownership within Aboriginal communities across Canada. This is the first build on First Nations settlement land and we are hoping that many more First Nations will follow suit.”

Jay Thakar, National Manager of the Aboriginal Housing Program, Habitat for Humanity Canada, which developed First House through local partnerships. The project received assistance from the federal government through Seed Funding. CMHC is the lead and founding national partner for the Aboriginal Housing Program. |

31

ENVIRONMENTAL CONTRIBUTIONS

Ongoing research and information transfer related to sustainable housing

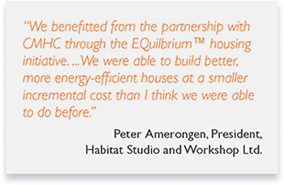

CMHC has a long history of providing both the housing industry and individual Canadians with information on how to improve the energy efficiency of housing. CMHC publishes Research Highlights and other information products on a regular basis and shares the knowledge gained from its EQuilibrium™ sustainable housing demonstration initiatives. CMHC also undertakes research, demonstration and information product development to promote the creation of culturally appropriate and energy-efficient housing in Canada’s North.

CMHC Green Home mortgage loan insurance product

The CMHC Green Home mortgage loan insurance product offers borrowers affordable options when purchasing an energy-efficient home or making energy-efficient improvements. Since its inception in 2004, CMHC Green Home has provided $8.2 million in premium rebates to more than 6,000 households choosing to purchase an environmentally friendly home or make energy-efficient renovations.

Reducing CMHC’s environmental footprint

| CMHC Green Team

Following the adoption of a comprehensive corporate-wide sustainable operations strategy in 2011, the focus for 2012 was to implement a five-year energy management program. The program aims to further reduce | |

| CMHC’s environmental footprint and continue to promote environmentally responsible behaviour in day to day business activities. A network of green teams collaborates on initiatives to promote more environmentally friendly practices. CMHC’s environmental footprint is reflected in the following table. | ||

32 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

CMHC’s Environmental Footprint

| 2010 | 2011 | 2012 | % Improvement | |||||

Paper consumption1 (total sheets) | 19,209,019 | 17,621,500 | 14,319,170 | 18.74 | ||||

Paper recycled (metric tonnes) | 109.18 | 110.77 | 111.21 | 0.40 | ||||

Electricity consumption (kWh) | 10,095,491 | 10,006,514 | 9,444,729 | 5.61 | ||||

Natural gas consumption (m3) | 380,586 | 433,339 | 410,959 | 5.16 | ||||

Building water consumption (m3) | 32,093 | 38,443 | 35,399 | 7.92 | ||||

Reduction in CO2emissions from energy management program (kg) | N/A | N/A | 135,888 | N/A |

| 1 | The figures for paper consumption are Corporate-wide. The figures for recycled paper, electricity, natural gas and water consumption are for the National Office complex only. |

As part of the National Office waste management program, audits are carried out by an independent environmental consulting firm throughout the year. Through recommendation from these audits and other initiatives, CMHC continues to show improvements in the amount of waste diverted from local landfill sites as shown in the following table:

| 2010 | 2011 | 2012 | ||||

Waste generated (tonnes) | 221 | 233 | 197 | |||

Total waste reused and recycled (tonnes) | 119 | 133 | 123 | |||

Estimated waste diversion rate | 54% | 59% | 62% |

Green procurement

CMHC modified its procurement policy in 2012 by integrating environmental performance considerations into the procurement process. Where procurement involves products with high levels of residual waste, vendors are required to submit a waste management plan.

Granville Island environmental program

Granville Island, which is managed by CMHC on behalf of the Government of Canada, continues to actively promote environmentally sustainable practices in support of the City of Vancouver’s plan to become the greenest city in the world. Granville Island continues to work towards the 70% municipally mandated rate for waste diversion. Zero-waste stations have been installed in the public market and other exterior locations to increase waste diversion. As a result of these initiatives, the overall waste diversion rate increased by 5% to 45% for organics, mixed paper, glass, metal, plastics, and cardboard in 2012.

33

ECONOMIC CONTRIBUTIONS

Housing-related spending in 2012 of $314.9 billion, which includes consumption-related spending in housing and residential investment1 represented approximately 17.3% of the GDP in Canada. This accounts for 1.2 million jobs in the residential construction, real estate, and leasing industries.

CMHC mortgage loan insurance has helped shape the housing finance system by enabling lenders throughout the country to provide financing to qualified borrowers at competitive interest rates for both homeowners and rental housing. CMHC manages its capital to ensure that the Corporation is able to withstand adverse economic conditions and maintain its financial strength.

CMHC’s securitization activities also contribute to the health and stability of Canada’s housing finance system by ensuring that lenders have access to an adequate supply of funds for residential mortgages. By encouraging competition amongst lenders, the marketplace and all Canadians benefit.

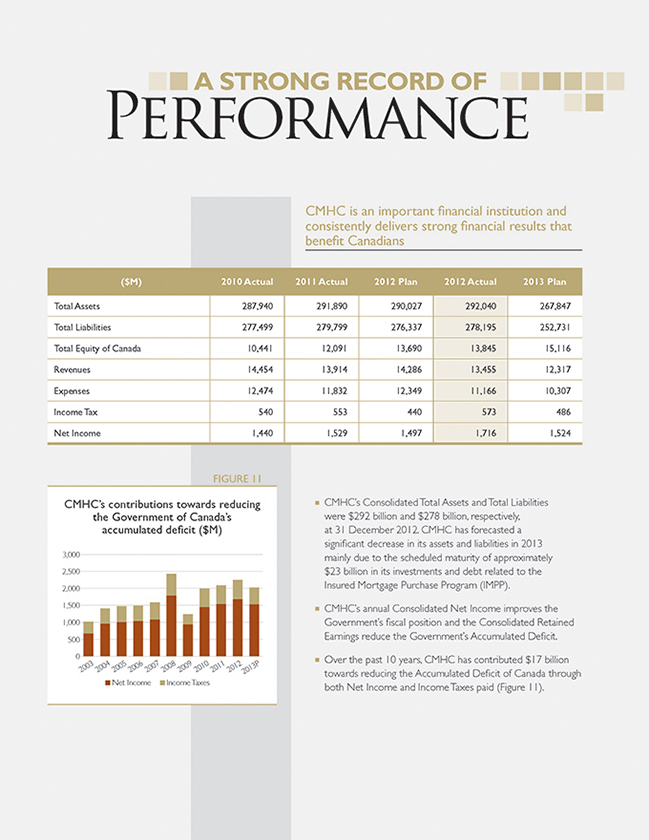

CMHC mortgage loan insurance and securitization businesses adhere to business practices that ensure commercial viability without having to rely on the Government of Canada for support, even in less favourable economic times. In fact, over the past decade, CMHC has contributed over $17 billion towards improving Canada’s fiscal position. This included $2 billion in 2012 alone.

| 1 | Consumption-related spending is the amount that households spend on shelter and includes imputed-rent spending but excludes spending related to water, electricity and heating consumption. Residential investment includes construction of new and changes to existing dwellings including transfer costs such as real estate commissions, land transfer and legal fees. It also includes maintenance and renovation spending. |

34 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

EMPLOYEES AND WORKPLACE COMMUNITY

CMHC has a number of initiatives to ensure respect, diversity and open communication in the workplace. The Corporation provides a comprehensive benefit plan, wellness programs and flexible working arrangements to support employee well-being. Learning and development programs, with a strong emphasis on on-the-job training, support the personal and professional growth of employees. Communication tools, such as the annual President’s tour, help keep CMHC’s values front and centre and provide employees with the opportunity to hear about CMHC’s objectives and challenges.

CMHC monitors the health of its culture and workplace community through a range of indicators. In 2012, CMHC sustained high employee engagement (at 94%) as well as strong retention and commitment, as evidenced by the low 2.4% voluntary turnover rate and the low sick leave usage.

2011

|

2012

| |||

Corporate Culture

| ||||

| Rate of employee engagement1 | 95% | 94% | ||

Percentage of CMHC employees who fully support the values for which CMHC stands | 92% | 90% | ||

Percentage of employees who believe that CMHC has a reputation as a good employer | 89% | 86% | ||

Voluntary turnover rate | 2.8% | 2.4% | ||

Diversity

| ||||

Percentage of employees who believe that CMHC supports diversity in the workplace | 87% | 84% | ||

Learning and Development

| ||||

| Percentage of employees with 2012 development plans in place | 97% | 96% | ||

Percentage of employees who believe they have improved their skills and capabilities over the past year | 78% | 76% | ||

Employee Well-Being

| ||||

Average number of sick days taken | 7.6 | 7.8 | ||

Percentage of employees participating in the Compressed Work Week Program | 30.1% | 28.4% | ||

| 1 | See Definition of Select Performance Measures in Other Information section. |

Since 2006, CMHC has had a talent management framework which brings together policies on multiple fronts to manage the renewal of the workforce and develop strategies to attract, motivate and retain employees with the diverse skills and backgrounds needed.

Learning and development opportunities make CMHC an appealing place to work. In 2012, 76% of CMHC employees indicated that they had improved their skills and capabilities over the past year. To help employees balance their commitments at home and at work, CMHC offers a variety of alternate work arrangements, family-related leave and parental benefits. CMHC also maintains an employee relations office to help employees, managers and human resources professionals build and maintain strong working relationships. When dealing with difficult personal or professional situations, our employees and their families also have access to a voluntary, confidential short-term counselling service to assist them in finding the help they need. In 2012, CMHC developed a new flexible group insurance plan that can be customized to better meet the unique needs of CMHC employees. The new benefits plans will be fully implemented in 2013.

CMHC places significant focus on ensuring that managers are able to effectively manage their employees. As part of managers’ yearly performance evaluations, their contributions to supporting workplace diversity and wellness, and to the growth and development of employees are assessed.

In 2012, CMHC was recognized as one of Canada’s 10 Most Admired Corporate CulturesTM in the broader public sector category by Waterstone Human Capital. This award recognizes CMHC for having a culture that has helped the Corporation enhance performance and sustain a competitive advantage, evidenced through the annual achievements outlined in this report.

35

| CMHC employees come to work knowing that they are contributing to increased affordability and quality of housing for Canadians

Krissy MacDonald Senior Risk Management Officer, National Office

“What inspired me to do my best? Both the expectation and the desire to perform beyond expectations I was part of a team that was committed to professionalism and excellence. And I knew that our contribution was important to CMHC.”

Tom McCarthy Advisor, Aboriginal Housing, Prairie and Territories Region

“I get the opportunity to see the effect of my job one-on-one with my Aboriginal clients. Each new house means so much to the people living in them. . . The reminder on a regular basis of why we do what we do is inspiration enough to work towards success.”

Tomo Brank Senior Representative, Business Development, Ontario Region

“The culture at CMHC is in line with my own personal values because we are always looking to do the right thing for the client and working with business partners that will truly help Canadians make better housing choices. Like no other organization I have worked with in the past, I am proud of the work we do every day.” |

36 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

THE OPERATING ENVIRONMENT IN 2012 AND OUTLOOK FOR 2013 | 38 | |||

SUMMARY OF FINANCIAL RESULTS | 42 | |||

PERFORMANCE BY OBJECTIVE | 51 | |||

RISK MANAGEMENT | 85 | |||

HUMAN RESOURCES AND OTHER INTERNAL SERVICES | 94 | |||

FINANCIAL HIGHLIGHTS FROM 2008 TO 2013 | 98 | |||

FORWARD-LOOKING STATEMENTS

CMHC’s Annual Report contains forward-looking statements regarding objectives, strategies and expected financial results. There are risks and uncertainties beyond the control of CMHC that include, but are not limited to, economic, financial and regulatory conditions, nationally and internationally. These factors, among others, may cause actual results to differ substantially from the expectations stated or implied in forward-looking statements.

37

THE OPERATING

ENVIRONMENT IN 2012

AND OUTLOOK FOR 2013

This section discusses deficit reduction measures, changes in CMHC’s legislative framework, socio-economic factors, and housing indicators that impact CMHC’s operating environment and influence the attainment of its objectives and financial results. More discussion on factors that impact specific activities can be found further on in this MD&A.

GOVERNMENT REVIEW OF SPENDING

CMHC receives Parliamentary appropriations to fund assisted housing and research and information transfer activities. In Budget 2012, the Government announced the results of its review of spending undertaken by all federal departments and agencies. It indicated that CMHC will contribute $102.4 million in ongoing savings by 2014-15. The majority of these savings ($79 million) will result from lower costs in administering CMHC’s social housing portfolio and other corporate operating efficiencies.

The remaining $23.4 million will result from administrative efficiencies related to certain portfolio management activities for some existing social housing projects ($3.1 million); the rationalization of research and information dissemination priorities ($9.8 million); and the discontinuation of export promotion activities ($10.5 million). These savings will have no impact on low-income Canadians receiving federal housing assistance. (Also see Budget 2012 Implementation in the Summary of Financial Results section of the MD&A)

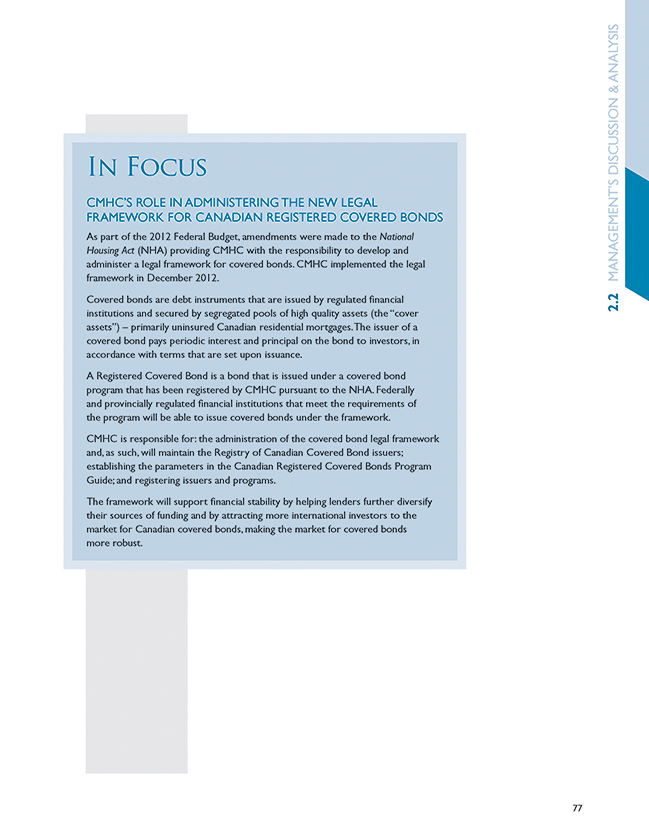

LEGISLATIVE AMENDMENTS

The legislative framework governing CMHC consists primarily of the Canada Mortgage and Housing Corporation Act (CMHC Act), the National Housing Act (NHA), and the Financial Administration Act (FAA).

Amendments to the CMHC Act and the NHA were made pursuant to Budget 2011 (the Supporting Vulnerable Seniors and Strengthening Canada’s Economy Act) and Budget 2012 (the Jobs, Growth and Long-term Prosperity Act).

In Budget 2011, the Government committed to introducing a legislative framework that would formalize existing mortgage loan insurance arrangements with private mortgage insurers and CMHC. The new legislative framework for mortgage loan insurance included the Protection of Residential Mortgage or Hypothecary Insurance Act (PRMHIA), which applies to private mortgage insurers, as well as consequential amendments to the National Housing Act. The PRMHIA and consequential amendments to the NHA have now come into force.

38 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

In addition, regulations necessary to fully implement the new legislative framework also came into force on January 1, 2013. These include regulations outlining minimum criteria for the designation of approved/ qualified lenders for CMHC and the private sector insurers, and regulations specifying the types of loans eligible for insurance underwritten by CMHC and private sector insurers.

With respect to Budget 2012, the Jobs, Growth and Long-term Prosperity Act received Royal Assent on June 29, 2012. Among other things, the Act enhances the governance and oversight framework for CMHC’s commercial activities and includes the following provisions:

| ¡ | the addition of a new objective for CMHC to ensure its commercial activities (mortgage loan insurance and securitization) and its activities with respect to administering the legal framework for Canadian covered bonds, promote and contribute to the stability of the financial system, including the housing market; |

| ¡ | legislative and regulatory authorities for the Minister of Finance regarding CMHC’s securitization activities and any new commercial programs; |

| ¡ | authorities for the Superintendent of Financial Institutions to review, at least annually, whether CMHC is carrying out its commercial activities in a safe and sound manner with due regard to its exposure to loss, and report the results to CMHC’s Board of Directors, the Minister of Finance and the Minister for CMHC, currently, the Minister of Human Resources and Skills Development; |

| ¡ | the addition of the Deputy Minister of the Minister for CMHC and the Deputy Minister of Finance to CMHC’s Board of Directors as ex-officio members; and |

| ¡ | a legal framework, administered by CMHC, for Canadian covered bonds. |

SOCIO-ECONOMIC FACTORS

Housing demand is subject to a range of demographic, social and economic influences. The growth in the housing stock is largely driven by household formation which in turn is closely linked to changes in population size, composition and employment rates. The following influence housing markets and CMHC’s operating environment:

Population growth and

international migration

Between 2006 and 2011, Canada’s population grew by 5.9%, up slightly from the previous five-year period (2001 to 2006) when it grew by 5.4%. However, the number of households increased by 5.5% between 2006 and 2011, down from 5.9% between 2001 and 2006.

The Canadian economy continues to relatively outperform many others in the Organisation for Economic Co-operation and Development. Canada’s attractive labour market has led to an estimated year-to-year increase of 23,000 persons in net migration to a total of 267,129 persons in 2012. Looking ahead, 2013 is expected to see net migration of 254,400 with a rebound to 268,900 in 2014. These increases will help support Canada’s housing sector.

Economic growth

Economic growth has slowed to 1.9% in 2012 compared to 2.7% in 2011. Given both global and domestic conditions, the Canadian economy is expected to grow by 1.8% in 2013. In accordance with the consensus among prominent Canadian economic forecasters, growth in gross domestic product is expected to rebound to 2.6% in 2014.

39

Interest rates and mortgage rates

The Bank of Canada has kept its target for the overnight interest rate at 1.0% since 2010. The five-year mortgage interest rate reached 5.24% in December 20121. According to CMHC’s base case scenario, the five-year mortgage rate is forecast to be within 5.00% to 5.75% in 2013 and will be within 5.50% to 6.25% in 2014.

Employment and income

In the 12 months to December 2012, employment grew by 1.8% (+310,300), leading to a decline in the unemployment rate to 7.1% from 7.5% in December 2011. Over this period, full-time employment rose 2.2% (+308,600), and part-time employment rose 0.1% (+1,700). In accordance with the consensus of prominent economists, employment is forecast to grow 1.3% in 2013 and 1.6% in 2014. The unemployment rate is expected to remain stable at 7.3% for 2013 and 2014.

Income grew in 2012 compared to 2011 and is expected to grow moderately in 2013 and 2014.

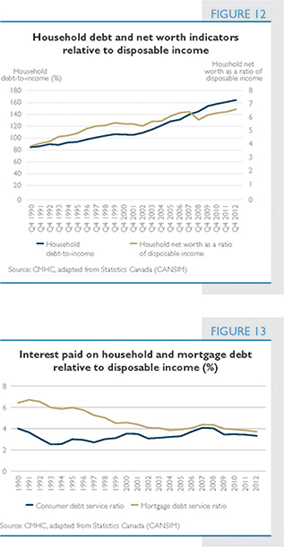

Household debt

There has been considerable attention paid to the household debt-to-income ratio. However, other ways to look at a household’s financial health include the household net worth-to-disposable income ratio which stood at 6.8, above the historical average of 5.6 since 1990 (Figure 12). In addition, indicators relating to Canadians’ ability to service their debt are also healthy by historical standards. Interest paid on mortgage debt as a share of monthly household disposable income in the fourth quarter of 2012 was 3.7%, well below the historical average of 4.8% (Figure 13).

HOUSING INDICATORS

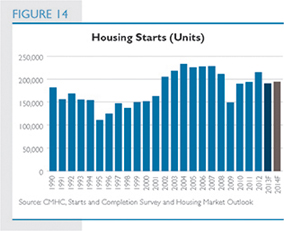

Housing starts

In 2012, housing starts increased to 214,827 as a result of strong gains in multiple starts, reflecting a high level of pre-sales in late 2010 and early 2011. CMHC expects a decline in both the singles and multiples segment which will result in a decline in

| 1 | This represents the conventional mortgage rate collected by CANNEX and calculated by CMHC. Actual mortgage rates offered by major Canadian lenders are often lower. |

40 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

total annual starts to 190,300 units in 2013. Growth in employment and economic activity will be tempered by increases in mortgage interest rates leading to a modest gain of 194,100 units in 2014.

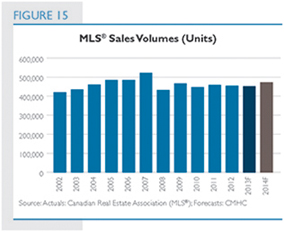

Sales of existing homes

In 2012, Multiple Listing Service®1 (MLS®) sales were 453,372 units, down from 458,636 units in 2011. CMHC forecasts that sales of existing homes through the MLS® will hold steady in 2013, and increase in 2014 due to economic and employment growth. CMHC’s point forecast is 451,100 MLS® sales for 2013 and 472,300 for 2014.

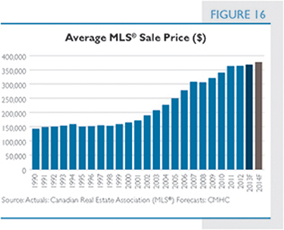

House prices

In 2012, house prices increased by 0.3% compared to 2011, reaching $363,740, up from $362,716 in 2011. Balanced market conditions are expected to prevail in most local housing markets and the average MLS® price should grow at a rate close to inflation, or slightly below, for 2013 and 2014. According to CMHC’s forecast, the average MLS® price is expected to be $367,500 in 2013 and $377,300 in 2014, representing increases of 1.0% and 2.7%, respectively.

Vacancy rates

The rental vacancy rate (all bedroom types in structures with three or more units) for Canada was 2.6% in October 2012, up from 2.2% in October 2011. Looking ahead, CMHC expects the vacancy rate to remain relatively unchanged at 2.5% in 2013.

| 1 | Multiple Listing Service® is a registered trademark owned by the Canadian Real Estate Association. |

41

SUMMARY

OF FINANCIAL RESULTS

CMHC reports on the following principal business activities and consolidates the accounts of the Canada Housing Trust, a separate legal entity:

| ¡ | Housing Programs: Expenditures and operating expenses are funded by Parliamentary appropriations. |

| ¡ | Lending: Revenues are earned from interest income on the loan portfolio which is funded through borrowings. |

Housing Programs and the Lending Activity provide support for Canadians in need and are operated on a planned breakeven basis.

| ¡ | Mortgage Loan Insurance: Revenues are earned from premiums, fees and investment income. Expenses consist of operating expenses and net claim expenses. The Corporation’s Net Income is primarily derived from this Activity. |

| ¡ | Securitization: Securitization revenues are earned from guarantee fees and interest income. Expenses consist primarily of interest expenses. Operating expenses and issuer fees under the new legal framework for covered bonds to be administered by CMHC are accounted for under this Activity. |

Mortgage Loan Insurance and Securitization Activities are operated on a commercial basis and are expected to generate reasonable returns. CMHC is expected to recover the costs of administering the legal framework for covered bonds from participating issuers.

| ¡ | Canada Housing Trust (CHT): CHT revenue is earned primarily from investment income. Revenue derived from investment income is used to cover operating expenditures and Canada Mortgage Bonds (CMB) interest expenses. |

42 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

CONSOLIDATED

FINANCIAL RESULTS

BALANCE SHEET HIGHLIGHTS

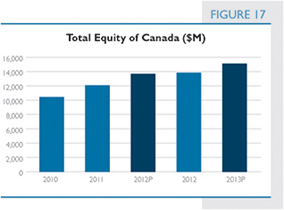

| 2012 | ||||||||||||||||||||

| ($M) | 2011 Actual | Plan | Actual | Variance to Plan | 2013 Plan | |||||||||||||||

Total Assets | 291,890 | 290,027 | 292,040 | 2,013 | 267,847 | |||||||||||||||

Total Liabilities | 279,799 | 276,337 | 278,195 | 1,858 | 252,731 | |||||||||||||||

Contributed Capital | 25 | 25 | 25 | - | 25 | |||||||||||||||

Accumulated Other Comprehensive Income (AOCI) | 902 | 499 | 1,038 | 539 | 731 | |||||||||||||||

Retained Earnings Set Aside for Capitalization | 9,727 | 9,884 | 10,764 | 880 | 11,481 | |||||||||||||||

Retained Earnings (Other)1 | 1,437 | 3,282 | 2,018 | (1,264) | 2,879 | |||||||||||||||

Total Equity of Canada | 12,091 | 13,690 | 13,845 | 155 | 15,116 | |||||||||||||||

| 1 | Includes Unappropriated Retained Earnings and Reserve Fund |

Total Assets and Total Liabilities

Total Assets were $292 billion and Total Liabilities were $278 billion as of 31 December 2012, of which $204 billion is related to CHT’s Canada Mortgage Bonds (CMB) program.

| ¡ | Compared to Plan |

Assets and liabilities both exceed plan by $2 billion. These variances result from lower than planned inter-company investments in Canada Mortgage Bonds, which are eliminated upon consolidation. The Corporation held less investments in CMBs than planned which resulted in lower inter-company elimination amounts and therefore increased the Investment Securities (Assets) and Canada Mortgage Bonds (Liabilities) balances in comparison to plan.

| ¡ | Compared to 2011 |

When compared to 2011, Total Assets have remained relatively stable with a $150 million (0.05%) increase.

Total Liabilities decreased by approximately $1.6 billion (0.6%) from 31 December 2011, mainly caused by $3.7 billion in net repayments of IMPP and the Lending Activity debt. This was partially offset by $2.3 billion in net issuances of CMB.

Equity of Canada

The Equity of Canada is made up of three components:

| ¡ | Contributed Capital |

The contributed capital of CMHC is determined by the Governor in Council. It is currently set at $25 million.

| ¡ | Accumulated Other Comprehensive Income (AOCI) |

AOCI is the accumulated unrealized gains or losses caused by the change in fair valuation of Available for Sale (AFS) investments in the Mortgage Loan Insurance and Securitization Activities. As at 31 December 2012, total AOCI was $1,038 million, $539 million higher than planned and $136 million higher than 2011. The variance to plan was mainly caused by a higher than planned increase in bond prices in 2011 and equity prices in 2012.

| ¡ | Retained Earnings |

Total Retained Earnings were $12,782 million of which $10,764 million was set aside for the capitalization of both the Mortgage Loan Insurance and Securitization Activities in accordance with CMHC’s Capital Management Framework. The residual $2,018 million in Retained Earnings is

43

comprised of Unappropriated Retained Earnings from the Mortgage Loan Insurance and Securitization Activities as well as the Reserve Fund in the Lending Activity. Total Retained Earnings variances are mainly driven by fluctuations in Net Income whereas component variances mainly arise as a result of the amounts that have been set aside for capitalization purposes. Further explanation is provided below as well as in the financial analysis sections of the strategic priorities.

Within the Public Accounts of Canada, CMHC’s annual Consolidated Net Income reduces the Government’s annual deficit, and the consolidated Retained Earnings and Accumulated Other Comprehensive Income reduces the Government’s accumulated deficit. Over the last decade, CMHC has contributed over $17 billion towards reducing the Government’s accumulated deficit through both its Net Income and Income Taxes.

The CMHC Act and National Housing Act (NHA) govern the use of the Corporation’s Retained Earnings.

Retained Earnings related to the Mortgage Loan Insurance Activity are appropriated in accordance with the Capital Management Framework which is based on guidelines developed by OSFI. For its Mortgage Loan Insurance Activity, CMHC has Appropriated Retained Earnings as well as AOCI representing its capital holding target of 200% Minimum Capital Test (MCT). Mortgage Loan Insurance Capital Available resulted in a 231% MCT as at 31 December 2012. In accordance with regulatory guidance issued by OSFI in 2012 for private mortgage insurers, the % MCT is now audited by CMHC’s external auditors annually.

Retained Earnings related to the Securitization Activity are also appropriated based on regulatory and economic capital principles. For its Securitization Activity, CMHC has Appropriated Retained Earnings as well as AOCI representing 100% of its target capital. Securitization Capital Available represented 156% of its target capital.

Earnings in relation to CMHC’s Lending Activity are retained to address interest rate risk exposures on pre-payable loans as well as credit risk exposure on the Municipal Infrastructure Lending Program loans. These Retained Earnings, referred to as the Reserve Fund, also include amounts representing unrealized fair market valuation changes of the Lending Activity as well as its portion of actuarial gains and losses from CMHC’s defined post-employment benefits.

The Reserve Fund for Lending is subject to a statutory limit of $240 million. Should the limit be exceeded, CMHC would be required to pay any excess to the Government of Canada. As at 31 December 2012, the Reserve Fund balance was negative $16 million. In the Reserve Fund, $102 million has been set aside to address interest rate risk and credit risk exposure. This is offset by $118 million in cumulative net unrealized losses resulting from fair market valuations, the majority of which was caused by Net Actuarial Losses on Post-Employment Benefits. A negative amount within the reserve has no implications on the statutory limit. For further information, see Lending Activity under strategic priority 1.1 of Objective 1.

As at year-end 2012, the Corporation’s Total Equity of Canada was relatively consistent with plan and $1,754 million (15%) higher than 2011. The year over year increase represents the Comprehensive Income recognized by CMHC during 2012.

44 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

STATEMENT OF INCOME AND

COMPREHENSIVE INCOME HIGHLIGHTS

| ($M) | 2011 Actual |

2012 | Variance to Plan | 2013 Plan | ||||||||||||||||

| Plan | Actual | |||||||||||||||||||

Revenues | 13,914 | 14,286 | 13,455 | (831) | 12,317 | |||||||||||||||

Expenses | 11,832 | 12,349 | 11,166 | (1,183) | 10,307 | |||||||||||||||

Income before Income Taxes | 2,082 | 1,937 | 2,289 | 352 | 2,010 | |||||||||||||||

Income Taxes | 553 | 440 | 573 | 133 | 486 | |||||||||||||||

Net Income | 1,529 | 1,497 | 1,716 | 219 | 1,524 | |||||||||||||||

Other Comprehensive Income (Loss) | 120 | - | 38 | 38 | (66) | |||||||||||||||

Comprehensive Income | 1,649 | 1,497 | 1,754 | 257 | 1,458 | |||||||||||||||

Revenues and Expenses

Total Revenues were $13,455 million and Total Expenses were $11,166 million for the year ended 31 December 2012 of which approximately $6,000 million was related to interest income and interest expenses from CHT’s CMB program.

| ¡ | Compared to Plan |

Revenues were $831 million (6%) lower than expected mainly due to $1 billion in lower interest income relating from the CHT CMB program caused by lower than forecasted interest rates. This variance was partially offset by higher than planned earned guarantee fees as NHA MBS issuances exceeded expectations and higher than planned Net Unrealized Gains from Financial Instruments mainly due to the unplanned consolidation of a foreign equity mutual fund in late 2011.

Similarly, the lower than expected interest rates for the CHT CMB program discussed above contributed to the $1 billion (10%) lower than planned Expenses.

| ¡ | Compared to 2011 |

Revenues and Expenses were $459 million and $666 million lower than 2011 mainly due to lower Interest Income and Interest Expense on the CMB Program as a result of a decrease in interest rates. The decrease in revenues was partially offset by $183 million in higher Net Unrealized Gains from Financial Instruments, primarily in the Mortgage Loan Insurance Activity, that were caused by favourable price movements on the consolidated foreign equity mutual fund.

Net Income

As a result of the above variances, Net Income of $1,716 million exceeded plan by $219 million (15%) and prior year results by $187 million (12%).

Other Comprehensive Income (Loss)

CMHC’s Other Comprehensive Income (OCI) consists of unrealized gains or losses caused by changes in the fair value of Available for Sale (AFS) investments in the Mortgage Loan Insurance and Securitization Activities. As these investments are classified as AFS, their unrealized gains/losses on fair valuation are recorded in OCI. Also included in OCI are net actuarial gains/losses from CMHC’s post-employment benefits.

| ¡ | Compared to Plan |

In 2012, total OCI was $38 million higher than expected mainly due to $208 million in higher than planned unrealized fair value fluctuations caused by market appreciation on investments securities. This variance was partially offset by higher than planned Reclassifications of Prior Years’ Net Unrealized Gains in Net Income of $61 million as a result of the sale of investments due to the implementation of a new Securitization asset allocation policy. Further offsetting the fair value gains, were $109 million in higher than planned Net Actuarial Losses from Post-employment Benefits caused by an unexpected decrease in the discount rate assumptions used in the calculation of the pension fund defined benefit obligation.

45

| ¡ | Compared to 2011 |

OCI decreased by $82 million in comparison to 2011 primarily as a result of lower Net Unrealized Gains on Available for Sale Financial Instruments and a higher Reclassification of Prior Years’ Net Unrealized Gains Realized in Net Income that were partially offset by lower Actuarial Losses from Post-employment Benefits.

Net Unrealized Gains on Available for Sale Financial Instruments were $144 million lower in 2012 mostly due to the stabilization of bond yields during the year, that were partially offset by an increase in equity prices in 2012.

Reclassifications of Prior Years’ Net Unrealized Gains were $21 million higher than last year. The increase resulted from the implementation of the new asset allocation policy within the Securitization Activity, as previously discussed.

These decreases to OCI were partially offset by an $83 million decrease in Net Actuarial Losses from Post-employment Benefits primarily due to an increase in the actual rate of return on pension fund assets.

Resource Management

Total Operating Expenses for the year ended 31 December 2012 were in line with the plan and $7 million higher than 2011. The year over year increase was largely due to a higher pension expense that resulted primarily from a decline in the assumption for the discount rate. This increase was slightly offset by cost saving measures as explained in the Budget 2012 Implementation section.

Staff-years of 1,900 were consistent with plan (98%) and 2011 figures (96%).

BUDGET 2012 IMPLEMENTATION

This section provides an overview of the savings measures announced in Budget 2012 in order to refocus government and programs; make it easier for Canadians and businesses to deal with their government; and modernize and reduce the back office.

Efforts to reduce the federal deficit were undertaken by all federal departments and agencies, including CMHC. The focus was on decreased spending, requiring a review of CMHC’s operations and government appropriation-based programs.

The global results of the spending review exercise were announced in Budget 2012. As noted in the Budget, CMHC will contribute $102.4 million in ongoing annual savings by 2014-2015. These savings will have no impact on low-income Canadians receiving federal housing assistance delivered through federal or provincial/territorial agreements. They will be achieved through lower program administration costs, operating efficiencies, rationalizing research and information dissemination priorities, and discontinuing CMHC’s housing export program. CMHC is on track to implement and realize all of its savings measures for 2012-2013.

Lower program administration costs

CMHC administers and funds social housing projects in Prince Edward Island, Quebec and Alberta, on-reserve housing across Canada as well as other social housing projects funded by previous programs, mostly co-operative housing projects in Ontario and British Columbia.

| ($M) | 2011 Actual | 2012 | Variance to Plan | 2013 Plan | ||||||||||||||||

| Plan | Actual | |||||||||||||||||||

Total Operating Expenses (included in Expenses in table on previous page) | 420 | 427 | 427 | - | 463 | |||||||||||||||

Staff FTEs (Full-time Equivalents) | 1,975 | 1,947 | 1,900 | (47) | 1,878 | |||||||||||||||

46 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

Lower than anticipated program administration costs will result in savings in administering CMHC’s social housing portfolio. These savings will have no impact on low-income Canadians receiving housing assistance through the federal or provincial/territorial government.

Program administration efficiencies

CMHC is responsible for the existing social housing portfolio off reserve where this portfolio has not been transferred to provinces and territories under Social Housing Agreements and for the existing CMHC-delivered social housing portfolio on reserve. CMHC undertakes portfolio management activities such as client visits and physical project inspections to ensure that this portfolio is well managed. With a significant number of projects to manage, CMHC is introducing a new approach for administering its programs and managing risk to be more effective and efficient.

CMHC has identified ways to streamline its processes and activities by reducing or eliminating certain portfolio management activities for some existing social housing projects.

These savings will have no impact on low-income Canadians receiving housing assistance.

Corporate operating efficiencies

CMHC has identified a number of operating efficiencies that will achieve savings while still maintaining services and providing tools and resources necessary for efficient operations. For example, travel, training and recruiting costs will be reduced. Equipment such as printers/photocopiers and devices will also be rationalized.

Rationalizing research and information dissemination priorities

CMHC will adjust its approach to research and survey expenditures to focus on fewer and higher priority research areas.

CMHC will continue to conduct and disseminate housing research aimed at improving market effectiveness, strengthening community well-being, addressing distinct housing needs, analyzing and reporting on housing need and improving housing performance.

Discontinuing CMHC’s housing export program

CMHC’s housing export program was created fifteen years ago to open doors and to provide technical assistance to help Canadian companies export their housing products and services abroad. As evidenced by the number of Canadian housing companies now operating in foreign markets, the program, which complements existing government export programs, has been successful in demonstrating how housing exporters can access foreign markets.

With this experience, supported by existing government export programs, housing exporters will continue to benefit from the opportunities that have been created over the last decade.

47

SAVINGS MEASURES

List By Program Alignment Architecture (in thousands $) | 2012-13 | 2013-14 | 2014-15 | Ongoing | ||||||||||||

Assisted Housing Programs | ||||||||||||||||

Resulting from Corporate operating efficiencies, lower program administration costs in administering CMHC’s social housing portfolio and program administration efficiencies | 658 | 3,045 | 79,457 | 79,457 | ||||||||||||

On-Reserve Housing Programs | ||||||||||||||||

Resulting from Corporate operating efficiencies and program administration efficiencies | 716 | 990 | 1,038 | 1,038 | ||||||||||||

Affordable Housing Initiative | 134 | 134 | 134 | 134 | ||||||||||||

Resulting from Corporate operating efficiencies | ||||||||||||||||

Housing Repair and Improvement Programs | 132 | 132 | 132 | 132 | ||||||||||||

Resulting from Corporate operating efficiencies | ||||||||||||||||

Research and Information Transfer | ||||||||||||||||

Resulting from Corporate operating efficiencies and rationalization of research and information dissemination priorities | 720 | 9,168 | 10,475 | 10,475 | ||||||||||||

International Activities | 1,349 | 10,120 | 10,494 | 10,494 | ||||||||||||

Resulting from the discontinuation of CMHC’s housing export program | ||||||||||||||||

Emergency Planning | 8 | 8 | 8 | 8 | ||||||||||||

Resulting from Corporate operating efficiencies | ||||||||||||||||

Canadian Housing Market Research and Analysis | 632 | 632 | 632 | 632 | ||||||||||||

Resulting from Corporate operating efficiencies | ||||||||||||||||

Total for Canada Mortgage and Housing Corporation | 4,349 | 24,229 | 102,370 | 102,370 | ||||||||||||

DISCLOSURE OF CHANGES IN ACCOUNTING POLICIES

CMHC’s significant accounting policies and changes in accounting policies are described in Note 2 (significant accounting policies) of CMHC’s 2012 Consolidated Financial Statements.

CMHC’s financial statements for 2012 have been prepared in accordance with International Financial Reporting Standards (IFRS) effective as at 31 December 2012, with the exception of the amendments to IAS 1 Presentation of Financial Statements which have been adopted in advance of the date they become effective for CMHC (1 January 2013).

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Judgments in Applying

Accounting Policies

In the process of applying CMHC’s accounting policies, CMHC Management is required to make various judgments that can significantly affect the amounts recognized in the financial statements. The judgments having the most significant effects on the financial statements are:

| ¡ | Derecognition: in assessing whether transfers of NHA MBS from Issuers to the Corporation under the CMB program (CHT) and IMPP (CMHC) qualify for derecognition, significant judgment is applied in determining whether substantially all the risks and rewards of ownership of the NHA MBS have been transferred. Per IAS 39: Financial Instruments – Recognition and Measurement requirements, CMHC has determined that the sellers of NHA MBS to the Corporation failed the derecognition criteria as they retain the risk and rewards of the NHA MBS through swap agreements. |

48 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

| ¡ | Consolidation: significant judgments are applied in the assessment of whether the substance of the relationship between CMHC and Canada Housing Trust (a special purpose entity) indicates that, as per Standing Interpretation Committee Interpretation 12: Consolidation – Special Purpose Entities, CMHC controls that special purpose entity. CMHC guarantees the timely payment of principal and interest on the Canada Mortgage Bonds, which exposes it to the majority of risks of Canada Housing Trust and as a result, CMHC consolidates the Canada Housing Trust. Significant judgments are also applied in the assessment of whether the substance of the relationship between CMHC and Nordea International Equity Fund (Nordea) indicates that CMHC controls it. As CMHC is the principal investor in the fund, Nordea is reliant on CMHC’s continued investment and CMHC, in effect, has the power to govern Nordea’s policies so as to obtain benefits from its activities. As a result, CMHC consolidates Nordea International Equity Fund. |

| ¡ | Impairment of Available for Sale Financial Instruments: significant judgment is applied in assessing if there is objective evidence of impairment, including whether declines in the fair value of AFS equity instruments below cost are significant and/or prolonged. |

Critical Accounting Estimates

The preparation of the Consolidated Financial Statements requires CMHC Management to make estimates and assumptions. These estimates and assumptions affect the reported amounts of assets, liabilities, comprehensive income and related disclosure. These estimates and underlying assumptions are reviewed on an ongoing basis. Where actual results differ from these estimates and assumptions, the impact will be recorded in future periods.

| ¡ | Provision for Claims: The Provision for Claims represents an estimate for expected claims and the related settlement expenses, net of the related expected property sale proceeds, for defaults from the mortgage loan insurance business that have occurred on or before the Consolidated Balance |

Sheet date. In calculating the estimated liability, an estimate of losses on defaults that have been incurred but not reported is made using historical experience and the time value of money, which considers prevailing legal, economic, social and regulatory trends. See Note 14 for further details. |

| ¡ | Unearned Premiums: Mortgage loan insurance premiums are deferred and recognized as revenue over the period covered by the insurance contracts using actuarially determined factors that are reviewed annually as part of the Actuarial Valuation. The premium earning factors are derived from claim occurrence patterns based on the principle that premiums will be earned at the same rate as claims are incurred. See Note 14 for further details. |

| ¡ | Financial Instruments: Financial instruments carried at fair value are measured based on quoted market prices observable in the market or amounts derived from cash flow models or other valuation methodologies. The fair value measurement hierarchy described in Note 17 reflects the significance of the inputs used in making these measurements. |

| ¡ | Post-employment Benefits: The annual cost of pension and other post-employment benefits earned by employees is actuarially determined using the projected unit credit method prorated on service and CMHC Management’s best estimate of expected long-term pension plan investment performance, compensation increases, retirement ages of employees, mortality of members and expected health care costs. These assumptions are of a long-term nature, which is consistent with the nature of post-employment benefits. See Note 21 for further details. |

FUTURE ACCOUNTING CHANGES

The International Accounting Standards Board (IASB) continues to develop and publish accounting standards in order to achieve high quality financial reporting. CMHC actively monitors the new standards and amendments to existing standards that have been issued by the IASB but are not yet effective on the date of issuance of these Consolidated Financial Statements. The following pronouncements, listed by

49

applicable annual accounting period effective date, have been identified as potentially having an impact on the Corporation’s results and Consolidated Financial Statements in the future.

| New Standards | Effective for or after | |||

| IFRS 10 | Consolidated Financial Statements | 1 January 2013 | ||

| IFRS 11 | Joint Arrangements | 1 January 2013 | ||

| IFRS 12 | Disclosure of Interests in Other Entities | 1 January 2013 | ||

| IFRS 13 | Fair Value Measurement | 1 January 2013 | ||

| IFRS 9 | Financial Instruments | 1 January 2015 | ||

| Amended Standards | ||||

| IFRS 10 | Consolidated Financial Statements | 1 January 2013 | ||

| IFRS 11 | Joint Arrangements | 1 January 2013 | ||

| IFRS 12 | Disclosure of Interests in Other Entities | 1 January 2013 | ||

| IFRS 7 | Financial Instruments: Disclosures | 1 January 2013 | ||

| IAS 19 | Employee Benefits | 1 January 2013 | ||

| IAS 32 | Financial Instruments: Presentation | 1 January 2014 | ||

IFRS 10 Consolidated Financial Statements provides a single consolidation model that identifies control as the basis for consolidation. As CMHC’s current accounting and consolidation practices are compliant under IFRS 10 consolidation guidelines, it does not expect that the new and amended standard will have a material impact on its Consolidated Financial Statements.

IFRS 11 Joint Arrangements establishes principles for financial reporting of joint arrangements. CMHC does not expect that the new and amended standard will have a material impact on its Consolidated Financial Statements.

IFRS 12 Disclosure of Interests in Other Entities enhances and replaces the disclosure requirements for subsidiaries, joint arrangements, associates and unconsolidated structured entities. CMHC has determined that this new standard and amendments will require adjustments to its current note disclosure.

IFRS 13 Fair Value Measurement defines fair value, sets out a single framework for measuring fair value and requires disclosures about fair value measurements.

While IFRS 13 does not introduce any new requirements, it reduces complexity and improves consistency by clarifying the definition of fair value and requiring its application to all fair value measurements. CMHC currently follows the IFRS 13 principles for determining fair value on most of its financial instruments, except for certain rent-producing real estate properties under the Lending Activity. These properties are fair valued based on the present value of expected future cash flows using a discount rate reflective of the characteristics of the property. Upon adoption of this new standard, all of CMHC’s real estate properties will be required to be valued at their highest and best use values, resulting in a potential increase in fair value of the properties as well as an increase to CMHC’s Net Income. CMHC also anticipates enhanced disclosure requirements relating to fair value measurement information.

Amendments to IFRS 7 Financial Instruments: Disclosures provide new disclosure requirements in netting arrangements to enable users of financial statements to better compare financial statements prepared in accordance with IFRS and U.S. GAAP. CMHC has determined that these amendments will require adjustments to its current note disclosure.

Amendments to IAS 19 Employee Benefits update the existing standard by eliminating the “corridor method” and improve the recognition, presentation and disclosure requirements for defined benefit plans. As CMHC has adopted the change from the corridor method upon implementation of IFRS, this component of the amendment will not affect the Consolidated Financial Statements. CMHC’s analysis of the other changes indicates that the amendments will result in an overall change in pension expenses reflected in Net Income with a corresponding offset in actuarial gains and losses recognized in Other Comprehensive Income. This change is due to the discount rate being applied to the plan assets to calculate the estimated return by the plan rather than the expected rate of return that was previously allowed. These amendments also include enhanced disclosure requirements.

In 2013, CMHC will determine the impact of the amendments to IAS 32 Financial Instruments: Presentation on its Consolidated Financial Statements.

50 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

PERFORMANCE BY OBJECTIVE

CORPORATE PLAN FRAMEWORK

At the beginning of 2012, CMHC’s 2012-2016 Corporate Plan comprised three objectives and seven strategic priorities. As part of the deficit reduction measures announced in Budget 2012, strategic priority 3.2 on CMHC’s export promotion activities was removed from the Framework as these activities were discontinued. (See discussion in the Summary of Financial Results section.) No other changes were made to the 2012-2016 Framework which guided CMHC’s planning and reporting of activities in 2012.

Amendments to the National Housing Act in June of 2012 led to further revisions to the Framework for the 2013-2017 planning period. Additional details are found in the 2013-2017 Summary of the Corporate Plan which was tabled in Parliament on March 22, 2013.This Summary is available on CMHC’s website.

Activities under strategic priorities 1.1, 1.2, 2.3, 3.1, and 3.2 in this year’s framework are funded by the Government of Canada through Parliamentary appropriations. Mortgage loan insurance and securitization activities under strategic priorities 2.1 and 2.2 are operated on a commercial basis at no cost to Canadian taxpayers.

Analysis of performance and financial results is provided for the seven strategic priorities as depicted by the following diagram. |

51

52 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N

OBJECTIVE 1 HELP CANADIANS IN NEED

Under this objective, CMHC pursues two strategic priorities which help address the housing needs of Canadians, including Aboriginal Canadians living both on and off reserve.

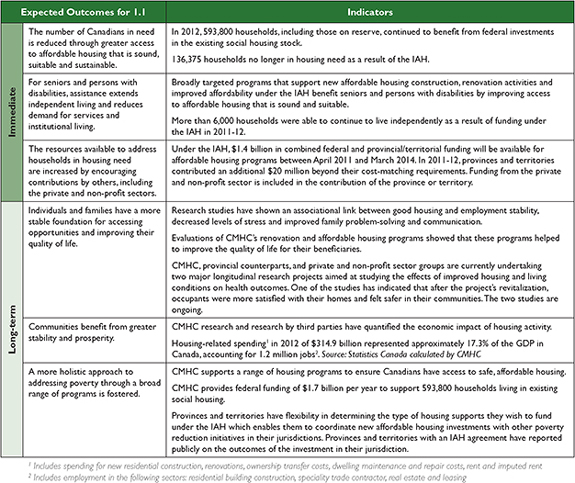

Access to affordable, sound and suitable housing provides individuals and families with a stable foundation from which to pursue educational and employment opportunities and contributes to improved health and overall quality of life. While the majority of Canadians are able to meet their housing needs without direct public assistance, many low-income individuals and families living on and off reserve require assistance. The federal government, through CMHC, provides significant investments in support of the existing social housing stock as well as new funding toward affordable housing programs to address housing need.

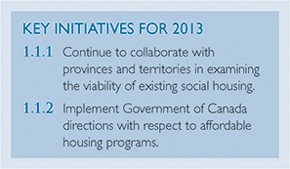

STRATEGIC PRIORITY | 1.1 | HELP CANADIANS IN NEED ACCESS AFFORDABLE, SOUND AND SUITABLE HOUSING |

RESOURCES

| OPERATING EXPENSES $55 MILLION | STAFF-YEARS 346 | ||

| Performance Measures |

2011 Actual | 2012 | 2013 Plan | |||||||||||||

| Plan | Actual | |||||||||||||||

Housing Programs expenses1 excluding operating expenses ($M) | 2,044 | 2,023 | 2,074 | 1,988 | ||||||||||||

Affordable housing expenditures2 ($M) | 127.1 | 411.5 | 367.0 | 257.8 | ||||||||||||

Direct Lending ($M) | 1,392.1 | 830.0 | 1,012.6 | 1,117.5 | ||||||||||||

Estimated number of households assisted through long-term social housing commitments | 604,200 | 597,800 | 593,800 | 585,800 | ||||||||||||

Affordable housing units facilitated by CMHC’s Affordable Housing Centre | 2,838 | 2,715 | 3,196 | 2,940 | ||||||||||||

| 1 | Includes Housing Programs expenses under 1.1, 1.2, 2.3, 3.1, and 3.2. |

| 2 | Includes expenditures under the IAH, AHI and renovation programs and are part of overall Housing Programs expenses; full take-up of the fiscal year budget is expected. |

PERFORMANCE ANALYSIS

CMHC provides federal investments in affordable, suitable and sound housing for low-income Canadians. These investments include ongoing subsidies for the existing social housing stock as well as new funding for affordable housing programs under the Investment in Affordable Housing (IAH) 2011-2014 Framework. CMHC also provides advice, information and financial assistance to groups wishing to develop affordable housing without the need for long-term federal subsidies through its Affordable Housing Centre.

CMHC substantially succeeded in meeting its performance targets. The affordable housing expenditure budget is provided on a fiscal year basis (April – March). As at 31 December 2012, spending of $367 million from this budget was lower than initially planned for two provinces, but full take-up of the budget by fiscal year-end is expected.

53

HOUSING NEED IN CANADA

According to Census-based estimates, 12.7% or 1.5 million Canadian households in 2006 were unable to find adequate and suitable housing without spending 30% or more of their income. This represents a 7.3% decrease in the incidence of core housing need since 2001. Although experiencing a decline in their respective core need incidences between 2001 and 2006, renters, lone parents, non-family households, Aboriginal Canadians and seniors continue to have a higher incidence of core housing need than the average Canadian household. Recent immigrants also experience a much higher incidence of core housing need.