Under the terms of our factoring agreement with GMAC Commercial Finance LLC, as amended, we may request advances from the factor of up to 80% of aggregate receivables purchased by the factor at an interest rate equal to the lower of the prime rate less 0.875% or the 30-day London Interbank Offered Rate plus 1.375%. The agreement, which has no specific expiration date and can be terminated by either party with sixty (60) days written notice after June 30, 2007, provides us with a $50 million credit facility with a $25 million sub-limit on the aggregate face amount of Letters of Credit. We also pay a fee that varies depending on the customer of between 0.15% and 0.25% of the gross invoice amount of each receivable purchased. We sell and assign a substantial portion of our receivables, principally without recourse, to the factor. As of December 31, 2007 and 2006, $272 and $260 of factored receivables, respectively, were sold by us with recourse. GMAC maintains a lien on all of our receivables and assumes the credit risk for all assigned accounts approved by them with certain restrictions.

Our Daniel M. Friedman Division had a factoring agreement with Wells Fargo Century that expired on June 30, 2007. Under the terms of the agreement, we were eligible to draw down 85% of our invoiced receivables at an interest rate equal to the prime rate. We paid a fee equal to 0.45% of the gross invoice amount of each receivable purchased. Wells Fargo Century maintained a lien on all of Daniel M. Friedman’s receivables and assumed the credit risk for all assigned accounts approved by them with certain restrictions. As of July 1, 2007, Daniel M. Friedman has been incorporated into the GMAC agreement.

The STEVE MADDEN and/or STEVE MADDEN plus Design trademarks and service marks have been registered in numerous International Classes in the United States (Int’l Cl. 25 for clothing and footwear; Int’l Cl. 18 for leather goods, such as handbags and wallets; Int’l Cl. 9 for eyewear; Int’l Cl. 14 for jewelry; Int’l Cl. 3 for cosmetics and fragrances; Int’l Cl. 20 for picture frames; Int’l Cl. 16 for paper goods; and Int’l Cl. 35 for retail store services). We also have pending trademark applications in the United States for the mark STEVE MADDEN and/or STEVE MADDEN (design) in numerous international classes (Class 14 for watches, Class 18 for bags and leather goods, and Class 26 for hair accessories).

We also have trademark registrations in the United States for the marks EYESHADOWS BY STEVE MADDEN (Int’l Cl. 9 for eyewear), ICE TEE (Int’l Cl. 25 for clothing and footwear), SHOE BIZ BY STEVE MADDEN (Int’l Cl. 25 for clothing and footwear; and Int’l Cl. 35 for retail store services) STEVEN M. (Int’l Class 25 for clothing and footwear); and STEVEN (Int’l Cl. 25 for clothing and footwear, Class 3 for cosmetics and fragrances, Class 14 for jewelry, Class 18 for leather goods, Class 26 for hair accessories, Class 35 for retail store services, and Class 9 for eyewear). We also own a registration for the mark SOHO COBBLER and SOHO COBBLER (design) in the U.S. in Class 25 for clothing.

We also have several pending applications in the U.S. for MADDEN in Class 18 for bags, Class 14 for jewelry, and Class 25 for clothing and footwear. We also have a registration in the U.S. for STEVEN BY STEVE MADDEN in Class 25 (belts), and pending applications in the U.S. for STEVEN BY STEVE MADDEN or STEVEN BY STEVE MADDEN (design) in Classes 9 (cd cases and cell phone cases), 14 (watches and clocks), 18 (bags and small leather goods) 24 (bedding), and 25 (clothing and footwear), 28 (video game cases), and for MADDEN BY STEVE MADDEN in Class 14 for jewelry and watches, and Class 18 for bags.

Additionally, we have trademark and service mark registrations and applications in the United States for various marks, including STEVE MADDEN LUXE registered in Class 25 for clothing and footwear and pending in Class 14 for watches and clocks; RULE STEVE MADDEN pending (in Class 3 for perfume and cosmetics, Class 4 for candles, Class 6 for key rings and key chains, Class 9 for eyewear and CDs, Class 11 for lamps, Class 14 for jewelry, Class 16 for stationery and notebooks, Class 18 for bags, Class 20 for furniture, Class 21 for housewares, Class 24 for bedding, Class 25 for clothing and footwear, Class 26 for hair accessories, Class 27 for carpets and rugs, Class 28 for toys and games, Class 32 for light beverages, and Class 35 for retail store services); FIX, FIX (design), and STEVE MADDEN’S FIX pending in Class 25 (clothing and footwear); LITTLE MISS COMFORT pending in Class 18 (bags) and 25 (clothing); MADDEN ACTIVE, MADDEN BOYZ, MADDEN GIRL, MADDEN GIRLZ, MADDEN KIDZ, MADDEN NEW YORK, and MADDEN SPORT all pending in Class 25 (clothing and footwear); and NATURAL COMFORT registered in Class 25 (footwear).

We further own registrations for the STEVE MADDEN and/or STEVE MADDEN plus Design trademarks and service marks in various International Classes in Argentina, Armenia, Aruba, Australia, Bahrain, Belize, Brazil, Canada, Chile, China, Colombia, El Salvador, Guatemala, Hong Kong, Israel, Italy, Japan, Korea, Lebanon, Mexico, Netherland Antilles, New Zealand, the Netherlands, Nicaragua, Norway, Oman, Panama, the Philippines, Qatar, Russia, Saudi Arabia, Singapore, South Africa, Taiwan, Thailand, Turkey, the United Arab Emirates, Uzbekistan, the European Union, and the Benelux countries and have pending applications for registration of the STEVE MADDEN and/or STEVE MADDEN plus Design trademarks and service marks in Aruba, Azerbaijan, Bahamas, Belarus, Canada, China, Costa Rica, Ecuador, Egypt, Estonia, Georgia, Guatemala, Honduras, India, Indonesia, Jordan, Kazakhstan, Korea, Kuwait, Kyrgyzstan, Latvia, Lithuania, Moldova, Oman, Paraguay, Peru, the Philippines, Saudi Arabia, Tajikistan, Turkmenistan, Ukraine, Venezuela, and the United Arab Emirates.

Additionally, we own registrations for the STEVEN trademark and service mark in various International Classes in Australia, Bahrain, Belize, China, the Dominican Republic, El Salvador, Hong Kong, Israel, Japan, Lebanon, Malaysia, New Zealand, Netherland Antilles, Norway, the Philippines, Qatar, Russia, Saudi Arabia, South Africa, Thailand, Taiwan, Turkey, and the United Arab Emirates and have pending applications for registration of the STEVEN trademark and service mark in China, Columbia, Costa Rica, Ecuador, Egypt, the European Union, Guatemala, India, Indonesia, Israel, Italy, Jordan, Korea, Kuwait, Malaysia, Nicaragua, Oman, Philippines, Taiwan, Thailand, Turkey, Taiwan, and Venezuela.

We further own registrations for the “torch stripe” design in Class 25 in the European Union and Panama, and China.

We further own registrations for the mark STEVEN BY STEVE MADDEN in various international classes in the European Union, Hong Kong, Panama, and Taiwan, and have pending applications for the mark STEVEN BY STEVE MADDEN in various international classes in Aruba, Canada, China, Egypt, India, Israel, Korea, and Venezuela.

We further have pending applications for the mark STEVE MADDEN’S FIX* in international class 25 in China, the European Union, Mexico, and Turkey.

We further have pending applications for the mark MADDEN GIRL in international class 25 in Egypt, India, Kuwait, and Saudi Arabia.

8

We further have pending applications for the mark NATURAL COMFORT in various international classes in Egypt, India, Kuwait, and Saudi Arabia.

We further own registrations for the mark SM NEW YORK and/or SM NEW YORK in International Class 25 (clothing and footwear) in Aruba, Belize, the Dominican Republic, Ecuador, El Salvador, Hong Kong, Guatemala, India, Netherland Antilles, and New Zealand, Nicaragua, Panama, and has pending applications for registration of the SM NEW YORK mark in International Class 25 (clothing and footwear) in Australia, Columbia, Costa Rica, Indonesia, Saudi Arabia, South Africa, and Venezuela.

Additionally, we, through our Diva Acquisition Corp. and Diva International, Inc. subsidiaries, own registrations for the DAVID AARON trademark in the United States in Class 25 for clothing Class 18 for handbags and wallets, and Class 35 for retail store services, and in Australia, Canada, the European Union, Hong Kong, Japan, Panama and South Africa in some or all of Classes 3, 18, and 25, and for our D. AARON trademark in Class 25 in Spain. Also, we own registrations for our DAVID AARON trademark in International Class 3 for perfume and cosmetics; International Class 9 for eyewear; International Class 14 for jewelry; International Class 16 for paper goods; International Class 18 for bags; International Class 24 for bed and bath products; International Class 25 for clothing and footwear and International Class 26 hair accessories in Korea.

We, through our Stevies, Inc. subsidiary, also own various registrations for the STEVIES and /or STEVIES plus Design trademark and service mark in a number of International Classes in the United States (Int’l Class 25 for clothing and footwear; Int’l Class 18 for leather goods, such as handbags and wallets; International Class 35 for retail store services; International Class 14 for jewelry; International Class 28 for toys; Int’l Class 16 for magazines; Int’l Class 3 for perfume and cosmetics, Int’l Class 9 for CDs and eyewear; Int’l Cl. 27 for rugs and carpets; and Int’l Class 26 for hair accessories), and for STEVIES BY STEVE MADDEN in Class 14 for jewelry, Class 9 for eyewear, Class 3 for perfume and cosmetics, Class 25 for clothing and footwear, Class 28 for toys and games, Class 35 for retail services, Class 16 for magazines, Class 18 for bags.

Additionally, Stevies, Inc. has pending trademark and service mark applications and/or existing registrations for the STEVIES and STEVIES plus Design marks in various International Classes in Aruba, Argentina, Australia, Bahrain, Brazil, Canada, China, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, Egypt, El Salvador, European Union, Guatemala, Hong Kong, Honduras, Indonesia, India, Israel, Japan, Korea, Kuwait, Lebanon, Malaysia, Mexico, Netherland Antilles, Nicaragua, New Zealand, Oman, Panama, Peru, Qatar, Saudi Arabia, Singapore, South Africa, Taiwan, Thailand, Turkey, the United Arab Emirates and Venezuela.

We believe that our trademarks have a significant value and are important to the marketing of our products. There can be no assurance, however, that we will be able to effectively obtain rights to our marks throughout all of the countries of the world. Moreover, no assurance can be given that others will not assert rights in, or ownership of, our trademarks and other proprietary rights or that we will be able to successfully resolve such conflicts. Our failure to protect such rights from unlawful and improper appropriation may have a material adverse effect on our business and financial condition, results of operations and liquidity.

Employees

On February 5, 2008, we employed approximately one thousand five hundred and ten (1,510) employees, of whom approximately seven hundred forty (740) work on a full-time basis and approximately seven hundred seventy (770) work on a part-time basis, most of whom work in the Retail Division. Our management considers relations with our employees to be good.

9

Seasonality

Historically, our merchandising businesses have experienced holiday retail seasonality. In addition to seasonal fluctuations, our operating results fluctuate quarter to quarter as a result of the timing of holidays, weather, the timing of larger shipments of footwear, market acceptance of our products, the mix, pricing and presentation of the products offered and sold, the hiring and training of additional personnel, inventory write downs for obsolescence, the cost of materials, the product mix between wholesale, retail and licensing businesses, the incurrence of other operating costs and factors beyond our control, such as general economic conditions and actions of competitors.

Backlog

We had unfilled wholesale customer orders of $113.8 million and $103.7 million, as of February 21, 2008 and 2007, respectively. Our backlog at a particular time is affected by a number of factors, including seasonality, timing of market weeks and wholesale customer purchases of our core basic products through our open stock program. Accordingly, a comparison of backlog from period to period may not be indicative of eventual shipments.

You should carefully consider the risks and uncertainties we describe below and the other information in this Annual Report or Form 10-K incorporated by reference herein before deciding to invest in, sell or retain shares of our common stock. These are not the only risks and uncertainties that we face. Additional risks and uncertainties that we do not currently know about or that we currently believe are immaterial, or that we have not predicted, may also harm our business operations or adversely affect us. If any of these risks or uncertainties actually occurs, our business, financial condition, results of operations and liquidity could be materially harmed.

Fashion Industry Risks. Our success will depend in significant part upon our ability to anticipate and respond to product and fashion trends as well as to anticipate, gauge and react to changing consumer demands in a timely manner. There can be no assurance that our products will correspond to the changes in taste and demand or that we will be able to successfully market products that respond to such trends. If we misjudge the market for our products, we may be faced with significant excess inventories for some products and missed opportunities for others. In addition, misjudgments in merchandise selection could adversely affect our image with our customers resulting in lower sales and increased markdown allowances for customers which could have a material adverse effect on our business, financial condition, results of operations and liquidity.

The industry in which we operate is cyclical, with purchases tending to decline during recessionary periods when disposable income is low. Purchases of contemporary shoes and accessories tend to decline during recessionary periods and also may decline at other times. There can be no assurance that we will be able to grow or even maintain our current level of revenues and earnings, or remain profitable in the future. A recession in the national or regional economies or uncertainties regarding future economic prospects, among other things, could affect consumer-spending habits and have a material adverse effect on our business, financial condition, results of operations and liquidity.

In recent years, the retail industry has experienced consolidation and other ownership changes. In the future, retailers in the United States and in foreign markets may further consolidate, undergo restructurings or reorganizations, or realign their affiliations, any of which could decrease the number of storesthat carry our products or increase the ownership concentration within the retail industry. While such changes in the retail industry to date have not had a material adverse effect on our business or financial condition, results of operations and liquidity, there can be no assurance as to the future effect of any such changes.

10

Inventory Management. The fashion-oriented nature of our products and the rapid changes in customer preferences leave us vulnerable to an increased risk of inventory obsolescence. Thus, our ability to manage our inventories properly is an important factor in our operations. Inventory shortages can adversely affect the timing of shipments to customers and diminish sales and brand loyalty. Conversely, excess inventories can result in lower gross margins due to the excessive discounts and markdowns that might be necessary to reduce inventory levels. Our inability to effectively manage our inventory could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Dependence upon Customers and Risks Related to Extending Credit to Customers. Our customers consist principally of department stores and specialty stores, including shoe boutiques. Certain of our department store customers, including some under common ownership, account for significant portions of our wholesale business.

We generally enter into a number of purchase order commitments with our customers for each of our lines every season and do not enter into long-term agreements with any of our customers. Therefore, a decision by a significant customer of ours, whether motivated by competitive conditions, financial difficulties or otherwise, to decrease the amount of merchandise purchased from us or to change its manner of doing business could have a material adverse effect on our business, financial condition, results of operations and liquidity. We sell our products primarily to retail stores across the United States and extend credit based on an evaluation of each customer’s financial condition, usually without collateral. While various retailers, including some of our customers, have experienced financial difficulties in the past few years which increased the risk of extending credit to such retailers, our losses due to bad debts have been limited. Pursuant to the terms of our factoring agreement, GMAC currently assumes the credit risk related to approximately 84% of our accounts receivable. However, financial difficulties of a customer could cause us to curtail business with such customer or require us to assume more credit risk relating to such customer’s accounts receivable.

Impact of Foreign Manufacturers. During the year ended December 31, 2007, approximately 99% of our products were purchased through arrangements with a number of foreign manufacturers, primarily from China, Brazil, Italy and Spain.

Risks inherent in foreign operations include work stoppages, transportation delays and interruptions, changes in social, political and economic conditions which could result in the disruption of trade from the countries in which our manufacturers or suppliers are located, the imposition of additional regulations relating to imports, the imposition of additional duties, taxes and other charges on imports, significant fluctuations of the value of the dollar against foreign currencies, or restrictions on the transfer of funds, any of which could have a material adverse effect on our business, financial condition, results of operations and liquidity. We do not believe that any such economic or political condition will materially affect our ability to purchase products, since a variety of materials and alternative sources are available. We cannot be certain, however, that we will be able to identify such alternative sources without delay (if ever) or without greater cost to us. Our inability to identify and secure alternative sources of supply in this situation could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Our imported products are also subject to United States custom duties. The United States and the countries in which our products are produced or sold, from time to time, impose new quotas, duties, tariffs, or other restrictions, or may adversely adjust prevailing quota, duty or tariff levels, any of which could have a material adverse effect on our business, financial condition, results of operations and liquidity.

11

Possible Adverse Impact of Unaffiliated Manufacturers’ Inability to Manufacture in a Timely Manner, Meet Quality Standards or to Use Acceptable Labor Practices. As is common in the footwear industry, we contract for the manufacture of 99% of our products to our specifications through foreign manufacturers. We do not own or operate any manufacturing facilities and we are therefore dependent upon independent third parties for the manufacture of all of our products. Our products are manufactured to our specifications by both domestic and international manufacturers. The inability of a manufacturer to ship orders of our products in a timely manner or to meet our quality standards could cause us to miss the delivery date requirements of our customers for those items, which could result in cancellation of orders, refusal to accept deliveries or a reduction in purchase prices, any of which could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Although we enter into a number of purchase order commitments each season specifying a time frame for delivery, method of payment, design and quality specifications and other standard industry provisions, we do not have long-term contracts with any manufacturer. As a consequence, any of these manufacturing relationships may be terminated, by either party, at any time. Although we believe that other facilities are available for the manufacture of our products, both within and outside of the United States, there can be no assurance that such facilities would be available to us on an immediate basis, if at all, or that the costs charged to us by such manufacturers would not be greater than those presently paid.

We do not control our licensing partners or independent manufacturers or their labor practices. The violation of labor or other laws by an independent manufacturer of ours or by one of our licensing partners, or the divergence of an independent manufacturer’s or licensing partner’s labor practices from those generally accepted as ethical in the United States, could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Intense Industry Competition. The fashion footwear industry is highly competitive and barriers to entry are low. Our competitors include specialty companies as well as companies with diversified product lines. The recent market growth in the sales of fashion footwear has encouraged the entry of many new competitors and increased competition from established companies. Most of these competitors, including Nine West, Skechers, Kenneth Cole, Nike and Guess may have significantly greater financial and other resources than us and there can be no assurance that we will be able to compete successfully with other fashion footwear companies. Increased competition could result in pricing pressures, increased marketing expenditures and loss of market share, and could have a material adverse effect on our business, financial condition, results of operations and liquidity. We believe effective advertising and marketing, branding of the Steve Madden name, fashionable styling, high quality and value are the most important competitive factors and we plan to continually employ these elements as we develop our products. Our inability to effectively advertise and market our products could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Expansion of Retail Business. Our continued growth depends to a significant degree on further developing the Steve Madden®, Stevies®, Steven®, Madden Girl, Steve Madden Mens, Natural Comfort and Candie’s® brands, creating new product categories and businesses and operating company-owned Steve Madden® and Steven® stores on a profitable basis. During the year ended December 31, 2007, we opened seven (7) Steve Madden® retail stores and have plans to open three (3) additional stores in the year ending December 31, 2008. Our expansion plan includes the opening of stores in new geographic markets as well as strengthening existing markets. New markets have in the past presented, and will continue to present, competitive and merchandising challenges that are different from those faced by us in our existing markets. There can be no assurance that we will be able to open new stores, and if opened, that such new stores will be able to achieve sales and profitability levels consistent with management’s expectations. Our retail expansion is dependent on a number of factors, including our ability to locate and obtain favorable store sites, the performance of our wholesale and retail operations, and our ability to manage such expansion and hire and train personnel. Past comparable store sales results may not be indicative of future results, and there can be no assurance that our comparable store sales results can be maintained or will increase in the future. In addition, there can be no assurance that our strategies to increase other sources of revenue, which may include expansion of our licensing activities, will be successful or that our overall sales or profitability will increase or not be adversely affected as a result of the implementation of such retail strategies.

12

Management of Growth. Our operations have increased and will continue to increase demand on our managerial, operational and administrative resources. We have recently invested significant resources in, amongst other things, our management information systems and hiring and training new personnel. However, in order to manage currently anticipated levels of future demand, we may be required to, among other things, expand our distribution facilities, establish relationships with new manufacturers to produce our product, and continue to expand and improve our financial, management and operating systems. There can be no assurance that we will be able to manage future growth effectively and a failure to do so could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Seasonal and Quarterly Fluctuations. Our results may fluctuate quarter to quarter as a result of the timing of holidays, weather, the timing of larger shipments of footwear, market acceptance of our products, the mix, pricing and presentation of the products offered and sold, the hiring and training of additional personnel, inventory write downs for obsolescence, the cost of materials, the product mix between wholesale, retail and licensing businesses, the incurrence of other operating costs and factors beyond our control, such as general economic conditions and actions of competitors. In addition, we expect that our sales and operating results may be significantly impacted by the opening of new retail stores and the introduction of new products. Accordingly, the results of operations in any quarter will not necessarily be indicative of the results that may be achieved for a full fiscal year or any future quarter.

Trademark and Service Mark Protection. We believe that our trademarks and service marks and other proprietary rights are important to our success and our competitive position. Accordingly, we devote substantial resources to the establishment and protection of our trademarks on a worldwide basis. Nevertheless, there can be no assurance that the actions taken by us to establish and protect our trademarks and other proprietary rights will be adequate to prevent imitation of our products by others or to prevent others from seeking to block sales of our products on the basis that they violate the trademarks and proprietary rights of others. Moreover, no assurance can be given that others will not assert rights in, or ownership of, trademarks and other proprietary rights of ours or that we will be able to successfully resolve such conflicts. In addition, the laws of certain foreign countries may not protect proprietary rights to the same extent as do the laws of the United States. Our failure to establish and then protect such proprietary rights from unlawful and improper utilization could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Foreign Currency Fluctuations. We make approximately 99% of our purchases in U.S. dollars. However, we source substantially all of our products overseas and, as such, the cost of these products may be affected by changes in the value of the relevant currencies. Changes in currency exchange rates may also affect the relative prices at which we and our foreign competitors sell products in the same market. There can be no assurance that foreign currency fluctuations will not have a material adverse effect on our business, financial condition, results of operations and liquidity.

13

Outstanding Options. As of March 6, 2008, there were outstanding options to purchase an aggregate of approximately 559,000 shares of our common stock. Holders of such options are likely to exercise them when, in all likelihood, the market price of our stock is significantly higher than the exercise price of the options. Further, while options are outstanding, they may adversely affect the terms on which we could obtain additional capital, if required.

Economic and Political Risks. The present economic condition in the United States and concern about uncertainties could significantly reduce the disposable income available to our customers for the purchase of our products. In addition, current unstable political conditions, including the potential or actual conflicts in Iraq, North Korea or elsewhere, or the continuation or escalation of terrorism, could have a material adverse effect on our business, financial condition, results of operations and liquidity.

| |

ITEM 1B | UNRESOLVED STAFF COMMENTS |

None.

We maintain approximately 40,000 square feet for our executive offices and sample production facilities at 52-16 Barnett Avenue, Long Island City, NY 11104. The lease for our headquarters expires on June 30, 2013.

The Steve Madden showroom is located at 1370 Avenue of the Americas, New York, NY. All of our brands are displayed for sale from this 9,917 square foot space. The lease for our showroom expires on February 28, 2013.

Daniel M. Friedman maintains approximately 20,000 square feet for its offices and showroom space at 10 West 33rd Street, New York, NY. The lease expires on December 31, 2014.

We maintain approximately 7,200 square feet as a storage facility at 25-15 Borough Place, Woodside, NY. The lease for this space expires on October 31, 2008 and can be extended, at our option, through October 31, 2010.

We maintain approximately 1,400 square feet as a design facility in Boston, Massachusetts. The lease for this space expires on February 28, 2010.

We also maintain an 807 square foot showroom located at Fashion Center Dallas in the World Trade Center, Dallas, Texas. The lease for this showroom expires on April 30, 2010. We also currently engage three independent distributors to warehouse and distribute our products.

All of our retail stores are leased pursuant to leases that, under their original term, extend for an average of ten years in length. A majority of the leases include clauses that provide for contingent rental payments if gross sales exceed certain targets. In addition, a majority of the leases enable us and/or the landlord to terminate the lease in the event that our gross sales do not achieve certain minimum levels during a prescribed period. Many of the leases contain rent escalation clauses to compensate for increases in operating costs and real estate taxes.

14

The current terms of our retail store leases expire as follows:

| | | | |

Years Lease Terms Expire | | Number of Stores | |

|

|

|

|

2008 | | 6 | | |

2009 | | 9 | | |

2010 | | 7 | | |

2011 | | 13 | | |

2012 | | 9 | | |

2013 | | 11 | | |

2014 | | 7 | | |

2015 | | 11 | | |

2016 | | 6 | | |

2017 | | 14 | | |

2018 | | 7 | | |

2019 | | 1 | | |

Except as set forth below, no material legal proceedings are pending to which we or any of our property is subject.

On August 10, 2005, the U.S. Customs Department (“Customs”) issued a report that asserts that certain commissions that we treated as “buying agents’ commissions” (which are non-dutiable) should be treated as “selling agents’ commissions” and hence are dutiable. In the report, Customs estimates that we had underpaid duties during the calendar years of 1998 through 2004 in the amount of $1million. As of June 30, 2006, based on discussions with legal counsel, we believed that the liability in this case, including interest, was not likely to exceed $1.5 million. Accordingly, as of December 31, 2006, we recorded a reserve of $1.5 million. In September of 2007, Customs notified us that it had finalized its assessment of the underpaid duties to be $1.4 million. Pursuant to this assessment, management, with the advice of legal counsel, has re-evaluated the liability in the case, including interest and penalties, and believes that it is not likely to exceed $2.7 million. We increased our reserve by $1.2 million in the third quarter of 2007. Such reserve is subject to change to reflect the status of this matter.

We have been named as a defendant in certain other lawsuits in the normal course of business. In the opinion of management, after consulting with legal counsel, the liabilities, if any, resulting from these matters should not have a material effect on our financial position or results of operations. It is the policy of management to disclose the amount or range of reasonably possible losses in excess of recorded amounts.

| |

ITEM 4 | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted to a vote of the holders of our common stock during the last quarter of our fiscal year ended December 31, 2007.

15

PART II

| |

ITEM 5 | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our shares of common stock have traded on The NASDAQ Global Select Market since August 1, 2006 and were traded on The NASDAQ National Market prior to that date. The following table sets forth the range of high and low closing sales prices for our common stock during each fiscal quarter during the two-year period ended December 31, 2007 as reported by The NASDAQ Global Select and The NASDAQ National Market. The trading volume of our securities fluctuates and may be limited during certain periods. As a result, the liquidity of an investment in our securities may be adversely affected.

| | | | | | | | | | | | | | | | |

Common Stock |

|

| | High | | Low | | | | | High | | Low | |

| |

| |

| | | | |

| |

| |

2007 | | | | | | | | | 2006 | | | | | | | |

Quarter ended March 31, 2007 | | | 37.00 | | | 28.12 | | | Quarter ended March 31, 2006 | | | 24.53 | | | 18.63 | |

Quarter ended June 30, 2007 | | | 33.51 | | | 29.49 | | | Quarter ended June 30, 2006 | | | 37.17 | | | 23.20 | |

Quarter ended September 30, 2007 | | | 32.96 | | | 18.11 | | | Quarter ended September 30, 2006 | | | 40.69 | | | 26.59 | |

Quarter ended December 31, 2007 | | | 24.01 | | | 17.50 | | | Quarter ended December 31, 2006 | | | 44.70 | | | 33.99 | |

As of March 6, 2008, there were 20,120,983 shares of common stock outstanding and 86 holders of record.

Equity Compensation Plans. Information regarding our equity compensation plans as of December 31, 2007 is disclosed in Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Issuer Repurchases of Equity Securities.We did not repurchase any shares of common stock during the fourth quarter of fiscal 2007. In February and August of 2007, our Board of Directors authorized increases of our previously announced share repurchase program of $30 million and $37 million, respectively. At December 31, 2007, an aggregate of $46 million remained authorized to repurchase our Common Stock. The program has no set expiration or termination date.

Pursuant to an agreement reached on February 2, 2005 with an 8% shareholder, we agreed to commit $25 million during the twelve months ended January 31, 2006 and $10 million during the twelve months ended January 31, 2007 to a combination of share repurchases and/or dividends, such programs to be implemented at such time and such manner as determined by the board of directors in its sole discretion. As of January 31, 2007, we satisfied this agreement by the repurchase of 909,000 shares for $14.7 million and the payment of dividends in the amount of $34.9 million.

16

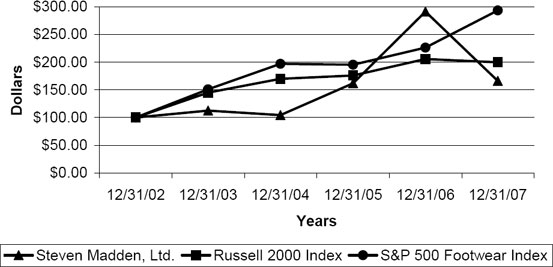

Performance Graph. The following graph compares the yearly percentage change in the cumulative total stockholder return on our common stock during the period beginning on December 31, 2002 and ending on December 31, 2007 with the cumulative total return on the Russell 2000 Index and the S&P 500 Footwear Index. The comparison assumes that $100 was invested on December 31, 2002 in our common stock and in the foregoing indices and assumes the reinvestment of dividends.

| | | | | | | | | | | | | | | | | | | |

| | 12/31/2002 | | 12/31/2003 | | 12/31/2004 | | 12/31/2005 | | 12/31/2006 | | 12/31/2007 | |

| |

| |

| |

| |

| |

| |

| |

Steven Madden, Ltd. | | $ | 100.00 | | $ | 112.89 | | $ | 104.37 | | $ | 161.76 | | $ | 291.28 | | $ | 166.02 | |

Russell 2000 Index | | $ | 100.00 | | $ | 145.37 | | $ | 170.08 | | $ | 175.73 | | $ | 205.61 | | $ | 199.96 | |

S&P 500 Footwear Index | | $ | 100.00 | | $ | 151.33 | | $ | 196.87 | | $ | 195.74 | | $ | 226.36 | | $ | 293.67 | |

| | | | | | | | | | | | | | | | | | | |

17

| |

ITEM 6 | SELECTED FINANCIAL DATA |

The following selected financial data has been derived from our audited Consolidated Financial Statements. The Income Statement Data relating to 2007, 2006 and 2005, and the Balance Sheet Data as of December 31, 2007 and 2006 should be read in conjunction with our audited Consolidated Financial Statements and notes thereto appearing elsewhere herein.

| | | | | | | | | | | | | | | | |

| | Year Ended December 31, | |

| |

| |

| | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

| |

| |

| |

| |

| |

| |

INCOME STATEMENT DATA: | | | | | | | | | | | | | | | | |

Net sales | | $ | 431,050,000 | | $ | 475,163,000 | | $ | 375,786,000 | | $ | 338,144,000 | | $ | 324,204,000 | |

Cost of sales | | | 257,646,000 | | | 276,734,000 | | | 236,631,000 | | | 218,601,000 | | | 201,487,000 | |

Gross profit | | | 173,404,000 | | | 198,429,000 | | | 139,155,000 | | | 119,543,000 | | | 122,717,000 | |

Commissions and licensing fee - net | | | 18,351,000 | | | 14,246,000 | | | 7,119,000 | | | 4,588,000 | | | 5,742,000 | |

Operating expenses | | | (138,841,000 | ) | | (134,377,000 | ) | | (114,185,000 | ) | | (105,150,000 | ) | | (94,833,000 | ) |

Impairment of goodwill | | | — | | | — | | | (519,000 | ) | | — | | | — | |

Income from operations | | | 52,914,000 | | | 78,298,000 | | | 31,570,000 | | | 18,981,000 | | | 33,626,000 | |

Interest income | | | 3,876,000 | | | 3,703,000 | | | 2,554,000 | | | 2,009,000 | | | 1,611,000 | |

Interest expense | | | (65,000 | ) | | (100,000 | ) | | (164,000 | ) | | (68,000 | ) | | (54,000 | ) |

Gain (loss) on sale of marketable securities | | | (589,000 | ) | | (967,000 | ) | | (500,000 | ) | | 32,000 | | | 136,000 | |

Income before provision for income taxes | | | 56,136,000 | | | 80,934,000 | | | 33,460,000 | | | 20,954,000 | | | 35,319,000 | |

Provision for income taxes | | | 20,446,000 | | | 34,684,000 | | | 14,260,000 | | | 8,679,000 | | | 14,865,000 | |

Net Income | | $ | 35,690,000 | | $ | 46,250,000 | | $ | 19,200,000 | | $ | 12,275,000 | | $ | 20,454,000 | |

Basic income per share | | $ | 1.73 | | $ | 2.21 | | $ | 0.95 | | $ | 0.62 | | $ | 1.05 | |

Diluted income per share | | $ | 1.68 | | $ | 2.09 | | $ | 0.92 | | $ | 0.58 | | $ | 0.96 | |

Basic weighted average shares of common stock | | | 20,647,181 | | | 20,905,673 | | | 20,111,576 | | | 19,723,304 | | | 19,477,898 | |

Effect of potential shares of common stock from exercise of options | | | 645,010 | | | 1,195,394 | | | 806,487 | | | 1,611,120 | | | 1,729,869 | |

Diluted weighted average shares of common stock outstanding | | | 21,292,191 | | | 22,101,067 | | | 20,918,063 | | | 21,334,424 | | | 21,207,767 | |

| | | | | | | | | | | | | | | | |

| | At December 31, | |

| |

| |

| | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

| |

| |

| |

| |

| |

| |

BALANCE SHEET DATA: | | | | | | | | | | | | | | | | |

Total assets | | $ | 266,521,000 | | $ | 251,392,000 | | $ | 211,728,000 | | $ | 186,430,000 | | $ | 177,870,000 | |

Working capital | | | 121,138,000 | | | 151,711,000 | | | 114,066,000 | | | 101,417,000 | | | 105,140,000 | |

Noncurrent liabilities | | | 3,470,000 | | | 3,136,000 | | | 2,757,000 | | | 2,088,000 | | | 1,828,000 | |

Stockholders’ equity | | $ | 215,334,000 | | $ | 211,924,000 | | $ | 182,065,000 | | $ | 164,665,000 | | $ | 159,187,000 | |

18

| |

ITEM 7 | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion of our financial condition and results of operations should be read in conjunction with the audited Consolidated Financial Statements and Notes thereto appearing elsewhere in this document.

Statements in this “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this document as well as statements made in press releases and oral statements that may be made by us or our officers, directors or employees acting on our behalf that are not statements of historical or current fact constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks, uncertainties and other unknown factors that could cause our actual results to be materially different from the historical results or from any future results expressed or implied by such forward-looking statements. In addition to statements which explicitly describe such risks and uncertainties, readers are urged to consider statements labeled with the terms “believes,” “belief,” “expects,” “intends,” “anticipates,” “projects” or “plans” and statements in the future tense to be uncertain forward-looking statements. The forward-looking statements contained herein are also subject generally to risks set forth in “Item 1A-A Risk Factors” and to other risks and uncertainties that are described from time to time in our reports and registration statements filed with the Securities and Exchange Commission.

Overview

($ in thousands, except retail sales data per square foot, share and earnings per share data)

Steven Madden, Ltd. (and its subsidiaries) designs, sources, markets and retails fashion-forward footwear for women, men and children. In addition, we design, source, market and retail name brand and private label fashion handbags and accessories through our Daniel M. Friedman Division. We distribute products through our retail stores, our e-commerce website, department and specialty stores throughout the United States and through special distribution arrangements in Canada, Europe, Central and South America, Australia and Asia. Our product line includes a broad range of updated styles which are designed to establish or capitalize on market trends, complemented by core products. We have established a reputation for our creative designs, popular styles and quality products at affordable price points.

The year 2007 proved to be a challenging year for the Company. The absence of fashion trends in the marketplace and the lack of big items that would drive significant sales volume resulted in a decrease in sales across several of our divisions. The weakening economy also adversely affected sales volume. In addition, net sales for the year ended December 31, 2006 included approximately $15,251 in net sales from Rule, l.e.i. and Jump, three brands that were discontinued late in 2006. For the year ended December 31, 2007, consolidated net sales decreased to $431,050 compared to $475,163 in the prior year. Gross margin in 2007 decreased to 40.2% compared to 41.8% in 2006. Including a one-time benefit of $2,498 resulting from tax savings related to prior periods and a one-time charge of $1,208 ($737 net of tax effect) related to the provision for prior years’ custom duties, net income for the year was $35,690 compared to $46,250 last year. Including a one-time benefit of $0.12 per share resulting from the above mentioned tax savings offset by a one-time charge of $0.03 per share related to the provision for prior years’ customs duties, diluted EPS for 2007 was $1.68 per share on 21,292,000 diluted weighted average shares outstanding compared to $2.09 per share on 22,101,000 diluted weighted average shares outstanding last year.

The recent expansion and growth of our international business, as well as the increase in private label business, resulted in an increase in the commission and licensing income. For the year ended December 31, 2007, income from operations in this segment increased to $14,674 from $11,321 in the prior year.

We have pursued a number of initiatives to enhance gross margins such as reducing freight costs, closeouts, store-to-store transfers and inventory shrinkage combined with better inventory controls. As a result, the gross margin in the Retail Division has increased to 56.8% in 2007 from 54.0% in 2006. This increase in gross margin was achieved despite the decrease in comparative sales results. Same store sales (sales of those stores, including the e-commerce website, that were in operation throughout all of 2007 and 2006) decreased 7.6%. Sales per square foot declined to $655 in 2007 compared to sales per square foot of $719 achieved in 2006.

19

A recent growth in our New York based income, combined with revisions in state and local tax law, prompted us to re-evaluate our tax filing strategies. We have elected to file our New York State and New York City tax returns on a combined basis which maximized the tax benefits provided by recent changes in New York State allocation regulations. We filed combined returns in 2006 and we were able to file amended New York State and New York City returns for 2003 through 2005 resulting in an additional one-time tax benefit in 2007. The election to file combined New York State and City returns in concert with the one-time benefit of filing past years’ amended returns has reduced our effective tax rate to 36.4% in 2007 from 42.9% in 2006. We anticipate that our effective tax rate in 2008 will be approximately 39%.

Pursuant to developments in the case with U.S. Customs, we have, in conjunction with legal counsel’s advice, increased the provision for the liability in the case from the $1,500 previously recorded to $2,700. Accordingly, an additional provision of $1,208 was made during the year ended December 31, 2007.

Our inventory turnover increased to 7.4 times in 2007 from 7.2 in 2006, because of our ability to manage inventory levels during a period of decreasing sales volume. Our accounts receivable average collection days improved to 58 days as of December 31, 2007 from 59 days on December 31, 2006. As of December 31, 2007, we had $109,857 in cash, cash equivalents and marketable securities, no short- or long-term debt, and total stockholders’ equity of $215,334. Working capital decreased to $121,138 as of December 31, 2007, compared to $151,711 on December 31, 2006, primarily due to our purchase during 2007 of $50,094 of our common stock for treasury. During the year ended December 31, 2007, net cash provided by operating activities increased to $59,907 as compared to $43,408 in the same period last year.

In line with prior commitments to enhance shareholders value, on February 19, 2008, we announced a tender offer to purchase up to 2,600,000 shares of our common stock at a price not greater than $20.00 nor less than $16.50 per share. As of December 31, 2007, there were 20,117,983 shares of our common stock issued and outstanding, not including 5,662,055 of our issued shares held in treasury. The 2,600,000 shares that we are offering to purchase represent approximately 13% of the total number of issued shares. We anticipate that we will pay for the shares tendered in the offer from our available cash.

20

The following tables set forth information on operations for the periods indicated:

| | | | | | | | | | | | | | | | | | | |

| | Years Ended

December 31

($ in thousands) | |

| | 2007 | | 2006 | | 2005 | |

| |

| |

| |

| |

CONSOLIDATED: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 431,050 | | 100 | % | | $ | 475,163 | | 100 | % | | $ | 375,786 | | 100 | % | |

Cost of sales | | | 257,646 | | 60 | | | | 276,734 | | 58 | | | | 236,631 | | 63 | | |

Gross profit | | | 173,404 | | 40 | | | | 198,429 | | 42 | | | | 139,155 | | 37 | | |

Other operating income – net of expenses | | | 18,351 | | 4 | | | | 14,246 | | 3 | | | | 7,119 | | 2 | | |

Operating expenses | | | 138,841 | | 32 | | | | 134,377 | | 28 | | | | 114,185 | | 31 | | |

Impairment of goodwill | | | — | | — | | | | — | | — | | | | 519 | | 0 | | |

Income from operations | | | 52,914 | | 12 | | | | 78,298 | | 16 | | | | 31,570 | | 8 | | |

Interest and other income- net | | | 3,222 | | 1 | | | | 2,636 | | 1 | | | | 1,890 | | 1 | | |

Income before income taxes | | | 56,136 | | 13 | | | | 80,934 | | 17 | | | | 33,460 | | 9 | | |

Net income | | | 35,690 | | 8 | | | | 46,250 | | 10 | | | | 19,200 | | 5 | | |

| | | | | | | | | | | | | | | | | | | |

By Segment: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

WHOLESALE DIVISION: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 310,405 | | 100 | % | | $ | 347,509 | | 100 | % | | $ | 254,275 | | 100 | % | |

Cost of sales | | | 205,584 | | 66 | | | | 218,014 | | 63 | | | | 175,292 | | 69 | | |

Gross profit | | | 104,821 | | 34 | | | | 129,495 | | 37 | | | | 78,983 | | 31 | | |

Other operating income | | | 3,677 | | 1 | | | | 2,925 | | 1 | | | | 2,286 | | 1 | | |

Operating expenses | | | 73,362 | | 24 | | | | 75,328 | | 22 | | | | 59,958 | | 24 | | |

Income from operations | | | 35,136 | | 11 | | | | 57,092 | | 16 | | | | 21,311 | | 8 | | |

| | | | | | | | | | | | | | | | | | | |

RETAIL DIVISION: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 120,645 | | 100 | % | | $ | 127,654 | | 100 | % | | $ | 121,511 | | 100 | % | |

Cost of sales | | | 52,062 | | 43 | | | | 58,720 | | 46 | | | | 61,339 | | 50 | | |

Gross profit | | | 68,583 | | 57 | | | | 68,934 | | 54 | | | | 60,172 | | 50 | | |

Operating expenses | | | 65,479 | | 54 | | | | 59,049 | | 46 | | | | 54,227 | | 45 | | |

Impairment of goodwill | | | — | | — | | | | — | | — | | | | 519 | | 0 | | |

Income from operations | | | 3,104 | | 3 | | | | 9,885 | | 8 | | | | 5,426 | | 5 | | |

Number of stores | | | 101 | | | | | | 96 | | | | | | 98 | | | | |

| | | | | | | | | | | | | | | | | | | |

FIRST COST DIVISION: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

Other commission income - net of expenses | | $ | 14,674 | | 100 | % | | $ | 11,321 | | 100 | % | | $ | 4,833 | | 100 | % | |

21

RESULTS OF OPERATIONS

($ in thousands)

Year Ended December 31, 2007 vs. Year Ended December 31, 2006

Consolidated:

Total net sales for the year ended December 31, 2007 decreased by 9% to $431,050 from $475,163 for the comparable period of 2006. Net sales generated by the Retail Division decreased by 5% while net sales generated by the Wholesale Division decreased by 11%. Overall gross profit margin decreased to 40% for the year ended December 31, 2007 from 42% for the prior year. A decrease in the Wholesale gross profit margin to 34% in 2007 compared to 37% in the same period in the prior year was partially offset by an increase in the Retail gross profit margin to 57% in 2007 from 54% in the same period last year. Operating expenses increased in 2007 to $138,841, or 32% of net sales, from $134,377, or 28% of net sales, in 2006, primarily due to the incremental costs associated with the new retail stores opened this year. Commission and licensing fee income was $18,351 for the year ended December 31, 2007 compared to $14,246 for the prior year. Including a one-time charge of $1,208 related to the provision for prior years’ custom duties, operating income for the year ended December 31, 2007 was $52,914, compared to $78,298 in the prior year. Our effective tax rate decreased to 36.4% in 2007 compared to 42.9% in the prior year due to a reduction in the effective tax rate and a one-time tax benefit related to prior periods, connected to our election to file combined tax returns for both New York State and New York City and certain recent changes in tax law. Including the above-mentioned one-time tax benefit of $2,498 and the one-time charge of $1,208 ($737 net of tax effect) related to prior years’ custom duties, net income for the year ended December 31, 2007 was $33,929, compared to $46,250 in 2006. The decrease in income was primarily due to the decrease in net sales and gross profit margins.

Wholesale Division:

Net sales generated by the Wholesale Division was $310,405, or 72%, and $347,509, or 73%, of our total net sales for the years ended December 31, 2007 and 2006, respectively. The decrease in sales was driven primarily by declines in four of our wholesale brands. In the Steve Madden Womens Division and the Steven Division, the decrease in sales was due primarily to an absence of fashion trends in the marketplace and the lack of big items that would drive significant sales volume. In the Steve Madden Mens Division, the continued weakness in the sport casual business resulted in disappointing net sales. Net sales in the Candie’s Division decreased due to a significant increase in markdown allowances to Kohl’s. In addition, net sales for the year ended December 31, 2006 included approximately $15,251 in net sales from Rule, l.e.i. and Jump, three brands that were discontinued late in 2006. These decreases were partially offset by the double-digit net sales increases achieved in both the Madden Girl and the Stevies Divisions and a 6% net sales increase in the Daniel M. Friedman Division.

Gross profit margin decreased to 34% in the year ended December 31, 2007 from 37% in the prior year, due primarily to a significant increase in markdown allowances in the Candie’s and Steven Divisions. Our remaining wholesale divisions also experienced increases in markdown activities as well as an increase in promotional selling reflective of the difficult retail environment in 2007. Operating expenses decreased in 2007 to $73,362 compared to $75,328 in the prior year due to a decrease in variable selling expenses that were partially offset by an increase in non-cash stock based compensation. Income from operations for the Wholesale Division decreased to $35,136 for the year ended December 31, 2007 compared to $57,092 for the year ended December 31, 2006.

Retail Division:

Net Sales generated by the Retail Division accounted for $120,645, or 28%, and $127,654, or 27%, of total Company net sales for the years ended December 31, 2007 and 2006, respectively. We opened seven new stores and closed two under-performing stores during the year ended December 31, 2007. As a result, we had 101 retail stores as of December 31, 2007 compared to 96 stores as of December 31, 2006. The 101 stores currently in operation include 94 under the Steve Madden brand, six under the Steven brand and one e-commerce website. Comparable store sales (sales of those stores, including the e-commerce website, that were open for all of 2007 and 2006) decreased 8% for the year ended December 31, 2007 due primarily to the lack of any significant fashion trends and the softening retail environment in the second half of the year. We have pursued a number of initiatives to enhance gross margins such as reducing freight costs, closeouts, store-to-store transfers and inventory shrinkage combined with better inventory controls. As a result, the gross margin in the Retail Division has increased to 57% for the year ended December 31, 2007 from 54% in the comparable period of 2006. Income from operations for the Retail Division was $3,104 for the current year compared to $9,885 for the same period of 2006.

22

First Cost Division:

The First Cost Division generated net commission income and design fees of $14,674 for the year ended December 31, 2007, compared to $11,321 for the comparable period of 2006. The increase was the result of the continued growth in our private label business as well as the recent expansion of our international business.

Year Ended December 31, 2006 vs. Year Ended December 31, 2005

Consolidated:

Total net sales for the year ended December 31, 2006 increased by 26% to $475,163 from $375,786 for the comparable period of 2005. The total increase resulted from a 37% growth in the Wholesale Division combined with a 5% growth in the Retail Division.

Gross profit margin increased to 42% for the year ended December 31, 2006 from 37% for the prior year. Both the Wholesale and the Retail Divisions achieved significant increases in their gross profit margins. The gross profit margin for the Wholesale Division increased to 37% for the year ended December 31, 2006 from 31% for the comparable period of 2005, and in the Retail Division, the gross profit margin increased to 54% as compared to 50% for the comparable period of 2005. A portion of the increased gross margin was the result of improved inventory management which resulted in fewer markdowns.

Operating expenses increased to $134,377 in the year ended December 31, 2006 from $114,185 in the same period of 2005. The increase in dollars was primarily caused by the incremental costs associated with the acquisition of Daniel M. Friedman and the addition of the SMNY/Madden Girl Division, an increase in sales growth related variable expenses such as warehouse and distribution costs, and an increase in incentive based employee compensation. As a percentage of net sales, operating expenses decreased to 28% for the year ended December 31, 2006 from 31% in the same period of 2005, reflecting our ability to leverage our expense structure against the increase in sales.

Income from operations was $78,298 for the year ended December 31, 2006 compared to $31,570 for the comparable period of 2005. Net income increased by 141% to $46,250 for the year ended December 31, 2006 compared to $19,200 for the year ended December 31, 2005. This increase in income was primarily due to the increase in net sales, the higher gross profit margin, a substantial increase in commission income and the contribution of the Daniel M. Friedman Division.

Wholesale Division:

Net sales from the Wholesale Division accounted for $347,509, or 73%, and $254,275, or 68%, of total net sales for the years ended December 31, 2006 and 2005, respectively. This increase resulted from the incremental sales contributed by the recently acquired Daniel M. Friedman and significant sales growth in Madden Womens, Madden Mens, Candie’s and Steven as well as the contribution of the new brands, SMNY/Madden Girl and Natural Comfort. Gross profit margin increased to 37% of net sales for the year ended December 31, 2006 from 31% in the prior year, primarily due to a significant decrease in off-price sales and lower inventory markdowns and allowances. Operating expenses increased to $75,328 for the year ended December 31, 2006 from $59,958 in the comparable period of 2005. This increase is primarily due to an increase in direct selling expenses reflective of the 37% growth in sales, incentive bonuses and the incremental costs associated with the new brands SMNY/Madden Girl and Natural Comfort, as well as the acquisition of Daniel M. Friedman. As a percentage of net sales, operating expenses decreased to 22% for the year ended December 31, 2006 from 24% for the prior year, reflecting our ability to leverage our expense structure against the increase in sales. Income from operations for the Wholesale Division increased to $57,092 for the year ended December 31, 2006 compared to $21,311 for the year ended December 31, 2005.

23

Retail Division:

Net sales from the Retail Division accounted for $127,654, or 27%, and $121,511, or 32%, of total net sales for the years ended December 31, 2006 and 2005, respectively. We opened four new stores and closed six under-performing stores during the current year. As a result, we had 96 retail stores as of December 31, 2006 compared to 98 stores as of December 31, 2005. The 96 stores in operation include 93 under the Steve Madden name, two under the Steven name and one e-commerce website. Comparable store sales (sales of those stores, including the internet store, that were open for all of 2006 and 2005) for the year ended December 31, 2006 increased 4% over the same period of 2005. Gross profit as a percentage of net sales increased to 54% for the year ended December 31, 2006 from 50% in the comparable period of 2005, primarily due to a significant decrease in promotional sales, improved inventory controls and freight savings. Operating expenses for the Retail Division were $59,049 for the year ended December 31, 2006 and $54,227 for the comparable period of 2005. This increase was primarily due to the non-cash write off of unamortized assets associated with the remodeling of nine stores and the closing of six stores in the current period that accounted for $1,858. Income from operations for the Retail Division was $9,885 for the year ended December 31, 2006 compared to $5,426 for the same period in 2005.

First Cost Division:

The First Cost Division generated net commission income and design fees of $11,321 for year ended December 31, 2006, compared to $4,833 for the comparable period of 2005. The increase was the result of growth in the private label business and, in addition, our ability to leverage the strength of our Steve Madden brands and product designs resulting in a partial recovery of its design, product and development costs through its suppliers.

LIQUIDITY AND CAPITAL RESOURCES

($ in thousands)

Working capital was $121,138 at December 31, 2007 compared to $151,711 at December 31, 2006. The decrease was primarily due to the repurchase of approximately 1,962,000 shares of our common stock at a total cost of $50,094.

Under the terms of a factoring agreement with GMAC, we are eligible to borrow 80% against its receivables at an interest rate equal to the lower of the prime rate less 0.875% or the 30-day London Interbank Offered Rate plus 1.375%. This agreement, which has no specific expiration date and can be terminated by either party with 60 days written notice after June 30, 2009, provides us with a $50 million credit facility with a $25 million sub-limit on the aggregate face amount of Letters of Credit with some other stipulations.

As of December 31, 2007, we held marketable securities valued at $80,411, consisting primarily of corporate and municipal bonds, U.S. Treasury notes, auction rate securities, certificates of deposit and equities.

At December 31, 2007, we held $37,325 in auction rate securities. The contractual maturities of the investments underlying the auction rate securities mature at various dates through 2046, however, all our auction rate securities, or ARSs, have a reset period of less than 30 days. Through March 7, 2008, we had reduced our total holdings in ARSs to $16,300, principally by investing in other short-term investments as individual ARS reset periods came due and the securities were once again subject to the auction process. Through March 7, 2008, auctions for $8,800 of these securities were not successful, resulting in our continuing to hold these securities and the issuers paying interest at the maximum contractual rate. Based on current market conditions, it is likely that auctions related to more of these securities will be unsuccessful in the near term. Unsuccessful auctions could result in our holding securities beyond their next scheduled auction reset dates if a secondary market does not develop, therefore limiting the short-term liquidity of these investments. Accordingly, $16,300 of auction rate securities are classified as long term as of December 31, 2007. While these failures in the auction process have affected our ability to access these funds in the near term, we do not believe that the underlying securities or collateral have been affected. We believe that the higher reset rates on failed auctions provide sufficient incentive for the security issuers to address this lack of liquidity. If the credit rating of the security issuers deteriorates, we may be required to adjust the carrying value of these investments through an impairment charge. We expect to continue to earn interest at the prevailing rates on the ASR’s that we hold.

24

On February 19, 2008, we announced a tender offer to purchase up to 2,600,000 shares of our common stock at a price not greater than $20.00 nor less than $16.50 per share. As of December 31, 2007, there were 20,117,983 shares of our common stock issued and outstanding, not including 5,662,055 of our issued shares held in treasury. The 2,600,000 shares that we are offering to purchase represent approximately 13% of the total number of issued shares. We anticipate that we will pay for the shares tendered in the offer from our available cash.

Management believes that, based upon our current financial position and available cash, cash equivalents and marketable securities, we will meet all of our financial commitments and operating needs, including the tender offer, for at least the next twelve months.

OPERATING ACTIVITIES

($ in thousands)

During the year ended December 31, 2007, net cash provided by operating activities was $59,907. The primary sources of cash were net income of $35,690, increases in accounts payable and accrued expenses of $9,443, decrease in inventories of $6,463, and decreases in the amount due from factor of $5,409. The primary uses of cash were increases in prepaid expenses, prepaid taxes, deposits and other assets of $3,189, a decrease in accrued incentive compensation of $3,359 and an increase in note receivable of $3,126.

INVESTING ACTIVITIES

($ in thousands)

During the year ended December 31, 2007, we invested $66,505 in marketable securities and received $76,192 from the maturities and sales of securities. Also, we invested $9,080 in the acquisition of privately held Compo Enhancements, LLC, which served as a third party provider of e-commerce solutions for us since late in 2005. The acquisition enables us to fully integrate our e-commerce business into our Retail Division and operate its online business internally. Additionally, we made capital expenditures of $12,965, principally for the seven new stores opened in the current period, the construction of two new stores scheduled to open in the early part of 2008, and the remodeling of ten existing stores, additional office space and upgrades to the telephone and management information systems.

FINANCING ACTIVITIES

($ in thousands)

During the year ended December 31, 2007, we repurchased approximately 1,962,000 shares of our common stock at an average price of $25.53 for a total cost of $50,094. We received $5,607 in cash and also realized a tax benefit of $7,180 in connection with the exercise of stock options.

25

CONTRACTUAL OBLIGATIONS

($ in thousands)

Our contractual obligations as of December 31, 2007 were as follows:

| | | | | | | | | | | | | | | | |

| | | | | Payment due by period | |

Contractual Obligations | | Total | | 2008 | | 2009-2010 | | 2011-2012 | | 2013 and

after | |

| |

| |

| |

| |

| |

| |

| | | | | | | | | | | |

Operating lease obligations | | $ | 126,172 | | $ | 16,560 | | $ | 32,765 | | $ | 29,997 | | $ | 46,850 | |

| | |

Purchase obligations | | | 48,558 | | | 48,558 | | | 0 | | | 0 | | | 0 | |

| | |

Other long-term liabilities (future minimum royalty payments) | | | 1,936 | | | 522 | | | 1,414 | | | 0 | | | 0 | |

| | |

| |

| |

| |

| |

| |

|

Total | | $ | 176,666 | | $ | 65,640 | | $ | 34,179 | | $ | 29,997 | | $ | 46,850 | |

| | |

| |

| |

| |

| |

| |

At December 31, 2007, we had un-negotiated open letters of credit for the purchase of inventory of approximately $1,974.

We have an employment agreement with Steven Madden, our Creative and Design Chief, which provides for an annual base salary of $600 subject to certain specified adjustments through June 30, 2015. The agreement also provides for annual bonuses based on EBITDA, revenue of any new business, and royalty income over $2 million, plus an equity grant and a non-accountable expense allowance.

On May 16, 2007, we acquired all of the outstanding equity interest of privately held Compo. The acquisition was completed for a consideration of $9,679, including transaction costs.

On February 7, 2006 we acquired all of the equity interest of Daniel M. Friedman. The acquisition was completed for a consideration of $18,710 including transaction costs. In addition, the purchase agreement includes certain earn-out provisions based on financial performance through 2008. The 2007 earn-out provision of $3,956 was charged to goodwill and increased the total acquisition cost to $22,666.

We have employment agreements with certain executive officers, which provide for the payment of compensation aggregating approximately $2,372 in 2008 and $1,080 in 2009. In addition, some of the employment agreements provide for a discretionary bonus and some provide for incentive compensation based on various performance criteria as well as other benefits including stock options. Our Chief Operating Officer is entitled to deferred compensation calculated as a percentage of his base salary.

Ninety-nine percent (99%) of our products are produced at overseas locations, the majority of which are located in China, with a small percentage located in Brazil, Italy, India and Spain. We have not entered into any long-term manufacturing or supply contracts with any of these foreign companies. We believe that a sufficient number of alternative sources exist outside of the United States for the manufacture of our products. We currently make approximately 99% of our purchases in U.S. dollars.

INFLATION

We do not believe that the relatively low rates of inflation experienced over the last few years in the United States, where we primarily compete, have had a significant effect on sales, expenses or profitability.

26

CRITICAL ACCOUNTING POLICIES AND THE USE OF ESTIMATES

Management’s Discussion and Analysis of Financial Condition and Results of Operations is based upon our Consolidated Financial Statements which have been prepared in accordance with generally accepted accounting principles in the United States. The preparation of these financial statements requires management to make estimates and judgments that affect the reported amounts of assets, liabilities, sales and expenses, and related disclosure of contingent assets and liabilities. Estimates by their nature are based on judgments and available information. Estimates are made based upon historical factors, current circumstances and the experience and judgment of management. Assumptions and estimates are evaluated on an ongoing basis and we may employ outside experts to assist in evaluations. Therefore, actual results could materially differ from those estimates under different assumptions and conditions. Management believes the following critical accounting estimates are more significantly affected by judgments and estimates used in the preparation of our Condensed Consolidated Financial Statements: allowance for bad debts, returns and customer chargebacks; inventory reserves; valuation of intangible assets; litigation reserves and cost of sales.

Allowances for bad debts, returns and customer chargebacks. We provide reserves against our trade accounts receivables for future customer chargebacks, co-op advertising allowances, discounts, returns and other miscellaneous deductions that relate to the current period. The reserve against our non-factored trade receivables also includes estimated losses that may result from customers’ inability to pay. The amount of the reserve for bad debts, returns, discounts and compliance chargebacks are determined by analyzing aged receivables, current economic conditions, the prevailing retail environment and historical dilution levels for customers. As a result of a reevaluation of the retail environment, we revised our method for evaluating our allowance for customer markdowns and advertising chargebacks in the fourth quarter of 2005. In the past, we would look at historical dilution levels for customers to determine the allowance amount. Under the new methodology, we evaluate anticipated chargebacks by reviewing several performance indicators for our major customers. These performance indicators (which include inventory levels at the retail floors, sell through rates and gross margin levels) are analyzed by key account executives and the Vice President of Wholesale Sales to estimate the amount of the anticipated customer allowance. Failure to correctly estimate the amount of the reserve could materially impact our results of operations and financial position.

Inventory reserves. Inventories are stated at lower of cost or market, on a first-in, first-out basis. We review inventory on a regular basis for excess and slow moving inventory. The review is based on an analysis of inventory on hand, prior sales and expected net realizable value through future sales. The analysis includes a review of inventory quantities on hand at period-end in relation to year-to-date sales and projections for sales in the foreseeable future as well as subsequent sales. We consider quantities on hand in excess of estimated future sales to be at risk for market impairment. The net realizable value, or market value, is determined based on the estimate of sales prices of such inventory through off-price or discount store channels. The likelihood of any material inventory write-down is dependent primarily on the expectation of future consumer demand for our product. A misinterpretation or misunderstanding of future consumer demand for our product, the economy, or other failure to estimate correctly, in addition to abnormal weather patterns, could result in inventory valuation changes, either favorably or unfavorably, compared to the valuation determined to be appropriate as of the balance sheet date.

Valuation of intangible assets. SFAS No. 142, “Goodwill and Other Intangible Assets”, which was adopted by us on January 1, 2002, requires that goodwill and intangible assets with indefinite lives no longer be amortized, but rather be tested for impairment at least annually. This pronouncement also requires that intangible assets with finite lives be amortized over their respective lives to their estimated residual values, and reviewed for impairment in accordance with SFAS No. 144, “Accounting for Impairment or Disposal of Long-lived Assets.” In accordance with SFAS No. 144, long-lived assets, such as property, equipment, leasehold improvements and goodwill subject to amortization, are reviewed for impairment annually or whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to the estimated undiscounted future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future cash flows, an impairment charge is recognized by the amount by which the carrying amount of the asset exceeds the fair value of the asset.

Litigation reserves. Estimated amounts for litigation claims that are probable and can be reasonably estimated are recorded as liabilities in our Consolidated Financial Statements. The likelihood of a material change in these estimated reserves would be dependent on new claims as they may arise and the favorable or unfavorable events of a particular litigation. As additional information becomes available, management will assess the potential liability related to the pending litigation and revise its estimates. Such revisions in management’s estimates of the contingent liability could materially impact our results of operation and financial position.

27

Cost of sales.All costs incurred to bring finished products to our distribution center and, in the Retail Division, the costs to bring products to our stores, are included in the cost of sales line item on our Consolidated Statement of Income. These include the cost of finished products, purchase commissions, letter of credit fees, brokerage fees, material and labor and related items, sample expenses, custom duty, inbound freight, royalty payments on licensed products, labels and product packaging. All warehouse and distribution costs are included in the operating expenses line item of our Consolidated Statement of Income. We classify shipping costs, if any, to customers as operating expenses. Our gross profit margins may not be comparable to other companies in the industry because some companies may include warehouse and distribution as a component of cost of sales, while other companies report on the same basis as we do and include them in operating expenses.

| |

ITEM 7A | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

($ in thousands) |

We do not engage in the trading of market risk sensitive instruments in the normal course of business. Our financing arrangements are subject to variable interest rates primarily based on the prime rate and LIBOR. An analysis of our credit agreement with GMAC and Wells Fargo Century can be found in Note C, “Due From Factors” to the Consolidated Financial Statements included in this Annual Report on Form 10-K.