Exhibit 99.1

REIT WORLD NAREIT’S ANNUAL CONVENTION FOR ALL THINGS REIT NOVEMBER 15 - 17, 2016 PAGE TITLE HERE 1

SUNBELT FOCUSED APARTMENT REIT 2 HIGH QUALITY EARNINGS STREAM; FULL - CYCLE PERFORMANCE PROFILE ▪ High recurring and diversified earnings stream drives steadily growing dividend and value growth ▪ Balanced and sector - differentiated investment strategy lowers earnings volatility and cyclicality ▪ Straightforward investment model, balance sheet and value proposition FOCUS ON HIGH GROWTH REGION AND MARKETS ▪ Strong regional demand for apartment housing; strong/steady job growth ▪ Portfolio offers a product and price point that appeals to a broad segment of the rental market ▪ Unique portfolio segmentation and balanced submarket allocation across the region HIGH QUALITY PORTFOLIO; DISCIPLINED CAPITAL DEPLOYMENT ▪ $3.1 billion of transactions (excluding CLP and PPS mergers) since 2011 ▪ Both CLP and PPS mergers further improve asset quality and enhance AFFO growth profile ▪ Average age of portfolio of 14 years; newer than sector average ▪ Long - term record of high balance sheet productivity and superior ROIC performance COMPETITIVE ADVANTAGES DRIVE COMPOUNDING VALUE ▪ Scale and operating efficiencies drive operating margin outperformance across the region ▪ Transaction execution capabilities (speed and size) drive high volume of opportunities ▪ Platform, scale and balance sheet strength establish meaningful competitive advantages COMPELLING VALUE OPPORTUNITY ▪ Meaningful value to be captured through upcoming PPS merger ▪ Disconnect between traditional cap rate modeling and actual entity - level earnings results achieved ▪ Sector earnings multiple versus MAA’s established record of performance suggests upside ▪ Sector average implied cap rate versus MAA’s earnings record drives more compelling IRR ESTABLISHED RECORD OF STRONG VALUE CREATION AND SUPERIOR LONG - TERM SHAREHOLDER RETURN REIT WORLD NOV 2016

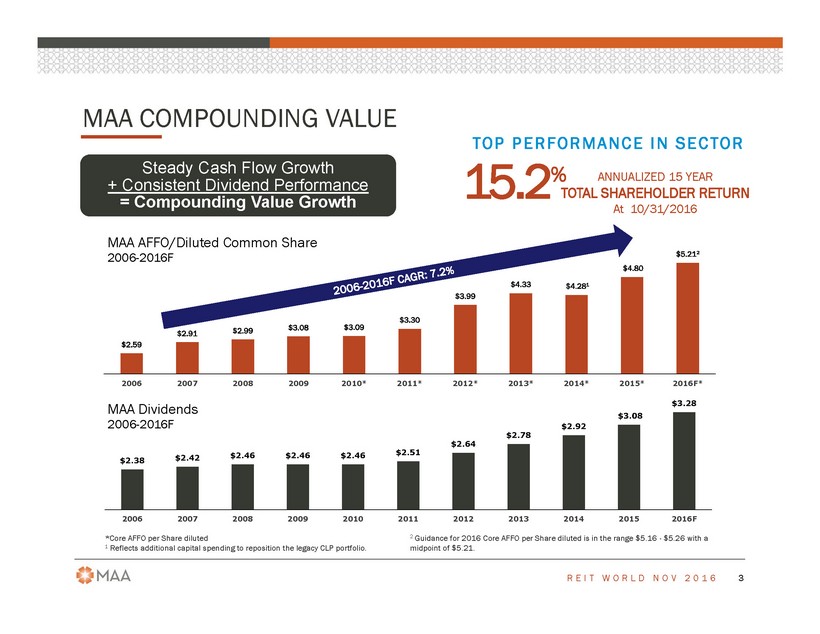

A NNUALIZED 15 YEAR TOTAL SHAREHOLDER RETURN At 10/31/2016 MAA COMPOUNDING VALUE 3 $2.38 $2.42 $2.46 $2.46 $2.46 $2.51 $2.64 $2.78 $2.92 $3.08 $3.28 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F MAA Dividends 2006 - 2016F *Core AFFO per Share diluted 1 Reflects additional capital spending to reposition the legacy CLP portfolio . 2 Guidance for 2016 Core AFFO per Share diluted is in the range $5.16 - $5.26 with a midpoint of $5.21. Steady Cash Flow Growth + Consistent Dividend Performance = Compounding Value Growth $2.59 $2.91 $2.99 $3.08 $3.09 $3.30 $3.99 $4.33 $ 4.28 1 $4.80 $ 5.21 2 2006 2007 2008 2009 2010* 2011* 2012* 2013* 2014* 2015* 2016F* MAA AFFO/Diluted Common Share 2006 - 2016F 15.2 % REIT WORLD NOV 2016 TOP PERFORMANCE IN SECTOR

4 NEW MAA BALANCED & UNIQUELY DIVERSIFIED PORTFOLIO SUPPORTS FULL CYCLE OUTPERFORMANCE TOP LARGE MARKETS % of Q3 2016 NOI 1 1. Atlanta , GA 14.5% 2. Dallas, TX 9.9% 3. Charlotte, NC 7.1% 4. Tampa, FL 6.8% 5. Austin, TX 6.7% 6. Orlando, FL 5.8% 7. Raleigh, NC 4.9% 8. Washington D.C. Metro 4.8% 9. Fort Worth, TX 3.8% 10. Nashville, TN 3.7% 1. Total 68.0% 7 5 % Large Markets Secondary Markets TOP SECONDARY MARKETS % of Q3 2016 NOI 1 1. Jacksonville, FL 3.0% 2. Charleston, SC 2.9% 3. Savannah, GA 2.2% 4. Richmond, VA 1.7% 5. San Antonio, TX 1.4% 6. Memphis, TN 1.4% 7. Greenville, SC 1.4% 8. Birmingham, AL 1.3% 9. Little Rock, AR 1.1% 10. Jackson, MS 1.1% 1. Total 17.4% 2 5 % REIT WORLD NOV 2016 1 NOI percentage based on 3Q16 pro forma percentage of New MAA same s tore NOI 2 Percentages based on 9/30/2016 pro forma of New MAA gross asset Diversified in markets 2 50% Inner Loop 45% A to A+ 42% Suburban 55% B to B+ 8% Downtown/CBD

RATIONALE AND TRANSACTION BENEFITS 5 ENHANCED COMPETITIVE ADVANTAGE ▪ Dominant Sunbelt owner/operator will drive superior deal flow and new growth opportunities ▪ Superior cost of capital benefits over full cycle to enhance accretive investment opportunities ▪ Platform scale drives operating cost advantages and NOI margin benefits ▪ Combined development platforms augment MAA’s ability to strategically recycle capital ▪ Strengthened platform through integration of best practices of both companies ENHANCED MARGINS AND SYNERGY OPPORTUNITIES ▪ Reconciliation of revenue management program and practices ▪ Higher efficiency in on - site product and service procurement ▪ Ability to further scale local and regional management operations; G&A efficiencies ▪ Cost elimination from duplicate public company costs and platform ENHANCED PORTFOLIO QUALITY & BALANCED EARNINGS PROFILE ▪ Increased presence in high growth markets with favorable demand fundamentals ▪ Improved diversification in submarkets with balanced penetration in key urban/infill locations ▪ Enhanced ability to increase proactive and opportunistic capital recycling ▪ Proven “full cycle” performance strategy strengthened by market and product diversification and enhanced development capabilities ENHANCED BALANCE SHEET ▪ Debt to gross asset ratio declines by 550 basis points ▪ Improved investment grade metrics and limited near - term debt maturities ▪ Larger scale enhances both debt and equity capital market accessibility and liquidity ▪ Positioned to achieve lower cost of capital over the long - term CONTINUES MAA’S ESTABLISHED STRATEGY WITH AN ENHANCED PLATFORM FOR EXECUTION AND VALUE CREATION REIT WORLD NOV 2016 MAA - PPS MERGER TRANSACTION

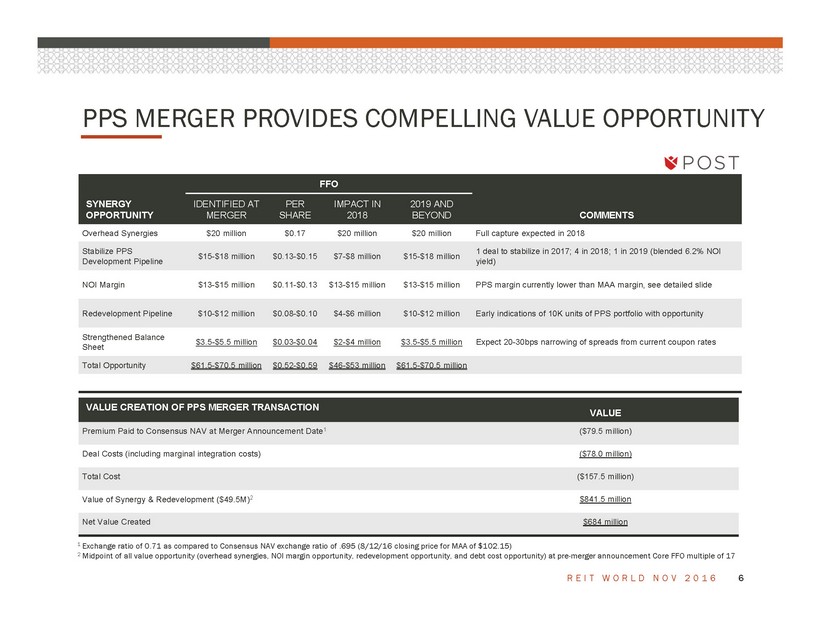

PPS MERGER PROVIDES COMPELLING VALUE OPPORTUNITY REIT WORLD NOV 2016 6 SYNERGY OPPORTUNITY FFO COMMENTS IDENTIFIED AT MERGER PER SHARE IMPACT IN 2018 2019 AND BEYOND Overhead Synergies $20 million $0.17 $20 million $20 million Full capture expected in 2018 Stabilize PPS Development Pipeline $15 - $18 million $0.13 - $0.15 $7 - $8 million $15 - $18 million 1 deal to stabilize in 2017; 4 in 2018; 1 in 2019 (blended 6.2% NOI yield) NOI Margin $13 - $15 million $0.11 - $0.13 $13 - $15 million $13 - $15 million PPS margin currently lower than MAA margin, see detailed slide Redevelopment Pipeline $10 - $12 million $0.08 - $0.10 $4 - $6 million $10 - $12 million Early indications of 10K units of PPS portfolio with opportunity Strengthened Balance Sheet $3.5 - $5.5 million $0.03 - $0.04 $2 - $4 million $3.5 - $5.5 million Expect 20 - 30bps narrowing of spreads from current coupon rates Total Opportunity $61.5 - $70.5 million $0.52 - $0.59 $46 - $53 million $61.5 - $70.5 million VALUE CREATION OF PPS MERGER TRANSACTION VALUE Premium Paid to Consensus NAV at Merger Announcement Date 1 ($79.5 million) Deal Costs (including marginal integration costs) ($78.0 million) Total Cost ($157.5 million) Value of Synergy & Redevelopment ($49.5M) 2 $841.5 million Net Value Created $684 million 1 Exchange ratio of 0.71 as compared to Consensus NAV exchange ratio of .695 (8/12/16 closing price for MAA of $102.15) 2 Midpoint of all value opportunity (overhead synergies, NOI margin opportunity, redevelopment opportunity, and debt cost oppor tun ity) at pre - merger announcement Core FFO multiple of 17

PRIOR CLP MERGER CREATES VALUE REIT WORLD NOV 2016 7 EXCEEDS EXPECTATIONS SYNERGY OPPORTUNITY CORE FFO/SHARE COMMENTS IDENTIFIED AT MERGER 2014 IMPACT MARGINAL 2015 IMPACT CUMULATIVE 2016+ IMPACT G&A Synergies $0.32 $0.32* $0.00 $0.32 Full Impact captured in 2014; maintained in 2015 NOI Operating Synergies $0.05 - $0.11 $0.08 $0.03 $0.12 Margin improvement due to pricing; personnel; R&M; insurance; 180bp combined same store margin improvement from 2013 to 2015 Stabilize Development Pipeline $0.10 - $0.14 $0.05 $0.05 $0.13 $200 million pipeline at merger date, final property stabilized in Q1 of 2016. Achieved blended yield between 7.0 - 7.5% Recycle Non - Earning Assets $0.05 - $0.08 $0.01 $0.01 $0.06 Bulk of this transaction activity to occur in 2016 - 17 Redevelopment of CLP Assets $0.10 - $0.17 $0.01 $0.03 $0.24 Initially identified 30 - 50% of the portfolio for redevelopment; actual opportunity to exceed 50% of the CLP portfolio Total Opportunity $0.62 - $0.82 $0.47 $0.12 $0.87 *Excludes integration costs VALUE CREATION OF CLP MERGER TRANSACTION VALUE IDENTIFIED AT MERGER CURRENT VALUE EXPECTATION Premium Paid 1 ($226.5 million) ($226.5 million) Deal Costs ($68.0 million) ($68.0 million) Total Cost ($294.5 million) ($294.5 million) Value of Synergy & Redevelopment ($42M identified at merger; current expectation of $54M) 2 $579.6 million $743.0 million Net Value Created $285.1 million $448.5 million 1 Implied price paid based on day of announcement at .360x exchange rate (05/31/2013: $67.97 - MAA; $24.47 - CLP) 2 Using pre - merger announcement FFO multiple of 13.8 and midpoint of synergy opportunity

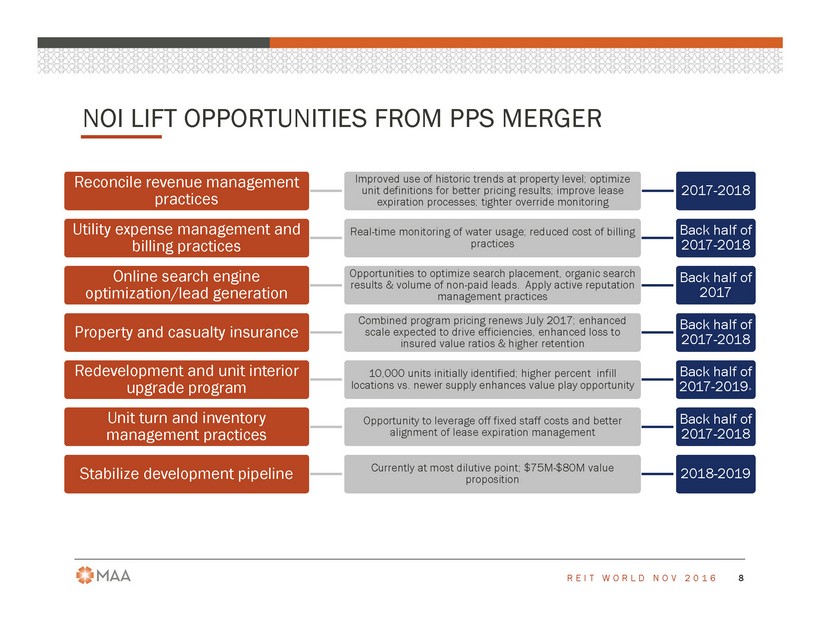

NOI LIFT OPPORTUNITIES FROM PPS MERGER REIT WORLD NOV 2016 8 Reconcile revenue management practices Improved use of historic trends at property level; optimize unit definitions for better pricing results; improve lease expiration processes; tighter override monitoring 2017 - 2018 Utility expense management and billing practices Real - time monitoring of water usage; reduced cost of billing practices Back half of 2017 - 2018 Online search engine optimization/lead generation Opportunities to optimize search placement, organic search results & volume of non - paid leads. Apply active reputation management practices Back half of 2017 Property and casualty insurance Combined program pricing renews July 2017; enhanced scale expected to drive efficiencies, enhanced loss to insured value ratios & higher retention Back half of 2017 - 2018 Redevelopment and unit interior upgrade program 10,000 units initially identified; higher percent infill locations vs. newer supply enhances value play opportunity Back half of 2017 - 2019 + Unit turn and inventory management practices Opportunity to leverage off fixed staff costs and better alignment of lease expiration management Back half of 2017 - 2018 Stabilize development pipeline Currently at most dilutive point; $75M - $80M value proposition 2018 - 2019

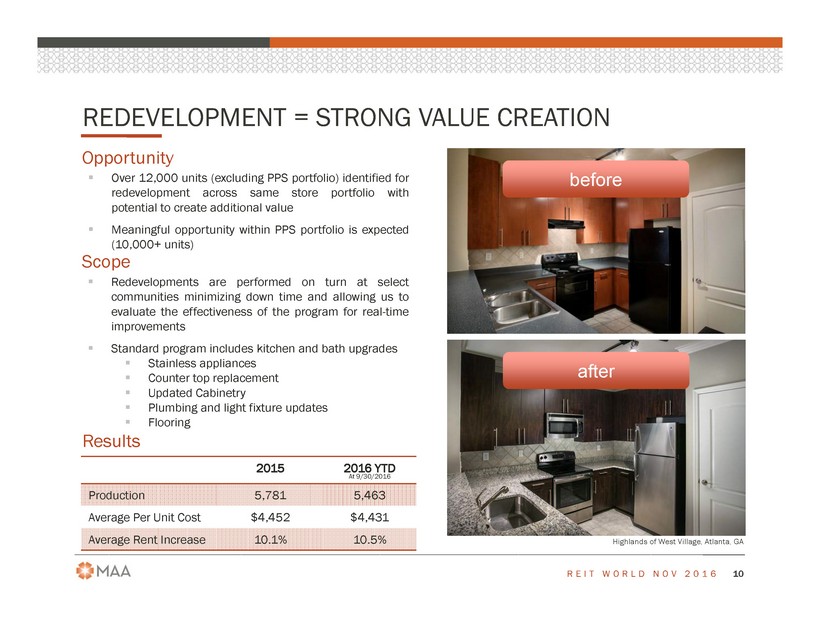

REPOSITIONED PORTFOLIO WITH ENHANCED EARNINGS PROFILE PPS MERGER SUPPORTS CONTINUED EXPANSION IN NOI MARGINS REIT WORLD NOV 2016 9 $750 $799 $863 $910 $970 $1,037 $4,684 $5,164 $5,766 $6,141 $6,782 $7,496 2011* 2012* 2013* 2014^ 2015^ 2016F^ Same Store Effective Rent/Unit After Capex NOI/Unit Same Store NOI Margin after Normal Capital Improvements Same Store Effective Rent & A fter Normal Capital Improvements, NOI/Unit * Legacy MAA portfolio ^ Combined MAA/CLP portfolio 48.0% 49.9% 51.8% 52.0% 53.0% 55.1% 2011* 2012* 2013* 2014^ 2015^ 2016F^ 710 bps Improvement ▪ PPS average monthly rent of $ 1 , 482 , 61 % NOI margin compares to MAA average monthly rent of $ 1 , 032 , 62 % NOI margin ; suggests opportunity 1 1225 South Church, Charlotte, NC 1 YTD same store average effective rent and NOI margins at 9/30/2016 ▪ Active recycling program has enhanced scale and efficiencies and strengthened the legacy MAA platform ▪ Over $ 3 . 1 billion in transactions and new development since 2011 (non - merger)

▪ Redevelopments are performed on turn at select communities minimizing down time and allowing us to evaluate the effectiveness of the program for real - time improvements ▪ Standard program includes kitchen and bath upgrades ▪ Stainless appliances ▪ Counter top replacement ▪ Updated Cabinetry ▪ Plumbing and light fixture updates ▪ Flooring 2015 2016 YTD At 9/30/2016 Production 5,781 5,463 Average Per Unit Cost $4,452 $4,431 Average Rent Increase 10.1% 10.5% REDEVELOPMENT = STRONG VALUE CREATION REIT WORLD NOV 2016 10 ▪ Over 12 , 000 units (excluding PPS portfolio) identified for redevelopment across same store portfolio with potential to create additional value ▪ Meaningful opportunity within PPS portfolio is expected ( 10 , 000 + units) Highlands of West Village, Atlanta, GA before after Scope Results Opportunity

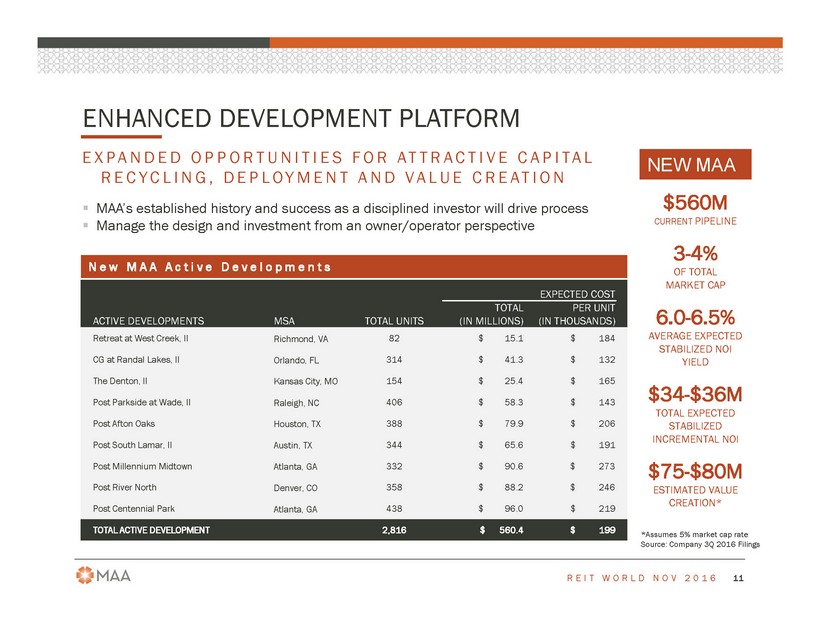

EXPANDED OPPORTUNITIES FOR ATTRACTIVE CAPITAL RECYCLING, DEPLOYMENT AND VALUE CREATION ▪ MAA’s established history and success as a disciplined investor will drive process ▪ Manage the design and investment from an owner/operator perspective ENHANCED DEVELOPMENT PLATFORM REIT WORLD NOV 2016 11 EXPECTED COST ACTIVE DEVELOPMENTS MSA TOTAL UNITS TOTAL (IN MILLIONS) PER UNIT (IN THOUSANDS) Retreat at West Creek, II Richmond, VA 82 $ 15.1 $ 184 CG at Randal Lakes, II Orlando, FL 314 $ 41.3 $ 132 The Denton, II Kansas City, MO 154 $ 25.4 $ 165 Post Parkside at Wade, II Raleigh, NC 406 $ 58.3 $ 143 Post Afton Oaks Houston, TX 388 $ 79.9 $ 206 Post South Lamar, II Austin, TX 344 $ 65.6 $ 191 Post Millennium Midtown Atlanta, GA 332 $ 90.6 $ 273 Post River North Denver, CO 358 $ 88.2 $ 246 Post Centennial Park Atlanta, GA 438 $ 96.0 $ 219 TOTAL ACTIVE DEVELOPMENT 2,816 $ 560.4 $ 199 $560M CURRENT PIPELINE 3 - 4% OF TOTAL MARKET CAP 6.0 - 6.5% AVERAGE EXPECTED STABILIZED NOI YIELD $34 - $36M TOTAL EXPECTED STABILIZED INCREMENTAL NOI $75 - $80M ESTIMATED VALUE CREATION* New MAA Active Developments NEW MAA * Assumes 5% market cap rate Source : Company 3Q 2016 Filings

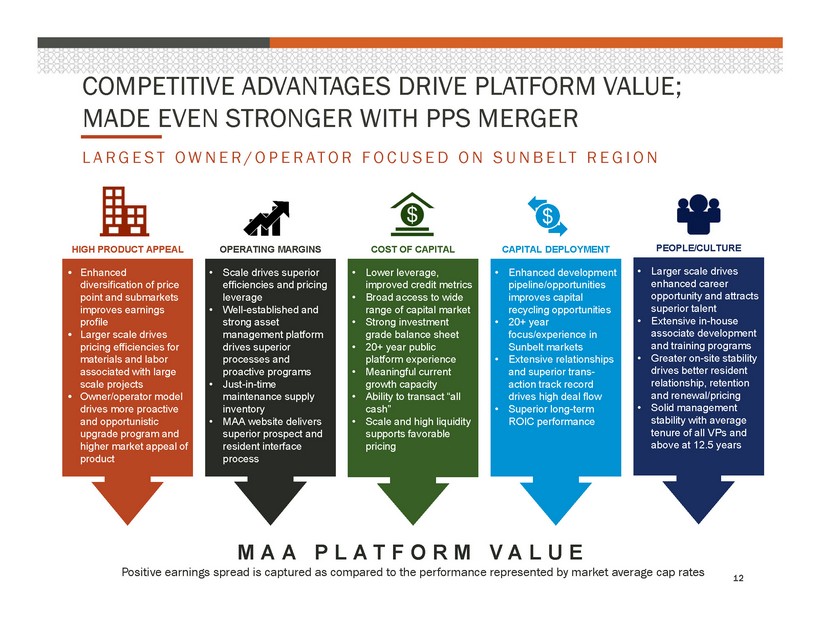

REIT WORLD NOV 2016 COMPETITIVE ADVANTAGES DRIVE PLATFORM VALUE; MADE EVEN STRONGER WITH PPS MERGER 12 LARGEST OWNER/OPERATOR FOCUSED ON SUNBELT REGION • Enhanced diversification of price point and submarkets improves earnings profile • Larger scale drives pricing efficiencies for materials and labor associated with large scale projects • Owner/operator model drives more proactive and opportunistic upgrade program and higher market appeal of product • Larger scale drives enhanced career opportunity and attracts superior talent • Extensive in - house associate development and training programs • Greater on - site stability drives better resident relationship, retention and renewal/pricing • Solid management stability with average tenure of all VPs and above at 12.5 years • Lower leverage, improved credit metrics • Broad access to wide range of capital market • Strong investment grade balance sheet • 20+ year public platform experience • Meaningful current growth capacity • Ability to transact “all cash” • Scale and high liquidity supports favorable pricing • Enhanced development pipeline/opportunities improves capital recycling opportunities • 20+ year focus/experience in Sunbelt markets • Extensive relationships and superior trans - action track record drives high deal flow • Superior long - term ROIC performance • Scale drives superior efficiencies and pricing leverage • Well - established and strong asset management platform drives superior processes and proactive programs • Just - in - time maintenance supply inventory • MAA website delivers superior prospect and resident interface process MAA PLATFORM VALUE Positive earnings spread is captured as compared to the performance represented by market average cap rates HIGH PRODUCT APPEAL PEOPLE/CULTURE COST OF CAPITAL CAPITAL DEPLOYMENT OPERATING MARGINS $

ENHANCED INVESTMENT GRADE PRO FORMA BALANCE SHEET AND MANAGEABLE DEBT MATURITY PROFILE REIT WORLD NOV 2016 13 Credit metrics at 9/30/2016 MAA New MAA Unencumbered assets to gross real estate assets 74.6% 80.6% 1 Secured debt / gross assets 1 14.4% 11.3% 2 Net d ebt / recurring EBITDA 5.6x 5.2x Net debt / gross assets 39.7% 34.2% 2 LTM Fixed charge coverage 3 4.3x 4.6x 0.0% 10.8% 6.1% 13.5% 57.0% 12.6% $80 $333 $481 $777 $618 $1,897 $339 2016 2017 2018 2019 2020 2021+ Other debt Unsecured credit facility 4 5 New MAA Debt maturity profile ($M) 1 New MAA gross real asset value based on transaction value of PPS standalone 2 New MAA gross asset value based on transaction value of PPS standalone 3 Fixed charge coverage represents Recurring EBITDA divided by interest expense, capitalized interest, preferred dividends and adj usted for mark - to - market debt adjustment % MATURING 2% 7% 11% 17% 21% 42% New MAA Weighted Average Interest Rate 3.6% Weighted Average Maturity 4.2 years 4 Other debt maturities exclude principal amortization and include pro rata share of joint venture debt and a fair market value ad justment to PPS debt of ~$23M 5 Unsecured Credit Facility includes PPS’ outstanding credit facility balance as of September 30, 2016 as well as $70M related to estimated transaction costs

SOLID PRO FORMA INVESTMENT GRADE BALANCE SHEET REIT WORLD NOV 2016 14 Pro Forma Debt Summary ($ in millions) September 30, 2016 Secured Debt Fixed or Hedged Rate 1,245 Variable Rate 190 Total Secured Debt $1,435 Unsecured Debt Unsecured Bonds $1,850 Unsecured Term Loans 850 Unsecured Credit Facilities 339 Total Unsecured Debt $3,039 Unconsolidated JV Debt 50 Total Debt $4,524 Note : Pro Forma common e quity and debt assumes $ 70 M related to estimated transaction costs, a fair market value adjustment to PPS debt of ~ $ 23 M and excludes ~ $ 43 M of pro forma preferred equity . Total Pro Forma Market Capitalization equals the total number of shares of common stock and units times the closing stock price as of 9 / 30 / 2016 plus total debt outstanding including preferred equity Secured Debt 10% Unsecured Debt 19% Common Equity 71% $11.0B Common Equity $4.5B Total Pro Forma Debt/Total Market Capitalization: 28.9%

PRO FORMA INVESTMENT GRADE BALANCE SHEET METRICS Net debt / Recurring EBITDA 1 Fixed charge coverage ratio 2 Net debt / gross assets 3 Secured debt / gross assets 3 Source: Company filings Note: All of the companies listed above may not calculate these metrics in the same manner. 1 Recurring EBITDA represents the last twelve months ended 9/30/2016 2 Fixed charge coverage represents Recurring EBITDA divided by interest expense, capitalized interest, preferred dividends and adj usted for mark - to - market debt adjustment 3 Gross assets is defined as the total assets plus accumulated depreciation REIT WORLD NOV 2016 15 4.3x 4.9x 5.2x 5.3x 5.7x 6.0x 6.9x 0.0x 1.0x 2.0x 3.0x 4.0x 5.0x 6.0x 7.0x 8.0x CPT EQR New MAA AVB ESS UDR AIV Moody’s Baa1 Baa1 A3 Baa1 Baa1 NR S&P BBB+ A - A - BBB+ BBB+ BBB - Fitch A - A - NR BBB+ NR BBB - 4.8x 4.6x 4.6x 4.4x 4.0x 2.9x 2.9x 0.0x 1.0x 2.0x 3.0x 4.0x 5.0x 6.0x AVB New MAA CPT ESS UDR EQR AIV Moody’s A3 Baa1 Baa1 Baa1 Baa1 NR S&P A - BBB+ BBB+ BBB+ A - BBB - Fitch NR A - BBB+ NR A - BBB - 29% 30% 32% 34% 41% 41% 45% 0% 10% 20% 30% 40% 50% CPT EQR AVB New MAA UDR ESS AIV GAV($B) $7.9 $26.6 $21.2 $13.1 $10.5 $14.4 $8.7 Moody’s Baa1 Baa1 A3 Baa1 Baa1 NR S&P BBB+ A - A - BBB+ BBB+ BBB - Fitch A - A - NR NR BBB+ BBB - 11% 13% 13% 16% 18% 19% 42% 0% 10% 20% 30% 40% 50% New MAA AVB CPT EQR UDR ESS AIV GAV($B) $13.1 $21.2 $7.9 $26.6 $10.5 $14.4 $8.7 Moody’s A3 Baa1 Baa1 Baa1 Baa1 NR S&P A - BBB+ A - BBB+ BBB+ BBB - Fitch NR A - A - NR BBB+ BBB -

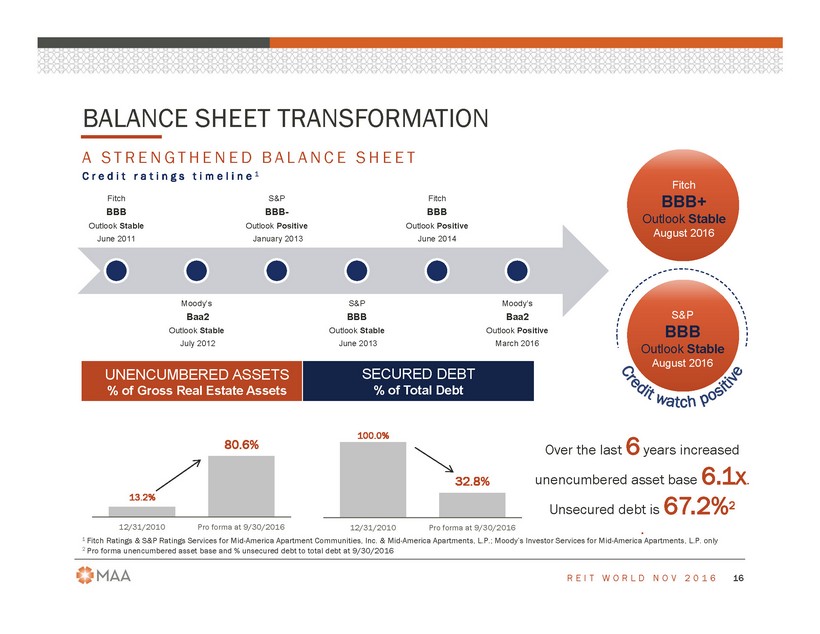

100.0% 32.8 % 12/31/2010 Pro forma at 9/30/2016 Fitch BBB Outlook Stable June 2011 Moody’s Baa2 Outlook Stable July 2012 S&P BBB - Outlook Positive January 2013 S&P BBB Outlook Stable June 2013 Fitch BBB Outlook Positive June 2014 Moody’s Baa2 Outlook Positive March 2016 BALANCE SHEET TRANSFORMATION REIT WORLD NOV 2016 16 A STRENGTHENED BALANCE SHEET UNENCUMBERED ASSETS % of Gross Real Estate Assets 13.2% 80.6 % 12/31/2010 Pro forma at 9/30/2016 SECURED DEBT % of Total Debt Over the last 6 years increased unencumbered asset base 6.1x . Unsecured debt is 67.2% 2 . Fitch BBB+ Outlook Stable August 2016 S&P BBB Outlook Stable August 2016 1 Fitch Ratings & S&P Ratings Services for Mid - America Apartment Communities, Inc. & Mid - America Apartments, L.P.; Moody’s Investor Services for Mid - America Apartments, L.P. only 2 Pro f orma unencumbered asset base and % unsecured debt to total debt at 9/30/2016 Credit ratings timeline 1

STRONG DIVIDEND GROWTH & COVERAGE REIT WORLD NOV 2016 17 $2.38 $2.42 $2.46 $2.46 $2.46 $2.51 $2.64 $2.78 $2.92 $3.08 $3.28 91.9% 83.2% 82.3% 79.9% 79.6% 76.1% 66.2% 64.2% 68.2% 64.2% 63.0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F MAA Dividends and AFFO Payout Ratio 1 2006 - 2016F Dividends Core AFFO Payout Ratio 91 Consecutive quarterly cash dividends paid MAA is one of only 3 apartment REITs not to suspend or reduce cash dividends during recession MAA’s dividend constitutes 40% of 15 - year annual compounded return 2 MAA excess cash after all cap ex and dividends 3 2016 forecast is expected to be in range of $85M to $90M 1 Payout Ratio here is defined as annual Core AFFO per Share diluted divided by annual dividends paid 2 At September 30, 2016 3 Core FFO less all capital expenditures on existing communities and less all dividends paid to shareholders

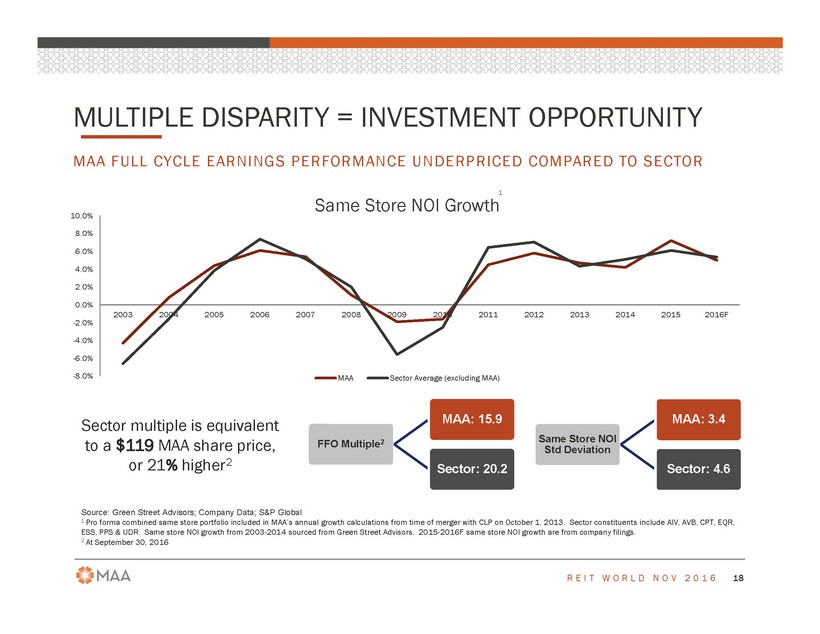

MULTIPLE DISPARITY = INVESTMENT OPPORTUNITY REIT WORLD NOV 2016 18 MAA FULL CYCLE EARNINGS PERFORMANCE UNDERPRICED COMPARED TO SECTOR FFO Multiple 2 MAA: 15.9 Sector: 20.2 Sector multiple is equivalent to a $119 MAA share price, or 21 % higher 2 Same Store NOI Std Deviation MAA: 3.4 Sector: 4.6 Source : Green Street Advisors; Company Data; S&P Global 1 Pro forma combined same store portfolio included in MAA’s annual growth calculations from time of merger with CLP on October 1, 2013. Sector constituents include AIV, AVB, CPT, EQR, ESS, PPS & UDR. Same store NOI growth from 2003 - 2014 sourced from Green Street Advisors. 2015 - 2016 F same store NOI growth are from company filings. 2 At September 30, 2016 -8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F Same Store NOI Growth MAA Sector Average (excluding MAA) 1

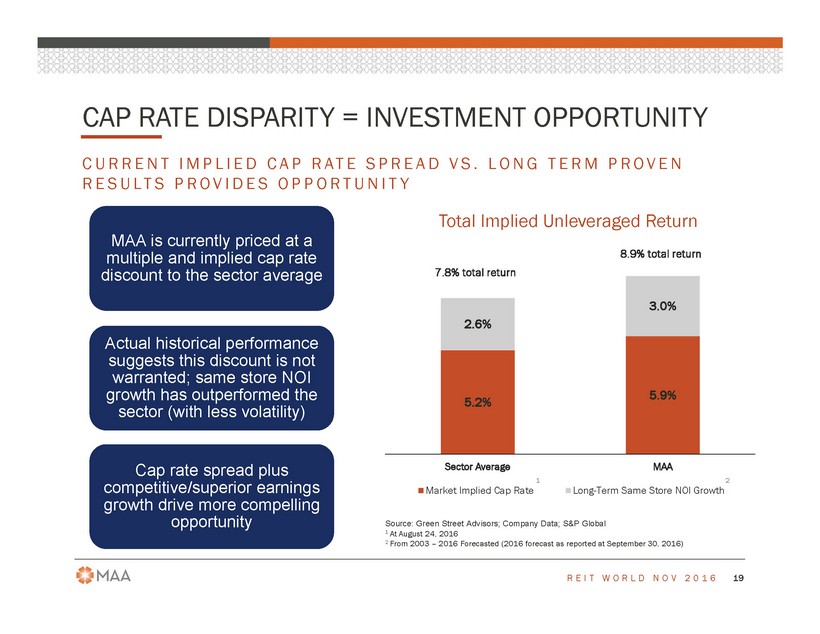

CURRENT IMPLIED CAP RATE SPREAD VS. LONG TERM PROVEN RESULTS PROVIDES OPPORTUNITY 5.2% 5.9% 2.6% 3.0% Sector Average MAA Market Implied Cap Rate Long-Term Same Store NOI Growth Total Implied Unleveraged Return CAP RATE DISPARITY = INVESTMENT OPPORTUNITY REIT WORLD NOV 2016 19 MAA is currently priced at a multiple and implied cap rate discount to the sector average Actual historical performance suggests this discount is not warranted; same store NOI growth has outperformed the sector (with less volatility) Cap rate spread plus competitive/superior earnings growth drive more compelling opportunity Source: Green Street Advisors; Company Data; S&P Global 1 At August 24, 2016 2 From 2003 – 2016 Forecasted (2016 forecast as reported at September 30, 2016) 7.8% total return 8.9% total return 1 2

STRATEGY AND LONG TERM OUTLOOK REIT WORLD NOV 2016 20 ▪ Retain focus on driving growing cash flows with lower levels of volatility through the cycle ▪ Retain focus on balanced capital allocation across the high - growth Sunbelt region ▪ Largest owner/operator focused on high - growth Sunbelt region; competitive advantages support future growth and value creation ▪ Enhanced development capability to support strategic capital recycling and value growth ▪ Proactive and opportunistic capital recycling program ▪ Increased diversification in higher asset quality and pricing spectrum enhances performance over the cycle ▪ “Full cycle” dividend growth strengthened ▪ Strengthened and diversified long - term earnings profile ▪ Greater capital markets access and cost of capital advantage ▪ Significant opportunity to realize synergies and NOI lift from PPS portfolio CR at Medical District Dallas, TX Post SoHo Square Tampa, FL Post Meridian Dallas, TX River’s Walk Charleston, SC 220 Riverside Jacksonville, FL Post South End Charlotte, NC

FORWARD LOOKING STATEMENTS REIT WORLD NOV 2016 21 This investor presentation contains forward - looking statements within the meaning of Section 27 A of the U . S . Securities Act of 1933 as amended and Section 21 E of the U . S . Securities Exchange Act of 1934 , as amended . These forward - looking statements, which are based on current expectations, estimates and projections about the industry and markets in which MAA and Post Properties, Inc . operate and beliefs of and assumptions made by MAA management involve uncertainties that could significantly affect the financial results of MAA or Post Properties, Inc . or the combined company . Words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” and variations of such words and similar expressions are intended to identify such forward - looking statements, which generally are not historical in nature . Such forward - looking statements include but are not limited to, statements about the anticipated benefits of the proposed merger between MAA and Post Properties, Inc . , including future financial and operating results, the attractiveness of the value to be received by Post shareholders, and the combined company’s plans, objectives, expectations and intentions . All statements that address operating performance, events or developments that we expect or anticipate will occur in the future – including statements relating to expected synergies, improved liquidity and balance sheet strength – are forward - looking statements . These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict . Although we believe that expectations reflected in any forward - looking statements are based on reasonable assumptions, we can give no assurance that our expectations will be attained and therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward - looking statements . Some of the factors that may affect outcomes and results include, but are not limited to : (i) national, regional and local economic climates, (ii) changes in financial markets and interest rates, or to the business or financial condition of either company or business, (iii) increased or unanticipated competition for the companies’ properties, (iv) risks associated with acquisitions, including the integration of the combined companies’ businesses, (v) the potential liability for the failure to meet regulatory requirements, including the maintenance of REIT status, (vi) availability of financing and capital, (vii) risks associated with achieving expected revenue synergies or cost savings, (vii) risks associated with the companies’ ability to consummate the merger and the timing of the closing of the merger, and (ix) those additional risks and factors discussed in reports filed with the Securities and Exchange Commission (“SEC”) by MAA and Post Properties, Inc . from time to time, including those discussed under the headings “Risk Factors” in their respective most recently filed reports on Forms 10 - K and 10 - Q . Neither MAA nor Post Properties, Inc . undertakes any duty to update any forward - looking statements appearing in this investor presentation . Eric Bolton Chairman and CEO 901 - 248 - 4127 eric.bolton@maac.com Al Campbell EVP, CFO 901 - 248 - 4169 al.campbell@maac.com Tim Argo SVP, Finance 901 - 248 - 4149 tim.argo@maac.com Jennifer Patrick Investor Relations 901 - 435 - 5371 jennifer.patrick@maac.com Contact

ADDITIONAL INFORMATION ABOUT THE PROPOSED MERGER AND WHERE TO FIND IT REIT WORLD NOV 2016 22 For information on how non - GAAP metrics, including NOI, EBITDA and AFFO, have been calculated in this presentation and for historical reconciliations to the nearest comparable financial measures under GAAP, see supplemental information provided with MAA’s earnings release and accompanying supplemental data on the SEC’s website at www . sec . gov or on MAA’s website at www . maac . com . In connection with the merger with Post Properties, Inc . , MAA has filed the Form S - 4 , the Joint Proxy Statement/Prospectus and other relevant documents with the SEC . INVESTORS ARE URGED TO READ THE FORM S - 4 , THE JOINT PROXY STATEMENT/PROSPECTUS AND OTHER RELEVANT DOCUMENTS FILED AND TO BE FILED WITH THE SEC BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION . You may obtain a free copy of the Form S - 4 , the Joint Proxy Statement/Prospectus and other relevant documents filed by MAA with the SEC at the SEC’s website at www . sec . gov . Copies of the documents filed by MAA with the SEC will be available free of charge on MAA’s website at www . maac . com or by contacting MAA Investor Relations at investor . relations@maac . com or contacting Tim Argo, Senior Vice President, Director of Investor Relations at 888 - 576 - 9689 . This document shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction . No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the U . S . Securities Act of 1933 , as amended .