UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS PURSUANT TO

SECTIONS 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 0-24277

(Exact name of Registrant as specified in its Charter)

| Delaware | 58-1972600 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) |

One Landmark Square

Stamford, Connecticut 06901

(Address of principal office, including zip code)

(203) 428-2000

(Registrant's telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: None

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: Common Stock,

par value $.0001

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange

Act. YES o NO x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statement incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. Large accelerated filer o Accelerated filer x Non-accelerated filer o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) YES o NO x

The aggregate market value of the voting stock and non-voting common equity held by non-affiliates of the Registrant at June 30, 2006 was approximately $94.5 million based on $6.45 per share, the closing price of the common stock as quoted on the OTC Pink Sheets Electronic Quotation Service.

The number of shares of the Registrant's common stock outstanding at March 8, 2007 was 17,119,504 shares.

DOCUMENT INCORPORATED BY REFERENCE

Portions of our Proxy Statement for the 2007 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days of the Registrant's 2006 fiscal year end are incorporated by reference into Part III of this report.

TABLE OF CONTENTS

| PAGE | ||

PART I | ||

| ITEM 1. | BUSINESS | 1 |

| FORWARD-LOOKING STATEMENTS | 1 | |

| OVERVIEW | 1 | |

| BUSINESS | 1 | |

| PRIOR BUSINESS | 2 | |

| EMPLOYEES | 3 | |

| AVAILABLE INFORMATION | 3 | |

| ITEM 1A. | RISK FACTORS | 4 |

| ITEM 1B. | UNRESOLVED STAFF COMMENTS | 7 |

| ITEM 2. | PROPERTIES | 7 |

| ITEM 3. | LEGAL PROCEEDINGS | 7 |

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS | 8 |

PART II | ||

| ITEM 5. | MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 9 |

| ITEM 6. | SELECTED FINANCIAL DATA | 13 |

| ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 14 |

| ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 20 |

| ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTAL DATA | 21 |

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 41 |

| ITEM 9A. | CONTROLS AND PROCEDURES | 41 |

| ITEM 9B | OTHER INFORMATION | 42 |

PART III | ||

| ITEM 10. | DIRECTORS AND EXECUTIVE OFFICERS OF THE REGISTRANT | 42 |

| ITEM 11. | EXECUTIVE COMPENSATION | 42 |

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 42 |

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 42 |

| ITEM 14. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 42 |

PART IV | ||

| ITEM 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 43 |

| SIGNATURES | 46 | |

| EXHIBIT INDEX | 49 | |

ITEM 1. BUSINESS

FORWARD-LOOKING STATEMENTS

This report contains certain forward-looking statements, including information about or related to our future results, certain projections and business trends. Assumptions relating to forward-looking statements involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. When used in this report, the words "estimate," "project," "intend," "believe," "expect" and similar expressions are intended to identify forward-looking statements. Although we believe that our assumptions underlying the forward-looking statements are reasonable, any or all of the assumptions could prove inaccurate, and we may not realize the results contemplated by the forward-looking statements. Management decisions are subjective in many respects and susceptible to interpretations and periodic revisions based upon actual experience and business developments, the impact of which may cause us to alter our business strategy or capital expenditure plans that may, in turn, affect our results of operations. In light of the significant uncertainties inherent in the forward-looking information included in this report, you should not regard the inclusion of such information as our representation that we will achieve any strategy, objectives or other plans. The forward-looking statements contained in this report speak only as of the date of this report, and we have no obligation to update publicly or revise any of these forward-looking statements.

These and other statements, which are not historical facts, are based largely upon our current expectations and assumptions and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those contemplated by such forward-looking statements. These risks and uncertainties include, among others, our planned effort to redeploy our assets and use our cash, cash equivalents and marketable securities to enhance stockholder value following the sale of substantially all of our electronic commerce business, which represented substantially all of our revenue generating operations and related assets, and the risks and uncertainties set forth in the section headed "Risk Factors" of Part I, Item 1A of this Report and described in "Management's Discussion and Analysis of Financial Condition and Results of Operations" of Part II of this Report. We cannot assure you that we will be successful in our efforts to redeploy our assets or that any such redeployment will result in Clarus’ future profitability. Our failure to redeploy our assets could have a material adverse effect on the market price of our common stock and our business, financial condition and results of operations.

OVERVIEW

Clarus Corporation ("Clarus" or the "Company," which may be referred to as "we," "us," or "our") was formerly a provider of e-commerce business solutions until the sale of substantially all of its operating assets in December 2002. We are currently seeking to redeploy our cash, cash equivalents and marketable securities to enhance stockholder value and are seeking, analyzing and evaluating potential acquisition and merger candidates. We were incorporated in Delaware in 1991 under the name SQL Financials, Inc. In August 1998, we changed our name to Clarus Corporation. Our principal corporate office is located at One Landmark Square, Stamford, Connecticut 06901 and our telephone number is (203) 428-2000.

BUSINESS

At the 2002 annual meeting of our stockholders held on May 21, 2002, Warren B. Kanders, Burtt R. Ehrlich and Nicholas Sokolow were elected by our stockholders to serve on our Board of Directors. Under the leadership of these new directors, our Board of Directors adopted a strategy of seeking to enhance stockholder value by pursuing opportunities to redeploy our assets through an acquisition of, or merger with, an operating business that will serve as a platform company, using our cash, cash equivalents, marketable securities, other non-operating assets (including, to the extent available, our net operating loss carryforward) and our publicly-traded stock to enhance future growth. The strategy also sought to reduce significantly our cash expenditure rate by targeting, to the extent practicable, our overhead expenses to the amount of our investment income until the completion of an acquisition or merger. While the Company's operating expenses, excluding transaction expenses, have remained relatively stable during the past three fiscal years, management currently believes that the Company's operating expenses, excluding potential unsuccessful transaction expenses, may exceed investment income during 2007.

As part of our strategy to enhance stockholder value, on December 6, 2002, we consummated the sale of substantially all of the assets of our electronic commerce business, which represented substantially all of our revenue generating operations and related assets, to Epicor Software Corporation ("Epicor"), a Delaware corporation, for a purchase price of $1.0 million in cash (the "Asset Sale"). Epicor is traded on the NASDAQ National Market under the symbol "EPIC." The sale included licensing, support and maintenance activities from our eProcurement, Sourcing, View (for eProcurement), eTour (for eProcurement), ClarusNET, and Settlement software products, our customer lists, certain contracts and certain intellectual property rights related to the purchased assets, maintenance payments and certain furniture and equipment. Epicor agreed to assume certain of our liabilities, such as executory obligations arising under certain contracts, agreements and commitments related to the transferred assets. We remained responsible for all of our other liabilities including liabilities under certain contracts, including any violations of environmental laws and for our obligations related to any of our indebtedness, employee benefit plans or taxes that were due and payable in connection with the acquired assets on or before the closing date of the Asset Sale.

1

Upon the closing of the sale to Epicor, Warren B. Kanders assumed the position of Executive Chairman of the Board of Directors, Stephen P. Jeffery ceased to serve as Chief Executive Officer and Chairman of the Board, and James J. McDevitt ceased to serve as Chief Financial Officer and Corporate Secretary. Mr. Jeffery agreed to continue to serve on the Board of Directors and serve in a consulting capacity for a period of three years. In addition, the Board of Directors appointed Nigel P. Ekern as Chief Administrative Officer to oversee the operations of Clarus and to assist with our asset redeployment strategy. Mr. Ekern resigned December 31, 2006. Philip A. Baratelli assumed the role of Chief Financial Officer on February 1, 2007.

On January 1, 2003, we sold the assets related to our Cashbook product, which were excluded from the Epicor transaction, to an employee group headquartered in Limerick, Ireland. This completed the sale of nearly all of our active software operations as part of our strategy to limit operating losses and enable us to reposition our business in order to enhance stockholder value. In anticipation of the redeployment of our assets, our cash, cash equivalents and marketable securities are being held in short-term, highly rated instruments designed to preserve safety and liquidity and to exempt us from registration as an investment company under the Investment Company Act of 1940.

We are currently working to identify suitable merger partners or acquisition opportunities. Although we are not targeting specific industries for potential acquisitions, we plan to seek businesses with substantial operations and free cash flow, experienced management teams, and operations in markets offering substantial growth opportunities. In addition, we believe that our common stock, which has a strong institutional stockholder base, offers us flexibility as acquisition currency and will enhance our attractiveness to potential merger or acquisition candidates. This strategy is, however, subject to certain risks. See "Risk Factors" below.

As previously disclosed in our Current Report on Form 8-K filed with the Securities and Exchange Commission on October 4, 2004, the Company's common stock was delisted from the NASDAQ National Market effective with the open of business on October 5, 2004. The delisting followed a determination by the NASDAQ Listing Qualifications Panel that the Company was a "public shell" and should be delisted due to policy concerns raised under NASDAQ Marketplace Rules 4300 and 4300(a)(3). The Company's common stock is now quoted on the OTC Pink Sheets Electronic Quotation Service under the symbol "CLRS.PK."

At the Company's annual stockholders meeting on July 24, 2003, the stockholders approved an amendment (the "Amendment") to our Amended and Restated Certificate of Incorporation to restrict certain acquisitions of Clarus' securities in order to help assure the preservation of its net operating loss tax carryforward ("NOL"). Although the transfer restrictions imposed on our securities are intended to reduce the likelihood of an impermissible ownership change, no assurance can be given that such restrictions would prevent all transfers that would result in an impermissible ownership change. The Amendment generally restricts and requires prior approval of our Board of Directors of direct and indirect acquisitions of the Company's equity securities if such acquisition will affect the percentage of our capital stock that is treated as owned by a 5% stockholder. The restrictions will generally only affect persons trying to acquire a significant interest in our common stock.

During the year ended December 31, 2006, the Company incurred $1.4 million in expenses related to acquisition negotiations and due diligence processes that terminated without the consummation of the acquisitions. During 2005, the Company recognized a credit of $59,000 relating to the final settlement of outstanding expenses arising out of an acquisition negotiation and due diligence process that terminated in September 2004. Transaction expenses represent the costs incurred during due diligence and negotiation of potential acquisitions, such as legal, accounting, appraisal and other professional fees and related expenses.

PRIOR BUSINESS

Prior to the sale of substantially all of our operating assets in December 2002, we developed, marketed and supported Internet-based business-to-business e-commerce software that automated the procurement, sourcing, and settlement of goods and services. Our software was designed to help organizations reduce the costs associated with the purchasing and payment settlement of goods and services, and help to maximize procurement economies of scale.

There were several milestones in the evolution of our business prior to the December 2002 sale:

| - | On May 26, 1998, we completed an initial public offering of our common stock in which we sold 2.5 million shares of common stock at $10.00 per share, resulting in net proceeds to us of approximately $22.0 million. |

| - | On October 18, 1999, we sold substantially all of the assets of our financial and human resources software ("ERP") business to Geac Computer Systems, Inc. and Geac Canada Limited. In this sale, we received approximately $13.9 million. |

| - | On March 10, 2000, we sold 2,243,000 shares of common stock in a secondary public offering at $115.00 per share resulting in net proceeds to us of approximately $244.4 million. |

2

EMPLOYEES

All of our employees are based in the United States. As of December 31, 2006, we had a total of seven employees, all of which are located in our Stamford, Connecticut headquarters. Our employees only devote as much of their time as is necessary to the affairs of the Company and also serve in various capacities with other public and private entities. None of our employees are represented by a labor union or are subject to a collective bargaining agreement. We have not experienced any work stoppages and consider our relationship with our employees to be good.

Executive Officers of the Registrant

Pursuant to General Instruction G(3), the information regarding our executive officers called for by Item 401(b) of Regulation S-K is hereby included in Part I of this Annual Report on Form 10-K.

The executive officers of our Company as of March 14, 2007 are as follows:

Warren B. Kanders, 48, has served as one of our directors since June 2002 and as Executive Chairman of our Board of Directors since December 2002. Mr. Kanders has served as the Founder and Chairman of the Board of Armor Holdings, Inc. since January 1996 and as its Chief Executive Officer since April 2003. Mr. Kanders has served as the Executive Chairman of the Board of Net Perceptions, Inc. since April 2004 and as the Chairman of the Board of Directors of Langer, Inc. since November 2004. From October 1992 to May 1996, Mr. Kanders served as Founder and Vice Chairman of the Board of Benson Eyecare Corporation. Mr. Kanders also serves as President of Kanders & Company, Inc. ("Kanders & Company"), a private investment firm owned and controlled by Mr. Kanders that makes investments in and renders consulting services to public and private entities. Mr. Kanders received a B.A. degree in Economics from Brown University in 1979.

Philip A. Baratelli, 39, has served as our Chief Financial Officer, Secretary and Treasurer since February 2007. From June 2001 until January 2007, Mr. Baratelli was employed by Armor Holdings, Inc., as its Corporate Controller and held the additional position of Treasurer of Armor Holdings, Inc., from March 2003 until January 2007. Prior to joining Armor Holdings, Inc., Mr. Baratelli was employed by PriceWaterhouseCoopers LLP from 1998 to 2001 in various positions ranging from Associate to Senior Associate. From 1991 to 1997, Mr. Baratelli worked for Barnett Bank, Inc. in various finance and credit analysis positions. Mr. Baratelli received a Bachelor of Science in finance from Florida State University in 1989 and a Bachelor of Business Administration in accounting from the University of North Florida in 1995. Mr. Baratelli is a certified public accountant. There are no family relationships between Mr. Baratelli and any director of the Company.

AVAILABLE INFORMATION

Our Internet address is www.claruscorp.com. We make available free of charge on or through our Internet website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, and the proxy statement for our annual meeting of stockholders as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. Forms 3, 4 and 5 filed with respect to our equity securities under section 16(a) of the Securities Exchange Act of 1934, as amended, are also available on our Internet website. All of the foregoing materials are located at the ‘‘SEC Filings’’ tab. The information found on our website shall not be deemed incorporated by reference by any general statement incorporating by reference this report into any filing under the Securities Act of 1933, as amended, or under the Securities Exchange Act of 1934, as amended, and shall not otherwise be deemed filed under such Acts.

We have adopted a Code of Ethics for Senior Executive Officers and Senior Financial Officers, a Code of Business Conduct and Ethics for directors, officers, employees, agents, representatives, subsidiaries and affiliates, an Audit Committee Charter, Complaint Procedures for Accounting and Auditing Matters, a Compensation Committee Charter, a Nominating/Corporate Governance Committee Charter, and Corporate Governance Guidelines, all of which are available at our Internet website at the tab ‘‘Investor Relations.’’ We will provide to any person without charge, upon request, a copy of the foregoing materials. We intend to disclose future amendments to the provisions of the foregoing documents, policies and guidelines and waivers therefrom, if any, on our Internet website and/or through the filing of Current Report on Form 8-K with the Securities and Exchange Commission.

Materials we file with the Securities and Exchange Commission may be read and copied at the Securities and Exchange Commission’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Securities and Exchange Commission’s Public Reference Room by calling the Securities and Exchange Commission at 1-800-SEC-0330. The Securities and Exchange Commission also maintains an Internet website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the Securities and Exchange Commission at www.sec.gov. In addition, you may request a copy of any such materials, without charge, by submitting a written request to: Clarus Corporation, c/o the Secretary, One Landmark Square, 22nd Floor, Stamford, Connecticut 06901.

Information on our Internet website does not constitute a part of this Annual Report on Form 10-K.

3

ITEM 1A. RISK FACTORS

In addition to other information in this Annual Report on Form 10-K, the following risk factors should be carefully considered in evaluating our business because such factors may have a significant impact on our business, operating results, liquidity and financial condition. As a result of the risk factors set forth below, actual results could differ materially from those projected in any forward-looking statements. Additional risks and uncertainties not presently known to us, or that we currently consider to be immaterial, may also impact our business, operating results, liquidity and financial condition. If any of the following risks occur, our business, operating results, liquidity and financial condition could be materially adversely affected. In such case, the trading price of our securities could decline, and you may lose all or part of your investment.

RISKS RELATED TO CLARUS CORPORATION

WE CONTINUE TO INCUR OPERATING LOSSES.

As a result of the sale of substantially all of our electronic commerce business, we will no longer generate revenue previously associated with the products and contracts comprising our electronic commerce business. We are not profitable and have incurred an accumulated deficit of $282.2 million from our inception through December 31, 2006. Our current ability to generate revenues and to achieve profitability and positive cash flow will depend on our ability to redeploy our assets and use our cash, cash equivalents and marketable securities to reposition our business whether it is through a merger or acquisition. Our ability to become profitable will depend, among other things, (i) on our success in identifying and acquiring a new operating business, (ii) on our development of new products or services relating to our new operating business, and (iii) on our success in distributing and marketing our new products or services.

WE MAY BE UNABLE TO REDEPLOY OUR ASSETS SUCCESSFULLY.

As part of our strategy to limit operating losses and enable Clarus to redeploy its assets and use its cash, cash equivalents and marketable securities to enhance stockholder value, we have sold our electronic commerce business, which represented substantially all of our revenue generating operations and related assets. We are pursuing a strategy of identifying suitable merger partners and acquisition candidates that will serve as a platform company. Although we are not targeting specific business industries for potential acquisitions, we plan to seek businesses with operations and free cash flow, experienced management teams, and operations in markets offering significant growth opportunities. We may not be able to successfully identify such a business, obtain financing for such acquisition, or successfully operate any business that we identify. We have been working without success since December 2002 to identify a suitable merger partner and consummate an acquisition. Failure to redeploy successfully will result in our inability to become profitable.

Even if we identify an appropriate acquisition opportunity, we may be unable to negotiate favorable terms for that acquisition. We may be unable to select, manage or absorb or integrate any future acquisitions successfully. Any acquisition, even if effectively integrated, may not benefit our stockholders. Any acquisitions that we attempt or complete may involve a number of unique risks including: (i) executing successful due diligence; (ii) our exposure to unforeseen liabilities of acquired companies; and (iii) our ability to integrate and absorb the acquired company successfully. We may be unable to address these problems successfully. Our failure to redeploy our assets could have a material adverse effect on the market price of our common stock and our business, financial condition and results of operations.

WE WILL INCUR SIGNIFICANT COSTS IN CONNECTION WITH OUR EVALUATION OF SUITABLE MERGER PARTNERS AND ACQUISITION CANDIDATES.

As part of our plan to redeploy our assets, our management is seeking, analyzing and evaluating potential acquisition and merger candidates. We have incurred and will continue to incur significant costs, such as due diligence and legal and other professional fees and expenses, as part of these redeployment efforts. We incurred approximately $1.4 million of transaction related expenses during 2006 for due diligence and negotiation of potential acquisitions. In 2004, we incurred $1.6 million of transaction related expenses during due diligence and negotiation of potential acquisitions. Notwithstanding these efforts and expenditures, we cannot give any assurance that we will identify an appropriate acquisition opportunity in the near term, or at all.

WE WILL LIKELY HAVE NO OPERATING HISTORY IN OUR NEW LINE OF BUSINESS, WHICH IS YET TO BE DETERMINED, AND THEREFORE WE WILL BE SUBJECT TO THE RISKS INHERENT IN ESTABLISHING A NEW BUSINESS.

We have not identified what our new line of business will be; therefore, we cannot fully describe the specific risks presented by such business. It is likely that we will have had no operating history in the new line of business and it is possible that the target company may have a limited operating history in its business. Accordingly, there can be no assurance that our future operations will generate operating or net income, and as such our success will be subject to the risks, expenses, problems and delays inherent in establishing a new line of business for Clarus. The ultimate success of such new business cannot be assured.

4

THE REPORTING REQUIREMENTS UNDER RULES ADOPTED BY THE SECURITIES AND EXCHANGE COMMISSION RELATING TO SHELL COMPANIES MAY DELAY OR PREVENT US FROM MAKING CERTAIN ACQUISITIONS.

As a result of the final rules adopted by the Securities and Exchange Commission on June 29, 2005, Clarus may be deemed to be a shell company. The rules are designed to ensure that investors in shell companies that acquire operations have timely access to the same kind of information as is available to investors in public companies generally. The rules prohibit the use by shell companies of a Form S-8 and revise the Form 8-K to require a shell company to include extensive registration-level information required to register a class of securities under the Securities Exchange Act of 1934 (the “Exchange Act”), in the filing on Form 8-K that the shell company files to report the acquisition of a business.

The extensive registration-level information includes a detailed description of a company’s business and properties, management, executive compensation, related party transactions, legal proceedings and historical market price information, as well as audited historical financial statements and management’s discussion and analysis of results of operations. The revised Form 8-K rules also require a shell company to file pro forma financial statements giving effect to the acquisition not later than four business days after completion of the acquisition, instead of 75 days as required by non-shell companies.

The time and additional costs that may be incurred by some acquisition prospects to prepare such detailed disclosures and obtain audited financial statements may significantly delay or essentially preclude consummation of an otherwise desirable acquisition by Clarus, or deter potential targets from negotiating with Clarus. If Clarus were to be deemed a shell company, any increased difficulty in Clarus’ ability to identify and consummate an acquisition with an appropriate merger candidate can materially adversely affect Clarus’ ability to successfully implement its redeployment strategy.

WE MAY BE UNABLE TO REALIZE THE BENEFITS OF OUR NET OPERATING LOSS ("NOL") AND TAX CREDIT CARRYFORWARDS.

NOLs may be carried forward to offset federal and state taxable income in future years and eliminate income taxes otherwise payable on such taxable income, subject to certain adjustments. Based on current federal corporate income tax rates, our NOL and other carryforwards could provide a benefit to us, if fully utilized, of significant future tax savings. However, our ability to use these tax benefits in future years will depend upon the amount of our otherwise taxable income. If we do not have sufficient taxable income in future years to use the tax benefits before they expire, we will lose the benefit of these NOL carryforwards permanently. Consequently, our ability to use the tax benefits associated with our substantial NOL will depend significantly on our success in identifying suitable merger partners and/or acquisition candidates, and once identified, successfully consummate a merger with and/or acquisition of these candidates.

Additionally, if we underwent an ownership change, the NOL carryforward limitations would impose an annual limit on the amount of the taxable income that may be offset by our NOL generated prior to the ownership change. If an ownership change were to occur, we may be unable to use a significant portion of our NOL to offset taxable income. In general, an ownership change occurs when, as of any testing date, the aggregate of the increase in percentage points of the total amount of a corporation's stock owned by "5-percent stockholders" within the meaning of the NOL carryforward limitations whose percentage ownership of the stock has increased as of such date over the lowest percentage of the stock owned by each such "5-percent stockholder" at any time during the three-year period preceding such date is more than 50 percentage points. In general, persons who own 5% or more of a corporation's stock are "5-percent stockholders," and all other persons who own less than 5% of a corporation's stock are treated together as a public group.

The amount of NOL and tax credit carryforwards that we have claimed has not been audited or otherwise validated by the U.S. Internal Revenue Service (the “IRS”). The IRS could challenge our calculation of the amount of our NOL or our determinations as to when a prior change in ownership occurred and other provisions of the Internal Revenue Code may limit our ability to carry forward our NOL to offset taxable income in future years. If the IRS was successful with respect to any such challenge, the potential tax benefit of the NOL carryforwards to us could be substantially reduced.

CERTAIN TRANSFER RESTRICTIONS IMPLEMENTED BY US TO PRESERVE OUR NOL MAY NOT BE EFFECTIVE OR MAY HAVE SOME UNINTENDED NEGATIVE EFFECTS.

On July 24, 2003, at our Annual Meeting of Stockholders, our stockholders approved an amendment (the "Amendment") to our Amended and Restated Certificate of Incorporation to restrict certain acquisitions of our securities in order to help assure the preservation of our NOL. The Amendment generally restricts direct and indirect acquisitions of our equity securities if such acquisition will affect the percentage of Clarus' capital stock that is treated as owned by a "5-percent stockholder."

Although the transfer restrictions imposed on our capital stock are intended to reduce the likelihood of an impermissible ownership change, there is no guarantee that such restrictions would prevent all transfers that would result in an impermissible ownership change. The transfer restrictions also will require any person attempting to acquire a significant interest in us to seek the approval of our Board of Directors. This may have an "anti-takeover" effect because our Board of Directors may be able to prevent any future takeover. Similarly, any limits on the amount of capital stock that a stockholder may own could have the effect of making it more difficult for stockholders to replace current management. Additionally, because the transfer restrictions will have the effect of restricting a stockholder's ability to acquire our common stock, the liquidity and market value of our common stock might suffer.

5

WE COULD BE REQUIRED TO REGISTER AS AN INVESTMENT COMPANY UNDER THE INVESTMENT COMPANY ACT OF 1940, WHICH COULD SIGNIFICANTLY LIMIT OUR ABILITY TO OPERATE AND ACQUIRE AN ESTABLISHED BUSINESS.

The Investment Company Act of 1940 (the "Investment Company Act") requires registration, as an investment company, for companies that are engaged primarily in the business of investing, reinvesting, owning, holding or trading securities. We have sought to qualify for an exclusion from registration including the exclusion available to a company that does not own "investment securities" with a value exceeding 40% of the value of its total assets on an unconsolidated basis, excluding government securities and cash items. This exclusion, however, could be disadvantageous to us and/or our stockholders. If we were unable to rely on an exclusion under the Investment Company Act and were deemed to be an investment company under the Investment Company Act, we would be forced to comply with substantive requirements of the Investment Company Act, including: (i) limitations on our ability to borrow; (ii) limitations on our capital structure; (iii) restrictions on acquisitions of interests in associated companies; (iv) prohibitions on transactions with affiliates; (v) restrictions on specific investments; (vi) limitations on our ability to issue stock options; and (vii) compliance with reporting, record keeping, voting, proxy disclosure and other rules and regulations. Registration as an investment company would subject us to restrictions that would significantly impair our ability to pursue our fundamental business strategy of acquiring and operating an established business. In the event the Securities and Exchange Commission or a court took the position that we were an investment company, our failure to register as an investment company would not only raise the possibility of an enforcement action by the Securities and Exchange Commission or an adverse judgment by a court, but also could threaten the validity of corporate actions and contracts entered into by us during the period we were deemed to be an unregistered investment company. Moreover, the Securities and Exchange Commission could seek an enforcement action against us to the extent we were not in compliance with the Investment Company Act during any point in time.

FOR FIVE YEARS AFTER THE CLOSING OF THE ASSET SALE TO EPICOR, WE WILL BE PROHIBITED FROM COMPETING WITH THE ASSETS SOLD TO EPICOR.

The Noncompetition Agreement we entered into with Epicor provides that for a period of five years after the closing of the Asset Sale (December 6, 2002), neither we nor any of our affiliated entities are permitted, directly or indirectly, anywhere in the world: (i) to engage in any business that competes with the business of developing, marketing and supporting Internet-based business-to-business, electronic commerce solutions that automate the procurement, sourcing and settlement of goods and services including through the eProcurement, Sourcing, View (for eProcurement), eTour (for eProcurement), ClarusNET and Settlement software products and all improvements and variations of these products; (ii) to attempt to persuade any customer or vendor of Epicor to cease to do business with Epicor or reduce the amount of business being conducted with Epicor; (iii) to solicit the business of any customer or vendor of Epicor, if the solicitation could cause a reduction in the amount of business that Epicor does with the customer or vendor; or (iv) to hire, solicit for employment or encourage to leave the employment of Epicor any person who was an employee of Epicor within 90 days before the closing of the Asset Sale.

The prohibitions contained in our Noncompetition Agreement with Epicor will restrict the business opportunities available to us and therefore may have a material adverse effect on our ability to successfully redeploy our remaining assets.

RISKS RELATED TO OUR COMMON STOCK

OUR COMMON STOCK IS NO LONGER LISTED ON THE NASDAQ NATIONAL MARKET.

On October 5, 2004, our common stock was delisted from the NASDAQ National Market. The delisting followed a determination by the NASDAQ Listing Qualifications Panel that the Company was a "public shell" and should be delisted due to policy concerns raised under NASDAQ Marketplace Rules 4300 and 4300(a)(3). Additional information concerning the delisting is set forth in the Company's Current Report on Form 8-K filed with the Securities and Exchange Commission on October 4, 2004. The Company's common stock is now quoted on the OTC Pink Sheets Electronic Quotation Service under the symbol "CLRS.PK." As a result of the delisting, stockholders may find it more difficult to dispose of, or to obtain accurate quotations as to the price of, our common stock, the liquidity of our stock may be reduced, making it difficult for a stockholder to buy or sell our stock at competitive market prices or at all, we may lose support from institutional investors and/or market makers that currently buy and sell our stock and the price of our common stock could decline.

6

WE ARE VULNERABLE TO VOLATILE MARKET CONDITIONS.

The market prices of our common stock have been highly volatile. The market has from time to time experienced significant price and volume fluctuations that are unrelated to the operating performance of particular companies. Please see the table contained in Item 5 of this Report which sets forth the range of high and low closing prices of our common stock for the calendar quarters indicated.

WE DO NOT EXPECT TO PAY DIVIDENDS ON OUR COMMON STOCK IN THE FORESEEABLE FUTURE.

Although our stockholders may receive dividends if, as and when declared by our Board of Directors, we do not intend to pay dividends on our common stock in the foreseeable future. Therefore, you should not purchase our common stock if you need immediate or future income by way of dividends from your investment.

OUR AMENDED AND RESTATED CERTIFICATE OF INCORPORATION AUTHORIZES THE ISSUANCE OF SHARES OF PREFERRED STOCK.

Our Amended and Restated Certificate of Incorporation provides that our Board of Directors will be authorized to issue from time to time, without further stockholder approval, up to 5,000,000 shares of preferred stock in one or more series and to fix or alter the designations, preferences, rights and any qualifications, limitations or restrictions of the shares of each series, including the dividend rights, dividend rates, conversion rights, voting rights, terms of redemption, including sinking fund provisions, redemption price or prices, liquidation preferences and the number of shares constituting any series or designations of any series. Such shares of preferred stock could have preferences over our common stock with respect to dividends and liquidation rights. We may issue additional preferred stock in ways which may delay, defer or prevent a change in control of Clarus without further action by our stockholders. Such shares of preferred stock may be issued with voting rights that may adversely affect the voting power of the holders of our common stock by increasing the number of outstanding shares having voting rights, and by the creation of class or series voting rights.

WE MAY ISSUE A SUBSTANTIAL AMOUNT OF OUR COMMON STOCK IN THE FUTURE, WHICH COULD CAUSE DILUTION TO CURRENT INVESTORS AND OTHERWISE ADVERSELY AFFECT OUR STOCK PRICE.

A key element of our growth strategy is to make acquisitions. As part of our acquisition strategy, we may issue additional shares of common stock as consideration for such acquisitions. These issuances could be significant. To the extent that we make acquisitions and issue our shares of common stock as consideration, your equity interest in us will be diluted. Any such issuance will also increase the number of outstanding shares of common stock that will be eligible for sale in the future. Persons receiving shares of our common stock in connection with these acquisitions may be more likely to sell off their common stock, which may influence the price of our common stock. In addition, the potential issuance of additional shares in connection with anticipated acquisitions could lessen demand for our common stock and result in a lower price than might otherwise be obtained. We may issue common stock in the future for other purposes as well, including in connection with financings, for compensation purposes, in connection with strategic transactions or for other purposes.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None

Our corporate headquarters is currently located in Stamford, Connecticut where we lease approximately 8,600 square feet for $25,156 per month, pursuant to a lease, which expires on March 31, 2019.

We also leased approximately 5,200 square feet near Toronto, Canada, at a cost of approximately $11,000 per month, which prior to October 2001, was used for the delivery of services as well as research and development. This lease expired on February 14, 2006. This facility had been sub-leased for approximately $5,000 a month, pursuant to a sublease, which expired on January 30, 2006.

We are not a party to nor are any of our properties subject to any pending legal, administrative or judicial proceedings other than routine litigation incidental to our business.

A complaint was filed on May 14, 2001 in the United States District Court for the Northern District of Georgia on behalf of all purchasers of common stock of the Company during the period beginning December 8, 1999 and ending on October 25, 2000. Generally the complaint alleged that the Company and certain of its directors and officers made material misrepresentations and omissions in public filings made with the Securities and Exchange Commission and in certain press releases and other public statements. The Company agreed to settle the class action in exchange for a payment of $4.5 million, which was covered by insurance. The Court approved the final settlement and dismissed the action on January 6, 2005.

7

No matters were submitted to a vote of security holders, through the solicitation of proxies or otherwise, during the quarter ended December 31, 2006.

8

PART II

Our common stock was listed on the NASDAQ National Market System on May 26, 1998, the effective date of our initial public offering, until October 5, 2004, when our common stock was delisted from the NASDAQ National Market following a determination by the NASDAQ Listing Qualifications Panel that the Company was a "public shell" and should be delisted due to policy concerns raised under NASDAQ Marketplace Rules 4300 and 4300(a)(3). Additional information concerning the delisting is set forth in the Company's Current Report on Form 8-K filed with the Securities and Exchange Commission on October 4, 2004. The Company's common stock is now quoted on the OTC Pink Sheets Electronic Quotation Service under the symbol "CLRS.PK".

The following table sets forth, for the indicated periods, the range of high and low bids for our common stock as reported by the OTC Pink Sheets Electronic Quotation Service. The quotes listed below reflect inter-dealer prices or transactions solely between market-makers, without retail mark-up, mark-down or commission and may not represent actual transactions.

| High | Low | |||||||

| Calendar Year 2007 | ||||||||

| First Quarter (through March 8, 2007) | $ | 7.95 | $ | 7.05 | ||||

| Year ended December 31, 2006 | ||||||||

| First Quarter | $ | 8.45 | $ | 6.90 | ||||

| Second Quarter | $ | 7.19 | $ | 6.30 | ||||

| Third Quarter | $ | 7.34 | $ | 6.40 | ||||

| Fourth Quarter | $ | 7.50 | $ | 6.70 | ||||

| Year ended December 31, 2005 | ||||||||

| First Quarter | $ | 9.50 | $ | 7.90 | ||||

| Second Quarter | $ | 9.00 | $ | 7.20 | ||||

| Third Quarter | $ | 8.50 | $ | 7.27 | ||||

| Fourth Quarter | $ | 8.75 | $ | 7.60 | ||||

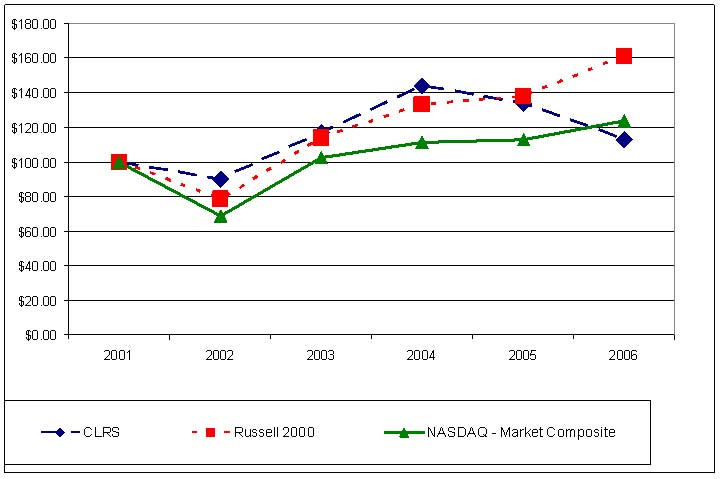

PERFORMANCE GRAPH

Set forth below is a line graph comparing the yearly percentage change in the cumulative total stockholder return on our common stock to the cumulative total return of the NASDAQ National Market Composite and The Russell 2000 Index for the period commencing on December 31, 2001 and ending on December 31, 2006 (the “Measuring Period”). The graph assumes that the value of the investment in our common stock and each index was $100 on December 31, 2001. The yearly change in cumulative total return is measured by dividing (1) the sum of (i) the cumulative amount of dividends for the Measuring Period, assuming dividend reinvestment, and (ii) the change in share price between the beginning and end of the Measuring Period, by (2) the share price at the beginning of the Measuring Period.

The Company considered providing a comparison consisting of a group of peer companies in an industry or line-of-business similar to us, but could not reasonably identify a group of comparable peer companies that the Company believed would provide our stockholders with a meaningful comparison. The stock price performance on the following graph is not necessarily indicative of future stock price performance.

9

COMPARISON OF CUMULATIVE TOTAL RETURN*

AMONG CLARUS, THE NASDAQ NATIONAL MARKET COMPOSITE AND

THE RUSSELL 2000 INDEX

12/31/01 | 12/31/02 | 12/31/03 | 12/31/04 | 12/31/05 | 12/31/06 | ||||||||||||||

CLARUS CORPORATION | $ | 100.00 | $ | 90.06 | $ | 116.99 | $ | 144.23 | $ | 133.81 | $ | 112.98 | |||||||

NASDAQ NATIONAL MARKET COMPOSITE | $ | 100.00 | $ | 68.47 | $ | 102.72 | $ | 111.54 | $ | 113.08 | $ | 123.84 | |||||||

THE RUSSELL 2000 INDEX | $ | 100.00 | $ | 78.42 | $ | 114.00 | $ | 133.38 | $ | 137.81 | $ | 161.24 | |||||||

* $100 INVESTED ON 12/31/01 IN STOCK OR INDEX -

INCLUDING REINVESTMENT OF DIVIDENDS.

10

STOCKHOLDERS

On March 8, 2007, the last reported sales price for our common stock was $7.80 per share. As of March 8, 2007, there were 145 holders of record of our common stock.

DIVIDENDS

We currently anticipate that we will retain all future earnings for use in our business and do not anticipate that we will pay any cash dividends in the foreseeable future. The payment of any future dividends will be at the discretion of our Board of Directors and will depend upon, among other things, our results of operations, capital requirements, general business conditions, contractual restrictions on payment of dividends, if any, legal and regulatory restrictions on the payment of dividends, and other factors our Board of Directors deems relevant.

RECENT SALES OF UNREGISTERED SECURITIES

None.

RECENT PURCHASES OF OUR REGISTERED EQUITY SECURITIES

We did not purchase any shares of our common stock during the Company’s fourth quarter of 2006.

SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS

The following table sets forth certain information regarding our equity plans as of December 31, 2006:

Plan Category | (A) Number of securities to be issued upon exercise of outstanding options, warrants and rights | (B) Weighted-average exercise price of outstanding options, warrants and rights | (C) Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (A)) | |||||||

| Equity compensation plans approved by security holders (1) (2) | 1,082,536 | $ | 5.97 | 4,434,679 | ||||||

| Equity compensation plans not approved by security holders (3) (4) (5) | 1,100,000 | $ | 7.83 | -- | ||||||

Total | 2,182,536 | $ | 6.91 | 4,434,679 | ||||||

(1) Consists of stock options and restricted stock awards issued under the Amended and Restated Stock Incentive Plan of Clarus Corporation (the “2000 Plan”). Also consists of stock options issued and issuable under the 2005 Clarus Corporation Stock Incentive Plan (the “2005 Plan”).

(2) Includes 920,134 shares of our common stock remaining available for future issuance under the Clarus Corporation Employee Stock Purchase Plan and the Global Employee Stock Purchase Plan (collectively, the “Plans”). Under the Plans, employees have an opportunity to purchase shares of the Company’s common stock at a discount. Generally, eligible employees, as defined in the plan documents, may elect to have up to 15 percent of their annual salary, up to a maximum of $12,500 per six-month purchase period, withheld to purchase the Company’s common stock at a price equal to the lower of 85 percent of the market price of our common stock at either the beginning or the end of the six-month offering period.

(3) Includes options granted to the Company’s Executive Chairman, Warren B. Kanders to purchase 400,000 shares of common stock, having an exercise price of $7.50 per share.

11

(4) Includes options granted to the Company’s Executive Chairman, Warren B. Kanders to purchase 400,000 shares of common stock, having an exercise price of $10.00 per share.

(5) Includes 300,000 shares of restricted stock granted to the Company’s Executive Chairman, Warren B. Kanders, having voting, dividend, distribution and other rights, which shall vest and become nonforfeitable if Mr. Kanders is an employee and/or a director of the Company or a subsidiary or affiliate of the Company on the earlier of (i) the date the closing price of the Company’s common stock equals or exceeds $15.00 per share for each of the trading days during a ninety consecutive day period, or (ii) April 11, 2013, subject to acceleration in certain circumstances.

12

ITEM 6. SELECTED FINANCIAL DATA

Our selected financial information set forth below should be read in conjunction with our consolidated financial statements, including the notes thereto and "Management's Discussion and Analysis of Financial Condition and Results of Operations" of Part II of this Report. The following statement of operations and balance sheet data have been derived from our audited consolidated financial statements and should be read in conjunction with those statements and "Management's Discussion and Analysis of Financial Condition and Results of Operations" of Part II of this Report.

Years ended December 31, | ||||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | ||||||||||||

| (in thousands, except per share data) | ||||||||||||||||

Statement of Operations Data: | ||||||||||||||||

| Revenues: | ||||||||||||||||

| License fees | $ | -- | $ | -- | $ | 1,106 | $ | -- | $ | 2,808 | ||||||

| Service fees | -- | -- | -- | 130 | 6,226 | |||||||||||

| Total Revenues | -- | -- | 1,106 | 130 | 9,034 | |||||||||||

| Cost of Revenues: | ||||||||||||||||

| License fees | -- | -- | -- | -- | 26 | |||||||||||

| Service fees | -- | -- | -- | -- | 5,498 | |||||||||||

| Total Cost of Revenues | -- | -- | -- | -- | 5,524 | |||||||||||

| Operating expenses: | ||||||||||||||||

| Research and development | -- | -- | -- | -- | 7,263 | |||||||||||

| Sales and marketing | -- | -- | -- | -- | 7,938 | |||||||||||

| General and administrative | 3,530 | 3,504 | 3,395 | 4,986 | 12,574 | |||||||||||

| Provision/(credit) for doubtful accounts | -- | -- | -- | 18 | (560 | ) | ||||||||||

| Transaction expense | 1,431 | (59 | ) | 1,636 | -- | -- | ||||||||||

| Loss on impairment of goodwill and intangible assets | -- | -- | -- | -- | 10,360 | |||||||||||

| Loss on sale or disposal of assets | -- | -- | -- | 36 | 1,748 | |||||||||||

| Depreciation and amortization | 346 | 334 | 186 | 762 | 4,243 | |||||||||||

| Total Operating Expenses | 5,307 | 3,779 | 5,217 | 5,802 | 43,566 | |||||||||||

| Operating Loss | (5,307 | ) | (3,779 | ) | (4,111 | ) | (5,672 | ) | (40,056 | ) | ||||||

| Other income/(expense) | -- | (2 | ) | 19 | 169 | 27 | ||||||||||

| Interest income | 4,016 | 2,490 | 1,203 | 1,238 | 2,441 | |||||||||||

| Interest expense, including amortization of debt discount | -- | -- | -- | (66 | ) | (225 | ) | |||||||||

| Net Loss | $ | (1,291 | ) | $ | (1,291 | ) | $ | (2,889 | ) | $ | (4,331 | ) | $ | (37,813 | ) | |

| Loss Per Share | ||||||||||||||||

| Basic | $ | (0.08 | ) | $ | (0.08 | ) | $ | (0.18 | ) | $ | (0.27 | ) | $ | (2.42 | ) | |

| Diluted | $ | (0.08 | ) | $ | (0.08 | ) | $ | (0.18 | ) | $ | (0.27 | ) | $ | (2.42 | ) | |

| Weighted Average Common Shares Outstanding | ||||||||||||||||

| Basic | 16,613 | 16,329 | 16,092 | 15,905 | 15,615 | |||||||||||

| Diluted | 16,613 | 16,329 | 16,092 | 15,905 | 15,615 | |||||||||||

Balance Sheet Data: | As of December 31, | |||||||||||||||

| 2006 | 2005 | 2004 | 2003 | 2002 | ||||||||||||

| Cash and cash equivalents | $ | 1,731 | $ | 23,270 | $ | 48,377 | $ | 15,045 | $ | 42,225 | ||||||

| Marketable securities | $ | 82,634 | $ | 61,601 | $ | 35,119 | $ | 73,685 | $ | 52,885 | ||||||

| Total assets | $ | 86,673 | $ | 88,278 | $ | 86,437 | $ | 89,445 | $ | 97,764 | ||||||

| Total stockholders' equity | $ | 85,716 | $ | 86,609 | $ | 84,854 | $ | 86,819 | $ | 89,360 | ||||||

13

FORWARD-LOOKING STATEMENTS

This report contains certain forward-looking statements, including information about or related to our future results, certain projections and business trends. Assumptions relating to forward-looking statements involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. When used in this report, the words "estimate," "project," "intend," "believe," "expect" and similar expressions are intended to identify forward-looking statements. Although we believe that our assumptions underlying the forward-looking statements are reasonable, any or all of the assumptions could prove inaccurate, and we may not realize the results contemplated by the forward-looking statements. Management decisions are subjective in many respects and susceptible to interpretations and periodic revisions based upon actual experience and business developments, the impact of which may cause us to alter our business strategy or capital expenditure plans that may, in turn, affect our results of operations. In light of the significant uncertainties inherent in the forward-looking information included in this report, you should not regard the inclusion of such information as our representation that we will achieve any strategy, objectives or other plans. The forward-looking statements contained in this report speak only as of the date of this report, and we have no obligation to update publicly or revise any of these forward-looking statements.

These and other statements, which are not historical facts, are based largely upon our current expectations and assumptions and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those contemplated by such forward-looking statements. These risks and uncertainties include, among others, our planned effort to redeploy our assets and use our substantial cash, cash equivalents and marketable securities to enhance stockholder value following the sale of substantially all of our electronic commerce business, which represented substantially all of our revenue generating operations and related assets, and the risks and uncertainties set forth in the section headed "Risk Factors" of Part I, Item 1A of this Report and described in "Management's Discussion and Analysis of Financial Condition and Results of Operations" of Part II of this Report. We cannot assure you that we will be successful in our efforts to redeploy our assets or that any such redeployment will result in Clarus’ future profitability. Our failure to redeploy our assets could have a material adverse effect on the market price of our common stock and our business, financial condition and results of operations.

OVERVIEW

AS PART OF OUR PREVIOUSLY ANNOUNCED STRATEGY TO LIMIT OPERATING LOSSES AND ENABLE THE COMPANY TO REDEPLOY ITS ASSETS AND USE ITS SUBSTANTIAL CASH, CASH EQUIVALENTS AND MARKETABLE SECURITIES TO ENHANCE STOCKHOLDER VALUE, ON DECEMBER 6, 2002, WE SOLD SUBSTANTIALLY ALL OF OUR ELECTRONIC COMMERCE BUSINESS, WHICH REPRESENTED SUBSTANTIALLY ALL OF OUR REVENUE GENERATING OPERATIONS AND RELATED ASSETS. THE INFORMATION APPEARING BELOW, WHICH RELATES TO PRIOR PERIODS, IS THEREFORE NOT INDICATIVE OF THE RESULTS THAT MAY BE EXPECTED FOR ANY SUBSEQUENT PERIODS. RESULTS FOR THE YEAR ENDED DECEMBER 31, 2006 AND ANY FUTURE PERIODS PRIOR TO A REDEPLOYMENT OF OUR ASSETS ARE EXPECTED PRIMARILY TO REFLECT, GENERAL AND ADMINISTRATIVE EXPENSES AND TRANSACTION EXPENSES ASSOCIATED WITH THE CONTINUING ADMINISTRATION OF THE COMPANY AND ITS EFFORTS TO REDEPLOY ITS ASSETS.

CRITICAL ACCOUNTING POLICIES AND USE OF ESTIMATES

The Company's discussion of financial condition and results of operations is based on the consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these consolidated financial statements require management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent liabilities at the date of the consolidated financial statements. Estimates also affect the reported amounts of revenues and expenses during the reporting periods. The Company continually evaluates its estimates and assumptions including those related to revenue recognition, impairment of long-lived assets, impairment of investments, and contingencies and litigation. The Company bases its estimates on historical experience and other assumptions that are believed to be reasonable under the circumstances. Actual results could differ from these estimates.

The Company believes the following critical accounting policies include the more significant estimates and assumptions used by management in the preparation of its consolidated financial statements. Our accounting policies are more fully described in Note 1 of our consolidated financial statements.

- The Company accounts for its marketable securities under the provisions of Statement of Financial Accounting Standards ("SFAS") No. 115, "Accounting for Certain Investments in Debt and Equity Securities". Pursuant to the provisions of SFAS No. 115, the Company has classified its marketable securities as available-for-sale. Available-for-sale securities have been recorded at fair value and related unrealized gains and losses have been excluded from earnings and are reported as a separate component of accumulated other comprehensive income (loss) until realized.

14

- The Company accounts for income taxes pursuant to Statement of Financial Accounting Standards No. 109, "Accounting for Income Taxes" ("SFAS 109"). Under the asset and liability method specified thereunder, deferred taxes are determined based on the difference between the financial reporting and tax bases of assets and liabilities. Deferred tax liabilities are offset by deferred tax assets relating to net operating loss carryforwards, tax credit carryforwards and deductible temporary differences. Recognition of deferred tax assets is based on management’s belief that it is more likely than not that the tax benefit associated with temporary differences and operating and capital loss carryforwards will be utilized. A valuation allowance is recorded for those deferred tax assets for which it is more likely than not that the realization will not occur.

- On January 1, 2006, the Company adopted Statement of Financial Accounting Standards No. 123 (revised 2004), “Share-Based Payments” (“SFAS 123R”), requiring recognition of expense related to the fair value of stock option awards. The Company recognizes the cost of the share-based awards on a straight-line basis over the requisite service period of the award. Prior to January 1, 2006, the Company accounted for stock option plans under the recognition and measurement provisions of Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees” (“APB 25”) and related interpretations, as permitted by Statement of Financial Accounting Standard No. 123, “Accounting for Stock-Based Compensation” (“SFAS 123”). Under SFAS 123R, compensation cost recognized during 2006 would include: (a) compensation cost for all share-based payments granted prior to, but not yet vested as of January 1, 2006, based on the grant date fair value estimated in accordance with the original provisions of SFAS 123, and (b) compensation cost for all share-based payments granted subsequent to January 1, 2006, based on the grant-date fair value estimated in accordance with the provisions of SFAS 123R. The Company recorded total non-cash stock compensation expense of approximately $301,000 related to unvested restricted stock and incurred no compensation expense related to options under SFAS 123R in 2006.

- Through 2004, the Company had recognized revenue in connection with its prior business from two primary sources, software licenses and services. Revenue from software licensing and services fees was recognized in accordance with Statement of Position ("SOP") 97-2, "Software Revenue Recognition", and SOP 98-9, "Software Revenue Recognition with Respect to Certain Transactions" and related interpretations. The Company recognized software license revenue when: (1) persuasive evidence of an arrangement existed; (2) delivery had occurred; (3) the fee was fixed or determinable; and (4) collectibility was probable.

SOURCES OF REVENUE

Prior to the December 6, 2002 sale of substantially all of the Company's revenue generating operations and assets, the Company's revenue consisted of license fees and services fees. License fees were generated from the licensing of the Company's suite of software products. Services fees were generated from consulting, implementation, training, content aggregation and maintenance support services. Following the sale of substantially all of the Company's operating assets, the Company's revenue consisted solely of the recognition of deferred services fees that were recognized ratably over the maintenance term of the license agreements for our prior suite of software products. The remaining deferred revenue was fully recognized by September 30, 2004 upon expiration of the maintenance term.

Until a redeployment of the Company's assets occurs, the Company's principal income will consist of interest, dividend and other investment income from cash, cash equivalents and marketable securities, which is reported as interest income in the Company's statement of operations.

OPERATING EXPENSES

General and administrative expense include salaries and employee benefits, rent, insurance, legal, accounting and other professional fees, state and local non income based taxes, board of director fees as well as public company expenses such as transfer agent and listing fees and expenses.

Transaction expense consists primarily of professional fees and expenses related to due diligence, negotiation and documentation of acquisition, financing and related agreements.

RESTRUCTURING AND RELATED COSTS

During fiscal 2002 and fiscal 2001, the Company's management approved restructuring plans to reorganize and reduce operating costs. Restructuring and related charges of $12.8 million were expensed in fiscal 2001 and fiscal 2002 in an attempt to align the Company's cost structure with projected revenue.

During fiscal 2003, the Company determined that actual restructuring and related charges were in excess of the amounts provided for in fiscal 2002 and fiscal 2001 and recorded additional restructuring charges of $250,000. This amount was charged to general and administrative costs during fiscal 2003. The charges for fiscal 2003 were comprised of $223,000 for employee separation costs and $27,000 for facility closure and consolidation costs.

15

During fiscal 2004, the Company recorded an additional restructuring charge of $33,000 for facility closure costs. The increase was the result of significant fluctuations in exchange rates and increased rent expense. Expenditures for fiscal 2004 totaled $190,000 consisting of $125,000 for employee separation costs and $65,000 for facility closing costs.

During fiscal 2006 and fiscal 2005, expenditures for facility closing costs totaled $17,000 and $56,000 respectively. As of December 31, 2006, the balance for restructuring and related costs was zero.

On December 6, 2002, the Company completed the disposition of substantially all its operating assets, and the Company is now evaluating alternative ways to redeploy its cash, cash equivalents and marketable securities into new businesses. The discussion below is therefore not meaningful to an understanding of future revenue, earnings, operations, business or prospects of the Company following such a redeployment of its assets.

REVENUES

Total revenues for fiscal 2006 and fiscal 2005 were zero.

GENERAL AND ADMINISTRATIVE EXPENSE

During the years ended December 31, 2006 and 2005, general and administrative expenses remained stable at $3.5 million. This trend is consistent with management's stated strategy to limit our expenditure rate to the extent practicable, to levels of our investment income until the completion of an acquisition or merger. General and administrative expenses include salaries and employee benefits, rent, insurance, legal, accounting and other professional fees, state and local non income based taxes, board of director fees as well as public company expenses such as transfer agent and listing fees and expenses. General and administrative expenses for the year ended December 31, 2006, also includes a one-time charge of $250,000 representing the severance payment related to Mr. Nigel P. Ekern’s resignation, effective December 31, 2006.

TRANSACTION EXPENSE

The Company incurred approximately $1.4 million of transaction expense during the year ended December 31, 2006, arising out of acquisition negotiations and due diligence processes that terminated without the consummation of the acquisitions. In the first quarter of 2005, the Company incurred $92,000 in expenses related to an acquisition negotiation and due diligence process and also recognized a credit of $151,000 in expenses from the final settlement of outstanding expenses arising out of an acquisition negotiation and due diligence process that terminated in September 2004 without the consummation of the acquisition.

Transaction expense consists primarily of professional fees and expenses related to due diligence, negotiation and documentation of acquisition, financing and related agreements.

DEPRECIATION EXPENSE

Depreciation expense for the year ended December 31, 2006 increased slightly to $0.35 million compared to $0.33 million for the year ended December 31, 2005. The increase is primarily attributable to the purchase of new equipment during the year.

INTEREST INCOME

Interest income increased to $4.0 million for the year ended December 31, 2006 compared to $2.5 million for the year ended December 31, 2005. Interest income for the years ended December 31, 2006 and 2005, includes $2.5 million and $1.5 million in discount accretion and premium amortization, respectively. The increase in interest income was due primarily to higher rates of return on investments. The weighted average interest rate for our investments for fiscal 2006 was 4.82% compared to 2.99% for fiscal 2005. The current earnings rate as of December 31, 2006 is 5.18%.

INCOME TAXES

As a result of the operating losses incurred since the Company's inception, no provision or benefit for income taxes was recorded in the years ended December 31, 2006 or 2005.

16

COMPARISON OF RESULTS OF OPERATIONS BETWEEN THE YEARS ENDED DECEMBER 31, 2005 AND 2004

On December 6, 2002, the Company completed the disposition of substantially all its operating assets, and the Company is now evaluating alternative ways to redeploy its cash, cash equivalents and marketable securities into new businesses. The discussion below is therefore not meaningful to an understanding of future revenue, earnings, operations, business or prospects of the Company following such a redeployment of its assets.

REVENUES

Total revenues decreased to zero for the year ended December 31, 2005 compared to $1.1 million for the year ended December 31, 2004. This decrease is entirely due to a non-recurring deferred license fee revenue recognized in the third quarter of fiscal 2004 that was recognized upon the expiration of the maintenance term of the license agreements for our prior suite of software products.

GENERAL AND ADMINISTRATIVE EXPENSE

During the year ended December 31, 2005, general and administrative expenses were $3.5 million compared to $3.4 million in 2004. This trend is consistent with management's stated strategy to limit our expenditure rate to the extent practicable, to levels of our investment income until the completion of an acquisition or merger. General and administrative expenses include salaries and employee benefits, rent, insurance, legal, accounting and other professional fees, state and local non income based taxes, board of director fees as well as public company expenses such as transfer agent and listing fees and expenses.

TRANSACTION EXPENSE

In the fourth quarter of fiscal 2005, the Company incurred $92,000 in expenses related to an acquisition negotiation and due diligence process and also recognized a credit of $151,000 in expenses from the final settlement of outstanding expenses arising out of an acquisition negotiation and due diligence process that terminated in September 2004 without the consummation of the acquisition. In the third quarter of 2004, the Company recognized $1.5 million in transaction expense arising out of negotiations associated with a terminated acquisition in September 2004. The Company incurred an additional $0.1 million of transaction expenses during the fourth quarter of fiscal 2004.

Transaction expense represents the costs incurred during due diligence and negotiation of potential acquisitions, such as legal, accounting, appraisal and other professional fees and related expenses.

DEPRECIATION EXPENSE

Depreciation expense for the year ended December 31, 2005 increased to $0.3 million compared to $0.2 million for the year ended December 31, 2004. The increase is primarily attributable to the depreciation of the Company's headquarters located in Stamford, Connecticut. Occupancy of the space commenced in the second quarter of fiscal 2004.

INTEREST INCOME

Interest income increased to $2.5 million for the year ended December 31, 2005 compared to $1.2 million in the year ended December 31, 2004. Interest income for the years ended December 31, 2005 and 2004, includes $1.5 million and $0.6 million in discount accretion and premium amortization, respectively. The increase in interest income was due to higher rates of return on investments. The weighted average interest rate for our investments for fiscal 2005 was 2.99% compared to 1.43% for fiscal 2004.

INCOME TAXES

As a result of the operating losses incurred since the Company's inception, no provision or benefit for income taxes was recorded in the years ended December 31, 2005 or 2004.

The Company's cash and cash equivalents decreased to $1.7 million at December 31, 2006 from $23.3 million at December 31, 2005 due to a shift in the composition of the investment portfolio to marketable securities. Marketable securities are investments with a longer duration under the accounting principles generally accepted in the United States of America. Marketable securities increased to $82.6 million at December 31, 2006 from $61.6 million at December 31, 2005. The overall combined decrease of $0.5 million in cash, cash equivalents and marketable securities is primarily due to the liquidation of investments required to fund transaction expenses.

Cash used in operating activities was approximately $3.0 million during fiscal 2006. The cash used was primarily attributable to the Company’s net loss, a decrease in accounts payable and accrued liabilities offset by a decrease in deposits and other long term assets, and an increase in deferred rent and other non-cash items. Cash used in operating activities was approximately $1.8 million during fiscal 2005. The cash used in fiscal 2005 was primarily attributable to the Company's net loss, a decrease in accounts payable and accrued liabilities offset by an increase in interest receivable, prepaids and other current assets, deferred rent and non-cash items. The trend in cash used in operating activities is consistent with management's stated strategy, following the sale of substantially all of the Company's operating assets in December 2002, to reduce our cash expenditure rate by targeting, to the extent practicable, our overhead expenses to the amount of our investment income until the completion of an acquisition or merger. While the Company's operating expenses, excluding transaction expenses, have remained relatively stable during the past three fiscal years, management currently believes that the Company's operating expenses, excluding potential unsuccessful transaction expenses, may exceed investment income during 2007.

17

Cash used by investing activities was approximately $18.6 million during fiscal 2006. The cash was used for the purchase of marketable securities partially offset by the maturity of marketable securities. Cash used by investing activities was approximately $25.9 million during fiscal 2005. The cash was used for the purchase of marketable securities and transaction related costs including legal and professional fees partially offset by the maturity of marketable securities.

There was no cash provided by financing activities during fiscal 2006 compared to $2.6 million during fiscal 2005. Cash provided by financing activities during 2005 was attributable to stock option exercises. There were no stock option exercises during fiscal 2006.

On January 1, 2006, the Company adopted Statement of Financial Accounting Standards No. 123 (revised 2004), “Share-Based Payments” (“SFAS 123R”), requiring recognition of expense related to the fair value of stock option awards. The Company recognizes the cost of the share-based awards on a straight-line basis over the requisite service period of the award. Prior to January 1, 2006, the Company accounted for stock option plans under the recognition and measurement provisions of Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees” (“APB 25”) and related interpretations, as permitted by Statement of Financial Accounting Standard No. 123, “Accounting for Stock-Based Compensation” (“SFAS 123”). Under SFAS 123R, compensation cost recognized during 2006 includes: (a) compensation cost for all share-based payments granted prior to, but not yet vested as of January 1, 2006, based on the grant date fair value estimated in accordance with the original provisions of SFAS 123, and (b) compensation cost for all share-based payments granted subsequent to January 1, 2006, based on the grant-date fair value estimated in accordance with the provisions of SFAS 123R.

On December 30, 2005, the Company’s Board of Directors accelerated the vesting of unvested stock options previously awarded to employees, officers and directors of the Company under its Amended and Restated Stock Incentive Plan of Clarus Corporation (as amended and restated effective as of June 13, 2000) and the Clarus Corporation 2005 Stock Incentive Plan, subject to such optionee entering into lock-up, confidentiality and non-competition agreements. As a result of this action, options to purchase 676,669 shares of common stock that would have vested over the next one to three years became fully vested.

The decision to accelerate the vesting of these options was made primarily to reduce non-cash compensation expense that would have been recorded in future periods following the Company’s application of the Financial Accounting Standards Board Statement No. 123, “Share Based Payment (revised 2004) (“SFAS 123R”). The Company adopted the expense recognition provisions of SFAS 123R beginning January 1, 2006. The acceleration of the options is expected to reduce the Company’s non-cash compensation expense related to these options by approximately $1.5 million or $0.09 per share (pre-tax) for the years 2006 - 2008, based on estimated value calculations using the Black-Scholes methodology.