Exhibit 99.2

Gardner Denver

2011 Analyst Day

November 7, 2011

Gardner

Denver

Safe Harbor Disclosure

All of the statements made by Gardner Denver in this presentation or made orally in connection with it, other than historical facts, are forward-looking statements. As a general matter, forward-looking statements are those focused upon anticipated events or trends, expectations, and beliefs relating to matters that are not historical in nature. The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for these forward-looking statements. In order to comply with the terms of the safe harbor, the Company notes that forward-looking statements are subject to known and unknown risks, uncertainties, and other factors relating to the Company’s operations and business environment, all of which are difficult to predict and many of which are beyond the control of the Company. These known and unknown risks, uncertainties, and other factors could cause actual results to differ materially from those matters expressed in, anticipated by or implied by such forward-looking statements.

Factors that could cause or contribute to such differences include, but are not limited to: changing economic conditions; pricing of the Company’s products and other competitive market pressures; the costs and availability of raw materials; fluctuations in foreign currency rates and energy prices; risks associated with the Company’s current and future litigation; and the other risks detailed from time to time in the Company’s SEC filings, including but not limited to, its annual report on Form 10-K for the fiscal year ending December 31, 2010, and its quarterly reports on Form 10-Q.

These statements reflect the current views and assumptions of management with respect to future events. The Company does not undertake, and hereby disclaims, any duty to update these forward-looking statements, although its situation and circumstances may change in the future. The inclusion of any statement in this presentation does not constitute admission by the Company or any other person that the events or circumstances described in such statement are material.

Gardner

Denver

2

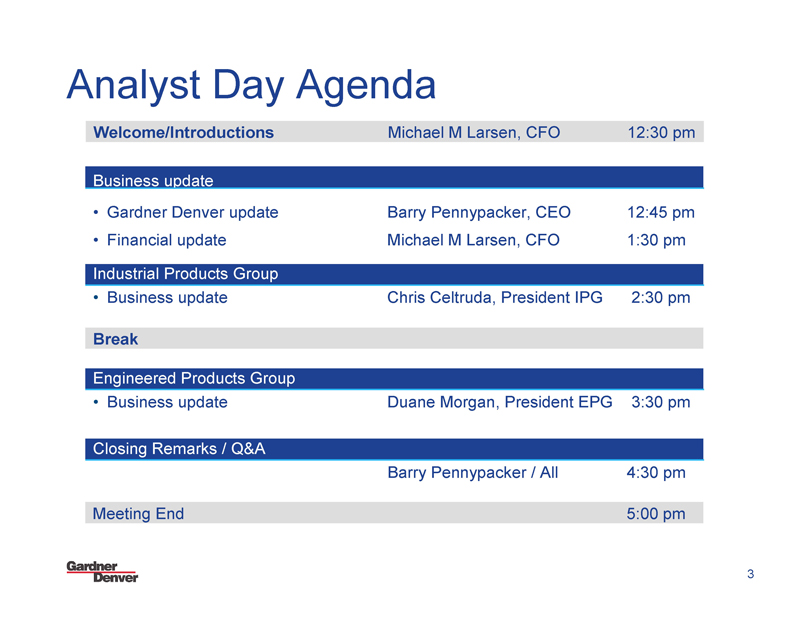

Analyst Day Agenda

Welcome/Introductions

Business update

• Gardner Denver update

• Financial update

Industrial Products Group

• Business update

Break

Engineered Products Group

• Business update

Closing Remarks / Q&A

Meeting End

Michael M Larsen, CFO

Barry Pennypacker, CEO

Michael M Larsen, CFO

Chris Celtruda, President IPG

Duane Morgan, President EPG

Barry Pennypacker / All

12:30 pm

12:45 pm

1:30 pm

2:30 pm

3:30 pm

4:30 pm

5:00 pm

Gardner

Denver

3

Gardner Denver Video

Strategic update

Gardner Denver Overview

~$2.4B(1) global Company with diverse and attractive end markets

Leading brands and technologies ... strong distribution

New, operationally focused team driving “The Gardner Denver Way”

Growing, profitable aftermarket opportunity

Strong track record on analyzing and integrating acquisitions

Focused on superior cash and earnings growth

Early stages of transformation to a high quality, high margin Industrial Company with Energy exposure

(1) Company estimates (see note on p. 66)

Gardner

Denver

6

A global leader in compressed air and gas, vacuum and fluid transfer technologies

We serve a wide range of industries with efficient & reliable products

Energy Medical Mining Transportation Food & Beverage

Gardner Denver

7

Two business segments aligned to effectively serve our customers

2011 Sales by segments(1)

Engineered Products Group

GD

GARDNER DENVER

THOMAS

A Gardner Denver Product

NASH

A Gardner Denver Product

WELCH

A Gardner Denver Product

EMCO WHEATON

A Gardner Denver Product

~$1.1B

~$1.2B

Industrial Products Group

HOFFMAN

A Gardner Denver Product

BOTTARINI

GD

GARDNER DENVER

CHAMPION

GD Belliss & Morcom

CompAir

MAKO

ROBUSCHI®

A great portfolio of brands and businesses

(1) Company estimates (see note on p. 66)

Gardner

Denver

8

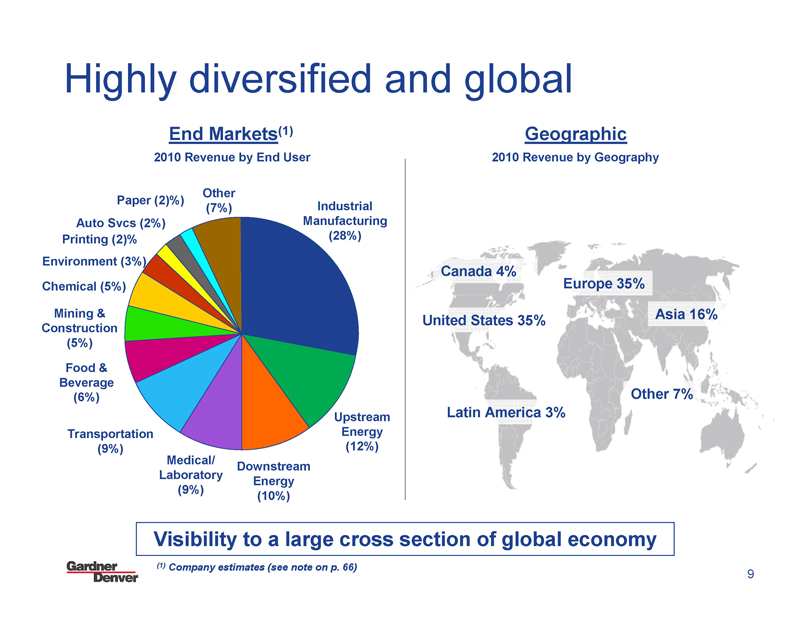

Highly diversified and global

End Markets(1)

2010 Revenue by End User

Other (7%)

Paper (2)%)

Auto Svcs (2%)

Printing (2)%

Environment (3%)

Chemical (5%)

Mining & Construction (5%)

Food & Beverage (6%)

Transportation (9%)

Medical/ Laboratory (9%)

Industrial Manufacturing (28%)

Upstream Energy (12%)

Downstream Energy (10%)

Geographic

2010 Revenue by Geography

Canada 4%

United States 35%

Latin America 3%

Europe 35%

Asia 16%

Other 7%

Visibility to a large cross section of global economy

(1) Company estimates (see note on p. 66)

Gardner

Denver

9

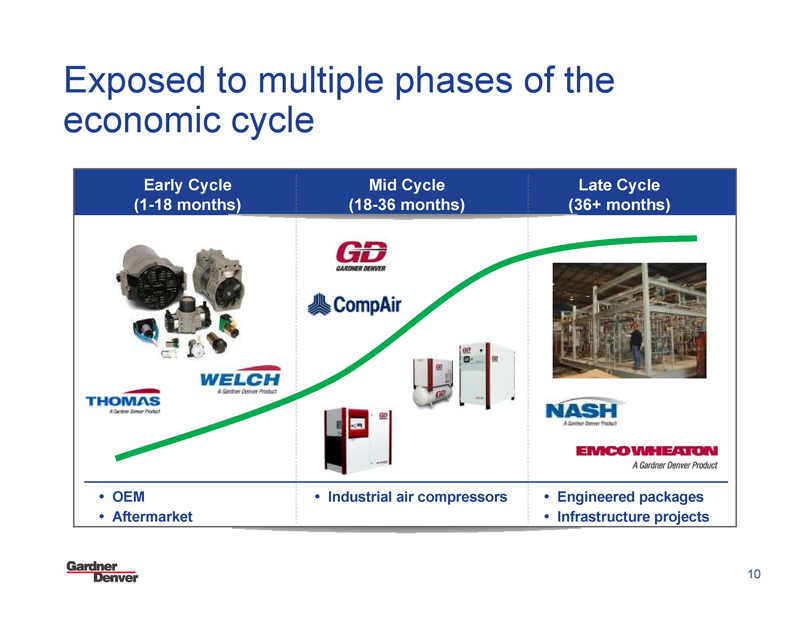

Exposed to multiple phases of the economic cycle

Early Cycle

(1-18 months)

THOMAS

A Gardner Denver Product

WELCH

A Gardner Denver Product

Mid Cycle (18-36 months)

GD

GARDNER DENVER

CompAir

Late Cycle (36+ months)

NASH

A Gardner Denver Product

EMCO WHEATON

A Gardner Denver Product

• OEM

• Aftermarket

• Industrial air compressors

• Engineered packages

• Infrastructure projects

Gardner

Denver

10

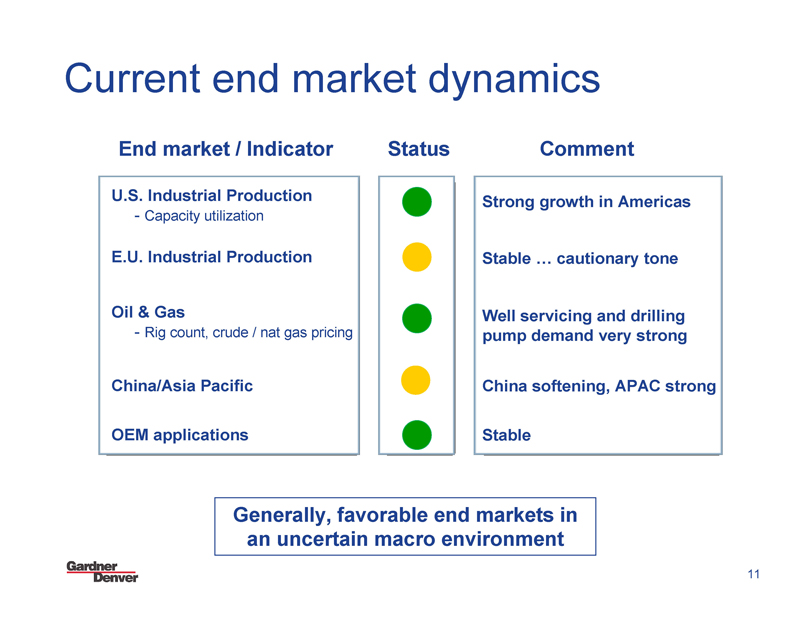

Current end market dynamics

End market / Indicator Status Comment

U.S. Industrial Production

- Capacity utilization

E.U. Industrial Production

Oil & Gas

- Rig count, crude / nat gas pricing

China/Asia Pacific

OEM applications

Strong growth in Americas

Stable ... cautionary tone

Well servicing and drilling pump demand very strong

China softening, APAC strong

Stable

Generally, favorable end markets in an uncertain macro environment

Gardner

Denver

11

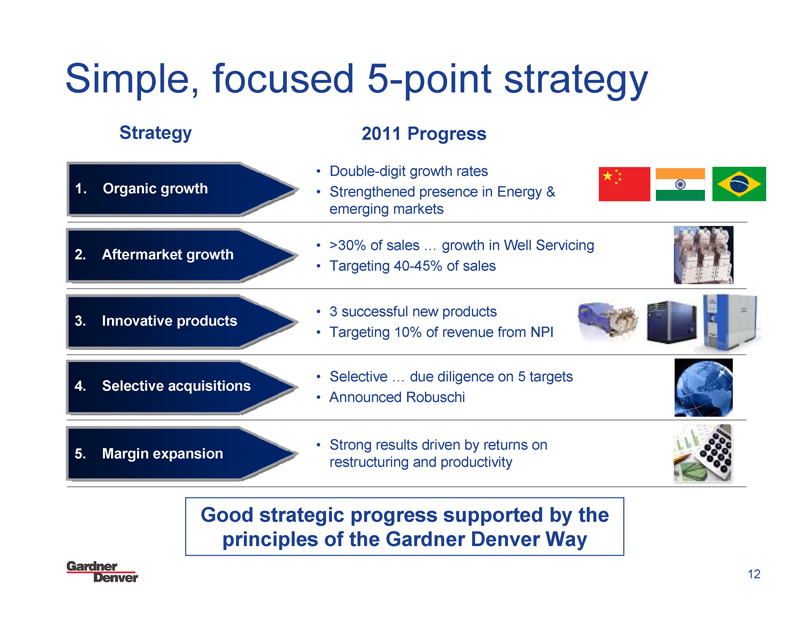

Simple, focused 5-point strategy

Strategy

1. Organic growth

2. Aftermarket growth

3. Innovative products

4. Selective acquisitions

5. Margin expansion

2011 Progress

• Double-digit growth rates

• Strengthened presence in Energy & emerging markets

• >30% of sales ... growth in Well Servicing

• Targeting 40-45% of sales

• 3 successful new products

• Targeting 10% of revenue from NPI

• Selective … due diligence on 5 targets

• Announced Robuschi

• Strong results driven by returns on restructuring and productivity

Good strategic progress supported by the principles of the Gardner Denver Way

Gardner

Denver

12

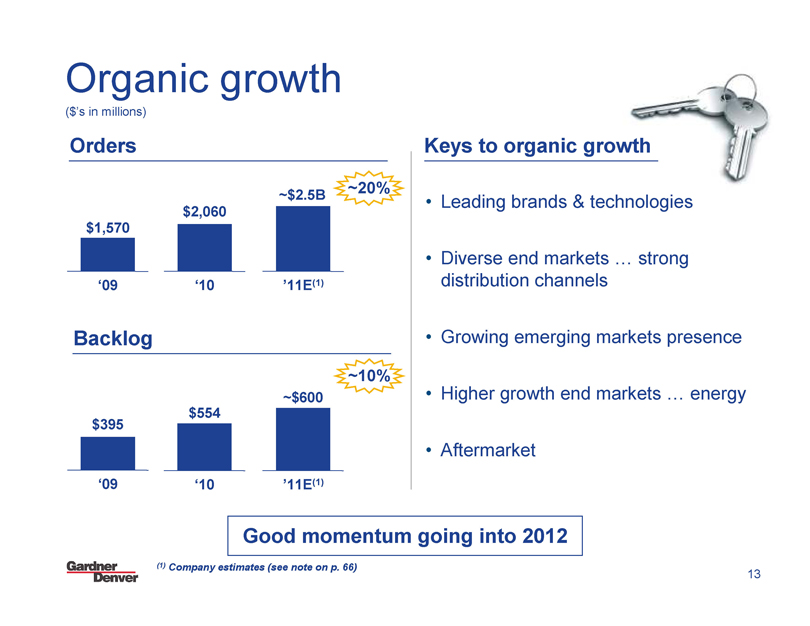

Organic growth

($’s in millions)

Orders

$1,570

‘09

$2,060

‘10

~$2.5B

’11E(1)

~20%

Backlog

$395

‘09

$554

‘10

~$600

’11E(1)

~10%

Keys to organic growth

• Leading brands & technologies

• Diverse end markets ... strong distribution channels

• Growing emerging markets presence

• Higher growth end markets … energy

• Aftermarket

Good momentum going into 2012

(1) Company estimates (see note on p. 66)

Gardner

Denver

13

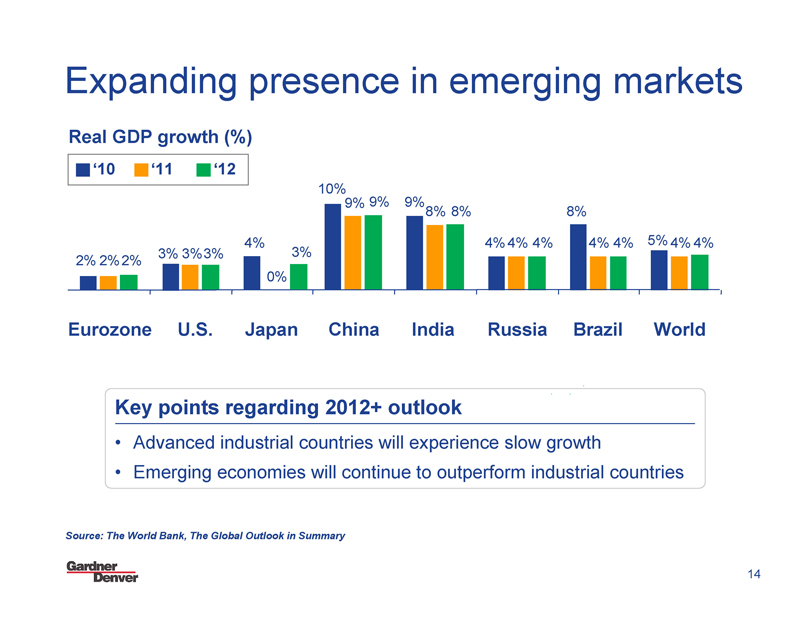

Expanding presence in emerging markets

Real GDP growth (%)

‘10 ‘11 ‘12

2%

2%

2%

3%

3%

3%

4%

0%

3%

10%

9%

9%

9%

8%

8%

4%

4%

4%

8%

4%

4%

5%

4%

4%

Eurozone U.S. Japan China India Russia Brazil World

Key points regarding 2012+ outlook

• Advanced industrial countries will experience slow growth

• Emerging economies will continue to outperform industrial countries

Source: The World Bank, The Global Outlook in Summary

Gardner

Denver

14

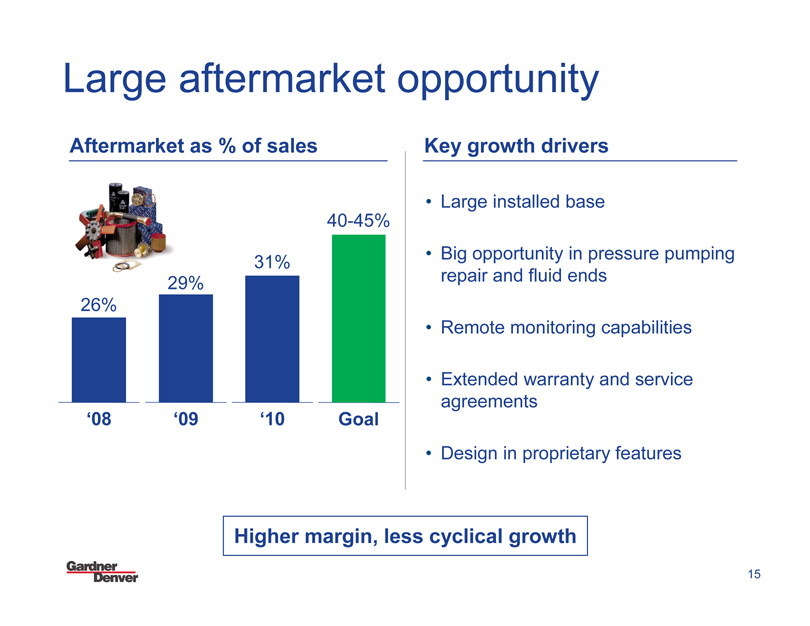

Large aftermarket opportunity

Aftermarket as % of sales

26%

‘08

29%

‘09

31%

‘10

40-45%

Goal

Key growth drivers

• Large installed base

• Big opportunity in pressure pumping repair and fluid ends

• Remote monitoring capabilities

• Extended warranty and service agreements

• Design in proprietary features

Higher margin, less cyclical growth

Gardner

Denver

15

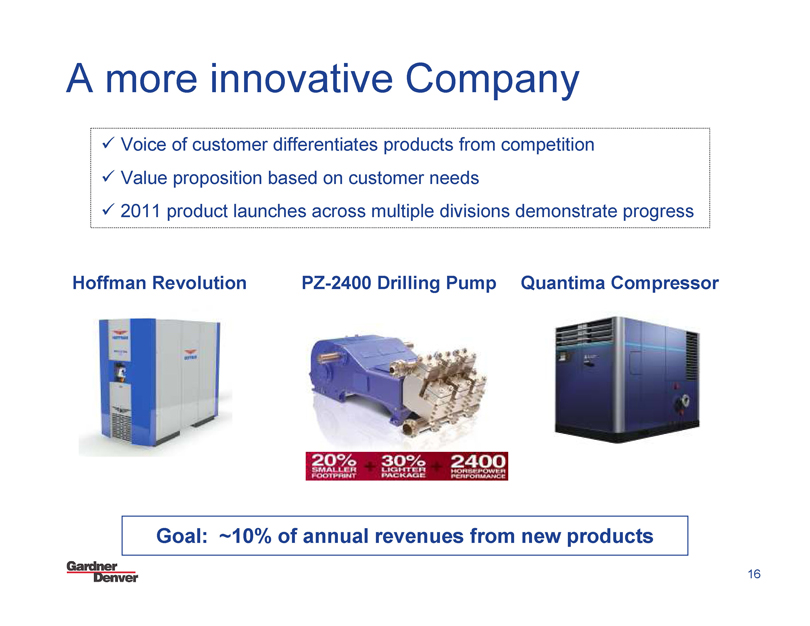

A more innovative Company

Voice of customer differentiates products from competition

Value proposition based on customer needs

2011 product launches across multiple divisions demonstrate progress

Hoffman Revolution

PZ-2400 Drilling Pump

Quantima Compressor

20%

SMALLER

FOOTPRINT

30%

LIGHTER

PACKAGE

2400

HORSEPOWER

PERFORMANCE

Goal: ~10% of annual revenues from new products

Gardner

Denver

16

24 acquisitions over 15 years

Engineered Products Group

TCM

Twentieth Century Mfg.

GEOQUIP

Water Jetting

• Butterworth

• CRS Power Flow

• Jetting Systems

NASH

SYLTONE

INNOVATIVE SYSTEMS FOR TRANSPORT

TODO

ILMVAC

vakuum mit zukunft

Chaparral

THOMAS

1996

Wittig

BOTTARINI

2011

TAMROTOR

AIR RELIEF

HOFFMAN

CompAir

LAMSON

CHAMPION

Invincible

Elmo Rietschle

ROBUSCH

Industrial Products Group

Bellis & Morcom

BEST AIRE

Strong track record on selective acquisitions

Gardner

Denver

17

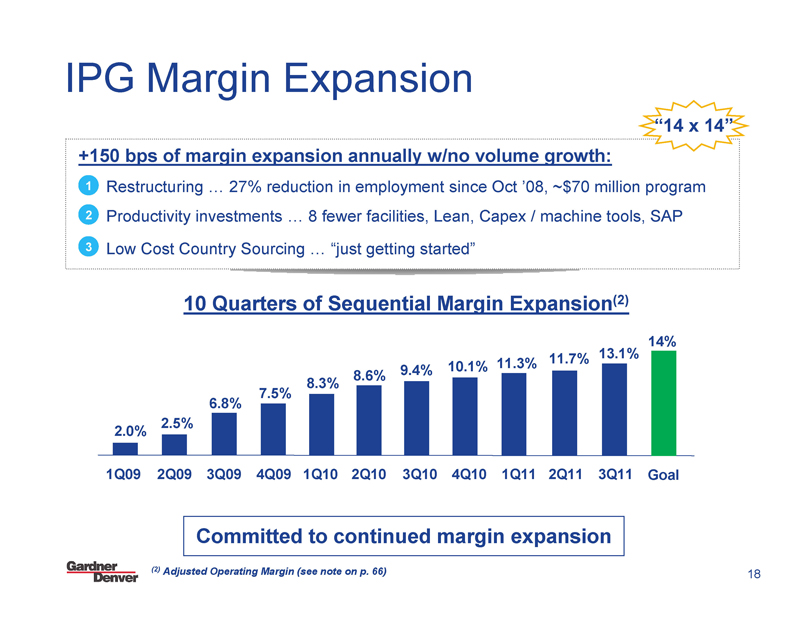

IPG Margin Expansion

“14 x 14”

+150 bps of margin expansion annually w/no volume growth:

1 Restructuring ... 27% reduction in employment since Oct ’08, ~$70 million program

2 Productivity investments ... 8 fewer facilities, Lean, Capex / machine tools, SAP

3 Low Cost Country Sourcing ... “just getting started”

10 Quarters of Sequential Margin Expansion(2)

2.0%

1Q09

2.5%

2Q09

6.8%

3Q09

7.5%

4Q09

8.3%

1Q10

8.6%

2Q10

9.4%

3Q10

10.1%

4Q10

11.3%

1Q11

11.7%

2Q11

13.1%

3Q11

14%

Goal

Committed to continued margin expansion

(2) Adjusted Operating Margin (see note on p. 66)

Gardner

Denver

18

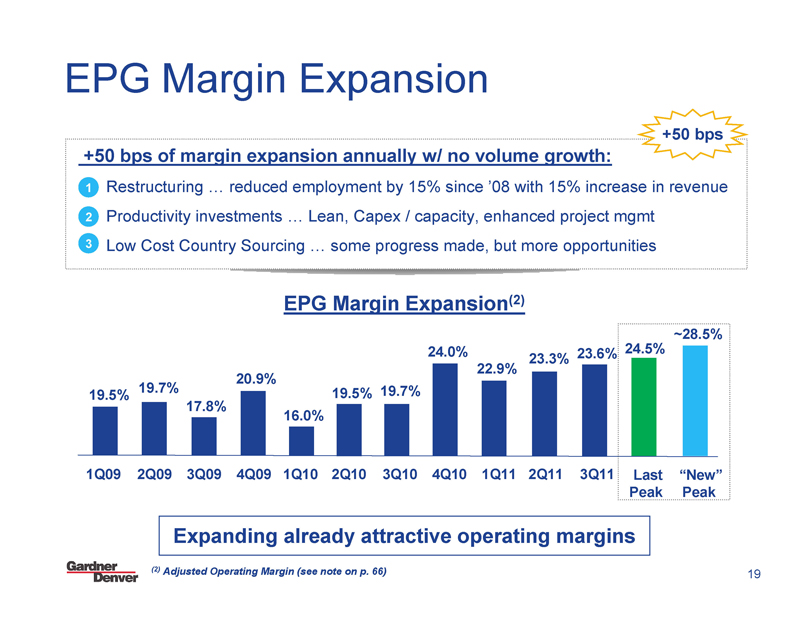

EPG Margin Expansion

+50 bps

+50 bps of margin expansion annually w/ no volume growth:

1 Restructuring ... reduced employment by 15% since ’08 with 15% increase in revenue

2 Productivity investments ... Lean, Capex / capacity, enhanced project mgmt

3 Low Cost Country Sourcing ... some progress made, but more opportunities

EPG Margin Expansion(2)

19.5%

1Q09

19.7%

2Q09

17.8%

3Q09

20.9%

4Q09

16.0%

1Q10

19.5%

2Q10

19.7%

3Q10

24.0%

4Q10

22.9%

1Q11

23.3%

2Q11

23.6%

3Q11

24.5%

Last Peak

~28.5%

“New” Peak

Expanding already attractive operating margins

(2) Adjusted Operating Margin (see note on p. 66)

Gardner

Denver

19

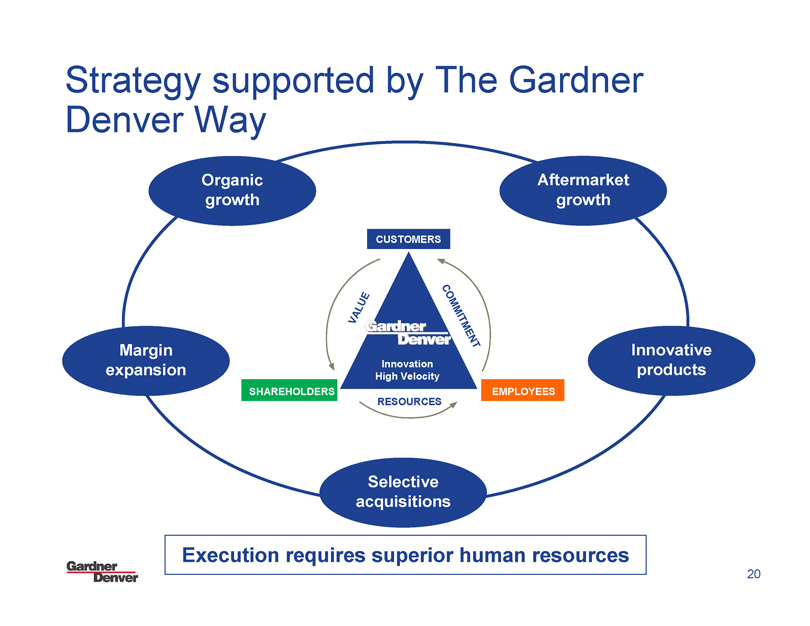

Strategy supported by The Gardner Denver Way

Organic growth

Margin expansion

Selective acquisitions

Innovative products

Aftermarket growth

CUSTOMERS

SHAREHOLDERS

EMPLOYEES

VALUE

COMMITMENT

RESOURCES

Gardner

Denver

Innovation

High Velocity

Execution requires superior human resources

Gardner

Denver

20

Building a high performance culture

Operationally focused team

Policy deployment

Operating rhythms

Clear accountability

Continuous improvement

New, operationally focused management

SF

team driving transformation

21

Financial Update

Track record of financial results

Favorable dynamics in diverse end markets support future growth

Margin expansion goals within reach ... “The Gardner Denver Way”

Ability to manage through uncertain times ... contingency planning

Strong cash generation and balance sheet ... disciplined deployment

Track record on accretive M&A ... active pipeline

Focused on delivering superior cash and earnings growth

Gardner

Denver

23

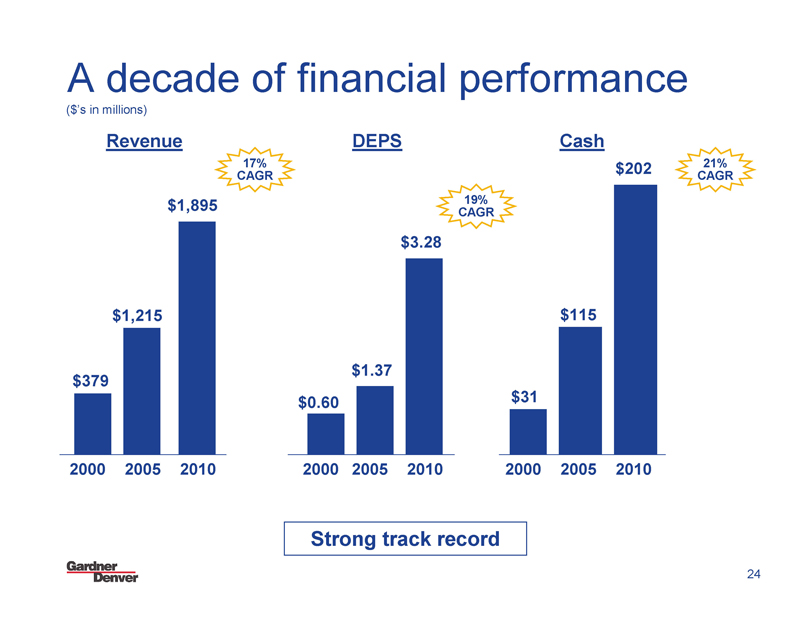

A decade of financial performance

($’s in millions)

Revenue DEPS Cash

$379

2000

$1,215

2005

$1,895

2010

17% CAGR

$0.60

2000

$1.37

2005

$3.28

2010

19% CAGR

$31

2000

$115

2005

$202

2010

21% CAGR

Strong track record

Gardner

Denver

24

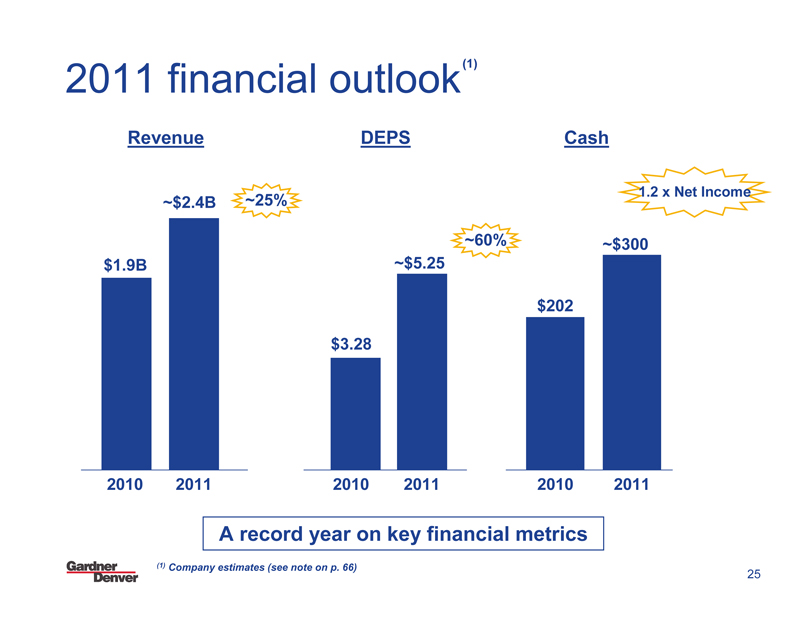

2011 financial outlook (1)

Revenue DEPS Cash

~400 bps

~25%

~$2.4B

$1.9B

2010

2011

$3.28

~$5.25

~60%

$202

~$300

2010

2011

2010

2011

1.2 x Net Income

A record year on key financial metrics

(1) Company estimates (see note on p. 66)

Gardner

Denver

25

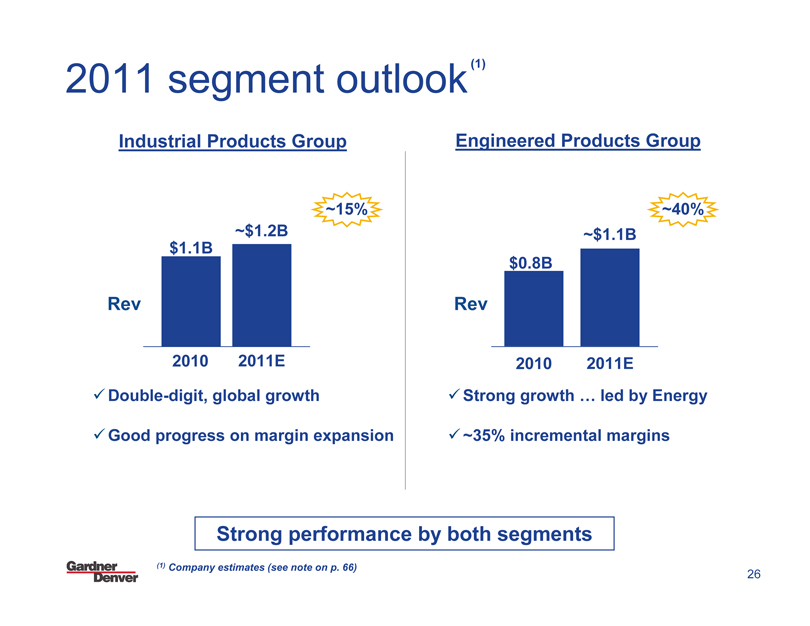

2011 segment outlook (1)

Industrial Products Group Engineered Products Group

Rev

$1.1B

~$1.2B

~15%

2010

2011E

Double-digit, global growth

Good progress on margin expansion

Rev

$0.8B

~$1.1B

~40%

2010

2011E

Strong growth ... led by Energy

~35% incremental margins

Strong performance by both segments

(1) Company estimates (see note on p. 66)

Gardner

Denver

26

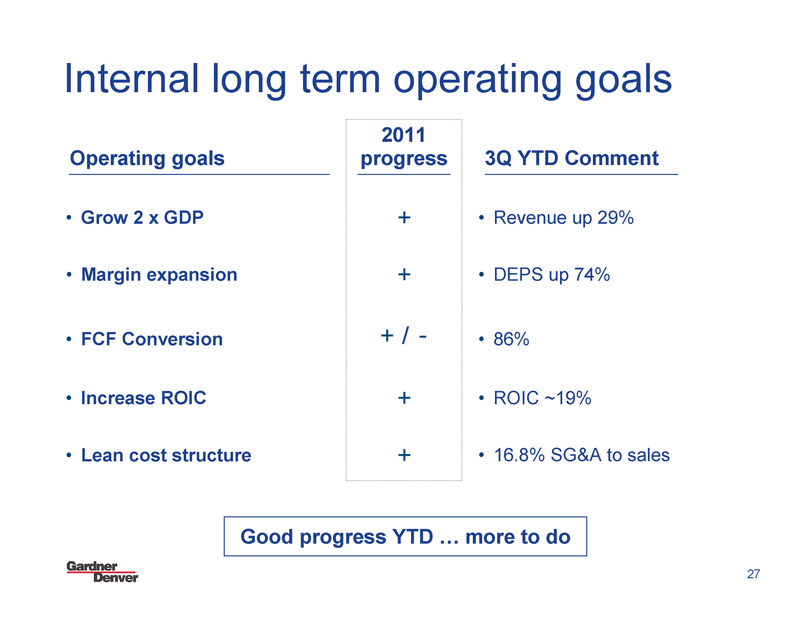

Internal long term operating goals

Operating goals

2011 progress

3Q YTD Comment

• Grow 2 x GDP + • Revenue up 29%

• Margin expansion + • DEPS up 74%

• FCF Conversion + / - • 86%

• Increase ROIC + • ROIC ~19%

• Lean cost structure + • 16.8% SG&A to sales

Good progress YTD ... more to do

Gardner

Denver

27

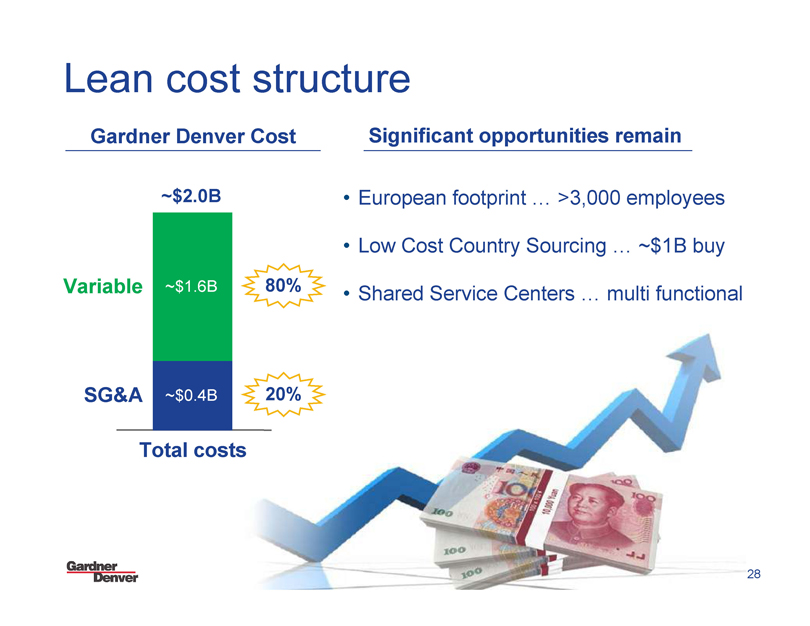

Lean cost structure

Gardner Denver Cost

~$2.0B

Variable ~$1.6B 80%

SG&A ~$0.4B 20%

Total costs

Significant opportunities remain

• European footprint ... >3,000 employees

• Low Cost Country Sourcing ... ~$1B buy

• Shared Service Centers ... multi functional

Gardner

Denver

28

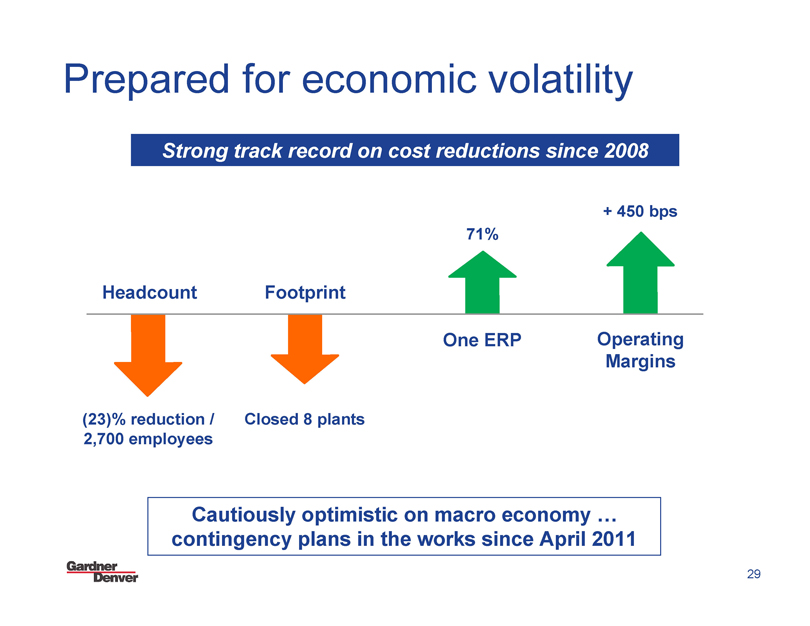

Prepared for economic volatility

Strong track record on cost reductions since 2008

Headcount

(23)% reduction / 2,700 employees

Footprint

Closed 8 plants

71%

One ERP

+ 450 bps

Operating Margins

Cautiously optimistic on macro economy ... contingency plans in the works since April 2011

Gardner

Denver

29

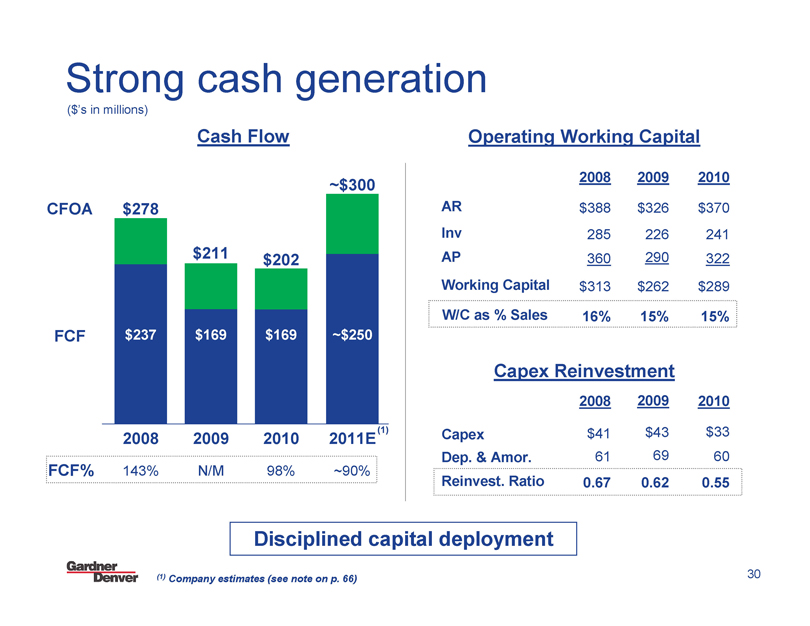

Strong cash generation

($’s in millions)

Cash Flow

CFOA

FCF

$278 $237 2008

$211 $169 2009

$202 $169 2010

~$300

~$250

(1)

2011E

FCF% 143% N/M 98% ~90%

Operating Working Capital

2008 2009 2010

AR $388 $326 $370

Inv 285 226 241

AP 360 290 322

Working Capital $313 $262 $289

W/C as % Sales 16% 15% 15%

Capex Reinvestment

2008 2009 2010

Capex $41 $43 $33

Dep. & Amor. 61 69 60

Reinvest. Ratio 0.67 0.62 0.55

Disciplined capital deployment

(1) Company estimates (see note on p. 66)

Gardner

Denver

30

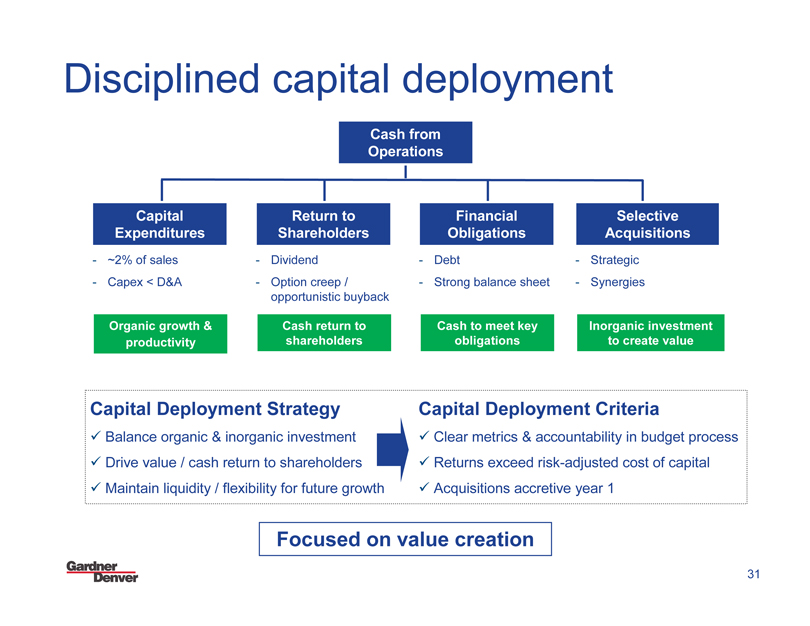

Disciplined capital deployment

Cash from Operations

Capital Expenditures

- ~2% of sales

- Capex < D&A

Organic growth & productivity

Return to Shareholders

- Dividend

Option creep/ opportunistic buyback

Cash return to shareholders

Financial Obligations

- Debt

- Strong balance sheet

Cash to meet key obligations

Selective Acquisitions

- Strategic

- Synergies

Inorganic investment to create value

Capital Deployment Strategy

Balance organic & inorganic investment

Drive value / cash return to shareholders

Maintain liquidity / flexibility for future growth

Capital Deployment Criteria

Clear metrics & accountability in budget process

Returns exceed risk-adjusted cost of capital

Acquisitions accretive year 1

Focused on value creation

Gardner

Denver

31

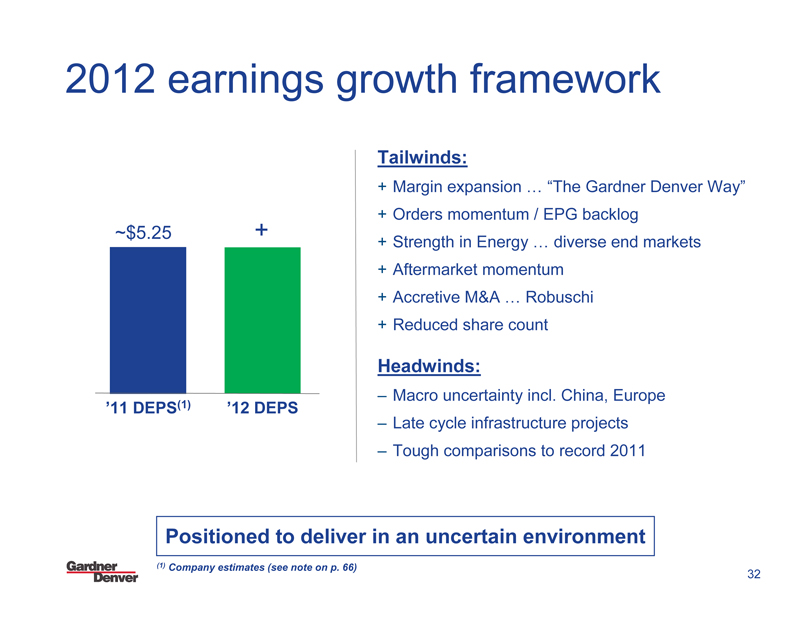

2012 earnings growth framework

~$5.25

’11 DEPS(1)

+

’12 DEPS

Tailwinds:

+ Margin expansion ... “The Gardner Denver Way”

+ Orders momentum / EPG backlog

+ Strength in Energy ... diverse end markets

+ Aftermarket momentum

+ Accretive M&A ... Robuschi

+ Reduced share count

Headwinds:

– Macro uncertainty incl. China, Europe

– Late cycle infrastructure projects

– Tough comparisons to record 2011

Positioned to deliver in an uncertain environment

(1) Company estimates (see note on p. 66)

Gardner

Denver

32

Industrial Products Group

Industrial Products Group

Compressors

CompAir

hydrovane

CHAMPION

Quantima

BOTTARINI A Gardner Denver Product

Key Applications & Customers

Industrial Manufacturing

Power and Energy

Transportation

Petrofac

P

GRAINGER

GE

HYUNDAI HEAVY INDUSTRIES CO.,LTD.

H

Blowers

GARDNER DENVER

Elmo Rietschle A Gardner Denver Product

GD Belliss & Morcom

HOFFMAN A Gardner Denver Product

H

ROBUSCHI

LAMSON A Gardner Denver Product

Wastewater and Process

Food and Beverage

Mining / Construction

Nestle

AIR LIQUIDE

Coca-Cola

CeresPower

PROTECTS WHAT’S GOODTM Tetra Pak

A ~$1.2B global leader in air movement

Gardner Denver

34

Industrial Products Group

Strategy 2012+ Focus

1. Organic growth

• Strengthen presence in emerging markets

• Custom Engineered Packages

• Leverage strong distribution

2. Aftermarket growth

• Reduce lead times and # of distribution centers

• Centrifugal impeller manufacturing, 3rd party repair

3. Innovative products

• High speed centrifugals; Quantima, Revolution

• Low cost, localized packages: Airgen, “The Dragon”

• Oil free / oil less compressors & blowers

4. Selective acquisitions

• Robuschi integration

• Expand product portfolio and market access

5. Margin improvement

• # 1 priority ... restructuring, productivity, sourcing

• Footprint rationalization ... Europe

• Value engineering of legacy products

Simple, focused 5-point strategy

Gardner Denver

35

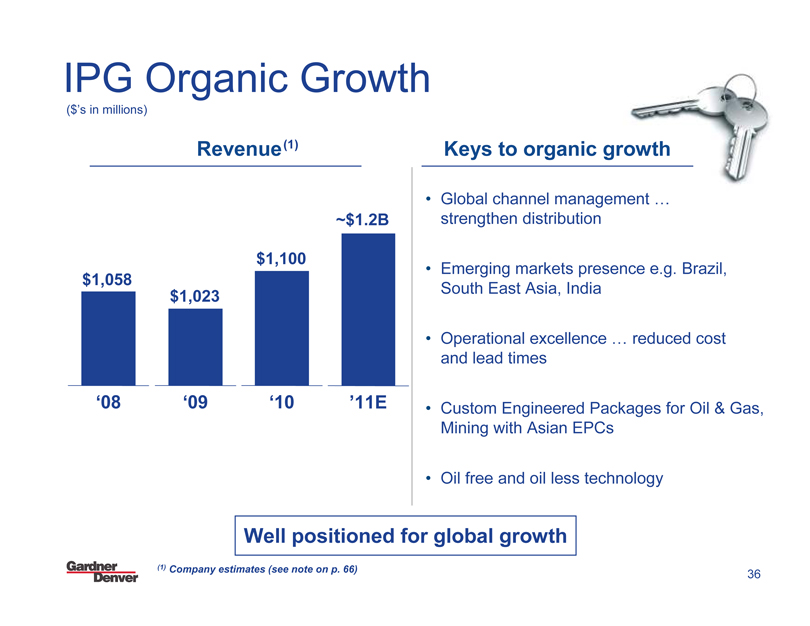

IPG Organic Growth

($’s in millions)

Revenue (1)

$1,058 $1,023 $1,100 ~$1.2B

Rev

‘08 ‘09 ‘10 ’11E

Keys to organic growth

• Global channel management ... strengthen distribution

• Emerging markets presence e.g. Brazil, South East Asia, India

• Operational excellence ... reduced cost and lead times

• Custom Engineered Packages for Oil & Gas, Mining with Asian EPCs

• Oil free and oil less technology

Well positioned for global growth

(1) Company estimates (see note on p. 66)

Gardner Denver

36

Investing in aftermarket growth

Third party repair solutions

AIR RELIEF

A Gardner Denver Product

Investing in 5 Axis impeller manufacturing

3rd party centrifugal compressor repairs

Developing crankshaft remanufacturing process

3rd Party Locomotive Compressors

Managed care partnerships

CHAMPION

National contracts for installation & maintenance

Availability based service center solutions

4,000+

Locations

GOOD YEAR MORE DRIVEN.

sears

Walmart Save money. Live better.

PEPBOYS

Sam’s CLUB

Savings Made Simple

Building repair capabilities & customer relationships

Gardner Denver

37

Custom Engineered Packages

~$500MM Market

Global growth

Adapting and integrating core compressor and blower technology

Attractive global infrastructure build in Oil, Gas, Mining and Manufacturing

Investing in regional relationships with Engineering Project Companies

~2 x increase in Asia Pacific orders

Repositioning and reorganizing team to focus on global opportunity

Winning in a high value, high growth market

38

Gardner Denver

Innovation in high speed centrifugals

Quantima

~$500MM Market

Innovative and proprietary design

- 2 stage, high speed motor

- Active magnetic bearings

- Variable speed / energy efficient

- No gearbox ... oil free

Great customer feedback

REVOLUTION

~$300MM Market

H HOFFMAN

High Speed American made solution

- High efficiency impeller

- Permanent magnet motor

- Direct drive

- Self enclosed cooling

Energy savings of ~50%

Technology drives total customer value

Gardner Denver

39

Video

Innovation for emerging markets

“The Dragon”

~$500MM Market

Localized range of industrial screw compressors

Rapid prototyping ... launched 2Q’11

~30% cost savings with comparable performance

Airgen Blower

Value engineered side channel blower Entered volume production 2Q’11 ~20% cost savings with comparable performance

Adapting solutions to meet needs of local markets

~$120MM Market

airgen A Gardner Denver Product

Gardner Denver

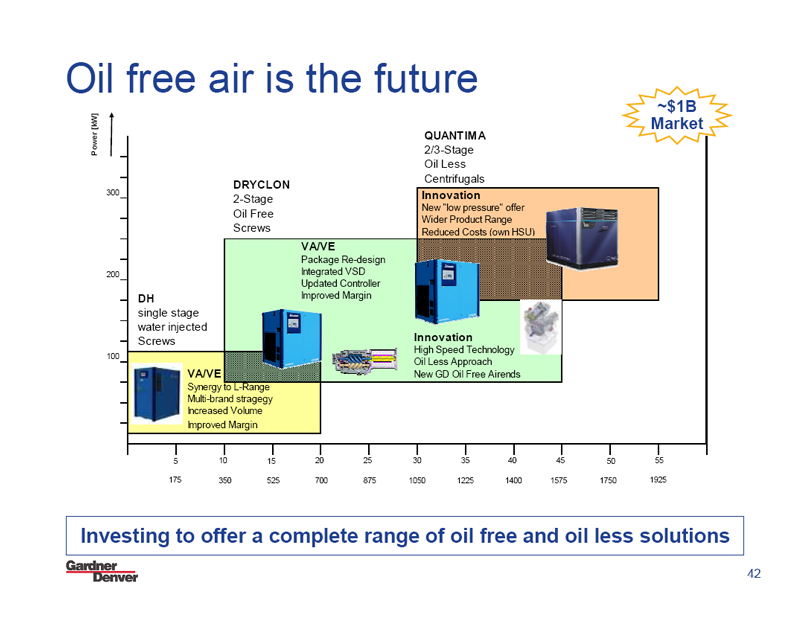

Oil free air is the future

~$1B

Market

Power [kW]

300 200 100

DH single stage water injected Screws

DRYCLON

2-Stage Oil Free Screws

QUANTIMA

2/3-Stage Oil Less Centrifugals

VA/VE

Synergy to L-Range Multi-brand stragegy Increased Volume Improved Margin

VA/VE

Package Re-design Integrated VSD Updated Controller Improved Margin

Innovation

New “low pressure” offer Wider Product Range Reduced Costs (own HSU)

Innovation

High Speed Technology Oil Less Approach New GD Oil Free Airends

5 10 15 20 25 30 35 40 45 50 55

175 350 525 700 875 1050 1225 1400 1575 1750 1925

Investing to offer a complete range of oil free and oil less solutions 42

Gardner Denver

Selective acquisitions ... Robuschi

Strong brand and reputation

Robox evolution RBS

ROBUSCHI ROBOX

Complimentary product range ... channel leverage / sales synergies, dry technology

Large installed base

Diverse customer base / emerging markets

Well run business with ~$100MM sales, ~20% EBITDA ... closing ~ Nov. 30, 2011

“The Gardner Denver Way”

Large, 300,000 sq.ft. advanced manufacturing facility in Parma, Italy

Enabler for lower cost in IPG Europe ... ~20% cost advantage vs. Germany/UK

Aftermarket currently @ ~10%

Low cost country sourcing

Channel leverage ... complementary global sales channels & markets

Accretive in year 1 ... enables European footprint consolidation

Gardner Denver

43

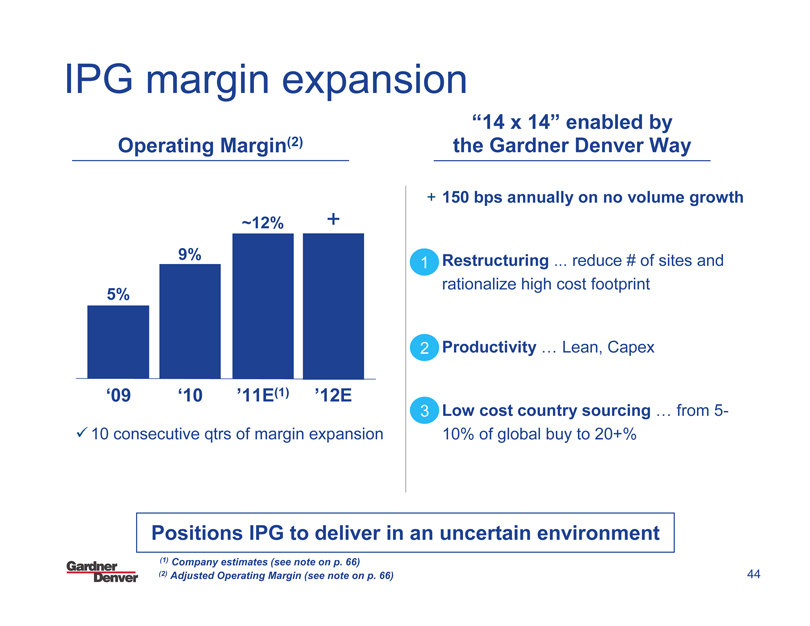

IPG margin expansion

Operating Margin(2)

+

~12%

9%

5%

‘09 ‘10 ’11E(1) ’12E

10 consecutive qtrs of margin expansion

“14 x 14” enabled by the Gardner Denver Way

+ 150 bps annually on no volume growth

1 Restructuring . reduce # of sites and rationalize high cost footprint

2 Productivity ... Lean, Capex

3 Low cost country sourcing ... from 5-10% of global buy to 20+%

Positions IPG to deliver in an uncertain environment

(1) Company estimates (see note on p. 66) (2) Adjusted Operating Margin (see note on p. 66)

Gardner Denver

44

Low cost country sourcing

1 Global Sourcing Team Established

New global leader for sourcing & materials

15 team members in China & India

China distribution hub established

2 Leveraging Global Commodity Spend

Localizing simple parts and kits

Combine global spend for high volume/value parts

Global sourcing team

Targeting doubling of spend in lower cost regions

Gardner Denver

45

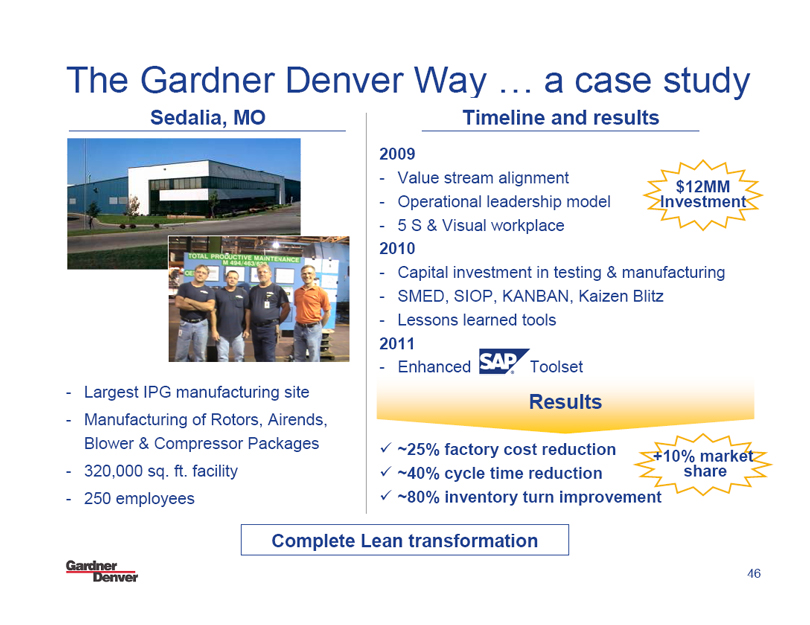

The Gardner Denver Way ... a case study

Sedalia, MO

- Largest IPG manufacturing site

- Manufacturing of Rotors, Airends,

Blower & Compressor Packages

- 320,000 sq. ft. facility

- 250 employees

Timeline and results

$12MM

Investment

2009

- Value stream alignment

- Operational leadership model

- 5 S & Visual workplace

2010

- Capital investment in testing & manufacturing

- SMED, SIOP, KANBAN, Kaizen Blitz

- Lessons learned tools

2011

- Enhanced SAP® Toolset

Results

+10% market

share

~25% factory cost reduction

~40% cycle time reduction

~80% inventory turn improvement

Complete Lean transformation

Gardner Denver

46

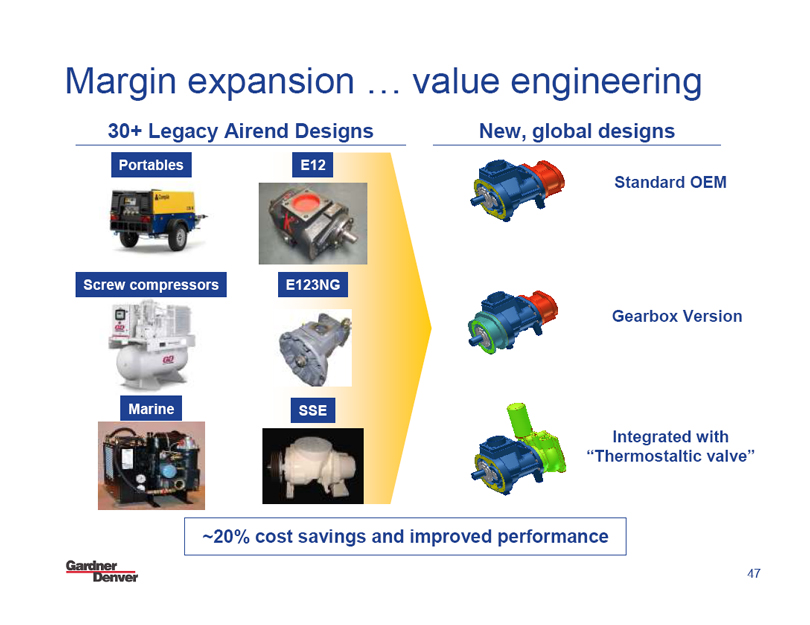

Margin expansion ... value engineering

30+ Legacy Airend Designs

Portables

Screw compressors

Marine

E12

E123NG

SSE

New, global designs

Standard OEM

Gearbox Version

Integrated with

“Thermostaltic valve”

~20% cost savings and improved performance

Gardner Denver

47

Break

Engineered Products Group

Engineered Products Group

GD GARDNER DENVER NASH A Gardner Denver Product THOMAS A Gardner Denver Product EMCO WHEATON

• Pressure pumping • Power Generation • Medical • Transportation

• On/Off Shore Drilling • Mining & Paper • Environmental • Energy

• Industrial Pumps • Chemical Processing • Lab/Life Sciences • Chemical

• Oil & Gas • Auto & Industrial

BAKER HUGHES H&P Inc PETROBRAS INVACARE Yes, you can: PHILIPS RESPIRONICS sense and simplicity BECHTEL

Schlumberger VALE TEIJIN

A $1B+ global leader in pumps and fluid transfer

Gardner Denver

50

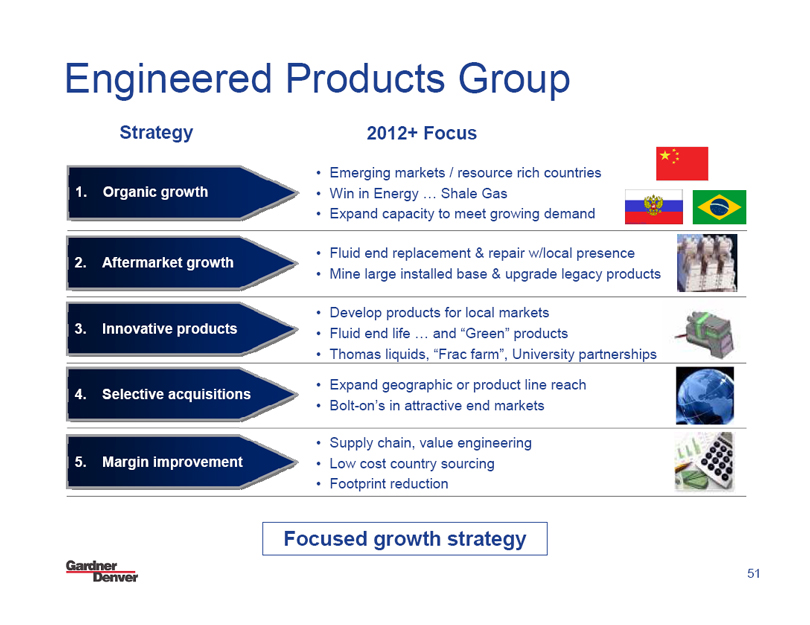

Engineered Products Group

Strategy 2012+ Focus

• Emerging markets / resource rich countries

1. Organic growth • Win in Energy ... Shale Gas

• Expand capacity to meet growing demand

• Fluid end replacement & repair w/local presence

2. Aftermarket growth • Mine large installed base & upgrade legacy products

• Develop products for local markets

3. Innovative products • Fluid end life … and “Green” products

• Thomas liquids, “Frac farm”, University partnerships

• Expand geographic or product line reach

4. Selective acquisitions • Bolt-on’s in attractive end markets

• Supply chain, value engineering

5. Margin improvement • Low cost country sourcing

• Footprint reduction

Focused growth strategy

Gardner Denver

51

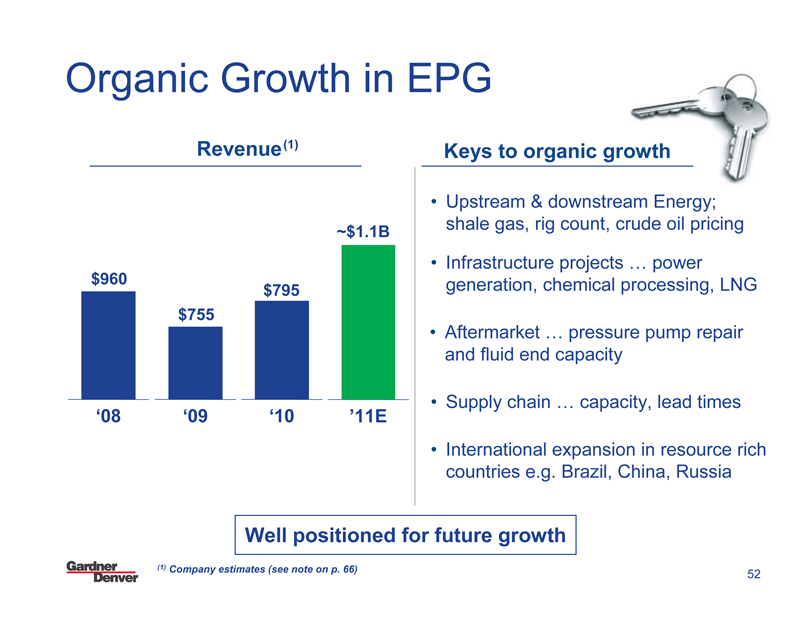

Organic Growth in EPG

Revenue(1)

~$1.1B

$960 $795 $755

Rev

‘08 ‘09 ‘10 ’11E

Keys to organic growth

• Upstream & downstream Energy; shale gas, rig count, crude oil pricing

• Infrastructure projects ... power generation, chemical processing, LNG

• Aftermarket ... pressure pump repair and fluid end capacity

• Supply chain ... capacity, lead times

• International expansion in resource rich countries e.g. Brazil, China, Russia

Well positioned for future growth

(1) Company estimates (see note on p. 66)

Gardner Denver

52

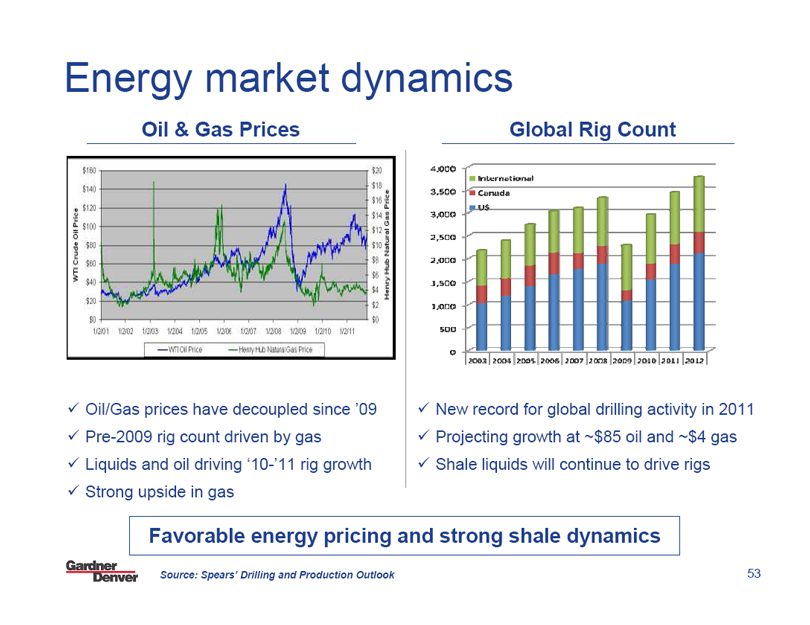

Energy market dynamics

Oil & Gas Prices

WTI Crude Oil Price

$150 $140 $120 $100 $80 $60 $40 $20 $0

$20 $18 $16 $14 $12 $10 $8 $6 $4 $2 $0

Henry Hub Natural Gas Price

1/2/01 1/2/02 1/2/03 1/2/04 1/2/05 1/2/06 1/2/07 1/2/08 1/2/09 1/2/10 1/2/11

WTI Oil Price Henry Hub Natural Gas Price

Oil/Gas prices have decoupled since ’09

Pre-2009 rig count driven by gas

Liquids and oil driving ‘10-’11 rig growth

Strong upside in gas

Global Rig Count

International

Canada

US

4,000 3,500 3,000 2,500 2,000 1,500 1,000 500 0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

New record for global drilling activity in 2011

Projecting growth at ~$85 oil and ~$4 gas

Shale liquids will continue to drive rigs

Favorable energy pricing and strong shale dynamics

Source: Spears’ Drilling and Production Outlook

Gardner Denver

53

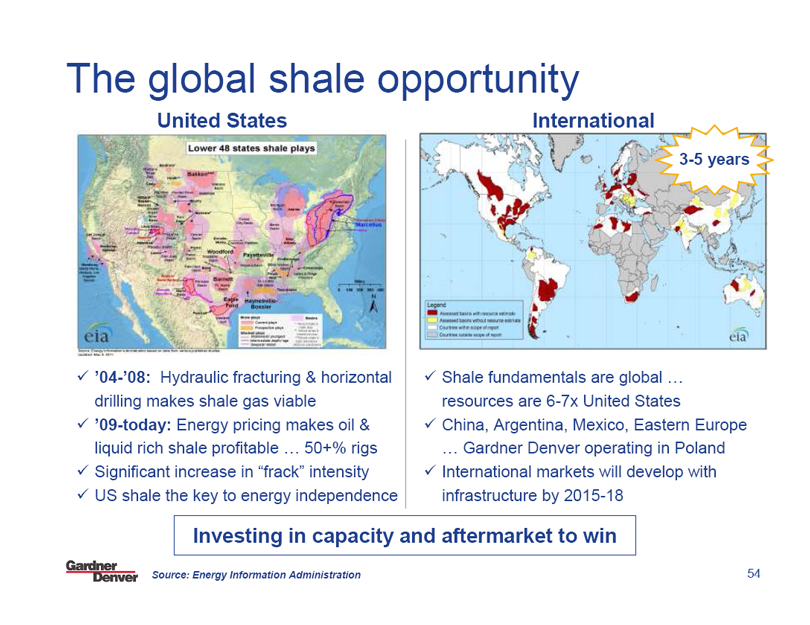

The global shale opportunity

United States

Lower 48 states shale plays

’04-’08: Hydraulic fracturing & horizontal drilling makes shale gas viable

’09-today: Energy pricing makes oil & liquid rich shale profitable ... 50+% rigs

Significant increase in “frack” intensity

US shale the key to energy independence

International

3-5 years

Shale fundamentals are global ... resources are 6-7x United States

China, Argentina, Mexico, Eastern Europe ... Gardner Denver operating in Poland

International markets will develop with infrastructure by 2015-18

Investing in capacity and aftermarket to win

Source: Energy Information Administration

Gardner Denver

54

International headlines

Baker Hughes Fractures its First Unconventional Shale Well in Argentina Baker Hughes Opens New Facility in Australia Baker Hughes Awarded Horizontal Well Completion Contract for China Gas Field

Lane Energy Poland and Schlumberger Deliver First Shale Gas Well in Baltic Basin

Eurasia Drilling Company Limited and Schlumberger Announce Completion of Transactions and Strategic Alliance

H&P Awarded FlexRig4M® Contract for Drilling in Bahrain

Baker Hughes, Schlumberger, H&P ... “as they go, we go”

BAKER HUGHES Schlumberger H&P Inc

Gardner Denver

55

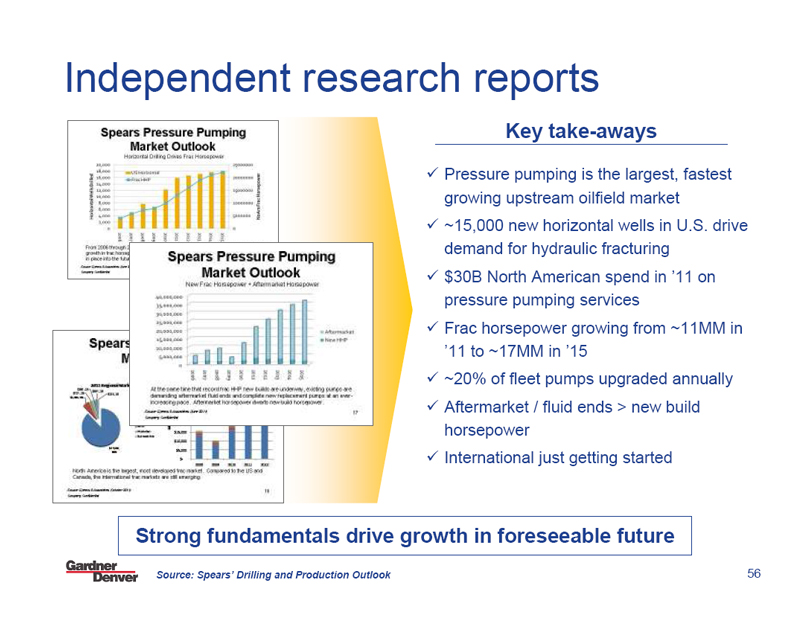

Independent research reports

Spears Pressure Pumping Market Outlook

Spears Pressure Pumping Market Outlook

Key take-aways

Pressure pumping is the largest, fastest growing upstream oilfield market

~15,000 new horizontal wells in U.S. drive demand for hydraulic fracturing

$30B North American spend in ’11 on pressure pumping services

Frac horsepower growing from ~11MM in ’11 to ~17MM in ’15

~20% of fleet pumps upgraded annually

Aftermarket / fluid ends > new build horsepower

International just getting started

Strong fundamentals drive growth in foreseeable future

Source: Spears’ Drilling and Production Outlook

Gardner Denver

56

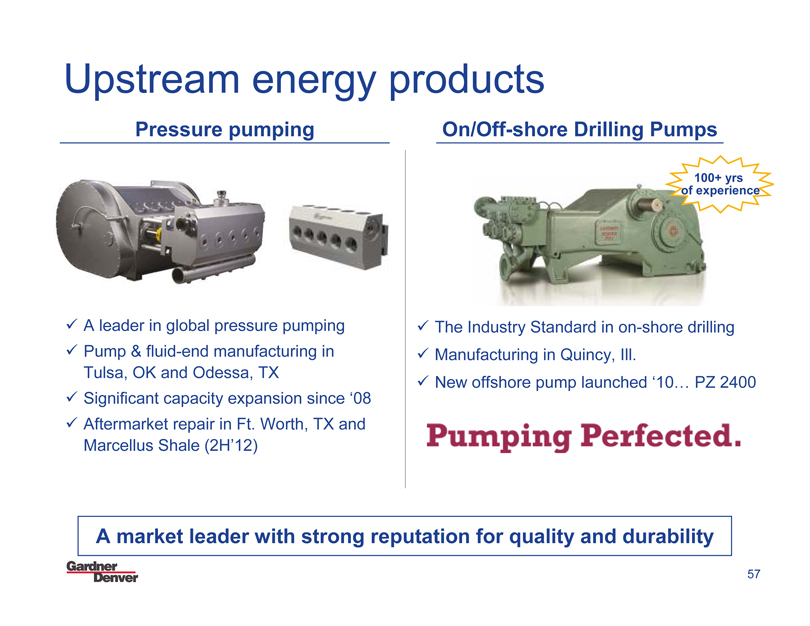

Upstream energy products

Pressure pumping

A leader in global pressure pumping

Pump & fluid-end manufacturing in Tulsa, OK and Odessa, TX

Significant capacity expansion since ‘08

Aftermarket repair in Ft. Worth, TX and Marcellus Shale (2H’12)

On/Off-shore Drilling Pumps

100+ yrs of experience

The Industry standard in onshore drilling.

Manufacturing in Quincy, III.

New offshore pump launched ‘10... PZ 2400

Pumping Perfected.

A market leader with strong reputation for quality and durability

Gardner Denver

57

Video

THE TULSA TRANSFORMATION

Gardner Denver

58

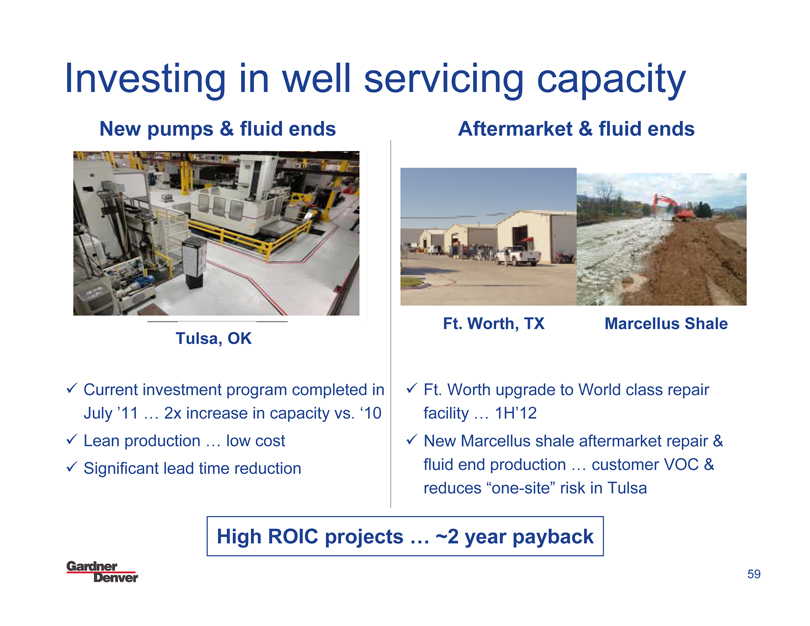

Investing in well servicing capacity

New pumps & fluid ends

Tulsa, OK

Current investment program completed in July ’11 ... 2x increase in capacity vs. ‘10

Lean production ... low cost

Significant lead time reduction

Aftermarket & fluid ends

Ft. Worth, TX Marcellus Shale

Ft. Worth upgrade to World class repair facility ... 1H’12

New Marcellus shale aftermarket repair & fluid end production ... customer VOC & reduces “one-site” risk in Tulsa

High ROIC projects ... ~2 year payback

Gardner Denver

59

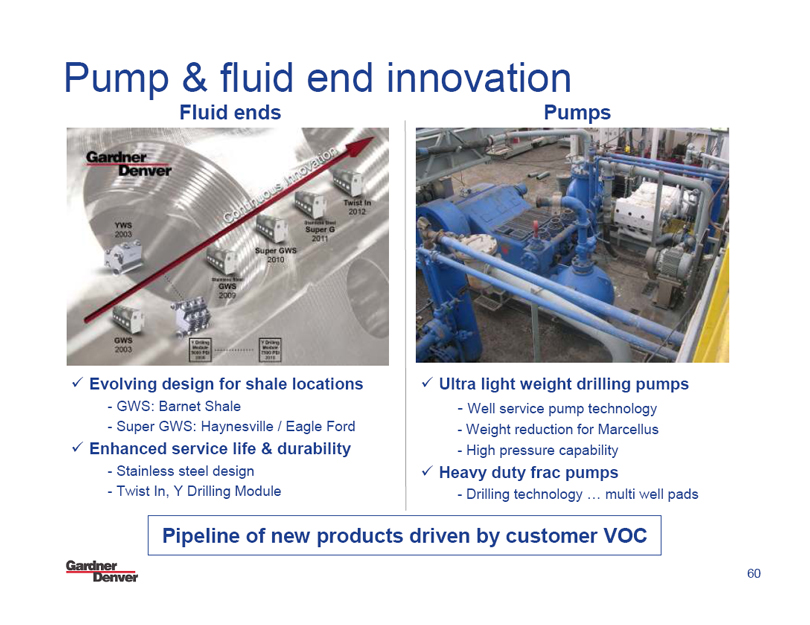

Pump & fluid end innovation

Fluid ends

Gardner Denver

Continuous Innovation

YWS 2003 GWS 2003 GWS 2009 Super GWS 2010 Super G 2011 Twist in 2012

Evolving design for shale locations

- GWS: Barnet Shale

- Super GWS: Haynesville / Eagle Ford

Enhanced service life & durability

- Stainless steel design

- Twist In, Y Drilling Module

Pumps

Ultra light weight drilling pumps

- Well service pump technology

- Weight reduction for Marcellus

- High pressure capability

Heavy duty frac pumps

- Drilling technology ... multi well pads

Pipeline of new products driven by customer VOC

Gardner Denver

60

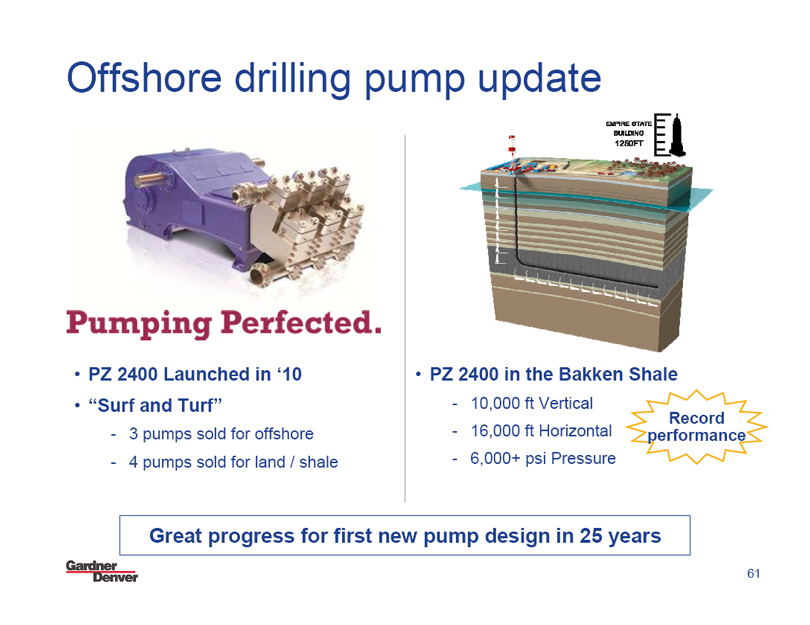

Offshore drilling pump update

Pumping Perfected.

• PZ 2400 Launched in ‘10

• “Surf and Turf”

- 3 pumps sold for offshore

- 4 pumps sold for land / shale

EMPIRE STATE

BUILDING

1250FT

• PZ 2400 in the Bakken Shale

- 10,000 ft Vertical

- 16,000 ft Horizontal

- 6,000+ psi Pressure

Record performance

Great progress for first new pump design in 25 years

Gardner Denver

61

Winning in emerging markets

Brazil

2x revenue in 2011

75,000 Sq Ft stand alone with low cost manufacturing capabilities

~130 employees

Strong growth in Mining and Oil & Gas

PETROBRAS

VALE

metso

NASH A Gardner Denver Product

Boshan, China

150,000 Sq Ft advanced manufacturing capabilities ... domestic and export

~300 employees

Strong local end markets ... power, chemicals

CHINA NATIONAL PETROLEUM CORPORATION

Strong local presence in high growth geographies

Gardner Denver

62

Exposure to great long term trends

THOMAS

A Gardner Denver Product

Oxygen concentrator

Blood analyzer

Growth opportunities in attractive end markets

- Environmental ... Government regulations

- Lab/Life Sciences ... University research

- Medical... aging demographics

Product translation to emerging end markets

Innovation ... “Pump with built-in intelligence”

EMCO WHEATON

Global movement of energy drives growth

Strong growth prospects in emerging markets

Floating Production/Storage/Offloading (FPSOs)

Energy Bridge Regasification Vessels (EBRVs)

Significant aftermarket opportunities

Becoming a solution provider

Significant growth opportunities

Gardner Denver

63

Closing Remarks/ Q&A

Gardner Denver

2011 Analyst Day

November 7, 2011

Gardner Denver

Presentation notes

• Note 1: Company estimates

• Note 2: Adjusted Operating Income, Adjusted Operating Margins, Adjusted Net Income and Adjusted DEPS are financial measures that are not in accordance with US GAAP. Adjusted Operating Income, Adjusted Operating Margins and Adjusted DEPS exclude the impact of expenses incurred for profit improvement initiatives, non-recurring items and impairment charges.

Adjusted net income is net income excluding non-cash impairment charges, net of related changes in deferred tax assets and liabilities.

Gardner Denver believes the non-GAAP financial measure of Adjusted Operating Income, Adjusted Operating Margins, Adjusted Net Income and Adjusted DEPS provide important supplemental information to both management and investors regarding financial and business trends used in assessing its results of operations. Gardner Denver believes excluding the specified items from the aforementioned financial measures provides a more meaningful comparison to the corresponding prior year periods and internal budgets and forecasts, assists investors in performing analysis that is consistent with financial models developed by investors in performing and research analysts, provides management with a more relevant measurement of operating performance, and is more useful in assessing management performance.

Gardner Denver

66