Exhibit 99.2

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Searchable text section of graphics shown above

Investors’ Overview

September 22, 2003

• | ||

|

|

|

• | ||

|

|

|

• | ||

|

|

|

• | ||

|

|

|

• | ||

| • | |

| • | |

| • | |

| • | |

| • | |

| • | |

| • | |

[LOGO]

1

Monoline Financial Guaranty Insurance Industry

2

The Aaa/AAA-Rated Monoline Financial Guaranty Insurance Industry

• Big Four primary providers: AMBAC (1971), MBIA (1973), FGIC (1983), FSA (1985)

• New entrants: XLCA (2000), CIFG (2002)

• Insure municipal/governmental and asset-backed bonds, domestically and internationally

• All rated Aaa/AAA/AAA by Moody’s/S&P/Fitch Ratings

• Regulated by

• Government agencies

• Rating agencies

• Barriers to entry

• Significant capital requirements

• Experienced management requirements

• Strong ownership/business model requirements

• Market recognition & acceptance - - trading value and liquidity

• Staffing infrastructure requirements

• Weak returns in early years of start-up

• Underwrite investment-grade transactions

• No forced acceleration – insurer is only required to make principal and interest payments as scheduled

• Low industry loss experience

3

• Transaction level

• Shadow rating assigned to each insured transaction by sector specialist

• Capital charges assigned for each specific exposure

• Insurance company level

• Continuous review of operations, risk management practices, profitability, liquidity and quality of management

• Review capital sources and investment practices

• Evaluate worst-case loss potential from claims

• Assess capital adequacy under stress scenarios

• S&P’s FER (Financial Enhancement Ratings)

• Measures willingness to pay claims and commitment to maintain Triple-A

4

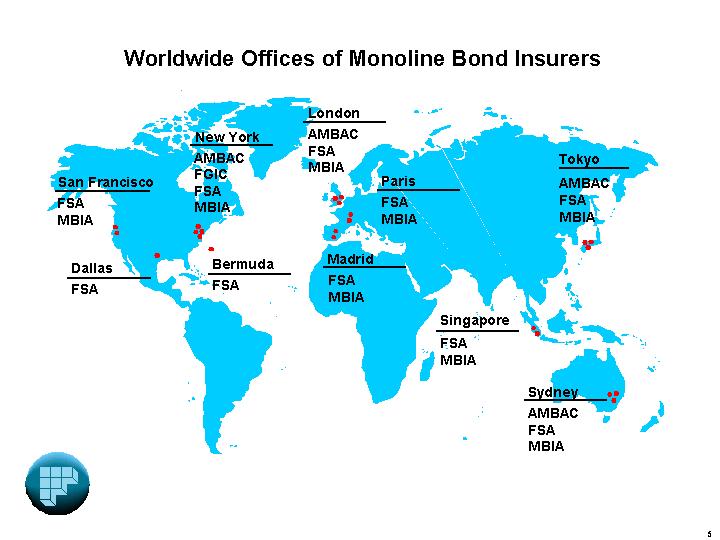

Worldwide Offices of Monoline Bond Insurers

[GRAPHIC]

5

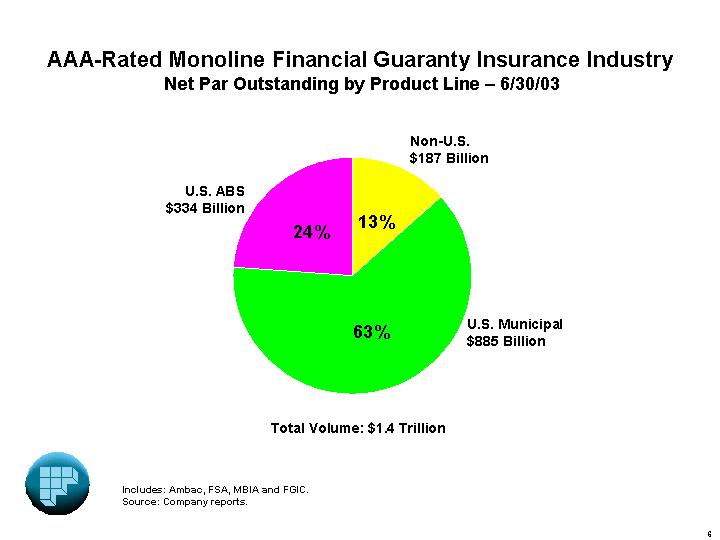

AAA-Rated Monoline Financial Guaranty Insurance Industry

Net Par Outstanding by Product Line – 6/30/03

[CHART]

Total Volume: $1.4 Trillion

Includes: Ambac, FSA, MBIA and FGIC.

Source: Company reports.

6

AAA-Rated Monoline Financial Guaranty Insurance Industry Annual Gross Par Originated

Strong Growth in Originations and Growing Diversification

[CHART]

Sources: FSA, MBIA, Ambac and FGIC company reports. Includes secondary market transactions.

(1) Includes ABS, MBS and funded and unfunded CDOs and CDSs.

7

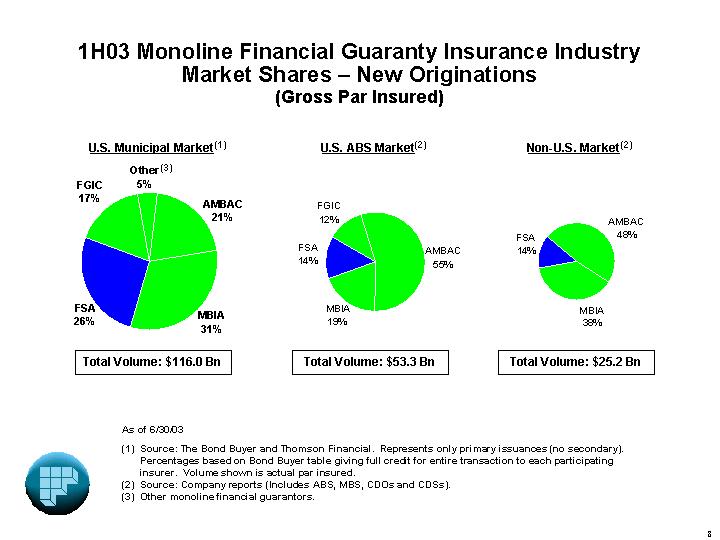

1H03 Monoline Financial Guaranty Insurance Industry

Market Shares – New Originations

(Gross Par Insured)

U.S. Municipal Market(1) |

| U.S. ABS Market(2) |

| Non-U.S. Market(2) |

|

|

|

|

|

[CHART] |

| [CHART] |

| [CHART] |

|

|

|

|

|

Total Volume: $116.0 Bn |

| Total Volume: $53.3 Bn |

| Total Volume: $25.2 Bn |

As of 6/30/03

(1) Source: The Bond Buyer and Thomson Financial. Represents only primary issuances (no secondary). Percentages based on Bond Buyer table giving full credit for entire transaction to each participating insurer. Volume shown is actual par insured.

(2) Source: Company reports (Includes ABS, MBS, CDOs and CDSs).

(3) Other monoline financial guarantors.

8

U.S. ABS Insured Penetration Rate

for Monoline Bond Insurers

(Public and 144A ABS Market - Par Insured)(1)

2001 |

| 2002(2) |

| 1st Half 2003 |

$332 Billion |

| $411 Billion |

| $220 Billion |

|

|

|

|

|

[CHART] |

| [CHART] |

| [CHART] |

(1) Source: Asset-Backed Alert: Figures exclude collateralized bond obligations and MBS (agency and jumbos). Insurers were given credit for the entire size of each deal they guaranteed in 2001 figures, however beginning in 2002, insurers receive credit for only the insured amount.

(2) For 1H03, the insured penetration rate for certain sectors was: auto leases 100%, home equity lines of credit 93%, subprime auto loans 59%, equipment leases 44%, subprime home loans 16%.

9

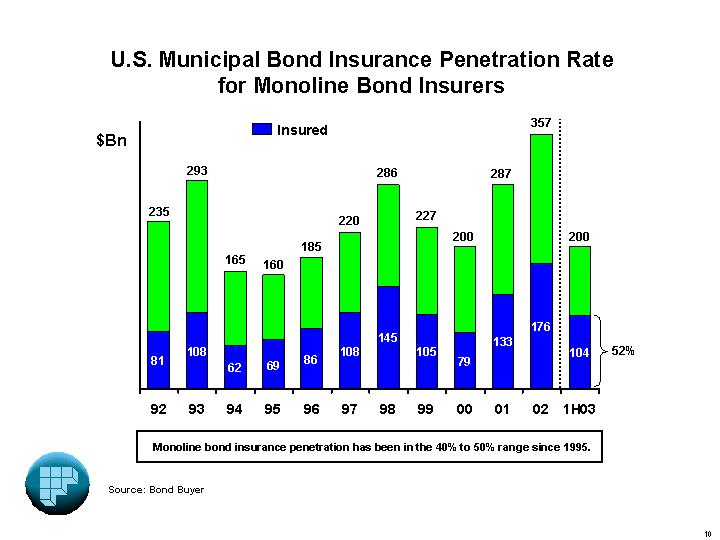

U.S. Municipal Bond Insurance Penetration Rate

for Monoline Bond Insurers

[CHART]

Monoline bond insurance penetration has been in the 40% to 50% range since 1995.

Source: Bond Buyer

10

Financial Security Assurance (FSA)

11

• Founded in 1985

• Rated Triple-A by S&P, Moody’s, Fitch Ratings, and Rating and Investment Information (Japan)

• Pioneered the asset-backed securities market

• Since inception, FSA has insured in excess of $332 billion of gross principal in ABS transactions

• Entered municipal market in 1990

• Since inception, FSA has insured in excess of $277 billion of gross principal related to municipal transactions

• Independent public company (NYSE) from 1994-2000

• Acquired by Dexia in July 2000

• Continues as a separately managed franchise, with oversight from Dexia

• Acquired minority ownership interest in Fairbanks Capital Holdings Corp. in 1998

As of 6/30/03

12

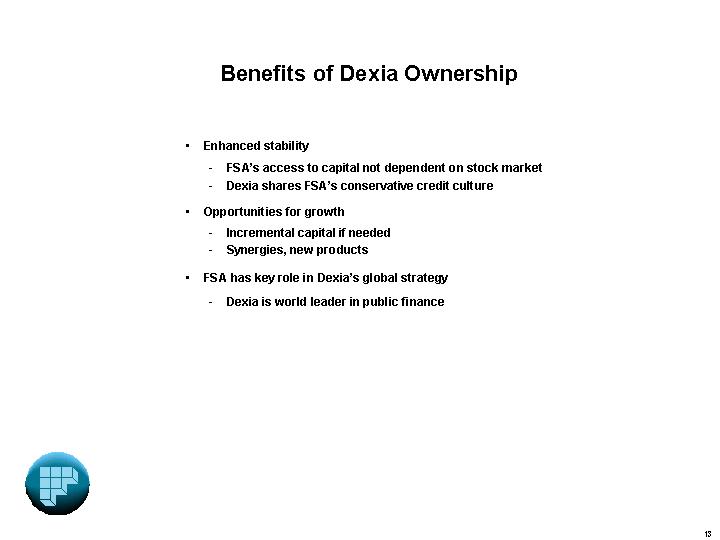

• Enhanced stability

• FSA’s access to capital not dependent on stock market

• Dexia shares FSA’s conservative credit culture

• Opportunities for growth

• Incremental capital if needed

• Synergies, new products

• FSA has key role in Dexia’s global strategy

• Dexia is world leader in public finance

13

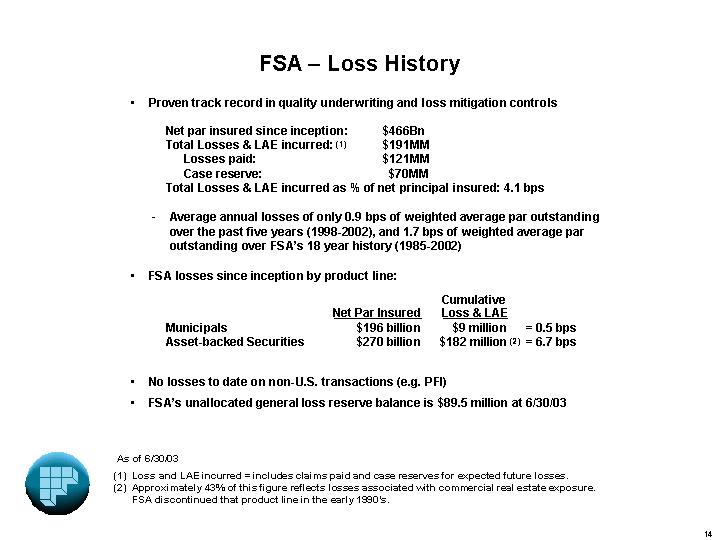

• Proven track record in quality underwriting and loss mitigation controls

Net par insured since inception: |

| $ | 466 | Bn |

Total Losses & LAE incurred: (1) |

| $ | 191 | MM |

Losses paid: |

| $ | 121 | MM |

Case reserve: |

| $ | 70 | MM |

Total Losses & LAE incurred as % of net principal insured: 4.1 bps

• Average annual losses of only 0.9 bps of weighted average par outstanding over the past five years (1998-2002), and 1.7 bps of weighted average par outstanding over FSA’s 18 year history (1985-2002)

• FSA losses since inception by product line:

|

| Net Par Insured |

| Cumulative |

| |||

|

|

|

|

|

| |||

Municipals |

| $ | 196 | billion | $ | 9 | million | = 0.5 bps |

Asset-backed Securities |

| $ | 270 | billion | $ | 182 | million(2) | = 6.7 bps |

• No losses to date on non-U.S. transactions (e.g. PFI)

• FSA’s unallocated general loss reserve balance is $89.5 million at 6/30/03

As of 6/30/03

(1) Loss and LAE incurred = includes claims paid and case reserves for expected future losses.

(2) Approximately 43% of this figure reflects losses associated with commercial real estate exposure.

FSA discontinued that product line in the early 1990’s.

14

FSA’s Loss History vs. U.S. Banks

1991-2002

[CHART]

1991 - 2002 FSA Weighted Avg Annual Losses = 1.8 bps

Despite the stressful economic environment and related poor credit conditions over the past few years, FSA’s losses have remained consistent with historic levels.

(1) Source: FDIC reports. Information from FDIC available beginning in 1991

(2) Excludes FSA’s single-name credit default swap termination charge of $42 million

15

Priority Number One:

Preservation of Aaa/AAA Capital Strength

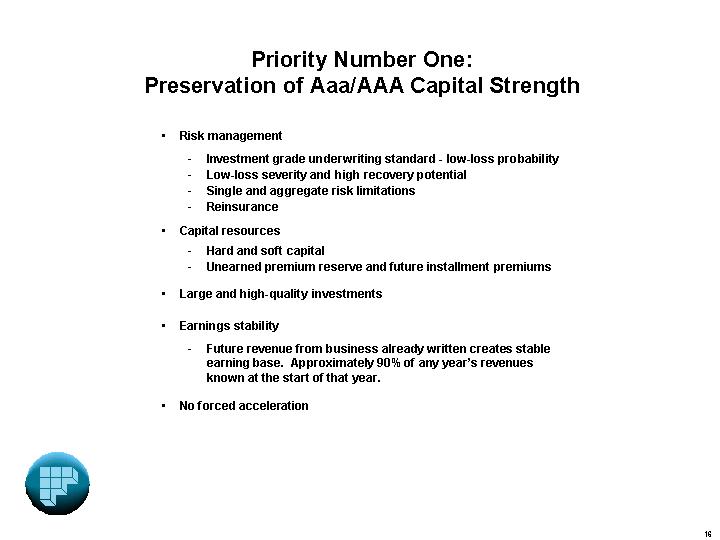

• Risk management

• Investment grade underwriting standard - low-loss probability

• Low-loss severity and high recovery potential

• Single and aggregate risk limitations

• Reinsurance

• Capital resources

• Hard and soft capital

• Unearned premium reserve and future installment premiums

• Large and high-quality investments

• Earnings stability

• Future revenue from business already written creates stable earning base. Approximately 90% of any year’s revenues known at the start of that year.

• No forced acceleration

16

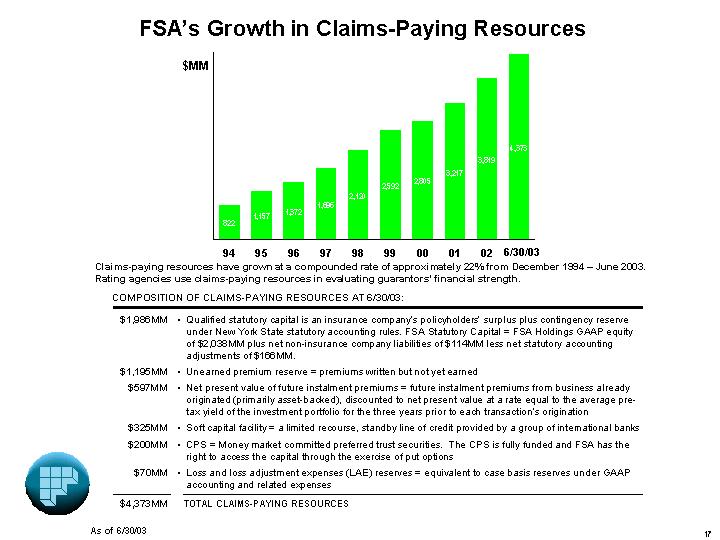

FSA’s Growth in Claims-Paying Resources

[CHART]

Claims-paying resources have grown at a compounded rate of approximately 22% from December 1994 – June 2003. Rating agencies use claims-paying resources in evaluating guarantors’ financial strength.

COMPOSITION OF CLAIMS-PAYING RESOURCES AT 6/30/03: |

$ | 1,986MM | • | Qualified statutory capital is an insurance company’s policyholders’ surplus plus contingency reserve under New York State statutory accounting rules. FSA Statutory Capital = FSA Holdings GAAP equity of $2,038MM plus net non-insurance company liabilities of $114MM less net statutory accounting adjustments of $166MM. |

|

|

| |

$ | 1,195MM | • | Unearned premium reserve = premiums written but not yet earned |

|

|

| |

$ | 597MM | • | Net present value of future instalment premiums = future instalment premiums from business already originated (primarily asset-backed), discounted to net present value at a rate equal to the average pretax yield of the investment portfolio for the three years prior to each transaction’s origination |

|

|

| |

$ | 325MM | • | Soft capital facility = a limited recourse, standby line of credit provided by a group of international banks |

|

|

| |

$ | 200MM | • | CPS = Money market committed preferred trust securities. The CPS is fully funded and FSA has the right to access the capital through the exercise of put options |

|

|

| |

$ | 70MM | • | Loss and loss adjustment expenses (LAE) reserves = equivalent to case basis reserves under GAAP accounting and related expenses |

|

|

| |

$ | 4,373MM |

| TOTAL CLAIMS-PAYING RESOURCES |

As of 6/30/03

17

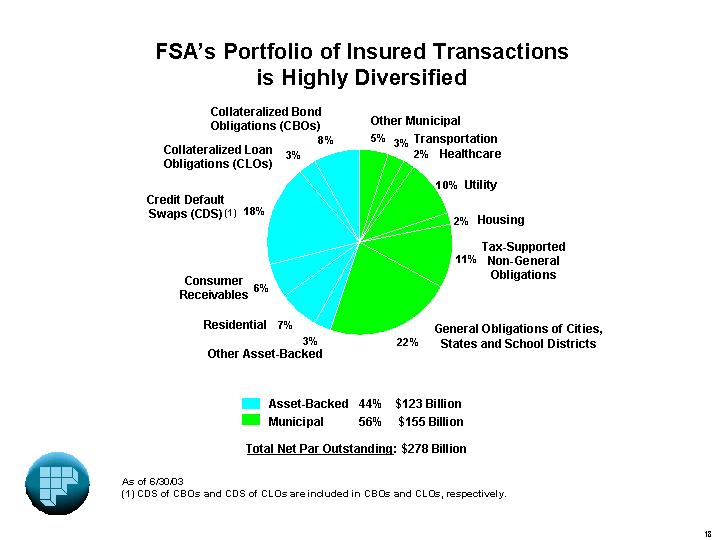

FSA’s Portfolio of Insured Transactions

is Highly Diversified

[CHART]

Total Net Par Outstanding: $278 Billion

As of 6/30/03

(1) CDS of CBOs and CDS of CLOs are included in CBOs and CLOs, respectively.

18

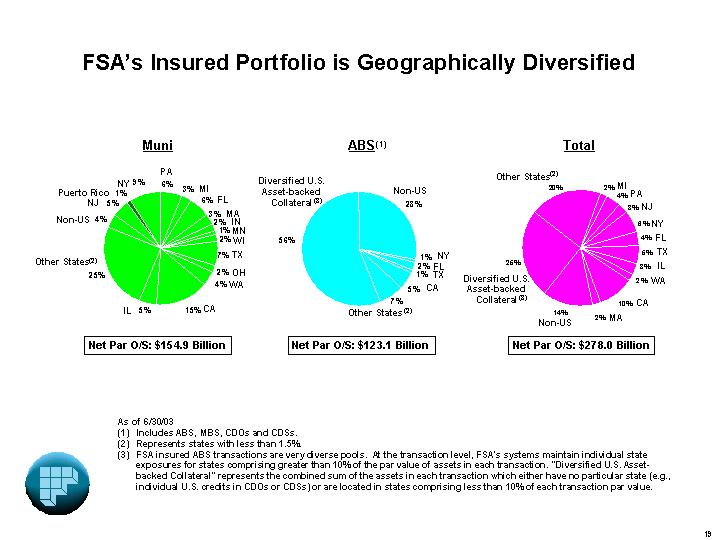

FSA’s Insured Portfolio is Geographically Diversified

Muni |

| ABS(1) |

| Total |

|

|

|

|

|

[CHART] |

| [CHART] |

| [CHART] |

|

|

|

|

|

Net Par O/S: $154.9 Billion |

| Net Par O/S: $123.1 Billion |

| Net Par O/S: $278.0 Billion |

As of 6/30/03

(1) Includes ABS, MBS, CDOs and CDSs.

(2) Represents states with less than 1.5%.

(3) FSA insured ABS transactions are very diverse pools. At the transaction level, FSA’s systems maintain individual state exposures for states comprising greater than 10% of the par value of assets in each transaction. “Diversified U.S. Asset-backed Collateral” represents the combined sum of the assets in each transaction which either have no particular state (e.g., individual U.S. credits in CDOs or CDSs) or are located in states comprising less than 10% of each transaction par value.

19

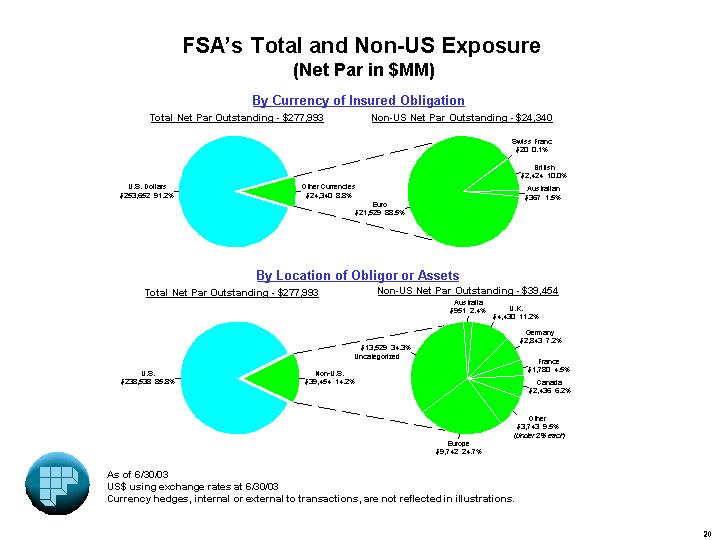

FSA’s Total and Non-US Exposure

(Net Par in $MM)

By Currency of Insured Obligation

Total Net Par Outstanding - $277,993 |

| Non-US Net Par Outstanding - $24,340 |

|

|

|

[CHART] |

| [CHART] |

|

|

|

By Location of Obligor or Assets | ||

Total Net Par Outstanding - $277,993 |

| Non-US Net Par Outstanding - $39,454 |

|

|

|

[CHART] |

| [CHART] |

As of 6/30/03

US$ using exchange rates at 6/30/03

Currency hedges, internal or external to transactions, are not reflected in illustrations.

20

FSA’s Insured Portfolio

Categorized by Shadow Rating

(Net Par Outstanding)

Municipal |

| ABS (1) |

| Overall Combined (1) |

|

|

|

|

|

[CHART] |

| [CHART] |

| [CHART] |

The pie charts on this page demonstrate the high quality of FSA’s underlying transactions, expressed as shadow ratings.

FSA utilizes layered loss reinsurance for many of its ABS transactions. Layered loss reinsurance reduces risk to FSA, which is often reflected in a higher shadow rating assigned to FSA for a given transaction.

As of 6/30/03

(1) Reflects benefit of layered loss reinsurance.

21

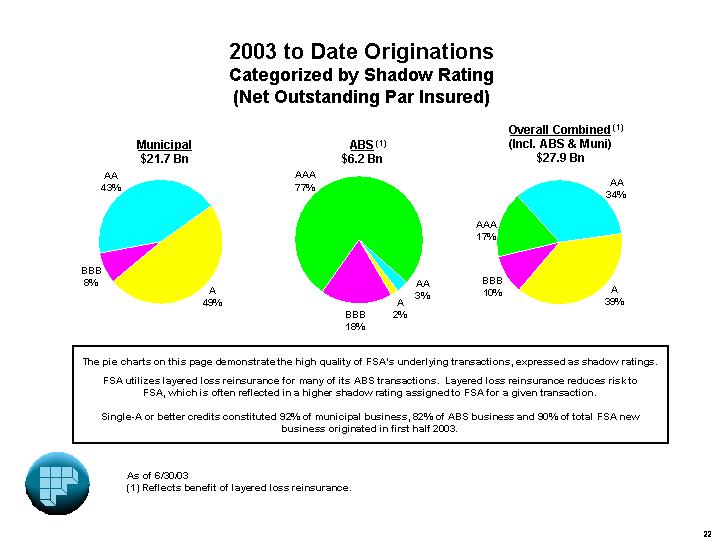

2003 to Date Originations

Categorized by Shadow Rating

(Net Outstanding Par Insured)

Municipal |

| ABS (1) |

| Overall Combined(1) |

|

|

|

|

|

[CHART] |

| [CHART] |

| [CHART] |

The pie charts on this page demonstrate the high quality of FSA’s underlying transactions, expressed as shadow ratings.

FSA utilizes layered loss reinsurance for many of its ABS transactions. Layered loss reinsurance reduces risk to FSA, which is often reflected in a higher shadow rating assigned to FSA for a given transaction.

Single-A or better credits constituted 92% of municipal business, 82% of ABS business and 90% of total FSA new business originated in first half 2003.

As of 6/30/03

(1) Reflects benefit of layered loss reinsurance.

22

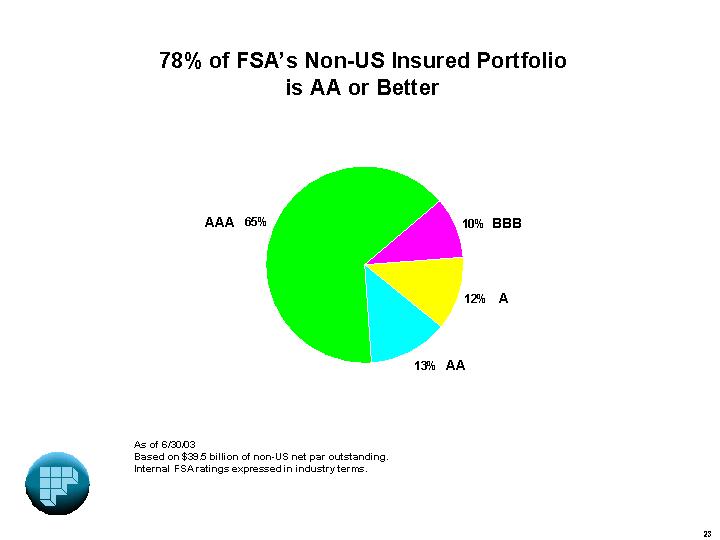

78% of FSA’s Non-US Insured Portfolio is AA or Better

[CHART]

As of 6/30/03

Based on $39.5 billion of non-US net par outstanding.

Internal FSA ratings expressed in industry terms.

23

• Single Risk Limitations

• Layered Loss Reinsurance

[CHART]

Example: | |

|

|

• | $ 100MM in assets |

|

|

• | FSA insured $97MM tranche, which is shadow-rated BBB |

|

|

• | $ 3MM subordinate tranche, (not insured by FSA) and excess spread provide first coverage for transaction losses |

As a result of layered loss reinsurance, FSA increases FSA’s amount of credit enhancement protection to 8% (3% subordinate tranche plus 5% layered loss reinsurance) from 3%, thereby effectively increasing the FSA shadow rating for this transaction to AA from BBB. In this example, layered loss reinsurance also decreases FSA’s credit gap, creating more capacity for FSA to this particular seller/servicer. For BBB shadow-rated transactions, the aggregate dollar amount of the BBB-AAA credit gap for a given servicer shall not exceed 20% of FSA statutory capital.

24

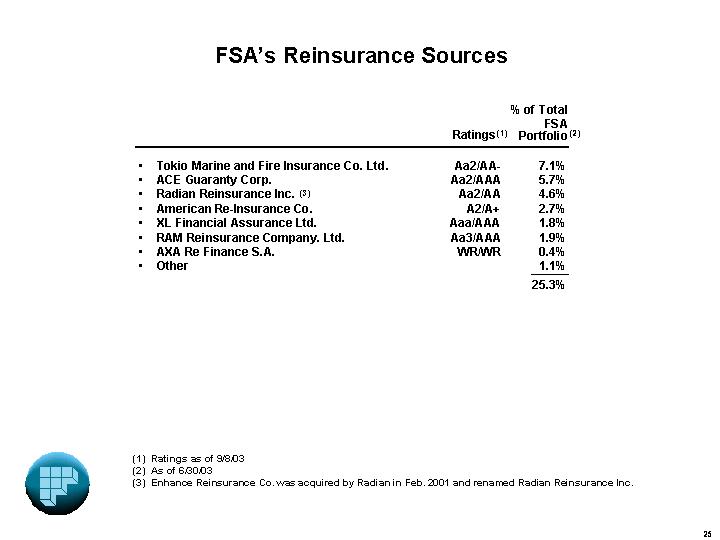

|

|

|

| Ratings (1) |

| % of Total |

|

|

|

|

|

|

|

|

|

• |

| Tokio Marine and Fire Insurance Co. Ltd. |

| Aa2/AA- |

| 7.1 | % |

• |

| ACE Guaranty Corp. |

| Aa2/AAA |

| 5.7 | % |

• |

| Radian Reinsurance Inc. (3) |

| Aa2/AA |

| 4.6 | % |

• |

| American Re-Insurance Co. |

| A2/A+ |

| 2.7 | % |

• |

| XL Financial Assurance Ltd. |

| Aaa/AAA |

| 1.8 | % |

• |

| RAM Reinsurance Company. Ltd. |

| Aa3/AAA |

| 1.9 | % |

• |

| AXA Re Finance S.A. |

| WR/WR |

| 0.4 | % |

• |

| Other |

|

|

| 1.1 | % |

|

|

|

|

|

| 25.3 | % |

(1) Ratings as of 9/8/03

(2) As of 6/30/03

(3) Enhance Reinsurance Co. was acquired by Radian in Feb. 2001 and renamed Radian Reinsurance Inc.

25

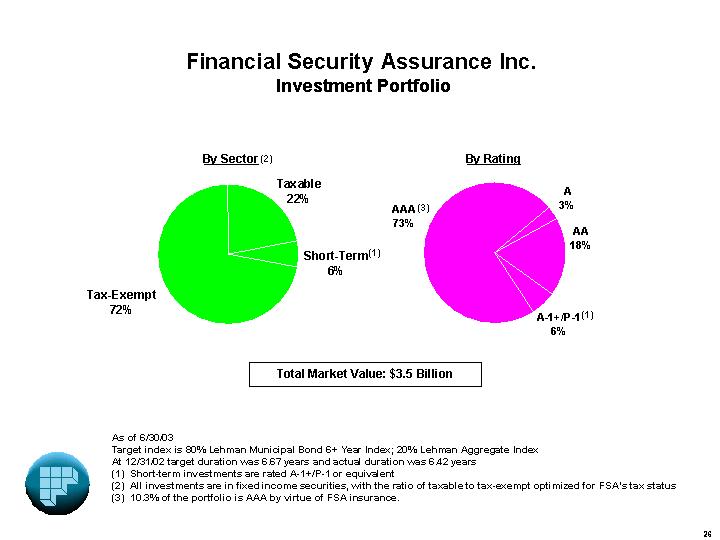

Financial Security Assurance Inc.

Investment Portfolio

By Sector(2) |

| By Rating |

|

|

|

[CHART] |

| [CHART] |

Total Market Value: $3.5 Billion

As of 6/30/03

Target index is 80% Lehman Municipal Bond 6+ Year Index; 20% Lehman Aggregate Index At 12/31/02 target duration was 6.67 years and actual duration was 6.42 years

(1) Short-term investments are rated A-1+/P-1 or equivalent

(2) All investments are in fixed income securities, with the ratio of taxable to tax-exempt optimized for FSA’s tax status

(3) 10.3% of the portfolio is AAA by virtue of FSA insurance.

26

FSA’s New Business Revenue Growth

is Strong and Diverse…

[CHART]

As of 6/30/03

27

…Creating a Stable Revenue Base for FSA

Approximately 90% of any Year’s Revenues are Known at Start of that Year

Revenues if FSA wrote no |

| If FSA continues to write at 2002 levels, |

|

|

|

[CHART] |

| [CHART] |

Assumes no transaction or portfolio losses or other adverse factors. Also assumes no new business growth or portfolio gains or other positive factors. For all these reasons, these charts are not predictors of future performance.

28

29

• Municipal / Governmental: Financial guaranty insurance policies on municipal securities

• Public Finance: bonds issued by governmental entities (general obligation, revenue bonds)

• Other Municipal Finance: bonds issued by not-for-profit entities operating essential public services (e.g., healthcare)

• Infrastructure Finance: essential infrastructure financings (PFI / PPP / Project Finance)

• ABS: Financial guaranty insurance policies on asset-backed securities

• Consumer receivables (auto loans, credit cards, etc.)

• Residential mortgage-backed securities

• Pooled corporate (CDOs, CDSs, etc.)

• Other asset-backed

• Financial Products

• Guaranteed Investment Contracts (GICs)

• Variable Interest Entities (SPEs)

30

• General Obligations

• Secured by municipality’s pledge to levy taxes to service debt

• Other Tax-Supported Issues

• Secured by specific tax revenues, such as sales taxes or special assessments

• Revenue Bonds

• Secured by dedicated revenue streams from essential public services such as highway tolls, mass transit fares, airport revenues, electricity receivables, etc.

• Affordable Housing Bonds

• Secured by revenues from single-family and multi-family housing programs of state and local housing finance agencies (generally subsidized to produce below-market rents or loans)

• FSA losses from inception through 6/30/03 (including case reserves for future losses) 0.5 bps ($9MM)

• According to Moody’s, municipal bonds have experienced lower loss rates and higher recover rates than Aaa rated corporate bonds (only 18 issuers from 1970 to 2000)(1)

(1) “Moody’s U.S. Municipal Bond Rating Scale”, November 2002.

As of 6/30/03

31

International Infrastructure Finance

(PFI / Project Finance)

• Net exposure of 1.0% of total portfolio

• Conservative underwriting standards

• No currency mismatch

• Sovereign foreign and local currency ratings to be at least investment-grade (100% AA or better domestic currency ratings)

• Essential public facilities

• Appropriate structures to mitigate risks

• Extensive use of reinsurance arrangements

• PFI: UK-type Public Private Partnership with no material revenue risk

• Project Finance: limited to essential infrastructure concession-based projects (e.g., government accommodations, public hospitals, toll roads)

• No losses to date

As of 6/30/03

32

• Consumer Receivables (autos and credit cards) - secured by diversified pools of loans to individuals, collateralized by:

• Security interests in automobiles in the case of autos

• Overcollateralization of insured notes

• Cash reserves

• Excess interest spread

• Mortgages - secured by diversified pools of residential mortgage loans to homeowners. Includes home equity loans, home equity lines of credit, NIMs, jumbo and Alt. A mortgages collateralized by:

• Mortgage filed against the homes

• Overcollateralization of insured notes

• Excess interest spread

• Pooled corporates - secured by diversified pools of corporate loans, corporate bonds or other corporate obligations, collateralized by:

• Overcollateralization of insured notes and excess interest spread with CBOs and CLOs

• First loss deductibles with CDS

• FSA losses from inception through 6/30/03 (including case reserves for future losses) 6.7 bps ($182MM)(1)

(1) Approximately 43% of this figure reflects losses associated with commercial real estate exposure.

FSA discontinued that product line in the early 1990’s.

33

Guaranteed Investment Contracts (GICs)

• FSA combines low cost of funding with investments in high quality, liquid ABS/MBS to earn an attractive Net Interest Margin (NIM)

• Structure

• FSA receives funds and, in return, issues a GIC

• FSA invests proceeds to earn NIM

• Credit exposure of the GIC invested assets are included in FSA’s reported leverage

• The rating agencies review and apply capital charges to these risks

• Two primary funding channels

• Municipal GICs – sub-LIBOR funding available because U.S. tax-exempt municipal issuers are subject to tax arbitrage rules limiting returns

• Structured GICs – attractive funding available because of need for AAA certainty in one component of larger, complex transaction

• Investment strategy

• At 6/30/03, $2.84 Bn in GICs principal outstanding

• All assets and liabilities swapped to floating rate – eliminating material interest rate risk

• Asset duration equal to or shorter than funding

• Focus on ABS investments to maximize use of FSA analytical skills and market knowledge

• Very high credit standards (underlying ratings currently 97% AAA)*

* 32% of portfolio is AAA by virtue of FSA insurance.

34

Variable Interest Entities (SPE)

Since all investments (other than high-quality, short-term investments in the SPEs) are insured by FSA, the rating agencies incorporate these risks in their analysis of FSA’s insured portfolio.

Assets in these programs go through the same underwriting and senior management approval process as all other securities insured by FSA.

Credit exposure of the SPE invested assets are included in FSA’s reported leverage.

In January 2003, FASB issued Interpretation No. 46 on “Consolidation of Variable Interest Entities”. FSA intends to comply with the new requirements.

• FSA Global Funding Limited (“FSA Global”): Established in 1998, FSA Global issues FSA-insured medium-term notes through a process known as “reverse inquiry” (meaning that the investor requests the issuance of a note to suit its own specific investments needs – resulting in lower-than-market funding costs for FSA). Proceeds from these notes are invested in FSA-insured obligations, have cash flow that substantially match those of the FSA issued notes (matched funding of assets and liabilities) and produce a positive interest margin, which results in additional remuneration on an existing risk. At 6/30/03 liabilities were $2.2 Bn. (1)

• Canadian Global Funding Corporation (“Canadian Global”): Established in 1994, Canadian Global was established to provide a source of funded liquidity to refinance FSA-insured transactions that experienced difficulty in meeting debt service obligations. Canadian Global invests its undeployed funds in high-quality, short-term investments. At 6/30/03, the amount of this facility was $186.9 MM, of which $125.2 MM was unutilized. The facility expires in 2004.

(1) Excludes $7.5 Bn in economically defeased tax lease transactions. The $7.5 Bn receivable to Global is offset by a corresponding note issued by Global to Premier International Funding Co. – a company whose payment obligations are insured by FSA, that acts as payment undertaker in leverage lease transactions.

35

Monoline Financial Guarantor Comparison

36

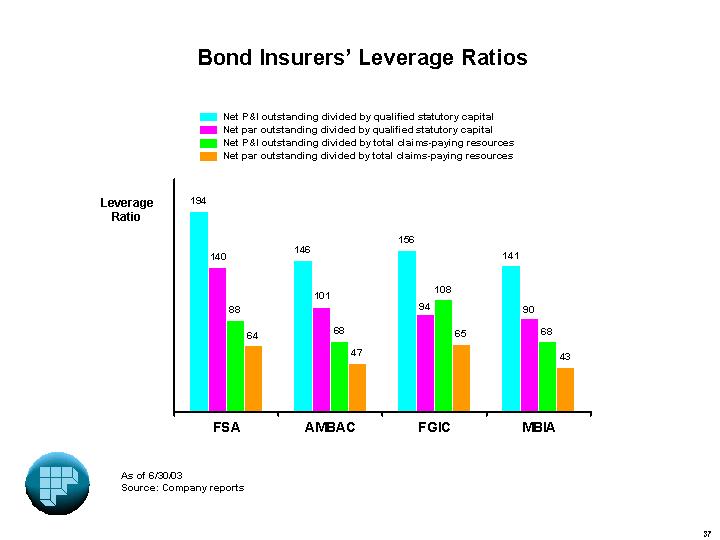

Bond Insurers’ Leverage Ratios

[CHART]

As of 6/30/03

Source: Company reports

37

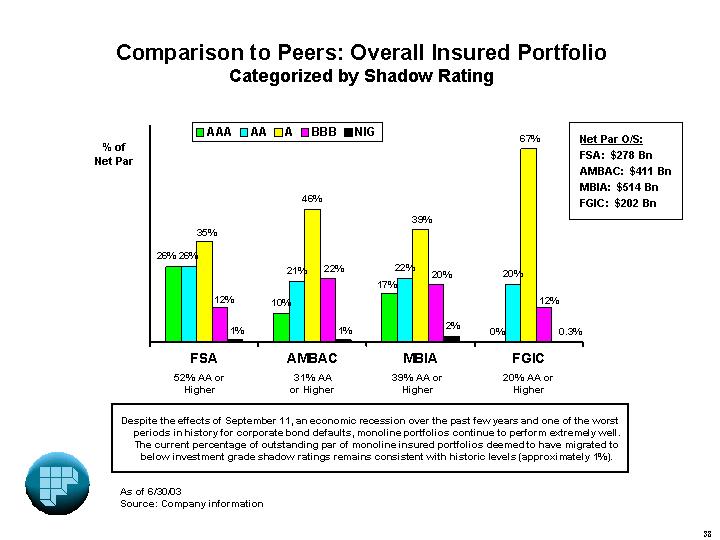

Comparison to Peers: Overall Insured Portfolio

Categorized by Shadow Rating

[CHART]

Despite the effects of September 11, an economic recession over the past few years and one of the worst periods in history for corporate bond defaults, monoline portfolios continue to perform extremely well. The current percentage of outstanding par of monoline insured portfolios deemed to have migrated to below investment grade shadow ratings remains consistent with historic levels (approximately 1%).

As of 6/30/03

Source: Company information

38

FSA Has One of the Highest Quality Insured Portfolios

Based on S&P’s Capital Charges

Muni

[CHART]

ABS

[CHART]

FSA’s capital charges are among the lowest in both the municipal and asset-backed sectors, signifying the most conservative underwriting standards in the industry.

Weighted average capital charge on all outstanding issues, reported by S&P in June 2003 in its annual review of each company (as of 12/31/02).

39

[CHART]

S&P Depression Model Format:

• Simulates losses in a 4-year “AAA” depression (i.e. only AAA underlying credits are certain to survive without a claim on the insurer)

• Depression begins 3 years in the future

• Each insurer is assumed to grow its originations by 15% annually during those 3 years leading up to the start of the depression

• During 4-year depression, losses equal 100% of capital charges (existing and projected exposure)

• Investments and reinsurance also experience loss

• Capital includes all claims-paying resources, including soft capital facilities

• Must survive this “depression scenario” with 25% more claims-paying resources than necessary to cover 100% of losses

S&P’s Margin of Safety Model shows FSA can withstand claims in excess of 150% of those incurred in a

“Triple-A depression.”

Source: S&P, June 2003 (as of 12/31/02).

40

• Monte Carlo estimate of the probability distribution of potential credit losses on the existing portfolio

• Each (obligor-based) exposure is defined by its

• Net par (adjusted for benefit from reinsurance)

• Expected default rate (rating, maturity, sector-specific)

• Expected loss severity (PV concept, sector-specific)

• Sources of correlation risk explicitly modeled

• Seller/servicer risk concentrations

• Country-level emerging market concentrations

• Industry risk concentrations

• Macroeconomic volatility

41

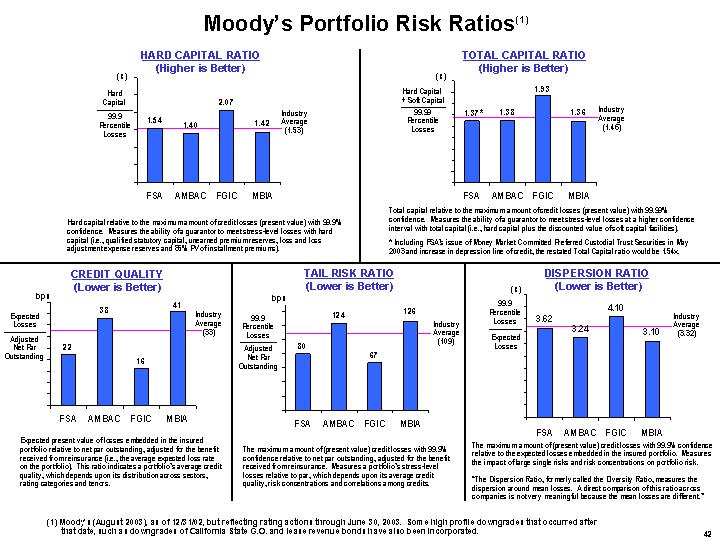

Moody’s Portfolio Risk Ratios (1)

HARD CAPITAL RATIO

(Higher is Better)

[CHART]

Hard capital relative to the maximum amount of credit losses (present value) with 99.9% confidence. Measures the ability of a guarantor to meet stress-level losses with hard capital (i.e., qualified statutory capital, unearned premium reserves, loss and loss adjustment expense reserves and 85% PV of installment premiums).

TOTAL CAPITAL RATIO

(Higher is Better)

[CHART]

Total capital relative to the maximum amount of credit losses (present value) with 99.99% confidence. Measures the ability of a guarantor to meet stress-level losses at a higher confidence interval with total capital (i.e., hard capital plus the discounted value of soft capital facilities).

* Including FSA’s issue of Money Market Committed Preferred Custodial Trust Securities in May 2003 and increase in depression line of credit, the restated Total Capital ratio would be 1.54x.

CREDIT QUALITY

(Lower is Better)

[CHART]

Expected present value of losses embedded in the insured portfolio relative to net par outstanding, adjusted for the benefit received from reinsurance (i.e., the average expected loss rate on the portfolio). This ratio indicates a portfolio’s average credit quality, which depends upon its distribution across sectors, rating categories and tenors.

TAIL RISK RATIO

(Lower is Better)

[CHART]

The maximum amount of (present value) credit losses with 99.9% confidence relative to net par outstanding, adjusted for the benefit received from reinsurance. Measures a portfolio’s stress-level losses relative to par, which depends upon its average credit quality, risk concentrations and correlations among credits.

DISPERSION RATIO

(Lower is Better)

[CHART]

The maximum amount of (present value) credit losses with 99.9% confidence relative to the expected losses embedded in the insured portfolio. Measures the impact of large single risks and risk concentrations on portfolio risk.

“The Dispersion Ratio, formerly called the Diversity Ratio, measures the dispersion around mean losses. A direct comparison of this ratio across companies is not very meaningful because the mean losses are different.”

(1) Moody’s (August 2003), as of 12/31/02, but reflecting rating actions through June 30, 2003. Some high profile downgrades that occurred after that date, such as downgrades of California State G.O. and lease revenue bonds have also been incorporated.

42

A: ABS Transactions – FSA’s Underwriting Approach

B: CDO Portfolio – Overview

C: Monoline Default Swap Spreads

D: Municipal Bond Industry Loss and Recovery Rates

E: What a Typical Guarantee Covers

F: Recent Rating Agency Comments

43

ABS Transactions – FSA’s Underwriting Approach

44

• Due diligence staff responsible solely for conducting loan file reviews

• On-site operational reviews to evaluate the quality of the servicers’ operations

• Loan charge-off reviews to evaluate servicers’ adherence to collection procedures and to develop expected loss severity assumptions

• Corporate Underwriting Research Group responsible for performing extensive corporate credit review of the issuer/servicer to ascertain financial stability and management expertise

• In-house attorneys responsible for legal aspects of document review and legal structuring of transaction

45

• Minimize direct corporate exposures

• Bankruptcy remote SPVs

• Term to term servicing agreements

• Maintain active relationship with back-up servicers

• Transactions structured to improve over time

• Credit enhancement levels of approximately 2-5x coverage of expected losses

• Use of excess spread and reserves to create additional protection

• Cross-collateralization structures with some issuers

• Use of performance trigger events to increase collateral protection

• 3-Month rolling average delinquency test

• Cumulative net losses as a % of original principal balance test

• 3-Month rolling average net losses as a % of declining principal balance test - “Step-up” required reserves and/or over-collateralization levels

• Use technical default triggers to protect FSA and bondholders in instances of negative performance

• Servicer termination rights

• FSA is the controlling party

• Supplemental premiums

• Use of 100% of asset cash flows to “turbo” principal payments on insured bonds

46

Organization

• 20+ professionals organized into teams of specialists that are responsible for monitoring each ABS transaction through maturity

Objectives

• Identify and intervene early in transactions not performing up to expectations

• Provide feedback to underwriting process to benefit future transactions

• Handle all post closing matters (amendments, waivers, etc.)

• Conduct on-site servicing reviews

• Monitor payments and compliance

• Update shadow ratings on transactions based upon actual versus originally expected performance and FSA coverage levels

• Recommend case specific reserves for transactions in which loss is probable and can be reasonably estimated

Performance

• Have successfully transferred servicing in auto, mortgage and CDO transactions

• Have detected misapplication of funds in transactions which led to corrective action prior to a “problem” developing

• Have worked with servicers to develop creative solutions to deficiencies

47

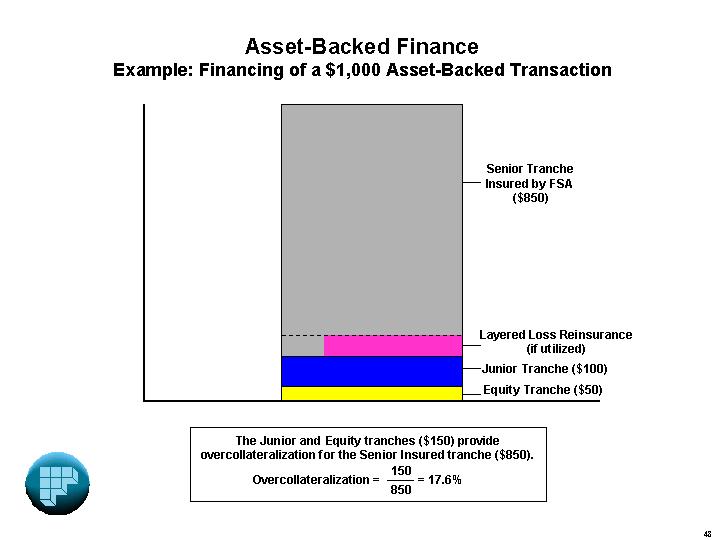

Asset-Backed Finance

Example: Financing of a $1,000 Asset-Backed Transaction

[CHART]

The Junior and Equity tranches ($150) provide

overcollateralization for the Senior Insured tranche ($850).

Overcollateralization = |

| 150 |

| = 17.6% |

| 850 |

|

48

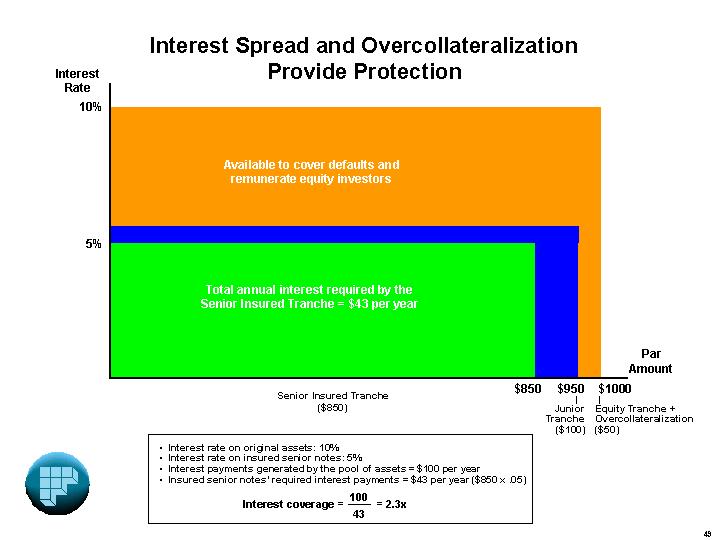

Interest Spread and Overcollateralization

Provide Protection

[CHART]

• Interest rate on original assets: 10%

• Interest rate on insured senior notes: 5%

• Interest payments generated by the pool of assets = $100 per year

• Insured senior notes’ required interest payments = $43 per year ($850 x ..05)

Interest coverage = |

| 100 |

| = 2.3x |

| 43 |

|

49

FSA Insured Auto Transaction

Example of FSA Performance Triggers

3 Month 31+ Day Delinquencies

[CHART]

Net Cumulative Losses

as % of Original Principal Balance

[CHART]

Cumulative Defaults

as % of Original Principal Balance

[CHART]

FSA’s ABS Surveillance Group monitors portfolio performance versus benchmarks established by FSA at the onset of the transaction. This transaction breached a Step-up Event (net cumulative loss trigger in Month 29 and a delinquency trigger in Month 32) and subsequently an I&I Event of Default (delinquency trigger in Month 33).

50

Effect of Trigger Being Breached

[CHART]

As illustrated on the prior page, the cumulative net losses and delinquencies on this transactions were higher than the cumulative net loss and delinquency benchmarks established by FSA when it underwrote the transaction. As a result, the spread account held for the benefit of FSA and the insured bondholders is required to increase to 11% of the outstanding pool balance from an original level of 7% of outstanding pool balance (a 57% increase).

51

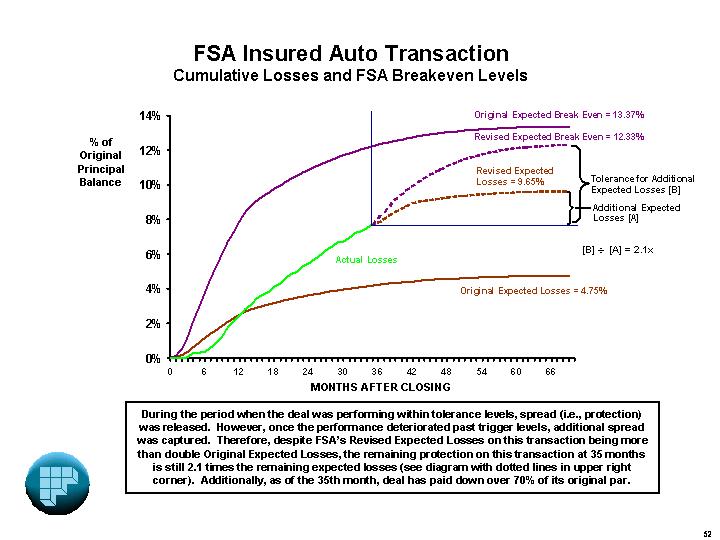

Cumulative Losses and FSA Breakeven Levels

[CHART]

MONTHS AFTER CLOSING

During the period when the deal was performing within tolerance levels, spread (i.e., protection) was released. However, once the performance deteriorated past trigger levels, additional spread was captured. Therefore, despite FSA’s Revised Expected Losses on this transaction being more than double Original Expected Losses, the remaining protection on this transaction at 35 months is still 2.1 times the remaining expected losses (see diagram with dotted lines in upper right corner). Additionally, as of the 35th month, deal has paid down over 70% of its original par.

52

FSA Credit Protection Multiple(1)

[CHART]

FSA’s credit protection multiple remains very strong despite the negative performance of the transaction. In addition, for ease of illustration, this example ignores the additional credit protection for this transaction provided by cross collateralization with several other transactions insured for this issuer.

53

CDO Portfolio - Overview

54

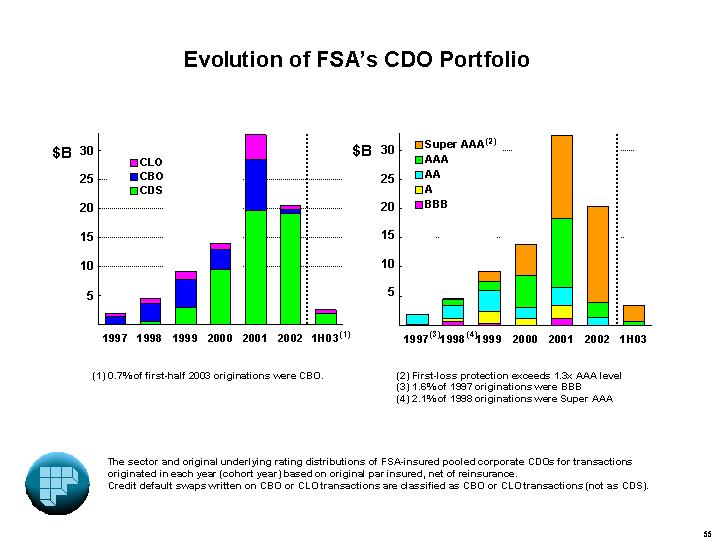

Evolution of FSA’s CDO Portfolio

[CHART]

(1) 0.7% of first-half 2003 originations were CBO.

[CHART]

(2) First-loss protection exceeds 1.3x AAA level

(3) 1.6% of 1997 originations were BBB

(4) 2.1% of 1998 originations were Super AAA

The sector and original underlying rating distributions of FSA-insured pooled corporate CDOs for transactions originated in each year (cohort year) based on original par insured, net of reinsurance.

Credit default swaps written on CBO or CLO transactions are classified as CBO or CLO transactions (not as CDS).

55

CLO

$8.9 Bn

[CHART]

CBO

$20.0 Bn

[CHART]

CDS

$49.2 Bn

[CHART]

Combined Total

$78.1 Bn

[CHART]

As of 6/30/03

*First-loss protection exceeds 1.3x level required for Aaa/AAA underlying rating.

CDS of CBOs and CDS of CLOs are included in CBOs and CLOs, respectively.

56

Moody’s U.S. One-Year Speculative Grade Default Rates

[CHART]

• 2001 peak default rate is similar to the 1991 level

• Moody’s U.S. default rate hit 11.1% in 2001 and declined to 7.3% in 2002 and to 5.8% for 2003(1)

(1) For 12 months trailing through August 2003.

Source: Moody’s

57

Monoline Default Swap Spreads

58

Monoline Default Swap Spreads

• Default swap spreads on monolines widened from 35 to 40 bps in 1Q02 to a high of almost 200 bps (for one monoline) in 3Q02 before tightening to the current level of 35 to 57 bps (September ’03)

• Drivers of monoline default swap spreads

• Few natural sellers of monoline protection (supply/demand inbalance)

• Thinly traded market

• Difficulty of quantifying “credit event” risk across the full spectrum of the monoline’s insured book

• Wide array of potential reference obligations and deliverable obligations (for settling a loss protection amount)

• Hedgers of specific obligations must evaluate joint probability of default of FSA and the insured underlying obligation

• Hedge fund speculation activity

• Despite volatility in monoline default swap spreads, spreads on monoline wrapped funded securities remain stable

59

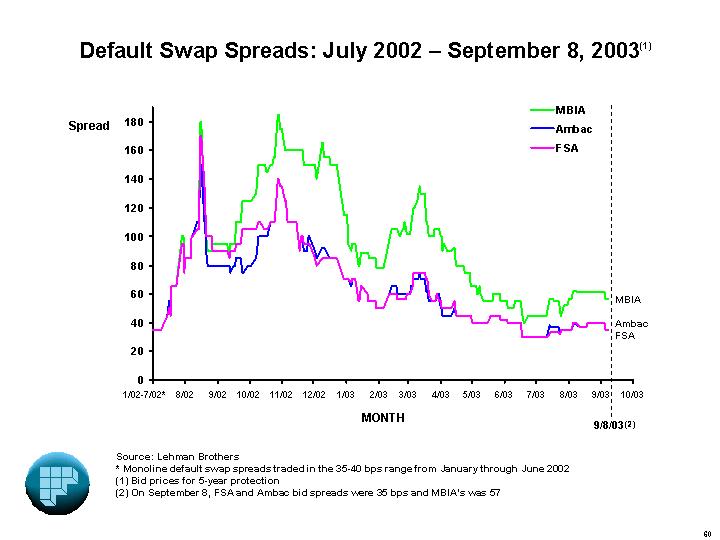

Default Swap Spreads: July 2002 — September 8, 2003(1)

[CHART]

Source: Lehman Brothers

* Monoline default swap spreads traded in the 35-40 bps range from January through June 2002

(1) Bid prices for 5-year protection

(2) On September 8, FSA and Ambac bid spreads were 35 bps and MBIA’s was 57

60

Municipal Bond Industry Loss and Recovery Rates

61

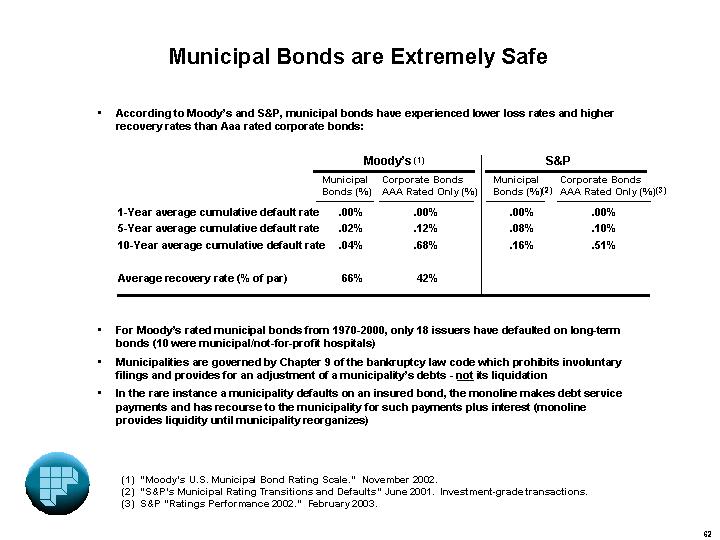

Municipal Bonds are Extremely Safe

• According to Moody’s and S&P, municipal bonds have experienced lower loss rates and higher recovery rates than Aaa rated corporate bonds:

|

| Moody’s (1) |

| S&P |

| ||||

|

| Municipal |

| Corporate Bonds |

| Municipal |

| Corporate Bonds |

|

|

|

|

|

|

|

|

|

|

|

1-Year average cumulative default rate |

| .00 | % | .00 | % | .00 | % | .00 | % |

5-Year average cumulative default rate |

| .02 | % | .12 | % | .08 | % | .10 | % |

10-Year average cumulative default rate |

| .04 | % | .68 | % | .16 | % | .51 | % |

|

|

|

|

|

|

|

|

|

|

Average recovery rate (% of par) |

| 66 | % | 42 | % |

|

|

|

|

• For Moody’s rated municipal bonds from 1970-2000, only 18 issuers have defaulted on long-term bonds (10 were municipal/not-for-profit hospitals)

• Municipalities are governed by Chapter 9 of the bankruptcy law code which prohibits involuntary filings and provides for an adjustment of a municipality’s debts - not its liquidation

• In the rare instance a municipality defaults on an insured bond, the monoline makes debt service payments and has recourse to the municipality for such payments plus interest (monoline provides liquidity until municipality reorganizes)

(1) “Moody’s U.S. Municipal Bond Rating Scale.” November 2002.

(2) “S&P’s Municipal Rating Transitions and Defaults” June 2001. Investment-grade transactions.

(3) S&P “Ratings Performance 2002.” February 2003.

62

What a Typical Guarantee Covers

63

What a Typical FSA Guarantee Covers*

Mortgage Transactions

• Timely payment of monthly interest at the note rate

• Timely payment of monthly scheduled principal (based on reductions to the mortgage pool balance) such that the outstanding principal balance of the FSA-Insured Notes is not greater than the outstanding principal balance of the mortgage pool collateral

• Ultimate payment of any outstanding principal balance of the FSA-Insured Notes on the final legal maturity date

Automobile Loan Transactions

• Timely payment of monthly interest at the note rate

• Timely payment of monthly scheduled principal (based on reductions to the automobile loan pool balance) such that, the ratio of the outstanding balance of the FSA-Insured Notes divided by the outstanding balance of the automobile loan pool is no less than the ratio existing at the time the FSA-insured notes were originally issued. (For example, assume $90MM of FSA-Insured Notes were issued and the initial automobile loan collateral pool was $100MM. Each month, FSA guarantees that the outstanding principal balance of the FSA-Insured Notes will never be greater than 90% of the outstanding principal balance of the automobile loan pool.)

• Ultimate payment of any outstanding principal balance of the FSA-Insured Notes on the final legal maturity date

Collateralized Debt Obligations

• Timely payment of monthly interest at the note rate

• Ultimate payment of the outstanding principal balance of the FSA-Insured Notes on the stated maturity date

* This page is intended to provide a general description of the most common forms of coverage provided by an FSA insurance policy within each of FSA’s three main ABS product lines. Certain policies issued by FSA may contain forms of coverage that differ from the forms described above.

64

The Value of FSA Insurance

• Irrevocable and unconditional guaranty of principal and interest

• FSA waives ALL defenses - including fraud, and non-payment of premiums

• Downgrade protection/market value protection

• 8.16% of U.S. ABS securities and 7.87% of U.S. CDO securities were downgraded by S&P in the first six months of 2003 (1)

• FSA’s underwriting process includes intensive due diligence and documentation which provides remedies and establishes FSA as the “controlling party”

• Unlike a trustee, FSA has capital at risk, and interests aligned with bondholders

• Active surveillance

• FSA’s surveillance team provides ongoing oversight of transaction servicer’s operations

• FSA’s quick remedial action (e.g. transfer of servicing) in certain ABS transactions has mitigated “headline risk” to bondholders

• FSA provides consultation for investors

(1) Source: S&P, based on number of ratings outstanding as of the beginning of the year

65

Recent Rating Agency Comments

66

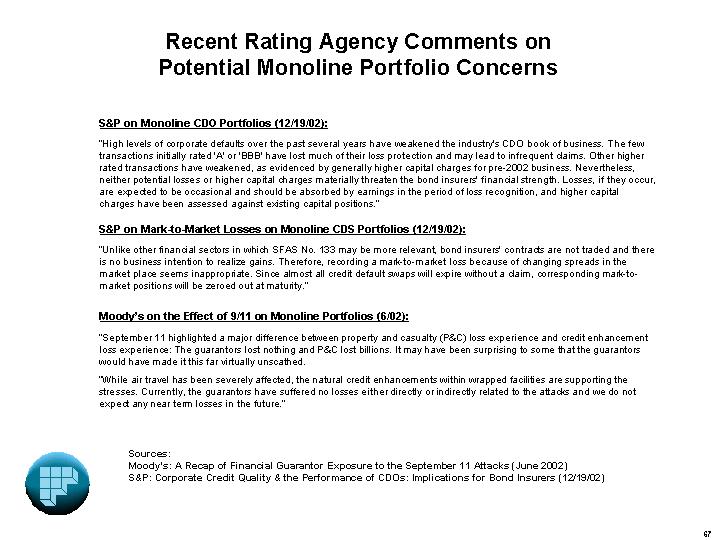

Recent Rating Agency Comments on

Potential Monoline Portfolio Concerns

S&P on Monoline CDO Portfolios (12/19/02):

“High levels of corporate defaults over the past several years have weakened the industry’s CDO book of business. The few transactions initially rated ‘A’ or ‘BBB’ have lost much of their loss protection and may lead to infrequent claims. Other higher rated transactions have weakened, as evidenced by generally higher capital charges for pre-2002 business. Nevertheless, neither potential losses or higher capital charges materially threaten the bond insurers’ financial strength. Losses, if they occur, are expected to be occasional and should be absorbed by earnings in the period of loss recognition, and higher capital charges have been assessed against existing capital positions.”

S&P on Mark-to-Market Losses on Monoline CDS Portfolios (12/19/02):

“Unlike other financial sectors in which SFAS No. 133 may be more relevant, bond insurers’ contracts are not traded and there is no business intention to realize gains. Therefore, recording a mark-to-market loss because of changing spreads in the market place seems inappropriate. Since almost all credit default swaps will expire without a claim, corresponding mark-to-market positions will be zeroed out at maturity.”

Moody’s on the Effect of 9/11 on Monoline Portfolios (6/02):

“September 11 highlighted a major difference between property and casualty (P&C) loss experience and credit enhancement loss experience: The guarantors lost nothing and P&C lost billions. It may have been surprising to some that the guarantors would have made it this far virtually unscathed.

“While air travel has been severely affected, the natural credit enhancements within wrapped facilities are supporting the stresses. Currently, the guarantors have suffered no losses either directly or indirectly related to the attacks and we do not expect any near term losses in the future.”

Sources:

Moody’s: A Recap of Financial Guarantor Exposure to the September 11 Attacks (June 2002)

S&P: Corporate Credit Quality & the Performance of CDOs: Implications for Bond Insurers (12/19/02)

67

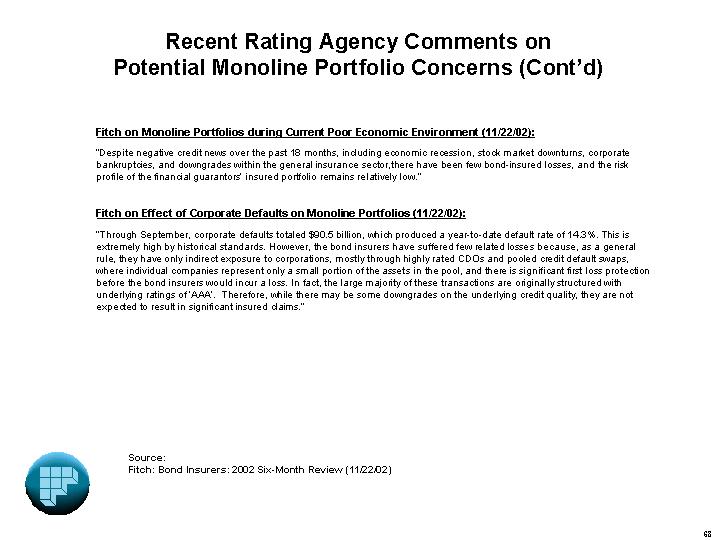

Fitch on Monoline Portfolios during Current Poor Economic Environment (11/22/02):

“Despite negative credit news over the past 18 months, including economic recession, stock market downturns, corporate bankruptcies, and downgrades within the general insurance sector,there have been few bond-insured losses, and the risk profile of the financial guarantors’ insured portfolio remains relatively low.”

Fitch on Effect of Corporate Defaults on Monoline Portfolios (11/22/02):

“Through September, corporate defaults totaled $90.5 billion, which produced a year-to-date default rate of 14.3%. This is extremely high by historical standards. However, the bond insurers have suffered few related losses because, as a general rule, they have only indirect exposure to corporations, mostly through highly rated CDOs and pooled credit default swaps, where individual companies represent only a small portion of the assets in the pool, and there is significant first loss protection before the bond insurers would incur a loss. In fact, the large majority of these transactions are originally structured with underlying ratings of ‘AAA’. Therefore, while there may be some downgrades on the underlying credit quality, they are not expected to result in significant insured claims.”

Source:

Fitch: Bond Insurers: 2002 Six-Month Review (11/22/02)

68

Additional Holding Company Information

69

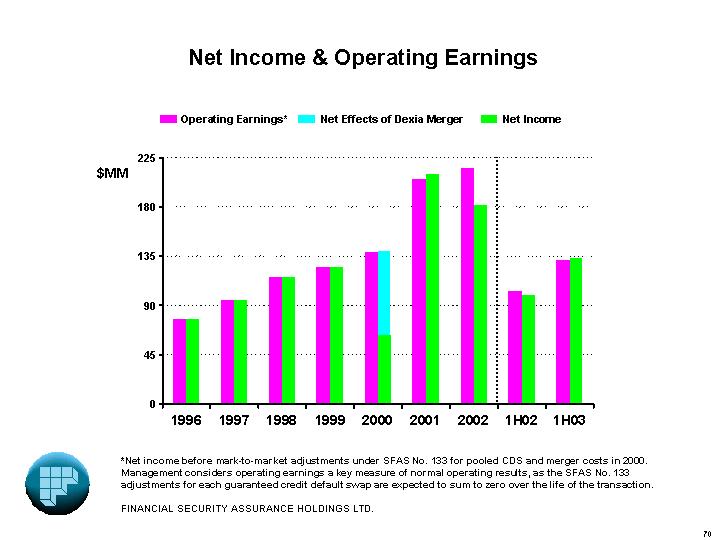

Net Income & Operating Earnings

[CHART]

*Net income before mark-to-market adjustments under SFAS No. 133 for pooled CDS and merger costs in 2000. Management considers operating earnings a key measure of normal operating results, as the SFAS No. 133 adjustments for each guaranteed credit default swap are expected to sum to zero over the life of the transaction.

FINANCIAL SECURITY ASSURANCE HOLDINGS LTD.

70

Book Value and Adjusted Book Value Per Share

Since the Merger with Dexia, FSA’s ABV Has Grown

at an Annualized Rate of 18.8%, BV at 17.3%*

[CHART]

Adjusted book value (ABV) per share at June 30, 2003 ($88.39) = Book value ($61.35) + after-tax net deferred premium revenue, net of deferred acquisition cost ($14.43) + PV of future installment premiums and net interest margin ($12.61).

Note that book value, by definition, is calculated after loss reserves.

* Growth rates include dividends

71

The Company relies upon the safe harbor for forward-looking statements provided by the Private Securities Litigation Reform Act of 1995. This safe harbor requires that the Company specify important factors that could cause actual results to differ materially from those contained in forward-looking statements made by or on behalf of the Company. Accordingly, forward-looking statements by the Company and its affiliates are qualified by reference to the following cautionary statements.

In its filings with the SEC, reports to investors, press releases and other written and oral communications, the Company from time to time makes forward-looking statements. Such forward-looking statements include, but are not limited to, (i) projections of revenues, income (or loss), earnings (or loss), dividends, market share or other financial forecasts; (ii) statements of plans, objectives or goals of the Company or its management, including those related to growth in adjusted book value or return on equity; and (iii) expected losses on, and adequacy of loss reserves for, insured transactions. Words such as “believes”, “anticipates”, “expects”, “intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements.

The Company cautions that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in forward-looking statements made by the Company. These factors include: (i) changes in capital requirements or other criteria of securities rating agencies applicable to financial guaranty insurers in general or to FSA specifically; (ii) competitive forces, including the conduct of other financial guaranty insurers in general; (iii) changes in domestic or foreign laws or regulations applicable to the Company, its competitors or its clients; (iv) changes in accounting principles or practices that may result in a decline in securitization transactions; (v) an economic downturn or other economic conditions (such as a rising interest rate environment) adversely affecting transactions insured by FSA or its investment portfolio; (vi) inadequacy of loss reserves established by the Company; (vii) temporary or permanent disruptions in cash flow on FSA-insured structured transactions attributable to legal challenges to such structures; (viii) downgrade or default of one or more of FSA’s reinsurers; (ix) the amount and nature of business opportunities that may be presented to the Company; (x) market conditions, including the credit quality and market pricing of securities issued; (xi) capacity limitations that may impair investor appetite for FSA-insured obligations; (xii) market spreads and pricing on insured credit default swap exposures, which may result in gain or loss due to mark-to-market accounting requirements; (xiii) prepayment speeds on FSA-insured asset-backed securities and other factors that may influence the amount of installment premiums paid to FSA; (xiv) changes in the value or performance of strategic investments made by the Company; and (xv) other factors, most of which are beyond the Company’s control. The Company cautions that the foregoing list of important factors is not exhaustive. In any event, such forward-looking statements made by the Company speak only as of the date on which they are made, and the Company does not undertake any obligation to update or revise such statements as a result of new information, future events or otherwise.

72