|

AURIZON MINES LTD.

CORPORATE PRESENTATION

January 2013

Aurizon Mines Ltd.

Recommends shareholders REJECT the Alamos Offer

|

Forward Looking Statements

This presentation contains forward-looking information (as defined in the Securities Act (British Columbia)) and forward-looking statements (collectively, “forward-looking statements”) that are prospective in nature. These statements refer to future events and include information concerning the Alamos Offer and the business operations, prospects and financial performance of Aurizon, which are subject to certain risks, uncertainties and assumptions.

Such forward-looking statements include statements regarding the value of the Company, estimates regarding production, costs of production, capital expenditures, expected recoveries, developments and exploration at Casa Berardi in 2013 as well as future production levels from and value estimates in respect of Casa Berardi, mineral resource estimates and exploration plans and potential in respect of other Company projects, the potential for alternative transactions and the terms thereof and risks relating to Alamos’s properties. All statements other than statements of historical fact may be forward-looking statements. Generally these forward-looking statements can often be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases, or statements that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved.

These forward-looking statements are based on a number of assumptions, including, but not limited to: assumptions regarding the Alamos Offer and the value of Aurizon’s assets, in particular Casa Berardi; whether or not an alternative transaction superior to the Alamos Offer may emerge; the successful completion of new development projects, planned expansions or other projects within the timelines anticipated and at anticipated production levels; the accuracy of reserve and resource estimates, grades, mine life and cash cost estimates; whether mineral resources can be developed; that pre-production capital costs, operating costs and sustaining and restoration costs will be as estimated; the availability of an experienced workforce and suppliers for the project; that equipment will be available when required and at estimated costs; that the assumptions underlying mineral resource estimates are valid and that no unforeseen accident, fire, ground instability, flooding, labour disruption, equipment failure, metallurgical, environmental or other events that could delay or increase the cost of development will occur; that the results of exploration activities will be consistent with the Company’s expectations; that the current price of and demand for gold will be sustained or will improve; that the supply of gold will remain stable; that the general business, political and economic conditions as well as those specific to the Company’s operations will not change in a material adverse manner; and that financing will be available if and when needed on reasonable terms. Although management of Aurizon believes that the assumptions made and the expectations represented by such statements are reasonable, there can be no assurance that a forward-looking statement herein will prove to be accurate.

Actual results and developments are likely to differ, and may differ materially, from those expressed or implied by the forward-looking statements contained in this presentation and even if such actual results and developments are realized or substantially realized, there can be no assurance that they will have the expected consequences or effects. Factors which could cause actual results to differ materially from current expectations include the availability of any superior alternatives to present to Aurizon Shareholders, whether any such alternative can be sufficiently advanced before the expiry of the Alamos Offer; the risk that some or all of the assumptions on which forward-looking statements are based prove to be invalid including that the cost of labour, equipment or materials, including power, will increase more than expected; that development and production inputs will become less available than expected; that the price of gold will decline; that the Canadian dollar will strengthen against the U.S. dollar; that mineral reserves or mineral resources are not as estimated; that actual costs or actual results of reclamation activities are greater than expected; that actual grades or recovery rates are lower than expected; the risk of unexpected occurrences that affect rates of production, including failure or disruption to plant, process or equipment, labour unrest, unexpected variations in ore reserves, grade or recovery rates and the occurrence of accidents; and the risks set forth in Aurizon’s Annual Information Form dated March 30, 2012 which is available under Aurizon’s profile on SEDAR at www.sedar.com. You should not place undue reliance on any forward-looking statements contained in this presentation.

Aurizon specifically disclaims any obligation to reissue or update these forward-looking statements as a result of new information or events after the date hereof, except as may be required by law. These forward-looking statements should not be relied upon as representing Aurizon’ views as of any date subsequent to the date of this presentation.

AURIZON MINES LTD.

2

|

Cautionary Statement

CAUTIONARY NOTE TO US READERS

Aurizon is required to describe mineral reserves associated with its properties utilizing Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) definitions of “proven” or “probable”, which categories of reserves are recognized by Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”), but which differ from those definitions in the disclosure requirements promulgated by the United States Securities and Exchange Commission (“SEC”) and contained in Industry Guide 7. In addition, under NI 43-101 the Company is required to describe mineral resources associated with its properties utilizing CIM definitions of “measured”, “indicated” or “inferred”, which categories of resources are recognized by Canadian regulations but are not defined terms under Industry Guide 7 and are not permitted to be used in reports and registration statements of United States companies filed with the SEC.

Accordingly, information contained in this presentation regarding our mineral deposits may not be comparable to similar information disclosed by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations of the SEC thereunder. In particular, this presentation uses the terms “measured” and “indicated” resources. U.S. readers are cautioned that while these terms are recognized and required by Canadian regulations, the SEC does not recognize them. U.S. investors are cautioned not to assume that all or any part of measured mineral resources or indicated mineral resources will ever be converted into mineral reserves.

This presentation also uses the term “inferred” resources. U.S readers are cautioned that while this term is recognized and required by Canadian regulations, the SEC does not recognize it. “Inferred resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. U.S. readers are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally mineable.

For additional information regarding reserves and resource information set forth in this presentation, refer to our public filings, including our NI 43-101 technical reports, available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

AURIZON MINES LTD.

3

|

Overview

Aurizon’s Board of Directors Unanimously Recommends Shareholders REJECT the Alamos Hostile Take-Over Bid

Any Aurizon Shareholder who has already deposited Aurizon Shares under the Alamos Offer should WITHDRAW their Aurizon Shares

The Alamos offer does NOT provide sufficient value for Aurizon and its assets, and introduces increased risks to Aurizon’s shareholders

Aurizon in discussions with third parties to maximize shareholder value

REJECT and Do NOT TENDER your shares

AURIZON MINES LTD.

4

|

Aurizon Board Actions

Formed Special Committee to review Alamos Offer

Engaged Scotia Capital Inc. and CIBC World Markets as financial advisors

Hired independent counsel

Reviewing strategic alternatives

Confidentiality agreements signed with third parties

On-line data room established

Discussions and due diligence with third parties in progress

Ongoing communication with shareholders

AURIZON MINES LTD.

5

|

Reasons for REJECTION

OPPORTUNISTIC AND INADEQUATE

Inadequate from a financial point of view to Aurizon’s shareholders

Alamos is seeking to acquire control without paying an adequate premium for that control

Opportunistic timing ahead of future growth

Alamos’ assets are subject to significant risks

AURIZON MINES LTD.

6

Reasons for REJECTION

OPPORTUNISTIC AND INADEQUATE

Decreases Aurizon’s shareholders exposure to its own assets

Exposes Aurizon’s shareholders to increased geopolitical risk in Mexico and Turkey

Exposes Aurizon’s shareholders to increased development risk

Exposes Aurizon’s shareholders to dilution through potential future equity issuances to fund development of Turkish assets

Board is aggressively pursuing value maximizing alternatives

AURIZON MINES LTD

Reasons to REJECT the Alamos Offer Alamos Offer fails to recognize the potential of the Joanna Hosco Pit Project, Hosco West Extension and the Heva properties Joanna and other exploration assets total $195 million¹ Hosco Area – Mineral Reserves and Resources (In-Pit)² Proven & Probable Reserves: 1,660,400 ounces Measured & Indicated Resources: 601,000 ounces Inferred Resources: 266,000 ounces Updating Resources Heva Resource Inventory³: (Non-refractory) Q1 2013 Measured & Indicated: 270,000 ounces Inferred: 421,000 ounces Alamos Offer DOES NOT RECOGNIZE the potential of the Hosco and Heva properties, and their favourable location along the Golden Highway in Quebec ¹ Based on research analyst net asset value (“NAV”) consensus estimates ²,³See Aurizon news release dated June 5, 2012, available on www.aurizon.com and on SEDAR AURIZON MINES LTD

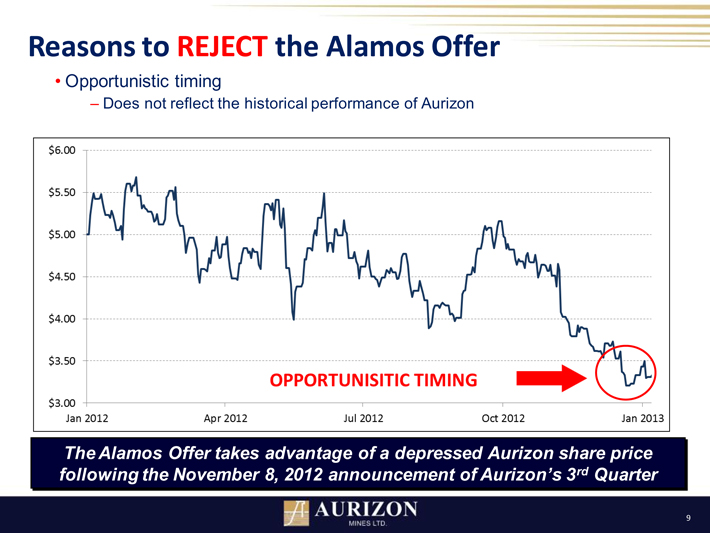

Reasons to REJECT the Alamos Offer Opportunistic timing Does not reflect the historical performance of Aurizon The Alamos Offer takes advantage of a depressed Aurizon share price following the November 8, 2012 announcement of Aurizon’s 3rd Quarter AURIZON MINES LTD

|

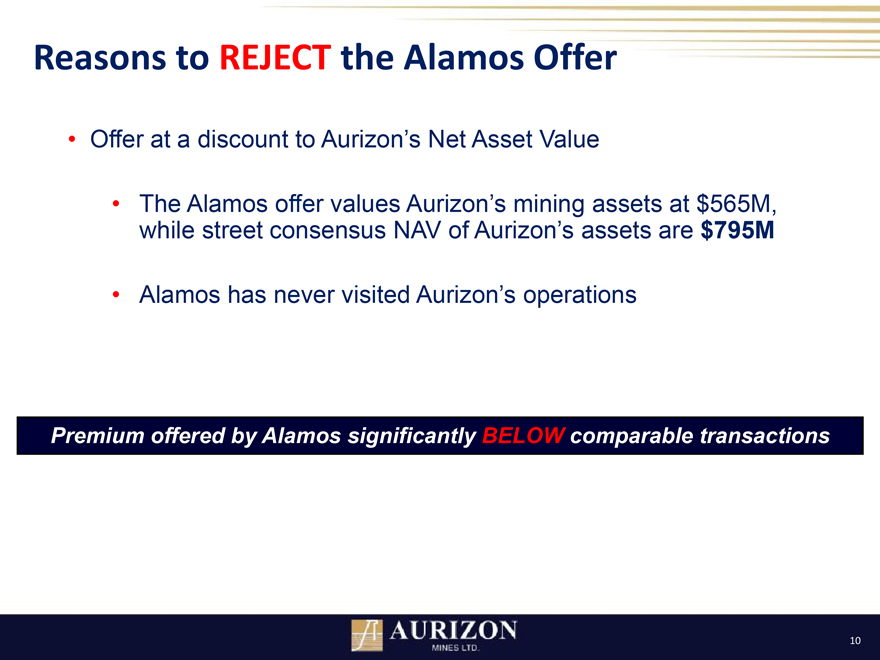

Reasons to REJECT the Alamos Offer

Offer at a discount to Aurizon’s Net Asset Value

The Alamos offer values Aurizon’s mining assets at $565M, while street consensus NAV of Aurizon’s assets are $795M

Alamos has never visited Aurizon’s operations

Premium offered by Alamos significantly BELOW comparable transactions

AURIZON MINES LTD.

10

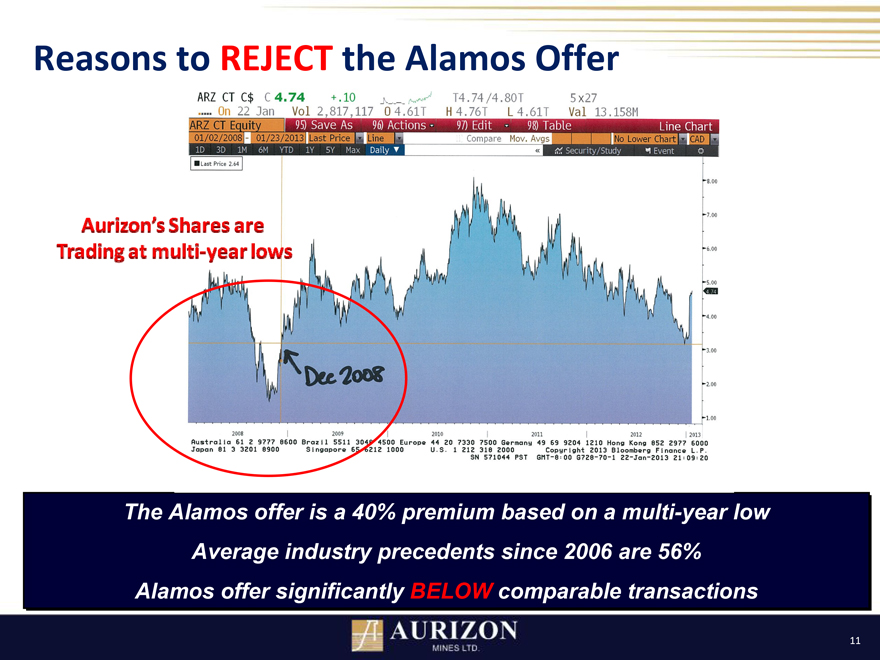

Reasons to REJECT the Alamos Offer

Aurizon’s Shares are Trading at multi-year lows

The Alamos offer is a 40% premium based on a multi-year low Average industry precedents since 2006 are 56% Alamos offer significantly BELOW comparable transactions

11

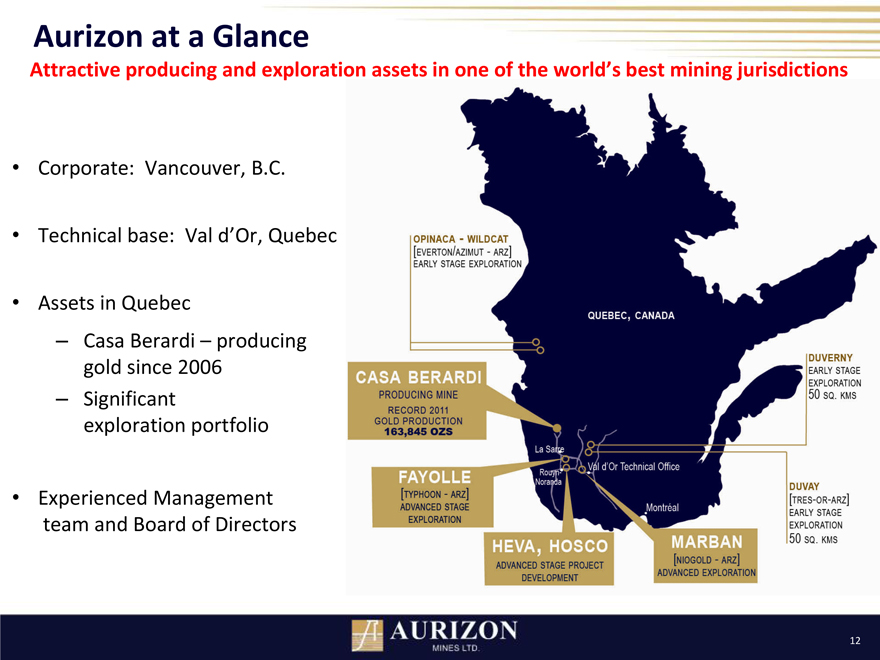

Aurizon at a Glance

Attractive producing and exploration assets in one of the world’s best mining jurisdictions

Corporate: Vancouver, B.C.

Technical base: Val d’Or, Quebec

Assets in Quebec

Casa Berardi – producing gold since 2006

Significant exploration portfolio

Experienced Management team and Board of Directors

12

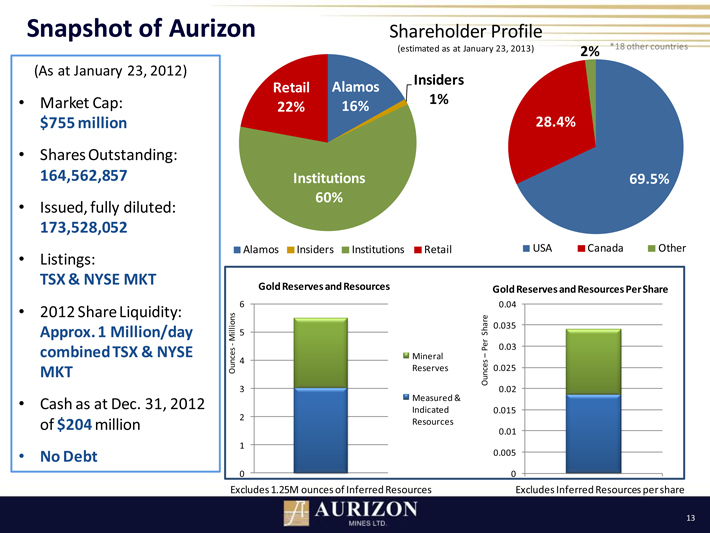

Snapshot of Aurizon (As at January 23, 2012) Market Cap: $755 million Shares Outstanding: 164,562,857 Issued, fully diluted: 173,528,052 Listings: TSX & NYSE MKT 2012 Share Liquidity: Approx. 1 Million/day combined TSX & NYSE MKT Cash as at Dec. 31, 2012 of $204 million No Debt Excludes 1.25M ounces of Inferred Resources Excludes Inferred Resources per share

Analyst Coverage (January 24, 2013) As of January 24, 2013 ‐Recent Analyst Coverage Current Price Name Analyst Target BMO Capital Brian Quast $4.65 CIBC Cosmos Chiu $6.00 Desjardins Securities Adam Melnyk $5.50 Dundee Securities¹ Joe Fazzini (Current Analyst) $5.00 Edison Investment Research Charles Gibson $5.55² Euro Pacific Capital Inc. Heiko Ihle $5.20 Global Hunter Securities Jeff Wright $6.50 Loewen, Ondaatje, McCutcheon Ltd. Michael Fowler $6.00 Mackie Research Barry Allen/Ryan Hanley $5.50 NBF Paolo Lostritto $5.00 Scotia Capital Ovais Habib $6.50 ¹ Latest Report written by former analyst Ron Stewart ² Edison provides a share price valuation Average Analyst Share Price Target – pre‐announcement $5.41 post‐announcement $5.68

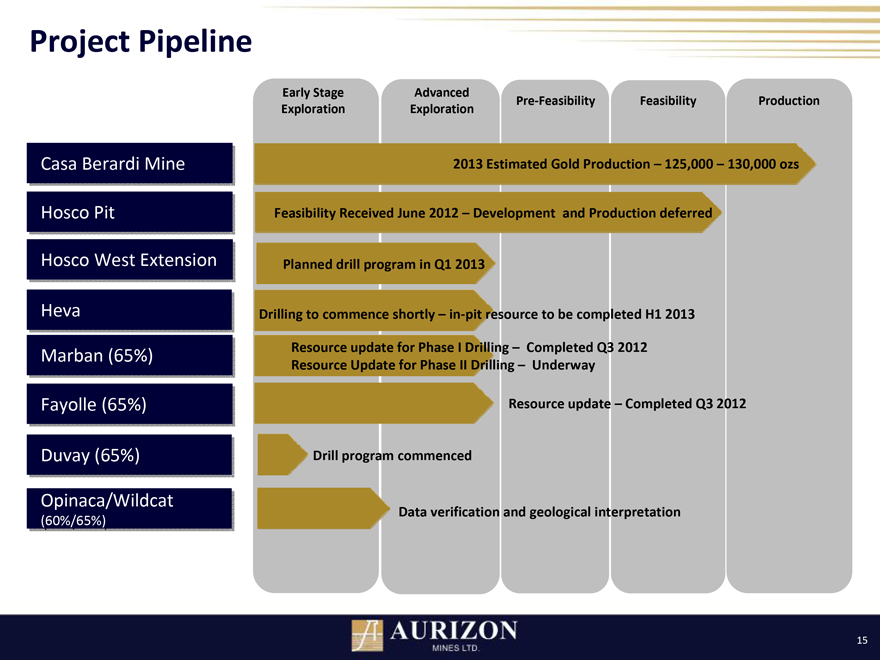

Project Pipeline

Early Stage Advanced

Pre-Feasibility Feasibility Production

Exploration Exploration

Casa Berardi Mine 2013 Estimated Gold Production – 125,000 – 130,000 ozs

Hosco Pit Feasibility Received June 2012 – Development and Production deferred

Hosco West Extension Planned drill program in Q1 2013

Heva Drilling to commence shortly – in-pit resource to be completed H1 2013

Marban (65%) Resource update for Phase I Drilling – Completed Q3 2012

Resource Update for Phase II Drilling – Underway

Fayolle (65%) Resource update – Completed Q3 2012

Duvay (65%) Drill program commenced

Opinaca/Wildcat

Data verification and geological interpretation

(60%/65%)

15

Casa Berardi Overview

16

Casa Berardi

2012 production – 136,848 ounces

Tonnes processed – 693,859 at an average grade of 6.8 g/t with recoveries for the year of 90.6%

1,896 tonnes per day underground production rate

Five -seven underground and three surface drill rigs will be active in 2013

Currently in transition phase at Casa Berardi while we are installing the required infrastructure to commence mining new areas east of the production shaft

These new areas will be the foundation of future underground production at Casa Berardi

Shaft sinking and lateral development out to the 118 and 123 Zones are in progress, and operation is expected to transition from the existing mining areas over the next 18 months

17

Casa Berardi -2013

Commencing its seventh year of production

Operating flexibility will be constrained in the first half of 2013 during the continued shaft sinking and lateral development out to the 118 and 123 Zones

Estimated production of 125,000 – 130,000 ounces of gold in 2013

Average estimated grade of 7.2 grams of gold per tonne

Gold production should gradually increase through the year as more stopes become available and should reach historic levels in the second half

Major shutdowns are planned for 2013, particularly in the first quarter, in order to switch over to the deepened shaft and incorporate new infrastructure into the mining schedule

Average daily ore throughput is estimated at 1,760 tonnes per day

Mine sequencing in 2013 will result in ore grades that are expected to be 6% higher than 2012 at approximately 7.2 grams per tonne

Zone 118 is expected to provide ore for the first time in Q3 with an anticipated average grade in 2013 of approximately 7.9 grams per tonne

18

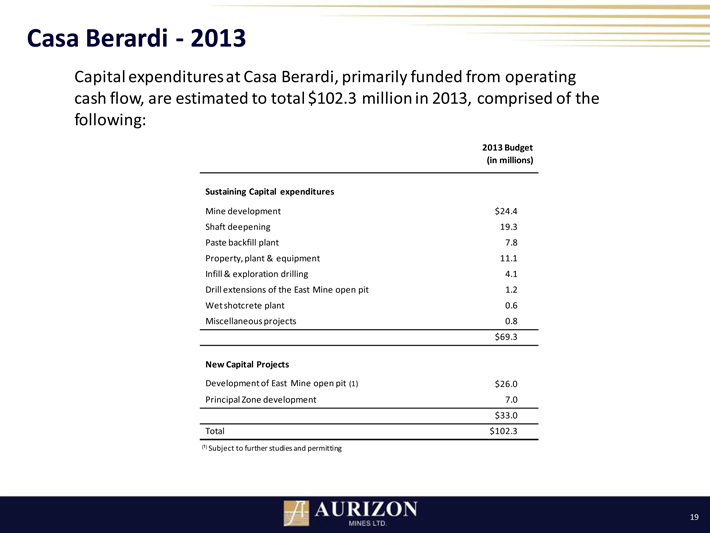

Casa Berardi 2013 , cash flow, are estimated to total $102.3 million in 2013, comprised of the following: 2013 Budget (in millions) Sustaining Capital expenditures Mine development $24.4 Shaft deepening 19.3 Paste backfill plant 7.8 Property, plant & equipment 11.1 Infill & exploration drilling 4.1 Drill extensions of the East Mine open pit 1.2 Wet shotcrete plant 0.6 Miscellaneous projects 0.8 $69.3 New Capital Projects Development of East Mine open pit (1) $26.0 Principal Zone development 7.0 $33.0 Total $102.3 (¹) Subject to further studies and permitting

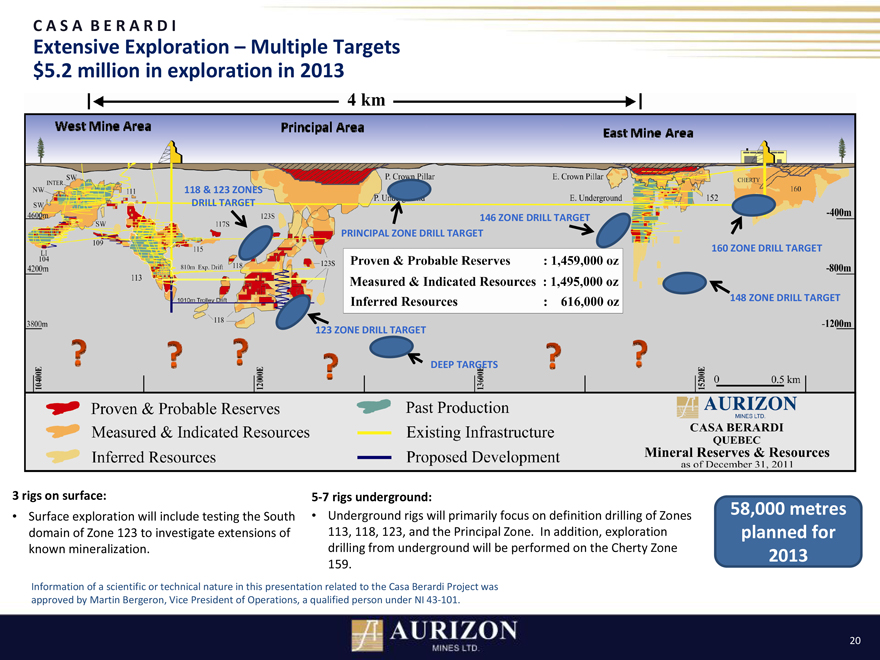

CAS A B E R A R D I

Extensive Exploration – Multiple Targets $5.2 million in exploration in 2013

West Mine Area Principal Area

East Mine Area

118 & 123 ZONES DRILL TARGET

146 ZONE DRILL TARGET PRINCIPAL ZONE DRILL TARGET

160 ZONE DRILL TARGET

148 ZONE DRILL TARGET

123 ZONE DRILL TARGET

DEEP TARGETS

3 rigs on surface: 5-7 rigs underground:

Surface exploration will include testing the South Underground rigs will primarily focus on definition drilling of Zones domain of Zone 123 to investigate extensions of 113, 118, 123, and the Principal Zone. In addition, exploration known mineralization. drilling from underground will be performed on the Cherty Zone 159.

Information of a scientific or technical nature in this presentation related to the Casa Berardi Project was approved by Martin Bergeron, Vice President of Operations, a qualified person under NI 43-101.

58,000 metres planned for 2013

20

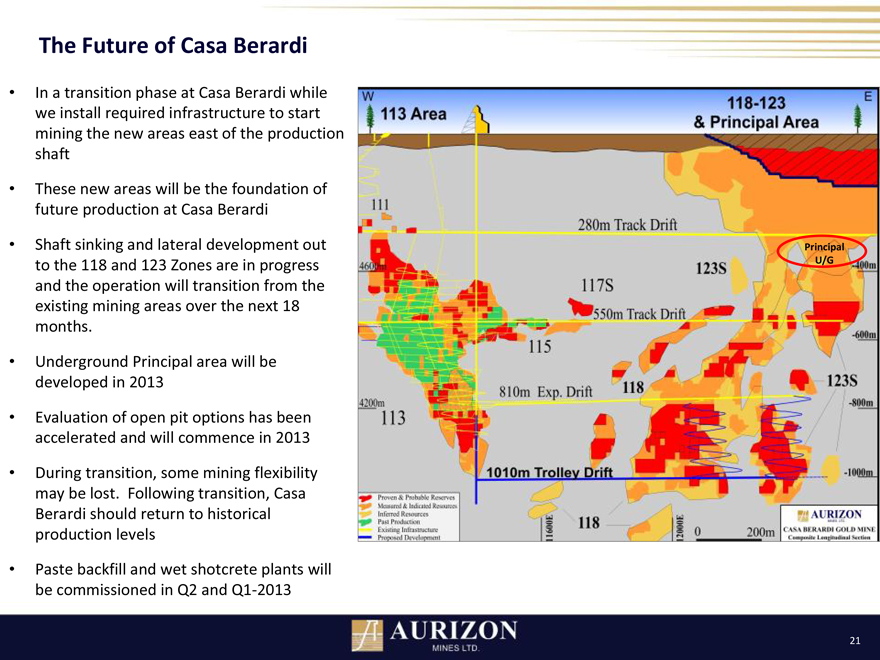

The Future of Casa Berardi

In a transition phase at Casa Berardi while we install required infrastructure to start mining the new areas east of the production shaft

These new areas will be the foundation of future production at Casa Berardi

Shaft sinking and lateral development out to the 118 and 123 Zones are in progress and the operation will transition from the existing mining areas over the next 18 months.

Underground Principal area will be developed in 2013

Evaluation of open pit options has been accelerated and will commence in 2013

During transition, some mining flexibility may be lost. Following transition, Casa Berardi should return to historical production levels

Paste backfill and wet shotcrete plants will be commissioned in Q2 and Q1-2013

21

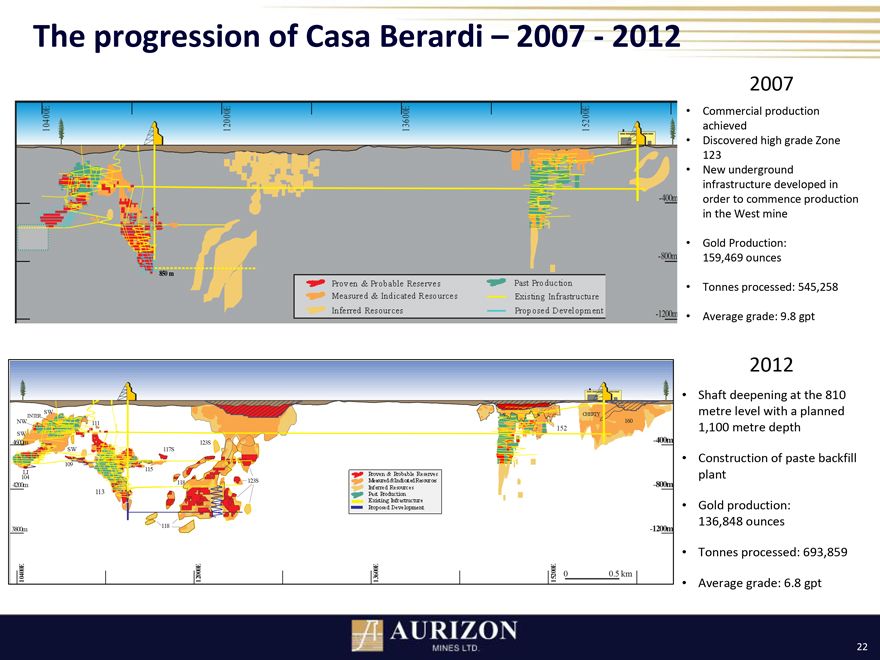

The progression of Casa Berardi – 2007 -2012

2007

Commercial production achieved Discovered high grade Zone 123 New underground infrastructure developed in order to commence production in the West mine

Gold Production: 159,469 ounces

Tonnes processed: 545,258

Average grade: 9.8 gpt

2012

Shaft deepening at the 810 metre level with a planned 1,100 metre depth

Construction of paste backfill plant

Gold production: 136,848 ounces

Tonnes processed: 693,859

Average grade: 6.8 gpt

22

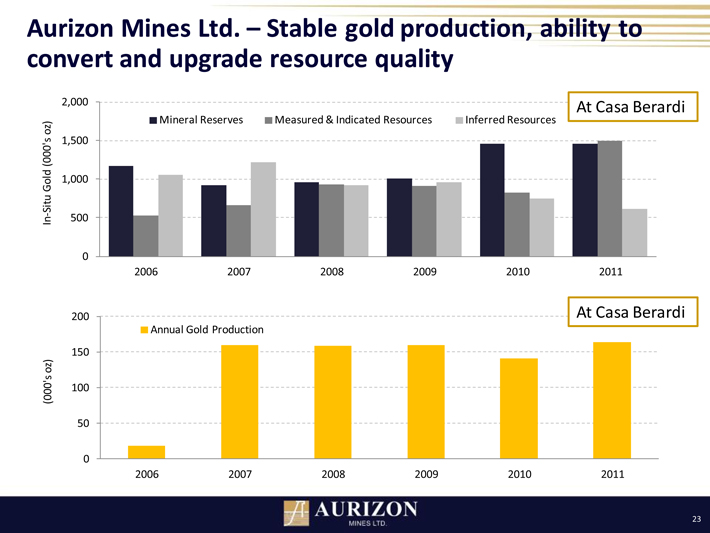

Aurizon Mines Ltd. –Stable gold production, ability to convert and upgrade resource quality 2,000 At Casa Berardi Mineral Reserves Measured & Indicated Resources Inferred Resources oz) 0’s 1,500 (00 1,000 Gold Situ 500 In 0 2006 2007 2008 2009 2010 2011 200 At Casa Berardi Annual Gold Production 150 oz) s (000’ 100 50 0 2006 2007 2008 2009 2010 2011

Heva and Hosco West Extension and the Joanna Hosco Pit

Development Property Location location location

Extending 6 kilometres along the Cadillac Break

20 kilometres east of the city of Rouyn-Noranda

Aurizon owns a 100% interest, subject to certain underlying royalties, in all of the sectors comprising the Joanna Project.

Positive Feasibility study in June 2012 – Hosco Very encouraging drill results-Heva

24

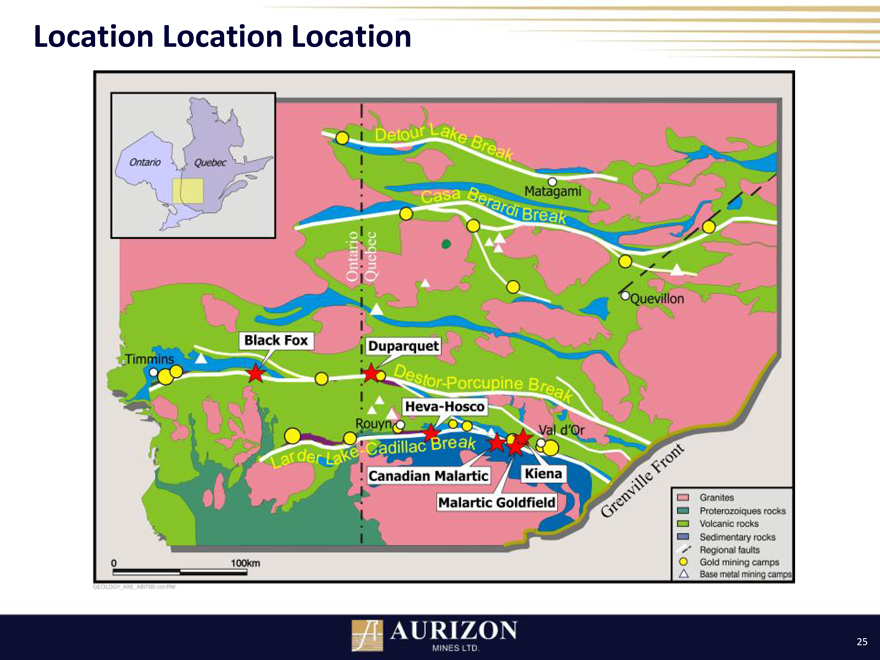

Location Location Location

25

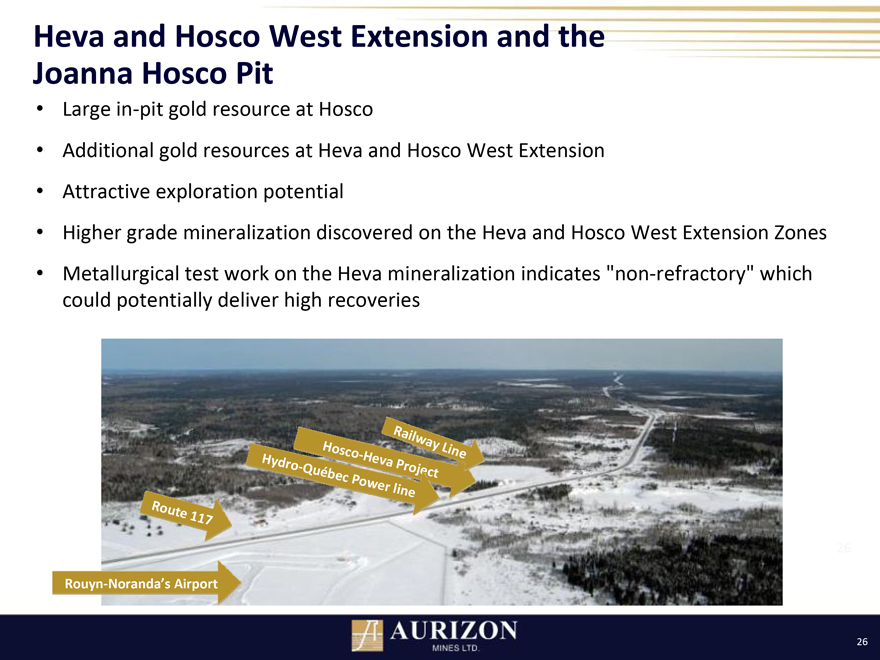

Heva and Hosco West Extension and the Joanna Hosco Pit

Large in-pit gold resource at Hosco

Additional gold resources at Heva and Hosco West Extension

Attractive exploration potential

Higher grade mineralization discovered on the Heva and Hosco West Extension Zones

Metallurgical test work on the Heva mineralization indicates “non-refractory” which could potentially deliver high recoveries

Rouyn-Noranda’s Airport,

Route 117

Hydro-Quebec Power line

Hosco-Heva Project

Railway Line

26

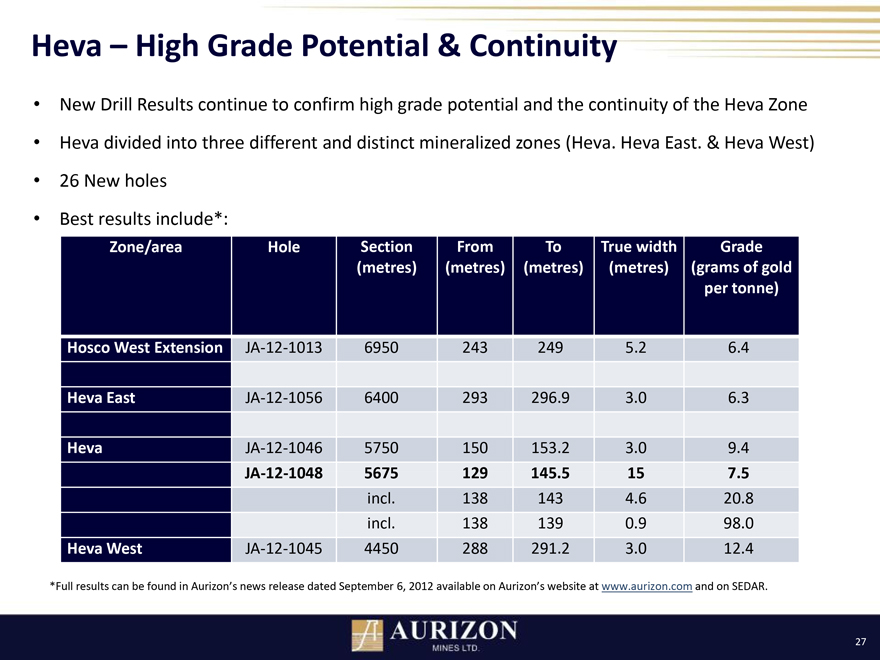

Heva – High Grade Potential & Continuity

New Drill Results continue to confirm high grade potential and the continuity of the Heva Zone

Heva divided into three different and distinct mineralized zones (Heva. Heva East. & Heva West)

26 New holes

Best results include*:

Zone/area Hole Section From To True width Grade

(metres)(metres)(metres)(metres)(grams of gold

per tonne)

Hosco West Extension JA-12-1013 6950 243 249 5.2 6.4

Heva East JA-12-1056 6400 293 296.9 3.0 6.3

Heva JA-12-1046 5750 150 153.2 3.0 9.4

JA-12-1048 5675 129 145.5 15 7.5

incl. 138 143 4.6 20.8

incl. 138 139 0.9 98.0

Heva West JA-12-1045 4450 288 291.2 3.0 12.4

*Full results can be found in Aurizon’s news release dated September 6, 2012 available on Aurizon’s website at www.aurizon.com and on SEDAR.

27

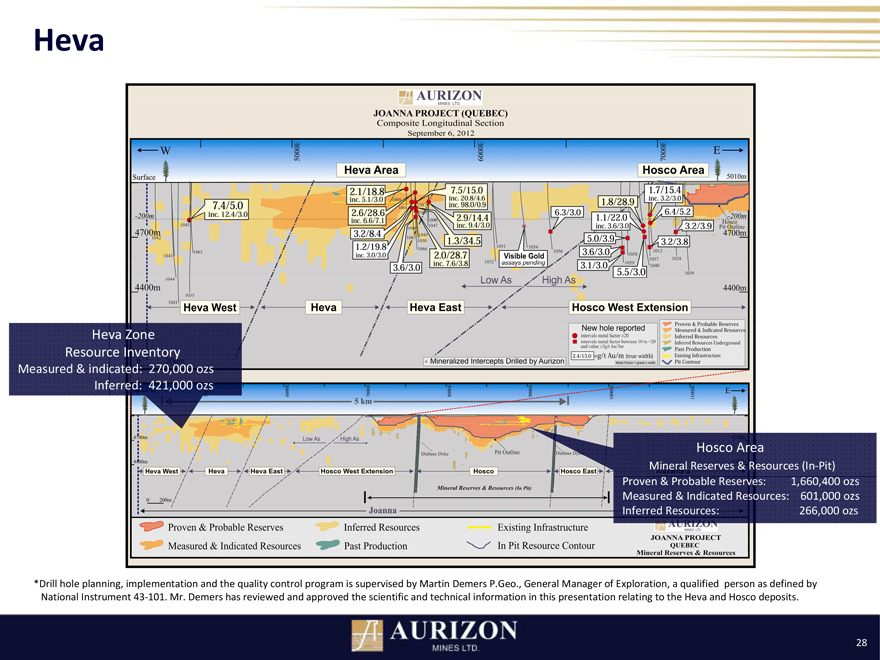

Heva

Heva Zone Resource Inventory

Measured & indicated: 270,000 ozs Inferred: 421,000 ozs

Hosco Area

Mineral Reserves & Resources (In-Pit)

Proven & Probable Reserves: 1,660,400 ozs Measured & Indicated Resources: 601,000 ozs

Inferred Resources: 266,000 ozs

*Drill hole planning, implementation and the quality control program is supervised by Martin Demers P.Geo., General Manager of Exploration, a qualified person as defined by National Instrument 43-101. Mr. Demers has reviewed and approved the scientific and technical information in this presentation relating to the Heva and Hosco deposits.

28

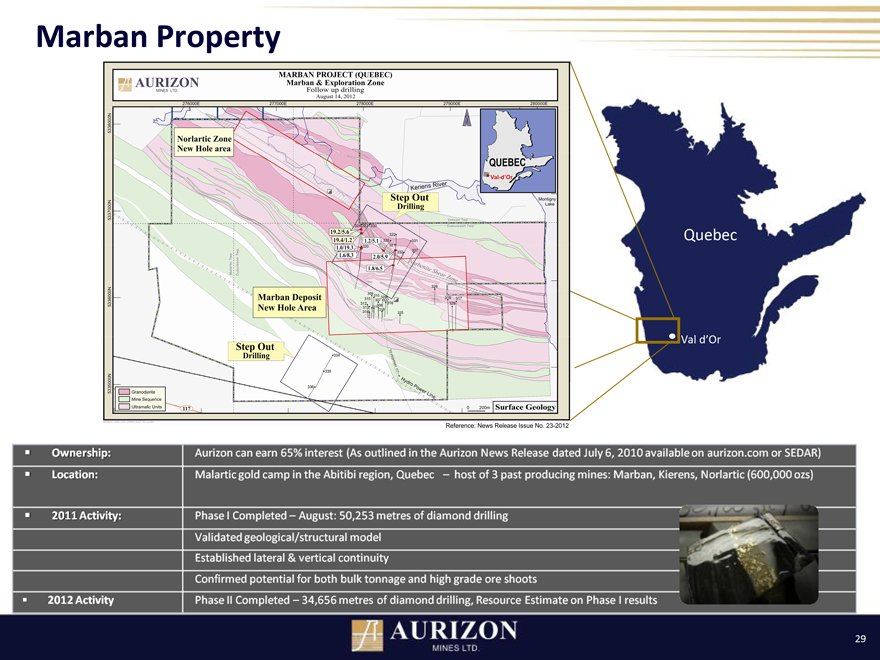

Marban Property

Quebec

Val d’Or

Ownership: Aurizon can earn 65% interest (As outlined in the Aurizon News Release dated July 6, 2010 available on aurizon.com or SEDAR)

Location: Malartic gold camp in the Abitibi region, Quebec – host of 3 past producing mines: Marban, Kierens, Norlartic (600,000 ozs)

2011 Activity: Phase I Completed – August: 50,253 metres of diamond drilling

Validated geological/structural model

Established lateral & vertical continuity

Confirmed potential for both bulk tonnage and high grade ore shoots

2012 Activity Phase II Completed – 34,656 metres of diamond drilling, Resource Estimate on Phase I results

29

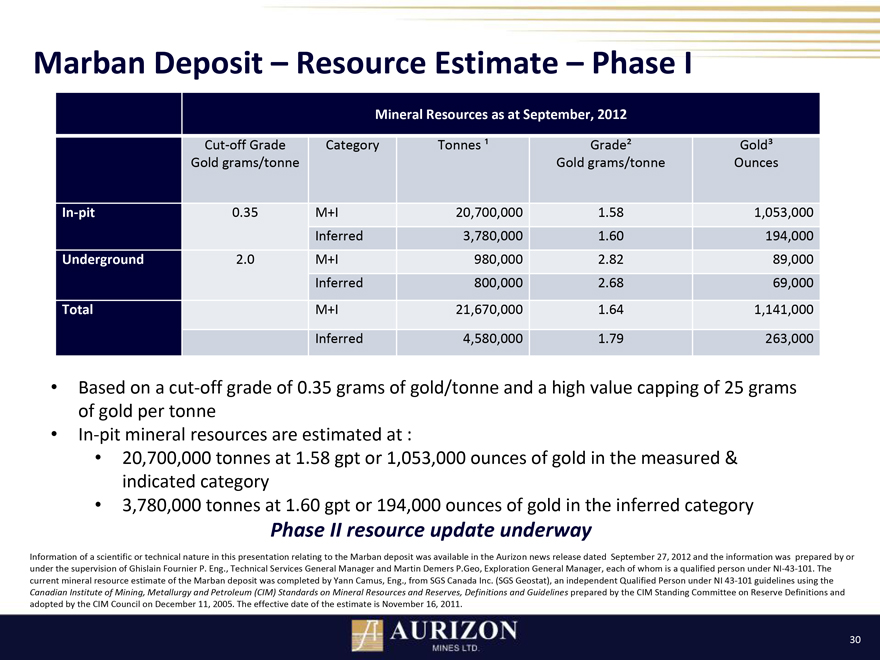

Marban Deposit – Resource Estimate – Phase I

Mineral Resources as at September, 2012

Cut-off Grade Category Tonnes ¹ Grade² Gold³

Gold grams/tonne Gold grams/tonne Ounces

In-pit 0.35 M+I 20,700,000 1.58 1,053,000

Inferred 3,780,000 1.60 194,000

Underground 2.0 M+I 980,000 2.82 89,000

Inferred 800,000 2.68 69,000

Total M+I 21,670,000 1.64 1,141,000

Inferred 4,580,000 1.79 263,000

Based on a cut-off grade of 0.35 grams of gold/tonne and a high value capping of 25 grams of gold per tonne

In-pit mineral resources are estimated at :

20,700,000 tonnes at 1.58 gpt or 1,053,000 ounces of gold in the measured & indicated category

3,780,000 tonnes at 1.60 gpt or 194,000 ounces of gold in the inferred category

Phase II resource update underway

Information of a scientific or technical nature in this presentation relating to the Marban deposit was available in the Aurizon news release dated September 27, 2012 and the information was prepared by or under the supervision of Ghislain Fournier P. Eng., Technical Services General Manager and Martin Demers P.Geo, Exploration General Manager, each of whom is a qualified person under NI-43-101. The current mineral resource estimate of the Marban deposit was completed by Yann Camus, Eng., from SGS Canada Inc. (SGS Geostat), an independent Qualified Person under NI 43-101 guidelines using the

Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by the CIM Council on December 11, 2005. The effective date of the estimate is November 16, 2011.

30

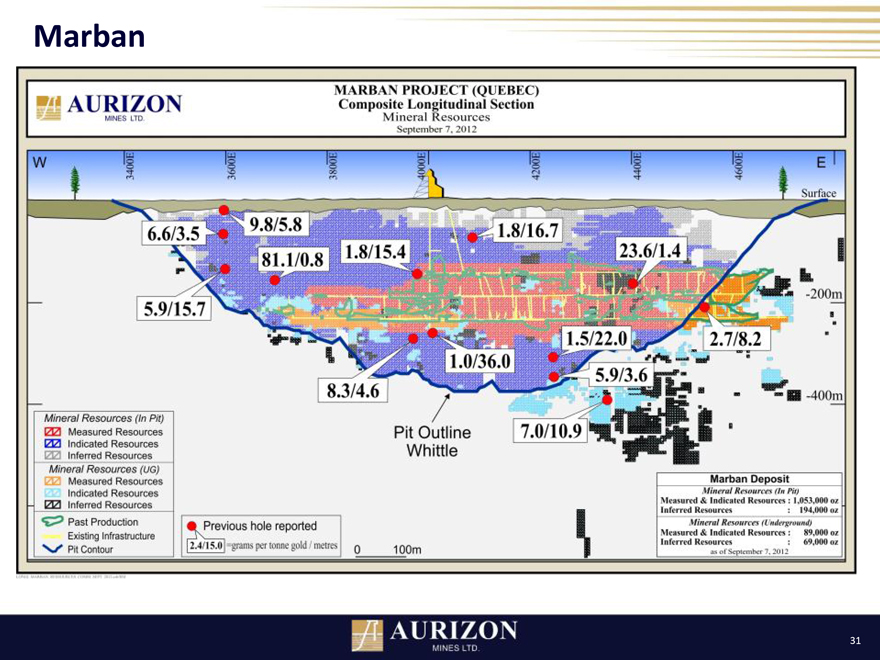

Marban

31

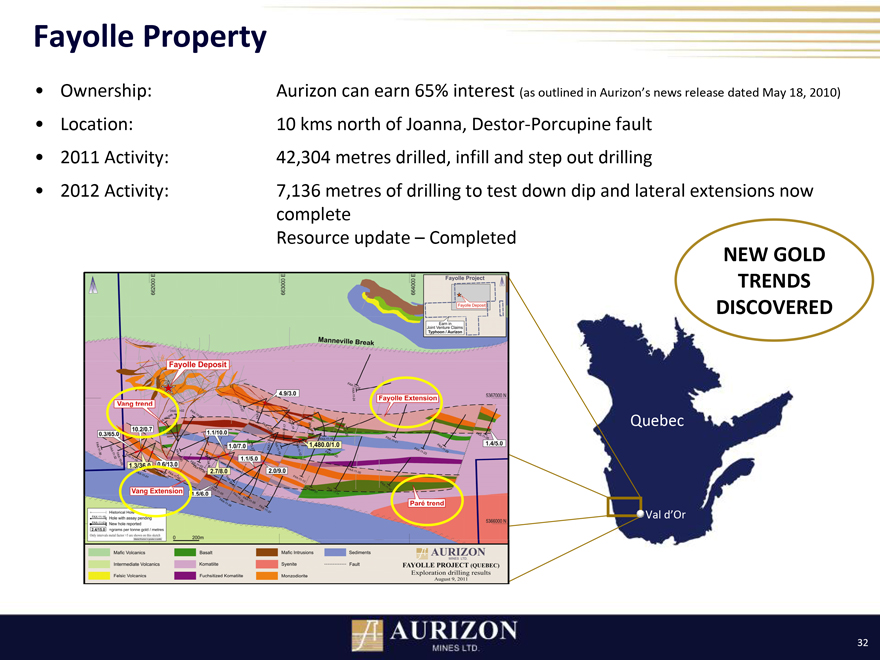

Fayolle Property

Ownership: Aurizon can earn 65% interest (as outlined in Aurizon’s news release dated May 18, 2010)

NEW GOLD TRENDS DISCOVERED

Location: 10 kms north of Joanna, Destor-Porcupine fault

2011 Activity: 42,304 metres drilled, infill and step out drilling

2012 Activity: 7,136 metres of drilling to test down dip and lateral extensions now complete Resource update – Completed

Quebec

Val d’Or

32

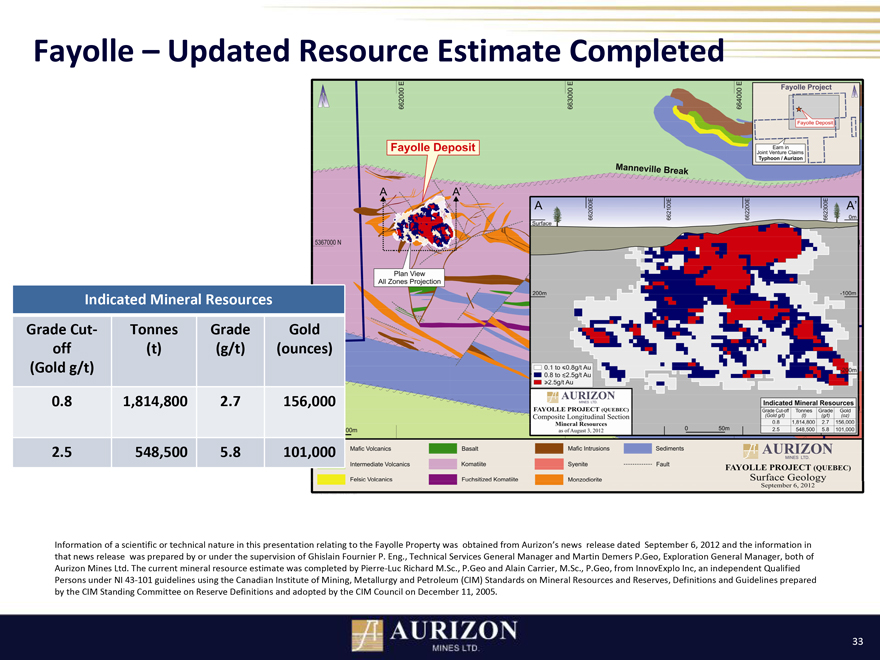

Fayolle – Updated Resource Estimate Completed

Indicated Mineral Resources

Grade Cut- Tonnes Grade Gold

off(t)(g/t)(ounces)

(Gold g/t)

0.8 |

| 1,814,800 2.7 156,000 |

2.5 |

| 548,500 5.8 101,000 |

Information of a scientific or technical nature in this presentation relating to the Fayolle Property was obtained from Aurizon’s news release dated September 6, 2012 and the information in that news release was prepared by or under the supervision of Ghislain Fournier P. Eng., Technical Services General Manager and Martin Demers P.Geo, Exploration General Manager, both of Aurizon Mines Ltd. The current mineral resource estimate was completed by Pierre-Luc Richard M.Sc., P.Geo and Alain Carrier, M.Sc., P.Geo, from InnovExplo Inc, an independent Qualified Persons under NI 43-101 guidelines using the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by the CIM Council on December 11, 2005.

33

Well Positioned Continued Positive Growth Results

Strong balance sheet Open for opportunities to

Heva, Hosco and Casa Unhedged, debt free grow and de-risk Berardi

Casa Berardi

Transitioning to the new areas Building a foundation for future production

Installing infrastructure to improve future mining efficiencies Open pit and Principal underground opportunities

34

Questions?

January 2013

Aurizon Mines Ltd.

Recommends shareholders REJECT the Alamos Offer

Aurizon Mines Ltd.

Recommends shareholders REJECT the Alamos

Contact Information

Stock Symbols:

George Paspalas

ARZ:TSX

President and Chief Executive Officer

AZK: NYSE MKT

Ian S. Walton

Corporate Office:

Executive Vice President and Chief Financial Officer

Suite 1120-925 W. Georgia Street,

Vancouver, BC V6C 3L2

Martin Bergeron

Phone: 604-687-6600

Vice President, Operations

Fax: 604-687-3932

Website: www.aurizon.com

Julie Kemp

Email: info@aurizon.com

Corporate Secretary

Quebec Office:

Martin Demers, 1010 – 3rd Avenue East

General Manager, Exploration

Val-d’Or, Quebec

J9P 4P5

Jennifer North

Phone: 819-874-4511

Manager, Investor Relations

Fax: 819-874-3391

info@aurizon.qc.ca

Marc Turcotte

Director of Corporate Development

January 2013

Notes Regarding Disclosure of Technical Information

Notes Regarding Disclosure of Technical Information

Reserve and resource information for the Heva/Hosco West Extension properties is derived from Aurizon’s news release dated June 5, 2012, which is available on SEDAR at www.sedar.com under Aurizon’s profile. In-pit mineral reserves of 1.66 million ounces of gold is based on 41.1 million tonnes at 1.26 grams/tonne using a cut-off grade of 0.5 g/t. The measured resource estimate (exclusive of mineral reserves) of 69,196 ounces of gold for the Hosco deposit is based on 1,887,011 tonnes at 1.14 g/t using a cut-off grade of 0.5 g/t. The indicated resource estimate (exclusive of mineral reserves) of an aggregate of 806,567 ounces of gold for the Hosco and Heva deposits is based on (i) 13,922,298 tonnes at 1.19 g/t using a cut-off grade of 0.5 g/t for Hosco (in-pit), (ii) 50,000 tonnes at 2.65 g/t using a cut-off grade of 2.0 g/t for Hosco (underground), and (iii) 4,410,000 tonnes at 1.90 g/t using a cut-off grade of 0.5 g/t for Heva. The inferred mineral resource estimate of an aggregate of 831,000 ounces of gold for the Hosco, Heva, and Alexandria deposits is based on (i) 6,950,000 tonnes at 1.19 g/t using a cut-off grade of 0.5 g/t for Hosco (in-pit), (ii) 590,000 tonnes at 2.54 g/t using a cut-off grade of 2.0 g/t for Hosco (underground), (iii) 7,680,000 tonnes at 1.70 g/t using a cut-off grade of 0.5 g/t for Heva, (iv) 650,000 tonnes at 2.80 g/t using a cut-off grade of 2.0 g/t for Heva (underground), and (v) 980,000 tonnes at 1.20 g/t using a cut-off grade of 0.5 g/t for Alexandria.

Reserve and resource information for the Casa Berardi project is derived from Aurizon’s news release dated February 27, 2012, which is available on SEDAR at www.sedar.com under Aurizon’s profile. Mineral reserves of 1.46 million ounces of gold is based on 4.7 million tonnes at 6.7 g/t (underground) and 3.8 million tonnes at 3.7 g/t (open pit). Measured resources (exclusive of mineral reserves) of 350,300 ounces of gold is based on 1.85 million tonnes at 5.9 g/t. Indicated resources (exclusive of mineral reserves) of 1.14 million ounces of gold is based on 9.02 million tonnes at 3.9 g/t. Inferred resources of 616,000 ounces of gold is based on 4.95 million tonnes at 3.9 g/t.

Mineral resources that are not mineral reserves do not have demonstrated economic viability.