Gardner Denver Investor Presentation November, 2011 Exhibit 99.1 |

SF PowerPoint Template 03-27-08/2 2 Safe Harbor Disclosure All of the statements made by Gardner Denver in this presentation or made orally in connection with it, other than historical facts, are forward-looking statements. As a general matter, forward-looking statements are those focused upon anticipated events or trends, expectations, and beliefs relating to matters that are not historical in nature. The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for these forward-looking statements. In order to comply with the terms of the safe harbor, the Company notes that forward-looking statements are subject to known and unknown risks, uncertainties, and other factors relating to the Company’s operations and business environment, all of which are difficult to predict and many of which are beyond the control of the Company. These known and unknown risks, uncertainties, and other factors could cause actual results to differ materially from those matters expressed in, anticipated by or implied by such forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to: changing economic conditions; pricing of the Company’s products and other competitive market pressures; the costs and availability of raw materials; fluctuations in foreign currency rates and energy prices; risks associated with the Company’s current and future litigation; and the other risks detailed from time to time in the Company’s SEC filings, including but not limited to, its annual report on Form 10-K for the fiscal year ending December 31, 2010, and its quarterly reports on Form 10-Q. These statements reflect the current views and assumptions of management with respect to future events. The Company does not undertake, and hereby disclaims, any duty to update these forward- looking statements, although its situation and circumstances may change in the future. The inclusion of any statement in this presentation does not constitute admission by the Company or any other person that the events or circumstances described in such statement are material. |

Gardner Denver Overview |

4 Gardner Denver Overview Early stages of transformation to a high quality, high margin Industrial Company with Energy exposure Leading brands and technologies … strong distribution New, operationally focused team driving “The Gardner Denver Way” ~$2.4B (1) global Company with diverse and attractive end markets Growing, profitable aftermarket opportunity Focused on superior cash and earnings growth Strong track record on analyzing and integrating acquisitions (1) Company estimates (see note on p. 31) |

SF PowerPoint Template 03-27-08/5 5 A global leader in compressed air and gas, vacuum and fluid transfer technologies We serve a wide range of industries with efficient & reliable products Energy Medical Mining Transportation Food & Beverage |

6 Two business segments aligned to effectively serve our customers Engineered Products Group Industrial Products Group 2011 Sales by segment ~$1.2B ~$1.1B (1) Company estimates (see note on p. 31) (1) Petroleum pumps Liquid ring pumps Loading arms OEM compressors Compressors (>50psi) Blowers (<50psi) Great portfolio of brands and businesses |

SF PowerPoint Template 03-27-08/7 7 Well established sales channels Distribution 10% Direct 57% OEM 33% Engineered Products Group Industrial Products Group Distribution 48% Direct 33% OEM 19% Products designed for customer specific applications Primarily standard configuration products |

8 Highly diversified and global End Markets (1) Geographic Industrial Manufacturing (28%) Upstream Energy (12%) Downstream Energy (10%) Medical/ Laboratory (9%) Transportation (9%) Food & Beverage (6%) Mining & Construction (5%) Chemical (5%) Environment (3%) Printing (2)% Auto Svcs (2%) Paper (2)%) Other (7%) 2010 Revenue by End User Canada 4% United States 35% Latin America 3% Europe 35% Other 7% Asia 16% 2010 Revenue by Geography Visibility to a large cross section of global economy (1) Company estimates (see note on p. 31) |

SF PowerPoint Template 03-27-08/9 9 Exposed to multiple phases of the economic cycle Early Cycle (1-18 months) Late Cycle (36+ months) Mid Cycle (18-36 months) Engineered packages Infrastructure projects Industrial air compressors OEM Aftermarket |

SF PowerPoint Template 03-27-08/10 10 Current end market dynamics Comment Status Strong growth in Americas Well servicing and drilling pump demand very strong China softening, APAC strong Stable U.S. Industrial Production - Capacity utilization E.U. Industrial Production Oil & Gas - Rig count, crude / nat gas pricing China/Asia Pacific OEM applications End market / Indicator Stable … cautionary tone Generally, favorable end markets in an uncertain environment |

SF PowerPoint Template 03-27-08/11 11 Prepared for economic volatility Cautiously optimistic on macro economy … contingency plans in the works since April 2011 Strong track record on cost reductions since 2008 Headcount (23)% reduction / 2,700 employees Footprint Closed 8 plants One ERP 71% + 450 bps Operating Margins |

Growth Strategy |

13 • Strengthen presence in attractive end markets & emerging markets 4. Selective acquisitions • Access to faster growing end markets and generate synergies Strategy Focus 2. Aftermarket growth • Higher margin, less cyclical 5. Margin expansion • Cost reductions and operational excellence 3. Innovative products • Expand share with differentiated technologies Simple, focused 5-point strategy Execution supported by the principles of the Gardner Denver Way 1. Organic growth |

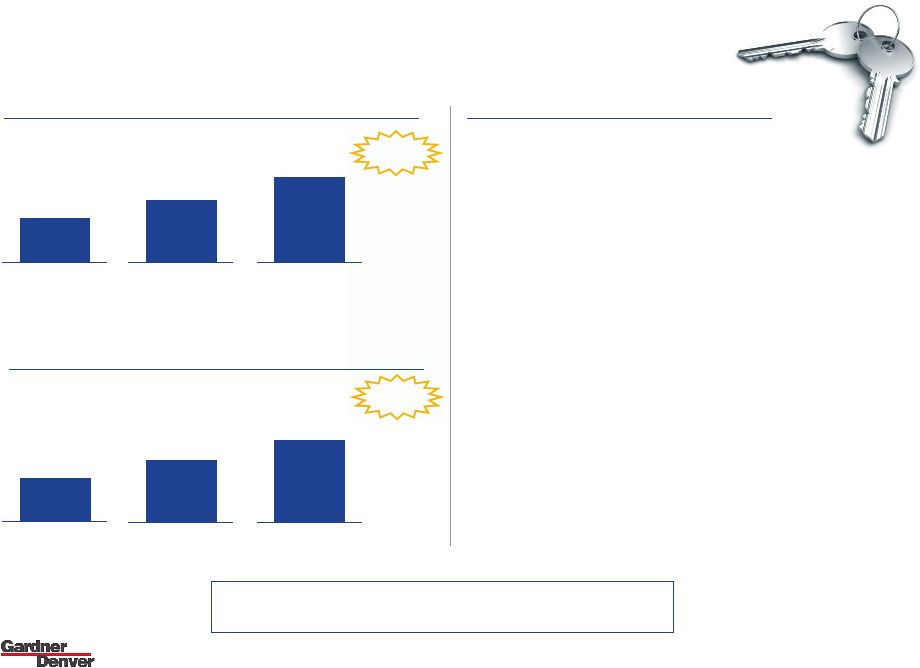

SF PowerPoint Template 03-27-08/14 14 ’11E (1) ~$600 Organic growth Keys to organic growth • Leading brands & technologies Orders ~10% • Diverse end markets … strong distribution channels ‘10 $554 Backlog ’11E (1) ~$2.5B ~20% ‘10 $2,060 ‘09 $1,570 ‘09 $395 • Growing emerging markets presence • Higher growth end markets … energy • Aftermarket ($’s in millions) (1) Company estimates (see note on p. 31) Good momentum going into 2012 |

SF PowerPoint Template 03-27-08/15 15 Build out the aftermarket Key growth drivers • Large installed base Aftermarket as % of sales • Big opportunity in pressure pumping repair and fluid ends ‘10 31% ‘09 29% ‘08 26% • Remote monitoring capabilities • Design in proprietary features Goal 40-45% • Extended warranty and service agreements Higher margin, less cyclical growth |

SF PowerPoint Template 03-27-08/16 16 A more innovative Company Voice of customer differentiates products from competition Value proposition based on customer needs 2011 product launches across multiple divisions demonstrate progress PZ-2400 Drilling Pump Hoffman Revolution Quantima Compressor Goal: ~10% of annual revenues from new products |

17 24 acquisitions over 15 years 1996 2011 Engineered Products Group Industrial Products Group TCM Twentieth Century Mfg . Water Jetting • Butterworth • CRS Power Flow • Jetting Systems Strong track record on analyzing & integrating acquisitions |

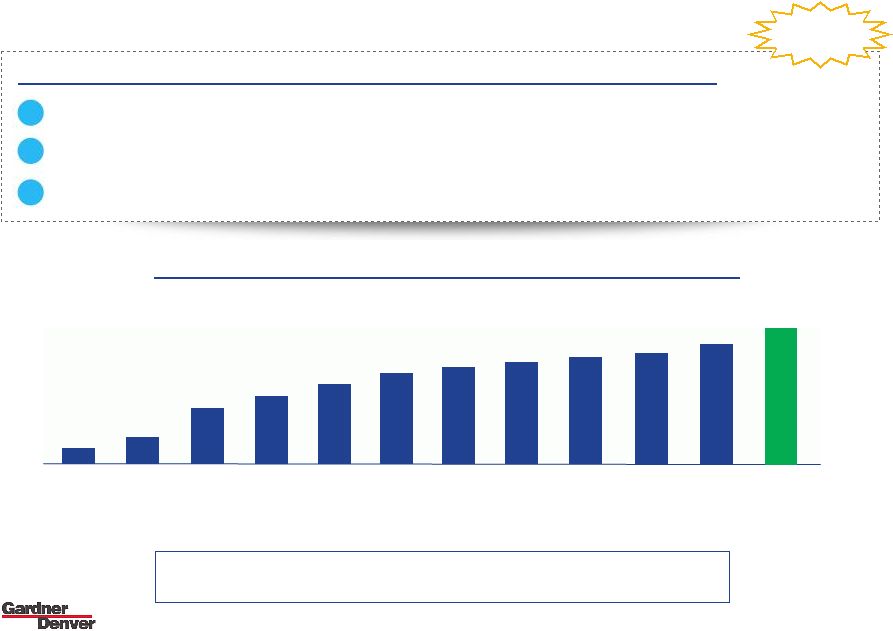

18 IPG Margin Expansion 1Q09 1Q10 2.0% 2Q09 3Q09 4Q09 10 Quarters of Sequential Margin Expansion (2) 2Q10 2Q11 3Q10 4Q10 1Q11 3Q11 2.5% 6.8% 7.5% 8.3% 8.6% 9.4% 10.1% 11.3% 11.7% 13.1% Goal 14% +150 bps of margin expansion annually w/no volume growth: Restructuring … 27% reduction in employment since Oct ’08, ~$70 million program Productivity investments … 8 fewer facilities, Lean, Capex / machine tools, SAP Low Cost Country Sourcing … “just getting started” 1 2 3 “14 x 14” (2) Adjusted Operating Margin (see note on p. 31) Committed to continued margin expansion |

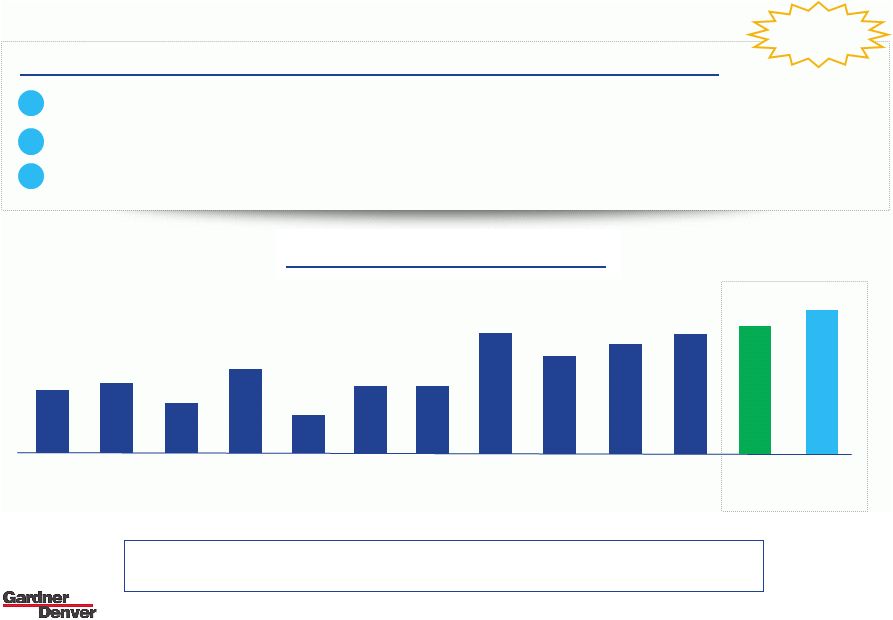

19 EPG Margin Expansion 1Q09 1Q10 19.5% 2Q09 3Q09 4Q09 EPG Margin Expansion (2) 2Q10 2Q11 3Q10 4Q10 1Q11 3Q11 19.7% 17.8% 20.9% 16.0% 19.5% 19.7% 24.0% 22.9% 23.3% 23.6% Last Peak 24.5% +50 bps of margin expansion annually w/ no volume growth: Restructuring … reduced employment by 15% since ’08 with 15% increase in revenue Productivity investments … Lean, Capex / capacity, enhanced project mgmt Low Cost Country Sourcing … some progress made, but more opportunities 1 2 3 +50 bps “New” Peak ~28.5% (2) Adjusted Operating Margin (see note on p. 31) Expanding already attractive operating margins |

Financial Results |

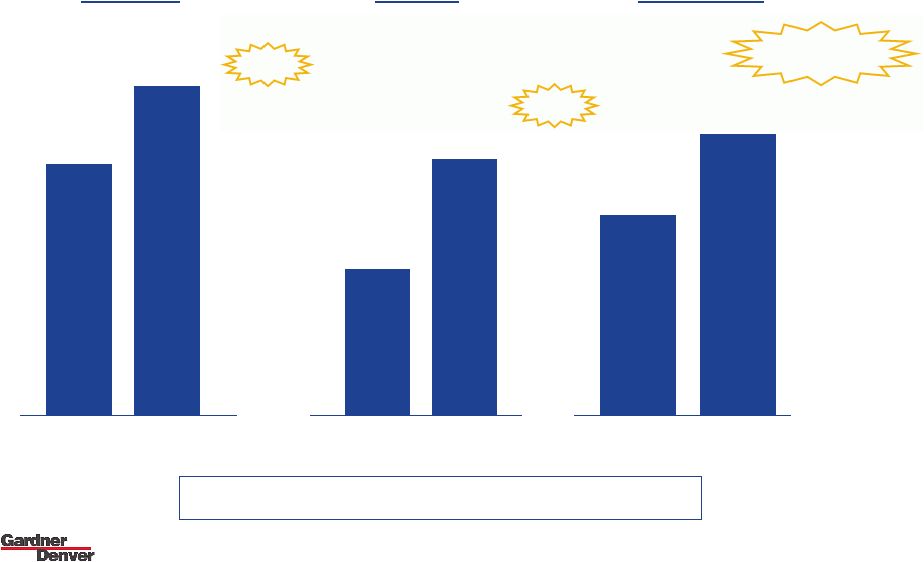

SF PowerPoint Template 03-27-08/21 21 2000 $379 $1,215 2005 $1,895 2010 Revenue $3.28 2010 2005 $1.37 $0.60 2000 DEPS 2000 $31 2005 $115 2010 $202 Cash Flow from Operations A decade of financial performance 17% CAGR Strong track record 19% CAGR 21% CAGR ($’s in millions) |

22 $1.9B 2010 ~$2.4B 2011 Revenue $5.44 - $5.49 2011 2010 $3.39 Adjusted DEPS (2) 2010 $202 2011 ~$300 2011 financial outlook ~25% ~60% 1.2 x Net Income A record year on key financial metrics (1) Company estimates (see note on p. 31) (1) Cash Flow from Operations (2) Adjusted DEPS (see note on p. 31) (in line with guidance) |

SF PowerPoint Template 03-27-08/23 23 Strong cash generation 2008 $237 $169 2009 $169 2010 Cash Flow Disciplined capital deployment FCF CFOA 2011E $278 $211 $202 ~$300 ~$250 FCF Conv. 143% N/M 98% ~90% (1) ($’s in millions) (1) Company estimates (see note on p. 31) Capital expenditures… organic growth and productivity 1 2 3 4 Capital Deployment Strategy Financial objectives… reduce debt, strong balance sheet Selective acquisitions… inorganic investment to create value Return to shareholders... dividend, opportunistic buyback |

SF PowerPoint Template 03-27-08/24 24 Internal long term operating goals progress • Grow 2 x GDP Operating goals Good progress YTD … more to do 3Q YTD Comment • Margin expansion • FCF Conversion • Increase ROIC • Lean cost structure + + + / + + • Revenue up 29% • DEPS up 74% • 86% • ROIC ~19% • 16.8% SG&A to sales - 2011 |

25 2012 earnings growth framework Tailwinds: + Margin expansion “The Gardner Denver Way” + Orders momentum / EPG backlog + Strength in Energy end markets + Aftermarket momentum + Accretive M&A … Robuschi + Reduced share count Headwinds: – Macro uncertainty incl. China, Europe – Late cycle infrastructure projects – Tougher comparisons to record 2011 ’11 Adj DEPS (2) ~$5.44-5.49 ’12 Adj DEPS + (2) Adjusted DEPS (see note on p. 31) Positioned to deliver in an uncertain environment |

The Gardner Denver Way |

27 Aftermarket growth Innovative products Selective acquisitions Margin expansion Organic growth CUSTOMERS Innovation High Velocity RESOURCES Strategy supported by The Gardner Denver Way Execution requires superior human resources SHAREHOLDERS EMPLOYEES |

28 Building a high performance culture New, operationally focused management team driving transformation Operationally focused team Policy deployment Operating rhythms Clear accountability Continuous improvement |

29 Gardner Denver Summary Early stages of transformation to a high quality, high margin Industrial Company with Energy exposure Leading brands and technologies … strong distribution New, operationally focused team driving “The Gardner Denver Way” ~$2.4B (1) global Company with diverse and attractive end markets Growing, profitable aftermarket opportunity Focused on superior cash and earnings growth Strong track record on analyzing & integrating acquisitions (1) Company estimates (see note on p. 31) |

Gardner Denver Investor Presentation November, 2011 |

SF PowerPoint Template 03-27-08/31 31 Presentation notes • Note 1: Company estimates • Note 2: Adjusted Operating Income, Adjusted Operating Margins, Adjusted Net Income and Adjusted DEPS are financial measures that are not in accordance with US GAAP. Adjusted Operating Income, Adjusted Operating Margins and Adjusted DEPS exclude the impact of expenses incurred for profit improvement initiatives, non-recurring items and impairment charges. Adjusted net income is net income excluding non-cash impairment charges, net of related changes in deferred tax assets and liabilities. Gardner Denver believes the non-GAAP financial measure of Adjusted Operating Income, Adjusted Operating Margins, Adjusted Net Income and Adjusted DEPS provide important supplemental information to both management and investors regarding financial and business trends used in assessing its results of operations. Gardner Denver believes excluding the specified items from the aforementioned financial measures provides a more meaningful comparison to the corresponding prior year periods and internal budgets and forecasts, assists investors in performing analysis that is consistent with financial models developed by investors in performing and research analysts, provides management with a more relevant measurement of operating performance, and is more useful in assessing management performance. |