United States

Securities And Exchange Commission

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-8056 |

MMA Praxis Mutual Funds

(Exact name of registrant as specified in charter)

P.O. Box 483, Goshen, IN 46527

| (Address of principal executive offices) | (Zip code) |

Anthony Zacharski, Dechert LLP, 200 Clarendon Street, 27th Floor, Boston, MA 02116

(Name and address of agent for service)

| Registrant's telephone number, including area code | (513) 878-4066 |

| Date of fiscal year end: | 12/31 | |

| Date of reporting period: | 12/31/09 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Annual Report

| Table of contents |

Table of contents

| Message from the President | 1 | |

| MMA Praxis Stewardship Investing Report | 2 | |

| MMA Praxis Intermediate Income Fund | ||

| Portfolio managers’ letter | 5 | |

| Performance review | 7 | |

| Schedule of portfolio investments | 9 | |

| MMA Praxis Core Stock Fund | ||

| Portfolio managers’ letter | 19 | |

| Performance review | 20 | |

| Schedule of portfolio investments | 22 | |

| MMA Praxis Value Index Fund | ||

| Portfolio manager’s letter | 27 | |

| Performance review | 28 | |

| Schedule of portfolio investments | 30 | |

| MMA Praxis Growth Index Fund | ||

| Portfolio manager’s letter | 40 | |

| Performance review | 41 | |

| Schedule of portfolio investments | 43 | |

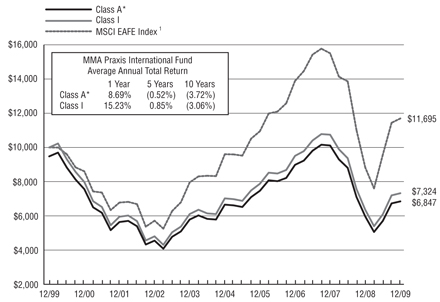

| MMA Praxis International Fund | ||

| Portfolio manager’s letter | 53 | |

| Performance review | 56 | |

| Schedule of portfolio investments | 58 | |

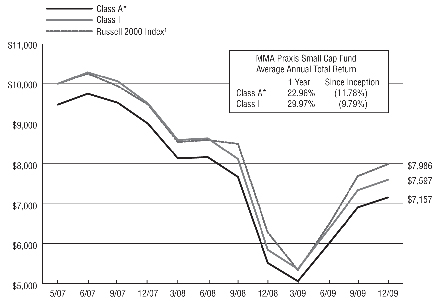

| MMA Praxis Small Cap Fund | ||

| Portfolio manager’s letter | 67 | |

| Performance review | 68 | |

| Schedule of portfolio investments | 70 | |

| Statements of assets and liabilities | 75 | |

| Statements of operations | 79 | |

| Statements of changes in net assets | 81 | |

| Financial highlights | 83 | |

| Notes to financial statements | 95 | |

| Report of Independent Registered Public Accounting Firm | 112 | |

| Additional fund information (unaudited) | 113 | |

| Management of the Trust (unaudited) | 123 | |

Glossary of Terms

Barclay’s Capital Aggregate Bond Index is an unmanaged index composed of the Barclay’s Capital Government/Credit Index and the Barclay’s Capital Mortgage-Backed Securities Index and includes Treasury issues, agency issues, corporate bond issues and mortgage-backed securities, and is intended to be generally representative of the bond market as a whole .

The Morgan Stanley Capital International-Europe, Australia and the Far East Index (MSCI EAFE Index) is a widely recognized unmanaged index composed of a sample of companies representative of the developed markets throughout the world, excluding the United States and Canada.

The Morgan Stanley Capital All Country World Free (ex. U.S.) Index is a widely recognized, unmanaged index composed of a sample of companies representative of the markets of both developed and emerging markets throughout the world, excluding the United States.

Standard & Poor’s 500 Composite Stock Price Index (the “S&P 500 Index”) is a widely recognized, unmanaged index of 500 selected common stocks, most of which are listed on the New York Stock Exchange.

Standard & Poor’s 500/Citigroup Value Index (the “S&P 500/Cititgroup Value Index”), is an unmanaged constructed by dividing the stocks in the S&P 500 Index into two categories, growth and value, according to price-to-book ratios. Prior to December 16, 2005, this index represented the S&P/Barra Value Index.

The FTSE KLD 400 Social Index is a float-adjusted market capitalization-weighted, common stock index of U.S. equities. It is a widely recognized benchmark for measuring the impact of social and environmental screening on portfolios.

MSCI US Prime Market Growth Index represents the growth companies of the MSCI US Prime Market 750 Index. The MSCI US Prime market 750 Index represents the universe of large and medium capitalization companies in the US equity market.

MSCI US Prime Market Value Index represents the value companies of the MSCI US Prime Market 750 Index. The MSCI Prime Market 750 Index represents the universe of large and medium capitalization companies in the U.S. equity market.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. Equity Universe. It measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

Gross Domestic Product (the “GDP”), is the measure of the market value of the goods and services produced by labor and property in the United States.

Consumer Price Index (the “CPI”), is an index of prices used to measure the change in the cost of basic goods and services in comparison with a fixed base period.

Price-to-Earnings Ratio (the “P/E Ratio”), is a valuation ratio of a company's current share price compared to its per-share earnings.

SuperComposite 1500 Index. Large-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price to-book ratio, and three-year sales-per share growth value, compared to the S&P 500 Index.

The above indices are unmanaged and do not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. An investor cannot invest directly in an index, although they can invest in the underlying securities.

| Message from the President |

Message from the President

One year ago, we were looking back on a 12-month period that was extremely difficult for investors. Today, while there is still a sense of uncertainty about the future, the economic climate in the United States and internationally seems to be improving.

The domestic equity markets performed well in 2009, predicting the current economic recovery. Earlier readings of leading economic indicators were confirmed by a 5.9 percent growth rate during the fourth quarter, but unemployment remains high. In spite of the negatives, we are pleased with progress that is being made.

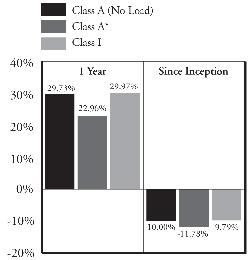

Domestic equities, as measured by the Standard & Poor’s 500 Index, rose by 26.47 percent for the one-year period ending Dec. 31, 2009. The MMA Praxis Core Stock Class A Share (NAV) outperformed its benchmark and rose 29 percent. Over the same period the Class A Share (NAV) of the MMA Praxis Value Index Fund rose by 22.64 percent and the MMA Praxis Growth Index Fund rose by 34.38 percent. The Class A Share (NAV) of the MMA Praxis Small Cap Fund rose by 29.73 percent.

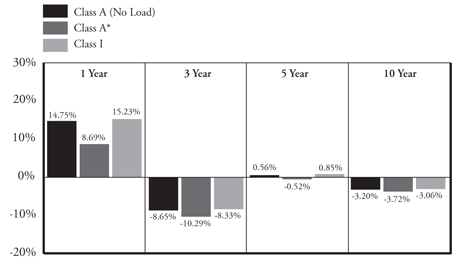

The international equity benchmark MSCI EAFE Index was up by 32.46 percent for the one-year period ending Dec. 31, 2009. The MMA Praxis International Class A Share (NAV) underperformed its benchmark over the one year period and was up a disappointing 14.75 percent. The majority of the Fund's shortfall relative to its benchmark occurred during the first few weeks of the global equity rally that began in early March. At that time, the fund owned financially sound companies in an effort to preserve capital, during what was expected to be an extended difficult period. Instead, sentiment shifted quickly to a positive trend and investors favored the riskiest stocks over more stable companies during March and April. The sub-advisor for this Fund, Evergreen Investments, provides additional commentary in the section devoted to reports from the portfolio managers.

We are pleased to report that the MMA Praxis Intermediate Income Fund continued to outperform its benchmark, the Barclays Capital Aggregate Bond Index. The Class A Share (NAV) posted a gain of 10.49 percent for the year, against a benchmark return of 5.93 percent. The 3-year annualized returns were 6.45 percent and 5-year annualized returns were 4.94 percent. We are grateful for the stewardship of this fund led by investment co-managers, Delmar King and Benjamin Bailey of MMA Capital Management.

In the following pages you will find portfolio managers’ letters and performance review for each of the Funds. Please read them for further expansion and explanation of the events of 2009.

Thank you for being an investor with MMA Praxis Mutual Funds. As a faith-based mutual fund family, we remain committed to being stewards of the resources you entrust to us, and we are grateful for your confidence.

Sincerely,

David C. Gautsche

President

MMA Praxis Mutual Funds

1

| MMA Praxis Stewardship Investing Report |

MMA Praxis Stewardship Investing Report

New shareholder advocacy themes bring opportunities and challenges

MMA Praxis added two new themes to help focus its shareholder advocacy efforts for the years ahead. These themes – while not excluding other important, emerging issues – help staff focus energy and build relationships to bring impact to our shareholder advocacy efforts.

Modern slavery

In response to growing concerns about human trafficking and its presence in business supply chains, MMA Praxis will focus on several aspects of this issue in partnership with other faith-based institutional investors.

The following issue areas will provide MMA Praxis with opportunities for corporate engagement on this topic in the coming year:

• Extractive industries in the Democratic Republic of Congo (DRC)

• Cotton in Uzbekistan

• Cocoa production in west Africa

• Pig-iron production in South America

• International sex trafficking

• Forced labor in auto supply chain

• Awareness of human trafficking (modern slavery) among health care providers

Food/Water safety and security

Concerns related to food touch all our lives deeply and personally. Food shapes people’s sense of dignity; its scarcity can breed conflict and violence; its distribution raises issues of justice; it can threaten communities and individuals; and, it impacts environmental sustainability – all these concerns are part of MMA Praxis’ stewardship investing core values.

Water is fast becoming the planet’s most precious, limited resource. Unsustainable practices are not only a threat to safety of consumers and the environment, but a threat to the company’s image and long-term profitability.

MMA Praxis has been working with some food companies for more than a year and seeks to address concerns while encouraging them on a more sustainable path. Areas we plan to address include:

• Reduction of waste, energy, and water use throughout supply chains.

• Instituting conservation and pollution prevention measures for the full product life-cycle.

• Labeling products for country of origin.

• Safety testing and systems to ensure identity preservation and traceability “from farm to fork.”

• Pesticide use reduction by potato farmers.

• Reductions in antibiotic use in large-scale farming operations.

Shareholders pursue DRC conflict minerals

MMA Praxis has joined with other investors in signing a shareholder letter stating opposition toward the ongoing conflict in the Democratic Republic of the Congo over “conflict minerals.”

Armed groups control a significant number of the mines in the eastern Congo, and the minerals reaped from these mines are a major source of income for them. These conflict minerals end up in refined electronics goods such as laptops, video game consoles, mobile phones, and equipment in medical devices and automobiles. This investor statement urges companies to take action to ensure their products are free of conflict minerals originating in the DRC.

2

To do their part to stop the continuing violence, investors recommend that companies take immediate and decisive action to:

| • | Make a public statement condemning the use of mineral revenue to fuel the ongoing conflict in the DRC and explain the steps the company is taking to address the issue; |

| • | Develop policies and procedures to identify where the raw metals in their products originate from and ensure conflict minerals are not entering into their supply chain; |

| • | Work with suppliers throughout their entire supply chain to ensure internal policies on sourcing conflict minerals are being adhered to; |

| • | Work with non-governmental organizations, industry associations, investors and other stakeholders to support various corporate social responsibility, legislative, and diplomatic strategies that will help end the exchange of minerals from the DRC that finance the ongoing conflict. |

Safer alternatives sought for natural gas development

As part of its creation care advocacy, MMA Praxis co-filed a shareholder resolution at EOG Resources calling for a report on the environmental impact of its hydraulic fracturing operations and potential policies for the company to adopt – above and beyond regulatory requirements – to reduce or eliminate hazards to air, water, and soil quality from fracturing.

EOG Resources is a major natural gas company and has significant gas reserves that require unconventional production techniques to recover, i.e., hydraulic fracturing, which injects a mix of water, chemicals and particles underground to create fractures through which gas can flow for collection. Fracturing operations potentially increase incidents of toxic spills from waste water ponds, impact to local water quantity and quality, and degradation of air quality.

MMA Praxis believes hydraulic drilling activities increase the potential for reputational damage and vulnerability to litigation, and weak and uneven regulatory controls necessitate that companies go above and beyond regulatory requirements to reduce environmental hazards and protect their own long-term interests.

MMA Praxis and the other filers believe the policies explored should include, among other things, the use of less toxic fracturing fluids, recycling or reuse of waste fluids, and other structural or procedural strategies to reduce fracturing hazards.

MMA Praxis Intermediate Income Fund invests in World Bank Green Bonds

As a reflection of environmental stewardship, MMA Praxis strives to care for God’s creation through investment activities. The MMA Praxis Intermediate Income Fund has shown this commitment by making a $2 million purchase in World Bank Green Bonds. Green Bonds were recently launched by the World Bank to connect capital markets to climate change-related initiatives. The World Bank is a global development cooperative owned by 186 member countries whose goal is to help overcome poverty and improve standards of living for people worldwide.

Green Bonds support World Bank projects that meet specific criteria for development activities that help lower global carbon emissions.

Community Development Investing—more important than ever

With the deepest recession since the Great Depression still impacting lives, the significance of community development financial institutions is clear—providing access to capital at fair terms and in the client’s best interest, to individuals/organizations that most mainstream financial services firms pass by.

3

Through MMA Community Development Investments (MMA CDI), MMA Praxis Mutual Funds, has invested more than $7 million in community development financial institutions across the United States and around the world. And while the economic downturn has posed significant challenges for these institutions, MMA CDI has yet to experience a loss of interest or principal from these investments.

One empowering story of the ongoing need and opportunity is the continued growth of The Isaiah Funds, the nation’s first interfaith partnership for disaster recovery investing. Founded by MMA CDI and five other faith-based investor organizations, the Isaiah Funds is dedicated to investing in communities devastated by disaster. Beginning with a focus on the Gulf Coast in the wake of hurricanes Katrina and Rita, the Isaiah Funds raised over $5 million to support rebuilding by local communities. The Fund’s first investment of $500,000 helped launch the construction of a significant housing project in the Central City region of New Orleans called The Muses. Now well into construction, The Muses will provide more than150 affordable housing units—nearly 60 percent designated for low-income families—strategically poised between the historically black, Central City community and the historically white, wealthy St. Charles Avenue neighborhood. It is hoped that The Muses will not only provide much needed housing, but also lay the foundations for economic growth as well.

Mark Regier

Director of Stewardship Investing

4

| MMA Praxis Intermediate Income Fund |

MMA Praxis Intermediate Income Fund

Annual report to shareholders

Portfolio managers’ letter

Returns for the MMA Praxis Intermediate Income Fund were the best ever relative to the Fund’s benchmark, the Barclays Capital Aggregate Index. For the year, the total return for A shares (NAV) was 10.49 percent. This compared very favorably with the benchmark return of 5.93 percent. For the fourth quarter, the return was .34 percent (A shares NAV) versus .20 percent for the Barclay’s Capital Aggregate Index.

There were several reasons for this strong performance. As reported in previous investor letters, earlier in 2009, we aggressively added to the corporate allocation of the portfolio and drew down the mortgage weight. This helped substantially given the very strong 18.68 percent return for Corporate holdings versus the 5.89 percent return from mortgages.

Another overweighted sector was commercial mortgage backed securities (CMBS). CMBS returned 28.45 percent for 2009. The heavy weights in Corporate and CMBS relative to the benchmark accounted for a substantial portion of the excess return.

The other large positive factor that helped the Fund’s returns was the lack of Treasury securities. Since the Funds avoid Treasuries and substitutes Agencies for them, the return advantage of Agencies, which was 1.95 percent versus the Treasury returns of -3.57 percent, helped overall.

The three overweight areas discussed above were the drivers of the Fund’s outperformance. Beyond that there were other small positives, but their impacts were dwarfed by the relative performance of agencies, CMBS, and Corporate.

Outlook

2010 will be a very different year from 2009. First, we believe the opportunities ahead are very modest compared with 2009. There are economic uncertainties that will be central to how investment grade bonds perform. Among these are the strength of the recovery, the impact of the Federal Reserve withdrawal from its asset acquisition program, possible international imports from sovereign debt problems, and possible state and local solvency issues.

Our outlook for 2010 is for an economic recovery that is well below historical norms. We expect the recovery will be more like the early 1990 and early 2000 experiences. There are severe constraints on the rate of recovery. Among these are tight credit for small businesses, a continued drag from housing and probably further house price declines, a smaller manufacturing sector, drags from tax increases and budget cuts by state and local governments, and commercial real estate problems.

Our current thinking is that the recovery will be strong enough that interest rates will rise moderately. The heavy financing by the federal government will put some upward pressure on rates. Offsetting that will be very low inflation and limited private credit demand as businesses build cash and reduce debt with consumers responding similarly.

We still believe that credit has some room to perform better. This reflects strong corporate cash flows and restrained business capital spending. CMBS valuations on a risk-adjusted basis are attractive as well on the highest rated tranches. Selected municipal bonds look interesting. On the other hand, mortgage-backed securities appear expensive and potentially risky when the Fed stops buying.

We believe there are still opportunities in bonds, but 2010 looks like it will possibly be more like a normal bond year in many ways.

5

Our final comment is about inflation. There is widespread concern about inflation as a result of the large deficit spending and aggressive monetary policy of the government. This combination of government borrowing and easy money policies would be highly inflationary if the economy were operating anywhere near capacity, but we believe that the economy is far below potential.

Even if real growth averages 4 percent over the next few years and assuming long-term potential growth is 2.6 percent (a rate that is in line with historical trends), some leading economists suggest it will take almost seven years to get back to full employment. This suggests that unemployment and sluggish growth will be the biggest concern for 2010 and possibly longer.

This does not mean we are ignoring the potential for inflation risks. As long as deficits require foreign financing and absorb a large percentage of domestic savings there is ample reason to be mindful of inflation risks.

Delmar King

MMA Praxis Intermediate Income Fund

Co-fund Manager

Benjamin J. Bailey, CFA®

MMA Praxis Intermediate Income Fund

Co-fund Manager

6

| Performance review |

MMA Praxis Intermediate Income Fund

Performance review

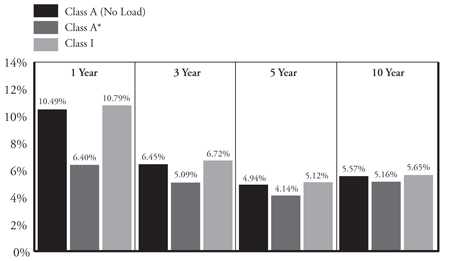

Average annual total returns as of 12/31/09

| Inception | Expense Ratio** | ||||||

| Date | 1 Year | 3 Year | 5 Year | 10 Year | Gross | Net | |

| Class A (No Load) | 5/12/99 | 10.49% | 6.45% | 4.94% | 5.57% | 1.21% | 0.93% |

| Class A* | 5/12/99 | 6.40% | 5.09% | 4.14% | 5.16% | ||

| Class I | 5/1/06 | 10.79% | 6.72% | 5.12% | 5.65% | 0.64% | 0.64% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit mmapraxis.com.

| * | Reflects maximum front-end sales charge of 3.75%. |

Class I Share of this Fund was not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Share since inception of 1/4/94 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

The total return set forth reflects certain expenses that were contractually or voluntarily reduced, reimbursed or paid by third party. In such instances, and without this activity, total return would have been lower.

| ** | Reflects the expense ratios as reported in the Prospectus dated May 1, 2009. Contractual fee waivers are in effect from May 1, 2009 through April 30, 2010 for Class A. Voluntary fee waivers were in effect through December 31, 2009 for Class I. |

7

MMA Praxis Intermediate Income Fund

Performance review

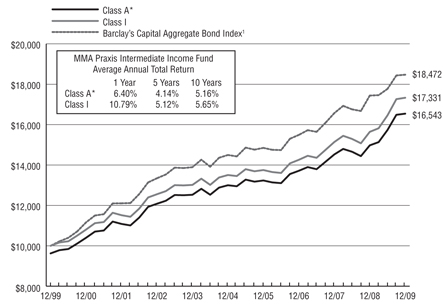

Growth of $10,000 investment 12/31/99 to 12/31/09

This chart represents historical performance of a hypothetical investment of $10,000 in the Intermediate Income Fund from 12/31/99 to 12/31/09, and represents the reinvestment of dividends and capital gains in the Fund.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit mmapraxis.com.

The total return set forth reflects certain expenses that were contractually or voluntarily reduced, reimbursed or paid by third party. In such instances, and without this activity, total return would have been lower.

| * | Reflects maximum front-end sales charge of 3.75%. |

Class I Share of this Fund was not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Share since inception of 1/4/94 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

| 1 | Barclay's Capital Aggregate Bond Index is an unmanaged index composed of the Barclay's Capital Government/Credit Index and the Barclay's Capital Mortgage-Backed Securities Index and includes Treasury issues, agency issues, corporate bond issues and mortgage-backed securities, and is intended to be generally representative of the bond market as a whole. |

The above indices are for illustrative purposes only and the Barclay's Capital Aggregate Bond Index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund's performance reflects the deduction of these value-added services. An investor cannot invest directly in an index, although they can invest in its underlying securities.

8

| Schedule of portfolio investments |

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| ASSET BACKED SECURITIES—0.2% | ||||||||

| Discover Card Master Trust, 5.10%, 10/15/13 | $ | 500,000 | $ | 523,147 | ||||

| Residential Funding Mortgage Securities II, Inc., 5.53%, 2/25/36 | 8,752 | 8,680 | ||||||

| TOTAL ASSET BACKED SECURITIES | 531,827 | |||||||

| COLLATERALIZED MORTGAGE OBLIGATION—0.2% | ||||||||

| JPMorgan Mortgage Trust, 4.50%, 9/25/34 | 381,998 | 367,356 | ||||||

| COMMERCIAL MORTGAGE BACKED SECURITIES—8.4% | ||||||||

| Banc of America Commercial Mortgage, Inc., 5.12%, 7/11/43 | 500,000 | 517,598 | ||||||

| Bear Stearns Commercial Mortgage Securities, 4.95%, 2/11/41 | 268,910 | 270,136 | ||||||

| Bear Stearns Commercial Mortgage Securities, 5.12%, 2/11/41+ | 1,000,000 | 978,605 | ||||||

| Bear Stearns Commercial Mortgage Securities, 4.67%, 6/11/41 | 1,000,000 | 956,604 | ||||||

| Bear Stearns Commercial Mortgage Securities, 5.54%, 9/11/41 | 2,000,000 | 1,947,880 | ||||||

| Bear Stearns Commercial Mortgage Securities, 4.52%, 11/11/41 | 500,000 | 496,031 | ||||||

| Bear Stearns Commercial Mortgage Securities, 4.56%, 2/13/42+ | 979,347 | 978,637 | ||||||

| Bear Stearns Commercial Mortgage Securities, 5.74%, 9/11/42+ | 1,000,000 | 963,096 | ||||||

| Bear Stearns Commercial Mortgage Securities, 5.13%, 10/12/42+ | 1,125,000 | 1,131,422 | ||||||

| Bear Stearns Commercial Mortgage Securities, 5.61%, 6/11/50 | 1,000,000 | 1,014,258 | ||||||

| Chase Commercial Mortgage Securities Corp., 7.32%, 10/15/32 | 851,811 | 872,280 | ||||||

| First Union National Bank Commercial Mortgage, 6.22%, 12/12/33 | 500,000 | 523,540 | ||||||

| GE Capital Commercial Mortgage Corp., 6.53%, 5/15/33 | 850,000 | 882,694 | ||||||

| GMAC Commercial Mortgage Securities, Inc., 6.47%, 4/15/34 | 933,369 | 966,958 | ||||||

| Heller Financial Commercial Mortgage Asset, 7.75%, 1/17/34 | 427 | 426 | ||||||

| JPMorgan Chase Commercial Mortgage Securities Corp., 4.90%, 10/15/42 | 1,000,000 | 945,267 | ||||||

| JPMorgan Chase Commercial Mortgage Securities Corp., 4.92%, 10/15/42+ | 1,000,000 | 961,432 | ||||||

| JPMorgan Chase Commercial Mortgage Securities Corp., 5.40%, 5/15/45 | 2,000,000 | 1,857,949 | ||||||

| JPMorgan Chase Commercial Mortgage Securities Corp., 4.63%, 3/15/46 | 644,843 | 644,270 | ||||||

| Morgan Stanley Capital, 4.83%, 6/12/47 | 1,000,000 | 998,732 | ||||||

| Morgan Stanley Capital I, 5.81%, 8/12/41+ | 1,000,000 | 1,007,672 | ||||||

| Morgan Stanley Capital I, 5.01%, 1/14/42 | 1,000,000 | 1,006,832 | ||||||

| Morgan Stanley Dean Witter Capital I, 5.93%, 12/15/35 | 1,225,000 | 1,268,872 | ||||||

| TOTAL COMMERCIAL MORTGAGE BACKED SECURITIES | 21,191,191 | |||||||

| FOREIGN BONDS—0.8% | ||||||||

| Province of Ontario, Canada, 4.10%, 6/16/14 | 1,000,000 | 1,043,615 | ||||||

| Republic of Austria, 2.00%, 11/15/12(a) | 1,000,000 | 1,010,000 | ||||||

| TOTAL FOREIGN BONDS | 2,053,615 | |||||||

9

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| MUNICIPAL BONDS—1.9% | ||||||||

| Cincinnati Ohio Water System Rev., 6.46%, 12/01/34 | $ | 600,000 | $ | 602,748 | ||||

| Houston Independent School District, 6.17%, 2/15/34 | 1,000,000 | 991,240 | ||||||

| Indianapolis Public School Multi-School Building, 5.73%, 7/15/29 | 1,500,000 | 1,398,570 | ||||||

| LL&P Wind Energy, Inc. (XLCA), 5.73%, 12/01/17(a) | 1,000,000 | 958,660 | ||||||

| Wisconsin State Transportation Rev., 5.84%, 7/01/30 | 800,000 | 767,552 | ||||||

| TOTAL MUNICIPAL BONDS | 4,718,770 | |||||||

| CORPORATE BONDS—42.1% | ||||||||

| ADVERTISING—0.4% | ||||||||

| Omnicom Group, Inc., 6.25%, 7/15/19 | 1,000,000 | 1,078,849 | ||||||

| AUTOMOBILE MANUFACTURERS—0.3% | ||||||||

| PACCAR, Inc., 6.88%, 2/15/14 | 760,000 | 857,325 | ||||||

| BIOTECHNOLOGY—0.4% | ||||||||

| Amgen, Inc., 5.70%, 2/01/19 | 500,000 | 536,176 | ||||||

| Biogen Idec, Inc., 6.00%, 3/01/13 | 500,000 | 531,049 | ||||||

| 1,067,225 | ||||||||

| BROADCASTING & CABLE TV—1.1% | ||||||||

| Comcast Corp., 5.70%, 5/15/18 | 500,000 | 525,625 | ||||||

| McGraw-Hill Cos., Inc., 5.38%, 11/15/12 | 1,000,000 | 1,058,487 | ||||||

| Thomson Reuters Corp., 6.20%, 1/05/12 | 1,200,000 | 1,291,211 | ||||||

| 2,875,323 | ||||||||

| CAPITAL MARKETS—0.7% | ||||||||

| BlackRock, Inc., 2.25%, 12/10/12 | 665,000 | 662,089 | ||||||

| BlackRock, Inc., 3.50%, 12/10/14 | 1,000,000 | 987,442 | ||||||

| 1,649,531 | ||||||||

| COMMERCIAL BANKS—1.8% | ||||||||

| American Express Bank FSB, 5.55%, 10/17/12 | 630,000 | 673,740 | ||||||

| Bank of New York Mellon Corp., 5.13%, 8/27/13 | 830,000 | 896,007 | ||||||

| State Street Corp., 7.35%, 6/15/26 | 1,000,000 | 1,054,797 | ||||||

| Wells Fargo & Co., 5.25%, 10/23/12 | 1,250,000 | 1,334,468 | ||||||

| Wells Fargo & Co., Perpetual Bond, 7.98%, 12/31/49+ | 500,000 | 501,250 | ||||||

| 4,460,262 | ||||||||

| COMMERCIAL SERVICES & SUPPLIES—0.6% | ||||||||

| GATX Corp., 9.00%, 11/15/13 | 445,010 | 491,710 | ||||||

| TTX Co., 4.90%, 3/01/15(a) | 1,000,000 | 930,212 | ||||||

| 1,421,922 | ||||||||

| COMMUNICATIONS EQUIPMENT—0.1% | ||||||||

| Cisco Systems, Inc., 4.45%, 1/15/20 | 200,000 | 196,197 | ||||||

| COMPUTERS & PERIPHERALS—0.2% | ||||||||

| Dell, Inc., 5.63%, 4/15/14 | 500,000 | 544,721 | ||||||

10

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| CORPORATE BONDS—42.1%, continued | ||||||||

| CONSTRUCTION MATERIALS—0.4% | ||||||||

| Martin Marietta Materials, Inc., 6.60%, 4/15/18 | $ | 1,000,000 | $ | 1,029,375 | ||||

| CONSUMER FINANCE—1.0% | ||||||||

| American Honda Finance Corp., 4.63%, 4/02/13(a) | 1,500,000 | 1,541,175 | ||||||

| Ford Motor Credit Co. LLC, 7.25%, 10/25/11 | 1,000,000 | 1,009,892 | ||||||

| 2,551,067 | ||||||||

| CONTAINERS & PACKAGING—0.2% | ||||||||

| Bemis Co., Inc., 5.65%, 8/01/14 | 500,000 | 532,192 | ||||||

| DIVERSIFIED FINANCIAL SERVICES—4.1% | ||||||||

| Allstate Life Global Funding Trusts, 5.38%, 4/30/13 | 500,000 | 533,737 | ||||||

| Citigroup, Inc., 5.13%, 5/05/14 | 1,000,000 | 995,309 | ||||||

| Equifax, Inc., 4.45%, 12/01/14 | 1,110,000 | 1,115,570 | ||||||

| General Electric Capital Corp., 6.15%, 8/07/37 | 1,000,000 | 944,324 | ||||||

| GMAC, Inc., 6.75%, 12/01/14(a) | 600,000 | 570,000 | ||||||

| Goldman Sachs Group, Inc., 6.88%, 1/15/11 | 500,000 | 530,213 | ||||||

| JPMorgan Chase & Co., 4.75%, 5/01/13 | 1,000,000 | 1,055,522 | ||||||

| Morgan Stanley, 5.63%, 9/23/19 | 1,500,000 | 1,510,965 | ||||||

| National Rural Utilities Cooperative Finance Corp., 10.38%, 11/01/18 | 780,000 | 1,033,559 | ||||||

| NYSE Euronext, 4.80%, 6/28/13 | 1,000,000 | 1,049,131 | ||||||

| Principal Life Global Funding I, 6.25%, 2/15/12(a) | 1,000,000 | 1,050,027 | ||||||

| 10,388,357 | ||||||||

| ELECTRIC UTILITIES—5.3% | ||||||||

| AEP Texas North Co., 5.50%, 3/01/13 | 1,000,000 | 1,051,741 | ||||||

| Atlantic City Electric Co., 7.75%, 11/15/18 | 500,000 | 593,726 | ||||||

| CenterPoint Energy Houston Electric LLC, 7.00%, 3/01/14 | 1,000,000 | 1,138,562 | ||||||

| Consumers Energy Co., 6.70%, 9/15/19 | 625,000 | 704,588 | ||||||

| Idaho Power Co., 4.50%, 3/01/20 | 500,000 | 477,660 | ||||||

| ITC Holdings Corp., 5.50%, 1/15/20(a) | 500,000 | 487,117 | ||||||

| MidAmerican Energy Co., 6.75%, 12/30/31 | 1,500,000 | 1,677,564 | ||||||

| Niagara Mohawk Power Corp., 4.88%, 8/15/19(a) | 500,000 | 495,741 | ||||||

| Pacific Gas & Electric Co., 8.25%, 10/15/18 | 500,000 | 610,524 | ||||||

| Pennsylvania Electric Co., 5.20%, 4/01/20 | 500,000 | 492,441 | ||||||

| Portland General Electric Co., 6.10%, 4/15/19 | 1,100,000 | 1,215,215 | ||||||

| Potomac Electric Power Co., 6.50%, 11/15/37 | 1,000,000 | 1,097,380 | ||||||

| Puget Sound Energy, Inc., 6.74%, 6/15/18 | 1,000,000 | 1,101,246 | ||||||

| TransAlta Corp., 4.75%, 1/15/15 | 500,000 | 503,481 | ||||||

| TransAlta Corp., 6.65%, 5/15/18 | 500,000 | 521,303 | ||||||

| Vectren Utility Holdings, Inc., 6.63%, 12/01/11 | 1,000,000 | 1,049,516 | ||||||

| 13,217,805 | ||||||||

| ELECTRICAL EQUIPMENT—0.6% | ||||||||

| Briggs & Stratton Corp., 8.88%, 3/15/11 | 1,000,000 | 1,048,750 | ||||||

| Thomas & Betts Corp., 5.63%, 11/15/21 | 500,000 | 488,778 | ||||||

| 1,537,528 | ||||||||

11

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| CORPORATE BONDS—42.1%, continued | ||||||||

| FOOD & STAPLES RETAILING—0.2% | ||||||||

| Kroger Co., 7.50%, 1/15/14 | $ | 500,000 | $ | 570,643 | ||||

| FOOD PRODUCTS—1.0% | ||||||||

| Cargill, Inc., 7.50%, 9/01/26(a) | 1,250,000 | 1,401,805 | ||||||

| Kellogg Co., 4.25%, 3/06/13 | 1,000,000 | 1,048,305 | ||||||

| 2,450,110 | ||||||||

| GAS UTILITIES—1.9% | ||||||||

| Indiana Gas Co., Inc., 6.55%, 6/30/28 | 250,000 | 233,744 | ||||||

| Michigan Consolidated Gas Co., 8.25%, 5/01/14 | 1,000,000 | 1,152,276 | ||||||

| National Fuel Gas Co., 6.50%, 4/15/18 | 500,000 | 519,155 | ||||||

| Northern Natural Gas Co., 5.38%, 10/31/12(a) | 1,000,000 | 1,086,650 | ||||||

| Sempra Energy, 6.50%, 6/01/16 | 600,000 | 650,705 | ||||||

| Southern Union Co., 8.25%, 11/15/29 | 1,050,000 | 1,172,432 | ||||||

| 4,814,962 | ||||||||

| HEALTH CARE EQUIPMENT & SUPPLIES—0.6% | ||||||||

| Beckman Coulter, Inc., 6.00%, 6/01/15 | 900,000 | 981,223 | ||||||

| Zimmer Holdings, Inc., 4.63%, 11/30/19 | 500,000 | 495,461 | ||||||

| 1,476,684 | ||||||||

| HEALTH CARE PROVIDERS & SERVICES—1.4% | ||||||||

| Express Scripts, Inc., 6.25%, 6/15/14 | 550,000 | 600,121 | ||||||

| Howard Hughes Medical Institute, 3.45%, 9/01/14 | 665,000 | 673,837 | ||||||

| McKesson Corp., 6.50%, 2/15/14 | 1,000,000 | 1,106,164 | ||||||

| Roche Holdings, Inc., 6.00%, 3/01/19(a) | 1,000,000 | 1,098,851 | ||||||

| 3,478,973 | ||||||||

| HOTELS, RESTAURANTS & LEISURE—0.4% | ||||||||

| Yum! Brands, Inc., 8.88%, 4/15/11 | 1,000,000 | 1,082,073 | ||||||

| HOUSEHOLD DURABLES—0.3% | ||||||||

| Stanley Works, 6.15%, 10/01/13 | 725,000 | 797,794 | ||||||

| INDUSTRIAL CONGLOMERATES—0.8% | ||||||||

| Cooper U.S., Inc., 5.45%, 4/01/15 | 1,000,000 | 1,078,254 | ||||||

| Harsco Corp., 5.75%, 5/15/18 | 1,000,000 | 984,312 | ||||||

| 2,062,566 | ||||||||

| INTEGRATED TELECOMMUNICATION SERVICES—1.3% | ||||||||

| AT&T, Inc., 4.95%, 1/15/13 | 1,000,000 | 1,066,880 | ||||||

| Sprint Capital Corp., 7.63%, 1/30/11 | 1,000,000 | 1,023,750 | ||||||

| Verizon Communications, Inc., 5.50%, 4/01/17 | 1,000,000 | 1,055,228 | ||||||

| 3,145,858 | ||||||||

| IT SERVICES—0.4% | ||||||||

| Dun & Bradstreet Corp., 6.00%, 4/01/13 | 1,000,000 | 1,029,450 | ||||||

| LIFE & HEALTH INSURANCE—0.2% | ||||||||

| Prudential Financial, Inc., 4.75%, 4/01/14 | 591,000 | 591,971 | ||||||

12

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| CORPORATE BONDS—42.1%, continued | ||||||||

| MULTI-LINE INSURANCE—0.4% | ||||||||

| American International Group, Inc., 4.25%, 5/15/13 | $ | 500,000 | $ | 461,854 | ||||

| Metropolitan Life Global Funding I, 5.13%, 6/10/14(a) | 500,000 | 529,148 | ||||||

| 991,002 | ||||||||

| MULTILINE RETAIL—0.5% | ||||||||

| Wal-Mart Stores, Inc., 7.55%, 2/15/30 | 1,000,000 | 1,239,056 | ||||||

| OFFICE ELECTRONICS—0.4% | ||||||||

| Xerox Corp., 6.35%, 5/15/18 | 1,000,000 | 1,043,128 | ||||||

| OIL, GAS & CONSUMABLE FUELS—3.2% | ||||||||

| BP Capital Markets plc, 3.88%, 3/10/15 | 1,500,000 | 1,541,121 | ||||||

| Conoco, Inc., 6.95%, 4/15/29 | 1,075,000 | 1,218,561 | ||||||

| Motiva Enterprises LLC, 5.20%, 9/15/12(a) | 1,000,000 | 1,027,540 | ||||||

| Ras Laffan Liquefied Natural Gas Co. Ltd. III, 5.83%, 9/30/16(a) | 1,000,000 | 1,047,210 | ||||||

| Shell International Finance BV, 4.00%, 3/21/14 | 1,000,000 | 1,043,531 | ||||||

| Texas Gas Transmission LLC, 4.60%, 6/01/15 | 1,000,000 | 1,012,422 | ||||||

| XTO Energy, Inc., 7.50%, 4/15/12 | 1,000,000 | 1,115,032 | ||||||

| 8,005,417 | ||||||||

| PERSONAL PRODUCTS—0.9% | ||||||||

| Avon Products, Inc., 5.63%, 3/01/14 | 1,000,000 | 1,089,898 | ||||||

| Johnson & Johnson, 5.95%, 8/15/37 | 500,000 | 549,914 | ||||||

| Mead Johnson Nutrition Co., 3.50%, 11/01/14(a) | 500,000 | 494,301 | ||||||

| 2,134,113 | ||||||||

| PHARMACEUTICALS—1.1% | ||||||||

| Abbott Laboratories, 5.13%, 4/01/19 | 1,000,000 | 1,045,968 | ||||||

| Merck & Co., Inc., 4.00%, 6/30/15 | 500,000 | 521,422 | ||||||

| Novartis Capital Corp., 4.13%, 2/10/14 | 1,250,000 | 1,313,971 | ||||||

| 2,881,361 | ||||||||

| PROPERTY & CASUALTY INSURANCE—1.4% | ||||||||

| Chubb Corp., 6.50%, 5/15/38 | 500,000 | 550,606 | ||||||

| Fidelity National Title, 7.30%, 8/15/11 | 1,000,000 | 1,030,324 | ||||||

| Markel Corp., 6.80%, 2/15/13 | 1,000,000 | 1,010,660 | ||||||

| W.R. Berkley Corp., 5.13%, 9/30/10 | 1,000,000 | 1,009,968 | ||||||

| 3,601,558 | ||||||||

| PUBLISHING—0.3% | ||||||||

| Washington Post Co., 7.25%, 2/01/19 | 575,000 | 631,426 | ||||||

| REAL ESTATE INVESTMENT TRUSTS (REITS)—0.5% | ||||||||

| Simon Property Group LP, 6.35%, 8/28/12 | 1,200,000 | 1,280,921 | ||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT—0.4% | ||||||||

| AMB Property LP, 6.13%, 12/01/16 | 1,000,000 | 987,488 | ||||||

13

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| CORPORATE BONDS—42.1%, continued | ||||||||

| ROAD & RAIL—1.1% | ||||||||

| Canadian National Railway Co., 4.40%, 3/15/13 | $ | 1,000,000 | $ | 1,042,487 | ||||

| CSX Transportation, Inc., 8.38%, 10/15/14 | 480,519 | 553,639 | ||||||

| ERAC USA Finance Co., 5.90%, 11/15/15(a) | 1,000,000 | 1,034,480 | ||||||

| 2,630,606 | ||||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—0.9% | ||||||||

| Analog Devices, Inc., 5.00%, 7/01/14 | 500,000 | 521,596 | ||||||

| Applied Materials, Inc., 7.13%, 10/15/17 | 500,000 | 559,881 | ||||||

| KLA-Tencor Corp., 6.90%, 5/01/18 | 1,000,000 | 1,052,141 | ||||||

| 2,133,618 | ||||||||

| SOFT DRINKS—0.4% | ||||||||

| Bottling Group LLC, 5.13%, 1/15/19 | 1,000,000 | 1,039,157 | ||||||

| SPECIALTY RETAIL—0.5% | ||||||||

| Home Depot, Inc., 5.25%, 12/16/13 | 500,000 | 535,279 | ||||||

| Staples, Inc., 9.75%, 1/15/14 | 500,000 | 609,225 | ||||||

| 1,144,504 | ||||||||

| SUPRANATIONAL—2.5% | ||||||||

| Corporation Andina de Fomento, 5.20%, 5/21/13 | 1,000,000 | 1,045,749 | ||||||

| Inter-American Development Bank, 3.50%, 7/08/13 | 1,000,000 | 1,040,628 | ||||||

| Inter-American Development Bank, 3.50%, 3/15/13 | 1,000,000 | 1,040,244 | ||||||

| International Bank for Reconstruction & Development, 2.00%, 12/04/13 | 2,000,000 | 1,965,786 | ||||||

| International Finance Facility for Immunisation (IFFIM), 5.00%, 11/14/11(a) | 1,000,000 | 1,063,978 | ||||||

| 6,156,385 | ||||||||

| THRIFTS & MORTGAGE FINANCE—0.4% | ||||||||

| Countrywide Financial Corp., 5.80%, 6/07/12 | 1,000,000 | 1,061,511 | ||||||

| TRUCKING—0.4% | ||||||||

| Golden State Petroleum Transport Corp., 8.04%, 2/01/19 | 895,004 | 926,651 | ||||||

| UTILITIES-OTHER—0.7% | ||||||||

| FPL Energy Caithness Funding, 7.65%, 12/31/18(a) | 656,213 | 674,030 | ||||||

| Salton Sea Funding Corp., 7.48%, 11/30/18 | 935,253 | 998,092 | ||||||

| 1,672,122 | ||||||||

| WATER UTILITIES—0.4% | ||||||||

| American Water Capital Corp., 6.09%, 10/15/17 | 1,000,000 | 1,044,904 | ||||||

| TOTAL CORPORATE BONDS | 105,513,691 | |||||||

14

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| CORPORATE NOTES—1.0% | ||||||||

| DEVELOPMENT AUTHORITIES—1.0% | ||||||||

| MMA Community Development Investment, Inc., 1.10%, 12/31/11(b) | $ | 802,500 | $ | 802,500 | ||||

| MMA Community Development Investment, Inc., 0.73%, 12/31/12(b) | 910,000 | 910,000 | ||||||

| MMA Community Development Investment, Inc., 1.10%, 12/31/13(b) | 802,500 | 802,500 | ||||||

| TOTAL CORPORATE NOTES | 2,515,000 | |||||||

| INTEREST ONLY BONDS—0.1% | ||||||||

| FREDDIE MAC REMICS — 0.1% | ||||||||

| 5.00%, 4/15/29 | 2,000,000 | 140,933 | ||||||

| GOVERNMENT NATIONAL MORTGAGE ASSOCIATION — 0.0% | ||||||||

| 0.85%, 4/16/27+ | 6,677,526 | 133,854 | ||||||

| TOTAL INTEREST ONLY BONDS | 274,787 | |||||||

| U.S. GOVERNMENT AGENCIES—40.2% | ||||||||

| FEDERAL FARM CREDIT BANK — 0.9% | ||||||||

| 4.88%, 12/16/15 | 2,000,000 | 2,155,142 | ||||||

| FEDERAL HOME LOAN BANK — 3.7% | ||||||||

| 3.88%, 6/14/13 | 300,000 | 317,275 | ||||||

| 4.13%, 8/13/10 | 1,000,000 | 1,021,715 | ||||||

| 5.00%, 11/17/17 | 4,000,000 | 4,326,876 | ||||||

| 5.00%, 12/10/21 | 2,625,000 | 2,766,514 | ||||||

| 6.63%, 11/15/10 | 900,000 | 946,605 | ||||||

| 9,378,985 | ||||||||

| FEDERAL HOME LOAN MORTGAGE CORP. — 12.8% | ||||||||

| 2.97%, 5/01/34+ | 496,030 | 509,924 | ||||||

| 2.97%, 5/01/34+ | 235,873 | 242,484 | ||||||

| 3.75%, 3/27/19 | 3,500,000 | 3,431,473 | ||||||

| 4.13%, 7/12/10 | 1,987,000 | 2,026,468 | ||||||

| 4.50%, 6/01/18 | 1,051,095 | 1,081,434 | ||||||

| 5.00%, 4/01/19 | 1,066,275 | 1,122,386 | ||||||

| 5.00%, 12/01/21 | 1,703,544 | 1,787,333 | ||||||

| 5.00%, 2/15/32 | 2,000,000 | 2,081,621 | ||||||

| 5.00%, 7/01/35 | 1,730,461 | 1,777,868 | ||||||

| 5.50%, 4/01/22 | 1,552,891 | 1,643,352 | ||||||

| 5.50%, 11/01/33 | 845,215 | 889,413 | ||||||

| 5.50%, 3/01/36 | 1,143,540 | 1,202,266 | ||||||

| 5.50%, 6/01/36 | 1,461,792 | 1,531,607 | ||||||

| 5.50%, 6/01/36 | 1,738,158 | 1,824,160 | ||||||

| 5.50%, 12/01/36 | 1,707,785 | 1,792,285 | ||||||

| 5.50%, 12/01/36 | 1,687,590 | 1,771,091 | ||||||

15

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT | VALUE | |||||||

| U.S. GOVERNMENT AGENCIES—40.2%, continued | ||||||||

| FEDERAL HOME LOAN MORTGAGE CORP. — 12.8%, continued | ||||||||

| 6.00%, 9/01/17 | $ | 701,782 | $ | 749,136 | ||||

| 6.00%, 4/01/27 | 1,705,208 | 1,824,214 | ||||||

| 6.00%, 6/01/36 | 1,164,006 | 1,235,301 | ||||||

| 6.00%, 8/01/37 | 1,073,370 | 1,139,114 | ||||||

| 6.88%, 9/15/10 | 1,081,000 | 1,129,874 | ||||||

| 7.00%, 2/01/30 | 326,264 | 355,866 | ||||||

| 7.00%, 3/01/31 | 275,042 | 299,996 | ||||||

| 7.50%, 7/01/30 | 539,875 | 589,019 | ||||||

| 32,037,685 | ||||||||

| FEDERAL NATIONAL MORTGAGE ASSOCIATION — 15.3% | ||||||||

| 2.81%, 5/01/34+ | 366,004 | 378,545 | ||||||

| 3.11%, 2/01/34+ | 373,164 | 384,689 | ||||||

| 3.90%, 6/01/33+ | 131,933 | 136,257 | ||||||

| 4.13%, 4/15/14 | 900,000 | 957,185 | ||||||

| 5.00%, 2/13/17 | 3,000,000 | 3,256,491 | ||||||

| 5.00%, 7/01/18 | 557,208 | 582,874 | ||||||

| 5.00%, 9/01/18 | 742,216 | 776,403 | ||||||

| 5.00%, 4/01/25 | 1,297,144 | 1,344,958 | ||||||

| 5.00%, 7/01/25 | 1,124,787 | 1,166,248 | ||||||

| 5.00%, 10/01/25 | 1,401,621 | 1,453,286 | ||||||

| 5.00%, 10/01/35 | 1,919,746 | 1,972,039 | ||||||

| 5.39%, 5/01/37+ | 1,910,085 | 2,016,024 | ||||||

| 5.50%, 6/01/22 | 1,244,436 | 1,317,311 | ||||||

| 5.50%, 11/01/25 | 370 | 391 | ||||||

| 5.50%, 2/01/34 | 720,530 | 754,943 | ||||||

| 5.50%, 1/01/35 | 1,506,670 | 1,578,629 | ||||||

| 5.50%, 10/01/35 | 2,199,401 | 2,304,445 | ||||||

| 5.50%, 11/01/36 | 1,789,950 | 1,875,438 | ||||||

| 6.00%, 10/01/33 | 389,484 | 412,853 | ||||||

| 6.00%, 11/01/34 | 1,506,554 | 1,596,947 | ||||||

| 6.00%, 10/01/35 | 963,172 | 1,020,962 | ||||||

| 6.00%, 6/01/36 | 970,853 | 1,029,104 | ||||||

| 6.63%, 11/15/30 | 6,750,000 | 8,112,204 | ||||||

| 7.00%, 7/01/15 | 5,091 | 5,636 | ||||||

| 7.00%, 11/01/19 | 43,155 | 47,954 | ||||||

| 7.00%, 11/01/19 | 73,993 | 82,222 | ||||||

| 7.25%, 1/15/10 | 3,450,000 | 3,459,965 | ||||||

| 8.50%, 9/01/26 | 232,254 | 267,511 | ||||||

| 38,291,514 | ||||||||

16

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT/ | ||||||||

| SHARES | VALUE | |||||||

| U.S. GOVERNMENT AGENCIES—40.2%, continued | ||||||||

| GOVERNMENT NATIONAL MORTGAGE ASSOCIATION — 1.2% | ||||||||

| 4.50%, 1/20/34+ | $ | 173,813 | $ | 178,452 | ||||

| 5.50%, 10/20/38 | 1,821,498 | 1,893,587 | ||||||

| 6.50%, 11/20/38 | 444,035 | 466,779 | ||||||

| 6.75%, 4/15/16 | 56,398 | 61,342 | ||||||

| 7.00%, 12/20/30 | 88,117 | 95,605 | ||||||

| 7.00%, 10/20/31 | 56,534 | 61,339 | ||||||

| 7.00%, 3/20/32 | 190,045 | 206,194 | ||||||

| 2,963,298 | ||||||||

| SMALL BUSINESS ADMINISTRATION — 0.2% | ||||||||

| 0.60%, 2/25/32+ | 601,140 | 590,900 | ||||||

| 1.00%, 9/25/18+ | 44,615 | 44,318 | ||||||

| 635,218 | ||||||||

| FDIC GUARANTEED—6.1% | ||||||||

| U.S. Central Federal Credit Union, 1.25%, 10/19/11 | 1,300,000 | 1,299,645 | ||||||

| General Electric Capital Corp., 1.63%, 1/07/11 | 1,400,000 | 1,414,706 | ||||||

| Citibank NA, 1.75%, 12/28/12 | 3,000,000 | 2,973,606 | ||||||

| PNC Funding Corp., 1.88%, 6/22/11 | 650,000 | 656,616 | ||||||

| U.S. Central Federal Credit Union, 1.90%, 10/19/12 | 2,000,000 | 1,998,436 | ||||||

| Citigroup Funding, Inc., 1.88%, 10/22/12 | 3,000,000 | 2,988,666 | ||||||

| Citigroup Funding, Inc., 1.88%, 11/15/12 | 1,330,000 | 1,326,571 | ||||||

| General Electric Capital Corp., 2.20%, 6/08/12 | 175,000 | 177,454 | ||||||

| JPMorgan Chase & Co., 2.63%, 12/01/10 | 1,000,000 | 1,019,658 | ||||||

| Regions Bank/Birmingham AL, 3.25%, 12/09/11 | 1,500,000 | 1,556,532 | ||||||

| 15,411,890 | ||||||||

| TOTAL U.S. GOVERNMENT AGENCIES | 100,873,732 | |||||||

| INVESTMENT COMPANY—0.5% | ||||||||

| MUTUAL FUND—0.5% | ||||||||

| Pax World High Yield Bond Fund | 167,685 | 1,291,177 | ||||||

| SHORT TERM INVESTMENT—4.8% | ||||||||

| JPMorgan U.S. Government Money Market Fund-Agency Shares | 12,025,905 | 12,025,905 | ||||||

| TOTAL INVESTMENTS (Cost* $244,424,173)—100.2% | $ | 251,357,051 | ||||||

| Net other assets (liabilities) — (0.2)% | (387,049 | ) | ||||||

| NET ASSETS—100% | $ | 250,970,002 | ||||||

17

MMA Praxis Intermediate Income Fund

Schedule of portfolio investments, continued

December 31, 2009

| + | Variable rate security. Rates presented are the rates in effect at December 31, 2009. |

| (a) | 144a security is restricted as to resale to institutional investors. These securities were deemed liquid under guidelines established by the Board of Trustees. At December 31, 2009, these securities were valued at $16,500,925 or 6.6% of net assets. |

| (b) | Represents affiliated restricted security as to resale to shareholders and is not registered under the Securities Act of 1933. These securities have been deemed illiquid under guidelines established by the Board of Trustees: |

| Acquisition | |||

| Security | Yield | Shares | Date |

| MMA Community Development Investment, Inc. | 0.73% | 910,000 | 12/2009 |

| MMA Community Development Investment, Inc. | 1.10% | 802,500 | 12/2009 |

| MMA Community Development Investment, Inc. | 1.10% | 802,500 | 12/2009 |

At December 31, 2009, these securities had an aggregate market value of $2,515,000, representing 1.0% of net assets.

| * | Represents cost for financial reporting purposes. |

plc – Public Liability Company.

Other Information:

The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in the accompanying Notes to Financial Statements.

| Valuation Inputs at Reporting Date: | ||||||||||||||||

| Description | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Investments at Value | ||||||||||||||||

| Corporate Bonds | $ | — | $ | 105,513,691 | $ | — | $ | 108,811,772 | ||||||||

| Corporate Notes | — | — | 2,515,000 | 2,515,000 | ||||||||||||

| U.S. Government Agencies | — | 100,873,732 | — | 97,575,651 | ||||||||||||

| Commercial Mortgage Backed Securities | — | 21,191,191 | — | 21,191,191 | ||||||||||||

| Short Term Investment | 12,025,905 | — | — | 12,025,905 | ||||||||||||

| Municipal Bonds | — | 4,718,770 | — | 4,718,770 | ||||||||||||

| Foreign Bonds | — | 2,053,615 | — | 2,053,615 | ||||||||||||

| Investment Company | 1,291,177 | — | — | 1,291,177 | ||||||||||||

| Asset Backed Securities | — | 531,827 | — | 531,827 | ||||||||||||

| Collateralized Mortgage Obligations | — | 367,356 | — | 367,356 | ||||||||||||

| Interest Only Bonds | — | 274,787 | — | 274,787 | ||||||||||||

| Total Investments | $ | 13,317,082 | $ | 235,524,969 | $ | 2,515,000 | $ | 251,357,051 | ||||||||

Following is a reconciliation of Level 3 assets for which significant unobservable inputs for Investments in Securities were used to determine fair value for each Fund:

| Intermediate | ||||

| Income Fund | ||||

| Balance as of December 31, 2008 | $ | 2,515,000 | ||

| Proceeds from Sales | (2,515,000 | ) | ||

| Purchases | 2,515,000 | |||

| Balance as of December 31, 2009 | $ | 2,515,000 | ||

See accompanying notes to financial statements.

18

| MMA Praxis Core Stock Fund |

MMA Praxis Core Stock Fund

Annual report to shareholders

Portfolio managers’ letter

For the year ended Dec. 31, 2009, the Class A shares of MMA Praxis Core Stock Fund (NAV) returned 29.00 percent, out-performing its benchmark, the Standard & Poor’s 500 Index (Index), which returned 26.47 percent.

Factors affecting the Fund’s performance

Information technology, materials and consumer discretionary were the sectors within the Index that turned in the strongest performance over the year. Telecommunication services and utilities had the weakest performance, although their performance was still positive.

The Fund’s financial companies were the strongest contributors to performance on an absolute basis. The Fund’s relative performance versus the Index benefited as the Fund’s financial companies out-performed the corresponding sector within the Index (up 27 percent versus up 17 percent for the Index). American Express and GAM Holding were among the top contributors to the Fund’s performance during the period. Bank of America, Wells Fargo, NIPPONKOA and Citigroup were among the top detractors from performance. The Fund no longer owns Bank of America, NIPPONKOA or Citigroup.

The Fund’s performance versus the Index received support from strong stock selection in the energy and health care sector. The Fund’s health care sector holdings out-performed the Index’s holdings (up 45 percent versus up 20 percent for the Index) and this factor was the largest contributor to the Fund’s positive relative performance. Schering Plough was a top contributor to performance before merging with Merck. The Fund’s energy sector outperformance (up 33 percent versus up 14 percent for the Index) was the second largest factor for the positive relative performance compared with the Index. EOG Resources and Canadian Natural Resources were among the leading contributors to performance. ConocoPhillips was the top detractor from performance.

Information technology companies were a contributor to performance on an absolute basis, however, when compared with the Index, the Fund suffered from having a lower relative weighting (10 percent versus 18 percent for the Index). Google, Microsoft, and Texas Instruments were among the most important contributors to performance.

The Fund held approximately 12 percent of its assets in foreign companies (including American Depositary Receipts) at Dec. 31, 2009. As a whole these companies outperformed the domestic companies held by the Fund.

Christopher C. Davis

Portfolio Manager and CEO of Davis Advisors

Kenneth C. Feinberg

Portfolio Manager

19

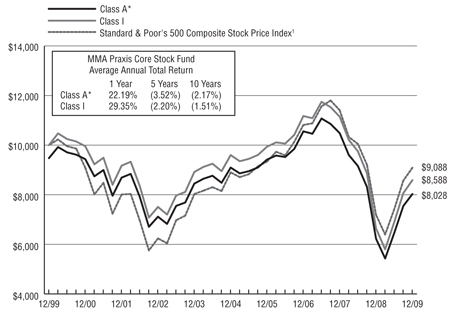

| Performance review |

MMA Praxis Core Stock Fund

Performance review

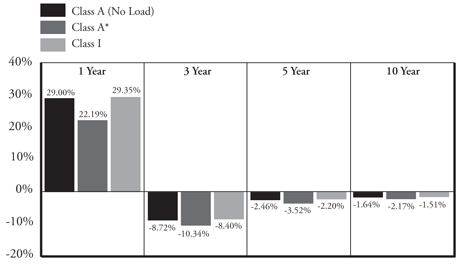

Average annual total returns as of 12/31/09

| Inception | Expense Ratio** | ||||||

| Date | 1 Year | 3 Year | 5 Year | 10 Year | Gross | Net | |

| Class A (No Load) | 5/12/99 | 29.00% | -8.72% | -2.46% | -1.64% | 1.56% | 1.56% |

| Class A* | 5/12/99 | 22.19% | -10.34% | -3.52% | -2.17% | ||

| Class I | 5/1/06 | 29.35% | -8.40% | -2.20% | -1.51% | 1.01% | 1.01% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit mmapraxis.com.

| * | Reflects maximum front-end sales charge of 5.25%. |

Class I Share of this Fund was not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Share since inception of 1/4/94 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

The total return set forth reflects certain expenses that were contractually or voluntarily reduced, reimbursed or paid by third party. In such instances, and without this activity, total return would have been lower.

| ** | Reflects the expense ratios as reported in the Prospectus dated May 1, 2009. Voluntary fee waivers were in effect through December 31, 2009 for Class A and Class I. |

20

MMA Praxis Core Stock Fund

Performance review

Growth of $10,000 investment 12/31/99 to 12/31/09

This chart represents historical performance of a hypothetical investment of $10,000 in the Core Stock Fund from 12/31/99 to 12/31/09, and represents the reinvestment of dividends and capital gains in the Fund.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit mmapraxis.com.

The total return set forth reflects certain expenses that were contractually or voluntarily reduced, reimbursed or paid by third party. In such instances, and without this activity, total return would have been lower.

| * | Reflects maximum front-end sales charge of 5.25%. |

Class I Share of this Fund was not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Share since inception of 1/4/94 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

| 1 | The S&P 500 Composite Stock Price Index (the "S&P 500 Index") is a widely recognized, unmanaged index of 500 selected common stocks, most of which are listed on the New York Stock Exchange. |

The above index is for illustrative purposes only and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The fund's performance reflects the deduction of these value-added services. An investor cannot invest directly in an index, although they can invest in its underlying securities.

21

| Schedule of portfolio investments |

MMA Praxis Core Stock Fund

Schedule of portfolio investments

December 31, 2009

| SHARES | VALUE | |||||||

| COMMON STOCKS—96.7% | ||||||||

| AIR FREIGHT & LOGISTICS—0.5% | ||||||||

| United Parcel Service, Inc., Class B | 17,900 | $ | 1,026,923 | |||||

| AUTOMOBILES—1.1% | ||||||||

| Harley-Davidson, Inc. | 83,100 | 2,094,120 | ||||||

| BEVERAGES—0.6% | ||||||||

| Coca-Cola Company | 19,300 | 1,100,100 | ||||||

| CAPITAL MARKETS—5.5% | ||||||||

| Ameriprise Financial, Inc. | 40,200 | 1,560,564 | ||||||

| Bank of New York Mellon Corp. | 146,600 | 4,100,402 | ||||||

| GAM Holding Ltd. (Switzerland) | 81,800 | 995,565 | ||||||

| Goldman Sachs Group, Inc. | 7,290 | 1,230,843 | ||||||

| Julius Baer Holding AG (Switzerland) | 81,800 | 2,876,779 | ||||||

| 10,764,153 | ||||||||

| CHEMICALS—0.3% | ||||||||

| Potash Corp of Saskatchewan, Inc. (Canada) | 4,627 | 502,029 | ||||||

| COMMERCIAL BANKS—4.3% | ||||||||

| Wells Fargo & Co. | 308,758 | 8,333,378 | ||||||

| COMMERCIAL SERVICES & SUPPLIES—1.5% | ||||||||

| Iron Mountain, Inc. (a) | 129,600 | 2,949,696 | ||||||

| COMPUTERS & PERIPHERALS—1.6% | ||||||||

| Hewlett-Packard Co. | 60,250 | 3,103,477 | ||||||

| CONSTRUCTION MATERIALS—1.6% | ||||||||

| Martin Marietta Materials, Inc. | 22,200 | 1,984,902 | ||||||

| Vulcan Materials Co. | 22,300 | 1,174,541 | ||||||

| 3,159,443 | ||||||||

| CONSUMER FINANCE—4.1% | ||||||||

| American Express Co. | 194,900 | 7,897,348 | ||||||

| CONTAINERS & PACKAGING—2.1% | ||||||||

| Sealed Air Corp. | 187,800 | 4,105,308 | ||||||

| DIVERSIFIED CONSUMER SERVICES—0.6% | ||||||||

| H&R Block, Inc. | 51,750 | 1,170,585 | ||||||

22

MMA Praxis Core Stock Fund

Schedule of portfolio investments, continued

December 31, 2009

| SHARES | VALUE | |||||||

| COMMON STOCKS—96.7%, continued | ||||||||

| DIVERSIFIED FINANCIAL SERVICES—3.3% | ||||||||

| JPMorgan Chase & Co. | 117,400 | $ | 4,892,058 | |||||

| Moody's Corp. | 54,800 | 1,468,640 | ||||||

| 6,360,698 | ||||||||

| ELECTRICAL EQUIPMENT—0.4% | ||||||||

| ABB Ltd.- ADR (Switzerland)(a) | 43,940 | 839,254 | ||||||

| ENERGY EQUIPMENT & SERVICES—0.9% | ||||||||

| Transocean Ltd. (Switzerland)(a) | 20,055 | 1,660,554 | ||||||

| FOOD & STAPLES RETAILING—9.9% | ||||||||

| Costco Wholesale Corp. | 244,400 | 14,461,148 | ||||||

| CVS Caremark Corp. | 151,122 | 4,867,640 | ||||||

| 19,328,788 | ||||||||

| FOOD PRODUCTS—0.2% | ||||||||

| Hershey Co. | 12,500 | 447,375 | ||||||

| HEALTH CARE EQUIPMENT & SUPPLIES—1.2% | ||||||||

| Becton Dickinson and Co. | 23,600 | 1,861,096 | ||||||

| CareFusion Corp. (a) | 19,465 | 486,820 | ||||||

| 2,347,916 | ||||||||

| HEALTH CARE PROVIDERS & SERVICES—2.3% | ||||||||

| Cardinal Health, Inc. | 38,930 | 1,255,103 | ||||||

| Express Scripts, Inc. (a) | 29,800 | 2,576,210 | ||||||

| Laboratory Corp of America Holdings (a) | 6,900 | 516,396 | ||||||

| UnitedHealth Group, Inc. | 5,700 | 173,736 | ||||||

| 4,521,445 | ||||||||

| HOUSEHOLD DURABLES—0.2% | ||||||||

| Hunter Douglas NV (Netherlands) | 8,300 | 404,905 | ||||||

| HOUSEHOLD PRODUCTS—4.1% | ||||||||

| Procter & Gamble Co. | 133,200 | 8,075,916 | ||||||

| INDEPENDENT POWER PRODUCERS & ENERGY TRADERS—0.2% | ||||||||

| AES Corp. (a) | 31,600 | 420,596 | ||||||

| INDUSTRIAL CONGLOMERATES—0.8% | ||||||||

| Tyco International Ltd. (Bermuda) | 43,890 | 1,565,995 | ||||||

| INSURANCE—11.1% | ||||||||

| Berkshire Hathaway, Inc., Class A (a) | 90 | 8,928,000 | ||||||

| Hartford Financial Services Group, Inc. | 36,600 | 851,316 | ||||||

| Loews Corp. | 138,300 | 5,027,205 | ||||||

23

MMA Praxis Core Stock Fund

Schedule of portfolio investments, continued

December 31, 2009

| SHARES | VALUE | |||||||

| COMMON STOCKS—96.7%, continued | ||||||||

| INSURANCE—11.1%, continued) | ||||||||

| Markel Corp. (a) | 525 | $ | 178,500 | |||||

| Principal Financial Group, Inc. | 15,900 | 382,236 | ||||||

| Progressive Corp. (a) | 239,300 | 4,305,007 | ||||||

| Transatlantic Holdings, Inc. | 37,743 | 1,966,788 | ||||||

| 21,639,052 | ||||||||

| INTERNET & CATALOG RETAIL—0.7% | ||||||||

| Amazon.com, Inc. (a) | 6,720 | 903,974 | ||||||

| Liberty Media Corp. - Interactive, Series A (a) | 41,375 | 448,505 | ||||||

| 1,352,479 | ||||||||

| INTERNET SOFTWARE & SERVICES—4.3% | ||||||||

| Google, Inc., Class A (a) | 13,460 | 8,344,931 | ||||||

| IT SERVICES—0.3% | ||||||||

| Visa, Inc., Class A | 6,970 | 609,596 | ||||||

| MACHINERY—0.2% | ||||||||

| PACCAR, Inc. | 12,810 | 464,619 | ||||||

| MARINE—1.0% | ||||||||

| China Shipping Development Co. Ltd., Class H (China) | 472,000 | 709,820 | ||||||

| Kuehne + Nagel International AG (Switzerland) | 12,000 | 1,165,837 | ||||||

| 1,875,657 | ||||||||

| MEDIA—4.1% | ||||||||

| Comcast Corp. - Special, Class A | 77,250 | 1,236,772 | ||||||

| DIRECTV, Class A (a) | 33,445 | 1,115,391 | ||||||

| Grupo Televisa SA- ADR (Mexico) | 43,600 | 905,136 | ||||||

| Liberty Media Corp. - Starz, Series A (a) | 3,344 | 154,326 | ||||||

| News Corp., Class A | 208,600 | 2,855,734 | ||||||

| Walt Disney Co. | 52,600 | 1,696,350 | ||||||

| 7,963,709 | ||||||||

| METALS & MINING—1.0% | ||||||||

| BHP Billiton plc (United Kingdom) | 32,000 | 1,031,143 | ||||||

| Rio Tinto plc (United Kingdom) | 17,400 | 952,742 | ||||||

| 1,983,885 | ||||||||

| OIL, GAS & CONSUMABLE FUELS—10.2% | ||||||||

| Canadian Natural Resources Ltd. (Canada) | 66,900 | 4,813,455 | ||||||

| ConocoPhillips | 13,750 | 702,212 | ||||||

| Devon Energy Corp. | 86,700 | 6,372,450 | ||||||

| EOG Resources, Inc. | 71,800 | 6,986,140 | ||||||

| OGX Petroleo e Gas Participacoes SA (Brazil) | 110,000 | 1,080,414 | ||||||

| 19,954,671 | ||||||||

24

MMA Praxis Core Stock Fund

Schedule of portfolio investments, continued

December 31, 2009

| SHARES | VALUE | |||||||

| COMMON STOCKS—96.7%, continued | ||||||||

| PAPER & FOREST PRODUCTS—1.1% | ||||||||

| Sino-Forest Corp.- ADR (Canada)(a)(b) | 3,400 | $ | 63,004 | |||||

| Sino-Forest Corp., Class A (Canada)(a) | 113,860 | 2,109,869 | ||||||

| 2,172,873 | ||||||||

| PERSONAL PRODUCTS—0.1% | ||||||||

| Natura Cosmeticos SA (Brazil) | 12,200 | 254,441 | ||||||

| PHARMACEUTICALS—6.4% | ||||||||

| Johnson & Johnson | 66,100 | 4,257,501 | ||||||

| Merck & Co., Inc. | 223,916 | 8,181,891 | ||||||

| 12,439,392 | ||||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT—1.3% | ||||||||

| Brookfield Asset Management, Inc., Class A (Canada) | 43,600 | 967,048 | ||||||

| Hang Lung Group Ltd. (Hong Kong) | 313,000 | 1,560,277 | ||||||

| 2,527,325 | ||||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—1.6% | ||||||||

| Texas Instruments, Inc. | 115,800 | 3,017,748 | ||||||

| SOFTWARE—2.6% | ||||||||

| Activision Blizzard, Inc. (a) | 81,500 | 905,465 | ||||||

| Microsoft Corp. | 135,600 | 4,134,444 | ||||||

| 5,039,909 | ||||||||

| SPECIALTY RETAIL—2.1% | ||||||||

| Bed Bath & Beyond, Inc. (a) | 63,500 | 2,453,005 | ||||||

| CarMax, Inc. (a) | 63,900 | 1,549,575 | ||||||

| 4,002,580 | ||||||||

| TRANSPORTATION INFRASTRUCTURE—1.3% | ||||||||

| China Merchants Holdings International Co. Ltd. (Hong Kong) | 636,175 | 2,071,790 | ||||||

| COSCO Pacific Ltd. (Bermuda) | 413,041 | 528,994 | ||||||

| 2,600,784 | ||||||||

| TOTAL COMMON STOCKS | 188,423,653 | |||||||

| COMMERCIAL PAPER—3.9% | ||||||||

| Three Pillars Funding Corp., 0.30%, 1/04/10(b) | 7,575,000 | 7,574,748 | ||||||

| CORPORATE BOND—0.6% | ||||||||

| AUTOMOBILES—0.6% | ||||||||

| Harley-Davidson, Inc., 15.00, 2/01/14(c) | 1,000,000 | 1,224,015 | ||||||

25

MMA Praxis Core Stock Fund

Schedule of portfolio investments, continued

December 31, 2009

| PRINCIPAL | ||||||||

| AMOUNT/ | ||||||||

| SHARES | VALUE | |||||||

| CORPORATE NOTES—1.5% | ||||||||

| DEVELOPMENT AUTHORITIES—1.5% | ||||||||

| MMA Community Development Investment, Inc., 1.10%, 12/31/11(d)+ | 1,016,000 | $ | 1,016,000 | |||||

| MMA Community Development Investment, Inc., 0.73%, 12/31/12(d)+ | 903,000 | 903,000 | ||||||

| MMA Community Development Investment, Inc., 1.10%, 12/31/13(d)+ | 1,016,000 | 1,016,000 | ||||||

| TOTAL CORPORATE NOTES | 2,935,000 | |||||||

| TOTAL INVESTMENTS (Cost* $189,916,692)—102.7% | $ | 200,157,416 | ||||||

| Net other assets (liabilities) — (2.7)% | (5,260,318 | |||||||

| NET ASSETS—100% | $ | 194,897,098 | ||||||

| + | Variable rate security. Rates presented are the rates in effect at December 31, 2009. |

| (a) | Non-income producing securities. |

| (b) | 144a security is restricted as to resale to institutional investors. These securities were deemed liquid under guidelines established by the Board of Trustees. At December 31, 2009, these securities were valued at $7,637,752 or 3.9% of net assets. |

| (c) | Security is illiquid. At December 31, 2009, these securities amounted to $1,224,015 or 0.62% of net assets. |

| (d) | Represents affiliated restricted security as to resale to shareholders and is not registered under the Securities Act of 1933. These securities have been deemed illiquid under guidelines established by the Board of Trustees: |

| Acquisition | |||

| Security | Yield | Shares | Date |

| MMA Community Development Investment, Inc. | 0.73% | 903,000 | 12/2009 |

| MMA Community Development Investment, Inc. | 1.10% | 1,016,000 | 12/2009 |

| MMA Community Development Investment, Inc. | 1.10% | 1,016,000 | 12/2009 |

At December 31, 2009, these securities had an aggregate market value of $2,935,000, representing 1.5% of net assets.

| * | Represents cost for financial reporting purposes. |

ADR – American Depositary Receipt.

plc – Public Liability Company.

Other Information:

The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in the accompanying Notes to Financial Statements.

| Valuation Inputs at Reporting Date: | ||||||||||||||||

| Description | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Investments at Value | ||||||||||||||||

| Common Stocks | $ | 188,423,653 | $ | — | $ | — | $ | 188,423,653 | ||||||||

| Commercial Paper | — | 7,574,748 | — | 7,574,748 | ||||||||||||

| Corporate Notes | — | — | 2,935,000 | 2,935,000 | ||||||||||||

| Corporate Bond | — | 1,224,015 | — | 1,224,015 | ||||||||||||

| Total Investments | $ | 188,423,653 | $ | 8,798,763 | $ | 2,935,000 | $ | 200,157,416 | ||||||||

Following is a reconciliation of Level 3 assets for which significant unobservable inputs for Investments in Securities were used to determine fair value for each Fund:

Core Stock Fund | ||||

| Balance as of December 31, 2008 | $ | 2,935,000 | ||

| Proceeds from Sales | (2,935,000 | ) | ||

| Purchases | 2,935,000 | |||

| Balance as of December 31, 2009 | $ | 2,935,000 | ||

See accompanying notes to financial statements.

26

| MMA Praxis Value Index Fund |

MMA Praxis Value Index Fund

Annual report to shareholders

Portfolio manager’s letter

The 26.47 percent return of the Standard & Poor’s 500 Index for 2009 will appear to be one of the better return years for the index when viewed in the fullness of history. But even this impressive return masks the 67.8 percent surge in equity prices that began on March 9 and continued unabated through the end of the year. A massive federal stimulus and the gradual realization that their worst fears were unfounded, led investors to bid stock prices higher in anticipation of a future economic recovery.

Early in the rally, the stocks that had fallen the hardest during the great credit crisis of 2008 had the highest returns. But as the year progressed, the benefits of a recovering economy and improving investor sentiment led to a widespread appreciation in prices. Still, the general level of equity prices remains well below market highs reached in late 2007.

The value style of investing trailed the growth style during the year. Still, the Fund’s A shares (NAV) returned 22.64 percent versus 19.54 percent for its benchmark, the MSCI Prime Market Value Index during the period. The Fund’s outperformance is primarily a result of its overweight to the financial industry that results from tighter screens on other sectors. The financial sector, whose returns lagged significantly in 2008, rebounded with gusto during the rally. The Fund’s positions in major banks, financial services companies, and corresponding underweight positions in major oil companies contributed to its outperformance.

Chad Horning, CFA®

MMA Praxis Value Index Fund Manager

27

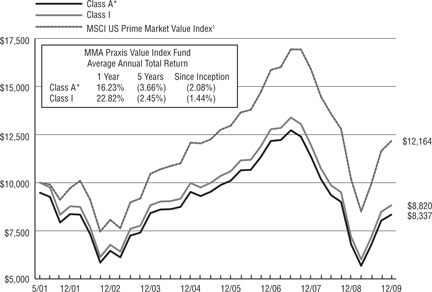

Performance review |

MMA Praxis Value Index Fund

Performance review

Average annual total returns as of 12/31/09

| Inception | Since | Expense Ratio** | |||||

| Date | 1 Year | 3 Year | 5 Year | Inception | Gross | Net | |

| Class A (No Load) | 5/1/01 | 22.64% | -11.84% | -2.62% | -1.47% | 1.27% | 1.27% |

| Class A* | 5/1/01 | 16.23% | -13.41% | -3.66% | -2.08% | ||

| Class I | 5/1/06 | 22.82% | -11.63% | -2.45% | -1.44% | 0.64% | 0.64% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit mmapraxis.com.

| * | Reflects maximum front-end sales charge of 5.25%. |

Class I Share of this Fund was not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Share since inception of 5/1/01 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

The total return set forth reflects certain expenses that were contractually or voluntarily reduced, reimbursed or paid by third party. In such instances, and without this activity, total return would have been lower.

| ** | Reflects the expense ratios as reported in the Prospectus dated May 1, 2009. Voluntary fee waivers were in effect through December 31, 2009 for Class A and Class I. |

28

MMA Praxis Value Index Fund

Performance review

Growth of $10,000 investment 5/1/01 to 12/31/09

This chart represents historical performance of a hypothetical investment of $10,000 in the Value Index Fund from 5/1/01 to 12/31/09, and represents the reinvestment of dividends and capital gains in the Fund.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit mmapraxis.com.

The total return set forth reflects certain expenses that were contractually or voluntarily reduced, reimbursed or paid by third party. In such instances, and without this activity, total return would have been lower.

| * | Reflects maximum front-end sales charge of 5.25%. |

Class I Shares of this Fund were not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Shares since inception of 5/1/01 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

| 1 | The MSCI US Prime Market Value Index represents the value companies of the MSCI US Prime Market 750 Index. (The MSCI US Prime Market 750 Index represents the universe of large and medium capitalization companies in the US equity market). The MSCI US Prime Market Value Index is a subset of the MSCI US Prime Market 750 Index. |

The above index is for illustrative purposes only and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The fund's performance reflects the deduction of these value-added services. An investor cannot invest directly in an index, although they can invest in its underlying securities.

29

| Schedule of portfolio investments |