EXHIBIT 99.2

2015 ANNUAL REPORT

WHY

Housing Matters

Canada

CMHC SCHL

CMHC

Canada’s authority

on housing

Our Mandate

Facilitate access

to housing

Contribute to

financial stability

Our Mission

We help

Canadians meet

their housing needs

Our Vision

The heart of a

world-leading

housing system

CONTENTS

MESSAGES 4

MANAGEMENT’S DISCUSSION AND ANALYSIS 9

Condensed Consolidated Financial Results 10

Operating Environment 12

Corporate Performance Framework 16

Risk Management 18

Performance by Activity 24

Market Analysis and Research 24

Assisted Housing 27

Mortgage Loan Insurance 33

Securitization 41

People and Processes 46

Historical Information 51

EXPECTED OUTCOMES 53

CONSOLIDATED FINANCIAL STATEMENTS 57

OTHER INFORMATION 117

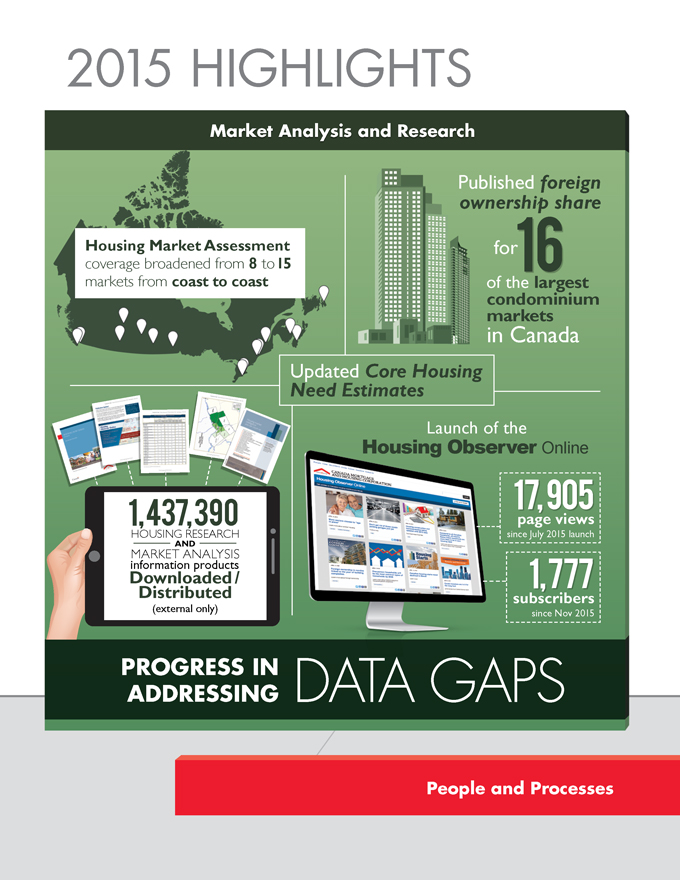

2015 HIGHLIGHTS

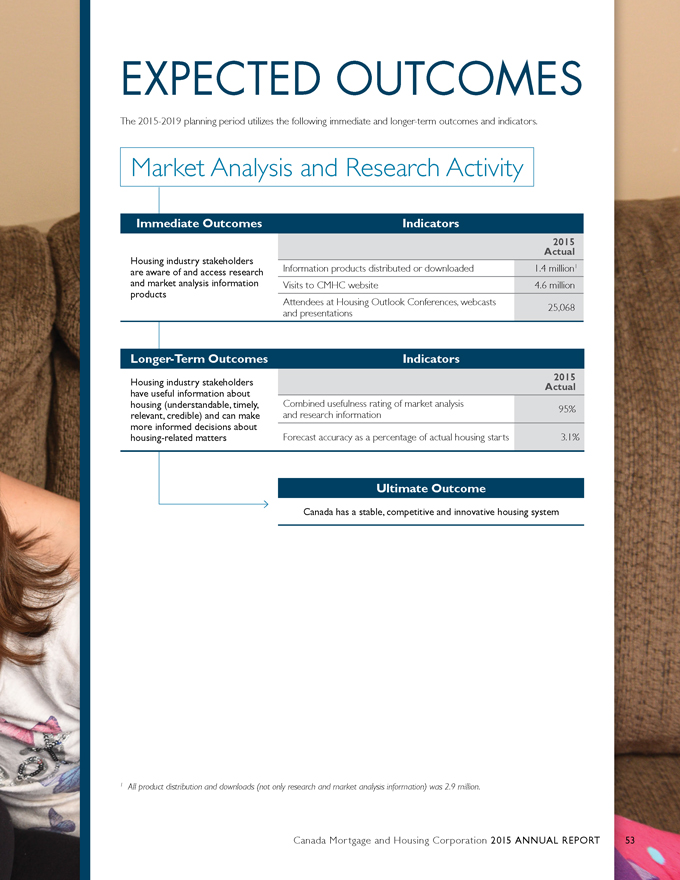

Market Analysis and Research

Housing Market Assessment

coverage broadened from 8 to 15 markets from coast to coast

Published foreign ownership share for 16 of the largest condominium markets in Canada

Updated Core Housing Need Estimates

1,437,390

HOUSING RESEARCH

AND

MARKET ANALYSIS

information products

Downloaded/Distributed

(external only)

Launch of the Housing Observer Online

17,905 page views since July 2015 launch

1,777 subscribers since Nov 2015

PROGRESS IN ADDRESSING

DATA GAPS

People and Processes

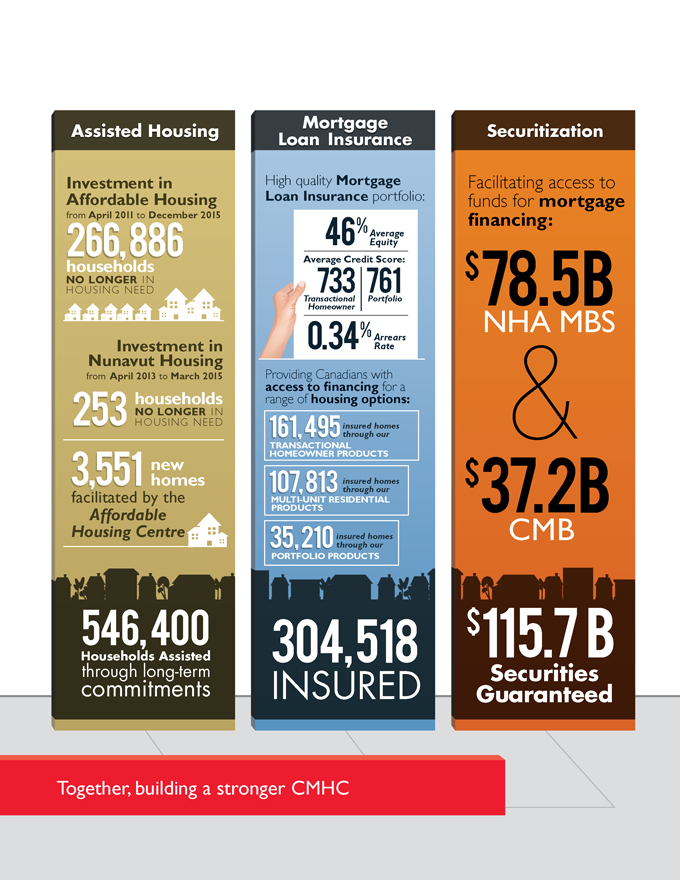

Assisted Housing

Investment in Affordable Housing from April 2011 to December 2015

266,886 households NO LONGER IN HOUSING NEED

Investment in Nunavut Housing from April 2013 to March 2015

253 households NO LONGER IN HOUSING NEED

3,551 new homes

facilitated by the Affordable Housing Centre

546,400 Households Assisted through long-term commitments

Mortgage Loan Insurance

High quality Mortgage Loan Insurance portfolio:

46% Average Equity

Average Credit Score:

733 Transactional Homeowner

761 Portfolio

0.34% Arrears Rate

Providing Canadians with access to financing for a range of housing options:

161,495 insured homes through our TRANSACTIONAL HOMEOWNER PRODUCTS

107,813 insured homes through our MULTI-UNIT RESIDENTIAL PRODUCTS

35,210 insured homes through our PORTFOLIO PRODUCTS

304,518 INSURED

Securitization

Facilitating access to funds for mortgage financing:

$78.5B NHA MBS & $37.2B CMB

$115,7B Securities Guaranteed

Together, building a stronger CMHC

MESSAGE FROM THE

CHAIRPERSON

On behalf of the Board of Directors, I am pleased to present CMHC’s 2015 Annual Report. During the year, the Board provided ongoing governance over CMHC’s activities on fulfilling its mandate.

Housing markets across Canada indicate increasing evidence of overvaluation with prices and household debt levels again rising faster than wages, most notably in Vancouver and Toronto. As a result, the Board was very supportive of the federal government’s announcement in December of an increase in the minimum down payment for mortgage loan insurance and OSFI’s intention to increase capital levels for mortgage assets held by lenders. Slowing global growth, deflation, debt levels and declining oil prices represent material risks to our national economy and to oil-producing provinces in particular.

We are pleased to note that residential mortgage arrears rates remained low and credit scores were good. CMHC’s profitability and capital levels remained strong. The Board supports CMHC’s ongoing efforts to enhance its financial disclosures, market analysis and commentary for Canadians. Strengthening risk management practices continues to be a priority, particularly in this environment.

By helping to facilitate access to mortgage financing for qualified Canadian borrowers, particularly first time homeowners, CMHC’s mortgage loan insurance and securitization guarantee programs contribute to the stability of the financial system. Further adjustments were made to these programs in 2015, with the goal of reducing taxpayer exposure to housing markets while ensuring that CMHC remains well-positioned to scale-up its housing finance activities if needed as a policy tool to address future economic disruptions.

Facilitating access to housing also means supporting Canadians in housing need.

In 2015, CMHC continued to work with a broad range of partners to deliver the federal investment in housing. Housing needs differ across the country, and the Board had the opportunity to learn about the unique housing challenges in Nunavut when we held our August meeting in Iqaluit. This experience deepened our understanding of housing needs in the North and our appreciation for the work CMHC is doing there. We are aware of the need for innovative new approaches to support Northerners and other Canadians whose housing needs are not being met in the market. In this regard, we were pleased to note the federal government’s related announcements in the recent budget.

I would like to thank the Corporation’s senior management team and employees across the country for their outstanding support to the Board again this year.

Robert P. Kelly Chairperson

4 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

MESSAGE FROM THE

PRESIDENT

2015 was another year of changes for CMHC. Continuing with the CMHC in motion framework launched in 2014, we built an organization that Canadians can count on in good times and in bad.

Results

We generated profits of $1.5 billion on revenues of $4.6 billion in 2015. These results were lower than plan primarily as a result of a lower than planned interest rate environment, which reduced our returns on investments; coupled with timing differences on the implementation of the new strategic asset allocation in the Mortgage Loan Insurance Activity. In terms of controllable factors, however, we delivered operating budget expenses of 11.1% of revenue received compared to a plan of 12.8%. Most of these savings were as a result of reduced post-employment benefits and slower than planned recruiting for open positions.

Our Insurance Claims Paid were $353 million, a 9.5% improvement compared to 2014 due to healthy real estate markets and improved underwriting. Our Loss Ratio improved from 19.4% in 2014 to 18.2% in 2015. Credit quality continues to improve on our Mortgage Loan Insurance portfolio and at year-end our arrears stood at 0.34% compared to 0.35% in 2014. These factors contributed to strong Return on Capital Holding Target of 12.9%. Securitization benefitted from higher guarantee fee rates and returned 17.9% on Required Capital.

Our Assisted Housing business delivered $2 billion directly on-reserve and via provinces and territories off-reserve. This business unit met or exceeded all of its performance targets in 2015, creating more homes than planned for Canadians.

We ended the year with $19.4 billion in total capital available. At 354% of our minimum capital target for the Mortgage Loan Insurance Activity, we have significant excess capital. We plan to work with the Department of Finance on a dividend policy in 2016 to help ensure the Government’s financial resources are most efficiently managed.

Building a Stronger CMHC

In addition to managing for results in 2015, together we devoted a lot of energy to building a stronger company for the future:

Putting People First

We started the year with a fully re-imagined organizational structure, reflecting new operating models designed specifically to achieve our strategy. We flattened the organization to eliminate bureaucracy and speed up decision making, reducing layers in the company from nine to six in most areas and expanding the average span of control of managers from three to six. These changes, while crucial, took some time to absorb.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 5

Through the year, we welcomed 352 new full time colleagues, people who brought fresh energy. At the end of the year, our workforce consisted of 57% women (53% members of Management Committee) and close to 25% members of minority groups, and we were recognized as one of Canada’s Best Diversity Employers. Last, we engaged in a dialogue about what we wanted our culture to be, culminating in ten new organizational values which you will find on the back cover of this report. We were again recognized as having one of Canada’s Most Admired Corporate Cultures.

We deepened our succession planning during the year, providing clearer career paths for members of our 129-person National Leadership Team. And we continued to focus on building a healthier workplace. By year-end, 95% of our employees were trained in mental health awareness and 100% of our senior leaders were trained as mental health ambassadors.

In the end, however, we fell short on our goals related to employee engagement and enablement. That said, our overall engagement level of 74% was still consistent with high-performing organizations. Our people are still adapting to a new organizational model. This change, along with an office move and the exploration of a third-party information and technology partnership, has hurt morale. We are determined to hit our targets, since we need the employee commitment and motivation they measure. Prioritizing work and creating time to allow people to innovate will help.

Strategy

The Board and senior management built on our work in 2014 to more clearly express our Strategic Directions, as described below.

| 1. | Align Risk With Mandate: Focusing our risk management on those areas we are best equipped to manage is the key to how we operate. We want to be a best-in-class risk manager for household mortgage credit, our most significant financial risk. Improvements in our internal controls continued in 2015, and significant progress was made in addressing the recommendations stemming from the Office of the Superintendent of Financial Institutions and Internal Audit reviews of our operations. In addition, we implemented new economic capital management discipline with new tools and personnel in 2015. We also devoted energy to improving our risk culture corporate-wide during the year, via training on our “Three Lines of Defence” risk governance model, resulting in average improvements of 65% of risk awareness among our staff. Last, we published for Canadians the result of our expanded stress testing results, both to be accountable and to invite improvements to our risk management approach. |

| 2. | Lead Through Information and Insight: As Canada’s authority on housing, we reclaimed a leadership role in the Canadian housing sector in 2015. We expanded our Housing Market Assessment framework, spawning more informed discussions about the state of local housing markets; and, we expanded our quarterly disclosure to include Securitization and Covered Bond supplements, in addition to the Mortgage Loan Insurance supplement we commenced in 2014. Critically, we also highlighted data gaps in the housing sector and worked with industry participants and commentators in developing tactics to improve transparency of information in housing markets. Finally, our policy team worked hard during the year to prepare the new Government’s ambitious housing initiatives. |

| 3. | Be a High-Performing Organization: Our goal is to be one of the truly special companies in Canada. In addition to all that we did to put people first in 2015, we modified our employee offering to promote better alignment with our mission and strategy. This involved a new performance management framework with clearer links between pay and performance. In addition, we announced the combination of two existing components of our pension plan - the legacy defined benefit and the new employee defined contribution - into one defined benefit pension plan for all which we think will be a model for other companies. Last, we improved our reporting against objectives, making it clearer with our people how we measure success in our business. |

Outlook

Moving into 2016, our work continues. Our key priorities this year are to focus on consistent execution and opportunities to innovate, particularly in the following areas:

| ¡ | | Achieving our Corporate Plan priorities – which includes further progress on internal controls and risk management; |

| ¡ | | Implementing the new government housing policies; |

| ¡ | | Expanding our succession planning and talent management activities; and |

| ¡ | | Developing a strategy to overcome years of under investment in our information and technology platform and capabilities. |

There remains much work to be done in 2016. Our people at CMHC have assumed a significant responsibility: both to do our best work day-to-day for Canadians as well as to build a high-performing organization. I am incredibly grateful for our employees’ dedication to CMHC and to the changes underway. After 70 years, there is much to be proud of. Together, we are creating an even prouder future.

Evan Siddall

President and Chief Executive Officer

MANAGEMENT’S

DISCUSSION

AND ANALYSIS

The following Management’s Discussion and Analysis (MD&A) of the financial condition and results of operations as approved by the Board of Directors on 23 March 2016 is prepared for the year ended 31 December 2015. This MD&A should be read in conjunction with the audited Consolidated Financial Statements. Unless otherwise indicated, all financial information in this report has been prepared in accordance with International Financial Reporting Standards (IFRS) and all amounts are expressed in Canadian dollars.

Forward-Looking Statements

Our Annual Report contains forward-looking statements which include, but are not limited to, statements with respect to our outlook for the regulatory environment in which we operate, the outlook and priorities for each activity and the risk environment. By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties which may cause actual results to differ materially from expectations expressed in the forward-looking statements.

Non-IFRS Measures

We use a number of financial measures to assess our performance. Some of these measures are not calculated in accordance with IFRS, are not defined by IFRS, and do not have standardized meanings that would ensure consistency and comparability with other institutions. These non-IFRS measures are presented to supplement the information disclosed in the Consolidated Financial Statements and Notes to the Consolidated Financial Statements which are prepared in accordance with IFRS and may be useful in analyzing performance and understanding the measures used by management in its financial and operational decision making. Where non-IFRS measures are used throughout the Annual Report, a definition of the term will be disclosed in the Glossary for Non-IFRS Financial Measures.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 9

Condensed Consolidated

Financial Results

Condensed Consolidated Balance Sheets

| | | | | | | | |

(in millions) | | | 2015 | | | | 2014 | |

Total Assets | | | 252,107 | | | | 248,490 | |

Total Liabilities | | | 232,468 | | | | 230,308 | |

Total Equity of Canada | | | 19,639 | | | | 18,182 | |

Total Assets increased by $3,617 million (1.5%) from 31 December 2014 primarily due to net purchases of National Housing Act Mortgage-Backed Securities (NHA MBS) in the Canada Mortgage Bonds (CMB) program, partially offset by the maturity of the Insured Mortgage Purchase Program (IMPP) in Q1 2015. Loan repayments in Assisted Housing outpaced new loans issued, also partially offsetting the increase in Loans.

Total Liabilities increased by $2,160 million (0.9%) from 31 December 2014 primarily due to net issuances of CMB, partially offset by the maturity of the IMPP in Q1 2015 as well as net repayments on the Assisted Housing borrowings.

Condensed Consolidated Statements of Income

and Comprehensive Income

| | | | | | | | |

(in millions) | | | 2015 | | | | 2014 | |

Total Revenues | | | 4,636 | | | | 6,199 | |

Total Expenses | | | 2,672 | | | | 2,712 | |

Income Taxes | | | 476 | | | | 862 | |

Net Income | | | 1,488 | | | | 2,625 | |

Other Comprehensive Loss | | | (31) | | | | (281) | |

Comprehensive Income | | | 1,457 | | | | 2,344 | |

Total Revenues were $4,636 million for the year ended 31 December 2015, a $1,563 million (25.2%) decrease from the prior year primarily due to lower Premium and Fees Earned and Net Realized Gains (Losses).

Premiums and Fees Earned decreased by $73 million (3.8%) primarily due to declining insured volumes in the Mortgage Loan Insurance Activity over the past several years, partially offset by the increases in premium and fee pricing implemented in both the Mortgage Loan Insurance and Securitization Activities.

Net Realized Gains (Losses) decreased by $1,489 million (102.4%) primarily due to the transition to the new investment asset mix in 2014 in the Mortgage Loan Insurance investment portfolio that resulted in a significant volume of investment security sales in that period.

Total Expenses decreased by $40 million (1.5%) from the prior year primarily due to Insurance Claims and Operating Expenses partially offset by an increase in Housing Programs Expenses.

Insurance Claims were $290 million in 2015, a $38 million (11.6%) decrease from prior year primarily due to improvements in underwriting practices implemented in 2012 where the parameters for eligible mortgages were changed; and as a result, the business written subsequent to 2012 has had improved risk characteristics compared to older business.

10 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Operating Expenses decreased by $41 million (11.0%) for the year ended 31 December 2015, primarily due to a reduction in costs from the recognition of a plan amendment gain resulting from the changes to the other post-employment benefit plans in 2015. In addition, employee related costs were lower in 2015 as there were no restructuring activities when compared to 2014.

Appropriations spending related to Housing Programs Expenses for the period ended 31 December 2015 was $2,049 million, an increase of $39 million (1.9%) when compared to 2014. The increase is primarily due to the timing of expenditures under the Investment in Affordable Housing (IAH), partially offset by the timing of expenditures for affordable housing in Nunavut.

Net Income was $1,488 million for the year ended 31 December 2015, a $1,137 million (43.3%) decrease from the prior year primarily due to lower Net Realized Gains (Losses), partially offset by the resulting decrease in Income Taxes.

Other Comprehensive Loss (OCL) was $31 million for the year ended 31 December 2015, a $250 million (89.0%) increase from the prior year primarily due to lower Reclassification of Prior Years’ Net Unrealized Gains Realized in the Period in Net Income from significantly lower trading activity in the Mortgage Loan Insurance investment portfolio and the impact of a constant discount rate in 2015 (compared to a decrease in the prior year) on Remeasurements of the Net Defined Benefit Plans. These increases to OCL were offset by the Net Unrealized Gains from Available for Sale Financial Instruments mainly due to modest declines in the yields compared to 2014 resulting in lower gains on the fixed income portfolio.

Performance against 2015 Plan

| | | | | | | | |

| | | | 2015 | |

(in millions) | | | Plan | | | | Actual | |

Total Revenues | | | 5,050 | | | | 4,636 | |

Total Expenses | | | 2,836 | | | | 2,672 | |

Income Taxes | | | 538 | | | | 476 | |

Net Income | | | 1,676 | | | | 1,488 | |

Total Assets | | | 253,611 | | | | 252,107 | |

Total Liabilities | | | 234,910 | | | | 232,468 | |

Total Equity of Canada | | | 18,701 | | | | 19,639 | |

Total Revenues were $414 million (8.2%) lower than plan primarily due to Investment Income and Net Realized Gains (Losses) which were lower than plan due to bond yields trending lower than expected, coupled with the timing of the implementation of the new investment asset mix. In addition, Parliamentary Appropriations for Housing Programs were lower than plan primarily due to timing of expenditures.

Total Expenses were $164 million (5.8%) lower than plan mainly due to timing of Housing Program Expenses as well as lower Operating Expenses due to the amendment gain resulting from the changes to the other post-employment benefit plans that was unplanned. In addition, there were fewer employees compared to plan resulting in reduced operating expenses.

Net Income was $188 million (11.2%) lower than plan primarily due to lower Investment Income and Net Realized Gains (Losses) offset by lower Operating Expenses as explained previously.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 11

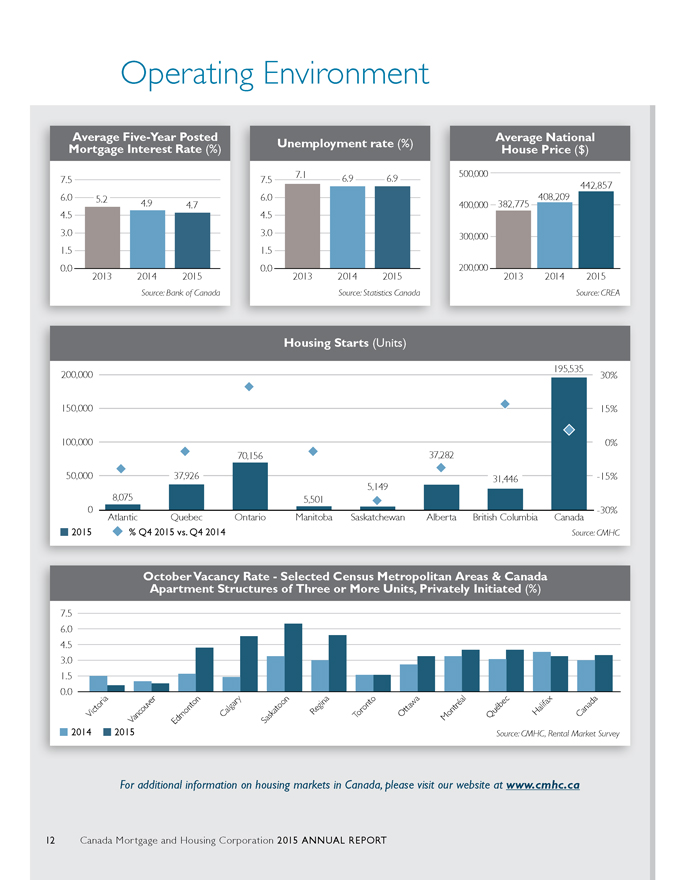

Operating Environment

Average Five-Year Posted Mortgage Interest Rate (%)

7.5 6.0 4.5 3.0 1.5 0.0 5.2 4.9 4.7

2013 2014 2015

Source: Bank of Canada

Unemployment rate (%)

7.5 6.0 4.5 3.0 1.5 0.0 7.1 6.9 6.9

2013 2014 2015

Source: Statistics Canada

Average National House Price ($)

500,000 400,000 300,000 200,000

382,775

408,209

442,857

2013 2014 2015

Source: CREA

Housing Starts (Units)

200,000

150,000

100,000

50,000

0

8,075

37,926

70,156

5,501

5,149

37,282

31,446

195,535

30% 15% 0% -15% -30%

Atlantic Quebec Ontario Manitoba Saskatchewan Alberta British Columbia Canada

2015 % Q4 2015 vs. Q4 2014

Source: CMHC

October Vacancy Rate - Selected Census Metropolitan Areas & Canada Apartment Structures of Three or More Units, Privately Initiated (%)

7.5 6.0 4.5 3.0 1.5 0.0

Victoria Vancouver Edmonton Calgary Saskatoon Regina Toronto Ottawa Montreal Quebec Halifax Canada

2014 2015

Source: CMHC, Rental Market Survey

For additional information on housing markets in Canada, please visit our website at www.cmhc.ca

12 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Economic Conditions And Housing Indicators

During 2015, the prolonged decline in oil prices triggered two consecutive quarters of contraction in the real gross domestic product (GDP). Nevertheless, overall housing activity continued to be supported by employment gains and low interest rates. Nationally, the average Multiple Listing Service® (MLS®)1 price increased by 8.5% relative to 2014 due in part to continued greater MLS® sales growth in more expensive markets in Ontario and British Columbia.

Total housing starts increased in 2015 compared to 2014, largely driven by the condominium market in Toronto; however, there were significant regional disparities in the pace of housing starts. For example, housing starts were higher in provinces less exposed to the energy sector, in particular British Columbia and Ontario improved as businesses benefitted from declining input costs as a result of lower oil prices, lower interest rates and a lower US dollar exchange rate. Strength in Ontario was particularly evident in Q4 2015 as housing starts rose 24.6% (versus Q4 2014) and finished up 18.6% in 2015 versus 2014. Meanwhile, in British Columbia, housing starts were also robust in Q4 2015 rising 16.8% (versus Q4 2014) and finished up 10.9% in 2015. On the other hand, housing starts activity slowed in oil-producing provinces, such as Newfoundland and Labrador, Saskatchewan and particularly in Alberta, where the decline in world oil prices had a particularly negative impact on economic conditions. In Alberta, housing starts were strong in Q1 2015 but weakened for the remainder of the year. In Q4 2015 housing starts in Alberta were down 11.8% compared to a year earlier and finished down 8.1% in 2015. In Saskatchewan, housing starts were weak throughout 2015, falling 26.6% in Q4 2015 (versus Q4 2014) and finished down 37.6% in 2015.

The rental vacancy rate increased in 2015, due to an increase in the supply of purpose-built homes available for rent, combined with reduced demand as a result of lower immigration to Canada and weaker employment prospects for younger Canadians. The largest increase in vacancy rates was registered in Alberta, followed by Saskatchewan. This reflects the fact that, among the provinces, Alberta and Saskatchewan generally saw the largest deterioration in net migration and employment conditions, due to the negative economic impact of oil prices, combined with increases in the supply of purpose-built homes available for rent in both provinces.

Draft Guideline E-21 Operational Risk Management

In August 2015, the Office of the Superintendent of Financial Institutions (OSFI) issued its draft Guideline E-21 Operational Risk Management for Federally Regulated Financial Institutions for which public comments were accepted until 9 October 2015. OSFI’s intent was to clarify its expectations for Federally Regulated Financial Institutions’ operational risk management and provide a comprehensive guideline. The draft guideline contains four principles: (i) fully integrated and appropriately documented operational risk management framework; (ii) supports the overall corporate governance structure, including an operational risk appetite statement; (iii) ensures effective accountability for operational risk management using a three lines of defence approach or other robust structure; and (iv) identification and assessment of operational risk through the use of appropriate management tools. Most of the practices and procedures in the draft guideline have already been adopted or are being deployed and we do not anticipate any significant changes to our operations upon the implementation of the final guideline.

1 Multiple Listing Service® (MLS®) is a registered trademark owned by the Canadian Real Estate Association.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 13

Mortgage Loan Insurance Developments

Minimum Capital Test for Mortgage Loan Insurers

OSFI is in the process of developing a new capital framework specific to mortgage insurers which will replace the current Minimum Capital Test (MCT). As a result, mortgage loan insurers are expected to use an interim capital framework, which is a modified version of the MCT for federally regulated property and casualty insurers that was released by OSFI on 24 September 2014. We implemented the new interim capital framework on 1 January 2015, which resulted in an increase in MCT required capital and a reduction in our MCT ratio.

Portfolio Insurance

For 2015, we continued to employ a lender allocation methodology and maintained our annual limit of issuance of portfolio insurance at $9 billion. This process helps to increase access to funding for small and medium-sized lenders while increasing market discipline in residential lending and reducing taxpayer exposure to the housing sector.

Substitution Feature on Portfolio Pools

In Budget 2015, the Government of Canada (Government) announced that it would implement regulatory measures that limit the extension of portfolio insurance through the substitution of mortgages in insured pools, tie the use of portfolio insurance to our securitization vehicles and prohibit the use of government-backed mortgages as collateral in securitization vehicles that are not sponsored by us.

We previously eliminated the substitution feature on new portfolio pools on 1 January 2014. The substitution feature continues to exist for portfolio pools insured on or before 31 December 2013.

Mortgage Loan Insurance Premiums

As a result of our annual review of insurance products and capital requirements, we increased homeowner mortgage loan insurance premiums for homebuyers with less than a 10% down payment. Effective 1 June 2015, mortgage loan insurance premiums for these homebuyers increased by approximately 15%. There were no changes to premiums for our portfolio insurance and multi-unit insurance products or to premiums for homebuyers who make down payments of 10% or more of the purchase price of their home.

Minimum Down Payment Rules

On 11 December 2015, the Government announced changes to the rules for government-backed mortgage insurance to contain risks in the housing market, reduce taxpayer exposure and support long-term stability. Effective 15 February 2016, the minimum down payment for new insured mortgages increased from 5% to 10% for the portion of the house price above $500,000. The 5% minimum down payment for properties up to $500,000 remains unchanged. Refer to the Mortgage Loan Insurance Activity section for further details.

Changes to Capital Requirements for Residential Mortgages

On 11 December 2015, OSFI announced its plans to update the regulatory capital requirements for loans secured by residential real estate properties (i.e. residential mortgages). The anticipated changes will impact the regulatory capital requirements for those deposit taking institutions using internal models for mortgage default risk and the standardized capital requirements for Canada’s private mortgage insurers.

14 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

For federally regulated private mortgage insurers, OSFI will introduce a new standardized approach that updates the capital requirements for mortgage guarantee insurance risk and will require more capital when house prices are high relative to borrower incomes.

OSFI will consult with federally regulated financial institutions and other stakeholders before making any changes and expects final rules to be in place no later than 2017. The anticipated changes may impact our regulatory capital requirements.

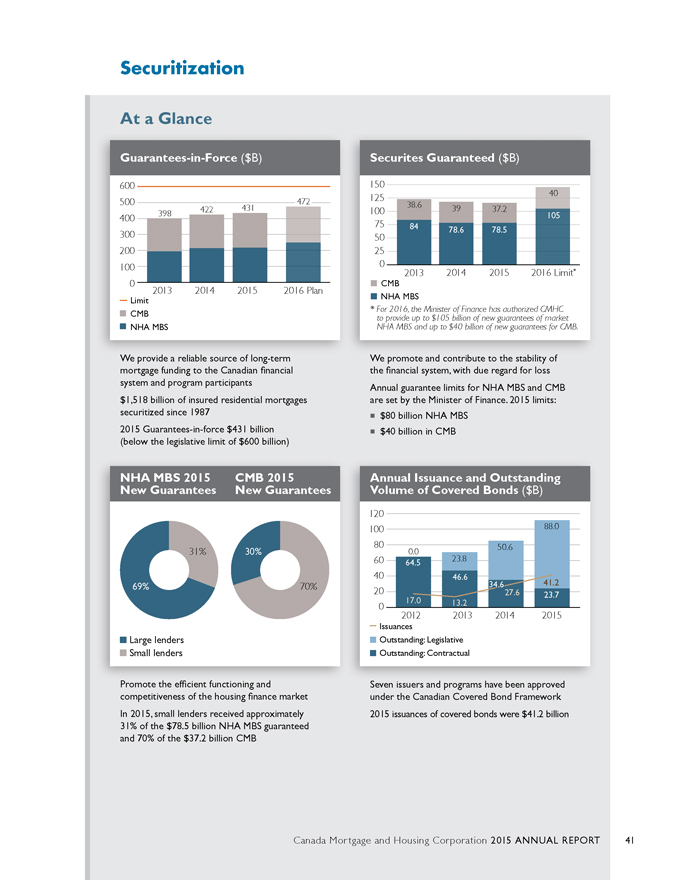

Securitization Developments

Annual Limits on New Securities Guaranteed

Pursuant to the National Housing Act (NHA), the Minister of Finance approves the terms and conditions for our Securitization Programs, including the maximum guarantees for the year. The 2015 approved limits were the same as the 2014 limits: $80 billion in NHA MBS and $40 billion in CMB.

Insured Mortgage Purchase Program

The IMPP, included within the Securitization Activity, matured in March 2015, at which time all loans and borrowings from the Government were repaid.

Securitization Guarantee Fees

Guarantee fees charged to Issuers of NHA MBS and CMB increased on 1 April 2015. These changes were made in support of the Government’s effort to enhance the Canadian housing finance framework by encouraging the development of alternative funding options in the private market.

Fees Payable to the Government of Canada

Effective 1 April 2015, the fees we pay to the Government in recognition of its financial backing of the CMB increased.

Changes to NHA MBS Guarantee Fees

On 11 December 2015, CMHC announced an increase to the NHA MBS guarantee fees across all NHA MBS terms effective 1 July 2016. The revised fee structure is intended to encourage the development of alternative funding options in the private market.

Revised Allocation Methodology for New Guarantees

of Market NHA MBS

In conjunction with the changes to the NHA MBS Guarantee fees previously described, we also announced on 17 December 2015, the introduction of a revised allocation methodology for new guarantees of Market NHA MBS.

Under the current allocation methodology related Approved Issuers, where one is designated as an Aggregator that participates in the NHA MBS program, do not obtain a separate Market NHA MBS allocation. The new allocation methodology will allow Issuers to transfer a portion or all of their quarterly Market NHA MBS allocation to Aggregators. With the new allocation methodology, mortgage lenders will continue to have access to CMB funding through Aggregators after the new CMB guarantee fee structure becomes effective 1 July 2016.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 15

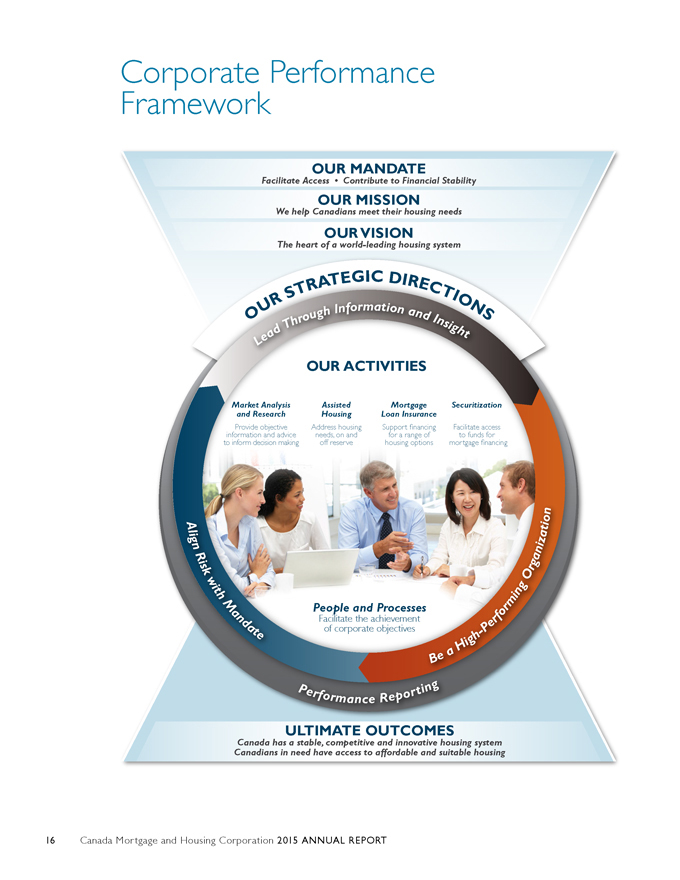

Corporate Performance Framework

OUR MANDATE

Facilitate Access • Contribute to Financial Stability

OUR MISSION

We help Canadians meet their housing needs

OUR VISION

The heart of a world-leading housing system

OUR STRATEGIC DIRECTIONS

Lead Through Information and Insight

OUR ACTIVITIES

Market Analysis and Research

Provide objective information and advice to inform decision making

Assisted Housing

Address housing needs, on and off reserve

Mortgage Loan Insurance

Support financing for a range of housing options

Securitization

Facilitate access to funds for mortgage financing

People and Processes

Facilitate the achievement of corporate objectives

Align Risk with Mandate

Be a High-Performing Organization

ULTIMATE OUTCOMES

Canada has a stable, competitive and innovative housing system Canadians in need have access to affordable and suitable housing

16 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Our corporate performance framework is organized around the needs of our clients and stakeholders. We deliver our mandate through four business activities – Market Analysis and Research, Assisted Housing, Mortgage Loan Insurance, and Securitization; all of which are supported by our infrastructure of people and processes. In support of our mission and vision, in 2015, we reviewed the drivers and risks affecting our business and developed strategic directions to guide decisions over the medium term.

Strategic Directions

In spring 2015, the Board of Directors approved three strategic directions to guide the Corporation over the next five years. These strategic directions will focus our efforts and activities to help Canadians meet their housing needs:

Align Risk with Mandate

Fulfilling its mandate to facilitate access to housing and contributing to financial stability means that we have a significant presence in the Canadian housing and financial system. By their very nature, our core business activities have the potential to expose taxpayers to a substantial amount of risk. Understanding and effectively managing these risks is critical to becoming a best-in-class risk manager and to the development of a consistent risk culture across the organization.

Lead Through Information and Insight

Given the importance of housing to the economy and to Canadians, we have responded to our stakeholders’ increasing request for more varied and comprehensive information on Canadian housing markets and the housing system. Being the heart of a world-leading housing system requires that we become Canada’s authority on housing. We will continue to improve outcomes through timely and relevant data analysis and knowledge.

Be a High-Performing Organization

Being a high-performing organization means continuously identifying and leveraging opportunities to improve. Four key traits of a high-performing organization are a focused role, an accountable culture, enabled people and efficient processes. Giving employees the tools to do their jobs through planned investments in financial and information and technology systems will move us toward a culture built around the principles of accountability.

Assessment of Performance Indicators

For each of our Activities, there are a number of performance indicators and immediate and longer-term outcomes that CMHC strives to attain. The performance indicators developed in the Summary of CMHC’s 2015-2019 Corporate Plan process are assessed based on the following:

| ¢ | Green to indicate target met or within 5% of plan. |

| ¢ | Red to indicate target was not met or achievement not within 5% of plan. |

Readers are encouraged to refer to the Summary of CMHC’s 2016-2020 Corporate Plan, which is available at www.cmhc.ca, for additional details on future directions and initiatives.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 17

Risk Management

To ensure that we continue to Align Risk with our Mandate, we have a structured risk management approach that ensures regular risk assessment and reporting, including an annual review and approval of the Enterprise Risk Management (ERM) policies, regular updates to the ERM Risk Register, Risk Appetite and Tolerance Statements and Quarterly Risk Management Reports.

We also conduct our Own Risk and Solvency Assessment (ORSA) to identify risks and assess the adequacy of our risk management and current and likely future capital needs and solvency positions. Stress testing is an important element of the ORSA process. Our stress testing framework specifies that we conduct our corporate-wide stress testing program in parallel with our annual corporate planning process.

ERM Framework

Our ERM framework includes the following components:

Risk Governance Model

We follow a “Three Lines of Defence” model to further enhance our risk governance structure and reinforce a strong risk management culture. This model promotes clear accountability for risk management, monitoring, independent oversight and independent assurance by delineating and defining roles and responsibilities across the Corporation. The graphic shown on the next page illustrates our Three Lines of Defence risk governance model.

The Board of Directors has the ultimate accountability and responsibility for risk management. The Board oversees the ERM framework and approves, on an annual basis, the corporate risk appetite statement. The Board is kept informed of key risks and mitigating strategies through a variety of reporting mechanisms and assistance from the Board Risk Management Committee. The Committee ensures that appropriate policies, procedures and controls are in place to identify, assess, and manage the key risks we face.

The President and CEO is accountable for ensuring that all key risks are appropriately identified and managed, and provides the Board with assurance that these activities are being completed in the annual ERM Letter of Representation.

The Chief Risk Officer (CRO) is responsible for the independent oversight of the management function of risks inherent in our activities, including establishing ERM policies and a framework to manage risk in alignment with our risk appetite and business strategies. The CRO is responsible for promoting an effective risk culture, implementing ERM policies and processes, and in helping the organization achieve its public policy mandate and objectives while paying due regard to its exposure to loss.

All members of Management play an integral role in ERM activities by identifying, monitoring and reporting potential risks within their areas of responsibilities and overseeing activities performed within and across the Three Lines of Defence.

The Risk Committee is a senior management committee which is involved in reviewing and approving all ERM reports prior to their presentation to the Board.

The CRO and Management are assisted in their risk management efforts by the ERM Committee which is comprised of senior level managers, representing all business activities and support functions. The ERM Committee is actively involved in the process of identifying, assessing, monitoring and reporting key risks including new and emerging risks.

18 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

BOARD OF DIRECTORS

Audit Committee

Risk Management Committee

Other Board Committees

SENIOR MANAGEMENT

Set CMHC’s risk appetite

Ensure risk taking is aligned with strategic plan and direction

Ensure a strong oversight & control structure is in place

Ensure clear accountability & ownership of risk and control with Businesses and Functions

1st Line of Defence

Identify and Control

1A – Business Areas and Support Functions Teams

(front line)

Take, manage and identify risks in day-to-day activities

Execute risk and control procedures on a day-to-day basis

Ensure risks are within CMHC’s risk appetite and risk management and control policies

1B – Operations Support Teams

(within Business Areas and Support Functions)

Monitor and test risk management activities performed by 1A

Monitor compliance with CMHC’s risk appetite and risk management and control policies

Provide input for risk reporting

2nd Line of Defence

Set Standards and Challenge

Chief Risk Officer (CRO) Sector, Chief Financial Officer (CFO) Sector (including Actuarial) and Chief Compliance Officer (CCO) Function

Develop and facilitate effective risk management and control policies

Independently challenge and oversee the 1st line of defence

Monitor and report risk exposure (incl. internal control) status

Provide training, tools, advice and support to 1st line

3rd Line of Defence

Independent Assurance

Internal Audit

Provide independent assurance on the effectiveness of governance, risk management, and internal controls, including the manner in which the other lines of defence achieve risk management and control objectives

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 19

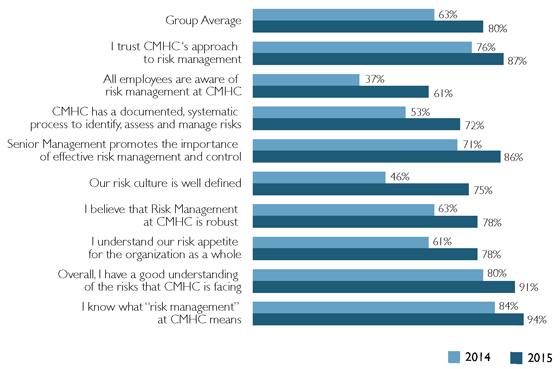

Risk Culture

We constantly cultivate a strong risk culture by promoting risk management knowledge, encouraging open communications and transparency on all aspects of risk, and providing regular risk management training across business lines.

We regularly assess risk culture among all employees through a comprehensive survey that allows the CRO sector to identify areas for improvement and to continue to empower employees with respect to their risk management responsibilities. The following table shows the results of our risk culture survey completed in 2014 and 2015. The results show the proportion of employees who agreed (strongly or somewhat) with the various statements.

Risk Management Policies

Comprehensive ERM policies guide our activities and encourage a risk-aware culture through discussion, evaluation and management of risks across our organization.

The ERM Policies are updated at least annually, with review and approval by senior management and the Board.

Risk Appetite Framework

CMHC has a Risk Appetite framework which is a key component of the organization’s risk management and governance structure. The objective of the Risk Appetite Framework is to establish, define and reinforce a prudent and common understanding of acceptable and unacceptable material risk leading to a robust risk culture throughout CMHC. The Framework is used to establish and understand the amounts and types of risks which the organization is able and willing to accept and those risks which should be avoided.

A Risk Capacity statement, Risk Appetite Principles, entity level and activity level Risk Appetite Statements and Risk Tolerance statements form the foundation of CMHC’s Risk Appetite Framework. These statements and principles are annually approved by senior management and the Board and regular semi-annual reporting against these statements ensures regular consideration and oversight of key risks for CMHC.

20 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

ERM Risk Categories

Our seven key risks are identified in the diagram below. This categorization is used throughout our business activities to identify, assess, manage and report on risks.

Reporting on Risk

Our Risk Register provides an assessment of key risks on a corporate-wide basis. This assessment is done on a five-year horizon and includes short-term, medium-term and long-term risks to the Corporation. The table below outlines our key risks with risk rating as at 31 December 2015.

| | | | |

Risk Category | | Definition | | Risk Rating |

Strategic Risk | | Strategic Risk is the potential for loss or other undesirable outcomes resulting from insufficient or inappropriate responses to changes in the business environment, inappropriate strategies and/or poor execution of strategic decisions. | | * |

Reputation Risk | | Reputation Risk is the potential for loss or other undesirable outcomes resulting from negative perceptions and/or publicity. | | † |

Operational Risk | | Operational Risk is the potential for loss or other undesirable outcomes resulting from people actions, inadequate or failed internal processes and systems, or from external events. | | * |

Insurance and Guarantee Risk | | Insurance and Guarantee Risk is the potential for loss arising from actual experience varying from what was expected or predicted. | | † |

Credit Risk | | Credit Risk is the potential for loss if a counterparty fails to honour a transaction/financial obligation. | | † |

Market Risk | | Market Risk is the potential for loss arising from adverse changes in market prices and market rates. | | † |

Liquidity Risk | | Liquidity Risk is the potential for loss if we have insufficient funds to meet all financial obligations as they come due. | | † |

| * | Figure is shaded yellow to indicate Medium Cautionary - requiring ongoing management attention; action may be required. |

| † | Figure is shaded green to indicate Low Acceptable - risk is low or appropriately managed, no action required. |

Our Strategic Risk was assessed as medium cautionary to reflect the following aspects:

| ¡ | | The economic uncertainty and the impact on our financial position – The global and Canadian economic environments continue to be uncertain and potentially volatile. We will continue to enhance our scenario planning and analysis capacity to better prepare our business for potential economic shocks. |

| ¡ | | The Mortgage Loan Insurance Market Share – Revisions to our vision and our strategic directions, combined with changes in the business environment, have resulted in a decline in Mortgage Loan Insurance market share. If market share declines rapidly and materially there may be negative financial and operational impacts including lower volumes and premiums (which may require significant restructuring) as well as negative impacts on appropriations based activities (which share overhead costs with Mortgage Loan Insurance). Declining market share could also lead to adverse selection and claims performance, and an inability to provide service adequately in all markets. |

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 21

Operational Risk was also assessed as medium cautionary given the following:

| ¡ | | Outdated Technology/Cybersecurity – The current aging technology platforms and need for significant modernization and transformation of existing systems represents significant risk and may contribute to inefficient business processes. In addition, technology and information security risks remain significant due to the constantly growing sophistication and volume of cyber attacks. Significant resources continue to be devoted to monitoring the security of our systems and additional investments in these capabilities will continue over the coming years. |

| ¡ | | Execution of the CMHC in motion change initiative – The significant execution risk involved in this broad change management exercise has contributed to our cautionary ratings for people and process risks. |

In order to manage our risks at a more granular level, our risk appetite statement is supplemented by business activity risk appetite statements which are described in the respective activity section. Our operational risks are pervasive across all business activities.

Stress Testing

Stress testing is a best practice risk management tool. It provides a formalized mechanism for companies to look at risks in a systematic and structured way and to assess the impact of extreme events.

The credit crisis underlined the need for institutions, like CMHC, to conduct stress tests to ensure they are able to handle emergencies and remain solvent through severe economic challenges. Since 2008, regulators have set strict requirements regarding the type and severity of risk scenarios that institutions must use annually.

We follow the guidance set by OSFI with respect to stress testing and, as such, use certain severe and extreme scenarios in our stress testing. We develop our own stress testing cases for business planning purposes.

Corporate-wide stress testing scenarios are developed early in the year, are vetted internally, and are approved by CMHC’s Board of Directors.

In 2015, CMHC tested its Mortgage Loan Insurance and Securitization businesses against several extreme scenarios, including the following stress events:

| 1. | Global economic deflation – severe house price declines and high unemployment over five years. |

| 2. | Vancouver earthquake – economic impact following a magnitude 9 earthquake event. |

| 3. | US-style housing crisis – 30% decline in house prices and 5 percentage points increase in unemployment. |

| 4. | Oil price shock – extreme fall in oil prices, sustained low prices over the next five years accompanied by a global recession. |

The underlying variables within each of the scenarios were developed based on a combination of hypothetical modeling and historical economic analysis. The final version of each scenario was independently reviewed by an internal model validation team and economists within CMHC’s Market Analysis Centre.

22 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Results

It is important to remember that stress testing is not predicting or forecasting – it involves searching out extreme “what-if” scenarios that have a very remote chance of happening, and planning for them.

| | | | | | | | | | |

| For the 2015-2020 period | | Base Case | | Global

Deflation | | Earthquake | | US-style

Housing Crisis | | Oil Price Shock |

Peak unemployment rate | | 6.6% | | 15.9% | | 6.8% | | 11.6% | | 12.6% |

Change in housing prices (Peak-to-Trough) | | 9.1% | | (43.7%) | | 9.9% | | (30%) | | (25.7%) |

Cumulative Net Income (Loss) | | $7.6B | | ($8.9B) | | $5.2B | | ($3.5B) | | $0.4B |

Lowest Mortgage Loan Insurance Capital (% MCT) | | 365% in 2015 | | 147% in 2020 | | 374% in 2015 | | 289% in 2018 | | 370% in 2015 |

Each hypothetical case stresses CMHC’s business differently and results indicate the global deflation scenario would have the most detrimental effect on CMHC’s financial position. High unemployment and large declines in house prices would potentially lead to a significant number of borrowers being unable to pay their mortgages, resulting in over $20 billion in mortgage loan insurance losses over the planning period, which is ten times greater than normal.

Impact on Capital

None of these scenarios would deplete CMHC’s capital below the minimum capital target of 100% MCT – on par with OSFI-mandated minimum levels for private competitors.

It would take a very severe housing downturn and a sustained high unemployment rate to start eroding CMHC’s capital in a significant manner or impact CMHC’s capacity to underwrite new mortgage loan insurance business.

Operational Risk

Stress testing also provides an opportunity to assess a firm’s operational resiliency to respond to a crisis; for example, how well will processes, systems and people handle unexpected events or emergencies.

CMHC conducted a tabletop exercise in 2015 to assess its readiness to respond to a cyberattack on a key business system. The scenario involved both the main operational site and backup site being down for a significant period of time. A number of lessons were learned from this exercise, including the need to better coordinate business resumption communications internally and externally.

2016 Stress Testing

The Office of the CRO works with different business areas across the Corporation, including an internal model validation team, to develop new or revised scenarios for CMHC’s annual stress testing exercise. The scenario themes being developed for 2016 are expected to be similar to the 2015 scenarios, with only minor changes to the economic assumptions and variables used in the models reflecting the current global economic environment.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 23

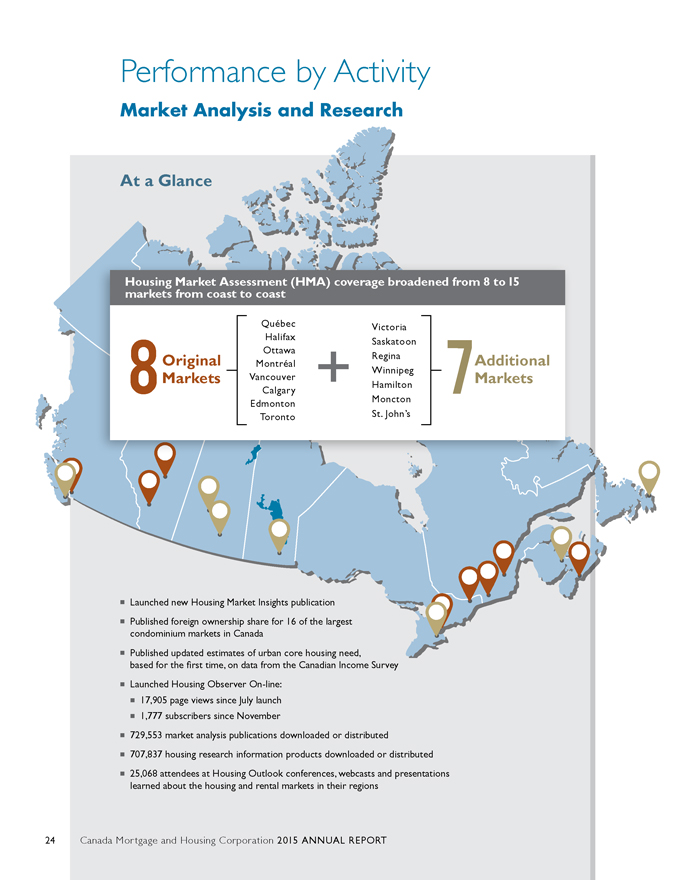

Performance by Activity

Market Analysis and Research

At a Glance

Housing Market Assessment (HMA) coverage broadened from 8 to 15 markets from coast to coast

8 Original Markets

Québec

Halifax

Ottawa

Montréal

Vancouver

Calgary

Edmonton

Toronto

+

Victoria

Saskatoon

Regina

Winnipeg

Hamilton

Moncton

St. John’s

7 Additional Markets

Launched new Housing Market Insights publication

Published foreign ownership share for 16 of the largest condominium markets in Canada

Published updated estimates of urban core housing need, based for the first time, on data from the Canadian Income Survey

Launched Housing Observer On-line:

17,905 page views since July launch

1,777 subscribers since November

729,553 market analysis publications downloaded or distributed

707,837 housing research information products downloaded or distributed

25,068 attendees at Housing Outlook conferences, webcasts and presentations learned about the housing and rental markets in their regions

24 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Description of Activity

Ultimately, our Market Analysis and Research Activities aim to facilitate access to housing and contribute to financial stability. We support informed decision making through the creation, interpretation and sharing of housing-related data and information. We conduct timely and relevant surveys at the local, provincial and national levels, analyse data, prepare scenario analyses, and undertake research on a range of issues that support a well-functioning housing system and promote housing affordability and choice.

We develop timely information and analysis that supports our business activities, informs corporate directions, fills critical housing-related information gaps that would not otherwise be filled, and, ultimately, supports informed decision making by housing policy makers and governments. We work with external partners, such as provinces and territories and housing stakeholders, to share information and consider issues from a range of perspectives. These efforts improve the understanding of current and future housing challenges in Canada and facilitate the development of housing-related policy.

Risk Arising from Market Analysis and Research Activity

In addition to Operational Risk, as described in the Risk Management section, the key risk associated with this activity is described below:

Reputation Risk

In order to meet client needs, the information and advice that we provide must be timely, relevant and accurate. A wide range of communications approaches and platforms are used to share information resulting from our market analysis and research. Communications and marketing, including stakeholder and media relations activities, promote CMHC’s knowledge creation and sharing role. Internal and external clients are consulted to ensure our priorities reflect information gaps and policy/research needs. In addition, surveys are conducted to measure the usefulness of our information products.

Financial Performance

| | | | | | | | |

| (in millions) | | 2015 | | | 2014 | |

Assisted Housing Recovery | | | 44 | | | | 50 | |

Mortgage Loan Insurance Recovery | | | 15 | | | | 17 | |

Total Revenues | | | 59 | | | | 67 | |

Market Analysis | | | 39 | | | | 45 | |

Research | | | 20 | | | | 22 | |

Total Expenses | | | 59 | | | | 67 | |

Net Income | | | - | | | | - | |

Market Analysis and Research Activities are cost-recovered from revenues from Assisted Housing’s Parliamentary Appropriations for Housing Programs and Lending Programs as well as under the Mortgage Loan Insurance Activity.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 25

Performance Analysis

The following key performance indicators represent how we have assessed the effectiveness of our Market Analysis and Research Activity in 2015.

| | | | | | | | |

| | | 2015 | |

| Performance Indicators (%) | | Plan | | | Actual | |

Full expenditure of grants and contribution budget for research and information transfer for 2015-16 (Target at 31 December 2015 – 60%1) | | | 100 | | | | 65 | † |

Usefulness of market analysis and research information | | | 85 | | | | 95 | † |

Forecast accuracy of housing starts | |

| Within 10%

of actual |

| | | 3.1†, | 2 |

| † | Figure is shaded green to indicate target met or within 5% of plan. |

| 1 | Plan figure is based on Government fiscal year – 100% by 31 March 2016. |

| 2 | CMHC Forecast was 189,500 starts and Actual was 195,535 starts resulting in a difference of 3.1%. |

Our refocused research activities in 2015 advanced our understanding of the housing needs of Canadians. This was accomplished through:

| ¡ | | Continued collaboration with territorial housing agencies and other stakeholders in research on energy-efficient and culturally-appropriate new housing and retrofits in the North; |

| ¡ | | Webinars posted online showing housing options for people living with dementia and strategies related to affordable sustainable housing; and |

| ¡ | | Research Highlights on topics such as: the design, construction and performance of the Northern Sustainable Houses; housing conditions and characteristics of Inuit households; understanding seniors’ housing intentions; the cost of including accessibility features in new housing; and the adequacy, suitability and affordability of Canadian housing. |

Outlook

In order to improve housing outcomes through timely, relevant data analysis and knowledge, the following medium-term initiatives, which support our strategic direction to Lead Through Information and Insight, will be pursued in 2016. We will:

| ¡ | | Increase public availability of quality housing information that can help facilitate access to affordable housing and contribute to stability of the financial system and housing markets including addressing data and information gaps; |

| ¡ | | Engage stakeholders and decision makers to obtain their insights on priority housing issues, including using the National Housing Research Committee as a hub and catalyst for housing research; and |

| ¡ | | Continue to provide high-quality policy advice to Government. |

26 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

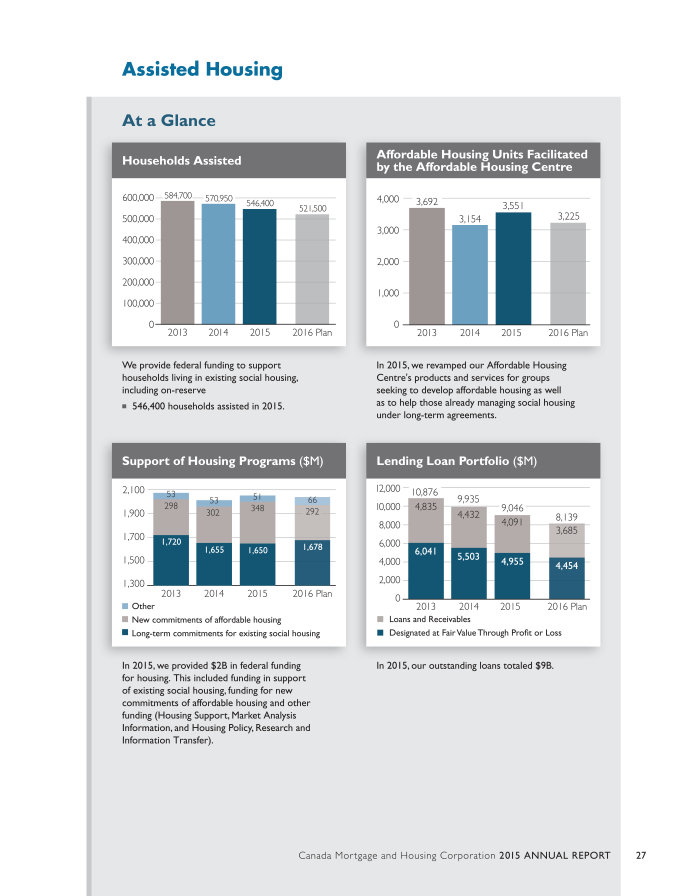

Assisted Housing

At a Glance

Households Assisted

600,000

584,700

570,950

546,400

521,500

500,000

400,000

300,000

200,000

100,000

0

2013

2014

2015

2016

Plan

We provide federal funding to support households living in existing social housing, including on-reserve

546,400 households assisted in 2015.

Support of Housing Programs ($M)

2,100

53

53

51

66

298

348

1,900

302

292

1,700

1,720

1,655

1,650

1,678

1,500

1,300

2013

2014

2015

2016

Plan

Other

New commitments of affordable housing

Long-term commitments for existing social housing

In 2015, we provided $2B in federal funding for housing. This included funding in support of existing social housing, funding for new commitments of affordable housing and other funding (Housing Support, Market Analysis Information, and Housing Policy, Research and Information Transfer).

Affordable Housing Units Facilitated by the Affordable Housing Centre

4,000

3,692

3,551

3,154

3,225

3,000

2,000

1,000

0

2013

2014

2015

2016

Plan

In 2015, we revamped our Affordable Housing Centre’s products and services for groups seeking to develop affordable housing as well as to help those already managing social housing under long-term agreements.

Lending Loan Portfolio ($M)

12,000

10,876

9,935

10,000

4,835

9,046

4,432

8,139

8,000

4,091

3,685

6,000

6,041

5,503

4,000

4,955

4,454

2,000

0

2013

2014

2015

2016

Plan

Loans and Receivables

Designated at Fair Value Through Profit or Loss

In 2015, our outstanding loans totaled $9B.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 27

Description of Activity

We provide federal funding in support of housing programs for Canadians in need, including on-reserve. Our activities also include lending programs for social housing. The ultimate outcome of our activities is to help Canadians in need have access to affordable and suitable housing.

Lending Programs

We make loans to social housing sponsors, First Nations, provinces, territories and municipalities, as well as non-subsidized housing support. We can offer loans at below market interest rates due to our ability to obtain funding through the Crown Borrowing Program. We operate our Lending Programs on a long-term, breakeven basis in order to help reduce project operating costs, thereby lowering direct subsidies for social housing.

Housing Programs

We receive Parliamentary Appropriations to fund our Housing Programs. Housing Programs operate on a breakeven basis as appropriations equal expenditures each year. The majority of the funding in Housing Programs helps support low-income households living in existing social housing on and off-reserve.

Through the IAH, the federal government is working with provinces and territories to help reduce the number of Canadians in housing need by investing more than $1.9 billion over 8 years to March 2019. In recognition of the distinctive needs of Nunavut, $100 million was provided over two years (April 2013 to March 2015) to support new affordable housing. Since April 2011, 267,139 households have benefitted from this combined funding.

We also manage assets transferred from the Federal Co-operative Housing Stabilization Fund (Fund) since the termination of its Indenture of Trust in April 2010. The Fund was set up under the federal Co-operative Housing Program and provides assistance to co-operative housing projects (co-ops) in financial difficulty committed under this program. The assets transferred from the Fund are available to assist co-ops with an Indexed Linked Mortgage (ILM) in financial difficulty. Transferred mortgage receivables under administration during the year decreased from $45.0 million to $43.1 million at year-end. Other assets transferred from the Fund to us that are available to assist ILM co-ops in financial difficulty were $18.1 million at year-end, which included $3.1 million in restricted funds for loan commitments approved but not yet advanced.

Risk Arising from Assisted Housing Activity

In addition to Operational Risk, as described in the Risk Management section, the key risks associated with our Assisted Housing Activity are described below.

Reputation Risk

Changing economic conditions have resulted in increased scrutiny on the role that CMHC and the Government play in social housing and the housing market and the effectiveness of current policies. We undertake a number of proactive strategies and approaches to engage or inform our stakeholders including advising the Government on options for social housing.

28 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Credit Risk

We hold and make loans under the NHA to social housing sponsors, First Nations, provinces, territories and municipalities for federally-subsidized housing. The estimated fair value of loans arising from the Lending Programs is $10 billion on an outstanding balance of $9 billion as at 31 December 2015.

Credit risk in the Lending Programs’ portfolio arises from the risk of loss due to the failure of counterparties to meet their contractual obligations. Losses due to default are largely recoverable from various levels of government.

Our Lending Program is assured full collection of principal and accrued interest on the majority of the loans. As at 31 December 2015, we are assured full collection of principal and accrued interest on 77% of our loans (2014 – 77%). The remaining 23% of loans (largely under the Municipal Infrastructure Lending Program) are assessed on a regular basis to determine if provisions for loss are necessary. As at year-end 2015, there was one impaired loan identified and a $23 million provision for loss was recorded (2014 - $22 million).

Market Risk

Prepayment activity, including the restructuring of closed loans, has the potential to cause us to incur losses. We mitigate our exposure to prepayment risk by applying the terms and conditions of our loans, including prepayment clauses.

We are also exposed to interest rate risk when asset and liability principal and interest cash flows have different interest payments or maturity dates. The severity of the risk is dependent on the size and direction of interest rate changes and the size of the mismatched positions. Our risk management policies specify that the maximum exposure of the financing margin to interest rate movements with a confidence level of 95% be fixed at $1.5 million over a 12-month horizon.

Direct Lending interest rates are set based on operating costs, slippage, funding costs and related hedging costs. A review of Direct Lending costs is conducted periodically to determine if the rate charged to Direct Lending borrowers is sufficient to recover our administrative costs in respect of this program.

Financial Performance

| | | | | | | | |

| (in millions) | | 2015 | | | 2014 | |

Parliamentary Appropriations for Housing Programs | | | 2,049 | | | | 2,010 | |

Net Interest Income | | | 9 | | | | 19 | |

Other Income1 | | | 36 | | | | 66 | |

Total Revenues | | | 2,094 | | | | 2,095 | |

Housing Programs Expenses | | | 2,049 | | | | 2,010 | |

Operating Expenses | | | 18 | | | | 21 | |

Total Expenses | | | 2,067 | | | | 2,031 | |

Income before Income Taxes | | | 27 | | | | 64 | |

Income Taxes | | | 2 | | | | 12 | |

Net Income | | | 25 | | | | 52 | |

| 1 | Other Income includes Net Realized Gains (Losses), Net Unrealized Gains and Other Income. |

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 29

Appropriations spending related to Housing Programs Expenses for the year ended 31 December 2015 was $2,049 million, an increase of $39 million (1.9%) when compared to 2014. The increase is primarily due to the timing of expenditures under the Investment in Affordable Housing, partially offset by the timing of expenditures for affordable housing in Nunavut.

Net Interest Income decreased by $10 million (52.6%) from the prior year primarily due to the reduced balance of loans.

Other Income decreased by $30 million (45.5%) from the prior year mainly due to the reversal of a deferred net gain on direct lending borrowings and loans recorded in the 2014 period, partially offset by higher unrealized gains on financial instruments caused by a smaller decline in medium term interest rates in 2015.

Total Expenses increased by $36 million (1.8%) primarily as a result of higher Housing Programs expenses of $39 million (1.9%) as explained in the Total Revenues section.

Net Income decreased by $27 million (51.9%) from the prior year due primarily to the decrease in Other Income and Net Interest Income and its corresponding tax impact as explained in the Total Revenues section.

Capital Management

We manage our capital to address risk exposures in our Lending portfolio due to declining business which affects our ability to maintain breakeven programs. We do not hold capital for Housing Programs as this activity does not present risks to the Corporation that would require capital to be set aside.

Refer to the Consolidated Financial Statements Note 18 - Capital Management for complete disclosure on Capital Management.

Reporting on Use of Appropriations

The following table reconciles the amount of appropriations authorized by Parliament as available to CMHC during the Government fiscal year (31 March) with the total amount recognized by us in our financial statements.

| | | | | | | | |

| For the year ended 31 December (in millions) | | 2015 | | | 2014 | |

AMOUNTS AUTHORIZED IN 2014/15 (2013/14) | | | | | | | | |

Main Estimates | | | 2,097 | | | | 2,131 | |

Less: Portion recognized in calendar 2014 (2013) | | | (1,423 | ) | | | (1,498 | ) |

Less: Appropriations lapsed for 2014/15 (2013/14) | | | (44 | ) | | | (46 | ) |

2014/15 (2013/14) portions recognized in 2015 (2014) | | | 630 | | | | 587 | |

AMOUNTS AUTHORIZED IN 2015/16 (2014/15) | | | | | | | | |

Main Estimates | | | 2,026 | | | | 2,097 | |

Less: Portion to be recognized in calendar 2016 (2015) | | | (576 | ) | | | (630 | ) |

Forecasted lapse for 2015/16 (Actual lapse in 2014/15) | | | (31 | ) | | | (44 | ) |

2015/16 (2014/15) portions recognized in 2015 (2014) | | | 1,419 | | | | 1,423 | |

Total appropriations recognized – twelve months ended 31 December | | | 2,049 | | | | 2,010 | |

30 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Performance Analysis

The following key performance indicators represent how we have assessed the effectiveness of our Assisted Housing Activity in 2015.

| | | | | | | | |

| | | 2015 | |

| Performance Indicators | | Plan | | | Actual | |

Affordable housing facilitated by CMHC’s Affordable Housing Centre (homes) | | | 3,100 | | | | 3,551 | † |

Direct Lending - subsequent renewals ($M) | | | 929 | | | | 925 | † |

Housing Programs Expenses excluding Operating Expenses for 2015-16 ($M) (Target at 31 December 2015 – 1,325)1 | | | 1,864 | | | | 1,320 | † |

New homes committed under the On-Reserve Non-Profit Housing Program (homes) (Target at 31 December 2015 – 292)1 | | | 529 | | | | 298 | † |

Initiative(s) created and implemented to maximize housing delivery on and off-reserve | | | 2 | | | | 2 | † |

Reduction in the higher risk projects in CMHC managed portfolio (%) | | | 2 | | | | 5.9 | † |

Working with INAC, measures are developed and implemented to improve the capacity of First Nations | |

| Capacity development

plans are in place;

Undertake 1 joint

initiative with INAC |

| | | Achieved | † |

Increase in Take-up of products and services (%) | | | 15 | | | | 17 | † |

| † | Figure is shaded green to indicate target met or within 5% of plan. |

| 1 | The Plan performance indicators are based on the Government fiscal year basis (1 April – 31 March). Actual results from 1 April 2015 to 31 December 2015 are shown. |

Overall, we met or exceeded our performance measures for 2015. Our core activities include both calendar year and fiscal year targets. In 2015, our Affordable Housing Centre facilitated the creation of 3,551 affordable homes. The Centre provides information and advice as well as funding for up-front costs to help get projects off the ground. Approximately 72,900 homes have been facilitated since the Centre’s inception.

Our Housing Programs expenditures are measured on a fiscal year basis and are on track to meet the 2015-16 plan. Through our On-Reserve Non-Profit Housing Program, we provide assistance for the construction, purchase and rehabilitation of rental housing on-reserve. We committed funding for 298 new homes made available for rent under our Social Housing Activity so far for the 2015-16 fiscal year (on track for plan of 529) and continued to subsidize 26,900 existing homes provided under our Social Housing Activity on-reserve in 2015.

In 2015, we created and implemented two initiatives to maximize housing delivery on and off-reserve. We made changes to align our expertise and tools in a more client-focused approach in support of social and affordable housing. We updated our Affordable Housing Centre’s products and services for groups seeking to develop affordable housing as well as to help those already managing social housing under long-term agreements. This included updating our Seed Funding Program to better meet the needs of affordable housing proponents, particularly in large markets. In addition, as a result of a review and update to our planning approach in 2015 to ensure that full take-up of allocated funding is achieved, new homes committed under the On-Reserve Non-Profit Housing Program are expected to increase over the coming years.

Additionally, we focused on aligning risk with our mandate by taking action to improve the risk rating for the higher risk projects in our managed portfolio; we exceeded our 2% reduction target and achieved a 5.9% reduction.

We also focused on leading through information and insight in 2015, achieving a 17% increase in the take-up of products and services over the 2014 actual, exceeding our target of a 15% increase.

Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT 31

Outlook

As part of Budget 2016, Growing the Middle Class, the Government announced several initiatives that the Corporation will be delivering:

| ¡ | | Affordable Housing – A total of $1.4B over two years starting in 2016 broken down as follows: |

| | ¡ | | $504.4 million related to measures to support the construction of new affordable housing units, the renovation and repair of existing affordable housing, measures to support housing affordability such as rent supplements and measures to foster safe and independent living which are expected to benefit more than 100,000 Canadian households; |

| | ¡ | | $200.7 million to support the construction, repair and adaption of affordable housing for seniors which is expected to improve housing conditions for more than 5,000 low-income households; |

| | ¡ | | $89.9 million for the construction and renovation of over 3,000 shelter spaces for victims of family violence; |

| | ¡ | | $573.9 million for retrofits and renovations to existing homes provided under our Social Housing Activity to address the increasing demand for repairs, as well as improve efficiency and reduce energy use, lowering utility costs and making housing more affordable; and |

| | ¡ | | $30 million to help federally administered providers maintain rent-geared-to-income for low-income households living in social housing. |

| ¡ | | Up to $500 million per year for five years to provide low cost loans to municipalities and housing developers for the construction of new affordable housing projects. This initiative would encourage the construction of affordable rental housing by making low-cost capital available to developers during the earliest, most risky phases of development. |

| ¡ | | $208.3 million over five years to be invested in an Affordable Rental Housing Innovation Fund that would be used to test innovative business approaches – such as housing models with a mix of rental income and home ownership. |

| ¡ | | Northern & Inuit Housing - $177.7 million over two years starting in 2016 to address urgent housing needs in the North and Inuit communities. |

| ¡ | | On-Reserve - $137.7 million over two years starting in 2016 most of which would support the renovation and retrofit of existing housing and $10.4 million over three years starting in 2016 to support the renovation and construction of new shelters for victims of family violence in First Nations communities. |

| ¡ | | Up to $30 million over three years, starting in 2016-2017, to help homeowners dealing with costly structural problems in their homes as a result of the presence of the mineral pyrrhotite in their foundations. |

| ¡ | | $5 million for 2016-2017 to support internships for up to 625 Indigenous youth. The additional funding for CMHC’s Housing Internship Initiative for First Nations and Inuit Youth (HIIFNIY) comes from the $165.4 million investment to expand opportunities for young Canadians under the Youth Employment Strategy announced in Budget 2016. |

32 Canada Mortgage and Housing Corporation 2015 ANNUAL REPORT

Mortgage Loan Insurance

At a Glance

Insurance-in-force ($B)

600

500

400

300

200

100

0

557

50

219

288

2013

543

53

206

284

2014

526

58

193

275

2015

516

59

193

264

2016 Plan

Multi-unit Residential Limit

Portfolio

Transactional Homeowner (high and low ratio)

2015 Insurance-in-force total of $526 billion (below the legislative limit of $600 billion)

Insured Volumes ($B)

70

60

50

40

30

20

10

0

61.1

6.4

10.4

44.2

2013

55.6

5.9

8.0

41.7

2014

55.3

7.4

8.7

39.2

2015

Multi-unit Residential

Portfolio

Transactional Homeowner (high and low ratio)

Our presence is a source of confidence in Canadian housing finance markets $55.3 billion (304,518 insured homes) total insured mortgages for 2015

Average Credit Score at Origination

900

600

300

0

745 747 756 754

Transactional Homeowner (high and low ratio)

Portfolio

2014 2015

New Mortgage Loan Insurance business in 2015:

Average insured loan amount at origination of $181,684

Average credit score at origination of 747 for Transactional Homeowner and 754 for Portfolio

The Insurance-in-force portfolio quality remained high with credit scores of 733 for Transactional Homeowner and 761 for Portfolio.

Average Outstanding Loan Amount ($)

200,000

150,000

100,000

50,000

0

173,415 184,281191,246

152,749 155,250 139,221

52,676 56,966

Overall

Transactional Homeowner

Portfolio

Multi-unit Residential (per unit)

2014 2015