Exhibit 99.1

The Irreplaceable CornerTM Company

Institutional Quality Real Estate

Operating Platform Approaching $1 Billion

Invested in Three of the Top Six Employment Growth Markets in U.S.

Creating Value for a Quarter of a Century

The Irreplaceable Corner™ Company

Disclosure

Additional Information and Where to Find It

In connection with the proposed merger, the Company has filed but not yet distributed to shareholders a proxy statement with the Securities and Exchange Commission. The proxy statement distributed to shareholders will contain information about the Company, the proposed merger and related matters. SHAREHOLDERS ARE URGED TO READ THE PROXY STATEMENT CAREFULLY WHEN IT IS AVAILABLE, AS IT WILL CONTAIN IMPORTANT INFORMATION THAT SHAREHOLDERS SHOULD CONSIDER BEFORE MAKING A DECISION ABOUT THE MERGER. In addition to receiving the proxy statement from the Company by mail, shareholders will be able to obtain the proxy statement, as well as other filings containing information about the Company, without charge, from the Securities and Exchange Commission’s website (http://www.sec.gov) or, without charge, from the Company at http://www.amreit.com or by directing such request to AmREIT, 8 Greenway Plaza, Suite 1000, Houston, TX 77046, Attention: Investor Relations.

Participants in the Solicitation

The Company and its directors and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies in respect of the merger. Information about the Company’s directors and executive officers and their ownership of the Company’s common stock is set forth in the proxy statement related to the merger, as well as the proxy statement for the Company’s 2009 Annual Meeting of Shareholders, which was filed with the SEC on April 7, 2007, and the Company’s Annual Report on Form 10-K, which was filed with the SEC on March 31, 2009. Shareholders may obtain additional information regarding the interests of the Company and its directors and executive officers in the merger, which may be different than those of the Company’s shareholders generally, by reading the proxy statement and other relevant documents regarding the merger, when filed with the SEC.

Cautionary Statement Regarding Forward-Looking Statements

The Company has made forward-looking statements in these materials which are subject to risks and uncertainties. These statements are based on the beliefs and assumptions of the Company, and on the information currently available to the Company.

When used or referred to in these materials, these forward-looking statements may be preceded by, followed by or otherwise include the words “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “projects” or similar expressions, or statements that certain events or conditions “will” or “may” occur. These forward-looking statements are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. The following factors, among others, could cause actual results to differ materially from those described in the forward-looking statements:

cost savings expected from the merger may not be fully realized;

Revenue of the combined company following the merger may be lower than expected

Occupancy rates from the Company’s properties may deteriorate or fail to recover as predicted;

The Company may not be able to sustain the rental rate increases upon lease renewals that it has recently experienced;

The Company may experience tenant defaults due to recessionary conditions, as well as tenant bankruptcies and abandonments of leases;

General economic conditions, either internationally or nationally or in the jurisdictions in which REITPlus or AmREIT are doing business, may be less favorable than expected;

Legislative or regulatory changes, including changes in environmental regulation, may adversely affect the businesses in which REITPlus and AmREIT are engaged;

There may be environmental risks and liability under federal, state and foreign environmental laws and regulations; and

Changes may occur in the securities or capital markets.

Except for its ongoing obligations to disclose material information as required by the federal securities laws, the Company has no intention or obligation to update these forward-looking statements after it distributes these materials.

www.amreit.com

2

Vision 2010 - Phases

Phase I:

Business Model – changes to reach greater efficiency and reduce volatility

of earnings. This phase includes the elimination of the general contracting

business and IBD Securities business. Estimated G&A Savings of $4 -

$4.5 million per year. Phase I was executed during the 3rd and 4th quarters

of 2008.

Phase II:

Capital Structure – changes to reach greater efficiency and reduce

volatility of earnings. This will include the simplification of AmREIT’s equity

capitalization into one Class of stock, the consolidation of AmREIT into

REITPlus and the privatization of the Company. Phase II will be executed

during 2009.

Phase III:

Growth & Liquidity – made possible by Phase I and II as we pursue our

goal to grow our platform within seven of the top growth markets of the U.S.

and to provide shareholders liquidity through an IPO of our shares or a

recapitalization with institutional investors as capital markets thaw and the

economic markets move from recession to recovery.

www.amreit.com

3

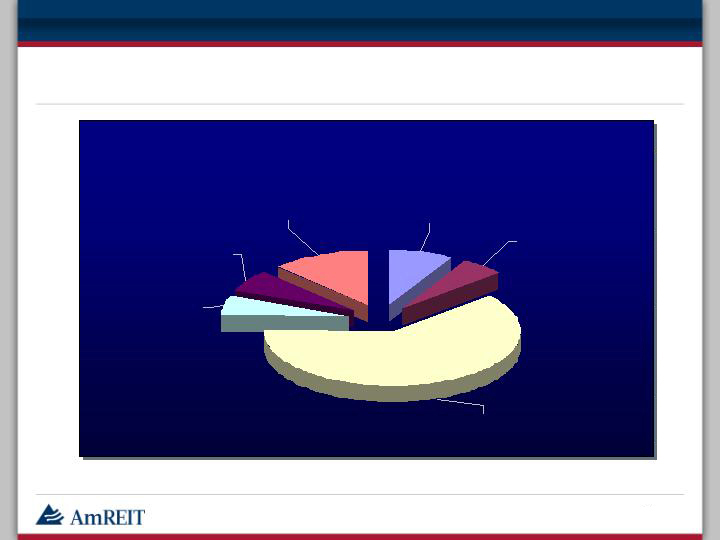

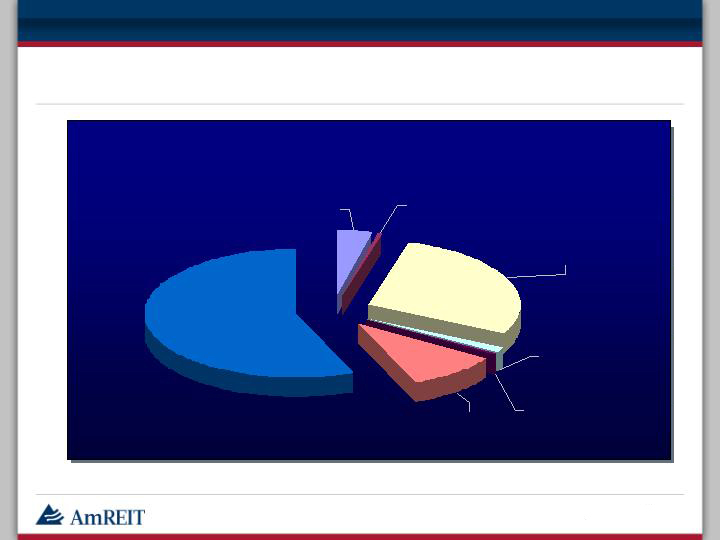

Expense Management – Pre-Vision 2010 Phase I

2008 Expenses ($15.9 mm)

Conferences and

Seminars

5%

Legal and

Professional

8%

Other G

&

A

12%

Marketing

7%

Travel and

Entertainment

5%

Salary

&

Benefits

63%

4

www.amreit.com

Expense Management – Post Vision 2010 Phase I

2009 Estimated Expenses ($6.9 mm)

Conferences and

Seminars

0%

Legal and

Professional

4%

Marketing

1%

Travel and

Entertainment

1%

Other G&A

10%

Salary

&

Benefits

28%

Cost Savings

56%

Includes:

Salaries - $5.3 mm

Marketing - $945,000

Conference - $784,000

Legal - $707,000

Other G & A - $1.1 mm

5

www.amreit.com

Vision 2010 - Phases

Phase I:

Business Model – changes to reach greater efficiency and reduce volatility of earnings. This phase includes the elimination of the general contracting business and IBD Securities business. Estimated G&A Savings of $4 -

$4.5 million per year. Phase I was executed during the 3rd and 4th quarters of 2008.

Phase II:

Capital Structure – changes to reach greater efficiency and reduce volatility of earnings. This will include the simplification of AmREIT’s equity capitalization into one Class of stock, the consolidation of AmREIT into REITPlus and the privatization of the Company. Phase II will be executed during 2009.

Phase III:

Growth & Liquidity– made possible by Phase I and II as we pursue our goal to grow our platform within seven of the top growth markets of the U.S. and to provide shareholders liquidity through an IPO of our shares or a recapitalization with institutional investors as capital markets thaw and the economic markets move from recession to recovery.

6

www.amreit.com

AmREIT

$450 Million

$8 Million

New

Company

Phase II – Capital Structure (Three Step Combination)

Step One:

Privatization through

voluntary De-listing of Class

A Shares from trading on

NYX

Step Two:

Re-domicile AmREIT from

Texas to Maryland,

positioning us for Step Three

Step Three:

Reverse merger of AmREIT

into REITPlus

Of the Shareholders who voted, 93% voted “yes”

7

www.amreit.com

AmREIT Valuation

$0.00

$3.00

$6.00

$9.00

$12.00

$15.00

$18.00

Net Asset Value

Discounted Cash Flow

Analysis

Retail REIT Public Comps-

LTM Cap Rate

Price Per Share

Class A Share Price - $9.50

Source: KeyBanc Capital Markets

$9.50

$7.25 to $9.75

$7.50 to $10.75

$10.75 to $11.75

8

www.amreit.com

AmREIT – Exchange Ratio

Initial

Anticipated

Anticipated

REITPlus

Exchange

Actual

Investment

Premium

(1)

Consideration

Share Value

Ratio

Consideration

(2)

Class C

10.00

$

1.00

$

11.00

$

9.50

$

1.16

11.00

$

Class D

10.00

$

0.55

$

10.55

$

9.50

$

1.11

10.55

$

Class D - Drip

9.50

$

-

$

9.50

$

9.50

$

1.00

9.50

$

(1)

The Anticipated Premium represents the conversion premium. For Class C, this is stated as 10%, for Class D, this is stated as a total of 7.7%, amortized 1.1% per year. For Class D, we have used a five-year holding period. The Class D Drip shares do not receive a conversion premium.

(2)

Calculated by multiplying the Exchange Ratio by the REITPlus Share Value.

9

www.amreit.com

AmREIT Dividend Exchange Analysis

5.2%

5.8%

6.1%

5.2%

5.2%

Pro-forma Dividend

Rate

($150.00)

($100.00)

($120.00)

$ -

$200.00

Annual Difference per

1,000 shares

$0.50

$0.55

$0.58

$0.50

$0.50

Per Annum

$0.0416

$0.0458

$0.0483

$0.0416

$0.0416

Per Month

Dividend Post Merger on

Exchange of Value

$0.65

$0.65

$0.70

$0.50

$0.30

Per Year

$0.0541

$0.0541

$0.0583

$0.0416

$0.025

Per Month

Dividend Pre Merger

Class D

Drip Stock

Class D

Stock

Class C

Stock

Class A

Stock

REITPlus

10

www.amreit.com

Vision 2010 - Phases

Phase I:

Business Model – changes to reach greater efficiency and reduce volatility of earnings. This phase includes the elimination of the general contracting business and IBD Securities business. Estimated G&A Savings of $4 - $4.5 million per year. Phase I was executed during the 3rd and 4th quarters of 2008.

Phase II:

Capital Structure – changes to reach greater efficiency and reduce volatility of earnings. This will include the simplification of AmREIT’s equity capitalization into one Class of stock, the consolidation of AmREIT into REITPlus and the privatization of the Company. Phase II will be executed during 2009.

Phase III:

Growth & Liquidity – made possible by Phase I and II as we pursue our goal to grow our platform within seven of the top growth markets of the U.S. and to provide shareholders liquidity through an IPO of our shares or a recapitalization with institutional investors as capital markets thaw and the economic markets move from recession to recovery.

11

www.amreit.com

Investing in Three of the Top Six U.S. Growth Markets

Three Top U.S. Growth Markets

Prior/Non-core Holdings

12

www.amreit.com

AmREIT’s Markets

Rank

Metropolitan Statistacal Area

Increase from

2007 to 2008

%

Increase

1

Dallas-Fort Worth-Arlington, TX

146,532

2.4%

2

Houston-Sugar Land-Baytown, TX

130,185

2.3%

3

Phoenix-Mesa-Scottsdale, AZ

115,978

2.8%

4

Atlanta-Sandy Springs-Marietta, GA

114,989

2.2%

5

Austin-Round Rock-San Antonio, TX

106,536

3.0%

6

Los Angeles-Long Beach-Santa Ana, CA

88,196

0.7%

7

New York-Northern New Jersey-Long Island, NY-NJ-PA

84,227

0.4%

8

Chicago-Naperville-Joliet, IL-IN-WI

72,771

0.8%

9

San Francisco-Oakland-Fremont, CA

58,406

1.4%

10

Washington-Arlington-Alexandria, DC-VA-MD-WV

55,835

1.1%

Top 10 U.S. Population Growth Markets: 2007-2008

Employment Growth in 10 Largest U.S. Metros: LTM Sep 2008

AmREIT’s core portfolio of

Irreplaceable Corners TM are corner

properties located in top United States

growth markets.

Currently, the Company’s properties

are located in 3 of the top 6 population

and employment growth markets in the

U.S. (Houston, Dallas, and San

Antonio.

Rank

Metropolitan Statistacal Area

LTM

Sep 2008

1

Houston-Sugar Land-Baytown, TX

55,700

2

Dallas-FortWorth-Arlington, TX

54,300

3

Washington-Arlington-Alexandria, DC-VA-MD-WV

40,700

4

Seattle-Tacoma-Bellevue, WA

33,900

5

New York-Northern New Jersey-Long Island, NY_NJ-PA

20,200

5a.

Austin-Round Rock-San Antonio, TX

32,000

6

Boston-Cambridge-Quincy, MA

19,300

7

San Antonio, TX

17,400

8

Virginia Beach-Norfolk-Newport News, VA-NC

17,000

9

Austin-Round Rock, TX

14,600

10

Charleston-North Charleston-Summerville, SC

13,500

13

www.amreit.com

AmREIT’s Markets

Rank

Metropolitan Statistacal Area

Rate

1

New Orleans-Metairie-Kenner, LA

5.3%

2

Oklahoma City, OK

5.6%

3

San Antonio, TX

5.9%

4

Washington-Arlington-Alexandria, DC-VA-MD-WV

5.9%

5

Austin-Round Rock-San Antonio, TX

6.2%

6

Houston-Sugar Land-Baytown, TX

6.5%

7

Virginia Beach-Norfolk-Newport News, VA-NC

6.9%

8

Dallas-Fort Worth-Arlington, TX

7.0%

9

Phoenix-Mesa-Scottsdale, AZ

7.2%

10

Baltimore-Towson, MD

7.4%

Rank

Metropolitan Statistacal Area

GLA

(SQ FT)

% of

Total

1

Houston-Sugar Land-Baytown, TX

656,538

59.1%

2

Dallas-Fort Worth-Arlington, TX

271,221

24.4%

3

San Antonio, TX

65,932

5.9%

Top Three Total

993,691

89.4%

Other

118,038

10.6%

Total Portfolio

1,111,729

100.0%

AmREIT Real Estate Portfolio

Top 10 Lowest U.S. Unemployment Rate: March 2009

14

www.amreit.com

AmREIT – Debt Maturities as of March 31, 2009

13%

$ 19,900

2017

13%

$ 20,000

2016

33%

$ 49,000

2015

27%

$ 39,614

2013

9.1%

$ 12,812

2012

2%

$ 3,075

2011

0%

$ -

2010

3.1%

$ 4,567

2009

Percent of

Total

Outstanding

Amount

Year

Secured Debt Maturities

As of 9/30/08, AmREIT’s Unsecured Revolving Credit Facility Balance is $27,880,000.

2013

27%

2015

33%

2016

13%

2017

13%

2011

2%

2009

3%

2010

0%

2012

9%

15

www.amreit.com

2,300

1,794

1,326

1,268

1,121

962

919

0

500

1,000

1,500

2,000

2,500

AMY

FRT

WRI

KIM

REG

EQY

DDR

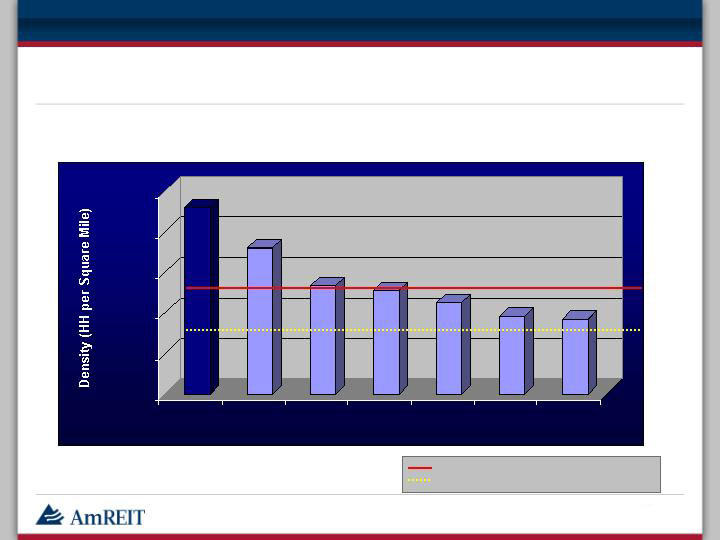

AmREIT Portfolio - Household Population Density Comparison

Shopping Center REIT Average: 1,232

National Average: 800

Source: Merrill Lynch Research, as of September 2007.

AmREIT’s portfolio population density is 87% greater than the shopping center sample

group and 188% greater than the national average.

16

www.amreit.com

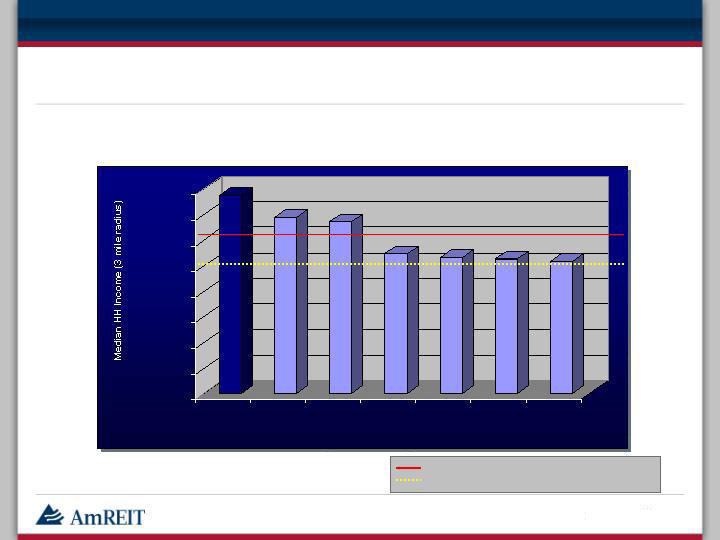

$77,556

$68,828

$67,381

$54,670

$53,489

$52,864

$51,683

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

AMY

FRT

REG

KIM

DDR

EQY

WRI

Peer Group REITs

AmREIT Portfolio - Household Income Comparison

Shopping Center REIT Average: $58,153

National Average: $48,775

Source: Merrill Lynch Research, as of September 2007.

AmREIT’s median household income is 34% greater than the shopping center

sample group and 60% higher than the national average.

17

www.amreit.com

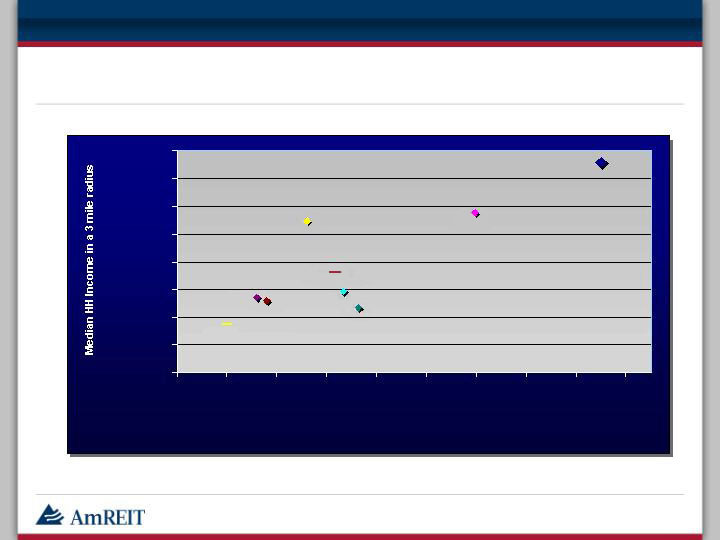

AmREIT Portfolio - REIT Demographic Positioning

Source: Merrill Lynch Research, as of September 2007.

AMY

FRT

REG

EQY

WRI

National Avg

KIM

DDR

Shopping Center Avg

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000

$75,000

$80,000

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

Households per Square Mile

18

www.amreit.com

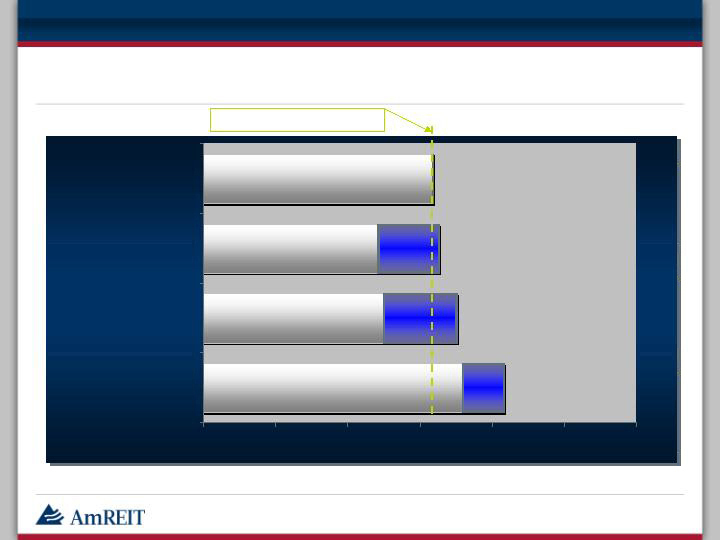

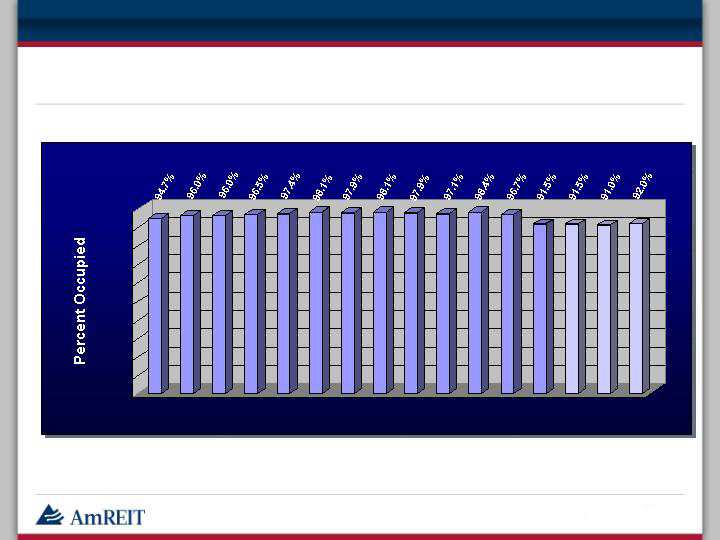

AmREIT Portfolio – Three Year Portfolio Occupancy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q

2006

2Q

2006

3Q

2006

4Q

2006

1Q

2007

2Q

2007

3Q

2007

4Q

2007

1Q

2008

2Q

2008

3Q

2008

4Q

2008

1Q

2009

2Q

2009

3Q

2009

4Q

2009

Portfolio Occupancy

19

www.amreit.com

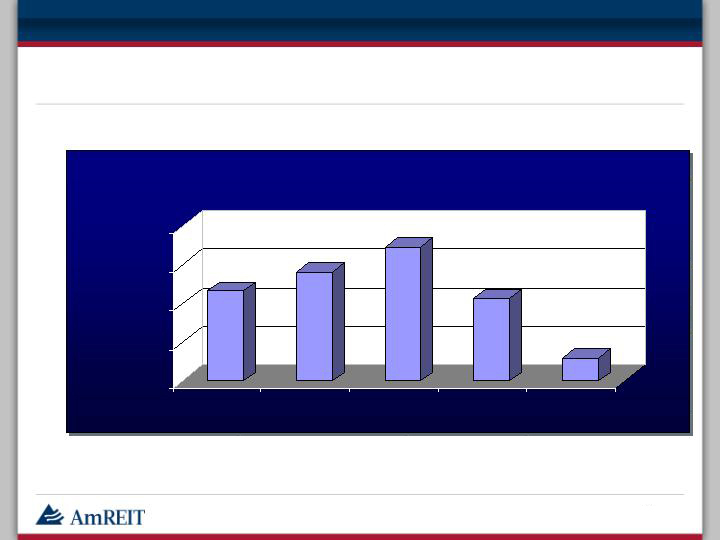

AmREIT Portfolio – Rental Rate Increase Upon Renewal

11.69%

14.16%

17.33%

10.70%

3.00%

0.00%

5.00%

10.00%

15.00%

20.00%

2006

2007

2008

1Q09A

2009E

Rental Rate Increase Upon Renewal

20

www.amreit.com

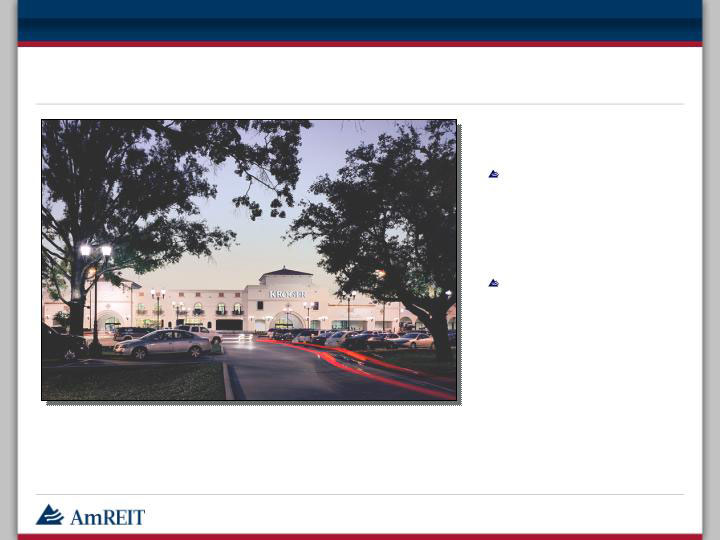

Plaza in the Park; Houston, Texas

Center is anchored by the

top grossing Kroger in

Texas and the #4 store in

the country (out of

approximately 2,500 stores

nationwide).

Entrance to the affluent

West University submarket.

3 Miles 5 Miles

Estimated Population: 148,619 410,882

Estimated Ave. HHI: $110,381 $83,529

Year Acquired: 2004

Retail SF: 344,623 SF

21

www.amreit.com

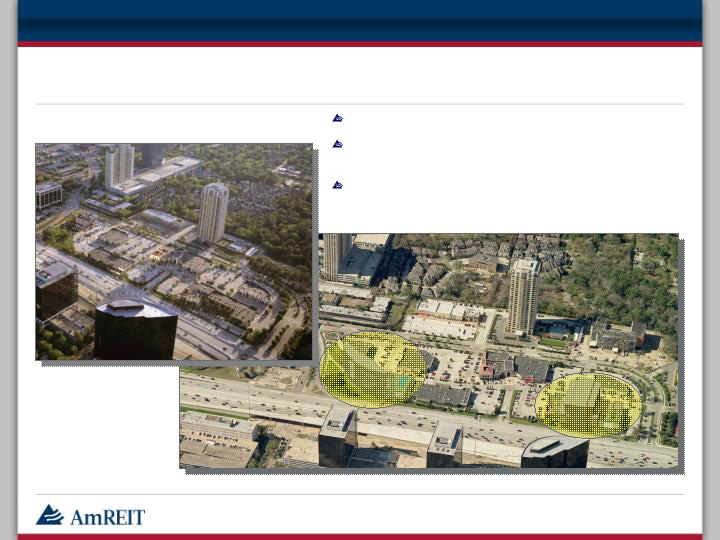

Courtyard on Post Oak; Houston, Texas

Uptown Plaza; Houston, Texas

Capitalized Income Value (at

6.5%) is approximately $7.7

million. Land value (at $150/s.f.)

is over $10 million.

Capitalized Income Value (at

6.5%) is approximately $17.7

million. Land value (at $175/s.f.)

is over $20 million.

22

www.amreit.com

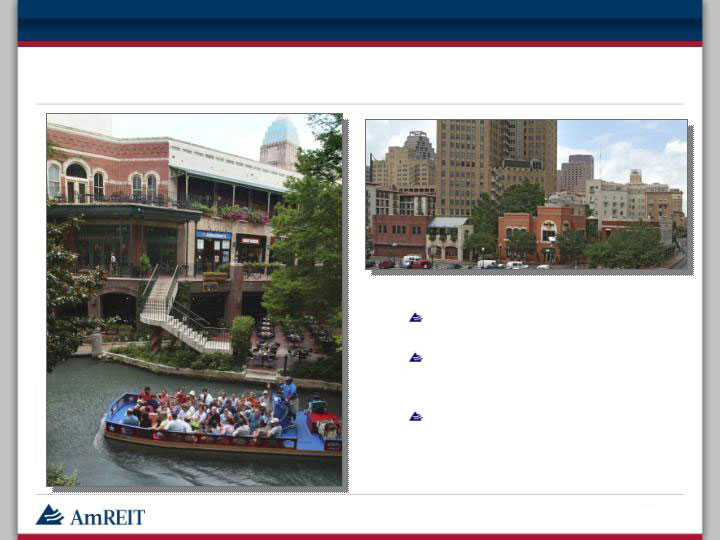

South Bank on the Riverwalk; San Antonio, TX

The Alamo and Riverwalk are the #1

and #2 tourist destinations in Texas.

Due to percentage rent, NOI was

$190,000 more than the original

projection upon acquisition.

Tenant sales have increased consistently for over 10 years.

23

www.amreit.com

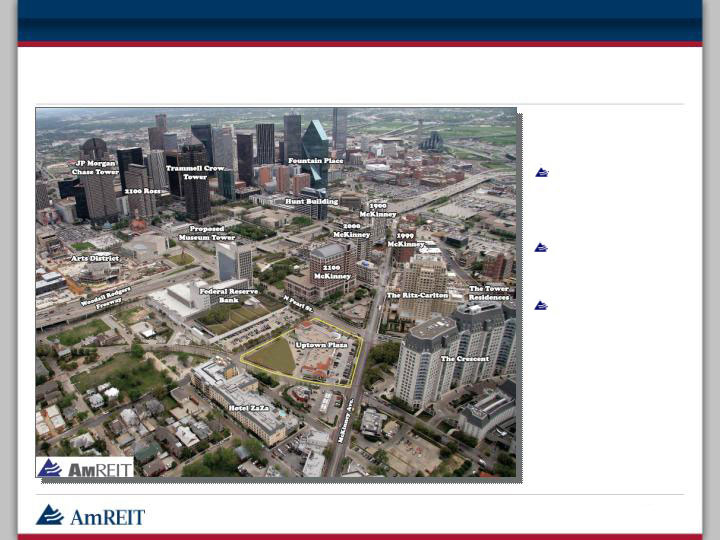

Uptown Plaza; Dallas, TX

Across from the

prestigious Crescent

Court and the Ritz

Carlton.

Assembled two

properties to control

city block.

0.9 acre development

tract under contract

with option to invest in

the development.

24

www.amreit.com

Uptown Park; Houston, TX – Future Development Potential

Uptown Park Houston TX - June 2005

Urban Context Conceptual Rendering

Demographics better than Buckhead and Beverly Hills.

Development potential for 200 room hotel and 200,000

s.f. office.

Market rents have increased from high $20’s to low

$40’s with NOI exceeding initial underwriting by

$800,000.

25

www.amreit.com

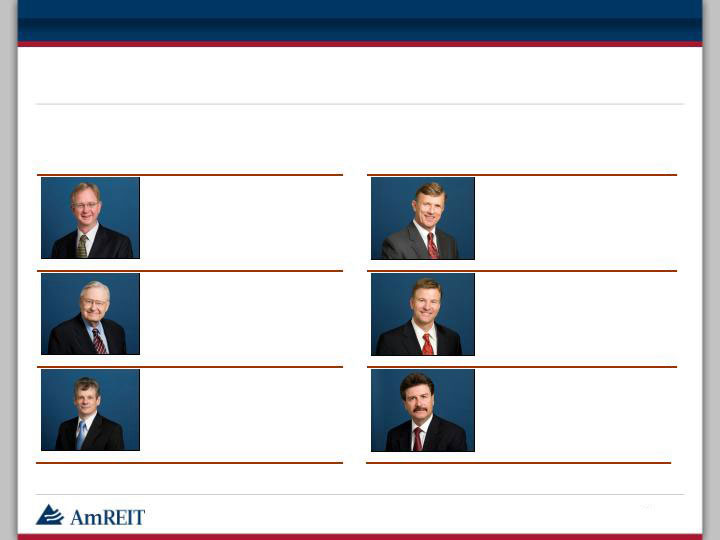

Independent Board of Directors

AmREIT Board of Directors

REITPlus Board of Directors

Mack D. Pridgen, III

Attorney with tax and audit experience and top executive of Highwoods (NYSE) while they grew from $250 million to $4.5 Billion.

Scot J. Luther

CEO and founder of retail real estate development company.

Brent M. Longnecker

Former national partner with Deloitte Touche, author of eight books on governance and compensation and CEO of national consulting organization.

H.L. “Hank” Rush, Jr.

CEO Star of Hope. Formerly top executive of BMC Software and Stewart Title.

Phillip Taggart

President and Chief Executive Officer of Taggart Financial Group, Inc. and co-author of “Taking Your Company Public”.

Robert S. Cartwright, Jr.

Graduate of Harvard (BA) and Stanford (PHD). Distinguished professor of Rice University.

26

www.amreit.com