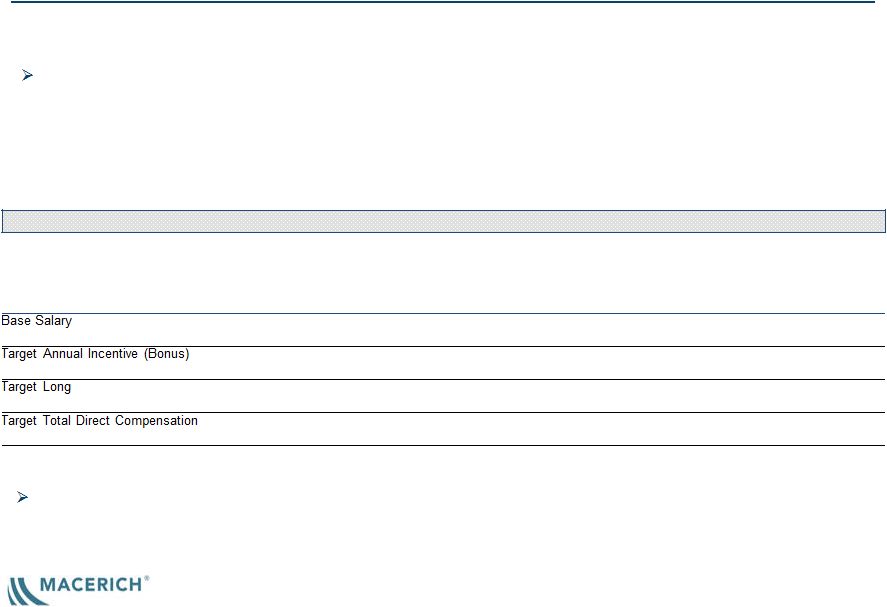

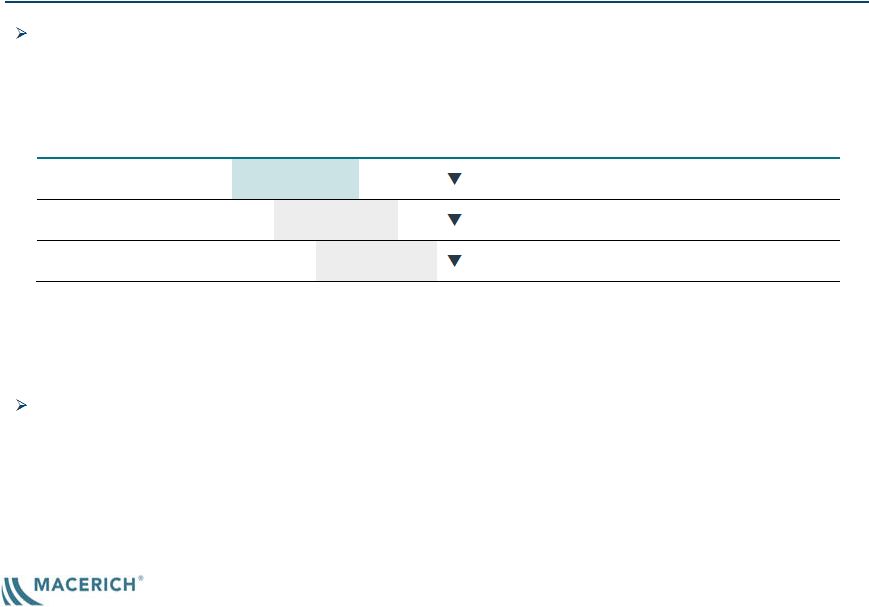

2 Annual Meeting of Stockholders to be Held on June 7, 2019 We ask for your support by voting in accordance with the recommendations of our Board of Directors on all of the proposals included in our 2019 Proxy Statement, which was filed on April 26, 2019. In particular, we are requesting your vote FOR Proposal 3, the approval of the annual advisory vote on the compensation paid to our named executive officers (“NEOs”). We take a very disciplined, “pay-for-performance” approach to executive compensation. We believe that our executive compensation program strongly aligns the compensation of our NEOs with our performance, as detailed in the section of our 2019 Proxy Statement entitled “Compensation Discussion and Analysis.” Glass Lewis has recommended a FOR vote for Proposal 3. However, ISS recommended an AGAINST vote on Proposal 3. Notwithstanding the ISS recommendation, the Company believes that the executive compensation program supports our financial and strategic objectives and is appropriately aligned with the interests of our stockholders. ISS’ negative recommendation was unexpected because, among other reasons, in connection with CEO succession in 2018 the target total direct compensation of our CEO, CFO and next three highest paid executive officers for 2019 decreased 47% from that of the same group in 2018. We strongly disagree with ISS’ recommendation on Proposal 3, as well as the stated reasons behind it. This presentation is intended to facilitate discussions with stockholders as part of our engagement with them in advance of our Annual Meeting and sets forth the reasons for Macerich’s substantive disagreement with ISS. We were pleased to receive the support of approximately 89% of the votes cast on our say-on-pay proposal the prior two years, and over 97% in 2016. We look forward to receiving strong support again this year. |