UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08228

The Timothy Plan

(Exact name of registrant as specified in charter)

1055 Maitland Center Commons, Maitland, FL 32751

(Address of principal executive offices) (Zip code)

Art Ally, The Timothy Plan

1055 Maitland Center Commons, Maitland, FL 32751

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-846-7526

Date of fiscal year end: 9/30

Date of reporting period: 9/30/12

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Registrant’s audited annual financial reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 are as follows:

-2-

ANNUAL REPORT

September 30, 2012

TIMOTHY PLAN FAMILY OF FUNDS

Letter from the President

September 30, 2012

Arthur D. Ally

Dear Shareholder,

As you review the details on the following pages, you should be pleased to see that all of our funds turned in, in our opinion, anywhere from respectable to good performance for the twelve months of our past fiscal year (10-1-11 thru 9-30-12). Of course, as you probably know, past performance does not guarantee future results.

However as I reported last year, although we cannot guarantee any actual outcome, I am confident of a couple of things:

| | • | | If the November, 2012 elections result in replacing a number of liberal members of Congress (as well as the current Administration) with common sense conservatives, the capital markets could react very favorably, and |

| | • | | All of our sub-advisors remain, in our opinion, among the best in the industry and they each continue to honor our overall policy that they manage their respective Funds both in accordance with our screening restrictions and with a conservative bias. |

You will find each of our sub-advisors’ annual review letters along with their economic outlook in the pages that follow.

Finally, I would once again like to thank you for your moral convictions that led you to becoming part of the Timothy Plan Family.

Yours in Christ,

ARTHUR D. ALLY,

President

Timothy Plan Fund Performance

[2]

Letter from the Manager

September 30, 2012

Aggressive Growth Fund

We are pleased to report that the Fund advanced 27.47% over the last 12 months ended September 30, 2012. This is a 0.77% percentage-point outperformance against our benchmark, the Russell Mid-Cap Growth index, which rose 26.7% over the same period.

The market had strong advances in 3 of the last 4 quarters, only pausing to take a breather in the second quarter of this year. We have rarely witnessed a time when the old adage of the market “climbing a wall of worry” has been more apt. The litany of concerns during the last year has included: the European Sovereign Debt crisis, China (and much of the world’s) slowing growth, the looming U.S. “fiscal cliff,” consumer de-leveraging and unprecedented government balance-sheet expansion, and a tightly-contested upcoming presidential election. The market has taken a “glass-half-full” view, and focused on the positives - central bankers’ massive amounts of easing, ongoing healthy corporate profits, a nascent recovery in housing, and the relative attractiveness of stocks given extremely-low bond yields.

After such a powerful rally - and with many issues yet to be resolved - we are keeping our guard up. We have recently had our cash balances a little higher than average, and we are being cautious with our stock selection. We think that earnings growth is going to slow and that negative surprises will be more commonplace, hence, with our portfolio holdings we are focusing as much on the sustainability of earnings as with the absolute level of earnings growth.

CHARTWELL INVESTMENT PARTNERS, L.P.

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. Class A shares performance quoted excludes sales charge.

Timothy Plan Fund Performance

[3]

Fund Performance | Aggressive Growth

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Aggressive Growth Fund - Class A (With Sales Charge) | | | | 20.71 | % | | | | -1.26 | % | | | | 7.17 | % | | | | | |

Russell Mid-Cap Growth Index | | | | 26.69 | % | | | | 2.54 | % | | | | 11.11 | % | | | | | |

Timothy Aggressive Growth Fund - Class C * | | | | 27.08 | % | | | | -0.86 | % | | | | 3.49 | % | | | | (a) | |

Russell Mid-Cap Growth Index | | | | 26.69 | % | | | | 2.54 | % | | | | 6.91 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

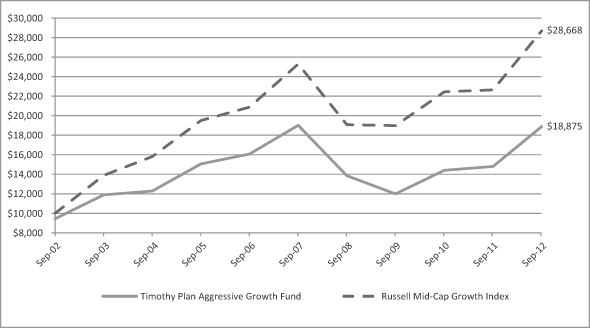

Timothy Plan Aggressive Growth Fund vs. Russell Mid-Cap Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell Mid-Cap Growth Index on September 30, 2002 and held through September 30, 2012. The Russell Mid-Cap Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[4]

Letter from the Manager

September 30, 2012

International Fund

Central bankers around the world put on their full armor and deployed their bazookas with the Federal Reserve and the European Central Bank (ECB) leading the way. Bankers’ unprecedented use of unconventional monetary policies hit on all cylinders as the ECB’s Mario Draghi announced plans for unlimited buying of sovereign debt with yet another program, this time called the Outright Monetary Transactions (OMT) on top of the successful bank lending program named the LTRO earlier in the year. The Fed’s Ben Bernanke was not to be outdone as he announced open-ended buying of mortgage-backed securities to the tune of up to $40bn per month going forward.

These liquidity measures flooding the markets translate to very low interest rates for borrowers of all kinds, including corporations. The all-out assault from the ECB on speculative attacks on the euro and Eurozone sovereign markets seemed to soothe equity markets in Europe. With low valuations in the Eurozone, the ECB’s aggressive stance to protect the monetary union sent equity markets there surging in the third quarter of 2012, translating into significant gains for European equity markets. Although economic figures showed some signs of hope in the US housing market, most other global economic measures appear to show continued weakness across Europe, Japan, and even the emerging economies. Such uncertainty led to bouts of “risk on” and “risk off” markets during the year. In spite of such volatility and rotations in sector leadership, the Fund performed well relative to the MSCI EAFE benchmark for the year.

Strong stock selection in eight of the ten sectors helped the Fund outperform its benchmark. The best returns for the Fund relative to the benchmark came from the Telecom Services, Materials, and Financials sectors from a stock selection standpoint. In Telecoms, the Fund’s holdings in Philippines telcos proved the right strategy as they performed well for the period. In Materials, an overweight to agro-chemicals benefited the Fund as strong agricultural markets led to strong demand for fertilizers and specialty chemicals. For the Financials sector, even though the Fund was underweight the sector, which hurt performance, this was more than compensated by very good stock selection, in particular holdings in Singapore and Hong Kong. The Fund maintains an underweight to Japan as we find better opportunities in the emerging markets and Canada which have proven to be the right strategy given Japan’s poor performance during this period.

The portfolio’s defensive posture throughout the year, with higher than average cash levels, was the biggest drag on performance. In spite of this, the Fund performed well. We have reduced the cash to more normal levels and will continue to take advantage of volatile markets to invest in solid companies from around the world at a time that international equity valuations remain at attractive levels. The Financials sector along with Japan and the eurozone remain the largest underweights in the Fund while the largest overweights at the start of the new fiscal year are in telecom services, energy, Canada, and the emerging markets.

EAGLE GLOBAL ADVISORS

Timothy Plan Fund Performance

[5]

Fund Performance | International

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | Average

Annual Return

Since Inception (a) |

Timothy International Fund - Class A (With Sales Charge) | | | | 9.38 | % | | | | -7.52 | % | | | | -5.36 | % |

MSCI EAFE Index | | | | 10.01 | % | | | | -8.07 | % | | | | -7.00 | % |

Timothy International Fund - Class C * | | | | 14.88 | % | | | | -7.15 | % | | | | -5.10 | % |

MSCI EAFE Index | | | | 10.01 | % | | | | -8.07 | % | | | | -7.00 | % |

| | (a) | For the period May 3, 2007 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

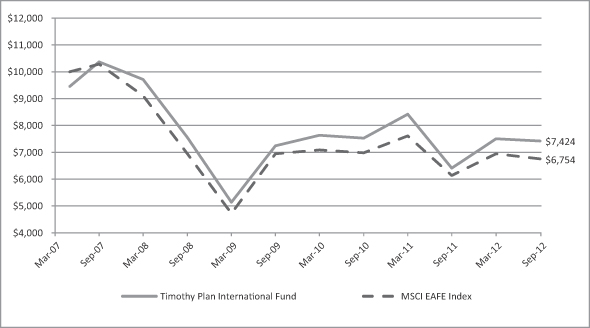

Timothy Plan International Fund vs. MSCI EAFE Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the MSCI EAFE Index on May 3, 2007 and held through September 30, 2012. The MSCI EAFE Index is a widely recognized unmanaged index of equity prices and is representative of equity market performance of developed countries, excluding the U.S. and Canada. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[6]

Letter from the Manager

September 30, 2012

Large/Mid Cap Growth Fund

We are pleased to report that the Fund advanced 26.61% over the last 12 months ending September 30, 2012, essentially matching the return of the benchmark, the Russell 1000 Growth Index, which rose 29.1% over the same period.

The market had strong advances in 3 of the last 4 quarters, only pausing to take a breather in the second quarter of this year. We have rarely witnessed a time when the old adage of the market “climbing a wall of worry” has been more apt. The litany of concerns during the last year has included: the European Sovereign Debt crisis, China (and much of the world’s) slowing growth, the looming U.S. “fiscal cliff,” consumer de-leveraging and unprecedented government balance-sheet expansion, and a tightly-contested upcoming presidential election. The market has taken a “glass-half-full” view, and focused on the positives - central bankers’ massive amounts of easing, ongoing healthy corporate profits, a nascent recovery in housing, and the relative attractiveness of stocks given extremely-low bond yields.

After such a powerful rally - and with many issues yet to be resolved - we are keeping our guard up. We have recently had our cash balances a little higher than average, and we are being cautious with our stock selection. We think that earnings growth is going to slow and that negative surprises will be more commonplace, hence, with our portfolio holdings we are focusing as much on the sustainability of earnings as with the absolute level of earnings growth.

CHARTWELL INVESTMENT PARTNERS, L.P.

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. Class A shares performance quoted excludes sales charge.

Timothy Plan Fund Performance

[7]

Fund Performance | Large/Mid Cap Growth

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Large/Mid Cap Growth Fund - Class A (With Sales Charge) | | | | 19.69 | % | | | | -0.31 | % | | | | 5.16 | % | | | | | |

Russell 1000 Growth Index | | | | 29.19 | % | | | | 3.24 | % | | | | 8.41 | % | | | | | |

Timothy Large/Mid Cap Growth Fund - Class C * | | | | 25.47 | % | | | | 0.07 | % | | | | 2.63 | % | | | | (a) | |

Russell 1000 Growth Index | | | | 29.19 | % | | | | 3.24 | % | | | | 5.38 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

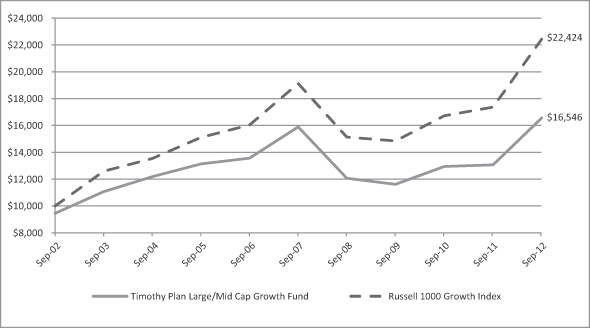

Timothy Plan Large/Mid Cap Growth Fund vs. Russell 1000 Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 1000 Growth Index on September 30, 2002 and held through September 30, 2012. The Russell 1000 Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[8]

Letter from the Manager

September 30, 2012

Small Cap Value Fund

We are pleased to provide you with our report for the Timothy Plan Small Cap Value Fund for the twelve months ending September 30, 2012 and would like to thank you for entrusting your assets with us.

The past twelve months equity markets, while withstanding some volatility, generally moved higher. Stocks moved higher in 4th quarter 2011 and into the 1st quarter of 2012 on what appeared to be strengthening economic data and optimism surrounding the Europea n debt crisis. Investor sentiment turned negative by the second quarter as we saw renewed concerns over the European crisis and a slowdown in both the U.S. and Chinese economies. Third quarter markets turned higher again on hopes the U.S. and Europe would engineer more stimulus to help their respective economies. During such periods, it can be difficult for active managers who employ bottom-up, fundamental research to generate high levels of alpha. Investors have sought out economically-sensitive and global firms during much of the fiscal year, while the safe-haven, high-yielding securities led the market during times of uncertainty, such as in the 2nd quarter. We have historically outperformed for many years following an economic recovery, and even though the recovery has taken longer due to the depth of the financial crisis, we are pleased that our small-cap strategy has performed well. As we take on the next fiscal year, we will, as long-term investors, remain disciplined, keep emotions in check and be opportunistic.

For the twelve months ending September 30, 2012, the Timothy Plan Small Cap Value Fund produced a return of 36.23%, while the Russell 2000 Index produced a return of 31.18%. Smaller market capitalization company stocks, which tend to have revenues that are more sensitive to the business cycle, outperformed the broad U.S. market. Security selection was the primary driver of relative outperformance and centered in the Consumer Discretionary, Energy, Producer Durables and REITs (Real Estate Investment Trusts) sectors. Optimism about the economy aided the performance of economically-sensitive companies. Specifically, Saia and EnerSys surged along with an improvement in investor sentiment and confidence in the U.S. economy. North American heavy truck demand rose and also boosted SAIA based on its ability to achieve pricing power and control operating costs, which allows for greater operating leverage. An increase in water heater sales in China boosted earnings and made for a positive 2013 outlook for A.O. Smith Corp. Kodiak Oil & Gas announced an equity offering to accelerate their drilling programs and investors bid up the name due to continued confidence in their operations. Last, Chemical Financial performed very well. Holdings in Financial Services performed well as banks rallied on the positive results from the U.S. “stress test” and the stabilization of the U.S. housing market.

Security selection in Health Care coupled with an underweight in both Consumer Discretionary and Health Care detracted from performance. Consumer Discretionary and Health Care index sectors outperformed the market and our holdings failed to keep pace. In Energy, holdings related to natural gas and coal detracted from performance including Basic Energy Services, which provides ancillary services to natural gas companies. Basic Energy Services also experienced slower oil service activity and declined on pricing pressures among their varying lines of business. Gastar Exploration reported weak earnings and lower production guidance for the rest of the year. Also a drag on relative performance was Layne Christensen, which reported disappointing margins and a foreign corruption investigation, while Tellabs lowered forward guidance and reported slower revenue growth than previously expected. Last, in Financial Services, Knight Capital experienced a bug in the new trading software that erroneously unleashed orders for millions of shares onto U.S. exchanges. With investors worried about their survival, the stock was sold.

WESTWOOD MANAGEMENT CORPORATION

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. Class A shares performance quoted excludes sales charge.

Timothy Plan Fund Performance

[9]

Fund Performance | Small Cap Value

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Small Cap Value Fund - Class A (With Sales Charge) | | | | 28.73 | % | | | | 0.17 | % | | | | 7.47 | % | | | | | |

Russell 2000 Index | | | | 31.18 | % | | | | 2.96 | % | | | | 10.55 | % | | | | | |

Timothy Small Cap Value Fund - Class C * | | | | 35.08 | % | | | | 0.55 | % | | | | 3.88 | % | | | | (a) | |

Russell 2000 Index | | | | 31.18 | % | | | | 2.96 | % | | | | 5.75 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

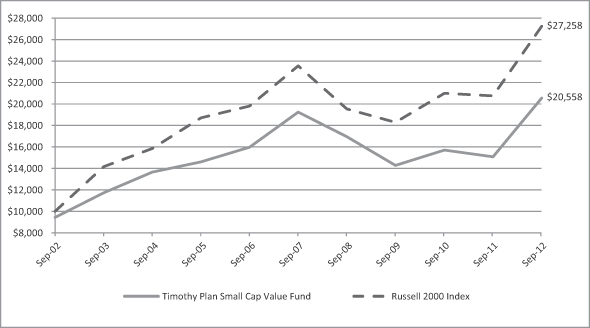

Timothy Plan Small Cap Value Fund vs. Russell 2000 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 2000 Index on September 30, 2002 and held through September 30, 2012. The Russell 2000 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[10]

Letter from the Manager

September 30, 2012

Large/Mid Cap Value Fund

We are pleased to provide you with our report for the Timothy Plan Large/Mid Cap Value Fund for the twelve months ending September 30, 2012 and would like to thank you for entrusting your assets with us.

The past twelve months equity markets, while withstanding some volatility, generally moved higher. Stocks moved higher in 4th quarter 2011 and into the 1st quarter of 2012 on what appeared to be strengthening economic data and optimism surrounding the European debt crisis. Investor sentiment turned negative by the second quarter as we saw renewed concerns over the European crisis and a slowdown in both the U.S. and Chinese economies. Third quarter markets turned higher again on hopes the U.S. and Europe would engineer more stimulus to help their respective economies. During such periods, it can be difficult for active managers who employ bottom-up, fundamental research to generate high levels of alpha. Investors have sought out economically-sensitive and global firms during much of the fiscal year, while the safe-haven, high-yielding securities led the market during times of uncertainty, such as in the 2nd quarter. We have historically outperformed for many years following an economic recovery, but this recovery has taken longer due to the depth of the financial crisis. Fundamental analysis has worked during earnings season and when Euro fears are not driving sentiment. Looking ahead, volatility is likely to remain high given the U.S. election, U.S. fiscal cliff and global growth slowdown. However, we are confident that our positioning in high-quality companies with under-appreciated earnings growth potential should fare well in this environment.

For the twelve months ending September 30, 2012, the Timothy Plan Large/Mid Cap Value Fund produced a return of 25.39%, while the S&P 500 Index produced a return of 30.2%. Security selection in Energy, Producer Durables and Material & Processing aided relative performance. The Financial Services sector has been a consistent outperformer and our overweight in this sector also benefited the Fund. Many of the Fund’s top performers were in sectors levered to economic growth. Optimism about the global economy aided the performance of pro-cyclical, global companies, such as Energy holding National Oilwell Varco, Materials & Processing holding Sherwin-Williams and Producer Durables’ holdings Flowserve and Union Pacific. Additionally, company-specific news benefitted selected holdings such as Union Pacific, which was bid up as the company reported continued strong execution, including rising revenues and pricing. In Financial Services, INVESCO and other asset managers held in the portfolio rose with the market.

Security selection in Consumer Discretionary, Technology and Utilities was the largest detractor to relative performance in the prior twelve months. Technology and Consumer Discretionary index sectors outperformed the market and our holdings failed to keep pace. Technology’s Western Digital and Consumer Discretionary’s Lear Corp. suffered from concerns surrounding economic weakness as well as a decline in European auto sales, respectively. In Producer Durables, Xylem declined as its water infrastructure business could suffer slowdowns as the domestic economy remains slow. Goodrich lagged as commercial sales disappointed and last, FirstEnergy pulled back forward guidance based on new regulations and power auctions that could impact 2013 earnings.

WESTWOOD MANAGEMENT CORPORATION

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. Class A shares performance quoted excludes sales charge.

Timothy Plan Fund Performance

[11]

Fund Performance | Large/Mid Cap Value

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Large/Mid Cap Value Fund - Class A (With Sales Charge) | | | | 18.48 | % | | | | -1.28 | % | | | | 8.55 | % | | | | | |

S&P 500 Index | | | | 30.20 | % | | | | 1.05 | % | | | | 8.01 | % | | | | | |

Timothy Large/Mid Cap Value Fund - Class C * | | | | 24.41 | % | | | | -0.91 | % | | | | 6.14 | % | | | | (a) | |

S&P 500 Index | | | | 30.20 | % | | | | 1.05 | % | | | | 8.01 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

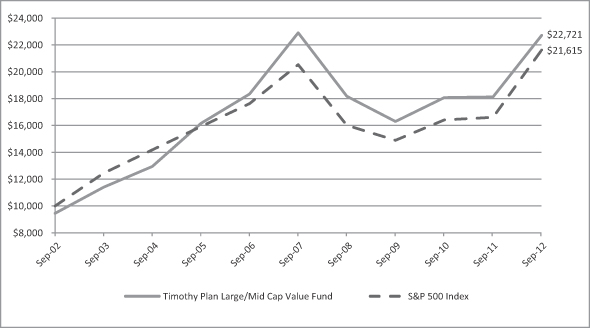

Timothy Plan Large/Mid Cap Value Fund vs. S&P 500 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the S&P 500 Index on September 30, 2002 and held through September 30, 2012. The S&P 500 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[12]

Letter from the Manager

September 30, 2012

Fixed Income Fund

Over the past 12-months, Central banks globally continued their response to weak economic news with more “balance sheet expansion” policies in hopes of promoting stronger economic growth. In the U.S., concern over the unemployment rate and potential downside risks to growth prompted the Federal Open Market Committee (FOMC) to institute yet another much anticipated round of Quantitative Easing (QE3). Unlike the first two rounds of QE, this program is open-ended and will further expand the Federal Reserve’s unprecedented $2.9 trillion balance sheet. Policy makers have committed to maintaining low interest rates for an extended period with little concern over potential ramifications.

The FOMC’s “all-in” action is the latest attempt to stimulate economic activity by increasing home sales, creating mortgage refinancing opportunities for homeowners, and inciting a “wealth effect” by reflating risk assets. There is no doubt the monetary actions implemented since the financial crisis began have muted the negative effects of consumer and corporate deleveraging. Evidence also confirms a firming in economic activity that includes better retail sales, auto sales, consumer confidence and stronger consumer spending. There is even encouraging news in the housing sector, as both sales and prices have enjoyed a recent rise, while foreclosures are reported to be “normalizing”. The question is whether extraordinary monetary policy measures alone can create lasting economic growth.

The unemployment rate has remained stubbornly above 8% over the past eleven months having finally moved to 7.8% in September 2012. However, the broader measure of labor that includes people involuntarily working part-time is at 14.7%, illustrating the economic malaise that remains. We would argue the effectiveness of the Fed’s policy tools needs an appropriate fiscal stimulus policy as well to be effective. A responsible resolution for the “Fiscal cliff” issues, including the U.S. government debt ceiling limit and a reasonable long term tax policy, is needed for business leaders. Their confidence level remains low with recent data indicating it is the lowest since 2009, coincidently the end of the last recession. In this environment the market has experienced declining interest rates, with the Treasury 10-Year bond yield falling from 1.92% on September 30, 2011 to 1.63% on September 30, 2012.

With all the uncertainty, the portfolio was managed in a cautious strategy resulting in the Timothy Fixed Income Fund A shares generating a total return of 3.73% over the twelve months ended September 30, 2012, as compared to a 5.16% return for the Barclays Aggregate index benchmark. The portfolio’s above market allocation to investment grade credit benefited performance as corporate bond yield spreads narrowed to Treasury rates. A defensive allocation to Treasury Inflation Protected Securities (TIPS) also aided fund performance as Barclays reported this sector was up 9.1%. However, offsetting these positions was an underweight in bank issues, which was the best performing industry, up 14.2% according to Barclays indices.

We continue to position the portfolio conservatively for the uncertainty of the current market environment. Investment grade corporate bonds are over-weighted to add yield, and our position in TIPS remains near 5%. The portfolio’s Mortgage Backed Securities are in GNMA issues that have a full faith and credit guarantee of the U.S. Treasury and provide an attractive yield.

BARROW, HANLEY, MEWHINNEY & STRAUSS

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. Class A shares performance quoted excludes sales charge.

Timothy Plan Fund Performance

[13]

Fund Performance | Fixed Income

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Fixed Income Fund - Class A (With Sales Charge) | | | | -0.98 | % | | | | 4.25 | % | | | | 3.96 | % | | | | | |

Barclays Capital U.S. Aggregate Bond Index | | | | 5.16 | % | | | | 6.53 | % | | | | 5.32 | % | | | | | |

Timothy Fixed Income Fund - Class C * | | | | 2.88 | % | | | | 4.44 | % | | | | 3.37 | % | | | | (a) | |

Barclays Capital U.S. Aggregate Bond Index | | | | 5.16 | % | | | | 6.53 | % | | | | 5.40 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

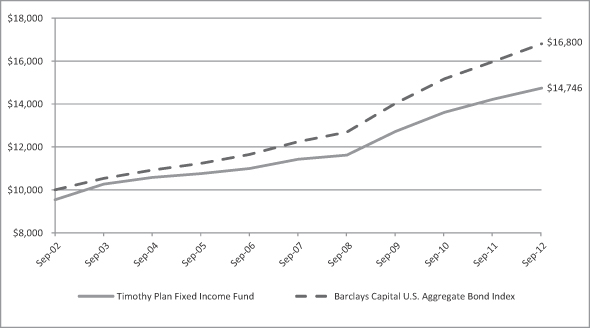

Timothy Plan Fixed Income Fund vs. Barclays Capital U.S. Aggregate Bond Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Barclays Capital U.S. Aggregate Bond Index on September 30, 2002 and held through September 30, 2012. The Barclays Capital U.S. Aggregate Bond Index is a widely recognized, unmanaged index of bond prices. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[14]

Letter from the Manager

September 30, 2012

High Yield Bond Fund

Continuing evidence of a slowing U.S. economy and a faltering global recovery continued to drive Central Banks globally to enact unprecedented expansionary monetary policies over the past 12 months. In the U.S., concern over the unemployment rate and realization of potential downside risks to growth prompted the Federal Open Market Committee (FOMC) to institute yet another much anticipated round of Quantitative Easing (QE3). Unlike the first two rounds of QE, this program is open-ended and will further expand the Federal Reserve’s unprecedented $2.9 trillion balance sheet. Policy makers have committed to maintaining low interest rates for an extended period with no concern over potential ramifications.

The FOMC’s “all-in” action is the latest attempt to stimulate economic activity by increasing home sales, creating mortgage refinancing opportunities for homeowners, and inciting a “wealth effect” by reflating risk assets. There is no doubt the monetary actions implemented since the financial crisis began have muted the negative effects of consumer and corporate deleveraging. Evidence also confirms a firming in economic activity that includes better retail sales, auto sales, consumer confidence and stronger consumer spending. The extended period of low interest rate policies by the Federal Reserve has created significant demand for income and increased the appetite for risk assets including High Yield (HY) bonds. For the first 9 months in 2012, inflows into HY mutual funds stood at $35.4 billion, setting an all-time record. The investor demand for yield helped drive the Barclays Ba/B High Yield Index yield spread down 238 basis points over the one-year period ended September 2012, leading to a strong total return.

Timothy High Yield Fund A shares returned 15.17% compared to 18.19% for the Barclays Ba/B High Yield Index benchmark for the 12 month period ended September 30, 2012. According to Barclays, the top performing sector in HY was Financials, especially Banks, while the worst performers in 2012 through September were Basic Industry and Energy. The 12 month performance lag for the Fund’s A shares was primarily a result of the 2Q12 return of -0.01%, as cyclical holdings and especially energy were weak performers. A contributing factor to this result was the bond market’s reaction to increased evidence of a global slowdown, especially in China. Also, the portfolio was underweight in the top performing financial sector. However, the portfolio rebounded during 3Q12 as the Fund’s A shares were up 4.94% versus 4.40% for the Barclays Ba/B High Yield Index, as concerns about a global recession faded allowing a recovery in cyclical holdings.

Current credit fundamentals remain supportive of the HY market. For example, Fitch reports HY default rates of only 2.2% which is about half of their long term average rate. The portfolio focuses on the higher rated portion of the HY market and has an overweight in the Utility sector and an underweight in Financials. Security selection for the portfolio focuses on a company’s sources and uses of cash, access to liquidity, debt maturity schedule and sustainable cash flow.

BARROW, HANLEY, MEWHINNEY & STRAUSS

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. Class A shares performance quoted excludes sales charge.

Timothy Plan Fund Performance

[15]

Fund Performance | High Yield Bond

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | Average

Annual Return

Since Inception (a) |

Timothy High Yield Bond Fund - Class A (With Sales Charge) | | | | 9.99 | % | | | | 5.41 | % | | | | 4.93 | % |

Barclays Ba/B High Yield Index | | | | 18.19 | % | | | | 8.72 | % | | | | 7.97 | % |

Timothy High Yield Bond Fund - Class C * | | | | 14.33 | % | | | | 5.56 | % | | | | 5.05 | % |

Barclays Capital U.S. Corporate High Yield Bond Index | | | | 18.19 | % | | | | 8.72 | % | | | | 7.97 | % |

| | (a) | For the period May 7, 2007 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

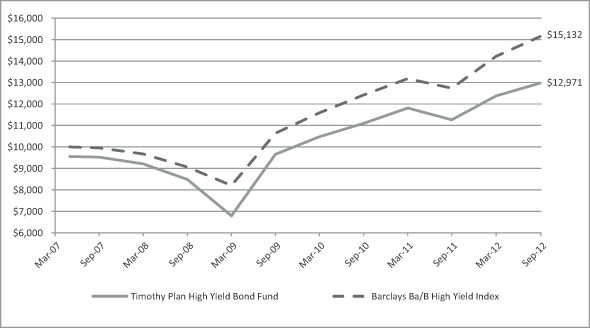

Timothy Plan High Yield Bond Fund vs. Barclays Capital U.S. Corporate High Yield Bond Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Barclays Capital U.S. Corporate High Yield Bond Index on May 7, 2007 and held through September 30, 2012. The Barclays Capital U.S. Corporate High Yield Bond Index is a widely recognized unmanaged index of non-investment grade, fixed rate, taxable corporate bonds. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[16]

Letter from the Manager

September 30, 2012

Israel Common Values Fund

The global backdrop of slowing economic growth across the world has affected global trade and henceforth reduced market expectations for GDP growth in Israel. The latest Bloomberg economist’s consensus estimates less than 3% GDP growth for Israel in 2012 then bouncing back above 3% in 2013 after two strong years of greater than 4% growth in 2010 and 2011. Even though growth has slowed somewhat, Israel appears to be weathering the storm much better than its developed market peers. Inflation is under control with most estimates hovering around 2% for both 2012 and 2013.

With the Arab Winter and Spring revolts and Iran’s nuclear ambitions, turmoil in the region hurt equity performance in the beginning of 2012. With the Muslim Brotherhood now in control of Egypt and with outright civil war in Syria, the Israeli equity market was soft for most of the beginning of 2012 before bouncing back strongly after aggressive central bank monetary policies across the world. Valuations remain reasonable and expectations appear modest for corporate results in the coming year.

The Timothy Plan Israel Common Values Fund performed well for the year in absolute terms and relative to the Israel TA-100 index mostly on the back of strong sector allocation in Telecom Services, Financials, and Information Technology and good stock selection in Telecom Services, Energy, and Industrials. Although the Fund benefited from larger than normal cash weightings in its first few months since inception, as the year progressed and markets rallied, cash was a drag to performance. The largest negative effect on the Fund’s performance was not owning enough of the big winners relative to their weight in the index as well as the significant underweight in the Health Care sector as the two largest firms there performed well.

The Fund has shifted to an overweight stance in Financials given better valuations and prospects there while maintaining the overweight to Consumer Staples and Information Technology. The two significant underweights remain Telecom Services where we believe competitive forces keep pressures on earnings in the sector while the large underweight in Health Care will likely remain for the foreseeable future as the two largest Health Care stocks in the index do not pass the Timothy screens. The Fund maintains its focus on directing its efforts in identifying those companies with the best prospects and that champion the entrepreneurial and innovative spirit of Israel.

EAGLE GLOBAL ADVISORS, LLC

Timothy Plan Fund Performance

[17]

Fund Performance | Israel Common Values

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | Average

Annual Return

Since Inception (a) |

Timothy Israel Common Values Fund - Class A (With Sales Charge) | | | | N/A | | | | | N/A | | | | | -3.78 | % |

Israel TA 100 Index | | | | N/A | | | | | N/A | | | | | 7.46 | % |

Timothy Israel Common Values Fund - Class C * | | | | N/A | | | | | N/A | | | | | 1.00 | % |

Israel TA 100 Index | | | | N/A | | | | | N/A | | | | | 7.46 | % |

| | (a) | For the period October 12, 2011 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

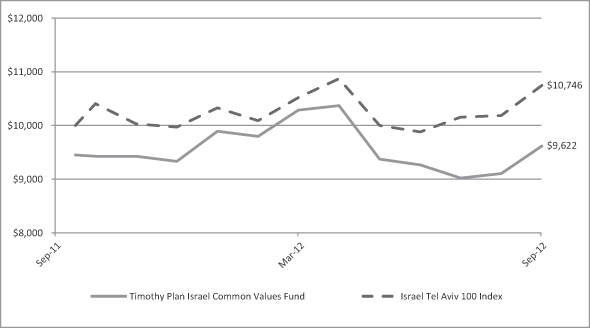

Timothy Israel Common Values Fund vs. Israel Tel Aviv 100 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Israel TA 100 Index on October 12, 2011 and held through September 30, 2012. The Israel Tel Aviv 100 Index is an unmanaged index of equity prices representing the 100 most highly capitalized companies listed on the Tel Aviv Stock Exchange. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[18]

Letter from the Manager

September 30, 2012

Defensive Strategies Fund

Dear Shareholder,

The Defensive Strategies Fund has been designed and managed to do what its name implies, i.e. hedge against a possible scenario of hyper-inflation which could result from our nation’s leadership’s proven unwillingness to address our core problems of too much spending, too much taxation and too many onerous government regulations. If we elect a real reform government in the November, 2012 elections, we believe many of these problems could be on a path to being solved. We have, therefore, built in the flexibility to either adjust to a possible risk of extreme deflation with the ability to convert our inflation sensitive assets to cash and fixed income securities that should perform well during a deflationary environment or to a more normal, traditional investment strategy. As I stated in last year’s report, although we will do our very best to be successful, we cannot guarantee results in any of these scenarios.

While no one can predict future events, as I stated in my President’s letter, I am confident of a couple of things:

| | • | | If the November, 2012 elections result in replacing a number of liberal members of Congress (as well as the current Administration) with common sense conservatives, the capital markets could react very favorably, and |

| | • | | Our sub-advisors (i.e. money management firms that manage the various sleeves of this Fund) are, in our opinion, among the best in the industry and they each continue to honor our overall policy that they manage their respective Fund sleeve both in accordance with our screening restrictions and with a conservative bias. |

Finally, I would once again like to thank you for your moral convictions that led you to become part of the Timothy Plan Family.

Yours in Christ,

ARTHUR D. ALLY

Fund Advisor

Timothy Plan Fund Performance

[19]

Fund Performance | Defensive Strategies

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | Average

Annual Return

Since Inception (a) |

Timothy Defensive Strategies Fund - Class A (With Sales Charge) | | | | 8.52 | % | | | | N/A | | | | | 8.74 | % |

Dow Jones Moderately Conservative U.S. Portfolio Index | | | | 19.24 | % | | | | N/A | | | | | 11.94 | % |

Timothy Defensive Strategies Fund - Class C * | | | | 13.91 | % | | | | N/A | | | | | 10.07 | % |

Dow Jones Moderately Conservative U.S. Portfolio Index | | | | 19.24 | % | | | | N/A | | | | | 11.94 | % |

| | (a) | For the period November 4, 2009 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

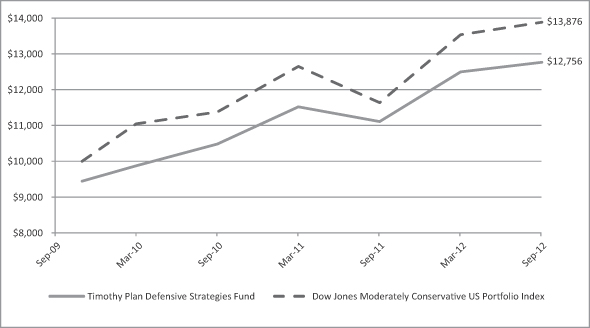

Timothy Plan Defensive Strategies Fund vs. Dow Jones Moderately Conservative U.S. Portfolio Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Dow Jones Moderately Conservative U.S. Portfolio Index on November 4, 2009 and held through September 30, 2012. The Dow Jones Moderately Conservative U.S. Portfolio Index is a widely recognized unmanaged index of stocks, bonds and cash. Performance figures include the change in value of the asset classes in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[20]

Letter from the Manager

September 30, 2012

Strategic Growth Fund

Dear Strategic Growth Fund Shareholder:

The Timothy Plan Strategic Growth Fund is simply an asset allocation fund that invests in a number of Timothy Plan underlying funds. Although the allocation percentages will vary somewhat from time to time as a result of changing economic conditions, the allocation at September 30, 2012 was as follows:

| | | | | | | | | | |

• Large/Mid Cap Growth Fund | | | (16.45%) | | | • Small Cap Value Fund | | | ( 6.73%) | |

• Large/Mid Cap Value Fund | | | (16.53%) | | | • Aggressive Growth Fund | | | (6.25%) | |

• International Fund | | | (15.60%) | | | • High Yield Bond Fund | | | (12.85%) | |

• Defensive Strategies Fund | | | (17.16%) | | | • Israel Common Values Fund | | | (5.56%) | |

• Cash | | | (2.87%) | | | | | | | |

I am pleased to report that performance was, in our opinion, quite respectable over the past twelve months and was reasonably comparable to the Fund’s market benchmark - the Dow Jones Global Moderately Aggressive Portfolio Index. As we manage this Fund, we plan to continue to attempt to adjust to (what could be) rapidly changing economic conditions.

We realize that the volatility and uncertainty of the markets over the past twelve months may have been unsettling for many investors; however as a group, although our sub-advisors expect this pattern to continue into 2013, they also expect a somewhat upward bias with respect to performance in our underlying funds.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is that every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment with which you can feel comfortable.

Sincerely,

ARTHUR D. ALLY,

President

Timothy Plan Fund Performance

[21]

Fund Performance | Strategic Growth

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Strategic Growth Fund - Class A (With Sales Charge) | | | | 12.22 | % | | | | -3.23 | % | | | | 4.92 | % | | | | | |

Dow Jones Global Moderately Aggressive Portfolio Index | | | | 19.63 | % | | | | 1.78 | % | | | | 9.63 | % | | | | | |

Timothy Strategic Growth Fund - Class C * | | | | 18.04 | % | | | | -2.90 | % | | | | 2.06 | % | | | | (a) | |

Dow Jones Global Moderately Aggressive Portfolio Index | | | | 19.63 | % | | | | 1.78 | % | | | | 6.46 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

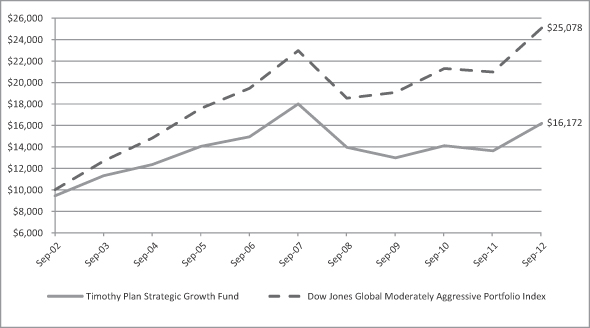

Timothy Plan Strategic Growth Fund vs. Dow Jones Global Moderately Aggressive Portfolio Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Dow Jones Global Moderately Aggressive Portfolio Index on September 30, 2002 and held through September 30, 2012. The Dow Jones Global Moderately Aggressive Portfolio Index is a widely recognized index that measures global stocks, bonds and cash which are in turn represented by multiple sub-indexes. Performance figures include the change in value of the investments in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[22]

Letter from the Manager

September 30, 2012

Conservative Growth Fund

Dear Conservative Growth Fund Shareholder:

The Timothy Plan Conservative Growth Fund is simply an asset allocation fund that invests in a number of Timothy Plan underlying funds. Although the allocation percentages will vary slightly from time to time as a result of changing economic conditions, the allocation at September 30, 2012 was as follows:

| | | | | | | | | | |

• Large/Mid Cap Growth Fund | | | (11.67%) | | | • Small Cap Value Fund | | | (5.21%) | |

• Large/Mid Cap Value Fund | | | (14.22%) | | | • Aggressive Growth Fund | | | (2.36%) | |

• International Fund | | | (5.42%) | | | • High Yield Bond Fund | | | (8.53%) | |

• Defensive Strategies Fund | | | (18.09%) | | | • Fixed Income Fund | | | (29.27%) | |

• Israel Common Values Fund | | | (4.03%) | | | • Cash | | | (1.20%) | |

I am pleased to report that performance was, in our opinion, quite respectable over the past twelve months and reasonably comparable to the Fund’s market benchmark - the Dow Jones Global Moderate Portfolio Index. We plan to continue to manage this Fund conservatively as we attempt to adjust to (what could be) rapidly changing economic conditions.

We realize that the volatility and uncertainty of the markets over the past twelve months may have been unsettling for many investors; however as a group, although our sub-advisors expect this pattern to continue into 2013, they also expect a somewhat upward bias with respect to performance in our underlying Funds.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is that every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment with which you can feel comfortable.

Sincerely,

ARTHUR D. ALLY,

President

Timothy Plan Fund Performance

[23]

Fund Performance | Conservative Growth

As of September 30, 2012 - (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Fund/Index | | 1 Year

Total Return | | 5 Year

Average

Annual Return | | 10 Year

Average

Annual Return | | |

Timothy Conservative Growth Fund - Class A (With Sales Charge) | | | | 7.02 | % | | | | -0.41 | % | | | | 5.12 | % | | | | | |

Dow Jones Global Moderate Portfolio Index | | | | 15.58 | % | | | | 3.02 | % | | | | 8.67 | % | | | | | |

Timothy Conservative Growth Fund - Class C * | | | | 12.50 | % | | | | 0.01 | % | | | | 3.12 | % | | | | (a) | |

Dow Jones Global Moderate Portfolio Index | | | | 15.58 | % | | | | 3.02 | % | | | | 6.16 | % | | | | (a) | |

| | (a) | For the period February 3, 2004 (commencement of investment in accordance with objective) to September 30, 2012. |

| | * | With Maximum Deferred Sales Charge |

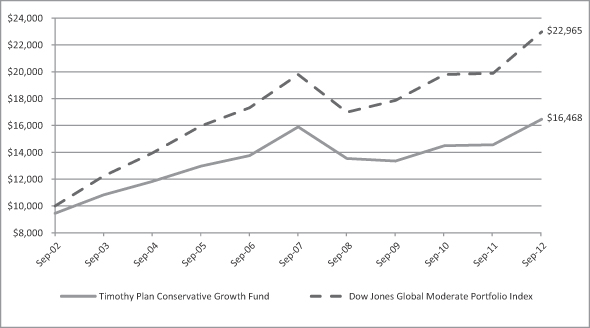

Timothy Plan Conservative Growth Fund vs. Dow Jones Global Moderate Portfolio Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Dow Jones Global Moderate Portfolio Index on September 30, 2002 and held through September 30, 2012. The Dow Jones Global Moderate Portfolio Index is a widely recognized index that measures global stocks, bonds and cash which are in turn represented by multiple sub-indexes. Performance figures include the change in value of the investments in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

[24]

Fund Profile

As of September 30, 2012 - (Unaudited)

Aggressive Growth Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Genesse & Wyoming, Inc. | | | 2.45% | |

Casey’s General Stores, Inc. | | | 2.05% | |

FleetCor Technologies, Inc. | | | 2.00% | |

Dollar General Corp. | | | 1.95% | |

Ross Stores, Inc. | | | 1.91% | |

XL Group PLC | | | 1.86% | |

Sally Beauty Holdings, Inc. | | | 1.78% | |

Fiserv, Inc. | | | 1.65% | |

Group 1 Automotive, Inc. | | | 1.55% | |

American Campus Communities, Inc. | | | 1.52% | |

| | | | |

| | | 18.72% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Retail | | | 19.10% | |

Information Technology | | | 13.50% | |

Financial/Investment Services | | | 8.90% | |

Healthcare | | | 6.20% | |

Banks | | | 5.80% | |

Oil & Natural Gas | | | 5.30% | |

Transportation | | | 3.70% | |

Electronics | | | 2.70% | |

Pharmaceuticals | | | 2.50% | |

Commercial Services | | | 2.40% | |

Other Assets Less Liabilities | | | 29.90% | |

| | | | |

| | | 100.00% | |

| | | | |

International Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Henkel AG & Co. (ADR) | | | 5.11% | |

Singapore Telecommunications, Ltd. (ADR) | | | 4.71% | |

Fresenius Medical Care AG & Co. (ADR) | | | 4.21% | |

Smith & Nephew PLC (ADR) | | | 3.68% | |

WM Morrison Supermarkets PLC (ADR) | | | 2.92% | |

DBS Group Holdings, Ltd. (ADR) | | | 2.92% | |

Agrium, Inc. | | | 2.80% | |

Lukoil OAO (ADR) | | | 2.74% | |

Zurich Insurance Group AG | | | 2.63% | |

Hitachi, Ltd. (ADR) | | | 2.35% | |

| | | | |

| | | 34.07% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Chemicals | | | 10.10% | |

Banks | | | 10.00% | |

Telecommunications | | | 9.90% | |

Oil & Natural Gas | | | 8.60% | |

Healthcare | | | 7.90% | |

Industrials | | | 5.00% | |

Minerals & Mining | | | 4.40% | |

Automotive | | | 4.40% | |

Consumer Goods | | | 4.30% | |

Food | | | 3.70% | |

Other Assets Less Liabilities | | | 31.70% | |

| | | | |

| | | 100.00% | |

| | | | |

Large/Mid Cap Growth Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Exxon Mobil Corp. | | | 4.76% | |

Autozone, Inc. | | | 3.25% | |

Western Union Co. | | | 2.93% | |

Occidental Petroleum Corp. | | | 2.81% | |

McCormick & Co., Inc. | | | 2.71% | |

Amphenol Corp. - Class A | | | 2.58% | |

ACE, Ltd. | | | 2.47% | |

Covidien PLC | | | 2.39% | |

Thermo Fisher Scientific, Inc. | | | 2.35% | |

Amerisource Bergen Corp. | | | 2.04% | |

| | | | |

| | | 28.29% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Retail | | | 12.90% | |

Oil & Natural Gas | | | 10.20% | |

Electronics | | | 8.80% | |

Healthcare | | | 8.80% | |

Financial/Investment Services | | | 6.40% | |

Consumer Goods | | | 5.10% | |

Information Technology | | | 5.00% | |

Banks | | | 3.90% | |

Insurance | | | 3.70% | |

Commercial Services | | | 3.70% | |

Other Assets Less Liabilities | | | 31.50% | |

| | | | |

| | | 100.00% | |

| | | | |

[25]

Fund Profile

As of September 30, 2012 - (Unaudited)

Small Cap Value Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Beacon Roofing Supply, Inc. | | | 2.43% | |

A.O. Smith Corp. | | | 2.40% | |

Orthofix International NV | | | 2.32% | |

J2 Global, Inc. | | | 2.25% | |

KapStone Paper and Packaging Corp. | | | 2.25% | |

Moog, Inc. | | | 2.23% | |

Children’s Place Retail Stores | | | 2.22% | |

Wolverine World Wide, Inc. | | | 2.21% | |

AMERISAFE, Inc. | | | 2.21% | |

NorthWestern Corp. | | | 2.20% | |

| | | | |

| | | 22.72% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Banks | | | 16.20% | |

Industrials | | | 8.80% | |

REITs | | | 8.80% | |

Insurance | | | 6.40% | |

Electric Power | | | 5.50% | |

Oil & Natural Gas | | | 5.30% | |

Healthcare | | | 4.50% | |

Computers | | | 4.30% | |

Electric & Equipment | | | 4.30% | |

Transportation | | | 4.30% | |

Other Assets Less Liabilities | | | 31.60% | |

| | | | |

| | | 100.00% | |

| | | | |

Large/Mid Cap Value Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Covidien PLC | | | 3.25% | |

Exxon Mobil Corp. | | | 3.10% | |

Union Pacific Corp. | | | 2.82% | |

Flowserve Corp. | | | 2.69% | |

ACE, Ltd. | | | 2.56% | |

Invesco, Ltd. | | | 2.53% | |

Emerson Electric Co. | | | 2.51% | |

Public Storage, Inc. | | | 2.46% | |

EQT Corp. | | | 2.40% | |

Arch Capital Group, Ltd. | | | 2.36% | |

| | | | |

| | | 26.68% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Oil & Natural Gas | | | 20.00% | |

Healthcare | | | 12.90% | |

Insurance | | | 9.00% | |

Consumer Goods | | | 8.70% | |

Financial & Investment Services | | | 6.60% | |

REITs | | | 6.50% | |

Electric Power | | | 5.90% | |

Retail | | | 4.60% | |

Information Technology | | | 4.20% | |

Industrials | | | 3.70% | |

Other Assets Less Liabilities | | | 17.90% | |

| | | | |

| | | 100.00% | |

| | | | |

Fixed Income Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Federal Farm Credit Bank, 5.125%, 8/25/2016 | | | 3.51% | |

GNMA Pool 4520, 5.00%, 8/20/2039 | | | 2.50% | |

GNMA Pool 4947, 5.00%, 2/20/2041 | | | 2.73% | |

GNMA Pool 701961, 4.50%, 6/15/2039 | | | 3.78% | |

GNMA Pool 783060, 4.00%, 8/15/2040 | | | 2.27% | |

GNMA Pool MA0155, 4.00%, 6/20/2042 | | | 4.81% | |

TIPS, 2.50%, 7/15/2016 | | | 2.36% | |

U.S Treasury Bond, 3.875%, 5/15/2018 | | | 2.80% | |

U.S Treasury Note, 3.125%, 5/15/2021 | | | 6.83% | |

U.S. Treasury Bond, 4.50%, 2/15/2036 | | | 4.79% | |

| | | | |

| | | 36.38% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Corporate Bonds | | | 33.60% | |

Government Mortgage-Backed Securities | | | 29.50% | |

Government Notes & Bonds | | | 27.20% | |

TIPS | | | 4.30% | |

Other Assets Less Liabilities | | | 5.40% | |

| | | | |

| | | 100.00% | |

| | | | |

[26]

Fund Profile

As of September 30, 2012 - (Unaudited)

High Yield Bond Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Genesis Energy LP, 7.875%, 12/15/2018 | | | 2.28% | |

Energy Transfer Equity LP, 7.50%, 10/15/2020 | | | 1.63% | |

LyondellBasell Industries NV, 5.75%, 4/15/2024 | | | 1.63% | |

United Rentals North America, Inc., 9.25%, 12/15/2019 | | | 1.61% | |

Iron Mountain, 7.75%, 10/01/2019 | | | 1.61% | |

Schaeffler Finance BV, 8.50%, 2/15/2019 | | | 1.60% | |

Cloud Peak Energy Resources LLC, 8.50%, 12/15/2019 | | | 1.58% | |

Omnicare, Inc., 7.75%, 6/01/2020 | | | 1.58% | |

Targa Resources Partners LP, 7.875%, 10/15/2018 | | | 1.57% | |

Masco Corp., 5.95%, 3/15/2022 | | | 1.56% | |

| | | | |

| | | 16.65% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Corporate Bonds | | | 95.00% | |

Other Assets Less Liabilities | | | 5.00% | |

| | | | |

| | | 100.00% | |

| | | | |

Israel Common Values Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Mellanox Technologies, Ltd. | | | 4.95% | |

Noble Energy, Inc. | | | 3.39% | |

Israel Chemicals, Ltd. | | | 3.31% | |

Elbit Systems, Ltd. | | | 3.11% | |

The Israel Chemicals, Ltd. | | | 3.09% | |

Rami Levi Chain Stores | | | 3.06% | |

Allot Communications, Ltd. | | | 3.03% | |

Bank Hapoalim BM | | | 3.03% | |

Bayside Land Corp., Ltd. | | | 2.99% | |

Gazit-Globe, Ltd. | | | 2.92% | |

| | | | |

| | | 32.88% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Real Estate | | | 13.70% | |

Telecommunications | | | 11.20% | |

Oil & Natural Gas | | | 8.80% | |

Banks | | | 7.70% | |

Software | | | 7.60% | |

Semiconductors | | | 6.20% | |

Chemicals | | | 6.00% | |

Food | | | 5.60% | |

Healthcare Products | | | 4.30% | |

Biotechnology | | | 3.80% | |

Other Assets Less Liabilities | | | 25.10% | |

| | | | |

| | | 100.00% | |

| | | | |

[27]

Fund Profile

As of September 30, 2012 - (Unaudited)

Defensive Strategies Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

SPDR Gold Shares | | | 6.69% | |

Exxon Mobil Corp. | | | 3.53% | |

TIPS, 1.75%, 1/15/2028 | | | 3.17% | |

PowerShares DB Agriculture Fund | | | 3.16% | |

TIPS, 2.00%, 1/15/2014 | | | 3.15% | |

Potash Corp. of Saskatchewan, Inc. | | | 3.04% | |

TIPS, 2.125%, 1/15/2019 | | | 2.85% | |

Syngenta AG (ADR) | | | 2.78% | |

TIPS, 1.625%, 1/15/2015 | | | 2.57% | |

TIPS, 1.125%, 1/15/2021 | | | 2.51% | |

| | | | |

| | | 33.45% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

TIPS | | | 26.60% | |

Exchange Traded Funds | | | 17.10% | |

REITs | | | 14.80% | |

Chemicals | | | 12.40% | |

Oil & Gas | | | 10.00% | |

Mining | | | 6.30% | |

Government Mortgage-Backed Securities | | | 2.50% | |

Oil & Gas Services | | | 0.90% | |

Iron/Steel | | | 0.70% | |

Machinery | | | 0.40% | |

Other Assets Less Liabilities | | | 8.30% | |

| | | | |

| | | 100.00% | |

| | | | |

Strategic Growth Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Timothy Plan - Defensive Strategies Fund | | | 17.16% | |

Timothy Plan - Large/Mid Cap Value Fund | | | 16.53% | |

Timothy Plan - Large/Mid Cap Growth Fund | | | 16.45% | |

Timothy Plan - International Fund | | | 15.60% | |

Timothy Plan - High Yield Bond Fund | | | 12.85% | |

Timothy Plan - Small Cap Value Fund | | | 6.73% | |

Timothy Plan - Aggressive Growth Fund | | | 6.25% | |

Timothy Plan - Israel Common Values Fund | | | 5.56% | |

| | | | |

| | | 97.13% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Mutual Funds | | | 97.13% | |

Other Assets Less Liabilities | | | 2.87% | |

| | | | |

| | | 100.00% | |

| | | | |

Conservative Growth Fund

| | | | |

| Top Ten Holdings | | | |

| (% of Net Assets) | | | |

Timothy Plan - Fixed Income Fund | | | 29.27% | |

Timothy Plan - Defensive Strategies Fund | | | 18.09% | |

Timothy Plan - Large/Mid Cap Value Fund | | | 14.22% | |

Timothy Plan - Large/Mid Cap Growth Fund | | | 11.67% | |

Timothy Plan - High Yield Bond Fund | | | 8.53% | |

Timothy Plan - International Fund | | | 5.42% | |

Timothy Plan - Small Cap Value Fund | | | 5.21% | |

Timothy Plan - Israel Common Values Fund | | | 4.03% | |

Timothy Plan - Aggressive Growth Fund | | | 2.36% | |

| | | | |

| | | 98.80% | |

| | | | |

| | | | |

| Top Ten Industries | | | |

| (% of Net Assets) | | | |

Mutual Funds | | | 98.80% | |

Other Assets Less Liabilities | | | 1.20% | |

| | | | |

| | | 100.00% | |

| | | | |

[28]

| | |

| Timothy Plan Family of Funds | | Aggressive Growth |

| | |

Schedule of Investments | | As of September 30, 2012 |

| | | | | | | | | | | | |

| Common Stocks – 94.3% | | | | Shares | | Fair

Value |

AEROSPACE/DEFENSE – 0.7% | | | | | | | | | | | | |

BE Aerospace, Inc. | | * | | | | 2,840 | | | | $ | 119,564 | |

| | | | | | | | | | | | |

AUTO REPAIR – 0.7% | | | | | | | | | | | | |

Monro Muffler Brake, Inc. | | | | | | 3,520 | | | | | 123,869 | |

| | | | | | | | | | | | |

APPAREL – 1.7% | | | | | | | | | | | | |

Carter’s, Inc. | | * | | | | 2,300 | | | | | 123,832 | |

Crocs, Inc. | | * | | | | 2,530 | | | | | 41,011 | |

Oxford Industries, Inc. | | | | | | 2,150 | | | | | 121,367 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 286,210 | |

| | | | | | | | | | | | |

BANKS – 5.8% | | | | | | | | | | | | |

CIT Group, Inc. | | * | | | | 5,675 | | | | | 223,538 | |

Cardinal Financial Corp. | | | | | | 11,905 | | | | | 170,241 | |

Cathay General Bancorp | | | | | | 12,750 | | | | | 220,065 | |

First Horizon National Corp. | | | | | | 5,800 | | | | | 55,854 | |

State Bank Financial Corp. | | | | | | 2,400 | | | | | 39,576 | |

TCF Financial Corp. | | | | | | 5,650 | | | | | 67,461 | |

Zions Bancorp | | | | | | 8,895 | | | | | 183,726 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 960,461 | |

| | | | | | | | | | | | |

BIOTECHNOLOGY – 0.6% | | | | | | | | | | | | |

Dynavax Technologies Corp. | | * | | | | 10,330 | | | | | 49,171 | |

Incyte Corp, Ltd. | | * | | | | 3,155 | | | | | 56,948 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 106,119 | |

| | | | | | | | | | | | |

CHEMICALS – 1.0% | | | | | | | | | | | | |

Ashland, Inc. | | | | | | 2,250 | | | | | 161,100 | |

| | | | | | | | | | | | |

COMMERCIAL SERVICES – 2.4% | | | | | | | | | | | | |

Team, Inc. | | * | | | | 3,906 | | | | | 124,406 | |

Verisk Analytics, Inc. | | * | | | | 2,960 | | | | | 140,926 | |

WNS Holdings, Ltd. | | * | | | | 12,365 | | | | | 126,618 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 391,950 | |

| | | | | | | | | | | | |

CONSUMER GOODS – 0.9% | | | | | | | | | | | | |

Brunswick Corp. | | | | | | 6,910 | | | | | 156,373 | |

| | | | | | | | | | | | |

DISTRIBUTION/WHOLESALE – 1.9% | | | | | | | | | | | | |

MWI Veterinary Supply, Inc. | | * | | | | 570 | | | | | 60,808 | |

Wesco International, Inc. | | * | | | | 4,360 | | | | | 249,392 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 310,200 | |

| | | | | | | | | | | | |

ELECTRICAL – 1.6% | | | | | | | | | | | | |

Hubbell, Inc. | | | | | | 775 | | | | | 62,573 | |

Universal Display Corp. | | * | | | | 5,700 | | | | | 195,966 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 258,539 | |

| | | | | | | | | | | | |

ELECTRONICS – 2.7% | | | | | | | | | | | | |

Amphenol Corp. | | | | | | 2,850 | | | | | 167,808 | |

Trimble Navigation, Ltd. | | * | | | | 2,830 | | | | | 134,878 | |

Waters Corp. | | * | | | | 1,675 | | | | | 139,578 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 442,264 | |

| | | | | | | | | | | | |

ENGINEERING & CONSTRUCTION – 0.5% | | | | | | | | | | | | |

Dycom Industries, Inc. | | * | | | | 5,740 | | | | | 82,541 | |

| | | | | | | | | | | | |

ENTERTAINMENT – 1.4% | | | | | | | | | | | | |

Six Flags Entertainment Corp. | | | | | | 3,895 | | | | | 229,026 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Common Stocks (Continued) | | | | Shares | | Fair

Value |

FINANCIAL/INVESTMENT SERVICES – 8.9% | | | | | | | | | | | | |

Affiliated Managers Group, Inc. | | * | | | | 1,440 | | | | $ | 177,120 | |

Cardtronics, Inc. | | * | | | | 3,570 | | | | | 106,315 | |

Discover Financial Services | | | | | | 3,769 | | | | | 149,742 | |

FleetCor Technologies, Inc. | | * | | | | 7,426 | | | | | 332,685 | |

IntercontinentalExchange, Inc. | | * | | | | 715 | | | | | 95,388 | |

KBW, Inc. | | | | | | 3,625 | | | | | 59,704 | |

Ocwen Financial Corp. | | * | | | | 7,225 | | | | | 198,037 | |

Validus Holdings, Ltd. | | | | | | 1,225 | | | | | 41,540 | |

XL Group PLC | | | | | | 12,870 | | | | | 309,266 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,469,797 | |

| | | | | | | | | | | | |

FOOD – 1.5% | | | | | | | | | | | | |

Hain Celestial Group, Inc. | | * | | | | 1,900 | | | | | 119,700 | |

McCormick & Co., Inc. | | | | | | 2,175 | | | | | 134,937 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 254,637 | |

| | | | | | | | | | | | |

HEALTHCARE – 6.2% | | | | | | | | | | | | |

Cepheid, Inc. | | * | | | | 475 | | | | | 16,392 | |

Cyberonics, Inc. | | * | | | | 1,995 | | | | | 104,578 | |

Insulet Corp. | | * | | | | 1,710 | | | | | 36,902 | |

Intuitive Surgical, Inc. | | * | | | | 155 | | | | | 76,823 | |

IPC The Hospitalist Co. | | * | | | | 1,880 | | | | | 85,916 | |

NuVasive, Inc. | | * | | | | 3,725 | | | | | 85,340 | |

NxStage Medical, Inc. | | * | | | | 3,045 | | | | | 40,224 | |

Sirona Dental Systems, Inc. | | * | | | | 1,552 | | | | | 88,402 | |

Thoratec Corp. | | * | | | | 2,650 | | | | | 91,690 | |

Tornier NV | | * | | | | 6,200 | | | | | 117,490 | |

Trinity Biotech PLC | | | | | | 1,800 | | | | | 22,626 | |

Volcano Corp. | | * | | | | 5,950 | | | | | 169,991 | |

WellCare Health Plans, Inc. | | * | | | | 1,640 | | | | | 92,742 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,029,116 | |

| | | | | | | | | | | | |

HOME BUILDERS – 1.2% | | | | | | | | | | | | |

D R Horton, Inc. | | | | | | 9,660 | | | | | 199,382 | |

| | | | | | | | | | | | |

HOUSEHOLD PRODUCTS – 0.5% | | | | | | | | | | | | |

Tumi Holdings, Inc. | | * | | | | 3,475 | | | | | 81,802 | |

| | | | | | | | | | | | |

INDUSTRIALS/MACHINERY – 2.3% | | | | | | | | | | | | |

Clean Harbors, Inc. | | * | | | | 1,815 | | | | | 88,663 | |

Rush Enterprises, Inc. – Class A | | * | | | | 8,100 | | | | | 156,006 | |

United Rentals, Inc. | | * | | | | 1,935 | | | | | 63,294 | |

Waste Connections, Inc. | | | | | | 2,360 | | | | | 71,390 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 379,353 | |

| | | | | | | | | | | | |

INFORMATION TECHNOLOGY – 13.5% | | | | | | | | | | | | |

Active Network, Inc. | | * | | | | 10,265 | | | | | 128,620 | |

Aspen Technology, Inc. | | * | | | | 7,690 | | | | | 198,710 | |

Citrix Systems, Inc. | | * | | | | 1,200 | | | | | 91,884 | |

Cognizant Technology Solutions Corp. – Class A | | * | | | | 2,285 | | | | | 159,767 | |

F5 Networks, Inc. | | * | | | | 1,150 | | | | | 120,405 | |

Fair Isaac Corp. | | | | | | 3,515 | | | | | 155,574 | |

Fiserv, Inc. | | * | | | | 3,695 | | | | | 273,541 | |

Fortinet, Inc. | | * | | | | 2,160 | | | | | 52,142 | |

Informatica Corp. | | * | | | | 2,925 | | | | | 101,819 | |

Interactive Intelligence Group | | * | | | | 1,910 | | | | | 57,395 | |

| | |

| Timothy Plan Family of Funds | | Aggressive Growth (Continued) |

| | |

Schedule of Investments | | As of September 30, 2012 |

| | | | | | | | | | | | |

| Common Stocks (Continued) | | | | Shares | | Fair

Value |

INFORMATION TECHNOLOGY (continued) | | | | | | | | | | | | |

Manhattan Associates, Inc. | | * | | | | 2,740 | | | | $ | 156,920 | |

MedAssets, Inc. | | * | | | | 7,275 | | | | | 129,495 | |

Parametric Technology Corp. | | * | | | | 6,175 | | | | | 134,615 | |

QLIK Technologies, Inc. | | * | | | | 3,600 | | | | | 80,676 | |

Super Micro Computer, Inc. | | * | | | | 3,950 | | | | | 47,519 | |

Syntel, Inc. | | | | | | 1,110 | | | | | 69,275 | |

Teradata Corp. | | * | | | | 1,935 | | | | | 145,918 | |

Tibco Software, Inc. | | * | | | | 4,285 | | | | | 129,536 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,233,811 | |

| | | | | | | | | | | | |

METAL FABRICATE HARDWARE – 0.4% | | | | | | | | | | | | |

RBC Bearing, Inc. | | * | | | | 1,480 | | | | | 71,188 | |

| | | | | | | | | | | | |

MISCELLANEOUS MANUFACTURING – 2.3% | | | | | | | | | | | | |

Hexcel Corp. | | * | | | | 5,830 | | | | | 140,037 | |

Trimas Corp. | | * | | | | 10,285 | | | | | 247,971 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 388,008 | |

| | | | | | | | | | | | |

MISCELLANEOUS SERVICES – 1.1% | | | | | | | | | | | | |

HFF, Inc. – Class A | | * | | | | 12,600 | | | | | 187,740 | |

| | | | | | | | | | | | |

OIL & NATURAL GAS – 5.3% | | | | | | | | | | | | |

Approach Resources, Inc. | | * | | | | 3,925 | | | | | 118,260 | |

Cabot Oil & Gas Corp. | | | | | | 2,640 | | | | | 118,536 | |

Concho Resources, Inc. | | * | | | | 1,450 | | | | | 137,387 | |

Gulfport Energy Corp. | | * | | | | 1,775 | | | | | 55,487 | |

Kodiak Oil & Gas Corp. | | * | | | | 11,130 | | | | | 104,177 | |

Oil States International | | * | | | | 1,545 | | | | | 122,766 | |

Rex Energy Corp. | | * | | | | 10,949 | | | | | 146,169 | |

Thermon Group Holdings, Inc. | | * | | | | 3,125 | | | | | 78,094 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 880,876 | |

| | | | | | | | | | | | |

PHARMACEUTICALS – 2.5% | | | | | | | | | | | | |

Akorn, Inc. | | * | | | | 9,705 | | | | | 128,300 | |

Catamaran Corp. | | * | | | | 753 | | | | | 73,771 | |

Impax Laboratories, Inc. | | * | | | | 5,480 | | | | | 142,261 | |

Mead Johnson Nutrition Co. | | | | | | 1,000 | | | | | 73,280 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 417,612 | |

| | | | | | | | | | | | |

RETAIL – 19.1% | | | | | | | | | | | | |

Autozone, Inc. | | * | | | | 545 | | | | | 201,470 | |

Bloomin’ Brands, Inc. | | * | | | | 14,230 | | | | | 234,083 | |

Casey’s General Stores, Inc. | | | | | | 5,950 | | | | | 339,983 | |

Cheesecake Factory, Inc. | | | | | | 2,465 | | | | | 88,124 | |

Chico’s FAS, Inc. | | | | | | 4,950 | | | | | 89,645 | |

Dick’s Sporting Goods, Inc. | | | | | | 3,295 | | | | | 170,846 | |

Dollar General Corp. | | * | | | | 6,285 | | | | | 323,929 | |

Domino’s Pizza, Inc. | | | | | | 2,550 | | | | | 96,135 | |

Genesco, Inc. | | * | | | | 1,410 | | | | | 94,089 | |

Group 1 Automotive, Inc. | | | | | | 4,280 | | | | | 257,784 | |

Hibbett Sports, Inc. | | * | | | | 1,855 | | | | | 110,280 | |

| | | | | | | | | | | | |

| Common Stocks (Continued) | | | | Shares | | Fair

Value |

RETAIL (continued) | | | | | | | | | | | | |

Krispy Kreme Doughnuts, Inc. | | * | | | | 22,425 | | | | $ | 177,830 | |

Lululemon Athletica, Inc. | | * | | | | 900 | | | | | 66,546 | |

Panera Bread Co. | | * | | | | 495 | | | | | 84,591 | |

Pier 1 Imports, Inc. | | | | | | 7,070 | | | | | 132,492 | |

Ross Stores, Inc. | | | | | | 4,900 | | | | | 316,540 | |

Sally Beauty Holdings, Inc. | | * | | | | 11,815 | | | | | 296,438 | |

Texas Roadhouse, Inc. | | | | | | 4,950 | | | | | 84,645 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,165,450 | |

| | | | | | | | | | | | |

SEMICONDUCTORS – 2.3% | | | | | | | | | | | | |

Avago Technologies, Ltd. | | | | | | 2,725 | | | | | 95,007 | |

Cavium, Inc. | | * | | | | 2,025 | | | | | 67,493 | |

Ultratech, Inc. | | * | | | | 5,610 | | | | | 176,042 | |

Volterra Semiconductor Corp. | | * | | | | 2,290 | | | | | 50,082 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 388,624 | |

| | | | | | | | | | | | |

TELECOMMUNICATIONS – 1.6% | | | | | | | | | | | | |

Aruba Networks, Inc. | | * | | | | 3,125 | | | | | 70,266 | |

Finisar Corp. | | * | | | | 3,970 | | | | | 56,771 | |

NETGEAR, Inc. | | * | | | | 3,465 | | | | | 132,155 | |

| | | | | | | | | | �� | | |

| | | | | | | | | | | 259,192 | |

| | | | | | | | | | | | |

TRANSPORTATION – 3.7% | | | | | | | | | | | | |

Genesse & Wyoming, Inc. – Class A | | * | | | | 6,085 | | | | | 406,843 | |

Old Dominion Freight Line, Inc. | | * | | | | 7,040 | | | | | 212,326 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 619,169 | |

| | | | | | | | | | | | |

Total Common Stocks

(Cost $14,180,732) | | | | | | | | | | $ | 15,653,973 | |

| | | | | | | | | | | | |

| | | |