UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08228

The Timothy Plan

(Exact name of registrant as specified in charter)

1055 Maitland Center Commons, Maitland, FL 32751

(Address of principal executive offices) (Zip code)

Art Ally, The Timothy Plan

1055 Maitland Center Commons, Maitland, FL 32751

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-846-7526

Date of fiscal year end: 9/30

Date of reporting period: 9/30/14

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Registrant’s audited annual financial reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 are as follows:

Letter from the President

September 30, 2014

Arthur D. Ally

Dear Fellow Shareholder,

As you review the important information that each of our sub-advisors have provided on the following pages, I hope you will share my satisfaction with how all of our funds have performed for our past fiscal year (10-1-13 thru 9-30-14). Of course, as you are no doubt aware, past performance does not guarantee future results.

However as I report each year, although we cannot guarantee, or even predict, future performance, I continue to believe that all of our sub-advisors are among the best in the industry. Additionally, each one continues to honor our policy of investing in strict conformity with our screening restrictions and with conservation of capital a foremost consideration.

Please find each of our sub-advisor’s annual review letters in the pages that follow. Each one discusses their respective Fund’s past performance, the reasons behind that performance, and their economic outlook for the next fiscal year.

Finally, I would once again like to thank you for your moral convictions that led you to becoming part of the Timothy Plan Family.

Yours in Christ,

Arthur D. Ally

President

1

Letter from the Manager

September 30, 2014

Aggressive Growth Fund

The Aggressive Growth Fund Class A advanced 8.2% over the 12 months ending September 30, 2014. This compares to +14.4% for the Russell MidCap Growth Index and +8.1% for the Russell 2500 Growth Index for the same period.

The upward march of the equity markets has been quite remarkable not only for its magnitude, but also for the absence of significant corrections during the climb. Except for the reverberations from the “polar vortex” of last winter, economic growth has accelerated from the “new-normal” +/- 2% to now averaging around +3% (GDP). This step-up in growth, accompanied by unusually-low inflation and contained interest rates, has provided for the “goldilocks” environment that has buoyed stocks. The market has also taken the end of Q.E. in stride and is preparing for the Fed to start raising rates in mid/later 2015. Europe continues to provide angst, as some countries teeter on the verge of recession, and deflation looms as a risk. Between this and China “hard-landing” fears, the U.S. stands out as relatively stable. Corporate profits are strong and balance sheets have rarely been in better shape. Volatility in energy markets and the normalization of interest rates could well provide the script for the year to come.

For the portfolio, there has been no change to our time-tested, bottom up fundamental approach to managing small and mid-cap growth investments, although we have increased our turnover around market rallies and pullbacks. Our commitment to identifying quality investments at a time of unprecedented challenges is unaltered and should be rewarded as leading companies gain market share, protect margins, and manage ample capital for shareholder benefit over time.

Chartwell Investment Partners, Inc.

2

Fund Performance - (Unaudited)

September 30, 2014

Aggressive Growth Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return | | |

Timothy Aggressive Growth Fund - Class A (With Sales Charge) | | 2.31% | | 15.35% | | 7.13% | | |

Russell Mid-Cap Growth Index | | 14.43% | | 17.12% | | 10.24% | | |

Timothy Aggressive Growth Fund - Class C * | | 6.50% | | 15.75% | | 6.96% | | |

Russell Mid-Cap Growth Index | | 14.43% | | 17.12% | | 10.24% | | |

Timothy Aggressive Growth Fund - Class I | �� | 8.43% | | N/A | | 8.65% | | (a) |

Russell Mid-Cap Growth Index | | 14.43% | | 17.12% | | 13.30% | | (a) |

| (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

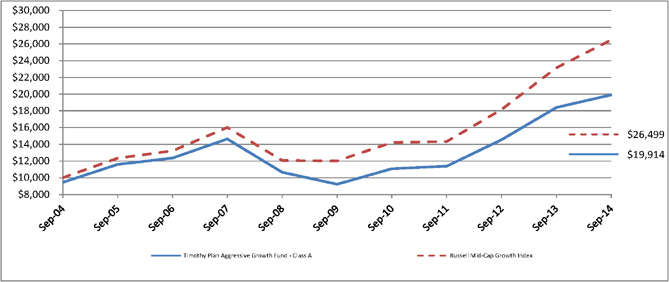

Timothy Plan Aggressive Growth Fund vs. Russell Mid-Cap Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell Mid-Cap Growth Index on September 30, 2004 and held through September 30, 2014. The Russell Mid-Cap Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

3

Letter from the Manager

September 30, 2014

International Fund

The Fund performed well during a difficult period. Weakening economic conditions in Europe and Japan together with increased geopolitical risks induced episodes of sharp swings in equity prices and volatility during this period.

Japan’s consumption tax increase in April led to a sharp decline in economic conditions in the country that proved too difficult to overcome. With a surprise announcement to hold snap elections, PM Shinzo Abe appears to be focused on gaining momentum to delay the next round of tax increases. A sharp acceleration in the expansion of Japan’s quantitative easing that includes buying equity ETFs and REITs led to another sharp depreciation of the Yen against most major currencies. While Japan’s economy failed to gain any momentum, the UK continued to perform well while the Eurozone decelerated throughout the year. With Eurozone inflation at dangerously low levels, economic growth decelerating, and a lack of bank lending, the European Central Bank maintained the foot on the accelerator with new monetary stimulus. With the US ending its QE program while Japan and the Eurozone expand theirs, the US dollar is likely to stay stronger for longer versus these currencies leading to some positive tailwinds for exporters from the Eurozone and Japan.

The good relative performance of the Fund during this period was mostly on the back of very good stock selection but sector allocation was also positive. An underweight to the Materials sector added the most from sector allocation as commodity prices declined markedly during the period on the back of a strong dollar, weaker Chinese demand, and supply increases. The soft commodity prices, the Russian incursion into Ukraine and subsequent Western sanctions as well as mismanagement of Brazil’s economy led to underperformance of the Fund’s positions in the emerging markets. Although, strong stock selection in the Health Care, Consumer Discretionary, IT, Consumer Staples, and Industrials sectors more than offset those headwinds. Of note was the Fund’s overweight to the global auto parts sector at a time of consolidation, margin improvement, and improving auto sales as both Valeo (France) and Magna (Canada) performed well. Other positive areas included good stock selection in Japanese IT with Fujifilm and Hitachi performing well in addition to Health Care where the Fund’s European holdings benefitted from M&A activity in the sector. The best country performance for the Fund relative to the benchmark was in the UK, France, and Canada.

We remain constructive on the attractive valuations of international equities relative to US equities. With the US slowly taking away the QE punch bowl while the Eurozone and Japan add to theirs, volatility is likely to remain for global equities, interest rates, and currencies on the back of uncertain monetary conditions. We are positive on international equities and believe companies outside the US have an opportunity to begin a margin upgrade cycle over the next few years that should benefit equity prices.

Eagle Global Advisors, LLC

4

Fund Performance - (Unaudited)

September 30, 2014

International Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | Average Annual Return Since Inception |

Timothy International Fund - Class A (With Sales Charge) | | (0.99)% | | 3.89% | | (1.01)% | | (a) |

MSCI EAFE Index | | 1.53% | | 3.52% | | (2.56)% | | (a) |

Timothy International Fund - Class C * | | 2.87% | | 4.29% | | (1.03)% | | (a) |

MSCI EAFE Index | | 1.53% | | 3.52% | | (2.56)% | | (a) |

Timothy International Fund - Class I | | 4.85% | | N/A | | 6.15% | | (b) |

MSCI EAFE Index | | 1.53% | | 3.52% | | 5.12% | | (b) |

| (a) | For the period May 3, 2007 (commencement of investment in accordance with objective) to September 30, 2014. |

| (b) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

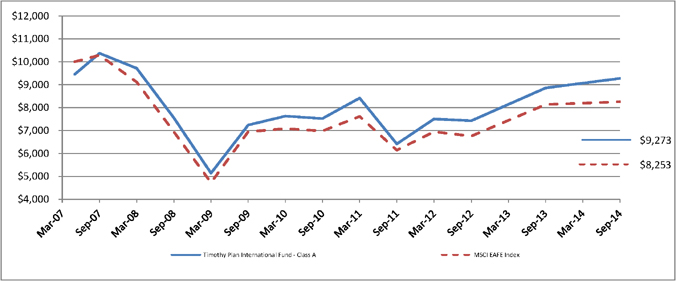

Timothy Plan International Fund vs. MSCI EAFE Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the MSCI EAFE Index on May 3, 2007 and held through September 30, 2014. The MSCI EAFE Index is a widely recognized unmanaged index of equity prices and is representative of equity market performance of developed countries, excluding the U.S. and Canada. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

5

Letter from the Manager

September 30, 2014

Large/Mid Cap Growth Fund

The Large/Mid Cap Growth Fund Class A advanced 14.7% over the last 12 months ending September 30, 2014, while the return of the benchmark, the Russell 1000 Growth Index, was up 19.2% for the same period.

The upward march of the equity markets has been quite remarkable not only for its magnitude, but also for the absence of significant corrections during the climb. Except for the reverberations from the “polar vortex” of last winter, economic growth has accelerated from the “new-normal” +/- 2% to now averaging around +3% (GDP). This step-up in growth, accompanied by unusually-low inflation and contained interest rates, has provided for the “goldilocks” environment that has buoyed stocks. The market has also taken the end of Q.E. in stride and is preparing for the Fed to start raising rates in mid/later 2015. Europe continues to provide angst, as some countries teeter on the verge of recession, and deflation looms as a risk. Between this and China “hard-landing” fears, the U.S. stands out as relatively stable. Corporate profits are strong and balance sheets have rarely been in better shape. Volatility in energy markets and the normalization of interest rates could well provide the script for the year to come.

For the portfolio, there has been no change to our time-tested, bottom up fundamental approach to managing large and mid-cap growth investments, although we have increased our turnover around market rallies and pullbacks. Our commitment to identifying quality investments at a time of unprecedented challenges is unaltered and should be rewarded as leading companies gain market share, protect margins, and manage ample capital for shareholder benefit over time.

Chartwell Investment Partners, Inc.

6

Fund Performance - (Unaudited)

September 30, 2014

Large/Mid Cap Growth Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return |

Timothy Large/Mid Cap Growth Fund - Class A (With Sales Charge) | | 8.08% | | 13.42% | | 5.98% | | |

Russell 1000 Growth Index | | 19.15% | | 16.50% | | 8.94% | | |

Timothy Large/Mid Cap Growth Fund - Class C * | | 12.48% | | 13.83% | | 5.75% | | |

Russell 1000 Growth Index | | 19.15% | | 16.50% | | 8.94% | | |

Timothy Large/Mid Cap Growth Fund - Class I | | 14.66% | | N/A | | 13.17% | | (a) |

Russell 1000 Growth Index | | 19.15% | | 16.50% | | 17.46% | | (a) |

| (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

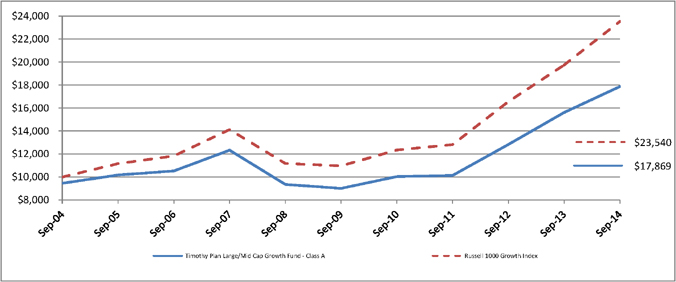

Timothy Plan Large/Mid Cap Growth Fund vs. Russell 1000 Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 1000 Growth Index on September 30, 2004 and held through September 30, 2014. The Russell 1000 Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

7

Letter from the Manager

September 30, 2014

Small Cap Value Fund

We are pleased to provide you with our report for the Timothy Plan Small-Cap Value Fund for the twelve months ending September 30, 2014 and would like to thank you for entrusting your assets with us.

Over the past twelve months equity markets, while withstanding brief corrections, generally moved higher. Equity market gains were fueled by US economic data, new relative stability in the US fiscal situation and better than expected 4Q corporate earnings. Despite concerns about the impact of weaker emerging market economies and ongoing conflicts in the Ukraine and with global terrorism, investors remained favorable to the equity asset class. Additionally, the anticipation of reduced monetary stimulus contributed to greater market volatility throughout the fiscal year, as well as higher dispersion among stock prices. This has historically caused a differentiated performance environment that favors higher quality, fundamentally sound companies with predictable earnings growth.

For the twelve months ending September 30, 2014, the Timothy Plan Small-Cap Value Fund Class A again produced a strong return of 7.6%, while the Russell 2000 Index produced a return of 3.9%. Small caps, however, have underperformed their large cap counterparts over this time period. Investors have shown a preference for large cap over this time period and small cap Energy, a top performer in 2013, has underperformed most recently through the 3rd quarter 2014. Security selection was the primary driver of relative outperformance and centered in the Health Care, Materials & Processing, Energy and Producer Durables sectors. Top performing securities were in sectors levered to economic growth and included Trex Company, KapStone Paper and Packaging, US Silica and Synergy Resources. Materials & Processing was the largest overall driver of relative outperformance with several holdings producing returns over 50% for the last 12 months.

Security selection in Consumer Discretionary coupled with overweight allocations in the Energy and Producer Durables sectors detracted from relative performance. Consumer Discretionary holding Arctic Cat was a bottom performer on an absolute basis, after it reported lower than expected guidance for 2015 revenues and earnings. Allocations to Energy and Producer Durables also negatively impacted performance as these sectors underperformed the index as a whole.

The Small Cap Value team is focusing on well-run companies with growth prospects that are underappreciated by the marketplace. We look for companies with above average growth and strong balance sheets that are generating good cash flows and superior relative returns. We have been finding many opportunities in the Energy, Materials & Processing and Producer Durables spaces leading us to overweight positions in these sectors. In Energy, we are finding exploration and production companies with best in class production growth that are selling at or below peer group multiples. In Materials & Processing, we have found value in stocks that are tied to a housing recovery that the market is somewhat skeptical about. In the Producer Durables space, our businesses will benefit from improving economic activity, while generating strong free cash flow and earnings growth. As economic growth continues, we feel our companies are positioned to achieve higher earnings and our portfolio should perform well.

We thank you for your continued confidence in the Westwood process and investment teams and we look forward to serving your investment needs through the years ahead.

Westwood Management Corporation

8

Fund Performance - (Unaudited)

September 30, 2014

Small Cap Value Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return |

Timothy Small Cap Value Fund - Class A (With Sales Charge) | | 1.51% | | 15.01% | | 7.73% | | |

Russell 2000 Index | | 3.93% | | 14.29% | | 8.19% | | |

Timothy Small Cap Value Fund - Class C * | | 5.72% | | 15.46% | | 7.53% | | |

Russell 2000 Index | | 3.93% | | 14.29% | | 8.19% | | |

Timothy Small Cap Value Fund - Class I | | 7.69% | | N/A | | 9.40% | | (a) |

Russell 2000 Index | | 3.93% | | 14.29% | | 4.77% | | (a) |

| (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

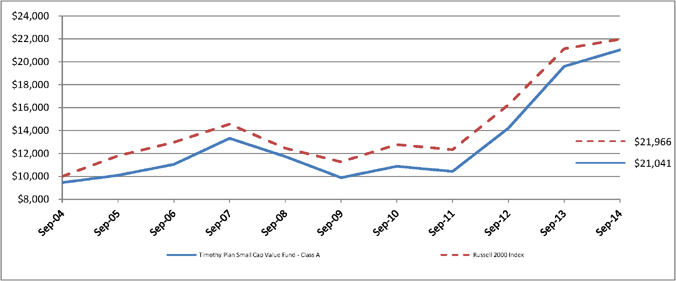

Timothy Plan Small Cap Value Fund vs. Russell 2000 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 2000 Index on September 30, 2004 and held through September 30, 2014. The Russell 2000 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

9

Letter from the Manager

September 30, 2014

Large/Mid Cap Value Fund

We are pleased to provide you with our report for the Timothy Plan Large/Mid-Cap Value Fund for the twelve months ending September 30, 2014 and would like to thank you for entrusting your assets with us.

Over the past twelve months equity markets, while withstanding brief corrections, generally moved higher. Equity market gains were fueled by US economic data, new relative stability in the US fiscal situation and better than expected 4Q corporate earnings. Despite concerns about the impact of weaker emerging market economies and ongoing conflicts in the Ukraine and with global terrorism, investors remained favorable to the equity asset class. Additionally, the anticipation of reduced monetary stimulus contributed to greater market volatility throughout the fiscal year, as well as higher dispersion among stock prices. This has historically caused a differentiated performance environment that favors higher quality, fundamentally sound companies with predictable earnings growth.

For the twelve months ending September 30, 2014, the Timothy Plan Large/Mid-Cap Value Fund Class A produced a return of 16.1%, while the S&P 500 Index produced a return of 19.7%. Security selection in Technology, Consumer Discretionary and Utilities sectors aided relative performance. The Technology sector has been a strong performer and produced significant returns for the fund. Many of the fund’s top performers were in sectors such as Technology, which are levered to economic growth. Optimism aided the performance of pro-cyclical companies, such as Avago Technologies, Skyworks Solutions and Advance Auto Parts.

Security selection in Health Care, Financial Services and Materials & Processing was the largest detractor to relative performance in the prior twelve months. Index sectors Health Care outperformed the market and our holdings failed to keep pace. Individual detractors to performance in the REIT sector included HCP Inc., which traded lower as investors rotated out of REITs on interest rate fears and the impact this could have on future acquisitions. Additionally, Energy holdings such as Oasis Petroleum and Anadarko Petroleum underperformed on falling oil and gas prices.

The Timothy Plan Large/Mid-Cap Value Fund performed well in the past twelve months on an absolute basis, producing a gross total return of nearly 18% in fiscal 2014.

The team remains focused on high-quality businesses with undervalued growth prospects, high returns on invested capital, strong balance sheets, and attractive future growth rates in earnings and cash flow. From a sector standpoint, we see value in many names within the industrial area. These businesses are able to benefit from improving economic activity, while maintaining stronger free cash flow profiles than other businesses in more commoditized areas of the market. Finally, many of our technology names continue to benefit from growth in mobile. As the number of handsets continues to grow, as well as the increased content within each handset, future earnings growth remains very attractive and underappreciated by the market in our view. As a result, we believe we are well-positioned. Given the current Fed outlook, we have historically outperformed when monetary stimulus is reduced, the economy matures and investor risk appetites fall. During such periods, a portfolio filled with high-quality companies that have visible earnings growth has provided an attractive risk-adjusted return for investors.

We thank you for your continued confidence in the Westwood process and investment teams and we look forward to serving your investment needs through the years ahead.

Westwood Management Corporation

10

Fund Performance - (Unaudited)

September 30, 2014

Large/Mid Cap Value Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return |

Timothy Large/Mid Cap Value Fund - Class A (With Sales Charge) | | 9.74% | | 13.48% | | 9.00% | | |

S&P 500 Index | | 19.73% | | 15.70% | | 8.11% | | |

Timothy Large/Mid Cap Value Fund - Class C * | | 14.26% | | 13.90% | | 8.80% | | |

S&P 500 Index | | 19.73% | | 15.70% | | 8.11% | | |

Timothy Large/Mid Cap Value Fund - Class I | | 16.43% | | N/A | | 13.64% | | (a) |

S&P 500 Index | | 19.73% | | 15.70% | | 15.62% | | (a) |

| (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

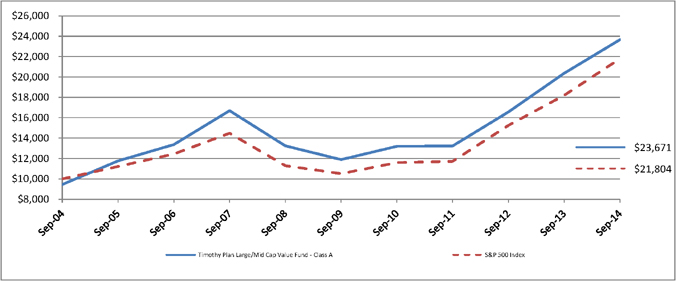

Timothy Plan Large/Mid Cap Value Fund vs. S&P 500 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the S&P 500 Index on September 30, 2004 and held through September 30, 2014. The S&P 500 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

11

Letter from the Manager

September 30, 2014

Fixed Income Fund

TIMOTHY PLAN FIXED INCOME MANAGER’S COMMENTARY SEPTEMBER 2014

BARROW, HANLEY, MEWHINNEY & STRAUSS

The broad investment grade U.S. bond market as defined by the Barclays Aggregate index began the last 12 months with a yield of 2.34% and ended at 2.36% on September 30, 2014. Examining only the endpoint yields of the U. S. bond market disguises the fact that significant changes took place. Rates across the Treasury yield curve moved in quite different directions as the U.S. Treasury (UST) five year rate increased 37 basis points while the UST 30 year rate declined 49 basis points. The shorter maturity end of the UST yield curve saw rates rise as the Federal Reserve’s Quantitative Easing tapered toward an end generating market debates about the timing of the first policy rate increase. Higher short rates flattened the yield curve back toward a more normal historical relationship.

However, the decline in long rates over the past 12 months further flattened the UST yield curve and was not expected by most market participants. The past year began with U.S. economic data stronger thanks to a string of solid payroll increases and a boost in capital goods spending that led to higher long UST rates in 4Q13. However, Global economic growth slowed with persistently weak European GDP and faltering Chinese and emerging market economies leading to tepid inflation data from slumping commodity prices. Slowing global growth and lower inflation has global central banks engaging in massive monetary stimulus. These global concerns have led to demand for UST long bonds as a safe haven driving their yields lower. Even with the decline in UST rates they remain well above their developed market sovereign peers.

The yield spread sectors of the bond market, corporate and mortgage back bonds, also showed significant changes over the past 12 months. Following the improvement in the U.S. economy yield spreads to UST issues narrowed. From the beginning of the period Investment Grade Credit spreads narrowed from 141 basis points (bps) to 98 bps on June 30th generating higher returns for spread sectors. However with increased concerns over global growth and shareholder friendly actions by company managements modestly diluting bond holders interests, yield spreads widened back out to 112 bps by September 30, 2014 giving back some of the early performance gains.

The Timothy Fixed Income Fund Class A shares returned 2.64% over the 12 months ended September 30, 2014 with most of the return simply income. The Barclays Aggregate index was slightly better at 3.96% over the trailing 12 months. The portfolio’s positioning favored intermediate over long maturities in corporate bonds and higher coupon GNMA mortgages with their shorter average life which detracted from results over the past 12 months. We are keeping a close watch on the timing of the Fed’s first policy-rate increase and their decisions about what to do with a $4.4 trillion bloated balance sheet. The portfolio’s positioning remains focused on generating income consistent with a prudent level of risk.

BARROW, HANLEY, MEWHINNEY & STRAUSS

12

Fund Performance - (Unaudited)

September 30, 2014

Fixed Income Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return |

Timothy Fixed Income Fund - Class A (With Sales Charge) | | (1.83)% | | 2.02% | | 2.88% | | |

Barclays Capital U.S. Aggregate Bond Index | | 3.96% | | 4.12% | | 4.62% | | |

Timothy Fixed Income Fund - Class C * | | 1.02% | | 2.22% | | 2.59% | | |

Barclays Capital U.S. Aggregate Bond Index | | 3.96% | | 4.12% | | 4.62% | | |

Timothy Fixed Income Fund - Class I | | 3.16% | | N/A | | 3.50% | | (a) |

Barclays Capital U.S. Aggregate Bond Index | | 3.96% | | 4.12% | | 4.25% | | (a) |

| (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

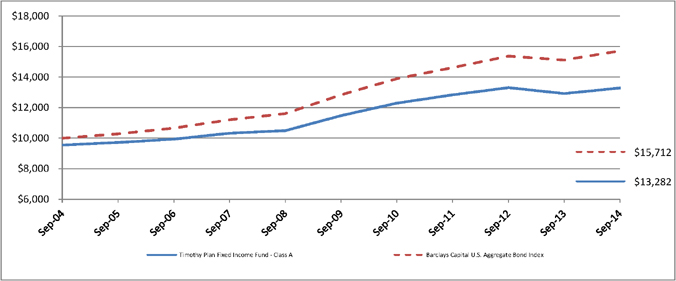

Timothy Plan Fixed Income Fund vs. Barclays Capital U.S. Aggregate Bond Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Barclays Capital U.S. Aggregate Bond Index on September 30, 2004 and held through September 30, 2014. The Barclays Capital U.S. Aggregate Bond Index is a widely recognized, unmanaged index of bond prices. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

13

Letter from the Manager

September 30, 2014

High Yield Bond Fund

TIMOTHY PLAN HIGH YIELD MANAGER’S COMMENTARY SEPTEMBER 2014

BARROW, HANLEY, MEWHINNEY & STRAUSS

The U.S. High Yield bond market as defined by the Barclays BA/B index began the last 12 months with a yield of 5.53% and ended at 5.51% on September 30, 2014. Examining only these endpoint yields disguises the fact that significant changes took place. Rates across the Treasury yield curve moved in quite different directions as the U.S. Treasury (UST) five year rate increased 37 basis points while the 30 year rate declined 49 basis points. The short maturity end of the yield curve saw rates rise as the Federal Reserve’s Quantitative Easing tapered toward an end generating market debates about the timing of the first policy rate increase. The decline in long UST rates over the past 12 months was not expected by most market participants as global economic concerns led to demand for the safety of UST long bonds driving their yields lower.

The last 12 months began with U.S. economic data mostly stronger thanks to a string of solid payroll increases and a boost in capital goods spending. Against the backdrop of a good economy, corporate earnings gains, and the search for income High Yield bonds attracted significant buyers driving yield spreads narrower starting at 392 basis points (bps) at the beginning of the period down to 272 bps by June 30th for the Barclays BA/B index. The resultant rate decline from 5.53% to 4.45% generated significant market gains, and as 3Q14 began investors were quick to sell and recognize those gains.

Increased concern in the High Yield market from slowing global growth and slumping commodity prices led to yield spreads to widen to 361 bps. In 3Q14 High Yield rates rose over 100 bps from 4.45% to 5.51% ending the 12 month period only 2 bps from where it began. Price volatility came back to the High Yield market over the past 12 months, so income was essentially the primary source of returns.

The Timothy High Yield Fund Class A shares returned 5.71% over the 12 months ended September 30, 2014 with most of the return simply income. The Barclays Ba/B (3% cap) index was modestly higher at 7.25%. The portfolio’s positioning favored the energy sector and underweighted communications\media both of which detracted slightly from results. With today’s historically low yields and economic uncertainty we are keeping a close watch on any upticks in the default rate which remains very low. The portfolio’s positioning remains focused on generating income consistent with a reasonable level of risk.

BARROW, HANLEY, MEWHINNEY & STRAUSS

14

Fund Performance - (Unaudited)

September 30, 2014

High Yield Bond Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year

Average

Annual Return | | Average

Annual Return

Since Inception |

Timothy High Yield Bond Fund - Class A (With Sales Charge) | | 1.08% | | 7.21% | | 4.97% | | (a) |

Barclays Ba/B High Yield Index | | 7.25% | | 9.99% | | 7.62% | | (a) |

Timothy High Yield Bond Fund - Class C * | | 4.00% | | 7.42% | | 4.83% | | (a) |

Barclays Ba/B High Yield Index | | 7.25% | | 9.99% | | 7.62% | | (a) |

Timothy High Yield Bond Fund - Class I | | 6.07% | | N/A | | 5.33% | | (b) |

Barclays Ba/B High Yield Index | | 7.25% | | 9.99% | | 6.46% | | (b) |

| (a) | For the period May 7, 2007 (commencement of investment in accordance with objective) to September 30, 2014. |

| (b) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

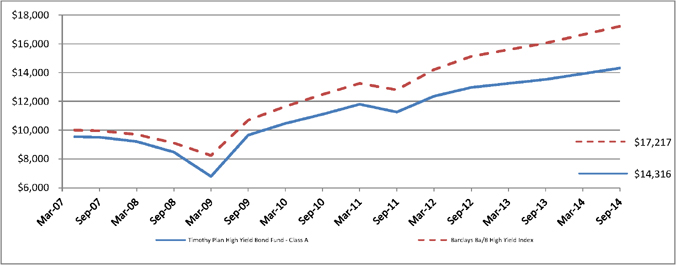

Timothy Plan High Yield Bond Fund vs. Barclays Ba/B High Yield Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Barclays Ba/B High Yield Index on May 7, 2007 and held through September 30, 2014. The Barclays Ba/B High Yield Index measures the performance of bonds with Ba or B ratings. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

15

Letter from the Manager

September 30, 2014

Israel Common Values Fund

Israel equities overall struggled during this period as economic conditions decelerated on the back of a worsening external environment and the effects of the Gaza war Operation Protective Edge. With more than 1/3 of GDP made up from exports, disappointing global trade had a negative effect on Israeli economic growth. With slowing growth, a strong currency, and declining inflation expectations, the Bank of Israel, under the new leadership of Ms. Karnit Flug, acted quickly by surprising the market with several interest rate cuts bringing the short term rate from 1.25% to 0.25% during this 12-month period. The shekel finally reacted to the lower rates and lower economic growth by depreciating sharply in the third quarter of 2014. This should lead to some relief for the Israeli export sector.

The Timothy Plan Israel Common Values Fund struggled a bit during this period mostly as a couple of screened out health care companies that are large components of the Israel TA-100 index had a great year. In spite of this, the Fund had good stock selection in Materials and Information Technology although an overweight to the IT sector detracted from performance. Moreover, an allocation to the food retail industry hurt performance as the government competition commission investigated the industry due to high food prices. On the positive front, Given Imaging, which manufactures diagnostic products for gastrointestinal disorders, was acquired leading to strong gains for the stock. Frutarom Industries, a global leading manufacturer of flavors and ingredients continued to perform well for the Fund. Other notable positive performance occurred in semiconductors with Tower Semi performing well in addition to pharmaceuticals with strong performance from Taro Pharma.

The near term prospects for global trade have deteriorated somewhat leading to signs of headwinds for the country’s GDP growth. Yet, the recent currency depreciation should alleviate some of the pressures on export companies. We remain positive on the prospects for innovation from Israeli companies translating into positive long term equity returns. While geopolitical risks have risen lately, history suggests that Israeli corporates are prepared to weather storms and come out stronger in the end.

Eagle Global Advisors, LLC

16

Fund Performance - (Unaudited)

September 30, 2014

Israel Common Values Fund

| | | | | | |

| Fund/Index | | 1 Year Total Return | | Average

Annual Return

Since Inception |

Timothy Israel Common Values Fund - Class A (With Sales Charge) | | (3.35)% | | 7.10% | | (a) |

Israel TA 100 Index | | 14.31% | | 10.10% | | (a) |

Timothy Israel Common Values Fund - Class C * | | 0.52% | | 8.31% | | (a) |

Israel TA 100 Index | | 14.31% | | 10.10% | | (a) |

Timothy Israel Common Values Fund - Class I | | 2.44% | | 5.39% | | (b) |

Israel TA 100 Index | | 14.31% | | 15.99% | | (b) |

| (a) | For the period October 12, 2011 (commencement of investment in accordance with objective) to September 30, 2014. |

| (b) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

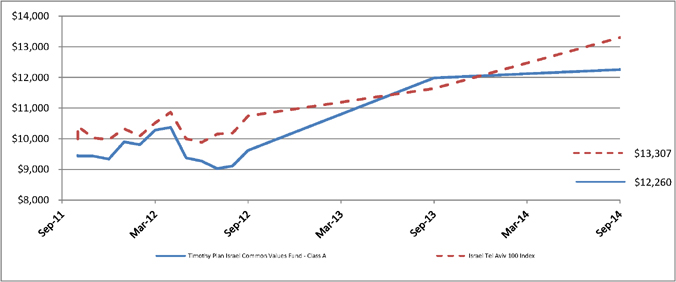

Timothy Plan Israel Common Values Fund vs. Israel Tel Aviv 100 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Israel TA 100 Index on October 12, 2011 and held through September 30, 2014. The Israel Tel Aviv 100 Index is an unmanaged index of equity prices representing the 100 most highly capitalized companies listed on the Tel Aviv Stock Exchange . Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

17

Letter from the Manager

September 30, 2014

Defensive Strategies Fund

The Defensive Strategies Fund has been designed and managed to do what its name implies, i.e. hedge against a possible scenario of hyper-inflation which could result from our nation’s leadership’s proven unwillingness to address our core problems of too much spending, too much taxation and too many onerous government regulations. We have, therefore, built in the flexibility to either adjust to a possible risk of extreme deflation with the ability to convert our inflation sensitive assets to cash and fixed income securities that should perform well during a deflationary environment or to a more normal, traditional investment strategy. As I stated in last year’s report, although we will do our very best to be successful, we cannot guarantee results in any of these scenarios.

I would also like to point out that, since there does not exist an appropriate benchmark index with which to compare our performance, we have created a blended index comprised of roughly 1/3 each of U.S. Government TIPs, FTSE NAREIT Equity Index and Dow Jones UBS Commodity Index (the “Blended Index”). We believe this better matches the makeup of our fund than the previously used Dow Jones US Moderate 40 Index which contains no commodities.

For the fiscal year ended September 30, 2014, the Defensive Strategies Fund Class A achieved a total return of 3.06%, vs a total return of 2.58% for the Blended Index, the Fund’s benchmark. This Fund invests in four different categories of securities, each category being managed by a sub-advisers to our other Funds. The sub-advisers have provided discussions of the factors that affected their Fund’s performance, as well as their thoughts for the next fiscal year, and I encourage you to read them carefully. During the last fiscal year, we managed the Fund with a decidedly conservative bias, and we plan to continue to manage this fund conservatively as we attempt to adjust to (what could be) rapidly changing economic conditions.

While no one can predict future events, as I stated in my President’s letter, I remain confident that our sub-advisors (i.e. money management firms that manage the various sleeves of this Fund) are, in our opinion, among the best in the industry and they each continue to honor our overall policy that they manage their respective Fund sleeve both in accordance with our screening restrictions and with a conservative bias.

Finally, I would once again like to thank you for your moral convictions that led you to become part of the Timothy Plan family.

Yours in Christ,

Arthur D. Ally

Fund Advisor

18

Fund Performance - (Unaudited)

September 30, 2014

Defensive Strategies Fund

| | | | | | |

| Fund/Index | | 1 Year Total Return | | Average

Annual Return

Since Inception |

Timothy Defensive Strategies Fund - Class A (With Sales Charge) | | (2.63)% | | 3.93% | | (a) |

Dow Jones Moderately Conservative U.S. Portfolio Index | | 10.73% | | 12.16% | | (a) |

Timothy Defensive Strategies Fund Blended Index (c) | | 2.58% | | 6.42% | | (a) |

Timothy Defensive Strategies Fund - Class C * | | 1.27% | | 4.37% | | (a) |

Dow Jones Moderately Conservative U.S. Portfolio Index | | 10.73% | | 12.16% | | (a) |

Timothy Defensive Strategies Fund Blended Index (c) | | 2.58% | | 6.42% | | (a) |

Timothy Defensive Strategies Fund - Class I | | 3.39% | | 2.90% | | (b) |

Dow Jones Moderately Conservative U.S. Portfolio Index | | 10.73% | | 9.31% | | (b) |

Timothy Defensive Strategies Fund Blended Index (c) | | 2.58% | | 1.92% | | (b) |

| (a) | For the period November 4, 2009 (commencement of investment in accordance with objective) to September 30, 2014. |

| (b) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| (c) | The Timothy Defensive Strategies Fund Blended Index reflects an unmanaged portfolio of 33% of the Barclays U.S. TIPs Index, 33% of the FTSE NAREIT ALL REITs Index and 34% of the Dow Jones Commodity Total Return Index. |

| * | With Maximum Deferred Sales Charge |

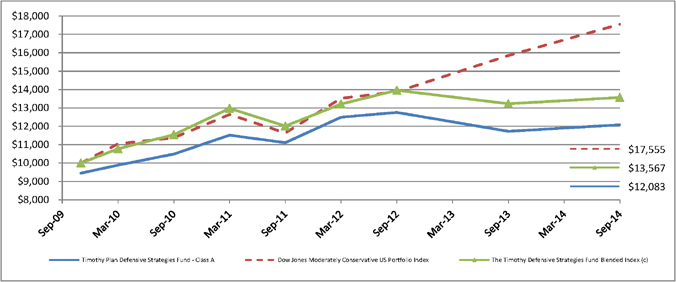

Timothy Plan Defensive Strategies Fund vs. Dow Jones Moderately Conservative U.S. Portfolio Index vs. The Timothy Defensive Strategies Fund Blended Index (c)

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares, Dow Jones Moderately Conservative U.S. Portfolio Index and the Timothy Defensive Strategies Fund Blended Index (c) on November 4, 2009 and held through September 30, 2014. The Dow Jones Moderately Conservative U.S. Portfolio Index is a widely recognized unmanaged index of stocks, bonds and cash. Performance figures include the change in value of the asset classes in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

19

Letter from the Manager

September 30, 2014

Strategic Growth Fund

Dear Strategic Growth Fund Shareholder:

The Timothy Plan Strategic Growth Fund is an asset allocation fund that invests in a number of Timothy Plan underlying funds. The allocation percentages will vary somewhat from time to time as a result of changing economic conditions, At September 30, 2014, this Fund was invested in the following underlying Timothy Plan Funds:

| | | | | | |

| Large/Mid-Cap Growth Fund | | (13.5%) | | Small-Cap Value Fund | | (6.25%) |

| | | |

| Large/Mid-Cap Value Fund | | (13.0%) | | Aggressive Growth Fund | | (5.75%) |

| | | |

| International Fund | | (15.25%) | | High-Yield Bond Fund | | (12.75%) |

| | | |

| Defensive Strategies Fund | | (12.5%) | | Israel Common Values Fund | | (5.0%) |

| | | |

| Emerging Markets Fund | | (6.0%) | | Growth & Income Fund | | (10.0%) |

For the fiscal year ended September 30, 2014, the Strategic Growth Fund Class A achieved a total return of 6.82%, vs a total return of 9.67% for the Dow Jones Global Moderate Index, the Fund’s benchmark. This Fund’s performance is directly affected by the factors that influence the performance of each of the underlying Funds. The sub-advisers to each underlying Fund have provided discussions of the factors that affected their Fund’s performance, as well as their thoughts for the next fiscal year, and I encourage you to read them carefully. During the last fiscal year, we managed the Fund with a decidedly conservative bias, and we plan to continue to manage this fund conservatively as we attempt to adjust to (what could be) rapidly changing economic conditions.

We continue to realize that the volatility and uncertainty of the markets may have been unsettling for many investors; however as a group, although our sub-advisors expect this pattern to continue into 2015, they also expect a somewhat upward bias with respect to performance in our underlying funds.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is that every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment with which you can feel comfortable.

Thank you for your continued support.

Arthur D. Ally

20

Fund Performance - (Unaudited)

September 30, 2014

Strategic Growth Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year

Average

Annual Return | | 10 Year Average

Annual Return |

Timothy Strategic Growth Fund - Class A (With Sales Charge) | | 0.89% | | 7.23% | | 4.06% |

Dow Jones Global Moderately Aggressive Portfolio Index | | 9.67% | | 10.95% | | 8.01% |

Timothy Strategic Growth Fund - Class C * | | 5.12% | | 7.64% | | 3.85% |

Dow Jones Global Moderately Aggressive Portfolio Index | | 9.67% | | 10.95% | | 8.01% |

| * | With Maximum Deferred Sales Charge |

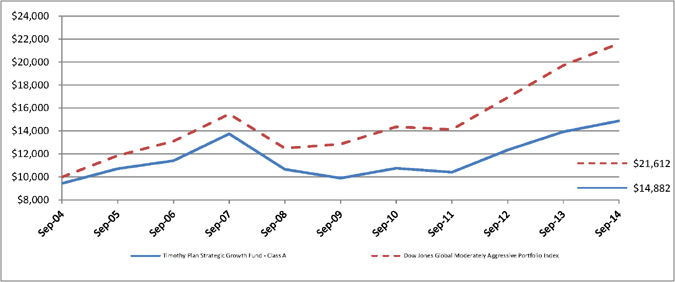

Timothy Plan Strategic Growth Fund vs. Dow Jones Global Moderately Aggressive Portfolio Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Dow Jones Global Moderately Aggressive Portfolio Index on September 30, 2004 and held through September 30, 2014. The Dow Jones Global Moderately Aggressive Portfolio Index is a widely recognized index that measures global stocks, bonds and cash which are in turn represented by multiple sub-indexes. Performance figures include the change in value of the investments in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

21

Letter from the Manager

September 30, 2014

Conservative Growth Fund

Dear Conservative Growth Fund Shareholder:

The Timothy Plan Conservative Growth Fund is an asset allocation fund that invests in a number of Timothy Plan underlying funds. The allocation percentages will vary slightly from time to time as a result of changing economic conditions, At September 30, 2014, the Fund was invested in the following underlying Timothy Plan Funds as follows:

| | | | | | |

| Large/Mid-Cap Growth Fund | | (8.25%) | | Small-Cap Value Fund | | (5.25%) |

| | | |

| Large/Mid-Cap Value Fund | | (7.75%) | | Aggressive Growth Fund | | (2.25%) |

| | | |

| International Fund | | (10.0%) | | High-Yield Bond Fund | | (8.5%) |

| | | |

| Defensive Strategies Fund | | (12.0%) | | Fixed Income Fund | | (29.0%) |

| | | |

| Israel Common Values Fund | | (4.0%) | | Growth & Income Fund | | (10.0%) |

| | | |

| Emerging Markets Fund | | (3.0%) | | | | |

For the fiscal year ended September 30, 2014, the Conservative Growth Fund Class A achieved a total return of 5.23%, vs a total return of 7.93% for the Dow Jones Global Moderate Index, the Fund’s benchmark. This Fund’s performance is directly affected by the factors that influence the performance of each of the underlying Funds. The sub-advisers to each underlying Fund have provided discussions of the factors that affected their Fund’s performance, as well as their thoughts for the next fiscal year, and I encourage you to read them carefully. During the last fiscal year, we managed the Fund with a decidedly conservative bias, and we plan to continue to manage this fund conservatively as we attempt to adjust to (what could be) rapidly changing economic conditions.

We continue to realize that the volatility and uncertainty of the markets may have been unsettling for many investors; however as a group, although our sub-advisors expect this pattern to continue into 2015, they also expect a somewhat upward bias with respect to performance in our underlying funds.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is that every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment with which you can feel comfortable.

Thank you for your continued support.

Arthur D. Ally

22

Fund Performance - (Unaudited)

September 30, 2014

Conservative Growth Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year

Average

Annual Return | | 10 Year Average

Annual Return |

Timothy Conservative Growth Fund - Class A (With Sales Charge) | | (0.45)% | | 5.49% | | 3.95% |

Dow Jones Global Moderate Portfolio Index | | 7.93% | | 9.12% | | 7.08% |

Timothy Conservative Growth Fund - Class C * | | 3.50% | | 5.88% | | 3.77% |

Dow Jones Global Moderate Portfolio Index | | 7.93% | | 9.12% | | 7.08% |

| * | With Maximum Deferred Sales Charge |

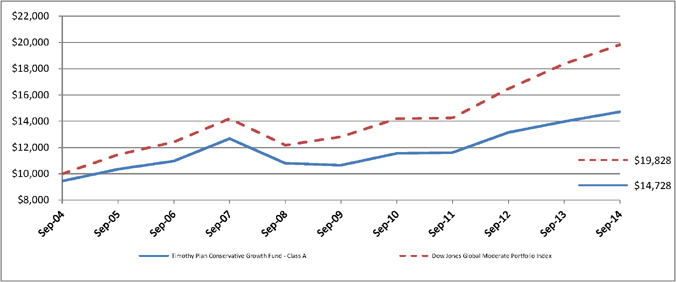

Timothy Plan Conservative Growth Fund vs. Dow Jones Global Moderate Portfolio Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Dow Jones Global Moderate Portfolio Index on September 30, 2004 and held through September 30, 2014. The Dow Jones Global Moderate Portfolio Index is a widely recognized index that measures global stocks, bonds and cash which are in turn represented by multiple sub-indexes. Performance figures include the change in value of the investments in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

23

Letter from the Manager

September 30, 2014

Emerging Markets Fund

We will discuss sector-, country- and stock-specific factors that affected the Fund’s performance and describe changes in the Fund’s composition during the 12 months ended September 30th, 2014. In addition, we will share insight into how the Fund is currently positioned for the future.

The Markets

Emerging-market stocks declined in the third quarter of 2014 as the investor optimism that propelled them during the first half of the year seemed to dissipate. Fears that the U.S. Federal Reserve was moving closer to raising interest rates caused market concern about a potential repeat of last year’s sell-off and led investors to take a more cautious stance toward the asset class.

Russian equities fell on the heels of the Russia-Ukraine crisis escalation, while Brazilian stocks and currency suffered as investors’ hope of an economic reform was dimmed when President Dilma Rousseff regained popularity ahead of the upcoming presidential election.

Additionally, uncertainty over the ongoing pro-democracy protest in Hong Kong against the Chinese government further weighed on market sentiment toward emerging markets.

The Fund

As one might expect given the portfolio activity over the past year, the strategy’s allocations at the end of the third quarter were very similar to those earlier in 2014.

Allocation to companies in Russia continues to be a key investment topic. As of September 30, 2014, Russian equities, as a whole, traded at what we considered very attractive valuation multiples—lower than emerging markets as a group, or any other region/country in the world for that matter. We have maintained our holdings in Russia, and, in some cases, selectively averaged down on our positions. Additionally, as discussed earlier, we initiated a position in ITE Group, which is effectively a Russian company.

As the situation remains fluid with many unknowns, we have re-assessed the intrinsic value estimates of our holdings in Russia and are searching new opportunities there, while also considering the shorter-term implications of current or potential future sanctions. For example, Sberbank is being sanctioned by the European Union (EU) in regards to dealing with or purchasing securities issued after August 1, 2014. We continue to monitor the situation very closely. At the moment, Sberbank’s stock price seems depressed by current EU sanctions and the fear of more severe sanctions against Russia or Russian companies. Moreover, our analysis shows that the stock price also implies a very bleak scenario for Sberbank’s earnings, including margin compression on net interest income, a slowdown in loan and fee income growth, and deteriorating credit quality.

While the EU sanctions are designed to restrict Sberbank’s access to funding, Sberbank has actually low dependency on external funding, with its wholesale foreign-currency debt representing only 3% of total liabilities. Due to its systemic importance to the banking system in Russia and being approximately 51% owned by the Central Bank of Russia, Sberbank will likely have incremental access to central bank funding support if necessary.

24

Letter from the Manager

September 30, 2014

Emerging Markets Fund - Continued

We believe Sberbank has very attractive long-term growth prospects as the dominant retail and commercial banking franchise in Russia. We also think that the risk/reward proposition presented by Sberbank’s current stock price appears very favorable for the long-term investor.

Outlook

The number of events—and the gravity of some of them—evolving in emerging markets seemed to have led many short-term oriented investors and speculators to take on a “risk on, risk off” approach to emerging-market stocks. This can be seen in the market sentiment swings toward the asset class just over the last several months.

As long-time investors in emerging markets, however, we understand that while macroeconomic events need to be considered, they affect each emerging-market company differently. Our established global research infrastructure, which encompasses a team of analysts with extensive knowledge about their specific industries, allows us to think and invest independently from the market consensus.

Our willingness and ability to look beyond the short term give us confidence that the Brandes Emerging Market Strategy continues to offer compelling valuations and investment opportunities. As always, thank you for your business and continued trust.

Brandes Investment Partners, L.P.

This material is intended for informational purposes only. The information provided in this material should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings, or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Portfolio holdings and allocations are subject to change at any time. Strategies discussed herein are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. Market conditions may impact performance.

International and emerging markets investing is subject to certain risks such as currency fluctuation and social and political changes, differences in financial reporting standards and less stringent regulation of securities markets which may result in greater share price volatility; such risks are increased when investing in emerging markets. Additional risks associated with emerging markets investing include smaller-sized markets, liquidity risks, and less established legal, political, social, and business systems to support securities markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Index Guide

The MSCI Emerging Markets Index with gross dividends measures equity market performance of emerging markets.

25

Fund Performance - (Unaudited)

September 30, 2014

Emerging Markets Fund

| | | | | | |

| Fund/Index | | 1 Year Total Return | | Average

Annual Return

Since Inception |

Timothy Emerging Markets Fund - Class A (With Sales Charge) | | (4.81)% | | 0.07% | | (a) |

MSCI Emerging Markets Index | | 1.81% | | (0.13)% | | (a) |

Timothy Emerging Markets Fund - Class C * | | (1.14)% | | 2.45% | | (a) |

MSCI Emerging Markets Index | | 1.81% | | (0.13)% | | (a) |

Timothy Emerging Markets Fund - Class I | | 0.81% | | 5.62% | | (b) |

MSCI Emerging Markets Index | | 1.81% | | 4.59% | | (b) |

| (a) | For the period December 3, 2012 (commencement of investment in accordance with objective) to September 30, 2014. |

| (b) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| * | With Maximum Deferred Sales Charge |

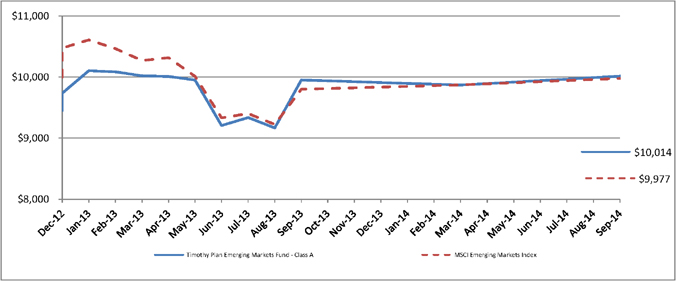

Timothy Plan Emerging Markets Fund vs. MSCI Emerging Markets Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the MSCI Emerging Markets Index on December 3, 2012 and held through September 30, 2014. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

26

Letter from the Manager

September 30, 2014

Growth & Income Fund

We are pleased to provide you with our first report for the Timothy Plan Growth and Income Fund for the period ending September 30, 2014. Like you, our company and some of our officers have invested some of corporate retirement and personal assets into the fund. We certainly thank you for entrusting your assets with us.

This is the first year of operation for the fund and it was an interesting time. Large capitalization stocks, with just a few minor setbacks, moved ahead. The same cannot be said of small capitalization stocks. They experienced a lot more volatility and didn’t make much progress. During this time bonds surprised many as longer term interest rates fell, leading to gains in those bonds. One of the major contributors to market activities was the Federal Reserve and its move to taper Quantitative Easing. This has certainly forced investors to revaluate risk and potential reward.

For the period starting 1 October 2013 through 30 September 2014, the Growth & Income Fund Class A returned 9.50%. A combination of 50% of the Russell 3000 Total Return Index and 50% Barclay’s Intermediate US/Govt Corp Index returned 9.36%. The Industrial and Basic Material sectors were the top performers while Consumer Cyclical and Utility stocks did the worst. Two of the top performers were American Railcar, which is a manufacturer of oil tanker railcars, and Trinity Industries, which supports the Energy and Transportation sectors.

This fund has two main objectives, growth and income but also the preservation of capital in declining markets. We have been managing similar assets for over 40 years. We will adjust equity and fixed income levels according to our analysis of risk. We do this on a weekly basis. Over the last year we saw lower risks in larger companies but higher risks in smaller companies. At the end of September, we actually saw over six in ten small stocks (less than $1 billion in market capitalization) in their personal bear market. That is falling 20% or more from their recent highs. At the time only about one in ten stocks in the S&P 500 were suffering in a like manner.

Our outlook has shifted some from seeing the better risk/reward opportunity moving from bonds to stocks. We don’t think interest rates will surge higher, but we think the best returns in bonds are probably behind us. At the same time, the September swoon in stocks appears to present some better opportunities for adding to equity levels. Our research points to a reasonably healthy outlook for stocks in the year ahead. However, we think volatility will tend to rise. If our research works well, this actually could give us opportunities to take advantage of these shifts.

We thank you for your trust in the James Investment Research Inc., we are grateful for the opportunity to serve you.

James Investment Research Inc.

27

Fund Performance - (Unaudited)

September 30, 2014

Growth & Income Fund

| | | | |

| Fund/Index | | Average

Annual Return

Since Inception |

Timothy Growth & Income Fund - Class A (With Sales Charge) | | 4.58% | | (a) |

Timothy Growth & Income Fund Blended Index (b) | | 9.36% | | (a) |

Timothy Growth & Income Fund - Class C * | | 7.70% | | (a) |

Timothy Growth & Income Fund Blended Index (b) | | 9.36% | | (a) |

Timothy Growth & Income Fund - Class I | | 9.60% | | (a) |

Timothy Growth & Income Fund Blended Index (b) | | 9.36% | | (a) |

| (a) | For the period October 1, 2013 (commencement of investment in accordance with objective) to September 30, 2014. |

| (b) | The Timothy Growth & Income Fund Blended Index reflects an unmanaged portfolio of 50% of the Barclays Intermediate Government/Credit Index and 50% of the Russell 3000 Total Return Index. |

| * | With Maximum Deferred Sales Charge |

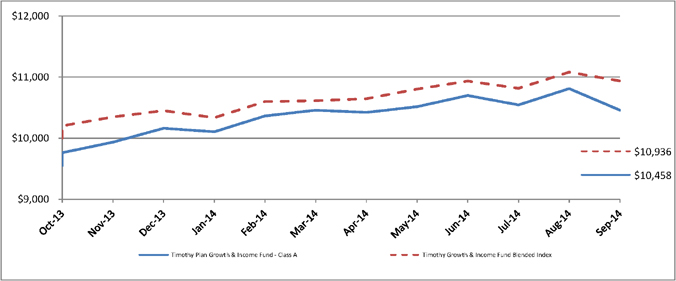

Timothy Growth & Income Fund vs. Timothy Growth & Income Fund Blended Index (b)

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Timothy Growth & Income Fund Blended Index on October 1, 2013 and held through September 30, 2014. The Timothy Growth & Income Fund Blended Index reflects an unmanaged portfolio of 50% of the Barclays Intermediate Government/Credit Index and 50% of the Russell 3000 Total Return Index. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

28

Fund Profile

As of September 30, 2014 (Unaudited)

Aggressive Growth Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Commercial Services | | | 12.3 | % |

Banks | | | 8.5 | % |

Diversified Financial Services | | | 7.7 | % |

Retail | | | 7.3 | % |

Healthcare | | | 7.1 | % |

Software | | | 6.8 | % |

Computers | | | 5.5 | % |

Apparel | | | 4.8 | % |

Oil & Natural Gas | | | 3.7 | % |

Telecommunications | | | 3.7 | % |

Other Assets Less Liabilities - Net | | | 32.6 | % |

| | | 100.0 | % |

Large/Mid Cap Growth Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Retail | | | 12.9 | % |

Semiconductors | | | 10.0 | % |

Oil & Natural Gas | | | 8.2 | % |

Electronics | | | 6.1 | % |

Software | | | 5.9 | % |

Banks | | | 5.6 | % |

Chemicals | | | 4.8 | % |

Commercial Services | | | 4.1 | % |

Food | | | 3.8 | % |

Insurance | | | 3.5 | % |

Other Assets Less Liabilities - Net | | | 35.1 | % |

| | | 100.0 | % |

Large/Mid Cap Value Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Electronics | | | 9.7 | % |

Oil & Natural Gas | | | 9.4 | % |

Semiconductors | | | 6.2 | % |

Banks | | | 6.1 | % |

Diversified Financial Services | | | 6.1 | % |

Food | | | 5.8 | % |

Retail | | | 5.1 | % |

Money Market Fund | | | 5.1 | % |

Healthcare Products | | | 4.0 | % |

Miscellaneous Manufacturing | | | 3.7 | % |

Other Assets Less Liabilities - Net | | | 38.8 | % |

| | | 100.0 | % |

High Yield Bond Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Corporate Bonds | | | 97.4 | % |

Money Market Fund | | | 1.5 | % |

Other Assets Less Liabilities - Net | | | 1.1 | % |

| | | 100.0 | % |

International Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Banks | | | 12.6 | % |

Automotive | | | 8.8 | % |

Insurance | | | 8.8 | % |

Healthcare | | | 8.6 | % |

Food | | | 5.8 | % |

Money Market Fund | | | 5.1 | % |

Oil & Natural Gas | | | 4.8 | % |

Pharmaceutical | | | 4.7 | % |

Diversified Financial Services | | | 4.6 | % |

Telecommunications | | | 4.4 | % |

Other Assets Less Liabilities - Net | | | 31.8 | % |

| | | 100.0 | % |

Small Cap Value Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Banks | | | 14.8 | % |

Oil & Natural Gas | | | 9.3 | % |

REITs | | | 8.9 | % |

Building Materials | | | 7.9 | % |

Machinery | | | 5.2 | % |

Healthcare | | | 4.3 | % |

Insurance | | | 4.2 | % |

Electric | | | 3.9 | % |

Retail | | | 3.9 | % |

Transportation | | | 3.9 | % |

Other Assets Less Liabilities - Net | | | 33.7 | % |

| | | 100.0 | % |

Fixed Income Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Corporate Bonds | | | 39.8 | % |

Government Mortgage - Backed Securities | | | 28.8 | % |

Government Notes & Bonds | | | 27.3 | % |

Money Market Fund | | | 3.7 | % |

Other Assets Less Liabilities - Net | | | 0.4 | % |

| | | 100.0 | % |

Israel Common Values Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Oil & Natural Gas | | | 11.9 | % |

Real Estate | | | 11.2 | % |

Telecommunications | | | 10.8 | % |

Banks | | | 10.3 | % |

Software | | | 8.8 | % |

Semiconductors | | | 6.7 | % |

Pharmaceuticals | | | 5.0 | % |

Food | | | 4.5 | % |

Chemicals | | | 4.3 | % |

Electronics | | | 4.2 | % |

Other Assets Less Liabilities - Net | | | 22.3 | % |

| | | 100.0 | % |

29

Fund Profile (Continued)

As of September 30, 2014 (Unaudited)

Defensive Strategies Fund

Top Ten Industries

(% of Net Assets)

| | | | |

REITs | | | 30.0 | % |

TIPS | | | 25.2 | % |

Oil & Natural Gas | | | 8.5 | % |

Exchange Traded Funds | | | 8.4 | % |

Mining | | | 6.6 | % |

Chemicals | | | 5.5 | % |

Money Market Fund | | | 4.8 | % |

Corporate Bonds | | | 3.3 | % |

Government Mortgage - Backed Securities | | | 2.8 | % |

Oil & Gas Services | | | 1.9 | % |

Other Assets Less Liabilities - Net | | | 3.0 | % |

| | | 100.0 | % |

Conservative Growth Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Mutual Funds | | | 99.7 | % |

Money Market Fund | | | 0.3 | % |

| | | 100.0 | % |

Growth & Income Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Government Notes & Bonds | | | 49.0 | % |

Money Market Fund | | | 6.5 | % |

Commercial Services | | | 5.7 | % |

Oil & Natural Gas | | | 5.7 | % |

Insurance | | | 5.2 | % |

Chemicals | | | 4.3 | % |

Electric | | | 2.6 | % |

Retail | | | 2.3 | % |

Auto Parts & Equipment | | | 2.2 | % |

Miscellaneous Manufacturing | | | 2.1 | % |

Other Assets Less Liabilities - Net | | | 14.4 | % |

| | | 100.0 | % |

Strategic Growth Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Mutual Funds | | | 100.3 | % |

Other Assets Less Liabilities - Net | | | (0.3 | %) |

| | | 100.0 | % |

Emerging Markets Fund

Top Ten Industries

(% of Net Assets)

| | | | |

Banks | | | 14.4 | % |

Food | | | 7.2 | % |

Retail | | | 7.2 | % |

Electric | | | 6.6 | % |

Diversified Financial Services | | | 6.4 | % |

Oil & Natural Gas | | | 6.3 | % |

Iron/Steel | | | 5.2 | % |

Automotive | | | 4.7 | % |

Preferred Stock | | | 4.7 | % |

Reits | | | 4.0 | % |

Other Assets Less Liabilities - Net | | | 33.3 | % |

| | | 100.0 | % |

30

Schedule of Investments | Aggressive Growth

As of September 30, 2014

| | | | | | |

| |

| Shares | | | | Fair Value | |

| |

| | |

| | COMMON STOCK - 96.2 % | | | | |

| | APPAREL - 4.8 % | | | | |

| 2,725 | | Carter’s, Inc. | | $ | 211,242 | |

| 1,330 | | Hanesbrands, Inc. | | | 142,895 | |

| 17,560 | | Steven Madden Ltd. * | | | 565,959 | |

| 2,710 | | VF Corp. | | | 178,941 | |

| | | | | | |

| | | | | 1,099,037 | |

| | | | | | |

| | BANKS - 8.5 % | | | | |

| 4,280 | | Cardinal Financial Corp. | | | 73,059 | |

| 19,975 | | First Horizon National Corp. | | | 245,293 | |

| 3,670 | | First NBC Bank Holding Co. * | | | 120,193 | |

| 3,700 | | PacWest Bancorp. | | | 152,551 | |

| 8,465 | | Popular, Inc. * | | | 249,167 | |

| 11,745 | | PrivateBancorp, Inc. | | | 351,293 | |

| 32,079 | | Synovus Financial Corp. | | | 758,348 | |

| | | | | | |

| | | | | 1,949,904 | |

| | | | | | |

| | BIOTECHNOLOGY - 2.0 % | | | | |

| 695 | | Alexion Pharmaceuticals, Inc. * | | | 115,245 | |

| 1,800 | | BioMarin Pharmaceutical, Inc. * | | | 129,888 | |

| 3,030 | | Incyte Corp. Ltd. * | | | 148,622 | |

| 2,845 | | MacroGenics, Inc. * | | | 59,461 | |

| | | | | | |

| | | | | 453,216 | |

| | | | | | |

| | COMMERCIAL SERVICES - 12.3 % | | | | |

| 2,900 | | Advisory Board Co. * | | | 135,111 | |

| 2,490 | | Cardtronics, Inc. * | | | 87,648 | |

| 1,150 | | DeVry Education Group, Inc. | | | 49,232 | |

| 2,270 | | Euronet Worldwide, Inc. * | | | 108,483 | |

| 1,179 | | FleetCor Technologies, Inc. * | | | 167,559 | |

| 3,050 | | H&E Equipment Services, Inc. | | | 122,854 | |

| 5,655 | | Heartland Payment Systems, Inc. | | | 269,856 | |

| 24,210 | | Information Services Group, Inc. * | | | 91,998 | |

| 2,195 | | MAXIMUS, Inc. | | | 88,085 | |

| 3,255 | | Monro Muffler Brake, Inc. | | | 157,965 | |

| 10,740 | | SEI Investments Co. | | | 388,358 | |

| 1,575 | | United Rentals, Inc. * | | | 174,983 | |

| 6,525 | | Vantiv, Inc. - Cl. A * | | | 201,623 | |

| 34,170 | | WNS Holdings Ltd. - Cl. A * | | | 769,167 | |

| | | | | | |

| | | | | 2,812,922 | |

| | | | | | |

| | COMPUTERS - 5.5 % | | | | |

| 6,595 | | Cognizant Technology Solutions Corp. * | | | 295,258 | |

| 8,625 | | Electronics For Imaging, Inc. * | | | 380,966 | |

| 2,605 | | iGATE Corp. * | | | 95,655 | |

| 1,550 | | IHS, Inc. - Cl. A * | | | 194,045 | |

| 2,080 | | Manhattan Associates, Inc. * | | | 69,513 | |

| 1,967 | | NetScout Systems, Inc. * | | | 90,088 | |

| 3,775 | | VeriFone Systems, Inc. * | | | 129,785 | |

| | | | | | |

| | | | | 1,255,310 | |

| | | | | | |

| | COSMETICS/PERSONAL CARE - 0.6 % | | | | |

| 5,400 | | Inter Parfums, Inc. | | | 148,500 | |

| | | | | | |

| | |

| | DISTRIBUTION/WHOLESALE - 1.5 % | | | | |

| 4,295 | | Wesco International, Inc. * | | | 336,127 | |

| | | | | | |

| | |

| | DIVERSIFIED FINANCIAL SERVICES - 7.7 % | | | | |

| 24,020 | | Cowen Group, Inc. * | | | 90,075 | |

| 8,835 | | E*TRADE Financial Corp. * | | | 199,582 | |

| 6,400 | | Encore Capital Group, Inc. * | | | 283,584 | |

| 2,975 | | Evercore Partners, Inc. - Cl. A | | | 139,825 | |

| 2,980 | | IntercontinentalExchange Group, Inc. | | | 581,249 | |

| 10,880 | | Invesco Ltd. | | | 429,542 | |

| 800 | | MarketAxess Holdings, Inc. | | | 49,488 | |

| | | | | | |

| | | | | 1,773,345 | |

| | | | | | |

| | ELECTRICAL - 0.4 % | | | | |

| 675 | | Acuity Brands, Inc. | | | 79,454 | |

| | | | | | |

| | |

| | ELECTRONICS - 2.7 % | | | | |

| 430 | | Mettler-Toledo International, Inc. * | | | 110,136 | |

| 2,895 | | Thermo Fisher Scientific, Inc. | | | 352,322 | |

| 4,785 | | Trimble Navigation Ltd. * | | | 145,943 | |

| | | | | | |

| | | | | 608,401 | |

| | | | | | |

The accompanying notes are an integral part of these financial statements.

31

Schedule of Investments | Aggressive Growth (Continued)

As of September 30, 2014

| | | | | | |

| |

| Shares | | | | Fair Value | |

| |

| |

| | ENVIRONMENTAL CONTROL - 1.2 % | |

| 2,310 | | MSA Safety, Inc. | | $ | 114,114 | |

| 3,060 | | Waste Connections, Inc. | | | 148,471 | |

| | | | | | |

| | | | | 262,585 | |

| | | | | | |

| | FOOD - 1.1 % | | | | |

| 2,515 | | Hain Celestial Group, Inc. * | | | 257,410 | |

| | | | | | |

| | |

| | HEALTHCARE - 7.1 % | | | | |

| 14,425 | | Bruker biosciences Corp. * | | | 267,079 | |

| 4,700 | | Globus Medical, Inc. - Cl. A * | | | 92,449 | |

| 4,580 | | ICON PLC * | | | 262,113 | |

| 1,350 | | IPC The Hospitalist Co., Inc. * | | | 60,467 | |

| 2,450 | | LDR Holding Corp. * | | | 76,269 | |

| 3,225 | | NuVasive, Inc. * | | | 112,455 | |

| 5,475 | | Spectranetics Corp * | | | 145,471 | |

| 12,195 | | Tornier NV * | | | 291,461 | |

| 3,375 | | Trinity Biotech PLC | | | 61,661 | |

| 8,605 | | Wright Medical Group, Inc. * | | | 260,732 | |

| | | | | | |

| | | | | 1,630,157 | |

| | | | | | |

| | HOLDING COMPANIES - 0.6 % | |

| 11,330 | | Horizon Pharma Plc * | | | 139,132 | |

| | | | | | |

| | |

| | HOME BUILDERS - 0.9 % | | | | |

| 5,155 | | Lennar Corp. | | | 200,168 | |

| | | | | | |

| | |

| | INSURANCE - 2.7 % | | | | |

| 12,475 | | Assured Guaranty Ltd. | | | 276,446 | |

| 23,868 | | Radian Group, Inc. | | | 340,358 | |

| | | | | | |

| | | | | 616,804 | |

| | | | | | |

| | INTERNET - 2.8 % | | | | |

| 3,950 | | Endurance International Group Holdings, Inc. * | | | 64,266 | |

| 16,725 | | Move, Inc. * | | | 350,556 | |

| 4,200 | | SPS Commerce, Inc. * | | | 223,230 | |

| | | | | | |

| | | | | 638,052 | |

| | | | | | |

| | LEISURE - 2.4 % | | | | |

| 12,775 | | Brunswick Corp. | | | 538,338 | |

| | | | | | |

| |

| | MACHINERY-DIVERSIFIED - 2.0 % | |

| 5,220 | | Columbus McKinnon Corp. | | | 114,788 | |

| 2,495 | | Flowserve Corp. | | | 175,947 | |

| 2,250 | | Nordson Corp. | | | 171,158 | |

| | | | | | |

| | | | | 461,893 | |

| | | | | | |

| | METAL FABRICATE/HARDWARE - 0.6 % | |

| 4,970 | | Rexnord Corp. * | | | 141,397 | |

| | | | | | |

| |

| | MISCELLANEOUS MANUFACTURING - 1.2 % | |

| 3,075 | | Hexcel Corp. * | | | 122,078 | |

| 5,995 | | TriMas Corp. * | | | 145,858 | |