As filed with the Securities and Exchange Commission on January 6, 2025.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Smithfield Foods, Inc.

(Exact name of registrant as specified in its charter)

| Virginia | 2013 | 52-0845861 | ||||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) | ||||||

200 Commerce Street

Smithfield, Virginia 23430

(757) 365-3000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

C. Shane Smith

President and Chief Executive Officer

200 Commerce Street

Smithfield, Virginia 23430

(757) 365-3000

(Name, address, including zip code, and telephone number, including area code, of registrant’s agent for service)

With copies to:

Colin Diamond Brandon Bortner Alex Herman Paul Hastings LLP 200 Park Avenue New York, New York 10166 (212) 318-6000 | Andrew J. Pitts Ryan J. Patrone Cravath, Swaine & Moore LLP Two Manhattan West 375 Ninth Avenue New York, New York, 10001 (212) 474-1000 | |||||||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ☐ | Accelerated filer | o | ||||||||

| Non-accelerated filer | ☒ | Smaller reporting company | o | ||||||||

| Emerging growth company | o | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities nor a solicitation of an offer to buy these securities in any jurisdiction where the offer and sale is not permitted.

Preliminary Prospectus (Subject to completion, dated January 6, 2025)

Shares

Smithfield Foods, Inc.

Common Stock

This is the initial public offering of common stock of Smithfield Foods, Inc. We are offering shares of our common stock, and SFDS UK Holdings Limited (the “selling shareholder”), an indirect wholly owned subsidiary of our parent company, WH Group Limited (“WH Group”), is offering shares of our common stock. We will not receive any proceeds from the sale of stock by our selling shareholder.

There is currently no public market for shares of our common stock. We expect that the initial public offering price of our common stock will be between $ and $ per share. We have applied to list our common stock on the Nasdaq Global Select Market, under the symbol “SFD.” We will not consummate this offering of our common stock unless our common stock is approved for listing on the Nasdaq Global Select Market.

After the completion of this offering, WH Group will beneficially own approximately % of the voting power of our common stock (or approximately % if the underwriters exercise in full their option to purchase additional shares of our common stock). As a result, we will be a “controlled company” within the meaning of the corporate governance standards of The Nasdaq Stock Market LLC, or Nasdaq, and qualify for, and intend to rely on, exemptions from certain corporate governance requirements as described herein. See “Management—Controlled Company Exemption.” There is no single shareholder or group of shareholders which owns 50% or more of the voting power of WH Group as of the date of this prospectus. As a result, WH Group would not be considered a controlled company within the meaning of the corporate governance standards of Nasdaq.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 31 to read about factors you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission, or the SEC, nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | ||||||||||

| Initial public offering price | $ | $ | |||||||||

Underwriting discounts and commissions (1) | $ | $ | |||||||||

| Proceeds, before expenses, to us | $ | $ | |||||||||

| Proceeds, before expenses, to selling shareholder | $ | $ | |||||||||

________________

(1)See “Underwriting” for additional information regarding underwriting compensation.

At our request, the underwriters have reserved up to 2% of the shares of our common stock offered by this prospectus for sale at the initial public offering price through a directed share program to our directors, officers and certain of our employees. See “Underwriting—Directed Share Program.”

The selling shareholder has granted the underwriters a 30-day option from the date of this prospectus to purchase up to additional shares of our common stock. Such shares are offered by the selling shareholder at the initial public offering price listed on the cover page of this prospectus, less underwriting discounts and commissions.

The underwriters expect to deliver the shares on or about , 2025 through the book-entry facilities of The Depository Trust Company.

| Morgan Stanley | BofA Securities | Goldman Sachs & Co. LLC | ||||||

| Barclays | Citigroup | UBS Investment Bank | ||||||

| BNP PARIBAS | HSBC | |||||||

The date of this prospectus , 2025.

TABLE OF CONTENTS

| Page | |||||

i

We, the selling shareholder and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any amendment or supplement to this prospectus or any free writing prospectus prepared by us or on our behalf. We, the selling shareholder and the underwriters take no responsibility for, and cannot assure you as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares of our common stock offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so.

The information contained in this prospectus is current only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of shares of our common stock. Our business, results of operations or financial condition may have changed since that date.

We, the selling shareholder and the underwriters have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of our common stock and the distribution of this prospectus outside the United States.

ii

ABOUT THIS PROSPECTUS

Unless otherwise indicated or the context otherwise requires, references in this prospectus to “Smithfield,” “our company,” “we,” “us” and “our” refer to Smithfield Foods, Inc., a Virginia corporation and its consolidated subsidiaries.

Prior to August 26, 2024, we conducted business operations in the United States, Mexico and Europe. On August 26, 2024, we completed the carve out of our European operations, or the European Carve-out, pursuant to which we transferred our operations in Europe to WH Group. Following the European Carve-out, we principally engage in operations in the United States and Mexico. Unless otherwise expressly stated or the context otherwise requires, the description of our business included in this prospectus reflects our business after giving effect to the European Carve-out. The results of operations, assets and liabilities, and cash flows of the European operations as presented in our consolidated financial statements have been condensed into separate line items and presented in the consolidated statements of income, the consolidated balance sheets and the consolidated statements of cash flows, respectively, as discontinued operations, and this treatment has been applied retrospectively to all periods presented. Unless otherwise expressly stated, the financial information of our company included in this prospectus reflects the historical financial statements of Smithfield (which has been an indirect, wholly owned subsidiary of WH Group), as retroactively adjusted to remove the impact of the discontinued operations.

Industry and Market Data

Within this prospectus, we reference information and statistics regarding the market for our products. We have obtained some of this information and statistics from various independent third-party sources, including government agencies, independent industry publications, reports by market research firms and other independent sources. Some data and other information contained in this prospectus are also based on management’s estimates and calculations, which are derived from our review and interpretation of internal surveys and independent sources. Data regarding the industries in which we compete and our market position and market share within these industries are inherently imprecise and are subject to significant business, economic and competitive uncertainties beyond our control, but we believe they generally indicate size, position and market share within this industry. In addition, assumptions and estimates of our and our industries’ future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors. These and other factors could cause our future performance to differ materially from our assumptions and estimates. See “Forward-Looking Statements.”

The sources of certain statistical data, estimates and forecasts contained in this prospectus include the following independent industry publications or reports:

•Agriculture and Horticulture Development Board, “2022 pig cost of production in selected countries: Overview,” December 13, 2023;

•Business Research Insights, “Dry Sausage Market Size, Share, Growth, and Industry Analysis, By Type (Pork Dry Sausage, Beef Dry Sausage, Poultry Dry Sausage), By Application (Pizza, Ready to Eat Food, Meals), Regional Forecast to 2031,” last updated September 9, 2024;

•Circana Retail/Deli database, last accessed October 2024;

•Euromonitor International Limited, Global & U.S. Meat report;

•Euromonitor International Limited, Meat & Value-Added report;

•International Food Information Council, 2024 IFIC Food & Health Survey;

•Iowa State University forecasts – Study; Estimated Returns – Swine (Farrow to Finish) latest month data collected July 2024;

•Ipsos, “Nearly nine in ten Americans consume meat as part of their diet,” https://www.ipsos.com/en-us/news-polls/nearly-nine-ten-americans-consume-meat-part-their-diet, May 12, 2021;

iii

•Mintel Group – Reports:

•Protein and Protein Alternatives – US – 2024 (April 24, 2024);

•The Future of Foodservice – US – 2024 (January 31, 2024);

•Bacon and Lunchmeat – US – 2023 (September 30, 2023);

•Hot Dogs and Sausages – US – 2023;

•Protein and Protein Alternatives – US – 2022; and

•Grocery Retailing – US – 2024 (June 26, 2024);

•National Hog Farmer, “NHF Snapshot - Packer Capacity,” May/June 2024 Issue;

•Organization for Economic Co-operation and Development, “Indicators – Meat Consumption, OECD-FAO Agricultural Outlook,” 2023-2032;

•Progressive Grocer, “The PG 100: The Top Food Retailers in North America,” May 20, 2024;

•U.S. Department of Agriculture, “Interagency Agricultural Projections Committee,” October 2023; and

•U.S. Department of Agriculture, “USDA Agricultural Projects to 2033,” February 2024.

Trademarks, Trade Names, Service Marks and Copyrights

We own or have rights to use various trademarks, tradenames, service marks and copyrights, which are protected under applicable intellectual property laws, including, for example: Smithfield, Eckrich, Farmland, Armour, Farmer John, Kretschmar, John Morrell, Cook’s, Gwaltney, Carando, Margherita, Curly’s and Smithfield Culinary. This prospectus also contains trademarks, tradenames, service marks and copyrights of other companies, which are, to our knowledge, the property of their respective owners. Solely for convenience, certain trademarks, tradenames, service marks and copyrights referred to in this prospectus may appear without the ©, ®, and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, tradenames, service marks and copyrights. We do not intend our use or display of other parties’ trademarks, tradenames, service marks or copyrights to imply, and such use or display should not be construed to imply a relationship with, or endorsement or sponsorship of us by, these other parties.

Presentation of Financial Information

Our fiscal year is the 52-week or 53-week period which ends on the Sunday nearest to December 31. Unless otherwise noted, all references to “2023”, “2022” and “2021” are to the 52-week periods ended December 31, 2023, January 1, 2023 and January 2, 2022, respectively.

The consolidated financial statements in this prospectus were prepared in accordance with accounting principles generally accepted in the United States of America, or GAAP, which requires us to make estimates and use assumptions that affect the amounts reported in the consolidated financial statements and the accompanying notes. It is possible that actual results could differ materially from those estimates. The information reflects all normal recurring adjustments that we believe are necessary to present fairly the financial position and results of operations for all periods included. Totals and percentages may be affected by rounding.

Non-GAAP Measures

This prospectus contains certain financial measures, including Adjusted Net Income and Adjusted Net Income Margin, EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, Net Debt, Ratio of Net Debt to Adjusted EBITDA, Adjusted Segment Profit, Adjusted Segment Profit Margin and Free Cash Flow that are not required by, or prepared in accordance with, GAAP. We refer to these measures as “non-GAAP” financial measures. See

iv

“Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Measures” for our definitions of these non-GAAP measures, information about how and why we use these non-GAAP measures and a reconciliation of each of these non-GAAP measures to its most directly comparable financial measure calculated in accordance with GAAP. You should be aware that our presentation of these and other non-GAAP financial measures in this prospectus may not be comparable to similarly titled measures used by other companies.

v

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before deciding to invest in our common stock. You should read the entire prospectus carefully, including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision.

Our Mission

Good food. Responsibly.® At Smithfield, we are helping to feed a world of nearly eight billion people. Our products are found on tables everywhere. We provide families with wholesome, safe and affordable food while finding new and innovative ways to care for our people, communities, animals and planet. It is our responsibility and our promise. We make more than good food. Good is what we do.

Our Company

Smithfield is an American food company and an industry leader in value-added packaged meats and fresh pork with over $14 billion in annual sales. We employ approximately 34,000 people in the United States and approximately 2,500 people in Mexico. We maintain high-quality standards, meeting demand through our strong relationships with thousands of U.S. family farmers and blue-chip global customers. We are a market leader due to our scale, diverse portfolio of strong brands and products and reputation as a trusted partner known for quality. We market our products under a leading portfolio of iconic brands including Smithfield, Eckrich and Nathan’s Famous, among many others.

Our ambition is to be the most trusted food and protein company in North America as we feed people in the United States and around the world, while embracing a culture of responsibility, operational excellence and innovation. We produce and distribute a wide variety of packaged meats and fresh pork products both domestically and abroad. We conduct our operations through three reportable segments: Packaged Meats, Fresh Pork and Hog Production. We are a leading provider of packaged meats in the United States, with the number two branded market position by volume across the 25 key packaged meats categories in which we compete, according to Circana. These 25 key packaged meats categories represent a total addressable market opportunity of $43 billion annually, of which we had an approximate 20% market share by volume (including our private label sales) as of September 2024. We are also the largest fresh pork processor in the United States with approximately 23% market share as of Fall 2023, according to National Hog Farmer. We sell our products across diverse channels including retail and foodservice, distributing in all 50 states in the United States, as well as export markets. We are a leading exporter of pork and pork products, with export sales representing 13% of our total sales for the nine months ended September 29, 2024.

Our Packaged Meats segment is the cornerstone of our business with a value-added product portfolio and profitability that has more than doubled since 2014. Alongside our Packaged Meats segment, our Fresh Pork and Hog Production segments remain integral parts of our business, providing significant scale and operational benefits in support of our product offerings and our ability to meet demand consistently across economic cycles. We believe our emphasis on value-added packaged meats, along with our commitment to food quality, strong financial position and steadfast devotion to our stated mission, will continue delivering value for our shareholders.

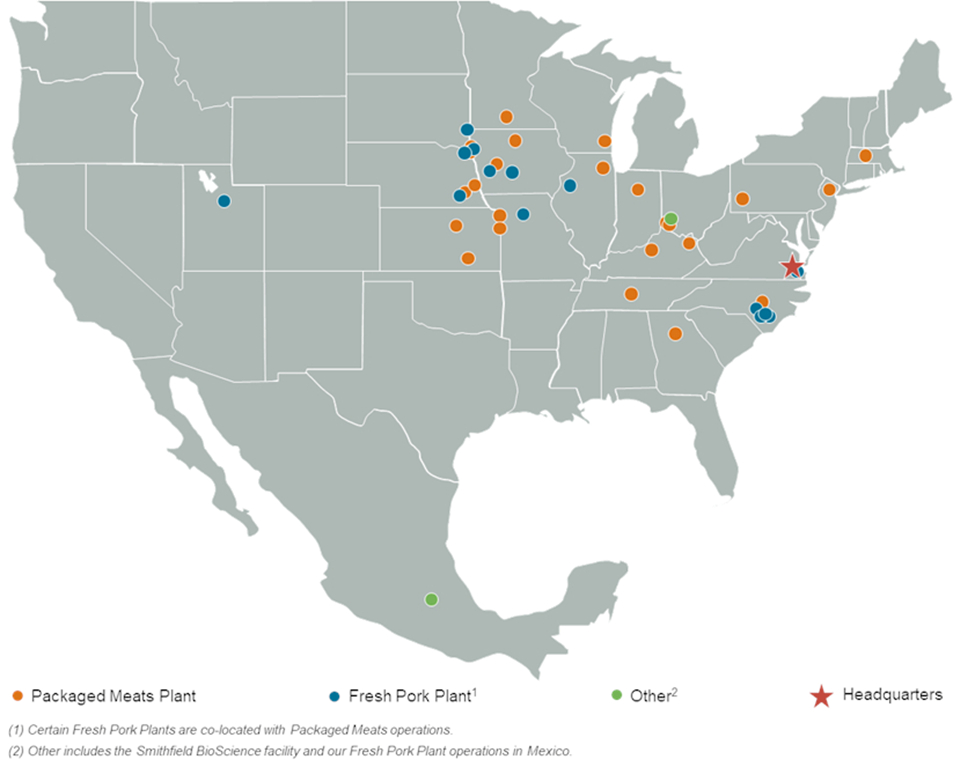

Smithfield’s supply chain includes company-owned and contract farms in the United States and Mexico, as well as long-standing relationships with more than 4,000 independent U.S. family farms who meet our animal care and quality standards. Our model offers a resilient supply chain, providing us with several competitive advantages, including an assured supply of consistent, high-quality protein, the ability to innovate and lead in areas such as group-housed pork and the ability to deliver differentiated products to meet customer specifications. We operate 39 facilities producing fresh pork and packaged meats in the United States and one fresh pork facility in Mexico, and we focus on continually optimizing our operations by identifying opportunities to reduce costs and increase flexibility to meet market demand. Additionally, we remain committed to investing in innovation across our products, packaging and manufacturing processes. We seek to be the supplier of choice to our customers and maintain our reputation for high-quality, safe and delicious products.

1

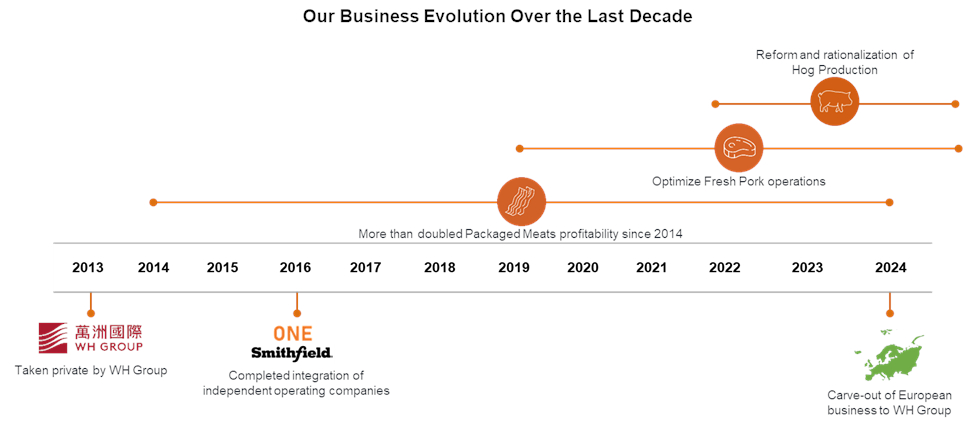

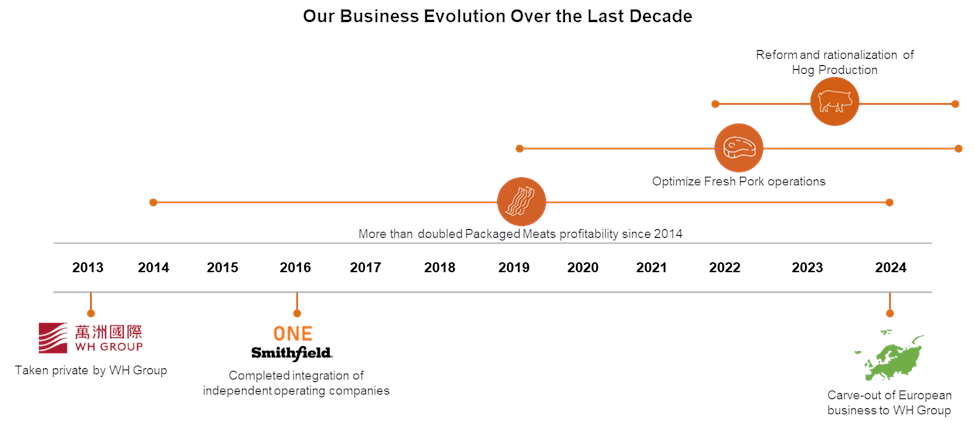

A New Smithfield in the Public Eye

Founded in 1936, we began as a pork processing operation named The Smithfield Packing Company. Through a series of acquisitions beginning in the 1980s, we became the largest fresh pork processor in the United States. In 2013, Smithfield was taken private and became a wholly owned subsidiary of Hong Kong-based WH Group, which is publicly traded on The Stock Exchange of Hong Kong Limited. WH Group is a limited liability company incorporated in the Cayman Islands, the shares of which have been listed on the Main Board of the Stock Exchange since August 2014. Through its subsidiaries, WH Group is principally engaged in the production and sale of packaged meats and pork.

Following the acquisition of Smithfield by WH Group, we focused on integrating our independent operating companies into a cohesive business. Our “One Smithfield” initiative unified our operations, brands and employees under one corporate umbrella, achieving synergies and enhancing profitability through disciplined cost management and balance sheet strength.

In recent years, we have transformed into a differentiated American food company with a leading position in value-added packaged meats and fresh pork, and our headquarters remains in our namesake town of Smithfield, Virginia.

In August 2024, we completed a carve-out of our European operations to focus our local management teams on the different market dynamics of North America and Europe. Pursuant to the European Carve-out, our operations in Europe were transferred to WH Group.

Led by growth in our Packaged Meats segment, our product portfolio has evolved to a higher concentration of value-added packaged meats offerings, significantly improving profitability. Additionally, we have reduced complexity and improved our cost structure in our plant operations by rationalizing our SKU count. Since 2019, we have reduced our Packaged Meats SKU count by over 40% and increased volume velocity (pounds/item) by over 60%.

The growth in our Packaged Meats segment has helped to increase our overall scale and profit margins and to stabilize our earnings and cash flows during volatile commodity cycles and economic downturns. This is the anchor of our strong financial position and fuels continued investment in our business. We have invested over $3 billion in capital expenditures since 2013, driving our organic growth strategy and improving our operations, including automating processes.

2

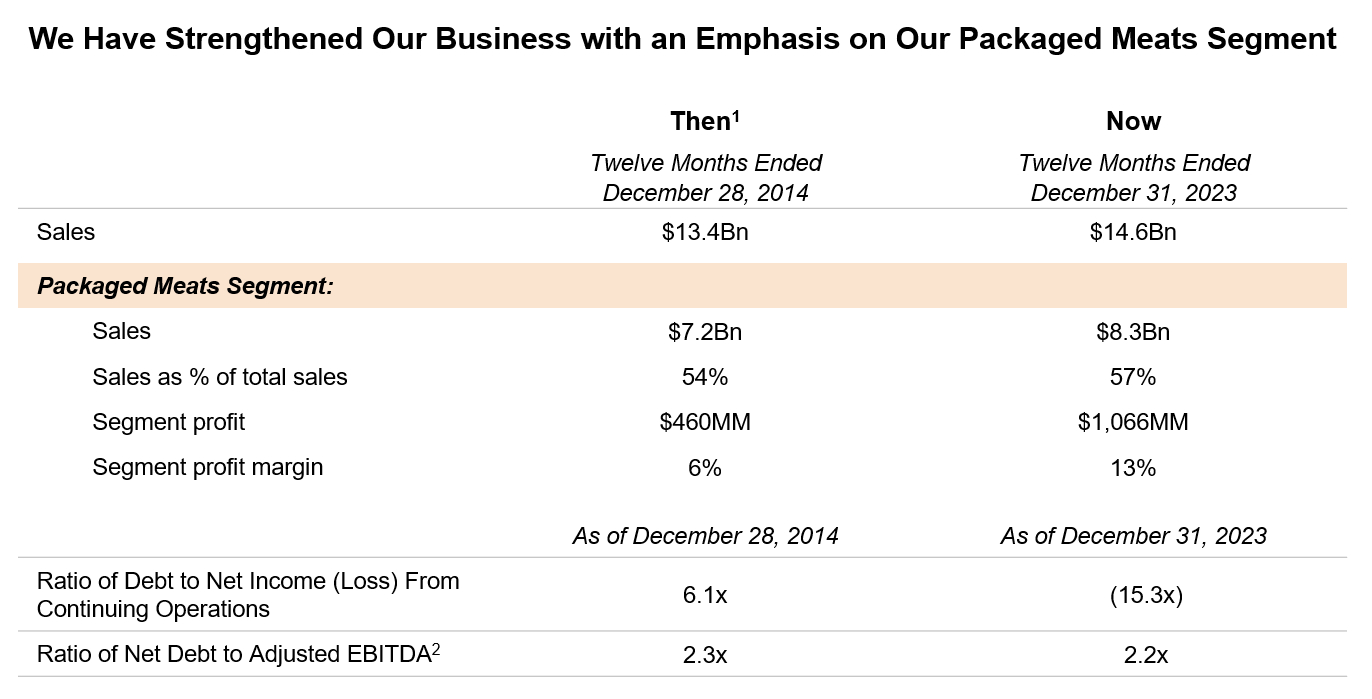

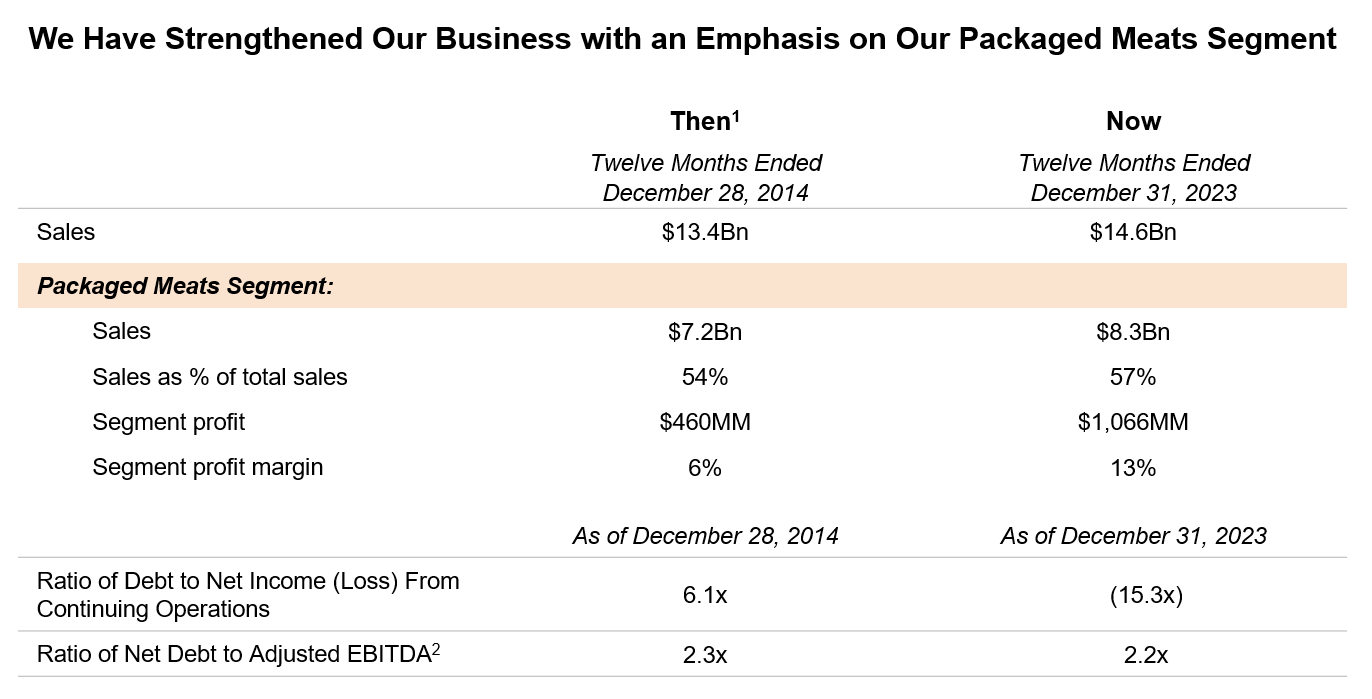

The following table sets forth certain metrics for our business for 2014 and 2023 and highlights our strategic growth and evolution led by our Packaged Meats segment.

______________

(1)Based on our historical financial statements for the year ended December 28, 2014, which are not included or incorporated by reference in this prospectus. We do not believe the adoption of accounting standards after that date would have a material effect on the financial measures presented. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Measures” for more information.

(2)Ratio of Net Debt to Adjusted EBITDA is defined as net debt divided by Adjusted EBITDA. Net debt is defined as long-term debt and finance lease obligations, including the current portion, minus cash and cash equivalents. Ratio of Net Debt to Adjusted EBITDA is a non-GAAP measure that should not be considered in isolation or as a substitute for other financial measures calculated and presented in accordance with GAAP. For additional information regarding Ratio of Net Debt to Adjusted EBITDA, including a reconciliation to ratio of debt to net income, the most directly comparable GAAP measure, see “Management’s Discussion and Analysis of our Financial Condition and Results of Operations – Non-GAAP Measures.”

Packaged Meats Segment

The Packaged Meats segment produces a wide variety of value-added products and sells them primarily in the United States. For the nine months ended September 29, 2024, the segment had $5.9 billion in sales, comprising 58% of our total sales, $855 million in segment profit, comprising 109% of our total operating profit and a 15% operating profit margin. For the year ended December 31, 2023, we sold approximately 2.9 billion pounds of packaged meats products. The segment has achieved strong growth with a fiscal year 2014 to fiscal year 2023 segment profit compound annual growth rate, or CAGR, of 9.8%.

Our Packaged Meats portfolio is diversified across product categories, brands and channels and spans all meal occasions. For the nine months ended September 29, 2024, 63% of the segment sales were conducted through the retail channel, 31% through the foodservice channel and 6% through the industrial channel (i.e., other protein processors) and other.

We serve 100% of the top 10 ranked national grocery retailers, as identified by Progressive Grocer based on 2023 annual sales, including blue-chip customers, such as Walmart, Sam’s Club, Costco, Kroger and Albertsons. In the foodservice industry, we serve approximately 70% of the top 50 ranked national foodservice chains, including McDonald’s, Subway, IHOP and Jersey Mike’s, as well as all of the top foodservice distributors, including Sysco, U.S. Foods and Performance Food Group. Within the foodservice industry, we leverage our reputation for high-

3

quality products through our Smithfield Culinary brand, and we are the most recognized pork processor by chefs and foodservice operators, with 49% unaided awareness based on a 2024 study by Datassential.

We produce a wide variety of packaged meats products, including bacon, sausage, hot dogs, deli and lunch meats, dry sausage products (such as pepperoni and genoa), ham products, ready-to-eat products and prepared foods (such as pre-cooked entrees, bacon and sausage). We address all dayparts, with our products featured during breakfast, weekday school lunches, football weekends, holiday dinners and at snack time. While pork is our primary protein offering, approximately 17% of the volume utilized in our Packaged Meats segment for the nine months ended September 29, 2024 was non-pork products made with other proteins—primarily poultry and beef.

Our Packaged Meats segment’s branded retail offerings generated $3.2 billion, or 22% of consolidated sales, in 2023. Our products are available at most major food retailers where we continue to drive penetration and have strong on-shelf performance with attractive dollar velocities for our largest categories relative to competition.

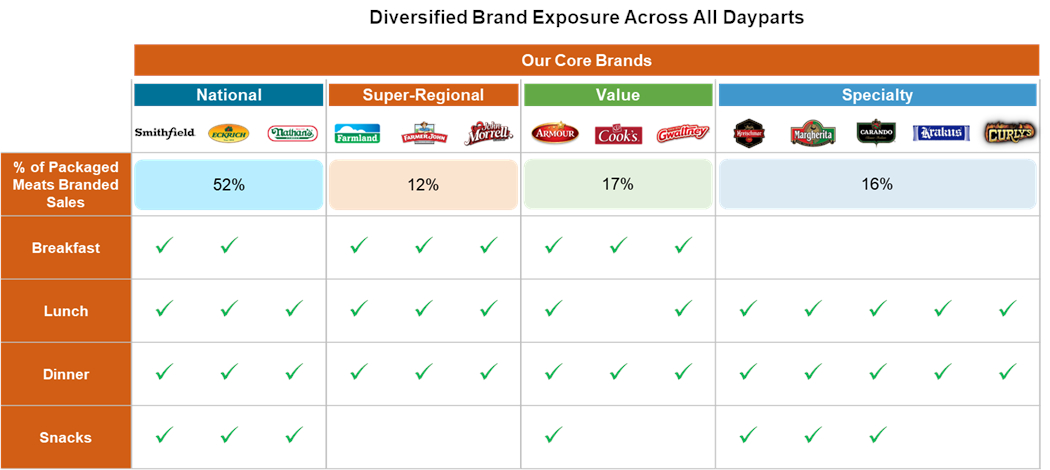

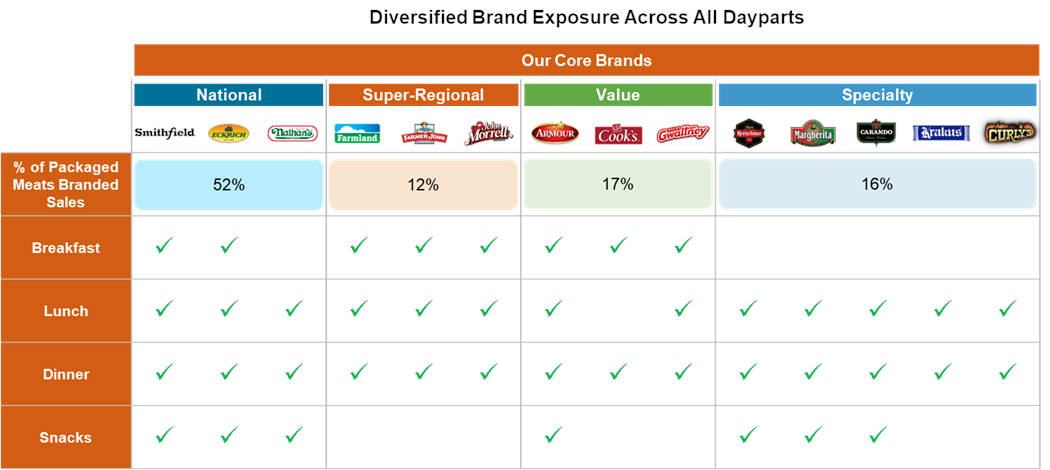

Led by our flagship Smithfield brand, our portfolio of brands has strong consumer recognition and robust brand equity, and we target on-trend product categories for growth. We market our domestic packaged meats products under a strategic set of core brands, including national, super-regional, value and specialty brands that deliver value to our ultimate consumers across a wide range of price points.

The following table illustrates the percentage of our Packaged Meats segment’s branded sales in the retail channel in 2023 for each of our top brands, along with the relevance these brands represent across dayparts:

Additionally, private label represented 38% of our packaged meats retail channel sales volume in 2023. Our private label products make our offerings more valuable to blue-chip retail customers by providing consumers quality selections up and down the value chain. In addition, our private label business helps to optimize our manufacturing footprint and increases the efficiency and profitability of our plants.

Fresh Pork Segment

As the largest fresh pork processor in the United States, our Fresh Pork segment produces a wide variety of primal, sub-primal and offal products, such as bellies, butts, hams, loins, picnics and ribs. Our Fresh Pork segment had $5.9 billion in sales for the nine months ended September 29, 2024, comprising 58% of our total sales, $196 million in segment profit, comprising 25% our total operating profit and a 3% operating profit margin. For the year ended December 31, 2023, we processed approximately 29 million head through the Fresh Pork segment. Approximately one-third of our fresh pork products, including the majority of hams, bellies and trimmings, is transferred to our Packaged Meats segment, providing it with approximately 80% of its raw material requirements for the nine months ended September 29, 2024.

4

Our strategy is to drive our Fresh Pork segment’s profitability to exceed commodity meat values by maximizing the use of our raw materials. This includes offering value-added products, such as marinated fresh pork, a category in which we hold the leading position, and case-ready fresh pork. The export strategy is particularly important to our ongoing initiative to maximize hog utilization by selling byproducts to drive profitability.

Vertically Integrated Supply Chain and Hog Production Segment

Our supply chain, supported by our upstream businesses, is differentiated from our competitors’ supply chains and provides benefits that we believe are hard to replicate. Nearly all of the Hog Production segment’s sales are intercompany sales of live hogs to our Fresh Pork segment. Our Fresh Pork segment sources hogs from a mix of company-owned and contract farms, which raise company-owned hogs, comprising our Hog Production segment. Our Fresh Pork segment further supplements our supply by sourcing hogs from independent farmers with whom we partner across the United States through multi-year agreements. Contract farms and independent farms are held to the same animal care and quality standards as our company-owned farms and thereby form a key part of our integrated supply chain.

We have unmatched scale in hog production, which enables us to consistently supply high-quality raw materials for our Fresh Pork segment and, ultimately, our Packaged Meats segment. Today, we internally supply approximately 50% of the raw material needs of our Fresh Pork segment. We believe that it is important to maintain a certain level of internal production to enable supply to our Fresh Pork processing facilities, particularly to support our East Coast processing operations. Our scale has also enabled us to be an early mover in group-housing for pregnant sows on company-owned farms with the result that these farms supply the majority of our group-housed pork needs which is a differentiated product for which our customers pay a premium.

Beyond scale, our internally supplied hog production is geographically diverse, with locations in the East Coast, Midwest, Missouri and Utah, whereas our largest competitors are located predominantly in the Midwest. Our geographic diversity reduces risk by mitigating the impact of a potential disease outbreak in one part of the country. In addition, our East Coast hog production operations provide an efficient supply to two of our largest Fresh Pork and Packaged Meats processing facilities co-located in North Carolina. Our East Coast location provides us with a significant strategic advantage in our ability to export to more than 30 countries, because it gives us close proximity to East Coast ports, unlike our competitors who need to transport product from the Midwest more than 1,000 miles to either the East or West Coast ports.

In recent years, we embarked on a strategy to optimize the size of our hog production operations and procure a larger percentage of hogs from independent suppliers under long-term, market-based supply agreements. Our Hog Production segment’s transformation strategy is integral to our ongoing objective to further transition our business toward an increased mix of value-added, high-margin products. This transformation allows us to reduce our capital investment and exposure to more volatile areas of the value chain. We plan to reduce the size of the segment’s production from approximately 50% of fresh pork supply today to approximately 30% in the medium term, which is still significantly higher than our competitors. We have made material progress in executing our strategy, reducing the size of our segment’s production from a peak of 17.6 million head in 2019, and we continue to further optimize production levels. In the year ended December 31, 2023, we produced approximately 15.8 million head through the Hog Production segment. We ended 2024 at 14.6 million head, and we expect to end 2025 at approximately 11.5 million head. We believe this strategy will maintain an appropriate supply of high-quality inputs to meet business needs and improve our cost structure while achieving flexibility in our retained hog production business. See also “Risk Factors—Risks Relating to Our Business and Operations—An inability to realize savings and efficiency gains could adversely affect profitability and we may be unable to achieve any or all of our financial and operational targets.”

Our Financial Performance

We believe the rebound in our 2024 performance following a challenging year for our industry demonstrates the resilience of our business model, effectiveness of our strategy and operational discipline, while our stable cash flows and strong balance sheet allow us to invest in our continued operations and return value to shareholders.

5

The charts below depict our recent financial performance:

We believe maintaining a healthy financial position is critical to the execution of our strategy, efficiency of our operations and our ability to manage effectively through industry and macroeconomic headwinds. We are committed to maintaining investment-grade credit ratings and target the following metrics:

•Ratio of Net Debt to Adjusted EBITDA of 2.0x. As of , our Ratio of Net Debt to Adjusted EBITDA was x and our ratio of debt to net income from continuing operations was x. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Measures” for our definitions of Ratio of Net Debt to Adjusted EBITDA, information about how and why we use this non-GAAP measure and, for historical periods, a reconciliation of this non-GAAP measure to ratio of debt to net income from continuing operations, its most directly comparable financial measure calculated in accordance with GAAP.

•Minimum liquidity of $1.0 billion. As of , our liquidity was $ . We define liquidity as cash and cash equivalents plus available borrowing capacity under our credit facilities.

6

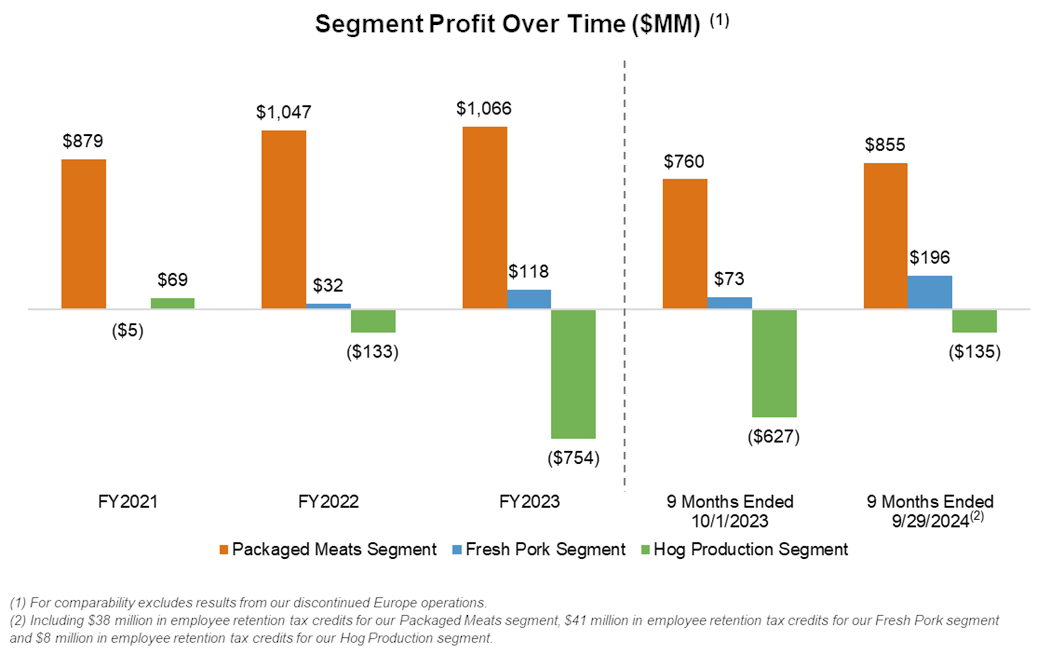

In addition, the charts below depict our segment profit over time:

The evolution of our business to value-added products with higher margins supports stronger cash flow generation, which is allocated toward investment in growth and shareholder return. Our capital allocation strategy is focused on:

•Driving top-line growth and achieving operational efficiencies by allocating $400 million to $500 million annually towards capital expenditures.

•Returning excess capital to shareholders in the form of a regular dividend after funding investments in our strategic priorities. We initially expect to pay annual dividends in an amount equal to 50% of our net income, subject to the discretion of the board.

•Conducting opportunistic and financially disciplined acquisitions, primarily focused on growing our Packaged Meats segment, with assets and capabilities that complement our robust manufacturing platform and strong brands and product offerings.

7

Our Industry

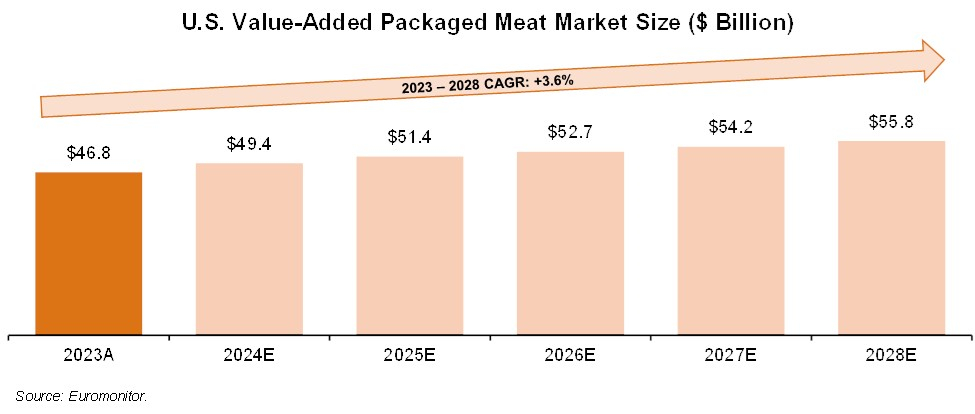

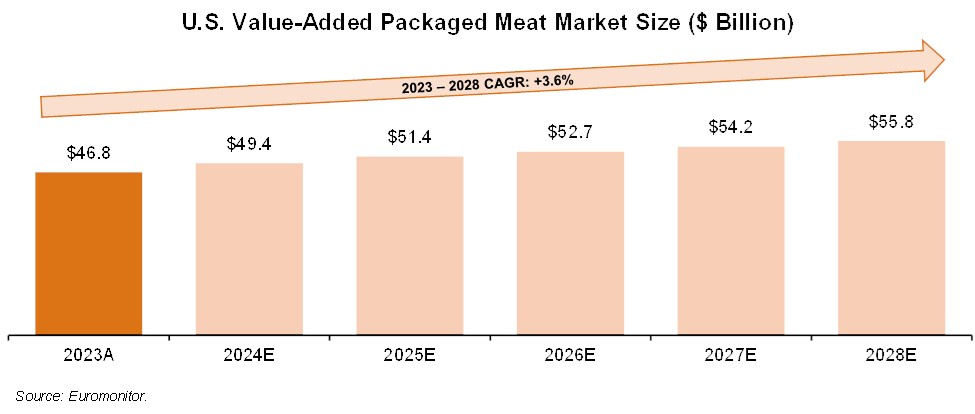

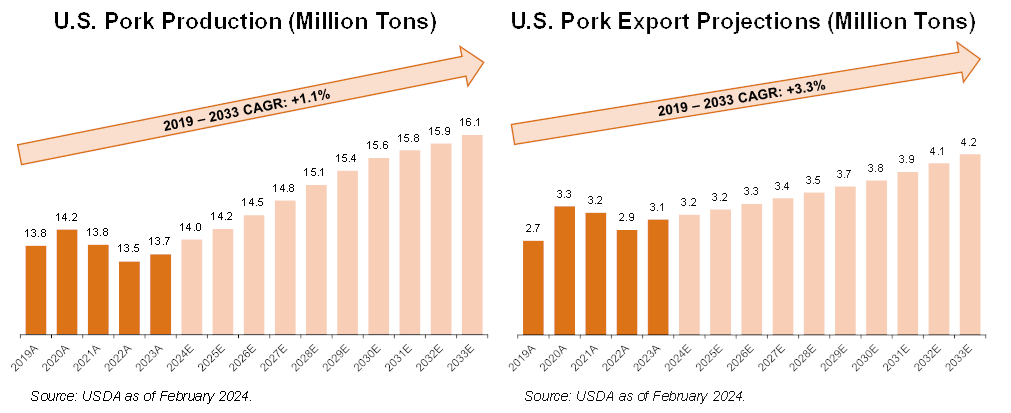

We operate in the large and growing global packaged and fresh meats market, which includes value-added fresh, refrigerated and frozen proteins. Our business operations are primarily concentrated in North America, but, as a leading exporter to major international markets, we also benefit from significant global demand for our products. According to Euromonitor, the global meat market reached $1.1 trillion in 2023 and is projected to grow at a 6.5% CAGR between 2023 and 2028. Per Euromonitor, U.S. value-added packaged meats represented a $47 billion market in 2023 and is forecasted to grow at a 3.6% CAGR between 2023 and 2028. Value-added packaged meats refers to the processed meats category as defined by Euromonitor and includes meat products that have undergone additional processing, such as adding an additional ingredient or characteristic, and are sold pre-packaged via retail and foodservice outlets.

The following table sets forth information about size of the U.S. value-added packaged meat market:

Consumer Trends in U.S. Packaged Meats and Fresh Pork

The U.S. packaged meats market is supported by long-term secular tailwinds, including consumer demand for high-protein diets, high-quality nutrition, product versatility and convenience. We expect these tailwinds to continue to drive increases in overall meat consumption. Consumers associate protein with healthiness and energy. A 2024 International Food Information Council consumer survey reported that a high-protein diet is the most popular diet type in the United States. According to market research firm Ipsos, 89% of Americans include animal protein in their diets as of 2021. Data from the Organization for Economic Co-operation and Development shows that pork represented 24% of all meat protein consumed in the United States in 2023.

According to Mintel, many packaged meats products are household staples for U.S. consumers, including bacon, lunch meat, hot dogs, fresh sausage and dry sausage. Mintel reports that, as of September 2023, U.S. bacon and lunch meat represented an estimated $27.0 billion market in 2023 that is expected to grow at a 4.2% CAGR between 2023 and 2028, and U.S. hot dogs and sausages were estimated to represent a $12.3 billion market in 2023 that is expected to grow at a 1.0% CAGR between 2023 and 2027. According to Business Research Insights, U.S. dry sausage for charcuterie, snacking, sandwiches, pizza toppings and other uses, typically higher margin products, represented a $4.7 billion market in 2023 that is expected to grow at a 3.9% CAGR between 2023 and 2030.

Mintel reports that 86% of U.S. consumers anticipate eating the same amount of pork or more pork in the coming year according to a survey conducted in February 2024, and pork consumption is distributed relatively equally across income groups. According to Mintel, packaged pork products benefit from growing demand for convenience, as consumers value marinated, ready-to-cook and ready-to-eat options. Mintel reports that pork is an affordable and convenient protein.

8

Pork is also a highly versatile protein, with a wide variety of cuts and flavor profiles. Use occasions for pork products benefit from strong daypart distribution, which is unique relative to all other meat proteins. Products like bacon, sausage and ham appear on tables at every meal. According to the National Pork Board, bacon is by far the most beloved packaged meats product, and pork is a highly snacked meat protein and the most popular pizza topping in the United States.

Additionally, increased U.S. demand for global cuisines supports the domestic pork market. Asian and Mexican cuisines, for which pork is a leading protein, continue to gain popularity with U.S. consumers, particularly among Generation Z (the generational cohort aged 12 to 27 years) and Millennials (the generational cohort aged 28 to 43 years). We believe that the continued growth of global cuisines in the United States introduces consumers to different pork preparations and flavor profiles and serves as an incremental long-term tailwind for pork.

According to Mintel, most U.S. consumers are concerned about the environmental impact of meat production, and health and nutrition are important factors to consumers of meat. Many cuts of pork offer lower levels of cholesterol and saturated fat relative to cuts of beef. Lean cuts of pork, including pork tenderloin, offer a superior nutritional profile to chicken breast. Additionally, relative to beef, pork production generally has a lower carbon footprint and lower rate of land usage. Nevertheless, changes in market trends and consumer preferences could adversely affect our results of operations. For more information, see “Risk Factors—Risks Relating to Our Business and Operations—Changes in consumer preferences and failure to maintain favorable consumer perception of our brands could negatively impact our business.”

Our Competitive Strengths

We attribute our track record of success to a combination of the following competitive strengths. We believe these strengths are central to our business model and position us well for long-term success.

Leader in Packaged Meats with Diverse Portfolio of Strong Brands

We have grown our Packaged Meats business to become a leading provider of value-added pork and other protein products for U.S. customers and consumers. Consumers choose our products for consistent high-quality and delicious taste, helping us achieve an 81% repeat purchase rate as of September 2024. Our Net Promoter Scores, a gauge of brand affinity, are superior to peers across key categories, including smoked ham, fresh pork, Italian specialty, hot dogs, everyday ham and bacon. We continue to see increasing loyalty and unaided awareness across our key brands and categories. Our longstanding commitment to our values and corporate heritage resonates with consumers who share our ideals, including our commitment to sustainability and American agriculture.

Our trusted brands have made us one of the country’s leading food companies. Led by our flagship Smithfield brand, we have a diverse portfolio of national, super-regional, value and specialty brands with strong customer loyalty. We complement our national brands with super-regional brands to capitalize on each brand’s history and strong consumer affinity. Our value brands offer consumers choices across price points, and our specialty brands address various on-trend categories such as dry sausage and convenient preparation items, including barbecue and meatballs.

9

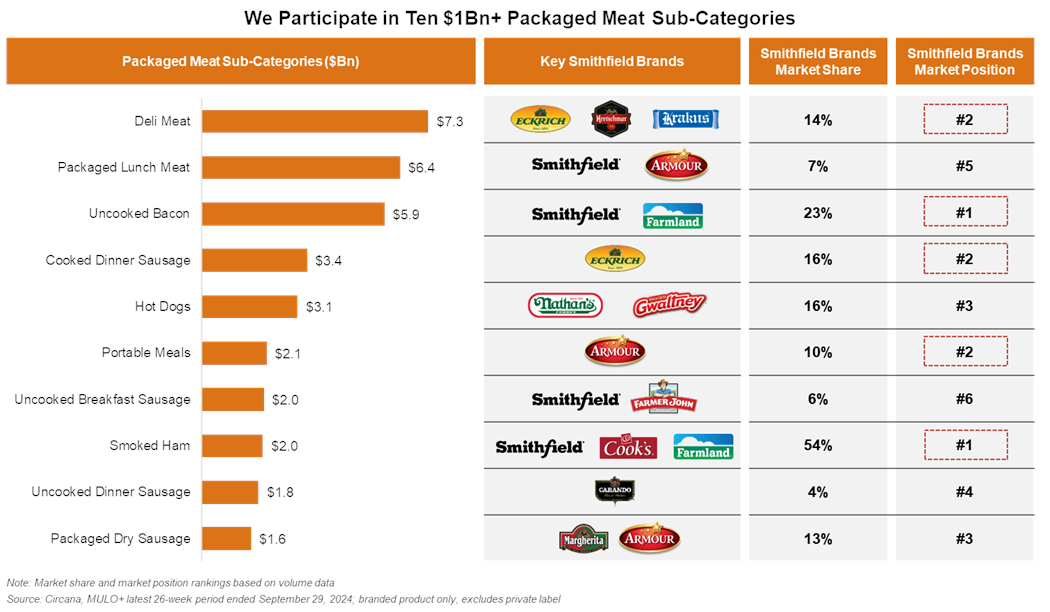

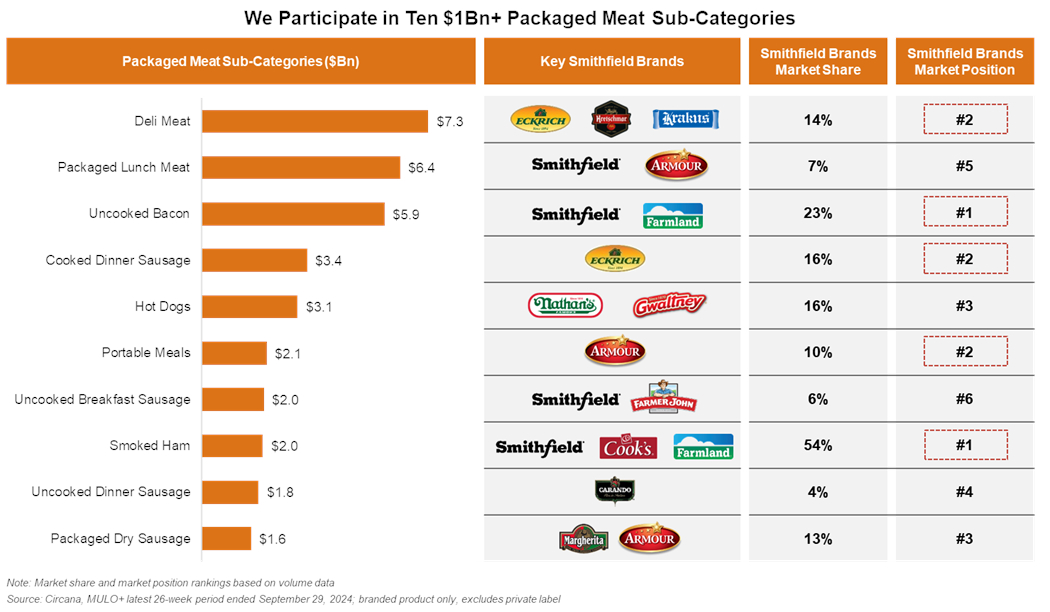

As a branded player across the United States, we have a leading position in 15 of the 25 key categories in which we compete. We have a significant presence in 10 categories each over $1 billion in size, including the number one or two position by volume in uncooked bacon, smoked ham, deli meat, cooked dinner sausage and portable meals as shown in the table below:

We market our products to customers and consumers across multiple categories and price points. We have a balanced sales mix with approximately 64% branded and 36% private label in the retail channel as of September 2024. Our participation in both branded and private label helps us attract and retain consumers as they move across the value spectrum, enabling us to meet shifting consumer preferences during periods of economic downturn and to capture wallet share when they trade up to premium brands.

10

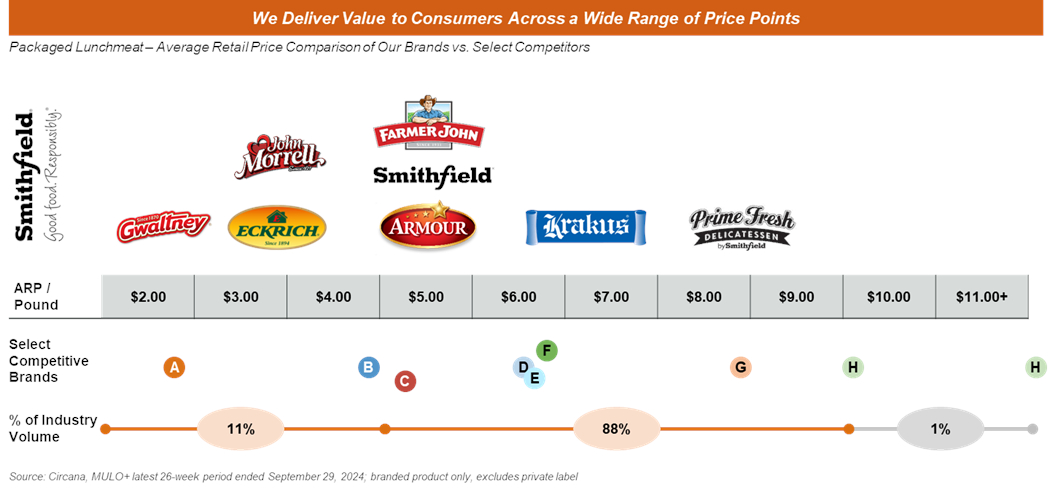

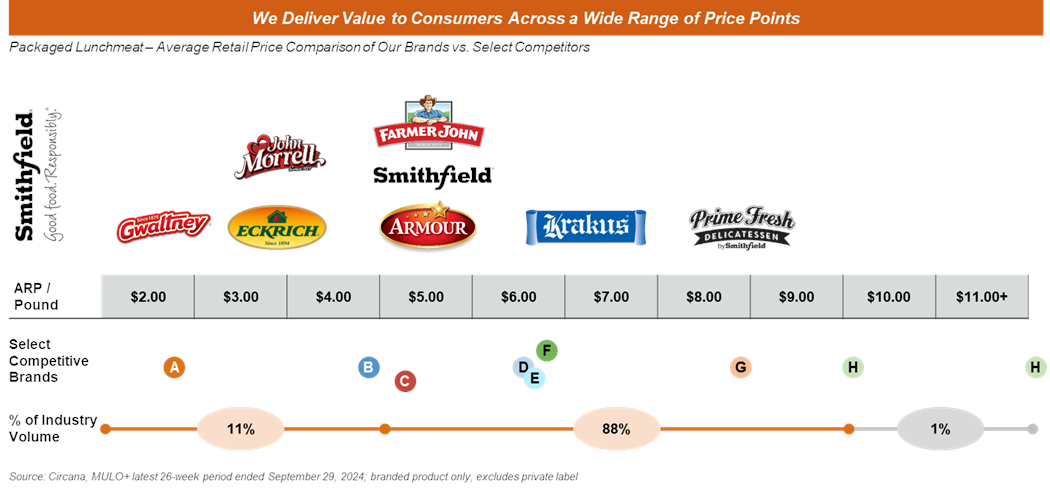

For example, in the packaged lunch meat category, almost 98% of the volume is sold on average in the $2.00-$9.00 price per pound range. Our packaged lunch meat offering exemplifies how we cover a wide range of retail price points from our best value with Gwaltney (at approximately $2.50 average retail price per pound) to our premium Smithfield Prime Fresh (at approximately $8.50 average retail price per pound) as of September 2024.

While some of our competitors may choose to focus on consumers at only the high or low end of the value spectrum, our strategy enables us to meet consumer demand across various price points, as shown in the chart below:

For information about challenges we face in the highly-competitive food market, see “Risk Factors—Risks Relating to Our Business and Operations—The food industry in which we operate is highly competitive, and our inability to compete successfully, or the effects of such competition, could adversely affect our business, financial condition and results of operations.”

Trusted and Scaled Partner Known for Quality

We have a nearly 90-year history of providing great tasting, quality products across the United States and abroad. We pride ourselves on producing safe, wholesome and high-quality protein, and we continually train our team members in the latest animal welfare and food safety and quality best practices across our supply chain. Producing Good food. Responsibly.® is at the core of our purpose-driven culture. Consumers trust our high-quality brands and products, and we are a trusted partner to customers, suppliers and farmers across the value chain.

Through years of investment and growth, we have created an asset base that we believe would be hard to replicate. Our scale and integrated operating model enable us to reliably meet demand across economic cycles and offer a differentiated value proposition to our customers and consumers. We believe that we are a preferred supplier to our partners because we consistently provide comprehensive end-to-end support and reliably deliver high-quality products on time. Our commitment and reputation for high-quality products and service is evidenced by the numerous awards received from our retail and foodservice customers, recognizing Smithfield as a supplier of choice.

Leveraging our scale and global distribution channels, we are also a leading exporter of pork and pork products, with sales to export markets representing 13% of our total sales for the nine months ended September 29, 2024. Export markets promote whole hog utilization due to differentiated demand for parts of the animal across the globe, which helps us to operate sustainably while supporting American agriculture.

11

Strong Financial Profile Marked by Robust Growth and Profitability Metrics

We are focused on delivering long-term sustainable results and have built our business to generate resilient growth, profitability and cash flow. Our track record of sales and earnings growth reflects strong demand for our products and successful management of commodity volatility across economic cycles. In 2024, we demonstrated a strong rebound in our results after a challenging 2023 for our industry.

The resilience of our business model is underscored by our history of maintaining a strong balance sheet and moderate leverage. Sustaining a healthy financial position creates operational flexibility and helps to insulate us from industry and macroeconomic headwinds. We are committed to a target Ratio of Net Debt to Adjusted EBITDA of < 2.0x and a target minimum liquidity of $1.0 billion, as well as maintaining investment grade ratings.

We have a strong track record of disciplined capital allocation, generating higher profitability and cash flows by executing projects that drive organic growth and unlock operational efficiencies. While organic growth has been the backbone of our growth strategy over the past decade, we will continue to supplement our organic growth with a disciplined acquisition strategy. Our acquisition strategy primarily focuses on packaged meats assets and capabilities that complement our manufacturing platform, strong brands and product offerings.

Innovative Sustainability Initiatives

Sustainability has been a key focus for our business for over twenty years. Our strategy today is built around three objectives: being good stewards of the environment and our animals; doing good work in the communities where our employees live and work; and producing good food with a commitment to food safety, quality and nutrition. We have been at the forefront of the industry in achieving sustainability milestones, including becoming the first major protein company to adopt and publicly report a comprehensive sustainability program, to achieve International Standards Organization 14001 certification globally, to develop and adopt a comprehensive animal care management program, to begin reporting antibiotics usage in 2007 and to publish an online ingredient glossary.

We leverage on-the-ground resources to strive to achieve our sustainability goals. We co-founded Align RNG, LLC, or Align, as well as Monarch Bioenergy LLC, or Monarch, to advance developments in methane capture and manure-to-energy conversion. In 2022, TPG Rise Climate invested in Monarch, helping us to further scale the business.

Our sustainability activities have been recognized externally. We were awarded the prestigious “Profit with a Purpose” award by the World Sustainability Awards, or WSA, in 2021 for our innovative renewable natural gas programs. These programs convert methane from hog manure into clean energy, creating new income opportunities for family farmers. Additionally, we received a “Highly Commendable” mention in the WSA’s External Partnership category in 2021 for our collaboration with a leading environmental organization to implement sustainable farming practices within our supply chain.

We are consistently recognized as an employer of choice for U.S. veterans. We have a long history of supporting veterans and military families through monetary and food donations, employee volunteerism and partnerships. We honor the service and sacrifice of American veterans and their families through the Helping Our Heroes program, which focuses on hiring initiatives, career development and strengthening the community and family support systems veterans rely on every day.

Proven, Execution-Oriented Management Team and Culture

We are an iconic American food company with a management team based in Smithfield, Virginia. We employ approximately 34,000 people in the United States and approximately 2,500 people in Mexico. Our energetic and highly experienced management team, whose dedication and commitment to our mission permeates throughout our business, has made us one of the world’s foremost protein companies, sets the tone for our success and drives the agility necessary to continue to transform Smithfield into a leading packaged food company. We foster a culture of responsibility, operational excellence and innovation that serves as the foundation for the transformation in our business.

12

C. Shane Smith, President and Chief Executive Officer since 2021, is a veteran of our company and has served in a wide range of roles during his 21-year tenure. He previously served as President of Smithfield’s European operations and as our Chief Strategy Officer, and he has held other roles in finance and our Hog Production segment. He has been instrumental in overseeing the continued execution of our “One Smithfield” vision, fortifying our position as a leading food company and improving operational efficiency to enhance market competitiveness.

Mark L. Hall, our Chief Financial Officer, has 26 years of experience in the food industry and leads our finance, accounting, treasury, tax, mergers and acquisitions, data analytics and risk management functions. Since joining Smithfield in 2014, Mark has played a crucial role in developing and executing our strategy, including during his tenure as head of finance within the Packaged Meats segment.

Our senior leadership team has extensive food industry experience. Steven France, Donovan Owens and Kraig A. Westerbeek lead our Packaged Meats, Fresh Pork and Hog Production segments, respectively, and have nearly a century of combined industry experience, including over 80 years of experience at Smithfield. Our leadership, combined with our integrated operating structure, solid financial foundation and the support of over 36,000 employees, create a cohesive and coordinated platform to further Smithfield’s growth as a leading food company creating value for a range of stakeholders.

Our Growth Strategies

Since the last time we were a public company in 2013, we have grown sales to $14.6 billion while significantly improving our profitability and leverage position. The strategic initiatives we are executing across our segments are complemented and enabled by our strong balance sheet and ongoing operational investments, positioning us for future growth.

Drive Growth of Packaged Meats

Our Packaged Meats segment is core to our growth strategy and has been a major driver in transforming our business since 2014. We have methodically shifted our business mix to focus on this higher-margin segment over time. The segment contributed 58% of our sales and 109% of our overall operating profit for the nine months ended September 29, 2024.

We plan to accelerate the growth of our Packaged Meats segment through several strategic initiatives, including:

•continuing to shift our portfolio toward a higher mix of value-added and premium products, such as:

•converting one-time seasonal commodity bone-in ham purchase occasions to increased unit sales of everyday, convenient products such as quarter-weight ham, Anytime Favorites ham and Prime Fresh sliced lunch meat, which is underscored by our ability to generate a 19% increase in ham units sold from 2019 to 2023 while volume increased only by 2% for that same period; and

•increasing penetration of higher-margin dry sausage products through expanding distribution points and manufacturing capacity, as evidenced by a 29% increase in dry sausage units sold from 2019 to 2023 and the recent acquisition of a dry sausage plant;

•harnessing our powerful brands to continue to expand product offerings and drive awareness, loyalty and increased market share;

•leveraging the breadth of our platform and national and specialty brands to further penetrate dayparts and households;

•expanding in under-indexed geographical locations and moving into new categories;

•attracting new consumers, particularly younger demographics, through product and packaging innovation and effective and appealing marketing strategies while maintaining our promise to consumers to offer high-quality products for every budget; and

13

•deepening our presence across our distribution channels through our integrated sales force, which leverages our scale and breadth to provide a unified, reliable and consistent customer experience.

We believe that these proven strategies will drive profitable organic growth in our Packaged Meats segment. As an example, we see significant potential for our Packaged Meats segment to generate continued growth through our distribution expansion opportunities across brands to expand unit count within our existing product portfolio.

Further Enhance Fresh Pork

We continually seek greater efficiencies as we manufacture and market fresh pork products. Our capabilities and supply chain allow us to provide differentiated products and high service levels to our customers. We deliver a high-quality, consistently available supply to our Packaged Meats segment and maximize the value of our raw materials. We will seek to enhance the profitability of our Fresh Pork segment by:

•maximizing the value of each hog and expanding use of raw materials, including unprocessed fresh and value-added pork, snacks, pharmaceuticals and pet food treats and ingredients;

•capitalizing on export markets as an outlet for increasing the value of raw materials through whole-hog utilization, and appealing to differentiated, global tastes and preferences;

•leveraging our relationship with WH Group to inform product development opportunities for the Asian market and to benefit from WH Group’s distribution network; and

•appealing to ever-changing consumer preferences and demand for flavor enhancements through ongoing product innovation.

As we seek to grow our fresh pork business profitably, we remain committed to demonstrating that profitability can go hand-in-hand with sustainable operations. We will further our mission of producing good food the right way by seeking new and unique ways to use our raw materials.

Continue Investing in Innovation

We will continue to invest in product, packaging and operational innovations in our Packaged Meats and Fresh Pork segments to drive growth, enhance our profitability and expand our total addressable market. We are focused

14

on strengthening relationships with customers and consumers by being first-to-market with new products and solutions.

Within our branded packaged meats portfolio, we are introducing more value-added and premium innovations. We see a significant opportunity to increase distribution of our innovative Smithfield Prime Fresh packaged lunch meat offering. Smithfield Prime Fresh embodies the quality of bulk deli meat but is displayed in the packaged lunch meat section of the retail wall. This enables our retail partners to increase average revenue per pound and reduce in-store labor costs while providing a convenient lunch meat option for consumers.

In addition, our Smithfield Double Thick/Double Smoked bacon and Smithfield Maple Thick Cut bacon demonstrate our ability to introduce premium, higher-margin offerings with new cut and flavor characteristics. These products sell at a higher velocity than the category average.

In the Fresh Pork segment, we are investing in value-added products and adding new cuts and flavors, such as Sweet & Smokey BBQ, Chipotle and Lemon & Garlic marinated fresh pork loin filet.

Innovation does not stop with our products. In our plants, we are committed to advancing automation and strategically redeploying labor. On our farms, innovative approaches to animal nutrition are increasing feed conversion and lowering our cost basis. Byproducts that were once considered waste are now used to create renewable natural gas through our biogas joint ventures and lifesaving pharmaceuticals through our bioscience business.

Our culture of responsibility, operational excellence and innovation serves as a catalyst for our ongoing business transformation. We conduct company-wide competitions and recognition events for grassroots projects that drive innovation throughout our organization. By fostering this entrepreneurial spirit, we will seek to drive growth in our top- and bottom-line results and build on Smithfield’s competitive advantage.

Optimize Our Operations and Supply Chain to Decrease Our Cost Basis

We have implemented many initiatives over the past several years to reduce costs and realize operational efficiencies. These initiatives have enabled us to offset inflation and enhance margins across our entire business.

We continue to optimize the size of our company-owned hog production operations and procure a greater mix of hogs from independent suppliers with market-based supply agreements. Additionally, we continue to implement cost-saving initiatives in our retained hog production operations to improve our cost structure.

We employ automation in all of our plants to redeploy labor to higher value tasks, improve yields and drive efficiency by reducing complexity to lower our cost basis and help offset inflationary pressures.

In our logistics and distribution network, we have reduced transportation and warehousing costs through transportation efficiencies, maximizing utilization of our storage and trucking assets, improving supply and demand

15

planning and optimizing inventory levels. These actions increase profitability and improve customer service levels, which we believe is essential to being a supplier of choice.

We remain committed to optimizing our operations and supply chain through a series of targeted actions, which in the past have supported meaningful margin improvement:

| Hog Production | Packaged Meats & Fresh Pork | Logistics | ||||||

| “Reform and Rationalize” | “Best-In-Class Lean Manufacturing” | “Improve Service at Optimal Cost” | ||||||

•Optimize number of company-owned hogs •Improve herd health •Transform genetics •Drive procurement and nutrition savings | •Offset inflation with cost savings programs •Employ automation •Improve yields and maximize raw material usage •Reduce complexity | •Be the supplier of choice •Maximize assets (reduce transport miles, warehouse utilization) •Improve supply and demand planning •Optimize inventory levels | ||||||

Implementation of our growth strategies requires us, in particular, to continue to grow our Packaged Meats segment and to reduce our exposure to commodity price volatility through optimization and continued reduction of the size of our company-owned hog production operations. For information about challenges that we face in implementing this strategy and our other growth strategies, please see “Risk Factors—Risks Relating to Our Business and Operations—Our results of operations are cyclical and could be adversely affected by fluctuations in the commodity prices for meat, livestock (primarily hogs) and feed ingredients,” and “—Disruption of our supply chain could adversely affect our business, financial condition and results of operations.”

Execute Synergistic M&A in North America

We intend to execute opportunistic, complementary M&A to bolster our value-added product portfolio and production capacity in North America. While acquisitions are not a primary growth driver for us, our team is experienced in identifying strategic acquisition targets and integrating them successfully into our business. We believe our integration expertise allows us to capture both cost synergies and incremental revenue opportunities. We will remain disciplined in our acquisition approach and maintaining our investment grade ratings, while pursuing opportunities that we believe will prove accretive to earnings and enhance our operational profile. For example, we recently acquired a dry sausage plant in Nashville, Tennessee from Cargill Meat Solutions Corporation, or Cargill, which is strategically located and offers important capacity for some of our fast-growing, higher margin packaged meats products. This acquisition will help serve the growing demand for high-quality pepperoni, deli, charcuterie and other dry sausage products.

Recent Developments

Murphy Family Farms Investment

On December 27, 2024, we became a member of a North Carolina-based company, Murphy Family Farms LLC, by contributing $3 million in cash in exchange for a 25% minority interest. We additionally sold approximately 150,000 sows located on company-owned and contract farms in North Carolina to Murphy Family Farms. On December 30, 2024, we sold the commercial hog inventories associated with such sows to Murphy Family Farms. Murphy Family Farms is now a hog supplier to us and will supply approximately 3.2 million hogs annually. We will supply animal feed and provide certain support services to Murphy Family Farms.

VisionAg Hog Production Investment

On December 20, 2024, we entered into an agreement to become a member of a North Carolina-based company, VisionAg Hog Production, LLC, whereby we will contribute $450,000 in cash in exchange for a 9% minority interest in VisionAg Hog Production, with the existing owner retaining a 91% interest. As part of the agreement, we will sell to VisionAg Hog Production approximately 28,000 sows and the associated commercial hog

16

inventories located on certain company-owned and contract farms in North Carolina. VisionAg Hog Production will become a hog supplier to us, expected to supply approximately 600,000 hogs annually. In addition, we will supply animal feed and provide certain support services to VisionAg Hog Production. The transaction is expected to close during the first quarter of 2025. Closing of the transaction is subject to satisfaction of customary closing conditions.

Sale of Utah Hog Production Assets.

On December 17, 2024, we sold our hog production assets in Utah, excluding the live animals, for $58 million. The transaction resulted in a gain of $32 million, which was recognized in operating gains in the fourth quarter of fiscal year 2024. As part of the agreement, we will lease back certain farm and feed properties, which we will continue to operate.

Sale of Missouri Hog Farms

On November 26, 2024, we sold certain hog farms in Missouri, most of which were previously inactive, for $32 million. The transaction resulted in a loss of $4 million, which was recognized in cost of sales in the fourth quarter of fiscal year 2024.

Preliminary Results for the Three Months Ended December 29, 2024

We have set forth below our preliminary estimates of selected unaudited financial information for the three months ended December 29, 2024 and actual unaudited financial results for the three months ended December 31, 2023. We have provided estimates and ranges of certain preliminary results below because our closing procedures for the three months ended December 29, 2024 are not yet complete.

Our preliminary estimates of the financial results set forth below are based solely on information available to us as of the date of this prospectus and are inherently uncertain and subject to change. Our actual results for the three months ended December 29, 2024 remain subject to the completion of management’s final review and our other closing procedures as well as the effects of potential subsequent events. Accordingly, you should not place undue reliance on these preliminary financial results set out below, which may differ from actual results. See “Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and accompanying notes included elsewhere in this prospectus.

The preliminary estimated unaudited financial results included in this prospectus have been prepared by, and are the responsibility of, our management. Our independent registered public accounting firm, Ernst & Young LLP, has not audited, reviewed, compiled or performed any procedures with respect to the preliminary financial results. Accordingly, Ernst & Young LLP does not express an opinion or any other form of assurance with respect thereto.

The preliminary estimates and actual results provided below do not represent a comprehensive statement of our financial results and should not be viewed as a substitute for full quarterly financial statements prepared in accordance with GAAP. In addition, the preliminary estimates and actual results provided below are not necessarily indicative of the results to be achieved in any future period. The unaudited actual results for the three months ended December 31, 2023 have been derived from the books and records of our company. For additional information regarding the presentation of our financial information, see “Note 1: Summary of Significant Accounting Policies—Basis of Presentation,” in the consolidated financial statements and accompanying notes included elsewhere in this prospectus.

Additionally, the estimates and actual results reported below include certain financial measures that are not required by, or presented in accordance with, GAAP. Management believes that investors’ understanding of our performance is enhanced by including these non-GAAP financial measures as a reasonable basis for comparing our ongoing results of operations. These non-GAAP financial measures have limitations as analytical tools, are not measurements of our performance under GAAP and should not be considered as alternatives to net income or any other performance measures derived in accordance with GAAP and should not be used by investors or other users of our financial statements in isolation for formulating decisions, as such non-GAAP measures exclude a number of important cash and non-cash charges. A reconciliation of EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin to net income and net income margin is provided below. See also “Management’s Discussion and Analysis

17

of Financial Condition and Results of Operations—Non-GAAP Measures.” You should be aware that our presentation of these and other non-GAAP financial measures in this prospectus may not be comparable to similarly titled measures used by other companies.

The following table reflects certain preliminary results for the three months ended December 29, 2024 and actual results for the three months ended December 31, 2023:

| Three Months Ended | |||||||||||||||||

December 29, 2024 (estimated) | December 31, 2023 (actual) | ||||||||||||||||

| Low | High | ||||||||||||||||

| (in millions except margin data) | |||||||||||||||||

| Consolidated Statements of Income Data: | |||||||||||||||||

| Sales | $ | $ | $ | 3,998 | |||||||||||||

| Gross profit | 285 | ||||||||||||||||

| Operating profit (loss) | (116) | ||||||||||||||||

| Net income (loss) from continuing operations | $ | $ | (131) | ||||||||||||||

| Net income (loss) margin from continuing operations | % | % | (3.3) | % | |||||||||||||

| Consolidated Balance Sheet Data (at end of period): | |||||||||||||||||

| Cash and cash equivalents | $ | $ | $ | 687 | |||||||||||||

Working capital (1) | 2,470 | ||||||||||||||||

| Total assets | 13,317 | ||||||||||||||||

| Current portion of long-term debt and finance lease obligations | 27 | ||||||||||||||||

| Long-term debt and finance lease obligations | 2,006 | ||||||||||||||||

| Total shareholder’s equity | 7,241 | ||||||||||||||||

| Non-GAAP Financial Measures: | |||||||||||||||||

| EBITDA from continuing operations | $ | $ | $ | (24) | |||||||||||||

| Adjusted EBITDA from continuing operations | $ | $ | $ | 279 | |||||||||||||

| Adjusted EBITDA margin from continuing operations | % | % | 7.0 | % | |||||||||||||

________________

(1)We define working capital as current assets less current liabilities.

For the three months ended December 29, 2024, we estimate that our sales will range from $ million to $ million, as compared to $3,998 million for the three months ended December 31, 2023. Such was primarily due to .

For the three months ended December 29, 2024, we estimate that our gross profit will range from $ million to $ million, as compared to a gross profit of $285 million for the three months ended December 31, 2023. Such was primarily due to .

For the three months ended December 29, 2024, we estimate that our operating profit will range from $ million to $ million, as compared to an operating loss of $116 million for the three months ended December 31, 2023. Such was primarily due to .

For the three months ended December 29, 2024, we estimate that our net income (loss) from continuing operations will range from $ million to $ million, as compared to a net loss from continuing operations of $131 million for the three months ended December 31, 2023. Such was primarily due to .

18

The following table reflects certain preliminary segment results for the three months ended December 29, 2024 and actual results for the three months ended December 31, 2023:

| Three Months Ended | |||||||||||||||||

December 29, 2024 (estimated) | December 31, 2023 (actual) | ||||||||||||||||

| Low | High | ||||||||||||||||

| (in millions except margin data) | |||||||||||||||||

| Segment Sales: | |||||||||||||||||

| Packaged Meats | $ | $ | $ | 2,404 | |||||||||||||

| Fresh Pork | 1,836 | ||||||||||||||||

| Hog Production | 819 | ||||||||||||||||

Other (1) | 178 | ||||||||||||||||

| Intersegment | (1,240) | ||||||||||||||||

| Consolidated | $ | 3,998 | |||||||||||||||

| Segment Profit: | |||||||||||||||||

| Packaged Meats | $ | $ | $ | 306 | |||||||||||||

| Fresh Pork | 45 | ||||||||||||||||

| Hog Production | (127) | ||||||||||||||||

Other (1) | 13 | ||||||||||||||||

________________

(1)Consists of our Mexico and Bioscience operations.

Segment Sales

Packaged Meats sales for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Fresh Pork sales for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Hog Production sales for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Segment Profit

Packaged Meats segment profit for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Fresh Pork segment profit for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Hog Production segment profit for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Segment profit from our Other segment operations for the three months ended December 29, 2024 by approximately $ million compared to the three months ended December 31, 2023, primarily attributable to .

Non-GAAP Measures

EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin are non-GAAP measures that should not be considered in isolation or as a substitute for other financial measures calculated and presented in accordance with

19

GAAP. For our definitions of EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin and information about how and why we use these non-GAAP measures, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Measures.”

The following table provides a preliminary reconciliation of preliminary estimated net income, the most directly comparable financial measure calculated in accordance with GAAP, to preliminary estimated EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin for the three months ended December 29, 2024, and a reconciliation of actual net income and actual net income margin to actual EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin for the three months ended December 31, 2023:

| Three Months Ended | |||||||||||||||||

December 29, 2024 (estimated) | December 31, 2023 (actual) | ||||||||||||||||

| Low | High | ||||||||||||||||

| (in millions except margin data) | |||||||||||||||||

| Net income (loss) from continuing operations | $ | $ | $ | (131) | |||||||||||||

| Interest expense, net | 17 | ||||||||||||||||

| Income tax expense (benefit) | $ | (42) | |||||||||||||||

| Depreciation and amortization | 131 | ||||||||||||||||

| EBITDA from continuing operations | $ | $ | $ | (24) | |||||||||||||

Litigation Charges (1) | 196 | ||||||||||||||||

West Coast Exit and Hog Production Reform (2) | 106 | ||||||||||||||||

| Incremental costs from destruction of property | 2 | ||||||||||||||||

| Adjusted EBITDA from continuing operations | $ | $ | $ | 279 | |||||||||||||

| Net income (loss) margin from continuing operations | % | % | (3.3) | % | |||||||||||||

| Adjusted EBITDA margin from continuing operations | % | % | 7.0 | % | |||||||||||||

________________

(1)Consists of accruals for the antitrust price-fixing and antitrust wage-fixing litigation matters that are described in “Note 17: Regulation and Contingencies” in the consolidated financial statements and accompanying notes included elsewhere in this prospectus.

(2)Consists of costs related to the closure of our Vernon, California processing facility, the sale or closure of certain farms in Arizona, California, Missouri and Utah and certain residual operating and restructuring expenses, including the termination of a number of agreements with contract farmers workforce reduction, due to discontinuation of operations in the West Coast and efforts to improve the cost structure of our Hog Production segment.

Summary of Risk Factors

Investing in our common stock involves a high degree of risk. You should carefully consider the risks described in “Risk Factors” before making a decision to invest in our common stock. If any of these risks actually occurs, our business, consolidated results of operations and consolidated financial condition, including cash flows, may be materially adversely affected. In such case, the trading price of our common stock may decline and you may lose part or all of your investment. Below is a summary of some of the principal risks we face.

•Our results of operations are cyclical and could be adversely affected by fluctuations in the commodity prices for meat, livestock (primarily hogs) and feed ingredients.

•Disruption of our supply chain could adversely affect our business, financial condition and results of operations.

•An inability to realize savings and efficiency gains could adversely affect profitability and we may be unable to achieve any or all of our financial and operational targets.

20